Sparse Unit-Sum Regression

Abstract

This paper considers sparsity in linear regression under the restriction that the regression weights sum to one. We propose an approach that combines - and -regularization. We compute its solution by adapting a recent methodological innovation made by Bertsimas et al. (2016) for -regularization in standard linear regression. In a simulation experiment we compare our approach to -regularization and -regularization and find that it performs favorably in terms of predictive performance and sparsity. In an application to index tracking we show that our approach can obtain substantially sparser portfolios compared to -regularization while maintaining a similar tracking performance.

Keywords: Sparsity, Regularization, Lasso, Best subset selection, Linear regression, Portfolio optimization.

1 Introduction

Linear regression with coefficients that sum to one (henceforth unit-sum regression) is used in portfolio optimization and other economic applications such as forecast combinations (Timmermann, 2006) and synthetic control (Abadie et al., 2010).

In this paper, we focus on obtaining a sparse solution (i.e. containing few non-zero elements) to the unit-sum regression problem. A sparse solution may be desirable for a variety of reasons, such as making a model more interpretable, improving estimation efficiency if the underlying parameter vector is known to be sparse, remedying identification issues if the number of variables exceeds the number of observations, or application-specific reasons such as reducing cost by limiting the amount of constituents in a portfolio.

A popular method to produce sparsity is to use regularization. Theoretically, the most straightforward way to obtain a sparse solution is to use -regularization (also known as best-subset selection), which amounts to restricting the number of non-zero elements in the solution. However, the use of -regularization is NP-hard (Coleman et al., 2006; Natarajan, 1995) and has traditionally been seen as computationally infeasible for problems with more than about 40 variables, both in unit-sum regression and standard linear regression.

Due to these computational difficulties, -regularization has often been replaced by -regularization, also known as Lasso (Tibshirani, 1996). In -regularization, the -norm restriction that restricts the number of non-zero elements is replaced by an -norm restriction that restricts the absolute size of the coefficients. This turns the problem into an easier to solve convex optimization problem. An -norm restriction shrinks the weights towards zero and, as a consequence of the shrinkage, produces sparsity by setting some weights exactly equal to zero.

The use of -regularization in the presence of a unit-sum restriction was first considered by DeMiguel et al. (2009) and Brodie et al. (2009) in the context of portfolio optimization. They show that -regularization is able to produce sparsity in combination with a unit-sum restriction. In addition, they demonstrate that the combination can be viewed as a restriction on the sum of the negative weights. In some applications it is highly desirable to have a parameter that explicitly controls the sum of the negative weights. For example, in a portfolio optimization context negative weights represent potentially costly short positions.

However, the unit-sum restriction causes a problem when using -regularization: due to the unit-sum restriction the -norm of the weights cannot be smaller than 1. This imposes a lower bound on the amount of shrinkage produced by -regularization. In turn, this places an upper bound on the sparsity produced by -regularization. This upper bound depends entirely on the data, which makes it difficult to rely on -regularization if a specific level of sparsity is desired. In addition, due to the bound there does not always exist a value of the tuning parameter that guarantees the existence of a unique solution. Furthermore, Fastrich et al. (2014) point out that a combination of a non-negativity restriction and a unit-sum restriction fixes the -norm of the weights to 1, which renders -regularization useless.

In order to address these issues and obtain sparse solutions in unit-sum regression, we use a recent innovation in -regularization in the standard linear regression setting by Bertsimas et al. (2016). They show that modern Mixed-Integer Optimization (MIO) solvers can find a provably optimal solution to -regularized regression for problems of practical size. To achieve this, the solver is provided with a good initial solution obtained from a discrete first-order (DFO) algorithm. In a simulation study, they show that -regularization performs favorably compared to -regularization in terms of predictive performance and sparsity.

An extended simulation study comparing - and -regularization in the standard linear regression setting is performed by Hastie et al. (2017). They find that find that -regularization outperforms -regularization if the signal-to-noise ratio (SNR) is high, while -regularization performs better if the SNR is low. Additionally, they find that if the tuning parameters are selected to optimize predictive performance, -regularization yields substantially sparser solutions.

A combination of - and -regularization (-regularization) is studied in the standard linear regression context by Mazumder et al. (2017). They observe that this combination yields a predictive performance similar to -regularization if the SNR is low, and a predictive performance similar to -regularization if the SNR is high. In addition, they find that -regularization produces more sparsity compared to -regularization, if the tuning parameters are selected in order to optimize predictive performance.

Motivated by the results in the standard linear regression setting, we propose the use of -regularization in unit-sum regression. Specifically, let be a -vector and let be a matrix, then we consider the problem

| (1) |

where are the elements of , is the -norm of , is the -norm of , and . Notice that this problem is equivalent to -regularized unit-sum regression if is sufficiently large, and equivalent to -regularized unit-sum regression if .

The formulation in (1) provides users with explicit control over both the sparsity of the solution and the sum of the negative weights of the solution. In addition, if the tuning parameters are selected in order to maximize predictive performance, we find in a simulation experiment that -regularization:

-

•

performs better than -regularization in terms of predictive performance, especially if the signal-to-noise ratio is low.

-

•

performs well compared to -regularization in terms of predictive performance, especially for higher signal-to-noise ratios, while at the same time producing much sparser solutions.

The main contributions of this paper can be summarized as follows. [1] We propose -regularization for the unit-sum regression problem. [2] We analyze the problem for orthogonal design matrices and provide an algorithm to compute its solution. [3] We show how the algorithm for the orthogonal design case can be used in finding a solution to the general problem by extending the framework of Bertsimas et al. (2016) to unit-sum regression. [4] We perform a simulation experiment which shows that our approach performs favorably compared to -regularization or -regularization. [5] We demonstrate in an application to stock index tracking that a -regularization is able to find substantially sparser portfolios than -regularization, while maintaining a similar out-of-sample tracking error.

The remainder of the paper is structured as follows. In Section 2, problem (1) is studied under the assumption that is orthogonal and an algorithm for the orthogonal case is presented. Section 3 analyzes the sparsity production for the orthogonal case and yields some intuitions about the problem. Section 4 links the algorithm for the orthogonal case to the framework of Bertsimas et al. (2016) in order to find a solution to the general problem. In Section 5, the simulation experiments are presented. Section 6 provides an application to index tracking.

2 Orthogonal Design

As problem (1) is difficult to study in its full generality, we first consider the special case that is orthogonal. We derive properties of a solution to (1) under orthogonality and use these properties in order to construct an algorithm that finds a solution. The algorithm is presented at the end of the section. In Section 4 this algorithm is used in finding a solution to the general problem by extending the framework of Bertsimas et al. (2016). In Section 3 we analyze the sparsity of the solution under orthogonality.

Assume that , where is the identity matrix. Let us write , so that minimizing in is equivalent to minimizing . Define

| (2) |

Then, problem (1) can be written as .

We assume the elements of are different and . Without further loss of generality we assume . In Section 2.4 we relax the assumption that and allow for .

Let

where , so that . If , then for some . Let us denote this value of with . We will now show that can be computed from the signs of its elements and . In order to show this, we first solve a related problem and then show that is equal to the solution of a specific case of this related problem.

Let and be disjoint sets with cardinalities and , respectively, where . Define

Minimization of over the affinely restricted set has the solution

| (3) |

Recall that and let and . Furthermore, let be the set of vectors with elements that have the same signs as the elements of , then . Notice that the difference between and is that there are no sign restrictions on elements , for which . Consequently,

However, if , then for sufficiently small . Furthermore, as is a parabola in with a minimum at , we find that for small . As , this is a contradiction. Hence, , which is our first result.

Proposition 1.

If , then .

So, the problem can be decomposed into finding the components of the triplet that minimizes . Next, we will study the properties of these components.

2.1 Properties of as a function of and

The sorting of reveals an ordered structure in the sets and that minimize . This structure is described in the following result.

Proposition 2.

If , then and if , and if .

The proof is given in the Appendix. For sets such as and , we use the notation , as in (3). The following result shows that and should be maximized such that .

Lemma 1.

If and , where , , , then .

The proof is given in the Appendix.

We will now consider the relationship between and the pair . With reference to (3), let us consider the sets

| (4) | ||||

| (5) |

with cardinalities and . As

we find , and similarly if and if . Additionally, we find that is increasing in , and similarly that is increasing in . So, by Lemma 1 we have following result for .

Proposition 3.

If and , then .

We will now analyze how varies with if , and use this to find a minimizer if . The case that is treated separately in Section 2.3.

2.2 Properties of as a function of for

As and are integers, they increase discontinuously as increases. In this subsection we show that and its derivative are continuous in despite these discontinuities in and . This will allow us to show that if .

Let and , for . We then find the ordering , and

| (6) |

Consequently, if , then

| (7) |

Similarly, let and , for . Then and

| (8) |

Consequently, if , then

| (9) |

Using the cardinalities and of the sets and in (4) and (5), let . If , then . If , then . The loss function

is a continuous function of for , with derivative

| (10) |

which is continuous for . That is, using (6), if , then

and if , then

A similar continuity holds for the second term of (10) due to (8). The derivative (10) is increasing in , but it is negative for due to (7) and (9), which imply

We summarize these results in a proposition.

Proposition 4.

The function is continuous in for , and the derivative with respect to is negative for .

As is strictly decreasing in over if , we conclude that if .

2.3 The case that

If , then . So an alternative approach is required. By Lemma 1 and the fact that , we should compare the objective values for all pairs for which , and . In order to do so for a given pair , we need to find the value of that minimizes . This minimizing value, which we will denote by , must satisfy . We will now show that is either equal to or to .

We find

where

As is quadratic in with a minimum at , we find that if , then , and if , then .

In the case that , the minimum does not exist, since as . Furthermore, . So if then for some , by Proposition 3 and due to the negative gradient of . In the case that , then or , and . So if , then by Lemma 1. Similarly if , then . So if , then for all .

Hence, if , we can compute for each pair that satisfies , and and use this to compute the objective value . By comparing the objective values, we can find the triplet for which .

Combining these findings with the findings from the previous sections, we can construct an algorithm to find an element of . This algorithm is presented in Algorithm 1.

2.4 Extension

The case can be treated in a way similar to the case , except that in the proof of Proposition 2 the assumption was needed. We therefore provide a proof for .

Proposition 5.

Proposition 2 holds true when .

The proof is given in the Appendix.

3 Sparsity Under Orthogonality

In this section, we use the results from Section 2 to study the sparsity of the solution to (1) under orthogonality.

As both - and -regularization produce sparsity, we can analyze how the sparsity of the solution to (1) depends on the tuning parameters and . From Algorithm 1, it is straightforward to observe that the amount of non-zero elements in is equal to where and . So the -regularization component only produces additional sparsity if .

In order to gain some insights into the sparsity produced by the -regularization component, we consider the maximum sparsity produced by -regularization if . Notice that the sparsity is maximized if is minimized, which happens when . Furthermore, if , then . So, the minimum number of non-zero elements is equal to

| (11) |

where . This shows that the maximum sparsity produced by -regularization depends entirely on the size of the gaps between the largest elements of . So the maximum amount of sparsity does not change if the same constant is added to each element of .

To further analyze the maximum sparsity produced by the -regularization component, we consider two special cases of : one case without noise and one case with noise.

Linear and Noiseless. Suppose that the largest elements of are linearly spaced with distance (i.e. for some ). Then, using (11), we can derive the following closed-form expression for the minimum number of non-zero elements:

where rounds down to the nearest integer. As this function is weakly decreasing in , the maximum sparsity is increasing in . So, we obtain the intuition that if the largest elements of are more similar, then less sparsity can be produced by -regularization.

Equal and Noisy. Let , where has i.i.d. elements , , and is an -vector with elements for all . As all elements of are equal, the gaps between the elements of are equal to the gaps between the order statistics of , scaled by the constant . So, the size of the gaps between the largest elements of is increasing in . Therefore, according to (11), the maximum sparsity is increasing in . As an increase in represents an increase in noise, we can draw the intuitive conclusion that if has elements of similar size, then the maximum amount of sparsity produced by -regularization increases with noise.

4 General Case

In this section, we describe how a solution can be found for the general case, in which is not required to be orthogonal. To do so, we adapt the framework laid out by Bertsimas et al. (2016) for standard linear regression. This framework consists of two components. The first component is a Discrete First-Order (DFO) algorithm that uses an algorithm for the orthogonal problem as a subroutine in each iteration. The solution to this DFO algorithm is then used as an initial solution for the second component. The second component relies on reformulating (1) as an MIO problem, which can be solved to provable optimality by using an MIO solver.

4.1 Discrete First-Order Algorithm

In the construction of the DFO algorithm, we closely follow Bertsimas et al. (2016), but use a different constraint set that includes an additional -norm restriction and unit-sum restriction.

Denote the objective function as

This function is Lipschitz continuously differentiable, as

where is the largest absolute eigenvalue of . So, we can apply the following result.

Proposition 6 (Nesterov, 2013; Bertsimas et al., 2016).

For a convex Lipschitz continuous function , we have

| (12) |

for all , and , where is smallest constant such that .

Given some fixed , we can minimize the bound in (12) with respect to under the constraint set , as given in (2). Following Bertsimas et al. (2016), we find

| (13) |

Notice that (13) can be computed using Algorithm 1. Therefore, it is possible to use iterative updates in order to decrease the objective value. Specifically, let and recursively define , for all . Then by Proposition 6,

In Algorithm 2, we present an algorithm that uses this updating step until some convergence criterion is reached.

4.2 Mixed-Integer Optimization

In this section, an MIO formulation for problem (1) is presented. In order to formulate problem (1) as an MIO problem, we use three sets of auxiliary variables. The variables and are used to specify the positive and negative parts of the arguments , . The variable serves as an indicator function for whether is different from zero, . The MIO formulation is given as follows:

| s.t. | |||

where has elements , and and are big-M parameters. These big-M parameters are used to enforce the sparsity constraint as follows: if then , and if then . Hence, and should be sufficiently large in absolute value to ensure that the solution to the MIO problem is the solution to (1). On the other hand, they should not be too large as tighter bounds decrease the size of the search space and improve the speed of the solver.

The -restriction provides natural choices and . However, these bounds are conservative in practice. Mazumder et al. (2017) suggest the use of bounds based on the solution of the DFO algorithm. Similarly, we propose to use and , where is the th element of the solution of the DFO algorithm.

5 Numerical Results

In this section we compare the performance of our -regularized approach to -regularization and -regularization on simulated datasets, generated with multiple signal-to-noise ratios and values of .

5.1 Setup Simulation Experiments

The setup of our simulation experiments largely follows the numerical experiments found in Mazumder et al. (2017) and Hastie et al. (2017). For a given set of parameters (number of observations), (number of variables), (number of non-zero weights), (number of positive weights), (number of negative weights), (sum of the negative weights), (autocorrelation between the variables) and SNR (signal-to-noise ratio), the experiments are conducted as follows:

-

1.

We randomly select elements of and set of the elements equal to , and of the elements equal to . The remaining elements are set equal to zero.

-

2.

The rows of matrix are drawn i.i.d. from , where has elements , .

-

3.

The vector is drawn from , where in order to fix the signal-to-noise ratio.

-

4.

We apply -regularization, -regularization and -regularization to and for a range of tuning parameters. For both methods, we select the tuning parameter(s) that minimize(s) the prediction error on a separate dataset , , generated in the same way as and .

-

5.

We record several performance measures of the solutions that were found using the selected tuning parameters.

We repeat the above steps 100 times for each parameter setting. Throughout the experiments we use , , , . For each setting, we choose and SNR . This choice of covers the case where the negative weights are small in comparison to the positive weights, as well as the case where the positive and negative weights are equal in magnitude. The tuning parameters corresponding to and are simultaneously selected over the grid .

For each different combination of and SNR, we record the following performance measures:

-

-

Relative risk. As measure of predictive performance we use relative risk, defined for a solution as

This is one of the measures used in Hastie et al. (2017), and is similar to the predictive performance measures used in Bertsimas et al. (2016) and Mazumder et al. (2017). For this measure, a lower value is indicative of a better predictive performance and its minimum value is 0. The null score to beat is 1 (if ).

-

-

Number of non-zero elements. As a second measure, we consider the number of non-zero elements in the estimated weights, in order to compare the sparsity obtained by both methods.

-

-

Sum of negative weights. As a final measure, we consider the sum of the negative estimated weights. This allows us to compare the shrinkage produced by the -regularization component of both methods.

5.2 Implementation and Stopping Criteria

In order to compute the solution to -regularized unit-sum regression, we use an adaptation of the LARS method for -regularization (Efron et al., 2004), based on the algorithm described by DeMiguel et al. (2009). The -regularization solution is computed in the same way as the -regularization solution by fixing the parameter to some sufficiently large value.

For the -regularization approach, we terminate the DFO algorithm if the improvement in the squared error is below some value , where we set . As the DFO algorithm can be sensitive to its initialization, we initialize it with the Forward-Stepwise Selection (FSS). We found that this typically yields a better performance than using the best solution out of 50 random initializations as used by Bertsimas et al. (2016). The FSS solution is implemented using successive applications of the adapted LARS algorithm.

The MIO formulation is implemented in the R-interface of Gurobi 7.1. Each instance is given 10 minutes of computation time. If the optimality of the solution is not confirmed within the allotted time, the solver is terminated and its best solution so far is used. This means that the combined maximum computation time is 44000 hours. However, in practice we find that the DFO algorithm often provides optimal or near-optimal solutions to the MIO solver. As a result, the MIO solver rarely uses the full 10 minutes and typically certifies optimality in seconds. The total computation time for the simulation experiments was approximately 600 hours on a single machine, including the computation of the initial solutions.

5.3 Results of Simulation Experiments

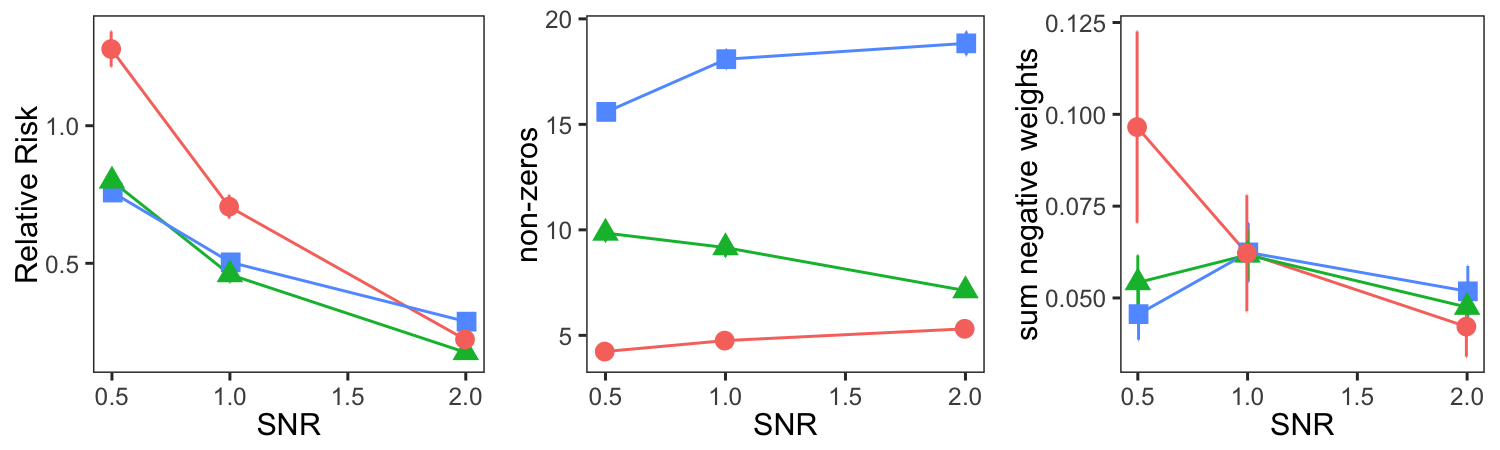

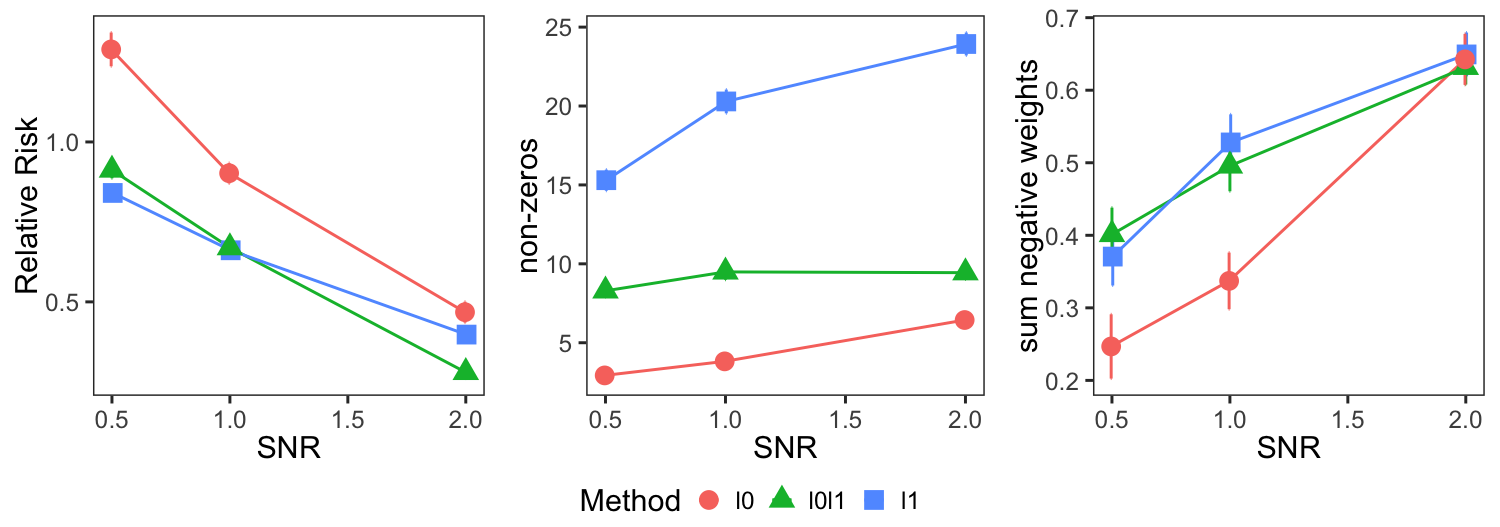

The results of the simulation experiments are displayed in Figure 1. We make the following observations.

Prediction.

It can be observed that -regularization typically performs worse than the other methods, especially when the SNR is low. Furthermore, -regularization seems to outperform -regularization for higher SNRs in terms of relative risk, while -regularization fares similarly or even somewhat better for lower SNRs.333These results differ slightly from the findings by Mazumder et al. (2017) for standard linear regression. They find that -regularization performs as well as -regularization if the SNR is low. We suspect that this difference could be caused by the fact that they do not consider an SNR below 1 and use a fixed-design setup where .

Sparsity.

We find that -regularization delivers considerably denser solutions than the other methods for all values of SNR and . In addition, the number of non-zeros seems to move away from the true number of non-zeros as the SNR increases. On the other hand, -regularization yields overly sparse solutions below the true value , especially if the SNR is low. The number of non-zeros produced by -regularization lies between the values other two methods, and is typically closer than the number of non-zeros produced by -regularization or -regularization.

Shrinkage. In the third column of Figure 1, it can be seen that the sum of the negative weights of the solutions tends to be smaller than . However, for the case that , there is a clear trend towards the true value of as the SNR increases. Interestingly, both -regularization and -regularization have a similar sum of negative weights, despite the fact that the solutions of -regularization are much sparser. This implies that the average magnitude of the weights of the -regularization solution is much smaller than that of the -regularization solution.

6 Application: Index Tracking

In order to demonstrate the use of our proposed methodology in practice, we consider an application to index tracking. Index tracking concerns the construction of a portfolio that replicates a stock index as closely as possible, while limiting the cost of holding the portfolio. Such a portfolio can be represented by a weight vector that sums to one, with positive elements that correspond to long positions and negative elements that correspond to short positions.

Two standard ways to limit the cost of holding the portfolio are to restrict the number of constituents in the portfolio and to avoid short positions. Using historical returns data, it is possible to find such a portfolio using -regularized unit-sum regression. Specifically, let represent the historical returns of a stock index and let each column of represent the historical returns of one of its constituents. Then, using , problem (1) minimizes the squared error between the actual index returns and the returns of the portfolio, that consists of at most constituents and has no short positions.

Notice that even if the component is omitted, or equivalently , then the remaining -regularization may still produce a sparse portfolio (DeMiguel et al., 2009; Brodie et al., 2009). However, as the returns of an index are typically a dense linear combination of its constituent returns, with positive weights of similar magnitude, the intuitions from the orthogonal design case from Section 3 suggest that -regularization may not be very effective in producing sparsity.

To compare the sparsity production and tracking performance of -regularization and -regularization, we use the index tracking datasets of the OR-library (Beasley et al., 2003; Canakgoz and Beasley, 2009). These datasets contain 290 weekly returns of 8 indexes varying from 31 to 2153 constituents.444Only the constituents that are part of the index for the entire period are included. Each dataset is split into two halves of 145 observations, where the first half is used to construct the portfolio and the second half is used to measure the performance of the portfolio.555From the second index (DAX) we removed two large consecutive outliers from the out-of-sample data. These two outliers were the largest two returns (in absolute value) and of opposing sign, suggesting a bookkeeping error in the index returns. This is supported by the fact that the outliers are not reflected in the returns of the constituents. The performance is measured in out-of-sample , on the second half of the datasets. The results are presented in Table 1.

From the results we can make several observations regarding the sparsity of the solutions and the tracking performance. First it should be noted that -regularization by itself is not able to find a unique portfolio for the largest two stock indexes. In addition, even if -regularization does have a unique solution, it is generally not able to produce a substantial amount of sparsity. In terms of out-of-sample tracking performance, lower values of do generally result in worse performance. However, the difference is small, especially for the larger values of .

7 Appendix

Proof of Proposition 2: If , then and if .

Proof.

We show that if , then two conditions hold true:

We prove the -condition. The proof of the -condition is similar. Assume the -condition is not true. In that case, we show that an index set exists, such that and , which is a contradiction, showing the validity of the -condition.

Assuming the -condition is not true, let . As , we have , which is equivalent to . Define

Let . As if , we find

Consequently, . Therefore, the index set , where is the maximum index such that , exists. Let .

We now show . Let with cardinality . As has cardinality , the cardinalty of equals . Let

We find

As , and , the first term is negative. As and if , and hence , the second term is negative as well. Consequently, , which is a contradiction. ∎

Proof of Lemma 1: If and , where , , , then .

Proof.

We can use the convexity of the quadratic function to show

where , and . In a similar way we find . ∎

Proof of Proposition 3: If and , then .

Proof.

Using Proposition 1, let where and have cardinalities and , respectively, where . We will show that if .

Suppose , then

| (A.1) |

Consequently,

has a positive derivative

As a result, does not have a minimum. If

then contains zeros, so that . ∎

Setting

Setting

Setting

| Index | #nz | Index | #nz | |||||

|---|---|---|---|---|---|---|---|---|

| 5 | 5 | 0.909 | 20 | 20 | 0.922 | |||

| Hang | 15 | 15 | 0.982 | Nikkei | 60 | 60 | 0.957 | |

| Seng | 25 | 25 | 0.991 | (m = 225) | 100 | 100 | 0.961 | |

| (m = 31) | 31 | 25 | 0.991 | 225 | 127 | 0.961 | ||

| 10 | 10 | 0.940 | 20 | 20 | 0.780 | |||

| DAX | 30 | 30 | 0.979 | S&P | 60 | 60 | 0.839 | |

| (m = 85) | 50 | 50 | 0.981 | 500 | 100 | 100 | 0.857 | |

| 85 | 78 | 0.985 | (m = 457) | 457 | 122 | 0.855 | ||

| 10 | 10 | 0.652 | 20 | 20 | 0.646 | |||

| FTSE | 30 | 30 | 0.948 | Russel | 60 | 60 | 0.679 | |

| (m = 89) | 50 | 50 | 0.959 | 2000 | 100 | 100 | 0.691 | |

| 89 | 68 | 0.966 | (m = 1319) | 1319 | - | - | ||

| 10 | 10 | 0.815 | 20 | 20 | 0.767 | |||

| S&P | 30 | 30 | 0.932 | Russel | 60 | 60 | 0.821 | |

| 100 | 50 | 50 | 0.960 | 3000 | 100 | 100 | 0.836 | |

| (m = 98) | 98 | 77 | 0.969 | (m = 2152) | 2152 | - | - |

References

- Abadie et al. (2010) Abadie, A., Diamond, A., and Hainmueller, J., 2010. Synthetic control methods for comparative case studies: Estimating the effect of california’s tobacco control program. Journal of the American Statistical Association, 105(490):493–505.

- Beasley et al. (2003) Beasley, J. E., Meade, N., and Chang, T.-J., 2003. An evolutionary heuristic for the index tracking problem. European Journal of Operational Research, 148(3):621–643.

- Bertsimas et al. (2016) Bertsimas, D., King, A., Mazumder, R., et al., 2016. Best subset selection via a modern optimization lens. The Annals of Statistics, 44(2):813–852.

- Brodie et al. (2009) Brodie, J., Daubechies, I., De Mol, C., Giannone, D., and Loris, I., 2009. Sparse and stable markowitz portfolios. Proceedings of the National Academy of Sciences, 106(30):12267–12272.

- Canakgoz and Beasley (2009) Canakgoz, N. A. and Beasley, J. E., 2009. Mixed-integer programming approaches for index tracking and enhanced indexation. European Journal of Operational Research, 196(1):384–399.

- Coleman et al. (2006) Coleman, T. F., Li, Y., and Henniger, J., 2006. Minimizing tracking error while restricting the number of assets. Journal of Risk, 8(4):33.

- DeMiguel et al. (2009) DeMiguel, V., Garlappi, L., Nogales, F. J., and Uppal, R., 2009. A generalized approach to portfolio optimization: Improving performance by constraining portfolio norms. Management Science, 55(5):798–812.

- Efron et al. (2004) Efron, B., Hastie, T., Johnstone, I., Tibshirani, R., et al., 2004. Least angle regression. The Annals of Statistics, 32(2):407–499.

- Fastrich et al. (2014) Fastrich, B., Paterlini, S., and Winker, P., 2014. Cardinality versus q-norm constraints for index tracking. Quantitative Finance, 14(11):2019–2032.

- Hastie et al. (2017) Hastie, T., Tibshirani, R., and Tibshirani, R. J., 2017. Extended comparisons of best subset selection, forward stepwise selection, and the lasso. arXiv preprint arXiv:1707.08692.

- Mazumder et al. (2017) Mazumder, R., Radchenko, P., and Dedieu, A., 2017. Subset selection with shrinkage: Sparse linear modeling when the snr is low. arXiv preprint arXiv:1708.03288.

- Natarajan (1995) Natarajan, B. K., 1995. Sparse approximate solutions to linear systems. SIAM journal on computing, 24(2):227–234.

- Nesterov (2013) Nesterov, Y., 2013. Introductory lectures on convex optimization: A basic course, volume 87. Springer Science & Business Media.

- Tibshirani (1996) Tibshirani, R., 1996. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society. Series B (Methodological), pages 267–288.

- Timmermann (2006) Timmermann, A., 2006. Forecast combinations. Handbook of economic forecasting, 1:135–196.