Optimality of impulse control problem in refracted Lévy model with Parisian ruin and transaction costs

Abstract.

In this paper we investigate an optimal dividend problem with transaction costs, where the surplus process is modelled by a refracted Lévy process and the ruin time is considered with Parisian delay. Presence of the transaction costs implies that one need to consider the impulse control problem as a control strategy in such model. An impulse policy , which is to reduce the reserves to some fixed level whenever they are above another level is an important strategy for the impulse control problem. Therefore, we give sufficient conditions under which the above described impulse policy is optimal. Further, we give the new analytical formulas for the Parisian refracted -scale functions in the case of the linear Brownian motion and the Crámer-Lundberg process with exponential claims. Using these formulas we show that for these models there exists a unique policy which is optimal for the impulse control problem. Numerical examples are also provided.

Keywords: Refracted Lévy process, Parisian ruin, Dividend problem, Impulse control.

A. Kaszubowski is partially supported by the National Science Centre Grant No. 2015/17/B/ST1/01102.

1. Introduction

For many years applied mathematicians has been trying to create the models that allow to describe reality in the terms of mathematics. A special role is played by models used to describe phenomena that develop over time and in which there is a some factor of randomness. In such case, it is important to approximate some certain characteristics or to find some event probabilities. For example, insurance companies need to estimate the amount of reserves that will allow them to be solvent with a very high probability. In this case, the question arises about the size of these reserves. Another example can be hedging companies, which, when valuing financial instruments, often use stochastic models.

In this paper, we focus on another classic problem affecting the companies, namely on the issue of the optimal dividend payments. Dividend is the transfer of a certain portion of the company’s finances to the investors, so it is one of the tools for shareholders to receive the profits from the company’s support. Dividends also may attract new investors to the company, and thus provide further financing. On the other hand, significant dividend payments result in the reduction of the company funds, and thus may lead to a significant increase of the probability of losing liquidity. Therefore dividend payments must be made in an optimal way, and they may be made up to the company’s bankruptcy. The problem of the bankruptcy is related to the ruin theory, traditionally considered in the context of the insurance companies, where the ruin moment is related to the process of financial surplus, and in particular with its size at a given moment. The classically defined moment of ruin is the first moment when the surplus process goes below the level zero. Nowadays, such a moment of ruin has a small chance of occurrence. The reason for that is the fact that such companies control (and are controlled) so that the probability of such event stays at a very low level, whether through the impact of the additional cash or prior fixing of the financial reserves. Probability of the ruin as well as the theory of ruin plays therefore a different role. It is a determinant of the financial situation of the company, which allows to make strategic decisions in the company management. Therefore, it is important to investigate different definitions of the ruin and choose the proper one for our case.

The classical ruin seems to be an intuitively obvious definition and if such a moment comes, we expect that the company will immediately declare bankruptcy. In practice, very often the investors or the government try to save the company from bankruptcy. Additionally, the too restrictive definition of the ruin as an economic determinant causes freezing of too much cash securing, and so the company grows weaker. Analysing this problem in the terms of the above doubts, it can be concluded that there is a natural need for a different definition of the ruin and in particular the separation of the technical ruin, i.e. exceeding the zero level, and the actual moment of the bankruptcy announcement. For this reason, many alternatives appeared in the literature, for example the so-called Parisian ruin model, which is considered in this paper. In this approach we say that the company announces bankruptcy if the risk process to goes below zero (or to the so-called red zone) and stays there longer than a certain fixed time . Such Parisian stopping times have been studied by Chesney et al. [7] in the context of barrier options in mathematical finance. In another paper Czarna and Palmowski [4] gave the first description of the Parisian ruin probability for a general spectrally negative Lévy processes.

Now, let us define a class of the processes that are usually used to model the financial surplus. One of the most known stochastic processes used in the theory of ruin is the Crámer-Lundberg process, which can be presented in the following form

where represents the initial capital, is the constant intensity of the premium income, is a homogeneous Poisson process with the intensity and are positive i.i.d random variables. Therefore, the compound Poisson the claims of the customers. The form of the Crámer-Lundberg process has some benefits in the aspect of ease of calculations, however, sometimes it may turn out to be too far-reaching simplification. For example, one can see that between successive claims this process is deterministic, so it does not take into account certain market fluctuations. In addition, in the form of this process, we are not able to distinguish large and small claims, and what is done in practice for insurance companies. Therefore, one can consider a wider class of spectrally negative Lévy processes, which contain the Crámer-Lundberg process. This class of the processes include also linear Brownian motion, Cauchy process and -stable processes.

As was mentioned before, one would like to distinguish the moment of exceeding the zero level with the actual bankruptcy by considering the Parisian ruin time. However, to further approximate the model to the reality, we will add an additional assumption. Namely, when the surplus process is in the red zone (i.e. below zero) we assume that it receive a steady flow of cash with the intensity of , until it will reach the positive values. It reflects saving the company from bankruptcy by investors or government. In order for such assumption to be added, one need to use the so-called spectrally negative refracted Lévy process, which was introduced by Kyprianou and Loeffen [16].

Therefore, using the above mentioned assumptions, our goal is to analyse the problem of the optimal dividend payments, where each payment is be accompanied by a certain fixed transaction fee .

Historically, many papers have been written on this topic. The first problem was examined by de Finetti in [8]. He postulated that if the risk process behaves like a random walk with the increments of 1, then the optimal dividend strategy is of barrier type. The barrier strategy is that the company pays everything above a certain fixed level . The next step was to consider the continuous-type processes. In the framework of the linear Brownian motion process as well as the Cramer-Lundberg process, a similar result was obtained, i.e. the optimal strategy is the barrier strategy, see [9], [10] and [12]. Finally, in [1], the optimal barrier strategy for the entire class of spectrally negative Lévy processes was examined. The authors received certain conditions that would ensure that this strategy is the optimal one. Moreover, they expressed these conditions in the language of the so-called scale functions, which will be introduced in Subsection 2.3. Note that in the all above-mentioned papers there were no transaction cost. The only exception is [20], where this assumption was made, also for the class of the spectrally negative Lévy processes. Due to this assumption, further consideration of the barrier strategy was not possible, thus it was replaced by an impulse control strategy, which will be described in details in the following chapters. Moreover, in Section 3.2, the sufficient conditions were obtained providing the optimality of this dividend strategy.

The rest of the paper is organized as follows. First, we introduce some basic notation and definitions related to the spectrally negative Lévy processes and the refracted counterpart. In particular, we will introduce the scale functions and explain why in this theory they play the key role. In Subsection 2.2 we will describe the dividend problem and will explain what means that the dividend strategy is the optimal strategy. Section 3 is the main part of this paper. We will introduce there the impulse policy and we will provide sufficient conditions that the derivative of Parisian refracted scale must fulfils to ensure that the strategy is optimal. The last part of this paper is an examples section, where we will give the new analytical formulas for the Parisian refracted scale functions in the case of the linear Brownian motion and the Crámer-Lundberg process with exponential claims. Using these formulas we will show that for these models there exists a unique impulse policy which is optimal for the impulse control problem. Numerical examples will be also provided.

2. Mathematical model

2.1. Surplus process

Let , be the probability space which satisfy usual conditions. On this probability space we consider process being a spectrally negative Lévy process, namely the stochastic process issued from the origin which has stationary and independent increments and càdlàg paths that have no positive jump discontinuities. To avoid degenerate cases, we exclude the case where has monotone paths. As a strong Markov process we shall endow with probabilities such that under we have with probability one. Further denotes expectation with respect to . Recall that and . Every spectrally negative Lévy process can be represented by the triple where , and is a measure on which satisfies

The Laplace exponent of is defined through

for any . For background on spectrally negative Lévy processes we refer the reader to [2, 15].

We assume that in our model the surplus process is modelled by spectrally negative refracted Lévy process which means that we allow injecting (in continuous way) certain amount of money with intensity when reserves are below zero. Namely, one can define such process as unique strong solution to the following stochastic differential equation:

Note that, refracted process with was examined before by Kyprianou and Loeffen in [16]. As in [18] we focus here on the case when the refraction level equals zero. Moreover, to be compatible with [16] and [18], we subtract on the positive half-line instead of adding it on the negative half-line, however, the practical effect is the same.

From the above equation it is easy to observe that above the level process evolves as process . Since the process is a spectrally negative Lévy process with the Lévy triplet its Laplace exponent is given by

In particular, process retains the probabilistic properties of the process , e.g. the bounded/unbounded variation of the paths. Moreover, we want to emphasize here that process is no longer spatial homogeneous which means that it is not a Lévy process. In Section 3.2 we will prove that process is a Feller process and we will present the form of its infinitesimal generator.

2.2. Dividend problem

Let us now formally introduce the problem studied in this paper, in particular we define the optimization criterion, and then define the candidate for the optimal strategy. Denote as a dividend or control strategy, where is a non-decreasing, left-continuous -adapted process which starts at zero. We will assume that process is a pure jump process, i.e.

| (1) |

Here we mean by the jump of the process at time s. Therefore, random variable can be interpreted as a cumulated dividends to the time . Note that, pure jump assumption is taken directly from the presence of non-zero transaction costs and such control strategies as (1) are known as impulse controls. Let us define the controlled risk process by the dividend strategy :

The company pays dividends up to its bankruptcy moment which in our model is the Parisian ruin time. Let us formally define it as

where is the so-called Parisian delay.

Let us define the value function of a dividend strategy :

where is the discount rate and denotes the transaction cost which occurs whenever the company pays dividends. Since (1) is assumed, the above integral can be interpreted as the following sum

We call a strategy admissible if we do not get to the red zone due to dividend payments, i.e.

| (2) |

Let be the set of all admissible dividend strategies. Our main goal is to find the optimal value function given by

and the optimal strategy such that

2.3. Exit problems and scale functions

In this section we introduce key tools that will allow the optimality of dividend strategy to be investigated. From the application point of view, one of the most important issues studied in the theory of Lévy processes are so-called exit problems. The classical de Finetti dividend problem can also be expressed using exit identities, therefore we will recall here basic results from this topic.

First, for a , we define the following first-passage stopping times

One can be interested in obtaining an analytical representation of the following expression (the so-called two-sided exit problem)

Namely, we would like to examine a unit payment made when the level is reached before the first moment when the level zero is exceeded. This payment is additionally discounted by a discount factor . To obtain the analytical expression for the above expectation let us define the following function.

For each there exists a function , called the -scale function, which satisfies for and is characterised on as a strictly increasing and continuous function whose Laplace transform is given by

where is the right-inverse of . We define the second scale function by

It turns out that for and (see e.g., [15])

and also for

Analogously we can define the scale functions for Lévy process , and we will use notation and for the first and second scale functions for , respectively. Define the scale function for refracted process as follows: For and

| (3) |

In particular, we write when . One can see that the above definition differs from the definition of scale functions for and . However, in [16] it was proved that for and

Therefore, one can see that for process , function gives the same representation for the two-sided exit problem as scale functions and .

In this paper we additionally consider Parisian ruin time, and from [18] it is known that

| (4) |

where

Since scale functions occur in many fluctuation identities, the natural question is if it is possible to calculate them explicitly. The answer is that for some particular examples like Brownian motion with drift or Cramér-Lundberg process with exponential jumps, the form of functions , , can be obtained explicitly (see [2, 11, 14, 15, 18]).

2.4. Properties of scale functions

In this part, we will investigate properties of the scale functions, which will be crucial for further proofs in this paper.

At the beginning, let us cover the behaviour of the scale functions at zero. Recall that is a Lévy triple of the process and set when process is of bounded variation this quantity then represents drift of the process. Then

| (5) |

From (3) one can see that the initial value of equals . Whereas, for , one can find in [18, 21] that

| (6) |

The initial value of equals (see e.g., [15])

Moreover, for the following proposition was proved in [6].

Proposition 1.

In general, is a.e. continuously differentiable and its derivative is of the form

In particular, if is of unbounded variation, then is . On the other hand, if we assume that for is of bounded variation, then is also .

3. Impulse strategy with the Parisian ruin

Let us present the candidate to be an optimal strategy for the dividend problem described in Section 2.2. Formally, define the so-called impulse strategy . Set two constants and such that and . Next, fix as a set of the stopping times, such that:

The strategy is defined as

Then, the controlled risk process is of the form . Note that in the terms of one can write

and for . Therefore, the impulse strategy is to reduce the risk process to whenever the process exceeds level . It is assumed that the distance between and must be greater than , because after paying the transaction costs there must be something left for shareholders. Additionally, the condition that is a consequence of (2).

Before we give necessary conditions for strategy to be optimal, we need to consider the form of the value function as a helping tool for the further investigations.

3.1. Representation of the value function

Proposition 2.

The function for the strategy with the ruin time is of the form:

| (7) |

Proof.

At the beginning of the proof note that it is sufficient to prove this Proposition only for , because is a Markov process and if we are above level we put the process into level immediately. Also recall the discussions that precede equality (4).

Assume that . The first time when we paid dividends is that means that we must wait until the first time when process is greater that . Using strong Markov property we have that:

| (8) |

where last equality follow from (4). If we are at point we paid and decrease by . Again by strong Markov property we have:

Next step is to just solve above equation with respect to . We obtain:

Finally, we must put above formula into to get the result. ∎

The idea of finding optimal points leads to finding minimum of the function below

| (9) |

Let us denote domain of this function as . Let be a set of from that minimize function g:

Also fix set

Proposition 3.

For the set is not empty and for each we have

| (10) |

Also we know that in this case there are following possibilities : or .

Proof.

At the beginning we will show that if function is not attaining its minimum.

In the first inequality we used

| (11) |

Next inequality follows from the mean value theorem and the simple fact that . Last inequality is a consequence of for all and all . Note that and for that reason last statement follows. We get that, is not attained when , thus we can assume that there exist such that

In the next step we will show the same for . Namely

Note that we used only (11) in the first inequality and the property that is increasing in the second inequality. Last step is to consider the case when converge to the line .

We used, again, mean value theorem and fact that . We check that infimum of is not reached when or or converge to . Because of it and the continuity of we get that is not empty and we are left with the following possibilities

-

(i)

First is that belong to the interior of . In this case, using the fact that is partial differentiable in and , we get that

And hence we obtain (10) and .

-

(ii)

The second possibility is when . Then we have that minimizes function . We get because .

∎

To start the optimisation reasoning, we need the following proposition and lemma.

Proposition 4.

Assume that . Then for each we have that

Proof.

Lemma 5.

Let and . Then:

| (12) |

Proof.

Note that is an increasing function and because of that one can assume . Consider the following possibilities:

-

(1)

for

-

(2)

For ,

The above inequality follows from fact that , so minimize function

-

(3)

For ,

Since , the last inequality follows from point (2) with .

∎

3.2. Optimality

For the remainder of the paper, we will focus on verifying the optimality of the impulse strategy at threshold level . The proof is led by standard Markovian arguments to show that the impulse strategy fulfils the Verification Lemma. However at the beginning we will prove the following fact.

Fact 6.

Refracted process is a Feller process and its infinitesimal generator is of the form

| (13) |

where and f is a function on such that is well defined.

Proof.

For , and a non-negative or bounded measurable function define . It is sufficient to verify the following conditions:

-

(1)

For all , .

-

(2)

For all , .

-

(3)

For all , is a map from to .

-

(4)

For all , .

Here denotes the space of continuous functions vanishing at infinity. It is a Banach space when equipped with

the uniform norm .

Since the process is a Strong Markov process (for details see [16]) one can observe that condition

(1) is automatically fulfilled. Condition (2) is obvious. To prove (3) and (4) the reasoning is similar as in [22] except that we need to use fluctuation identities obtained in [16].

The form of the generator follows i.a. from [13] with and . ∎

Lemma 7 (Verification Lemma).

Suppose is an admissible dividend strategy such that is sufficiently smooth on (i.e. its first or second derivative (for of bounded or unbounded variation respectively) has at most finite number of single discontinuities), satisfies

| (14) | ||||

| (15) |

Then for almost every and hence is an optimal strategy.

Proof.

By the definition of as a supremum, it follows that for all . We write and show that for all for all .

Fix . Let be the sequence of stopping times defined by . Since is a semimartingale (see e.g., [24], [25]) and is sufficiently smooth on we will use to the stopped process the Bouleau and Yor [3] formula for bounded variation processes and the change of variables/Meyer-Itô’s formula (cf. Theorem IV.71 of [23]) for unbounded variation case, and deduce that under :

where we use the following notation: and for any process with left-hand limits. Rewriting the above equation leads to

where is a zero-mean -martingale. Hence using the assumptions (14), (15) we obtain that

| (16) |

Now, taking expectations in (16), using the fact that is a zero-mean -martingale and , letting and go to infinity ( -a.s.), and the dominated convergence gives

which completes the proof. ∎

Remark 8.

The lemma presented below requires some smoothness on the NPV of a policy. In the view of Proposition 4 it means that some smoothness conditions on the scale function are required. We will call the scale function sufficiently smooth if when is of bounded variation. From Theorem 2.9 of [17] one can see that a necessary and sufficient condition for this is that the Lévy measure has no atoms. When X is of unbounded variation we call the scale function sufficiently smooth if and is absolutely continuous on with a density which is bounded on sets of the form , . Moreover, in Theorem 2.6 of [17] it is proved that if the Gaussian coefficient is strictly positive. Note that the term sufficiently smooth is used here in a slightly weaker sense (which is explained in detail in the Lemma below).

Proof.

From Lemma 5 one can see that it is sufficient to prove that (14) holds. At first to get that , for one can observe that from Proposition 4 (for ) it is enough to show that is a -martingale. Indeed, let , using (4) together with fact that , one can get

From Proposition 1 the derivative of scale function does not exist at , when is of bounded variation. Moreover, when the second left-derivative of at does not equal zero and hence is not well defined. Therefore we claim that the result below holds for almost every . Indeed, it is sufficient to show that for any

| (17) |

almost surely, where is the right-continuous modification of . One can prove it using the occupation formula for the semi-martingale local time (see e.g. [23], Corollary 1, p.219). For details see Lemma 6 in [20], where the case was considered. Since process of bounded variation is a quadratic pure jump semimartingale (see e.g. [23], Theorem 26, p.71) then (17) automatically holds. ∎

Theorem 10.

Suppose that is sufficiently smooth and that there exists such that

| (18) |

Then the strategy is an optimal strategy for the impulse control problem.

Proof.

From Lemma 5 one can see that it is sufficient to prove that (14) holds. At first, from the proof of Lemma 9 we obtain that , for . On the other hand, if we get that . This follows from the Proposition 4 which gives that , where is the value of the barrier strategy at level in the de Finetti problem and fact that

The above inequality one can prove using ideas from [20][Theorem 2] together with (18). ∎

4. Examples

In this part, we will present the results concerning the numerical calculations of the optimal impulse policy . From Proposition 2 we know that when is not an empty set, then need to satisfy one of the possibilities listed there. Such an observation will define the way of constructing numerical calculations. However, to even start the computations one need to know how to calculate Parisian refracted scale function. Therefore, we will find analytical representation for and for the linear Brownian motion and for the Crámer-Lundberg process with the exponential claims. Moreover, we will prove that for these two processes there is a unique policy which is optimal for the impulse control problem.

4.1. Linear Brownian motion

Let us assume that process is a linear Brownian motion, which can be represented as

where and . Fix and . Recall that (see, e.g. [5])

where

and

Our first step is to present the formula for .

Proposition 11.

For the linear Brownian motion the function is of the following form

Proof.

The proof contains simple calculations which involves the following relations between parameters of and

| (19) |

∎

Now we will consider the formula for the function .

Proposition 12.

In the linear Brownian motion setting function is of the following form.

-

•

For

-

•

For

where is the cumulative distribution function of the standard normal variable.

Proof.

We will separate our proof into two parts

-

•

For . Using formula for the from the last proposition one can get

Hence, one need to calculate two integrals

and

For the first integral, one can use . However, for the second integral we need to do some calculations. One can get the following

Therefore, for the formula for the Parisian refracted scale function is of the following form

-

•

Let us assume that . Then

Therefore, after some calculations one can get that

∎

Proposition 13.

Fix any and , there exist a constant such that the function is decreasing on and is increasing on . This also implies the same for .

Proof.

To prove the thesis, we will examine the second derivative with respect to of . Indeed, using Proposition 11 and the above explicit formula for the scale function , we get

where . The constant is strictly positive, because the scale function is increasing and strictly positive on whole positive half-line. Now, if , then function is positive for all and hence . If , then is an increasing and unbounded function of as a sum of two increasing exponential functions. This completes the proof for . For we get the thesis directly from its definition. ∎

Theorem 14.

For the linear Brownian motion model there is a unique policy which is optimal for the impulse control problem.

Proof.

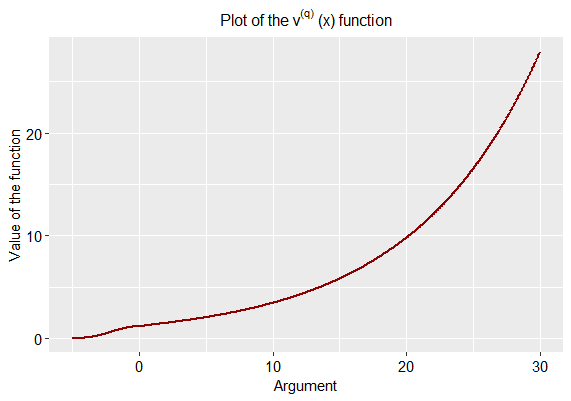

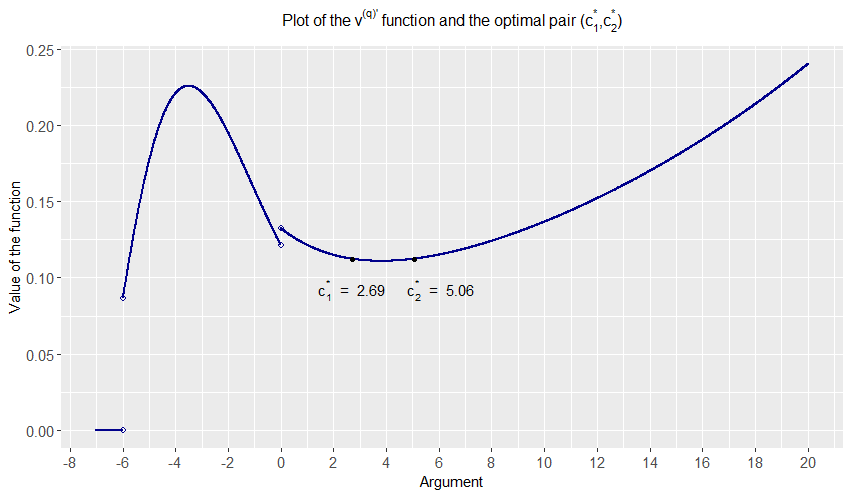

Now, we will start numerical examples with the picture of and . Let us consider the following parameters

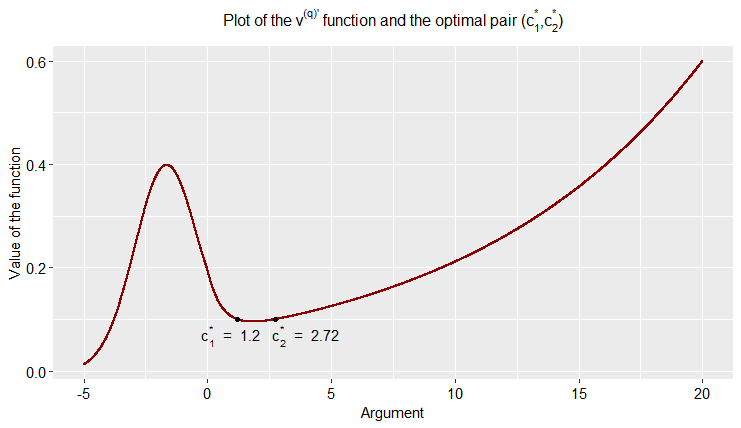

Note that the shape of this function is similar as for the classic scale function for linear Brownian motion. In the next picture we will consider with the optimal points and

The first interesting observation is the shape of this function for . One can see that belongs to the set from the Proposition 3. One can also observe that our optimal pair satisfy condition from the Theorem 10.

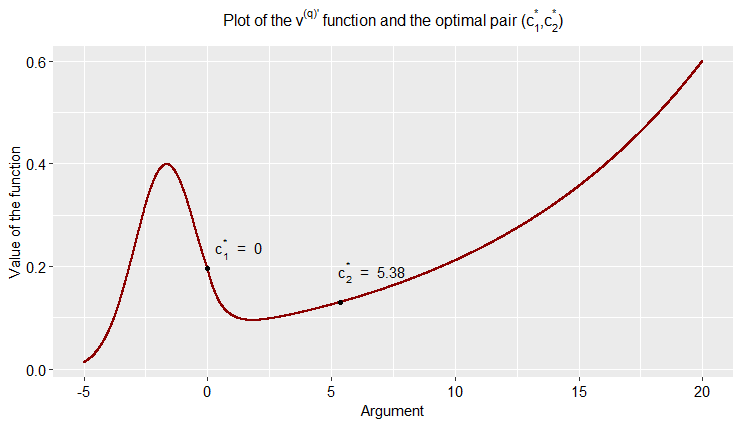

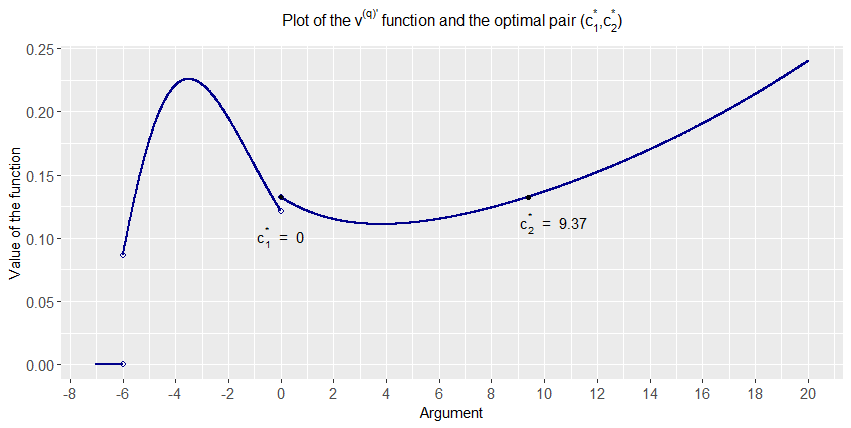

Moreover, one can be interested in the behaviour of the optimal pair with the respect to the change of the parameter . Therefore, let us set

Thus, one can see that depending on the parameters of the process one can get different possibilities from the Proposition 3.

4.2. Cramér-Lundberg process

In the second example we will consider the Cramér-Lundberg process

where , is an sequence of exponential random variables with the parameter , is a homogeneous Poisson process with the intensity . We also assume that the Poisson process and the exponential random variables are mutually independent. For this process the scale function is of the following form (see, e.g. [5])

where

Scale function for the process is of the form

where

Proposition 15.

For , we have that

Proof.

To obtain such representation we had to used the following relations between the parameters of scale functions

and

∎

For a Parisian refracted scale function we will obtain formula, which will be divided into three parts. Nevertheless, before we state the representation we have from [21], that

| (20) |

Proposition 16.

In the Crámer-Lundberg setting the function is of the following form

-

•

For

where

-

•

For

-

•

For

where is an incomplete gamma function.

Proof.

We will divide this proof into the following parts

- •

-

•

For

Note that, in this case, is of the following formWith the probability one, random variable , can achieve at most value and we know that iff , thus

Using this observation rest of the proof involve simply, but long, calculations, thus let us omit this.

-

•

For

As we state in the previous case, when then . Therefore and

∎

Proposition 17.

Fix and , there exist a constant such that the function is decreasing on and is increasing on . This also implies the same for .

Proof.

At the beginning let us note that

| (21) |

From the above and Proposition 15 one can obtain

Therefore, one can rewrite formula for as

From this, one can also obtain more explicit form

Let us fix the following notation

Then can be written as

One can check that and and thus

Then, from one can conclude that . Next, we are interested in the sign of

If then is positive on the whole positive half-line. In such case . If then one can see that is an increasing and unbounded function. This ends the proof. ∎

Theorem 18.

For the Cramér-Lundberg model there is a unique policy which is optimal for the impulse control problem.

Proof.

Using the above results one can plot the picture of the example of and for this process. Namely, let us set

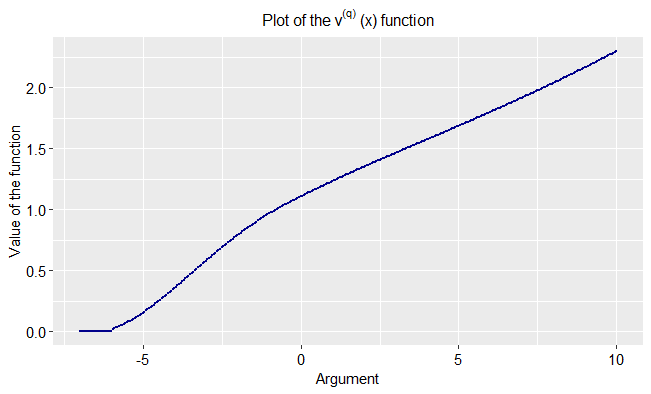

Note that, we set such parameters that . Moreover, we know that if , therefore we will consider x

As in the linear Brownian motion setting, one can also see the similar shape of Parisian scale function with the shape of classical scale function. However, even if this is not directly clear from the Figure 4, is not a continuous function at . Now, we will also show the plot of the with the optimal points with

One can see from the Figure 5 that we are in the case when belongs to the set . In addition, let us note that optimal pair satisfy the condition from the Theorem 10. As in the case of the linear Brownian motion we would like to manipulate with the parameter . Let us set

One can see from the Figure 6 that in such case costs of the transaction are to high and after dividend payment surplus level is moved into level zero. Note that we put point and into plot of only for illustrating purpose. It is clear that in such case we are not interested in the value of because such function is not well define in this point.

References

- [1] Avram F., Palmowski Z. and Pistorius M. R., On the optimal dividend problem for a spectrally negative Lévy process, The Annals of Applied Probability, 17 156-180 (2007)

- [2] Bertoin, J. Lévy Processes, Cambridge Tracts in Mathematics (1996)

- [3] Bouleau N. and Yor M., Sur la variation quadratique des temps locaux de certaines semimartingales, C. R. Acad. Sci. Paris 292 (1981) 491–494.

- [4] Czarna I. and Palmowski Z., Ruin probability with Parisian delay for a spectrally negative Lévy risk process, Appl. Probab. 48 984–1002. (2011)

- [5] Czarna I., Parisian ruin probability with a lower ultimate bankrupt barrier, Scandinavian Actuarial Journal, Vol. 2016, No. 4, 319-337 (2016)

- [6] Czarna I., Pérez J.-L., Rolski T., Yamazaki K., Fluctuation theory for level-dependent Lévy risk processes, Stochastic Processes and their Applications, doi.org/10.1016/j.spa.2019.03.006 (2019)

- [7] Chesney M., Jeanblanc-Picqué M., Yor M., Brownian excursions and Parisian barrier options, Adv. in Appl. Probab. 29 165–184. (1997)

- [8] de Finetti B., Su un’impostazion alternativa dell teoria collecttiva del rischio, Transactions of the XVth International Congress of Actuaries 2, 433-443 (1957)

- [9] Gerber H. U. and Shiu E. S. W., Optimal dividends: Analysis with Brownian motion, North American Actuarial J. 8 1–20. (2004)

- [10] Gerber H. U. and Shiu E. S. W., On Optimal Dividend Strategies in the Compound Poisson Model, North American Actuarial Journal, Vol. 10 (2006)

- [11] Hubalek F. and Kyprianou E. Old and New Examples of Scale Functions for Spectrally Negative Lévy Processes, In Seminar on Stochastic Analysis, Random Fields and Applications VI, (R. Dalang, M. Dozzi and F. Russo, eds.). Progress in Probability 63 119-145. Springer Basel. (2011)

- [12] Jeanblanc M. and Shiryaev A. N., Optimization of the flow of dividends, Russian Math. Surveys 50 257–277 (1995)

- [13] Khoshnevisan D. and Schilling R., From Lévy-Type Processes to Parabolic SPDEs, Advanced Courses in Mathematics - CRM Barcelona, Birkhäuser Basel (2016)

- [14] Kuznetsov A., Kyprianou A.E., Rivero V. The Theory of Scale Functions for Spectrally Negative Lévy Processes, In: Lévy Matters II. Lecture Notes in Mathematics, Vol. 2061. Springer, Berlin, Heidelberg (2012)

- [15] Kyprianou A. E., Introductory Lectures on Fluctuations of Lévy Processes with Applications, Springer, Berlin (2006).

- [16] Kyprianou A. E., and Loeffen R. L., Refracted Lévy processes, Annales de l’Institut Henri Poincaré - Probabilités et Statistiques 46, no. 1, 24-44 (2010)

- [17] Kyprianou A.E., Rivero V. and Song R., Smoothness and convexity of scale functions with applications to de Finetti’s control problem, J. Theor. Probab. (2010) 23: 547.

- [18] Lkabous M. A., Czarna I. and Renaud J.-F., Parisian ruin for a refracted Lévy process, Insurance: Mathematics and Economics, Vol. 47, 153-165 (2017)

- [19] Loeffen R. L., On optimality of the barrier strategy in de Finetti’s dividend problem for spectrally negative Lévy processes, Ann. Appl. Probab. Volume 18, Number 5, 1669-1680. (2008)

- [20] Loeffen R. L., An optimal dividends problem with transaction costs for spectrally negative Lévy processes, Ann. Appl. Probab. Vol. 18, no. 5, 1669-1680 (2008)

- [21] Loeffen R. L., Czarna I. and Palmowski Z., Parisian ruin probability for spectrally negative Lévy processes, Bernoulli 19(2), 599-609 (2013)

- [22] Noba K. and Yano K., Generalized refracted Lévy process and its application to exit problem, Stochastic Processes and their Applications Vol. 129, no. 5, p. 1697-1725 (2019)

- [23] Protter P., Stochastic integration and differential equations, 2nd ed., version 2.1, Springer, 2005.

- [24] Schilling R.L., Growth and Hölder conditions for the sample paths of a Feller process, Probab. Theor. Relat. Fields 112, 565–611 (1998)

- [25] Schnurr A., On the semimartingale nature of Feller processes with killing, Stoch. Proc. Appl. 122, 2758–2780 (2012)