A Class of Solvable Multidimensional Stopping Problems in the Presence of Knightian Uncertainty

Abstract

We investigate the impact of Knightian uncertainty on the optimal timing policy of an ambiguity averse decision maker in the case where the underlying factor dynamics follow a multidimensional Brownian motion and the exercise payoff depends on either a linear combination of the factors or the radial part of the driving factor dynamics. We present a general characterization of the value of the optimal timing policy and the worst case measure in terms of a family of an explicitly identified excessive functions generating an appropriate class of supermartingales. In line with previous findings based on linear diffusions, we find that ambiguity accelerates timing in comparison with the unambiguous setting. Somewhat surprisingly, we find that ambiguity may result into stationarity in models which typically do not possess stationary behavior. In this way, our results indicate that ambiguity may act as a stabilizing mechanism.

AMS Subject Classification: 60J60, 60G40, 62L15, 91G80

Keywords: -ambiguity, multidimensional Brownian motion, diffusion processes, Bessel processes.

1 Introduction

Gaussian processes and, more precisely, Brownian motion plays a prominent role in modeling factor dynamics in standard financial models considering the optimal timing of irreversible decisions in the presence of uncertainty. In the benchmark setting all the uncertainty affecting the decision is summarized into a single probability measure describing completely the probabilistic structure of the underlying intertemporally fluctuating factor dynamics. However, as originally pointed out in Knight, (1921), in reality there are circumstances where a decision maker faces unmeasurable uncertainty on the plausibility or credibility of a particular probability measure (so-called Knightian uncertainty). In such a case a decision maker may have to make a decision based on several or even a continuum of different measures describing the probabilistic structure of the alternative states of the world.

Ambiguity was first rigorously axiomatized based on the pioneering work by Knight, (1921) in a atemporal multiple priors setting in by Gilboa and Schmeidler, (1989) (for further refinements, see also Bewley, (2002), Klibanoff et al., (2005), Maccheroni et al., (2006) and Nishimura and Ozaki, (2006)). The atemproal axiomatization was subsequently extended into an intertemporal recursive multiple priors setting by, among others, Epstein and Wang, (1994), Chen and Epstein, (2002), Epstein and Miao, (2003), and Epstein and Schneider, (2003). The impact of ambiguity on optimal timing decisions was originally studied in Nishimura and Ozaki, (2004) in a job search model. They subsequently extended their original analysis in Nishimura and Ozaki, (2007) by considering the impact of Knightian uncertainty on the optimal timing decisions of irreversible investment opportunities in a continuous time model based on geometric Brownian motion. Alvarez E., (2007) focused on the impact of Knightian uncertainty on monotone one-sided stopping problems and expressed the value as well as the optimality conditions for the stopping boundaries in terms of the minimal excessive mappings of the underlying diffusion under the worst case measure. Riedel, (2009), in turn, analyzed discrete time optimal stopping problems in the presence of ambiguity aversion and developed a general minmax martingale approach for solving the considered problems (see also Miao and Wang, (2011) for an analysis of the problem for a general discrete time Feller-continuous Markov processes). The approach developed in Riedel, (2009) was subsequently extended to a continuous time setting in Cheng and Riedel, (2013). In Cheng and Riedel, (2013), the value of the optimal policy was proven to be the smallest right continuous -martingale dominating the exercise payoff process. Christensen, (2013) investigated the optimal stopping of linear diffusions by ambiguity averse decision makers in the presence of Knightian uncertainty and identified explicitly the minimal excessive mappings generating the worst case measure as well as the appropriate class of supermartingales needed for the characterization of the value of the optimal policy. Epstein and Ji, (2019) investigated optimal learning in the case where the underlying driving Brownian motion is subject to drift ambiguity. More recently, Alvarez E. and Christensen, (2019) extended the approach developed in Christensen, (2013) to a multidimensional setting and investigated the impact of Knightian uncertainty on the optimal timing policies of ambiguity averse investors in the case where the exercise payoff is positively homogeneous and the underlying diffusion is a two-dimensional geometric Brownian motion. They found that in a multidimensional case, ambiguity does not only affect the optimal policy by altering the rate at which the underlying processes are expected to grow, it also impacts the rate at which the problem is discounted.

Given the findings in Alvarez E. and Christensen, (2019), our objective in this paper is to analyze the impact of Knightian uncertainty on the optimal timing policy of an ambiguity averse decision maker in the case where the underlying follows a multidimensional Brownian motion. We study the general stopping problem and identify two special cases under which the problem can be explicitly solved by reducing the dimensionality of the problem and then utilizing the approach developed in Christensen, (2013). We characterize the value and optimal timing policies as the smallest majorizing element of the exercise payoff in a parameterized function space. Our results demonstrate that Knightian uncertainty does not only accelerate the optimal timing policy in comparison with the unambiguous benchmark case, it also may result into stationary behavior to the controlled system even when the underlying system does not possess a long run stationary distribution. This observation illustrates how ambiguity may in some cases have a nontrivial impact on the stochastic dynamics of the underlying processes under the worst case measure.

The contents of this paper are as follows. In Section 2 we present the underlying stochastic dynamics, state the considered class of optimal stopping problems and state a characterization of the impact of ambiguity on the optimal timing policy and its value. In Section 3 we focus on payoffs depending on linear combinations of the driving factors. In Section 4 we then focus on radially symmetric payoffs. Finally, Section 5 concludes our study.

2 Underlying Dynamics and Problem Setting

Let be -dimensional standard Brownian motion under the measure and assume that . As usually in models subject to Knightian uncertainty, let the degree of ambiguity be given and denote by the set of all probability measures, that are equivalent to with density process of the form

for a progressively measurable process satisfying the inequality for all . That is, we assume that the density generator processes satisfy the inequality for all .

Assume now that denotes the underlying diffusion under the measure . Our objective is now to consider the following optimal stopping problem

| (2.1) |

where is a measurable function which will be specified below in the two cases considered in this paper. As usually, we denote by the continuation region where stopping is suboptimal and by the stopping region. The specification of the considered stopping problem results into the following lemma characterizing the impact of ambiguity on the optimal stopping policy and its value in a general setting.

Lemma 2.1.

Increased ambiguity accelerates optimal timing by decreasing the value of the optimal policy and, thus, shrinking the continuation region where waiting is optimal. Formally, if then for all and .

Proof.

Assume that . Since we notice that

implying that for all . Assume now that . Since in that case we notice that as well. Consequently, completing the proof of our lemma. ∎

Lemma 2.1 shows that the sign of the relationship between the degree of ambiguity and optimal timing is positive. At the same time, increased ambiguity decreases the value of the optimal stopping policy showing that the highest value is attained in the absence of ambiguity. This mechanism is naturally not that surprising since it essentially states that the larger the set of potentially detrimental outcomes gets, the smaller is the achievable value.

We now notice that under the measure defined by the likelihood ratio

we naturally have that

where denotes -Brownian motion. Introduce the differential operator associated with the underlying processes under the measure by

For a twice continuously differentiable function , the Itô-Döblin theorem yields that under the measure

| (2.2) | ||||

Now, minimizing with respect to under the condition leads to the worst case density generator

where denotes the standard Euclidean norm. Assume now that there exists a twice continuously differentiable function satisfying the partial differential equation

| (2.3) |

on some . In that case

| (2.4) | ||||

where and is open with compact closure in . Taking expectations result in

with identity only when . Unfortunately, solving the partial differential equation (2.3) explicitly is typically impossible. Fortunately, there are two cases where dimension reduction techniques apply and permit the transformation of the original multidimensional problem into a solvable one-dimensional setting. We will focus on these problems in the following sections.

3 Payoff Depending on a Linear Combination of Factors

Linear combinations of independent normally distributed random variables are normally distributed. On the other hand, linear combinations of independent Brownian motions are continuous martingales and, hence, constitute a time change of Brownian motion. Given these observations, consider now the case where the exercise payoff reads as

| (3.1) |

where is a constant parameter vector and is a measurable function. Focusing now on functions

results into the worst case prior characterized by the density generator

In this case, solving

results into solving

on and

on on . Defining now the constants

, and then shows that

on and

on . Given these functions, let be an arbitrary reference point and define the twice continuously differentiable and strictly convex function as , where

are two mappings satisfying the conditions and . Therefore, the function constitutes the solution of the boundary value problem

Analogously, we let and denote the solutions associated with the extreme cases where or . As was demonstrated in Christensen, (2013) these functions generate an useful class of supermartingales for solving optimal stopping problems in the presence of ambiguity. To see that this is indeed the case in this multidimensional setting as well, we notice by applying the Itô-Döblin theorem to the function that

Since for admissible density generators satisfying the condition , we observe that for all and, therefore, that

with identity only when Consequently, we notice that in the present case

for all . Utilizing standard optional sampling arguments show that the process is actually a positive -martingale and, therefore, a supermartingale.

It is also at this point worth pointing out that the process satisfies the SDE

| (3.2) |

Since for admissible density generators satisfying the condition we notice that (3.2) has a unique strong solution. Especially, under we have

which is a standard Brownian motion with alternating drift. Interestingly, we observe that while standard Brownian motion does not have a stationary distribution, the controlled process does. More precisely, for a fixed reference point the stationary distribution of the controlled diffusion reads as (a Laplace-distribution)

Moreover, the process is positively recurrent meaning that hitting times to constant boundaries are almost surely finite.

Having characterized the underlying dynamics and the class of harmonic functions resulting into the class of supermartingales needed in the characterization of the value, we now observe that the conditions of Theorem 1 in Christensen, (2013) are satisfied and, therefore, that we can characterize the value in a semiexplicit form as stated in the following.

Theorem 3.1.

(A) For all we have that

| (3.3) |

and the infimum with respect the reference point is a minimum.

(B) A point is in the stopping region if, and only if, there exists a such that

and .

Proof.

The alleged claims are direct implications of Theorem 1 in Christensen, (2013). ∎

Theorem 3.1 extends the findings of Theorem 1 in Christensen, (2013) to the present case. The main reason for the validity of this extension is naturally the fact the even though the process is multidimensional, the process is not and we can, therefore, analyze the problem in terms of the one-dimensional characteristics. The representation (3.3) is naturally useful in the determination of the value and the associated worst case prior since it essentially reduces the analysis of the original problem into the analysis of a ratio with known properties without having to invoke strong smoothness or regularity conditions. In order to illustrate the usefulness of the finding of Theorem 3.1 we now consider an interesting class of exercise payoffs resulting into an explicitly solvable symmetric setting within this class of models. Our main findings on these problems are summarized in the following.

Theorem 3.2.

Assume that the exercise payoff is even, that is, that for all . Then, the ratio is even as well and if there exists a unique threshold

so that is increasing on and decreasing on , then the value of the optimal stopping policy reads as

| (3.4) |

Moreover, the optimal density generator resulting into the worst case measure is

Proof.

We first observe utilizing the identities and that for all . Consequently, we notice that the ratio is even as claimed. Assume now that there exists a unique maximizer of the ratio so that is increasing on and decreasing on .

Denote now by the first exit time of the process from the set and by the proposed value function (3.5). It is clear that since we have for any admissible stopping time that

Consequently, we find that

Consider now the process

As was shown earlier, is a positive -martingale. Moreover, since the process characterized by the SDE

is positively recurrent we know that the first exit time is -almost surely finite. Consequently, the assumed maximality of the ratio guarantees that Theorem 4 of Beibel and Lerche, (1997) applies and we find that (see also Lerche and Urusov, (2007), Christensen and Irle, (2011), and Gapeev and Lerche, (2011))

proving that for all . In order to reverse this inequality we first observe that if then we naturally have that

proving that for all and that for . Finally, if , then -almost surely and

completing the proof of our theorem. ∎

Remark 3.1.

It is worth pointing out that the positive homogeneity of degree of the constants as functions of the parameter vector guarantees that the function remains unchanged for parameter vectors of equal Euclidean length, that is, for vectors satisfying the condition . Consequently, solving the stopping problem with respect one results into an optimal policy and value for an entire class of problems constrained by the requirement that .

It is furthermore interesting to note that already in dimension the underlying process under the worst case measure is a Brownian motion with broken drift as studied in Mordecki and Salminen, (2019). Therefore, in the class of problems studied in this paper, optimal stopping problems with broken drift naturally arise. Here, however, the breaking point always lies in the continuation set.

Theorem 3.2 characterizes the optimal timing policy in the symmetric case where the exercise payoff is even and the ratio attains a unique global maximum on (and by symmetry also on ). The findings of Theorem 3.2 clearly indicate that in the present setting symmetry is useful in the characterization of the value and the worst case measure. To see that this is indeed the case, we now present a general observation valid for symmetric periodic payoffs.

Theorem 3.3.

Assume that the exercise payoff satisfies the following conditions

-

(A)

The function is periodic with period length ;

-

(B)

There exists a threshold so that , where , for all ;

-

(C)

The function satisfies the symmetry condition for all .

Assume also that there exists a unique interior threshold

so that is increasing on and decreasing on . Then, the value of the optimal stopping policy reads as

| (3.5) |

where and , . Moreover, the optimal density generator resulting into the worst case measure is

Proof.

The assumed periodicity and symmetry of the exercise payoff implies that we can focus on the behavior of the ratio on (from a maximum to the next). It is clear that since and we have

for . Consequently, assumption (C) guarantees that

for all . On the other hand, our assumption on the existence of an interior maximizing threshold and the symmetry of guarantees that

and

Combining this result with the assumed periodicity of the payoff then shows that

The alleged optimality and characterization of the optimal density generator is now identical with the proof of our Theorem 3.2. ∎

3.1 Discontinuous Asymmetric Digital Option

In order to illustrate our general findings, we now focus on the discontinuous asymmetric digital option case, where , where are known positive constants. In the present setting it suffices to investigate the behavior of the functions and Standard differentiation yields and , where

Since

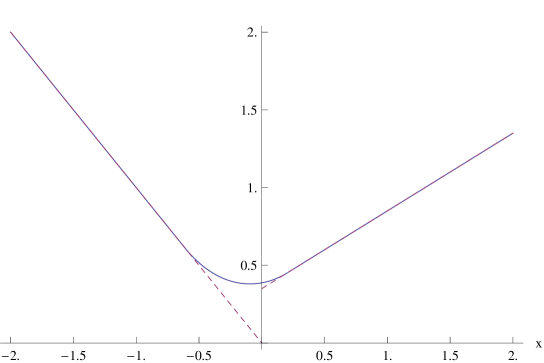

, and we notice that there exists two thresholds and so that the first order conditions are satisfied. Moreover, the thresholds are increasing as functions of the reference point and satisfy the limiting conditions , and . Thus, we notice by utilizing our results above that , and . Consequently, we notice that there is a unique such that is met. Two cases arise. If , then is the optimal state at which the density generator switches from one extreme to another and the value of the optimal policy reads as

Especially, the value satisfies the smooth-fit condition at the optimal boundaries and . This case is illustrated in Figure 1 under the assumptions that , and (implying that , and )

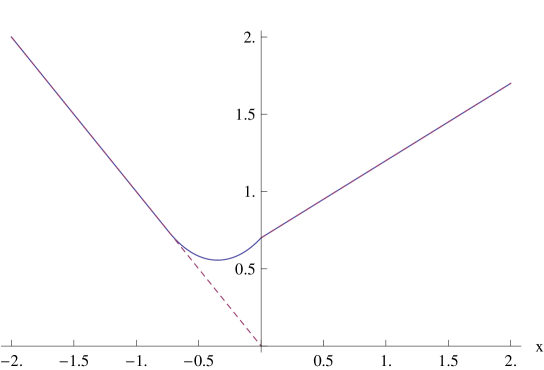

However, if then the situation changes since in that case becomes an optimal stopping boundary at which the value coincides with the payoff in a nondifferentiable way. In that case the value reads as

where the optimal boundary and the critical switching state are the unique roots of the equations

This case is illustrated in Figure 2 under the assumptions that , and (implying that , and )

It is at this point worth pointing out that in the case where and the exercise payoff is continuous and even and the findings of Theorem 3.2 applies. In that case, the optimal boundaries can be solved from the optimality condition .

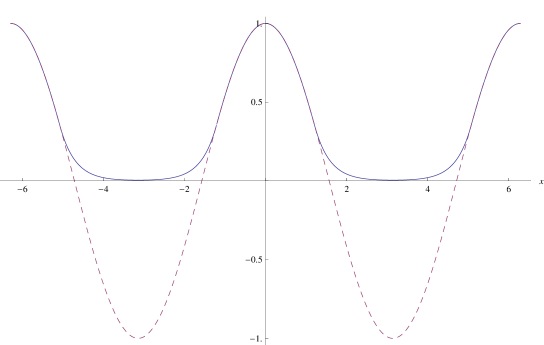

3.2 Periodic and Even Payoff

In order to illustrate how the approach applies in the periodic setting resulting into multiple boundaries, consider the periodic payoff . Since the payoff is even, attains its maxima at the points , its minima at the points , and is symmetric on the sets , , we notice that we can extend the findings of Theorem 3.2 and make an ansatz that the optimal reference point is . To see that this is indeed the case, we first observe that if then , since and

for all and . Consequently, it is sufficient to investigate the ratio on . Standard differentiation yields , where

Noticing now that ,

and

we notice that equation has a unique root such that

It is now clear that the value of the optimal stopping policy reads as

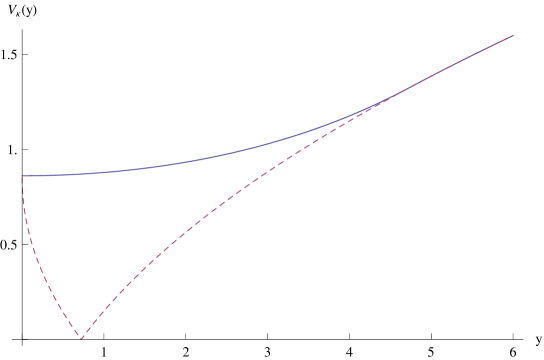

This value and the optimal policies are illustrated for in Figure 3 under the assumptions that and (implying that the optimal thresholds are ).

It is worth noticing that the worst case prior is induced in the present case by the density generator

for all . Essentially, the optimal density generator tends to drive the dynamics of the underlying diffusion towards the

minim points of the exercise payoff.

4 Radially Symmetric Payoff

It is well-known from the literature on linear diffusions that the radial part of a multidimensional Brownian motion constitutes a Bessel process. Our objective is now to exploit this connection by focusing on exercise payoffs which are radially symmetric. More precisely, we now assume that the payoff is of the form

| (4.1) |

where is a known measurable function. We now make an ansatz and focus on functions which are radially symmetric, that is, on functions of the form

where is assumed to be twice continuously differentiable on . In this case, a short calculation yields that the worst case prior becomes

so that the worst case drift points towards the origin or away from it, resp. In this case, solving

results into solving

on and

on on . Denote now by and by the Whittaker functions of the first and second type, respectively, and define the functions , and , where

, and

Making the substitution show that the solutions of these ODEs read as (cf. Linetsky, (2004))

on and as

on . As in the previous subsection, we now let be an arbitrary reference point and define the twice continuously differentiable function as the solution of the boundary value problem

| (4.2) | ||||

We again find that , where

, and . As in the case of the previous subsection, we define the two cases associated with the extreme reference points by

where and denote the confluent hypergeometric functions of the first and second type, respectively. It is worth noticing that since the lower boundary is entrance for the underlying diffusion process we have that (cf. p. 19 in Borodin and Salminen, (2015))

when . The upper boundary is, in turn, natural for the underlying diffusion process and, hence, we have that (cf. p. 19 in Borodin and Salminen, (2015))

when . However, in contrast with natural boundary behavior, we now notice that in the extreme case

Again, we observe that the function is convex.

Lemma 4.1.

The function is strictly convex on .

Proof.

is nonnegative and decreasing on . Consequently, we notice by invoking (4.2) that

demonstrating that is strictly convex on . On the other hand, (4.2) also implies that on we have

Since

where , we notice by integrating from to that

On the other hand, since

we finally find that

proving that is strictly convex on as well. ∎

Utilizing the Itô-Döblin theorem now shows that the process satisfies the SDE

| (4.3) |

where is a Brownian motion under the measure characterized by the density generator

Hence, we again observe that the controlled process has a stationary distribution for a fixed reference point . In the present case it reads as

where

and

It is also worth noticing that utilizing the Itô-Döblin theorem to the process results into the SDE

which constitutes a Bessel process of order with an alternating drift.

A modified characterization of the representation presented in Theorem 3.1 is naturally valid in this case as well, since in the present case the set of admissible reference points is . It is also worth noticing that the function is no longer symmetric and, hence, similar representations with the ones developed in Theorem 3.2 and in Theorem 3 are no longer possible. Moreover, since the lower boundary is entrance for the underlying process, policies which are radically different from the case considered in the previous section may appear. We will illustrate this point explicitly in the following subsection.

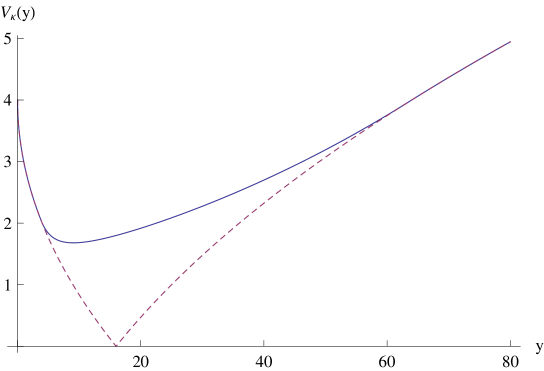

4.1 Nonlinear Straddle Option

In order to illustrate the peculiarities associated with the present case, let us consider the nonlinear straddle option case , where is an exogenously set fixed strike price. Consider first the behavior of the function

We notice that and

demonstrating that

Since is monotonically increasing and satisfies the inequality for , where is the unique root of , we find that for we have that

Hence, demonstrating that there is a unique satisfying the condition Noticing that

in turn demonstrates that is the unique threshold at which the ratio

is maximized. Moreover, , , and , where the threshold is the unique root of the first order optimality condition

Define now the monotonically increasing and continuously differentiable function as

Since is nonnegative and dominates for all it dominates as well. Hence, we observe by utilizing similar arguments as in the proof of Theorem 3.2 that

Given this function we immediately notice that if condition

is met, then dominates the exercise payoff for all as well. Therefore, we notice that in that case

However, if

| (4.4) |

then the optimal policy is no longer a standard single boundary policy. To see that this is indeed the case consider the behavior of the ratio

for all and . Define now for an arbitrary state the continuous difference as

Consider first the extreme case . It is clear from our analysis on the single boundary case treated above that is monotonically decreasing on , monotonically increasing on , and satisfies the limiting conditions and

by assumption (4.4). Combining these observations show that for all and, consequently, that . Consider now, in turn, the other extreme setting . Utilizing now completely analogous arguments as before, we notice that is monotonically increasing on , bounded for , and satisfies the limiting conditions and Consequently, we notice that for we have ,

and, therefore, that . Combining these results with the continuity of the difference proves that there is at least one such that implying that

Moreover, the optimal thresholds satisfy the ordinary first order optimality conditions

In this case the value reads as

Naturally, the set constitutes the stopping set in the present example.

In order to illustrate our findings numerically, we now assume that , and (implying that the critical cost below which the problem becomes a single boundary problem is ). The two boundary setting is illustrated in Figure 4 under the assumption that (implying that , and ).

The single boundary setting is, in turn, illustrated in Figure 5 under the assumption that (implying that ).

4.2 A truly two-dimensional modification

The explicit solvability of the problem described before is based on the dimension reduction due to the symmetry of the situation. Even when slightly breaking this symmetry, there is usually no hope to find such explicit solutions anymore. In the rest of this section, we will illustrate this by an example and show how these more general problems may be treated. We consider again the radially symmetric payoffs (4.1), but instead of assuming for the density process, we now assume that

and denote the set of all corresponding probability measures by We note that this ambiguity structure has been considered in Alvarez E. and Christensen, (2019). We write

and for the corresponding continuation set. As , it is clear that for all

and therefore

For the sake of simplicity, we now restrict our attention to the case and . In this case, it is – using the results of this section – easily seen that and are circles around 0. Although there is little hope for finding and explicitly, it is easy to infer the structure of the solution: The worst case measure is characterized by the density generator

Due to symmetry of the situation, the optimal stopping problem to be solved can be written as

for is in the upper quadrant , where is a Brownian motion with drift and (orthogonal) reflection on the boundaries of . Note that reflected Brownian motion in the quadrant were studied extensively, see Harrison and Reiman, (1981); Williams, (1985) to mention just two. Recently, the Green kernel has been found semi-explicitly (in the transient case), see Franceschi, (2019). This opens the door to characterize the unknown optimal stopping boundary using integral equation techniques, see Peskir and Shiryaev, (2006) for the general theory and Christensen et al., (2019) for a specific setting quite close to this one.

5 Conclusions

We analyzed the impact of Knightian uncertainty on the optimal timing policy of an ambiguity averse decision maker in the case where the underlying follows a multidimensional Brownian motion. We identified two special cases under which the problem can be explicitly solved and illustrated our findings in explicitly parameterized examples. Our results indicate that Knightian uncertainty does not only accelerate the optimal timing policy in comparison with the unambiguous benchmark case, it also may add stability to the dynamics of the underlying under the worst case measure. More precisely, even thought the underlying multidimensional Brownian motion does not converge in a long run to a stationary distribution, the controlled process does. This observation shows that ambiguity may in some circumstances have a profound and nontrivial impact on the underlying dynamics.

This study modeled the underlying random factor dynamics as a multidimensional Brownian motion and focused on two functional forms permitting the utilization of dimension reduction techniques and in that way resulting into stopping problems of linear diffusions. There is at least three natural directions towards which our chosen modeling framework could be attempted to be extended. First, even though most standard factor models rely on linear combinations of the driving factors, it would naturally be of interest to analyze how potential nonlinearities would affect the optimal timing decision in the presence of ambiguity. Especially, introducing state-dependent factors would cast light on the mechanisms how nonlinearities in factor dynamics affect the decisions of ambiguity averse decision makers. Second, carrying out a thorough analysis of the truly two-dimensional modification presented in subsection 4.2 would provide valuable information on the difference between the problems allowing dimensionality reduction and the problems which do not. Third, adding Bayesian learning to the considered class of problems would also be an interesting direction towards which our analysis could be extended. All these extensions are extremely challenging and at the present outside the scope of the this study.

References

- Alvarez E., (2007) Alvarez E., L. H. R. (2007). Knightian uncertainty, -ignorance, and optimal timing. Technical Report 25, Aboa Center of Economics, University of Turku.

- Alvarez E. and Christensen, (2019) Alvarez E., L. H. R. and Christensen, S. (2019). A Solvable Two-dimensional Optimal Stopping Problem in the Presence of Ambiguity. arXiv:1905.0542.

- Beibel and Lerche, (1997) Beibel, M. and Lerche, H. R. (1997). A new look at optimal stopping problems related to mathematical finance. Statist. Sinica, 7(1):93–108. Empirical Bayes, sequential analysis and related topics in statistics and probability (New Brunswick, NJ, 1995).

- Bewley, (2002) Bewley, T. F. (2002). Knightian decision theory. I. Decis. Econ. Finance, 25(2):79–110.

- Borodin and Salminen, (2015) Borodin, A. N. and Salminen, P. (2015). Handbook of Brownian motion-facts and formulae. Birkhäuser.

- Chen and Epstein, (2002) Chen, Z. and Epstein, L. (2002). Ambiguity, risk, and asset returns in continuous time. Econometrica, 70(4):1403–1443.

- Cheng and Riedel, (2013) Cheng, X. and Riedel, F. (2013). Optimal stopping under ambiguity in continuous time. Math. Financ. Econ., 7(1):29–68.

- Christensen, (2013) Christensen, S. (2013). Optimal decision under ambiguity for diffusion processes. Math. Methods Oper. Res., 77(2):207–226.

- Christensen et al., (2019) Christensen, S., Crocce, F., Mordecki, E., and Salminen, P. (2019). On optimal stopping of multidimensional diffusions. Stochastic Process. Appl., 129(7):2561–2581.

- Christensen and Irle, (2011) Christensen, S. and Irle, A. (2011). A harmonic function technique for the optimal stopping of diffusions. Stochastics, 83(4-6):347–363.

- Epstein and Ji, (2019) Epstein, L. G. and Ji, S. (2019). Optimal Learning under Robustness and Time-Consistency. Preprint, Boston University.

- Epstein and Miao, (2003) Epstein, L. G. and Miao, J. (2003). A two-person dynamic equilibrium under ambiguity. J. Econom. Dynam. Control, 27(7):1253–1288.

- Epstein and Schneider, (2003) Epstein, L. G. and Schneider, M. (2003). Recursive multiple-priors. J. Econom. Theory, 113(1):1–31.

- Epstein and Wang, (1994) Epstein, L. G. and Wang, T. (1994). Intertemporal asset pricing under knightian uncertainty. Econometrica, 62(2):283–322.

- Franceschi, (2019) Franceschi, S. (2019). Green’s functions with oblique neumann boundary conditions in a wedge. arXiv:1905.04049.

- Gapeev and Lerche, (2011) Gapeev, P. V. and Lerche, H. R. (2011). On the structure of discounted optimal stopping problems for one-dimensional diffusions. Stochastics, 83(4-6):537–554.

- Gilboa and Schmeidler, (1989) Gilboa, I. and Schmeidler, D. (1989). Maxmin expected utility with nonunique prior. J. Math. Econom., 18(2):141–153.

- Harrison and Reiman, (1981) Harrison, J. M. and Reiman, M. I. (1981). On the distribution of multidimensional reflected Brownian motion. SIAM J. Appl. Math., 41(2):345–361.

- Klibanoff et al., (2005) Klibanoff, P., Marinacci, M., and Mukerji, S. (2005). A smooth model of decision making under ambiguity. Econometrica, 73(6):1849–1892.

- Knight, (1921) Knight, F. (1921). Risk, Uncertainty, and Profit. Houghton Miffin.

- Lerche and Urusov, (2007) Lerche, H. R. and Urusov, M. (2007). Optimal stopping via measure transformation: the Beibel-Lerche approach. Stochastics, 79(3-4):275–291.

- Linetsky, (2004) Linetsky, V. (2004). The spectral representation of Bessel processes with constant drift: applications in queueing and finance. J. Appl. Probab., 41(2):327–344.

- Maccheroni et al., (2006) Maccheroni, F., Marinacci, M., and Rustichini, A. (2006). Ambiguity aversion, robustness, and the variational representation of preferences. Econometrica, 74(6):1447–1498.

- Miao and Wang, (2011) Miao, J. and Wang, N. (2011). Risk, uncertainty, and option exercise. J. Econom. Dynam. Control, 35(4):442–461.

- Mordecki and Salminen, (2019) Mordecki, E. and Salminen, P. (2019). Optimal stopping of Brownian motion with broken drift. HighFrequency, 2:113–120.

- Nishimura and Ozaki, (2004) Nishimura, K. G. and Ozaki, H. (2004). Search and Knightian uncertainty. J. Econom. Theory, 119(2):299–333.

- Nishimura and Ozaki, (2006) Nishimura, K. G. and Ozaki, H. (2006). An axiomatic approach to -contamination. Econom. Theory, 27(2):333–340.

- Nishimura and Ozaki, (2007) Nishimura, K. G. and Ozaki, H. (2007). Irreversible investment and Knightian uncertainty. J. Econom. Theory, 136(1):668–694.

- Peskir and Shiryaev, (2006) Peskir, G. and Shiryaev, A. (2006). Optimal stopping and free-boundary problems. Lectures in Mathematics ETH Zürich. Birkhäuser Verlag, Basel.

- Riedel, (2009) Riedel, F. (2009). Optimal stopping with multiple priors. Econometrica, 77(3):857–908.

- Williams, (1985) Williams, R. J. (1985). Recurrence classification and invariant measure for reflected Brownian motion in a wedge. Ann. Probab., 13(3):758–778.