Common Decomposition of Correlated Brownian Motions and its Financial Applications

Abstract

In this paper, we develop a theory of common decomposition for two correlated Brownian motions, in which, by using change of time method, the correlated Brownian motions are represented by a triplet of processes, , where and are independent Brownian motions. We show the equivalent conditions for the triplet being independent. We discuss the connection and difference of the common decomposition with the local correlation model. Indicated by the discussion, we propose a new method for constructing correlated Brownian motions which performs very well in simulation. For applications, we use these very general results for pricing two-factor financial derivatives whose payoffs rely very much on the correlations of underlyings. And in addition, with the help of numerical method, we also make a discussion of the pricing deviation when substituting a constant correlation model for a general one.

1 Introduction

The correlation between assets plays an important role in finance. Whenever we meet a problem involving two stochastic factors, the correlation risk is unavoidable. The problem may be from areas of asset allocation, pairs trading, risk management and typically, multi-assets derivative’s pricing. In financial derivatives’ pricing, there are quite a lot chances to meet with the situation of handling two stochastic factors. For example, in stochastic volatility models, the risky price and the stochastic volatility are two factors; in cross-currency derivatives, the evolution of two currencies are driven by different stochastic factors; in two-asset or multi-asset derivatives, the price movements may be modeled by two stochastic processes, etc. Generally speaking, there are two methods in financial modelling to induce dependence between assets, one is by copula, the other is in SDE models by assuming a correlation structure for processes driving the model. Hence, modeling the stochastic factors by two Brownian motions has been a common-used method, see, among others, Heston (1993),Dai et al. (2004) and Hurd and Zhou (2010). In most situations, from a practical aspect, the two stochastic factors (hence the two Brownian motions) should be correlated with each other. Since Brownian motion is the most commonly used driving process stemming from Bachelier, correlation between Brownian motions is crucially important in the latter.

To formulate correlated Brownian motions, many models adopt the constant local correlation assumption, i.e., or conventionally, , for Brownian motions and and a constant . However, more and more empirical works proved that the dependence between financial factors varies over time and depending on the economic status, e.g., Bahmani-Oskooee and Saha (2015) for cross-currency derivatives, Engle and Sheppard (2001) for multi-asset and Benhamou et al. (2010) for stochastic volatility models. Other empirical evidences are as follows, Chiang et al. (2007) found a significant increasing for correlations between Asian market after the crisis, Syllignakis and Kouretas (2011) and Junior and Franca (2012) getting similar results for the European and global markets, Xiong et al. (2018) discovered time-varying correlation between policy index and stock return in China and Balcilar et al. (2018) found dynamic correlation between oil price and inflation in South Africa.

Probably for this reason, there is a growing literature in recent years applying dynamic local correlation for financial problems. Since the value of local correlation, i.e., introduced above, must be in , these literatures adopted various techniques to assure this. Osajima (2007) and Fernández et al. (2013) modeled as a bounded deterministic function of time for SABR model while Teng et al. (2015) adopted the same idea in geometric Brownian motion model and applied it to pricing Quanto option. Note that in these models, is dynamic but nonstochastic. For stochastic , Van Emmerich (2006), Langnau (2010), Teng et al. (2016c) and Carr (2017) expressed as a bounded function of some stochastic state processes and applied it in derivatives’ pricing problems. And some literatures modeled directly by a bounded stochastic process. For example, bounded Jacobi process is a kind of bounded diffusion process driven by Brownian motion and was introduced to model with applications in option pricing and assets management, including vanilla option (Teng et al., 2016b), correlation swap (Meissner, 2016), Quanto (Ma, 2009a) and multi-asset option (Ma, 2009b), and in portfolio selection and risk management (Buraschi et al., 2010). Hull et al. (2010) modeled the local correlation as a step process where each step is a beta-distributional random variable. Márkus and Kumar (2019) made a comparison of several stochastic local correlation models. Moreover, regime switching model is a well used model in finance where all the parameters, including , could be driven by a common continuous-time finite-state stationary Markov process, and thus provide another way to model stochastic local correlation, e.g. Zhou and Yin (2003). Wishart process can establish stochastic covariance directly, and the local correlation obtained from covariance matrix is stochastic as well. Da Fonseca et al. (2007) discussed the Wishart process for multi-asset option pricing and found that there is a correlation leverage affect in call on max style option. Double Heston model also allows a special kind of local correlation between asset and stochastic volatility, see Costabile et al. (2012) and Christoffersen et al. (2009) for more details.

Except correlated Brownian motions, there are also other ways to construct correlated stochastic processes. Wang (2009) obtained correlated variance gamma processes by Brownian motions with constant correlation compound with time changes. Mendoza-Arriaga and Linetsky (2016) and Barndorff-Nielsen et al. (2001) describe correlated stochastic processes by independent background stochastic processes with dependent Lévy subordinators. Ballotta and Bonfiglioli (2016) proposed factor model for Lévy process, each asset is governed by a systematic component and a specific component.

The main focus of this paper is on proposing a new method which we call Common Decomposition for formulation and analysis of the dependency structure for general correlated Brownian motions. By introducing a time change process, the two correlated Brownian motions can be decomposed as two independent Brownian motions, where the two independent Brownian motions characterize the common and counter movements of the original two correlated Brownian motions. Hence, the key point of dependency structure of two original Brownian motions is the time change process. Comparing with the local correlation, an important advantage of common decomposition is that time change process is observable while the local correlation is usually unobservable. Time change is a developed technique to construct stochastic processes (Barndorff-Nielsen and Shiryaev, 2015), and is widely applied to mathematical finance (Carr et al., 2003; Geman et al., 2001b). However, as far as we know, there are few works apply time change technique into modeling correlated Brownian motions. An interesting thing is that we find common decomposition is invariance after change of measure under proper conditions.

Conversely, we also consider how to construct correlated Brownian motions by common decomposition. Comparing with the Euler-Maruyama method (Kloeden and Platen, 2013) of Local Correlation model, we find that common decomposition method simulate the correlated Brownian motions much faster. Under some conditions, there is no simulation error in common decomposition method which is impossible for Euler-Maruyama method of local correlation model.

After construct correlated Brownian motions, we apply our method into financial derivatives pricing, such as Quantos, covariance and correlation swap, 2-assets option, etc. For 2-assets option, it is hard to obtain closed form directly, hence we provide a analytical solution based on Fourier transform. Fourier transform method in option pricing is proposed by Carr and Madan (1999b), more recent papers studied Fourier transform method to price multi-asset options, e.g. Hurd and Zhou (2010) for spread option, Wang (2009) for rainbow options and Leentvaar and Oosterlee (2008) gave a numerical method for multi-asset options without explicit expression. Through Fourier method, we find a unified analytical tractable expression of prices of 2-assets options.

We investigate the pricing error between constant correlation model and stochastic correlation model for 2-assets option by numerical experiments. The numerical results shows that for most out-of-the-money options, the constant correlation model perform poorly while the constant correlation model perform well for at-the-money and in-the-money options.

This paper is organized as follows. In Section 2, we give the definition of common decomposition and discuss the independency properties of stochastic processes obtained from common decomposition. Besides, we consider the relationship between common decomposition method and local correlation model. In Section 3, we provide a sufficient condition for constructing correlated Brownian motions and compare the simulation efficiency between common decomposition and traditional method. Financial applications for derivatives pricing are given in Section 4. Numerical results are shown in Section 5. Proofs of this paper are given in Section 6.

2 Common Decomposition of Two Correlated Brownian Motions

In this section, we consider the new method which is called the common decomposition of two correlated Brownian motions. Firstly, we propose the definition of common decomposition of two correlated Brownian motions and give some notations. Secondly, we investigate the distribution and independency property of stochastic processes obtained from the common decomposition. Finally, we study the connection of the common decomposition and local correlation of two correlated Brownian motions.

In the financial market, if the time interval of observing asset price tends to , then the realized variance of observed asset price tends to the quadratic variation of asset price. Note that the quadratic variation of continuous local martingale is same as the predictable quadratic variation (Revuz and Yor, 2013, Chapter IV, Theorem 1.8), and the stochastic process involved in this paper are all continuous local martingales, hence we replace with if there is no confusion.

2.1 Definition of Common Decomposition

On a complete probability space , we consider two correlated Brownian motions, and , with respect to the same filtration which is assumed to satisfy the usual conditions.

Define

| (1) |

where denotes the cross variation of and . Note that and are Brownian motions, hence . Consequently , which implies is quadratic variation of . Similarly, is quadratic variation of . By immediate calculation, when we have

| (2) |

hence

| (3) |

Consequently, and are increasing processes with and thus they are both absolutely continuous with respect to . Then by Radon-Nikodym theorem, and are derivable with respect to .

Example 2.1.

If the correlation coefficient of and is constant, i.e., , then and . Particularly,

-

•

when and are completely positive correlated, then , and ;

-

•

when and are completely negative correlated, then , and ;

-

•

when and are independent with each other, then .

We will explain in Section 2.3 that and could be regarded as special “timers” that records the time with special correlation information. Next, let

| (4) |

By definition, and are time changes111A time change is a family of stopping times such that the map are a.s. increasing and right-continuous (Revuz and Yor (2013),Chapter V, Definition 1.2). of filtration , and on the contrary, is a time change of and is a time change of .

When and for any , the so-called common decomposition in this article could be given through time-changed processes. Let

| (5) |

If ,it is evident that according to (5). If , for any , we have by the continuity of and the definition of . Note that is the quadratic variation of , hence for any according to Revuz and Yor (2013). Consequently, . If , by the similar approach, we have . In summary, if and , we have

| (6) |

Thus we obtained a representation of through the three new-defined processes (it always holds that ). We call (6) the common decomposition of and the triplet of common decomposition is denoted by . Note that the concept of common decomposition was first proposed by Chen et al. (2018) for the correlated random walks. In this article, we focus on the common decomposition in correlated Brownian motions.

Given ,

Whenever is finite, is not well-defined for . For example, if and are completely negative correlated, then , for any , and . The same happens to and . In order to overcome this limitation, we apply the similar method as in Revuz and Yor (2013, Chapter V) to modify the definition of and . We assume the probability space are rich enough to support Brownian motions that are independent of known Brownian motions and .

By Revuz and Yor (2013, Chapter V, Proposition 1.8), exists on ; Similarly, exists on . Suppose is a 2-dimensional Brownian motion independent from . We modify the definition of and as follows:

| (7) |

In the following, and will be abbreviated as and when there is no confusion. If , note that , hence we have from the previous discussion; if , since is quadratic variation of , we have according to (7) and Revuz and Yor (2013, Chapter IV, Proposition 1.13). Because for any , we have for any . With the similar proof, we have for any . As a consequence, after modifying the definition of and , the common decomposition (6) holds for any .

Remark 2.1.

The choice of can only influence the definition of , but has no influence on the decomposition of and . To be more specific, for , if , by definition, does not depend on ; if , then , does not depend on , either. The same is true for .

In the following, suppose and both satisfy (6), then

which implies is unique in the sense of almost sure. Thus, by the definition of , if ,

Note that , which indicates is unique in the interval . Similarly, is unique in . In the common decomposition (6), and are only related with the values in the time interval and respectively, hence the common decomposition is unique.

For convenience, we introduce some notations here:

-

•

: natural filtration of stochastic process .

-

•

: and are conditional independent given .

It is remarkable that .

2.2 Main Theories of the Common Decomposition

In the previous section, we introduced the so called common decomposition of Brownian motions and . In this part we give some basic properties of the decomposition. Proofs can be found in Section 6.

Our first result illustrates the distribution of , and the path property of .

Theorem 2.1.

Given Brownian motions and with respect to and their common decomposition is denoted as , the following statements hold.

- (i)

-

is a Brownian motion of the filtration , is a Brownian motion of the filtration , and are independent;

- (ii)

-

is derivable with respect to , and

where

(8)

In (8), is called the local correlation process of and . Further discussion of local correlation and common decomposition can be found in Section 2.3.

From Theorem 2.1, the common decomposition represents (resp. ) as the sum (resp. difference) of two time-changed Brownian motions. The dependency structure of and is embodied in as well as in the dependencies between and the two new-defined Brownian motions and . Hence for clarity and convenience, the independency of , and is worth studying. In the following theorem, a sufficient and necessary condition is given for mutual independency of them.

Theorem 2.2.

Under the conditions and notations as in Theorem 2.1, the common decomposition triplet , and are mutually independent if and only if:

- (C1)

-

and .

As an example to understand the condition, when and has a constant correlation say, , (C1) is satisfied since and is a trivial -algebra. More general cases will be discussed later.

The above two theorems give a more visual interpretion of the common decomposition. During the two Brownian motions’ movings, sometimes they move as if with positive correlation and sometimes quite the contrary. These “common” or “opposite” moving times are picked out to form new “clocks” or . And their revolutions are decomposed thereupon according to the new clocks. By Theorem 2.1, under the new clocks, they keep their Brownian-motion features and these features are independent under the two clocks. Thus dependency structures and Brownian features of the original correlated Brownian motions are separated. By Theorem 2.2, if they satisfy the condition (C1), their dependency information is only contained in , the decomposition is quite complete and clear. In this case, we can focus on the process in common decomposition if we want to study the dependency structure of two correlated Brownian motions.

The following proposition gives an equivalent condition of (C1) from another aspect.

Proposition 2.1.

Suppose the assumptions in Theorem 2.1 hold. Then the condition (C1) is equivalent with the following statement.

- (C2)

-

Given two processes and , which are progressively measurable with and satisfy

(9) Let

then is a martingale and defines a probability measure such that

(10) where

This proposition link the independency of the decomposition triplet with conditions similar to Girsanov theorem. Undoubtedly it may attract our attention to consider its application in financial modelling.

Example 2.2.

In financial models, the Girsanov transform is typically used to change the drift parts of diffusions that modelling the prices. Consider two drifted Brownian motions,

where are bounded, progressively measurable with . According to Theorem 2.1, and can be decomposed into . And consequently the two drifted Brownian motions can be represented as

Let denote the densities of and ,

and suppose that . Then satisfy (9), where

If satisfies the condition (C1), then from Proposition 2.1, the two drifted Brownian motions can be transformed to

| (11) |

Under the probability as defined in Proposition 2.1, it is notable that by (10),

| (12) |

thus the drift parts vanish after change of probability measure. Consider the common decomposition of , denoted by . From (11), we have

| (13) |

Moreover, from (10) we have

| (14) |

Remark 2.2.

Equation (13) and (14) reveal the invariance property of under change of measure. From the application point of view, this implies that in financial modelling after change of numeraire, the common decomposition method is still valid. And from empirical view, we can estimate parameters from real probability measure and apply to risk neutral measure directly. For example, Ballotta and Bonfiglioli (2016) bring correlation matrix estimated from observed asset prices (real probability measure) into option pricing model (risk neutral probability measure) directly, and we show the theoretical foundation of such operation. This is quite convenient for derivatives pricing which are lack of public data.

This also shows that we can simplify two correlated Brownian motions with drifts by changing of measure, and keep the dependency structure of original processes.

2.3 Common Decomposition and Local Correlation Model

In this section, we take a new look at the common decomposition via the local correlation process. We consider the difference and connection between the common decomposition method and the local correlation model. As before, the proofs can be found in Section 6.

2.3.1 Relationship Between Common Decomposition and Local Correlation Model

Let us first recall a well used decomposition method representing correlated Brownian motions as linear combinations of independent Brownian motions based on . Suppose is a Brownian motion independent of and , then we define

| (15) |

Particularly, if , a.s., then

It is not difficult to verify that , hence is a Brownian motion independent of , and that the local correlation of and is .

By definition of , we have the local-correlation based decomposition of ,

| (16) |

If we start from the right side of the equation, i.e., starting from independent Brownian motions and local correlation process , we have got a commonly used model for constructing correlated Brownian motions .

As a comparison, by the common decomposition in the current paper, has the representation

Similarly, if we start from the right side, i.e., from independent Brownian motions and time-change process , and make the construction, then are correlated Brownian motions under some conditions. Following the procedure, we can get a new construction method of . We will make further discussions of this new construction method of correlated Brownian motions in Section 3.

Remark 2.3.

The different ideas behind the two methods look clear from the above comparison: the local-correlation method characterize dependency of the Brownian motions from a spatial perspective while the common-decomposition method from a temporal perspective. And characterized the correlation between and at time , but characterized the correlation in the time period . Namely, represent the correlation locally, but characterize the correlation in the whole time period .

The next proposition gives a connection between local-correlation based decomposition and common decomposition. The two method would share the same equivalent conditions when considering completely-independent decomposition.

Proposition 2.2.

Remark 2.4.

Suppose are two continuous local martingales with respect to and , then Theorem 2.1 can be generalized directly, where

and are defined similarly with Section 2.1. Theorem 2.2 and Proposition 2.1 remains valid if we replace by in condition the (C1) and (C2)333In Brownian motion case, . Moreover, if is absolute continuous with respect to , then according to martingale representation theorem, we can rewrite as

where and are two independent Brownian motions and . It is evident that . Hence, Proposition 2.2 is still correct if is replaced with in the condition (C3).

Particularly, the equivalent condition of , and are mutually independent in 1-dimension situation, i.e. Ocone martingale, illustrated in Kallsen (2006) and Vostrikova and Yor (2000) is a special case of . Ocone martingale has been widely used in financial mathematics, such as Carr et al. (2005) and Geman et al. (2001a).

2.3.2 Further Discussions for and

From the setup, we can see play an important role in the common decomposition. Since and are independent, is relevant to the dependency structure of in the common decomposition triplet. Particularly, in the case of complete decomposition where , and are independent, contains all the dependency information. On the other hand, if we treat as a special timer, a ”clock”, it is obvious that this clock’s movements are affected by the correlation of . In this section, we make further discussions of via to get a better understanding of the common decomposition.

First, by Theorem 2.1, and are connected as follows:

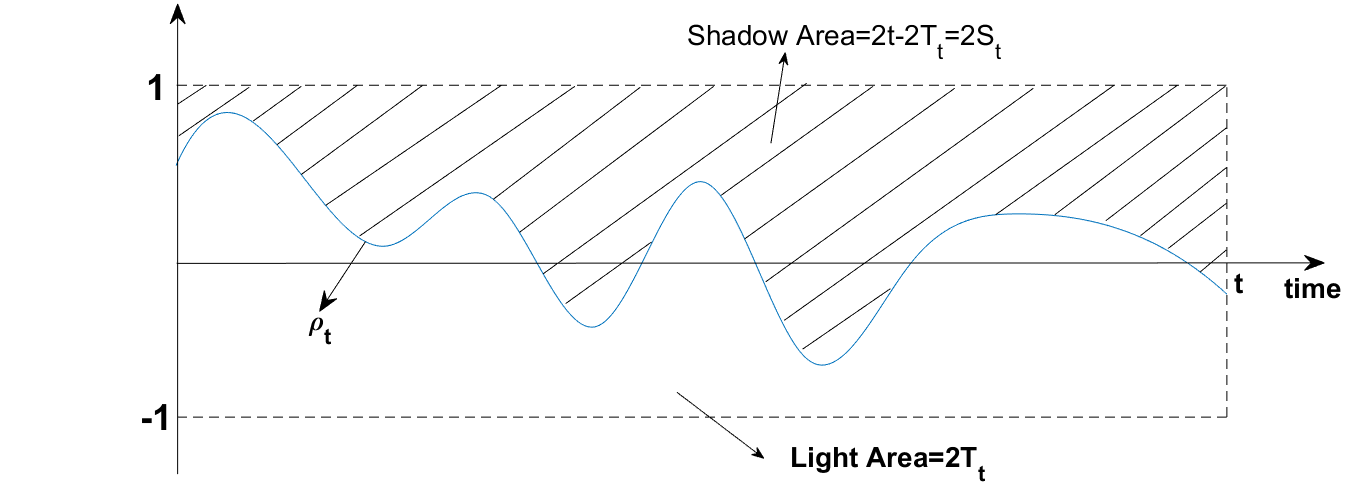

in which, is in fact the distance between local correlation and , is the distance between and , and the denominator is the distance between and . Thus the integrands could be regarded as normalizations of the deviation of ’s correlation from complete correlation. For instance, Figure 1 shows a path of , in which the shadow part represents and the light part represents . Think of the case when is always close to and far away from , then the ”clock ” runs faster than , and the ”clock T” focuses on positive correlation.

Consider the values of and , at any time , they satisfy

That is to say, the sum of the readings of two clocks represents the calender time, while the difference of them shows the cumulated correlation of till time .

The average correlation coefficient process is defined as

| (17) |

and it could also be represented by and ,

Another main difference between and is observability. is always observable through quadratic covariation while is usually unobservable. In statistics, we can only estimate the correlation coefficient for a period of time, that is to say, the estimation of in statistics is actually but not itself. Hence, if the local correlation is dynamic, statistics can help us to study well.

Consider the two-factor derivative’s pricing in finance. When local correlation of the two factors varies stochastically over time, it is always difficult to obtain the option prices. The average correlation coefficient process, , usually plays an important role under this circumstances. For example, the price of foreign equity option was approximated by the moments of in Ma (2009a), and Van Emmerich (2006) and Teng et al. (2016c) show that the price of a Quanto is determined by the Laplace transform of . In our method, , this is one of the reasons indicating the advantage of using common-decomposition method in financial modelling. We will discuss this further in Section 4.

In the next part we use a simple example to reveal the concepts mentioned above.

Example 2.3.

Suppose and are two Brownian motions with constant correlation . Then by the local-correlation method,

where has been defined in (15). In this case, the condition in Proposition 2.2 is satisfied, thus the processes of the common decomposition triplet, and , are mutually independent. And they can be calculated accurately,

and the decomposition of is

In this example, we summarize three statements as follows.

- (i)

-

and conform a decomposition of the “calender time” in any time period. They are composed by special “time points” picked out according to the correlation structure of . They can be considered as special clocks that moves only at special time.

- (ii)

-

If , the clock runs faster than the clock , vice versa.

- (iii)

-

Consider , the family of generalized convex combinations of and . The correlation coefficient of every two processes in with parameters and is

If , . Otherwise, we have if , or , . In other words, is the only process in that is strictly positive correlated with any other process in . Note that this process is in fact under clock , thus represents the common structures in and . Similarly, represents the common structures in and . Namely, and are two extreme cases, and they are taken from and by the common decomposition. In fact, the background of the set is from a financial example. Suppose and represent returns of two assets, then represents the return of portfolio on these two assets. And or represents the short selling of assets.

Remark 2.5.

Actually, if the local correlation of and is not constant, the three statements for Example 2.3 remain valid. For (i) and (ii), the results remain the same. For (iii), we can prove

where and denote covariance and correlation respectively. With the similar discussion, is the only process in that is strictly positive correlated with any convex combination of and .

2.4 Illustration of the Common Decomposition via Discretization

The example in previous section demonstrated what the processes in common decomposition look like and how to construct the clock when . In this section, similar analysis is carried out from a distributional aspect for general cases by discretizing . In this part, we also start with two correlated Brownian motions and with local correlation process , and all the other notations defined in previous sections are followed.

Given , let be a partition of :

and write . Given , for , define444The choice of is not unique. can be any Borel set as long as , where denotes the Lebesgue measure on .

Note that by the construction of , the stochastic processes and are predictable.

Set

i.e., keeps in step with in and stays stationary at other time while performs oppositely. Let

| (18) |

Then is a Brownian motion moving commonly with in and oppositely in . And and represent the common movements and counter movements of and .

At any time , the time period is divided into two parts: the commonly-moving period and the oppositely-moving period , whose total lengths could be calculated respectively as (suppose )

where denotes the Lebesgue measure on . Obviously,

| (19) |

The following proposition considers the limitation property of in distribution.

Proposition 2.3.

Suppose the assumptions in model setup and the conditions in Proposition 2.2 hold. For any given , as , we have

Proposition 2.3 guarantees that as , any finite dimensional distribution of converges to in the sense of distribution. For simplicity, we denote this finite dimensional distribution convergence of processes by ””. Thus,

as a consequence,

| (20) |

The convergence properties (20) and (19) reveal the connections of and with common and counter movements of in some sense, and give an intuitive explanation for and to be considered as clocks recording positive correlation and negative correlation of .

3 Construction and Simulation of Correlated Brownian Motions Based on the Common Decomposition

In the previous section, the common decomposition of two correlated Brownian motions has been demonstrated. For any two Brownian motions and , we can find a triplet to represent them by change of time method. While in practice, a converse problem may also be worth concerning and studying. That is, is it possible to construct two Brownian motions with desired dependency structure from two independent Brownian motions by common decomposition method? In this section we will focus on this problem. Furthermore, the simulation method based on the common decomposition is also given.

3.1 A New Method for Construction of Correlated Brownian Motions

In this section, we construct correlated Brownian motions by common decomposition method under some conditions and give an example to show the application of this new construction method.

Theorem 3.1.

Let be a 2-dimensional standard Brownian motion and , be time changes with respect to . If and , then and are martingales with respect to . Furthermore, if , are strictly increasing and , then

are two correlated Brownian motions with respect to and .

Immediately, we have a convenient way to construct correlated Brownian motions from Theorem 3.1.

Corollary 3.1.

Suppose that are strictly increasing processes satisfying , and are independent Brownian motions. If are mutually independent, then

are two correlated Brownian motions with respect to and .

In the following, we consider constructing correlated Brownian motions through common decomposition and regime switching model.Regime switching is a commonly used model in finance, and it fits financial data well. For example, Schaller and Norden (1997) found very strong evidence for state-dependent switching behaviour in stock market returns. Regime switching model for correlations in discrete time have been considered, e.g. Casarin et al. (2018) and Pelletier (2006). Hence, we consider regime switching model to construct correlated Brownian motions by common decomposition method in the next example.

Example 3.1.

(Regime switching model) Suppose is a continuous time stationary Markov process taking values in a finite state space , where

denotes the unit vector. The Markov process has a stationary transition probability matrix , where

The homogeneous generator exists and is defined as

where denotes the identity matrix. Then we have

Solving this ODE we obtain

| (21) |

Let , and

Obviously, are increasing processes. Let be 2-dimensional standard Brownian motion independent with . Then from Corollary 3.1, we have and are two correlated Brownian motions.

3.2 A New Method for Simulation of Correlated Brownian motions

Simulation is also an important part of constructing correlated Brownian motions. In this section, a new way to simulate correlated Brownian motions is given by the common decomposition method. The local correlation model characterize the correlation in the micro view and only focus on the correlation at the moment; however, the common decomposition characterize the correlation over the entire period of time, which is from the macro view. This difference of two methods may bring advantages of the new simulation method compared with the simulation method from local correlation model.

One of the most common simulation method for local correlation model is Euler-Maruyama scheme, see Kloeden and Platen (2013). Firstly, given a partition of , let

| (22) |

where and is defined as

Secondly, simulate by applying (22). Thus, the simulation result is eventually, and there always exist simulation errors.

Under the condition that , and are mutually independent, Table 3.2 and Table 3.2 show the specific steps of simulation by common decomposition method when we do not have the explicit expression of ’s distribution. As a comparison, the Euler-Maruyama scheme of local correlation model is also shown in the second column of Table 3.2 and Table 3.2. The common decomposition of is denoted as . From Table 3.2, compared with Euler-Maruyama scheme, the differences and the advantages of common decomposition method are as follow:

-

•

If the trajectory is not necessary, and we only need and at time , common decomposition method can reduce the time of simulations. If is a stochastic process, we have to simulate random numbers in Euler-Maruyama scheme, i.e. , , , . However, in common decomposition method we only need to simulate random numbers, i.e. , and .

-

•

If we have the explicit expression of ’s distribution, we can simulate directly, then we only need to simulate and , hence simulation can be reduced to 3 times.

-

•

The simulation error can be controlled as long as the simulation error of can be controlled, since

Therefore, if the explicit expression of ’s distribution is obtained, one can simulate directly, and then simulate and with the similar steps in Table 3.2 and Table 3.2. Then there is no simulation error for , hence we can simulate accurately while this is impossible for local correlation model. If the explicit expression of ’s distribution is inexplicit, the simulation error of two methods is the same, because both the methods simulate .

From Table 3.2 if the trajectory is needed, and we do not have the explicit expression of ’s distribution , there is little difference between the two simulation methods.

[htbp] Simulate for a given (Explicit expression of ’s distribution is unobtained) Common decomposition method Local correlation model (Euler-Maruyama scheme) Step 1 Simulate in order1 Simulate in order Step 2 Simulate and 2 Simulate , , , and , , , Step 3 Calculate Calculate

-

1

According to , complexity of simulating is equal to simulating .

-

2

Under the condition of , and are independent normal distributions with mean zero and variance and respectively.

[htbp] Simulate trajectory of in (Explicit expression of ’s distribution is unobtained) Common decomposition method Local correlation model (Euler-Maruyama scheme) Step 1 Simulate in order same with Step 1 in Table 3.2 Step 2 Simulate , , , and , , , 1 same with Step 2 in Table 3.2 Step 3 Calculate and Calculate and

-

1

Under the condition of , the random variables are independent normal distributions with mean zero and variance , respectively.

Example 3.2.

Take parameters as follow,

| (23) |

Figure 2(a), Figure 2(b), Figure 2(c) display how we simulate the trajectory of in through common decomposition method (explicit expression of ’s distribution is unobtained) step by step

We consider the regime switching model in Example 3.1. Thanks to (21), simulation for regime switching model is feasible. Take the same parameters as in (23), we calculate the expectation of by simulating 555Note that we do not need to simulate the trajectory here. with replications. We implement Monte Carlo methods by MATLAB2017b with a Core i7 2.8GHZ CPU.

Table 1 shows that the standard deviation of two methods are very close, hence their simulation error are truly close. And common decomposition method runs much faster than local correlation model with Euler-Maruyama scheme.

| Std Dev | Running time | ||||

|---|---|---|---|---|---|

|

-0.0034 | 3.1868 seconds | |||

|

0.0265 | 11.4762 seconds |

4 Financial Derivatives Valuation by Applying the Common Decomposition Method

In the previous two sections, the common decomposition of two Brownian motions is considered, in which dependence structure could be very general. We showed how to decompose Brownian motions to a triplet , and we also answered how to construct two correlated Brownian motions from a given triplet . In this section, we will apply the common decomposition method to study the pricing problem of some typical two-factor derivatives that modeled by two correlated Brownian motions. We first give two examples showing direct usage of the common decomposition triplet in pricing covariation swap, covariation option and Quanto option. And then we will focus on the pricing problem of two-color rainbow options. There are several typical examples for two-color rainbow options, one is given by option-bonds, see Stulz (1982) for details; besides, a special kind of two-color rainbow options, spread options, are ubiquitous in financial markets, including equity, fixed income, foreign exchange, commodities and energy markets, Carmona and Durrleman (2003) present a overview of examples and common features of spread options.

For simplicity, we assume that and are mutually independent in this section, i.e., is independent from (, ) in the local correlation model by Proposition 2.2. This assumption is not so rigorous as to go against the reality. For example, in Ma (2009a), when considering the pricing problem of foreign equity options with stochastic correlations, the author illustrated independency of , and from an empirical view.

4.1 Pricing Covariance Swap and Covariance Option

Options which depend on exchange rate movements, such as those paying in a currency different from the underlying currency, have an exposure to the correlation between the asset and the exchange rate. This risk may be eliminated by two ways, a straightforward approach is Quanto option which will be discussed in Section 4.2; the other approach that we focus on this section is Covariance Options or Correlation Options, see Swishchuk (2016) for more details. By combining variance and covariance options, the realised variance of return on a portfolio can be locked in. Carr and Madan (1999a) illustrated that the covariance swaps can be constructed by options and futures, in other words, options can be perfectly hedged by covariance swaps and futures. In the following part, we consider the so called covariance options which is designed to cope with the covariance risks of two underlying assets.

Suppose that the prices of the two assets, , can be characterized as

| (24) |

where the drifts and volatilities of underlying assets are assumed to be constant.

Example 4.1 (Swap and Option on Realized Covariance of Returns).

Consider two risky assets whose prices evolve as in (24). Then according to Example 2.2, could be transformed to, under proper conditions,

where and are Brownian motions under the risk neutral measure , and denotes the constant risk free interest rate.

Continuously compounded rate returns of two assets are and . Accordingly, the realized covariance of returns of two underlying assets is defined as the cross variation of and

then the payoff of covariance swap and covariance option of the underlying equity and at expiration is

and

where represent the strike price. Note that

the price of covariance swap and covariance option only depend on the expectation and distribution of . Note that is observable in real probability measure, and the distribution of under real probability measure and risk neutral probability measure is coincident according to Example 2.2, hence we can easily obtain the distribution and expectation of from historical data and then obtain the price of covariance swap and covariance option. The result of correlation swap and correlation option is similar.

4.2 Pricing Quanto Option

Quanto option is a famous cross-currency financial product trading in organized exchanges as well as in OTC. Its payoff is calculated in one currency but is settled in another currency at a fixed exchange rate. It is designed to hedge the risks of delivering foreign investments to domestic currency. Hence the correlation between the underlying price and the exchange rate plays an ultimate role in pricing. Usually, this correlation structure is modeled by two correlated Brownian motons. In Section 2, we have showed that part of the dependency of two Brownian motions could be described by in common decomposition. In the following example, we will show the essential role of in the pricing of an European-style Quanto.

Example 4.2.

Consider an European-style Quanto. Suppose the price of underlying equity in foreign currency and the exchange rate are modeled, under the risk neutral probability in the domestic currency, as follows:

and the payoff of a Quanto put option is

Let represent the risk free interest under domestic currency and foreign currency respectively. Under the arbitrage free assumption in domestic currency world, any discounted asset should be a martingale in risk neutral probability. Hence, consider the bank account and stock account in foreign currency, one can get

| (25) |

| (26) |

Note that

and under the condition (C3), we have

After simple calculations,

According to Van Emmerich (2006) and Teng et al. (2016c), Quantos’ price is

where

Note that

then Quantos’ price is actually determined by Laplace transform of , similar with Example 4.1, we can obtain the Laplace transform of by the distribution of from historical data.

4.3 Pricing 2-Color Rainbow Options

In this section, we focus on a class of multi-asset options, the 2-color rainbow option which is written on the maximum or minimum of two risky assets. This kind of option was first studied in Margrabe (1978), and in Stulz (1982), the author showed its extensive applications in valuing many financial instruments such as foreign currency bonds, option-bonds, risk-sharing contracts in corporate finance, secured debt, etc.

In this part we use the same asset-price models as in Section 4.1. We find an unified and analytical expression of the prices of different rainbow options.

The payoff of a rainbow option with maturity may have the forms listed in Table 2 (Ouwehand and West, 2006). We will demonstrate that all these types of rainbow options could be valuated through a unified approach.

| Option Style | Payoff |

|---|---|

| Best of assets or cash | |

| Put 2 and Call 1 | |

| Call on max | |

| Call on min | |

| Put on max | |

| Put on min |

Define a 2-dimensional process . Similar to the cases studied in Carr and Wu (2004), the payoffs in Table 2 could be reformulated as

with some proper parameters and .

For example, consider the Call-on-max option, whose payoff is , the parameters are (for )

It is easy to check that

Now we can present a unified valuation approach for options with payoffs in Table 2 through process . First, for given parameters , an intermediate valuation function is defined as

| (27) |

where indicates the expectation under the risk-neutral measure . It is obvious that the initial price of a rainbow option could be given by as

| (28) |

For simplicity, we omit the parameters in the function expressions when there is no confusion. The following proposition gives a general rule to calculate function .

Proposition 4.1.

Suppose and are mutually independent. Let be given as in (27), and represent the Laplace transform of . Then the characteristic function of is as follows,

| (29) |

Moreover, the generalized fourier transform of denoted by , is given as

| (30) |

where . In particular, if is a constant, then and can be obtained from (29) and (30).

Given Proposition 4.1, the function could be calculated by the inversion formula and numerical method, then the prices of rainbow options are obtained from (28).

Remark 4.1.

For general cases where the payoffs can not be represented as before, Proposition 4.1 is un available. But we can still apply the Fourier-transform method directly to pricing functionals. For given parameters , rewrite the option payoffs as , where . Denote by the joint probability density of and under , then the price of is

According to Leentvaar and Oosterlee (2008), the Fourier transform of is

where denotes the Fourier transform of . In general, has no explicit expression and thus usually be calculated numerically.

When the correlation coefficient of and is constant, could be calculated explicitly,

In this case, Leentvaar and Oosterlee (2008) have put forward a numerical method to calculate .

When the correlation coefficient of and is not constant, we can still use similar approaches as in Leentvaar and Oosterlee (2008) by means of common decomposition. Continuing to use the notions as before, we have

Consequently,

| (31) |

Hence when the Laplace transform of is known, the price can be obtained by inverse Fourier transform formula.

In the previous discussion, we considered how to calculate the price of a rainbow option. Actually, following similar approach outlined in Proposition 4.1, we could give a Fourier-transform method for calculating Greeks. The next corollary set forth an example of this.

Corollary 4.1.

Consider the Delta of for a Call-on-Max option listed in Table 2, which is denoted by . After calculations, we have

where

The Fourier transform of has an explicit expression as

and the expression of Fourier transform of is

can be obtained by the inverse Fourier transform formula. Other Greeks can be derived along the same procedure.

From the foregoing content of this section, we know that, thanks to the common decomposition method, in order to calculate the price and Greeks of a rainbow option, we only need to find out the Laplace transform of . We consider some specific models of in the following examples to give the readers more intuitive insights.

Example 4.3.

In the next example, has a specific modelling through a bounded function of some stochastic processes and the Laplace transform of is given by a PDE.

Example 4.4.

Suppose that is a bounded function with values in and is a diffusion process satisfying the following SDE

where is a Brownian motion and are determined functions such that the SDE have an unique solution.

Sometimes, there is no closed-form solution of financial derivatives, so Monte Carlo method is needed. The simulation method through common decomposition have been illustrated in Section 3.

5 Numerical Results

In literatures that study the pricing problem of two-assets derivatives with models driven by two Brownian motions, , it is a commonly used assumption that the local correlation of is a constant, i.e., for some . However, as we have mentioned before, this assumption is inconsistent with empirical studies. For example, based on data from different markets around the world, Chiang et al. (2007), Syllignakis and Kouretas (2011) and Junior and Franca (2012) all found that the correlation coefficients changed as time and economic situations changed. Then it is natural to ask, when the actual correlation coefficient is dynamic and stochastic, how much it would influent the pricing error if we still applied the constant-correlation model?

In this part, we consider the price of two-color rainbow options as an example. We investigate the difference of option prices under constant and dynamic correlations by numerical experiments and try to summarize when this difference is negligible or nonnegligible.

Since our concern is in the correlation of underlying assets, we assume for simplicity that all coefficients of the underlying assets, except for the local correlation, are constants. Thus the underlying prices are assumed to satisfy (under the risk neutral probability)

For the dependency structure of , we apply the regime switching model in this section which has been introduced in Example 3.1 and Example 4.3. Suppose that the market has three different states described by a finite-state-space Markov process with an initial value and a transition rate matrix . Thus the local correlation process of and is as follows,

Note that , hence indicates the switching states for local correlation coefficient of log prices. For example, if , at any time , switches among and according to the market conditions. In the rest of this section, parameters are taken as follow unless otherwise specified,

| (33) |

Consider the two-color rainbow options as in Section 4.3, note that, under the above model, if is considered as a constant, the option prices can be given in closed form as in Stulz (1982). While for the actual case with a regime-switching , we can apply Proposition 4.1 to derive the true prices. Following the notations in Proposition 4.1, by the inversion fourier formula, we have

| (34) |

where denote the imaginary part of and .

Since is well defined only for with strictly positive imaginary, we choose in the subsequent numerical experiment. Note that (34) remains valid for any . And we approximate (34) by

where we set and .

Suppose that the contract life of the option is and the strike is . Let , then the regime switching model degenerates to the constant correlation model. We verified the group of parameters are accurate enough and the difference of option price obtained from Stulz (1982) and Proposition 4.1 is smaller than .

In the following subsection, we compare the option prices induced by the constant- models in Stulz (1982) to the prices given by the regime-switching- models through (28). Since we have assumed the regime-switching case to be actual, the latter could be regarded as the “true” prices. And thus the comparison results will indicate how large the pricing error would be when we substituted a constant for the original nonconstant . For clarity, we make comparison in an ideal situation that the investor knows exactly the other coefficients except for .666In empirical, the risk free interest can be observed and can be calibrated precisely from vanilla options.

5.1 Numerical Experiments of Pricing Rainbow Options

In Section 5.1.1, we compare the constant correlation model and dynamic correlation model in a more theoretical way. We assume that the investor estimates historically from the observed stock prices. The numerical results in this section show that there may be big differences between the prices of two models. In Section 5.1.2, we adopt an approach more close to the practical procedure. We suppose the investor calibrate the constant correlation model to option prices he observed (which were calculated from the regime-switching model). And then the calibrated model is used for pricing. And it shows that there will be a big pricing error by using constant correlation model, especially for those options deep out of the money. This is in line with the results given in Costin et al. (2016) for CDS options.

5.1.1 Numerical Analysis of Constant and Nonconstant Correlation in Pricing Rainbow Options

In this section, we estimate a constant correlation coefficient from the historical data which are given by the regime switching model, and then calculate the option prices derived from this 777We have illustrated in Remark 2.2 that it is feasible to apply directly the estimated from historical data into option pricing.. By comparing these option prices with those deriving directly from the regime switching model, we can get a general idea of the error we would make when applying constant correlation model in the situations where the actual correlation coefficients are dynamic and stochastic. For the robustness of the results, we consider the comparisons in different cases with different vector s.

Since we have assumed that all the other parameters can be obtained precisely, the investor actually could get the data of by observing prices of the underlying assets. Suppose that the investor has got these historical data of a long term and with a relatively high frequency as , where . According to definition, the estimated constant correlation based on data till time is

Note that, setting , we have

and according to the Ergodic Theorem of Markov processes,

where denotes the stationary distribution of the Markov process .

Therefore, as long as we assume these data to be long-term and with a relatively high frequency, we always have

| (35) |

In this case, no matter how violently the correlation coefficient switches over time, the investors may have similar estimates from long-term historical data. And thus the option prices calculated along these estimates may deviate a lot from the “true” prices. We will show these prices’ deviations by the relative error defined as

| (36) |

In the numerical experiments, for each case, we simulate a path of to present the historical data, where we choose and . In order to make consistent comparison, we randomly choose different , which all satisfy the condition . That is to say, by (35), the option prices calculated from the estimated coefficients are similar since in all cases . While on the contrary, we shall see that the prices calculated from original model are quite different from each other.

We list the numerical results in Table 3, in which the second column shows the “true” prices calculated from the original regime switching model, the third column shows the estimated from the ”historical data”, the forth column shows the prices obtained by constant correlation model with , while the last column shows the relative errors defined as in (36).

| True Prices | Prices with | Relative errors | ||

|---|---|---|---|---|

| 37.2642 | 0.2377 | 35.2623 | -5.37% | |

| 38.2361 | 0.2103 | 35.3671 | -7.50% | |

| 35.9230 | 0.2436 | 35.2398 | -1.90% | |

| 33.8134 | 0.1911 | 35.4403 | 4.81% | |

| 35.4064 | 0.2177 | 35.3388 | 0.19% |

It is obviously from Table 3 that there may be big pricing errors when using constant correlation coefficient estimated from historical data. In this numerical example, although all the other coefficients were assumed to induce zero error, the relative errors for pricing can mount to unacceptable levels. It is almost certain that these high errors come from the substitution of s for the real dynamic stochastic s. As a verification, we consider the case of , where the regime switching model degenerates to the constant correlation model. The results are shown in the last row of the table. We can see that there is only a small relative error, , which presents the technical error other than substitution of constant correlations to dynamic ones.

More specifically, we can see that in all cases the estimated s are around , and thus the resulting option prices are around , while the true prices deviate from as high as to as low as . There would be a big unexpected loss if the investor applied the constant correlation model to value these options and used these prices as a guidance of his investments.

5.1.2 Calibrating a Constant Correlation Model from Data Given by the Dynamic Correlation Model

In this section, we investigate the difference between option prices under constant correlation model and dynamic stochastic correlation model through a more practical way. First, in practice, when considering derivatives’ pricing, investors do not use coefficients estimated from historical data commonly. More often, they observe the market prices of a class of derivatives, and calibrate the theoretical model to the observed prices. In our case, the ”market prices” are supposed to be given by the regime switching model, and the ” theoretical model” held by investors is supposed to be the constant correlation model. And ”calibration of the theoretical model” reduces to ” finding the optimum to fit the market prices” since this is assumed to be the only unknown parameter for the theoretical model. On the other hand, just like the idea of ”implied volatility”, each observed option price can deduce an ”implied correlation”, . The change of with strikes can also indicate the deviation of option prices given by constant correlation model from actual prices based on dynamic correlation.

The numerical simulations are carried out along the procedure in the following.

First, we give the prices for options with a maturity and strikes under regime switching model by the Fourier transform method. These will play the part of ”initial market data” in our numerical experiment.

Then based on these data, we calibrate the constant correlation model to a proper .999Just as before, all the other coefficients are supposed to be known exactly. This is done by minimizing the following cumulative square error function by Gradient Descent method, 101010The initial value is taken as . The step size is set as where denotes the first derivative of . The gradient descent method terminates when is smaller than .

And then, the calibrated correlation coefficients are applied to the constant correlation model for pricing options with strikes , , , . The resulting prices will be compared with the prices under regime switching model.

To see the variations of implied correlation, we apply the definition of given by Da Fonseca et al. (2007) which satisfies

to the prices given by regime switching models with more strikes .

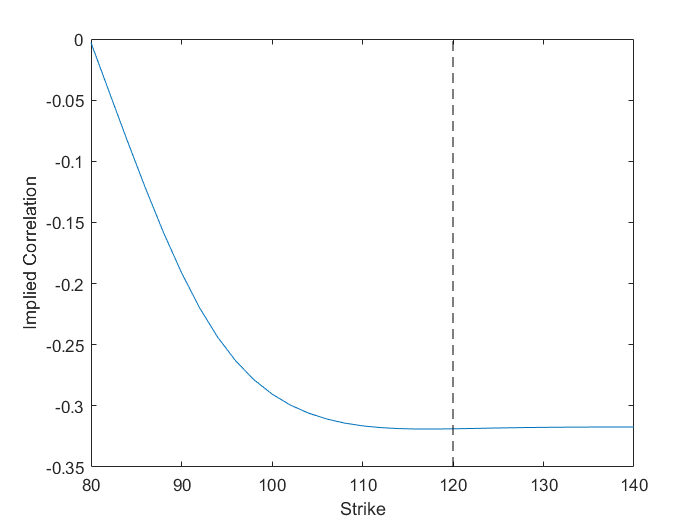

In the following, we run through the calibrating-pricing procedure for Call on Min, Call on Max, Put on Max and Put on Min options, consider their relative errors defined as in (36), and calculate the implied correlations respectively. We show the results in Figures 3-6. In each figure, the dotted line separates the curve into two parts, the out-of-the-money case (in figures, the left part for puts or the right for calls) and the in-the-money case. The intersection is at-the-money case.

On the first try, we choose parameters and to generate the regime switching model. The immediate observation is the huge pricing error for deep-out-of-the-money options of Put on Max and Call on Min. The relative error reaches more than , which is shown in Figure 3(a) and 5(a). While for Call on Max option, the relative error is no more than , as shown in Figure 4(a). And it is also small for Put on Min option whose figure is omitted here since the relative error always lies below the level .

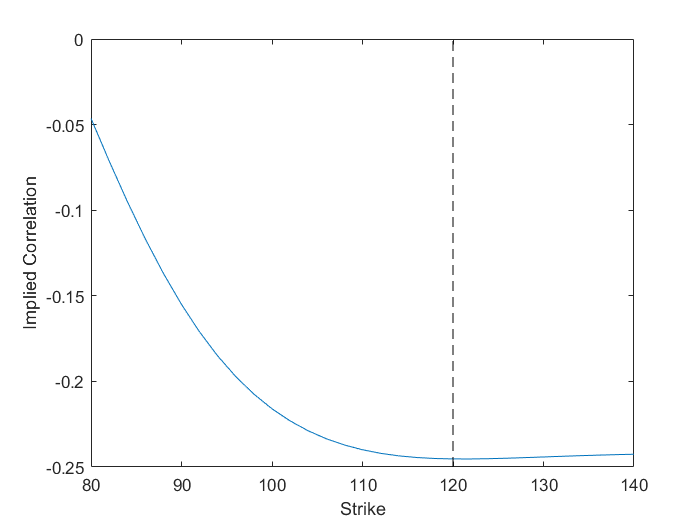

To see whether this is a common property or not, we change the initial regime switching model to a new one with parameters and , and repeat the calibrating-pricing procedure. For Call on Max, Call on Min and Put on Max, the results are really similar with the previous group of parameters and we omit the figures. But for Put on Min, the result is different from former one, relative error could be more than for out-of-the-money options as shown in Figure 6 which is also nonnegligible.

On the other side, for implied correlation, we can see in Figure 3(b)-6(b), the implied correlation always changes sharply for out-of-the money cases and mildly for in-the-money cases, which is similar with the calibrated . For Call on Max options, though there are only tiny pricing errors, the implied correlations change a lot with different strikes.

Figure 7 investigates Put on Max options again and the maturity considered as . Comparing with Figure 5, we can find in Figure 7, the calibrated error is a little smaller and the implied correlation changes a little milder. But the main features of them are similar, this implies the maturity has little effect on our discoveries.

We will try to give a reasonable explanation for different performances of 4 kinds of rainbow options in the next section, Section 5.2. And also there in addition, we will explain why the calibrated option prices perform well for in-the-money and at-the-money options but terribly bad for deep-out-of-the-money options and why the Call on Max seems different from the other options.

5.2 Error Analysis

The pricing errors coming from setting the dynamic stochastic correlation of underlying log prices to be constant are further analyzed in this part. This analysis is from a theoretical view but with the help of numerical simulations. Through this analysis, we try to explain the phenomenon discovered in Section 5.1.

Now we consider options with payoffs ,111111Note that all the payoffs considered in previous numerical simulations are in this way then the price of the option is

where denotes the risk neutral probability measure.

When the local correlation process is a constant , since , the option price is a function of which will be denoted as in the following.

For more general case where is a stochastic process, we first recall the term of average correlation coefficient , which by the common decomposition, can be rewritten as

| (37) |

Since under the condition of , , following the discussions in the constant- case, the option price ( denoted by ) equals

If is an affine function of , i.e., , we have

| (38) |

In other words, when the option price under constant- model is linear in , the price under a general dynamic correlation model is exactly the same as that with a constant correlation coeeficient .

Otherwise, for general , by Taylor’s expansion, we can get the following approximation formula,

| (39) |

(38) and (39) indicate that the main cause of pricing errors between constant correlation model and dynamic correlation model is nonlinear property of .

In the following, based on the above analysis, we try to explore causes for the big pricing errors in Section 5.1.1 and the two phenomena found in Section 5.1.2: (i) the pricing errors seem more remarkable for out-the-money options when applying constant correlation model; (ii) the pricing errors for Call-on-Max options seem relatively small than other kind of options.

We first consider relations between and in the cases of in-the-money, at-the-money and out-of-the-money for Put-on-Max options.

Example 5.1.

Choosing parameters as , we draw diagrams for when (in the money), (at the money) and (out of the money) and list them in Figure 8.

Example 5.1 show that, for in-the-money and at-the-money cases, reveals a strong linearity on except when is near to . But it is quite nonlinear for out-of-the-money case. We conduct similar diagraming with different parameters for Put-on-Max option as well as Put-on-Min, Call-on-Min and Call-on-Max options, and get similar results. Recall the approximations (38) and (39), the above results give an explanation for why constant correlation model performs well on the whole for in-the-money and at-the-money options but poorly for out-of-the-money options. We can find in Figure 3(b),4(b),5(b),6(b),7(b) and Table 4, when strike is in-the-money and at-the-money, the implied correlation of each option is very close to ; on the contrary, when strike is out-of-the-money, the implied correlation changes sharply and far away from . This is coincident with the conclusion in previous.

| -0.3177 | -0.2488 | |

| 0.5784 | 0.5298 |

Comparing the numerical experiments in Section 5.1.1 and the data in Table 4, we find that there are big differences between the historical local correlation coefficient and the expectation of correlation coefficient in the future, which explains the pricing errors in Section 5.1.1.

We now turn to the Call-on-Max option whose performance in calibration in Section 5.1.2 seemed quite different from the others that the calibrated constant correlation model always performs well, even for out-of-the-money case. Note that as mentioned before, we have already got diagrams for this kind of option which have similar linear or nonlinear shapes like other options and we did not include them in the main text. A interesting question is, now that the shape of for out-of-the-money case looks apparently nonlinear, why does it still approximate the true price well? We choose the same parameters as before except for and draw the diagram of for Call-on-Max option for the case (out-of-the-money) in Figure 9. The diagram looks still quite nonlinear, but it is worth noting that in Figure 9 just changes from to . In other words, when changes in its full range, the price changes only about which implies that, for Call-on-max option, the correlation between underlying assets has only a small, almost negligible, impact on the option price. While on the contrary, think about calibrating from option prices, a small deviation in the price may cause great changes in the implied . This result on one hand explains why the implied correlation of Call-on-Max option is volatile but the calibrated constant correlation model always performs well and on the other hand indicates that when the data are from out-of-the-money Call-on-Max options, correlation-coefficient calibrating may be unsuitable since the implied correlation is too sensitive with the price.

6 Proofs

6.1 Preparation Works

In the first place, we give some lemmas as preparations.

The following lemma which will be often used in Section 6.2 gives a sufficient condition for a special kind of stochastic process to be a martingale.

Lemma 6.1.

Suppose is a continuous local martingale with respect to . If is a -progressively measurable process such that

| (40) |

then

is a martingale with respect to .

Proof.

First note that

therefore is well-defined. By Itô’s lemma, is a local martingale obviously. Hence there is a sequence of stopping times satisfy , and

is a martingale. Consequently, . Observe that are always positive, then according to Fatou’s lemma, i.e., is a supermartingale. From (40) and Karatzas and Shreve (2012)[Chapter 3, Proposition 5.12], we have

which implies is a martingale immediately. ∎

Before going further, we first introduce the condition (E) as follows:

- (E)

-

For any -progressively measurable processes and that guarantee

(41) we have

Next, we establish an equivalence relation between the condition (E) and the independency of and by Lemma 6.2. Then in Section 6.2 we complete the proofs of Theorem 2.2 and Proposition 2.1 through the condition (E). Besides, Lemma 6.2 also give other two necessary conditions for the independency of and , which will be used in the proof of Corollary 3.1 and Theorem 2.2 respectively.

Lemma 6.2.

Suppose is a 2-dimensional standard Brownian motion and , are two increasing processes with . If , and are mutually independent, then we have the following consequences:

-

(i)

the condition (E) holds;

-

(ii)

and ;

-

(iii)

and are martingales with respect to .

Moreover, if is a triplet of common decomposition, i.e. the conditions in Theorem 2.1 hold, then the statement (i) is also sufficient for the independency property of , and .

Proof.

We first prove the statements (i), (ii) and (iii).

-

(i)

Let and be the inverse of and as defined in (4), and be any progressively measurable processes satisfy (41). Define and as follows,

Then

(42) and by (41),

Hence and are well defined and

(43) Observe that and are martingales with respect to by the independency of , and according to (41) and (42), thus by Lemma 6.1,

is a martingale. Consequently

(44) Substituting (42) and (43) into (44), we have

Note that is measurable with , and the desired result holds immediately.

-

(ii)

First note that, when are independent, by the former result, the condition (E) is true. As a direct consequence of the condition (E), and is conditional independent given , . Thus for every -measurable random variable , . Furthermore, by the truth , , we have

(45) To prove the result of this part, i.e., and are conditional independent given , it is sufficient to prove that for any -progressively measurable process satisfying (41), the following equation holds

By (45),

where the second equality comes from the condition (E) immediately. Since , applying (45) again, we have

which is the desired conclusion. By similar proofs, we have .

-

(iii)

Given , for any and , we can obtain the characteristic functions of , and respectively according to the condition (E) by some special and . Besides, the condition (E) also gives the joint characteristic function of them, which implies the mutual independency of , and . By the arbitrary chosen for and , we have , and are mutually independent. Hence,

Observe that , thus is a martingale with . The same arguments hold for .

In the following, we prove that if the conditions in Theorem 2.1 hold, then the condition (E) is a sufficient condition for the independency of , and .

For , and we consider the joint distribution of conditional on by calculating

| (46) |

where .

Define

It is easy to verify , and

By definitions of and (for simplicity, we set when ), we have121212In the proofs of this section and Section 6.3, the time-change formula for stochastic integral such as (47) and (48) will be often used. If the stochastic integral is well-defined and the integrand is progressively measurable, then the time-change formula for stochastic integral is available, in which the conditions are quite relaxed. For more details, please refer to Karatzas and Shreve (2012)[Chapter 3, Proposition 4.8] or Revuz and Yor (2013)[Chapter V, Proposition 1.5].

| (47) |

| (48) |

Thus

| (49) |

It is not difficult to verify that is a continuous local martingale with respect to and . Then according to Lemma 6.1, is a martingale. Hence,

| (50) |

Substituting (6.1) into (49), we have

Then from the condition (E), we obtain

By the definition of and , the previous equation comes to

which implies and are independent and does not affect the distribution of . Hence, , and are mutually independent. ∎

Note that the condition (E) is actually equivalence with the independency of , and under the conditions in Theorem 2.1.

Lemma 6.3 is a generalization of Girsanov Theorem, and it may be useful in the proof of Proposition 2.1.

Lemma 6.3.

Suppose is a Brownian motion and is a nondecreasing stochastic process independent with . Given and , which are progressively measurable with and

let

Then we have

Proof.

Given , from

and Lemma 6.1 we have is a martingale with respect to . Let

Note that is a Brownian motion with respect to , then by Girsanov theorem,

is a Brownian motion with under probability measure . Hence is a martingale under , then by optional stopping theorem131313In Girsanov theorem, we need to determine an upper bound in advance, then is a Brownian motion with in . Thanks to , optional stopping theorem for remains valid., we obtain

i.e.,

Note that , thus we get desired result immediately. ∎

6.2 Proofs of Results in Section 2

First we prove Theorem 2.1.

Proof of Theorem 2.1. We prove (i) first. Note that and are continuous martingales and

By the definitions of and ,

Then according to Revuz and Yor (2013)[Chapter V, Theorem 1.10], and are two independent Brownian motions.

As for (ii), (2) implies is absolutely continuous with respect to , hence is derivable. Then (1) leads to the result immediately. ∎

Proof of Theorem 2.2. For the “if” part: since and ,

| (51) |

therefore the process is a martingale with respect to , so is the process by similar analysis.

As a consequence, and are martingales with respect to the same filtration. So for any -progressively measurable processes , satisfying (41),

is a martingale with respect to by Lemma 6.1. Moreover,

implies exists. Thus

i.e.

According to Lemma 6.2, the desired result is obtained.

For the“only if” part: if , and are independent, by Lemma 6.2, and are martingales with respect to .

Consequently, are martingales with respect to . Since , and are Brownian motions with respect to according to Lévy characterisation.

On the other hand, and are Brownian motions with respect to as well. That is to say, for any , the conditional distribution of the process given is coincident with its conditional distribution given . Then we can conclude that . Similarly, . ∎

In the following, we complete the proof of Proposition 2.1.

Proof of Proposition 2.1. We prove that the independency of , and is equivalent with the condition (C2), then from Theorem 2.2, we have the condition (C1) is equivalent with the condition (C2).

For the ”” part: It is obvious that is a martingale from Lemma 6.1.

Suppose are bounded determined processes, then

| (52) |

According to the independency of , we have

| (53) |

where . Observe that , then from Lemma 6.3 we have

| (54) |

Substituting (53) and (54) into (52),

Applying Lemma 6.3 to the former equation again, we obtain

If are complex, the proof remains valid, hence we have immediately.

For the ”” part: Suppose and satisfy (41). Note that the range of and in (41) is smaller than the condition (C2), then

accordingly exists. We first claim that

To see this, we only need to prove for any ,

| (55) |

Let

note that , so is a -system and obviously is a -system, moreover, . Suppose , where is a Borel set, then for any we have

| (56) |

Since and

so we have i.e., . Consequently,

| (57) |

From (56) and (57) we know that . According to theorem we can conclude

hence, we have proved our claim (55). implies

we complete proof by Lemma 6.2.

∎

We prove Proposition 2.2 by the equivalence of the condition (C3) and the condition (C1).

Proof of Proposition 2.2.

”(C1)(C3)”: According to and (51), we have is a martingale with respect to . Because (actually, ), then for any ,

which is equivalent with . Hence,

and equivalently, is a martingale with respect to . With the same arguments, is a martingale with respect to as well. Obviously, is a martingale with respect to , so from the definition of , we know is a martingale with respect to and . According to Lévy characterisation (see Shreve (2004)[Theorem 4.6.4]), and are two independent Brownian motions with respect to . Since and are adapted with , so and are also two independent Brownian motions with respect to . Consequently, the joint distribution of and is the same under the condition of and , which implies

| (58) |

In (58), let we obtain . Note that is also independent with , hence we can conclude that , and are mutually independent.

”(C3)(C1)”: Note that , and obviously , and are mutually independent given by the condition (C3). Then for any ,

with similar approach we can prove as well, immediately

which is equivalent to .

As for , we first observe that and are martingales with respect to by the independecy of , and . So according to

is a martingale with respect to . Since and , and note that is adapted to and respectively, so is a martingale with respect to and respectively. Hence, by Lévy characterisation, is a Brownian motion with respect to and respectively. Thus, the distribution of is the same under the condition of and , which result in .

∎

We prove Proposition 2.3 by comparing the distribution of discrete local correlation model and discrete common decomposition model.

Observe that given , the conditional distribution of is

which is just the same as the conditional distribution of . If the condition (C3) holds, and are independent Brownian motions with respect to . Hence, by the independent property of increments, given , we have

Consequently,

| (59) |

Next, for any given , we consider the difference between the distribution of and . Let

For any , we first give a small enough141414Since we focus on the properties when , we can only consider the case that . Then , , , hence there always exists a satisfy the condition. such that for any and ,

| (60) |

Observe that

similar inequality holds for . Let

then

| (61) |

Note that (59) implies

and compared the first term and last term in the right hand of (61), we have

| (62) |

Substituting (62) into (61), we obtain

| (63) |

where denotes the standard normal distribution. For given , it is not difficult to verify that, if

we have

thus

| (64) |

As a consequence of (60), (63) and (64),

similarly,

i.e.

| (65) |

From the definition of Itô’s integral, we have

| (66) |

Combining (65) and (66), as , we have

∎

6.3 Proofs of Results in Section 3

Proof of Theorem 3.1. By optional stopping theorem, , are martingales under , respectively and , guarantee that

which give the martingale properties of and .

If and are strictly increasing and , then (3) holds. With the same discussion in the beginning of Section 2.1, and are derivable with respect to , let

and , be defined as in (4). Then, and , are continuous and strictly increasing processes.

Next, we claim that . We first consider the case that for any . Observe that

| (67) |

| (68) |

then

| (69) |

Since is a time change of , so is adapted to , and is adapted to , consequently is adapted to . Similarly, is adapted to as well. According to (69), the stochastic processes