Convergence Analysis of a Collapsed Gibbs Sampler for Bayesian Vector Autoregressions

Abstract

We study the convergence properties of a collapsed Gibbs sampler for Bayesian vector autoregressions with predictors, or exogenous variables. The Markov chain generated by our algorithm is shown to be geometrically ergodic regardless of whether the number of observations in the underlying vector autoregression is small or large in comparison to the order and dimension of it. In a convergence complexity analysis, we also give conditions for when the geometric ergodicity is asymptotically stable as the number of observations tends to infinity. Specifically, the geometric convergence rate is shown to be bounded away from unity asymptotically, either almost surely or with probability tending to one, depending on what is assumed about the data generating process. This result is one of the first of its kind for practically relevant Markov chain Monte Carlo algorithms. Our convergence results hold under close to arbitrary model misspecification.

1 Introduction

Markov chain Monte Carlo (MCMC) is often used to explore the posterior distribution of a vector of parameters given data . To ensure the reliability of an analysis using MCMC it is essential to understand the convergence properties of the chain in use [6, 7, 9, 10, 20, 26, 48] and, accordingly, there are numerous articles establishing such properties for different MCMC algorithms [e.g. 1, 2, 13, 15, 17, 21, 32, 38, 46]. It has been common in this literature to treat the data as fixed, or realized. Thus, the model for how the data are generated has typically been important only insofar as it determines the likelihood function based on an arbitrary realization—the stochastic properties of the data prescribed by that model have not been emphasized. This is natural since the target distribution, i.e. the posterior distribution, treats the data as fixed. On the other hand, due to the rapid growth of data available in applications, it is also desirable to understand how performance is affected as the number of observations increases. When this happens, the data are more naturally thought of as stochastic; each time the sample size increases by one, the additional observation is randomly generated. The study of how convergence properties of MCMC algorithms are affected by changes in the data is known as convergence complexity analysis [35] and it has attracted increasing attention recently [16, 32, 34, 49, 50].

Accounting for randomness in the data and letting the sample size grow leads to a more complicated analysis than when the data are fixed. In fact, to date, convergence complexity analysis has only been successfully carried out for a few, maybe even one [32], practically relevant MCMC algorithms, by which we mean MCMC algoritms for settings where one could not easily sample by less complicated methods. We study a MCMC algorithm for a fundamental model in time series analysis: a Bayesian vector autoregression with predictors (VARX). Briefly, the VARX we consider assumes that and satisfy, for ,

| (1) |

with independent and multivariate normally distributed with mean zero and common covariance matrix , the set of symmetric and positive definite (SPD) matrices, , , and . As we will see, the likelihood for the VARX is closely related to that of a multivariate linear regression and, consequently, our results apply also to that model. Moreover, (1) simplifies to a multivariate linear regression if for all . We focus on the VARX because it motivates our study and, in particular, our choice of priors. More details on the model specification, priors, and resulting posterior distributions are given in Section 2.

The target distribution of our algorithm is the posterior distribution of given . We will consider both fixed and growing data and refer to the two settings as the small- and large- setting, respectively. By being small we mean that it is fixed and possibly small in comparison to and , but throughout. Many large VARs in the literature [3, 11, 24] are covered by this setting. By being large we mean that it is increasing and that the data are stochastic.

The algorithm we consider is a collapsed Gibbs sampler that simplifies to a commonly considered (non-collapsed) Gibbs sampler when there are no predictors in the model; that is, when in (1). To discuss our results, we require some more notation. Let denote the VARX posterior distribution having density with support on for some and let () be the -step transition kernel for a Markov chain with state space , started at a point . We assume throughout that all discussed Markov chains are irreducible, aperiodic, and Harris recurrent [31], and that sets on which measures are defined are equipped with their Borel -algebra. Our analysis is focused on convergence rates in total variation distance, by which we mean the rate at which approaches zero as tends to infinity, where denotes the total variation norm. If this convergence happens at a geometric (or exponential) rate, meaning there exist a and an such that for every and

| (2) |

then the Markov chain, or the kernel , is said to be geometrically ergodic. The geometric convergence rate is the infimum of the set of such that (2) holds [32]. Since all probability measures have unit total variation norm, is always in , and is geometrically ergodic if and only if . A substantial part of the literature on convergence of MCMC algorithms is centered around geometric ergodicity, for good reasons: under moment conditions, a central limit theorem (CLT) holds for functionals of geometrically ergodic Markov chains [5, 18] and the variance in the asymptotic distribution given by that CLT can be consistently estimated [8, 19, 47], allowing principled methods for ensuring reliability of the results [39, 48]. Our main result in the small- setting gives conditions that ensure when the data are fixed and is the kernel corresponding to the algorithm we consider.

Notice that, although it is suppressed in the notation, , , , and, hence, typically depend on . In the large- setting, we are no longer considering a single dataset, but a sequence of datasets , where here denotes a dataset with observations. Consequently, for every there is a posterior distribution and a Markov chain with kernel that is used to explore it. To each kernel there also corresponds a geometric convergence rate . Since depends on , the sequence is now one of random variables, ignoring possible issues with measurability. If the convergence rate tends to one in probability or almost surely as , we say that the convergence rate is unstable; in practice, we expect an algorithm that generates a chain with geometric convergence rate tending to one to be less reliable when applied to large datasets. Thus, we are interested in bounding away from unity asymptotically, in either one of two senses: first, if there exists a sequence of random variables such that for every and almost surely, then we say that is asymptotically geometrically ergodic almost surely, or the geometric ergodicity is asymptotically stable almost surely. Secondly, if instead of the upper limit being less than unity almost surely it holds that , then we say that is asymptotically geometrically ergodic in probability, or that the geometric ergodicity is asymptotically stable in probability. In the large- setting, we give conditions for asymptotically stable geometric ergodicity, in both of the two senses, of the Markov chain generated by our algorithm. An intuitive, albeit somewhat loose, interpretation of our main results is that the geometric ergodicity is asymptotically stable if the sample covariance matrix tends to some positive definite limit. In particular, as long as this holds, the geometric ergodicity of the Markov chain we study is asymptotically stable under arbitrary model misspecification. Our small- and large- results are complementary: the small- results establish geometric ergodicity for fixed but do not ensure asymptotic geometric ergodicity, while the laarge- results give asymptotic geometric ergodicity but do not imply geometric ergodicity for fixed .

The rest of the paper is organized as follows. We begin in Section 2 by completing the specification of the model and priors. Because some of the priors may be improper we derive conditions which guarantee the posterior exists and is proper. In Section 3 we develop a collapsed Gibbs sampler for exploring the posterior. Conditions for geometric ergodicity for small are presented in Section 4 and conditions for asymptotically stable geometric ergodicity are given in Section 5. Some concluding remarks are given in Section 6.

2 Bayesian vector autoregression with predictors

Recall the definition of the VARX in (1). To complete the specification, we assume that the starting point is non-stochastic and known and that the predictors are strongly exogenous. By the latter we mean that is independent of and has a distribution that does not depend on the model parameters. With these assumptions the following lemma is straightforward. Its proof is provided in Appendix B for completeness. Let , , , , and . Let also and , where is the vectorization operator, stacking the columns of its matrix argument.

Lemma 2.1.

The joint density for observations in the VARX is with given by

where .

For fixed data, is the same as for a multivariate linear regression with partitioned design matrix and coefficient matrix . However, our choice of priors is guided by the vector autoregression. Let denote the set of symmetric positive semi-definite (SPSD) matrices and, to define priors, let , , , and be hyperparameters. Our prior on is of the form , with

and

where means the determinant when applied to matrices. The flat prior on is standard in multivariate scale and location problems, including in particular the multivariate regression model. The priors on and are common in macroeconomics [23] and the prior on includes the inverse Wishart () and Jeffreys prior () as special cases. In other work on similar models it is often assumed that has full rank or that the prior for is proper [1, 2, 11, 13, 25, 44]. Treating and differently is appealing in the current setting: it adheres to the common practice of using flat priors for regression coefficients such as , while and can be chosen to reflect the fact that many commonly studied time series are known to be near non-stationary in the unit root sense. In particular, with economic and financial data it is often reasonable to expect the diagonal elements of to be near one. For a more thorough discussion of popular priors in Bayesian VARs we refer the reader to Karlsson [23].

The following result gives two different sets of conditions that lead to a proper posterior. Though we focus on proper normal or flat priors for in the rest of the paper, it may be relevant for other work to note that the proposition holds for any prior satisfying the conditions. For example, could be truncated to impose stability of the VARX, which if corresponds to a prior with support only on for which the spectral norm of is less than one [see e.g. 28, for definitions].

Proposition 2.2.

If either

-

1.

, has full column rank, , and is proper; or

-

2.

has full column rank, , and is bounded,

then the posterior distribution is proper; if, in addition, , then with , the posterior density is characterized by

| (3) |

Proof.

Appendix B. ∎

The first set of conditions is relevant to the small -setting. It implies that if the prior on is a proper inverse Wishart density, so that and , then the posterior is proper if is proper and has full column rank. In particular, or can be arbitrarily large in comparison to . Thus, this setting is compatible with large VARs [3, 11, 24]. The second set of conditions allows for the use of improper priors also on and when is large in comparison to all of , , and . The full column rank of is natural in large- settings. In practice, one expects it to hold unless the squares regression of on and gives residuals that are identically zero.

The literature on convergence properties of MCMC algorithms for Bayesian VAR(X)s is limited. An MCMC algorithm for a multivariate linear regression model has been proposed and its convergence rate in the small- setting studied [13]. By the preceding discussion, this includes the VARX as a special case, however, the (improper) prior used is which is not compatible with the large VARXs we allow for in the small- setting. A two-component ( and ) Gibbs sampler for Bayesian vector autoregressions without predictors has been proposed [22], but the analysis of it is simulation-based and as such does not provide any theoretical guarantees. Our results address this since, as we will discuss in more detail below, the algorithm we consider simplifies to this Gibbs sampler when there are no predictors.

3 A collapsed Gibbs sampler

If the precision matrix in the prior on , , is a matrix of zeros, then the VARX posterior is a normal-(inverse) Wishart for which MCMC is unnecessary. However, when the posterior is analytically intractable and there are many potentially useful MCMC algorithms. For example, the full conditional distributions have familiar forms so it is straightforward to implement a three-component Gibbs sampler. Another sensible option is to group and and update them together. Here, we will instead make use of the particular structure the partitioned matrix offers and devise a collapsed Gibbs sampler [27]; that is, a Gibbs sampler where some updates are not using full conditional distributions, but conditional distributions with one or more components integrated out. As we will see, the structure of the collapsed sampler, and in particular relations between the convergence rates of marginal chains and the full chain, is instrumental to our development. For a discussion more generally of how operator norms of collapsed and non-Collapsed Gibbs samplers compare we refer the reader to [27].

For the case where the precision matrix in the prior on is positive definite and , so that the predictor matrix plays no role in the model, a two-component Gibbs sampler has been proposed [23]. We will show that the algorithm we study includes this Gibbs sampler as a special case, with minor modifications, and as a consequence our results apply almost verbatim to that sampler. A formal description of one iteration of the collapsed Gibbs sampler is given in Algorithm 1.

We next give the conditional distributions necessary for its implementation. Let denote the matrix normal distribution with mean and scale matrices and , that is, the distribution of a matrix whose vectorization is multivariate normal with mean and covariance matrix , where is the Kronecker product. Let also denote the inverse Wishart distribution with scale matrix and degrees of freedom. For any real matrix , define to be the projection onto its column space and the projection onto the orthogonal complement of its column space. Finally, define and .

Lemma 3.1.

If one of the two sets of conditions in Proposition 2.2 holds, then

Proof.

Appendix B. ∎

The collapsed Gibbs sampler in Algorithm 1 simulates a realization from a Markov chain having one-step transition kernel defined, for any measurable , by

where the subscript is short for collapsed. However, instead of working directly with we will use its structure to reduce the problem in a convenient way. Consider the sequence , , obtained by ignoring the component for in Algorithm 1. The sequence is essentially generated by a two-component Gibbs sampler. More precisely, if is replaced by the identity in the conditional distributions of and used in Algorithm 1, then the algorithm defined by steps 1, 2, 3, and 5 is a two-component Gibbs sampler exploring the posterior for the model that takes in (1). The transition kernel for is, for any measurable ,

A routine calculation shows that since , by construction, has invariant distribution , then has the VARX posterior as its invariant distribution.

The sequences and are also Markov chains. The transition kernel for the sequence is, for any measurable ,

| (4) |

The transition kernel, , for the sequence is constructed similarly. The kernel satisfies detailed balance with respect to the posterior marginal and similarly for and hence each has the respective posterior marginal as its invariant distribution. However, the kernels and do not satisfy detailed balance with respect to their invariant distributions.

In Sections 4 and 5 we will establish geometric ergodicity of and study its asymptotic stability, respectively. Our approach, which is motivated by the following lemma, will be to analyze in place of ; the lemma says we can analyze either of , or in place of (see also [36]). The proof of the lemma uses only well known results about de-initializing Markov chains [37] and can be found in Appendix B.

Lemma 3.2.

For any , and ,

The primary tool we will use for investigating both geometric ergodicity and asymptotic stability is the following well known result [40, Theorem 12], which has been specialized to the current setting. Note that the kernel acts to the left on measures, that is, for a measure , we define

Theorem 3.3.

Suppose is such that for some and some

| (5) |

Also suppose there exists , a measure , and some such that

| (6) |

Then is geometrically ergodic and, moreover, if

then, for any initial distribution ,

| (7) |

It is common for the initial value to be chosen deterministically, in which case (7) suggests choosing a starting value to minimize . Theorem 3.3 has been successfully employed to determine sufficient burn-in in the sense that the upper bound on the right-hand side of (7) is below some desired value [20, 21, 41], but, unfortunately, the upper bound is often so conservative as to be of little utility. However, our interest is twofold; it is easy to see that there is a such that and hence if satisfies the conditions, then it is geometrically ergodic and, as developed and exploited in other recent research [32], the geometric convergence rate is upper bounded by . Outside of toy examples, we know of no general state space Monte Carlo Markov chains for which is known.

Consider the setting where the number of observations tends to infinity; that is, there is a sequence of data sets and corresponding transition kernels with . If almost surely, then we say the drift (5) and minorization (6) are asymptotically unstable in the sense that, asymptotically, they provide no control over . On the other hand, because establishing that almost surely or that , leads to asymptotically stable geometric ergodicity as defined in the introduction.

Notice that depends on the drift function through , , and . Thus the choice of drift function which establishes geometric ergodicity for a fixed may not result in asymptotic stability as . Indeed, in Section 4 we use one to show that is geometrically ergodic under weak conditions when is fixed, while in Section 5 a different drift function and slightly stronger conditions are needed to achieve asymptotically stable geometric ergodicity of .

4 Geometric ergodicity

In this section we consider the small- setting. That is, is fixed and the data and observed, or realized, and hence treated as constant. Accordingly, we do not use a subscript for the sample size on the transition kernels. We next present some preliminary results that will lead to geometric ergodicity of , and hence and .

We fix some notation before stating the next result. Let denote the Euclidean norm when applied to vectors and the spectral (induced) norm when applied to matrices, denotes the Frobenius norm for matrices, and superscript denotes the Moore–Penrose pseudo-inverse. Least squares estimators of and are denoted by and , respectively, and .

Lemma 4.1.

Define by . If and at least one of the two sets of conditions in Proposition 2.2 holds, then for any and with

the kernel satisfies the drift condition

Proof.

Assume first ; the general case is then recovered by replacing and by and everywhere. Using (4) and Fubini’s Theorem yields

Lemma 3.1 and standard expressions for the moments of the multivariate normal distribution [42, Theorem 10.18] give for the inner integral that

The triangle inequality gives . We work separately on the last two summands. First, since is SPSD, we get by Lemma A.2 that

Secondly,

Now by Lemma A.3, with and taking the roles of what is there denoted and , we have for any generalized inverse (denoted by superscript ) that

is upper bounded by

| (8) |

Lemma A.4 says that is one such generalized inverse. Using that the Moore–Penrose pseudo-inverse distributes over the Kronecker product [30], the middle part of this generalized inverse can be written as . Thus, for this particular choice of generalized inverse (8) is equal to

Thus, using also that by Lemma A.2 since SPSD, is less than

Since the right-hand side does not depend on , the proof is completed upon integrating both sides with respect to . ∎

Lemma 4.2.

If at least one of the two sets of conditions in Proposition 2.2 holds, then for any and such that , there exists a probability measure and

such that

Proof.

We will prove that there exists a function , depending on the data and hyperparameters, such that and for every such that , or, equivalently, . This suffices since if such a exists, then we may take and define the distribution by, for any Borel set ,

Let and so that can be written

To establish existence of a with the desired properties we will lower bound the first and third term in using two inequalities, namely

and, for every such that ,

We prove the former inequality first. Since , it suffices to prove that . For this, Lemma A.2.3 says it is enough to prove that is SPSD. But the Frisch–Waugh–Lovell theorem [29, Section 2.4] says , and therefore

which is clearly SPSD.

For the second inequality we get, using the triangle inequality, submultiplicativity, and that the Frobenius norm upper bounds the spectral norm,

Since the spectral norm for SPSD matrices is the maximum eigenvalue, we have shown that is SPSD. Thus, is also SPSD and, hence,

which is what we wanted to show. We have thus established that is greater than

Finally, the stated expression for , and that it is indeed positive, follows from that under the first set of conditions in Proposition 2.2 is SPD, and under the second set of conditions is SPD by Lemma A.1; in either case, both and are SPD and, consequently, is proportional to an inverse Wishart density with scale matrix and degrees of freedom. ∎

We are ready for the main result of this section.

Theorem 4.3.

If and at least one of the two sets of conditions in Proposition 2.2 holds, then the transition kernels , , and are geometrically ergodic.

Proof.

We note that, since is unbounded off compact sets and it is routine to show that is weak Feller [31, p. 124], the theorem can in fact be proven without using Lemma 4.2 [31, Lemma 15.2.8]. However, with Lemma 4.2 we also get an explicit bound on the convergence rate, through Theorem 3.3, which will be useful in what follows.

5 Asymptotic stability

We consider asymptotically stable geometric ergodicity as . Motivated by Lemma 3.2, we focus on the sequence of kernels , where is the kernel with the dependence on the sample size made explicit; we continue to write when is arbitrary but fixed. Similar notation applies to the kernels and .

It is clear that as changes so do the data and . Treating and as fixed is not appropriate unless we only want to discuss asymptotic properties holding pointwise, i.e. for particular, or all, paths of the stochastic process , which is unnecessarily restrictive. We assume that , are defined on a common probability space so the joint distribution of and exists for every , and we allow for model misspecification; that is, and need not satisfy (1).

Recall that Theorem 3.3 is instrumental to our strategy: if satisfies Theorem 3.3 with some , , , , and , then there exists a that upper bounds . We focus on the properties of those , , as tends to infinity. Throughout the section we assume that the priors, and in particular the hyperparameters, are the same for every . The latter is not necessary and could be replaced by appropriate bounds on how the hyperparameters change with ; however, doing so complicates notation and does not lead to fundamental insights in our setting. For example, could be allowed to vary with as long as its eigenvalues are bounded away from zero and from above.

Clearly, the choice of drift function is important for the upper bound one obtains. The drift function used for the small- regime is not well suited for the asymptotic analysis in this section. Essentially, problems occur if , , or so that the corresponding upper bounds satisfy almost surely [32, Proposition 2]. Consider Theorem 4.3. Since we can take for all , only or can lead to problems. Because is essentially a quadratic in , it is clear that if and only if , while we show in Appendix B.1 that almost surely as if

We expect this to occur in many relevant configurations. Indeed, we expect the order of will often be at least that of . To see why, consider the case without predictors and data generated according to the VARX. Then , where denotes the maximum eigenvalue, and is the maximum likelihood estimator of which is known to be consistent, for example, if data are generated from a stable VAR with i.i.d. Gaussian innovations [28]. For such VARs it also holds that converges in probability to some SPD limit [28], and hence . Similar arguments can be made for any other data generating processes for which and are suitably bounded in probability or almost surely as .

The intuition as to why the drift function that works in the small- regime is not suitable for convergence complexity analysis is that the drift function should be centered (minimized) at a point the chain in question can be expected to visit often [32]. The function defined by is minimized when , but there is in general no reason to believe the -component of the chain will visit a neighborhood of the origin often. On the other hand, if the number of observations grows fast enough in comparison to other quantities and we suppose momentarily that the data are generated from the VARX, then we expect the marginal posterior density of to concentrate around the true , i.e. the according to which the data is generated. We also expect that for large the least squares and maximum likelihood estimator is close to the true . Thus, intuitively, the -component of the chain should visit the vicinity of often. Formalizing and extending this intuition to cases where the model can be misspecified, so that no true exists, leads to the main result of the section.

Let us re-define by . We will use the following lemma to verify the drift condition in (9) for all large enough almost surely or with probability tending to one. The probabilistic qualifications are needed because, in contrast to in the small setting, here depends on the data. Accordingly, the given in the lemma depends on and, consequently, need not be less than one for a fixed or a particular sample.

Lemma 5.1.

Proof.

Suppose first that and notice that has full column rank, and hence exists. Since is a multivariate normal density, standard expressions for the moments of the multivariate normal distribution gives

| (9) |

For the second term we use cyclical invariance of the trace to write

Since and are both SPD, the last expression is in the form required by Lemma A.2, and hence

where the last line uses that the trace of a projection matrix is the dimension of the space onto which it is projecting. Focusing now on the first term on the right hand side in (9) we have, defining and using , that

is upper bounded by

| (10) |

Moreover, since the Woodbury identity gives so that the first term in (10) can be upper bounded as follows:

Here, the power , , for a SPD matrix is defined by taking the spectral decomposition , where and denote the largest and smallest eigenvalues, respectively, and setting

Now by standard properties of eigenvalues and eigenvectors of Kronecker products [14, Theorem 4.2.12] we get

In addition, using Lemma A.2,

It remains to deal with the second term in (10). Using a similar technique as with the previous term, applying sub-multiplicativity and Lemma A.2 twice, we have

Putting things together we have shown that, for any ,

and hence we get from (9)

The proof for the case is completed by upper bounding , integrating both sides with respect to , and noting that

where we have used that , and that . The general case is recovered by replacing and by and , respectively, and invoking Lemma A.1. That is invertible also in the general case follows from the same lemma. ∎

Lemma 5.2.

If at least one of the two sets of conditions in Proposition 2.2 holds, then for any and such that , there exists a probability measure and

such that

Proof.

The proof idea is similar to that for Lemma 4.2. We prove that there exists a , depending on the data and the hyperparameters, such that and for every such that .

Assume first that and let be the degrees of freedom in the full conditional distribution for . Using that is SPSD and that , we get by Lemma A.2 that

Moreover, for any such that ,

where the first inequality follows from that and that, therefore, is SPSD, and the second inequality follows from that the Frobenius norm upper bounds the spectral norm, so that .

With the determinant and trace inequalities just established, we have that is, for any satisfying the hypotheses, lower bounded by

Noticing that so defined is proportional to an inverse Wishart density and using well known expression for its normalizing constant finishes the proof for the case where . The general case is recovered upon replacing and by and everywhere and invoking Lemma A.1. ∎

We are ready to state the main result of the section. Recall, denotes the largest eigenvalue of its argument matrix; let denote the smallest.

Theorem 5.3.

If

-

(a)

,

-

(b)

there exists a constant such that, with and , almost surely as ,

then , and are asymptotically geometrically ergodic almost surely.

Proof.

By Lemma 3.2, it is enough to prove that almost surely for the corresponding to . Inspecting the definition of in Theorem 3.3 one sees that it suffices to show that Lemmas 5.1 and 5.2 apply and that the , , , and they give almost surely satisfy, respectively: (i) , (ii) , (iii) , and (iv) . The prior is bounded since is positive definite by (a), and (b) implies has full column rank almost surely for all large enough , so Lemma 5.1 applies for all large enough almost surely. Moreover, the Frisch–Waugh–Lovell theorem [29, Section 2.4] says is the upper block in the least squares coefficient estimate in the regression of on , i.e. . Hence, with probability tending to one,

which follows from upper bounding the Frobenius norm by the spectral norm times and using the Minimax Principle [4, Corollary III.1.2]; in particular, since and are the trailing and leading block of , respectively, their eigenvalues must be bounded between the smallest and largest of , and so also between and almost surely as . Since we have shown , it follows that , so (i) holds. That and give , i.e. (ii) holds, and hence we can pick a sequence , , such that (iii) holds. For (iv), we have with denoting the th eigenvalue of ,

Now, we have picked so that , and since is the Schur complement of in , its eigenvalues are bounded between and almost surely as [43, Theorem 5]. Thus, (say) for all large enough almost surely, for every . Thus, almost surely,

where the final inequality follows from that the fraction in parentheses is and that the exponent is of the same order as ; this finishes the proof. ∎

If assumption (b) is relaxed to holding with probability tending to one instead of almost surely, then the conclusion can be weakened accordingly to give the following corollary. We omit the proof since it is essentially the same as the proof of Theorem 5.3, arguing that the necessary conditions hold with probability tending to one.

Corollary 5.1.

If and there exists an such that with probability tending to one as , then , and are asymptotically geometrically ergodic in probability.

5.1 Example

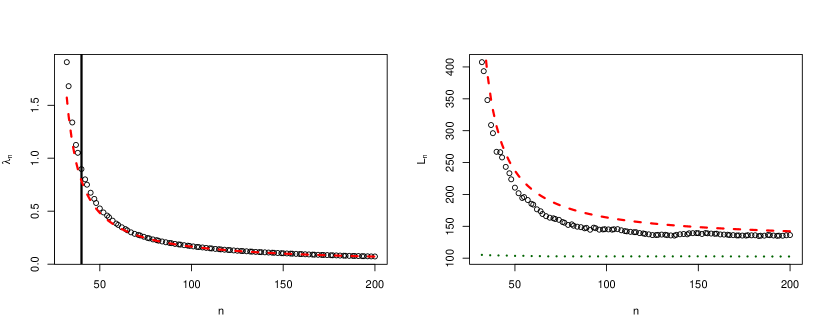

We illustrate the behavior of , , and from Lemmas 5.1 and 5.2 in a stable VARX of order ; that is and in (1). Stability makes some the arguments in this example easy to motivate formally, but we emphasize that it is not needed for the preceding results. We take for all , , , and pick hyperparameters , , , and . We first examine , , and analytically and then illustrate those calculations using simulations.

In the present setting, the expressions for and in Lemma 5.1 simplify to

Because the VARX is stable, and are consistent for and , respectively, as [28], which implies

and

Clearly, and . To get some intuition for how affects and , let us ignore the stochastic terms that are of lower order when grows with fixed; that is, consider the approximations

Because , it holds that for large enough even if grows, as long as . By contrast, is of order if grows, regardless of . This suggests, at least informally, that can stay below one if grows with but that may not be bounded in such settings.

To investigate how behaves, note that we can take with and have with probability tending to one as grows with fixed. Thus, using that in probability and that the determinant is a continuous mapping,

Consider the approximation and note, as argued previously, . Thus, if grows, then is of the order , regardless of , and therefore we do not expect to behave well if grows with .

To investigate the finite sample behavior, we generate one sample path from the VARX and compute , , and using the first observations in that sample path, for different values of . We compare these quantities to the corresponding ones from Lemmas 4.1 and 4.2, that is, those that are obtained in the small- setting. For simplicity we also refer to the latter quantities as obtained using a non-centered drift function. Code producing the results is available at https://github.com/koekvall/gibbs-bvarx.

When generating data, we fix and , so . We construct by letting have entries drawn independently from the uniform distribution on and taking

which ensures .

The first plot in Figure 1 shows the calculated using the centered drift function from the large- setting, is less than when is greater than 40 in our sample, but greater than one for smaller samples; this illustrates the fact that our large- results do not control the convergence rate in small (fixed) samples.

The second plot in Figure 1 shows the observed values of , calculated using the centered drift function, appear to tend to their probability limit

where for the used to generate our sample path. Figure 1 also shows the behavior of and calculated using the centered drift function is, as changes, similar to that observed if and are replaced by and . We have not plotted the calculated using the non-centered drift-function since it can be identically zero. However, the obtained from that drift function is plotted and is smaller (better) than that for the centered drift function for every considered (second plot, Figure 1).

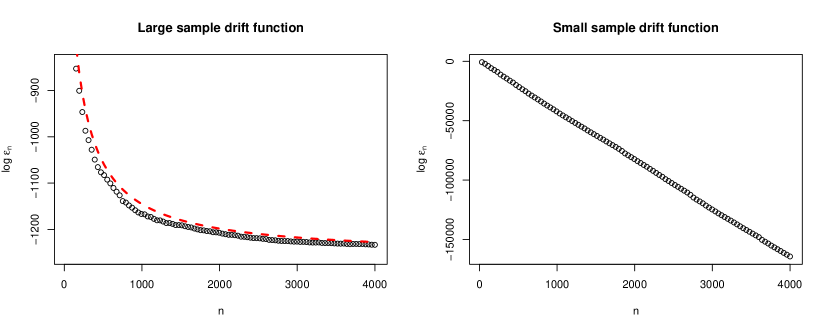

The first plot in Figure 2 indicates calculated using the centered drift function decreases towards as increases, and that there is decent agreement with the approximation obtained by replacing and by and . In comparison to and , it seems a much larger is needed for to get close to its probability limit. Note also that, unlike for and , larger values of correspond to better convergence rate bounds.

The second plot in Figure 2 shows the from Lemma 4.2, calculated using the non-centered drift function. That appears to tend to zero at an exponential rate (linear for its logarithm). This rate is straightforward to verify analytically by noting that, in the expression for in Lemma 4.2, the exponent is of order and what is inside the exponent tends in probability to a number between zero and one in the current setting. Hence, unlike the from Lemma 5.2, it does not provide any control over the convergence rate asymptotically.

In summary, this example shows the drift parameters and are typically smaller (better) for the non-centered drift function used in the small- setting, but the minorization parameter obtained using that drift function tends to zero as tends to infinity.

NOTE: Circles correspond to observed and calculated as in Lemma 5.1. Dashed lines are those and but with and replaced by and . The vertical line indicates , the smallest for which . The dotted line is calculated as in Lemma 4.1; the from that lemma is not shown because it can be taken to be for all ..

6 Discussion

Markov chain Monte Carlo is used in a wide range of problems, including but not limited to the Bayesian settings considered here. However, the theoretical properties of algorithms used by practitioners are not always well understood. We have focused on the case of Bayesian vector autoregressions with predictors. This is one of the most common models in time series, and in particular in the analysis and forecasting of macroeconomic time series. Moreover, due to similarities of the likelihoods of vector autoregressions and multivariate linear models, our results apply also to the latter. The Gibbs sampler has been suggested for exploring the posterior distribution of the parameters and when there are no predictors [23], but there has been a lack of theoretical support. We have addressed this by proposing a collapsed Gibbs sampler that handles predictors and studying its convergence properties. Since our algorithm simplifies to the usual Gibbs sampler when there are no predictors, our results apply also in that setting.

We have proven that our algorithm generates a geometrically ergodic Markov chain under reasonable assumptions (Theorem 4.3). This result is applicable both in classical settings where the sample size is large (but fixed) in comparison to the number of parameters, and in large VARXs where the dimension of the process or the lag length is large in comparison to the number of observations. Though we have not emphasized it, this geometric ergodicity holds also if the model is misspecified. Indeed, once the data are fixed and the posterior specified, it is of no importance for the convergence rate how the data were actually generated, as long as they satisfy the conditions laid out in the relevant lemmas and theorem. Thus, with the algorithm we consider, characteristics of the posterior distribution can be reasonably estimated using principled approaches to ensuring the simulation results are trustworthy [7, 20, 48]. Our asymptotic analysis, or convergence complexity analysis, indicates our algorithm should perform well also in large samples; we have proven that, as the sample size tends to infinity, the geometric ergodicity of the sequence of transition kernels corresponding to our algorithm is asymptotically stable. This result is one of the first of its kind for practically relevant MCMC algorithms. As with our results for small samples, our asymptotic results hold under almost arbitrary model mispecification, as specified in Theorem 5.3.

Avenues for future research include convergence complexity analysis of cases where the dimension of the process or the lag length tends to infinity, either together with the sample size or for a fixed sample size. Our proof uses the intuition that the posterior concentrates near the least squares estimator, and it may be possible to formalize this intuition also in settings where , , or grows with . However, it is likely that the drift function would need to be adjusted, perhaps by using a different norm: the Frobenius norm has convenient properties that we used in our proofs but is often less useful in high-dimensional settings [45]. If the sample size is fixed or grows slowly in comparison to other quantities, one would likely have to use a different drift function altogether or move to an approach that avoids the use of the minorization condition [33, 34].

Acknowledgements

The authors thank an Associate Editor, two reviewers, and Dootika Vats for suggestions and insightful comments that improved the paper. Ekvall gratefully acknowledges support by the FWF (Austrian Science Fund, https://www.fwf.ac.at/en/) [P30690-N35].

References

- [1] T. Abrahamsen and J. P. Hobert. Convergence analysis of block Gibbs samplers for Bayesian linear mixed models with . Bernoulli, 23:459–478, 2017.

- [2] G. Backlund and J. P. Hobert. A note on the convergence rate of MCMC for robust Bayesian multivariate linear regression with proper priors. Computational and Mathematical Methods, 2, 2020.

- [3] M. Bańbura, D. Giannone, and L. Reichlin. Large Bayesian vector autoregressions. Journal of Applied Econometrics, 25:71–92, 2009.

- [4] R. Bhatia. Matrix Analysis. Springer New York, 2012.

- [5] K. S. Chan and C. J. Geyer. Comment on “Markov chains for exploring posterior distributions”. The Annals of Statistics, 22:1747–1758, 1994.

- [6] C. R. Doss, J. M. Flegal, G. L. Jones, and R. C. Neath. Markov chain Monte Carlo estimation of quantiles. Electronic Journal of Statistics, 8:2448–2478, 2014.

- [7] J. M. Flegal, M. Haran, and G. L. Jones. Markov chain Monte Carlo: Can we trust the third significant figure? Statistical Science, 23:250–260, 2008.

- [8] J. M. Flegal and G. L. Jones. Batch means and spectral variance estimators in Markov chain Monte Carlo. The Annals of Statistics, 38:1034–1070, 2010.

- [9] J. M. Flegal and G. L. Jones. Implementing MCMC: Estimating with confidence. In S. Brooks, A. Gelman, X.-L. Meng, and G. L. Jones, editors, Handbook of Markov Chain Monte Carlo. Chapman & Hall, Boca Raton, 2011.

- [10] C. J. Geyer. Practical Markov chain Monte Carlo (with discussion). Statistical Science, 7:473–511, 1992.

- [11] S. Ghosh, K. Khare, and G. Michailidis. High-dimensional posterior consistency in Bayesian vector autoregressive models. Journal of the American Statistical Association, pages 1–14, 2018.

- [12] D. A. Harville. Matrix Algebra From a Statistician’s Perspective. Springer New York, 1997.

- [13] J. P. Hobert, Y. J. Jung, K. Khare, and Q. Qin. Convergence analysis of MCMC algorithms for Bayesian multivariate linear regression with non-Gaussian errors. Scandinavian Journal of Statistics, 2018.

- [14] R. A. Horn and C. R. Johnson. Topics in Matrix Analysis. Cambridge University Press, New York, 1991.

- [15] S. F. Jarner and E. Hansen. Geometric ergodicity of Metropolis algorithms. Stochastic Processes and Their Applications, 85:341–361, 2000.

- [16] J. E. Johndrow, A. Smith, N. Pillai, and D. B. Dunson. MCMC for imbalanced categorical data. Journal of the American Statistical Association, pages 1–10, 2018.

- [17] A. A. Johnson and G. L. Jones. Geometric ergodicity of random scan Gibbs samplers for hierarchical one-way random effects models. Journal of Multivariate Analysis, 140:325–342, 2015.

- [18] G. L. Jones. On the Markov chain central limit theorem. Probability Surveys, 1:299–320, 2004.

- [19] G. L. Jones, M. Haran, B. S. Caffo, and R. Neath. Fixed-width output analysis for Markov chain Monte Carlo. Journal of the American Statistical Association, 101:1537–1547, 2006.

- [20] G. L. Jones and J. P. Hobert. Honest exploration of intractable probability distributions via Markov chain Monte Carlo. Statistical Science, 16:312–334, 2001.

- [21] G. L. Jones and J. P. Hobert. Sufficient burn-in for Gibbs samplers for a hierarchical random effects model. The Annals of Statistics, 32:784–817, 2004.

- [22] K. R. Kadiyala and S. Karlsson. Numerical methods for estimation and inference in Bayesian VAR-models. Journal of Applied Econometrics, 12:99–132, 1997.

- [23] S. Karlsson. Forecasting with Bayesian vector autoregression. In Handbook of economic forecasting, pages 791–897. Elsevier, 2013.

- [24] G. M. Koop. Forecasting with medium and large Bayesian VARs. Journal of Applied Econometrics, 28:177–203, 2013.

- [25] D. Korobilis. Forecasting in vector autoregressions with many predictors. In Bayesian econometrics, pages 403–431. Emerald Group Publishing Limited, 2008.

- [26] K. Łatuszyński, B. Miasojedow, and W. Niemiro. Nonasymptotic bounds on the estimation error of MCMC algorithms. Bernoulli, 19:2033–2066, 2013.

- [27] J. S. Liu. The collapsed Gibbs sampler in Bayesian computations with applications to a gene regulation problem. Journal of the American Statistical Association, 89:958–966, 1994.

- [28] H. Lütkepohl. New Introduction to Multiple Time Series Analysis. Springer Berlin Heidelberg, 2005.

- [29] J. G. MacKinnon and R. Davidson. Econometric Theory and Methods. Oxford University Press, 2003-10-11, 2003.

- [30] J. R. Magnus and H. Neudecker. Matrix Differential Calculus With Applications in Statistics and Econometrics. Wiley John & Sons, 2002-07-11, 2002.

- [31] S. Meyn and R. L. Tweedie. Markov Chains and Stochastic Stability. Cambridge University Press, 2011.

- [32] Q. Qin and J. P. Hobert. Convergence complexity analysis of Albert and Chib’s algorithm for Bayesian probit regression. The Annals of Statistics, 47:2320–2347, 2019.

- [33] Q. Qin and J. P. Hobert. Geometric convergence bounds for Markov chains in Wasserstein distance based on generalized drift and contraction conditions. arXiv e-prints, page arXiv:1902.02964, 2019.

- [34] Q. Qin and J. P. Hobert. Wasserstein-based methods for convergence complexity analysis of MCMC with applications. arXiv e-prints, 2019.

- [35] B. Rajaratnam and D. Sparks. MCMC-Based inference in the era of big data: A fundamental analysis of the convergence complexity of high-dimensional chains. arXiv e-prints, page arXiv:1508.00947, 2015.

- [36] C. P. Robert. Convergence control methods for Markov chain Monte Carlo algorithms. Statistical Science, 10(3):231–253, 1995.

- [37] G. O. Roberts and J. S. Rosenthal. Markov chains and de-initializing processes. Scandinavian Journal of Statistics, 28:489–504, 2001.

- [38] G. O. Roberts and R. L. Tweedie. Geometric convergence and central limit theorems for multidimensional Hastings and Metropolis algorithms. Biometrika, 83:95–110, 1996.

- [39] N. Robertson, J. M. Flegal, D. Vats, and G. L. Jones. Assessing and visualizing simultaneous simulation error. Journal of Computational and Graphical Statistics (to appear), 2020.

- [40] J. S. Rosenthal. Minorization conditions and convergence rates for Markov chain Monte Carlo. Journal of the American Statistical Association, 90:558–566, 1995.

- [41] J. S. Rosenthal. Analysis of the Gibbs sampler for a model related to James–Stein estimators. Statistics and Computing, 6:269–275, 1996.

- [42] J. R. Schott. Matrix Analysis for Statistics. Wiley, Hoboken, New Jeresy, second edition, 2005.

- [43] R. L. Smith. Some interlacing properties of the Schur complement of a Hermitian matrix. Linear Algebra and its Applications, 177:137–144, 1992.

- [44] G. C. Tiao and A. Zellner. On the Bayesian estimation of multivariate regression. Journal of the Royal Statistical Society. Series B (Methodological), 26:277–285, 1964.

- [45] J. A. Tropp. An introduction to matrix concentration inequalities. Foundations and Trends in Machine Learning, 8(1-2):1–230, 2015.

- [46] D. Vats. Geometric ergodicity of Gibbs samplers in Bayesian penalized regression models. Electronic Journal of Statistics, 11:4033–4064, 2017.

- [47] D. Vats, J. M. Flegal, and G. L. Jones. Strong consistency of multivariate spectral variance estimators in Markov chain Monte Carlo. Bernoulli, 24:1860–1909, 2018.

- [48] D. Vats, J. M. Flegal, and G. L. Jones. Multivariate output analysis for Markov chain Monte Carlo. Biometrika, 106:321–337, 2019.

- [49] J. Yang and J. S. Rosenthal. Complexity results for MCMC derived from quantitative bounds. arXiv e-prints, 2019.

- [50] Y. Yang, M. J. Wainwright, and M. I. Jordan. On the computational complexity of high-dimensional Bayesian variable selection. The Annals of Statistics, 44:2497–2532, 2016.

Appendix A Preliminaries

Lemma A.1.

If , , , and has full column rank, then with , ,

-

1.

is invertible,

-

2.

is invertible, and

-

3.

.

Proof.

We start with 1. Suppose for contradiction that there exists such that , which is equivalent to . This can happen either if , which contradicts the full column rank of , or if is a non-zero vector in the column space of that also lies in the column space of , which again contradicts the full column rank of . The proof for 2 is exactly the same as that of 1 but with in place of . Point 3 is an immediate consequence the Frisch–Waugh–Lovell theorem [29, Section 2.4], which says among other things that . ∎

Lemma A.2.

For any , , and invertible ,

-

1.

,

-

2.

,

-

3.

, and

-

4.

.

Proof.

All claims can be reduced to the case where by either writing and replacing and by and , respectively, or by writing and replacing and by and , respectively. Assume thus that . Since is SPD, the eigenvalues of are the reciprocals of those of . But, letting denote the th eigenvalue in, say, decreasing order, Weyl’s inequalities [4, Corollary III.2.2] say , and hence , which proves the first claim. The remaining claims follow similarly since the spectral norm is the maximum eigenvalue for SPSD matrices and the determinant is the product of eigenvalues. ∎

Lemma A.3.

For any , , and ,

where superscript denotes an arbitrary generalized inverse.

Proof.

Consider the optimization problem of minimizing defined by

If , then any such that is a solution. Thus, for any generalized inverse, solves the problem [12, Theorem 9.1.2]. On the other hand, if then since has full rank, the unique solution is . Now a contradiction arises if for some , , which finishes the proof. ∎

Lemma A.4.

For and , we have that is a generalized inverse of , where superscript indicates a generalized inverse.

Proof.

We check the definition, namely that . Indeed, using that , . ∎

Appendix B Main results

Proof Lemma 2.1.

Let us suppress conditioning on the parameters for simplicity. We have

Consider an arbitrary term in the product. We have . Since is a function of , both and are fixed when conditioning on and . Thus, the distribution of is determined by that of . But are functions of and , and is an i.i.d. sequence independent of , and hence . Thus, , and, consequently, . Now the result follows by straightforward algebra and the fact that the distribution of does not depend on the model parameters. ∎

Proof Proposition 2.2.

Assuming the posterior is proper, the given expression for the density, up to scaling, follows from routine calculations. We prove the posterior is indeed proper under either of the two sets of conditions. Since

only the conditional density matters when deriving the posterior. Under either of the two sets of conditions, has full column rank so is invertible and we may define , , and . Let also and use to write

| (11) |

The right-most term is a kernel of a matrix normal density for with mean and scale matrices and . Thus, integrating with respect to gives,

Thus, to show that can be normalized to a proper posterior, we need only show that

| (12) |

Let us consider the two sets of conditions separately, starting with the first. Since

we can upper bound the integrand in (12) by

which since we are assuming that , i.e. that and that is SPD, is the product of a proper inverse Wishart and a proper density for . This finishes the proof for the first set of conditions.

For the second set of conditions, notice that for (12) it suffices, since is SPSD, and hence and both bounded, to show that

Let and so that . Using the same decomposition as before we have for the last integrand

Under the second set of assumptions, the last line is proportional to the product of an inverse Wishart density for with scale matrix and degrees of freedom and a matrix normal density for with mean and scale matrices and , and hence integrable. The assumption that has full column ensures that, by Lemma A.1, and are positive definite matrices. ∎

Proof of Lemma 3.1.

The full conditional distribution of is immediate from dropping terms not depending on in (B). Consider next the integrand in (12). The first term in the exponential is

Thus, the log of the integrand is quadratic as a function of , with Hessian and gradient , which implies the desired distribution for . Finally, the distribution of is immediate from dropping terms in the integrand in (12) not depending on . ∎

Proof Lemma 3.2.

Assume , are generated by the collapsed Gibbs sampler in Algorithm 1 started at some point . The equality follows from showing that and are co-de-initializing Markov chains [37, Corollary 1]. That they are both Markov chains is clear from the construction of the updates in Algorithm 1. That is de-initializing for , i.e. that the distribution of does not depend on , is immediate from that is a function (coordinate projection) of . The other direction, that is de-initializing for , is by construction of the algorithm: since is a coordinate projection of , the distribution of is determined by that of , and the distribution from which this value is drawn (line 4, Algorithm 1) does not depend on . Similarly, notice that the distribution of is the same as by construction of the algorithm. Thus, is de-initializing for and the inequality follows [37, Theorem 1]. ∎

B.1 Inadequacy of Drift Function in Theorem 4.3

Proposition B.1.

For the defined in Lemma 4.1 it holds for some and , depending on the hyperparameters but not the data, that

and hence if and only if .

Proof.

Since is SPD, the term is positive, and so dropping it and the term in the expression for gives

On the other hand, using that for any real numbers and ,

Now notice that and are both SPSD, and therefore

Thus, since and , we are done. ∎

Proposition B.2.

If, almost surely as ,

then the in Theorem 4.3 tends to zero almost surely as . In particular, almost surely if and have positive definite limits almost surely.

Proof.

Recall from Lemma 4.2 the definition of , , and . It suffices to show that almost surely since . We have

By Lemma A.2, . Thus,

Now using that and in another application of Lemma A.2,

which can be written as a product of terms, the th of which is

where is the th eigenvalue of . Since is fixed, the product of terms tends to is zero if and only if one of the terms does, which happens unless since is fixed. ∎