Cryptocurrency Egalitarianism:

A Quantitative Approach

Abstract

Since the invention of Bitcoin one decade ago, numerous cryptocurrencies have sprung into existence. Among these, proof-of-work is the most common mechanism for achieving consensus, whilst a number of coins have adopted “ASIC-resistance” as a desirable property, claiming to be more “egalitarian,” where egalitarianism refers to the power of each coin to participate in the creation of new coins. While proof-of-work consensus dominates the space, several new cryptocurrencies employ alternative consensus, such as proof-of-stake in which block minting opportunities are based on monetary ownership. A core criticism of proof-of-stake revolves around it being less egalitarian by making the rich richer, as opposed to proof-of-work in which everyone can contribute equally according to their computational power. In this paper, we give the first quantitative definition of a cryptocurrency’s egalitarianism. Based on our definition, we measure the egalitarianism of popular cryptocurrencies that (may or may not) employ ASIC-resistance, among them Bitcoin, Ethereum, Litecoin, and Monero. Our simulations show, as expected, that ASIC-resistance increases a cryptocurrency’s egalitarianism. We also measure the egalitarianism of a stake-based protocol, Ouroboros, and a hybrid proof-of-stake/proof-of-work cryptocurrency, Decred. We show that stake-based cryptocurrencies, under correctly selected parameters, can be perfectly egalitarian, perhaps contradicting folklore belief.

1 Introduction

In 2008, Satoshi Nakamoto proposed Bitcoin [25], the first and most successful cryptocurrency to date. Bitcoin introduced a cryptographic consensus protocol in which transactions are organized into blocks which are put in a globally agreed sequence, the blockchain, despite the presence of adversaries and without the need of any setup or identity system. Since its inception, a plethora of alternative cryptocurrencies, or “altcoins,” have sprung into existence, each claiming its own features.

A major thread of blockchain research has focused on the mechanics of consensus and specifically on the mechanism of identifying the party responsible for producing a new block at any point. Bitcoin, as well as the majority of altcoins, employs proof-of-work [12], where block generation is called mining and blocks are produced by miners who expend computational power to solve cryptographic puzzles. On the other hand, the most prominent alternative mechanism is proof-of-stake. In proof-of-stake, block generation is, some times, called minting and blocks are produced by minters who “stake” their coins, i.e., users who own a set of coins and use them to participate in the consensus protocol. Intuitively, in both cases a leader is drawn at regular intervals at random from the block generators’ population, with a probability of selection proportional to their computational power or stake respectively.

Block generators are incentivized to produce blocks by receiving a reward for each block they successfully produce and which is subsequently adopted in the resulting blockchain. In many cryptocurrencies, the rewards serve a dual purpose: incentivise the the miners/minters but also create and distribute the underlying cryptocurrency to the system’s maintainers. Taking this into account, in this paper, we consider the block generators as investors and focus on the comparison of the expected returns of investors with different purchasing power. The central economic property which arises is that of cryptocurrency egalitarianism. In an ideal world, investing a certain amount of capital to produce blocks should result in rewards proportional to that capital; that is, both a poor investor and a rich investor should receive returns in proportion to their investment in expectation. In this point of view, wealthy investors should not be rewarded with disproportionate rewards and everybody should have equal opportunity to both participate and earn rewards. As we will see, this is far from true with most cryptocurrencies today.

Until now, the term egalitarianism has been left undefined, although several cryptocurrencies claim to be more egalitarian than others [31] [24]. However, lacking a quantifiable metric, the question of whether some cryptocurrencies are more egalitarian than others remains ill posed. Our paper aims at putting forth the first concrete definition of egalitarianism, in a way which is generic and can be applied to any cryptocurrency. Our definition provides a metric, which can be practically measured and used to compare different cryptocurrencies. Using our model, we measure the egalitarianism of four indicative proof-of-work–based cryptocurrencies: Bitcoin, Litecoin [22], Ethereum [7, 32], and Monero [31]. Bitcoin, being the first and most successful cryptocurrency to date, was chosen as the baseline of comparison. Ethereum is the most promising altcoin and is currently the largest decentralized cryptocurrency by market cap after Bitcoin111All references to market cap in this paper are made according to https://coinmarketcap.com [January 2019].. Litecoin and Monero, although not next by market cap, make claims [31, 24] of increased egalitarianism because of their design. We assess their claims and find them in agreement with our data, thus presenting for the first time economic comparisons which quantify them precisely. On the pure proof-of-stake side, as will soon become clear, egalitarian behavior is similar across all coins independently of externalities such as hardware characteristics. Therefore, it suffices to perform a case study of an indicative proof-of-stake protocol. We study the case of pure proof-of-stake, applied on a protocol consistent with Ouroboros [20], as well as a hybrid proof-of-work/proof-of-stake cryptocurrency, Decred [10]. We find that pure proof-of-stake coins can be perfectly egalitarian, contrary to their proof-of-work counterparts. However, we note that variations of proof-of-stake, such as “delegated proof-of-stake,” may not be perfectly egalitarian, since the delegates, i.e., the leaders of the stake pools which are formed, typically earn extra profits for managing the stake pools [6]. Moreover, in both cases of proof-of-work and proof-of-stake we consider an open market that enables participants to invest in mining or minting without any barriers; introducing additional market constraints in acquiring mining equipment or stake can similarly disturb the egalitarianism of the underlying system.

Our Contributions and Roadmap. This work provides a quantitative evaluation of cryptocurrency egalitarianism. To the best of our knowledge this is the first work to provide a treatment of this property and acts as the foundation for comparing cryptocurrency fairness when it comes to reward distribution. Specifically, the contributions of our research are summarized as follows:

-

1.

We define an exact measure of cryptocurrency egalitarianism; to do this, we first define the egalitarian curve of a cryptocurrency from which we extract the measure.

-

2.

We measure and compare the egalitarian curve and egalitarianism of four indicative proof-of-work cryptocurrencies (Bitcoin, Ethereum, Litecoin, Monero), one representative proof-of-stake protocol (Ouroboros), and a hybrid cryptocurrency (Decred), using current market data.

-

3.

We show that proof-of-stake, when correctly parameterized, is, perhaps unexpectedly, perfectly egalitarian.

The rest of this paper is structured as follows. We begin by reviewing related work and preliminaries in Sections 2 and 3. Next, we put forth our definition for the egalitarian curve and egalitarianism of a cryptocurrency and motivate its intuition in Section 4. In Section 5 we present empirical data for several cryptocurrencies of interest and evaluate them under our model, in order to deduce whether previous intuitive claims are indeed correct. Finally, the conclusions of our research are drawn in Section 6.

2 Related work

The macro and microeconomics of blockchain design have been studied from several perspectives but remain an active area of research with a number of open questions. Incentives for block generation according to the honest protocol have been explored for both proof-of-work and proof-of-stake.

Proof-of-work protocols such as Bitcoin were formalized in the Bitcoin Backbone [15, 16] papers and follow-up works [26]. The seminal work of Selfish Mining [13], see also [29, 19] showed that honest behavior is not incentive-compatible. Alternative reward sharing mechanisms in the proof-of-stake setting make it feasible to behave better in terms of incentive compatibility for instance Ouroboros [20] can be designed from the ground up to be a Nash equilibrium under certain plausible conditions and similarly, in the proof-of-work setting [27]. The question of how to incentivize parties to conduct pool formation into the desired number of pools, or groups of minters, was studied in [6].

Egalitarianism has been studied before in proof-of-work systems from the perspective of memory-hard functions in [2, 4], under the premise that memory hardness provides egalitarianism in the sense that the it can be used to argue that the cost of one computational step will be roughly the same irrespective of the underlying computational platform (typically ASIC vs. generic, cf. [4]). The approach we take here instead, asking whether computational power grows proportionally to capital invested, i.e., whether larger wealth results in more than proportional rewards, is more general and it has not been previously studied to the best of our knowledge.

Equitability of cryptocurrencies. Fanti et al. analyze economic blockchain fairness in [14], where they define equitability. They study the evolution of a system after a series of rounds, putting forth the property that stake ownership remains in proportion before and after rewards have been awarded. By studying the behaviour of the returns’ variance under the randomness of executions, they introduce a geometric reward function and show its optimality in terms of equitability. Whereas their equitability metric jointly captures the normalized variance of rewards for every user conditioned on their initial resources (e.g., fraction of computational power for PoW), our egalitarianism metric instead captures the population-wide variation of best-case expected returns for an initial capital distribution among participants. In other words, our randomness is over the initial distribution of wealth, whereas theirs is over the evolution of a single blockchain execution. In our work, we show that computational power is not proportional to the invested capital, and hence the analogy between proof-of-work computational power and proof-of-stake capital breaks down, and a more detailed study is needed. Additionally, we remark that proof-of-work miners also reinvest their proceeds in the mining operation, albeit slowly, as proof-of-stake minters do. For example, empirical data show that large-scale miners pay for electricity using their proceeds [18]. Hence, both mining and minting follow Pólya processes as modelled by their paper. Regardless, egalitarianism and equitability are orthogonal. A cryptocurrency can be perfectly egalitarian and poorly equitable and vice versa. It is possible to obtain a cryptocurrency both egalitarian and equitable by adopting correctly parameterized proof-of-stake under a geometric reward function.

3 Preliminaries

Before studying the egalitarianism of different cryptocurrency consensus mechanisms, we provide a description of the leader election process, which is a central part of each blockchain consensus mechanism. We give an overview of the details of the two most common decentralized consensus mechanisms, proof-of-work and proof-of-stake, in order to establish an understanding of the differences in egalitarianism between the two models.

Proof-of-work. The core idea behind proof-of-work cryptocurrencies is solving the proof-of-work inequality. Specifically, the mining hardware is provided with two constants, previd and data, i.e., the id of the tip of the adopted blockchain and the data which need to be appended to it. The mining device then brute-force searches for some string nonce, such that for some hash function defined by the system. Here, is a —relatively— small number called the difficulty target, which is adjusted in order to ensure a stable block production rate, although typically remains constant for periods of consecutive blocks called epochs — for example, in Bitcoin, epochs are blocks long [5]. Because the search for solutions is exhaustive, the expected number of solutions found by a given miner is proportional to the number of evaluations of the hash function she can obtain in a given time frame.

The number of hash evaluations is one of the several critical parameters to consider when purchasing mining hardware. Other important parameters include the price of a mining unit, as well as its electricity consumption. Mining hardware is divided in various tiers based on performance, namely CPU miners, GPU miners, FPGA miners, and specialized ASIC miners [30]. Although the pricing of such devices may be similar, the hashing rate and, in turn, the return on investment, is highly dependent on the hardware’s tier. For example, the mining hardware “Whatsminer M10” produced by the company “MicroBT” costs per unit and produces per hour of operation in net gains, i.e., average mined Bitcoins per hour denominated in US dollars with today’s prices (December 2018) minus the electricity costs. On the other hand, the mining hardware “8 Nano Pro” produced by the company “ASICMiner” costs per unit, but produces per hour of operation in net gains, i.e., almost three times the hourly net gains of its cheaper competitor. Thus, if one can afford to purchase the more expensive hardware, each of their subsequent dollar invested in electricity returns more mined coins.

It has long been folklore knowledge in the blockchain community that mining becomes more egalitarian by using a memory-hard proof-of-work function. This intuition is correct, the core reason being the difficulty to construct specialized hardware for memory-hard functions. For example, no ASICs currently exist for Monero mining. Therefore, the only way to scale mining operations is by purchasing more general purpose hardware. However, since the mining hardware in this case varies little, both in terms of cost and performance, scaling returns become proportional to investments. To the best of our knowledge, our work is the first to confirm this correspondence between the memory-hardness of proof-of-work hash functions and the economics of mining.

Remark 1 (Block generation at scale).

We only analyze the scaling of the economics of mining with respect to hardware. We also do not take into account basic costs such as shipping and the availability of a basic machine to co-ordinate mining (such as a personal computer not performing mining itself). A multitude of additional factors play important roles for mining operations, such as space rental costs, machine cooling and maintenance costs, as well as bulk electricity purchase. As is common in economies of scale, these relative costs are reduced for large-scale operations, although they are similar for all proof-of-work cryptocurrencies and thus do not affect relative comparisons between them. We also remark that we analyze mining costs for small capital investments. If larger capital, e.g. above a few million US dollars, is available, corporations can develop their own specialized hardware and gain a competitive advantage by treating it as a trade secret [30]. Indeed, these details make our comparison in favour of proof-of-stake more pronounced, as proof-of-stake operations do not incur such types of costs and do not lend themselves to specialized mining hardware research. We leave the analysis and calculation of egalitarianism under these parameters for future work.

Proof-of-stake. In proof-of-stake, a minter is selected in proportion to the stake they hold, which is to say proportionally to the amount of money they own. There exist a number of flavors of this process. In one case, all coins automatically participate in the leader election process — this is the case for Ouroboros [20] and Ethereum’s Casper [8]. In a second flavour, the stake has to opt-in to participate in the election by a special process, such as purchasing a ticket or becoming a delegate of the stake of other users. This is the case for cryptocurrencies such as Decred [10] and EOS [21]. Among those participating in the election, a leader is elected at random, in proportion to their stake.

Proof-of-stake is often criticized for its lack of egalitarianism. The rationale is that, in proof-of-stake, the more money one stakes, the more money one generates. Thus, the rich get richer, which is precisely the opposite of egalitarianism. Additionally, in proof-of-stake systems, the money owners could constitute a closed, rich club, refusing to share the assets with any outsiders. In contrast, this argument claims, proof-of-work is naturally egalitarian: everyone is paid not according to the money they own, but according to the computational power they put to work. In this case, since computational power is a natural thing and cannot be exclusively owned, a closed rich club cannot be formed. Although this argument seems agreeable at first, the results of our work contradict it. In fact, correctly parameterized stake-based systems are much more egalitarian than work-based ones.

It is instructive to dispel the above argument intuitively, before we support our position with data. Firstly, the argument that money can be exclusively owned, but computational power cannot, is rather misguided. Indeed, this may be true in the case of a peculiar oligopoly, where a small faction of parties mutually agrees to never sell to outsiders, despite external demand. However, in an open market, both money and computational power can be freely purchased and, in fact, any non-negligible amount of computational power must be necessarily purchased that way. In the present work, we assume an open market for both mining hardware and financial capital which allows participation in the respective systems. Therefore, given that both money and computational power are purchasable, we now need to consider the funds one needs to invest either in technology or in financial capital in order to maximize the returns from a cryptocurrency’s block generation mechanisms. The amount of cryptocurrency generated by a given investment can be concretely measured and compared, thus the question can now be analyzed quantitatively and answered concretely.

We should note that variations of proof-of-stake, such as “delegated proof-of-stake,” may not be perfectly egalitarian, since the delegates, i.e., the leaders of the stake pools which are formed, typically earn extra profits for managing the stake pools [6]. In this paper, we only concern ourselves with non-delegated variants, i.e., pure proof-of-stake protocols. We leave the study of the contrast between pool formation mechanism truthfulness (or Sybil-resilience) and egalitarianism for future work.

4 Defining egalitarianism

Having established the basics of consensus mechanisms, we now propose the first definition of an economic measure of egalitarianism in cryptocurrencies. Before we present our definition, let us first state the desiderata of such a definition. First of all, we want to allow concrete measurements to be performed on cryptocurrencies and data to be extracted in a manner that is quantitative and not vague. Thus far, the claims for egalitarianism in various cryptocurrencies have been rather informal, using a rhetoric which fails to include exact data [31, 24]. As such, different cryptocurrencies claim egalitarianism over the others, without demonstrating the claims or provide conclusive arguments. Secondly, a definition of egalitarianism must measure the protocol maintenance returns of a “rich dollar” compared to that of a “poor dollar.” We thus desire a measure which, for a particular cryptocurrency, extracts a smaller value to indicate a lack of egalitarianism (e.g. a case where large wealth generates blocks disproportionately faster than small wealth) and a larger value to indicate perfect egalitarianism (where every invested dollar has exactly equal power in terms of cryptocurrency generation).

As a means towards establishing our egalitarianism definition, we define the egalitarian curve of a cryptocurrency. The horizontal axis of this curve plots the financial capital which is available for investment denominated in a fiat currency, USD.222Given that we explore a small investment duration, it makes little difference whether these are nominal USD or real USD, as long as they are the same when applying comparisons. The vertical axis plots the Return On Investment (ROI), which measures the cryptocurrency amount that is freshly generated in the investment period and remains unspent at the end of the investment period, given an optimal allocation of the initial capital. We require the Return On Investment is necessarily freshly generated cryptocurrency; thus, it must be newly mined or minted, and not part of the initial capital. Of course, purchasing cryptocurrency which has already been generated is an investment option, but it is immaterial to our egalitarianism definition, which focuses on measuring the egalitarianism of freshly generated cryptocurrency. Finally, the curve is plotted with a fixed investment duration in mind — in this paper, we use a duration of 1 year. Naturally, curves of different cryptocurrencies can be compared only if they use the same duration.

Definition 1 (Egalitarian curve).

Given a cryptocurrency , an investment period interval , the set of all possible investment strategies , we define the egalitarian curve of for investment period as:

The value identifies the maximum expectation of returns across all investment strategies , i.e., the amount of returns which the optimal strategy ensures for a given initial capital . The expectation is taken with the blockchain execution as a random variable, since returns vary by execution (the randomness of the execution can affect the returns of the strategy, as the same strategy can bring larger returns if the participant is “lucky” e.g., it happens to produce many blocks [14]).

We remark first that we do allow strategies to reinvest capital. For instance, returns earned from mining rewards can be reinvested in electricity costs for future mining. Furthermore, for unit consistency, we assume the strategy returns the freshly generated coins denominated in the same units as the capital was given in, such that represents a ROI; thus, we denominate the generated cryptocurrencies in USD using the market exchange rate. Second, we assume participants act independently and follow the protocol according to its specifications.

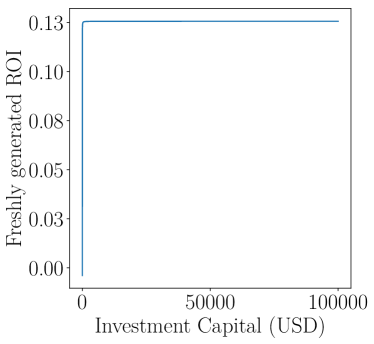

Based on the above, it is now straightforward to define the ideal egalitarian curve. In this case, the ROI is stable regardless of capital invested. Under these ideal conditions, the amount of freshly generated cryptocurrency is exactly proportional to the money invested. Thus, the ideal curve is any constant curve.

As an interesting thought experiment, consider the egalitarian curve which is decreasing. In this case, the poor would receive proportionally more newly created cryptocurrencies for every dollar they invest, i.e., it would be a redistribution of wealth from the rich to the poor. However, one can quickly see that, in decentralized cryptocurrencies where the identities of the participants are unknown, it is impossible to hope for something better than the constant curve. Indeed, the fact that decentralized cryptocurrencies allow anonymous generation of new identities [11] allows a rich investor to split their investment into smaller ones. Thus, if the curve were ever to have a negative slope, the sum of the smaller splits of the rich investment would achieve a higher gain. By the definition of the curve, which mandates that it depicts the ROI of an optimal investment, this would be a contradiction. The following lemma makes the above intuition more precise:

Lemma 1 (Sybil strategies).

Fix a cryptocurrency and an investment period interval . Given capital , for every natural number , it holds that .

The proof of this Lemma is available in Appendix 0.A.

Using our definition of the egalitarian curve, we now define egalitarianism as a concrete number. We begin by considering the initial capital as a random variable following a certain distribution . Egalitarianism is defined as the variance of the expected ROI when the capital is chosen from the given distribution.

Definition 2 (Egalitarianism).

Given a cryptocurrency , an investment period duration and an initial capital distribution , we define the egalitarianism of for investment duration under initial capital distribution as follows:

where is the egalitarian curve of .

The intuition behind this definition is that, to have egalitarianism, the ROI must remain the same across different capital investments. As such, any deviation from the mean is non-egalitarian. Naturally, if the egalitarianism of a certain cryptocurrency is higher than another’s, we say that the former is more egalitarian than the latter. Of course, to be accurate, such comparisons must only be made after fixing the parameters and as well as the initial capital distribution . We will now fix the distribution to be the uniform distribution between a minimum and a maximum capital. This choice corresponds to the intuition that the returns are the same for all initial capitals alike. Clearly a cryptocurrency with an ideal egalitarian curve is perfectly egalitarian, as we now define.

Definition 3 (Perfect egalitarianism).

A cryptocurrency is perfectly egalitarian for investment duration and initial capital distribution if .

5 Experimental results

Having established our theoretical framework, we now provide experimental results on the egalitarianism of various cryptocurrencies. Our experiments utilize the egalitarian curve definition of Section 4 in order to concretely confirm — or disprove — the egalitarianism claims of some of the major, both proof-of-work and proof-of-stake, cryptocurrencies.

In conducting our experiments we assume a static environment. Specifically, we assume that the token prices, as well as the distribution of funds which are available for purchasing mining hardware are static and follow the snapshot of the world which we took at the time of writing. Furthermore, we assume that our mining operation would not substantially affect these parameters if it were to be applied on this environment. Finally, we assume that the set of available strategies comprises of the honest strategies, e.g. not including selfish mining which could provide better ROI by diverging from the protocol.

Proof-of-work. We have experimentally analyzed the egalitarianism of the following proof-of-work coins: Bitcoin, Litecoin, Ethereum, and Monero. These cryptocurrencies act as a representative sample among the thousands of existing cryptocurrencies. Bitcoin is the largest and most successful cryptocurrency by market cap. Litecoin is the first cryptocurrency aimed at becoming more egalitarian by replacing Bitcoin’s SHA256 work function with scrypt [28], a memory-hard function [3]. Ethereum is one of the most promising alternative cryptocurrencies, the first to support smart contracts, and the second largest by market cap; its proof-of-work function is different from both Bitcoin and Litecoin. Finally, Monero is special with claims of strong egalitarianism due to its memory-hard mining function, Cryptonight [31]. Furthermore, its protocol is often updated to maintain egalitarianism [9].

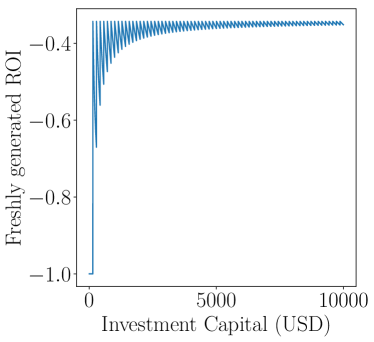

As expected, our experiments show that Bitcoin is the least egalitarian of the four, with Ethereum following next. Monero is more egalitarian than both, with Litecoin being the most egalitarian among the proof-of-work coins we have studied.

For our experimental setting, we worked as follows. First, we collected empirical data which describe the available mining hardware options in the market. For each machine choice, we determined the cost of investment. This is comprised of its initial price (in USD) as well as its energy cost of operation (in Watts). The cost of operation was translated to USD per hour by considering the electricity cost of KWh. As a reference, we used the lowest average KWh cost in the United States, i.e., per KWh [1]. This reference electricity cost is an estimation which can vary depending on the country of operation.

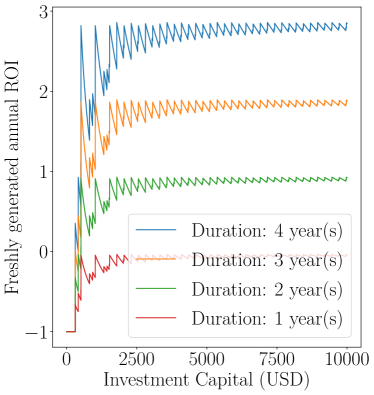

Second, we use the reported hash rate of each mining hardware machine to extract an expectation of the freshly mined coins it would generate per hour, if it were to run continuously. This expectation is taken over the randomness of all honest blockchain protocol executions. As such, each party is awarded block rewards in proportion to their computational power. The difference between revenue per unit of time and cost of operation per unit of time produces an income rate, which is measured in USD per hour. For our experiments, we use an interval of investment with year. Although this choice is arbitrary, it corresponds to the usual definition of ROI in traditional finance.

Our investment strategy is as follows. The initial available capital is allocated to an upfront technology investment, in which an integer instance of the Unbounded Knapsack problem [23] is solved using dynamic programming333The source code of our implementation for this calculation is available in our repository. to optimize the total cash flow. Subsequently, as long as the cash flow is positive, the purchased machines operate for the indicated total duration, reinvesting part of the freshly minted coins in electricity costs, in order to generate more coins. Eventually, this strategy produces an income of freshly generated coins, which have not been spent and are reported as the strategy’s income.

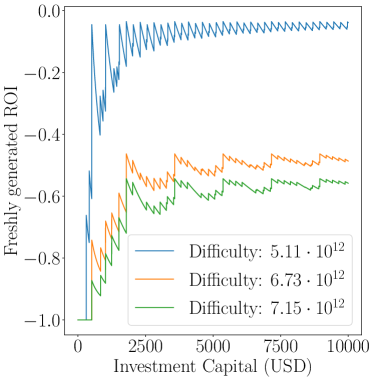

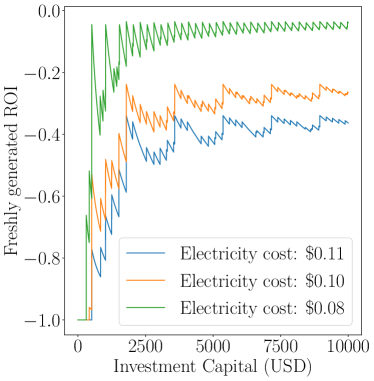

To calculate our concrete numbers, we employ the constants shown in Table 1. We use the expected block generation rates for each cryptocurrency, as well as the reward per block, token price, and mining difficulty at the time of writing, all of which we assume remain constant. The variance of electricity cost, the duration of investment, as well as small fluctuations in price and difficulty do not qualitatively change the shape of our egalitarian curves (see Appendix 0.C).

| Variable | Description | Unit | BTC | ETH | LTC | XMR | DCR |

| duration of investment | years | ||||||

| ec | electricity cost | USD / kWh | |||||

| block generation rate | blocks / s | 1 / 600 | 1 / 14.7 | 1 / 150 | 1 / 120 | 1 / 298 | |

| total hash rate | Thash / s | 34,727,437 | 179.50374 | 174.537 | 0.00033859 | 178,760 | |

| reward per block | tokens | 12.5 | 3 | 25 | 3.37 | 11.38 | |

| token price | token / USD | 4,074.25 | 126.12 | 32.10 | 47.27 | 18.62 | |

inline, caption=minipage-note, bordercolor=bordergreen, linecolor=bordergreen, color=lightgreen, fancyline ] Dionysis: confirm that changing the total hash rate maintains curve shapes and argue about it in the main text

Let denote the set of all available mining machines. For each machine , our empirically collected data specifies the following parameters: i) the energy consumption rate in Watts, ii) an initial cost of purchase in USD, and iii) a hash rate in Terahashes per second. Given the above, we can now calculate the expected income rate per hour for a given machine and a cryptocurrency . In the following equation, the first part identifies the income per hour, i.e., the amount of tokens (denominated in USD) which the machine produces per hour, whereas the second part of the equation identifies the electricity cost, i.e., the product of the consumed electricity multiplied by the price of a single KWh:

There are many possible configurations for technology investments. Each configuration comprises of a number of copies of every machine type . Therefore, we define each configuration as , with total initial cost of investment for such configuration being .

The above figure is given in USD per hour and, since the initial capital should suffice to buy the machines of the configuration, we require that , where is the initial available capital at the beginning of the simulation.

Now, in order to identify the strategy’s optimal net income for the interval , we iterate over all possible machine configurations, for which the above inequality holds, and choose the one with the maximum returns:

We note that this is only an approximation to the optimal (in our limited model) solution, which we used in our simulations. We consider this sufficiently close to optimal to allow for the calculation of egalitarianism. We give an integer programming formulation of the optimal strategy for capital allocation in Appendix 0.B. We remark here that the general problem of mining hardware allocation (including our simplified approximation) is computationally hard [17], as both the Knapsack and the Integer Programming problems are NP-complete.

As the simulation parameters are many and diverse, in order to allow others to run the experiments with different values, as well as for reasons of reproducibility and falsifiability, we openly release our mining investment optimizer as well as our data for public use444Our mining investment calculator and our mining hardware data are available under the MIT license and a Creative Commons 4.0 Attribution License respectively at https://github.com/decrypto-org/egalitarianism. .

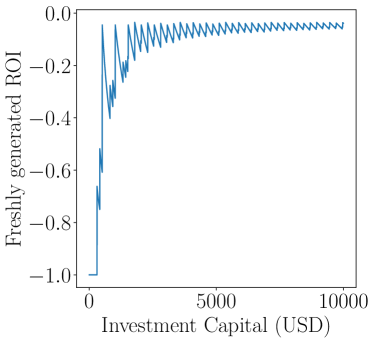

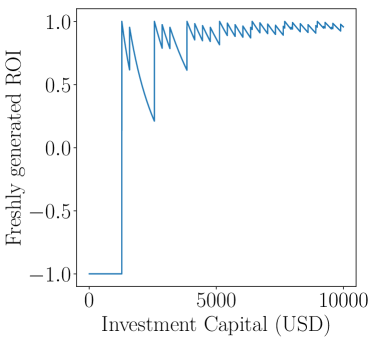

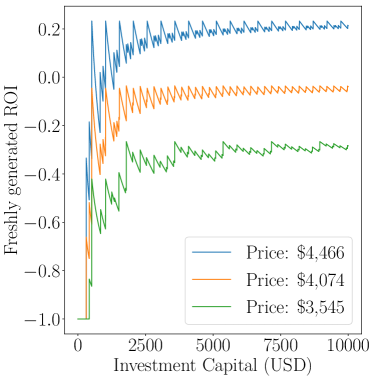

The egalitarianism of Bitcoin, Ethereum, Litecoin and Monero are shown in Figures 1(a), 1(b), 1(c), and 1(d) respectively. Decred is a hybrid proof-of-work/proof-of-stake cryptocurrency, in which block generation is a collaboration between miners and minters. Specifically, each block which is mined via proof-of-work needs to be “vouched for” by a certain number of minters, who give it a vote of confidence. Both the miners and the minters who participate in block generation are rewarded. An investor can therefore choose to participate in Decred by either investing in mining hardware and performing proof-of-work, or by purchasing stake and performing proof-of-stake (or a combination thereof). We note that the choice of whether to mine or mint Decred is not always clear. While mining may be more profitable for a certain initial capital, it can also carry various risks. For instance, if the difficulty increases, the mining hardware may be rendered inefficient and also hard to sell. Proof-of-work also carries the operational overhead discussed in Remark 1. On the other hand, stake can always be sold, although the price may fluctuate, and carries negligible operational overhead. As the decision between the two is not obvious, we analyze both strategies independently. The egalitarianism of proof-of-work mining for Decred is shown in Figure 1(d).

It is evident from all figures that the ROI is “capped” by a maximum value, which is observed in specified intervals. Indeed, this value identifies the ROI of the best available machine and is in line with Lemma 1. In other words, as long as an investor is able to buy the machine which returns the most profits, then they achieve the best possible ROI. In case an investor does not have enough capital to buy the best mining product, they may buy a less profitable machine and achieve less, though still positive, ROI. This observation explains the small spikes in ROI which may be seen e.g. in Bitcoin’s figure for capital in the range . Also, in case the capital is more than the cost of the machine, then the remaining capital is effectively discarded. Therefore, although two investors may start with initial capital , if their returns, in absolute terms, are the same, then the ROI of will be smaller as a percentage compared to the ROI of . This observation explains the decrease in ROI after the spikes. Finally, we observe that, as the capital increases, the ROI converges to the cap. This is explained by the fact that the “discarded” capital, i.e., the capital which cannot be invested in mining hardware, is a significantly smaller percentage of the total capital for large investments.

Proof-of-stake. We now analyze the proof-of-stake egalitarianism in two settings. First, we consider pure proof-of-stake, which can be applied on top of a protocol like Ouroboros. In this case, pure is in opposition to delegated proof-of-stake, a setting where the stakeholders are required to delegate their stake to other parties, namely “stake pools” and is deployed in cryptocurrencies such as EOS, Bitshares, and others. Second, we consider the case of minting Decred via its proof-of-stake mechanism.

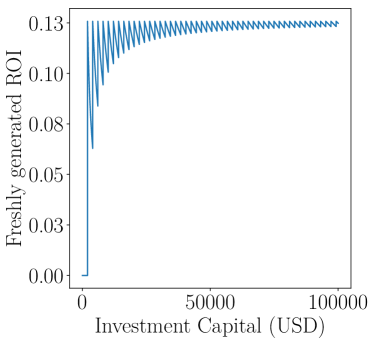

The egalitarian curve for staking Decred is illustrated in Figure 2(a). As mentioned above, Decred is an opt-in staking cryptocurrency, where staking occurs by purchasing so-called tickets. Since the price of a ticket is quantized, egalitarianism is harmed for capitals which are not multiples of ticket prices. However, one can see that the envelope of maxima of this curve is perfectly egalitarian. The spikes that cause the discontinuity of the curve are due to the large ticket price (currently ), which in Decred is determined by the market and is high due to the limited supply of tickets available per ticket pool, a parameter inherent in their protocol. Perfect egalitarianism could in principle be achieved by making the ticket price approach .

In the case of Ouroboros, every coin has the same probability of being chosen for extending the chain [20]. When a coin is eligible for block generation, its owner can create a block by providing a proof of ownership of the chosen coin. Consider the case of a cryptocurrency with coins in circulation. When a block needs to be created, a coin is chosen at random from the set of coins. Therefore, each coin may be chosen with probability. Then the address which owns the chosen coin, in other words the stakeholder which controls this coin, is eligible to generate a block and receive the block rewards associated with it.555In [20] the payout does not explicitly include freshly minted coins and is comprised of transaction fees. We consider an identical reward schedule as [20] but comprised only of freshly minted coins. In our experiments, we assume that every block is associated with a constant reward, which pertains to newly minted coins. Furthermore, since computational power does not affect the rate of block production, it is reasonable to assume that both the electricity and the hardware equipment’s price is constant for all users, regardless of stake accumulation, so all users can participate using — relatively — cheap resources (cf. Remark 1).

Figure 2(b) depicts the simulation of a pure proof-of-stake system. In this case, the users pay a set transaction fee666As of January , according to https://cardanoexplorer.com/, in the Cardano implementation of Ouroboros these fees are in the order of . for the purchase of the initial stake. The rest of their capital is allocated as stake. The figure suggests that this system is closer to perfect egalitarianism compared to the rest of our case studies.

Summary. Our findings are summarized in Table 2. We find that Bitcoin is the least egalitarian, followed in turn by Ethereum, Monero, and Litecoin777Litecoin may appear to have better egalitarianism compared to Monero due to limited availability of mining machines. More data are needed to economically compare scrypt and CryptoNight mining.. The latter two are the most egalitarian due to their use of CryptoNight and scrypt respectively. Mining with Decred provides the worst egalitarianism of all tested coins. However, the most egalitarian coins involve staking. Decred staking, due to its quantized ticket pricing, is only approximately egalitarian and comparable to the performance of mining Litecoin. Pure proof-of-stake, which allows continuous staking, is almost perfectly egalitarian, its small divergence from perfect egalitarianism stemming from the small capital which is required to pay the transation fees to participate in the staking process.

| Name | Consensus mechanism | Egalitarianism | ||||

| Bitcoin | Proof-of-work | -0.034490298 | ||||

| Ethereum | Proof-of-work | -0.006926114 | ||||

| Litecoin | Proof-of-work | -0.000271822 | ||||

| Monero | Proof-of-work | -0.002206135 | ||||

| Decred |

|

|

||||

| Ouroboros | Proof-of-stake | -0.000000295 |

6 Conclusion

In this work we explore the notion of egalitarianism of cryptocurrencies. Although this notion has long been discussed, we are the first to give a definition, which allows us to concretely argue about the egalitarianism of various existing systems.

The results of our experimental simulations are very optimistic in terms of usability of our metric, as they provide concrete figures which measure the egalitarianism of several popular cryptocurrencies. The most unexpected result arises from the comparison between the proof-of-work and proof-of-stake mechanisms. Although blockchain folklore argued in favour of proof-of-work systems in terms of egalitarianism, our results show that, in fact, it is proof-of-stake systems which are more egalitarian in our model.

Our work provides the first step towards establishing a concrete framework of egalitarianism evaluation in the cryptocurrency ecosystem. Future work will focus in evaluating more existing cryptocurrencies and investigating variations of consensus mechanisms such as delegated proof-of-stake. Additionally, we leave for future work the treatment of more complex economical models of the mining game such as dynamic systems and adversarial strategies, as well as economies of scale in the multitude of parameters we have ignored, such as electricity bulk pricing. We conjecture the consideration of such parameters will exacerbate the gap between proof-of-work and proof-of-stake which we have illustrated in this work.

Finally, we remark that neither proof-of-work nor proof-of-stake blockchains are politically egalitarian systems, in which the ideal of one human one vote is attained. Instead, at best, one coin one vote is attained in the case of well-parameterized proof-of-stake systems. Thus, as illustrated in this paper, blockchain systems are, for the time being, plutocratic. Whether decentralized decision making in which each human is allocated one vote is possible remains an open question. In such a system, the egalitarian curve would be strictly decreasing; however, our results, especially Lemma 1, hint towards our conjecture that such systems are impossible in a Sybil-resilient setting.

References

- [1] U.S. Energy Information Administration. Electric power monthly with data for november 2018. Technical report, Jan 2019.

- [2] Joël Alwen, Jeremiah Blocki, and Krzysztof Pietrzak. Depth-robust graphs and their cumulative memory complexity. In Annual International Conference on the Theory and Applications of Cryptographic Techniques, pages 3–32. Springer, 2017.

- [3] Joël Alwen, Binyi Chen, Krzysztof Pietrzak, Leonid Reyzin, and Stefano Tessaro. Scrypt is maximally memory-hard. In Jean-Sébastien Coron and Jesper Buus Nielsen, editors, Advances in Cryptology - EUROCRYPT 2017 - 36th Annual International Conference on the Theory and Applications of Cryptographic Techniques, Paris, France, April 30 - May 4, 2017, Proceedings, Part III, volume 10212 of Lecture Notes in Computer Science, pages 33–62, 2017.

- [4] Alex Biryukov and Dmitry Khovratovich. Egalitarian computing. In USENIX Security Symposium, pages 315–326, 2016.

- [5] Joseph Bonneau, Andrew Miller, Jeremy Clark, Arvind Narayanan, Joshua A. Kroll, and Edward W. Felten. SoK: Research perspectives and challenges for bitcoin and cryptocurrencies. In 2015 IEEE Symposium on Security and Privacy, pages 104–121. IEEE Computer Society Press, May 2015.

- [6] Lars Brünjes, Aggelos Kiayias, Elias Koutsoupias, and Aikaterini-Panagiota Stouka. Reward sharing schemes for stake pools. Computer Science and Game Theory (cs.GT) arXiv:1807.11218, 2018.

- [7] Vitalik Buterin et al. A next-generation smart contract and decentralized application platform. white paper, 2014.

- [8] Vitalik Buterin and Virgil Griffith. Casper the friendly finality gadget. arXiv preprint arXiv:1710.09437, 2017.

- [9] dEBRYUNE and dnaleor. Pow change and key reuse. Available at: https://www.getmonero.org/2018/02/11/PoW-change-and-key-reuse.html, Feb 2018.

- [10] The Decred Developers. Decred documentation. Available at: https://docs.decred.org/, 2016.

- [11] John R Douceur. The sybil attack. In International workshop on peer-to-peer systems, pages 251–260. Springer, 2002.

- [12] Cynthia Dwork and Moni Naor. Pricing via processing or combatting junk mail. In Ernest F. Brickell, editor, CRYPTO’92, volume 740 of LNCS, pages 139–147. Springer, Heidelberg, August 1993.

- [13] Ittay Eyal and Emin Gün Sirer. Majority is not enough: Bitcoin mining is vulnerable. In Nicolas Christin and Reihaneh Safavi-Naini, editors, FC 2014, volume 8437 of LNCS, pages 436–454. Springer, Heidelberg, March 2014.

- [14] Giulia Fanti, Leonid Kogan, Sewoong Oh, Kathleen Ruan, Pramod Viswanath, and Gerui Wang. Compounding of wealth in proof-of-stake cryptocurrencies. In International Conference on Financial Cryptography and Data Security. Springer, 2019.

- [15] Juan A. Garay, Aggelos Kiayias, and Nikos Leonardos. The bitcoin backbone protocol: Analysis and applications. In Elisabeth Oswald and Marc Fischlin, editors, EUROCRYPT 2015, Part II, volume 9057 of LNCS, pages 281–310. Springer, Heidelberg, April 2015.

- [16] Juan A. Garay, Aggelos Kiayias, and Nikos Leonardos. The bitcoin backbone protocol with chains of variable difficulty. In Jonathan Katz and Hovav Shacham, editors, CRYPTO 2017, Part I, volume 10401 of LNCS, pages 291–323. Springer, Heidelberg, August 2017.

- [17] Richard M Karp. Reducibility among combinatorial problems. In Complexity of computer computations, pages 85–103. Springer, 1972.

- [18] Olga Kharif. Many bitcoin miners are at risk of turning unprofitable. Bloomberg, Apr 2018.

- [19] Aggelos Kiayias, Elias Koutsoupias, Maria Kyropoulou, and Yiannis Tselekounis. Blockchain mining games. In Proceedings of the 2016 ACM Conference on Economics and Computation, pages 365–382. ACM, 2016.

- [20] Aggelos Kiayias, Alexander Russell, Bernardo David, and Roman Oliynykov. Ouroboros: A provably secure proof-of-stake blockchain protocol. In Jonathan Katz and Hovav Shacham, editors, CRYPTO 2017, Part I, volume 10401 of LNCS, pages 357–388. Springer, Heidelberg, August 2017.

- [21] Daniel Larimer and the EOS developers. Eos.io technical white paper v2. Available at: https://github.com/EOSIO/Documentation/commits/master/TechnicalWhitePaper.md, 2017.

- [22] Charles Lee. Litecoin, 2011.

- [23] George B Mathews. On the partition of numbers. Proceedings of the London Mathematical Society, 1(1):486–490, 1896.

- [24] Robert McMillan. Ex-googler gives the world a better bitcoin. WIRED, Aug 2013.

- [25] Satoshi Nakamoto. Bitcoin: A peer-to-peer electronic cash system. Available at: https://bitcoin.org/bitcoin.pdf, 2008.

- [26] Rafael Pass, Lior Seeman, and Abhi Shelat. Analysis of the blockchain protocol in asynchronous networks. In Annual International Conference on the Theory and Applications of Cryptographic Techniques, pages 643–673. Springer, 2017.

- [27] Rafael Pass and Elaine Shi. FruitChains: A fair blockchain. In Elad Michael Schiller and Alexander A. Schwarzmann, editors, 36th ACM PODC, pages 315–324. ACM, July 2017.

- [28] Colin Percival and Simon Josefsson. The scrypt password-based key derivation function. Technical report, 2016.

- [29] Ayelet Sapirshtein, Yonatan Sompolinsky, and Aviv Zohar. Optimal selfish mining strategies in bitcoin. In Jens Grossklags and Bart Preneel, editors, FC 2016, volume 9603 of LNCS, pages 515–532. Springer, Heidelberg, February 2016.

- [30] Michael Bedford Taylor. Bitcoin and the age of bespoke silicon. In Proceedings of the 2013 International Conference on Compilers, Architectures and Synthesis for Embedded Systems, page 16. IEEE Press, 2013.

- [31] Nicolas Van Saberhagen. Cryptonote v2.0. Available at: https://cryptonote.org/whitepaper.pdf, 2013.

- [32] Gavin Wood. Ethereum: A secure decentralised generalised transaction ledger. Ethereum project yellow paper, 151:1–32, 2014.

Appendix 0.A Proofs

See 1

Proof.

We prove the statement via contradiction. Assume that for capital exists a natural number such that . Also assume that for capital the optimal strategy is , so: . Then, for capital exists a strategy , such that the capital is split into equally-sized parts and the strategy is applied on each part. Given that the executions of the substrategies on these parts are independent, then the expected returns for the strategy are:

| (1) |

It also holds that is at best the optimal strategy, so:

| (2) |

However, it should hold that:

| (3) |

which is impossible. ∎

Appendix 0.B Integer programming formulation

In our experiments, we used a Dynamic Programming solution to solve the Knapsack problem in order to allocate mining machines upfront. An optimal solution could use the proceeds of mining not only to reinvest in electricity, but also to purchase new machines. This is captured by the Integer Programming formulation in Figure 3, which gives the optimal investment strategy in the full model.

This maximization problem tries to optimize the freshly generated proceeds. The variables to solve for, , describe the number of machines of type that the investor holds at time . We assume machines cannot be sold back to the market, hence . The investment starts with initial capital and no machines, hence . The program can then decide to purchase machines as time goes by. For any costs, it first uses up the initial capital to pay for them (this initial capital is useless to keep, as it does not contribute to freshly generated proceeds, which are our utility here), and subsequently uses the proceeds to pay for any remaining costs. Capital which is not expended to pay for costs is discarded by the operator in the maximization clause. The condition the integer program is subject to requires that the investment has non-negative capital at every point in time, and hence does not run out of money. In this formulation, it is assumed that is a set of consecutive integers representing indexed hours of execution (a more fine-grained solution can be obtained by increasing this temporal resolution as needed).

Maximize subject to

Appendix 0.C Parameters affecting egalitarianism

Throughout this paper, we have assumed certain parameters (cryptocurrency prices, electricity prices, duration of investment and mining difficulty) remain constant throughout the investment period. Furthermore, we have taken into account current market values to the best of our knowledge. We note that, while the actual egalitarianism numbers may change depending on these parameters, the general shape of egalitarian curves and the qualitative comparison between different cryptocurrencies remains the same. To illustrate this point, we have measured the egalitarian curve of Bitcoin for varying parameter values. Our results are demonstrated in Figure 4.

Appendix 0.D Machines

Data for mining machines was obtained from a multitude of resources on the Internet888An exhaustive list of our resources includes the online stores https://whattomine.com/, https://cryptominer.deals/, https://www.asicminervalue.com/, https://www.reddit.com/r/MoneroMining/comments/9omjfb/rtx_2080_ti_mining_monero_at_1228hs_and_more/, https://www.newegg.com/, https://www.amazon.com/, https://shop.bitmain.com.cn, https://www.cryptouniverse.at, https://canaan.io, http://miner.ebang.com.cn, https://swminershop.com, https://asicminer.co, https://estrahash.com, http://www.innosilicon.com, https://pangolinminer.com, https://www.bitfily.io, https://hashdeploy.net/, https://www.pantech.company, https://www.cryptominerbros.com, https://pandaminer.com, https://minersdeals.com, https://sharkmining.com, https://shop.miningstore.com, https://mineshop.eu, https://www.bitmart.co.za, https://shop.futurebit.io, https://www.aliexpress.com, https://bitech-mining.com, https://asicminermarket.com, https://www.baikalminer.com, https://prominerz.com. Data for graphics processing units (GPU) and central processing units (CPU) was obtained by calculating the median of multiple user benchmarks when available999https://www.xmrstak.com/tag/monero/, https://gpustats.com/, https://www.ethmonitoring.com/benchmark, https://monerobenchmarks.info/. The price of each machine used in our experiments is the reported retails price of machine at date of access. When a new machine is not available for sale, the price of a used or refurbished machine is used. For reproducibility purposes, our complete data set is openly available in our repository. For reference, we list a summary of those machines which provide a positive net gain per hour after purchase (and can thus be profitable under our assumed parameter values) in Table LABEL:tbl:machines.

| Bitcoin | |||

| Name | Hashes / s | Watt | Price (USD) |

| 8 Nano Pro | 4,000 | 6,000 | |

| Whatsminer M10S | 3,500 | 2,558 | |

| Ebit E11++ | 1,980 | 2,024 | |

| 8 Nano | 2,100 | 1,790 | |

| T3 43T | 2,100 | 2,279 | |

| Ebit E11+ 37 | 2,035 | 1,517 | |

| WX6 | 3,200 | 1,275 | |

| Whatsminer M10 | 2,145 | 1,022 | |

| T2T-32T | 2,200 | 1,568 | |

| Ebit E11 | 1,950 | 1,110 | |

| Antminer S15 (28T) | 1,596 | 1,249 | |

| Antminer S15 (27T) | 1,539 | 1,363 | |

| T2T-25T | 2,050 | 1,150 | |

| Snow Panther B1+ | 2,100 | 580 | |

| T2T-24T | 1,980 | 1,350 | |

| S11i | 2,300 | 937 | |

| Antminer T15 | 1,541 | 840 | |

| Antminer S11 | 1,435 | 512 | |

| AvalonMiner 921 | 1,800 | 415 | |

| Antminer S9-Hydro | 1,728 | 713 | |

| Ebit E10 | 1,650 | 2,999 | |

| T2 Terminator | 1,570 | 1,118 | |

| DragonMint T1 | 1,480 | 1,600 | |

| AvalonMiner 851 | 1,450 | 380 | |

| Antminer S9i | 1,365 | 440 | |

| Antminer S9j | 1,365 | 307 | |

| AvalonMiner 841 | 1,290 | 354.44 | |

| SX6i | 900 | 419 | |

| Ethereum | |||

| Name | Hashes / s | Watt | Price (USD) |

| A10 EthMaster | 850 | 5,399 | |

| A10 EthMaster | 740 | 4,799 | |

| Shark Extreme 2 (8NVIDIA GTX 1080 Ti) | 1,500 | 9,779 | |

| Maximus+ (81080TI) | 2,200 | 7,520 | |

| A10 EthMaster | 650 | 4,099 | |

| Ethereum Mining Rig (12x AMD RX 570 GPU) | 1,600 | 4,345 | |

| ULTRON (8P104) | 1,700 | 5,338 | |

| Ethereum Mining Rig (8 NVIDIA 1080 8GB GPU) | 1,100 | 6,267 | |

| Shark Extreme 2 (6NVIDIA GTX 1080 Ti) | 1,200 | 7,880 | |

| Shark Extreme 2 (8AMD Vega 56) | 1,700 | 6,879 | |

| Shark Extreme 2 (8NVIDIA GTX 1070 Ti 8 GB) | 1,400 | 6,679 | |

| Shark Extreme 2 (8AMD RX 580) | 1,100 | 4,590 | |

| Ethereum Mining Rig (8AMD MSI RX 580 GPU) | 1,000 | 3,453 | |

| IMPERIUM+ (8RX 570/580) | 1,300 | 3,577 | |

| Antminer G2 | 1,200 | 3,799 | |

| Shark Extreme 2 (6AMD Vega 56) | 1,275 | 5,680 | |

| Ethereum Mining Rig (8AMD MSI RX 570 GPU) | 950 | 3,2253 | |

| Shark Extreme 2 (4NVIDIA GTX 1080 Ti) | 800 | 4,979 | |

| Antminer E3 | 760 | 654 | |

| Shark Extreme 2 (6NVIDIA GTX 1070 Ti 8 GB) | 1,050 | 5,480 | |

| Shark Extreme 2 (6AMD RX 580) | 825 | 3,890 | |

| Ethereum Mining Rig (6AMD RX580 8gb GPU) | 900 | 2,342 | |

| Ethereum Mining Rig (6AMD MSI RX 580 GPU) | 860 | 1,967 | |

| Ethereum Mining Rig (6AMD MSI RX 580 GPU) | 750 | 2,156 | |

| Thorium 6580 GPU | 700 | 4,297 | |

| Thorium 6570 GPU | 750 | 3,974 | |

| Shark Extreme 2 (4NVIDIA GTX 1070 Ti 8 GB) | 600 | 3,580 | |

| Zodiac 6-1060 GPU | 750 | 3,222 | |

| Shark Extreme 2 (4AMD RX 580) | 550 | 2,590 | |

| Ethereum Mining Rig (6AMD MSI RX 560) | 370 | 1,823 | |

| GeForce RTX 2080Ti | 155 | 1,249 | |

| GeForce GTX 1080Ti | 175 | 999 | |

| RX Vega 64 | 230 | 399 | |

| GeForce RTX 2080 | 105 | 699 | |

| GeForce GTX TITAN X | 250 | 1,099 | |

| P104-100 | 127 | 569 | |

| RX Vega 56 | 210 | 339 | |

| GeForce RTX 2070 | 140 | 499 | |

| GeForce GTX 1080 | 121 | 633 | |

| RX 580 | 110 | 185 | |

| GeForce GTX 1070 | 108 | 319 | |

| GeForce GTX 1070Ti | 107 | 489 | |

| RX 570 | 65 | 142 | |

| RX 480 | 70 | 237 | |

| RX 470 | 60 | 340 | |

| GeForce GTX 1060 (6GB) | 95 | 264 | |

| GeForce GTX 1060 (3GB) | 69 | 189 | |

| GeForce GTX 1050Ti | 75 | 169 | |

| Litecoin | |||

| Name | Hashes / s | Watt | Price (USD) |

| A6 LTCMaster | 1,500 | 3,000 | |

| A4+ LTCMaster | 750 | 1,500 | |

| Apollo LTC Pod | 100 | 299 | |

| Monero | |||

| Name | Hashes / s | Watt | Price (USD) |

| Shark Extreme 2 (8AMD Vega 56) | 14,800 | 1,700 | 6,879 |

| Shark Extreme 2 (6AMD Vega 56) | 11,000 | 1,275 | 5,680 |

| Shark Extreme 2 (8AMD RX 580) | 6,880 | 1,100 | 4,590 |

| Shark Extreme 2 (6AMD RX 580) | 5,160 | 825 | 3,890 |

| Shark Extreme 2 (4AMD RX 580) | 3,440 | 550 | 2,590 |

| RX Vega 64 | 2,020 | 140 | 399 |

| RX Vega 56 | 1,920 | 140 | 339 |

| GeForce RTX 2080Ti | 1,200 | 150 | 1,249 |

| RX 580 | 976 | 89 | 185 |

| RX 480 | 965 | 140 | 237 |

| Ryzen Threadripper 1920X | 955 | 140 | 435 |

| GeForce RTX 2080 | 898 | 132 | 699 |

| GeForce GTX 2070 | 880 | 140 | 499 |

| RX 470 | 840 | 120 | 340 |

| GeForce GTX 1070 | 777 | 112 | 319 |

| RX 570 | 740 | 90 | 142 |

| Ryzen 7 2700X | 715 | 105 | 309 |

| Ryzen 5 1600X | 532 | 47 | 179 |

| Ryzen 5 1600 | 531 | 65 | 159 |

| Decred | |||

| Name | Hashes / s | Watt | Price (USD) |

| Whatsminer D1 | 2,200 | 1,588 | |

| Whatsminer DCR | 2,200 | 1,890 | |

| Antminer DR5 | 1,610 | 1,282 | |

| STU-U1+ | 1,850 | 1,560 | |

| STU-U1 | 1,600 | 1,389 | |