∗ Institute of Stochastics, Karlsruhe Institute of Technology (KIT), D-76128 Karlsruhe, Germany † Institute of Optimization and Operations Research, University of Ulm, D-89069 Ulm, Germany

Markov Decision Processes under Ambiguity

Abstract.

We consider statistical Markov Decision Processes where the decision maker is risk averse against model ambiguity. The latter is given by an unknown parameter which influences the transition law and the cost functions. Risk aversion is either measured by the entropic risk measure or by the Average Value at Risk. We show how to solve these kind of problems using a general minimax theorem. Under some continuity and compactness assumptions we prove the existence of an optimal (deterministic) policy and discuss its computation. We illustrate our results using an example from statistical decision theory.

otsep5

- Key words :

-

Model Ambiguity; Bayesian MDP; Entropic Risk Measure; Average Value at Risk; Dual Representation; Minimax Theorem

1. Introduction

The following experiment has (in a variant) been suggested by Ellsberg (1961) (see e.g. [9]): An agent has to choose between two bets. For this she is shown two urns, each containing 100 balls which are either red or black. Urn A contains 50 red and 50 black balls while there is no further information about urn B. Bet 1 is: ’the ball drawn from urn A is black’ and bet 2 is: ’the ball drawn from urn B is black’. In case of winning the bet, the agent receives 100 euros. Empirically it has been observed that most agents prefer bet 1. One explanation for this behavior is that in case of urn B agents consider a set of possible distributions for the colours of the balls and being ambiguity averse take into account the minimal expected utility.

This point of view has become popular in economics and has been formalized later on. In particular one has to specify the possible set of distributions which have to be taken into account. For example [11] consider in the framework of a continuous-time consumption problem the set of distributions whose relative entropy with respect to a fixed distribution is less or equal to a constant. Using a Lagrange approach this is equivalent to penalizing the robust problem with the distance of the distribution to Optimization criteria like this have been put on an axiomatic basis by [15].

As far as Markov Decision Processes (MDPs) are concerned, robust approaches have been considered in [13] among others. As in [11] model ambiguity is here treated with respect to the whole probability measure of the process. Since the probability measure in MDP theory is a product of transition kernels such robust optimization problems can also be interpreted as games against nature.

In this paper we will take another point of view which is related to the models introduced in [14]. There, the whole risk is separated into two parts: Model ambiguity and operating risk. One has to operate a system under an unknown probability law which is chosen by nature (from a finite set) in a worst case way. This model ambiguity is incorporated in the optimization criterion in a risk-sensitive way. For further literature on ambiguity see the survey [10].

We will start with a statistical Markov Decision Process where the transition kernel and cost functions depend on an unknown parameter for which we have a prior distribution. Only the states of the process are observable. Since the Ellsberg experiment suggests that the parameter (model) ambiguity should be treated different to uncertainty of the evolution of the process, we will consider the expected cost of a policy as a random variable and use the entropic risk measure for the model ambiguity. This is in this specific setting similar to the approach in [14], but different to approaches where the entropic risk measure is applied to the product measure of parameter uncertainty and uncertainty of process evolution. The latter approach has been pursued in [3] and extended to robust problems in [18]. Using the dual representation of the entropic risk measure we can show that there is a connection of our risk-sensitive optimization criterion to the robust penalty problem considered in [11]. Relations like this have already been discussed in [16]. However, note that in our setting nature chooses only the worst case measure with respect to the parameter uncertainty. Our model includes both the classical Bayesian MDP (with risk neutral attitude towards ambiguity) and the robust MDP as limiting cases. We use the general minimax theorem of Kneser, Fan, Sion (see [21]) and results of [20] to solve our problem. It is easy to see from our approach that the solution method not only applies to the case where model ambiguity is evaluated by the entropic risk measure, but to any convex risk measure with a suitable dual representation. Thus, we will also consider the case where model ambiguity is evaluated by the Average Value at Risk. This complements studies in which the Average Value at Risk is applied to the whole discounted cost (see e.g. [1, 6]).

Our paper is organized as follows: In the next section we introduce our statistical MDP with a given prior distribution and the optimization criterion which we consider. Alternative representations and interpretations are also discussed. Section 3 is then devoted to the minimax theorem and the existence of optimal polices. It will turn out that under some continuity and compactness assumptions, optimal policies exist and coincide with the optimal policy of a classical Bayesian MDP with different (more pessimistic) prior instead of . The model with Average Value at Risk is discussed in Section 4 and yields from a structural point of view the same policy. Section 5 explains how the problem can be solved in an algorithmic way. In the last section we explain our approach using a specific example from statistical decision theory. In this example we are able to derive the optimal policy for the entropic risk measure as well as for the Average Value at Risk.

2. MDP with Entropic Risk Measure for Model Ambiguity

We suppose that a statistical Markov Decision Processes is given which we introduce as follows: We assume that the state space is a Borel space, i.e., a Borel subsets of some Polish space endowed with the -algebra of Borel sets. Actions can be taken from a set which is again a Borel space. The set is a Borel subset for . By we denote the feasible actions depending on the state at time . We assume that contains the graph of a measurable mapping from to . Furthermore there is a non-empty parameter space endowed with some -algebra. The stochastic transition kernel from to which determines the distribution of the new state at time given the current state and action depends on a parameter . So is the probability that the next state at time is in , given the current state is and action is taken. is the distribution of the initial state. In what follows we assume that the law of motion is given by

We assume that are probability measures on . Moreover, let

be non-negative measurable functions on and for all respectively.

Remark 2.1.

In general, are assumed to be -finite measures for all . But then there exists a probability measure and a finite positive density such that . Then we can replace by and by and w.l.o.g. we may assume that are probability measures.

Next we introduce policies for the decision maker. Here it is important to consider the set of observable histories which are defined as follows:

An element denotes the observable history of the process up to time which consists of the sequence of states and actions. For a Borel set we denote by the set of all probability measures on . In what follows we consider MDPs with finite horizon .

Definition 2.2.

-

a)

A measurable mapping with the property that it holds for is called a randomized decision rule at stage .

-

b)

A sequence where is a randomized decision rule at stage for all , is called policy. We denote by the set of all policies.

-

c)

A decision rule is called deterministic if for some measurable function with Here is the one-point measure on . A policy is called deterministic if all decision rules are deterministic.

A policy induces according to the theorem of Ionescu-Tulcea a probability measure

on . Since depends measurably on , we may infer that for any , the mapping is a transition probability from into .

The corresponding stochastic decision process is given by and determines the state-action process.

Further we have measurable and bounded cost functions

on and a measurable and bounded terminal cost

on . All cost functions may depend on the unknown parameter . Note that in this case we assume that cost are not observable.

We are now interested in the cost incurred by this decision process over the finite time horizon . Therefore, we define for a policy

where is the expectation with respect to . Note that is measurable on . Suppose is a fixed initial belief about the unknown parameter . In the established theory of Bayesian MDP (see e.g. [2], Sec. 5) the aim would be to minimize

| (2.1) |

over all policies . This criterion implies that the decision maker is risk neutral with respect to the operating risk as well as with respect to model ambiguity, given in form of the prior . In what follows we will now consider the case that the decision maker is risk averse with respect to model ambiguity. More precisely, we consider

| (2.2) | |||||

| (2.3) |

with . For small the criterion is approximately equal to (see [5])

In particular for we obtain in the limit the classical Bayesian MDP (2.1). For the variability of the minimal cost in is penalized. Moreover, we have the following representation for (2.2), also known as ’dual’ representation (see [8], p.279) where

where for

is the relative entropy function or Kullback-Leibler distance. From this representation we see that the case corresponds to the case of a robust optimization problem or worst-case optimization problem where we minimize the cost if nature choose the least favourable measure for the parameter . For this means that potentially a whole range of beliefs about is considered but deviations from the belief are penalized. A similar criterion has been used in [11] where preferences of an agent for a bet are expressed by

In our paper we relate model ambiguity only to the unknown parameter . This is connected to what in economics is called two-stage approach and where ambiguity typically arises in the first (model) stage. Empirically this has been discovered in the famous Ellsberg experiment. In [14] it has been suggested to consider

as a preference function where is an increasing real-valued function which describes the agent’s attitude towards ambiguity and is a utility function.

In what follows we denote by

When we insert the dual representation in (2.3), then we obtain

| (2.4) |

Though it is well-known how the solution of the inner optimization looks like, namely

it is impossible to solve the outer minimization problem directly, nor get some information about the structure of the optimal policy, since depends on the policy, too.

3. Existence of Optimal Policies

It would be easier to solve the problem if we could interchange the sup and the inf in (2.4). In order to achieve this we use the general minimax theorem of Kneser, Fan, Sion (see [21]). The theorem uses the definition of concave-convexlike functions.

Definition 3.1.

A function on is called concave-convexlike, if

-

(i)

for all and , there is an such that

-

(ii)

for all and , there is an such that

Note in particular that any function on which is concave in the first component and convex in the second component is concave-convexlike. Then Theorem 4.2. in [21] tells us:

Theorem 3.2.

Let be any space and be a compact space, a function on that is concave-convexlike. If is lower semi-continuous in for all then

We would like to apply the theorem to the function

which is defined on A topology on can be introduced as follows: Denote by the probability measure on defined by

and let the set of all probability measures which are generated by policies. On we consider the ws∞-topology (see [19]), i.e. the coarsest topology such that is continuous for all such that is continuous and the function is bounded and measurable. Given the relativization of the ws∞-topology on we can then endow with the inverse image under the mapping of the topology on . This is the coarsest topology on for which is continuous.

For the next statements we need some assumptions for all .

- (C1):

-

The set is compact for all .

- (C2):

-

The function is lower semi-continuous for all and .

- (C3):

-

The function is lower semi-continuous for all and .

Then we obtain:

Lemma 3.3.

Under (C1)-(C3) it holds:

-

a)

is compact.

-

b)

The mapping is lower semi-continuous on for all and for all and there exists a policy such that for all

-

c)

is convex and is concave on .

Proof.

-

a)

This is Corollary 7.3 b) in [20].

-

b)

Follows from Corollary 7.3 a) in [20]. It suffices to show that is lower semi-continuous on . In order to see how our assumptions are needed we give the following sketch of the proof. First note that

where

We obtain . Then one can show (using the assumptions) that is lower semi-continuous on in the ws∞-topology. The lower semi-continuity of on follows since is continuous.

Note that for the second statement it is important to work with randomized policies.

-

c)

The convexity of the set is obvious. Concavity of the mapping can also be shown: For this purpose let According to the Radon-Nikodym theorem have densities w.r.t. say . Hence for the measure has density w.r.t. and we consider

Since obviously is convex for , we obtain that is concave. Since is linear, the statement follows.

∎

All assumptions of Theorem 3.2 are now satisfied and we obtain

Theorem 3.4.

Under assumptions (C1)-(C3) it holds:

-

a)

Min and sup can be interchanged, i.e.

(3.1) -

b)

There exists an optimal policy for (2.3), i.e.

Proof.

For the second main theorem we need further conditions for all :

- (C4):

-

The parameter space is a compact metric space (endowed with the -algebra of Borel subsets of ).

- (C5):

-

The function is lower semi-continuous on for all .

- (C6):

-

The function is continuous on for all and the function is continuous for all .

These assumptions imply that we obtain a worst prior measure (initial belief). Here we endow with the weak topology.

Theorem 3.5.

Proof.

a) compact implies that is weakly compact. Moreover, the mapping is upper semi-continuous in the weak topology, since is continuous by our assumptions (see Corollary 8.3 in [20]) and the entropy function is lower semi-continuous w.r.t. the weak topology (see Theorem 1 in [17]). Hence also is upper semi-continuous and attains its supremum on . The existence of a saddle point follows from the classical saddle point theorem of game theory.

Part b) follows directly from a) since is equivalent to . Part c) is well-known in Bayesian MDPs and follows with [12], Theorem 15.2 together with Lemma 15.1. ∎

Theorem 3.5 has the advantage that it is possible to solve the inner optimization problem explicitly. Since the entropy part does not depend on the policy , only the part is interesting and it can be solved with the established theory of Bayesian MDP (see Section 5). Of course, the resulting optimal policy depends on which has to be computed in a second step.

Remark 3.6.

It is possible to consider MDPs with infinite time horizon in the same way. I.e. instead of we take

and assume or a weaker convergence assumption. Then we obtain the same results as for finite-stage MDPs with agents who are ambiguity averse.

Remark 3.7.

The entropic risk measure motivates to penalize the robust MDP formulation by the deviation of the prior from the ’statistically correct’ prior . Instead of taking the relative entropy one could of course take any other distance which is convex. For example one could take the Bhattacharyya distance which for probability measures and with densities and is defined by

and is a convex mapping in for fixed . For details see [4].

4. MDP with Average Value at Risk for Model Ambiguity

Instead of the entropic risk measure one may apply any other convex risk measure to penalize model ambiguity. Convex risk measures have a representation in dual form (see [8], Theorem 4.33) which can be used to apply the minimax Theorem. In what follows we restrict the discussion to the Average Value at Risk. We consider the same Bayesian MDP framework as in Section 2 with a fixed initial belief and define the Value at Risk at level for the random variable on as

Note that we consider the actuarial point of view here where large positive outcomes are bad and is usually close to 1. Moreover, note that depends on .

When model ambiguity is measured by the Average Value at Risk, we obtain as optimization criterion

| (4.1) | |||||

| (4.2) |

If we get in the limit just the expectation and thus the classical risk neutral setting. For we obtain in the limit the worst-case risk measure. Using the dual representation of Average Value at Risk (see e.g. [8], Theorem 4.52) this amounts to

with and

The idea here is to proceed in the same way as in Section 3 and use the previously established results. We obtain with some slight changes to the previous section:

Theorem 4.1.

5. Solving the Bayesian Dynamic Decision Problem

Let be fixed. The problem is a standard Bayesian MDP. For a detailed explanation how these problems can be solved, see [2], Section 5. We give here only a rough idea. Note that in the context of Section 3 and 4 we have to replace by in the solution procedure. The problem can be solved by a state space augmentation. The state which has to be considered is where and is the current belief (conditional distribution) about . This belief has to be updated as follows:

gives the new belief, if the previous belief was , the previous state was , the new state is and action is chosen. is the new belief directly after the observation of the first state. Thus, starting with the prior we obtain a sequence of beliefs depending on the observations and the history of the process: . The state transition kernel is given by

Under well-known continuity and compactness assumptions it is then possible to show that the value

can be computed recursively by

If we denote by the (deterministic) minimizer of on the right-hand side of the equation for , then the deterministic policy is optimal for the given problem with

i.e. .

6. An Example

We consider the following example which is taken from [7], Example 2, Section 12.6. A statistician observes a sequence of Bernoulli random variables with unknown success probability . Suppose that is either or . She has an initial belief about the two probabilities. Two actions are available: Either stop the observation process and choose a terminal decision or make a further observation of the Bernoulli trial. The cost of one observation is and if the decision is correct, there is no cost. For a wrong terminal decision one has to pay the amount of . What is the optimal Bayesian strategy? We assume that the statistician is risk averse and uses the criteria presented in this paper.

We use Theorem 3.5 resp. Theorem 4.1 to solve these problems. We have to take as the state space the current belief about the two hypothesis. Since the parameter set is these beliefs are only two-point distributions. In what follows we assume that the interval is the state space where is the current belief that is the true parameter. The action space is where means to take another observation and means to stop the observation process and choose a terminal decision (which is then the hypothesis with higher belief). In this case the cost is given by

In case we decide to take another observation and the observation is a ’success’ (indicated by ’1’) we obtain the following new belief:

In case we observe a ’failure’ (indicated by ’0’) we obtain for the new belief

Then we obtain from the Bayesian MDP theory the following recursion:

Working through this recursion finally yields:

and for all , where

The optimal decision at the beginning is to take another observation if otherwise take a terminal decision immediately. After one observation the statistician will always take a terminal decision.

6.1. Problem with Entropic Risk Measure

When we want to solve the problem with risk aversion against ambiguity measured by the entropic risk measure, we now have to consider the following problem where is the initial belief

Using the fact that the function is symmetric i.e. this boils down to

| (6.2) | |||||

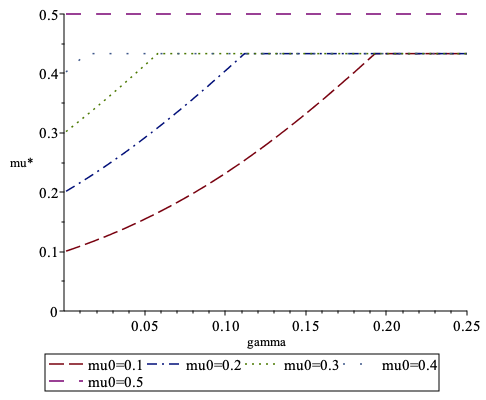

When the statistician is risk averse with parameter and has initial belief about the hypothesis she will rather solve the Bayesian MDP with . Observe that is most risk averse choice of the prior. In Figure 1 the optimal is plotted as a function of the risk aversion for different . Note that

What we observe in the example is that

-

(i)

For we have .

-

(ii)

-

(iii)

The interpretation of (i) is that a risk averse statistician will always shift the statistically correct prior in direction of the uniform distribution. The case is in the limit the classical Bayesian MDP with original prior . The case corresponds to the robust optimization where the most unfavourable prior is chosen. In this example the most unfavourable prior is any prior in the interval since this requires another observation.

6.2. Problem with Average Value at Risk

We can also consider this example with the ambiguity measured by the Average Value at Risk. Here we have to solve

The set corresponds to . The maximum point as a function of and is given by (in case on non-uniqueness we give the whole rang of optimal values)

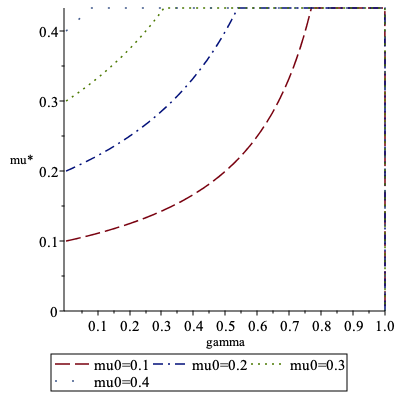

Due to symmetry reasons we restrict again to the case . In Figure 2 the optimal is plotted as a function of for different . Note that

We again observe in this case that

-

(i)

For we have .

-

(ii)

-

(iii)

Though in this case the interpretation of is different, the general behaviour of the optimal is the same.

7. Conclusion

In this paper we present a proposal to deal with model ambiguity for MDPs. Using a dual representation and a general minimax theorem we are able to solve the ambiguity problem. The solution procedure is illustrated by an example taken from statistical decision theory. The approach is closely related to robust MDPs.

References

- [1] N. Bäuerle and J. Ott. Markov decision processes with average-value-at-risk criteria. Mathematical Methods of Operations Research, 74(3), 361-379, 2011.

- [2] N. Bäuerle and U. Rieder, Markov Decision Processes with Applications to Finance. Springer-Verlag, Berlin Heidelberg, 2011.

- [3] N. Bäuerle and U. Rieder. Partially observable risk-sensitive Markov decision processes. Mathematics of Operations Research, 42(4), 1180-1196, 2017.

- [4] A. Bhattacharyya, On a measure of divergence between two statistical populations defined by the probability distributions. Bulletin of the Calcutta Mathem. Soc.. 35, 99-109, 1943.

- [5] T. Bielecki and S.R. Pliska, Economic properties of the risk sensitive criterion for portfolio management. Rev. Account. Fin. 2, 3-17, 2003.

- [6] Y. Chow, A. Tamar, S. Mannor and M. Pavone. Risk-sensitive and robust decision-making: a CVaR optimization approach. In Advances in Neural Information Processing Systems, pp. 1522-1530, 2015.

- [7] M.H. DeGroot, Optimal Statistical Decisions. McGraw-Hill, NewYork, 1970.

- [8] H. Föllmer and A. Schied. Stochastic finance: an introduction in discrete time. 4th edition. Walter de Gruyter, 2016.

- [9] I. Gilboa and D. Schmeidler. Maxmin expected utility with non-unique prior. Journal of Mathematical Economics, 18(2), 141-153, 1989.

- [10] M. Guidolin and F. Rinaldi. Ambiguity in asset pricing and portfolio choice: A review of the literature. Theory and Decision, 74(2), 183-217, 2013.

- [11] L. Hansen and T.J. Sargent. Robust control and model uncertainty. American Economic Review, 91(2), 60-66, 2001.

- [12] K. Hinderer, Foundations of non-stationary dynamic programming with discrete time parameter. Springer-Verlag, Berlin, 1970.

- [13] G.N. Iyengar. Robust dynamic programming. Mathematics of Operations Research, 30(2), 257-280, 2005.

- [14] P. Klibanoff, M. Marinacci, and S. Mukerji. A smooth model of decision making under ambiguity. Econometrica 73.6, 1849-1892, 2005.

- [15] F. Maccheroni, M. Marinacci and Rustichini, A. Ambiguity aversion, robustness, and the variational representation of preferences. Econometrica, 74(6), 1447-1498, 2006.

- [16] T. Osogami, T. Robustness and risk-sensitivity in Markov decision processes. In Advances in Neural Information Processing Systems, pp. 233-241, 2012.

- [17] E. Posner, Random coding strategies for minimum entropy. IEEE Transactions on Information Theory, vol. 21, no. 4, pp. 388-391, 1975.

- [18] M. Rasouli and S. Saghafian. Robust Partially Observable Markov Decision Processes. Preprint 2018.

- [19] M. Schäl, On dynamic programming: compactness of the space of policies. Stochastic Processes Appl. 3, no. 4, 345-364, 1975.

- [20] M. Schäl, On dynamic programming and statistical decision theory. The Annals of Statistics, vol. 7, no. 2, pp. 432-445, 1979.

- [21] M. Sion, On general minimax theorems. Pacific. J. Math. VIII, 171-176, 1958.