Universal Online Convex Optimization with Minimax Optimal -Order Dynamic Regret

Abstract

We introduce an online convex optimization algorithm which utilizes projected subgradient descent with optimal adaptive learning rates. Our method provides second-order minimax-optimal dynamic regret guarantee (i.e. dependent on the sum of squared subgradient norms) for a sequence of general convex functions, which may not have strong-convexity, smoothness, exp-concavity or even Lipschitz-continuity. The regret guarantee is against any comparator decision sequence with bounded path variation (i.e. sum of the distances between successive decisions). We generate the lower bound of the worst-case second-order dynamic regret by incorporating actual subgradient norms. We show that this lower bound matches with our regret guarantee within a constant factor, which makes our algorithm minimax optimal. We also derive the extension for learning in each decision coordinate individually. We demonstrate how to best preserve our regret guarantee in a truly online manner, when the bound on path variation of the comparator sequence grows in time or the feedback regarding such bound arrives partially as time goes on. We further build on our algorithm to eliminate the need of any knowledge on the comparator path variation, and provide minimax optimal second-order regret guarantees with no a priori information. Our approach can compete against all comparator sequences simultaneously (universally) in a minimax optimal manner, i.e. each regret guarantee depends on the respective comparator path variation. We discuss modifications to our approach which address complexity reductions for time, computation and memory. We further improve our results by making the regret guarantees also dependent on comparator sets’ diameters in addition to the respective path variations.

Index Terms:

online learning, convex optimization, gradient descent, dynamic regret, minimax optimal, universal guaranteeI Introduction

I-A Preliminaries

Convex programming, a major topic of online learning [1], is extensively studied in the fields of automatic control, computational learning theory, signal processing and analysis. In many tasks of optimization or prediction, the aim is to minimize some loss or error, many of which are convex functions, possibly time-varying. Examples include predictive control [2], network resource allocation [3], distributed agent optimization [4, 5], fault diagnosis [6], stochastic programming [7], adaptive filtering [8], beamforming [9] and classification [10, 11].

In the online optimization or learning setup, the convex objectives (i.e. the loss functions ) arrive sequentially. In particular, at each time , we, the learner, or the controller, produce a decision , and then, suffer the loss . The role of a learning procedure, or the controlling agent, is to choose so that the cumulative loss is minimized. To exemplify, in the sequential linear regression problem under absolute error, at each , we decide on a parameter vector , then, the nature reveals a feature vector and a desired output , and we suffer the loss , which is a convex function with respect to .

In this work, we derive a learning algorithm applicable for any convex loss function sequence , that may not necessarily display additional desirable properties such as strong-convexity, smoothness, exp-concavity or even Lipschitz-continuity, unlike [12, 13, 14, 15, 16, 17, 18, 19]. The performance of such an online learning algorithm is traditionally evaluated relative to the best fixed decision in hindsight, e.g. the optimal fixed parameter vector. This evaluation metric is called static regret, which measures the difference between cumulative losses of our algorithm and the best fixed decision . However, such a metric is insufficient in online dynamic scenarios where the best fixed decision itself performs poorly. To exemplify, consider an online learner to determine the optimal controller for a simple dynamic and time-varying zeroth-order (gain) discrete system with an open-loop (no feedback) circuit. Suppose the reference signal (desired output) is causal with the energy . For some , let the system gain be for and for , and also, and . The optimal static controller gain (lowest error energy) would be as opposed to a time-varying controller with gain for and for . Note that such an optimal dynamic controller would incur zero error, while the error of an optimal static controller could be very large, e.g., for and , the optimal (lowest energy) error signal would equal to the reference itself.

Henceforth, instead of the static regret, we measure performance with the generalized notion of dynamic regret, allowing a time-varying comparator decision sequence . State-of-the-art algorithms in the literature achieve dynamic regret guarantees by imposing additional assumptions on the properties of , which may not hold in real life scenarios, such as strong convexity [12, 13] (positive lower bound on the eigenvalues of Hessian matrix), Lipschitz-continuity [12, 14, 15, 16, 17, 18, 20, 21, 22, 23, 24] (upper bound on subgradient norms), Lipschitz-smoothness [13, 15, 25] (upper-bounded eigenvalues of Hessian), and bounded temporal functional variations [17].

More restrictive settings have also been investigated where a learner has access to the full information of the past functions [15] or queries the subgradient of each at multiple points without incurring any additional losses [26]. Such settings are also incompatible with many real life applications where the evaluation of each subgradient is costly (e.g. computationally) or even equivalent to making a decision, hence actually incurring a loss. In addition to the general online convex optimization, there exist dynamic studies for a specialized linear optimization problem, i.e. prediction with expert advice [27, 28, 29, 30]. Moreover, adaptive regret guarantees dependent on subgradient norms are achieved for static regret [31, 32, 33].

I-B Contributions

As the first time in the literature, we introduce an efficient online projected subgradient descent algorithm for any sequence of convex loss functions, with dynamic regret guarantee of

where is the diameter of the projection set (e.g. feasible decision set) to which all and belong, is the maximum distance between any , i.e. and is the path variation measuring the complexity of our competition, i.e. . This guarantee is simultaneously achieved against all comparators, universally.

Even though it is varying against different comparators (proportional to and ), it is shown to be minimax optimal for each comparator individually. This optimality is demonstrated by showing that the regret guarantees match the respective worst-case dynamic regret lower bounds with adaptive dependency on the subgradient norms instead of some preconceived bounds. Furthermore, via certain extensions, our complexities (computation, time, memory) can be efficiently reduced with certain (generally acceptable) trade-offs. The development of our results is summarized as follows.

We derive an algorithm which achieves minimax optimal guarantees against any comparator sequence where and is known a priori by the algorithm. We enhance our method with the ability to incorporate a time-growing , i.e. , which is reasonable as is nondecreasing with . Then, we alternatively suppose the knowledge of arrives partially throughout optimization which is a less restrictive setting.

We introduce our universal method which assumes no knowledge regarding , i.e. we compete against any comparator sequence , and each competition is individually minimax optimal where the regret bounds depend on each comparator sequence separately via

Our work on universality, e.g. parameter-free algorithm (no prior setting of and ), is the most novel, eliminating the need of any prior (hindsight) information and producing a truly online minimax optimal approach as a first in the literature.

I-C Organization

The work is constructed as follows. In Section II, we formally describe the problem. In Section III, we introduce our base algorithm and derive its dynamic regret upper bound for a known fixed , and show its simplicity and superiority against some existing approaches. Following that, we demonstrate the optimality of our algorithm by introducing a worst-case dynamic regret lower bound that matches our regret guarantee up to a constant factor and investigate the cases when path variation is coordinate-wise separable, knowledge on partially arrives and known grows in time, respectively. In Section IV, we adapt our algorithm so that no prior knowledge of is required, and show its capability to provide universal regret guarantees. Specifically, we demonstrate the ability to obtain guarantees for each possible path variation and effective diameters implied by each comparator sequence in a joint and universal manner. In Section V, we demonstrate our performance by simulating an optimization task. We conclude with Section VI. Many proofs of the analyses are given in the appendix.

II Problem Description

We have a sequence of convex functions for discrete times , where is a convex111For all , for any ., closed and bounded subset of . Each is a column vector, is its transpose, is its inner product with , and is its Euclidean norm. The projection solves , a relatively simple computation when is a hyper-ellipsoid/rectangle.

Convexity of each implies the first-order relation

| (1) |

for every pair and every subgradient .

Then, the dynamic regret, denoted as , is defined as

| (2) |

where and are the algorithm’s and comparator’s (best) decision sequences, respectively, and the inequality comes from (1) for any . This is a tight bound when are only known to be convex and holds with equality for linear functions .

Note that cannot be bounded in a nontrivial manner, i.e. sublinear bounds, without some restrictions on , which becomes apparent due to the worst-case (adversarial) regret lower bounds we discuss in Section III-C. Thus, we control the complexity of our competition class by considering such that where

with (naturally) for , which is the diameter of . The parameter of the competition class is also called path variation [15]. This class generalizes the special case corresponding to the static regret (best fixed decision).

III Online Projected Subgradient Descent

We use online subgradient descent with projection as shown in Algorithm 1 to update our decisions. It is a variant of the proximal descent method when we do not assume any underlying functional bias and it is still commonly studied [34]. Given the feasible decision set , and Euclidean projection operator , the utilized update is such that

for learning rates (step sizes) and subgradients . In the following theorem, we investigate a general regret guarantee for a nonincreasing positive learning rate sequence. Then, we show how to sequentially select ideal learning rates.

Theorem 1.

If we run Algorithm 1 with a nonincreasing positive sequence, the dynamic regret can be bounded as,

where is the diameter of , and for .

III-A Optimal Learning Rates

We first define the following quantities, which will be used to determine the optimal subgradient descent learning rates at each time, i.e. . For , with ,

| (3) |

Corollary 1.

If we were to use the optimal constant learning rate , which minimizes the right-hand side of the guarantee in Theorem 1, it yields and

for .

Proof.

If , . If instead, it follows from Theorem 1. ∎

The optimal constant rate requires the future information for . We now present an adaptive causal learning scheme using only the past information.

Corollary 2.

If we use , we obtain the following regret guarantee

which simplifies into

if , and is optimal (minimized) for .

III-B Comparing with Projections using Self Outer Products

The adaptive regret guarantee in Corollary 2 for outperforms , which is the static regret guarantee provided by the projected normalized sub-gradient descent using the root of self outer products sum , e.g. Ada-Grad with full matrix divergences [31].

Claim 1.

Given a vector sequence for ,

where the square root of the outer products sum on the right-hand side corresponds to its unique positive semidefinite principal square root, and the trace operation takes the sum of elements on the main diagonal.

There is a discrepancy between the left and right sides of Claim 1 which could rise up to a multiplicative term of (when the eigenvalues of the outer product sum are similar) -where is the dimension of our decision set - even though the algorithm we present is more efficient, i.e. at each time our algorithm computes the inner product while algorithms with full divergences compute the outer product .

III-C Minimax Dynamic Regret Lower Bounds

Given any online, i.e. sequential and causal, learning algorithm, we show that there exists a sequence of such that the regret in (2) is lower bounded as follows.

Theorem 2.

For , for any causal algorithm, there exists a sequence such that this algorithm may incur a worst-case dynamic regret as

where is the diameter of and .

The lower bound in Theorem 2 matches the upper bound in Corollary 2, within a factor, thus our adaptive algorithm is optimal in a strong (second-order) minimax sense.

In the following corollary, we also discuss how the lower bound behaves for a uniform gradient norm constraint, i.e. such that for all . We generate a zeroth-order bound and replace the need of a very mild assumption for the worst-case from before, requiring the sums of squared norms from consecutive time segments , i.e. , to be of the same order as each other, with Lipschitz continuity.

Corollary 3.

For instead,

III-D Separate Step Sizes for Each Decision Entry

We extend our results to the case when each entry (or block) employs independent learning rates. For that, we denote the entry block of decisions as , respectively.

Remark 1.

The minimax optimality is preserved if the decision set is separable, i.e.

where the number of coordinate blocks is , and

In the following subsections, we investigate various scenarios for path variations and gradually remove the need to pre-set the quantity .

III-E Partial Information on Path Variation

Here, we investigate the scenario where path variation constraint is not a priori known but is revealed gradually. Consider that, following for , we receive a hint that until (including) , we have a path variation for . The incurred regret can be upper bounded as shown in the following.

Theorem 3.

Assume for , each corresponding to the best decision sequence segments with and , is known at the latest following round. Under such conditions, if we reset Algorithm 1 following times and use the adaptive step sizes in Corollary 2 with for , we upper bound the incurred regret as

where is the feasible set diameter. Assuming is relatively low, i.e. for some constant , which is reasonable to assume as even the variation between successive “best” decisions, i.e. , can be up to , or is finite, this upper bound is minimax optimal within a constant factor in accordance with the worst-case lower bound in Theorem 2.

Remark 2.

If we consider the case where a path variation feedback can also refer to the past such that the feedback arriving after does not bound the path variation for but for with . Then, the run of the algorithm after step size resetting can utilize where the second argument of arises from the utmost limit of path variation during the new segment . Additionally, whenever there are time segments with no path variation feedback revealed in preparation for the corresponding run (e.g. ), then these gaps utilize the utmost limits, i.e., during , use .

III-F Best Sequence Constraint Grows in Time

We now investigate how to handle a time-increasing , i.e. a function such that

meaning is the upper bound of the best sequence path variation for the optimization of duration . We employ a sort of “doubling trick” with some knowledge on . For , we identify . To exemplify, considering the natural bound , and then, suppose for some real number . This means , where is the flooring function.

Note that we do not need to access in full a priori, i.e. for all integers . The identifications of for increasing can be done iteratively following . Then, after each , we reset Algorithm 1 with learning rates selected according to Corollary 2 with path variation set as for that run. When the differential is too great, the duration of run can even be , i.e. that specific run is effectively skipped. This scheme results in the following theorem.

Theorem 4.

When the best decision sequence path variation for a -length optimization is bounded by some nondecreasing , Algorithm 1 is reset following rounds , with . The new run lasts until (including) , and this run sets the path variation as . By using the path variation in full, from up to , our algorithm considers the possibility where we compete against a best decision sequence which had low to none path variation till now, i.e. . The resulting regret is

where , and is the diameter of decision set . This guarantee is minimax optimal within a constant factor in accordance with Theorem 2.

If we cannot even query every round, we can employ an exponential search method. Following remark explains this.

Remark 3.

Starting with the knowledge of some , query for until is identified, ensuring that . Then, we identify via binary search, such that we have . If the querying of is further restricted, e.g. it can be queried for both low number of times and only in increasing arguments, we can employ the doubling trick on , e.g. , with the mild assumption of a near subadditive property such that we have , which is somewhat reasonable as (i.e., is at most linear).

IV Universal Regret for Varying Path Variations

In this section, we build upon our previous findings and prepare parallel running algorithms as agents for an eventual mixing scheme (i.e., prediction with expert advice) to circumvent the need of any knowledge on the path variation . As the time horizon grows, the number of such agents can be limited to thanks to Corollary 2 by using . Then, the regret of running agent, which sets the path variation , with , is bounded as follows.

Corollary 4.

Consider runs of Algorithm 1, indexed as , with the resetting as in Theorem 3. These runs have no access to any path variation knowledge but use predefined values following set reset rounds , i.e. run uses and for . The last pair for run is set as (i.e. no more reset) and . In accordance with Theorem 3 -and Corollary 2-, each run incurs

whenever the actual overall path variation during the whole optimization is such that . The regret bound for is not needed for what follows. Also, for an and is minimax optimal up to some constant factor.

Proof.

Similar to Theorem 4. ∎

IV-A Explicit Linear Optimization

Here, we explain averting the need of subgradient evaluation for each agent separately running Algorithm 1. Similar to [16, 35], we show that the regret can be optimally bounded with a single subgradient evaluated at each time by considering the problem as purely linear. Using (2), we separate the bound into two sums where each is to be optimized by alternating between subgradient descents and expert mixtures. Thus,

| (4) | ||||

where denotes the static regret of the expert mixture scheme against the loss incurred by some running Algorithm 1 and denotes the linearized upper bound of the dynamic regret of the running Algorithm 1, all in accordance with Corollary 4, i.e. .

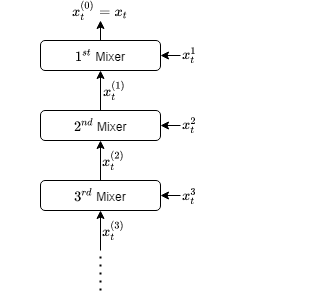

Hence, the alternating optimization will work as follows. At each time , during the first (initial) stage, is optimized for all agents in parallel, each indexed by a different , with each such agent producing a decision , and, during the second (final) stage, each is optimized by combining all , thus producing the final decision . All that remains is to construct the way to mix the decisions of these parallel running agents.

IV-B Recursive Mixture

We consider a recursive expert mixture similar to [27], where the base mixing algorithm is from [36] with 2 experts. The reason for this choice of mixture is twofold. First, since our setting is truly online, i.e. is not predetermined and unbounded, a straightforward application of the mixing method from [36] is not possible. It has to be supplemented with some variant of the doubling trick. Adding the fact that, the regret redundancy due to a regular expert mixture has an additional multiplier of where , the number of experts/agents (i.e., parallel runs of Algorithm 1) in the mixture, also grows to in an unbounded manner, the regret from such an expert mixture would gather a possible multiplicative optimality gap which grows with time, i.e. not finite and thus invalidating the minimax optimality claim.

We can circumvent this by obtaining differing mixture regret redundancies when compared to each expert individually, i.e. the regret guarantees against the optimal and any other experts may be different. Since the guarantees from Algorithm 1 differs for each expert, we want to carefully create this discrepancy in the mixture redundancies against each expert so that they are upper-bounded by the regret from their Algorithm 1 counterparts within a constant factor, thus preserving the minimax optimality claim.

The aforementioned discrepancy in mixture redundancies is achieved exactly by the recursive application of [36], where each mixing is done at the branching-out locations in the growing ensemble of the experts in a skewed tree form, as illustrated in Figure 2. The regret redundancy components are computed after the following separation of :

| (5) |

where is the decision obtained by recursive mixing of another mixture output and from run of Algorithm 1; , i.e. the final decision; and the sum is ignored for . Each mixing is in effect starting at their branch-out times, until then the mixing is pointless since the two experts output the same decision. Consequently, for competing against the running Algorithm 1, the overall regret redundancy from expert mixture is bounded by times the base regret bound for the mixture of two experts, which is as follows.

Lemma 1.

Producing each mixture decision results in a regret such that

is .

This brings us to the following corollary.

Corollary 5.

Theorem 5.

Proof.

It derives from the fact that for some constant . ∎

Up till now, we have considered that our comparators need to come from a feasible set with diameter , and nothing more. In the following subsections, we show that the regret has further efficiency for concentrated comparators.

IV-C Effective Decision Set

Suppose the comparator sequence is concentrated, i.e. are located near some point in set . To improve our regret bounds with regards to such an “effective” decision set , we first notice that the algorithms in both our subgradient descent and expert mixing are scale and translation free as follows.

Lemma 2.

Consider our previous algorithms, and two cases with same loss sequences but different feasible sets.

-

•

Loss sequence is .

-

•

Case 1: Feasible set is .

-

•

Case 2: Feasible set is .

Suppose and are one-to-one, i.e.,

for some scalar and center points . Then, our methods output and if algorithms start with for and for .

Keeping this in mind, consider that are such that

for some natural number , where and for some . Note that, for each , and are related as described in Lemma 2 with suitable .

Thanks to the universality of our algorithm, the regret becomes

where is the diameter of , and with the possibility to enforce equality when, only for a single , is allowed to change in succession. For , this can also be interpreted as

Thus, we have obtained dynamic guarantees, which no longer depend only on the diameter of the feasible set , but also the diameter of the set incurred from the comparator sequence . Hence, the regret result is also universal from a secondary perspective such that, for each comparator sequence generating from our feasible set, the diameter dependence is scale-free with respect to the comparator decisions, and this result is again achieved for all and not just for some “best” sequence. Furthermore, when comparing and , if is , the minimax optimality is also preserved overall. Even if is not , the dependency on our actual set diameter is the optimal one for a fixed comparator in previous works, so it is unlikely to achieve better results.

IV-D Unconstrained Optimization

Here, we show how to conduct online convex optimization when the decision set is not necessarily bounded. For that, select a center point, e.g. the origin. Then, using the scale-free and translation-free properties of our algorithms as in Lemma 2, consider a mapping from non-negative reals to feasible sets such that the set has diameter and center point , e.g. Euclidean ball centered at .

Next, we consider the following preliminary separation of the in (2).

| (6) |

where , and such that and . Manipulating (6), we get

Thus, we can optimize and separately. The second (latter) sum can be bounded by the techniques in our work as

Here, we have , and the path variation for sequence as before.

The first sum is a one-dimensional linear optimization problem, and can be solved with our technique by setting path-variation to , i.e. static comparator , with the feasible set being for some known upper-bound , where the regret bound component satisfy since . Alternatively, can be solved as a unconstrained optimization problem for unknown , in a follow the leader manner, with the techniques available in the said literature, where an example regret bound satisfies both or [37]. There are other techniques to solve this problem with differing regret results, which prioritizes other things and are not directly comparable to each other. Even from the sum, we can see that no information regarding the dynamic nature of is carried to the domain optimization, i.e. the optimality regarding in a stand-alone manner is preserved. The work on unbounded domain optimization is still ongoing and as long as that area of work improves, so does our guarantees.

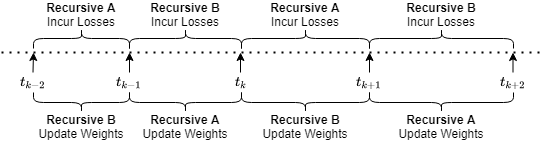

IV-E Finite-Per-Round Time/Computation Complexities

In this subsection, we investigate how to further reduce both the time and computational complexities to the level. The main idea consists of running a set of two mixture frameworks (denoted as and respectively) using a common set of expert (run) ensemble and utilizing a wait-and-update strategy, as illustrated in Figure 3, which shall be explained shortly. These mixture frameworks alternate among themselves to provide the mixing probabilities for the generation of our final decision .

A major difference between the two components of our overall regret, namely and , is that they are respectively static and dynamic, i.e., the comparator in one is fixed (weights) while it is time-variant (decisions) in the other. Consequently, we can follow a wait-and-update strategy for the mixture weights, i.e., wait for rounds and update the mixture weights afterwards using the accumulated losses in that -length time window. This would translate into a multiplicative redundancy of at most in the mixture static regret.

This bound results from each interval corresponding to a wait window during which the losses are accumulated. Since we have agents in use, we can employ such a strategy with time-variant for a time-frame starting at . In combination with the alternating framework approach, this strategy would reduce the per-round time and computational complexities regarding expert mixture to and would multiply by . Framework alternation itself has only a finite effect on the regret.

The same strategy of waiting would not work similarly for in the analyses since comparator sequence in question is not static, but dynamic, and is prone to change (however minor) during the waiting time-window. Without sacrificing deterministic regrets we had thus far, we can reduce only the time to , via parallel processing of our runs. The computational complexity remains since we update all the essential experts at each round separately, which we need to do, as the projection operation into the feasible set can be a rather complicated function in the analyses, even though its computation can be rather efficient. Then, all we can do is randomly update a constant-sized subset of experts at each round, e.g. only one of them. The random selection can be rather cost-efficient so long as we have access to a combination of low-complexity random number generator and a look-up table. In expected regret, since we have experts to randomly choose among, this would result in a multiplicative redundancy of in and in [38, Corollary 5], but not , since we can use all the losses incurred in mixture weight updates as previously discussed, thanks to the framework alternation and wait-and-update strategy. Even though, this regret guarantee is in expectation, since probability used to randomly select an expert is sufficiently high, i.e. , we can generate high probability guarantees using [39] by analyzing the squared dynamic regret, i.e. . After an application of for nonnegative values , we incur an additive redundancy of when the bound holds with probability at least .

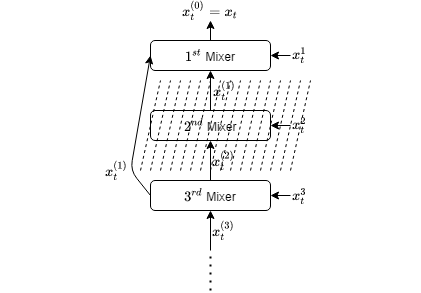

IV-F Lowering Memory Complexity

The regular memory usage has complexity, disregarding decision set dimension and the like. To limit this usage with another function of , i.e. , starting with the expert having lowest-set , we would need to eliminate the even-indexed (or possibly odd) experts and loop back, re-index the runs & repeat as needed to stay below the memory limit. With this, we can also reduce the number of cascading mixtures in effect. The procedure is illustrated in Figure 4. This would cause an increase in the dynamic regret in accordance with Corollaries 2 and 4. Let us assume in the end, between successive experts, we have at most a multiplicative discrepancy of , i.e. for all after re-indexing of the experts following eliminations. We would come across a multiplicative redundancy of in the dynamic regret where the first square root is due to being inside a root in the guarantee from Corollary 2 and the second square root is thanks to us having the ability to choose among and , which respectively lower and upper bound , as the best expert in (4). Thus, if is subpolynomial, which requires infinitely growing (number of expert) however slow in growth, we get subpolynomial multiplicative redundancy with respect to , i.e. it is for all . On the other hand, if the memory is finite, our multiplicative redundancy becomes for the constant memory limit, i.e. .

V Simulation

In this section, we simulate the performance of our approach and make relevant comparisons. Our simulation consists of a data stream, where we want to estimate the next sample point.

From the perspective of an automation system, or a control mechanism, this would correspond to the attempt of matching a given set of inputs to some desired outputs, which may very well act as the inputs themselves in some form (i.e., as a reference).

As shown next, our universal approach has superior performance in the problem of online convex optimization.

V-A Data Generation

The specifics of our learning environment are as follows.

-

•

We have the unknown target sequence , each of which is a two-dimensional vector.

-

•

When we decide on at time , we incur the error as the loss, i.e. .

-

•

There is no additional (e.g. contextual) information.

-

•

For each coordinate of , we observe whether our estimation was over or under, i.e., the sub-gradient is such that, for each dimension ,

where can be arbitrarily located in , e.g. .

-

•

The feasible set is an origin-centered Euclidean ball such that for some , where becomes the set diameter.

-

•

are constructed as , where and have different dynamics.

-

•

The two-dimensional vectors and are constructed as

where are randomly selected from via the uniform distribution in an independently and identically distributed manner.

-

•

The sequences of and are subject to change in time. The number of rounds between successive changes gets progressively larger. This ensures that the quantity of change with respect to the phases remains in , which makes learning possible. The distinction lies in the fact that sequence displays a less dynamic nature.

-

•

For a change following time , is selected from in a uniformly random manner. For , the change is such that , where is selected from in a uniformly random manner, where also gets progressively smaller.

V-B Subjects of Comparison

A total of five estimators are run for this estimation task, where two of them are for comparison and baseline generation. The first is True Oracle, which knows the phases (, ) and the stable magnitudes ,, which are the median . Since the randomness of amplitudes , occurs every round, the best candidate for the optimal competitor with sub-linear path variation is this true oracle. The second one is Last Best, which presumes to know the last target and sets . For the others, is partially known via (• ‣ V-A).

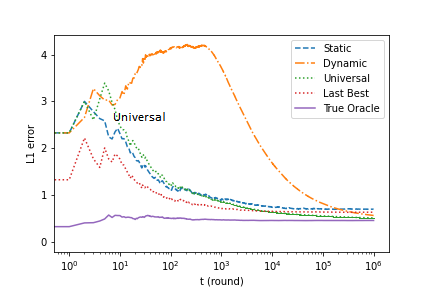

The other three are the sub-gradient based learning algorithms, as explained in this work. The first of these is Static, which competes against the best fixed decision. The second one is Dynamic, which presumes to know the path variation of the best possible-to-learn competitor (i.e. the true oracle) and competes against dynamic strategies, in a min-max optimal manner for the known path variation. The third on is Universal, which is the main result of this work, as in IV.

V-C Performances

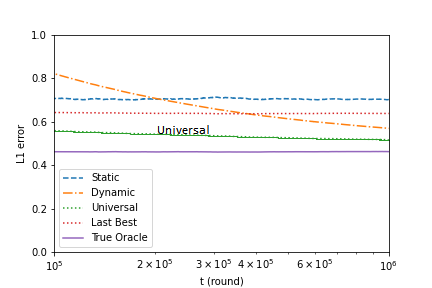

Figure 5 (semi-log) shows the performance of each estimator in Section V-B, where the errors are cumulatively averaged.

As we have expected, ‘True Oracle’ performs the best, since it is effectively the best strategy with sub-linear path variation. However, the true oracle is infeasible to acquire, so here, it serves as a goal (best achievable) for the other learners.

Until a certain round, ‘Dynamic’ performs the worst. This can be explained with the fact that its step-size during the starting rounds becomes detrimentally large, since it uses the true path variation, which is a sizable quantity for the duration of one million rounds. Regardless, the final result demonstrates the validity of our analyses, since its performance surpasses two of the others.

The ‘Universal’ algorithm performs the best and most robustly, as expected in Section IV-C.

VI Conclusion

We first introduced an optimal sequential selection of the learning rates for the projected online subgradient descent algorithm, and achieved the minimax optimal dynamic regret with the comparator path variation bounded as , for a decision set with the diameter and the squared subgradient norm sums abiding by . This guarantee is completely adaptive to the subgradient sequence in the minimax sense. We then introduced an approach to handle a time-growing , i.e. , via resetting the learning rates at critical rounds. This approach has resulted in a multiplicative regret guarantee redundancy, all the while preserving constant-per-round computational and memory complexity. Similarly, we have also investigated the case of partial feedback on with minimax optimal guarantees. Furthermore, we also showed the ability to distributively optimize the individual coordinates with independent runs of our algorithm and achieve minimax optimal dynamic regret guarantees for separable (e.g. hyper-rectangular) decision sets.

Beyond these, we have further managed to eliminate the requirement of knowledge regarding the path variation bound , whether a predetermined value (constant) or in the form of a time-growing function . We have accomplished this by transforming our initial procedure into a two-layered approach, where in one layer, we run multiple versions of the initial procedure as agents, with each agent having set a carefully selected but different possibilities for the unknown , and in the other layer, we combine the decisions produced by these versions under mixture of experts setting in a recursive and cascading manner. Hence, we decreased both the overall computational and memory complexities by allowing certain orders of discrepancies between the actual and the set by different parallel running versions of the original procedure, i.e. within a multiplicative constant factor where some is less than the double and greater than the half of true . This modification to our approach also comes with the property of universality such that any can be true , i.e. we compete against all comparator sequences and obtain regret guarantees which are minimax optimal with respect to the path variations of each comparator sequence separately. Additionally, to achieve a truly online behavior with no knowledge on the time horizon , we restructured these individual runs incorporating specific forms of time increasing , namely a piecewise combination achieved by a linearly increasing function followed by a constant indefinitely. This approach have also resulted in a branching-out formation in the expert (agent) ensemble similar to a stairway into the higher orders of as more runs are incorporated into the ensemble at critical rounds as time goes on, to account for the higher .

Finally, we introduced different approaches to reduce time, computational and memory complexities, to the extent of constant per round, with multiplicative regret redundancies. Moreover, we have also displayed that universality can also be achieved in the form of our decision set (namely its diameter), i.e. the dependence of our guarantees on diameter is replaced for optimal concentration center .

References

- [1] S. Shalev-Shwartz, “Online learning and online convex optimization,” Found. Trends Mach. Learn., vol. 4, no. 2, pp. 107–194, Feb. 2012. [Online]. Available: http://dx.doi.org/10.1561/2200000018

- [2] A. Bemporad, A. Casavola, and E. Mosca, “Nonlinear control of constrained linear systems via predictive reference management,” IEEE Transactions on Automatic Control, vol. 42, no. 3, pp. 340–349, 1997.

- [3] T. Chen, Q. Ling, and G. B. Giannakis, “An online convex optimization approach to proactive network resource allocation,” IEEE Transactions on Signal Processing, vol. 65, no. 24, pp. 6350–6364, Dec 2017.

- [4] S. Hosseini, A. Chapman, and M. Mesbahi, “Online distributed convex optimization on dynamic networks,” IEEE Transactions on Automatic Control, vol. 61, no. 11, pp. 3545–3550, 2016.

- [5] A. Koppel, F. Y. Jakubiec, and A. Ribeiro, “A saddle point algorithm for networked online convex optimization,” IEEE Transactions on Signal Processing, vol. 63, no. 19, pp. 5149–5164, Oct 2015.

- [6] J. Tan, S. Olaru, F. Xu, and X. Wang, “Toward a convex design framework for online active fault diagnosis of lpv systems,” IEEE Transactions on Automatic Control, vol. 67, no. 8, pp. 4154–4161, 2022.

- [7] A. Liu, V. K. N. Lau, and M. Zhao, “Online successive convex approximation for two-stage stochastic non-convex optimization,” IEEE Transactions on Signal Processing, pp. 1–1, 2018.

- [8] Y. Liang, D. Zhou, L. Zhang, and Q. Pan, “Adaptive filtering for stochastic systems with generalized disturbance inputs,” IEEE Signal Processing Letters, vol. 15, pp. 645–648, 2008.

- [9] K. Slavakis, S. Theodoridis, and I. Yamada, “Adaptive constrained learning in reproducing kernel hilbert spaces: The robust beamforming case,” IEEE Transactions on Signal Processing, vol. 57, no. 12, pp. 4744–4764, Dec 2009.

- [10] ——, “Online kernel-based classification using adaptive projection algorithms,” IEEE Transactions on Signal Processing, vol. 56, no. 7, pp. 2781–2796, July 2008.

- [11] K. Gokcesu and H. Gokcesu, “Optimally efficient sequential calibration of binary classifiers to minimize classification error,” arXiv preprint arXiv:2108.08780, 2021.

- [12] O. Besbes, Y. Gur, and A. Zeevi, “Non-stationary stochastic optimization,” Oper. Res., vol. 63, no. 5, pp. 1227–1244, Oct. 2015. [Online]. Available: https://doi.org/10.1287/opre.2015.1408

- [13] A. Mokhtari, S. Shahrampour, A. Jadbabaie, and A. Ribeiro, “Online optimization in dynamic environments: Improved regret rates for strongly convex problems,” in CDC. IEEE, 2016, pp. 7195–7201.

- [14] A. Jadbabaie, A. Rakhlin, S. Shahrampour, and K. Sridharan, “Online Optimization : Competing with Dynamic Comparators,” in Proceedings of the Eighteenth International Conference on Artificial Intelligence and Statistics, ser. Proceedings of Machine Learning Research, G. Lebanon and S. V. N. Vishwanathan, Eds., vol. 38. San Diego, California, USA: PMLR, 09–12 May 2015, pp. 398–406. [Online]. Available: http://proceedings.mlr.press/v38/jadbabaie15.html

- [15] T. Yang, L. Zhang, R. Jin, and J. Yi, “Tracking slowly moving clairvoyant: Optimal dynamic regret of online learning with true and noisy gradient,” in Proceedings of the 33nd International Conference on Machine Learning, ICML 2016, New York City, NY, USA, June 19-24, 2016, ser. JMLR Workshop and Conference Proceedings, M. Balcan and K. Q. Weinberger, Eds., vol. 48. JMLR.org, 2016, pp. 449–457. [Online]. Available: http://jmlr.org/proceedings/papers/v48/yangb16.html

- [16] L. Zhang, S. Lu, and Z. Zhou, “Adaptive online learning in dynamic environments,” CoRR, vol. abs/1810.10815, 2018. [Online]. Available: http://arxiv.org/abs/1810.10815

- [17] L. Zhang, T. Yang, R. Jin, and Z. Zhou, “Strongly adaptive regret implies optimally dynamic regret,” CoRR, vol. abs/1701.07570, 2017.

- [18] M. Zinkevich, “Online convex programming and generalized infinitesimal gradient ascent,” in Machine Learning, Proceedings of the Twentieth International Conference (ICML 2003), August 21-24, 2003, Washington, DC, USA, T. Fawcett and N. Mishra, Eds. AAAI Press, 2003, pp. 928–936. [Online]. Available: http://www.aaai.org/Library/ICML/2003/icml03-120.php

- [19] K. Gokcesu and H. Gokcesu, “Generalized huber loss for robust learning and its efficient minimization for a robust statistics,” arXiv preprint arXiv:2108.12627, 2021.

- [20] L. Rosasco, S. Villa, and B. C. Vũ, “Convergence of stochastic proximal gradient algorithm.” [Online]. Available: https://arxiv.org/abs/1403.5074

- [21] A. Salim, P. Bianchi, and W. Hachem, “Snake: a stochastic proximal gradient algorithm for regularized problems over large graphs,” 2017. [Online]. Available: https://arxiv.org/abs/1712.07027

- [22] A. Lesage-Landry, J. A. Taylor, and D. S. Callaway, “Online convex optimization with binary constraints,” IEEE Transactions on Automatic Control, vol. 66, no. 12, pp. 6164–6170, 2021.

- [23] K. Gokcesu and H. Gokcesu, “Regret analysis of global optimization in univariate functions with lipschitz derivatives,” arXiv preprint arXiv:2108.10859, 2021.

- [24] Y. Shen, T. Chen, and G. Giannakis, “Online ensemble multi-kernel learning adaptive to non-stationary and adversarial environments,” in Proceedings of the Twenty-First International Conference on Artificial Intelligence and Statistics, ser. Proceedings of Machine Learning Research, A. Storkey and F. Perez-Cruz, Eds., vol. 84. PMLR, 09–11 Apr 2018, pp. 2037–2046. [Online]. Available: https://proceedings.mlr.press/v84/shen18a.html

- [25] P. L. Combettes and L. E. Glaudin, “Proximal activation of smooth functions in splitting algorithms for convex image recovery,” 2018. [Online]. Available: https://arxiv.org/abs/1803.02919

- [26] L. Zhang, T. Yang, J. Yi, J. Rong, and Z. Zhou, “Improved dynamic regret for non-degenerate functions,” in NIPS, 2017, pp. 732–741.

- [27] K. Gokcesu and H. Gokcesu, “Recursive experts: An efficient optimal mixture of learning systems in dynamic environments,” 2020.

- [28] N. Cesa-Bianchi, P. Gaillard, G. Lugosi, and G. Stoltz, “A new look at shifting regret,” CoRR, vol. abs/1202.3323, 2012.

- [29] M. Herbster and M. K. Warmuth, “Tracking the best expert,” Mach. Learn., vol. 32, no. 2, pp. 151–178, Aug. 1998. [Online]. Available: https://doi.org/10.1023/A:1007424614876

- [30] K. Gokcesu and H. Gökcesu, “A generalized online algorithm for translation and scale invariant prediction with expert advice,” ArXiv, vol. abs/2009.04372, 2020.

- [31] J. C. Duchi, E. Hazan, and Y. Singer, “Adaptive subgradient methods for online learning and stochastic optimization,” Journal of Machine Learning Research, vol. 12, pp. 2121–2159, 2011. [Online]. Available: http://dl.acm.org/citation.cfm?id=2021068

- [32] H. B. McMahan and M. J. Streeter, “Adaptive bound optimization for online convex optimization,” in COLT 2010 - The 23rd Conference on Learning Theory, Haifa, Israel, June 27-29, 2010, A. T. Kalai and M. Mohri, Eds. Omnipress, 2010, pp. 244–256.

- [33] V. Gupta, T. Koren, and Y. Singer, “A unified approach to adaptive regularization in online and stochastic optimization,” CoRR, vol. abs/1706.06569, 2017. [Online]. Available: http://arxiv.org/abs/1706.06569

- [34] A. Hauswirth, S. Bolognani, G. Hug, and F. Dörfler, “Timescale separation in autonomous optimization,” IEEE Transactions on Automatic Control, vol. 66, no. 2, pp. 611–624, 2021.

- [35] L. Zhang, S. Lu, and Z.-H. Zhou, “Adaptive online learning in dynamic environments,” in Advances in Neural Information Processing Systems, S. Bengio, H. Wallach, H. Larochelle, K. Grauman, N. Cesa-Bianchi, and R. Garnett, Eds., vol. 31. Curran Associates, Inc., 2018, pp. 1323–1333. [Online]. Available: https://proceedings.neurips.cc/paper/2018/file/10a5ab2db37feedfdeaab192ead4ac0e-Paper.pdf

- [36] N. Cesa-Bianchi, Y. Mansour, and G. Stoltz, “Improved second-order bounds for prediction with expert advice,” Machine Learning, vol. 66, no. 2, pp. 321–352, Mar 2007. [Online]. Available: https://doi.org/10.1007/s10994-006-5001-7

- [37] A. Cutkosky, “Artificial constraints and hints for unbounded online learning,” in Proceedings of the Thirty-Second Conference on Learning Theory, ser. Proceedings of Machine Learning Research, A. Beygelzimer and D. Hsu, Eds., vol. 99. PMLR, 25–28 Jun 2019, pp. 874–894. [Online]. Available: https://proceedings.mlr.press/v99/cutkosky19a.html

- [38] H. Gokcesu and S. S. Kozat, “Minimax optimal online stochastic learning for sequences of convex functions under sub-gradient observation failures,” CoRR, vol. abs/1904.09369, 2019. [Online]. Available: http://arxiv.org/abs/1904.09369

- [39] A. Beygelzimer, J. Langford, L. Li, L. Reyzin, and R. Schapire, “Contextual bandit algorithms with supervised learning guarantees,” in Proceedings of the Fourteenth International Conference on Artificial Intelligence and Statistics, ser. Proceedings of Machine Learning Research, G. Gordon, D. Dunson, and M. Dudík, Eds., vol. 15. Fort Lauderdale, FL, USA: PMLR, 11–13 Apr 2011, pp. 19–26. [Online]. Available: http://proceedings.mlr.press/v15/beygelzimer11a.html

- [40] S. Bubeck, “Convex optimization: Algorithms and complexity,” Foundations and Trends in Machine Learning, vol. 8, no. 3-4, pp. 231–357, 2015. [Online]. Available: https://doi.org/10.1561/2200000050

- [41] F. Orabona and D. Pál, “Scale-free online learning,” CoRR, vol. abs/1601.01974, 2016. [Online]. Available: http://arxiv.org/abs/1601.01974

Proof of Theorem 1

Consider the first while loop at Line 2 in Figure 1, which terminates at , where . If the while loop does not terminate, it means all the sub-gradients are zero-vectors and according to (2), we trivially incur regret.

Define such that for . Then, using (2), we replace with and after rearranging the right-hand side, we get

since for .

Provided that where is a convex set, we have for [40].

Noting for , we upper bound with and, for , we further upper bound as

since where is the diameter of which includes all iterations and optimal points .

We also bound . After regrouping

where , and is a placeholder.

Since for , we further upper bound by replacing all with again. This turns the first sum of the right-hand side into a telescoping sum. After we additionally bound and ,

where . This concludes the proof.

Proof of Corollary 2

Proof of Claim 1

Denote . Consequently,

| (7) |

since trace is a linear operation, is equivalent to summing the eigenvalues, and only nonzero eigenvalue of is .

Denote the eigenvalues of as . We also note that positive semidefinite matrices sum to . Therefore, is also a positive semidefinite matrix where are all nonnegative. Consequently, the square root operation on the symmetric effectively replaces the eigenvalues with their square roots. This implies

| (8) |

Additionally, we have from (7) due to the trace operation. Comparing the squares of this and (8) while noting that , we arrive at the claim.

Proof of Theorem 2

To show that some sequence of functions exists -in accordance with our decisions- which results in at least the worst-case regret lower bound in hindsight as claimed in this theorem, we are free to restrict our analysis to linear functions, i.e. , and show that, in hindsight, a function sequence consisting of only such linear functions exists and satisfies the intended lower bound in the theorem. This can be thought of as easing the analysis by further lower bounding. Moreover, to prove the existence of such a function sequence, we only need to take expectation of the said regret lower bound over our candidate sequences with respect to some distribution, both of which are chosen by us in a purposeful manner. This step can also be thought of as further lower bounding. One thing to note is that both of these ”lower bounding” steps do not loosen the bounds much, as the results are shown to match with the regret guarantees (upper bounds) we have previously generated, up to a constant factor. Considering these, the worst-case dynamic regret satisfies

over some expectation for . We lower bound further by restricting such that it remains constant at certain time intervals, i.e. for where and , . This is a valid lower bounding as we effectively shrink the search space of operation and it is fully encapsulated by as . This results in a further lower bound

This worst-case regret lower bound can be simplified via an analysis similar of which can be found in [41, Appendix F] and shall not be repeated here explicitly. The analysis includes, by assuming ”the worst”, selecting such that they have norms and they are parallel to each other and the line joining any two points in farthest from each other. The direction of each is uniformly randomly selected using independent Rademacher distributions out of the two possible directions. The analysis concludes with the use of Khinchin’s inequality separately for each stationary , which gives

Then, there exists a scenario where sequence is such that . This is a rather mild assumption as we assume the setting to be adversarial, i.e. free in its choice of , and, furthermore, are selected by the adversary (environment/setting).

Thus, even in the presence of Lipschitz constraints, i.e., , for sufficiently large and relatively low (e.g. finite) , the adversary can enforce this assumption with arbitrarily small error. Consequently, replacing each summand in the lower bound with this mild assumption gives the bound in this theorem.

Proof of Corollary 3

We similarly restrict as in the proof of Theorem 2 such that it remains constant inside distinct time intervals. Then, in a scenario which is possibly the ”worst-case”, sequence can be such that, for each , we have , since can be freely chosen by the adversarial setting which ensures that, when the time segments are of equal length, can at least be for a total of segments. Since and each segment is at least of length , we also get which results in the corollary similar to Theorem 2.

Proof of Theorem 3

The regret inequality directly follows from Corollary 2 since the algorithm reset for durations corresponding to each which are known prior to the times they are needed for each respective run. This is a tight bound due to the following analysis.

Consider the sum with nonnegative constants ’s and variables ’s under the constraint

This sum is concave with respect to the variables and is maximized when for some . By summing both sides of this equation over all , we see that . Then, when we substitute for and, following that, also substitute for in the sum, it appears that

after we resubstitute for with . Back to the problem at hand, when we set and , we arrive at the theorem.

Proof of Theorem 4

We employ an analysis similar to the proof of Theorem 3. Then, the resets result in the regret

where, we know, . After bounding with and further arrangements, we arrive at our result. The optimality claim is apparent after noticing that maximizes the gap since, when , the disparity (ratio) between and its floor cannot exceed .

Proof of Lemma 1

The losses used in the mixture from [36] are

The regret component from the mixture reduces to

where and are the mixture weights which sum to . This bound is achieved after modifying the mixing method in [36] by considering only one-sided losses, hence eliminating the need for an additional redundancy to upper-bound where and having simplified mixture learning rates. One notices that both and are upper-bounded by since for some . Thus, we obtain the bound in this lemma.