Enhancing the Locality and Breaking the Memory Bottleneck of Transformer on Time Series Forecasting

Abstract

Time series forecasting is an important problem across many domains, including predictions of solar plant energy output, electricity consumption, and traffic jam situation. In this paper, we propose to tackle such forecasting problem with Transformer [1]. Although impressed by its performance in our preliminary study, we found its two major weaknesses: (1) locality-agnostics: the point-wise dot-product self-attention in canonical Transformer architecture is insensitive to local context, which can make the model prone to anomalies in time series; (2) memory bottleneck: space complexity of canonical Transformer grows quadratically with sequence length , making directly modeling long time series infeasible. In order to solve these two issues, we first propose convolutional self-attention by producing queries and keys with causal convolution so that local context can be better incorporated into attention mechanism. Then, we propose LogSparse Transformer with only memory cost, improving forecasting accuracy for time series with fine granularity and strong long-term dependencies under constrained memory budget. Our experiments on both synthetic data and real-world datasets show that it compares favorably to the state-of-the-art.

1 Introduction

Time series forecasting plays an important role in daily life to help people manage resources and make decisions. For example, in retail industry, probabilistic forecasting of product demand and supply based on historical data can help people do inventory planning to maximize the profit. Although still widely used, traditional time series forecasting models, such as State Space Models (SSMs) [2] and Autoregressive (AR) models, are designed to fit each time series independently. Besides, they also require practitioners’ expertise in manually selecting trend, seasonality and other components. To sum up, these two major weaknesses have greatly hindered their applications in the modern large-scale time series forecasting tasks.

To tackle the aforementioned challenges, deep neural networks [3, 4, 5, 6] have been proposed as an alternative solution, where Recurrent Neural Network (RNN) [7, 8, 9] has been employed to model time series in an autoregressive fashion. However, RNNs are notoriously difficult to train [10] because of gradient vanishing and exploding problem. Despite the emergence of various variants, including LSTM [11] and GRU [12], the issues still remain unresolved. As an example, [13] shows that language models using LSTM have an effective context size of about 200 tokens on average but are only able to sharply distinguish 50 tokens nearby, indicating that even LSTM struggles to capture long-term dependencies. On the other hand, real-world forecasting applications often have both long- and short-term repeating patterns [7]. For example, the hourly occupancy rate of a freeway in traffic data has both daily and hourly patterns. In such cases, how to model long-term dependencies becomes the critical step in achieving promising performances.

Recently, Transformer [1, 14] has been proposed as a brand new architecture which leverages attention mechanism to process a sequence of data. Unlike the RNN-based methods, Transformer allows the model to access any part of the history regardless of distance, making it potentially more suitable for grasping the recurring patterns with long-term dependencies. However, canonical dot-product self-attention matches queries against keys insensitive to local context, which may make the model prone to anomalies and bring underlying optimization issues. More importantly, space complexity of canonical Transformer grows quadratically with the input length , which causes memory bottleneck on directly modeling long time series with fine granularity. We specifically delve into these two issues and investigate the applications of Transformer to time series forecasting. Our contributions are three fold:

-

•

We successfully apply Transformer architecture to time series forecasting and perform extensive experiments on both synthetic and real datasets to validate Transformer’s potential value in better handling long-term dependencies than RNN-based models.

-

•

We propose convolutional self-attention by employing causal convolutions to produce queries and keys in the self-attention layer. Query-key matching aware of local context, e.g. shapes, can help the model achieve lower training loss and further improve its forecasting accuracy.

-

•

We propose LogSparse Transformer, with only space complexity to break the memory bottleneck, not only making fine-grained long time series modeling feasible but also producing comparable or even better results with much less memory usage, compared to canonical Transformer.

2 Related Work

Due to the wide applications of forecasting, various methods have been proposed to solve the problem. One of the most prominent models is ARIMA [15]. Its statistical properties as well as the well-known Box-Jenkins methodology [16] in the model selection procedure make it the first attempt for practitioners. However, its linear assumption and limited scalability make it unsuitable for large-scale forecasting tasks. Further, information across similar time series cannot be shared since each time series is fitted individually. In contrast, [17] models related time series data as a matrix and deal with forecasting as a matrix factorization problem. [18] proposes hierarchical Bayesian methods to learn across multiple related count time series from the perspective of graph model.

Deep neural networks have been proposed to capture shared information across related time series for accurate forecasting. [3] fuses traditional AR models with RNNs by modeling a probabilistic distribution in an encoder-decoder fashion. Instead, [19] uses an RNN as an encoder and Multi-layer Perceptrons (MLPs) as a decoder to solve the so-called error accumulation issue and conduct multi-ahead forecasting in parallel. [6] uses a global RNN to directly output the parameters of a linear SSM at each step for each time series, aiming to approximate nonlinear dynamics with locally linear segments. In contrast, [9] deals with noise using a local Gaussian process for each time series while using a global RNN to model the shared patterns. [20] tries to combine the advantages of AR models and SSMs, and maintain a complex latent process to conduct multi-step forecasting in parallel.

The well-known self-attention based Transformer [1] has recently been proposed for sequence modeling and has achieved great success. Several recent works apply it to translation, speech, music and image generation [1, 21, 22, 23]. However, scaling attention to extremely long sequences is computationally prohibitive since the space complexity of self-attention grows quadratically with sequence length [21]. This becomes a serious issue in forecasting time series with fine granularity and strong long-term dependencies.

3 Background

Problem definition

Suppose we have a collection of related univariate time series , where and denotes the value of time series at time 111Here time index is relative, i.e. the same in different time series may represent different actual time point.. We are going to predict the next time steps for all time series, i.e. . Besides, let be a set of associated time-based covariate vectors with dimension that are assumed to be known over the entire time period, e.g. day-of-the-week and hour-of-the-day. We aim to model the following conditional distribution

| (1) |

We reduce the problem to learning a one-step-ahead prediction model 222Since the model is applicable to all time series, we omit the subscript for simplicity and clarity., where denotes the learnable parameters shared by all time series in the collection. To fully utilize both the observations and covariates, we concatenate them to obtain an augmented matrix as follows:

where represents concatenation. An appropriate model is then explored to predict the distribution of given .

Transformer

We instantiate with Transformer 333By referring to Transformer, we only consider the autoregressive Transformer-decoder in the following. by taking advantage of the multi-head self-attention mechanism, since self-attention enables Transformer to capture both long- and short-term dependencies, and different attention heads learn to focus on different aspects of temporal patterns. These advantages make Transformer a good candidate for time series forecasting. We briefly introduce its architecture here and refer readers to [1] for more details.

In the self-attention layer, a multi-head self-attention sublayer simultaneously transforms 444At each time step the same model is applied, so we simplify the formulation with some abuse of notation. into distinct query matrices , key matrices , and value matrices respectively, with . Here and are learnable parameters. After these linear projections, the scaled dot-product attention computes a sequence of vector outputs:

| (2) |

Note that a mask matrix is applied to filter out rightward attention by setting all upper triangular elements to , in order to avoid future information leakage. Afterwards, are concatenated and linearly projected again. Upon the attention output, a position-wise feedforward sublayer with two layers of fully-connected network and a ReLU activation in the middle is stacked.

4 Methodology

4.1 Enhancing the locality of Transformer

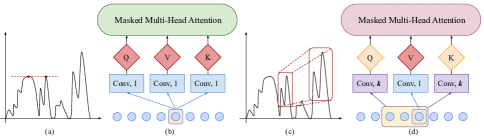

Patterns in time series may evolve with time significantly due to various events, e.g. holidays and extreme weather, so whether an observed point is an anomaly, change point or part of the patterns is highly dependent on its surrounding context. However, in the self-attention layers of canonical Transformer, the similarities between queries and keys are computed based on their point-wise values without fully leveraging local context like shape, as shown in Figure 1(a) and (b). Query-key matching agnostic of local context may confuse the self-attention module in terms of whether the observed value is an anomaly, change point or part of patterns, and bring underlying optimization issues.

We propose convolutional self-attention to ease the issue. The architectural view of proposed convolutional self-attention is illustrated in Figure 1(c) and (d). Rather than using convolution of kernel size with stride 1 (matrix multiplication), we employ causal convolution of kernel size with stride 1 to transform inputs (with proper paddings) into queries and keys. Note that causal convolutions ensure that the current position never has access to future information. By employing causal convolution, generated queries and keys can be more aware of local context and hence, compute their similarities by their local context information, e.g. local shapes, instead of point-wise values, which can be helpful for accurate forecasting. Note that when , the convolutional self-attention will degrade to canonical self-attention, thus it can be seen as a generalization.

4.2 Breaking the memory bottleneck of Transformer

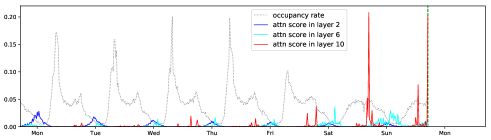

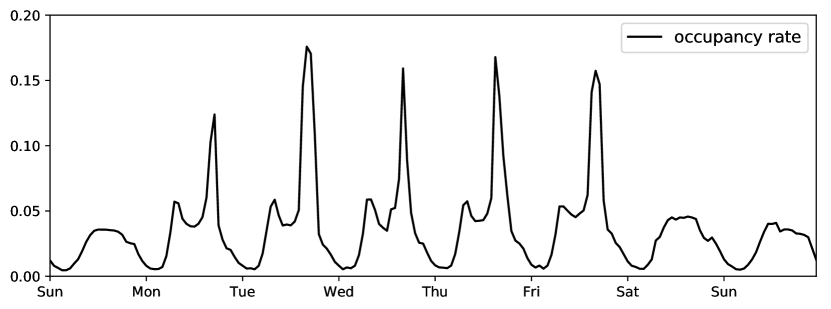

To motivate our approach, we first perform a qualitative assessment of the learned attention patterns with a canonical Transformer on traffic-f dataset. The traffic-f dataset contains occupancy rates of 963 car lanes of San Francisco bay area recorded every 20 minutes [6]. We trained a 10-layer canonical Transformer on traffic-f dataset with full attention and visualized the learned attention patterns. One example is shown in Figure 2. Layer 2 clearly exhibited global patterns, however, layer 6 and 10, only exhibited pattern-dependent sparsity, suggesting that some form of sparsity could be introduced without significantly affecting performance. More importantly, for a sequence with length , computing attention scores between every pair of cells will cause memory usage, making modeling long time series with fine granularity and strong long-term dependencies prohibitive.

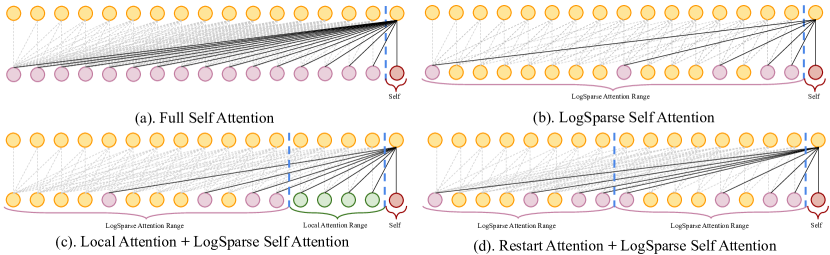

We propose LogSparse Transformer, which only needs to calculate dot products for each cell in each layer. Further, we only need to stack up to layers and the model will be able to access every cell’s information. Hence, the total cost of memory usage is only . We define as the set of indices of the cells that cell can attend to during the computation from layer to layer. In the standard self-attention of Transformer, , allowing every cell to attend to all its past cells and itself as shown in Figure 3(a). However, such an algorithm suffers from the quadratic space complexity growth along with the input length. To alleviate such an issue, we propose to select a subset of the indices so that does not grow too fast along with . An effective way of choosing indices is .

Notice that cell is a weighted combination of cells indexed by in th self-attention layer and can pass the information of cells indexed by to its followings in the next layer. Let be the set which contains indices of all the cells whose information has passed to cell up to layer. To ensure that every cell receives the information from all its previous cells and itself, the number of stacked layers should satisfy that for . That is, and , there is a directed path with edges, where , , , .

We propose LogSparse self-attention by allowing each cell only to attend to its previous cells with an exponential step size and itself. That is, and , , where denotes the floor operation, as shown in Figure 3(b).555Applying other bases is trivial so we don’t discuss other bases here for simplicity and clarity.

Theorem 1.

and , there is at least one path from cell to cell if we stack layers. Moreover, for , the number of feasible unique paths from cell to cell increases at a rate of .

The proof, deferred to Appendix A.1, uses a constructive argument.

Theorem 1 implies that despite an exponential decrease in the memory usage (from to ) in each layer, the information could still flow from any cell to any other cell provided that we go slightly “deeper” — take the number of layers to be . Note that this implies an overall memory usage of and addresses the notorious scalability bottleneck of Transformer under GPU memory constraint [1]. Moreover, as two cells become further apart, the number of paths increases at a rate of super-exponential in , which indicates a rich information flow for modeling delicate long-term dependencies.

Local Attention

We can allow each cell to densely attend to cells in its left window of size so that more local information, e.g. trend, can be leveraged for current step forecasting. Beyond the neighbor cells, we can resume our LogSparse attention strategy as shown in Figure 3(c).

Restart Attention

Further, one can divide the whole input with length into subsequences and set each subsequence length . For each of them, we apply the LogSparse attention strategy. One example is shown in Figure 3(d).

Employing local attention and restart attention won’t change the complexity of our sparse attention strategy but will create more paths and decrease the required number of edges in the path. Note that one can combine local attention and restart attention together.

5 Experiments

5.1 Synthetic datasets

To demonstrate Transformer’s capability to capture long-term dependencies, we conduct experiments on synthetic data. Specifically, we generate a piece-wise sinusoidal signals

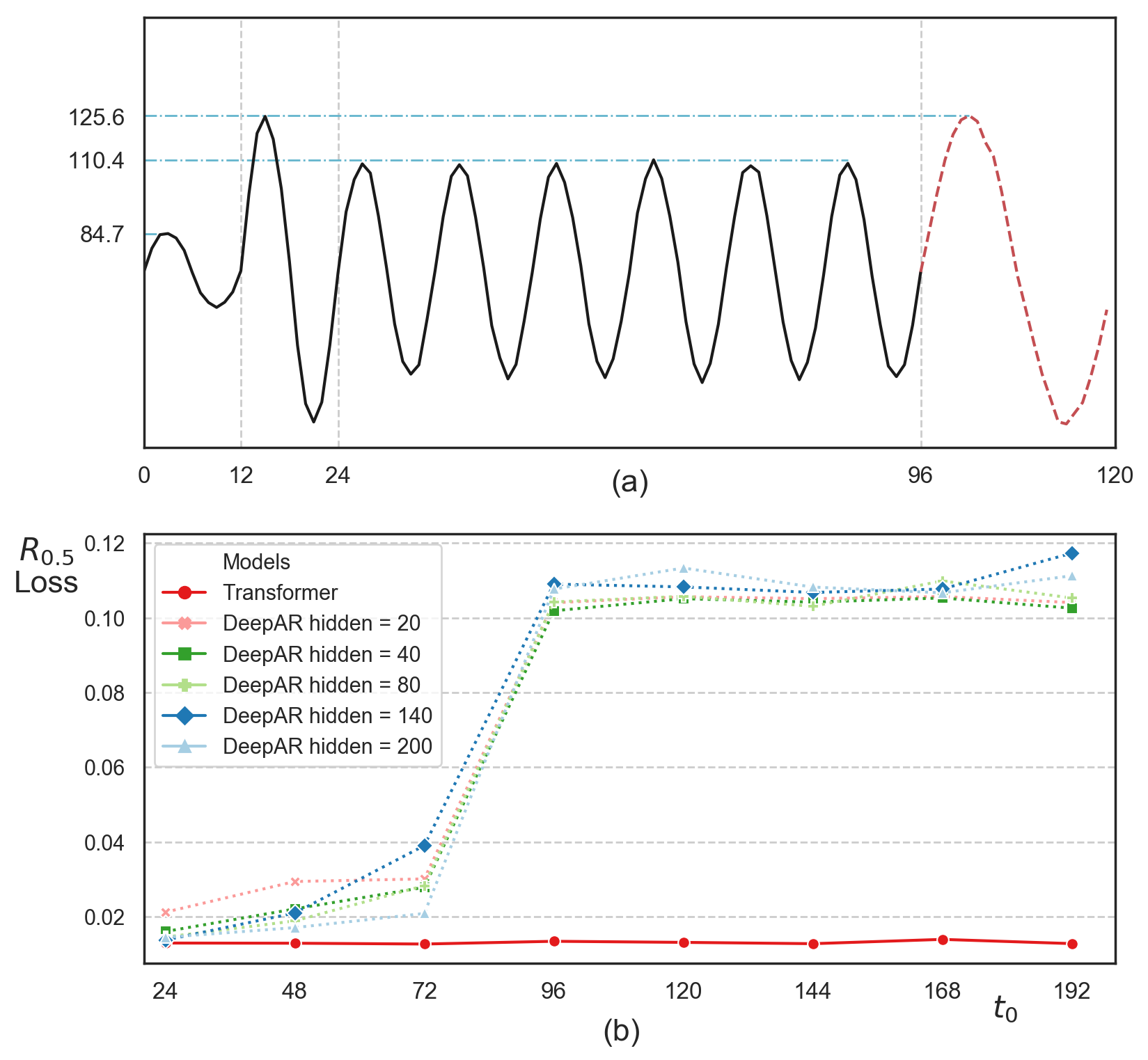

where is an integer, are randomly generated by uniform distribution on , and . Following the forecasting setting in Section 3, we aim to predict the last steps given the previous data points. Intuitively, larger makes forecasting more difficult since the model is required to understand and remember the relation between and to make correct predictions after steps of irrelevant signals. Hence, we create 8 different datasets by varying the value of within . For each dataset, we generate 4.5K, 0.5K and 1K time series instances for training, validation and test set, respectively. An example time series with is shown in Figure 4(a).

In this experiment, we use a 3-layer canonical Transformer with standard self-attention. For comparison, we employ DeepAR [3], an autoregressive model based on a 3-layer LSTM, as our baseline. Besides, to examine if larger capacity could improve performance of DeepAR, we also gradually increase its hidden size as . Following [3, 6], we evaluate both methods using -quantile loss with ,

where is the empirical -quantile of the predictive distribution and is an indicator function.

Figure 4(b) presents the performance of DeepAR and Transformer on the synthetic datasets. When , both of them perform very well. But, as increases, especially when , the performance of DeepAR drops significantly while Transformer keeps its accuracy, suggesting that Transformer can capture fairly long-term dependencies when LSTM fails to do so.

5.2 Real-world datasets

We further evaluate our model on several real-world datasets. The electricity-f (fine) dataset consists of electricity consumption of 370 customers recorded every 15 minutes and the electricity-c (coarse) dataset is the aggregated electricity-f by every 4 points, producing hourly electricity consumption. Similarly, the traffic-f (fine) dataset contains occupancy rates of 963 freeway in San Francisco recorded every 20 minutes and the traffic-c (coarse) contains hourly occupancy rates by averaging every 3 points in traffic-f. The solar dataset666https://www.nrel.gov/grid/solar-power-data.html contains the solar power production records from January to August in 2006, which is sampled every hour from 137 PV plants in Alabama. The wind777https://www.kaggle.com/sohier/30-years-of-european-wind-generation dataset contains daily estimates of 28 countries’ energy potential from 1986 to 2015 as a percentage of a power plant’s maximum output. The M4-Hourly contains 414 hourly time series from M4 competition [24].

Long-term and short-term forecasting

We first show the effectiveness of canonical Transformer equipped with convolutional self-attention in long-term and short-term forecasting in electricity-c and traffic-c dataset. These two datasets exhibit both hourly and daily seasonal patterns. However, traffic-c demonstrates much greater difference between the patterns of weekdays and weekends compared to electricity-c. Hence, accurate forecasting in traffic-c dataset requires the model to capture both long- and short-term dependencies very well. As baselines, we use classical forecasting methods auto.arima, ets implemented in R’s forecast package and the recent matrix factorization method TRMF [17], a RNN-based autoregressive model DeepAR and a RNN-based state space model DeepState [6]. For short-term forecasting, we evaluate rolling-day forecasts for seven days ( i.e., prediction horizon is one day and forecasts start time is shifted by one day after evaluating the prediction for the current day [6]). For long-term forecasting, we directly forecast 7 days ahead. As shown in Table 1, our models with convolutional self-attention get betters results in both long-term and short-term forecasting, especially in traffic-c dataset compared to strong baselines, partly due to the long-term dependency modeling ability of Transformer as shown in our synthetic data.

| ARIMA | ETS | TRMF | DeepAR | DeepState | Ours | |

|---|---|---|---|---|---|---|

| e-c1d | 0.154/0.102 | 0.101/0.077 | 0.084/- | 0.075⋄/0.040⋄ | 0.083⋄/0.056⋄ | 0.059/0.034 |

| e-c7d | 0.283⋄/0.109⋄ | 0.121⋄/0.101⋄ | 0.087/- | 0.082/0.053 | 0.085⋄/0.052⋄ | 0.070/0.044 |

| t-c1d | 0.223/0.137 | 0.236/0.148 | 0.186/- | 0.161⋄/0.099⋄ | 0.167⋄/0.113⋄ | 0.122/0.081 |

| t-c7d | 0.492⋄/0.280⋄ | 0.509⋄/0.529⋄ | 0.202/- | 0.179/0.105 | 0.168⋄/0.114⋄ | 0.139/0.094 |

Convolutional self-attention

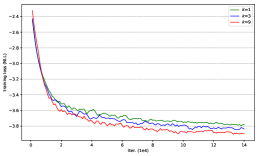

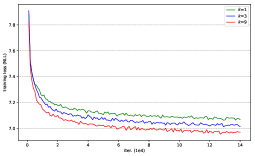

In this experiment, we conduct ablation study of our proposed convolutional self-attention. We explore different kernel size on the full attention model and fix all other settings. We still use rolling-day prediction for seven days on electricity-c and traffic-c datasets. The results of different kernel sizes on both datasets are shown in Table 2. On electricity-c dataset, models with kernel size obtain slightly better results in term of than canonical Transformer but overall these results are comparable and all of them perform very well. We argue it is because electricity-c dataset is less challenging and covariate vectors have already provided models with rich information for accurate forecasting. Hence, being aware of larger local context may not help a lot in such cases. However, on much more challenging traffic-c dataset, the model with larger kernel size can make more accurate forecasting than models with smaller ones with as large as relative improvement. These consistent gains can be the results of more accurate query-key matching by being aware of more local context. Further, to verify if incorporating more local context into query-key matching can ease the training, we plot the training loss of kernel size in electricity-c and traffic-c datasets. We found that Transformer with convolutional self-attention also converged faster and to lower training errors, as shown in Figure 5, proving that being aware of local context can ease the training process.

| electricity-c1d | 0.060/0.030 | 0.058/0.030 | 0.057/0.031 | 0.057/0.031 | 0.059/0.034 |

| traffic-c1d | 0.134/0.089 | 0.124/0.085 | 0.123/0.083 | 0.123/0.083 | 0.122/0.081 |

Sparse attention

Further, we compare our proposed LogSparse Transformer to the full attention counterpart on fine-grained datasets, electricity-f and traffic-f. Note that time series in these two datasets have much longer periods and are noisier comparing to electricity-c and traffic-c. We first compare them under the same memory budget. For electricity-f dataset, we choose with subsequence length and local attention length in each subsequence for our sparse attention model and in the full attention counterpart. For traffic-f dataset, we select with subsequence length and local attention length in each subsequence for our sparse attention model, and in the full attention counterpart. The calculation of memory usage and other details can be found in Appendix A.4. We conduct experiments on aforementioned sparse and full attention models with/without convolutional self-attention on both datasets. By following such settings, we summarize our results in Table 3 (Upper part). No matter equipped with convolutional self-attention or not, our sparse attention models achieve comparable results on electricity-f but much better results on traffic-f compared to its full attention counterparts. Such performance gain on traffic-f could be the result of the dateset’s stronger long-term dependencies and our sparse model’s better capability of capturing these dependencies, which, under the same memory budget, the full attention model cannot match. In addition, both sparse and full attention models benefit from convolutional self-attention on challenging traffic-f, proving its effectiveness.

To explore how well our sparse attention model performs compared to full attention model with the same input length, we set and on electricity-f and traffic-f, respectively. The results of their comparisons are summarized in Table 3 (Lower part). As one expects, full attention Transformers can outperform our sparse attention counterparts no matter they are equipped with convolutional self-attention or not in most cases. However, on traffic-f dataset with strong long-term dependencies, our sparse Transformer with convolutional self-attention can get better results than the canonical one and, more interestingly, even slightly outperform its full attention counterpart in term of , meaning that our sparse model with convolutional self-attention can capture long-term dependencies fairly well. In addition, full attention models under length constraint consistently obtain gains from convolutional self-attention on both electricity-f and traffic-f datasets, showing its effectiveness again.

| Constraint | Dataset | Full | Sparse | Full + Conv | Sparse + Conv |

|---|---|---|---|---|---|

| Memory | electricity-f1d | 0.083/0.051 | 0.084/0.047 | 0.078/0.048 | 0.079/0.049 |

| traffic-f1d | 0.161/0.109 | 0.150/0.098 | 0.149/0.102 | 0.138/0.092 | |

| Length | electricity-f1d | 0.082/0.047 | 0.084/0.047 | 0.074/0.042 | 0.079/0.049 |

| traffic-f1d | 0.147/0.096 | 0.150/0.098 | 0.139/0.090 | 0.138/0.092 |

Further Exploration

In our last experiment, we evaluate how our methods perform on datasets with various granularities compared to our baselines. All datasets except M4-Hourly are evaluated by rolling window 7 times since the test set of M4-Hourly has been provided. The results are shown in Table 4. These results further show that our method achieves the best performance overall.

| electricity-f1d | traffic-f1d | solar1d | M4-Hourly2d | wind30d | ||

|---|---|---|---|---|---|---|

| TRMF | 0.094/- | 0.213/- | 0.241/- | -/- | 0.311/- | |

| DeepAR | 0.082/0.063 | 0.230/0.150 | 0.222/0.093 | 0.090⋄/0.030⋄ | 0.286/0.116 | |

| Ours | 0.074/0.042 | 0.139/0.090 | 0.210 /0.082 | 0.067 /0.025 | 0.284/0.108 |

6 Conclusion

In this paper, we propose to apply Transformer in time series forecasting. Our experiments on both synthetic data and real datasets suggest that Transformer can capture long-term dependencies while LSTM may suffer. We also showed, on real-world datasets, that the proposed convolutional self-attention further improves Transformer’ performance and achieves state-of-the-art in different settings in comparison with recent RNN-based methods, a matrix factorization method, as well as classic statistical approaches. In addition, with the same memory budget, our sparse attention models can achieve better results on data with long-term dependencies. Exploring better sparsity strategy in self-attention and extending our method to better fit small datasets are our future research directions.

References

References

- [1] Ashish Vaswani, Noam Shazeer, Niki Parmar, Jakob Uszkoreit, Llion Jones, Aidan N Gomez, Łukasz Kaiser, and Illia Polosukhin. Attention is all you need. In Advances in neural information processing systems, pages 5998–6008, 2017.

- [2] James Durbin and Siem Jan Koopman. Time series analysis by state space methods. Oxford university press, 2012.

- [3] Valentin Flunkert, David Salinas, and Jan Gasthaus. Deepar: Probabilistic forecasting with autoregressive recurrent networks. arXiv preprint arXiv:1704.04110, 2017.

- [4] Alex Graves. Generating sequences with recurrent neural networks. arXiv preprint arXiv:1308.0850, 2013.

- [5] Ilya Sutskever, Oriol Vinyals, and Quoc V Le. Sequence to sequence learning with neural networks. In Advances in neural information processing systems, pages 3104–3112, 2014.

- [6] Syama Sundar Rangapuram, Matthias W Seeger, Jan Gasthaus, Lorenzo Stella, Yuyang Wang, and Tim Januschowski. Deep state space models for time series forecasting. In Advances in Neural Information Processing Systems, pages 7785–7794, 2018.

- [7] Guokun Lai, Wei-Cheng Chang, Yiming Yang, and Hanxiao Liu. Modeling long-and short-term temporal patterns with deep neural networks. In The 41st International ACM SIGIR Conference on Research & Development in Information Retrieval, pages 95–104. ACM, 2018.

- [8] Rose Yu, Stephan Zheng, Anima Anandkumar, and Yisong Yue. Long-term forecasting using tensor-train rnns. arXiv preprint arXiv:1711.00073, 2017.

- [9] Danielle C Maddix, Yuyang Wang, and Alex Smola. Deep factors with gaussian processes for forecasting. arXiv preprint arXiv:1812.00098, 2018.

- [10] Razvan Pascanu, Tomas Mikolov, and Yoshua Bengio. On the difficulty of training recurrent neural networks. In International conference on machine learning, pages 1310–1318, 2013.

- [11] Sepp Hochreiter and Jürgen Schmidhuber. Long short-term memory. Neural computation, 9(8):1735–1780, 1997.

- [12] Kyunghyun Cho, Bart Van Merriënboer, Dzmitry Bahdanau, and Yoshua Bengio. On the properties of neural machine translation: Encoder-decoder approaches. arXiv preprint arXiv:1409.1259, 2014.

- [13] Urvashi Khandelwal, He He, Peng Qi, and Dan Jurafsky. Sharp nearby, fuzzy far away: How neural language models use context. arXiv preprint arXiv:1805.04623, 2018.

- [14] Ankur P Parikh, Oscar Täckström, Dipanjan Das, and Jakob Uszkoreit. A decomposable attention model for natural language inference. arXiv preprint arXiv:1606.01933, 2016.

- [15] George EP Box and Gwilym M Jenkins. Some recent advances in forecasting and control. Journal of the Royal Statistical Society. Series C (Applied Statistics), 17(2):91–109, 1968.

- [16] George EP Box, Gwilym M Jenkins, Gregory C Reinsel, and Greta M Ljung. Time series analysis: forecasting and control. John Wiley & Sons, 2015.

- [17] Hsiang-Fu Yu, Nikhil Rao, and Inderjit S Dhillon. Temporal regularized matrix factorization for high-dimensional time series prediction. In Advances in neural information processing systems, pages 847–855, 2016.

- [18] Nicolas Chapados. Effective bayesian modeling of groups of related count time series. arXiv preprint arXiv:1405.3738, 2014.

- [19] Ruofeng Wen, Kari Torkkola, Balakrishnan Narayanaswamy, and Dhruv Madeka. A multi-horizon quantile recurrent forecaster. arXiv preprint arXiv:1711.11053, 2017.

- [20] Xiaoyong Jin, Shiyang Li, Yunkai Zhang, and Xifeng Yan. Multi-step deep autoregressive forecasting with latent states. URL http://roseyu.com/time-series-workshop/submissions/2019/timeseries-ICML19_paper_19.pdf, 2019.

- [21] Cheng-Zhi Anna Huang, Ashish Vaswani, Jakob Uszkoreit, Noam Shazeer, Curtis Hawthorne, Andrew M Dai, Matthew D Hoffman, and Douglas Eck. An improved relative self-attention mechanism for transformer with application to music generation. arXiv preprint arXiv:1809.04281, 2018.

- [22] Daniel Povey, Hossein Hadian, Pegah Ghahremani, Ke Li, and Sanjeev Khudanpur. A time-restricted self-attention layer for asr. In 2018 IEEE International Conference on Acoustics, Speech and Signal Processing (ICASSP), pages 5874–5878. IEEE, 2018.

- [23] Niki Parmar, Ashish Vaswani, Jakob Uszkoreit, Łukasz Kaiser, Noam Shazeer, Alexander Ku, and Dustin Tran. Image transformer. arXiv preprint arXiv:1802.05751, 2018.

- [24] Spyros Makridakis, Evangelos Spiliotis, and Vassilios Assimakopoulos. The m4 competition: Results, findings, conclusion and way forward. International Journal of Forecasting, 34(4):802–808, 2018.

- [25] Tomaso Poggio, Hrushikesh Mhaskar, Lorenzo Rosasco, Brando Miranda, and Qianli Liao. Why and when can deep-but not shallow-networks avoid the curse of dimensionality: a review. International Journal of Automation and Computing, 14(5):503–519, 2017.

- [26] Kunihiko Fukushima. Neocognitron: A self-organizing neural network model for a mechanism of pattern recognition unaffected by shift in position. Biological cybernetics, 36(4):193–202, 1980.

- [27] Hrushikesh N Mhaskar and Tomaso Poggio. Deep vs. shallow networks: An approximation theory perspective. Analysis and Applications, 14(06):829–848, 2016.

- [28] Diederik P Kingma and Jimmy Ba. Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980, 2014.

- [29] Aäron Van Den Oord, Sander Dieleman, Heiga Zen, Karen Simonyan, Oriol Vinyals, Alex Graves, Nal Kalchbrenner, Andrew W Senior, and Koray Kavukcuoglu. Wavenet: A generative model for raw audio. SSW, 125, 2016.

- [30] Anastasia Borovykh, Sander Bohte, and Cornelis W Oosterlee. Conditional time series forecasting with convolutional neural networks. arXiv preprint arXiv:1703.04691, 2017.

- [31] Scott Gray, Alec Radford, and Diederik P. Kingma. Gpu kernels for block-sparse weights. arXiv preprint arXiv:1711.09224, 2017.

- [32] Tim Cooijmans, Nicolas Ballas, César Laurent, Çağlar Gülçehre, and Aaron Courville. Recurrent batch normalization. arXiv preprint arXiv:1603.09025, 2016.

- [33] Rose Yu, Yaguang Li, Cyrus Shahabi, Ugur Demiryurek, and Yan Liu. Deep learning: A generic approach for extreme condition traffic forecasting. In Proceedings of the 2017 SIAM International Conference on Data Mining, pages 777–785. SIAM, 2017.

- [34] Guoqiang Zhang, B Eddy Patuwo, and Michael Y Hu. Forecasting with artificial neural networks:: The state of the art. International journal of forecasting, 14(1):35–62, 1998.

- [35] Rewon Child, Scott Gray, Alec Radford, and Ilya Sutskever. Generating long sequences with sparse transformers. arXiv preprint arXiv:1904.10509, 2019.

- [36] Peter J Liu, Mohammad Saleh, Etienne Pot, Ben Goodrich, Ryan Sepassi, Lukasz Kaiser, and Noam Shazeer. Generating wikipedia by summarizing long sequences. arXiv preprint arXiv:1801.10198, 2018.

- [37] Alec Radford, Karthik Narasimhan, Tim Salimans, and Ilya Sutskever. Improving language understanding by generative pre-training. URL https://s3-us-west-2. amazonaws. com/openai-assets/research-covers/languageunsupervised/language understanding paper. pdf, 2018.

- [38] Jacob Devlin, Ming-Wei Chang, Kenton Lee, and Kristina Toutanova. Bert: Pre-training of deep bidirectional transformers for language understanding. arXiv preprint arXiv:1810.04805, 2018.

- [39] Rewon Child, Scott Gray, Alec Radford, and Ilya Sutskever. Generating long sequences with sparse transformers. arXiv preprint arXiv:1904.10509, 2019.

- [40] Nikolay Laptev, Jason Yosinski, Li Erran Li, and Slawek Smyl. Time-series extreme event forecasting with neural networks at uber. In International Conference on Machine Learning, number 34, pages 1–5, 2017.

Appendix A Supplementary Materials

A.1 Proof of Theorem 1

Proof.

According to the attention strategy in LogSparse Transformer, in each layer, cell could attend to the cells with indicies in . To ensure that every cell receives the information from all its previous cells and itself, the number of stacked layers should satisfy that for . That is, and , there is a directed path with edges, where , . We prove the theorem by constructing a path from cell to cell , with length (number of edges) no larger than . Case is trivial, we only need to consider here. Consider the binary representation of , , where . Suppose is the subsequence and is the element of . A feasible path from to is . The length of this path is , which is no larger than . So

| (3) |

Furthermore, by reordering , we can generate multiple different paths from cell to cell . The number of feasible paths increases at a rate of along with . ∎

A.2 Training

| electricity-c | electricity-f | traffic-c | traffic-f | wind | solar | M4-Hourly | ||

| T | 32304 | 129120 | 4049 | 12435 | 10957 | 5832 | 748/1008 | |

| M | 370 | 370 | 963 | 963 | 28 | 137 | 414 | |

| S | 1 hour | 15 mins | 1 hour | 20 mins | 1 day | 1 hour | 1 hour |

To learn the model, we are given a time series dataset and its associated covariates , where is the length of all available observations and is the number of different time series. The dataset statistics is shown as Table 5. Following [3], we create training instances by selecting windows with fixed history length and forecasting horizon but varying the start point of forecasting from each of the original long time series. As a follow-up of [3], we sample training windows through weight sampling strategy in [3]. Note that during selecting training windows, data in the test set can never be accessed. As a result, we get a training dataset with sliding windows .

For positional encoding in Transformer, we use learnable position embedding. For covariates, following [3], we use all or part of year, month, day-of-the-week, hour-of-the-day, minute-of-the-hour, age and time-series-ID according to the granularities of datasets. age is the distance to the first observation in that time series [3]. Each of them except time series ID has only one dimension and is normalized to have zero mean and unit variance (if applicable). For time-series-ID, it has the same dimension as position embedding through ID embedding matrix so that they can be summed up (with broadcasting). The summation is then concatnated with aforementioned other covariates as the input of 1st layer in Transformer.

DeepAR [3] uses an encoder-decoder fashion, where the encoder is the same as the decoder and the final hidden state of the encoder is used to initialize the hidden state of the decoder. Such an architecture can be seen as a decoder-only network as the encoder and decoder are the same, where the objective is to predict the distribution of next point according to current input and last hidden state. Inspired by this observation, we use Transformer decoder-only mode [36] to model time series. Similar to [37], a fully-connected layer on the top of Transformer is stacked, which outputs the parameters of the probability distribution after scaling for the next time point with appropriate transformations. For example, for parameters requiring positivity, a softplus activation is applied. We use the same scale handling technique as in [3] to scale our input and output of our models. We refer readers to [3] for more details of scale handling. In our experiments, we use Gaussian likelihood since our training datasets are real-valued data. Note that one can also use other likelihood models, e.g. negative-binomial likelihood for positive count data. In synthetic datasets, we only count log-likelihood from to . On real-world datasets, we not only count log-likelihood from to , but also include the log-likelihood from to , similar to training in [3] and pre-training in [37].

During training, we use vanilla Adam optimizer [28] with early stopping except experiments on electricity-f and traffic-f to maximize the log-likelihood of each training instance. Our preliminary study show that training on these two datasets are very unstable with Adam. Rather, we found that BERTAdam [38] 888https://github.com/nlpdata/mrc_bert_baseline/blob/master/bert/optimization.py , a variant of Adam with warmup and learning rate annealing, can stabilize the training process on these two datasets.

For electricity-c and traffic-c, we take K training windows while for electricity-f and traffic-f, we select K and K training windows, respectively. For wind, M4-Hourly and solar, we choose K, K and K training windows, respectively. The window selection strategy is described above. For our Transformer models, all of them use heads and the dimension of position embedding and time series ID embedding are all 20. All of our models have 3 layers except experiments on electricity-f and traffic-f, where our models use 6 and 10 layers, respectively. The data before the forecast start time is used as the training set and split into two partitions. For each experiment on real-world datasets, we train our model on the first partition of the training set containing 90% of the data 5 times with different random seeds and we pick the one that has the minimal negative log-likelihood on the remaining 10%. The results on test set corresponding to minimal negative log-likelihood on the remaining 10% are reported. All models are trained on GTX 1080 Ti GPUs.

A.3 Evaluation

Following the experimental settings in [6], one week data from 9/1/2014 00:00 (included) 999Value in 00:00 is the aggregation of original value in 00:15, 00:30, 00:45 and 01:00. on electricity-c and 6/15/2008 17:00 (included) 101010Value in 17:00 is the mean of original value in 17:00, 17:10, 17:20, 17:30, 17:40 and 17:50. on traffic-c is left as test sets. For electricity-f and traffic-f datasets, one week data from 8/31/2014 00:15 (included) and 6/15/2008 17:00 (included) 111111Value in 17:00 is the mean of original value in 17:00 and 17:10. is left as test sets, respectively. For solar, we leave the last 7 days in August as test set. For wind, last 210 days in year 2015 are left as test set. For M4-Hourly, its training and test set are already provided. After training on previous settings, we evaluate our models on aforementioned test intervals and report standard quantile loss ( and ) on the test sets.

A.4 Implementation of sparse attention and its memory cost

During the implementation of our sparse attention, , one can allow such cell to densely attend all its past cells and itself without increasing space usage as query-key matching are parallelly computed in reality and maximum number of cells that a cell can attend is reached by cell .

Our current implementation of LogSparse attention is via a mask matrix and its relative memory usage is calculated ideally from the attention matrix, which is the memory bottleneck of Transformer.

For electricity-f dataset, we choose with subsequence length and local attention length in each subsequence for our sparse attention model, and in its full attention counterpart. We stack the same layers on both sparse attention and full attention models. Hence, we can make sure that their whole memory usage is comparable if their memory usage is comparable in every layer. In sparse attention equipped with local attention, every cell attends to cells in each subsequence at most, causing a cell attend to cells at most in total. Therefore, we get the memory usage of sparse attention in each layer is . Following such setting, the memory usage of the sparse attention model is comparable to that of the full attention model. For traffic-f dataset, one can follow the same procedure to check the memory usage.

A.5 Visualization of attention matrix

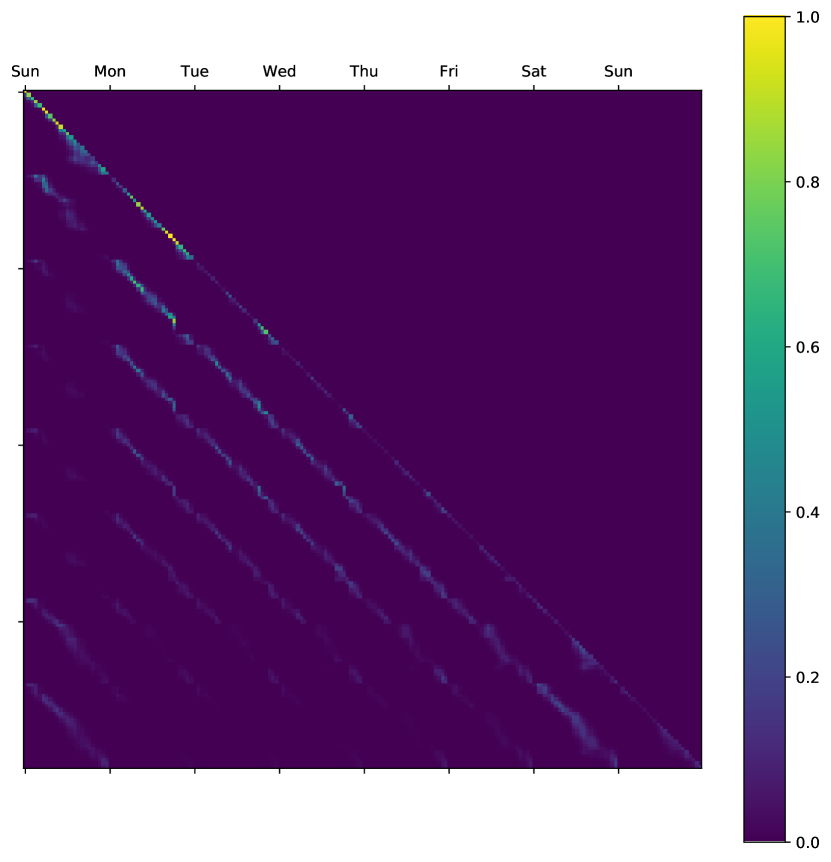

Here we show an example of learned attention patterns in the masked attention matrix of a head within canonical Transformer’s last layer on traffic-c dataset. Figure 6 (a) is a time series window containing 8 days in traffic-c . The time series obviously demonstrates both hourly and daily patterns. From its corresponding masked attention matrix, as shown in Figure 6 (b), we can see that for points in weekdays, they heavily attend to previous cells (including itself) at the same time in weekdays while points on weekends tend to only attend to previous cells (including itself) at the same time on weekends. Hence, the model automatically learned both hourly and daily seasonality, which is the key to accurate forecasting.