Asymptotic Network Independence in

Distributed Stochastic Optimization for Machine Learning 111The research was partially supported by the NSF under grants ECCS-1933027, IIS-1914792,

DMS-1664644, and CNS-1645681, by the

ONR under grant N00014-19-1-2571, by the NIH under grant 1R01GM135930, and by the SRIBD Startup Fund JCYJ-SP2019090001. (Corresponding author: Shi Pu.)

Abstract

We provide a discussion of several recent results which, in certain scenarios, are able to overcome a barrier in distributed stochastic optimization for machine learning. Our focus is the so-called asymptotic network independence property, which is achieved whenever a distributed method executed over a network of nodes asymptotically converges to the optimal solution at a comparable rate to a centralized method with the same computational power as the entire network. We explain this property through an example involving the training of ML models and sketch a short mathematical analysis for comparing the performance of distributed stochastic gradient descent (DSGD) with centralized stochastic gradient decent (SGD).

1 Introduction: Distributed Optimization and Its Limitations

First-order optimization methods, ranging from vanilla gradient descent to Nesterov acceleration and its many variants, have emerged over the past decade as the principal way to train Machine Learning (ML) models. There is a great need for techniques to train such models quickly and reliably in a distributed fashion over networks where the individual processors or GPUs may be scattered across the globe and communicate over an unreliable network which may suffer from message losses, delays, and asynchrony (see [2, 29, 1, 33]).

Unfortunately, what often happens is that the gains from having many different processors running an optimization algorithm are squandered by the cost of coordination, shared memory, message losses and latency. This effect is especially pronounced when there are many processors and they are spread across geographically distributed data centers. As is widely recognized by the distributed systems community, “throwing” more processors at a problem will not, after a certain point, result in better performance.

This is typically reflected in the convergence time bounds obtained for distributed optimization in the literature. The problem formulation is that one must solve

| (1) |

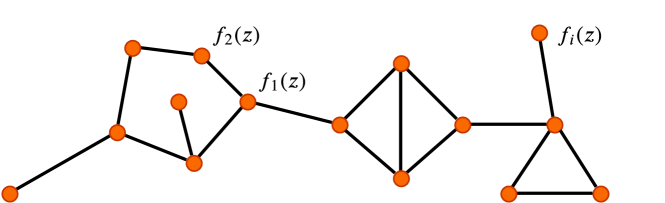

over a network of nodes (see Figure 1 for an example).

Only node has knowledge of the function , and the standard assumption is that, at every step when it is awake, node can compute the (stochastic) gradient of its own local function . These functions are assumed to be convex. The problem is to compute this minimum in a distributed manner over the network based on peer-to-peer communication, possible message losses, delays, and asynchrony.

This relatively simple formulation captures a large variety of learning problems. Suppose each agent stores training data points , where are vectors of features and are the associated responses (either discrete or continuous). We are interested to learn a predictive model , parameterized by parameters , so that for all . In other words, we are looking for a model that fits all the data throughout the network. This can be accomplished by empirical risk minimization

| (2) |

where

measures how well the parameter fits the data at node , with being a loss function measuring the difference between and . Much of modern machine learning is built around such a formulation, including regression, classification, and regularized variants [7].

It is also possible that each agent does not have a static dataset, but instead collects streaming data points repetitively over time, where represents an unknown distribution of . In this case we can find through expected risk minimization

| (3) |

where

This paper is concerned with the current limitations of distributed optimization and how to get past them in certain scenarios. To illustrate our main concern, let us consider the distributed subgradient method in the simplest possible setting, namely the problem of computing the median of a collection of numbers in a distributed manner over a fixed graph. Each agent in the network holds value , and the global objective is to find the median of . This can be incorporated in the framework of (1) by choosing

The distributed subgradient method (see [18]) uses the subgradients of at any point , to have agent update as

| (4) |

where denotes the stepsize at iteration , and are the weights agent assigns to agent ’s solutions: two agents and are able to exchange information if and only if ( otherwise). The weights are assumed to be symmetric. For comparison, the centralized subgradient method updates the solution at iteration according to

| (5) |

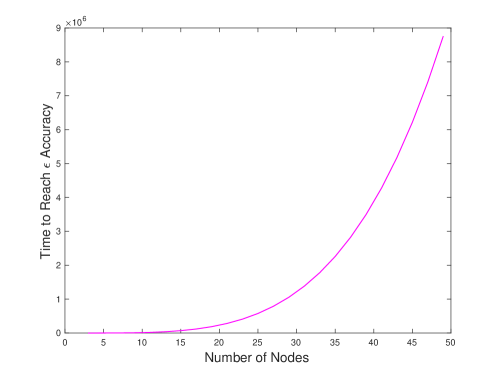

In Figure 2, we show the performance of Algorithm (4) as a function of the network size assuming the agents communicate over a ring network. As can be clearly seen, when the network size grows it takes a longer time for the algorithm to reach a certain performance threshold.

Clearly, this is an undesirable property. Glancing at the figure, we see that distributing computation over nodes can result in a convergence time on the order of iterations. Few practitioners will be enthusiastic about distributed optimization if the final effect is vastly increased convergence time.

One might hope that this phenomenon, demonstrated for the problem of median computation – considered here because it is arguably the simplest problem to which one can apply the subgradient method – will not hold for the more sophisticated optimization problems in the ML literature. Unfortunately, most work in distributed optimization replicates this undesirable phenomenon. We next give an extremely brief discussion of known convergence times in the distributed setting (for a much more extended discussion, we refer the reader to the recent survey [17]).

We would like to confine our discussion to the following point: most known convergence times in the distributed optimization literature imply bounds of the form

| (6) |

where denotes the time for the decentralized algorithm on nodes to reach accuracy (error ), and is the time for the centralized algorithm which can query gradients per time step to reach the same level of accuracy. The graph consists of the set of nodes and edges in the network, denoted by and , respectively. The function can usually be bounded in terms of some polynomial in the number of nodes .

For instance, in the subgradient methods, Corollary 9 of [17] implies that

where are initial estimates, denotes the optimal solution and bounds the -norm of the subgradients. The function is the inverse of the spectral gap corresponding to the graph, and will typically grow with ; hence, when is large, . In particular if the communication graphs are 1) path graphs, then ; 2) star graphs, then ; 3) geometric random graphs, then . The method developed in [20] achieves , but typically is at least .

By comparing and , we are keeping the computational power the same in both cases. Naturally, the centralized is always better: anything that can be done in a decentralized way could be done in a centralized way. The question, though, is how much better.

Framed in this way, the polynomial scaling in the quantity is extremely disconcerting. It is hard, for example, to argue that an algorithm should be run in a distributed manner with, say, if the quantity in Eq. (6) satisfies ; that would imply the distributed variant would be times slower than the centralized one with the same computational power.

Sometimes is written as the inverse spectral gap in terms of the second-eigenvalue of some matrix. Because the second-smallest eigenvalue of an undirected graph Laplacian is approximately away from zero, such bounds will translate into at least quadratic scalings with in the worst-case. Over time-varying -connected graphs, the best-known bounds on will be cubic in using the results of [16].

There are a number of caveats to the pessimistic argument outlined above. For example, in a multi-agent scenario where data sharing is not desirable or feasible, decentralized computation might be the only available option. Generally speaking, however, fast-growing will preclude the widespread applicability of distributed optimization. Indeed, returning to the back-of-the-envelope calculation above, if a user has to pay a multiplicative factor of 10,000 in convergence speed to use an algorithm, the most likely scenario is that the algorithm will not be used.

There are some scenarios which avoid the pessimistic discussion above: for example, when the underlying graph is an expander, the associated spectral gap is constant (see Chapter 6 of [8] for a definition of these terms as well as an explanation), and likewise when the graph is a star graph. In particular, on a random Erdős-Rényi random graph, the quantity is constant with high probability (Corollary 9, part 9 in [17]). Unfortunately, these are very special cases which may not always be realistic. A star graph requires a single node to have the ability to receive and broadcast messages to all other nodes in the system. On the other hand, an expander graph may not occur in geographically distributed systems. By way of comparison, a random graph where nodes are associated with random locations, with links between nodes close together, will not have constant spectral gap and will thus have that grows with (Corollary 9, part 10 of [17]). The Erdős-Rényi graph escapes this because, if we again associate nodes with locations, the average link in such a graph is a “long range” one connecting nodes that are geographically far apart. It is a consequence of Cheeger’s inequality that graphs based on connecting nearest neighbors (i.e., where nodes are regularly spaced in and each node is connected to a constant number of closest neghbors) will not have constant spectral gap.

2 Asymptotic Network Independence in Distributed Stochastic Optimization

In this paper, we provide a discussion of several recent papers which have obtained that, for a number of settings involving distributed stochastic optimization, , as long as is large enough. In other words, asymptotically, the distributed stochastic gradient algorithm converges to the optimal solution at a comparable rate to a centralized algorithm with the same computational power.

We call this property asymptotic network independence: it is as if the network is not even there. Asymptotic network independence provides an answer to the concerns raised in the previous section.

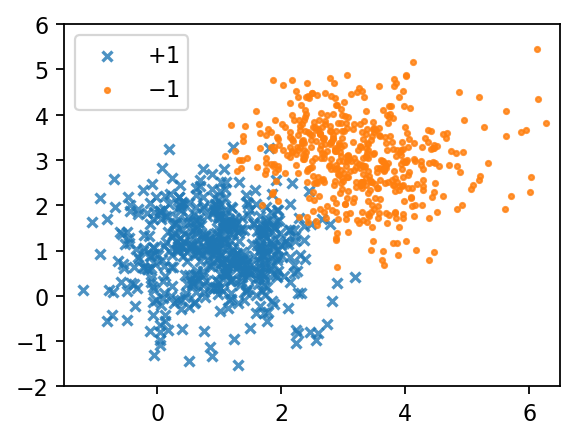

We begin by illustrating these results with a simulation from [21], shown in Figure 3. Here the problem to be solved is classification with a smooth support vector machine between overlapping clusters of points. The performance of the centralized algorithm is shown in orange, and the performance of the decentralized algorithm is shown in dark blue. The graph is a ring of 50 nodes, and the problem being solved is the search for a support vector classifier. The graph illustrates the main result, which is that a network of 50 nodes performs as well in the limit as a centralized method with 50 times the computational power of one node. Indeed, after iterations the orange and dark blue lines are almost indistinguishable.

We mention that similar simulations are available for other machine learning methods (training neural networks, logistic regression, elastic net regression, etc.). The asymptotic network independence property enables us to efficiently distribute the training process for a variety of existing learning methods.

The name “asymptotic network independence” is a slight misnomer, as we actually do not care if the asymptotic performance depends in some complicated way on the network. All we want is that the decentralized convergence rate can be bounded by times the convergence rate of the centralized method.

The papers [4, 5, 6, 31] gave the first crisp statement of the relationship between centralized and distributed methods in the setting of distributed optimization of smooth strongly convex functions in the presence of noise. Under constant stepsizes, the papers [4, 5, 6] were the first to show that when the stepsize is sufficiently small, a distributed stochastic gradient method achieves comparable performance to a centralized method in terms of the steady-state mean-square-error. The stepsize has to be small enough as a function of the network topology for this to hold. The paper [31] showed that the distributed stochastic gradient algorithm asymptotically achieves comparable convergence rate to a centralized method, but assuming that all the local functions have the same minimum. This gives the first “asymptotic network independence” result.222In this survey, all the mentioned algorithms that enjoy the asymptotic network independence property assume smooth objective functions, i.e., functions with Lipschitz continuous gradients.

The work in [22] approximated distributed stochastic gradient descent by stochastic differential equations in continuous time by assuming sufficiently small constant stepsize. It was shown that the distributed method outperforms a centralized scheme with synchronization overhead. However, it did not lead to straightforward algorithmic bounds. In our recent work [21], we generalized the results to graphs which are time-varying, with delays, message losses, and asynchrony. In a parallel recent work [9], a similar result was demonstrated with a further compression technique which allowed nodes to save on communication.

When the objective functions are not assumed to be convex, several recent works have obtained asymptotic network independence for distributed stochastic gradient descent. In [13, 14], a general stochastic approximation setting was considered with decaying step-sizes, and the convergence rates of centralized and distributed methods were shown to be asymptotically the same; the proof proceeded based on certain technical properties of stochastic approximation methods. The work in [12] was the first to show that distributed algorithms could achieve a speedup like a centralized method when the number of computing steps is large enough. Such a result was generalized to the setting of directed communication networks in [1] for training deep neural networks, where the push-sum technique was combined with the standard distributed stochastic gradient scheme.

In the rest of this section, we will give a simple and readable explanation of the asymptotic network independence phenomenon in the context of distributed stochastic optimization over smooth and strongly convex objective functions. 333For more references on the topic of distributed stochastic optimization, the readers may refer to [15, 10, 28, 30, 24, 23, 32] and the references therein.

2.1 Setup

We are interested in minimizing Eq. (1) over a network of communicating agents. Regarding the objective functions we make the following standing assumption.

Assumption 1

Each is -strongly convex with -Lipschitz continuous gradients, i.e., for any ,

| (7) |

Under Assumption 1, Problem (1) has a unique optimal solution , and the function defined as

has the following contraction property (see [26] Lemma 10).

Lemma 1

For any and , we have .

In other words, gradient descent with a small stepsize reduces the distance between the current solution and .

In the stochastic optimization setting, we assume that at each iteration of the algorithm, being the input for agent , each agent is able to obtain noisy gradient estimates that satisfy the following condition.

Assumption 2

For all and , each random vector is independent, and

| (8) |

Stochastic gradients appear, for instance, when the gradient estimation of in empirical risk minimization (2) introduces noise from various sources, such as sampling and quantization errors. For another example, when minimizing the expected risk in (3), where independent data points are gathered over time, is a stochastic, unbiased estimator of satisfying the first condition in (8). The second condition holds for popular problems such as smooth Support Vector Machines, logistic regression and softmax regression assuming the domain of is bounded.

The algorithm we discuss is the Distributed Stochastic Gradient Descent (DSGD) method adapted from DGD and the diffusion strategy [3]; note that in [3] this method was called “Adapt-then-Combine”. We let each agent in the network hold a local copy of the decision vector denoted by , and its value at iteration/time is written as . Denote for short. At each step , every agent performs the following update:

| (9) |

where is a sequence of nonnegative non-increasing stepsizes. The initial vectors are arbitrary for all , and is a mixing matrix.

DSGD belongs to the class of so-called consensus-based distributed optimization methods, where different agents mix their estimates at each iteration to reach a consensus of the solutions, i.e., for all and in the long run. To achieve consensus, the following condition is assumed on the mixing matrix and the communication topology among agents.

Assumption 3

The graph of agents is undirected and connected (there exists a path between any two agents). The mixing matrix is nonnegative, symmetric and doubly stochastic, i.e., and , where is the all one vector. In addition, for some .

Some examples of undirected connected graphs are presented in Figure 4 below.

Because of Assumption 3, the mixing matrix has an important contraction property.

Lemma 2

As a result, when running a consensus algorithm (which is just (9) without gradient descent)

| (10) |

the speed of reaching consensus is determined by . In particular, if we adopt the so-called lazy Metropolis rule for defining the weights, the dependency of on the network size is upper bounded by for some constant [20].

Lazy Metropolis rule for constructing : Notation: denotes the degree (number of “neighbors”) of node . Correspondingly, is the set of “neighbors” for agent .

Despite the fact that may be very close to with large , the consensus algorithm (10) enjoys geometric convergence speed, i.e.,

By contrast, the optimal rate of convergence for any stochastic gradient methods is sublinear, asymptotically (see [19]). This difference suggests that a consensus-based distributed algorithm for stochastic optimization may match the centralized methods in the long term: any errors due to consensus will decay at a fast-enough rate so that they ultimately do not matter.

In what follows, we discuss and compare the performance of the centralized stochastic gradient descent (SGD) method and DSGD. We will show that both methods asymptotically converge at the rate . Furthermore, the time needed for DSGD to approach the asymptotic convergence rate turns out to scale as .

2.2 Centralized Stochastic Gradient Descent (SGD)

The benchmark for evaluating the performance of DSGD is the centralized stochastic gradient descent (SGD) method, which we now describe. At each iteration , the following update is executed:

| (11) |

where stepsizes satisfy , and , i.e., is the average of noisy gradients evaluated at (by utilizing gradients at each iteration, we are keeping the computational power the same for SGD and DSGD). As a result, the gradient estimation is more accurate than using just one gradient. Indeed, from Assumption 2 we have

| (12) |

2.3 Distributed Stochastic Gradient Descent (DSGD)

We assume the same stepsize policy for DSGD and SGD. To analyze DSGD starting from Eq. (9), define

| (15) |

as the average of all the iterates in the network. Differently from the analysis for SGD, we will be concerned with two error terms. The first term , called the expected optimization error, defines the expected squared distance between and , and the second term , called the expected consensus error, measures the dissimilarities of individual estimates among all the agents. The average squared distance between individual iterate and the optimum is given by

| (16) |

Hence, exploring the two terms will provide us with insights into the performance of DSGD. To simplify notation, denote , , .

Inspired by the analysis for SGD, we first look for an inequality that bounds , which is analogous to in SGD. One such relation turns out to be [25]:

| (17) |

Comparing (17) to (14), we find two additional terms on the right-hand side of the inequality. Both terms involve the expected consensus error , thus reflecting the additional disturbances caused by the dissimilarities of solutions. Relation (17) also suggests that the convergence rate of can not be better than for SGD, which is expected. Nevertheless, if decays fast enough compared to , it is likely that the two additional terms are negligible in the long run, and we would guess that the convergence rate of is comparable to for SGD.

This indeed turns out to be the case, as it is shown in [25] that for . Plugging this into Eq. (17) leads to the inequality . Hence, when ,we have that

In other words, we have the asymptotic network independence phenomenon: after a transient, DSGD performs comparably to a centralized stochastic gradient descent method with the same computational power (e.g., which can query the same number of gradients per step as the entire network).

2.4 Numerical Illustration

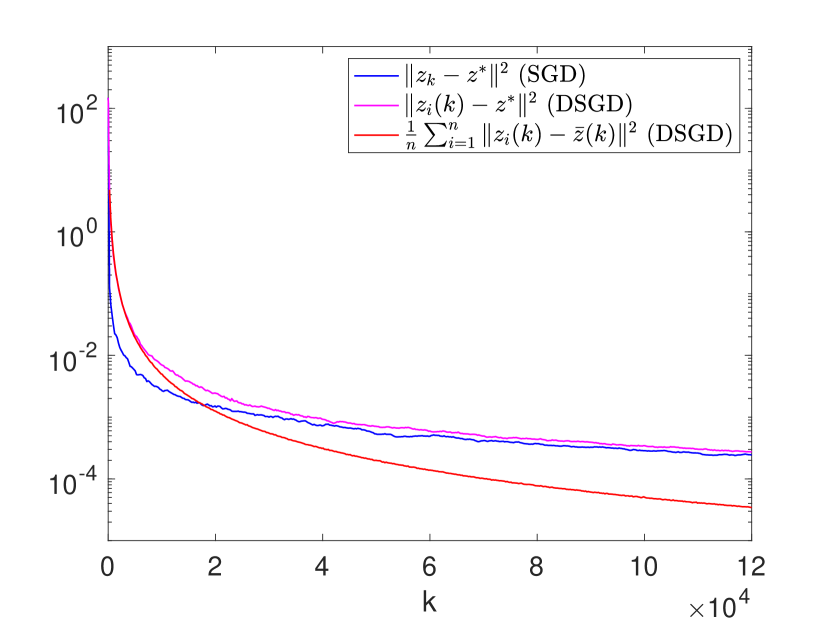

We provide a numerical example to illustrate the asymptotic network independence property of DSGD. Consider the on-line Ridge regression problem

| (18) |

where is a penalty parameter. Each agent collects data points in the form of continuously over time with representing the features and being the observed outputs. Suppose each is uniformly distributed, and is drawn according to , where are predefined parameters uniformly situated in , and are independent Gaussian random variables with mean and variance . Given a pair , agent can compute an estimated gradient of : , which is unbiased. Problem (18) has a unique solution given by .

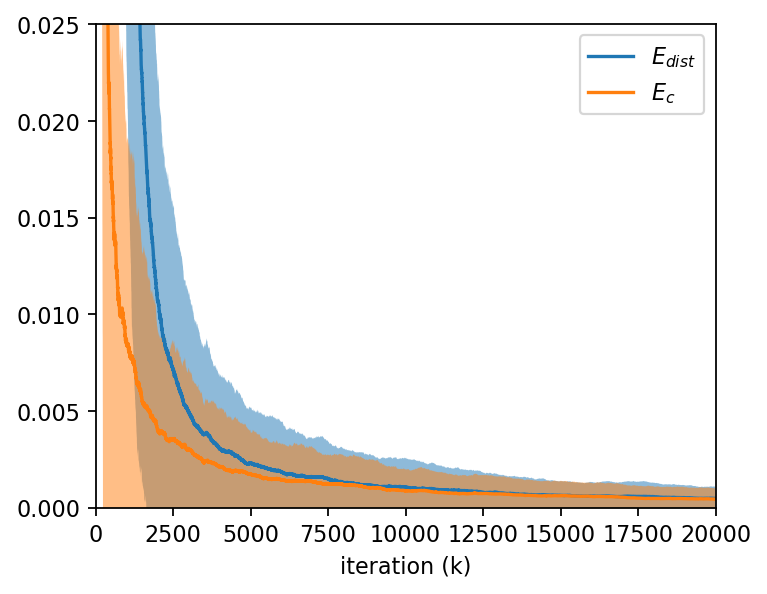

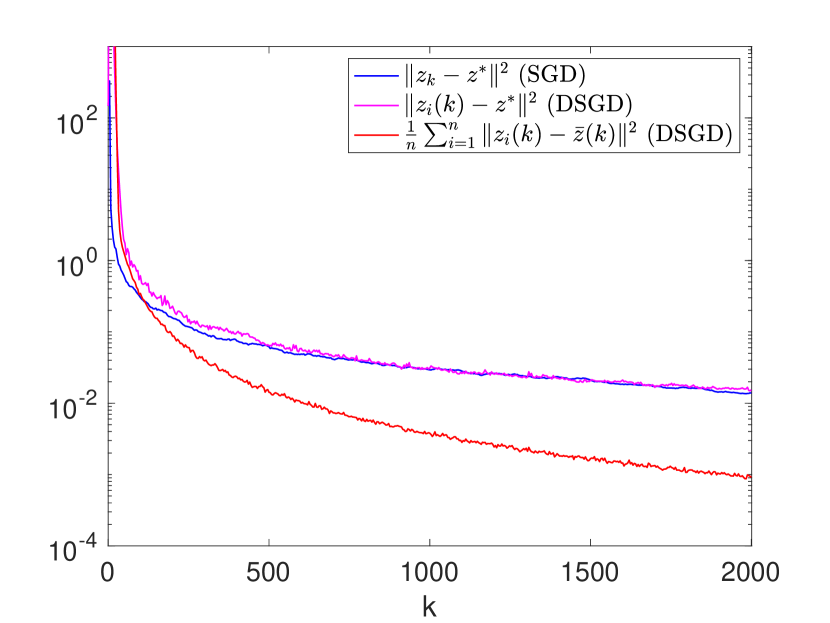

In the experiments, we consider two instances. In the first instance, we assume agents constitute a random network for DSGD, where every two agents are linked with probability . In the second instance, we let agents form a grid network. We use Metropolis weights in both instances. The problem dimension is set to and , the zero vector, for all . The penalty parameter is set to and the stepsizes . For both SGD and DSGD, we run the simulations times and average the results to approximate the expected errors.

The performance of SGD and DSGD is shown in Figure 5. We notice that in both instances the expected consensus error for DSGD converges to faster than the expected optimization error as predicted from our previous discussion. Regarding the expected optimization error, DSGD is slower than SGD in the first (resp., ) iterations for random network (resp., grid network). But after that, their performance is almost indistinguishable. The difference in the transient times is due to the stronger connectivity (or smaller ) of the random network compared to the grid network.

3 Conclusions

In this paper, we provided a discussion of recent results which have overcome a barrier in distributed stochastic optimization methods for machine learning under certain scenarios. These results established an asymptotic network independence property, that is, asymptotically, the distributed algorithm achieves comparable convergence rate to a centralized algorithm with the same computational power. We explain the property by examples of training ML models and provide a short mathematical analysis.

Along the line of achieving asymptotic network independence in distributed optimization, there are various future research directions, including considering nonconvex objective functions, reducing communication costs and transient time, and using exact gradient information. We next briefly discuss these.

First, distributed training of deep neural networks — the state-of-the-art machine learning approach in many application areas — involves minimizing nonconvex objective functions which are different from the main objectives considered in this paper. This area is largely unexplored with a few recent works in [14, 12, 29, 1].

In distributed algorithms, the costs associated with communication among the agents are often non-negligible and may become the main burden for large networks. It is therefore important to explore communication reduction techniques that do not sacrifice the asymptotic network independence property. The recent papers [1, 9] touched upon this point.

When considering asymptotic network independence for distributed optimization, an important factor is the transient time to reach the asymptotic convergence rate, as it may take a long time before the distributed implementation catches up with the corresponding centralized method. In fact, as we have shown in Section 2.1, this transient time can be a function of the network topology and grows with the network size. Reducing the transient time is thus a key future objective.

Finally, while several recent works have established the asymptotic network independence property in distributed optimization, they are mainly constrained to using stochastic gradient information. If the exact gradient is available, can distributed methods compete with the centralized ones? As we know, centralized algorithms typically enjoy a faster convergence speed with exact gradients. For example, plain gradient descent achieves linear convergence for strongly convex and smooth objective functions. To the best of the authors’ knowledge, as of writing this survey, with the exception of [11, 29], results on asymptotic network independence in this setting are currently lacking.

Acknowledgments

We would like to thank Artin Spiridonoff from Boston University for his kind help in providing Figure 3.

References

- [1] M. Assran, N. Loizou, N. Ballas, and M. Rabbat. Stochastic gradient push for distributed deep learning. In International Conference on Machine Learning, pages 344–353, 2019.

- [2] T. S. Brisimi, R. Chen, T. Mela, A. Olshevsky, I. C. Paschalidis, and W. Shi. Federated learning of predictive models from federated electronic health records. International Journal of Medical Informatics, 112:59–67, 2018.

- [3] J. Chen and A. H. Sayed. Diffusion adaptation strategies for distributed optimization and learning over networks. IEEE Transactions on Signal Processing, 60(8):4289–4305, 2012.

- [4] J. Chen and A. H. Sayed. On the limiting behavior of distributed optimization strategies. In 2012 50th Annual Allerton Conference on Communication, Control, and Computing (Allerton), pages 1535–1542. IEEE, 2012.

- [5] J. Chen and A. H. Sayed. On the learning behavior of adaptive networks—part i: Transient analysis. IEEE Transactions on Information Theory, 61(6):3487–3517, 2015.

- [6] J. Chen and A. H. Sayed. On the learning behavior of adaptive networks—part ii: Performance analysis. IEEE Transactions on Information Theory, 61(6):3518–3548, 2015.

- [7] R. Chen and I. C. Paschalidis. A robust learning approach for regression models based on distributionally robust optimization. The Journal of Machine Learning Research, 19(1):517–564, 2018.

- [8] R. Durrett. Random Graph Dynamics, volume 200. Cambridge university press Cambridge, 2007.

- [9] A. Koloskova, S. U. Stich, and M. Jaggi. Decentralized stochastic optimization and gossip algorithms with compressed communication. Proceedings of Machine Learning Research, 97(CONF), 2019.

- [10] G. Lan, S. Lee, and Y. Zhou. Communication-efficient algorithms for decentralized and stochastic optimization. Mathematical Programming, pages 1–48, 2017.

- [11] Z. Li, W. Shi, and M. Yan. A decentralized proximal-gradient method with network independent step-sizes and separated convergence rates. IEEE Transactions on Signal Processing, 67(17):4494–4506, 2019.

- [12] X. Lian, C. Zhang, H. Zhang, C.-J. Hsieh, W. Zhang, and J. Liu. Can decentralized algorithms outperform centralized algorithms? a case study for decentralized parallel stochastic gradient descent. In Advances in Neural Information Processing Systems, pages 5336–5346, 2017.

- [13] G. Morral, P. Bianchi, and G. Fort. Success and failure of adaptation-diffusion algorithms for consensus in multi-agent networks. In 53rd IEEE Conference on Decision and Control, pages 1476–1481. IEEE, 2014.

- [14] G. Morral, P. Bianchi, and G. Fort. Success and failure of adaptation-diffusion algorithms with decaying step size in multiagent networks. IEEE Transactions on Signal Processing, 65(11):2798–2813, 2017.

- [15] A. Nedić and A. Olshevsky. Stochastic gradient-push for strongly convex functions on time-varying directed graphs. IEEE Transactions on Automatic Control, 61(12):3936–3947, 2016.

- [16] A. Nedic, A. Olshevsky, A. Ozdaglar, and J. N. Tsitsiklis. On distributed averaging algorithms and quantization effects. IEEE Transactions on Automatic Control, 54(11):2506–2517, 2009.

- [17] A. Nedić, A. Olshevsky, and M. Rabbat. Network topology and communication-computation tradeoffs in decentralized optimization. Proceedings of the IEEE, 106(5):953–976, 2018.

- [18] A. Nedic and A. Ozdaglar. Distributed subgradient methods for multi-agent optimization. IEEE Transactions on Automatic Control, 54(1):48–61, 2009.

- [19] A. Nemirovski, A. Juditsky, G. Lan, and A. Shapiro. Robust stochastic approximation approach to stochastic programming. SIAM Journal on Optimization, 19(4):1574–1609, 2009.

- [20] A. Olshevsky. Linear time average consensus and distributed optimization on fixed graphs. SIAM Journal on Control and Optimization, 55(6):3990–4014, 2017.

- [21] A. Olshevsky, I. C. Paschalidis, and A. Spiridonoff. Robust asynchronous stochastic gradient-push: asymptotically optimal and network-independent performance for strongly convex functions. arXiv preprint arXiv:1811.03982, 2018.

- [22] S. Pu and A. Garcia. A flocking-based approach for distributed stochastic optimization. Operations Research, 66(1):267–281, 2017.

- [23] S. Pu and A. Garcia. Swarming for faster convergence in stochastic optimization. SIAM Journal on Control and Optimization, 56(4):2997–3020, 2018.

- [24] S. Pu and A. Nedić. Distributed stochastic gradient tracking methods. arXiv preprint arXiv:1805.11454, 2018.

- [25] S. Pu, A. Olshevsky, and I. C. Paschalidis. A non-asymptotic analysis of network independence for distributed stochastic gradient descent. arXiv preprint arXiv:1906.02702, 2019.

- [26] G. Qu and N. Li. Harnessing smoothness to accelerate distributed optimization. IEEE Transactions on Control of Network Systems, 2017.

- [27] A. Rakhlin, O. Shamir, and K. Sridharan. Making gradient descent optimal for strongly convex stochastic optimization. In Proceedings of the 29th International Coference on International Conference on Machine Learning, pages 1571–1578. Omnipress, 2012.

- [28] M. O. Sayin, N. D. Vanli, S. S. Kozat, and T. Başar. Stochastic subgradient algorithms for strongly convex optimization over distributed networks. IEEE Transactions on Network Science and Engineering, 4(4):248–260, 2017.

- [29] K. Scaman, F. Bach, S. Bubeck, Y. T. Lee, and L. Massoulié. Optimal convergence rates for convex distributed optimization in networks. Journal of Machine Learning Research, 20(159):1–31, 2019.

- [30] B. Sirb and X. Ye. Decentralized consensus algorithm with delayed and stochastic gradients. SIAM Journal on Optimization, 28(2):1232–1254, 2018.

- [31] Z. J. Towfic, J. Chen, and A. H. Sayed. Excess-risk of distributed stochastic learners. IEEE Transactions on Information Theory, 62(10):5753–5785, 2016.

- [32] R. Xin, U. A. Khan, and S. Kar. Variance-reduced decentralized stochastic optimization with gradient tracking. arXiv preprint arXiv:1909.11774, 2019.

- [33] B. Ying, K. Yuan, and A. H. Sayed. Supervised learning under distributed features. IEEE Transactions on Signal Processing, 67(4):977–992, 2018.