lemmatheorem \aliascntresetthelemma \newaliascntcorollarytheorem \aliascntresetthecorollary \newaliascntpropositiontheorem \aliascntresettheproposition \newaliascntdefinitiontheorem \aliascntresetthedefinition \newaliascntremarktheorem \aliascntresettheremark

Efficient stochastic optimisation by unadjusted Langevin Monte Carlo. Application to maximum marginal likelihood and empirical Bayesian estimation.

Abstract

Stochastic approximation methods play a central role in maximum likelihood estimation problems involving intractable likelihood functions, such as marginal likelihoods arising in problems with missing or incomplete data, and in parametric empirical Bayesian estimation. Combined with Markov chain Monte Carlo algorithms, these stochastic optimisation methods have been successfully applied to a wide range of problems in science and industry. However, this strategy scales poorly to large problems because of methodological and theoretical difficulties related to using high-dimensional Markov chain Monte Carlo algorithms within a stochastic approximation scheme. This paper proposes to address these difficulties by using unadjusted Langevin algorithms to construct the stochastic approximation. This leads to a highly efficient stochastic optimisation methodology with favourable convergence properties that can be quantified explicitly and easily checked. The proposed methodology is demonstrated with three experiments, including a challenging application to high-dimensional statistical audio analysis and a sparse Bayesian logistic regression with random effects problem.

1 Introduction

Maximum likelihood estimation (MLE) is central to modern statistical science. It is a cornerstone of frequentist inference [7], and also plays a fundamental role in parametric empirical Bayesian inference [11, 13]. For simple statistical models, MLE can be performed analytically and exactly. However, for most models, it requires using numerical computation methods, particularly optimisation schemes that iteratively seek to maximise the likelihood function and deliver an approximate solution. Following decades of active research in computational statistics and optimisation, there are now several computationally efficient methods to perform MLE in a wide range of classes of models [32, 8].

In this paper we consider MLE in models involving incomplete or “missing” data, such as hidden, latent or unobserved variables, and focus on Expectation Maximisation (EM) optimisation methods [18], which are the predominant strategy in this setting . While the original EM optimisation methodology involved deterministic steps, modern EM methods are mainly stochastic [49]. In particular, they typically rely on a Robbins-Monro stochastic approximation (SA) scheme that uses a Monte Carlo stochastic simulation algorithm to approximate the gradients that drive the optimisation procedure [48, 17, 37, 30]. In many cases, SA methods use Markov chain Monte Carlo (MCMC) algorithms, leading to a powerful general methodology which is simple to implement, has a detailed convergence theory [2], and can address a wide range of moderately low-dimensional models. Alternatively, some stochastic EM schemes use a Gibbs sampling algorithm [12], however this requires running several fully converged MCMC chains and can be significantly more computationally expensive as a result.

The expectations and demands on SA methods constantly rise as we seek to address larger problems and provide stronger theoretical guarantees on the solutions delivered. Unfortunately, existing SA methodology and theory do not scale well to large problems. The reasons are twofold. First, the family of MCMC kernels driving the SA scheme needs to satisfy uniform geometric ergodicity conditions that are usually difficult to verify for high-dimensional MCMC kernels. Second, the existing theory requires using asymptotically exact MCMC methods. In practice, these are usually high-dimensional Metropolis-Hastings methods such as the Metropolis-adjusted Langevin algorithm [51] or Hamiltonian Monte Carlo [33, 22], which are difficult to calibrate within the SA scheme to achieve a prescribed acceptance rate. For these reasons, practitioners rarely use SA schemes in high-dimensional settings.

In this paper, we propose to address these limitations by using inexact MCMC methods to drive the SA scheme, particularly unadjusted Langenvin algorithms, which have easily verifiable geometric ergodicity conditions, and are easy to calibrate [21, 15]. This will allow us to design a high-dimensional stochastic optimisation scheme with favourable convergence properties that can be quantified explicitly and easily checked.

Our contributions are structured as follows: Section 2 formalises the class of MLE problems considered and presents the proposed stochastic optimisation method, which is based on a SA approach driven by an unadjusted Langevin algorithm. Section 3 presents three numerical experiments that demonstrate the proposed methodology in a variety of scenarios. Detailed theoretical convergence results for the method are reported in Section 4, which also describes a generalisation of the proposed methodology and theory to other inexact Markov kernels. The online supplementary material includes additional theoretical results and some details on computational aspects.

2 The stochastic optimisation via unadjusted Langevin method

The proposed Stochastic Optimisation via Unadjusted Langevin (SOUL) method is useful for solving maximum likelihood estimation problems involving intractable likelihood functions. The method is a SA iterative scheme that is driven by an unadjusted Langevin MCMC algorithm. Langevin algorithms are very efficient in high dimensions and lead to an SA scheme that inherits their favourable convergence properties.

2.1 Maximum marginal likelihood estimation

Let be a convex closed set in . The proposed optimisation method is well-suited for solving maximum likelihood estimation problems of the form

| (1) |

where the parameter of interest is related to the observed data by a likelihood function involving an unknown quantity , which is removed from the model by marginalisation. More precisely, we consider problems where the resulting marginal likelihood

is computationally intractable, and focus on models where the dimension of is large, making the computation of (1) even more difficult. For completeness, we allow the use of a penalty function , or set to recover the standard maximum likelihood estimator.

As mentioned previously, the maximum marginal likelihood estimation problem (1) arises in problems involving latent or hidden variables [18]. It is also central to parametric empirical Bayes approaches that base their inferences on the pseudo-posterior distribution [11]. Moreover, the same optimisation problem also arises in hierarchical Bayesian maximum-a-posteriori estimation of given , with marginal posterior where denotes the prior for ; in that case [7].

Finally, in this paper we assume that is continuously differentiable with respect to and , and that is also continuously differentiable with respect to . A generalisation of the proposed methodology to non-smooth models is presented in a forthcoming paper [53] that focuses on non-smooth statistical imaging models.

2.2 Stochastic approximation methods

The scheme we propose to solve the optimisation problem (1) is derived in the SA framework [17], which we recall below.

Starting from any , SA schemes seek to solve (1) iteratively by computing a sequence associated with the recursion

| (2) |

where is some estimator of the intractable gradient at , denotes the projection onto , and is a sequence of stepsizes. From an optimisation viewpoint, iteration (2) is a stochastic generalisation of the projected gradient ascent iteration [8] for models with intractable gradients. For , Monte Carlo estimators for at are derived from the identity

| (3) | ||||

| (4) |

which suggests to consider

| (5) |

where is a sequence of batch sizes and is either an exact Monte Carlo sample from , or a sample generated by using a Markov Chain targeting this distribution.

Given a sequence generated by using (2), an approximate solution of (1) can then be obtained by calculating, for example, the average of the iterates, i.e.,

| (6) |

This estimate converges almost surely to a solution of (1) as provided that some conditions on , , , , and are fulfilled. Indeed, following three decades of active research efforts in computational statistics and applied probability, we now have a good understanding of how to construct efficient SA schemes, and the conditions under which these schemes converge (see for example [6, 29, 20, 1, 44, 2]).

SA schemes are successfully applied to maximum marginal likelihood estimation problems where the latent variable has a low or moderately low dimension. However, they are seldomly used them when is high-dimensional because this usually requires using high-dimensional MCMC samplers that, unless carefully calibrated, exhibit poor convergence properties. Unfortunately, calibrating the samplers within a SA scheme is challenging because the target density changes at each iteration. As a result, it is, for example, difficult to use Metropolis-Hastings algorithms that need to achieve a prescribed acceptance probability range. Additionally, the conditions for convergence of MCMC SA schemes are often difficult to verify for high-dimensional samplers. For these reasons, practitioners rarely use SA schemes in high-dimensional settings.

As mentioned previously, we propose to address these difficulties by using modern inexact Langevin MCMC samplers to drive (5). These samplers have received a lot of attention in the late because they can exhibit excellent large-scale convergence properties and significantly outperform their Metropolised counterparts (see [23] for an extensive comparison in the context of Bayesian imaging models). Stimulated by developments in high-dimensional statistics and machine learning, we now have detailed theory for these algorithms, including explicit and easily verifiable geometric ergodicity conditions [21, 15, 26, 16]. This will allow us to design a stochastic optimisation scheme with favourable convergence properties that can be quantified explicitly and easily checked.

2.3 Langevin Markov chain Monte Carlo methods

Langevin MCMC schemes to sample from are based on stochastic continuous dynamics for which the target distribution is invariant. Two fundamental examples are the Langevin dynamics solution of the following Stochastic Differential Equation (SDE)

| (7) |

or the kinetic Langevin dynamics solution of

| (8) |

where is a standard -dimensional Brownian motion. Under mild assumptions on , these two SDEs admit strong solutions for which and are the invariant probability measures. In addition, there are detailed explicit convergence results for to , and for to , under different metrics [25, 24].

However, sampling path solutions for these continuous-time dynamics is not feasible in general. Therefore discretizations have to be used instead. In this paper, we mainly focus on the Euler-Maruyama discrete-time approximation of (7), known as the Unadjusted Langevin Algorithm (ULA) [51], given by

| (9) |

where is the discretization time step and is a i.i.d. sequence of -dimensional zero-mean Gaussian random variables with covariance matrix identity. We will use this Markov kernel to drive our SA schemes.

Observe that (9) does not exactly target because of the bias introduced by the discrete-time approximation. Computational statistical methods have traditionally addressed this issue by complementing (9) with a Metropolis-Hastings correction step to asymptotically remove the bias [51]. This correction usually deteriorates the convergence properties of the chain and may lead to poor non-asymptotic estimation results, particularly in very high-dimensional settings (see for example [23]). However, until recently it was considered that using (9) without a correction step was too risky. Fortunately, recent works have established detailed theoretical guarantees for (9) that do not require using any correction [15, 21]. A main contribution of this work is to extend these guarantees to SA schemes that are driven by these highly efficient but inexact samplers.

2.4 The SOUL algorithm

We are now ready to present the proposed Stochastic Optimization via Unadjusted Langevin (SOUL) methodology. Let and be the sequences of stepsizes and batch sizes defining the SA scheme (2)-(5). For any and , denote by the Langevin Markov kernel (9) to approximately sample from , and by be the sequence of discrete time steps used.

Formally, starting from some and , for and , we recursively define on a probability space , where is a Markov chain with Markov kernel , given , and

where we recall that is the projection onto , and for all

| (10) |

Note that such a construction is always possible by Kolmogorov extension theorem [34, Theorem 5.16], hence for any , is -measurable. Then, as mentioned previously, we compute a sequence of approximate solutions of (1) by calculating, for example,

| (11) |

The pseudocode associated with the proposed SOUL method is presented in Algorithm 1 below. Observe that, for additional efficiency, instead of generating independent Markov chains at each SA iteration, we warm-start the chains by setting , for any .

To conclude, Section 3 below demonstrates the proposed methodology with three numerical experiments related to high-dimensional logistic regression and statistical audio analysis with sparsity promoting priors. A detailed theoretical analysis of the proposed SOUL method is reported in Section 4. More precisely, we establish that if the cost function defining (1) is convex, and if and go to sufficiently fast, then converges to and quantify the rate of convergence. Moreover, in the case where is held fixed, i.e. for all , , we show convergence to a neighbourhood of the solution, in the sense that there exist explicit such that . Finally, we also study the important case where is not convex. In that case, we use the results of [37] to establish that converges almost surely to a stationary point of the projected ordinary differential equation associated with and . We postpone this result to Appendix B in the supplementary document because it is highly technical.

3 Numerical results

We now demonstrate the proposed methodology with three experiments that we have chosen to illustrate a variety of scenarios. Section 3.1 presents an application to empirical Bayesian logistic regression, where (1) can be analytically shown to be a convex optimisation problem with an unique solution , and where we benchmark our MLE estimate against the solution obtained by calculating the marginal likelihood over a -grid by using an harmonic mean estimator. Furthermore, Section 3.2 presents a challenging application related to statistical audio compressive sensing analysis, where we use SOUL to estimate a regularisation parameter that controls the degree of sparsity enforced, and where a main difficulty is the high-dimensionality of the latent space (). Finally, Section 3.3 presents an application to a high-dimensional empirical Bayesian logistic regression with random effects for which the optimisation problem (1) is not convex. All experiments were carried out on an Intel i9-8950HK@2.90GHz workstation running Matlab R2018a.

3.1 Bayesian Logistic Regression

In this first experiment we illustrate the proposed methodology with an empirical Bayesian logistic regression problem [55, 45]. We observe a set of covariates , and binary responses , which we assume to be conditionally independent realisations of a logistic regression model: for any , given and has distribution , where is the regression coefficient, denotes the Bernoulli distribution with parameter and is the cumulative distribution function of the standard logistic distribution. The prior for is set to be , the -dimensional Gaussian distribution with mean and covariance matrix , where is the parameter we seek to estimate, , and is the -dimensional identity matrix. Following an empirical Bayesian approach, the parameter is computed by maximum marginal likelihood estimation using Algorithm 1 with the marginal likelihood given by

| (12) |

Appendix A in Appendix A of the supplementary document shows that (12) is log-concave with respect to . We use the proposed SOUL methodology to estimate for the Wisconsin Diagnostic Breast Cancer dataset555Available online: https://archive.ics.uci.edu/ml/datasets/Breast+Cancer+Wisconsin+(Diagnostic), for which and , and where we suitably normalise the covariates. In order to assess the quality of our estimation results, we also calculate over a grid of values for by using a truncated harmonic mean estimator.

To implement Algorithm 1 we derive the log-likelihood function

| (13) |

and obtain the following expressions for the gradients used in the MCMC steps (9) and SA steps (2) respectively

| (14) | ||||

| (15) |

For the MCMC steps, we use a fixed stepsize , and batch size , for any . On the other hand, we consider for the SA steps, the sequence of stepsizes , and . Finally, we first run burn-in iterations with fixed to warm-up the Markov chain, followed by iterations of Algorithm 1 to warm-up the iterates. This procedure is then followed by iterations of Algorithm 1 to compute .

(a)

(b)

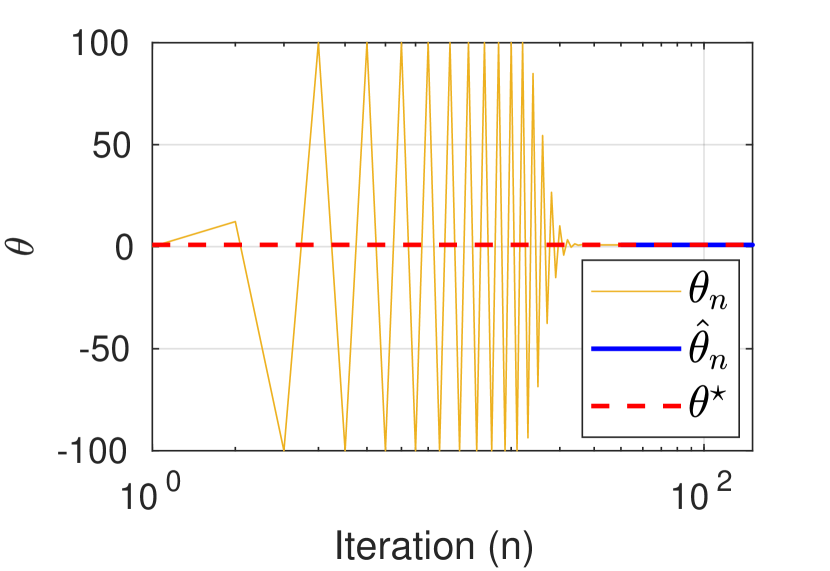

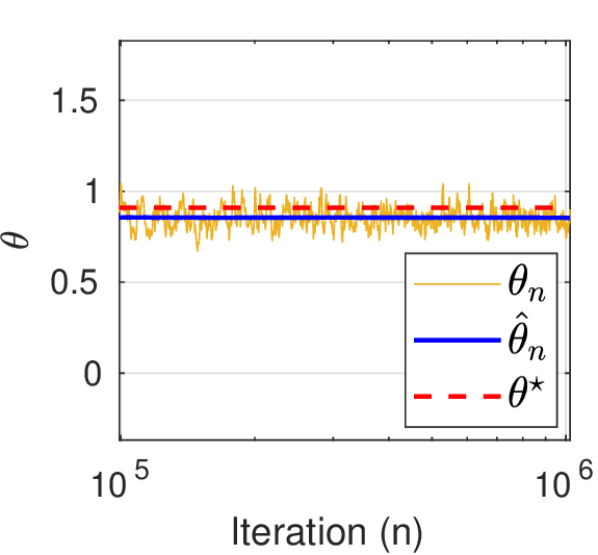

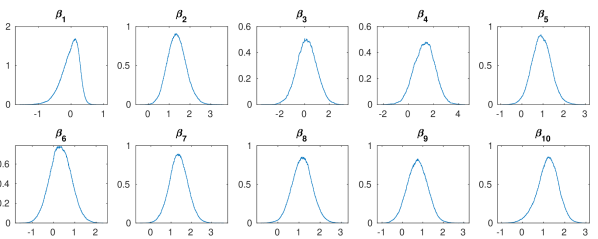

Figure 1(a) shows the evolution of the iterates during the first iterations. Observe that the sequence initially oscillates, and then stabilises close to after approximately iterations. Figure 1(b) presents the iterates for . For completeness, Figure 2 shows the histograms corresponding to the marginal posteriors , for , obtained as a by-product of Algorithm 1.

In order to verify that the obtained estimate is close to the true MLE we use a truncated harmonic mean estimator (THME) [50] to calculate the marginal likelihood for a range of values of . Although obtaining the THME is usually computationally expensive, it is viable in this particular experiment as is low-dimensional. More precisely, given samples from , we obtain an approximation of by computing

| (16) |

where is a -dimensional ball centered at the posterior mean , and with radius set such that . Using samples, we obtain the approximation shown in Figure 3(a), where in addition to the estimated points we also display a quadratic fit (corresponding to a Gaussian fit in linear scale), which we use to obtain an estimate of (the obtained log-likelihood values are small because the dataset is large ()).

To empirically study the estimation error involved, we replicate the experiment times. Figure 3 shows the obtained histogram of , where we observe that all these estimators are very close to the true maximiser . Besides, note that the distribution of the estimation error is close to a Gaussian distribution, as expected for a maximum likelihood estimator. Also, there is a small estimation bias of the order of , which can be attributed to the discretization error of SDE (7), and potentially to a small error in the estimation of .

(a)

(b)

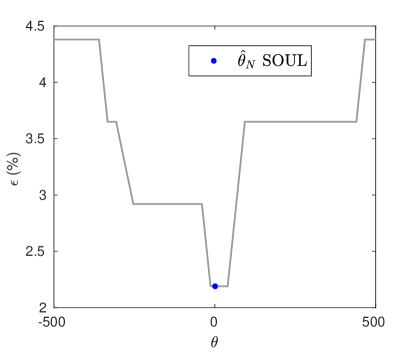

We conclude this experiment by using SOUL to perform a predictive empirical Bayesian analysis on the binary responses. We split the original dataset into an training set of size , and a test set of size , and use SOUL to draw samples from the predictive distribution . More precisely, we use SOUL to simultaneously calculate and simulate from , followed by simulation from . We then estimate the maximum-a-posteriori predictive response , and measure prediction accuracy against the test dataset by computing the error

| (17) |

and obtain . For comparison, Figure 4 below reports the error as a function of (the discontinuities arise because of the highly non-linear nature of the model). Observe that the estimated produces a model that has a very good performance in this regard.

3.2 Statistical audio compression

Compressive sensing techniques exploit sparsity properties in the data to estimate signals from fewer samples than required by the Nyquist–Shannon sampling theorem [10, 9]. Many real-world data admit a sparse representation on some basis or dictionary. Formally, consider an -dimensional time-discrete signal that is sparse in some dictionary , i.e, there exists a latent vector such that and . This prior assumption can be modelled by using a smoothed-Laplace distribution [38]

| (18) |

where is the Huber function given for any by

| (19) |

Acquiring directly would call for measuring univariate components. Instead, a carefully designed measurement matrix , with , is used to directly observe a “compressed” signal , which only requires taking measurements. In addition, measurements are typically noisy which results in an observation modeled as where we assume that the noise has distribution , and therefore the likelihood function is given by

| (20) |

leading to the posterior distribution

| (21) |

To recover from , we then compute the maximum-a-posteriori estimate

| (22) |

and set .

Following decades of active research, there are now many convex optimisation algorithms that can be used to efficiently solve (22), even when is very large [14, 43]. However, the selection of the value of in (22) remains a difficult open problem. This parameter controls the degree of sparsity of and has a strong impact on estimation performance.

A common heuristic within the compressive sensing community is to set , where for any , , as suggested in [35] and [28]; however, better results can arguably be obtained by adopting a statistical approach to estimate .

The Bayesian framework offers several strategies for estimating from the observation . In this experiment we adopt an empirical Bayesian approach and use SOUL to compute the MLE , which is challenging given the high-dimensionality of the latent space.

To illustrate this approach, we consider the audio experiment proposed in [5] for the “Mary had a little lamb” song. The MIDI-generated audio file has samples, but we only have access to a noisy observation vector with random time points of the audio signal, corrupted by additive white Gaussian noise with . The latent signal has dimension and is related to by a dictionary matrix whose row vectors correspond to different piano notes lasting a quarter-second long 666Each quarter-second sound can have one of 100 possible frequencies and be in 29 different positions in time. . The parameter for the prior (18) is set to . We used the heuristic as the initial value for in our algorithm. To solve the optimisation problem (22) we use the Gradient Projection for Sparse Reconstruction (GPSR) algorithm proposed in [28]. We use this solver because it is the one used in the online MATLAB demonstration of [5], however, more modern algorithms could be used as well. We implemented Algorithm 1 using a fixed stepsize , a fixed batch size , and 100 burn-in iterations.

The algorithm converged in approximately 500 iterations, which were computed in only 325 milliseconds. Figure 5 (left), shows the first 250 iterations of the sequence and of the weighted average . Again, observe that the iterates oscillate for a few iterations and then quickly stabilise. Finally, to assess the quality of the estimate , Figure 5 (right) presents the reconstruction mean squared error as a function of . The error is measured with respect to the reconstructed signal and is given by , where is the true audio signal. Observe that the estimated value is very close to the value that minimises the estimation error, and significantly outperforms the heuristic value commonly used by practitioners.

3.3 Sparse Bayesian logistic regression with random effects

Following on from the Bayesian logistic regression in Section 3.1, where is log-concave and hence unique, we now consider a significantly more challenging sparse Bayesian logistic regression with random effects problem. In this experiment is no longer log-concave, so SOUL can potentially get trapped in local maximisers. Furthermore, the dimension of in this experiment is very large (), making the MLE problem even more challenging. This experiment was previously considered by [2] and we replicate their setup.

Let be a vector of binary responses which can be modelled as conditionally independent realisations of a random effect logistic regression model,

| (23) |

where are the covariates, is the regression vector, are (known) loading vectors, are random effects and . In addition, recall that denotes the Bernoulli distribution with parameter and is the cumulative distribution function of the standard logistic distribution. The goal is to estimate the unknown parameters directly from , without knowing the value of , which we assume to follow a standard Gaussian distribution, i.e. . We estimate by MLE using Algorithm 1 to maximize (1), with marginal likelihood given by

| (24) |

and we use the penalty function

| (25) |

where is the Huber function defined in (19).

We follow the procedure described in [2] to generate the observations , with , and 777We renamed some symbols for notation consistency. What we denote by , , and , is denoted in [2] by , , and respectively.. The vector of regressors is generated from the uniform distribution on and of its coefficients are randomly set to zero. The variance of the random effect is set to 0.1, and the projection interval for the estimated is . Finally, the parameter in (25) is set to . We emphasize at this point that is high-dimensional in this experiment (), making the estimation problem particularly challenging.

The conditional log-likelihood function for this model is

| (26) |

To implement Algorithm 1 we use the gradients

| (27) | ||||

| (28) |

Finally the gradient of the penalty function is given by

| (29) |

where denotes the sign function, i.e. for any , if , and otherwise.

We use , , a fixed batch size , and as initial values. Moreover, we perform burn-in iterations with a fixed value of to warm-up the Markov chain, and further iterations of Algorithm 1 to warm-start the iterates. Following on from this, we run iterations of Algorithm 1 to compute . Computing this estimates required seconds in total.

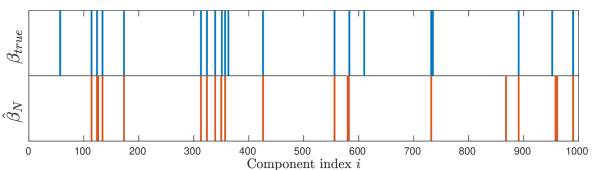

Figure 6 shows the evolution of the iterates throughout iterations, where we used as a summary statistic to track the number of active components. Because the Huber penalty (19) does not enforce exact sparsity on , to estimate the number of active components we only consider values that are larger than a threshold (we used ).

From Figure 6 we observe that converges to a value that is very close to , and that the number of active components is also accurately estimated. Moreover, Figure 7 shows that most active components were correctly identified. We also observe that stabilizes after approximately iterations, which correspond to Monte Carlo samples as =1. This is in close agreement with the results presented in [2, Figure 5], where they observe stabilization after a similar number of iterations of their highly specialised Polya-Gamma sampler.

It is worth emphasising at this point that [2] considers the non-smooth penalty instead of (25). Consequently, instead of using the gradient of , they resort to the so-called proximal operator of [14]. The generalisation of the SOUL methodology proposed in this paper to models that have non-differentiable terms is addressed in Vidal and Pereyra [54], Vidal et al. [53].

4 Theoretical convergence analysis for SOUL, and generalisation to other inexact MCMC kernels (SOUK)

In this section we state our main theoretical results for SOUL. For completeness, we first present the results in a general stochastic optimisation setting and by considering a generic inexact MCMC sampler, and then show that our results apply to the specific MLE optimisation problem (1), and to the specific Langevin algorithm (9) used in SOUL.

4.1 Notations and convention

Denote by the Borel -field of , the set of all Borel measurable functions on and for , . For a probability measure on and a -integrable function, denote by the integral of with respect to . For , the -norm of is given by . Let be a finite signed measure on . The -total variation distance of is defined as

| (30) |

If , then is the total variation denoted by . Let be a finite signed measure, then by the Hahn-Jordan theorem [19, Theorem D.1.3], there exists a pair of finite singular measures such that . The total variation measure is given by .

Let be an open set of . We denote by the set of -valued -differentiable functions, respectively the set of compactly supported -valued -differentiable functions. stands . Let , we denote by , the gradient of if it exists. is said to me -convex with if for all and ,

| (31) |

We recall that if is twice differentiable at point , its Laplacian is given by . For any , we denote by the boundary of . Let be a probability space. Denote by if is absolutely continuous with respect to and an associated density. Let be two probability measures on . Define the Kullback-Leibler divergence of from by

| (32) |

The complement of a set , is denoted by . We take the convention that and for , . All densities are w.r.t. the Lebesgue measure unless stated otherwise.

4.2 Stochastic Optimization with inexact MCMC methods

We consider the problem of minimizing a function with under the following assumptions.

A 1.

is a convex compact set and with .

A 2.

There exist an open set and such that , and satisfies for any

| (33) |

A 3.

For any , there exist and a probability distribution on satisfying that and for any

| (34) |

In addition, is measurable.

Note that for the maximum marginal likelihood estimation problem (1), corresponds to , for any , and is the probability distribution with density with respect to the Lebesgue measure .

To minimize the objective function we suggest the use of a SA strategy which extends the one presented in Section 2. More precisely, motivated by the methodology described in Section 2, we propose a SA scheme which relies on biased estimates of through a family of Markov kernels , for , such that for any and , admits an invariant probability distribution on . In the SOUL method, the Markov kernel stands for for any and , where is the Markov kernel associated with (9). We assume in addition that the bias associated to the use of this family of Markov kernels can be controlled with respect to to uniformly in , i.e. for example there exists such that for all and , with .

Let now and be sequences of stepsizes and batch sizes which will be used to define the sequence relatively to the variable similarly to (2) and (5). Let be a sequence of stepsizes which will be used to get approximate samples from , similarly to (9). Starting from and , we define on a probability space , by the following recursion for and

| (35) | ||||

where is the projection onto and is defined as follows for all

| (36) |

where is given by (35). Note that such a construction is always possible by the Kolmogorov extension theorem [34, Theorem 5.16], and by (35), for any , is -measurable. Then the sequence of approximate minimizers of is given by , (11).

Under different sets of conditions on and we obtain that converges almost surely to an element of . In particular in this section we consider the case where is assumed to be convex. We establish that if and go to sufficiently fast, goes to with a quantitative rate of convergence. In the case where is held fixed, i.e. for all , , we show that while does not converge to , there exists such that . In the case where is non-convex, we apply some results from stochastic approximation [37] which establish that the sequence converges almost surely to a stationary point of the projected ordinary differential equation associated with and . We postpone this result to Appendix B, since it involves a theoretical background which we think is out of the scope of the main document.

4.3 Main results

We impose a stability condition on the stochastic process defined by (35) and that for any and the iterates of are close enough to after a sufficiently large number of iterations.

H 1.

There exists a measurable function satisfying the following conditions.

- (i)

-

(ii)

There exist , such that for any , , and , has a stationary distribution and

(38) -

(iii)

There exists such that for any and

(39)

H 1-(ii) is an ergodicity condition in -norm for the Markov kernel uniform in . There exists an extensive literature on the conditions under which a Markov kernel is ergodic [41, 19]. H 1-(iii) ensures that the distance between the invariant measure of the Markov kernel and can be controlled uniformly in . We show that this condition holds in the case of the Langevin Monte Carlo algorithm in Section C.5.2.

We now state our mains results.

Theorem 1 (Increasing batch size 1).

Assume 1, 2, 3 hold and is convex. Let , be sequences of non-increasing positive real numbers and be sequences of positive integers satisfying , and

| (40) |

Let and be given by (35). Assume in addition that H 1 is satisfied and that for any and , . Then, the following statements hold:

-

(a)

converges almost surely to some ;

-

(b)

furthermore, almost surely there exists such that for any

(41)

Proof.

The proof is postponed to Section C.1. ∎

Note that in (35), for . This procedure is referred to as warm-start in the sequel. An inspection of the proof of Theorem 1 shows that could be any random variable independent from for any with . It is not an option in the fixed batch size setting of Theorem 3, where the warm-start procedure is crucial for the convergence to occur.

We extend this theorem to non convex objective function see Theorem 7 in Appendix B. Under the conditions of Theorem 1 with the additional assumption that is a smooth manifold we obtain that converges almost surely to some point such that with if and if , where is the tangent space of at point , see [3, Chapter 2].

In the case where is the Markov kernel associated with the Langevin update (9), under appropriate conditions Section C.5.2 shows that for any with , . In that case, assume then that there exist such that for any , , and then (40) is equivalent to

| (42) |

Suppose is given, then the previous equation reads

| (43) |

This illustrates a trade-off between the intrinsic inaccuracy of our algorithm through the family of Markov kernels (35) which do not exactly target and the minimization aim of our scheme. Note also that is allowed to be constant. This case yields and with .

In our next result we derive an non-asymptotic upper-bound of .

Theorem 2 (Increasing batch size 2).

Assume 1, 2, 3 hold and is convex. Let , be sequences of non-increasing positive real numbers and be a sequence of positive integers satisfying , . Let be given by (35). Assume in addition that H 1 is satisfied and that for any and , . Then, there exists such that for any

| (44) |

with for any ,

| (45) |

where and are given in Section C.1 and Section C.1 respectively.

Proof.

The proof is postponed to Section C.2. ∎

We recall that in the case where is the Markov kernel associated with the Langevin update (9), under appropriate conditions Section C.5.2 shows that for any with , . In that case, if there exist such that for any , , , and (42) holds, the accuracy, respectively the complexity, of the algorithm are of orders , respectively for . Thus, for a fix target precision , it requires that and the complexity reads . On the other hand, if we fix the complexity budget to the accuracy is of order . These two considerations suggest to set close to . In the special case where , we obtain that the accuracy is of order , which is similar to the order identified in the deterministic gradient descent for convex functionals.

A case of interest is the fix stepsize setting, i.e. for all . Assume that is non-increasing and . In addition, assume that then, by [46, Problem 80, Part I], it holds that

| (46) |

Therefore, we obtain that

| (47) |

Similarly, if the stepsize is fixed and the number of Markov chain iterates is fixed, i.e. for all , and with and , we obtain that

| (48) |

with

| (49) |

However if is constant the convergence cannot be obtained using Theorem 1. Strengthening the conditions of Theorem 1 and making use of the warm-start property of the algorithm we can derive the convergence in that case.

We now are interested in the case where the batch size is fixed, i.e. for all . For ease of exposition we only consider and let for any . However the general case can be adapted from the proof of the result stated below. More precisely we consider the setting where the recursion (35) can be written for any as

| (50) | ||||

with , and where is given by

| (51) |

We consider the following assumption on the family .

A 4.

There exists such that for any and ,

| (52) |

We consider a similar property as 4 on the family of Markov kernels , which weakens the assumption [2, H6].

H 2.

There exist a measurable function , and such that for any with , , and

| (53) |

The following theorem ensures convergence properties for similar to the ones of Theorem 1. The proof of this result is based on a generalization of [30, Lemma 4.2] for inexact MCMC schemes.

Theorem 3 (Fixed batch size 1).

Assume 1, 2, 3, 4 hold and is convex. Let , and be sequences of non-increasing positive real numbers satisfying , , , and

| (54) | ||||

Let be given by (50). Assume in addition that H 1 and H 2 are satisfied and that for any and , . Then the following statements hold:

-

(a)

converges almost surely to some ;

-

(b)

furthermore, almost surely there exists such that for any

(55)

Proof.

The proof is postponed to Section C.3. ∎

In the case where is the Markov kernel associated with the Langevin update (9), under appropriate conditions Section C.5.2 and Section C.6 show that for any with and , , and , for . Thus we obtain that the following series should converge

| (56) | ||||

If there exist such that and , then (56) is satisfied if which is not empty if .

Theorem 4 (Fixed batch size 2).

Assume 1, 2, 3, 4 hold and is convex. Let , be sequences of non-increasing positive real numbers and be a sequence of positive integers satisfying and . Let be given by (50). Assume in addition that H 1 and H 2 are satisfied and that for any and , . Then, there exists such that for any

| (57) |

with for any ,

| (58) | ||||

| (59) | ||||

| (60) |

where , and are given in Section C.3, Section C.3 and Section C.3 respectively.

Proof.

The proof is postponed to Section C.4. ∎

Theorem 4 improves the conclusions of Theorem 2 in the case where for any . Indeed, in that case, similarly to (48), assuming that , , for any , we obtain that for all

| (61) |

with . In the case where , is of order and is of order . Therefore if , even in the fixed batch size setting, the minimum of the objective function can be approached with arbitrary precision by choosing small enough.

4.4 Application to SOUL

We now apply our results to the SOUL methodology introduced in Section 2 where the Markov kernel with and is given by a Langevin Markov kernel and associated with recursion (9). Setting for any , , we consider the following assumption on the family of probability distributions .

L 1.

For any , there exists such that admits a probability density function with respect to to the Lebesgue measure proportional to . In addition is continuous, is differentiable for all and there exists such that for any ,

| (62) |

and is bounded.

In the case where for any and , the first line of (35) can be rewritten for any and

| (63) |

given , and a family of i.i.d -dimensional zero-mean Gaussian random variables with covariance matrix identity. In the following propositions, we show that the results above hold by deriving sufficient conditions under which H 1 and H 2 are satisfied.

Under L 1, the Langevin diffusion defined by (7) admits a unique strong solution for any . Consider now the following additional tail condition on which ensures geometric ergodicity of for any and , with which will be specified below.

L 2.

There exist and such that for any and ,

L 3.

There exists such that for any and

| (64) |

The next theorems assert that under L 1, L 2 and L 3 the SOUL algorithm introduced in Section 2 satisfy H 1 and H 2 and therefore Theorem 1, Theorem 2, Theorem 3 and Theorem 4 can be applied if in addition 1, 2, 3 and 4 hold.

Under L 2 define for any

| (65) |

Theorem 5.

Assume L 1 and L 2. Then, H 1 holds with , and where is given in Section C.5.2.

Proof.

The proof is postponed to Section C.5.∎

Theorem 6.

Assume L 1, L 2, L 3 and that for any and , . H 2 holds with and and for any , ,

| (66) |

where is given in Section C.6 in Section C.6.

Proof.

The proof is postponed to Section C.6. ∎

References

- Andrieu and Moulines [2006] C. Andrieu and É. Moulines. On the ergodicity properties of some adaptive MCMC algorithms. Ann. Appl. Probab., 16(3):1462–1505, 2006. ISSN 1050-5164. doi: 10.1214/105051606000000286. URL https://doi.org/10.1214/105051606000000286.

- Atchadé et al. [2017] Y. F. Atchadé, G. Fort, and E. Moulines. On perturbed proximal gradient algorithms. J. Mach. Learn. Res, 18(1):310–342, 2017.

- Aubin [2000] T. Aubin. A course in differential geometry. Graduate Studies in Mathematics. AMS, 2000. ISBN 9780821827093,082182709X.

- Bakry et al. [2014] D. Bakry, I. Gentil, and M. Ledoux. Analysis and geometry of Markov diffusion operators, volume 348 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer, Cham, 2014. ISBN 978-3-319-00226-2; 978-3-319-00227-9. doi: 10.1007/978-3-319-00227-9. URL http://dx.doi.org/10.1007/978-3-319-00227-9.

- Balzano et al. [2010] Laura Balzano, Robert Nowak, and J Ellenberg. Compressed sensing audio demonstration. website http://web.eecs.umich.edu/~girasole/csaudio, 2010.

- Benveniste et al. [1990] A. Benveniste, M. Métivier, and P. Priouret. Adaptive algorithms and stochastic approximations, volume 22 of Applications of Mathematics (New York). Springer-Verlag, Berlin, 1990. ISBN 3-540-52894-6. doi: 10.1007/978-3-642-75894-2. URL https://doi.org/10.1007/978-3-642-75894-2. Translated from the French by Stephen S. Wilson.

- Berger and Casella [2002] R. Berger and G. Casella. Statistical inference (2nd ed.). Duxbury / Thomson Learning, Pacific Grove, USA, 2002.

- Boyd and Vandenberghe [2004] Stephen Boyd and Lieven Vandenberghe. Convex optimization. Cambridge university press, 2004.

- Candès and Wakin [2008] Emmanuel J Candès and Michael B Wakin. An introduction to compressive sampling [a sensing/sampling paradigm that goes against the common knowledge in data acquisition]. IEEE signal processing magazine, 25(2):21–30, 2008.

- Candès et al. [2006] Emmanuel J Candès et al. Compressive sampling. In Proceedings of the international congress of mathematicians, volume 3, pages 1433–1452. Madrid, Spain, 2006.

- Carlin and Louis [2000] Bradley P. Carlin and Thomas A. Louis. Empirical Bayes: past, present and future. J. Amer. Statist. Assoc., 95(452):1286–1289, 2000. ISSN 0162-1459. doi: 10.2307/2669771. URL https://doi.org/10.2307/2669771.

- Casella [2001] G. Casella. Empirical Bayes Gibbs sampling. Biostatistics, 2(4):485–500, 2001.

- Casella [1985] George Casella. An introduction to empirical Bayes data analysis. Amer. Statist., 39(2):83–87, 1985. ISSN 0003-1305. doi: 10.2307/2682801. URL https://doi.org/10.2307/2682801.

- Chambolle and Pock [2016] Antonin Chambolle and Thomas Pock. An introduction to continuous optimization for imaging. Acta Numerica, 25:161–319, 2016.

- Dalalyan [2017] Arnak S. Dalalyan. Theoretical guarantees for approximate sampling from smooth and log-concave densities. J. R. Stat. Soc. Ser. B. Stat. Methodol., 79(3):651–676, 2017. ISSN 1369-7412. doi: 10.1111/rssb.12183. URL https://doi.org/10.1111/rssb.12183.

- De Bortoli and Durmus [2019] V. De Bortoli and A. Durmus. Convergence of diffusions and their discretizations:from continuous to discrete processes and back. arXiv preprint arXiv:1904.09808, 2019.

- Delyon et al. [1999] Bernard Delyon, Marc Lavielle, and Eric Moulines. Convergence of a stochastic approximation version of the em algorithm. Ann. Statist., 27(1):94–128, 03 1999. URL https://doi.org/10.1214/aos/1018031103.

- Dempster et al. [1977] A. P. Dempster, N. M. Laird, and D. B. Rubin. Maximum likelihood from incomplete data via the EM algorithm. J. Roy. Stat. Soc. Ser. B, 39(1):1–38, 1977.

- Douc et al. [2018] R. Douc, É. Moulines, P. Priouret, and P. Soulier. Markov Chains. Springer, 2018. to be published.

- Duchi et al. [2011] J. Duchi, E. Hazan, and Y. Singer. Adaptive subgradient methods for online learning and stochastic optimization. J. Mach. Learn. Res., 12:2121–2159, 2011. ISSN 1532-4435.

- Durmus and Moulines [2017] A. Durmus and É. Moulines. Nonasymptotic convergence analysis for the unadjusted Langevin algorithm. Ann. Appl. Probab., 27(3):1551–1587, 2017. ISSN 1050-5164. doi: 10.1214/16-AAP1238. URL https://doi.org/10.1214/16-AAP1238.

- Durmus et al. [2017] A. Durmus, E. Moulines, and E. Saksman. On the convergence of hamiltonian monte carlo. arXiv preprint arXiv:1705.00166, 2017.

- Durmus et al. [2018] Alain Durmus, Eric Moulines, and Marcelo Pereyra. Efficient bayesian computation by proximal markov chain monte carlo: when langevin meets moreau. SIAM Journal on Imaging Sciences, 11(1):473–506, 2018.

- Eberle et al. [2017] A. Eberle, A. Guillin, and R. Zimmer. Couplings and quantitative contraction rates for langevin dynamics. arXiv preprint arXiv:1703.01617, 2017.

- Eberle [2016] Andreas Eberle. Reflection couplings and contraction rates for diffusions. Probab. Theory Related Fields, 166(3-4):851–886, 2016. ISSN 0178-8051. doi: 10.1007/s00440-015-0673-1. URL https://doi.org/10.1007/s00440-015-0673-1.

- Eberle and Majka [2018] Andreas Eberle and Mateusz B Majka. Quantitative contraction rates for markov chains on general state spaces. arXiv preprint arXiv:1808.07033, 2018.

- Ethier and Kurtz [1986] Stewart N. Ethier and Thomas G. Kurtz. Markov processes. Wiley Series in Probability and Mathematical Statistics: Probability and Mathematical Statistics. John Wiley & Sons, Inc., New York, 1986. ISBN 0-471-08186-8. doi: 10.1002/9780470316658. URL https://doi.org/10.1002/9780470316658. Characterization and convergence.

- Figueiredo et al. [2007] Mário AT Figueiredo, Robert D Nowak, and Stephen J Wright. Gradient projection for sparse reconstruction: Application to compressed sensing and other inverse problems. IEEE Journal of selected topics in signal processing, 1(4):586–597, 2007.

- Fort and Moulines [2003] G. Fort and E. Moulines. Convergence of the Monte Carlo expectation maximization for curved exponential families. Ann. Statist., 31(4):1220–1259, 2003. ISSN 0090-5364. doi: 10.1214/aos/1059655912. URL https://doi.org/10.1214/aos/1059655912.

- Fort et al. [2011] G. Fort, E. Moulines, and P. Priouret. Convergence of adaptive and interacting Markov chain Monte Carlo algorithms. Ann. Statist., 39(6):3262–3289, 2011. ISSN 0090-5364. doi: 10.1214/11-AOS938. URL https://doi.org/10.1214/11-AOS938.

- Gardner [2002] R. J. Gardner. The Brunn-Minkowski inequality. Bull. Amer. Math. Soc. (N.S.), 39(3):355–405, 2002. ISSN 0273-0979. doi: 10.1090/S0273-0979-02-00941-2. URL https://doi.org/10.1090/S0273-0979-02-00941-2.

- Gentle et al. [2012] James E Gentle, Wolfgang Karl Härdle, and Yuichi Mori. Handbook of computational statistics: concepts and methods. Springer Science & Business Media, 2012.

- Girolami and Calderhead [2011] Mark Girolami and Ben Calderhead. Riemann manifold langevin and hamiltonian monte carlo methods. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 73(2):123–214, 2011. doi: 10.1111/j.1467-9868.2010.00765.x. URL https://rss.onlinelibrary.wiley.com/doi/abs/10.1111/j.1467-9868.2010.00765.x.

- Kallenberg [2006] O. Kallenberg. Foundations of modern probability. Springer Science & Business Media, 2006.

- Kim et al. [2007] Seung-Jean Kim, Kwangmoo Koh, Michael Lustig, Stephen Boyd, and Dimitry Gorinevsky. A method for large-scale l1-regularized least squares. IEEE Journal on Selected Topics in Signal Processing, 1(4):606–617, 2007.

- Kullback [1997] Solomon Kullback. Information theory and statistics. Dover Publications, Inc., Mineola, NY, 1997. ISBN 0-486-69684-7. Reprint of the second (1968) edition.

- Kushner and Yin [2003] Harold J. Kushner and G. George Yin. Stochastic approximation and recursive algorithms and applications, volume 35 of Applications of Mathematics (New York). Springer-Verlag, New York, second edition, 2003. ISBN 0-387-00894-2. Stochastic Modelling and Applied Probability.

- Lingala and Jacob [2012] Sajan Goud Lingala and Mathews Jacob. A blind compressive sensing frame work for accelerated dynamic mri. In 2012 9th IEEE International Symposium on Biomedical Imaging (ISBI), pages 1060–1063. IEEE, 2012.

- Meyn and Tweedie [1993a] S. P. Meyn and R. L. Tweedie. Markov chains and stochastic stability. Communications and Control Engineering Series. Springer-Verlag London, Ltd., London, 1993a. ISBN 3-540-19832-6. doi: 10.1007/978-1-4471-3267-7. URL https://doi.org/10.1007/978-1-4471-3267-7.

- Meyn and Tweedie [1993b] S. P. Meyn and R. L. Tweedie. Stability of Markovian processes. III. Foster-Lyapunov criteria for continuous-time processes. Adv. in Appl. Probab., 25(3):518–548, 1993b. ISSN 0001-8678. doi: 10.2307/1427522. URL http://dx.doi.org/10.2307/1427522.

- Meyn and Tweedie [1992] Sean P. Meyn and R. L. Tweedie. Stability of Markovian processes. I. Criteria for discrete-time chains. Adv. in Appl. Probab., 24(3):542–574, 1992. ISSN 0001-8678. doi: 10.2307/1427479. URL https://doi.org/10.2307/1427479.

- Meyn and Tweedie [1993c] Sean P. Meyn and R. L. Tweedie. Stability of Markovian processes. III. Foster-Lyapunov criteria for continuous-time processes. Adv. in Appl. Probab., 25(3):518–548, 1993c. ISSN 0001-8678. doi: 10.2307/1427522. URL https://doi.org/10.2307/1427522.

- Monga [2017] Vishal Monga. Handbook of Convex Optimization Methods in Imaging Science. Springer, 2017.

- Nemirovski et al. [2008] A. Nemirovski, A. Juditsky, G. Lan, and A. Shapiro. Robust stochastic approximation approach to stochastic programming. SIAM J. Optim., 19(4):1574–1609, 2008. ISSN 1052-6234. doi: 10.1137/070704277. URL https://doi.org/10.1137/070704277.

- Polson et al. [2013] Nicholas G Polson, James G Scott, and Jesse Windle. Bayesian inference for logistic models using pólya–gamma latent variables. Journal of the American statistical Association, 108(504):1339–1349, 2013.

- Pólya and Szegő [1998] George Pólya and Gabor Szegő. Problems and theorems in analysis. I. Classics in Mathematics. Springer-Verlag, Berlin, 1998. ISBN 3-540-63640-4. doi: 10.1007/978-3-642-61905-2. URL https://doi.org/10.1007/978-3-642-61905-2. Series, integral calculus, theory of functions, Translated from the German by Dorothee Aeppli, Reprint of the 1978 English translation.

- Revuz and Yor [1999] Daniel Revuz and Marc Yor. Continuous martingales and Brownian motion, volume 293 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, third edition, 1999. ISBN 3-540-64325-7. doi: 10.1007/978-3-662-06400-9. URL https://doi.org/10.1007/978-3-662-06400-9.

- Robbins and Monro [1951] Herbert Robbins and Sutton Monro. A stochastic approximation method. Ann. Math. Statistics, 22:400–407, 1951. ISSN 0003-4851. doi: 10.1214/aoms/1177729586. URL https://doi.org/10.1214/aoms/1177729586.

- Robert and Casella [2004] C. P. Robert and G. Casella. Monte Carlo Statistical Methods (2nd ed.). Springer-Verlag, New York, 2004.

- Robert and Wraith [2009] Christian P Robert and Darren Wraith. Computational methods for bayesian model choice. In Aip conference proceedings, volume 1193, pages 251–262. AIP, 2009.

- Roberts and Tweedie [1996] G. O. Roberts and R. L. Tweedie. Exponential convergence of Langevin distributions and their discrete approximations. Bernoulli, 2(4):341–363, 1996. ISSN 1350-7265. URL https://doi.org/10.2307/3318418.

- Stroock and Varadhan [2006] Daniel W. Stroock and S. R. Srinivasa Varadhan. Multidimensional diffusion processes. Classics in Mathematics. Springer-Verlag, Berlin, 2006. ISBN 978-3-540-28998-2; 3-540-28998-4. Reprint of the 1997 edition.

- Vidal et al. [2019] A. Vidal, V. De Bortoli, M. Pereyra, and A. Durmus. Maximum likelihood estimation of regularisation parameters: An empirical bayesian approach. 2019. in prepration.

- Vidal and Pereyra [2018] Ana Fernandez Vidal and Marcelo Pereyra. Maximum likelihood estimation of regularisation parameters. In 2018 25th IEEE International Conference on Image Processing (ICIP), pages 1742–1746. IEEE, 2018.

- Wakefield [2013] Jon Wakefield. Bayesian and frequentist regression methods. Springer Science & Business Media, 2013.

- Williams [1991] David Williams. Probability with martingales. Cambridge Mathematical Textbooks. Cambridge University Press, Cambridge, 1991. ISBN 0-521-40455-X; 0-521-40605-6. doi: 10.1017/CBO9780511813658. URL https://doi.org/10.1017/CBO9780511813658.

Appendix A Posterior convexity

Lemma \thelemma.

For any , given by (12) is log-concave.

Appendix B Non-convex objective function

In this section we turn to the case where is non-convex. We recall that the normal space of a sub-manifold at point is given by

| (69) |

where is the tangent space of the sub-manifold at point , see [3].

Theorem 7.

Assume 1, 2, 3 and that is a dimensional connected differentiable manifold with boundary and continuously differentiable outer normal. Let , , be sequences of non-increasing positive real numbers and be a sequence of positive integers such that , and (40) are satisfied. Let be given by (35). Assume in addition that H 1 is satisfied. Then defined by (35) converges almost surely to some .

Proof.

The proof is an application of [37, Chapter 5, Theorem 2.3] using the decomposition of the error term considered in the proof of Theorem 1 and Theorem 3. Indeed we decompose the error term defined by (77) as , where is a martingale increment. Then, we only need to show that the following sums converge

| (70) |

which is established in Section C.1 and Section C.1.∎

Appendix C Postponed proofs

We first derive the following technical lemmas.

Lemma \thelemma.

Let and with then and .

Proof.

Let and with . Using that for all , we have

| (71) |

and

| (72) |

which completes the proof. ∎

Lemma \thelemma.

For any probability measures on , measurable function such that and , we have

| (73) |

Proof.

Let . The statement is trivial if . We just need to consider the case where . Define . Using [19, Definition D.3.1] we get that

| (74) | ||||

| (75) | ||||

| (76) |

which concludes the proof using that . ∎

Jensen’s inequality implies that H 1-(i) holds for with since . Appendix C implies that H 1-(ii) holds replacing by , by and by . Similarly H 1-(iii) holds replacing by and by .

C.1 Proof of Theorem 1

Consider defined for any by

| (77) |

The proof of Theorem 1 relies on the two following lemmas. We consider the following decomposition for any , , where

| (78) |

We now give upper bounds on , and .

Proof.

Using the definition of , see (36), the Markov property, H 1-(ii)-(iii), Appendix C, Jensen’s inequality and that for any and , , we have for any

| (81) | |||

| (82) | |||

| (83) | |||

| (84) | |||

| (85) | |||

| (86) |

where for the last inequality we have used Appendix C. In a similar manner, we have

| (87) |

Lemma \thelemma.

Proof.

Let . We have using the Cauchy-Schwarz inequality

| (90) | |||

| (91) | |||

| (92) |

Using the Markov property, H 1-(i)-(ii), Appendix C, Appendix C and that for any and , we obtain that

| (93) | |||

| (94) | |||

| (95) | |||

| (96) |

We now give an upper-bound on the first term in the right-hand side of (92). Consider for any the Euclidean division of by there exist and such that . Therefore using the Cauchy-Schwarz inequality we can derive the following decomposition

| (97) | ||||

| (98) | ||||

| (99) | ||||

| (100) |

Setting for any and , . We now bound the two terms in the right-hand side. First, using the Cauchy-Schwarz inequality and H 1-(i)-(iii), the fact that and that for any and , we have

| (101) | ||||

| (102) |

Now consider the solution of the Poisson equation [39, Section 17.4.1] associated with , defined for any by

| (103) |

Note that by H 1-(ii), Appendix C and since for any and , , we have that for any

| (104) |

and in addition for any

| (105) |

Therefore, we have for any

| (106) | ||||

| (107) | ||||

| (108) |

Combining the Cauchy-Schwarz inequality and (108) we obtain that

| (109) |

with

| (110) | ||||

First, using (104) and H 1-(i) we get that

| (111) | ||||

| (112) |

We now give an upper-bound on . For any let generated by and the sequence of random variables . Using the Markov property we have for any and

| (113) |

Therefore, for any , is a martingale increment with respect to , Combining this result with the Markov property implies that for any and ,

| (114) | ||||

| (115) |

Define for any , . Using (115), H 1-(ii)-(iii) and (104) we obtain that

| (116) | ||||

| (117) | ||||

| (118) | ||||

| (119) | ||||

| (120) | ||||

| (121) |

Therefore, using (112) and (121) in (109) we obtain that

| (122) |

As a consequence, using (102) and (122) in (100) we get that

| (123) | |||

| (124) | |||

| (125) | |||

| (126) |

Combining (96) and (126) in (92) we obtain that

| (127) | |||

| (128) | |||

| (129) | |||

| (130) | |||

| (131) |

which concludes the proof for . The same inequality holds in the case where . ∎

We now turn to the proof of Theorem 1.

Proof of Theorem 1.

The proof is an application of [2, Theorem 2, Theorem 3].

-

(a)

To apply [2, Theorem 2], it is enough to show that the following series converge almost surely

(132) where and the sequences and are given in (92).

In the case where , since is bounded, we are reduced to proving that almost surely . Using (40), Section C.1 and Fubini-Tonelli’s theorem we obtain that

(133) We consider the case where . Let and be defined for any by and are -martingale by definition of in (92) and in (36). Therefore, using [56, Section 12.5], the Cauchy-Schwarz inequality and that the sequence is bounded, it suffices to show that . Using Section C.1 we get that

(134) Combining this result and (133) implies the stated convergence applying [2, Theorem 2].

- (b)

∎

C.2 Proof of Theorem 2

Proof.

Taking the expectation in (135) and using that is a martingale increment with respect to , we get that for every

| (136) | |||

| (137) | |||

| (138) |

Combining this result, Section C.1 and Section C.1 completes the proof. ∎

C.3 Proof of Theorem 3

We now introduce some tools needed for the proof. By 4 and H 1-(i)-(ii), for any and , there exists a function solution of the Poisson equation,

| (139) |

defined for any by

| (140) |

Note that using H 1-(ii) and Appendix C we have for any and

| (141) |

Define for any

| (142) |

Using (139) an alternative expression of is given for any by

| (143) | ||||

| (144) |

where

| (145) | ||||

To establish Theorem 3 we need to get estimates on moments of for . It is the matter of the following technical results.

Proof.

Using (142), that for any , 1, 2, 3 and H 1-(i) and that for any and , , we get for any ,

| (147) | ||||

| (148) |

∎

Lemma \thelemma.

Proof.

Lemma \thelemma.

Proof.

By (145) we have for any and

| (155) | |||

| (156) | |||

| (157) | |||

| (158) | |||

| (159) |

In addition, we have for any , using 1, 2, that is non-expansive, (50), H 1-(i) and that for any and ,

| (160) | |||

| (161) | |||

| (162) |

- (a)

-

(b)

Assume now (54). We show that almost surely the first term in (159) is absolutely convergence and the second term converges to .

∎

Lemma \thelemma.

Proof.

We start by giving an upper-bound on for with and, . Let be a measurable function satisfying . Using H 1-(i)-(ii), H 2, Appendix C and Appendix C, we get that for any with , and

| (175) | ||||

| (176) | ||||

| (177) | ||||

| (178) | ||||

| (179) |

Taking and using H 1-(ii), we obtain that for any and with ,

| (180) |

with given by(174). In what follows we give an upper bound on for any , with and . By (140) we have for any , with and ,

| (181) | ||||

| (182) | ||||

| (183) |

We now bound each term of the series in the right hand side. For any measurable functions with and such that with , , with , and , it holds that

| (184) | ||||

| (185) | ||||

| (186) | ||||

| (187) | ||||

| (188) |

Setting and , we obtain that

| (189) |

where

| (190) | ||||

| (191) | ||||

| (192) | ||||

| (193) | ||||

| (194) | ||||

| (195) | ||||

| (196) |

For the first term in (189), using H 1-(ii), H 2, Appendix C and and that for any and , we obtain for any , with , and

| (197) | |||

| (198) | |||

| (199) | |||

| (200) |

For the first term in (195), using H 1-(ii), Appendix C, (180) and that for any and , , we obtain for any , with , and

| (201) | |||

| (202) | |||

| (203) |

For the second term in (195), using 4, H 1-(ii) and Appendix C, we obtain for any , with , and

| (204) |

Combining (195), (200), (203), (204) in (189) and using Appendix C, we obtain that for any , with , that

| (205) |

with

| (206) |

Since for any , by (50) and the fact that for any and , and that is non-expansive, we get that for any ,

| (207) |

which implies by (145) and using H 1-(i) that

| (208) |

with given by (173).

∎

Proof.

We now turn to the proof of Theorem 3.

Proof of Theorem 3.

-

(a)

To apply [2, Theorem 2], it is enough to show that the following series converge almost surely

(210) with . almost surely by Section C.3 since . Since is a -martingale increment, see (51) and by Section C.3 and

(211) we obtain using [56, Section 12.5] that converges almost surely. Using 1, (54) and Section C.3 and Section C.3 we get that is absolutely convergent almost surely for . Finally converges almost surely by Section C.3-(b).

- (b)

∎

C.4 Proof of Theorem 4

The proof is similar to the one of Theorem 2, using Section C.3, Section C.3, Section C.3, Section C.3 and the fact that is a -martingale increment, see (51).

C.5 Proof of Theorem 5

In this section, we give the proof of Theorem 5 by showing that H 1 holds. First of all in Section C.5.1, we establish under L 1 and L 2 stability results uniform in the parameter for the Langevin diffusion (7) and the associated Euler-Maruyama discretization (9) based on a Foster-Lyapunov drift condition with constants independent of . Then, in Section C.5.2, we show that the stability conditions that we derive, are sufficient to prove that H 1 holds. The proof of Theorem 5 then consists in combining all these results and is presented in Section C.5.3.

Under L 1 and L 2, for any , (7) defines a Markov semi-group for any and by where is the solution of (7) with . Consider now the generator of for any , defined for any by

| (212) |

We say that a Markov kernel on satisfies a discrete Foster-Lyapunov drift condition if there exist , and a measurable function such that for all

| (213) |

We say that a Markov semi-group on with extended infinitesimal generator (see e.g. [42] for the definition of ) satisfies a continuous drift condition if there exist , and a measurable function with such that for all

| (214) |

C.5.1 Foster-Lyapunov drift conditions uniform on

Define for all by

| (215) |

Proposition \theproposition.

Proof.

Since is -Lipschitz, by the log-Sobolev inequality [4, Proposition 5.4.1], we have for any and ,

| (219) | ||||

| (220) |

where we have used Jensen’s inequality in the last line. Second, using L 2 and , we obtain that for any and ,

| (221) | ||||

| (222) | ||||

| (223) |

Therefore, using for any , , we get for any and ,

| (224) | ||||

| (225) | ||||

| (226) |

Therefore, combining this result with (219) and using that for any , and , we obtain for any and ,

| (227) |

Using (219), (225), and the fact that for any , we have for any and ,

The proof of (216) for and is then completed upon using that for all with . ∎

Proposition \theproposition.

C.5.2 Checking H 1

Lemma \thelemma.

Assume L 1 and let satisfying and , for any , where is defined by (212). .

-

(a)

Assume that there exist , and such that for any and , associated with the recursion (63), satisfies . Then for any and , admits an invariant probability measure on and there exists such that for any and

(234) In addition, for all and , .

-

(b)

Assume that there exist and such that for any , associated with (7) satisfies . Then for any , the diffusion is non-explosive, admits as an invariant probability measure and

(235) In addition, for all and , .

Proof.

-

(a)

for any and , is irreducible with respect to the Lebesgue measure on , has the Feller property and satisfies then [41, Section 4.4] applies and admits an invariant probability measure . The discrete drift condition and [21, Lemma 1] give that for any and

(236) We obtain that for all and , using [39, Theorem 16.0.1].

-

(b)

Using and [42, Theorem 2.1] we get that the diffusion process is non-explosive and thus is defined for any and . Using [52, Corollary 10.1.4] for any , is strongly Feller continuous, therefore any compact sets is petite for the Markov kernel , for any and , by [39, Theorem 6.0.1]. Using [47, Chapter 7, Proposition 1.5], [27, Chapter 4, Theorem 9.17], and the fact that for any and , we obtain that for any , is an invariant measure for . Using and [42, Theorem 4.5] we get that for all , . Finally, the convergence is ensured using [40, Theorem 5.1].

∎

As an immediate corollary we obtain that under the conditions of Section C.5.2 for any , and ,

| (237) |

Lemma \thelemma.

Proof.

By induction we obtain that

| (239) |

where is defined by (36). Similarly, we obtain for any ,

| (240) |

Define for and , , and . In addition, consider for any , and . Combining (239), (240) and Appendix C we get for any and

| (241) | ||||

| (242) |

Since is nonincreasing and for all , , we have for all ,

| (243) | |||

| (244) | |||

| (245) |

Combining this result and (241) completes the proof. ∎

Lemma \thelemma.

Let measurable and such that . Assume L 1 and that for any , and ,

| (246) |

with . Then for any and

| (247) |

Proof.

Proposition \theproposition.

Let measurable and such that . Assume L 1 and that there exist , and such that for any and satisifies . Assume that there exists such that for any , . Then there exists such that for any and

| (252) |

Proof.

Using Section C.5.2 we obtain that for any

| (253) |

We now give an upper bound on for with and . Using [16, Theorem 6] and that is invariant for with , see Section C.5.2, we obtain for all , and

| (254) | |||

| (255) | |||

| (256) | |||

| (257) |

where are the constants given by [16, Theorem 6] with minorization condition given by [16, Proposition 8a] with since L 1 holds and drift condition , since for all and we have that satisfies and therefore using Jensen’s inequality that satisfies .

We now give an upper bound on error . Indeed, since satisfies a and satisfies for any and , we obtain using (237) that for any and

| (258) |

Combining this result and Section C.5.2 we have for any and

C.5.3 Proof of Theorem 5

Combining Section C.5.1 and Section C.5.2 we get that H 1-(i) is satisfied with constant . L 1, L 2, Section C.5.1 and Section C.5.2-(a) ensure that H 1-(ii) is satisfied by [16, Theorem 14] with . H 1-(iii) is satisfied combining Section C.5.1, Section C.5.1 and Section C.5.2 with .

C.6 Proof of Theorem 6

We preface the proof by a technical lemma.

Proposition \theproposition.

Proof.

Let , and , . Using [21, Lemma 24] we have that

| (264) | |||

| (265) | |||

| (266) |

Denote for any and , the -dimensional Gaussian distribution with mean and covariance matrix . Using that for any and ,

| (267) |

In addition, if

| (268) |

Therefore, we obtain that

| (269) |

where satisfies

| (270) | ||||

| (271) | ||||

| (272) | ||||

| (273) | ||||

| (274) |

where we have used L 3 in the last line. Using L 3 again and that by L 1, we get for any

| (275) |

with . Combining this result, and and (274) in (269), it follows that

| (276) | |||

| (277) | |||

| (278) |

This result substituted in (266) completes the proof with the fact that for any , . ∎

Proof of Theorem 6.

L 1 and L 2 ensure a uniform drift condition on , see Section C.5.1 . Note that the Lyapunov function defined by Section C.5.1 satisfies . H 2 is then a direct consequence of Section C.6 ∎