A Stochastic Composite Gradient Method with Incremental Variance Reduction

Junyu Zhang

University of Minnesota

Minneapolis, Minnesota 55455

zhan4393@umn.edu &Lin Xiao

Microsoft Research

Redmond, Washington 98052

lin.xiao@microsoft.com

Abstract

We consider the problem of minimizing the composition of a smooth

(nonconvex) function and a smooth vector mapping, where the inner mapping

is in the form of an expectation over some random variable or a finite sum.

We propose a stochastic composite gradient method that employs an

incremental variance-reduced estimator for both the inner vector mapping

and its Jacobian.

We show that this method achieves the same orders of complexity

as the best known first-order methods for minimizing expected-value and

finite-sum nonconvex functions, despite the additional outer composition

which renders the composite gradient estimator biased.

This finding enables a much broader range of applications in machine

learning to benefit from the low complexity of

incremental variance-reduction methods.

1 Introduction

We consider stochastic composite optimization problems of the form

(1)

where is a smooth and possibly nonconvex function,

is a random variable,

each is a smooth vector mapping,

and is convex and lower-semicontinuous.

A special case we will consider separately is when is a discrete random

variable with uniform distribution over .

In this case the problem is equivalent to a deterministic optimization problem

(2)

The formulations in (1) and (2)

cover a broader range of applications than classical stochastic optimization

and empirical risk minimization (ERM) problems where each is a scalar

function () and is the scalar identity map.

A well-known example is policy evaluation in reinforcement

learning (RL) [e.g., 29].

With linear value function approximation, it can be formulated as

where and are random matrix and vector generated by

a Markov decision process (MDP) [e.g., 6].

Here we have , and .

Another interesting application is risk-averse optimization

[e.g., 27, 28],

which has many applications in RL and financial mathematics.

We consider a general formulation of mean-variance trade-off:

(3)

where each is a reward function

(such as total portfolio return).

The goal of problem (3) is to maximize the average

reward with a penalty on the variance which captures the potential risk.

It can be cast in the form of (1) by using the mappings

(4)

Here, the intermediate dimension is very low, i.e., .

This leads to very little overhead in computation

compared with stochastic optimization without composition.

Besides these applications, the composition structure

in (1) and (2) are of independent

interest for research on stochastic and randomized algorithms.

For the ease of notation, we define

(5)

In addition, let and denote the gradients of and

respectively,

and denote the Jacobian matrix of at .

Then we have

In practice, computing exactly can be very costly if not impossible.

A common strategy is to use stochastic approximation:

we randomly sample a subset of from its distribution and let

(6)

However, is always a

biased estimate of unless one can replace

with the full expectation .

This is in great contrast to the classical stochastic optimization problem

(7)

where in (6) is always an unbiased gradient

estimator for the smooth part .

Using biased gradient estimators can cause various difficulties for

constructing and analyzing randomized algorithms, but is often inevitable in

dealing with more complex objective functions other than the empirical risk

[see, e.g., 5, 11, 10, 18].

As a simplest model, the analysis of randomized algorithms

for (1) may provide insights for

solving more challenging problems.

In this paper, we develop an efficient stochastic composite gradient method

called CIVR (Composite Incremental Variance Reduction),

for solving problems of the forms (1)

and (2).

We measure efficiency by the sample complexity of the individual

functions and their Jacobian , i.e., the total number of times

they need to be evaluated at some point,

in order to find an -approximate solution.

For nonconvex functions, an -approximate solution is some

random output of the algorithm that satisfies

,

where is the proximal gradient mapping

of the objective function at

(see details in Section 2).

If , then

and the criteria for -approximation becomes

.

If the objective is convex, we require

where .

For smooth and convex functions, these two notions are compatible,

meaning that the dependence of the sample complexity on in terms

of both notions are of the same order.

Table 1: Sample complexities of CIVR (Composite Incremental Variance Reduction)

Assumptions (common: and Lipschitz and smooth, thus smooth)

Table 1 summarizes the sample complexities of the CIVR

method under different assumptions obtained in this paper.

We can define a condition number for -gradient dominant functions and for -optimally strongly convex functions, then the complexities become

and

for (1) and (2) respectively.

In order to better position our contributions,

we next discuss related work and then putting these results into context.

1.1 Related Work

We first discuss the nonconvex stochastic optimization

problem (7),

which is a special cases of (1).

When and is smooth,

Ghadimi and Lan [9] developed a randomized stochastic gradient method

with iteration complexity .

Allen-Zhu [2] obtained

with additional second-order guarantee.

There are also many recent works on solving its finite-sum version

(8)

which is a special case of (2).

By extending the variance reduction techniques

SVRG [13, 33]

and SAGA [7] to nonconvex optimization,

Allen-Zhu and Hazan [3] and

Reddi et al. [23, 24, 25]

developed randomized algorithms with sample complexity

.

Under additional assumptions of gradient dominance or strong convexity,

they obtained sample complexity

,

where is a suitable condition number.

Allen-Zhu [1] and Lei et al. [15] obtained

.

Based on a new variance reduction technique called SARAH [20],

Nguyen et al. [21] and Pham et al. [22]

developed nonconvex extensions to obtain sample complexities

and

for solving the expectation and finite-sum cases respectively.

Fang et al. [8] introduced another variance reduction technique

called Spider, which can be viewed as a more general variant of SARAH.

They obtained sample complexities

and

for the two cases respectively, but require small step sizes that are

proportional to .

Wang et al. [32] extended Spider to obtain the same

complexities with constant step sizes

and under the gradient-dominant

condition.

In addition, Zhou et al. [35] obtained similar results using

a nested SVRG approach.

In addition to the above works on solving special cases of (1)

and (2), there are also considerable recent works on a

more general, two-layer stochastic composite optimization problem

(9)

where is parametrized by another random variables ,

which is independent of .

When , Wang et al. [30] derived algorithms to find

an -approximate solution

with sample complexities , and

for the smooth nonconvex case,

smooth convex case and smooth strongly convex case respectively.

For nontrivial convex , Wang et al. [31] obtained improved sample

complexity of ,

and

for the three cases mentioned above respectively.

As a special case of (9), the following finite-sum

problem also received significant attention:

(10)

When and the overall objective function is strongly convex,

Lian et al. [17] derived two algorithms based on the SVRG scheme to attain

sample complexities and

respectively,

where is some suitably defined condition number.

Huo et al. [12] also used the SVRG scheme to obtain an

complexity for the smooth nonconvex case and

for strongly convex problems with nonsmooth .

More recently, Zhang and Xiao [34] proposed a composite randomized

incremental gradient method based on the SAGA estimator

[7], which matches the best known

complexity

when is smooth and nonconvex, and obtained an improved complexity

under

either gradient dominant or strongly convex assumptions.

When applied to the special cases (1)

and (2) we focus on in this paper (),

these results are strictly worse than ours in Table 1.

1.2 Contributions and Outline

We develop the CIVR method by extending the variance reduction technique of

SARAH [20, 21, 22]

and Spider [8, 32]

to solve the composite optimization problems (1)

and (2).

The complexities of CIVR in Table 1 match

the best results for solving the non-composite

problems (7) and (8),

despite the additional outer composition and the composite-gradient

estimator always being biased.

In addition:

•

It is shown in [8] that the

complexity

is nearly optimal for the non-composite finite-sum

optimization problem (8).

Therefore, we do not expect algorithms with better complexity for solving

the more general composite finite-sum problem (2).

•

Under the assumptions of gradient dominance or strong convexity, the

complexity only appeared for the special case (8)

in the recent work [16].

Our results indicate that the additional smooth composition

in (1) and (2)

does not incur higher complexity compared with (7)

and (8),

despite the difficulty of dealing with biased estimators.

We believe these results can also be extended to the two-layer

problems (9) and (10),

by replacing with in Table 1.

But the extensions require quite different techniques and we will address them

in a separate paper.

The rest of this paper is organized as follows.

In Section 2, we introduce the CIVR method.

In Section 3, we present convergence results of CIVR

for solving the composite optimization problems (1)

and (2) and the required parameter settings.

Better complexities of CIVR under the gradient-dominant and optimally strongly

convex conditions are given in Section 4.

In Section 5, we present numerical experiments for solving

a risk-averse portfolio optimization problem (3)

on real-world datasets.

2 The composite incremental variance reduction (CIVR) method

input:

initial point , step size , number of epochs ,

and a set of triples for ,

where is the epoch length and and are sample sizes

in epoch .

fordo

Sample a set with size from the distribution of ,

and construct the estimates

(11)

Compute

and update:

.

fordo

Sample a set with size from the distribution of ,

and construct the estimates

With the notations in (5), we can write the composite

stochastic optimization problem (1) as

(14)

where is smooth and is convex.

The proximal operator of with parameter is defined as

(15)

We assume that is relatively simple, meaning that its

proximal operator has a closed-form solution or can be computed efficiently.

The proximal gradient method

[e.g., 19, 4]

for solving problem (14) is

(16)

where is the step size.

The proximal gradient mapping of is defined as

(17)

As a result, the proximal gradient method (16)

can be written as .

Notice that when , becomes the identity

mapping and we have for any .

Suppose is generated by a randomized algorithm.

We call an -stationary point in expectation if

(18)

(We assume that is a constant that does not depend on .)

As we mentioned in the introduction, we measure the efficiency of an algorithm

by its sample complexity of and their Jacobian , i.e.,

the total number of times they need to be evaluated, in order to find

a point that satisfies (18).

Our goal is to develop a randomized algorithm that has low sample

complexity.

We present in Algorithm 1 the Composite Incremental Variance

Reduction (CIVR) method.

This methods employs a two time-scale variance-reduced estimator

for both the inner function value of

and its Jacobian .

At the beginning of each outer iteration (each called an epoch),

we construct a relatively accurate estimate for and

for respectively, using a relatively large sample

size .

During each inner iteration of the th epoch, we construct an estimate

for and for respectively,

using a smaller sample size and incremental corrections from the

previous iterations.

Note that the epoch length and the sample sizes and

are all adjustable for each epoch . Therefore, besides setting a constant

set of parameters, we can also adjust them gradually in order to obtain

better theoretical properties and practical performance.

This variance-reduction technique was first proposed as part of SARAH

[20] where it is called recursive variance reduction.

It was also proposed in [8] in the form of a

Stochastic Path-Integrated Differential EstimatoR (Spider).

Here we simply call it incremental variance reduction.

A distinct feature of this incremental estimator is that the inner-loop

estimates and are biased, i.e.,

(19)

This is in contrast to two other popular variance-reduction techniques,

SVRG [13] and SAGA [7],

whose gradient estimators are always unbiased.

Note that unbiased estimators for and are not

essential here, because the composite estimator

is always biased.

3 Convergence Analysis

In this section, we present theoretical results on the convergence properties

of CIVR (Algorithm 1) when the composite function is smooth.

More specifically, we make the following assumptions.

Assumption 1.

The following conditions hold concerning problems (1)

and (2):

•

is a smooth and -Lipschitz function and its gradient is -Lipschitz.

•

Each is a smooth and -Lipschitz vector mapping and its Jacobian is -Lipschtiz.

Consequently, in (5)

is -Lipschitz and its Jacobian is -Lipschitz.

•

is a convex and lower-semicontinuous function.

•

The overall objective function is bounded below, i.e.,

.

Assumption 2.

For problem (1), we further assume that

there exist constants and such that

(20)

As a result of Assumption 1,

is smooth and is -Lipschitz continuous with

(see proof in the supplementary materials).

For convenience, we also define two constants

(21)

It is important to notice that , since we will use step size

.

In the next two subsections, we present complexity analysis of CIVR for

solving problem (1) and (2) respectively.

Due to the space limitation,

all proofs are provided in the supplementary materials.

3.1 The composite expectation case

The following results for solving problem (1) are presented

with notations defined in (5),

(17) and (21).

Theorem 1.

Suppose Assumptions 1 and 2 hold.

Given any ,

we set and

Then as long as ,

the output of Algorithm 1 satisfies

(22)

As a result, the sample complexity of obtaining an -approximate

solution is .

Note that in the above scheme, the epoch lengths and

all the batch sizes and are set to be constant (depending on a

pre-fixed ) without regard of .

Intuitively, we do not need as many samples in the early stage of the algorithm

as in the later stage.

In addition, it will be useful in practice to have a variant of the algorithm

that can adaptively choose , and throughout the epochs

without dependence on a pre-fixed precision.

This is done in the following theorem.

Theorem 2.

Suppose Assumptions 1 and 2 hold.

We set and

where and .

Then as long as , we have

for any ,

(23)

As a result, obtaining an -approximate solution requires epochs and a total sample complexity of , where the notation hides logarithmic factors.

3.2 The composite finite-sum case

In this section, we consider the composite finite-sum optimization

problem (2).

In this case, the random variable has a uniform distribution over

the finite index set .

At the beginning of each epoch in Algorithm 1,

we use the full sample size

to compute and .

Therefore for all and

Equation (11) in Algorithm 1 becomes

(24)

Also in this case, we no longer need Assumption 2.

Theorem 3.

Suppose Assumptions 1 holds.

Let the parameters in Algorithm 1 be set as

and

for all .

Then as long as ,

we have for any ,

(25)

As a result, obtaining an -approximate solution requires

epochs and a total sample complexity of .

Similar to the previous section, we can also choose the epoch lengths and

sample sizes adaptively to save the sampling cost in the early stage of

the algorithm.

However, due to the finite-sum structure of the problem, when the batch size reaches , we will start to take the full batch at the beginning of each

epoch to get the exact and .

This leads to the following theorem.

Theorem 4.

Suppose Assumptions 1 holds.

For some positive constants and ,

denote .

When we set the parameters to be ; when , we set and .

Then as long as ,

(26)

As a result,

the total sample complexity of Algorithm 1 for

obtaining an -approximate solution is

, where hides logarithmic factors.

4 Fast convergence rates under stronger conditions

In this section we consider two cases where fast linear convergence can be guaranteed for CIVR.

4.1 Gradient-dominant function

The first case is when and

is -gradient dominant, i.e., there is some such that

(27)

Note that a -strongly convex function is -gradient dominant by this definition. Hence strong convexity is a special case of the gradient dominant condition, which in turn is a special case of the Polyak-Łojasiewicz condition with the Łojasiewicz exponent equal to 2

[see, e.g., 14].

In order to solve (1) with a pre-fixed precision ,

we use a periodic restart strategy depicted below.

Theorem 5.

Consider (1) with . Suppose

Assumptions 1 and 2 hold

and is -gradient dominant.

Given any , let

,

and

.

Then as long as ,

(28)

Therefore, we can periodically restart Algorithm 1 after

every epochs

(using the output of previous period as input to the new period),

then converges linearly to

with a factor of per period.

As a result, the sample complexity for finding an -solution is

.

The restart strategy also applies to the finite-sum case.

Theorem 6.

Consider problem (2) with .

Suppose Assumption 1 hold and is -gradient dominant.

If we set and

,

then as long as ,

(29)

By periodically restart Algorithm 1 after every epochs,

converges linearly to .

As a result, the sample complexity for finding an -solution is

.

4.2 Optimally strongly convex function

In this part, we assume a -optimally strongly convex condition

on the function , i.e., there exists a such that

(30)

We have the following two results for solving problems (1)

and (2) respectively.

Theorem 7.

Consider problem (1).

Suppose Assumptions 1 and 2 hold

and is -optimally strongly convex.

We set ,

and .

Then if we choose ,

(31)

By periodically restart Algorithm 1 after every epochs,

converges linearly to

As a result, the sample complexity for finding an -solution is

.

Theorem 8.

Consider the finite-sum problem (2).

Suppose Assumption 1 hold and is -optimally

strongly convex.

We set

and .

If , then

(32)

By periodically restart Algorithm 1 after every epochs,

converges linearly to with rate .

Therefore, the sample complexity of finding an -solution is

.

If we define a condition number , then

since , we have and the above

complexities become

and .

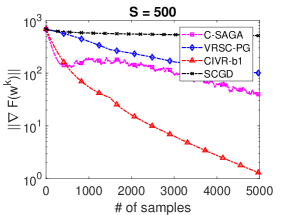

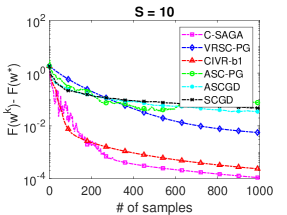

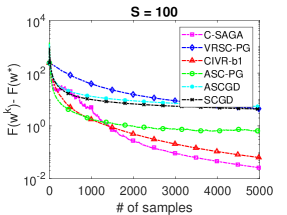

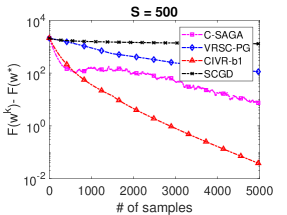

5 Numerical Experiments

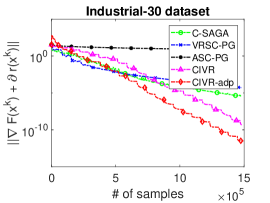

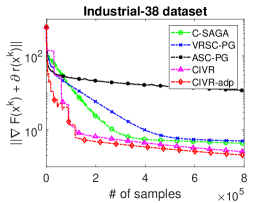

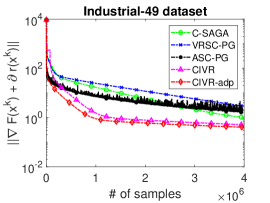

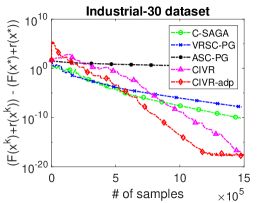

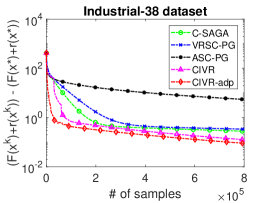

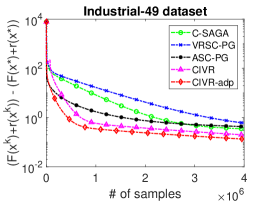

Figure 1: Experiments on the risk-averse portfolio optimization problem.

In this section, we present numerical experiments for a risk-averse

portfolio optimization problem.

Suppose there are assets that one can invest during time periods

labeled as .

Let be the return or payoff per unit of asset at time ,

and be the vector consists of .

Let be the decision variable, where each component represent

the amount of investment or percentage of the total investment allocated

to asset , for .

The same allocations or percentages of allocations are repeated over

the time periods. We would like to maximize the average return over

the periods, but with a penalty on the variance of the returns

across the periods

(in other words, we would like different periods to have similar returns).

This problem can be formulated as a finite-sum version of

problem (3),

with a discrete random variable

and for .

The function can be chosen as the indicator function

of an ball, or a soft regularization term.

We choose the later one in our experiments to obtain a sparse asset allocation.

Using the mappings defined in (4), it can be further

transformed into the composite finite-sum problem (2),

hence readily solved by the CIVR method.

For comparison,

we implement the C-SAGA algorithm [34] as a benchmark.

As another benchmark, this problem can also be formulated as a two-layer

composite finite-sum problem (10), which was done

in [12] and [17]. We solve the two-layer formulation

by ASC-PG [31] and VRSC-PG [12].

Finally, we also implemented CIVR-adp, which is the adaptive sampling variant

described in Theorem 4.

We test these algorithms on three real world portfolio datasets, which contain 30, 38 and 49 industrial portfolios respectively,

from the Keneth R. French Data Library111http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html.

For the three datasets, the daily data of the most recent 24452, 10000 and 24400 days are extracted respectively to conduct the experiments.

We set the parameter in (3)

and use an regularization .

The experiment results are shown in Figure 1.

The curves are averaged over 20 runs and are plotted against the number of samples of the component functions (the horizontal axis).

Throughout the experiments, VRSC-PG and C-SAGA algorithms use the batch size

while CIVR uses the batch size

, all dictated by their complexity theory.

CIVR-adp employs the adaptive batch size

for .

For Industrial-30 dataset, all of VRSC-PG, C-SAGA, CIVR and CIVR-adp use the

same step size .

They are chosen from the set

by experiments.

And works best for all four tested methods simultaneously.

Similarly, is chosen for the Industrial-38 dataset

and is chosen for the Industrial-49 dataset.

For ASC-PG, we set its step size parameters and

[see details in 31].

They are hand-tuned to ensure ASC-PG converges fast among a range of tested parameters.

Overall, CIVR and CIVR-adp outperform other methods.

References

Allen-Zhu [2017]

Zeyuan Allen-Zhu.

Natasha: Faster non-convex stochastic optimization via strongly

non-convex parameter.

In Proceedings of the 34th International Conference on Machine

Learning (ICML), volume 70 of Proceedings of Machine Learning

Research, pages 89–97, Sydney, Australia, 2017.

Allen-Zhu [2018]

Zeyuan Allen-Zhu.

Natasha 2: Faster non-convex optimization than SGD.

In Advances in Neural Information Processing Systems 31, pages

2675–2686. Curran Associates, Inc., 2018.

Allen-Zhu and Hazan [2016]

Zeyuan Allen-Zhu and Elad Hazan.

Variance reduction for faster non-convex optimization.

In Proceedings of the 33rd International Conference on Machine

Learning (ICML), pages 699–707, 2016.

Beck [2017]

Amir Beck.

First-Order Methods in Optimization.

MOS-SIAM Series on Optimization. SIAM, 2017.

Chaudhari et al. [2016]

Pratik Chaudhari, Anna Choromanska, Stefano Soatto, Yann LeCun, Carlo Baldassi,

Christian Borgs, Jennifer Chayes, Levent Sagun, and Riccardo Zecchina.

Entropy-sgd: Biasing gradient descent into wide valleys.

arXiv preprint, arXiv:1611.01838, 2016.

Dann et al. [2014]

Christoph Dann, Gerhard Neumann, and Jan Peters.

Policy evaluation with temporal differences: a survey and comparison.

Journal of Machine Learning Research, 15(1):809–883, 2014.

Defazio et al. [2014]

Aaron Defazio, Francis Bach, and Simon Lacoste-Julien.

SAGA: A fast incremental gradient method with support for

non-strongly convex composite objectives.

In Advances in Neural Information Processing Systems 27, pages

1646–1654, 2014.

Fang et al. [2018]

Cong Fang, Chris Junchi Li, Zhouchen Lin, and Tong Zhang.

Spider: Near-optimal non-convex optimization via stochastic

path-integrated differential estimator.

In Advances in Neural Information Processing Systems 31, pages

689–699. Curran Associates, Inc., 2018.

Ghadimi and Lan [2013]

Saeed Ghadimi and Guanghui Lan.

Stochastic first- and zeroth-order methods for nonconvex stochastic

programming.

SIAM Journal on Optimization, 23(4):2341–2368, 2013.

Gulcehre et al. [2016]

Caglar Gulcehre, Marcin Moczulski, Francesco Visin, and Yoshua Bengio.

Mollifying networks.

arXiv preprint, arXiv:1608.04980, 2016.

Hazan et al. [2016]

Elad Hazan, Kfir Yehuda Levy, and Shai Shalev-Shwartz.

On graduated optimization for stochastic non-convex problems.

In International conference on machine learning, pages

1833–1841, 2016.

Huo et al. [2018]

Zhouyuan Huo, Bin Gu, Ji Jiu, and Heng Huang.

Accelerated method for stochastic composition optimization with

nonsmooth regularization.

In Proceedings of the 32nd AAAI Conference on Artificial

Intelligence, pages 3287–3294, 2018.

Johnson and Zhang [2013]

Rie Johnson and Tong Zhang.

Accelerating stochastic gradient descent using predictive variance

reduction.

In Advances in Neural Information Processing Systems 26, pages

315–323, 2013.

Karimi et al. [2016]

Hamed Karimi, Julie Nutini, and Mark Schmidt.

Linear convergence of gradient method and proximal-gradient methods

under the Polyak-Łojasiewicz condition.

In Machine Learning and Knowledge Discovery in Database -

European Conference, Proceedings, pages 795–811, 2016.

Lei et al. [2017]

Lihua Lei, Cheng Ju, Jianbo Chen, and Michael I Jordan.

Non-convex finite-sum optimization via SCSG methods.

In Advances in Neural Information Processing Systems 30, pages

2348–2358. Curran Associates, Inc., 2017.

Li and Li [2018]

Zhize Li and Jian Li.

A simple proximal stochastic gradient method for nonsmooth nonconvex

optimization.

In Advances in Neural Information Processing Systems 31, pages

5564–5574. Curran Associates, Inc., 2018.

Lian et al. [2017]

Xiangru Lian, Mengdi Wang, and Ji Liu.

Finite-sum composition optimization via variance reduced gradient

descent.

In Proceedings of the 20th International Conference on

Artificial Intelligence and Statistics (AISTATS), pages 1159–1167, 2017.

Mobahi and Fisher [2015]

Hossein Mobahi and John W Fisher.

On the link between gaussian homotopy continuation and convex

envelopes.

In International Workshop on Energy Minimization Methods in

Computer Vision and Pattern Recognition, pages 43–56. Springer, 2015.

Nguyen et al. [2017]

Lam M. Nguyen, Jie Liu, Katya Scheinberg, and Martin Takáč.

SARAH: A novel method for machine learning problems using

stochastic recursive gradient.

In Doina Precup and Yee Whye Teh, editors, Proceedings of the

34th International Conference on Machine Learning (ICML), volume 70 of

Proceedings of Machine Learning Research (PMLR), pages 2613–2621,

Sydney, Australia, 2017.

Nguyen et al. [2019]

Lam M. Nguyen, Marten van Dijk, Dzung T. Phan, Phuong Ha Nguyen, Tsui-Wei Weng,

and Jayant R. Kalagnanam.

Finite-sum smooth optimization with sarah.

arXiv preprint, arXiv:1901.07648, 2019.

Pham et al. [2019]

Nhan H. Pham, Lam M. Nguyen, Dzung T. Phan, and Quoc Tran-Dinh.

ProxSARAH: An efficient algorithmic framework for stochastic

composite nonconvex optimization.

arXiv preprint, arXiv:1902.05679, 2019.

Reddi et al. [2016a]

Sashank J. Reddi, Ahmed Hefny, Suvrit Sra, Barnabas Poczos, and Alex Smola.

Stochastic variance reduction for nonconvex optimization.

In Proceedings of The 33rd International Conference on Machine

Learning, volume 48 of Proceedings of Machine Learning Research,

pages 314–323, New York, New York, USA, 2016a.

Reddi et al. [2016b]

Sashank J Reddi, Suvrit Sra, Barnabás Póczos, and Alex Smola.

Fast incremental method for smooth nonconvex optimization.

In 2016 IEEE 55th Conference on Decision and Control (CDC),

pages 1971–1977. IEEE, 2016b.

Reddi et al. [2016c]

Sashank J Reddi, Suvrit Sra, Barnabás Póczos, and Alexander J Smola.

Proximal stochastic methods for nonsmooth nonconvex finite-sum

optimization.

In Advances in Neural Information Processing Systems 29, pages

1145–1153, 2016c.

Rockafellar [1970]

R. Tyrrell Rockafellar.

Convex Analysis.

Princeton University Press, 1970.

Rockafellar [2007]

R. Tyrrell Rockafellar.

Coherent approaches to risk in optimization under uncertainty.

INFORMS TutORials in Operations Research, 2007.

Ruszczyński [2013]

Andrzej Ruszczyński.

Advances in risk-averse optimization.

INFORMS TutORials in Operation Research, 2013.

Sutton and Barto [1998]

Richard S Sutton and Andrew G Barto.

Reinforcement Learning: An Introduction.

MIT Press, Cambridge, MA, 1998.

Wang et al. [2017a]

Mengdi Wang, Ethan X Fang, and Han Liu.

Stochastic compositional gradient descent: algorithms for minimizing

compositions of expected-value functions.

Mathematical Programming, 161(1-2):419–449, 2017a.

Wang et al. [2017b]

Mengdi Wang, Ji Liu, and Ethan Fang.

Accelerating stochastic composition optimization.

Journal of Machine Learning Research, 18(105):1–23, 2017b.

Wang et al. [2018]

Zhe Wang, Kaiyi Ji, Yi Zhou, Yingbin Liang, and Vahid Tarokh.

SpiderBoost: A class of faster variance-reduced algorithms for

nonconvex optimization.

arXiv preprint, arXiv:1810.10690, 2018.

Xiao and Zhang [2014]

Lin Xiao and Tong Zhang.

A proximal stochastic gradient method with progressive variance

reduction.

SIAM Journal on Optimization, 24(4):2057–2075, 2014.

Zhang and Xiao [2019]

Junyu Zhang and Lin Xiao.

A composite randomized incremental gradient method.

In Proceedings of the 36th International Conference on Machine

Learning (ICML), number 97 in Proceedings of Machine Learning Research

(PMLR), Long Beach, California, 2019.

Zhou et al. [2018]

Dongruo Zhou, Pan Xu, and Quanquan Gu.

Stochastic nested variance reduced gradient descent for nonconvex

optimization.

In Advances in Neural Information Processing Systems 31, pages

3921–3932. Curran Associates, Inc., 2018.

Appendices

Appendix A Convergence analysis for composite expectation case

In this section, we focus on convergence analysis of CIVR for solving the

stochastic composite optimization problem (1),

and prove Theorems 1

and 2.

First, we show that under Assumption 1, the composite

function is smooth and has Lipschitz constant

.

where we used and ,

which are implied by the Lipschitz conditions on and respectively.

Although the incremental estimators used in CIVR are biased,

as shown in (19),

we can still bound their squared distances from the targets.

This is given in the following lemma.

Lemma 1.

Suppose Assumption 1 holds.

Let and be constructed according to (11)

and (12) in Algorithm 1.

For any and ,

we have the following mean squared error (MSE) bounds

(33)

Proof.

We first state a fact that allows us to decompose the MSE into a squared

bias term and a variance term, that is, for an arbitrary random vector

and a constant vector , we have

(34)

where . As a result,

For the bias term, we have . For the variance term, we have

where the second equality is due to the fact that is a constant

conditioning on and in the last inequality we used the

-Lipschitz continuity of . Consequently,

Recursively applying the above procedure yields

(35)

Similarly, the bound on can be shown by using the -Lipschitz continuity of .

∎

In Algorithm 1, we approximate the gradient of

by .

The next lemma bounds the MSE of this estimator.

Therefore, by substituting the MSE bounds provided in Lemma 1 into inequality (37), we obtain

(38)

Under Assumption 2, we can bound the MSE of

the estimates in (11) as

Combining these MSE bounds with (38) yields

the desired result.

∎

For the proximal gradient type of algorithms, no matter deterministic or stochastic, a common metric to quantify the optimality of is the norm of the so-called proximal gradient mapping

(39)

where is the step size used to produce the update

Since we use a constant throughout this paper, we will omit

the subscript and use to denote the

proximal gradient mapping at .

Our goal is to find a point with

.

However, in Algorithm 1,

we only have the approximate proximal gradient mapping

(40)

where is computed using the estimated gradient :

Hence we need to establish the connection between and ,

which is done in the next lemma.

Lemma 3.

For the two gradient mappings defined in (39) and (40),

we have

(41)

Proof.

Using the inequality

and the definitions of and , we have

where in the second inequality we used the non-expansive property of

proximal mapping [e.g., 26, Section 31].

∎

The next lemma bounds the amount of expected descent per iteration

in Algorithm 1.

Lemma 4.

Let the sequence be generated by Algorithm 1.

Then for all and ,

we have the following two inequalities

(42)

and

(43)

Proof.

By applying the -Lipschitz continuity of and the optimality of the -strongly convex subproblem, we have

Taking the expectation on both sides completes the proof of inequality (42). By inequality (41), we know that

Because all , and are taking their values independent of . We denote , and for all for clarity. By Lemma 4, summing up inequality (43) throughout the -th epoch and applying (36) gives

where the second inequality is due to the fact that

When we choose the parameters satisfying , then the coefficient which depends only on the parameter and some constant. If we choose the according to the theorem, then , yielding that

(44)

Summing this up throughout the epochs gives

where we have applied the fact that . By the random sampling scheme for output , we have

Note that for this set of parameters, we still have the relationship that . Therefore, within each epoch, (44) is still true with epoch specific and . Summing this up gives

(46)

By the random selection rule of , we have

(47)

Note that and We have

and

Substituting the above bounds into inequality (47) gives (23). As a result,

the total sample complexity is

Setting so that , we get sample complexity

.

∎

We can also choose a different set of parameters.

With , and letting , and , we also have

but the sample complexity, by setting so that the above bound is less than , is

This is more close to the classical results on stochastic optimization.

Appendix B Convergence analysis for composite finite-sum case

In this section, we consider the composite finite-sum problem (2) and prove Theorems 3 and 4.

In this case, the random variable uniformly takes value from the finite

index set .

At the beginning of each epoch in Algorithm 1, we can choose to

estimate and by their exact value rather than the approximate ones constructed by subsampling.

Namely, in (11) of Algorithm 1,

we choose for all .

Therefore,

and

(48)

As a result, the initial variances in Lemma 1 diminishes

and (33) reduces to

The proof follows similar steps as those in the proof of

Theorem 1.

So we only note down the significantly different steps here.

Specifically, following the proof of Theorem 1 in Section A.1, by applying (49) instead of (33), we get the following result instead of inequality (44),

Summing this up apply the random selection rule of gives

Therefore, we have to set to get an -solution. Note that the sample complexity per epoch is , the total sample complexity will be

.

∎

If , then the result is exactly what we proved from Theorem 2. Therefore, the first bound in (26) is already guaranteed.

If , when , then everything still runs identically to that described in Theorem 2. Consequently, the following bound is effective

(51)

When , the following bound becomes effective,

Therefore, we have

Note that

and

With the above two bounds, we have proved the second result in (26).

For any , if In this case, the algorithm will spend most epochs in the adaptive phase, whose sample complexity is . if , we need . By (26), we know

, this means that the total sample complexity will be

When , we have . When , we have . Combining the two cases together gives the sample complexity of .

∎

Appendix C Convergence analysis under gradient-dominant condition

Suppose we periodically restart the Algorithm 1 after every epochs, and set the outputs to be , where denotes

the number of restarts.

We use the output of the th period as the initial point

to start the next period, which produces .

As a result, the above inequality translates to

Equivalently,

which leads to

Therefore, the expected optimality gap converges linearly to a -ball around 0.

∎

Next we discuss the sample complexity with different parameter settings.

•

If we choose , , and ,

then the total sample complexity is

However, the above derivation needs to assume or at least , which means .

If this condition is not satisfied, then we have and the complexity is

Notice that the second term does not depend on or the conditions number.

•

If we choose , , and ,

the we also have

and the total sample complexity is

Defining the condition number , the above complexity becomes

Thus when , we have for deterministic optimization.

The proof is very similar to the previous one.

It actually becomes simpler by noticing that in the finite-sum case,

the terms involving disappear.

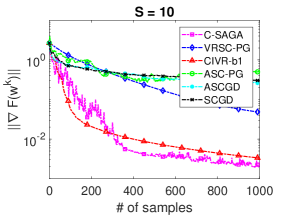

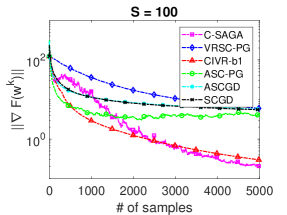

Appendix E Numerical experiments on policy evaluation for MDP

Figure 2: Experiments on policy evaluation for MDP for

cases with , and .

Here we provide additional numerical experiments on the policy

evaluation problem for MDP.

Let be the state space of some Markov decision process. Suppose a reward of is received after transitioning

from state to state .

Let be the transition probability matrix under some fixed policy . Then the evaluation of the value function under such policy is equivalent to solving the following Bellman equation:

Following the suggestion of [6, 31], we apply the linear function approximation

for a given set of feature vectors .

and would like to compute the optimal vector .

This can be formulated as the following problem

Let’s denote

Then by defining

and

the Least squares problem is transformed into the form of (2).

For this problem, we test the SCGD [30], the ASCGD

[30], the ASC-PG [31], the VRSC-PG

[12], C-SAGA [34] and our CIVR algorithms.

In Section 5, we already tested the algorithms under their

standard batch sizes, e.g. and .

However, small constant batch sizes are often preferred in practice. Therefore,

we would like to set the batch size to for all algorithms. For this

special case, we denote the CIVR as the CIVR-b1. To balance the sample

complexity between the initial full batch sampling and the later subsampling

with , we set the epoch length for VRSC-PG and CIVR-b1 to be .

Note that the last components of are all independent expectations,

therefore the variance reduction technique of VRSC-PG [12],

C-SAGA [34] and CIVR-b1 applied to each of these

components.

In the experiments, , and are generated randomly.

Similar to the experiments performed in Section 5,

the step sizes are chosen from by experiments for VRSC-PG, C-SAGA as

well as for CIVR-b1. For , works best for both C-SAGA and

CIVR-b1, while works best for VRSC-PG; For , works best for both C-SAGA and CIVR-b1, while works

best for VRSC-PG. For , works best for all three of

them.

When and , we choose and for SCGD, and

for ASCGD and and for ASC-PG.

When , we choose and for SCGD while ASCGD and ASC-PG fail to converge under various

trials of parameters. The meaning of these step size parameters can be found in

[31] and [30].

Figure 2 shows three experiments with sizes , and respectively.

We can see that both C-SAGA and CIVR-b1 preform much better than other

algorithms in our setting.

CIVR-b1 has more smooth and stable trajectory than C-SAGA.