Sample-constrained partial identification with application to selection bias

Abstract

Many partial identification problems can be characterized by the optimal value of a function over a set where both the function and set need to be estimated by empirical data. Despite some progress for convex problems, statistical inference in this general setting remains to be developed. To address this, we derive an asymptotically valid confidence interval for the optimal value through an appropriate relaxation of the estimated set. We then apply this general result to the problem of selection bias in population-based cohort studies. We show that existing sensitivity analyses, which are often conservative and difficult to implement, can be formulated in our framework and made significantly more informative via auxiliary information on the population. We conduct a simulation study to evaluate the finite sample performance of our inference procedure and conclude with a substantive motivating example on the causal effect of education on income in the highly-selected UK Biobank cohort. We demonstrate that our method can produce informative bounds using plausible population-level auxiliary constraints. We implement this method in the R package selectioninterval.

1 Introduction

1.1 General problem

Partial identification problems arise when the observable data are only sufficient to identify a set or interval in which a parameter of interest is contained. A classical example from [15] is the missing data problem, where is a discrete random variable and is a binary random variable indicating whether is observed () or not (). The distribution of can be decomposed into

| (1) |

for any in the support of . Given that is unobserved, the smallest value that could take is and the largest value is . Therefore, although itself cannot be point identified, it can be partially identified via the interval corresponding to the smallest and largest possible values.

As with the missing data example, many partial identification problems can be formulated as the optimal value of a population objective function, which we write as

| (2) |

where and .

The field of stochastic optimization also considers problems of the form in (2) and has built a large literature on estimation of, and inference to, when a sample analogue is observed instead of (where denotes the sample size). It will be convenient for us to frame the partial identification problem as a stochastic optimization problem and draw upon these existing results.

In this article we are primarily concerned with the more difficult setting where must also be estimated empirically. We specifically consider a setting where is characterized by inequality constraints of the form , where we may only observe corresponding estimators . Within this setting, our goal is to find a lower confidence bound for any such that

| (3) |

which will suffice to provide useful statistical inference in a wide set of applications.

1.2 Motivating application

Our investigation is motivated by an applied question: how will selection bias affect the conclusions of population-based cohort studies? Many statistical analyses begin by selecting a study sample from some population of interest. When the sample is drawn non-randomly, then valid inference for the population is no longer guaranteed [4]. Inverse probability weighting could be used to correct for this selection bias [12, 23], but data on non-selected observations may be limited or unavailable altogether, such that the weights cannot be estimated. In such settings, there exist approaches to assess the sensitivity of estimates to a range of plausible inverse probability weights [3, 24]. However, these approaches could be made more informative via a principled procedure for conducting statistical inference and the inclusion of relevant auxiliary information about the population. We demonstrate that such improvements can be made by casting these sensitivity analyses within the general framework described in Section 1.1.

We are specifically motivated by studies conducted in UK Biobank, which is a large population-based cohort study widely analysed by health researchers. Studies of this cohort are potentially biased since recruited participants are known to differ systematically from the rest of the UK population on measures such as education, health status, age and geographical location [10, 13].

1.3 Existing literature

Statistical inference procedures have been developed for some special cases of our general problem in eq. 3. An area of particular focus is the so-called ‘sample average approximation’ [21]. In this case, is the expected value of some function and is a sample average , where is some random variable and are independent draws of .

Statistical inference in the presence of has been developed for convex sample average approximations, such that is convex in and where and is convex in for all . [20] shows that the plug-in estimator

| (4) |

satisfies a central limit theorem under these convexity assumptions (and some additional regularity conditions), where .

Moving away from convex problems, [25] consider the special case of minimizing a known function subject to a single expected value constraint . Their approach consists of computing and introducing , where represents a (small) deviation from the true problem. Sample size is then selected so that is sufficiently close to one.

This work also overlaps with the partial identification literature in econometrics, much of which considers inference for identified sets characterized by conditional or unconditional moment inequalities, commonly interpreted as the set of minimizers of some criterion function [6, 2, 1]. A related literature provides inference for parameters lying within partially identified sets, as opposed to inference for the set itself [14, 22]. For a more comprehensive review of the partial identification literature, see [17].

2 Confidence intervals for sample-constrained partial identification

2.1 Confidence intervals under known constraints

In this section, we briefly summarize existing results on statistical inference for stochastic optimization when the set is observed, which forms the basis of our generalization to situations where an estimate of is observed instead. Suppose the parameter space is defined by a set of inequality constraints

| (5) |

where an equality constraint for some can be introduced by taking the inequality constraints of both and . Recall that our goal is to provide inference about the infimum .

Much of the literature in stochastic optimization is centered on the statistical properties of the estimator

| (6) |

Consistency of optimal values and optimal solutions to such stochastic optimization problems is typically achieved by imposing uniform convergence of to . First order asymptotic properties are obtained via the functional delta method. The key conditions are that the infimum, viewed as a function of , satisfies some notion of differentiability at (see [20] for technical details) and that converges to a Gaussian process.

To make the previous discussion more concrete, consider the following four assumptions commonly placed on the stochastic optimization problem described above.

Assumption 1.

The set of solutions to (2) is a singleton .

Assumption 2.

Let denote a compact set and denote the space of continuous functions on domain . Then , and with probability one.

Assumption 3.

converges to with probability one as uniformly on .

Assumption 4.

As , the sequence converges in distribution to a random element , where is Gaussian process with mean 0 and variance .

These assumptions are jointly sufficient to achieve consistency and asymptotic normality of .

Proposition 2.1.

Proposition 2.1 is identical to Theorem 5.3 in [21] under the condition that is unique.

Proposition 2.2.

Proposition 2.2 is an immediate consequence of Theorem 3.2 in [20]. Although we do not restate the proof here, the intuition is that Assumptions 1 and 2 allow a notion of differentiability of the infimum and 4 provides weak convergence of to a Gaussian process, thus providing the conditions needed for an application of the delta method.

To use Proposition 2.2 to construct a valid confidence interval, we must take into consideration that both and are unknown. To this end, we state an additional assumption followed by a proposition.

Assumption 5.

There exists a uniformly strongly consistent estimator for such that with probability one.

The proof is located in Appendix D. 5 applies uniform convergence to an estimator for the asymptotic variance of . This strong notion of convergence for allows us to construct a confidence bound of the form

| (8) |

where is the upper -quantile of the standard normal distribution. This choice of has asymptotically exact nominal coverage by Proposition 2.2, Proposition 2.3 and Slutsky’s theorem.

2.2 Confidence intervals under sample constraints

We now consider the more difficult setting where the constraint functions need to be estimated as well. We instead observe an estimator comprised of estimators of the constraint functions . We will discuss what properties must have to allow valid statistical inference for .

It is tempting to follow the approach of the previous section and construct a plug-in estimator for by simply replacing with and with and finding the corresponding infimum (this is in eq. 4). The problem with this approach is that may lie inside with very low probability, even asymptotically. This will prohibit the construction of a valid confidence interval for as illustrated by the contrived example below.

Example 2.1.

Consider a problem of the form and where is a normally-distributed random variable. The plug-in estimators are and , where is the mean of independent and identically distributed draws of . It follows that and , where is the plug-in estimator (4). The asymptotic variance of is , which we assume is known. The resulting confidence bound is , where is the confidence bound (3). A simple Monte Carlo simulation demonstrates that the corresponding 95% confidence interval for exhibits sub-nominal coverage of around 70%.

Existing approaches in stochastic optimization address the problem in Example 2.1 by restricting to sample average approximations and imposing convexity of both and . To allow inference for a broader class of problems, we propose an intuitive but conservative approach which replaces with an appropriate relaxation. In particular, we propose to use the relaxed set

| (9) |

where is some -dimensional sequence such that for all , chosen so that

| (10) |

for some . The exact forms of and are not crucial for our main results, provided (10) holds, which we discuss in more detail toward the end of this section.

Our proposed confidence bound is of the form for some , where is the upper -quantile of the standard normal distribution. We need to select a so that eq. 3 is satisfied. This is accomplished by finding the optimal value and solution over the relaxed constraint set,

| (11) |

and constructing a confidence bound of the form

| (12) |

We now need to demonstrate that covers with known probability in the limit. To this end, we need an additional technical assumption to hold.

Assumption 6.

Let be the optimal solution of over , then converges to in probability.

6 is imposed so that two important quantities become asymptotically close. The first quantity is , which is the infimum over all confidence bounds in . This confidence bound is important because it provides a lower bound for other quantities with known coverage probabilities, which is a fact we utilize in our main result in Theorem 2.1. The second quantity is , which is our main confidence bound proposed in (12).

We argue that 6 is reasonable in the sense that and are solutions over two objective functions which converge uniformly to the same limit. To make this intuition more concrete, we provide some sufficient conditions for 6 in Appendix B and prove their sufficiency in Lemma D.2. Essentially, if 3 is satisfied and and converge to and 0 for all uniformly on with probability one, then we can show that both and converge to with probability one.

We claim that provides an asymptotically valid lower confidence bound.

Theorem 2.1.

The proof of Theorem 2.1 can be found in Appendix D. Here we outline the key steps in the proof. We begin by defining a deterministic sequence where is some small constant. We then show that is bounded from below by the sum of two quantities: and . The second quantity converges to under 6. The remainder of the proof follows a similar argument to the main lemma of [5]. Whenever , we know that , which is the infimum over all confidence bounds in , will cover at least as often as , which is the confidence bound (8). Therefore, . We also know that by the law of total probability. In the limit, the first probability on the right-hand side is equal to by Proposition 2.2 and the second probability is at most by assumption. This allows us to arrive at our main result.

The proof sketch also provides some insight into why the naive plug-in estimator defined in eq. 4 may fail to yield a valid confidence interval. A crucial quantity is , which is known under an appropriate choice of . The corresponding quantity for the plug-in estimator is , which could be arbitrarily small. In Example 2.1, this probability is zero.

It remains to discuss how to construct a relaxed set . Whenever can be characterized by a set of moment inequalities (i.e. whenever ), the moment inequalities literature summarized in Section 1.3 could be used to construct . A more conservative relaxed set could be constructed via an application of the intersection bound. Suppose the following assumption holds on the constraint functions:

Assumption 7.

For all and , in distribution and is a consistent estimator for .

This fairly weak assumption means that is pointwise asymptotically normally distributed and that there is a consistent estimator for the variance. This assumption allows us to select

where . It is straightforward to show that this choice of satisfies (10). We could shrink the size of by assuming that converges pointwise to a multivariate Gaussian with covariance matrix and consistent estimator . This would allow us to construct as an ellipsoid confidence region.

Remark 2.1.

It remains to discuss how one would select and . As a rule-of-thumb, we typically choose the midpoint . It is tempting to select and choose as the largest confidence bound over all and satisfying this equality. This would mean that and are sample-dependent quantities and so Theorem 2.1 will not directly apply. However, we can reason heuristically that the best choice of and should lie at an interior point and . For a fixed sample, as and , and thus approaches the confidence interval over the unconstrained problem. As and , and thus the confidence interval becomes arbitrarily wide.

Remark 2.2.

So far we have focused on inference for the infimum, however, partial identification problems are often characterized by an identified set of the form , where and [14, 7]. Suppose is chosen so that . Moreover, let and denote the optimal values and and denote the corresponding optimal solutions. The estimated interval can be written as and we can construct a confidence interval by combining the lower confidence bound for and the upper confidence bound for , so that

will cover with probability at least . This is the two-sided analogue of the one-sided confidence interval proposed in eq. 12 and Theorem 2.1.

3 Sensitivity analysis via a logistic model

3.1 Set-up

We now return to the motivating example of selection bias in population-based cohort studies briefly described in Section 1.2. Specifically, we generalize the sensitivity analysis proposed in [24], who define a logistic model for the probability of sample selection and propose to select parameters based on domain knowledge, or enumerate a large number of possible parameters. This approach is challenging to implement in the presence of complicated selection mechanisms with many parameters. Plausible sets of parameters that introduce bias in estimates of interest may be overlooked. Therefore, we begin by framing [24] as an optimization problem over a space of plausible parameters, and describe how relevant auxiliary information could be introduced to further restrict the parameter space and provide more informative bounds (e.g. survey response rates, population means and negative controls). An additional sensitivity analysis, [3], is generalized in Appendix C.

Consider an independent and identically distributed draw of size from an infinite population. For concreteness, we can think of this finite draw as the set of individuals who are eligible to enter the sample. Let be a selection indicator for whether individual enrols in the sample, where indicates sample participation, and let the observed sample size be denoted by . For notational convenience, we assume and .

Within the observed sample (i.e. for ), we observe a vector of variables related to sample selection . As in [24], we assume that the probability of sample selection admits a logistic form,

| (13) |

where we define .

For illustration, suppose that our parameters and estimators of interest are (respectively) characterized by the solution to the instrumental variable moment conditions

| (14) |

where is a vector of instrumental variables, is a vector of explanatory variables and is a response variable [11]. This is equivalent to the least squares moment conditions whenever . The moment conditions are inverse weighted by the probability of sample selection ; this will weight the sample back to the population implied by the weights under a missing-at-random assumption that . For this reason, we write the parameters and estimators as functions of the parameters that characterize the sample selection probabilities. We also allow the instruments, explanatory variables and response (and their higher order and interaction terms) to be elements of .

Without loss of generality, suppose that our parameter of interest is the first element since we consider optimization of a scalar-valued function in our framework.

3.2 Sensitivity parameters

The key challenge is that we only observe those for whom so that the parameters cannot be estimated. A sensible approach is to place bounds on the possible values of and identify the smallest and largest values that the corresponding estimator could take. Since we have assumed a logistic form for the selection probabilities (13), we can select sensitivity parameters which have a natural interpretation in terms of odds ratios.

Without loss of generality, suppose each has mean zero and standard deviation one within the sample. We can then choose a parameter such that

| (15) |

We can interpret as the change in the conditional odds of sample selection from a one standard deviation increase in , holding all else fixed. When , sample selection is completely random. Of course, we could select sensitivity parameters on a variable-by-variable basis for , although choosing a single simplifies the interpretation of the sensitivity analysis.

The intercept term also needs to be bounded. We can choose two parameters such that

| (16) |

which can be interpreted as the odds of sample selection among those for whom for all .

Rearranging eqs. 15 and 16 shows that the sensitivity parameters characterize a compact subset of ,

| (17) |

From here, we can define the estimand and estimator (respectively) for the worst-case lower bound of as

We could of course estimate the worst-case upper bound for by taking the supremum of over (see Remark 2.2).

3.3 Auxiliary information constraints

We now introduce several common examples where there may be discordance between known population quantities and quantities implied by the inverse probability weights. In general, provided we can formulate the constraints as a statistical test with a known asymptotic distribution, they can be placed within our framework.

Example 3.1.

Suppose we know the response rate for a survey-based sample . It is straightforward to show that . This means that the within-sample expectation of the inverse selection probabilities is equal to the inverse response rate. The response rate constraint can be formulated as

| (18) |

where is the sample variance of .

Example 3.2.

Suppose we know the population mean of some . The inverse probability weighted sample mean of should therefore equal this mean in expectation, since

This is conceptually similar to the raking procedure in survey sampling [9], which adjusts sampling weights to match known marginal totals. The covariate mean constraint can be formulated as

| (19) |

where is the sample variance of .

Example 3.3.

Suppose we are confident that higher values of are associated with an increased probability of sample selection. For example, could be years of education and we might know from comparisons with representative samples (e.g. census) that better educated individuals are more likely to select into our sample, conditional on other selection variables, so that a priori.

Example 3.4.

Suppose we know that two variables and are uncorrelated in the population. The inverse probability weighted correlation between and should therefore be zero. For example, due to the independent assortment of chromosomes, biological sex and autosomal genetic variants should be independent in the population, however, [19] demonstrate that there is significant correlation within UK Biobank. This constraint can be formulated in several ways, for example fixing the regression coefficient of on to be zero.

Examples 3.1, 3.2 and 3.4 are two-sided constraints such that we also want these inequalities to hold for .

Remark 3.1.

In the population means setting, [16] demonstrate how to place shape constraints on the weighted empirical distribution of the response. Their approach involves constructing the worst-case weighted distribution given the [3] bounding assumptions (see Appendix C). This results in a set which contains the oracle weighted distribution with probability approaching one.

Provided we have a valid test, we can implement shape constraints within our framework without the need to characterize the worst-case weighted distribution. In the simplest case, we might want a variable to follow a known distribution in the population. For example, the distribution of IQ scores should be normal with mean 100 and standard deviation 15, which is a stronger constraint than Example 3.2. This could be formulated as a Kolmogorov-Smirnov test and the relaxed constraint set could be constructed via the null distribution of that test.

4 Simulations

The aim of these simulations is to provide a brief assessment of the finite sample and limiting properties of the inference procedure described in Section 2. For concreteness, we simulate the sensitivity analysis for selection bias described in Section 3. Our parameter and estimator are the coefficient of a linear regression, specifically the solution to the least squares moment conditions in eq. 14 for , where is the identity matrix, and . The selection variables are .

We consider three distinct scenarios for the constraints. In the first scenario, we impose only sensitivity parameters , and . In the second scenario, we also impose a direction constraint via Example 3.3. In the third scenario, we impose both the previous direction constraint and set the response rate equal to via Example 3.1. In each scenario, we use the discussion in Remark 2.2 to construct a two-sided 95% confidence interval for the identified set , where , and is of the form in eq. 17. The first and second scenarios have no sample constraints and so the confidence interval corresponds to the one in eq. 8. The third scenario employs the confidence interval proposed in eq. 12 and Theorem 2.1.

Each scenario has distinct properties. In the first scenario, there are two solutions to the population optimization problems, thus violating 1. In the second scenario, the addition of a direction constraint rules out one of the two solutions and satisfies 1. In the third scenario, the introduction of a sample constraint necessitates the use of our relaxed confidence bound. In this scenario, we use our rule-of-thumb from Remark 2.1 to select for both the upper and lower bounds of the two-sided confidence interval.

Table 1 summarizes the results and broadly aligns with our theoretical predictions. The first scenario violates 1 and the impact of this violation is substantial over-coverage of the confidence interval. Intuitively, this occurs because the sample solution will occur at (or near) the population solution that happens to minimize in that particular sample, which will result in a systematically wider confidence interval. The second scenario satisfies all assumptions for Proposition 2.2 and therefore converges to exact nominal coverage. The third scenario imposes a sample constraint and exhibits some over-coverage. This over-coverage can occur because our confidence bound in Theorem 2.1 sidesteps the covariance between the constraints and objective function , instead imposing a worst-case intersection bound.

| Sample size | |||||||

|---|---|---|---|---|---|---|---|

| Scenario | 10 | 25 | 50 | 100 | 200 | 500 | 1000 |

| 1 | 0.972 | 0.992 | 0.995 | 0.997 | 0.998 | 0.996 | 0.995 |

| 2 | 0.936 | 0.974 | 0.981 | 0.983 | 0.979 | 0.966 | 0.947 |

| 3 | 0.953 | 0.985 | 0.991 | 0.991 | 0.987 | 0.986 | 0.979 |

5 Applied example: effect of education on income

We consider an instrumental variable design looking at the effect of education on income in the UK Biobank cohort. Our instrument is exposure to an educational reform taking place in England in 1972. Our exposure is whether an individual remained in school at least until age 16 and our outcome is whether an individual earned more than £31,000 per year in 2006. We restrict our sample to individuals who turned 15 within 12 months of September 1972 and we control for sex and month-of-birth indicators. The unweighted estimate is 0.18 (95% confidence interval 0.08 - 0.28). An in-depth exposition of this design can be found in [8] and Appendix A.

To address this, we first apply the sensitivity analysis described in Section 3.2 without auxiliary constraints, where the probability weights contain sex, years of education, income, age, days of physical activity per week and an interaction term between education and income. We choose sensitivity parameters , and , so that the average individual in the sample has an odds of sample selection between and and each variable in the model can induce a marginal odds of sample selection between and . Using these parameters, our sensitivity analysis suggests that the effect estimate lies in the interval (95% confidence interval ). This interval is completely uninformative as it spans the full range of possible estimates.

One explanation for this conservativeness is that this simple sensitivity analysis does not utilize all of the information available to us on the target population and the sample selection mechanism. The minimizing (maximizing) weights corresponding to this interval imply that the proportion of males in the population is 38.52% (46.6%) and the proportion of households with a gross income greater than £31000 is 95.84% (95.66%), all of which are inconsistent with known characteristics of the UK population.

We consider four constraints that are typical of the information available to applied researchers using datasets such as UK Biobank. The first constraint is the response rate of UK Biobank (5.5%), which is the proportion of individuals who entered the cohort after receiving an invitation. The second constraint is the proportion of males in the UK population within the UK Biobank age range of 40-69 (49.5%). The third is the proportion of UK households earning more than £31000 per year at the date of UK Biobank recruitment in 2006 (21%). The fourth is the average age of individuals within our 2 year age bracket (48.98). All statistics were obtained from publicly available records from the UK’s Office of National Statistics.

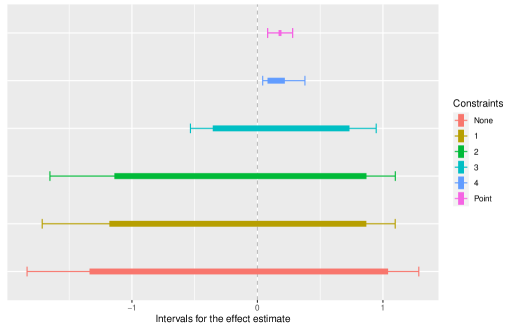

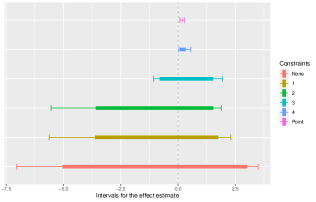

Figure 5.1 shows the resulting estimated intervals (thicker lines) and their corresponding confidence intervals (thinner lines) where each constraint is added sequentially. The estimated intervals and confidence intervals correspond to those described in Remark 2.2. We can see that each additional constraint reduces the width of the interval, with constraints 3 and 4 (the household income and age constraints respectively) seemingly having the largest marginal impact. The top interval includes all constraints and is quite informative for the desired effect, rejecting the null and suggesting an effect estimate in the range 0.08 - 0.22 (95% confidence interval 0.04 - 0.38). The unweighted estimate of 0.18 (95% confidence interval 0.08 - 0.28) reported in Appendix A still lies within this interval, but our sensitivity analysis suggests some increased uncertainty in the range of effect estimates. These results also suggest that, despite the potential conservativeness of the confidence interval in Theorem 2.1, it can still produce informative bounds in practice.

6 Discussion

There has been some existing work on bootstrap inference for Rosenbaum-type sensitivity analyses [26]. This approach considers a fixed parameter space . It is unclear how to select the relaxation parameter in a bootstrap analogue of our method under estimated constraints. Simple approaches, such as constructing via asymptotic approximations and then bootstrapping the distribution of , are plausible but their statistical properties remain to be explored.

In some instances, the target of inference is , where is some true parameter lying within , rather than . Suppose is known and we have a two-sided identified set , then if lies near the boundary of this set (and the set has positive width), the non-coverage probability of the corresponding confidence interval is effectively one-sided in the limit. A naive two-sided confidence interval constructed around the identified set may be too conservative. [14] discuss approaches for maintaining uniform coverage of . The central limit theorem established by [20] for known is amenable to their framework (although, to our knowledge, has not been formally used in this setting); extending this result to sample-constrained problems would be a valuable contribution. [22] further extends [14] by developing confidence intervals that exhibit uniform coverage for without relying on assumed superefficiency of the estimated interval width.

References

- [1] Donald W K Andrews and Xiaoxia Shi “Inference based on conditional moment inequalities” In Econometrica 81.2, 2013, pp. 609–666 DOI: 10.3982/ecta9370

- [2] Donald W K Andrews and Gustavo Soares “Inference for parameters defined by moment inequalities using generalized moment selection” In Econometrica 78.1, 2010, pp. 119–157 DOI: 10.3982/ecta7502

- [3] Peter M. Aronow and Donald K.K. Lee “Interval estimation of population means under unknown but bounded probabilities of sample selection” In Biometrika 100.1, 2013, pp. 235–240 DOI: 10.1093/biomet/ass064

- [4] Elias Bareinboim, Jin Tian and Judea Pearl “Recovering from selection bias in causal and statistical inference” In Proceedings of The Twenty-Eighth Conference on Artificial Intelligence, 2014, pp. 339–341

- [5] Roger L. Berger and Dennis D. Boos “P values maximized over a confidence set for the nuisance parameter” In Journal of the American Statistical Association 89.427, 1994, pp. 1012–1016 DOI: 10.1080/01621459.1994.10476836

- [6] Victor Chernozhukov, Han Hong and Ellie Tamer “Estimation and confidence regions for parameter sets in econometric models” In Econometrica 75.5, 2007, pp. 1243–1284

- [7] Victor Chernozhukov, Sokbae Lee and Adam M Rosen “Intersection bounds: Estimation and inference” In Econometrica 81.2, 2013, pp. 667–737 DOI: 10.3982/ecta8718

- [8] Neil M. Davies et al. “The causal effects of education on health outcomes in the UK Biobank” In Nature Human Behaviour 2.2 Springer US, 2018, pp. 117–125 DOI: 10.1038/s41562-017-0279-y

- [9] W. Deming and Frederick F. Stephan “On a least squares adjustment of a sampled frequency table when the expected marginal totals are known” In The Annals of Mathematical Statistics 11.4, 1940, pp. 427–444 DOI: 10.1214/aoms/1177731829

- [10] Anna Fry et al. “Comparison of sociodemographic and health-related characteristics of UK Biobank participants with those of the general population” In American Journal of Epidemiology 186.9, 2017, pp. 1026–1034 DOI: 10.1093/aje/kwx246

- [11] Fumio Hayashi “Econometrics” Princeton: Princeton University Press, 2000

- [12] D G Horvitz and DJ Thompson “A generalization of sampling without replacement from a finite universe” In Journal of the American Statistical Association 44.260, 1952, pp. 663–685 DOI: 10.1159/000150726

- [13] Rachael A. Hughes, Neil M. Davies, George Davey Smith and Kate Tilling “Selection bias when estimating average treatment effects using one-sample instrumental variable analysis” In Epidemiology 30.3, 2019, pp. 350–357 DOI: 10.1097/EDE.0000000000000972

- [14] Guido W. Imbens and Charles F. Manski “Confidence intervals for partially identified parameters” In Econometrica 72.6, 2004, pp. 1845–1857 DOI: 10.1111/j.1468-0262.2004.00555.x

- [15] Charles F. Manski “Partial identification of probability distributions” New York: Springer-Verlag, 2003, pp. 1–175

- [16] L.. Miratrix, S. Wager and J.. Zubizarreta “Shape-constrained partial identification of a population mean under unknown probabilities of sample selection” In Biometrika 105.1, 2018, pp. 103–114 DOI: 10.1093/biomet/asx077

- [17] Francesca Molinari “Microeconometrics with partial identification” In Handbook of Econometrics 7 Elsevier B.V., 2020, pp. 355–486 DOI: 10.1016/bs.hoe.2020.05.002

- [18] Aviv Nevo “Using weights to adjust for sample selection when auxiliary information is available” In Journal of Business and Economic Statistics 21.1, 2003, pp. 43–52 DOI: 10.1198/073500102288618748

- [19] Nicola Pirastu et al. “Genetic analyses identify widespread sex-differential participation bias” In Nature Genetics 53.5, 2021, pp. 663–671 DOI: 10.1038/s41588-021-00846-7

- [20] Alexander Shapiro “Asymptotic analysis of stochastic programs” In Annals of Operations Research 30, 1991, pp. 169–186 DOI: 10.1007/BF02204815

- [21] Alexander Shapiro, Darinka Dentcheva and Andrzej Ruszczyński “Lectures on Stochastic Programming: Modeling and Theory” In Lectures on Stochastic Programming Society for IndustrialApplied Mathematicsthe Mathematical Programming Society, 2009 DOI: 10.1137/1.9780898718751

- [22] Jörg Stoye “More on confidence intervals for partially identified parameters” In Econometrica 77.4, 2009, pp. 1299–1315 DOI: 10.3982/ecta7347

- [23] Elizabeth A. Stuart, Stephen R. Cole, Catherine P. Bradshaw and Philip J. Leaf “The use of propensity scores to assess the generalizability of results from randomized trials” In Journal of the Royal Statistical Society. Series A: Statistics in Society 174.2, 2011, pp. 369–386 DOI: 10.1111/j.1467-985X.2010.00673.x

- [24] Caroline A Thompson and Onyebuche A Arah “Selection bias modeling using observed data augmented with imputed record-level probabilities” In Annals of Epidemiology 24.10, 2014, pp. 747–753 DOI: 10.1016/j.annepidem.2014.07.014.SELECTION

- [25] Wei Wang and Shabbir Ahmed “Sample average approximation of expected value constrained stochastic programs” In Operations Research Letters 36.5, 2008, pp. 515–519 DOI: 10.1016/j.orl.2008.05.003

- [26] Qingyuan Zhao, Dylan S. Small and Bhaswar B. Bhattacharya “Sensitivity analysis for inverse probability weighting estimators via the percentile bootstrap” In Journal of the Royal Statistical Society: Series B 81.3, 2019, pp. 1–27 DOI: 10.1111/rssb.12327

Acknowledgements

The authors thank the referees and associate editor for their helpful and detailed comments. This research has been conducted using the UK Biobank Resource. UK Biobank received ethical approval from the Research Ethics Committee (REC reference for UK Biobank is 11/NW/0382). This research was approved as part of application 8786. Tudball would like to acknowledge financial support from the Wellcome Trust (grant number 220067/Z/20/Z). Bowden is supported by an Expanding Excellence in England (E3) award from the University of Exeter. For the purpose of Open Access, the author has applied a CC BY public copyright licence to any Author Accepted Manuscript version arising from this submission.

Appendix A Further details for the applied example

A.1 Description of the design

We implement an instrumental variable design for the effect of education on income in the UK Biobank cohort [8]. The proposed instrument is based on a September 1972 education reform in England which raised the school leaving age from 15 to 16. Individuals who turned 15 just prior to the implementation of this reform were allowed to leave school, while individuals who turned 15 just after were required to remain in school until they were 16. This created a sharp discontinuity in the policies that the two groups were exposed to. Under the assumption that individuals on either side of the age threshold are otherwise identical, we can use this policy reform as an instrumental variable.

A.2 Varying the sensitivity parameters

It is important to report a few choices for the sensitivity parameters to understand which parameters are driving the width of the interval. Selecting results in an empty constraint set, indicating that there are no parameters which satisfy all of the auxiliary information constraints provided. The response rate constraint of Example 3.1 appears to be more informative when the interval is wider, which is expected. For all choices of parameters we consider, the constraints are informative and recover an interval that rejects the null.

A.3 Visualizing the feasible region

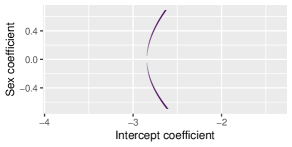

It is also illustrative to plot the feasible region for a couple of simple examples. Suppose that consists only of the sex variable. We select sensitivity parameters as usual and consider two constraints: setting the response rate to be 0.055 and setting the population mean of male sex to be 0.495.

Figure A.2 plots the two feasible regions. The feasible regions are both small in comparison to the space implied by the sensitivity parameters. Imposing both constraints simultaneously will result in a non-empty feasible region. In fact, [18] shows that the parameters of the selection model are exactly identified in this case provided each constraint provides a unique restriction on , in the sense that the outer product of the corresponding equality constraints is of full rank.

Appendix B Sufficient conditions for 6

Assumption 8.

For sufficiently large , with probability one.

Assumption 9.

For all , converges to and converges to 0 with probability one as uniformly on .

Assumption 10.

For any , let be the indices of active constraints, which could be empty. We assume that the gradient vectors , , are linearly independent.

Appendix C Extension of [3]

C.1 Extension to ratio estimators

Another sensitivity analysis that can be made more informative through the addition of auxiliary constraints is one proposed in [3]. This non-parametric sensitivity analysis computes bounds on an inverse probability weighted sample mean under the assumption that each weight is bounded between two known constants. To start, we provide a slight generalization of this sensitivity analysis to ratio estimators. Let the estimator be given by

| (20) |

where and . We assume that each is unknown (and some may be unmeasured) and lies between two user-specified constants .

To apply our theoretical results in Section 2, we need a set of fixed dimension. A simple assumption is that is discrete and finite, . Under this assumption, we can define equal to

where and are (respectively) the sample and population probability measures. This results in . From here, the infimum takes the usual form,

It remains to identify assumptions such that the conditions in Section 2 are satisfied.

Assumption 11.

For all , the denominators of and are non-zero with probability one.

Assumption 12.

For all , .

11 simply ensures that and are well-defined over . 12 is more subtle but will be needed to ensure a unique solution. If this assumption violated for some , then the infimum is identical for all values of , meaning that the solution is not unique. An example of a function violating this condition is the following:

In this example, and are both minimizers over . The minimum value is -7 but as well, which violates the condition. These assumptions jointly imply that has a unique minimizer. We begin with a technical lemma.

Lemma C.1.

is a global minimum over if and only if, for all , , where .

This leads to our main proposition.

Proposition C.1.

In fact, Proposition C.1 provides an explicit form for the sample minimizer,

| (21) |

and the population minimizer takes a similar form but with replaced with . Both Proposition 1 of [3] and Section 4.4 of [26] propose equivalent algorithms for computing the optimizing weights in the population means setting. Proposition C.1 shows that we can generalize this algorithm to ratio estimators. In short, we can order from smallest to largest and evaluate by enumerating over the weight at which changes to , which has computational complexity .

Proposition C.1 shows that 1 is satisfied for the generalized [3] estimator under relatively weak conditions. Furthermore, Assumptions 2, 4 and 3 are satisfied under 11 and the assumption that is finite. We therefore have that Proposition 2.2 is satisfied under these same relatively weak conditions.

C.2 Auxiliary information constraints

The constraints described in Examples 3.1 and 3.2 can be applied to this estimator. Let , then the response rate constraint can be formulated as

| (22) |

Suppose is an element of , then the covariate mean constraint can be formulated as

| (23) |

Both of these constraints are quadratic in and can therefore be solved by existing algorithms for quadratically-constrained linear programs. Example 3.3 cannot be extended to this setting because it is tied to a parametric model. Example 3.4 can be extended to this setting in principle, but the resulting optimization problem is intractable.

Uniqueness of over is needed to invoke Theorem 2.1. The population minimization problem over is a linearly-constrained linear fractional programming problem. For example, the population response rate constraint is

which is linear in . Since the level sets of are also linear, to establish uniqueness of it suffices to assume (in addition to Assumptions 11 and 12) that the coefficient vectors of and the level sets of over are not parallel.

Appendix D Technical details

Proof of Lemma C.1

Proof.

Consider the population problem. We will prove the ‘if’ statement since the ‘only if’ statement follows from some simple algebra. We will begin by noting that, since is the solution to a linear fractional programming problem and since is a compact, convex polyhedron, the maximizing weight vector will lie at a vertex. In other words, . Take an arbitrary weight vector . Suppose there are elements of which differ from . Without loss of generality, suppose these are the first elements. Then we can write

The same holds with probability one for the sample problem by replacing with . ∎

Proof of Proposition C.1

Proof.

Consider the population problem. Suppose that there are two global minima, and , such that and . Since and are both global minima then, by Lemma C.1, for all ,

| (24) |

Without loss of generality, we assume that and differ by the first elements. Then,

where . Rearranging, we obtain,

However, (24) implies that this equality will only hold if, for all , , which cannot be true by Assumption 1. Therefore, by contradiction, the set must be a singleton. The same holds with probability one for the sample problem by replacing with . ∎

Proof of Proposition 2.3

Proof.

where the last inequality holds by the uniform strong consistency and the second term on the last line goes to zero with probability one since with probability one by Proposition 2.1 and . ∎

Before proving Theorem 2.1, we begin with some notation and preliminary lemmas. Denote the confidence bound for a particular and as

and the sample minimum over at as

Recall that and , which is assumed to be unique. These quantities can be ordered deterministically as

The first lemma provides a lower bound for the coverage probability of .

Lemma D.1.

Let be a deterministic sequence where is any positive constant, then

Proof.

∎

Lemma D.2.

Proof.

The proof of this lemma combines Theorem 5.3 and Theorem 5.5 in [21]. Theorem 5.3 establishes consistency of optimal values and solutions when is known. Theorem 5.5 generalizes this result to an estimated constraint set, in our case .

In particular, Theorem 5.5 requires that the following two conditions are satisfied:

-

a)

If and converges with probability one to a point , then .

-

b)

There exists a sequence such that converges to with probability one.

We begin with the proof of condition (a). Suppose . Then there exists some such that , where is some constant. By the triangle inequality,

The first term converges to zero with probability one because converges to and , both with probability one. The second term also converges to zero with probability one by 9 because uniformly on with probability one. This means that for all there exists an such that

However, since and , such that , this is equivalent to

whenever . Without loss of generality, we can set . From here, we can rearrange,

which means that , which is a contradiction. Therefore, it must be that .

Proof of Theorem 2.1

Proof.

This follows from Proposition 2.3 and 6. A sufficient condition for satisfying this assumption is that and with probability one. This follows from Lemma D.2 since and both converge to with probability one uniformly on by 3. Therefore, we have that

where the last inequality follows by Slutsky’s theorem, Proposition 2.3 and Proposition 2.2. Since is an arbitrarily small constant, this lower bound can be set arbitrarily close to . ∎