dateenglish\monthname[\THEMONTH] \THEDAY, \THEYEAR

Bivariate FCLT for the Sample Quantile and Measures of Dispersion for Augmented GARCH(, ) processes

?abstractname?

In this paper, we build upon the asymptotic theory for GARCH processes, considering the general class of augmented GARCH(, ) processes. Our contribution is to complement the well-known univariate asymptotics by providing a joint (bivariate) functional central limit theorem of the sample quantile and the r-th absolute centred sample moment. This extends existing results in the case of identically and independently distributed random variables.

We show that the conditions for the convergence of the estimators in the univariate case suffice even for the joint bivariate asymptotics. We illustrate the general results with various specific examples from the class of augmented GARCH(, ) processes and show explicitly under which conditions on the moments and parameters of the process the joint asymptotics hold.

2010 AMS classification: 60F05; 60F17; 60G10; 62H10; 62H20

JEL classification: C13; C14; C30

Keywords: asymptotic distribution; functional central limit theorem; (augmented) GARCH; correlation; (sample) quantile; measure of dispersion; (sample) mean absolute deviation; (sample) variance

1 Introduction and Notation

Since the introduction of the ARCH and GARCH processes in the seminal papers by Engle, [13], and Bollerslev, [6], respectively, various GARCH modifications and extensions have been proposed and their statistical properties analysed (see e.g. [7] for an (G)ARCH glossary). Conditions for the stationarity of such processes, as well as central limit theorems (CLT) or functional central limit theorems (FCLT) have been obtained in various ways by exploiting the different dependence concepts underlying these GARCH type processes (see the introduction in [20] for references on CLT’s under different dependence conditions).

The limit theorems extend also to different estimators apart from the underlying process itself, as for example: powers of the process (e.g. [18] for augmented GARCH(,); [4], [20] for augmented GARCH(, )), sample autocovariance and sample variance (e.g. [22] for the GARCH(,); [2] for augmented GARCH(,)), or the sample quantile.

Still, joint asymptotics of such estimators have not been considered yet. It is what we are developing in this paper, providing bivariate functional central limit theorems for the sample quantile together with the r-th absolute centred sample moment. This includes the case of the sample variance and also the sample mean absolute deviation around the sample mean (MAD), two well-known and widely used measures of dispersion, extending the results obtained in [9] for identically and independently distributed (iid) random variables.

Note that the theoretical questions arised from previous studies in financial risk management, one (see [8]) where the correlation between a log-ratio of sample quantiles with the sample MAD is measured using log-returns from different stock indices, the other (see [32] and [33]) considering the correlation of ‘the realized volatilities with the centred volatility increment’ for different underlying processes. Thus, we think that those asymptotic results may be of great use for applications in statistics or other application fields. For instance, coming back to financial risk management and risk measure estimation, we could extend results obtained for the Value-at-Risk, when estimated by the sample quantile, to Expected Shortfall using once again the FCLT.

To cover a broad range of GARCH processes, we focus on so called augmented GARCH(, ) processes, introduced by Duan in [12]. They contain many well-known GARCH processes as special cases. Previous works on univariate CLT’s and stationarity conditions for this class of GARCH processes are, inter alia, [2],[4],[18] and [20].

The structure of the paper is as follows. We present in Section 2 the main results about the bivariate FCLT for the sample quantile and the r-th absolute centred sample moment for augmented GARCH(, ) processes. Then, we present specific examples of well-known GARCH models in Section 3 and show how the general conditions in the main result translate for these specific cases. The proofs are given in Section 4.

Notation

We introduce the same notation as in [9]: Let be a sample of size . Assuming the random variables ’s have a common distribution, denote their parent random variable (rv) with parent cumulative distribution function (cdf) , (and, given they exist,) probability density function (pdf) , mean , variance , as well as, for any integer the r-th absolute centred moment, and quantile of order defined as . We denote the ordered sample by .

We consider the sample estimators of the two quantities of interest, i.e. first the sample quantile for any order defined as , where , and , are the rounded-up, rounded-off integer-parts and the nearest-integer of a real number , respectively. Second, the r-th absolute centred sample moment defined, for , by

| (1) |

denoting the empirical mean. Special cases of this latter estimator include the sample variance () and the sample mean absolute deviation around the sample mean ().

Recall the standard notation for the transpose of a vector and, for the signum function, . By we denote the euclidean norm and the usual -norm is denoted by . Moreover the notations , , and correspond to the convergence in distribution, almost surely, in probability and in distribution of a random vector in the d-dimensional Skorohod space . Further, for real-valued functions , we write (as if and only if there exists a positive constant and a real number s.t. for all , and (as ) if for all there exists a real number s.t. for all . Analogously, for a sequence of rv’s and constants , we denote by the convergence in probability to 0 of .

2 The Bivariate FCLT

Let us introduce the augmented GARCH(, ) process , due to Duan in [12], namely, for integers and , satisfies

| (2) | ||||

| (3) |

where is a series of iid rv’s with mean and variance , and , are real-valued measurable functions. Also, as in [20], we restrict the choice of to the so-called group of either polynomial GARCH(, ) or exponential GARCH(, ) processes (see Figure 1 in the Appendix):

Clearly, for a strictly stationary solution to (2) and (3) to exist, the functions as well as the innovation process have to fulfill some regularity conditions (see e.g. [20], Lemma 1).

Alike, for the bivariate FCLT to hold, certain conditions need to be fulfilled; we list them in the following.

First, conditions concerning the dependence structure of the process . We use the concept of -near-epoch dependence (-NED),

using a definition due to Andrews in [1] but restricted to stationary processes. Let , be a sequence of rv’s and , for , the corresponding sigma-algebra.

Let us recall the -NED definition.

Definition 1 (-NED, [1]).

For , a stationary sequence is called -NED on if for

for non-negative constants such that as .

If for some , we say that is -NED of size .

If for some , we say that is geometrically -NED.

The second set of conditions concerns the distribution of the augmented GARCH(, ) process. We impose three different types of conditions as in the iid case (see [9]): First, the existence of a finite -th moment for any integer for the innovation process . Then, given that the process is stationary, the continuity or -fold differentiability of its distribution function (at a given point or neighbourhood) for any integer , and the positivity of its density (at a given point or neighbourhood). Those conditions are named as:

The third type of conditions is set on the functions of the augmented GARCH(, ) process of the family: Positivity of the functions used and boundedness in -norm for either the polynomial GARCH, , or exponential/logarithmic GARCH, , respectively, for a given integer ,

Note that condition requires the to be bounded functions.

Remark 2.

By construction, from (2) and (3), and are independent (and is a functional of ). Thus, the conditions on the moments, distribution and density could be formulated in terms of only. At the same time this might impose some conditions on the functions (which might not be covered by , or ). Thus, we keep the conditions on even if they might not be minimal.

Now, let us state the main result. To ease its presentation we introduce a trivariate normal random vector (functionals of ), , with mean zero and the following covariance matrix:

Theorem 3 (bivariate FCLT).

For an integer , consider an augmented GARCH(, ) process as defined in (2) and (3) satisfying condition , at for , and both conditions at . Assume also conditions , and either for belonging to the group of polynomial GARCH, or for the group of exponential GARCH. Introducing the random vector , we have the following FCLT: For , as ,

where is the 2-dimensional Brownian motion with covariance matrix defined for any by , where

being the trivariate normal vector (functionals of ) with mean zero and covariance given in , all series being absolute convergent.

Remark 4.

Note that the bivariate FCLT between the sample quantile and the r-th absolute centred sample moment requires exactly the same conditions in comparison to the respective univariate convergence (which might be apparent after having gone through the proof of Theorem 3):

Requiring at exactly correspond to the conditions for the CLT of the sample quantile of a stationary process which is -NED with polynomial rate. Further, or respectively, together with and at for , are the conditions for the univariate CLT of the r-th centred sample moment for augmented GARCH(, ) processes.

But this is no surprise, as the multivariate FCLT we apply is exactly based on proving univariate asymptotics and then deducing the multivariate convergence via Cramér-Wold and a univariate tightness argument, see the proof of [3].

Choosing in Theorem 3 provides the usual CLT that we state for completeness:

Corollary 5.

Consider an augmented GARCH(, ) process as defined in (2) and (3). Under the same conditions as in Theorem 3, the joint behaviour of the sample quantile (for ) and the -th absolute centred sample moment , is asymptotically bivariate normal:

| (4) |

where the asymptotic covariance matrix is as in Theorem 3.

As special case we can also recover the CLT between the sample quantile and the r-th absolute centred sample moment in the iid case, given by Theorem 7 in [9]:

Corollary 6.

Consider an augmented GARCH(, ) process as defined in (2) and (3), choosing such that is a positive constant for all . Under the same conditions as in Theorem 3, the joint behaviour of the sample quantile (for ) and the -th absolute centred sample moment , is asymptotically bivariate normal:

| (5) |

where the asymptotic covariance matrix simplifies to

Idea of the proof -

Let us briefly describe the idea of the proof of Theorem 3, developed in Section 4. To prove the FCLT, we need to show that two conditions are fulfilled for the vector . These specific conditions arise from the application of the multivariate FCLT (Theorem A.1 in [3], which extends the univariate counterpart from, e.g., Billingsley in [5]) and are the following:

-

A representation of given by the random vector with and , , such that we have, for all natural numbers ,

where is a measurable function and is a sequence of real-valued iid rv’s with mean and variance .

-

A -dependent approximation of the random vector introduced in , i.e. the existence of a sequence of random vectors such that, for any , we have

Checking the first condition, , is done in two steps. First, we show why we can use the Bahadur representation of the sample quantile given in [30] (Theorem 1). Second, we prove a corresponding representation for the r-th absolute centred sample moment (extending results from [9], [28]). These representations of the sample quantile and r-th absolute centred sample moment then naturally fulfil .

To prove the second condition , we need to find a -dependent approximation . For this, we show that the existence of our chosen can be reduced to the existence of a -dependent approximation for the process or powers of the process , for which results in [20] can be used.

3 Examples

In this section we review some well-known examples of augmented GARCH(, ) processes and discuss which conditions these models need to fulfill in order for the bivariate asymptotics of Theorem 3 to be valid.

Note that the moment condition on the innovations, , as well as the continuity and differentiability conditions, , , each at , and at for , remain the same for the whole class of augmented GARCH processes. But, depending on the specifications of the process, (2) and (3), the conditions, for polynomial GARCH or for exponential GARCH respectively, translate differently in the various examples.

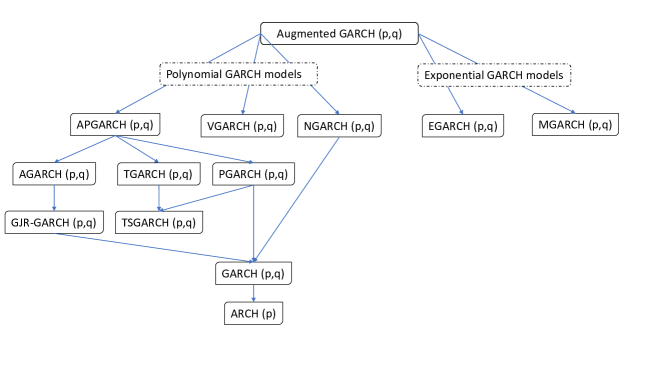

For this, we introduce in Table 1 different augmented GARCH(,) models by providing for each the corresponding volatility equation, (3), and the specifications of the functions and . We consider 10 models which belong to the group of polynomial GARCH () and two examples of exponential GARCH (). As the nesting of the different models presented is not obvious, we give a schematic overview in Figure 1 in the Appendix. An explanation of the abbreviations for, and authors of, the different models can be found there too. Note that the presented selection of augmented GARCH (,) processes is not exhaustive.

Note that in Table 1 the specification of is the same for the whole APGARCH family (only the change), whereas for the two exponential GARCH models, it is the reverse. The general restrictions on the parameters are as follows: for , . Further, the parameters in the GJR-GARCH (TGARCH) are denoted with an asterix (with a plus or minus) as they are not the same as in the other models (see the Appendix for details).

| standard formula for | corresponding specifications of in (3) | ||

|---|---|---|---|

| Polynomial GARCH | |||

| APGARCH family | |||

| AGARCH | |||

| GJR-GARCH | |||

| GARCH | |||

| ARCH | |||

| TGARCH | |||

| TSGARCH | |||

| PGARCH | |||

| VGARCH | and | ||

| NGARCH | and | ||

| Exponential GARCH | and | ||

| MGARCH | |||

| EGARCH |

In Tables 2 and 3 we present how the conditions or translate for each model. Table 2 treats the specific case of an augmented GARCH(, ) process with and is presented here whereas Table 3 treats the general case for arbitrary and is defered to the Appendix. In the first column we consider the conditions for the general r-th absolute centred sample moment, . Of biggest interest to us are the specific cases of the sample MAD () and the sample variance () as measure of dispersion estimators respectively, presented in the second and third column.

For the selected polynomial GARCH models the requirement in condition will always be fulfilled. Thus, we only need to analyse the condition .

Note that in Table 2 (and also Table 3) the restrictions on the parameter space, given by or respectively, are the same as the conditions for univariate FCLT’s of the process itself (see [4], [18]). For , they coincide with the conditions for e.g. -mixing with exponential decay (see [10]).

| augmented | |||

|---|---|---|---|

| GARCH (, ) | |||

| APGARCH | |||

| AGARCH | |||

| GJR-GARCH | |||

| GARCH | |||

| ARCH | |||

| TGARCH | |||

| TSGARCH | |||

| PGARCH | |||

| VGARCH | for any : | ||

| NGARCH | |||

| MGARCH | for any : and | ||

| EGARCH | for any : and | ||

4 Proofs

Before stating the proof of the main theorem, let us start with two auxiliary results. As it requires some work to find the asymptotics of for any integer , and such a result is of interest in its own right, we give it separately in Proposition 8. To prove it, we need the following Lemma, which extends Lemma 2.1 in [28] (case ) to any moment , and the iid case presented in Lemma 8 in [9].

Lemma 7.

Consider a stationary and ergodic time-series with parent rv which has ‘short-memory’, i.e. . Then, for or , given that the 2nd moment of exists, or, for any integer , given that the -th moment of exists, letting , it holds that

| (6) |

Proof.

The proof follows the lines of its equivalent in the iid case; see proof of Lemma 8 in [9]. The argumentation needs to be adapted only at the end in two points, using the stationarity, ergodicity and short-memory of the process. Here, it follows by these three properties that holds for any integer . Further, as a last step, we use the ergodicity of the process, instead of the strong law of large numbers, to conclude that

Now we are ready to state the asymptotic relation between the r-th absolute centred sample moment with known and unknown mean, respectively. This enables us to compute the asymptotics of (given that the necessary moments exist). As for Lemma 7, it is an extension to the stationary, ergodic and short-memory case of Proposition 9 in the iid case [9].

Proposition 8.

Consider a stationary and ergodic time-series with parent rv which has ‘short-memory’, i.e. . Then, for any integer , given that the -th moment of exists and at for , it holds, as , that

| (7) |

Proof.

Analogously to the proof of Lemma 7, the proof can be extended from the proof of Proposition 9 in the iid case in [9]. We comment on the differences compared to the iid case for the three different cases of :

Even integers - Recall that for the corresponding result in the iid case (see the proof of Proposition 9 in [9]) we refered to the example 5.2.7 in [21]. Therein they only consider the iid case but in this case, the argumentation still holds as , for , holds for an ergodic, stationary, short-memory process too.

Case - The result cited in the iid case holds for ergodic, stationary time-series too, see Lemma 2.1 in [28].

Odd integer - We point out the three differences to the corresponding proof in the iid case. First, as remarked above for even integers ,, for , follows from the stationarity, ergodicity and short-memory of the process. Second, we use the ergodicity instead of the law of large numbers. Third, we use Lemma 7 instead of its counterpart in the iid case, Lemma 8 in [9].

Finally, we state a multivariate FCLT which we will use to prove the theorem, and which is from [3] (adapted to our needs):

Lemma 9 (Theorem A.1 in [3]).

Consider a d-dimensional random process , which is centered and has finite variance, i.e.

| (8) |

and has a causal (possibly non-linear) representation in terms of an iid process, i.e.

| (9) |

where is a measurable function and is a sequence of real valued iid rv’s with mean and variance .

Suppose further, there exists a -dependent approximation of , i.e. a sequence of d-dimensional random vectors such that, for any , we have

| (10) | |||

| (11) |

where is a measurable function.

Then, the series converges (coordinatewise) absolutely and an FCLT holds for

where the convergence takes place in the d-dimensional Skorohod space and is a d-dimensional Brownian motion with covariance matrix , i.e. it has mean 0 and

.

Remark 10.

This multivariate FCLT extends the univariate counterpart from, e.g., Billingsley in [5]. For that, they prove in [3] that the univariate FCLT’s are sufficient to establish the multivariate version, using Cramér-Wold and the univariate tightness of the corresponding processes.

Proof.

of Theorem 3. The proof consists of four steps. We first show that the process fulfils the conditions required for having a Bahadur representation of the sample quantile, second, that a similar representation holds for the r-th absolute centred sample moment, third, that the conditions for an FCLT (Lemma 9) are fulfilled, which we then use in the fourth step to conclude the multivariate FCLT.

Step 1: Bahadur representation of the sample quantile - conditions.

The Bahadur representation of the sample quantile for a GARCH(, ) process is well known and can be obtained as a special case for Bahadur representations for processes with a certain dependence structure, see e.g. [19] and references therein. Here we want to establish the Bahadur representation for sample quantiles from augmented GARCH(, ) processes of the family.

We will use the Bahadur representation for general NED processes (see Theorem 1 in [30]). For the ease of comparison, we adapt some of the notation of Theorem 1 in [30]. It holds under some conditions that we need to verify:

-

-

Choosing the bivariate function , the non-negativity, boundedness, measurability, and non-decreasingness in the second variable, are straightforward. The function also satisfies the variation condition uniformly in some neighbourhood of if it is Lipschitz-continuous (see Example 1.5 in [30]). But the latter follows from condition .

-

-

The differentiability of and positivity of its derivative at are given by condition at .

- -

-

-

The stationarity of the process follows from assumption or , respectively, and Lemma 1 of [20].

-

-

Lastly, let us verify that the process is -NED with polynomial rate. Denoting, for , the sigma-algebra , we can write for any integer

But since holds. Notice that the property of being geometrically -NED, for some , implies -NED with polynomial rate, as

(12) for some . So it suffices showing that is geometrically -NED. For the polynomial GARCH, it follows from Corrollary 1 in [20], which can be applied as and hold. For the exponential GARCH case, it follows from Corrollary 3 in [20] as and hold.

Thus, we can use Theorem 1 of [30] and write, as ,

| (13) |

Note that we do not use the exact remainder bound as in [30] as for our purposes is enough.

Step 2: Representation of the r-th absolute centred sample moment -conditions.

The representation being given in Proposition 8 under some conditions, we only need to check that we fulfil them.

-

-

The stationarity of the process is satisfied under or as observed in Step 1.

-

-

For the moment condition, short-memory property and ergodicity, we simply verify that the conditions for a CLT of (or ) are fulfilled, distinguishing between the polynomial and exponential case. Conditions in the polynomial case, and in the exponential case respectively, imply the CLT, using Corollary 2 and 3 in [20], respectively.

Step 3: Conditions for applying the FCLT

In our case we want to apply Lemma 9 in a three-dimensional version. This simplifies the computation, and by applying the continuous mapping theorem we will finally get back a two-dimensional representation. This will be made explicit in Step 4.

Therefore, let us define, anticipating its use in Step 4 for the FCLT of ,

We need to verify that fulfils (8): holds by construction. is guaranteed since satisfies a CLT (see Step 2), thus also . Finally follows from Lemma 1 in [20], as we assume . Hence, this latter relation also holds for functionals of , so for , i.e. (9) is fulfilled.

Then, we define a -dependent approximation satisfying (10) and (11). Denote, for the ease of notation, , and set with for . Thus, (10) is fulfilled by construction. Let us verify (11). We can write

| (14) |

Obviously, a sufficient condition for (14) is the finiteness of its summands. If it holds that each summand is geometrically -NED, then its sum will be finite. E.g. assuming that is geometrically -NED, i.e. for some , it follows that .

The condition of geometric -NED of and is satisfied, on the one hand in the polynomial case under and via Corollary 2 in [20], on the other hand in the exponential case under and via Corollary 3 in [20]. Thus, as is geometric -NED this follows also for its bounded functional using Lemma 3.5 in [30] as we showed already in Step 1 that this functional satisfies the variation condition. The result in the case of an indicator function goes back to [26]).

Step 4: Multivariate FCLT

Having checked the conditions for the FCLT of Lemma 9 in Step 3, we can apply a trivariate FCLT for :

Using the Bahadur representation (13) of the sample quantile (ignoring the rest term for the moment), we can state:

| (15) |

where is the 3-dimensional Brownian motion with covariance matrix , i.e. the components , satisfy the same dependence structure as for the random vector described in , with all series being absolutely convergent. By the multivariate Slutsky theorem, we can add to the asymptotics in (15) without changing the resulting distribution (as ). Hence, as ,

| (16) |

Recalling the representation of in Proposition 8, we apply to (16) the multivariate continuous mapping theorem using the function with . Further, by Slutsky’s theorem once again, we can add to a rest of without changing the limiting distribution, to obtain, as ,

| (17) |

where follows from the specifications of above and the continuous mapping theorem.

?refname?

- [1] Andrews, D. Laws of large numbers for dependent non-identically distributed random variables. Econometric Theory 4, 3 (1988), 458–467.

- [2] Aue, A., Berkes, I., and Horváth, L. Strong approximation for the sums of squares of augmented GARCH sequences. Bernoulli 12, 4 (2006), 583–608.

- [3] Aue, A., Hörmann, S., Horváth, L., and Reimherr, M. Break detection in the covariance structure of multivariate time series models. The Annals of Statistics 37, 6B (2009), 4046–4087.

- [4] Berkes, I., Hörmann, S., and Horváth, L. The functional central limit theorem for a family of GARCH observations with applications. Statistics & Probability Letters 78, 16 (2008), 2725–2730.

- [5] Billingsley, P. Convergence of probability measures, 1st ed. John Wiley & Sons, 1968.

- [6] Bollerslev, T. Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31, 3 (1986), 307–327.

- [7] Bollerslev, T. Glossary to ARCH (GARCH). CREATES Research Paper 49 (2008).

- [8] Bräutigam, M., Dacorogna, M., and Kratz, M. Pro-cyclicality of traditional risk measurements: Quantifying and highlighting factors at its source. arXiv:1903.03969 (2019).

- [9] Bräutigam, M., and Kratz, M. On the dependence between functions of quantile and dispersion estimators. arXiv:1904.11871 (2019).

- [10] Carrasco, M., and Chen, X. Mixing and moment properties of various GARCH and stochastic volatility models. Econometric Theory 18, 1 (2002), 17–39.

- [11] Ding, Z., Granger, C., and Engle, R. A long memory property of stock market returns and a new model. Journal of Empirical Finance 1, 1 (1993), 83–106.

- [12] Duan, J. Augmented GARCH (p, q) process and its diffusion limit. Journal of Econometrics 79, 1 (1997), 97–127.

- [13] Engle, R. Autoregressive conditional heteroscedasticity with estimates of the variance of united kingdom inflation. Econometrica: Journal of the Econometric Society 50, 4 (1982), 987–1007.

- [14] Engle, R., and Ng, V. Measuring and testing the impact of news on volatility. The Journal of Finance 48, 5 (1993), 1749–1778.

- [15] Geweke, J. Modeling the persistence of conditional variances: a comment. Econometric Reviews 5 (1986), 57–61.

- [16] Glosten, L., Jagannathan, R., and Runkle, D. On the relation between the expected value and the volatility of the nominal excess return on stocks. The Journal of Finance 48, 5 (1993), 1779–1801.

- [17] Higgins, M., and Bera, A. A class of nonlinear ARCH models. International Economic Review 33, 1 (1992), 137–158.

- [18] Hörmann, S. Augmented garch sequences: Dependence structure and asymptotics. Bernoulli 14, 2 (2008), 543–561.

- [19] Kulik, R. Optimal rates in the bahadur-kiefer representation for GARCH sequences. arXiv preprint math/0605283 (2006).

- [20] Lee, O. Functional central limit theorems for augmented GARCH (p, q) and FIGARCH processes. Journal of the Korean Statistical Society 43, 3 (2014), 393–401.

- [21] Lehmann, E. Elements of Large-Sample Theory. Springer Science & Business Media, 1999.

- [22] Mikosch, T. Limit theory for the sample autocorrelations and extremes of a GARCH (1,1) process. The Annals of Statistics 28, 5 (2000), 1427–1451.

- [23] Milhøj, A. A multiplicative parameterization of ARCH models. Working Paper (1987).

- [24] Nelson, D. Conditional heteroskedasticity in asset returns: A new approach. Econometrica: Journal of the Econometric Society 59, 2 (1991), 347–370.

- [25] Pantula, S. Modeling the persistence of conditional variances: a comment. Econometric Reviews 5 (1986), 79–97.

- [26] Philipp, W. A functional law of the iterated logarithm for empirical distribution functions of weakly dependent random variables. The Annals of Probability (1977), 319–350.

- [27] Schwert, G. Why does stock market volatility change over time? The Journal of Finance 44, 5 (1989), 1115–1153.

- [28] Segers, J. On the asymptotic distribution of the mean absolute deviation about the mean. arXiv:1406.4151 (2014).

- [29] Taylor, S. Modelling financial time series. Wiley, New York, 1986.

- [30] Wendler, M. Bahadur representation for u-quantiles of dependent data. Journal of Multivariate Analysis 102, 6 (2011), 1064–1079.

- [31] Zakoian, J.-M. Threshold heteroskedastic models. Journal of Economic Dynamics and Control 18, 5 (1994), 931–955.

- [32] Zumbach, G. Correlations of the realized volatilities with the centered volatility increment. http://www.finanscopics.com/figuresPage.php?figCode=corr_vol_r_VsDV0, 2012. [Online; accessed 25-April-2019].

- [33] Zumbach, G. Discrete Time Series, Processes, and Applications in Finance. Springer Science & Business Media, 2012.

?appendixname? A Different Augmented GARCH models

As mentioned in the paper, we give an overview over the acronyms, authors and relation to each other of the augmented GARCH processes used.

The restrictions on the parameters, if not specified differently, are for , .

-

•

APGARCH: Asymmetric power GARCH, introduced by Ding et al. in [11]. One of the most general polynomial GARCH models.

-

•

AGARCH: Asymmetric GARCH, defined also by Ding et al. in [11], choosing in APGARCH.

-

•

GJR-GARCH: This process is named after its three authors Glosten, Jaganathan and Runkle and was defined by them in [16]. For the parameters it holds that and .

-

•

GARCH: Choosing all in the AGARCH model (or in the GJR-GARCH), gives back the well-known GARCH(, ) process by Bollerslev in [6].

-

•

ARCH: Introduced by Engle in [13]. We recover it by setting all .

-

•

TGARCH: Choosing in the APGARCH model leads us the so called threshold GARCH (TGARCH) by Zakoian in [31]. For the parameters it holds that .

- •

-

•

PGARCH: Another subfamily of the APGARCH processes is the Power-GARCH (PGARCH), also called sometimes NGARCH (i.e. non-linear GARCH) due to Higgins and Bera in [17].

-

•

VGARCH: The volatility GARCH (VGARCH) model by Engle and Ng in [14] is also a polynomial GARCH model but is not part of the APGARCH family.

-

•

NGARCH: This non-linear asymmetric model is due to Engle and Ng in [14], and sometimes also called NAGARCH.

- •

-

•

EGARCH: This model is called exponential GARCH, introduced by Nelson in [24].

Then we give a schematic overview of the nesting of the different models in Figure 1.

Lastly, we present in Table 3 how the conditions or respectively translate for those augmented GARCH(,) processes - this is the generalization of Table 2. As, in contrast to Table 2, we do not gain any insight by considering the choices of or , we only present the general case, .

When we need to consider coefficients for . In case they are not defined, we set them equal to 0.

| augmented | |

|---|---|

| GARCH (, ) | |

| APGARCH | |

| AGARCH | |

| GJR-GARCH | |

| GARCH | |

| ARCH | |

| TGARCH | |

| TSGARCH | |

| PGARCH | |

| VGARCH | |

| NGARCH | |

| MGARCH | and |

| EGARCH | and |