Simple Mechanisms for Profit Maximization in Multi-item Auctions

Abstract

We study a classical Bayesian mechanism design problem where a seller is selling multiple items to multiple buyers. We consider the case where the seller has costs to produce the items, and these costs are private information to the seller. How can the seller design a mechanism to maximize her profit? Two well-studied problems, revenue maximization in multi-item auctions and signaling in ad auctions, are special cases of our problem. We show that there exists a simple mechanism whose profit is at least of the optimal profit for multiple buyers with matroid-rank valuation functions. When there is a single buyer, the approximation factor is for general constraint-additive valuations and for additive valuations. Our result holds even when the seller’s costs are correlated across items.

We introduce a new class of mechanisms called permit-selling mechanisms. For single buyer case these mechanisms are quite simple: there are two stages. For each item , we create a separate permit that allows the buyer to purchase the item in the second stage. In the first stage, we sell the permits without revealing any information about the costs. In the second stage, the seller reveals all the costs, and the buyer can buy item by paying the item price if the buyer has purchased the permit for item in the first stage. We show that either selling the permits separately or as a grand bundle suffices to achieve the constant factor approximation to the optimal profit (6 for additive, and 11 for constrained additive). For multiple buyers, we sell the permits sequentially and obtain the constant factor approximation. Our proof is enabled by constructing a benchmark for the optimal profit by combining a novel dual solution with the existing ex-ante relaxation technique.

1 Introduction

We study the profit maximization problem for selling multiple items to multiple buyers. Unlike most works in Mechanism Design, we consider the case where the seller has costs for obtaining the items. As these costs usually depend on private information that is only available to the seller, we assume that the costs are private to the seller but are drawn from a distribution also known to the buyers. The goal is to design a mechanism that maximizes the profit, that is, the total revenue less the total cost. Revenue maximization in multi-item auctions, one of the most classical and widely studied problem in Bayesian Mechanism Design [11, 12, 6, 9, 2, 30, 17, 18, 26, 28], is a special case of our problem, where the seller always has cost for each item. Arguably, it is more natural and general to assume that there is a cost associated with each item. It may be production cost or opportunity cost, e.g., there is an outside option to sell the item at a certain price.

Despite being realistic and widely applicable, the profit maximization problem is not well-understood. To the best of our knowledge, the only case with non-zero costs that has been studied is in the context of ad auctions [4, 25, 21, 23, 19]. The problem models the following scenario. The auctioneer is selling an ad displaying slot to an advertiser. There are types of viewers of the webpage. The advertiser has value for displaying his ad to a type viewer. In an ad auction, only the auctioneer observes the type of the viewer, and the advertiser only knows a prior distribution from which the viewer-type is drawn from. What mechanism maximizes the auctioneer’s revenue? We can easily cast this problem as a profit maximization problem. Let there be items. When the viewer has type , assign item with cost and all the other items with cost . Clearly, maximizing revenue in the ad auction is equivalent to maximizing profit in the corresponding multi-item setting, as the seller will never sell any item with cost. Many results are known for this special case, which we will discuss in Section 1.4.

In revenue maximization, the optimal mechanism is known to be randomized and complex in multi-item settings. Instead of characterizing the optimal mechanisms, a major and successful research theme in Mechanism Design is devoted to designing simple and approximately optimal mechanisms [11, 12, 14, 2, 9, 28, 29, 32, 7, 10, 30]. As our problem generalizes the multi-item revenue maximization problem, it is clear that the profit-optimal mechanism also requires complex allocation rules and randomization. In this paper, we focus on designing simple and approximately optimal mechanisms for profit maximization.

To facilitate the discussion, we will first focus on the single buyer case. In our model, there are items for sale, and the seller has cost for parting with item . The costs are drawn from a distribution that is known to both the seller and the buyer. We allow the seller’s costs to be correlated across items. Consider constrained-additive buyers, that is, the buyer has a downward-closed feasibility constraint that specifies what bundles of items are allowed. The buyer has value for item , and her value for a bundle is defined as . Similar to most results in the simple vs. optimal literature, we assume to be drawn from independently across items.

Before we state our results, let us examine two natural but unsuccessful attempts to solve this problem.

Two unsuccessful attempts:

(i) Use a mechanism that (approximately) optimizes the revenue. This is a terrible solution as some of the items sold by the mechanism may have extremely high costs, and as a result the mechanism only generates low if any profit. (ii) After the seller sees the costs, reveal them to the buyer, then use the optimal or approximately optimal mechanism that is tailored to those particular costs. The reason why this mechanism may be far away from optimal is much more subtle. Let us consider the following example in the ad auction setting 222The example is similar to the example that shows the revenue of selling the items separately could be -factor worse than the optimal revenue in multi-item auctions with an additive bidder..

Example 1.

A random variable with support follows the equal revenue (ER) distribution if and only if . Let be the ER distribution for each item . Define to be the -dimensional vector whose -th entry is and all the other entries are . Let the costs have probability for each .

The expected profit of the mechanism in (ii): . Since for every , after revealing cost , the seller can only sell item to the buyer.

Consider an alternative mechanism which does not reveal the costs, but offers the buyer the following contract: if the buyer pays up front, the buyer can take any item that is available, e.g. has cost . The chance that the buyer accepts the contract is

and due to a Lemma by [28], we know that it is at least . Hence, the mechanism has profit at least .

Note that in the second mechanism of our example, the seller does not even reveal any information to the buyer and extracts much higher profit.

The two failed attempts highlight two major challenges of our problem: (i) how to balance the revenue and cost; (ii) how to capture the informational rent of the buyer, that is, leveraging the fact that the costs are private information to extract more revenue. We overcome these two challenges by considering what we called permit-selling mechanisms. These mechanisms have two stages. For each item , we create a separate permit that allows the buyer to purchase the item at its cost. In the first stage, we sell the permits without revealing any information about the actual costs. In the second stage, the seller reveals all the costs, and the buyer can buy item by only paying the cost if the buyer has purchased the permit for item in the first stage. How does the buyer make a decision in such a mechanism? In the first stage, the buyer needs to choose her favorite bundle of permits to purchase. Since she knows the distribution , she can compute her utility for each bundle of permits. In the second stage, the buyer simply picks her favorite set of items based on the permits she own, the costs of the items, and her valuation function. Why do the permit-selling mechanisms help addressing the two challenges? Note that the profit of the permit-selling mechanisms is exactly the revenue from the first stage, so any mechanism that achieves high revenue in the first stage also generates high profit. Moreover, the buyer needs to make a decision on what permits to purchase without learning the costs, therefore, the seller can extract the informational rent by pricing the permits appropriately.

Indeed, we do not even need to use any complex pricing scheme in the first stage. We sell the permits separately or sell them as a grand bundle. In our proof we need one more mechanism, which simply sells the items separately, and the prices change according to the seller’s costs. The reason why this class of mechanism is required is more subtle and we only sketch the intuition here. In the permit-selling mechanism, for a fixed buyer type profile t, the buyer purchases a set of permits and thus the seller can only extract revenue from items in , no matter what realized costs she has. However, for different cost vectors, the seller may have different items from which she can extract more revenue. By posting item prices that depend on her cost, the seller is able to target the profitable items based on her realized cost vector. This approach does not capture the informational rent but may generate high profit in certain cases.

Here are the mechanisms we use.

-

•

sell-items-separately (IS): for each possible cost vector , sell the items separately, and the price for item depends on c.

-

•

sell-permits-separately (PS): sell the permits separately, and the price for the -th permit is independent from the seller’s costs.

-

•

permit-bundling (PB): sell all the permits as a grand bundle at a price that is independent from the seller’s costs.

Since in all these mechanisms, the seller does not even ask the buyer to report her valuation, the mechanism is clear incentive compatible (IC) and individually rational (IR). We show that the best mechanism among these three classes of mechanisms can already achieve a constant fraction of the optimal profit.

Theorem 1.

For any valuation distribution , cost distribution , and any downward-closed feasibility constraint , the best mechanism among all sell-items-separately, sell-permits-separately, and permit-bundling mechanisms is an -approximation to the optimal profit.

When the buyer’s valuation is additive, we can improve the approximation factor to .

Theorem 2.

If the buyer has additive valuation, for any valuation distribution and cost distribution , the best mechanism among all sell-items-separately, sell-permits-separately, and permit-bundling mechanisms is a -approximation to the optimal profit.

We then generalize the result to accommodate multiple buyers with matroid-rank valuation functions. With multiple buyers, we sell the permits with a sequential mechanism: buyers arrive in some arbitrary order. When a buyer arrives, we first offer the buyer the permits without revealing any information about the seller’s cost or other buyers’ types. Next, the buyer is given the remaining item set as well as an item price for each item. For single buyer case the item price is always chosen as the seller’s cost for this item. Now we allow any prices that may depend on the cost vector.333In the proof, the item prices is always chosen to be no less than the seller’s cost. Again the buyer can purchase any item from the remaining item set by paying the corresponding item price, if she has the permit for it. The mechanism is BIC and interim IR as the buyer needs to purchase the permit without knowing the seller’s cost or what items are still available. In the proof ,we use Sequential Permit Posted Price (SPP) mechanisms that sell permits separately and Sequential Permit Bundling (SPB) mechanisms that sell permits as a whole bundle. Similar to the single buyer case, we need another mechanism called Constrained Sequential Item Posted Price mechanism (CSIP). It resembles the Sequential Posted Price mechanism from [12]: the items are sold sequentially with posted prices that depend on the seller’s cost vector. The mechanism also imposes a constraint on the set of items a buyer can purchase. See Section 2 for more details.

We prove that the best of three classes of mechanisms can already achieve a constant fraction of the optimal profit.

Theorem 3.

For any cost distribution and buyers’ valuation distributions, if every buyer has a matroid-rank valuation, the best mechanism among all CSIP, restricted SPP444It’s closed to the Sequential Permit Posted Price mechanism, except that the mechanism may hide some items randomly, preventing the buyer from buying some item even she has permit. See Section 2 for more details., and SPB mechanisms is a -approximation to the optimal profit.

1.1 Proof Sketch and Techniques

Since the costs are private, it is a priori not clear that it is sufficient to consider only direct mechanisms. Indeed, signaling mechanisms, a class of indirect mechanisms, are widely studied in the ad auction setting [4, 25, 21, 23, 19]. We first prove a revelation principle for our problem similar to the one proved in [19] for ad auctions. Our revelation principle states that w.l.o.g. we can restrict our attention to direct, BIC, and interim IR mechanisms. Moreover, we can formulate the profit maximization problem as an LP. We next apply the Cai-Devanur-Weinberg duality framework [7]. The framework has become a standard tool for analyzing the performance of simple mechanisms. In most of the results based on this duality approach, a particular family of dual variables, called the “canonical dual” [7, 10], is used to provide a benchmark for the objective function. However, this set of dual variables does not provide an appropriate benchmark due to the existence of costs. We propose a new set of dual variables that is tailored to handle the costs. Indeed, these dual variables are so informative that they inspired us to introduce the permit-selling mechanisms. In the multi-buyer case, the choice of the dual variables is also inspired by the ex-ante relaxation technique from [14]. A similar set of dual variables are used in [10] to provided a benchmark for the optimal revenue.

The benchmark induced by our dual variables can be easily decomposed into three components –

Most-Surplus, Prophet and Less-Surplus. Most-Surplus can be bounded by the profit of the CSIP mechanism using relatively standard analysis. For Prophet, we bound the term using the same class of mechanisms, with the help of the Online Contention Resolution Scheme [24].

For Less-Surplus, in order to establish a connection between profit maximization and revenue maximization, we provide a separate and clean proof for the single buyer case. Instead of directly analyzing the term, we construct an auxiliary revenue maximization problem for selling items to help approximate Less-Surplus. Intuitively, each item in the auxiliary problem corresponds to a permit. We first show that any mechanism in the auxiliary problem can be turned into a permit-selling mechanism in the original problem, such that the revenue in the auxiliary problem is the same as the profit of the permit-selling mechanism. Next, we argue that the buyer has subadditive valuation in the auxiliary problem whenever the buyer has constrained additive valuation in the original problem. Note that the better of selling the items separately and grand bundling is a constant factor approximation of the optimal revenue when the buyer has subadditive valuation [30, 10]. Unfortunately, we cannot use this approximation as a black-box, as it is not yet clear how the revenue in the auxiliary problem relates to the Less-Surplus term. Luckily, Cai and Zhao obtain their result via the CDW duality framework, and in their analysis, they show that a term identical to Less-Surplus can be approximated by the revenue of selling the items separately or grand bundling. Putting everything together, we prove that the profit of a sell-permits-separately or permit-bundling mechanism approximates Less-Surplus, and that completes our proof. For general case, it’s not straightforward build such a connection. We use the standard Core-Tail Decomposition technique [29, 7], dividing Less-Surplus further into two terms Tail and Core. Tail can be approximated using RSPP. For Core, it can be viewed as all buyers’ truncated welfare with respect to a related fractionally-subadditive valuation and we can bound it using SPB and RSPP, by applying the Talagrand s concentration inequality [31].

1.2 Our Contributions

Our main contributions in this paper are the followings:

-

•

We introduce the permit-selling mechanisms and demonstrate their ability to approximate the optimal profit.

-

•

We construct a new set of dual variables that can accommodate costs.

-

•

We establish a connection between profit maximization and revenue maximization for the single buyer case.

1.3 Our Model vs. Two-sided Markets

There has been increasing interest in two-sided markets in the Economics and Computation community recently [15, 16, 22, 3, 5, 1]. In a two-sided market, the mechanism should be designed to incentivize both buyers and sellers to reveal their true private information. Our model is related to the two-sided markets but differs in the following crucial way, that is, we assume that the seller has committing power: the seller commits to a mechanism and follows the mechanism honestly. In other words, the mechanism does not need to satisfy the seller’s Incentive Compatibility (IC) constraint in our model. This is a standard assumption used in both mechanism design for one-sided markets where the seller is also the designer of the mechanism, as well as in information design where the designer commits to a certain information structure. For example, in ad auctions, the seller receives a piece of private information, the type of the item, and sends a signal to the buyer based on this private information using a pre-committed signaling scheme. The model assumes that the seller follows the signaling scheme honestly and does not impose any IC constraints on the seller.

1.4 Related Work

There is a large body of beautiful work on simple vs. optimal for revenue maximization in multi-item auctions [11, 12, 13, 27, 9, 29, 2, 32, 7, 14, 30, 10]. They showed that simple mechanisms can extract a constant fraction of the optimal revenue in rich settings. If there is a single buyer, the state-of-the-art results [30, 10] apply to subadditive valuation functions; if there are multiple buyers, the state-of-the-art result [10] applies to XOS valuation functions. However, none of these results considered costs.

The ad auction problem has also been extensively studied in the literature [4, 25, 21, 23, 19]. Signaling mechanisms had been the focus. In a signaling mechanism, the seller first sends a signal to the buyer based on the type of the viewer and according to a signaling scheme known to the buyer. The buyer updates her posterior belief of the viewer type after observing the signal. The seller then uses a mechanism tailored to the buyer’s updated posterior to sell the ad displaying slot. Many results have been obtained regarding the revenue-optimal signaling scheme. Overall, the optimal signaling scheme may be highly complex and hard to pin down. Interestingly, Daskalakis et al. showed that even if we can find the optimal signaling scheme the corresponding mechanism can still be bounded away from the optimum [19]. They showed that the optimal mechanism is direct and does not involve any signaling. Motivated by their result, we focus on simple and direct mechanisms.

In [19], they also showed how to use simple mechanisms to approximate the auctioneer’s profit in an ad auction. They established the result by reducing the problem to revenue maximization in multi-item auctions with an additive buyer. However, their reduction is ad-hoc and heavily relies on a specific property of their cost distribution, that is, the cost is always one of the s (see Example 1 for the definition). When the cost distribution is general, their reduction no longer holds, and thus is inapplicable to our problem.

2 Preliminaries

We consider the auction where a seller is selling heterogeneous items to buyers. We denote buyer ’s type as , where is buyer ’s value for item . For each , , we assume is drawn independently from the distribution . Let be the distribution of buyer ’s type and be the distribution of the type profile. We use (or ) and (or ) to denote the support and density function of (or ). For notational convenience, we let t to be the types profile of all buyers, to be the types of all buyers except and (or to be the types of the first (or ) buyers. Similarly, we define , and for the corresponding distributions, support sets and density functions.

Each buyer has a constraint-additive valuation, which implies that she is additive over the items but is only allowed to receive a set of items that is feasible with respect to a downward-closed family . In other words, the buyer with type has value when receiving set . For multiple buyer setting we consider a special case of constraint-additive valuation called matroid-rank, where each is a matroid. On the other hand, the seller has a private cost for producing each item . Denote c the cost vector and c is drawn from distribution . Let be the support of . We allow correlated costs in our problem.

For any direct555By Lemma 1, the revelation principle holds in the profit maximization problem. It suffices to consider direct, BIC, and interim IR mechanisms. mechanism and any , denote the probability that buyer is receiving item , when the buyers has type profile t and seller has cost c. Let be the interim allocation probability. Similarly, use to denote the payment for buyer . For any t and c, buyer i’s utility . The seller has profit (revenue minus cost) . We now define the incentive compatibility and individual rationality for our setting.

-

•

Bayesian Incentive Compatible (BIC): reporting the true value maximizes the buyer’s expected utility .

-

•

Dominant Strategy Incentive Compatible (DSIC): for every c and every , reporting the true value maximizes the buyer’s utility .

-

•

interim Individual Rational (interim IR): reporting the true value induces non-negative expected utility. .

-

•

ex-post Individual Rational (ex-post IR): for every c and , reporting the true value induces non-negative utility. .

If the mechanism allocates set to some buyer, and the buyer is only interested in a feasible subset of items , the mechanism can simply allocate set instead. This does not affect the truthfulness for all buyers and increases the seller’s profit. In this paper, we will only consider mechanisms that always allocate a feasible set of items to each buyer . Denote the region for all feasible allocations .

For every mechanism , denote the seller’s expected profit in . We use for short when is clear and fixed.

As we will explain in Lemma 1, it is w.l.o.g. to only consider direct, BIC, and interim IR mechanisms. Let be the optimal profit among all BIC and interim IR mechanisms (use for short when is clear and fixed). Our goal is to use a simple mechanism to approximate .

2.1 Our Mechanisms

We bound the optimal profit by the following three classes of mechanisms. The first mechanism is a variant of the Sequential Item Posted Price (SIP) mechanism, which is first purposed by [12] in the revenue maximization problem. Here we allow the seller to decide posted prices according to her cost vector. Before the auction starts, the seller decides a posted price for each buyer and item , based on her cost vector c. Then buyers come one by one in an arbitrary order. Each buyer can choose her favorite bundle among all remaining items by paying the posted prices. The mechanism is DSIC and ex-post IR. We call the mechanism Constrained Sequential Item Posted Price (CSIP) if it further adds a sub-constraint on the set of items the buyer can purchase. The mechanism first decides a constraint on the ground set of all buyer-item pairs , based on her true cost c. A (possibly random) set represents a way of allocating the items. It’s feasible if

-

•

Each item is allocated to at most one buyer: .

-

•

Each buyer is allocated a feasible set of items: .

Let be the family of all feasible sets. must satisfy . When each buyer comes, she is only allowed to take the item that doesn’t ruin the constraint . See Mechanism 1 for details.

For the CSIP used in our proof, the corresponding sub-constraint can be computed efficiently. See Section 6.2 for more details. We use CSIP-Profit to denote the optimal seller’s profit among all CSIP mechanisms.

Next, we define the two Sequential Permit Selling mechanisms used in the proof. The second class of mechanism is called Sequential Permit Posted Price(SPP). Before the auction starts, the seller decides a posted price for each buyer and item , based on her cost vector c. Then buyers come one by one in an arbitrary order. For each buyer there are two stages: the permit-purchasing stage and item-purchasing stage. In the permit-purchasing stage, instead of selling the items, the seller sells a permit for each item. She decides a price for permit independent from the seller’s cost vector c and buyer type profile t. The buyer is allowed to purchase any permit by paying . The decision must be made before she sees the remaining item set . In the item-purchasing stage, the seller reveals and her cost vector c to the buyer, and the buyer can purchase any remaining item at a price of if the buyer has permit . The buyer is not allowed to purchase item if she does not have the corresponding permit. The buyer chooses her favorite bundle among the items that she is allowed to purchase. Notice that in the second stage, the buyer with set of permits will choose the bundle . Thus, in the first stage, by knowing her type , all the permit prices s, as well as the cost distribution , the buyer is able to calculate her expected surplus in the second stage for any . She will hence choose the best set that maximizes her expected utility in the whole auction and buy all the permits in set . The mechanism is only BIC and Interim IR as buyers have to make decisions before getting any information about other buyers’ types and the seller’s costs. See Mechanism 2 for details.

In our proof we will use restricted Sequential Permit Posted Price mechanisms (RSPP) by adding the following two changes to the mechanism: Firstly, the buyer is only allowed to purchase at most one permit on the permit-purchasing stage. Secondly, we will further allow the mechanism to hide some items from the buyer on the item-purchasing stage. Formally, the mechanism will choose a (possibly random) set and the buyer is only allowed to purchase item in . We will now briefly explain how our mechanism used in the proof chooses this set. In the proof, the item price are chosen such that for every , . We define the random set as follows: for any , put in with probability , independently. Now we have . This is a crucial property in the proof (See Lemma 19). In the rest of the paper, when we mention RSPP, we refer to the mechanism that hides the item as above. We denote RSPP-Profit the optimal profit of these mechanisms.

The third mechanism is Sequential Permit Bundling(SPB). When every buyer comes, the seller bundles the permit of all items together and sell them as a grand bundle at some price in the first stage. is independent from c. If the buyer refuses to pay the price, then she gets no permit and therefore cannot purchase anything in the second stage. If the buyer buys the permit bundle, the seller then reveals the remaining item set and the item prices to the buyer. The buyer then chooses her favorite bundle and pays the item prices. The mechanism is also BIC and interim IR due to a similar argument as for SPP. We use SPB-Profit to denote the optimal profit for all SPB mechanisms. See Mechanism 3 for details.

When there is a single buyer in the auction, the mechanisms described above becomes:

-

•

Item Posted Pricing (IP): for each cost vector c, sell the items separately at price .

-

•

Permit Posted Pricing (PP): sell the permits separately at price that is independent from the seller’s costs. We consider a specific type of mechanisms in the proof where the item price .

-

•

Permit Bundling (PB): sell all the permits as a grand bundle at a price that is independent from the seller’s costs. We consider a specific type of mechanisms in the proof where the item price .

More specifically, for PP and PB, we don’t hide items anymore as there is no competition from other buyers. Denote the optimal profit of the above mechanisms.

3 Paper Organization

In this section, we provide a roadmap for our paper. In Section 4, we introduce a benchmark of the optimal profit using the CDW duality framework. We formulate the maximization problem as an LP, take the Lagrangian dual (Section 4.1), and then define a new set of dual variables (a flow) to derive our benchmark (Section 4.2).

In Section 5, we prove our result for the single constraint-additive buyer case. We divide the benchmark into two terms – Most-Surplus and Less-Surplus – and bound them separately. For Most-Surplus, we bound it using the sell-items-separately mechanism (Section 5.1). For Less-Surplus, we first construct an auxiliary revenue maximization problem for selling items(called the revenue setting). We show that any mechanism in the auxiliary problem can be turned into a permit-selling mechanism in the original problem without changing the value of the objective (Lemma 5). Then we point out that in the benchmark of the optimal revenue in the auxiliary problem, one term is identical to Less-Surplus and can be approximated by the revenue of selling the items separately or grand bundling. Thus by converting the two mechanisms to the permit-selling mechanisms, we can bound Less-Surplus using the PS and PB mechanisms.

In Section 6 we study the case with multiple matroid-rank buyers. The benchmark now is divided into three terms Most-Surplus, Prophet and Less-Surplus. For Most-Surplus, we bound it using the Constrained Sequential Item Posted Price mechanism (Section 6.1). For Prophet, we bound it with the same class of mechanisms, with the help of Online Contention Resolution Scheme (Section 6.2). In Section 6.3, the last term Less-Surplus is bounded by both permit-selling mechanisms, using standard Core-Tail Decomposition technique.

4 Benchmark for the Maximum Profit

In this section, we construct a benchmark for the optimal profit using the Cai-Devanur-Weinberg duality framework. Before getting into the framework and benchmark, we first show that the revelation principle holds in the profit maximization problem. Therefore, it suffices to find a benchmark for the optimal profit attainable by any direct, BIC, and interim IR mechanisms. The proof is postponed to Appendix B.

Lemma 1.

Any ex-post implementable mechanism in the profit maximization problem can be implemented by a direct, BIC, and interim IR mechanism.

4.1 Duality Framework

The framework is first developed in [7] and is widely used in mechanism design. Here we apply the framework to our profit maximization problem. We obtain an upper bound of the optimal profit similar to the upper bound of the optimal revenue obtained in [7]. More specifically, the profit of any BIC, interim IR mechanism is upper bounded by the sum of all buyers’ virtual welfare minus the seller’s total cost for the same allocation, with respect to some virtual value function. We will only show a sketch of the framework in the main body and refer the readers to Appendix A for a complete description.

In the framework, we first formulate the profit maximization problem as an LP. Then take the partial Lagrangian dual of the LP by lagrangifying the BIC and interim IR constraints. Since the buyer’s payment is unconstrained in the partial Lagrangian, one can argue that to obtain any finite benchmark, the corresponding dual variables must form a flow. The virtual value function in the benchmark is then defined according to the choice of the dual variables/flow.

Lemma 2.

For any dual solution that induces a finite benchmark of the optimal profit and any BIC, interim IR mechanism ,

where

can be viewed as buyer ’s virtual value function. Here is the interim allocation. is the Lagrangian dual variable for the BIC/IR constraint that says when the buyer has true type she does not want to misreport .

4.2 Our Flow

Now we choose the dual variables carefully to induce a useful benchmark. First, let us use the single buyer case to provide some intuition behind our flow.

4.2.1 Single Buyer

In [7] and [10], they cleverly choose the canonical flow in the revenue maximization setting. They divide the type space into regions by finding the largest value among all items (called “favorite” item). It is the item that contributes the most to the buyer’s welfare. Then they let the flow go between two nodes only if they differs only on the -th coordinate. However, the same flow does not give us a useful benchmark in our setting, as the way to divide the type space does not even depend on the information of the seller’s costs (i.e. the realized cost c or the cost distribution ). In [7], they also analyze another flow that is considered as a distribution of several canonical flows. We could define our flow similar to theirs: first for any fixed cost vector , divide the region by which item has the largest value and use the above flow. Next, define our flow as a distribution of the flow for , over the randomness of . This attempt does take the cost distribution into account. Unfortunately, this flow does not work as the mechanism constructed based on the sampled cost will not represent the seller’s true profit based on c.

For single buyer, we introduce the following flow. For every , let . Define every as follows: contains all types such that is the smallest index among . We route the flow in a similar manner, that is, there is a flow between two nodes if they only differ on the -th coordinate (see Definition 3). Here is the intuition behind our division. Inspired by the canonical flow, we again want to identify the favorite item for the buyer and divide the regions accordingly. However, the favorite item now should be defined as the one that contributes the most to the buyer’s utility instead of the overall welfare. Note that is exactly the expected utility from item when the item price is , which is the lowest price that the seller is willing to sell the item. That is why we choose to represent the contribution of item to the buyer’s utility. Interestingly, the SPS mechanisms are inspired by our flow, because when there is only one buyer, can also be viewed as the buyer’s “value” for the -th permit when the item price . If we can design a mechanism to extract high revenue from selling the permits, then we have a mechanism that generates high profit. We will make this intuitive connection more concrete in Section 5.2.

4.2.2 Multiple Buyers

Inspired by the single buyer case, we again aim to extract high revenue from selling the permits to make sure our mechanism generates high profit. When there are multiple buyers in the auction, we sell items sequentially to the buyers and our mechanism should satisfy the following two properties:

-

•

The item price should be carefully chosen as the item can not be over-allocated. Usually in the sequential mechanism, the item price should be large enough, to make sure that the item is available to every buyer when she comes to the auction, with certain probability.

-

•

The item price should be at least the seller’s cost, to make sure the revenue extracted from selling the items is enough to cover the cost.

Intuitively, how the flow is chosen should also depend on the format of the mechanism we aim to use. To satisfy both properties, we combine our flow in Section 4.2.1 with the ex-ante relaxation technique purposed in [14]. [10] uses the same technique to construct the flow. They divide the type space by comparing the difference between value and the quantile induced from ex-ante allocation probability. Here we involve different quantile thresholds for different cost realization. Furthermore, in order to satisfy the second property, we choose our threshold as the maximum between the quantile and seller’s cost.

Definition 1.

(Ex-ante relaxation) Fix mechanism . For every and , define , and let

if . If not, for simplicity we assume that there exists such that . This is true for continuous distribution . For discrete distributions, our results will hold by dealing with a tie-breaking issue. We refer the readers to Section 5.3 of [10] for more details. In the further proof we will focus on continuous distributions and a same fix will apply for discrete distributions.

We denote the mappings from c to for all . Before defining the flow, we need the following definition.

Definition 2.

Fix . For every and set , define

Remark: is equal to by choosing .

For notational convenience, let 666For any value x, denote , which only depends on . It coincides with the definition in Section 4.2.1 with .

Now we are ready to define our flow for multiple buyer case.

Definition 3.

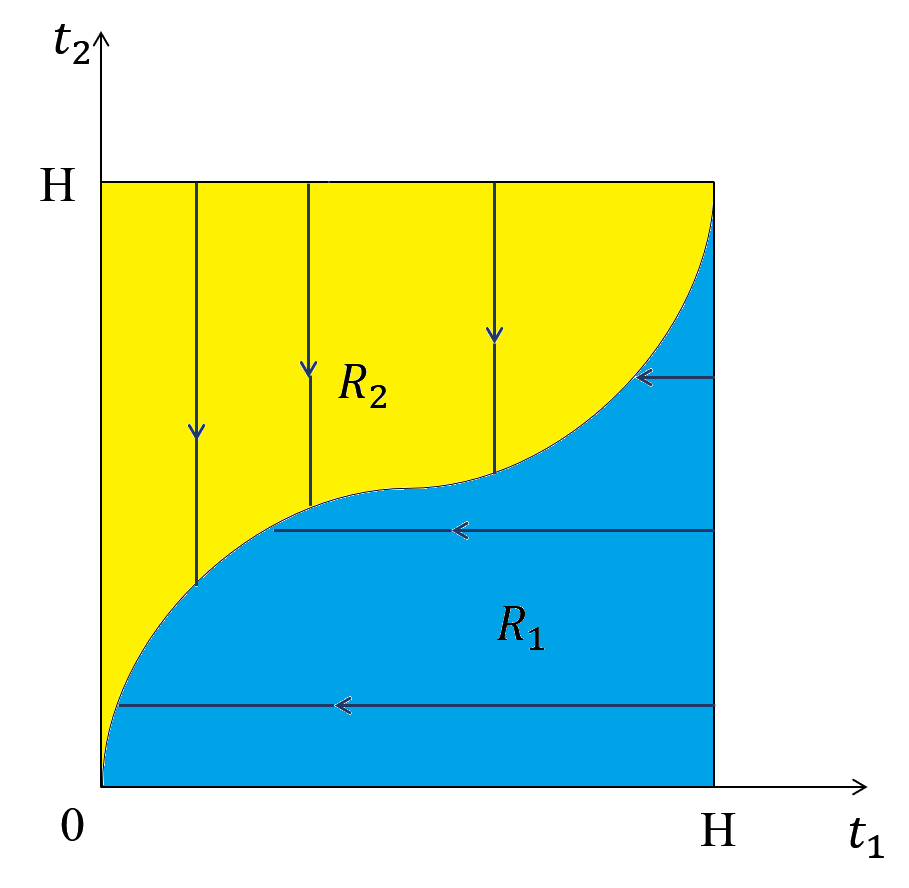

(Our flow) Fix . For every , contains all types such that is the smallest index among . Define the flow as follows: Each node receives flow of weight from the source. For every node , only if for all , and is the predecessor type of 777In other words, is the smallest value in the support set that is greater than .. For node , if there does not exist a successor type of such that , all flow entering node goes to the sink . Figure 1 shows an example of our flow for some buyer when . The curve in the graph contains all such that .

Since for all , is non-decreasing, each region is upward-closed: for every and , . With this property, we have the following Lemma from [7].

Lemma 3.

[7] Fix any . There exists a flow such that for every , ,

where is the Myerson’s ironed virtual value function w.r.t. .

With Lemma 2 and 3, we have obtained a benchmark for any BIC, interim IR mechanism and divide it into three terms. Note that the benchmark may differ for different mechanisms. The proof of Theorem 4 can be found in Appendix B.

Theorem 4.

For any BIC, interim IR mechanism , let be the mapping associated with in Definition 1, then

We use , and to denote the three terms accordingly. Note that all three terms depend on . For the rest of the paper we show that these three terms can be bounded by the profit of simple mechanisms for any induced by a BIC, interim IR mechanism . In fact, to prove an approximation of the optimal profit, it is sufficient to consider one specific induced by the optimal mechanism. In the proof, we fix and omit it in the notation.

5 Warm-up: Single, Constraint-Additive Buyer

In this section, we bound the benchmark for single, constraint-additive buyer. In this case, all s are set to 0 and thus . We will prove the following theorem.

Theorem 5.

When , for any valuation distribution , cost distribution and any downward-closed feasibility constraint ,

When the buyer’s valuation is additive,

Theorem 5 implies that a simple randomization among the three mechanisms achieves at least the optimal profit for any downward-closed . And for additive valuations, a randomization among the three mechanisms is a -approximation to the optimal profit.

5.1 Bounding Most-Surplus

To bound Most-Surplus, we will consider the Copies Setting from [12], which is a single-dimensional setting in the revenue maximization problem. Here is a sketch of the proof. For any fixed cost vector c, we first focus on a related revenue maximization problem with a single buyer and multiple items, by simply subtracting the fixed cost c from the buyer’s value t. Next, we show that the optimal revenue in the copies setting of the related revenue maximization problem is an upper bound of Most-Surplus. According to [12], there exists a posted price mechanism in the multi-item setting whose revenue approximates the optimal revenue in its copies setting. Finally, we show an Item Posted Pricing mechanism whose expected profit is the same as to the expected revenue of the posted price mechanism.

For any fixed c, we will first focus on the following revenue maximization problem with a single buyer and items. Buyer has value for each item , where is drawn independently from . Since c is a fixed vector, the buyer’s values are independent across items. The buyer is constraint-additive with respect to the feasibility constraint .

The Copies Setting of the above problem is as follows: there are buyers in the auction and copies to sell. Buyer only interests in the -th copy and has value for it, where is drawn independently from . Since c is a fixed vector, all buyers’ values are also independent. The seller has no cost for the copies but has a downward-closed constraint that specifies which copies can simultaneously be sold. Denote the optimal revenue for the copies setting. Since it is a single dimensional setting, Myerson’s auction achieves the optimal revenue, which equals to the maximum ironed virtual welfare

Moreover, let be the optimal revenue if we further restrict the seller to sell at most one copy. Similarly . We have the following lemma.

Lemma 4.

. When the buyer is additive, we further have . Moreover, there exists an IP mechanism where only depends on for every , such that .

Proof.

We first prove the result for arbitrary downward-closed constraint . Notice that for every t, the indicator is 1 for only one . Since , we have

| Most-Surplus | |||

By [12], there exists a posted price mechanism in the revenue maximization problem whose revenue is at least . Let be the posted price for item .

Now we move back to our profit maximization setting and define the IP mechanism as follows: For every cost vector c, define the posted price for item as . Notice that for every t and c, the buyer in will purchase the same bundle as the one in . Here . Thus the seller’s profit of is

When the buyer is additive, for any fixed c, it is not hard to realize that equals to the revenue of selling each item separately using the monopoly reserve in the revenue maximization problem. Let be the monopoly reserve for item in the revenue maximization problem. Following the same proof as above, the IP mechanism with price achieves expected profit at least

∎

5.2 Bounding Less-Surplus

Before bounding Less-Surplus, we will first prove a crucial lemma of this section. Consider the revenue maximization problem with a single buyer and items. The buyer’s type . She has valuation function when her type is t. For simplicity, we will call this revenue maximization problem the revenue setting, and the original profit maximization problem the profit setting. Recall that in the single buyer case,

The following lemma converts any truthful mechanism in the revenue setting into a BIC and interim IR mechanism in the profit setting, without changing the value of the objective (revenue and profit accordingly). The intuition behind the lemma is as follows. For any mechanism in the profit setting that sells the permit before revealing her true cost, the buyer with type t has expected “value” , that is, how much the buyer can make from the second stage if given a set of permits , for all set of permits . Thus, the mechanism can be viewed as a corresponding mechanism in the revenue setting where the permits are being sold and the buyer has valuation over the permits.

Lemma 5.

For any truthful mechanism in the revenue setting, there exists an IC and IR mechanism in the profit setting such that, the revenue of equals to the seller’s profit of .

Proof.

For any t, let be the (possibly random) set of items that the buyer is allocated in mechanism , when the buyer reports t. Let be the payment for the buyer in . Define as follows: in the first stage, the buyer reports her type t and the seller gives the set of permits to the buyer and charge . In the second stage, the seller reveals the cost vector c and the buyer can buy any item that she has a permit by paying item price . To prove is an IC and IR mechanism, it suffices to show that the buyer has no incentive to lie in the first stage. If the buyer with type t reports in , she will receive the set of permits and purchase her favorite bundle of items under item prices c. Her expected utility is

Here the expectation is taken over the randomness of . Since is truthful, for any 999Recall that contains the choice of not attending the auction., . It states that when the buyer has type t, reporting t in the first stage maximizes her expected utility. Thus is IC and IR. Notice that in the second stage of , the total item prices paid by the buyer is equal to the seller’s total cost. Thus the seller’s profit is exactly the payment in the first stage. Since use as the payment rule, the seller’s profit of equals to the revenue of . ∎

Now we are ready to bound the term Less-Surplus. Recall that

Consider the revenue setting where the buyer has valuation function and let be the optimal revenue among all truthful mechanisms. Here we omit and in the notation as they are fixed. Given Lemma 5, it is tempting to find a simple mechanism that approximates and convert it into a permit-selling mechanism. However, since we do not know what class of valuation belongs to, it not a priori clear any simple vs. optimal result applies here. As the original valuation in the profit setting is constrained additive, it is natural to think that is also constrained additive. Unfortunately, we are not able to prove such a claim as there is no clear feasibility that is associated with . The good news is that we are able to relax the class of valuations and show that is indeed a subadditive function, which allows us to leverage the result by [30, 10].

Let us first review their results. They bound when is subadditive over independent items (see Definition 4). In both proofs, they separate the benchmark of the optimal revenue into two terms (called “single” and “non-favorite” in [10]). They then bound the two terms by the optimal revenue of the Selling Separately mechanism() and Bundling mechanism() respectively. The second term “non-favorite” is defined as the expected welfare from all non-favorite items. Here for any fixed t, the favorite item is defined as the that maximizes . Interestingly, this is how we divide the region into s and the term “non-favorite” is exactly the same as Less-Surplus. We will use to denote “non-favorite” here to emphasize that it is from the revenue setting.

In order to apply the result in the revenue setting, we first show that the function in Definition 2 is indeed subadditive over independent items. The proof of Lemma 6 is postponed to Appendix C.

Definition 4.

[30] Suppose the buyer’s type t is drawn from a product distribution , her distribution of valuation function is subadditive over independent items if:

-

•

has no externalities, i.e., for each and , only depends on , formally, for any such that for all , .

-

•

is monotone, i.e., for all and , .

-

•

is subadditive, i.e., for all and , .

Lemma 6.

is monotone, subadditive and has no externalities.

Lemma 7.

[10] Suppose is subadditive over independent items, then

We only provide a sketch of their analysis here and refer the readers to their paper for a formal proof. They first use the Core-Tail Decomposition technique and divide into two terms and . The term can be bounded using . can be viewed as the buyer’s expected welfare under a truncated valuation. They show that the welfare concentrates via a concentration inequality for subadditive functions[31]. In particular, they show that the median of the welfare is comparable to the mean of the welfare. Thus, a grand bundling mechanism that uses the median as the price is able to approximate .

When the buyer is additive, [7] has an improved bound for using and .

Lemma 8.

[7] If is an additive function, then

By Lemma 5, the Selling Separately mechanism in the revenue setting can be converted to the PP mechanism in the profit setting and has profit equals to . Also the Bundling mechanism can be converted to PB and obtains profit . Furthermore, when the buyer is additive, there is no constraint and for every ,

Thus, is an additive function. We have the following Corollary:

Corollary 1.

. When the buyer is additive, .

When the buyer is additive, according to [28], , the revenue of the optimal bundling mechanism, is bounded by . Thus Corollary 1 implies an -approximation to the optimal profit with only IP and PP mechanisms. Both mechanisms sell the items separately. Thus the optimal profit for items is bounded by times the sum of the optimal profit for every single item.

Theorem 6.

When the buyer is additive,

Moreover,

where is the Myerson’s ironed virtual value function for .

Proof.

According to [28], . Combining this result with Lemma 4 and Corollary 1, we have the following: there exists an IP mechanism where the posted price only depends on for every , such that

Since the buyer is additive, is equivalent to the sum (over all ) of the profit that sells a single item with price . Note that for any PP mechanism with permit prices , the profit is equivalent to the sum (over all ) of the profit that sells a single item with permit price . Thus

It remains to prove that for every , the optimal profit when selling a single item , is at most . In the auction with a single item , by Lemma 2, we have following for any dual variable :

where . Note that in the auction for selling a single item , both the buyer’s value and seller’s cost are scalar. By Corollary 18 of [8], when the optimal dual variable is chosen, . Thus

where the last equality follows from . ∎

At the last of this section, we will prove the following lemma that connects the profit maximization problem to the revenue maximization problem. We show that any truthful mechanism in the revenue setting that is an -approximation to the optimal revenue can be converted to a BIC and interim IR mechanism in the profit setting that is a -approximation to the optimal profit.

Lemma 9.

Recall that the revenue setting is the revenue maximization problem where the buyer has valuation . Then any truthful mechanism in the revenue setting that is an -approximation to the optimal revenue can be converted to an IC and IR mechanism in the profit setting that is a -approximation to the optimal profit .

Proof.

By Lemma [10],

Let be the -approximation mechanism in the revenue setting. Then the revenue of satisfies:

By Lemma 5, there exists a BIC and interim IR mechanism in the profit setting such that . Notice that . By Theorem 4,

Thus a randomization between and the optimal Item Posted Pricing mechanism is a -approximation. ∎

6 Multiple, Matroid-Rank Buyers

In this section, we will bound the benchmark in Theorem 4 for multiple, matroid-rank buyers, using the mechanisms described in Section 2.

Theorem 7.

For any valuation distribution , cost distribution and any matroid feasibility constraints ,

Again a simple randomization among the three mechanisms achieves at least the optimal profit.

6.1 Bounding Most-Surplus

Similar to the single buyer case, for every fixed vector c, we consider the related revenue maximization problem where every buyer has value for item . The corresponding Copies Setting is a revenue maximization problem with buyers and items. Every buyer only interests in item and has value on it. For every , at most one can be served in the mechanism. We denote the optimal revenue of this setting. In Lemma 10 we first bound Most-Surplus by . Then according to [12], can be approximated by the revenue of the optimal sequential posted price mechanism in the related revenue maximization setting. Assume the posted price for buyer and item is . We show that in our setting, an SIP mechanism with has profit the same as the expected (over the randomness of c) revenue of the above sequential posted price mechanism.

Lemma 10.

.

Proof.

Recall that

For every BIC, interim IR mechanism and every c, consider the following mechanism in the Copies Setting: serves agent if and only if allocates item to buyer and . Since is feasible, for every there exist at most one such that is served in . Also since every stays in one region, for every there exists at most one such that is served in . Thus is feasible and the expected revenue equals to . Thus we have

By [12], for every c there exists a sequential posted price mechanism in the related revenue maximization setting101010Recall that in this setting every buyer has value for item ., where every buyer can purchase at most one item, such that its revenue is at least . Suppose the posted price for buyer and item is . Now let’s consider the Constrained Sequential Item Posted Price mechanism with in our profit maximization setting, where every buyer is only allowed to purchase at most one item. For every , let be the remaining item sets when buyer comes to the auction. Then she will choose her favorite item (or choose not to purchase anything). Notice that this is also buyer ’s favorite item in under the same scenario. Thus the allocation rule for CSIP under c is the same as the one for . Then profit of the constructed CSIP is equal to the expected revenue of over the randomness of c, as the extra item prices just cover the seller’s costs. According to [12], the profit is at least . The proof is done. ∎

6.2 Bounding Prophet

In this section we will bound Prophet with a Constrained Sequential Item Posted Price mechanism. The proof uses Online Contention Resolution Scheme(OCRS) developed by Feldman et al. [24]. It is defined under an online selection problem. For simplicity, we will just describe the setting considered in our proof. Each element in an ground set is revealed one by one, and an agent has to make a decision whether to take an element before the next one is revealed. In our proof the ground set is , the set containing all buyer-item pairs. And each element is one of the buyer-item pair. The agent can only take a feasible set of elements subject to the feasibility constraint . The set of active elements is random, and the agent can only take the active elements. Let be the random set of active elements, where vector . For each , each element is chosen as active or inactive independently and is the probability of being active. stays in the polytope corresponding to :

An OCRS for is an online algorithm that selects a feasible and active set: and . Specifically, a greedy OCRS uses a greedy scheme during the selection: for each , it determines a subfamily . It selects an element when arrives if, the set of elements selected still stays in after picking .

In the proof we will mainly consider the following property of a greedy OCRS called selectability. It is first defined in [24].

Definition 5.

[24] Let . A greedy OCRS is -selectable if for every ,

The above definition can be described as follows. With probability at least , over the randomness of , for any subset of the active elements that is feasible w.r.t. the subfamily , we can add element to the set without violating the feasibility. View as the set of elements being served by the greedy OCRS . When arrives, -selectability guarantees that not matter what set of elements has been chosen already (still a subset of ), with probability at least , adding element is still feasible. By Definition 5, one can show that by following the OCRS, the agent will select each element with probability at least , under any almighty adversary111111The adversary can determine the order of elements shown to the agent. An almighty adversary has all the information it needs to decide the order, including the agent’s type and strategies, and the realization of all possible randomness. In other words, the adversary will choose the worst order for the agent..

Lemma 11.

([24]) Consider the online selection setting described above. If there exists a -selectable greedy OCRS for , then for every , consider the strategy that the agent takes elements greedily subject to the sub-constraint . Then the agent will select each element with probability at least . The result applies for any almighty adversary.

Before getting to the proof, let’s first discuss the connection between OCRS and bounding Prophet. Recall that

Fix c. For every , let . Since is half the ex-ante probability that a feasible mechanism serves the pair when the true cost is c, thus . Now consider the CSIP with item prices . Then by Definition 1, each buyer can afford item with probability 121212It’s true when . For those such that , the corresponding term in Prophet is 0. We could simply never serve those pairs., i.e. the element is active with probability . In Lemma 12 we show that for one specific almighty adversary, the set of element chosen by the agent following the greedy OCRS is exactly same as the set of buyer-item pair served in the mechanism, for every type profile. Then -selectability guarantees that every buyer will purchase every item in the mechanism with probability at least given the fact that she can afford this item. This gives a lower bound of CSIP-Profit.

Lemma 12.

Fix seller’s cost vector c. Suppose there exists a -selectable greedy OCRS for polytope , for some constant . For every s such that , consider the CSIP under the specific cost profile c, with posted price and sub-constraint . Then the mechanism will gain profit at least

under cost c.

Proof.

Under cost c, consider the CSIP with posted price , associated with the constraint . When every buyer comes, let be the set of buyer-item pairs that have already been served. And let be her favorite bundle among the remaining items, such that after taking those items, the sub-constraint is not violated. Now consider the online selection setting with the following almighty adversary: Ground set is . The agent has value for each element . Each element is active if , i.e. is active with probability . The adversary divides the whole item-revealing process into stages. For each stage , let be the set of elements that have been selected in the past. The adversary first reveals all s where , one after another. Then it reveals the remaining s.

Notice that by following the greedy OCRS , the agent will follow the constraint and choose all the element where on each stage, as taking those elements won’t violate the constraint by the definition of . It’s equivalent to the buyer-item pair selection process in the CSIP. Thus under the above adversary, the set of element chosen by the agent is exactly same as the set of buyer-item pair served in the mechanism. Since each element is active with probability and , by Lemma 11, each element is chosen by the agent with probability at least . In other words, in CSIP, each buyer purchases item with probability at least , under cost c. Thus the obtained profit is at least

∎

Now it’s sufficient to show that there exists a -selectable greedy OCRS for . Recall that every satisfies:

-

•

Each item is allocated to at most one buyer: .

-

•

Each buyer is allocated a feasible set of items: .

Let (or ) be the subfamily that contains all set that satisfies the first(or second) bullet point. It’s straightforward to see that forms a partition matroid. We will show that is also a matroid, given the fact that every is a matroid.

Lemma 13.

is a matroid.

Proof.

Consider any such that . For every , let and . We have . Notice that , there must exist such that . Since is a matroid, there exists some such that . By definition of , we also have and . Thus is a matroid. ∎

Note that . is an intersection of two matroids. We can show that there exists a -selectable greedy OCRS for by the following two facts from [24].

Lemma 14.

([24])For every , there exists a -selectable greedy OCRS for matroid polytopes.

Lemma 15.

([24])Suppose there exists a -selectable greedy OCRS for and a -selectable greedy OCRS for . Then there exists a -selectable greedy OCRS for . Moreover, since , there exists a -selectable greedy OCRS for .

Put everything together, we are able to bound Prophet using CSIP-Profit.

Lemma 16.

.

Proof.

First for those such that , the corresponding term in Prophet is 0. We could simply never serve those pairs. Thus without loss of generality, we assume that for every . For every c, since is half the ex-ante probability that a feasible mechanism serves the pair when the true cost is c, thus . By Lemma 14 and 15, there exists a -selectable greedy OCRS for . We thus consider the CSIP with posted price , associated with the constraint . By Lemma 12, the profit of the mechanism is at least

∎

6.3 Bounding Less-Surplus

In this Section we will bound Less-Surplus. As discussed in Section 4, we will fix and omit it in the notation. We first give an informal proof by reducing the multiple buyer problem to single buyer problems with a new valuation in Definition 2. This shows a connection to the single buyer setting as well as the ex-ante relaxation by Chawla and Miller[14]. In their paper they solve the revenue maximization problem for multiple matroid-rank buyers, bounding the benchmark by the sum of optimal revenue for the single buyer problem under an ex-ante constraint.

Recall that

This is the sum of all buyer’s welfare contributed by those non-favorite “items”131313Here we use quotations on the word ‘item’ as in the corresponding single buyer problem, the goods sold to the buyers are permits, not real items., under a new valuation . Consider the Sequential Permit Selling mechanism with posted price . Since for every c, the profit of the mechanism will be at least the revenue extracted from the permit copies.

Notice that for every , buyer can afford the item price for with probability . Thus by union bound, each item is still available when buyer comes with probability at least . By Lemma 23, buyer ’s expected utility in the second stage after purchasing a set of permit copies , is at least . Now we have reduced the multiple buyer problem to single buyer problems where buyer has valuation for the set of permit copies. Thus from Section 5, the term can be extracted from selling the permit copies separately and as a whole bundle.

The above argument doesn’t give a formal proof because the buyer’s expected utility on the copies does not exactly equal to and thus a reduction like Lemma 5 cannot be directly obtained. Now we provide a formal and separate proof, bounding Less-Surplus with RSPP and SPB mechanisms. First we decompose the term using a standard Core-Tail decomposition technique [29, 7], according to . For every , define . For every , let .

Lemma 17.

Proof.

| Less-Surplus | |||

∎

6.3.1 Tail

We will bound Tail using RSPP mechanisms. For every , let , which is the optimal revenue from selling permit to buyer . Let . We first show that and then bound using a RSPP.

Lemma 18.

.

Proof.

| Tail | |||

∎

The following lemma bounds using the RSPP.

Lemma 19.

For any positive such that , we have

Proof.

Consider the RSPP mechanism with permit price and item price . Notice that for every buyer , her expected utility for purchasing each permit is . She will purchase every permit for sure if both of the events happen:

-

1.

She is willing to purchase permit , i.e., .

-

2.

She is not willing to purchase other permits, i.e., .

(1) happens with probability ; By union bound, (2) happens with probability at least as . Furthermore, both events are independent and thus buyer will purchase permit and pay the permit price with probability at least . ∎

We point out that in the above lemma, it’s necessary to make every buyer ’s expected utility for purchasing each permit to be exactly . This is the reason the RSPP mechanism needs to hide each item randomly to make each item available with probability exactly (See Section 2). If the mechanism doesn’t hide the item, we only know that her expected utility for each permit is at least that much. We are not able to lower bound the probability that (2) happens using union bound.

Lemma 20.

.

6.3.2 Core

In this section we bound Core using RSPP and SPB.

Theorem 8.

.

Recall that . In the proof we will consider the SPB mechanism with item prices and permit bundle price . In order to show that each buyer will accept this bundle price with at least half probability, we will prove the expected utility for the item-purchasing stage is at least . We need the following definition.

Definition 6.

Consider the above SPB mechanism. For every and , let

By Definition 6, buyer ’s expected utility for the item purchasing stage is . Recall that is the set of available items in the above SPB mechanism. We notice that for every , buyer can afford the item price for with probability . Thus by union bound, each item is still available when buyer comes with probability at least , i.e. . Then by showing that all s are XOS valuations, we prove that every buyer has expected utility at least to enter the auction.

Definition 7.

A function is XOS(or fractionally-subadditive) if for every , for some finite and additive functions .

Lemma 21.

([20]) A function is XOS if and only if for every , there exist prices (called supporting prices) such that

-

•

for all .

-

•

.

Lemma 22.

For every , is an XOS function.

Proof.

Fix . For every , let . Define supporting prices for set as follows: . It’s easy to check that s satisfy both constraints in Lemma 7. Thus is an XOS function. ∎

Lemma 23.

Consider the above SPB mechanism. For every , buyer will accept the bundle price with at least probability.

Proof.

As stated above, for every buyer with type , her expected utility on the item-purchasing stage is . For every , buyer can afford the item price for with probability . Thus by union bound, .

Thus buyer will pay with probability at least . ∎

Now it’s sufficient to show that is comparable to for every . This is obtained by applying the Talagrand¡¯s concentration inequality on . Let . We show that is subadditive and has small Lipschitz constant. The proof is Lemma 24 is postponed to Appendix D.

Definition 8.

A function is -Lipschitz if for any type , and set ,

where is the symmetric difference between and .

Lemma 24.

is monotone, subadditive, no exteralities and has Lipschitz constant .

Lemma 25.

[31] Let with be a function drawn from a distribution that is subadditive over independent items of ground set . If is -Lipschitz, then for all ,

The following corollary comes from [10]. It’s a corollary of Lemma 25. It shows that for every , is bounded by and the Lipschitz constant .

Corollary 2.

[10]

For the last step, can be bounded using the RSPP.

Lemma 26.

.

Proof.

Proof of Theorem 8: Consider the SPB mechanism with item prices and permit bundle price . According to Lemma 23, 26 and Corollary 2,

References

- [1] Moshe Babaioff, Yang Cai, Yannai A. Gonczarowski, and Mingfei Zhao. The best of both worlds: Asymptotically efficient mechanisms with a guarantee on the expected gains-from-trade. In Proceedings of the 2018 ACM Conference on Economics and Computation, Ithaca, NY, USA, June 18-22, 2018, page 373, 2018.

- [2] Moshe Babaioff, Nicole Immorlica, Brendan Lucier, and S. Matthew Weinberg. A Simple and Approximately Optimal Mechanism for an Additive Buyer. In the 55th Annual IEEE Symposium on Foundations of Computer Science (FOCS), 2014.

- [3] Liad Blumrosen and Shahar Dobzinski. (almost) efficient mechanisms for bilateral trading. CoRR, abs/1604.04876, 2016.

- [4] Peter Bro Miltersen and Or Sheffet. Send mixed signals: earn more, work less. In Proceedings of the 13th ACM Conference on Electronic Commerce, pages 234–247. ACM, 2012.

- [5] Johannes Brustle, Yang Cai, Fa Wu, and Mingfei Zhao. Approximating gains from trade in two-sided markets via simple mechanisms. In Proceedings of the 2017 ACM Conference on Economics and Computation, EC ’17, Cambridge, MA, USA, June 26-30, 2017, pages 589–590, 2017.

- [6] Yang Cai and Constantinos Daskalakis. Extreme-Value Theorems for Optimal Multidimensional Pricing. In the 52nd Annual IEEE Symposium on Foundations of Computer Science (FOCS), 2011.

- [7] Yang Cai, Nikhil R. Devanur, and S. Matthew Weinberg. A duality based unified approach to bayesian mechanism design. In the 48th Annual ACM Symposium on Theory of Computing (STOC), 2016.

- [8] Yang Cai, Nikhil R Devanur, and S Matthew Weinberg. A duality-based unified approach to bayesian mechanism design. SIAM Journal on Computing, (0):STOC16–160, 2019.

- [9] Yang Cai and Zhiyi Huang. Simple and Nearly Optimal Multi-Item Auctions. In the 24th Annual ACM-SIAM Symposium on Discrete Algorithms (SODA), 2013.

- [10] Yang Cai and Mingfei Zhao. Simple mechanisms for subadditive buyers via duality. In Proceedings of the 49th Annual ACM SIGACT Symposium on Theory of Computing, STOC 2017, Montreal, QC, Canada, June 19-23, 2017, pages 170–183, 2017.

- [11] Shuchi Chawla, Jason D. Hartline, and Robert D. Kleinberg. Algorithmic Pricing via Virtual Valuations. In the 8th ACM Conference on Electronic Commerce (EC), 2007.

- [12] Shuchi Chawla, Jason D. Hartline, David L. Malec, and Balasubramanian Sivan. Multi-Parameter Mechanism Design and Sequential Posted Pricing. In the 42nd ACM Symposium on Theory of Computing (STOC), 2010.

- [13] Shuchi Chawla, David L. Malec, and Balasubramanian Sivan. The power of randomness in bayesian optimal mechanism design. Games and Economic Behavior, 91:297–317, 2015.

- [14] Shuchi Chawla and J. Benjamin Miller. Mechanism design for subadditive agents via an ex-ante relaxation. In Proceedings of the 2016 ACM Conference on Economics and Computation, EC ’16, Maastricht, The Netherlands, July 24-28, 2016, pages 579–596, 2016.

- [15] Riccardo Colini-Baldeschi, Bart de Keijzer, Stefano Leonardi, and Stefano Turchetta. Approximately efficient double auctions with strong budget balance. In Proceedings of the Twenty-Seventh Annual ACM-SIAM Symposium on Discrete Algorithms, SODA 2016, Arlington, VA, USA, January 10-12, 2016, pages 1424–1443, 2016.

- [16] Riccardo Colini-Baldeschi, Paul W. Goldberg, Bart de Keijzer, Stefano Leonardi, Tim Roughgarden, and Stefano Turchetta. Approximately efficient two-sided combinatorial auctions. CoRR, abs/1611.05342, 2016.

- [17] Constantinos Daskalakis, Alan Deckelbaum, and Christos Tzamos. Mechanism design via optimal transport. In ACM Conference on Electronic Commerce, EC ’13, Philadelphia, PA, USA, June 16-20, 2013, pages 269–286, 2013.

- [18] Constantinos Daskalakis, Alan Deckelbaum, and Christos Tzamos. The complexity of optimal mechanism design. In the 25th Annual ACM-SIAM Symposium on Discrete Algorithms (SODA), 2014.

- [19] Constantinos Daskalakis, Christos Papadimitriou, and Christos Tzamos. Does information revelation improve revenue? In Proceedings of the 2016 ACM Conference on Economics and Computation, pages 233–250. ACM, 2016.

- [20] Shahar Dobzinski, Noam Nisan, and Michael Schapira. Approximation algorithms for combinatorial auctions with complement-free bidders. In STOC, pages 610–618, 2005.

- [21] Shaddin Dughmi, Nicole Immorlica, and Aaron Roth. Constrained signaling in auction design. In Proceedings of the twenty-fifth annual ACM-SIAM symposium on Discrete algorithms, pages 1341–1357. Society for Industrial and Applied Mathematics, 2014.

- [22] Paul Dütting, Tim Roughgarden, and Inbal Talgam-Cohen. Modularity and greed in double auctions. In ACM Conference on Economics and Computation, EC ’14, Stanford , CA, USA, June 8-12, 2014, pages 241–258, 2014.

- [23] Yuval Emek, Michal Feldman, Iftah Gamzu, Renato PaesLeme, and Moshe Tennenholtz. Signaling schemes for revenue maximization. ACM Transactions on Economics and Computation, 2(2):5, 2014.

- [24] Moran Feldman, Ola Svensson, and Rico Zenklusen. Online contention resolution schemes. In Proceedings of the Twenty-Seventh Annual ACM-SIAM Symposium on Discrete Algorithms, SODA 2016, Arlington, VA, USA, January 10-12, 2016, pages 1014–1033, 2016.

- [25] Hu Fu, Patrick Jordan, Mohammad Mahdian, Uri Nadav, Inbal Talgam-Cohen, and Sergei Vassilvitskii. Ad auctions with data. In Algorithmic Game Theory, pages 168–179. Springer, 2012.

- [26] Yiannis Giannakopoulos and Elias Koutsoupias. Duality and optimality of auctions for uniform distributions. In ACM Conference on Economics and Computation, EC ’14, Stanford , CA, USA, June 8-12, 2014, pages 259–276, 2014.

- [27] Sergiu Hart and Noam Nisan. Approximate Revenue Maximization with Multiple Items. In the 13th ACM Conference on Electronic Commerce (EC), 2012.

- [28] Sergiu Hart and Noam Nisan. Approximate revenue maximization with multiple items. Journal of Economic Theory, 172:313–347, 2017.

- [29] Xinye Li and Andrew Chi-Chih Yao. On revenue maximization for selling multiple independently distributed items. Proceedings of the National Academy of Sciences, 110(28):11232–11237, 2013.

- [30] Aviad Rubinstein and S. Matthew Weinberg. Simple mechanisms for a subadditive buyer and applications to revenue monotonicity. In Proceedings of the Sixteenth ACM Conference on Economics and Computation, EC ’15, Portland, OR, USA, June 15-19, 2015, pages 377–394, 2015.

- [31] Gideon Schechtman. Concentration, results and applications. Handbook of the geometry of Banach spaces, 2:1603–1634, 2003.

- [32] Andrew Chi-Chih Yao. An n-to-1 bidder reduction for multi-item auctions and its applications. In SODA, 2015.

Appendix A Duality Framework

The seller aims to maximize her profit among all direct, BIC, and interim IR mechanisms. This maximization problem can be captured by the following LP (see Figure 2). Here we use type to represent the choice of not participating in the mechanism. Now the IR constraint can be described as another BIC constraint that the buyer won’t report type . Let .

Variables:

•

, for all , , denotes the interim probability vector that buyer with type receives each item, when the seller has cost c.

•

, for all , , denoting the buyer ’s interim payment when she has type and the seller has cost c.

Constraints:

•

, for all , guaranteeing that the mechanism is BIC and interim IR.

•

, guaranteeing the allocation is implementable.

Objective:

•

, the expected seller’s profit.

We then take the partial Lagrangian dual of the LP in Figure 2 by lagrangifying the BIC and interim IR constraints. Let be the Lagrangian multiplier. The dual problem is described in Figure 3.

Variables:

•

and .

•

for all , the Lagrangian multiplier for buyer ’s BIC and interim IR constraints.

Constraints:

•

for all .

•

.

Objective:

•

.

| (1) | ||||

Definition 9.

A feasible dual solution is useful if .

Similar to [7], we show that every useful dual solution forms a flow.

Lemma 27.

A dual solution is useful if and only if it forms the following flow:

-

•

Nodes: For every and a node . A source and a sink .

-

•

For every and , a flow of weight from to .

-

•

For every and , a flow of weight from to .

Proof.

Suppose there exists such that

Without loss of generality, suppose it’s positive. Notice that is unconstrained. Thus when , the Lagrangian also goes to (see Equation 1). Hence for every ,

It’s essentially the flow conservation equation for node . Thus forms a flow. On the other hand, if forms a flow, the Lagrangian only depends on and thus bounded since is bounded. ∎

For any useful dual solution , by Lemma 27, we can replace by in Equation (1) and simplify . For any BIC and interim IR mechanism , both and are non-negative for all . Thus by Equation (1), . We have the following lemma.

Lemma 28.

(Restatement of Lemma 2) For any useful dual solution and any BIC, interim IR mechanism ,

where

can be viewed as buyer ’s virtual value function.

Appendix B Missing Proofs from Section 4

Proof of Lemma 1: Consider a mechanism that is ex-post implementable. For every , let be buyer ’s (possibly randomized) equilibrium strategy, when her type is . It specifies all the actions that the buyer takes in mechanism . For every c, let be the vector of (possibly randomized) indicator variables that indicate whether buyer gets each item when buyers choose strategies and the seller’s realized cost vector is c; let be the payment for the buyer. For every and , denote .

Since is an equilibrium strategy for the buyers, for every , acting as induces more utility than , when the buyer’s type is and other buyers follow strategy . We have

| (2) | ||||

We now define the direct mechanism as follows: for every profile , let and for all . It’s the allocation and payment rule when the reported type profile is t and the seller’s realized cost vector is c. Then Inequality (2) is equivalent to: for every

It’s exactly the BIC constraint for . Thus, is BIC.

Moreover, each buyer can choose not to participate in , so , which implies that . Hence, is also interim IR.

Proof of Theorem 4: Let be the virtual value function induced by the above canonical flow . By Lemma 2 and Lemma 3,

The first inequality is due to Lemma 2, and the first equality is due to Lemma 3. The second inequality is because: For the second term, notice that , we bound the indicator by 1 and use the fact that for every c; For the third term, notice that for every and c, since is feasible, we have

Taking expectation over c, the RHS equals to . Thus the inequality holds.