Estimation of Markovian-regime-switching models with independent regimes

Abstract

Markovian-regime-switching (MRS) models are commonly used for modelling economic time series, including electricity prices where independent regime models are used, since they can more accurately and succinctly capture electricity price dynamics than dependent regime MRS models can. We can think of these independent regime MRS models for electricity prices as a collection of independent AR(1) processes, of which only one process is observed at each time; which is observed is determined by a (hidden) Markov chain. Here we develop novel, computationally feasible methods for MRS models with independent regimes including forward, backward and EM algorithms. The key idea is to augment the hidden process with a counter which records the time since the hidden Markov chain last visited each state that corresponding to an AR(1) process.

Keywords: Electricity price model, forward-backward algorithm, hidden Markov model, Markov-switching time series

1 Introduction

A commonly used model for economic time series is the Markovian-regime-switching (MRS) model whereby multiple stochastic processes are interweaved by a Markov chain. The general idea is that there exist multiple regimes underlying the observation process, and depending on which regime the system is in, different characteristics are displayed. For example, for stock prices we could suppose that there is a bull regime where prices trend upward and are comparatively non-volatile, and a bear regime where prices trend downward and are relatively volatile. Our motivating application is electricity prices where it is common to model prices with an MRS model. Due to the fact that electricity cannot currently be stored efficiently, electricity prices show characteristics not seen in typical commodity markets, for example mean reversion, prices spikes, drops and negative prices. MRS models are able to capture these behaviours, and have been popular tools for modelling randomness in electricity markets. Typically MRS models with two or three regimes are used [9, 8, 13, 14]: a base regime where prices are relatively non-volatile, a spike regime where prices are volatile and high, and sometimes a drop regime is included, where prices are volatile and low. More broadly, models with Markovian switching find application in biology [1], weather modelling [23, 27], speech recognition [21] and more.

The earliest applications of MRS models for electricity prices are [9] and [8]. Their models specify that prices decay back to base levels following a spike according to an autoregressive process of order 1 (AR(1)). However, this is not consistent with observations from the market where a more immediate return to base levels is observed [16, 2]. For this reason, [14] introduce a three-regime MRS model which separates the behaviour of base and spike prices. They use one regime to capture base prices, one regime to capture spikes, and one regime to return prices to base levels following a spike. Motivated by the need to capture the distinct and abrupt price spikes in electricity markets, it has become popular to specify MRS models with independent regimes, which are able to capture this behaviour without the addition of the extra regime required by [14]. We may think of a dependent regime MRS models as a single process, where the dynamics of the process is governed by the hidden Markov chain, whereas we may think of an independent regime MRS model as a collection of independent AR(1) processes, and at each time , the hidden Markov chain chooses which process is observed.

We say a model has independent regimes if, given the hidden regime sequence, the observations generated from each regime are independent of observations generated from any other regime; and we say a model has dependent regimes otherwise. Independent regime MRS models were introduced in [13] and have since been popular [25, 17, 24]. In these models, typically at least one regime is specified as an AR(1) process. AR(1) processes have a dependence structure between values at successive times which, coupled with the independent regimes assumption in an MRS model, complicates the dependence structure between an observation at time and all prior observations – the dependence between prices is governed by the hidden regime process and is therefore random. It is for this reason that the forward, backward and expectation-maximisation (EM) algorithms for traditional (dependent regime) MRS models or hidden Markov models do not apply. For each time , the forward algorithm evaluates the probabilities that the hidden process is in each regime given the observed values up to time . The backward algorithm then uses the output of the forward algorithm to calculate the probabilities that the hidden process is in each regime given all observations. The EM algorithm is an iterative optimisation algorithm, iterating between an E-step and an M-step, used to find the maximum likelihood estimates of parameters for models with missing data or latent variables – the E-step is computed by the backward algorithm.

For simplicity, in this work, we focus on independent regime MRS models with AR(1) and i.i.d. regimes only, since these are the type of models used in the electricity price modelling literature. However, we believe the methods developed here are more general and apply to Markov-switching processes with regimes that are discrete-time Markov chains generally, and can also be extended to more general autoregressive processes. The most popular method of inference for the models used for electricity pricing is an approximation to the EM algorithm introduced by [17], which we show can be unreliable (see [22] also). Here, a novel, computationally feasible, and exact likelihood-based framework to solve this problem is developed. This work is related to the forward, backward, and EM algorithms for traditional MRS models, and, more closely, to the same algorithms for hidden semi-Markov models, where the idea of augmenting the hidden process with a counter is also used [26]. The novel algorithms have complexity where is the total number of regimes in the model, is the length of the observed data set, and is the number of AR(1) regimes in the model. As may be impractically large depending on the values of and , we also present an approximation to our algorithm that is where is the maximum length of the memory of the AR(1) processes, that is, we specify that the observations may depend only on for , and is independent of any for .

This paper is structured as follows. We formally introduce the MRS model, in particular the independent-regime type in Section 1.1, and discuss the approximate parameter inference algorithm of [17] in Section 1.2. A novel forward algorithm, which is used to evaluate the likelihood and filtered state probabilities for these models, is presented in Section 2. Using the outputs of the forward algorithm we develop a novel backward algorithm in Section 3. The backward algorithm is used to evaluate the smoothed state probabilities, which are applied in Section 4 to construct an EM algorithm. We introduce the truncated approximations of our algorithms at the end of Section 4. Section 5 provides simulation evidence that our EM algorithm is consistent and that the truncation approximations are reasonable, while in Section 6 we apply our algorithms to estimate MRS models for the South Australian wholesale electricity market. Finally, we make concluding remarks in Section 7.

1.1 MRS models: A brief introduction

An MRS model is built from two pieces, an unobservable regime sequence, , which is a finite-state Markov Chain, and an observation sequence, . Let us denote the state space of the hidden regime sequence as , and the transition matrix as .

The simplest MRS model is the hidden Markov model (HMM) where observations take values in a discrete set, and is independent of and given the regime at time , . In general, MRS models are specified in terms of distributions that allow dependence on past observations, given the current regime. That is, the model defines distributions,

for some distribution . The MRS model, as introduced by [10, 11], specifies that follows some time-series model (an autoregressive process of order , for example) with dependence on a finite number of past observations, but not on . That is, the dependence structure does not take into account which regime the past observations belong to. For example, the following is a dependent regime MRS model.

Example 1 (An MRS model with dependent regimes).

Let , and , and specify

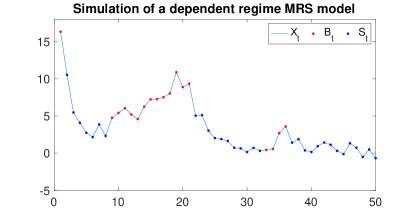

for i.i.d. N(0,1) for . So follows AR(1) dynamics in both Regimes 1 and 2. This is a dependent-regime MRS model since depends on regardless of which regime the lagged observation, , came from. Figure 1 (Left) shows a simulation of this model.

In this paper we relax the assumption that the current observation is conditionally independent of , in order to increase flexibility in these models. In particular, we consider models where, given , depends only on lagged values from Regime , thus the dependence structure is random as it is a function of . The following is an example of an independent regime MRS model.

Example 2 (An MRS model with independent regimes).

Let , and , and define the following AR(1) processes

where and are sequences of i.i.d. N(0,1) random variables. Then, construct the MRS model as follows

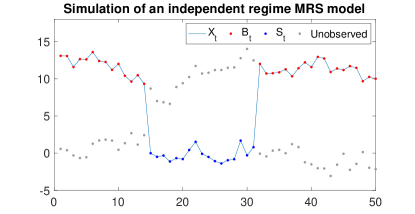

Figure 1 (Right) shows a simulation of this model.

A precise definition of dependent and independent regime models is the following. Define the sets , . We say that a model has independent regimes if, given the regime sequence, the sets , , are independent. Otherwise, it is a dependent regime model.

1.2 Existing methods

For the simplest form of MRS model, the HMM, likelihood evaluation and maximisation algorithms were first developed in a series of papers, [5], [4], and [6], and subsequent work on MRS models is typically closely related to this. The first algorithms for the more general dependent regime MRS model were presented by [10, 11]. The main issue for maximum likelihood estimation of models with hidden regimes is that the regime sequence is unobserved, thus to naively evaluate the likelihood requires calculation of the marginal distribution

| (1) |

where denotes the distribution function of a random vector with parameters , is a sequence of observed values, and is the space of all possible regime sequences of length , . The number of sequences in is which, for most realistic datasets, is computationally infeasible to evaluate in this form. In the context of HMMs, the sum (1) is made computationally feasible by the forward algorithm [6], and the maximisation of the likelihood is commonly performed via the Baum-Welch algorithm [6], which is a specific case of the EM algorithm [7] and uses the backward algorithm [6].

The works of [10, 11] extend the methods for HMMs to MRS models with dependent regimes by adapting the forward algorithm, developing a new algorithm to replace the backward algorithm and constructing an EM algorithm. [20] refines the work of Hamilton, developing a more efficient implementation of Hamilton’s smoothing algorithm. Kim’s algorithm is similar to the backward algorithm for HMMs.

Relevant to this paper, [17] extend Hamilton’s work and develop an approximate algorithm for MRS models with independent regimes, which we label the EM-like algorithm since it resembles Hamilton’s EM algorithm. However, it is not an example of the EM algorithm and so none of the EM theory holds. In Sections 1.2.1–1.2.3, we briefly review the work of [11], [20] and [17] in order to provide the motivation and background for our work.

1.2.1 Likelihood evaluation for dependent-regime models: The forward algorithm

Define for and write the likelihood as The forward algorithm [11] calculates and for from which it is straightforward to calculate the likelihood or loglikelihood:

Algorithm 1: The forward algorithm [11]

-

Step 1.

Initialise the algorithm with values , which may be assumed to be known a priori, or left as parameters to be inferred.

-

Step 2.

The term, , is calculated as where the density is known from the model specification.

-

Step 3.

For :

where is also known from the model specification. Furthermore, the probabilities can be calculated using Bayes’ Theorem,

(2) for . These are known as the forward/filtered probabilities.

The quantities are known as the prediction probabilities. In some applications, the forward and prediction probabilities may be quantities of interest in their own right, and they also appear as inputs to the backward algorithm (see Section 1.2.2).

1.2.2 Maximum likelihood for dependent-regime models: The EM algorithm

Hamilton’s forward algorithm [11] is a computationally feasible way to evaluate the loglikelihood, from which it is possible to use black-box optimisation methods to find the MLEs. However, it is common to use the EM algorithm [7] instead, particularly when the E-step and M-step of the algorithm are available in closed form. The EM algorithm proceeds by iterating between the E-step, constructing the function , and the M-step, maximising with respect to , where is the parameter space. This results in a sequence that converges to a local maximiser of the loglikelihood.

The EM algorithm for MRS models with dependent regimes proceeds as follows [11]. Define the random variable as the number of transitions from state to state in the sequence and let be the indicator function. The joint log-density of and can be written as

where denotes . In the th iteration, , for the E-step, taking the conditional expectation given parameters and observed values yields

where the expectation . The densities and , are given by the model specification.

The smoothed probabilities, and , required to construct are obtained using a backward recursion after running the forward algorithm with parameters , and storing the forward and prediction probabilities. Developed by [20], this backward recursion is in Algorithm 2, below.

Algorithm 2: The backward algorithm [20]

-

Step 1.

Evaluate using the forward algorithm (Algorithm 1).

-

Step 2.

For

where means the parameter under .

After executing Kim’s backward algorithm, we can construct the function . In the M-step, the maximisers of are found. In the dependent regime model, if the process is in Regime at time , then the observations evolve according to where and are parameters, and . Recall that, for the dependent regime model, is the last observed value (regardless of which regime generated it). The maximiser of at the th iteration of the EM algorithm, , for , is the following system of equations [11, 17]:

| where | |||

In general, the switching probabilities are updated using the following [20]

| (3) |

which rely on the smoothed, forward and prediction probabilities. For i.i.d. regimes the M-step can often be derived analytically; however, such expressions are not required for our discussion since there is no dependence on lagged values in these regimes and so they are omitted.

Thus, we implement the EM algorithm by initialising it with a guess of the true parameters, then alternating between the forward and backward algorithms (the E-step) and calculating the maximisers of (the M-step). The algorithm terminates when the step size is below a prespecified tolerance, i.e. where is some small tolerance.

1.2.3 Approximate maximum likelihood for independent-regime models: The EM-like algorithm

For independent-regime MRS models the EM algorithm is computationally infeasible if the densities , , , are computed naively, as this is a calculation for each , where is the number of regimes in the model. On the other hand, if we use our proposed foward algorithm, introduced in Section 2), calculation of these densities is for each , which may be computationally feasible when and are not too large.

Developed by [17], the EM-like algorithm is an approximation to the EM algorithm. For independent regime MRS models, the EM-like algorithm overcomes the problem of computational infeasibility by replacing lagged values for Regime (assuming this is an AR(1) regime) with approximations, . These are described as the expectations [17], where

Simply put, wherever appears verbatim in an expression related to Regime in the EM algorithm in Sections 1.2.1-1.2.2, it is replaced with at the iteration. The are calculated recursively as

| (4) |

where and are given by the forward algorithm which is part of the EM-like procedure. Janczura and Weron, [17], conduct simulation studies and show that this algorithm seems to work well for the datasets they generate. However, no theoretical results are available that show convergence of, or error bounds for, the EM-like algorithm; in particular, there is no guarantee that the parameter estimates produced by the EM-like algorithm are consistent. In contrasts, our algorithms rest on the theory of the EM algorithm.

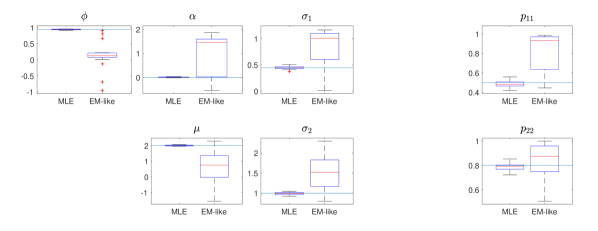

We can construct examples of independent-regime MRS models where the EM-like algorithm fails to get close to the true parameter values.

Example 3.

Consider the following independent-regime MRS model,

| (5) |

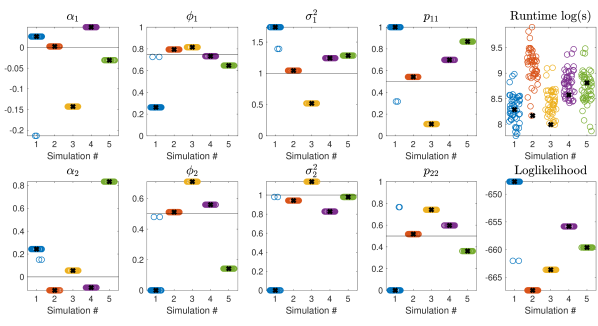

where is an AR(1) process, with being a sequence of i.i.d. N random variables, is an i.i.d. sequence of N random variables, and is a Markov chain with state space , transition matrix entries and , and initial probability distribution , so the process always starts in Regime 1. We simulated 20 realisations of length from this model and used the EM-like algorithm to try to recover the true parameters. To give the algorithm the best chance of converging to the true parameters, we initialise the EM-like algorithm at the true parameter values. The parameters recovered by the EM-like algorithm are summarised in Figure 2.

2 A novel forward algorithm

The general idea of the novel algorithms presented in this paper is to augment the hidden Markov chain with counters that record the last time each AR(1) regime was visited. This augmented process is a Markov chain, and similar arguments to those used to construct the forward-backward algorithm for MRS models with dependent regimes can be used to construct a forward and backward algorithms for these models. Our methods are related to the forward and backward algorithms for hidden semi-Markov models, where the hidden process is also augmented with a counter and the augmented hidden process is a Markov chain [26]. Though similar, the algorithms for hidden semi-Markov models (HSMMs) are not applicable to the models considered here since for HSMMs the counter counts the number of time steps since the last change of regime, whereas here the counters count the number of transitions since the last visit to a regime. Furthermore, in HSMMs, the counters do not appear in the conditional densities of the observations, as they do here.

2.1 The augmented hidden Markov chain

For the following, suppose that the first states, , correspond to AR(1) processes and all other regimes are i.i.d. That is, we have the following independent regime MRS model

where are AR(1) and are i.i.d. Our arguments also hold for with only slight modification, but here we treat the case only, since these are the types of models relevant to our application.

Now, define another Markov chain

where counts the number of time steps since the process was last in Regime before time , for each AR(1) regime . When there is no time with , then we set . Thus the augmented Markov chain lives on the state space

To describe the transitions of the Markov chain , let be an arbitrary vector of counters, with for or, at time , (it is possible that neither state nor state have been visited by time ). Also, define to be a row vector of ones of length , to be a row vector of length with all entries being 0 except the entry which is 1, and

The transition probabilities of are

| (6) |

In words, when the current state is and is not an AR(1) regime (so there is no counter associated with state ), then, at time , transitions to state with probability and all the counters are advanced by to , since there has been one more time step since was last in any state with a counter (any state in ). When the current state is , where is an AR(1) regime, then transitions to any state with probability , the counter for Regime , , is set to 1, since the last time in state was , and all other counters are advanced by . All other transition probabilities for are 0.

The state space of is countably infinite. However, due to the way is initialised and evolves, many states are inaccessible for , , and this makes our algorithm computationally feasible. Specifically, we suppose that the Markov chain is initialised with the probability distribution

| (7) |

The distribution can be any proper probability distribution. However, in line with existing algorithms for dependent regime MRS models, it can be either the stationary distribution of , or a point mass on a single state, or, when used as part of the EM algorithm, the probabilities calculated at the previous iteration of the EM algorithm. The following lemma gives all the states that can be in at time .

Lemma 4.

Define as a vector of ’s of length where is the number of AR(1) regimes. For each , let be the set of all vectors such that, for ,

-

(i)

,

-

(ii)

there are at most elements of with ,

-

(iii)

for all , unless .

Given is initialised with the distribution in Equation (7), it is possible for to reach states where and only. The cardinality of is

Proof.

First, we explain why contains all possible values of the counters of for .

At time the chain, , is initialised with the distribution in Equation (7), so

At time , either has never visited state , in which case , or last visited at time , in which case ; this is part (i). Since the process can only be in one regime at a time, it follows that for (unless ), which is part (iii) of the definition. Also, at time , the regime chain could only possibly have visited possible states; this is part (ii) of the definition.

Now, to prove the cardinality of . The elements of are of the form . At time , let be the possible number of counters that are not equal to , so is an element of . For each, there are ways of choosing which of the counters are not equal to . Next, each counter takes a distinct value in , so there are ways of choosing the value of the counters. There are possible permutations to allocate the chosen values to the counters. So, in total there are elements in . ∎

Lemma 4 says that if then for any . Therefore the elements of the set partition the space of all counters that the process has positive probability of reaching. Thus, for any (measurable) set and any , the law of total probability can be applied as We will use this fact multiple times to construct the forward algorithm.

2.2 Constructing the forward algorithm

The forward algorithm is multi-purpose. It can be used to evaluate the likelihood, and also to evaluate the filtered and prediction probabilities, which in turn are inputs to the backward algorithm. For clarity of exposition, we first present a simple, but impractical due to underflow, algorithm (Lemma 5) to calculate the likelihood for independent regime MRS models, then address the underflow issue later with a normalised version of the algorithm (Lemma 7). Define

for , , and .

Lemma 5 (A simple forward algorithm).

First, for calculate

| (8) |

Then for , , , calculate

| (9) |

Then the likelihood is given by

| (10) |

Proof.

First, from the law of total probability, we have

| (11) |

Now, if any for , then it must be that and for some . Thus, in this case, the double sum in Equation (11) simplifies to Otherwise, all elements of are greater than 1, in which case and , so the double sum in Equation (11) simplifies to

For both cases the following arguments are the same, so for notational convenience we will use to be either when for all , or when for some .

Lemma 6.

The complexity of the simple forward algorithm, as given by the total number of multiplications, is less than .

Proof.

For , calculating by (8) for all requires multiplications in total. For each , first consider the case where for all . Fix . Noting that

then there are multiplications to calculate all the necessary terms since , and . The sum then collapses this to terms, each of which is then multiplied by which requires multiplications.

Now consider the case where for some . Fix and . Compute the sums for each where and store them. After computing the sums, there are stored terms. Keep fixed, but allow to vary. Each of the stored sums is multiplied by and for and which gives a total of multiplications. Thus, the total number of multiplications required is

by the result . This can then be bounded by

From which we see the complexity is bounded by . ∎

To overcome possible underflow issues, we consider a normalised version of the algorithm. Define

Lemma 7 (A normalised algorithm).

Set from the simple algorithm. Then, for calculate

Then the loglikelihood is given by

| (12) |

Proof.

The definition of conditional densities gives

where

| (13) |

Using the same arguments as in the proof of Lemma 5, the right-hand side of (13) simplifies to

| (14) |

| (15) |

The summands in (14) and (15) can be written in the form

which proves the result for the iterations. Equation (12) holds from the law of total probability. ∎

Lemma 8.

The complexity of the normalised forward algorithms, as given by the total number of multiplications, is less than .

Proof.

The normalised algorithm is the same as the forward algorithm except that each term is divided by . The most efficient way to do this extra step is to do the division for first, which results in an additional multiplications in total. ∎

3 A novel backward algorithm

The goal of the backward algorithm is to calculate the smoothed probabilities

for , and . The smoothed probabilities are often of interest in their own right, but are also typically used to construct an EM algorithm. Recall that as a byproduct of the forward algorithm we obtain the filtered probabilities

as well as the prediction probabilities

for , , and all . These are the inputs to the backward algorithm.

Lemma 9 (A backward algorithm).

The smoothed probabilities can be calculated using the following procedure. Set Then, for and for calculate

Proof.

Consider the event . By the definition of , when , then , and when , then . Thus, when is known, then is also known. As a result,

| (16) |

for , and . Since the following arguments are the same for both cases, and , for notational convenience, let take the value when and the value when . The summands on the right hand side of (16) can be written as

| (17) |

where the last equality holds since is independent of given . Now, noting that is independent of given and , then the right-hand side of (17) equals

Writing out explicitly for the two cases completes the proof. ∎

Lemma 10.

The total complexity of the backward algorithm in Lemma 9, as measured by the total number of multiplications, is less than

Proof.

First, for each we need to calculate the ratio

for every corresponding and . This costs multiplications. This quantity is independent of , thus only needs to be done once for a given if we save the results.

Now consider , and fixed. The multiplication of and

is done for every which costs multiplications. The sum over results in a single term, which is then multiplied by the corresponding , and this costs an additional 1 multiplication. We do this for all and , which costs multiplications.

So, for a given we execute multiplications. This is done for every , so the total number of multiplications is

where we have used similar arguments to Lemma 6 to bound the complexity. ∎

Of importance to the next section, note that we can obtain from the backward algorithm, the smoothed probabilities

4 A novel EM algorithm

Here we show how the output from the backward algorithm can be used to implement an exact, computationally feasible EM algorithm for MRS models with independent regimes.

4.1 The E-step

Recall that the EM algorithm [7] is an iterative procedure, alternating between an expectation step and a maximisation step. In the expectation step the function is constructed as

| (18) |

where is a sequence of the hidden Markov chain , and is a sequence of the corresponding augmented hidden process . The information contained in the sequences and is entirely equivalent, but we opt for the latter representation to remain consistent with, and emphasise the place of, the work in the previous sections. In the M-step of the algorithm, the maximisers are found.

For MRS models can be written as

| (19) |

Using the augmented hidden Markov chain, , (19) can be written in such a way that the function is computationally feasible. First note that, given and , is independent of for which allows the function to be written as

| (20) | |||

| (21) |

Since , and similarly for , the expression (21) simplifies to

| (22) | |||

| (23) |

Taking the expectation of (23) with respect to the distribution (equivalently the distribution ) gives

Using similar arguments, is found to be

where is the random variable counting the number of transitions from state to state in the sequence . The expectation can be calculated as

So, the function is

| (24) |

Lemma 11.

The joint probabilities are given by

| (25) |

This proof follows similar arguments to those in [20], which develops algorithms for MRS models with dependent regimes.

Proof.

For the case , note that if and only if and we are done.

When all counters in are different from 1, so . Thus

| (26) |

The last equality holds since, given and , then is independent of . Focusing on the right-most term in Equation (26),

where is the parameter in ; the second equality holds since, given , then is independent of and .

Now, notice that

since , and that

with the sum in the denominator being over since only when is defined; this completes the proof. ∎

4.2 The M-step

Next, the maximisers, , are needed. The maximisers for the parameters of each regime are generally problem specific, but the maximisers for the parameters , , can be derived in general. By the work of [11],

However, note that to get this analytic update for the parameters, terms involving in Equation (24) have been treated as if they are unrelated to , . However, this is not true when is specified as the stationary distribution of the process , but holds for other cases, such as when is some predetermined distribution, or when is specified as a parameter to be inferred. Nonetheless, this simplification is appropriate if we assume that, as the sample size grows, the contribution of terms involving become insignificant.

4.3 Model-specific M-step updates

In electricity price models, it is common to specify spike or drop regimes as either shifted-Gamma, shifted-log-normal, or occasionally a Gaussian distribution. Here we derive M-step updates for these regimes.

Corollary 12.

Suppose Regime is i.i.d. . The M-step updates and , for , are

Proof.

The results holds after differentiating the and solving for zeros. That is a maximiser is shown by the second derivative test. Furthermore, can be shown to be a maximiser by comparing the value of when to the value of evaluated at any other value of , and utilising the inequality . ∎

At time , if is a shifted-Gamma regime so that , where is known, the M-step is not completely analytic. However, the dimension of the maximisation problem can be reduced from 2-dimensional to 1-dimensional via the following corollary.

Corollary 13.

Suppose Regime follows an i.i.d. shifted-Gamma distribution, that is, if is from Regime , then , and suppose the parameter is known. The M-step update for the scale parameter, , as a function of , is

The update for is then found by finding

where is the Gamma function.

Proof.

The result follows after differentiating with respect to , and solving for the stationary point, which is a maximum by the second derivative test. ∎

Corollary 14.

Suppose Regime follows i.i.d. shifted-log-normal dynamics, that is, if is from Regime , then , and suppose the parameter is known. The M-step updates are

Proof.

The proof is similar to the proof of Corollary 12. ∎

Note that Corollaries 13 and 14 assume the parameter is known. This is necessary for the shifted-log-normal distribution [12] and the shifted-Gamma distribution when the shape parameter is less than 1 [19]. Furthermore, for the shifted-Gamma distribution, [19] observe that related issues arise when is near 1, and advise against maximum likelihood estimation of when . Simulations suggest this is also good advice when fitting MRS models with shifted-Gamma regimes [22].

In electricity price modelling literature it is common to specify a ‘base regime’ as an AR(1) process. In existing literature the AR(1) regimes are assumed to evolve at every time but are only observed when in that regime. Another possibility is that the AR(1) processes evolve only when they are observed, that is, define , and the AR(1) process in Regime as . Our algorithms are applicable to both specifications; however, for simplicity, here we treat the former only. For more details on the latter specification, see [22].

Corollary 15.

If Regime is an AR(1) regime of an MRS model, the M-step of the EM algorithm can be executed as follows. The updates and as functions of are

| where | |||

The M-step update for is given by

where

Proof.

Differentiate with respect to and and solve for when the derivative is zero. The parameter can be shown to be a maximiser by the second derivative test, and can be seen to be a maximiser using the same argument as used in the proof of Corollary 12. Next, substitute the maximisers, and , into (24) and collect all terms involving , to give the function . That we need to search for the global maximiser of on the interval only comes from the fact that we have assumed Regime is a stationary or mean-reverting process, in which case is a necessary condition. ∎

Remark 4.1: Truncation

The forward and backward algorithms can be computationally costly when and/or are large, so it may be preferential (or necessary) to truncate the problem. We suggest that the memory of each of the AR(1) processes be truncated. That is, for all such that for some , we let where is a density that does not depend on . An appropriate choice of will be problem-specific. This truncation is equivalent to truncating the state space of so that , and adjusting the transitions of so that the counters remain at , rather than continuing to increase as they would in the original process. It can be shown that the complexities of the truncated algorithms are . For processes that decay to stationary between times at which they are observed (such as the AR(1) processes in independent-regime MRS models used in this paper, see Section 4.3), then taking as the stationary distribution in Regime is a logical choice. Furthermore, should be chosen large enough so that there is a low probability that ever visits any specific state for more than consecutive transitions and of course .

5 Simulation studies

We perform a simulation study to examine the properties of the algorithms. The models used in the simulations are the following:

| (Model 1) |

where is an AR(1) process defined by , i.i.d. , i.i.d N and is a Markov chain with state space , transition matrix entries , and initial distribution ;

| (Model 2) |

where are independent AR(1) process defined by and , i.i.d. , and is a Markov chain with state space , transition matrix entries , and initial distribution .

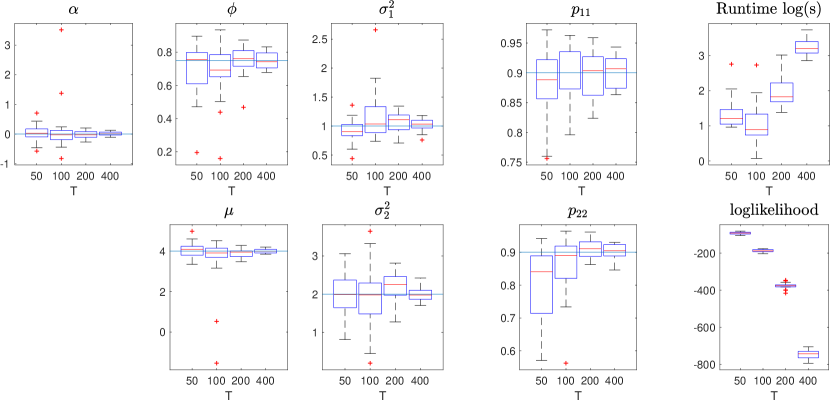

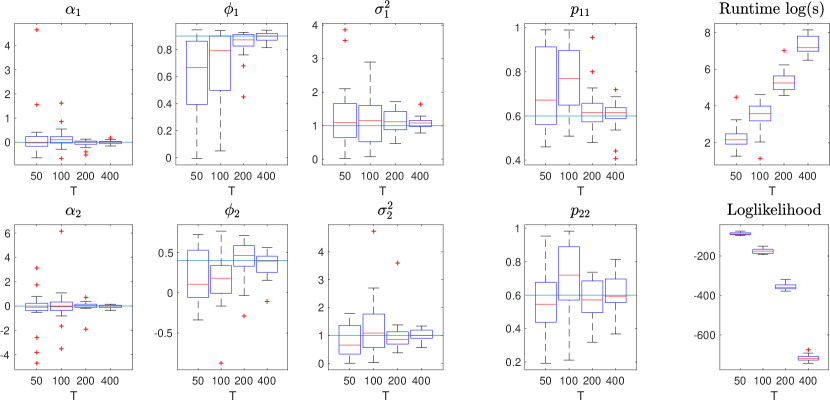

To investigate the bias and consistency of the MLE, 20 independent realisations of Models 1 and 2 were simulated for and , and the EM algorithm used to find the MLE. The terminating criteria for the algorithms was to stop when either the increase in the likelihood, or the step-size, as measure by was less that . To attempt to avoid local maxima, the EM algorithm was initialised from 100 randomised values centred around the true parameters. Of the corresponding 100 terminating points of the EM algorithm, the parameters that achieved the highest loglikelihood value were kept. Figure 3 shows box plots of the 20 terminating points of the EM algorithm, one for each simulation, as well as the log-runtime and value of the loglikelihood. For both models the MLE appears to be converging to the true parameter value as sample sizes increase. Generally, there appears to be a much larger variation in the MLEs for Model 2 than for Model 1. This could be because the inference problem for Model 2 is harder, as the regimes in Model 2 are more similar than they are in Model 1, or because of the nature of the hidden Markov chain is such that there is a lower probability of remaining in each regime ( for Model 2, compared to for Model 1), or both. Regarding the run time, for data sets of length 100 and greater, the empirical results suggest the complexity is approximately for Model 1 and for Model 2, which agrees with, and is significantly better than, our theoretical upper bound.

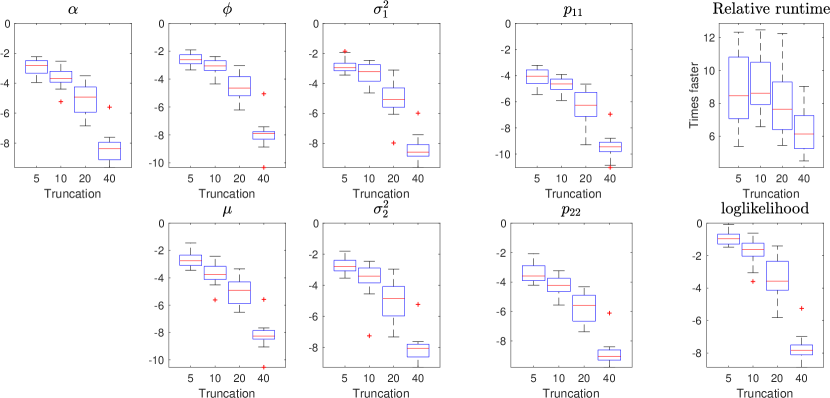

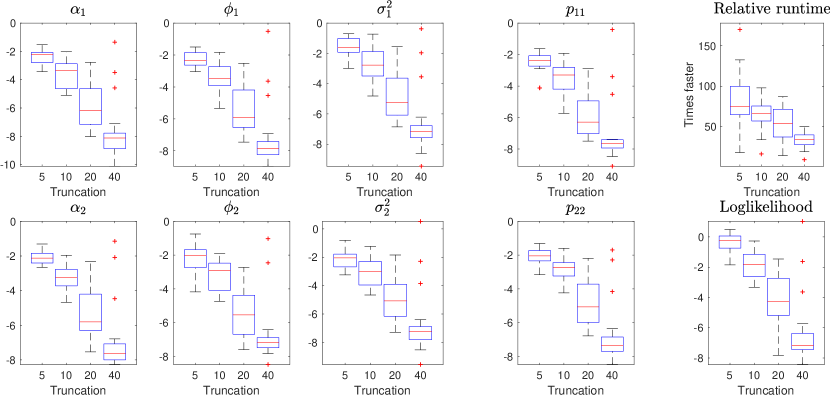

To investigate the truncation method, we used the same data sets simulated above for and applied our truncated algorithm to this data with various truncation levels, . The termination criteria for the EM algorithm was to stop when either the increase in the likelihood, or the step-size, as measure by was less that . Figure 4 plots the of the absolute value of the difference between the parameters recovered by the truncated algorithm and the full algorithm. Figure 4 also shows of the absolute value of the difference in the loglikelihoods achieved by the truncated algorithm and the full algorithm. Figure 4 also plots of the relative runtime of the truncated algorithm compared to the full algorithm, that is, the ratio of the time taken for the truncated algorithm compared to the full algorithm. The run times for the truncated algorithms are significantly lower than the full algorithm. For these data sets the truncated algorithm performs reasonably well, even when limiting the memory of the counters to just 5 time steps. For a truncation level of 40, the errors are of the order to for both models, which is similar to the stopping criteria for the EM algorithm which is of the order . For Model 1 the truncation appears to have a more significant negative effect on the parameter estimates compared to Model 2. This could be because the probability of staying in each regime is higher in Model 1 than in Model 2, and therefore the probability of remaining in one regime for more that consecutive transitions is lower in Model 2. It is likely that the error due to truncation of the algorithm is insignificant compared to statistical error of parameter estimates.

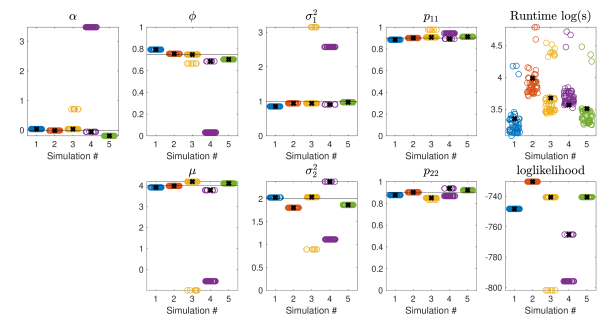

To investigate the convergence properties of the EM algorithm we used five of the simulated data from above with and used the truncated EM algorithm, with a truncation level of to search for maxima. For each of the five simulated datasets we ran the EM algorithm 50 times, sampling initial values for the algorithm independently each time and used the same terminating criteria as before. The sampling distributions for the initial parameter values of the algorithm are summarised in Table 1. For Model 2 we have ordered the terminating values of the EM algorithm such that for identifiability.

Observing Figure 5 we see that, for most of the simulations and most of the starting values, the EM algorithm finds a single maxima. In Figure 5 the black cross represents the point which achieved the highest maximum. We refer to this point as the optimal parameter value. The proportion of times that the algorithm converged to the optimal parameter value is reported in Table 2. Simulation 4 of Model 1 is outstanding since only 14% of initial values resulted in the algorithm finding the optimal value. In Figure 5 there are some instances when the algorithm terminates at a suboptimal point; in particular simulated datasets 3 and 4 for Model 1. As shown in. Figure 5, for Model 1 the optimal parameter set appears to reasonably estimate the true parameters for all simulated dataset.

Estimating Model 2 is much harder since the regimes are both very similar. Figure 5 shows that the optimal parameter set estimates the true parameters reasonably for simulated datasets 2-5, but not for simulated dataset 1. The behaviour of the algorithm for simulated dataset 1 for Model 2 is particularly interesting. For this dataset, the algorithm terminates at one of two distinct locations. One of these terminating points is at and hence Regime 1 is absorbing. This means the algorithm has converged to a point where all but the first observation are captured by Regime 1. As tends to the algorithm is able to send to achieve arbitrarily large values of the likelihood and the model is unidentifiable. To prevent this behaviour, we suggest that the parameters and are restricted so that they are away from the boundary. Indeed, for simulated dataset 1 of Model 2, if we take the terminating values of the algorithm which lie away from the boundary, then we get reasonable estimates of the true parameters. For more discussion see [22].

| Parameter | ||||||

|---|---|---|---|---|---|---|

| Distribution |

| Simulation | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|

| Model 1 | 1 | 1 | 0.86 | 0.14 | 1 |

| Model 2 | 0.96 | 1 | 1 | 1 | 1 |

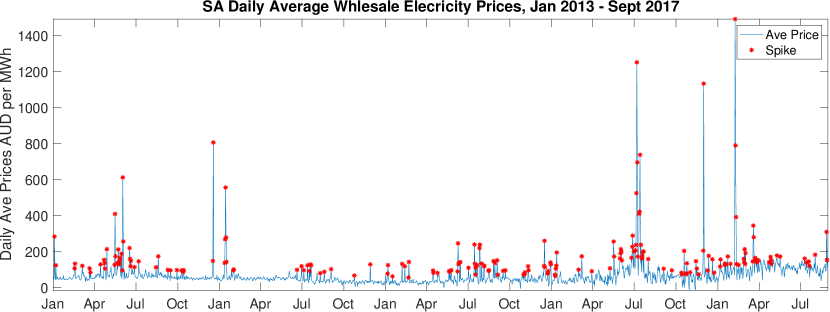

6 An application to South Australian wholesale electricity market

The dataset consists of 81,792 half-hourly spot prices from the South Australian electricity market (available at the AEMO website [3]) for the period 00:00 hours, of January 2013, to 23:30 hours, of September 2017. Note that this dataset contains a period of 14 days over which the market was suspended from 4:00pm, on the of September until 10:30pm on the of October. During this period prices were set by AEMO. We ignore this fact in our modelling and include them in the data set anyway.

Following a common practice in the literature we model daily average prices and thus we have a dataset of 1,704 daily average price observations to which we fit our model. The data that we model is plotted in Figure 6. To model the South Australian wholesale electricity market, we break the price process up in to two components, , where is the price on day , is a deterministic trend component, and is a stochastic component which is to be modelled by an independent regime MRS model.

Electricity spot prices exhibit seasonality on daily, weekly, and longer scales. To capture this multi-scale seasonality, the trend component consists of two parts: a short-term component, , and a long-term component, , so . We model the long-term component, , using wavelet filtering since it has been shown to perform well for this application [18], and use Daubechies 24 wavelets and a level 6 approximation [18]. We use the short-term component, , to capture the mean price for different days of the week and indicator functions to model this:

where , …, are the mean deviations from the long-term trend price on Monday, Tuesday, …, Sunday, respectively.

Following [18] we use the RFP (recursive filter on prices) method to estimate the seasonal component in the presence of extreme observations. The method first uses the raw price series to estimate the trend model, then removes this from the data. Next, the standard deviation of these altered prices is estimated, and any prices that are more than three standard deviations from the current estimate of the trend are replaced with the value of the estimated trend at that point. The procedure then re-estimates the trend component on the original data set with spikes removed.

We consider the following four models for the stochastic component:

| (M 1) |

where is an AR(1) process with i.i.d. N, and , where is a shifting parameter, follows either a Gamma distribution (M1-Gamma), or a log-normal distribution with parameters and (M1-LN). The last two models introduce a ‘drop’ regime as well:

| (M 2) |

where and are as above, and , where is a shifting parameter, follows a log-normal distribution with parameters and . The use of the shifting parameters and was proposed by [15]. As previosuly mentioned, estimating the shifting parameters of these distribution is known to be a difficult task [19], so we fix and as the first and third quantiles of the detrended data, as suggested by [17].

The models were fitted to the detrended data using the truncated EM algorithm with truncation level (8 weeks). The Bayesian Information Criterion (BIC) values of these models are reported in Table 3. From the BIC values we choose model M1-LN, with an AR(1) base regime and a log-normal spike regime. The parameters for this model are reported in Table 4. Of course, for a rigorous treatment of this modelling problem, model assumptions should be checked and we should not rely solely on the BIC. Using the smoothed probabilities obtained while fitting model M1-LN, the prices can be classified into which regime is most likely. This is shown in Figure 6, where prices are highlighted in red if , where is the MLE.

| Model | M1-LN | M1-Gamma | M2-LN | M2-Gamma |

|---|---|---|---|---|

| BIC | 15572 | 15681 | 15575 | 15706 |

| -3.257 | 0.6830 | 213.26 | 0.9140 | ||

| 7.106 | 3.751 | 1.268 | 0.3945 |

7 Conclusions

In this paper we have developed novel techniques for independent-regime MRS models. Specifically, we consider models that are a collection of independent AR(1) processes, where only one process is observed at each time , and which regime is observed is determined by a hidden Markov chain. We develop forward, backward and EM algorithms for these models, and show that the methods we develop here can outperform the existing method of inference used in the electricity price modelling literature, the EM-like algorithm [17].

The construction of these methods relies on the idea of augmenting the hidden Markov chain with a set of counters, which keep track of the number of transitions since the last visit to AR(1) regimes. The forward algorithm can be used to evaluate the likelihood and filtered and prediction probabilities, which are used as inputs to the backward algorithm. The backward algorithm is used to evaluate the smoothed probabilities. Together, the forward-backward procedure executes the E-step of the EM algorithm. We showed that the complexity of the forward and backward algorithms is , where is the number of regimes in the model, the length of the observed sequence, and the number of AR(1) regimes in the model. This complexity may be impractically large if or are large, so we introduce an approximation where the memory of AR(1) processes in the model is truncated. These truncated methods are , where is the memory of the counters.

Simulation suggests that the MLE found via the EM algorithm is consistent, and that, even for models with regimes with similar characteristics (such as Model 2), the MLE is still a reasonable estimator when the sample size is large enough (400 observations in this case). Simulations also suggest that the truncation method is a reasonable approximation to the full likelihood, while improving runtime and memory requirements significantly. As is typical for hill-climbing algorithms, there is the possibility of the algorithm terminating at sub-optimal values depending on the initial values of the algorithm. We explored some of this behaviour via a simulation study and found, at most, two local maxima of the likelihood function. Of course, the behaviour of the algorithm is going to be model- and data-specific. This simulation study also highlighted possible identifiability issues which can arise. However, these can be rectified by restricting parameters away from the boundary.

Lastly, we apply our methods to estimate four models for the South Australian wholesale electricity market and find that a 2-regime model with an AR(1) base regime and shifted log-normal spike regime is best as measured by the BIC. We also demonstrate how prices can be classified into regimes using the smoothed probabilities.

References

- Albert [1991] P. Albert. A two-state Markov mixture model for a time series of epileptic seizure counts. Biometrics, 47(4):1371—1381, December 1991. ISSN 0006-341X.

- Alvaro et al. [2002] E. Alvaro, I. P. J., and V. Pablo. Modelling electricity prices: International evidence. Oxford Bulletin of Economics and Statistics, 73(5):622–650, 2002.

- Australian Energy Market Operator [2018] Australian Energy Market Operator. Data dashboard, 2018. Accessed: 2018-02-17.

- Baum and Eagon [1967] L. E. Baum and J. A. Eagon. An inequality with applications to statistical estimation for probabilistic functions of Markov processes and to a model for ecology. Bulletin of the American Mathematical Society, 73(3):360–363, 05 1967.

- Baum and Petrie [1966] L. E. Baum and T. Petrie. Statistical inference for probabilistic functions of finite state Markov chains. The Annals of Mathematical Statistics, 37(6):1554–1563, 12 1966. doi: 10.1214/aoms/1177699147.

- Baum et al. [1970] L. E. Baum, T. Petrie, G. Soules, and N. Weiss. A maximization technique occurring in the statistical analysis of probabilistic functions of Markov chains. The Annals of Mathematical Statistics, 41(1):164–171, 02 1970. doi: 10.1214/aoms/1177697196.

- Dempster et al. [1977] A. P. Dempster, N. M. Laird, and D. B. Rubin. Maximum likelihood from incomplete data via the EM algorithm. Journal of the Royal Statistical Society. Series B (Methodological), 39(1):1–38, 1977. ISSN 00359246.

- Deng [2000] S. Deng. Stochastic models of energy commodity prices and their applications: Mean-reversion with jumps and spikes. Working Paper PWP-073, University of California Energy Institute, 2000.

- Ethier and Mount [1998] R. G. Ethier and T. D. Mount. Estimating the volatility of spot prices in restructured electricity markets and the implications for option values. PSerc Working Paper, Cornell University, 1998.

- Hamilton [1989] J. D. Hamilton. A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica, 57(2):357–384, 1989. ISSN 00129682, 14680262.

- Hamilton [1990] J. D. Hamilton. Analysis of time series subject to changes in regime. Journal of Econometrics, 45(1):39–70, 1990. ISSN 0304-4076.

- Hill [1963] B. M. Hill. The three-parameter lognormal distribution and Bayesian analysis of a point-source epidemic. Journal of the American Statistical Association, 58(301):72–84, 1963.

- Huisman and de Jong [2003] R. Huisman and C. de Jong. Option pricing for power prices with spikes. Energy Power Risk Management, 7(11):12–16, 2003.

- Huisman and Mahieu [2003] R. Huisman and R. Mahieu. Regime jumps in electricity prices. Energy Economics, 25(5):425–434, 2003.

- Janczura and Weron [2009] J. Janczura and R. Weron. Regime-switching models for electricity spot prices: Introducing heteroskedastic base regime dynamics and shifted spike distributions. In 2009 6th International Conference on the European Energy Market, pages 1–6, May 2009.

- Janczura and Weron [2010] J. Janczura and R. Weron. An empirical comparison of alternate regime-switching models for electricity spot prices. Energy Economics, 32(5):1059–1073, 2010. ISSN 0140-9883.

- Janczura and Weron [2012] J. Janczura and R. Weron. Efficient estimation of Markov regime-switching models: An application to electricity spot prices. Advances in Statistical Analysis, 96(3):385–407, 2012.

- Janczura et al. [2013] J. Janczura, S. Trück, R. Weron, and R. C. Wolff. Identifying spikes and seasonal components in electricity spot price data: A guide to robust modeling. Energy Economics, 38:96–110, 2013.

- Johnson et al. [1994] N. L. Johnson, S. Kotz, and N. Balakrishnan. Continuous univariate distributions. New York Wiley, 2nd edition, 1994. ISBN 0471584959.

- Kim [1994] C.-J. Kim. Dynamic linear models with Markov-switching. Journal of Econometrics, 60(1-2):1–22, January-February 1994.

- Levinson et al. [1983] S. E. Levinson, L. R. Rabiner, and M. M. Sondhi. An introduction to the application of the theory of probabilistic functions of a Markov process to automatic speech recognition. The Bell System Technical Journal, 62(4):1035–1074, April 1983.

- Lewis [2018] A. Lewis. Inference of Markovian-regime-switching models with application to South Australian electricity prices. Master’s thesis. The University of Adelaide, 2018.

- Thyer and Kuczera [2000] M. Thyer and G. Kuczera. Modeling long-term persistence in hydroclimatic time series using a hidden state Markov model. Water Resources Research, 36(11):3301–3310, 2000.

- Weron [2014] R. Weron. Electricity price forecasting: A review of the state-of-the-art with a look into the future. International Journal of Forecasting, 30(4):1030–1081, 2014.

- Weron et al. [2003] R. Weron, M. Bierbrauer, and S. Trück. Modeling electricity prices: jump diffusion and regime switching. HSC Research Reports HSC/03/01, Hugo Steinhaus Center, Wroclaw University of Technology, 2003.

- Yu [2016] S.-Z. Yu. Hidden Semi-Markov Models. Elsevier, Boston, 1st edition, 2016.

- Zucchini and Guttorp [1991] W. Zucchini and P. Guttorp. A hidden Markov model for space-time precipitation. Water Resources Research, 27(8):1917–1923, 1991.