Self-similar martingales derived from Root embedding

Abstract

Given a family of integrable mean-zero probability measures such that, for every , is the image of under the homothety , we provide a necessary and sufficient condition on under which the Root embedding algorithm yields a self-similar martingale with one-dimensional marginals . Precisely, if and denote the Root solution to the Skorokhod embedding problem (SEP) and the Root regular barrier for respectively, then this condition is equivalent to the property that is non-increasing in the sense of inclusion, which in turn is equivalent to the assertion that is non-decreasing a.s. We show that there are many examples for which this result applies and we provide some numerical simulations to illustrate the monotonicity property of regular barriers in this case.

keywords: Skorokhod embedding problem, Root embedding, regular barriers, self-similar martingales.

subclass MSC: 60E15, 60G44, 60J25.

1 Introduction

There are many results in the literature related to the construction of self-similar processes. In Madan-Yor [23], Fan-Hamza-Klebaner [10], Hamza-Klebaner [13], Hirsch-Profeta-Roynette-Yor [15], Bogso [6] and Henry-Labordère-Tan-Touzi [14], the authors provided many constructions of self-similar martingales with given marginal distributions. In particular, Madan and Yor [23], Hamza and Klebaner [13], and Henry-Labordère, Tan and Touzi [14] exhibited several examples of discontinuous fake Brownian motions. Albin [1] answered positively the question of the existence of continuous fake Brownian motion, and this result was extended by Baker-Donati-Martin-Yor [2] who exhibited a sequence of continuous martingales with Brownian marginal distributions and scaling property. A quite simple construction of continuous fake Brownian motion, based on Box-Muller transform, has been given by Oleszkiewicz [24]. The results on fake Brownian motion was extended by Hobson [17] to prove the existence of a continuous fake exponential Brownian motion. More recently, Jourdain and Zhou [19] provided a new class of fake Brownian motions which solve a special class of local and stochastic volatility SDEs. Certain of the works cited above use Skorokhod embedding solutions to construct self-similar martingales. Precisely, Madan and Yor [23] exploit the Azéma-Yor algorithm, Hirsch, Profeta, Roynette and Yor [15] apply Azéma-Yor, Hall-Breiman and Bertoin-Le Jan embedding solutions, and they provided a new Skorokhod embedding solution that gave another class of self-similar martingales. We show that the Root embedding solution also provides a class of martingales which enjoy Brownian scaling.

Let be a square-integrable mean-zero probability measure and let be a standard Brownian motion. Root [26] proved the existence of a closed time-space set , the so-called Root barrier, such that the first hitting time of by the time-space process solves the Skorokhod embedding problem for (SEP()), meaning that has distribution and is uniformly integrable. He also defined a barrier function attached to as and observed that is lower semi-continuous. The problem of the existence of a stopping-time for Brownian motion in such a way that the stopped value has a given distribution was first stated and solved by Skorokhod [28]. Note that different Root barriers may embed the same distribution. This was solved by Loynes [22] who introduced the notion of a regular barrier and proved that there exists exactly one regular barrier that solves SEP(). On the other hand, the Root’s solution is optimal in the sense that it has minimal variance among all stopping times such that has distribution and . This was conjectured by Kiefer [21] and was solved later by Rost [27]. We refer to Beiglböck, Cox and Huesmann [5] where a transport-based approach to the SEP has been developed to derive all known and a variety of new optimal solutions. Another interesting question on Root embedding is that it is not easy to find explicitely the regular Root barrier for a given distribution. Indeed, this barrier is constructed explicitely only for a handful of simple examples. Dupire [9] showed formally that the Root barrier is given by the solution of a nonlinear PDE. This was further developed by Cox and Wang [8] who use a variational formulation to calculate . A complete characterization of regular Root barriers as free boundaries of PDEs has been provided by Gassiat, Mijatovic and Dos Reis [12]. When the distribution is atom-free, Gassiat, Mijatovic and Oberhauser [11] established that the barrier function solves a nonlinear Volterra integral equation and that if, in addition, is continuous, then is the unique solution. More recently, Cox, Oblòj and Touzi [7] provided a characterization of regular Root barriers by means of an optimal stopping formulation and exploited this approach to establish a finitely-many marginals extension of the Root solution to the SEP. These authors also proved that their solution satisfies an optimality property which extends the optimality property of the one-marginal Root solution. Using the Cox, Hobson and Touzi results, Richard, Tan and Touzi [25] provided a full marginals extension on some compact time interval of the Root solution to SEP. Precisely, using a tightness result established by Källblad, Tan and Touzi [20, Lemma 4.5], they proved that the full marginals limit of the finitely-many marginals Root solution for the SEP exists and enjoys the same optimality property as the multiple-marginals Root solution provided in [7].

Here we consider the case of a family of integrable mean-zero probability measures where is the image of under the homothety . We apply Root solution for the SEP to embed simultaneously all ’s into a standard Brownian motion issued from . The Root embedding provides a family of regular barriers and a family of stopping times such that and has law . We apply the optimal stopping characterization of one-marginal Root solution to the SEP given in [7, Theorem 2.8] and Brownian scaling to prove that the regular barrier function defined on is self-similar in the sense that

where denotes the set of positive real numbers. This result can also be deduced from the viscosity PDE characterization of regular Root barriers obtained by Gassiat, Mijatovic and Dos Reis [12, Theorem 2]. We deduce from the monotonicity property of that, for every , is non-decreasing. The self-similarity property of the function given above allows us to obtain a necessary and sufficient condition on under which the family of Root barriers is non-increasing, in the sense that (i.e. includes ) for every . This monotonicity property of the family is equivalent to the assertion that is non-decreasing a.s. Then, as solves the SEP for , is a martingale with marginals . Moreover, we prove that enjoys the Brownian scaling and the Markovian properties.

In Section 2, we exploit the optimal stopping characterization of one-marginal Root solution for the SEP to prove that the function is self-similar. Then, we provide a sufficient condition on the barrier function under which the family of regular Root barrier is non-increasing. This allows us to exhibit a new class of martingales with Brownian scaling in Section 3. We also discuss the Markovian properties of these processes. In Section 4, we provide some numerical simulations to illustrate the monotonicity property of the regular barriers . The numerical scheme follows the idea of Gassiat-Oberhauser-Dos Reis [12, Section 4]. In particular, the Barles-Souganidis method [3, 4] can be applied to obtain the convergence of the scheme and a result due to Jakobsen [18] provides its convergence rate.

2 Root embedding under scaling

Let be an integrable probability measure, and let denote a one-dimensional Brownian. A solution to SEP() is any stopping time such that has law , and is uniformly integrable. In the case where has zero mean and a second moment, Root provided a Skorokhod embedding solution that is the first hitting time of a barrier, the so-called Root barrier.

Definition 2.1.

A closed subset of is called a Root barrier if

-

(i)

implies for all ,

-

(ii)

for all ,

-

(iii)

.

Given a Root barrier, one defines its barrier function as

Since is closed, then, as observed by Root [26] and Loynes [22], is a lower semi-continuous function. Moreover, one deduces from Property (i) in Defition 2.1 that is the epigraph of in the plane (see e.g. Cox-Oblòj-Touzi [7]), i.e.

There may exist different Root barriers which solve SEP(). But Loynes [22] introduced the notion of regular barrier and he provided a uniqueness result when we restrict ourselves to regular Root barriers.

Definition 2.2.

A Root barrier is said to be regular if its barrier function vanishes outside the interval , where and are respectively the first negative and the first positive zeros of .

Theorem 2.3.

The finite variance assumption in the preceding result has recently been relaxed to the condition that the measure has a finite first moment. This was first obtained by Gassiat-Oberhauser-Dos Reis [12] who provide a complete characterization of regular Root barriers as free boundaries of PDEs. The next result is a special case of Theorem 2 and Corollary 1 in [12].

Theorem 2.4.

(Gassiat-Oberhauser-Dos Reis [12, Theorem 2, and Corollary 1]). Let be an integrable and centered probability measure. For every , let be the image measure of under (in particular, ). The following equivalent assertions hold:

-

(i)

There exists a regular Root barrier such that solves SEP(),

-

(ii)

There exists a viscosity solution , decreasing in time, of

(2.1) where is the potential function of :

Moreover,

| (2.2) |

Precisely, is the unique regular Root barrier such that solves SEP() and is the free boundary (2.2) of the obstacle PDE (2.1).

Remark 2.5.

A characterization of Root solution to the Skorokhod embedding problem by means of an optimal stopping formulation has been provided recently by Cox-Oblój-Touzi [7, Theorem 2.8]. These authors proved this result using purely probabilistic methods. We state here a special case of Theorem 2.8 in [7].

Theorem 2.6.

(Cox-Oblój-Touzi [7, Theorem 2.8]). Consider a one-dimensional Brownian motion defined on a filtered probability space satisfying the usual conditions. Let be an integrable zero-mean probability measure. For every , let denote the image of under . Define

| (2.3) |

| (2.4) |

where is the collection of all -stopping times taking values in . Then the stopping region

| (2.5) |

is the regular barrier inducing the Root solution to the SEP(). Moreover,

For every , let denotes the barrier function of . The next result states that the function satisfies a self-similarity property.

Theorem 2.7.

Proof.

By Brownian scaling,

is a Brownian motion. As a consequence, rewrites

where is the collection of all -stopping times which take values in . Moreover, for every , , and ,

Hence, as , we have

We deduce from Point (i) that

where . Then, for every ,

which completes the proof. ∎

Remark 2.8.

To prove that the function is self-similar, one may apply alternatively either the PDE characterisation of Root barrier provided by Gassiat-Oberhauser-Dos Reis (Theorem 2.4 and Remark 2.5) or, when the barrier function of is continuous, the integral equation for Root barrier due to Gassiat-Mijatovic-Oberhauser [11].

1. Let be the unique viscosity solution of linear growth of the obstacle PDE

| (2.7) |

then, for every , the function defined by

is a viscosity solution of linear growth of (2.1), and one has

2. Suppose that is a family of atom-free probability measures such that, for every , is the image of under and the regular barrier function of the Root solution for SEP is continuous. This condition holds, for instance, when is symmetric around and admits a compact support and a bounded density which is nondecreasing on . (see e.g. [11, Proposition 1]). Since is also atom-free, its barrier function solves the following Volterra integral equation:

| (EVλ) |

for every , where and, for every ,

Moreover, we know from corollary 2 in [11] that, for every , is the unique continuous function that solves (EVλ). Observe that (EVλ) is still valid if one replaces by . Then, as is the image of under , (EVλ) rewrites

| (EV) |

But, since , (EV) is equivalent to

where, for every , . Hence is also a continuous function that solves (EV1). It then follows from the uniqueness result for (EV1) that

which is equivalent to (2.6).

3 Root self-similar martingales

In the next result we present a family of self-similar martingales. Precisely, we provide a necessary and sufficient condition so that the map is non-decreasing a.s.. We also show that several probability measures satisfy this condition.

Theorem 3.1.

Let be an integrable and centered probability measure. Let be a standard Brownian motion started at . For , let , and denote the image measure of under , the Root solution for SEP() and the regular barrier function of respectively.

-

(i)

If the map is a.s. non-decreasing, then is a martingale satisfying Brownian scaling such that has law for every . Moreover, the process is Markovian and if, in addition, has no atom, then the martingale is also Markovian.

-

(ii)

The map is a.s. non-decreasing if and only if

(3.1)

Proof.

Suppose that the map is a.s. non-decreasing. Let denote the natural filtration of . Since, for every , is uniformly integrable, then

which means that is a martingale. Moreover, by Brownian scaling,

is still a one-dimensional Brownian motion for every . As a consequence, we have

where

Now, one may also deduce from Point (ii) of Theorem 2.7 that

Indeed, one has

Hence,

and, as a consequence,

which shows that satisfies Brownian scaling.

Let be fixed. Since a.s., we have

where

and

It follows from the strong Markov property of Brownian motion that is a Brownian motion independent of . Then, for every bounded measurable function ,

where

which shows that is a (non-homogeneous) Markov process. If has no atom, then one deduces from Lemma 1 in [11] that a.s. and, as a consequence, that is Markovian.

Let denote the Root barrier given by the function . We first note that the map is a.s. non-decreasing if and only if the family is non-increasing in the sense of set inclusion, which means that is non-decreasing for every . Hence it remains to show that for every if and only if is non-decreasing on and non-increasing on . Suppose first that is non-decreasing for every . Let belong to . Since , one has

which shows that is non-decreasing on . Similarly, one may show that is non-increasing on . Conversely, suppose that is non-decreasing on and non-increasing on . As is positive, is non-decreasing. Moreover, for every , one may observe that

which shows that is still non-decreasing when . ∎

Remark 3.2.

Condition (3.1) is weaker than

| (3.2) |

Indeed, if (3.2) holds, then, as is positive, non-decreasing on , non-increasing on and as is non-negative, one deduces that is non-decreasing on , and non-increasing on . Many regular barrier functions given in the literature satisfy Condition (3.2) (see e.g. [16, Example 5.2] and [8, Section 2]).

We now present some examples to which Theorem 3.1 applies. We mention that, given a probability measure , it is hard to compute the regular barrier function that gives the Root Solution to SEP(). There are only few cases where this can be done explicitely. Numerical methods have been provided to compute Root barriers with great precision (see e.g. [11, Section 3] and [12, Section 4]).

Example 3.3.

If is a zero-mean normal distribution, then it is not difficult to see that is constant. Indeed, the Root solution to SEP() equals to the square-mean of . In this case is still a Brownian motion which may be non-standard.

If is of the form

where are real numbers such that , then the corresponding Root barrier function is (see e.g. [8, Section 2])

Suppose that has the form

Then the corresponding regular barrier function is

where is a nonnegative real number (see e.g. [16, Point 3 of Example 5.2]). Observe that is non-decreasing on and non-increasing on .

Let be an integrable probability measure on which satisfies the Assumption 1 in [11], that is has mean zero, and the Root barrier solving SEP() is given by a function which is symmetric around , continuous, and non-increasing on . There are several probability measures satisfying the above assumption. Indeed, as proved in [11, Proposition 1], symmetric probability measures around with compact support and bounded non-decreasing density on fulfill Assumption 1 in [11].

We mention that there are also probability measures to which Theorem 3.1 does not apply. For instance, if is the canonical measure on the middle Cantor set, then, by Root’s result, the resulting barrier function must be finite only on the Cantor set.

4 Numerics: Monotone self-similar Root barriers

The aim of this paragraph is to give some pictorial representations of the monotonicity property of certain self-similar regular Root barriers. We use an explicit finite differences scheme adapted from the scheme implemented in [12, Section 4] to simulate Root barriers. The Barles-Souganidis method [3, 4] gives a convergence result of this scheme.

Fix an integrable mean-zero probability measure whose support is denoted by supp. Fix also and . Let be the image of under . We distinguish two cases.

Choose such that supp, and consider the following time-space mesh of points in

where with large enough. As in [12, Section 4], we denote by the set of bounded function from to and by the subset of consists of bounded uniformly continuous functions. Since supp is bounded, the unique viscosity solution , resp. of (2.7), resp. (2.1) belongs to . Let (with ) denote the discrete approximation of . The values of are obtained by solving the system

with defined as

where we suppose that the usual CFL condition: holds. Let (with ) be the function given by when for some and . Observe that the restriction of to , which is also denoted by , belongs to . Since has bounded support, . By Proposition 1 in [12],

| (4.1) |

Moreover, Proposition 2 in [12] provides the rate of the convergence result (4.1) (see [18, Section 3] for more details). Hence, for sufficiently small , the subset of , defined as

| (4.2) |

nearly coincides with the regular Root barrier on the rectangle .

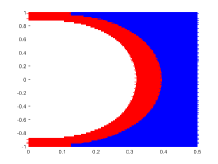

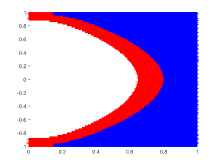

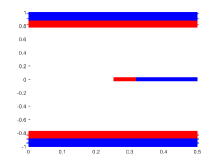

The figures below show that, for sufficiently small, includes when satisfies Condition (3.1) in Theorem 3.1. The barriers and are plotted in blue and red respectively. Figure 1 illustrate the fourth point in Example 3.3. Precisely, is a symmetric probability measure around with compact support and a bounded non-decreasing density on . Figure 2 is a pictorial representation of the third point of Example 3.3. Indeed, has the form

where and .

References

- Albin, [2008] Albin, J. M. P. (2008). A continuous non-brownian motion martingale with brownian motion marginal distributions. Statist. Probab. Letters, 78(6):682–686.

- Baker et al., [2011] Baker, D., Donati-Martin, C., and Yor, M. (2011). A sequence of albin type continuous martingales with brownian marginals and scaling. In Séminaire de probabilités XLIII, pages 441–449. Springer.

- Barles and Souganidis, [1990] Barles, G. and Souganidis, P. E. (1990). Convergence of approximation schemes for fully nonlinear second order equations. In 29th IEEE Conference on Decision and Control, pages 2347–2349 vol.4.

- Barles and Souganidis, [1991] Barles, G. and Souganidis, P. E. (1991). Convergence of approximation schemes for fully nonlinear second order equations. Asymptotic analysis, 4(3):271–283.

- Beiglböck et al., [2017] Beiglböck, M., Cox, A. M. G., and Huesmann, M. (2017). Optimal transport and skorokhod embedding. Inventiones mathematicae, 208(2):327–400.

- Bogso, [2015] Bogso, A. M. (2015). Mrl order, log-concavity and an application to peacocks. Stochastic Processes and their Applications, 125(4):1282–1306.

- Cox et al., [2017] Cox, A. M., Obłój, J., and Touzi, N. (2017). The root solution to the multi-marginal embedding problem: an optimal stopping and time-reversal approach. arXiv preprint arXiv:1505.03169v2.

- Cox et al., [2013] Cox, A. M., Wang, J., et al. (2013). Root’s barrier: Construction, optimality and applications to variance options. The Annals of Applied Probability, 23(3):859–894.

- Dupire, [2005] Dupire, B. (2005). Arbitrage bounds for volatility derivatives as free boundary problem. Presentation at PDE and Mathematical Finance, KTH, Stockholm.

- Fan et al., [2015] Fan, J. Y., Hamza, K., Klebaner, F., et al. (2015). Mimicking self-similar processes. Bernoulli, 21(3):1341–1360.

- Gassiat et al., [2015] Gassiat, P., Mijatović, A., Oberhauser, H., et al. (2015). An integral equation for root’s barrier and the generation of brownian increments. The Annals of Applied Probability, 25(4):2039–2065.

- Gassiat et al., [2017] Gassiat, P., Oberhauser, H., and dos Reis, G. (2017). Root’s barrier, viscosity solutions of obstacle problems and reflected fbsdes. Stochastic Process. Appl., 125(12):4601–4631.

- Hamza and Klebaner, [2007] Hamza, K. and Klebaner, F. C. (2007). A family of non-gaussian martingales with gaussian marginals. International Journal of Stochastic Analysis, 2007.

- Henry-Labordere et al., [2016] Henry-Labordere, P., Tan, X., and Touzi, N. (2016). An explicit martingale version of the one-dimensional brenier’s theorem with full marginals constraint. Stochastic Process. Appl., 126(9):2800–2834.

- Hirsch et al., [2011] Hirsch, F., Profeta, C., Roynette, B., and Yor, M. (2011). Constructing self-similar martingales via two skorokhod embeddings. In Séminaire de probabilités XLIII, pages 451–503. Springer.

- Hobson, [2011] Hobson, D. (2011). The skorokhod embedding problem and model-independent bounds for option prices. In Paris-Princeton Lectures on Mathematical Finance 2010, pages 267–318. Springer.

- Hobson, [2013] Hobson, D. G. (2013). Fake exponential brownian motion. Statist. Probab. Letters, 83(10):2386–2390.

- Jakobsen, [2003] Jakobsen, E. R. (2003). On the rate of convergence of approximation schemes for bellman equations associated with optimal stopping time problems. Mathematical Models and Methods in Applied Sciences, 13(05):613–644.

- Jourdain and Zhou, [2016] Jourdain, B. and Zhou, A. (2016). Existence of a calibrated regime switching local volatility model and new fake Brownian motions. ArXiv e-prints.

- Källblad et al., [2017] Källblad, S., Tan, X., and Touzi, N. (2017). Optimal skorokhod embedding given full marginals and azéma–yor peacocks. The Annals of Applied Probability, 27(2):686–719.

- Kiefer, [1972] Kiefer, J. (1972). Skorohod embedding of multivariate rv’s, and the sample df. Probability Theory and Related Fields, 24(1):1–35.

- Loynes, [1970] Loynes, R. M. (1970). Stopping times on brownian motion: Some properties of root’s construction. Probab. Theory Related Fields, 16(3):211–218.

- Madan and Yor, [2002] Madan, D. B. and Yor, M. (2002). Making markov martingales meet marginals: with explicit constructions. Bernoulli, 8(4):509–536.

- Oleszkiewicz, [2008] Oleszkiewicz, K. (2008). On fake brownian motions. Statist. Probab. Letters, 78(11):1251–1254.

- Richard et al., [2018] Richard, A., Tan, X., and Touzi, N. (2018). On the root solution to the skorokhod embedding problem given full marginals. arXiv preprint arXiv:1810.10048.

- Root, [1969] Root, D. H. (1969). The existence of certain stopping times on brownian motion. Ann. Math. Statist., 40(2):715–718.

- Rost, [1976] Rost, H. (1976). Skorokhod stopping times of minimal variance. In Séminaire de Probabilités X Université de Strasbourg, pages 194–208. Springer.

- Skorokhod, [2014] Skorokhod, A. V. (2014). Studies in the theory of random processes. Courier Corporation.