R.FONTANA

Department of Mathematical Sciences G. Lagrange, Politecnico di

Torino.

E. LUCIANO

ESOMAS Department and Collegio Carlo Alberto, Università di Torino

P. SEMERARO

Department of Mathematical Sciences G. Lagrange, Politecnico di

Torino

Elisa Luciano gratefully acknowledges financial support from the Italian

Ministry of Education, University and Research (MIUR), ”Dipartimenti di

Eccellenza” grant 2018-2022.Roberto Fontana and Patrizia Semeraro gratefully acknowledge financial support from the Italian

Ministry of Education, University and Research (MIUR), ”Dipartimenti di

Eccellenza” grant 2018-2022.

Abstract

The issue of model risk in default modeling has been known since inception

of the Academic literature in the field. However, a rigorous treatment requires a description of all

the possible models, and a measure of the distance between a single model

and the alternatives, consistent with the applications. This is the purpose

of the current paper. We first analytically describe all possible joint models for

default, in the class of finite sequences of exchangeable Bernoulli random variables. We then

measure how the model risk of choosing or calibrating one of them affects

the portfolio loss from default, using two popular and economically

sensible metrics, Value-at-Risk (VaR) and Expected Shortfall (ES).

keywords: Exchangeable Bernoulli distribution; risk measures; model risk.

1 Introduction

Models for default risk are prone to so-called model risk, in two senses:

adopting the wrong model for the occurrence of default and calibrating or

estimating a given model in a wrong way. The occurrence of model risk in the

first sense is inherent in default, because of the difficulty of describing

the causes of default or even of enumerating the determinants. Even the

occurrence of calibration or estimation risk is overwhelming, because of the

scarcity of observations, especially when looking at the joint default of

specific obligors or particular categories of obligors, and lack of data to

estimate parameters such as the correlation of defaults. The issue of model

risk is indeed particularly strong in joint defaults, because on top of the

model risk for marginal defaults there is model risk also in their joint

distribution. We focus on joint modeling.

The issue of model risk in default modeling has been known since inception

of the Academic literature in the field. Professionals are well aware of its

importance too. However, a rigorous treatment requires a description of all

the possible models and a measure of the distance between a single model

and the alternatives, consistent with the applications. This is the purpose

of the current paper. We first describe all possible joint models for

default, in the class of exchangeable Bernoulli random variables. We then

measure how the model risk of choosing or calibrating one of them affects

the portfolio loss from default, using two popular and economically

sensible metrics, Value-at-Risk (VaR) and Expected Shortfall (ES).

Univariate models of default belong to two families: structural and

reduced-form models. The structural models, initiated by [1],

reconduct default to the fact that the so-called asset value of a firm goes

below a given monetary threshold. Reduced-form models, whose seminal work is

due to [2], estimate from interest rates on

defaultable debt the intensity of default, which is then interpreted as a

fixed parameter or a stochastic process itself. For a survey of the

approaches see for instance [3].

Multivariate models either make use of a copula to aggregate univariate

default probabilities (see for instance [4], or [5], or use a Bernoulli mixture model

(see chapter 8 in [6]).

The difficulties in choosing the right model for univariate modeling and

calibrating it have been shown to be considerable. For structural models,

the asset value is unobservable. For reduced-form models, rates of return on

bonds are thought to include also a liquidity spread, which is difficult to

separate from the default spread.

The difficulties in choosing or calibrating a multivariate model are even

bigger (see the early recognition in [7]). Structural models can be calibrated, provided the correlation

matrix of asset values can be. Multivariate reduced-form models are usually

calibrated using the corresponding structural dependence (see chapter 10 in

[5]).

The previous literature which assesses model risk in joint default usually

takes as given the marginal probabilities of default, as we do: marginal

default indicators are Bernoulli variables. It tries to explore the range of

joint default probabilities, or the possible distribution of the loss from

credit risk, which is the weighted sum of the marginal Bernoulli variables,

where the weights are the exposures of the creditor towards different

obligors. To do that, the literature uses different copulas (see[8]). Here we use the fact that all joint distributions

or distributions of sums are generated starting from a finite number of

so-called ray densities. Differently from copulas, all the rays can be

found, either numerically or analytically.

[9] developed a simple method to represent all

the Bernoulli variables with some specified moments, as a convex hull of

densities belonging to the same class, the ray densities. They provide an

algorithm to find the extreme rays of a given class without restrictions

either on the number of variables or on the specified moments. The only

drawback of the method is the amount of computational effort required for

the numerical solution. The main contribution of the current paper consists

in finding analytically the convex hull generators for the class of exchangeable Bernoulli variables with given mean and for the class of exchangeable Bernoulli variables with given mean and correlation. The analytical solution allows us to work in any dimension.

Once the multivariate Bernoulli variables represent the default indicators

of a portfolio of obligors, the ray densities, that we can find analytically, allow

us to describe all the joint distributions of defaults, even for large

portfolios, and/or the possible distributions of the loss. There is a third

mathematical contribution that helps in doing that: we show that the VaR bounds are reached on ray densities and we find an analytical expression for them. We also explicitly found bounds for the ES.

We then measure the consequence of using a specific model (which might be

”wrong” one) or calibrating it in the ”wrong” way looking at the range of

the possible VaR and ES.

So, the paper is novel both for the Mathematical contribution, namely the

analytical description of the ray densities in high dimensions, and for the

Mathematical Finance one, namely measurement of model risk using all

possible multivariate distributions, obtained as linear convex combinations of generators that can be analytically found. This analytical solution allows us to find analogical bounds to measure model risk.

The paper unfolds as follows: Section 2 introduces the mathematical framework. Section 3 introduces the notion and properties of rays

for exchangeable Bernoulli variables. Section 4 introduce the risk measures and provide analytical bounds for exchangeable Bernoulli variables. Model risk is discussed in Section 5. Section 5.1 provides calibrated examples. Section 6

concludes.

2 Default indicators: mathematical background

We consider a credit portfolio with obligors.

Some notation is needed.

Let the random variable be the default

indicators for the portfolio and let us assume that the indicator is exchangeable, i.e. , where

is the class of -dimensional exchangeable Bernoulli

distributions. Let be the class of exchangeable Bernoulli

distributions with the same Bernoulli marginal distributions , where is the marginal default probability of each obligor. If is a random vector with joint distribution in , we denote

•

its cumulative distribution function by and its probability mass function (pmf)

by ;

•

the column vector which contains the values of

over , by

respectively; we make the non-restrictive hypothesis that the set of binary vectors is ordered according to the

reverse-lexicographical criterion. For example and ;

•

we denote by the set of permutations on ;

Recall that the expected value of is , . We denote .

We assume that vectors are column vectors.

2.1 Exchangeable Bernoulli variables

Let us consider a pmf of a -dimensional Bernoulli distribution with mean .

Since for any , any mass function in is given by if and .

Therefore we identify a mass function in with the corresponding vector . Furthermore, the moments depend only on their order, we therefore use to denote a moment of order , where .

We also observe that the

correlation between two Bernoulli variables and is related to the second-order moment as follows

(2.1)

2.2 Joint defaults, loss distribution and risk measures

To model the loss of a credit risk portfolio of obligors we consider

the sum of the individual losses

where and . In this paper we consider the case . The extension to unequal weights can be done numerically. For

equal weights, , where

represents the number of defaults. Therefore, the distribution of

represents the distribution of the loss. Since the vector of default indicators is assumed to be exchangeable, there is a one-to-one correspondence between the distribution of the number of defaults and the joint distribution of .

In fact, as said in the preliminaries,

since for any , any mass function in is given by if and . We can define

a one-to-one correspondence between and the class of the distributions on the number of defaults.

Let be the class of distributions on such that with . Let and .

The map:

(2.2)

is a one-to-one correspondence between and .

Therefore we have

(2.3)

We now prove that the class of distributions coincides with the entire class of discrete distributions with mean , say . This fact is useful to simplify the search of the generators of . The class is not of special interest in this context, but it is introduced for technical reasons.

Proposition 2.1.

It holds .

Proof.

1) . This is trivial.

2) . Let . Let us define and for all such that . The mass function is the mass function of a -dimensional Bernoulli random vector, which is exchangeabe by contruction. We have

(2.4)

Then .

Now let . We have and .

∎

Therefore the three classes , and are essentially the same class, i.e.

(2.5)

Thanks to the above proposition to find the generators of we can look for the generators of . This simplifies the search. The generators we find are in one-to-one relationship with the generators of .

3 Exchangeable Bernoulli generators

We build on the results in [9], where the authors represent the Fréchet class of multivariate -dimensional Bernoulli distributions with given margins and/or pre-specified moments as the points of a convex hull. The generators of the convex hull are mass functions in the class and they can be explicitly found. The range of application of this method is limited only by the computational effort required since the number of generators increases very quickly as the dimension increases. We show here that under the condition of exchangeability this limit can be overtaken because we analytically find the ray densities. As a consequence the dimension is no longer an issue. We focus on two classes: the class and the class , i.e. the class of exchangeable Bernoulli vectors with given and given correlation . The one to one correspondence between the distributions and is also a one-to-one correspondence between the distributions and .

In Section 3.1 we represent the class as a convex hull of

mass functions in the class, which we call ray densities, so that each mass

function is a convex combinations of ray densities belonging to . We analytically find the ray densities and their number, that depends on the dimension and the mean value . The one-to-one map between and and Proposition 2.1 are crucial.

In Section 3.2 we represent the class , as well as as a convex hull of ray densities.

We analyticall find them using the one-to-one correspondence between the

class and the class and between the relative subclasses and .

We prove that ray densities in have support on at most three points.

By so doing, also in this case the dimension is not an issue.

3.1 For given marginal default probabilities

Using the equivalence stated in Proposition 2.1 a pmf in is a pmf on with mean .

Thanks to the map in Equation 2.5 this is also equivalent to find a set of conditions that a pmf of a multivariate Bernoulli has to satisfy for being in . This fact is crucial in the following proposition.

Proposition 3.1.

Let be a discrete random variable defined over and let be its pmf. Then

(3.1)

Proof.

Let be a discrete random variable defined over . By Proposition 2.1 iff .

It holds

∎

Using Proposition 3.1 we can find all generators of that, thanks to the map is equivalent to find all the generators of .

We have to find the solutions of

(3.2)

with the conditions and . From the standard theory of linear equations we know that all the positive solutions of 3.2 are elements of the convex cone

(3.3)

where and is the identity matrix, and therefore can be generated as convex combinations of a set of generators which are referred to as extremal rays of the linear system. The proof of the following proposition follows Lemma 2.3 in [10].

Proposition 3.2.

Let us consider the linear system

(3.4)

where is a matrix, and . The extremal rays of the system 3.4 have at most non-zero components.

Proof.

Let be the convex cone of all the positive solutions of 3.4.

A solution of 3.2 is an extremal ray of iff for a submatrix , of and

(3.5)

Therefore and has at most non-zero components.

∎

Corollary 3.1.

The extremal rays of the convex cone in 3.3 have at most two non-zero components.

Proof.

Let , . The matrix is the row vector of the coefficients. Since then an extremal ray has at most two non-zero components.

∎

Proposition 3.3.

The extremal rays of of the convex cone in 3.3 are

(3.6)

with , , is the largest integer less that and is the smallest integer greater than pd.

By Corollary 3.1 the extremal rays have at most two non zero components, say . Therefore the extremal rays can be found considering the equations

(3.9)

where we make the non restrictive assumption . The equation 3.2 has positive solutions only if . We observe that for where is the largest integer less than and for where is the smallest integer greater than . In this case we have . It follows that for and we have . A positive solution of Equation 3.2 is

(3.10)

We have and then the normalized extremal rays corresponding to and are given by (3.6).

If is integer we have . It follows that (3.7) is also an extremal solution.

∎

We denote by and the random variables whose pmf are and respectively.

We will refer to and as ray densities and

and as ray random variables. Notice that .

Corollary 3.2.

If not integer there are ray densities.

If integer there are ray densities.

We have proved the following.

Theorem 3.1.

The following holds. iff there exist summing up to 1 such that

(3.11)

where are the ray densities and is the number of ray densities.

3.1.1 Second order moments

Let and let its second order cross moment.

Proposition 3.4.

Let . It holds

(3.12)

Proof.

By exchangeability we can fix any pair . It holds

∎

Thanks to the one-to-one map we can find the bounds for the second order moments of using the second order moments of .

We have

(3.13)

Proposition 3.5.

Let . Then

if is not integer

(3.14)

If is integer

(3.15)

Proof.

From (3.13) we have . Since its density is a convex linear combinations of the ray densities. It is known that the moments of are moments of the ray variables.

We obtain

(3.16)

and

(3.17)

To maximize we have to maximize . From (3.16) and (3.17) we easily get that the ray variable for which the second order moment is maximum is and we have . Then, after some computations, .

To minimize we have to minimize . We consider two cases.

If is not integer, from (3.16) we have that the ray variable for which the second order moment is minimum is , for which we have

and the assert follows.

If is integer the ray variable for which the second order moment is minimum is . Since , (3.15) follows.

∎

Thanks to equation (2.1), the next corollary to the above proposition provides bounds for the correlation coefficient.

Corollary 3.3.

Let . Then

if is not integer

(3.18)

If is integer

(3.19)

3.2 For given marginal default probabilities and default correlations

In this section we consider the class of multivariate exchangeable Bernoulli

mass functions with given margins and given correlation , i.e.

the class .

We now find the generators of .

Since iff and , we can define an homogeneous linear system whose solutions are the pmf in .

Proposition 3.6.

The following holds. iff there exist summing up to 1 such that

(3.20)

where are the normalized extremal rays of the cone defined by linear system:

(3.21)

The following corollary of Proposition 3.2 characterizes the ray densities of .

Corollary 3.4.

The extremal rays of have support on at most

three points.

Proof.

The extremal rays of (3.2) are the normalized extremal rays of the convex cone , where is the matrix coefficients of (3.21). We have .

From Proposition 3.2 it follows and to let have independent rows. Since , if , has only three non zero components, if , has only two non zero components, and if , has only one non zero component. In the latter case all the mass is one point.

and its solution can be determined by standard computation using Cramer’s formula.

∎

We conclude this section with the following proposition that gives necessary and sufficient conditions for a ray density in to be also a ray density in .

Proposition 3.8.

A ray density has support on two points iff it is a ray density in and , where is the second order cross moment of .

Proof.

If is a solution of (3.21) it is also a solution of (3.2) and since it has support of two poins by assumption it is an extremal solution. Thus is a ray density. Viceversa if it satisfies the first equation of (3.21) by definition and if it also satisfy the second equation by construction.

Since it has mass on two points it is an extremal solution of (3.21).

∎

4 Financial risk measures and their bounds

As measures of portfolio risk we consider the value at risk (VaR) and the

expected shortfall (ES) of . We recall their definition for a general random variable .

Definition 4.1.

Let be a random variable representing a loss with finite mean. Then the

at level is defined by

(4.1)

and the expected shortfall at level is defined by

(4.2)

The following proposition provides the bounds for the and of , for in a given class.

Proposition 4.1.

1.

Let and let be its value at risk. Then

where are the ray densities of .

2.

Let and let be its expected

shortfall. Then

where are the ray densities of .

Proof.

1.

Let . Let , and . It holds

(4.3)

thus .

It holds

(4.4)

with therefore we have . Thus and .

2.

and are trivial.

∎

The above propositions shows that reaches the maximum and minimum values in [] on the ray densities and

therefore we are able to explicitly find them.

Remark 1.

The bounds for are weaker and trivial. Nevertheless, at least in some cases, they cannot be improved. In fact, consider the ray density . If then . As a consequence for marginal default probabilities higher then the bound is reached.

Thanks to Proposition 3.3 that gives the analytical expression of the ray densities of , the following proposition provides the analytical bounds for in .

Proposition 4.2.

Let us consider the class and let .

1.

If , and , where is the largest integer smaller than .

2.

If , , where is the smallest integer greater or equal to and .

3.

If , and .

In this case, if is integer .

Proof.

Let us consider first the case not integer.

The ray densities are given in (3.6) with and . From the definition of we have

(4.5)

It follows

(4.6)

then

(4.7)

We also know that , so let us determine the point of intersection of and .

The solution of

(4.8)

is .

We distinguish three cases, depending on .

1.

. In this case it will follow that for all and then the minimum value of . With respect to the maximum value of it will be obtained by , where is the largest integer smaller than .

2.

. Let us define as the smallest integer greater or equal to . It follows that , with is the smallest integer greater or equal to . Then the minimum value of . The maximum value of is .

3.

. In this case . Then the minimum value of and the maximum value of . If is integer we also have .

∎

We can also explicitly find the bounds in by searching the maximum e minimum among the ray densities, whose analytical expression is given in Proposition 3.7. The analytical computation of is out of the aim of the present paper, here we simply serach for the minimum and the maximum among the ray densities.

5 Model risk analysis

The theory developed so far allows us to perform model risk analysis.

Consistently with it, let us suppose we have a credit portfolio with 100

obligors. Let the random vector

collect the default indicators for the portfolio and assume , where . The variable represents the number of

defaults and the distribution of represents the distribution of the

loss. We analytically find bounds of and , for

, and for two classes of

multivariate exchangeable Bernoulli variables and .

The analysis of these two classes of models allows us to study the two

aspects of model risk mentioned in the Introduction, the risk associated to

the pure choice of a ”wrong” model (pure model risk) and the one associated

to a ”wrong” calibration of the joint model, through default correlation

(calibration risk). In both cases we do not investigate the correctness of

the marginal default probability, which would be the case if we were

investigating marginal model risk.

The bounds of the first class provide an economically sensible measure of

pure joint model risk. To complete the picture, for any we provide

the range of admissible correlations for the hundred Bernoulli variables.

The bounds of the second class provide a measure of calibration risk. The

bounds are obtained for a specific correlation coefficient: we perform a

sensitivity analysis of their behavior when changes. For each

correlation, we also consider and associated

to a specific joint model (the Bernoulli mixture one), to show how the

method can be used to assess not calibration risk in general, but the

calibration risk of a specific model, considering how far its and are from the bounds.

In all cases we consider three scenarios corresponding to three marginal

default probabilities , and , which are the

1-year marginal default probabilities resulting from [11] table 13 page

40, for the rating

classes and .

5.1 Pure model risk

Here we deal with in the three scenarios and All the results in this section are analytical.

5.1.1 Scenario 1:

Before computing and for the class corresponding to Moody’s A rating, let us describe it. The class has ray densities that we can find analitically and we found that

all ray densities have different correlations. The bounds for the all moments of the distributions in the class are reached on the ray densities as proved in [9]. In this case the bounds for the second order moment and correlation are analytical, as proved in Section 3.1.1. The moments up to order four and correlation are given in Table 1. Obviously, the

first moment coincides with and its range is a singleton. Notice that all positive correlations and some

negative are allowed. This is possible since we consider finite sequences of Exchangeable Bernoulli variables and not only the mixing models, i.e. the De Finetti’s sequences. So, per se, independently of any model, a hundred

Bernoulli default indicators with equicorrelation cannot span negative

dependence, but are able to span any level of positive dependence and zero

correlation.

Order

Min moment

Max moment

1

0.003

0.003

2

0

0.003

3

0

0.003

4

0

0.003

-0.003

1

Table 1: Moments class of multivariate Bernoulli

Table 2 shows the bounds for the for the

three levels , and .

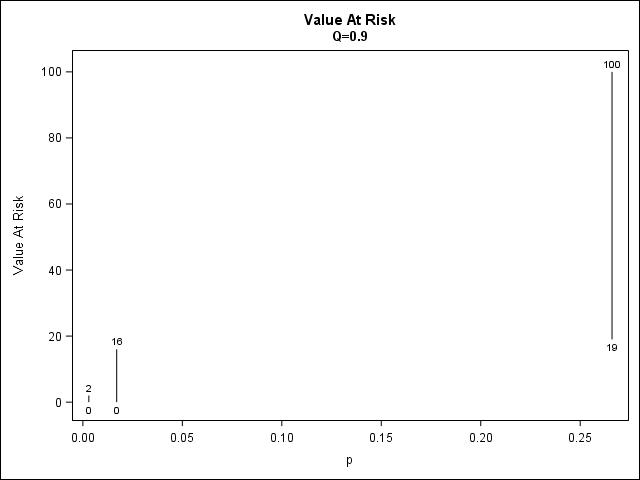

Quantile

Min

Max

0.9

0

2

0.95

0

5

0.99

0

29

Table 2: of the number of defaults for the class of

multivariate Bernoulli

Table 3 shows the bounds for the ES on the ray densities for the

three levels , and .

Quantile

Min ES

Max ES

0.9

0.3

2

0.95

0.3

5

0.99

0.3

29

Table 3: ES of the number of defaults for the class of

multivariate Bernoulli

5.1.2 Scenario 2

Let us assume , The class has ray

distributions of with different correlations. Table 4 provides the bound of the moments also for this class.

Order

Min moment

Max moment

1

0.017

0.017

2

0

0.017

3

0

0.017

4

0

0.017

-0.009

1

Table 4: Moments class of multivariate Bernoulli

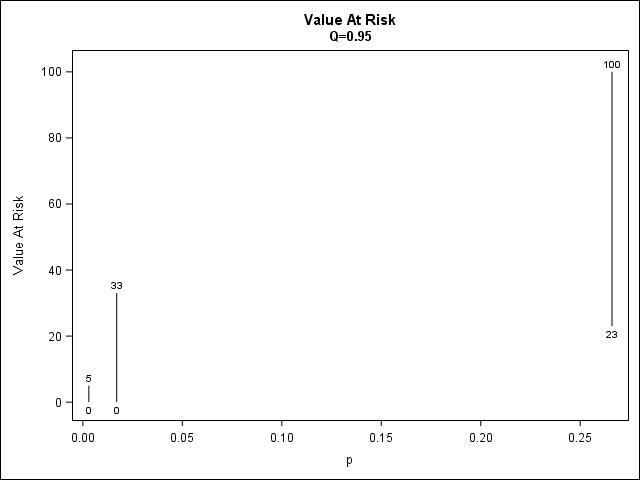

Table 5 shows the bounds for the for the

three levels ; and .

Quantile

Min

Max

0.9

0

16

0.95

0

33

0.99

1

100

Table 5: of the number of defaults for the class of

multivariate Bernoulli

Table 6 shows the bounds for the on the ray densities for the

three levels ; and . Since we have , as noticed in Remark 1.

Quantile

Min ES

Max ES

0.9

1.7

16

0.95

1.7

33

0.99

1.7

100

Table 6: ES of the number of defaults for the class of

multivariate Bernoulli

5.1.3 Scenario 3

We consider the class . The number of ray densities is

much higher relative to the other two classes considered since it is 1998. Table 7 shows that the range of the third and fourth moments of this class is wider that for the other classes.

Order

minmom

maxmom

1

0.266

0.266

2

0.069

0.266

3

0.017

0.266

4

0.004

0.266

-0.01

1

Table 7: Moments class of multivariate Bernoulli

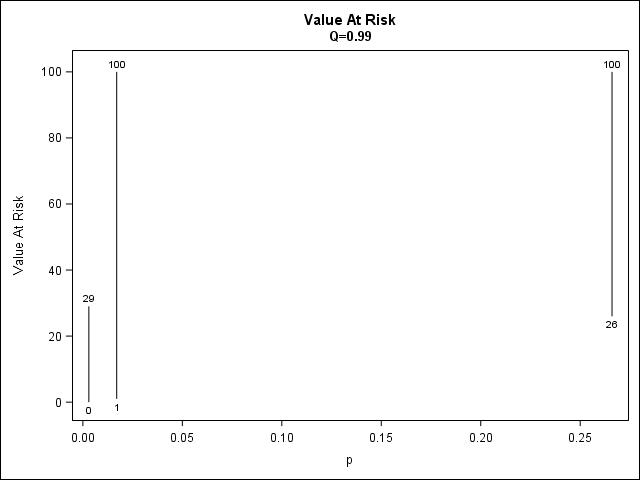

Table 8 shows the bounds for the for the

three levels ; and .

Quantile

Min

Max

0.9

19

100

0.95

23

100

0.99

26

100

Table 8: of the number of defaults for the class

of multivariate Bernoulli

The following Table 9 shows the bounds for the on the ray densities for the

three levels ; and . As one can see the maximum is d=100 for each , in fact .

Quantile

Min ES

Max ES

0.9

26.6

100

0.95

26.6

100

0.99

26.6

100

Table 9: ES of the number of defaults for the class of

multivariate Bernoulli

5.1.4 Cross scenario comparisons

The reader can appreciate how model risk increases, when the marginal

probability does, and when the risk measure is , looking at Figure 1. The computation permits to conclude that the VaR range increases with the marginal default probability, and not only with the level of confidence (which is the standard result). Also, both the minimum and the maximum are non decreasing with p.

5.2 Calibration risk

In this Section we examine the behavior of the loss under the three

scenarios above for the marginal default probability, when, on top of the

marginal, a specific value of the equicorrelation has been selected. We deal

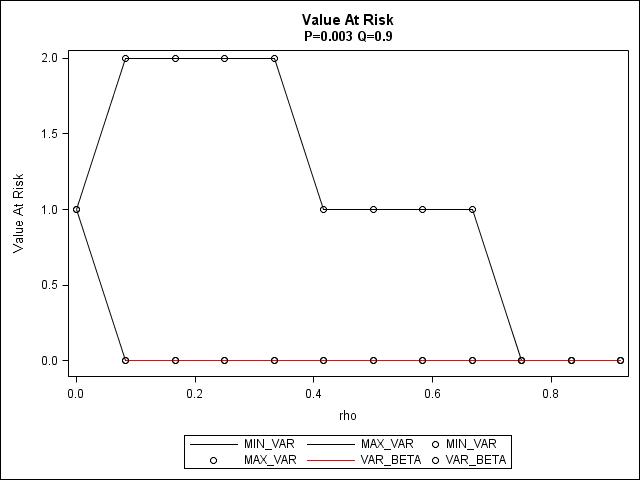

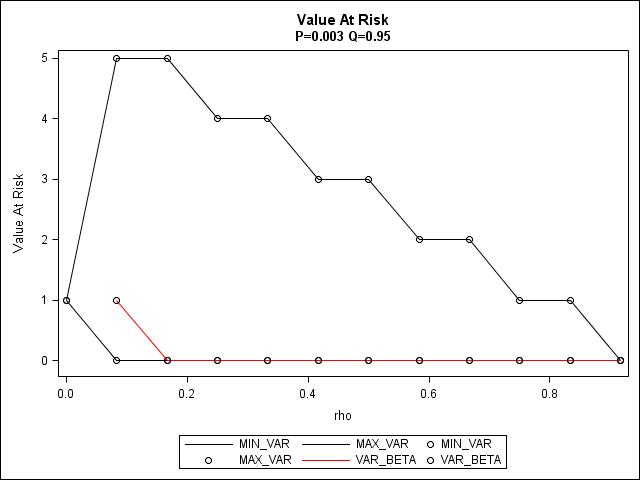

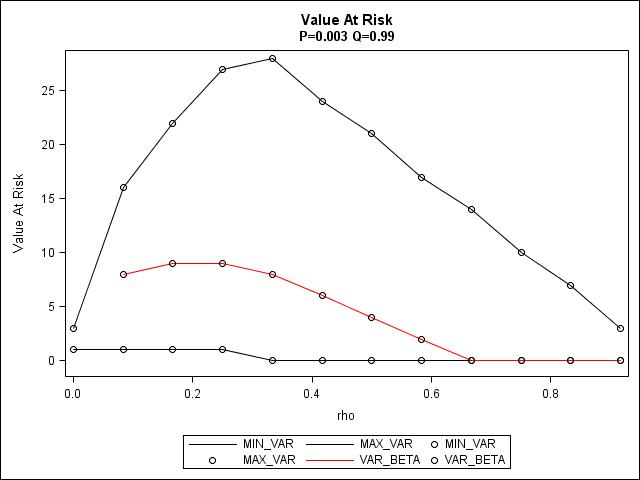

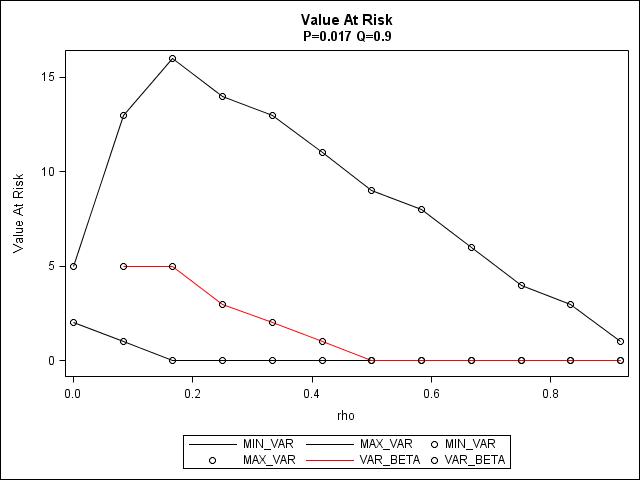

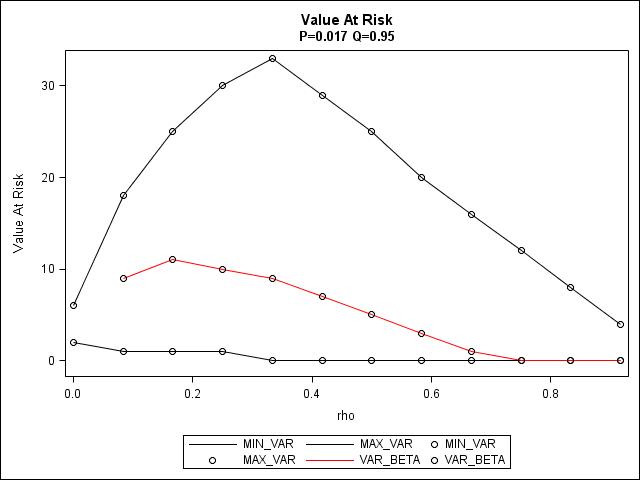

with in the three scenarios and and provide bounds for for three levels of correlation: .

Here, the ray densities are analytical as well as their VaR. The bounds are found by computationally searching the maximum and minimum VaR among the ray densities.

As a benchmark we choose an exchangeable Bernoulli mixing model from the credit risk literature. We estimate the -mixing model of each scenario and compute its .

Let be the number of default of the -mixing models, we have (for a complete overview see [6]):

(5.1)

where the mixing variable. We have

(5.2)

Therefore we estimate the parameters and by

(5.3)

Notice that for this model is not admissible.

5.2.1 Scenario 1

Table 10

provides the bounds of when only correlation is known and it

is and the corresponding measures for the -mixing

model.

Quantile

min

max

-

0.9

0

2

0

0.95

0

5

0

0.99

1

22

9

Table 10: of the number of defaults for the class of multivariate Bernoulli

Table 11

provides the bounds of when only correlation is known and it

is and the corresponding for the -mixing

model.

Quantile

min

max

-

0.9

0

1

0

0.95

0

3

0

0.99

0

21

4

Table 11: of the number of defaults for the class of multivariate Bernoulli

Table 12

provides the bounds of when correlation is known and it

is and the corresponding measure for the -mixing

model.

Quantile

min

max

-

0.9

0

0

0

0.95

0

1

0

0.99

0

7

0

Table 12: of the number of defaults for the class of multivariate Bernoulli

5.2.2 Scenario 2

Table 13

provides the bounds of when correlation is known and it

is and the the -mixing

model .

Quantile

min

max

-

0.9

0

16

5

0.95

1

25

11

0.99

2

55

29

Table 13: of the number of defaults for the class of multivariate Bernoulli

Table 14

provides the bounds of when correlation is known and it

is and the corresponding measure for the -mixing

model.

Quantile

min

max

-

0.9

0

9

0

0.95

0

25

5

0.99

1

93

57

Table 14: of the number of defaults for the class of multivariate Bernoulli

Table 15

provides the bounds of when correlation is known and it

is and the corresponding for the -mixing

model.

Quantile

min

max

-

0.9

0

3

0

0.95

0

8

0

0.99

61

100

94

Table 15: of the number of defaults for the class of multivariate Bernoulli

5.2.3 Scenario 3

Table

16

provides the bounds of when correlation is known and it

is and the corresponding measures for the -mixing

model.

In this case the number of generators of the class significantly increases.

In fact, the class is generated by 32.372

ray densities.

Quantile

min

max

-

0.9

21

82

53

0.95

26

100

62

0.99

38

100

76

Table 16: of the number of defaults for the class of multivariate Bernoulli

Table 17

provide the bounds of when correlation is known and it

is and the corresponding measure for the -mixing

model.

Quantile

min

max

- R

0.9

42

100

82

0.95

56

100

93

0.99

63

100

100

Table 17: of the number of defaults for the class of multivariate Bernoulli

Table 18

provide the bounds of when correlation is known and it

is and the corresponding measure for the -mixing

model.

Quantile

min

max

-

0.9

81

100

100

0.95

86

100

100

0.99

88

100

100

Table 18: of the number of defaults for the class of multivariate Bernoulli

5.2.4 Cross scenario comparisons

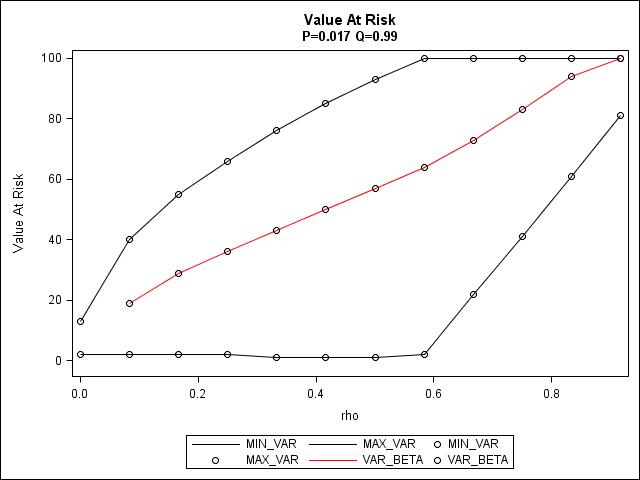

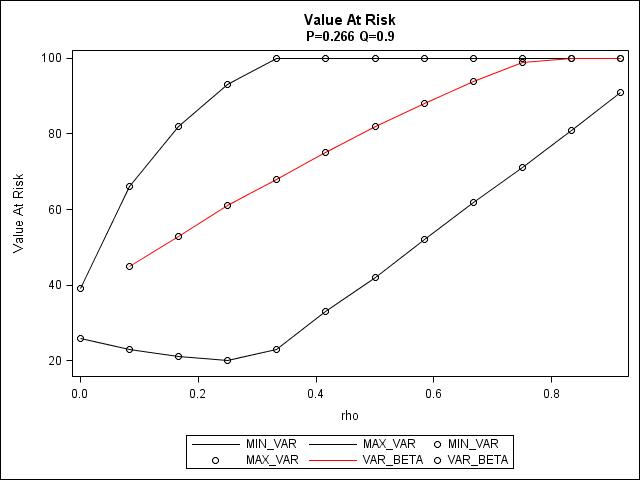

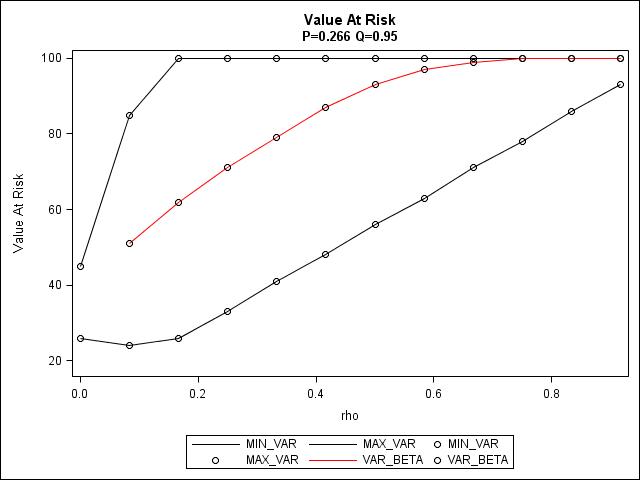

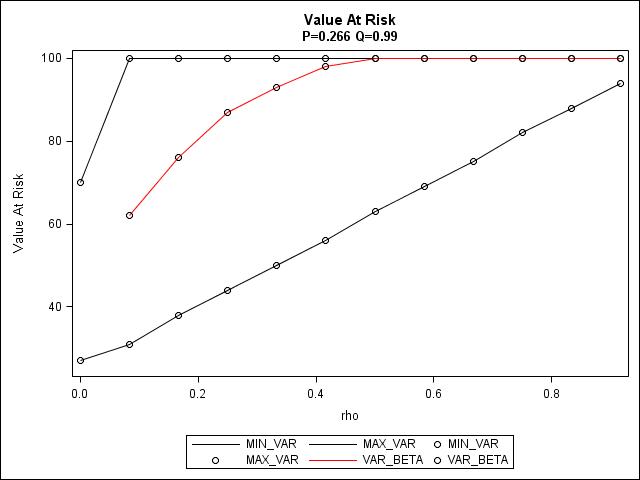

Figures 2, 3 and 4 plot the bounds for VaR when takes equispaced value in the range .

The reader can appreciate how calibration risk increases, when the marginal

probability and the correlation does. It also emerges that the of the -mixing model sometimes reaches the bound and depending on and its values with respect to the bounds significantly change. In particular for low the of the -mixing model coincides with the minimum .

The plots show that, even if the -mixing model is calibrated to match the moments of the Bernoulli, it tends to produce a VaR close to the minimum one for low , and close to the maximum for high . In any case, the width of the band between the minimum and the maximum, together with the specific location of the VaR within it, give a sense of how wrong the risk appreciation can go, when calibrating a specific correlation, and how stringent is the choice of a specific multivariate distribution within that calibration.

6 Conclusions

Measuring model risk in credit and default modeling is important, at least

to have a sense of the consequences of mispricing of financial products,

forecasting errors etc. Since, at present, model risk in credit and default

cannot be avoided, we can try to measure it. This paper does exactly that,

in a very general context (exchangeable, equicorrelated Bernoulli), using

two popular risk measures, VaR and ES.

The main contributions are the closed form results for the VaR bounds and the moments of the multivariate distributions, as well as the numerical examples which show how big model risk can be, with a portfolio of 100 obligors with equal exposure, especially when the marginal default probability is high.

References

[1]

R. C. Merton, “On the pricing of corporate debt: The risk structure of

interest rates,” The Journal of finance, vol. 29, no. 2, pp. 449–470,

1974.

[2]

R. A. Jarrow and S. M. Turnbull, Credit Risk: Drawing the Analogy,

vol. 5.

1992.

[3]

T. Bielecki, M. Jeanblanc, and M. Rutkowski, “Credit risk modeling.,” CSFI Lecture Notes Series, vol. 2, 2009.

[4]

U. Cherubini, E. Luciano, and W. Vecchiato, Copula methods in finance.

John Wiley & Sons, 2004.

[5]

D. Duffie and K. Singleton, “Credit risk: Pricing, measurement, and

menagement,” 2003.

[6]

A. J. McNeil, R. Frey, and P. Embrechts, Quantitative risk management,

vol. 3.

Princeton university press, 2005.

[7]

P. Embrechts, A. McNeil, and D. Straumann, “Correlation and dependence in risk

management: Properties and pitfalls.,” Risk management: value at risk

and beyond, ed. Dempster, M.

[8]

P. Embrechts, A. Höing, and A. Juri, “Using copulae to bound the

value-at-risk for functions of dependent risks,” Finance and

Stochastics, vol. 7, no. 2, pp. 145–167, 2003.

[9]

R. Fontana and P. Semeraro, “Representation of multivariate bernoulli

distributions with a given set of specified moments,” Journal of

Multivariate Analysis, vol. 168, pp. 290–303, 2018.

[10]

M. Terzer, Large scale methods to enumerate extreme rays and elementary

modes.

PhD thesis, ETH Zurich, 2009.

[11]

“Default, transition, and recovery: 2017 annual global corporate default study

and rating transitions.”

Figure 1: VAR ranges for

Figure 2: VAR bounds for and different and -mixing model VAR

Figure 3: VAR bounds for and different and -mixing model VAR

Figure 4: VAR bounds for and different and -mixing model VAR