Counterfactual Inference for Consumer Choice Across Many Product Categories

Abstract

This paper proposes a method for estimating consumer preferences among discrete choices, where the consumer chooses at most one product in a category, but selects from multiple categories in parallel. The consumer’s utility is additive in the different categories. Her preferences about product attributes as well as her price sensitivity vary across products and may be correlated across products. We build on techniques from the machine learning literature on probabilistic models of matrix factorization, extending the methods to account for time-varying product attributes and products going out-of-stock. We evaluate the performance of the model using held-out data from weeks with price changes or out of stock products. We show that our model improves over traditional modeling approaches that consider each category in isolation. One source of the improvement is the ability of the model to accurately estimate heterogeneity in preferences (by pooling information across categories); another source of improvement is its ability to estimate the preferences of consumers who have rarely or never made a purchase in a given category in the training data. Using held-out data, we show that our model can accurately distinguish which consumers are most price sensitive to a given product. We consider counterfactuals such as personally targeted price discounts, showing that using a richer model such as the one we propose substantially increases the benefits of personalization in discounts.

JEL Classification: C52, C55, D12, L81, M31

1 Introduction

Estimating consumer preferences among discrete choices has a long history in economics and marketing. Domencich and McFadden’s [1975] pioneering analysis of transportation choice articulated the benefits of using choice data to estimate latent parameters of user utility functions [see also Hausman and Wise, 1978]: once estimated, a model of user utility can be used to analyze counterfactual scenarios, such as the impact of a change in price or of the introduction of an existing product to a new market. McFadden (1974) also highlighted strong assumptions implicit in using off-the-shelf multinomial choice models to estimate preferences and introduced variants such as the nested logit that relaxed some of the strong assumptions (including “independent of irrelevant alternatives”).

Analysts have applied the discrete choice framework to a variety of different types of data sets, including aggregate, market-level data (see, e.g., Berry et al. [1995], Nevo [2001], and Petrin [2002])111This literature grapples with the challenge that to the extent prices vary across markets, the prices are often set in response to the market conditions in those markets. In addition, to the extent that products have quality characteristics that are unobserved to the econometrician, these unobserved quality characteristics may be correlated with the price., as well as data from individual choices for a cross-section of individuals. In this paper, we focus on models designed for a particularly rich type of data, consumer panel data, where the same consumer is observed making choices over a period of time. Supermarket scanner data is a classic example of this type of data, but e-commerce firms also collect panel data and use it to optimize their offerings and prices. Scanner data enables the analyst to enrich the analysis in a variety of ways, for example to account for dynamics (see Keane and Wasi [2013]) for a survey. The vast majority of the literature based on individual choice data focuses on one category222Throughout the paper we use category to refer to disjoint sets of products, such that products that are within the same category are partial substitutes. at the time, e.g. Ackerberg [2001, 2003] analyzes yogurt, Erdem et al. [2003] ketchup, Dubé [2004] soft drinks, and Hendel and Nevo [2006] detergent. Often these analyses focus on the impact of marketing interventions, such as advertising campaigns, coupons, or promotions, such as in the classic work by Rossi et al. [1996].

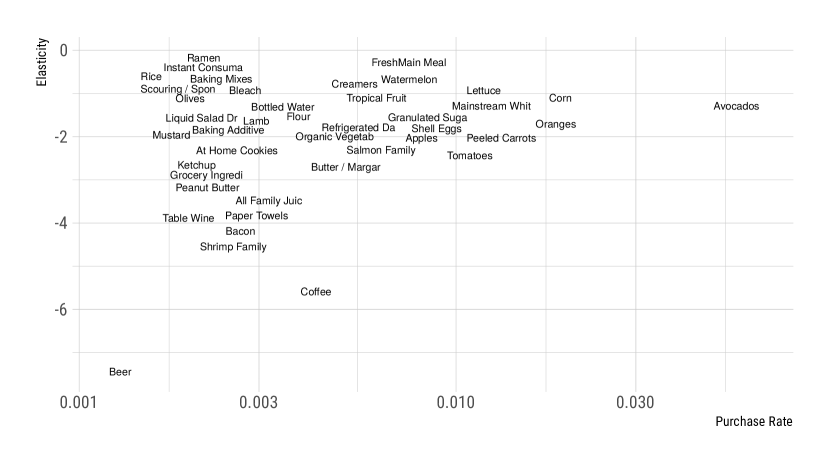

In this paper, we analyze the demand for a large number of categories in parallel. This approach has a number of advantages. First, there is the potential for large efficiency gains in pooling information across categories if the consumer’s preferences are related across categories. For example, the consumer’s sensitivity to price may be related across categories, and there may be attributes of products that are common across categories (such as being organic, convenient, healthy, or spicy). These efficiency gains are likely to be particularly pronounced for less commonly purchased items. Even among the top 100 categories in a supermarket, the baseline probability of purchasing an item in the category is very low on any particular trip, and there are thousands of categories in a typical store.333In the sample we use in our empirical exercise, among the top 123 categories the average category is only purchased on 3.7% of shopping trips. Only milk, lunch bread, and tomatoes are purchased on more than 15% of trips. Things are even sparser at the individual UPC level. The average purchase rate is 0.36% and only one, avocados, is purchased in more than 2% of the trips in our Tuesday-Wednesday sample. For e-commerce, there may be millions of products, most of which are rarely or never purchased by any particular consumer. But by pooling data across categories, it is possible to make personalized predictions about purchasing, even for categories in which the consumer has not purchased in the past.

A second advantage of analyzing many categories at once is that from the perspective of marketing, it is crucial for retailers to understand their consumers in terms of what drives their overall demand at the store, not just for individual products. For example, there may be products that are very important to high-volume shoppers, but where they are price-elastic; avoiding stock-outs on those products and offering competitive prices may be very important in store-to-store competition. Although this paper does not offer a complete model of consumers’ choice across stores, we view the demand model we introduce as an important building block for such a model.

Our model makes use of recent advances in machine learning and scalable Bayesian modeling to generate a model of consumer demand. Our approach learns a concise representation of consumer preferences across multiple product categories that allows for rich (latent, i.e. unobservable) heterogeneity in products as well as preferences across consumers. Our model assumes that consumers select a single item from a given category (a strong form of substitution, where in the empirical analysis we drop categories that have large violations of this assumption), and further assumes that purchases are independent across categories (thus ignoring budget constraints, which we argue are less likely to bind at the level of an individual shopping trip). From a machine learning perspective, we extend matrix factorization techniques developed by Gopalan et al. [2013] to focus on the case of shopping, which requires incorporating time-varying prices and demand shifts as well as an appropriate functional form. We introduce “sessions,” where prices and the availability of products are constant within a session; but these elements may change across sessions. It is common in stores for products to go in and out of stock, or to be promoted in various ways; accounting for these factors is helpful in allowing the model to estimate the parameters that are most useful for counterfactual inference. Finally, relative to the machine learning approach, we tune our model hyperparameters on the basis of performance on counterfactual estimates, and we show that this makes a difference relative to focusing on the typical machine learning objective, prediction quality. We are able to do this because our data contains a large number of distinct price changes and examples of products going out of stock, and thus we can hold out data related to some of these changes and evaluate performance of the model in predicting the impact of those changes.

The primitives of our model include the latent characteristics of products (a vector, whose dimension is tuned in the process of estimation on the basis of goodness of fit), as well as each consumer’s latent preferences for each dimension. These latent characteristics and preferences are constant over time. In addition, we do not assume that the consumer’s price sensitivity is constant across products; instead, each product has a vector of latent characteristics that relate to consumers’ price sensitivity toward the product, and each consumer’s price sensitivity is the inner product of a consumer-specific latent vector and the product’s latent characteristics that relate to price sensitivity. Thus, both the mean utility and the price sensitivity are allowed to flexibly vary across consumers and products.444We also ran alternative specifications with the per consumer price coefficients restricted to be the same across all products, however this lead to a substantial reduction along both the predictive and counterfactual fit measures of performance. In addition, the model includes controls for week-specific demand for product categories. We use a Bayesian approach, so our model produces a posterior distribution over each latent factor.

We apply our model to data from a single supermarket over a period of 23 months, where we observe the same consumers shopping over time. The data originate from shopper loyalty cards. Unlike many panels collected by third parties, the data is available at the level of the trip rather than aggregated to the weekly level, and we see shopping at a high enough frequency to identify the timing of price changes and stock-outs. In particular, we observe many weeks where prices change at midnight on Tuesday night; and otherwise, behavior is very similar between Tuesday and Wednesday. This allows us to identify the effects of price changes and be able to make counterfactual predictions. We conduct a variety of tests that assess our identification strategy, and in a departure from the machine learning literature on which we build, we evaluate model fit on the basis of the model’s ability to predict how behavior changes when prices change. We compare our model to a variety of commonly-used category-by-category models, including nested logit and mixed logit, showing that our model performs better both in terms of overall ability to fit on a representative test set, but also in terms of the model’s ability to predict responses to price changes. We examine both own-price and cross-price effects. We also examine whether the heterogeneity incorporated in our model is spurious or predictive by showing that our model tends to produce more heterogeneity across groups in terms of own-price and cross-price elasticities, and using held-out data, we show that this heterogeneity predicts heterogeneity in consumer response to price changes. We also show that our model has key advantages in terms of being able to predict the behavior of consumers who have rarely or never purchased in the training data.

2 Related Work

In the traditional discrete choice literature, it has become common to include many latent variables describing user preferences; for example, in a mixed logit model, it is common to include a user-item random effect, as well as individual-specific preference parameters for price and other observed item attributes [e.g. Berry et al., 2004, Train, 2009]. However, it is less common to model latent item attributes, other than perhaps a single dimension (quality). There are, however, several lines of work that estimate richer models that incorporate latent user characteristics, exploiting panel data.555In data from a single cross-section of consumers, Athey and Imbens [2007] show that only a single latent variable can be identified (or two if utility is restricted to be monotone in each) without functional form restrictions, arguing that panel data is critical to uncover common latent characteristics of products.

An early example is the “market mapping” literature, where each product is described as a vector of latent attributes. A market map can be used for a variety of exercises; for example, one can consider the entry of a new product into a position in the product space and forecast which consumers are likely to buy it. Empirical applications have also typically focused on a single category, such as laundry detergent (Elrod and Keane [1995] and Chintagunta [1994]).666Elrod and Keane use a factor analytic probit model with normally distributed preferences, whereas Chintagunta uses a logit model with discrete segments of consumer types.Elrod [1988a, b] use logit models to estimate up to two latent attributes and the distribution of consumer preferences. The former study uses a linear utility specification, and the latter uses an ideal-point model. Outside of shopping, there are several other social science applications making use of panel data to estimate latent item attributes and individual preferences. Goettler and Shachar [2001] study television viewing for a panel of users, and attempt to estimate latent attributes of television shows based on this panel. Another application area is political science, where panel data on legislators’ voting decisions is used to uncover their preferences and the latent characteristics of legislation. Poole and Rosenthal [1985] use a transformed logit model to estimate both the locations of legislators’ ideal points and the locations of legislative bills in a unidimensional attribute space.

There has been some progress on estimating multiple-discrete choice models in which consumers choose more than one of a single item [e.g. Hendel, 1999, Kim et al., 2002, Dubé, 2004], however a substantial portion of the literature continues to focus on categories in which the unit-demand assumption plausibly holds.

Despite the extensive literature making use of consumer panel data, very little literature in economics and marketing attempts to consider multiple categories simultaneously. A few papers study demand for bundles of products, where the products may be substitutes or complements, and where the models attempt to estimate the nature of interaction effects. These models are limited by the curse of dimensionality and generally have difficulty incorporating more than two or three categories (e.g. Athey and Stern [1998]; see Berry et al. [2014] for a review). The only paper we are aware of that estimates interaction effects across many categories is Ruiz et al. [2020] which uses a similar approach to this paper, but focuses on estimating interactions rather than exploiting available information about the category structure. We discuss this in more detail below.

Our model focuses on sharing information about consumer preferences for item attributes across categories where consumer preferences are additively separable across categories. Our model differs from the past literature in social sciences in the techniques used and in the scale and complexity of the model. In order to flexibly estimate consumer heterogeneity across multiple product categories, this paper builds on the Bayesian Hierarchical Poisson Factorization (HPF) model proposed in Gopalan et al. [2013]. The HPF model predicts the preferences each user (decision maker) has for each item (product) based on a sum of the product of a latent vector of item characteristics and a latent vector of consumer preferences for each of those item characteristics.777This approach has similarities to the econometrics literature on “interactive fixed effects models” although that literature has focused primarily on decomposing common trends across individuals over time rather than identifying common preferences for products across individuals [Moon and Weidner, 2015, Moon et al., 2014, Bai, 2009]

Gopalan et al. [2013] demonstrate that the HPF model can make accurate predictions888As is standard in the machine learning literature, the accuracy is estimated on a “held out” or “test” data set that is not used during the training of the model. This is a more accurate way to evaluate how well a model will be able to make predictions on new data that has not yet been observed. across a wide variety of contexts, including Netflix movies, New York Times articles, and scientific articles in a researcher’s Mendeley account. Despite the reputation that Bayesian methods have for being slow computationally, this model is scalable across large data set sizes999For example, when trained on Netflix data with 480,000 users, 17,700 movies, and 100 million observations, they report the model took 13 hours to converge on a single CPU. due to its use of mean-field variational inference to approximate the computationally intractable exact posterior.

The HPF model is related to the extensive recommender systems literature that uses matrix-factorization-based techniques to predict what items (movies, links, articles, search results, etc.) a user will enjoy based on their previous choice behavior [Koren et al., 2009, Bobadilla et al., 2013]. A core insight of this literature is that it is often very effective to predict a user’s interests based on the preferences of other users who have similar tastes. These approaches try to find a lower dimensional approximation of the full matrix of user and item preferences.101010The matrix has one row for each user and one column for each item. The entry corresponds to how much user “likes” item . We often only observe some of the entries of this large matrix, and would like to make predictions for the unobserved entries. e.g. predict how much a user will like a movie that they haven’t watched or rated yet. The resulting factorization often is able to make accurate predictions and can also provide an interpretable representation of the user preferences in the data.

In our empirical exercise, using data from a supermarket loyalty program, we show that simultaneously modeling consumers’ decisions across multiple product categories helps improve our ability to characterize individual level preferences relative to estimating preferences in each category independently. This has similarities to the growing area of transfer learning in machine learning [Pan and Yang, 2010, Oquab et al., 2014] in which training a model on one domain (e.g. one for which large amounts of data are available) can help improve the model’s ability to make predictions in a different domain (potentially one for which less data is available). This insight may have applications in other economics and marketing contexts, for example, data on consumers’ purchasing decisions in one domain in which purchases are frequent (grocery stores) may be able to improve our ability to estimate consumer demand in a seemingly unrelated domain in which purchases are much less frequent (cars).

Some researchers have begun using latent-factorization-based approaches in the context of customer purchasing habits in grocery and retail. Jacobs et al. [2016] extend a widely-used approach known as latent Dirichlet allocation (LDA) towards the task of predicting consumer purchases in online markets with large product assortments. More recently, Jacobs et al. [2021] further extended their approach to model a customer’s purchasing intents across multiple shopping trips and allow a customer to have multiple distinct motivations within the latent factorization. Wan et al. [2017] propose an alternative model for consumer grocery demand estimation which uses a latent factorization model with three stages. In the first stage, the consumer makes a binary choice for each category about whether or not to purchase something from the category. Next, the consumer makes a multinomial choice of which item from the category to purchase. Finally, the consumer makes a choice of how many of this item to purchase, drawn from a Poisson distribution. Latent factorization is carried out independently for each stage as regularized maximum likelihood estimation. Ruiz et al. [2020] use a model closely related to ours and the same grocery purchase data with a focus on heuristically identifying which products are likely to be substitutes or complements to each other.

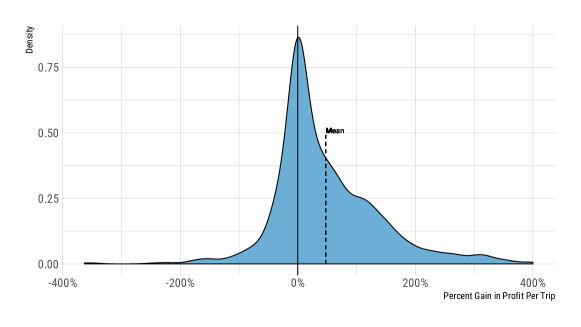

In comparison to these papers, this paper differs in its focus on designing a model able to accurately make counterfactual predictions about how customers will respond if prices were changed or the set of available products were different, for example, due to a product being out-of-stock. This goal motivates our introduction of two-stage nesting structure inspired by nested logistic regression, which allows the model to capture more realistic patterns of substitution between products. This paper also systematically evaluates the assumptions required to identify price elasticities, and conducts a comparison of alternative category-by-category demand models. In Section 6, we discuss in more detail the variety of approaches we use to evaluate the models. In particular, we show several ways to go beyond the focus on predictive fit in held-out data that is common in the machine learning literature. These approaches include evaluating our predictions across large numbers of what we call mini quasi-experiments, subsets of the held-out data that approximate the variation we would like to make counterfactual predictions about. In our application, we focus on pairs of sequential days in which either a product changes price or the set of available products changes due to a stock out, and evaluate the ability of models to predict the changes in individual-level and aggregate demand. We also evaluate the ability of each model to capture “intuitive priors”, beliefs that we expect to hold in a well-functioning model. For example, we look at whether the models predict higher cross-price elasticities between products that are more similar along characteristics that were not used while training the models. Finally, we contrast two approaches for evaluating the business impact of marketing decisions that could be powered by the model predictions. The first approach, which is common in the economics and marketing literature, is to use a model to predict impact of an alternative treatment policy, for example an allocation of coupons to a particular subset of customers. The impact of the new policy is estimated by treating the model’s fitted data generating process as ground truth. This approach can be useful for comparing the performance of different treatment policies, as shown in the seminal paper on the value of purchase history data in target marketing by Rossi et al. [1996]. However treating a model’s predictions as ground truth can overestimate the true impact, especially if one does not properly account for the uncertainty in the fitted data generating process. This over-confidence can be especially significant when using models that allow rich individual-level heterogeneity such as ours. An alternative approach is to evaluate and compare different pricing policies directly in the held-out data in a model-free way inspired by the policy learning literature [Dudik et al., 2011, Zhou et al., 2018]. We demonstrate this approach by selecting the two most common prices for each product in the data and using the model to assign each user to the price that is predicted to lead to higher profits. We can then evaluate in the held-out shopping trips whether we do in fact earn higher profits per trip when customers shop on days with their assigned price.

3 The Model

3.1 Random Utility Models and Independence of Irrelevant Alternatives

In this section, we introduce the canonical random utility model (RUM). Consider shopper on a shopping trip at time . In each product category, (e.g. bananas, laundry detergent, yogurt), there are products to choose between. Within each category, the shopper has unit demand and will purchase at most one item. To simplify the model, we assume that the product categories are disjoint and that there is no substitution or complementarity between products in separate categories.111111See Ruiz et al. [2020] for a related paper that uses a heuristic approach to identify potential substitutes and complements automatically based on patterns of co-purchase. The shopper purchases the item that provides her with the highest utility among the options in the category.

If we assume that the are drawn i.i.d. from an extreme value type 1 distribution121212Also known as the Gumbel distribution., then

| (1) |

The ratio of purchase probabilities between any two items and in the same category depend only on the ratio of their values.

| (2) |

Similarly if we consider some subset of the products in a category , then conditional on the purchase of an item from the subset, the relative purchase probability for item is given by

| (3) |

This property is known as “independence of irrelevant alternatives” (IIA). IIA imposes strong constraints on the patterns of substitution between products due to the assumption of the independence of the error terms . Suppose that product became unavailable or its attractiveness to the consumer decreases due to an increase in price. Under the assumption of IIA, the resulting customer choices will be reallocated proportionally to their initial levels; there can be no differential level of substitutability between products. How problematic this is in practice depends on what factors are included in the model of the terms. A model with no heterogeneity in preferences across users would be unable to capture the intuitive result that, when one product becomes unavailable, the other products most similar to it to gain a disproportionate fraction of the displaced purchases. Similarly, when predicting the effect of changing one product’s price on the demand for other products in the same category (the “cross-price elasticity”), the predicted effect will not depend on the similarity of the products.

This undesirable implication can be partially mitigated by extending the model to allow customer preferences to vary across the population, even if each individual’s demand is still assumed to satisfy IIA. For example, suppose that some customers like spicy salsa and other customers like mild salsa. Within each group, customer demand satisfies IIA and they proportionally substitute between the salsas that match their tastes. However, when we aggregate across the full population, we get the intuitive result that when one brand of spicy salsa goes on sale, it steals more market share from the other spicy salsas than from the mild salsas.131313McFadden [1974] provides a well known thought experiment illustrating this effect in the context of commuters choosing between driving a car, riding a red bus, or riding a blue bus. Steenburgh and Ainslie [2013] provides further details on the degree to which allowing heterogeneity in preferences reduces (but does not eliminate) the problems of the homogeneous logit model. However, even with rich heterogeneity in customer preferences, assuming IIA may still be problematic if there are unobserved factors that cause correlations in an individual consumer’s choice probabilities across time. For example, the weather, the contents of the household’s cupboards, or the shopper’s mood, might simultaneously affect the utilities of multiple products at the same time.141414In the context of the model, this would manifest as a correlation in the error terms across products, which the model assumes to be independent and identically distributed. Allowing customers to have different purchasing intentions on different shopping trips is one way to potentially address this limitation [e.g. Jacobs et al., 2021].

3.2 Estimation of the RUM using Nested Hierarchical Factorization Model

3.2.1 Nested Factorization Model

The Nested Factorization model builds on the Hierarchical Poisson Factorization (HPF) model proposed by Gopalan et al. [2013], adding a number of additional features important for capturing shopping behavior. It also extends the Time Travel Factorization Model (TTFM) introduced in Athey et al. [2018]. The TTFM model predicts the choice of where to go to lunch, treating all restaurants as single large category that a person is choosing from, rather than modeling preferences across multiple independent categories as we do here. A second important difference is that the TTFM model predicted choice of restaurant conditional on the choice to go out to eat, whereas in this paper, we wish to predict the unconditional purchase probabilities for each product.151515However these predictions are still conditioned on the shopper’s decision to visit the store, which we treat as exogenous. That is, we predict both whether or not the shopper will make a purchase from each product category and if so, which product she will choose. This is critical for making pricing decisions, since changes to prices may affect not only which product a customer chooses within a category, but also whether or not the customer buys anything at all.

Suppose we treated buying nothing from a category, the “outside good”, as one more option for the customer to choose from.161616i.e. we add an additional to each category, representing the decision to buy nothing from the category. Now the set of options for the consumer are mutually exclusive, and collectively exhaustive. On each shopping trip, for every category, a shopper either chooses something from the category or they choose the outside good. This, however, makes the assumption of IIA problematic, because the purchase rates for most product categories in a grocery store are less than 5%. If consumer purchases nothing from a category on 95% of trips, then assuming IIA implies that if a product is out-of-stock, or its price is increased, this change will almost never cause a consumer to purchase a different product from the same category. Instead, most customers will switch to buying nothing from the category, since that is the most common choice for most customers on most trips. Under this assumption, because shampoo is purchased relatively infrequently, a price increase for one brand of shampoo will mostly cause consumers to buy no shampoo at all, with very few consumers substituting to different choice of shampoo.

To address this concern, we introduce a structure similar to a nested logistic regression. This gives the model flexibility to fit the degree to which consumers substitute between different products within a product category rather than deciding to purchase nothing instead. In this particular application, we use a simple nesting structure with all of the products in a category in one nest and then a second nest with the outside good for the category. However, a similar approach could be used to allow for other more complex nesting structures, since it can be implemented via repeated runs of the same code used in the TTFM model. First, a model is trained to predict each customer’s choice of product conditional on the purchase of something from the product’s category. The results of this model are aggregated to calculate a user-category specific “inclusive value” term, which is used as an input into a second run that predicts from which categories each user will make purchases. With a more complex nesting structure, a similar process could be repeated in a bottoms up fashion, with a separate run of the model for each nest, the outputs of which can be aggregated up to use as inputs for the nests above it. While this multistage process is statistically inefficient relative to simultaneous estimation of the full model, it does substantially reduce the complexity and custom coding required for the computationally intensive portion of the estimation.171717Train [2009] section 4.2.4 provides a nice overview of the sequential estimation approach in the context of the traditional nested logit model.

3.2.2 Product Choice

To estimate the Nested Factorization model, we first train a model to predict the consumer’s choice of which products they would purchase conditional on the decision to purchase one item from the corresponding product category. For example, if the consumer has decided to purchase yogurt—which brand, flavor, and size of yogurt will she select. The mapping from utility values to conditional choice probabilities follows the standard multinomial logit form that arises from assuming a extreme value type 1 distribution for . Our model of product choice differs from the standard multinomial logit in that it allows for rich heterogeneity in preferences and price responsiveness across consumers and across items.

Similar to the HPF model from [Gopalan et al., 2013], the Nested Factorization model incorporates latent item characteristics () as well as latent user preferences for the latent item characteristics (). The Nested Factorization model extends that model by incorporating consumer and item level covariates, as well as allowing time varying characteristics such as price or product availability (e.g. a product being out-of-stock). These extensions allow for predictions at the level of individual shopping trips and for predictions of the patterns of substitution between similar products caused by price changes and changes to product availability. We assume consumers have latent preferences for observable item characteristics (), while observable user characteristics affect user preferences differentially for each product (). We allow for heterogeneity in price elasticities across users and items that depends on latent item characteristics () and latent user characteristics (). In addition, we allow for certain items to be out-of-stock or unavailable on a particular shopping trip ( if the item is out-of-stock, while otherwise).

| (4) |

| (5) |

| (6) |

3.2.3 Category Choice

We model the consumer’s choice of whether or not to purchase something from each category of goods as a series of independent binary choices. The choice to purchase from a category is assumed to depend on the utility values of items in the category, through their “inclusive value” , which is the expectation (over the realizations of the ) of the maximum of the utilities of all the available products in the category.181818If the are a standard Extreme Value Type 1 distribution, then there will be an extra term added which in practice does not matter since it can be absorbed into the constant term. Alternatively we can define to get rid of the extra term without affecting any of the choice probabilities.

| (7) | ||||

| (8) | ||||

| (9) |

The first three terms of equation 8 capture the user’s general propensity to purchase from this category, which is not affected by the utilities of any of the products in the category. The fourth term captures the impact of the inclusive value on the user’s choice. The fifth and sixth terms control for time trends that affect the popularity of product categories. This helps control for product categories that are systematically more popular at certain times of year or different days of the week. The two latent factorization terms allow for rich flexibility in capturing the correlations in preferences across users.

One interpretation of this model, is that the customer decision of whether or not to purchase from a category depends in part on her expectation of the utility she will get from choosing the product that maximizes her utility. In this interpretation, the coefficients modulate how much the consumer’s choice to buy from the category is affected by her expectation of utility she would get from picking an item in the category. If , then model simplifies to a non-nested logit—IIA holds across all nests. If , then model implies no substitution between items in different nests—no price change within the product nest would ever change your decision of whether or not to buy from the category.

An alternative interpretation of the model frames the nesting structure as capturing the correlation in the error terms of items that are in the same nest. In the context of the two group nested structure used in this paper, this correlation might reflect the consumer’s current need for products from this category, which depends on how much of the product he has at home and what he is planning on cooking for the week.

3.2.4 Estimation with Variational Bayes and Stochastic Gradient Descent

To estimate the Nested Factorization model, we build on the approach described in Ruiz et al. [2020] and Athey et al. [2018] to fit a hierarchical Bayesian model to the structure described in Section 3.2.1. We fit this model as a two step process using the same variational inference code for each step.

In the first step, we estimate the posterior distribution for the latent parameters that govern each customers conditional purchase probabilities for the products within each product category. Conditional on purchasing something from a product category, the model predicts the choice probabilities for each product within the category. In each shopping trip, only the categories that a user makes a purchase from are included in the likelihood. We denote the product purchase outcomes and the observed data which includes user characteristics, item characteristics, prices, availability, and user shopping dates. We would like to learn the posterior distribution of the latent parameters across all of the customers, products, and time periods.

As is common in many Bayesian models, the exact posterior distribution over the latent variables is computationally intractable. We instead approximate the posterior distribution using variational inference, which is typically faster on large scale Bayesian problems than classical methods such as Markov Monte Carlo sampling [Blei et al., 2017]. In variational inference, we select a flexible parameterized family of distributions over the latent variables of the model and then find the value of that makes “close” to the exact posterior in terms of Kullback-Leibler divergence.191919KL divergence is similar to a distance function in that it is non-negative and iff almost everywhere. It is not a true distance function, however, because it is not symmetric and does not satisfy the triangle inequality. In our application, we use a common approach of selecting a mean-field family for the variational distribution, in which the latent variables are mutually independent and each is distributed according to a normal distribution with its own variational parameters for mean and variance. Minimizing the KL divergence over that possible values of the variational parameters is equivalent to maximizing what is called the evidence lower bound (ELBO):

| (10) |

Although the expectations that form the ELBO are intractable, we can still seek to maximize it by noticing that the gradient of the ELBO can through clever rearrangement be rewritten as the expectation of a tractable formula.202020See Appendix 8.2 for more details and Blei et al. [2017], Ruiz et al. [2020], Athey et al. [2018] for additional exposition. This means we can use Monte Carlo estimation of the gradient in order to produce noisy-but-unbiased estimates of the gradient. We can then use stochastic gradient descent to find the variational parameters that maximize the ELBO by repeatedly taking small steps in the direction of these gradient estimates.

The result of this process is an approximation to the posterior distribution of the latent variables. We can then use this posterior to obtain a distribution over for every user, product, and shopping trip (including for products in categories a user did not make any purchases from). We use the means of these estimates to calculate the inclusive value term for each user and category as in equation 7.212121A downside of this two-step approach is that we are not able to take into account the full estimated distributions of the latent variables from the product-level model when estimating the second category-level model

We can then repeat the same variational inference process at the category level. In this stage, each user makes the choice for each category of whether or not to buy something from the category. In place of the price term from the first stage, we instead use the predicted inclusive value term . For this stage the latent parameters are

In order to reuse the variational inference code from the product level model, we fit the category choice model as if there were two products for each category: the “inside good” with calculated based on the products in the category, and “outside good” with . We then can transform the estimated parameters by subtracting the outside good’s parameters from both, to be equivalent with a model with the utility of the outside good equal to 0.

In order to make unconditional probabilities of purchase probabilities for each user, product, and trip, we combine the predictions from the two models.

4 Supermarket Application

4.1 Data

We apply the Nested Factorization model to scanner panel data from one store in a large national grocery store chain, using a data set originally assembled by Che et al. [2012]. The data is available to researchers at Stanford and Berkeley by application. This store is located in an isolated mountain region and has no other large grocery competitors within a 5 mile radius. For each transaction that a loyalty-card household makes between May 2005 and March 2007, we observe the price and quantity of each product purchased. In addition we incorporate several household demographic variables that the store has compiled from a variety of sources, including estimated age, gender, income, and household size (there are additional demographics in our data set but we restricted attention to a subset). We restrict our analysis to a sample of 2068 households who make between 20 and 300 shopping trips. These households collectively make 1,551,213 purchases during 333,585 shopping trips.222222We define a shopping trip as a set of all purchases a household makes on a calendar day. Of these, 455,445 purchases and 100,504 trips occur on a Tuesday or Wednesday. We use only the data from Tuesday and Wednesday and exclude weeks with major US holidays232323We exclude data from the week prior to Halloween, Thanksgiving, Christmas, 4th of July, and Labor Day. in our estimation approach due to concerns about the potential for price endogeneity as discussed in Section 5.

The data includes a product hierarchy for each product, with the smallest unit of analysis (the unit at which prices are set) being the universal product code (UPC). From examining the data, it is not a priori perfectly clear which level of the hierarchy best matches our desiderata for a “category,” which would be for the consumers to buy at most one item from each category, while purchasing decisions are not correlated across separate categories.242424At higher levels of aggregation, it was much more common to see multiple purchases in the same grouping on a single trip. At lower levels of aggregation, many categories were split into classes that contained products that seemed likely to be substitutes. For example, the category Apples is split into classes such as Fuji and Gala apples. Sharp Cheddar is in a separate class (but same category) as Mild Cheddar. To ensure a good match between the model and the application, we use the “category” level of the UPC hierarchy, and we focus on categories and items that pass certain filters, reducing the number of product categories from 235 to 123. Across these categories, a total of 1263 UPCs are included in the sample. The filters are reviewed in appendix Section 8.1, but important restrictions include eliminating highly seasonal categories, as well as categories without sufficient price variation, or where within-category price changes are highly correlated across products.

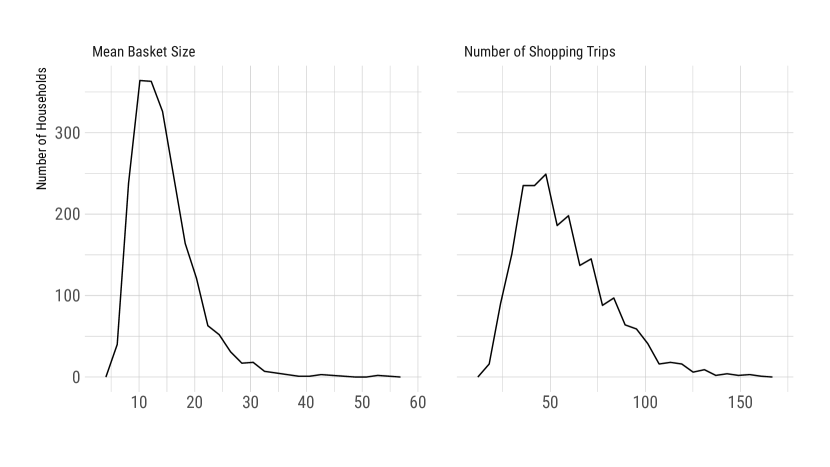

Figure 1 illustrates summary statistics on household shopping frequency and basket size in our restricted data set.

4.2 Models

4.2.1 Nested Factorization

Our primary model is the Nested Factorization model, as outlined in Section 3.2.1. The key hyperparameters of the model are the dimensionality of the latent factorizations of the user preferences and elasticities. Allowing for a higher dimensional factorization allows for more flexibility in the shopping patterns the model is able to fit, at the expense of slower estimation speeds and larger potential for overfitting the data. In order to choose the values for these hyperparameters, we follow the standard practice in the computer science literature of selecting based on performance on a “validation” subset of the data that is distinct from the subset used to train the models (and distinct from the “test” subset that is “held out” and not used until the final comparison between models). We discuss the model selection criteria in more depth in Section 6. We compare the performance of the Nested Factorization model against several alternative approaches described in the following sections.

4.2.2 Multinomial Logit

The simplest and most commonly used discrete choice model is the multinomial logit [Train, 2016], which has a long history in economics tracing back to Luce [1959] and McFadden [1974].

We focus on a baseline specification that controls for household demographics (gender, age, marital status, and income252525We divide age into buckets {Under 45, 45–55, Over 55}. We split income at $100k, which is roughly the median for this store.) and include the weekly mean category purchase rates as pseudo-fixed effects for each calendar week, which helps control for seasonal trends that shift the demand for the product category and which may be correlated with the product prices. We have also tried alternative specifications that add behavioral controls based on splitting the population into 20% buckets based on total spending in the store and a model without demographic controls, all of which had similar predictive performance. Because of its poor predictive performance across all of the measures we focus on in this paper, we have omitted the multinomial logit results from some of the results charts and tables, when the additional entries detract from clarity.

Homogeneous with Demographic Controls:262626In this model and all of the subsequent variations, “outside good” (the choice to not buy anything in the category, is assumed to take the form .

4.2.3 Mixed Logit

The mixed, or random coefficients, logit is one approach for increasing the flexibility of the multinomial logit. By allowing the coefficients of the model to vary across the population, the mixed logit allows for correlation in unobserved factors over time and for more flexible patterns of substitution between products. McFadden and Train [2000] show that any choice probabilities derived from random utility maximization can be approximated arbitrarily well by a appropriately chosen mixed logit model. As Steenburgh and Ainslie [2013] point out, the mixed logit still constrains demand at the individual level to satisfy IIA, so it “improves upon, but does not completely solve the problems of the homogeneous logit model.”

Mixed with Demographic Controls and Random Price:

Mixed with Random Intercept and Price:

With sufficiently flexible distributional assumptions for the random coefficients , a mixed logit model could have a similar degree of flexibility as the latent factorization based approach that we use in the Nested Factorization model.272727For a closer match to the Nested Factorization model, one could use a random coefficients nested logit model with product-specific random coefficients on the price in addition to the product intercepts. However, scaling such an approach can be computationally challenging, especially when the number of products is large. We estimate mixed logit models using the Stata implementation from Hole [2007], which allows each of the product intercepts to be distributed across households as independent normal distributions.

4.2.4 Nested Logit

Another method for relaxing the homogeneous logit model to allow for more flexible patterns of substitution is the nested logit model. In the nested logit model, the decisions a user faces are partitioned into “nests.” One interpretation of the nested logit structure is that a user first chooses which nest to purchase from, and then which product to choose from within the nest. An alternative interpretation frames the nesting structure as capturing common shocks that lead to correlation among the choice probabilities of products in the same nest. Within each nest, the choices satisfy the IIA substitution pattern, but the substitution between products in different nests is able to vary more flexibly. We choose the same simple nesting structure as was used in the NF model. We put the outside good in its own nest, and the remaining products in each category in a single shared nest. An additional term called the nesting coefficient or inclusive value term controls how the decision of which nest to choose depends on the utilities of the items within the nest. This nesting coefficient is analogous to the term in the Nested Factorization (equation 8) with the restriction that the value be homogeneous across households. Within the product nest, choice follows the same functional form as used in the homogeneous logit model with demographic controls. In essence, the Nested Factorization can be thought of as an extension to a nested logit that allows for rich heterogeneity in consumer preferences and price sensitivities by means of a latent factorization approach.

Nested with Demographics:

4.2.5 Discrete Choice Models with HPF Controls

One disadvantage of the Nested Factorization functional form relative to the HPF form used in Gopalan et al. [2013] is that it leads to substantially slower estimation of the approximate posterior. The choice of functional form and priors in the original HPF form allows for a closed form for the gradient of the variational Bayes objective function. With the Nested Factorization model, we have to perform stochastic gradient descent using a noisy estimate of the gradient. In practice this leads the model to require substantially more time and iterations before convergence.

This motivates an alternative approach that approximates the full Nested Factorization model with a two step approach. Estimate each shopper’s preferences over items using the HPF model.282828We extent the model proposed by Gopalan et al. [2013] to allow for each customer to face multiple independent choice occasions, one for each trip they make to the store. This extension also allows for time varying characteristics such as changes to prices and product availability. However for the application presented here, we do not include prices within the HPF model, since these outputs are used to plug into models that separately control for prices. Then, take the estimated utility values for each shopper and item and plug these values in as covariates into standard discrete choice models. This “HPF controls” approach can be thought of as an approximation to the generally infeasible approach of having separate fixed effects for each household item pair (i.e. separate parameters).

Hierarchical Poisson Factorization (HPF):292929Our extension of the original HPF model allows for observed user and item characteristics (including time varying characteristics), however on this dataset we found little or no improvement for out of sample predictive fit relative to a purely latent factorization.

This model predicts user will purchase item at a mean rate of , so we can analogize it to a discrete choice model within a category with utility taking the form , which will generate approximately the same choice probabilities for each item in the category .303030With the appropriate choice of utility for the outside good , so that This approximation works best when , which is generally true in our supermarket application, but may be less appropriate in other contexts where purchase probabilities are larger.

This two step procedure may also prove helpful in contexts where it is important to incorporate additional complications that are difficult to directly embed into the full NF Bayesian model. For example, it may be effective to include these HPF controls into models of dynamic discrete choice such as those that arise from storable goods [Hendel and Nevo, 2006] or from consumer learning [Ackerberg, 2003] as a simple way to allow richer heterogeneity in consumer preferences (at the cost of lower statistical efficiency and potentially bias from estimating as a two step procedure rather than simultaneously).

This approach may also add value by allowing researchers to take advantage of data that might otherwise go unused. Often researchers have access to a broader set of data than the sample they focus on for their primary analysis. This might be done in order to take advantage of a subset of the data which was affected by some source of quasi-experimental variation or may be due to other desirable properties of a particular subset of users or products. Latent factorization approaches, such as HPF, may be able to extract useful signal from the broader set of data, which can then be applied to improve the precision or flexibility of the primary analysis that focuses on a specific subsample of the data.

5 Identification and Placebo Tests

In our data, almost all price changes occur on Tuesday nights, near midnight, when very few customers are shopping. Thus, we can think of the price change as separating Tuesday and Wednesday. This motivates an empirical specification in which we use only the data from Tuesday and Wednesday in order to focus narrowly to the days immediately before and after price changes. We then include controls at the category level for each week and a indicator variable for Wednesday. The “identifying assumption” for learning price elasticities from this specification is that any differences in a particular consumer’s preferences for items between Tuesday and Wednesday are constant across weeks; in other words, weeks may differ from one another, but the Tuesday to Wednesday trend is constant over time. We also exclude the data from weeks immediately prior to major US Holidays out of a concern that this assumption is less likely to hold in these weeks e.g. the difference between the shopping patterns on the Tuesday and Wednesday before Thanksgiving may systematically differ from pattern that holds during more typical weeks. We find in our analysis that the Wednesday effect is small, with the average difference in category purchase probabilities between Tuesday and Wednesday of 0.127% (a 3.5% relative change in purchase probability).

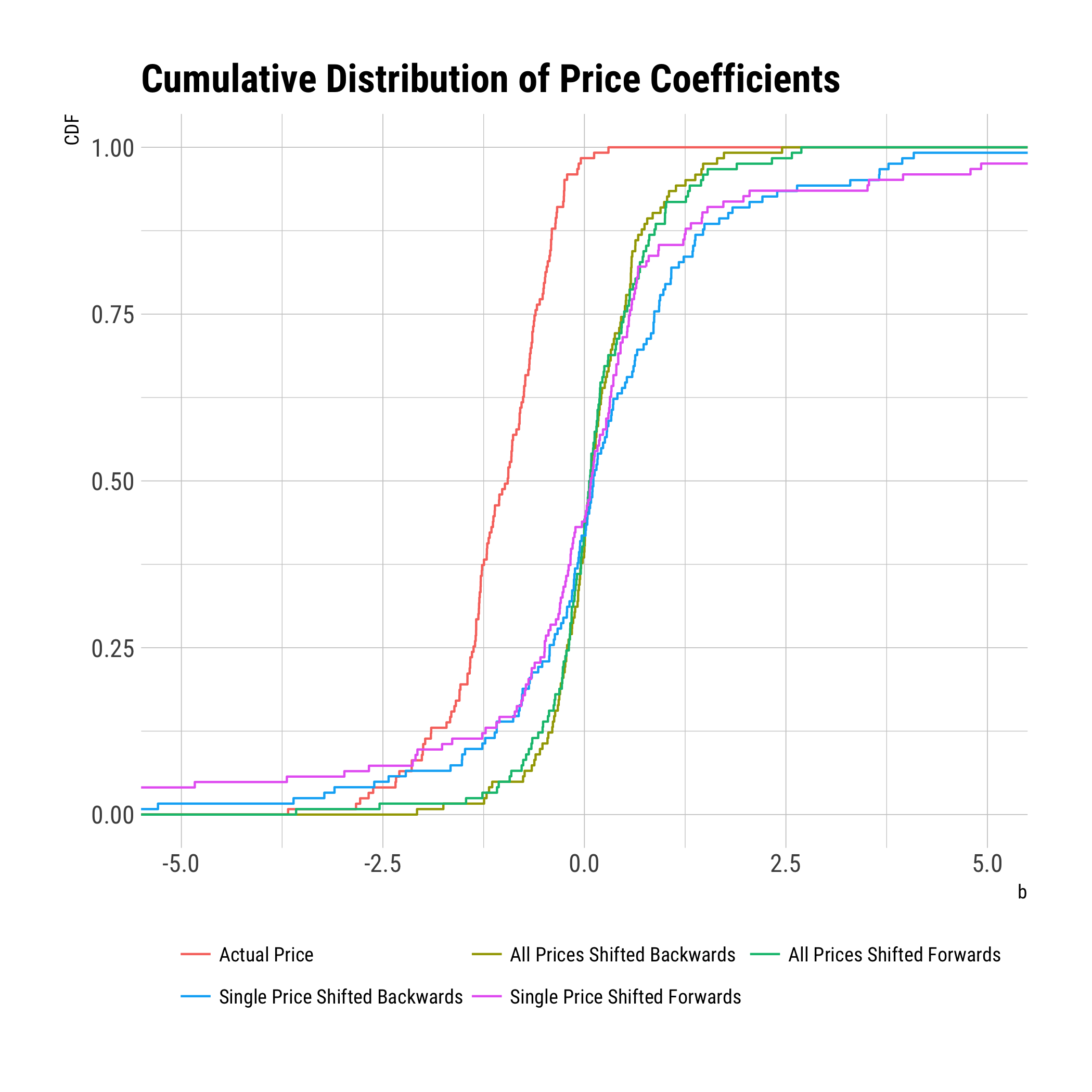

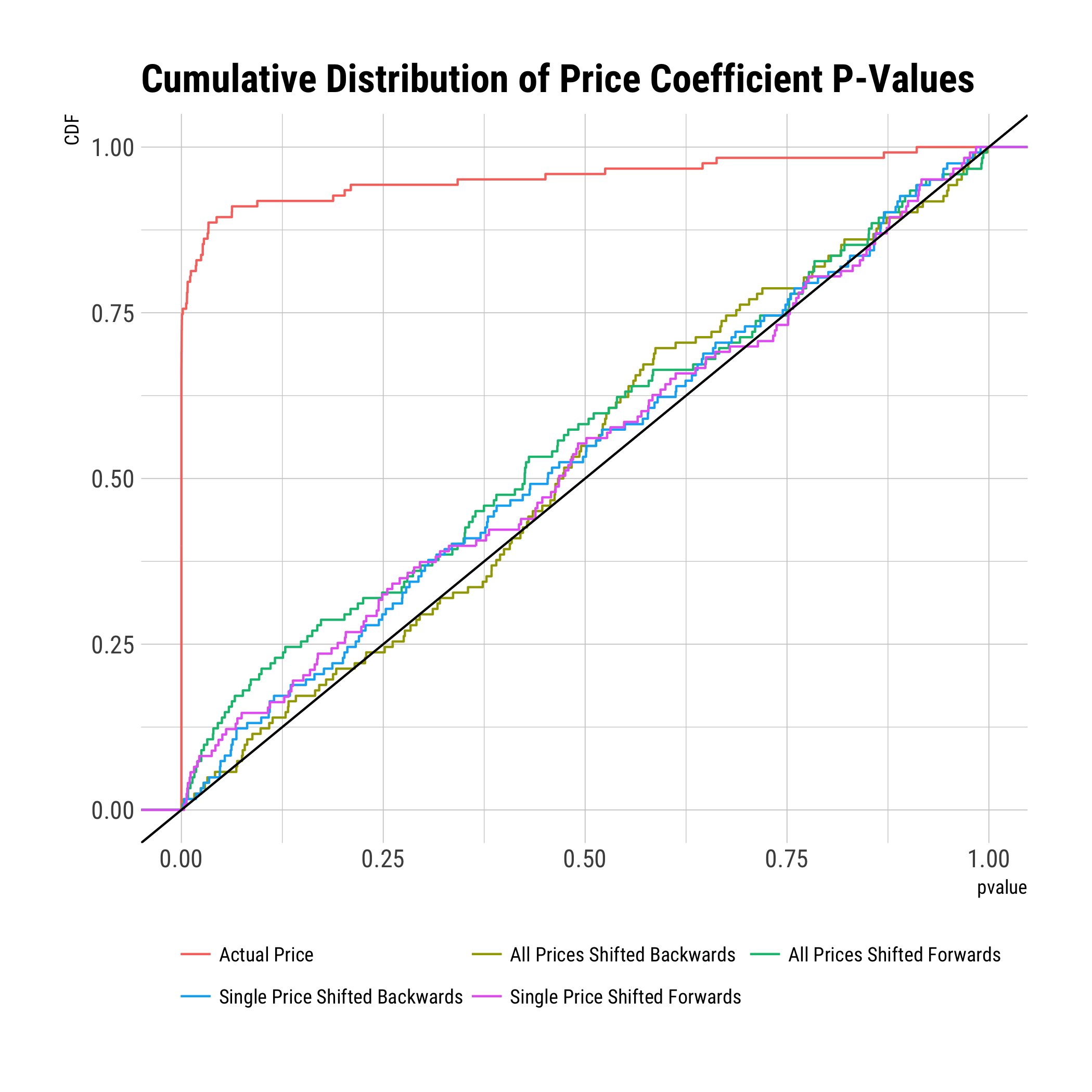

In order to assess the validity of our assumptions, we present some supplementary analysis in the spirit of the literature on treatment effects [Athey and Imbens, 2017]. In particular, we test for the presence of certain types of price endogeneity by taking the price coefficients we get from the actual price data and comparing to the price coefficients we would get from a model fit on a data with the prices shifted forwards or backwards across time. We do this in two ways, first by shifting the price of a single UPC in each category (and giving that UPC a separate price coefficient), and second by simultaneously shifting the prices of all items in the category. To create the forward shifted price series for a product, we move each week with a price change forward to the first week that had no price changes in the real data.313131Thus in the shifted data all price changes occur on weeks without price changes in the real data and all weeks with price changes in the real data have no price changes in the shifted data. A naive shift of all prices by exactly 1 week fails to break the correlation between the price changes in the shifted and real price data, due to the frequency of week-long temporary price changes. We repeat this process for each of the 123 product categories and plot the resulting distribution of price coefficients and p-values for the price coefficients. The desired result is that the shifted price series result in an approximately uniform distribution of p-values, since the artificial price changes should have no effect on consumer purchase behavior. The following results are based on the basic multinomial logit specification (with the pseudo week effects, which are calculated as the category level mean purchase rate in the week).323232We focus on the basic multinomial logit specification due to it’s computational speed and relative simplicity. Running similar tests for the other specifications including the Nested Factorization is possible in theory, but requires a larger computational cost.

Out of the 123 categories, 13 fail one of the four placebo tests at the 1% level. If we only considered unconfoundedness checks that shift prices backwards, only 4 categories fail one of the two backward shifting tests. Backwards shifts would fail in the presence of consumers who are aware of future price changes. Forward shifts can fail for goods for which stockpiling is possible. Some of the categories that fail with the forward shifted price are durable/storable (e.g. Baking Mixes, Ketchup, and Bag Frozen Vegetables), but other categories seem more likely be failing for other reasons (e.g. Refrigerated Turkey and Tomatoes).

6 Assessing Model Performance and Fit

In the machine learning literature, it is typical to split data into three non-overlapping parts: a training set, a validation set, and a test set. The training data is used to fit the parameters of the model. To the extent the model has hyperparameters333333For example the regularization coefficient in a LASSO regression, or in the case of Nested Factorization, the number of latent factors of each type to include. that must be set prior to estimation, the model estimation can be repeated under different values of the hyperparameters. The validation set is used to select a model (i.e. to make a choice of hyperparameters) based on each model’s predictive performance on the validation set. Finally, the predictive performance on held-out test data is used to evaluate the performance of the chosen model. Under the assumption that all observations are drawn from the same data generating process, then the predictive performance on the test set is an unbiased estimate of the model’s ability to make predictions on new data. In Section 6.1, we compare Nested Factorization and the set of alternative models in terms of their predictive fit on the held-out test sample of data.

However, this notion of predictive performance on held-out data does not evaluate the ability of a model to make causal predictions of what “would” happen if we took actions that changed the distribution of the data. For example, a model trained to predict the demand for hotel rooms, might correctly identify that hotels are often full when prices are high and have many empty rooms when prices are low. This, however, may be due to hotels setting prices in expectation of demand, rather than because consumers prefer to pay high prices. Such a model could be highly predictive of hotel demand based on a randomly selected held-out test set (which is drawn from data generated under the existing data generating process), however such a model would perform poorly at predicting what prices a hotel ought to charge (since changing prices will change the data generating process). It is concerns about such endogeneity of prices343434As discussed in Rossi [2014], with consumer level data, our biggest concern for the identification of price effects, is that the store may be setting prices in response to variations in expected demand caused by seasonal trends or advertising. For example, there is more demand for fresh berries when they are in season or for turkeys immediately before Thanksgiving. It is not always clear which direction such price endogeneity will bias our estimates. The retailer may decide to take advantage of high demand by raising prices, but in other cases we see prices reduced during high demand periods e.g. bags of candy going on sale before Halloween. that motivates our identification approach that relies on focusing on data immediately before and after price changes (Tuesdays and Wednesdays), including weekly time controls (which can absorb any seasonal/holiday trends), including a indicator variable for Wednesdays (to absorb any consistent differences in Tuesday vs Wednesday demand), and excluding data from the weeks of major US Holidays. Since all models include the weekly controls at the category level, they all have the ability to predict average demand in a week at that level. However, in weeks with price changes, only a model that has accurately estimated consumer preferences about price can account for which day within the week is expected to have more purchases.

To validate the ability to make predictions about counterfactuals, we focus on three types of changes that can occur during a week for a particular product: (a) change in the price of the product (b) a change in the price of a different product in the same category and (c) another item in the category going into or out of stock. If the identifying assumptions353535i.e. that controlling for week and day of week effects at the category level is sufficient to make potential demand orthogonal to price level and product availability. of our models hold, then we can think of each of these events as a small sources of quasi-experimental variation. While the outcomes of each of these quasi-experiments is likely to be noisy, we can improve the precision of our estimates by averaging across a large number of them.

In Section 6.2, we compare the log likelihoods of the individual household level predictions during weeks in which one of these “counterfactuals” occurs in order to evaluate how well each model is able to make predictions that capture the change in predicted demand before and after the change (relative to the week-level average captured by the weekly time controls). In addition, we also compare the ability of each model to make predictions about the change in aggregate demand from Tuesday to Wednesday during weeks in which one of these events occurs. Our test set holds out data at the household-week level; this allows us to estimate overall consumer preferences and test our ability to predict household purchases on trips that were excluded from the training data, and in particular in weeks where the week-category effect estimated using other consumers’ purchases in that week is insufficient to predict the average probability of consumers purchasing on a particular day of the week (since prices differ across days). We use select hyperparameters (tune the model) using only validation set data from item-weeks with price changes, and we evaluate performance in the test set based on the three changes (a)-(c) outlined above.

In Section 6.3, we further evaluate the performance of our model at making predictions in scenarios of interest for counterfactual inference. We compare models in terms of their ability to capture heterogeneity in preferences across the population of households and evaluate the degree to which the predicted heterogeneity is predictive of actual behavior in the held-out test set. For example, we compare the predictions made for households who in the training data sample never purchased a particular UPC or have made no purchases at all from an entire product category. Among this group of “never buyers”, we show that the Nested Factorization model is able to correctly predict which of these households are relatively more or less likely to make a purchase in the held-out test data.

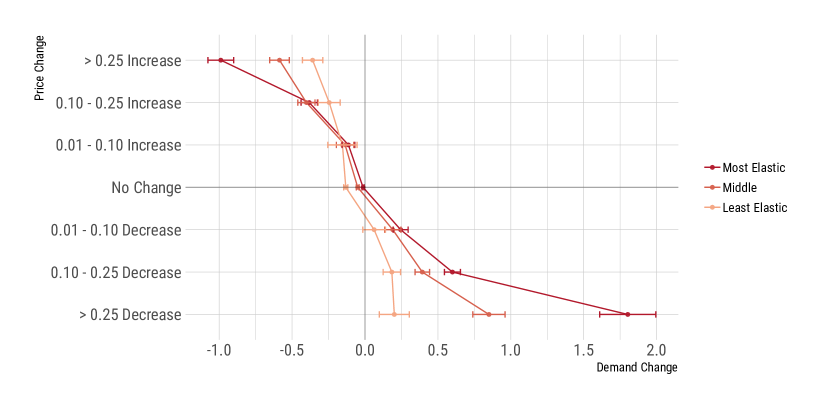

Section 6.4 examines the estimated own-price and cross-price elasticities. Finally, Section 6.5 looks at the potential for targeted marketing efforts that are personalized based on the rich heterogeneity estimated by the Nested Factorization model.

6.1 Predictive Fit

| Mean Log Likelihood | Mean Squared Error | |||

|---|---|---|---|---|

| Model | Train | Test | Train | Test |

| Nested Factorization | -4.2271 | -4.9096 | 0.8981 | 0.9268 |

| Mixed Logit with Random Price and HPF Controls | -4.9233 | -5.3125 | 0.9473 | 0.9660 |

| Nested Logit with HPF Controls | -5.2345 | -5.4230 | 0.9583 | 0.9650 |

| Multinomial Logit with HPF Controls | -5.2307 | -5.4248 | 0.9583 | 0.9651 |

| Mixed Logit with Random Price and Demographics | -5.2976 | -5.5690 | 0.9780 | 0.9898 |

| Mixed Logit with Random Price and Random Intercepts | -5.3956 | -5.5827 | 0.9785 | 0.9849 |

| Nested Logit with Demographic Controls | -5.6080 | -5.6779 | 0.9788 | 0.9801 |

| Multinomial Logit with Demographic Controls | -5.6142 | -5.6791 | 0.9791 | 0.9803 |

In Table 1, we compare the predictive fits of each of the models.363636Mean Log Likelihood and Mean Squared Error are calculated by dividing by the total number of purchases in order to make the values comparable between the test and training sets. Comparing the overall predictive accuracy across all models, the Nested Factorization model has the highest likelihood and the lowest sum of squared errors among all models on both the training data and the held-out test sample. In addition, each of the models that include HPF controls373737i.e. user-item specific covariates that are estimated from the HPF model run on all categories simultaneously as described in Section 4.2.5 perform better than the models that use control only for demographics.383838These trends also hold in additional specifications of the alternative logit models that included controls for shopping frequency and previous purchase behavior.

6.1.1 Comparison of Predictive Fit by Category

We can also compare how each model performs relative to the NF model at the level of individual categories. In Table 2, we calculate the relative rank of each model’s performance in the test set separately for each category. The Nested Factorization model has the highest log likelihood in 86% of categories and the lowest squared error in 96%. This demonstrates the effectiveness of learning preferences simultaneously across many product categories. Even if we were only interested in understanding consumer preferences in one particular category, e.g. yogurt, it can be effective to train a model using the data from other categories as well, either using the full Nested Factorization model or by using the HPF controls, which also consistently improve predictive performance on the held-out test data in most categories.

| Mean Rank | % Best Performance | |||

|---|---|---|---|---|

| Model | Log L | SE | Log L | SE |

| Nested Factorization | 1.53 | 1.10 | 86.2% | 95.9% |

| Mixed Logit with Random Price and HPF Controls | 2.40 | 5.33 | 9.8% | 0.8% |

| Nested Logit with HPF Controls | 3.87 | 3.38 | 0.0% | 0.8% |

| Multinomial Logit with HPF Controls | 4.21 | 3.63 | 0.8% | 0.8% |

| Mixed Logit with Random Price and Random Intercepts | 4.69 | 5.65 | 0.8% | 1.6% |

| Mixed Logit with Random Price and Demographics | 5.21 | 7.07 | 2.4% | 0.0% |

| Nested Logit with Demographic Controls | 6.96 | 4.93 | 0.0% | 0.0% |

| Multinomial Logit with Demographic Controls | 7.13 | 4.91 | 0.0% | 0.0% |

Mean rank is calculated as the average across product categories of the rank ordering of models based on predictive fit, with rank 1 corresponding to the model with the lowest error.

6.1.2 Comparison of Fits by Household and UPC

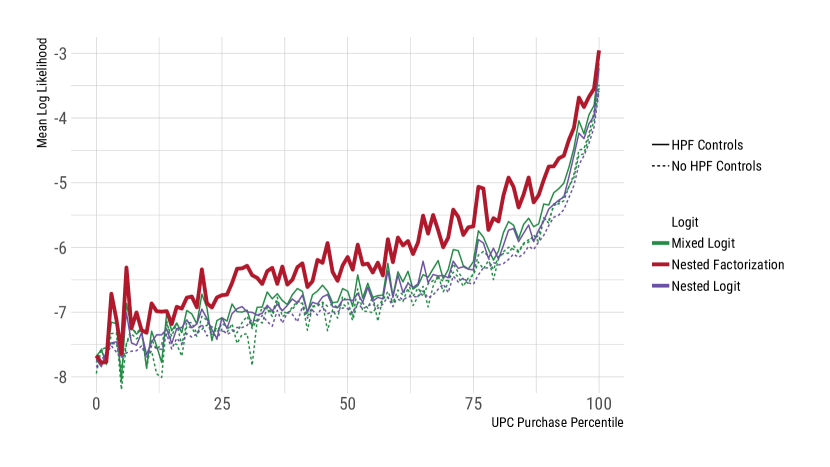

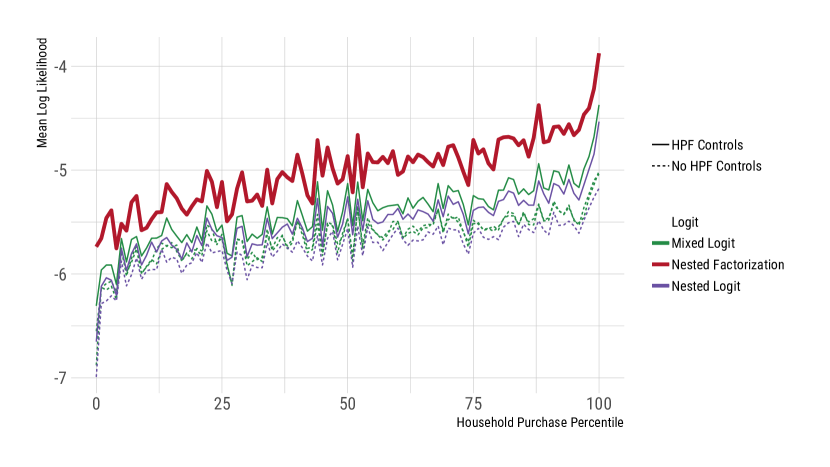

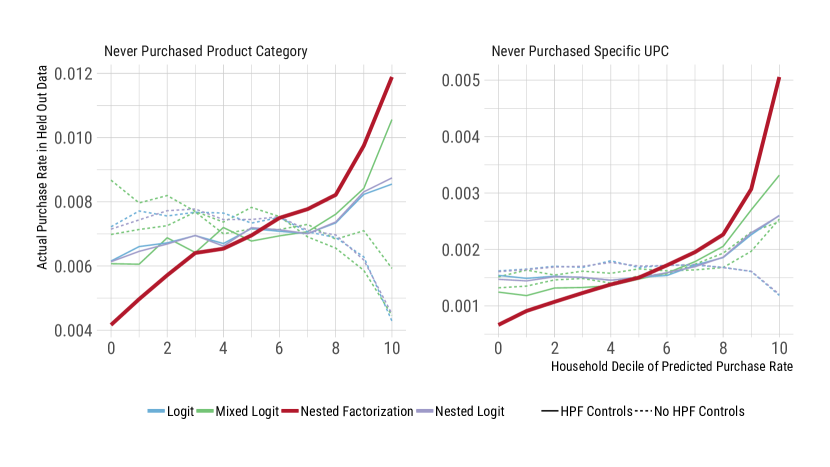

To help understand where the improvement in predictive performance is coming from, we can spit the results by the popularity of the products or by the shopping frequency of the households. In Figure 4, we can see that all models are more accurate in their predictions for the more commonly purchased UPCs (percentile 100) than for the less common items. Across all percentiles, the Nested Factorization model does consistently better than the alternative models. The models that use HPF effects (solid lines) have much smaller, but consistent gains over the nested and mixed logit models that use demographic or behavioral controls. Similar trends can be seen when we divide the results based on the number of purchases each household made in the training data in Figure 4. This suggests the benefits from a latent-factorization-based approach are relatively uniform across households and products.

6.2 Price Change and Availability Counterfactuals

In the economics and marketing literatures, models of consumer demand are used to make inferences about what would happen if change were made to a market. For example, such models have been used to predict what would happen if prices were changed, if products are added or removed from a market, or if competing firms in the market were to merge. As discussed in Section 6, evaluating the predictive fit of a model, even when done on a held-out test sample, does not reliably determine whether a model can be used to make predictions under counterfactual states of the world such as these. To evaluate the ability to make predictions under changes to prices or product availability, we focus on each model’s predictions on held-out test set data immediately before and after such changes occur. Under the assumption that these changes are exogenous conditional on our week and weekday controls, we can think of each of these changes as a miniature experiment. By pooling across many such small noisy experiments, we can increase our precision in detecting differences in performance. We focus on three types of changes that can occur between Tuesday and Wednesday for a particular UPC. First, we look at weeks in which the focal product’s price changes, which we can think of as evaluating the accuracy of the model’s own-price elasticity estimates. Second, we look at weeks in which some other product in the focal product’s category has a price change, in order to evaluate the predicted cross-price elasticities. Finally, we look at weeks in which some other product in the focal product’s category goes into or out of stock, which is another measure of the patterns of substitution between products.393939In all cases we exclude weeks in which the focal product is out-of-stock on either day. For the cross-price and out-of-stock counterfactuals, we exclude weeks in which the focal product has a price change. For the price change counterfactuals, we exclude weeks in which the magnitude of the price change is less than We asses fit on the test data using three measures. The first measure is the mean log likelihood of the individual household level predictions for product weeks that experienced the corresponding counterfactual event. The second and third measure compare the actual aggregate demand to the predicted aggregate demand across all households in the test set who shopped during the corresponding weeks. For products that are purchased at least 2.5 times on average per day, we calculate the likelihood of the Tuesday to Wednesday change in aggregate demand as approximated by a Skellam distribution.404040If the individual purchasing decisions are distributed as independent Bernoulli variables, then their sum, the aggregate demand has a Poisson distribution. Then the Tuesday-Wednesday change in aggregate demand has a Skellam distribution, which is the difference between two independent Poisson distributions For less popular products, we calculate the likelihood of observing aggregate demand greater than zero, which we approximate with a Bernoulli distribution whose mean is the sum of the household level predictions.

| Individual | Aggregate | |||

| Model | Popular | Less Common | Popular | Less Common |

| All Weeks | ||||

| Nested Factorization | -0.1070 (0.0004) | -0.0173 (0.0001) | -2.5356 (0.0146) | -1.3072 (0.0044) |

| Mixed Logit with Random Price and HPF Controls | -0.1156 (0.0004) | -0.0188 (0.0001) | -2.5562 (0.0145) | -1.3365 (0.0037) |

| Nested Logit with HPF Controls | -0.1194 (0.0005) | -0.0191 (0.0001) | -2.5568 (0.0154) | -1.3105 (0.0040) |

| Multinomial Logit with HPF Controls | -0.1194 (0.0005) | -0.0191 (0.0001) | -2.5554 (0.0154) | -1.3086 (0.0040) |

| Mixed Logit with Random Price and Random Intercepts | -0.1263 (0.0005) | -0.0194 (0.0001) | -2.5712 (0.0146) | -1.3316 (0.0037) |

| Mixed Logit with Random Price and Demographics | -0.1240 (0.0004) | -0.0195 (0.0001) | -2.5934 (0.0153) | -1.3543 (0.0038) |

| Multinomial Logit with Demographic Controls | -0.1290 (0.0005) | -0.0197 (0.0001) | -2.5722 (0.0157) | -1.3105 (0.0040) |

| Nested Logit with Demographic Controls | -0.1289 (0.0005) | -0.0197 (0.0001) | -2.5740 (0.0157) | -1.3113 (0.0041) |

| Cross Price Weeks | ||||

| Nested Factorization | -0.0925 (0.0008) | -0.0149 (0.0001) | -2.4527 (0.0262) | -1.2017 (0.0084) |

| Mixed Logit with Random Price and HPF Controls | -0.1006 (0.0008) | -0.0163 (0.0001) | -2.4846 (0.0258) | -1.2584 (0.0069) |

| Nested Logit with HPF Controls | -0.1041 (0.0009) | -0.0164 (0.0001) | -2.4844 (0.0277) | -1.2177 (0.0076) |

| Multinomial Logit with HPF Controls | -0.1041 (0.0009) | -0.0164 (0.0001) | -2.4836 (0.0276) | -1.2165 (0.0076) |

| Mixed Logit with Random Price and Random Intercepts | -0.1139 (0.0009) | -0.0168 (0.0001) | -2.5002 (0.0260) | -1.2527 (0.0069) |

| Mixed Logit with Random Price and Demographics | -0.1111 (0.0009) | -0.0170 (0.0001) | -2.5132 (0.0280) | -1.2752 (0.0071) |

| Multinomial Logit with Demographic Controls | -0.1162 (0.0010) | -0.0170 (0.0001) | -2.4966 (0.0279) | -1.2182 (0.0077) |

| Nested Logit with Demographic Controls | -0.1161 (0.0010) | -0.0170 (0.0001) | -2.5066 (0.0292) | -1.2194 (0.0078) |

| Own Price Weeks | ||||

| Nested Factorization | -0.1374 (0.0009) | -0.0229 (0.0001) | -2.7871 (0.0360) | -1.5544 (0.0104) |

| Mixed Logit with Random Price and HPF Controls | -0.1465 (0.0009) | -0.0243 (0.0001) | -2.8004 (0.0357) | -1.5475 (0.0086) |

| Nested Logit with HPF Controls | -0.1493 (0.0009) | -0.0249 (0.0001) | -2.7986 (0.0371) | -1.5356 (0.0092) |

| Multinomial Logit with HPF Controls | -0.1493 (0.0009) | -0.0249 (0.0001) | -2.7949 (0.0373) | -1.5321 (0.0092) |

| Mixed Logit with Random Price and Random Intercepts | -0.1530 (0.0009) | -0.0251 (0.0001) | -2.8003 (0.0348) | -1.5408 (0.0085) |

| Mixed Logit with Random Price and Demographics | -0.1525 (0.0009) | -0.0251 (0.0001) | -2.8544 (0.0374) | -1.5709 (0.0090) |

| Multinomial Logit with Demographic Controls | -0.1557 (0.0010) | -0.0256 (0.0002) | -2.8097 (0.0369) | -1.5344 (0.0092) |

| Nested Logit with Demographic Controls | -0.1555 (0.0010) | -0.0256 (0.0002) | -2.8186 (0.0372) | -1.5377 (0.0093) |

| Out of Stock Weeks | ||||

| Nested Factorization | -0.0924 (0.0040) | -0.0159 (0.0002) | -2.3349 (0.1114) | -1.2746 (0.0129) |

| Mixed Logit with Random Price and HPF Controls | -0.1033 (0.0044) | -0.0173 (0.0002) | -2.3679 (0.1225) | -1.3064 (0.0111) |

| Nested Logit with HPF Controls | -0.1068 (0.0046) | -0.0176 (0.0002) | -2.3427 (0.1243) | -1.2817 (0.0122) |

| Multinomial Logit with HPF Controls | -0.1068 (0.0046) | -0.0176 (0.0002) | -2.3446 (0.1259) | -1.2774 (0.0121) |

| Mixed Logit with Random Price and Demographics | -0.1091 (0.0045) | -0.0180 (0.0002) | -2.3669 (0.1132) | -1.3249 (0.0118) |

| Mixed Logit with Random Price and Random Intercepts | -0.1125 (0.0046) | -0.0181 (0.0002) | -2.3403 (0.1156) | -1.3068 (0.0113) |

| Multinomial Logit with Demographic Controls | -0.1146 (0.0048) | -0.0183 (0.0002) | -2.3261 (0.1189) | -1.2800 (0.0122) |

| Nested Logit with Demographic Controls | -0.1145 (0.0047) | -0.0183 (0.0002) | -2.2974 (0.0990) | -1.2840 (0.0123) |

6.3 Comparison of Degree of Personalization across Households

To examine the extent to which each of these models is able to flexibly model the differences in preferences between households, we calculate two measures of the degree of “personalization” of the predicted purchase rates that each model predicts for each household. First, we compare the coefficient of variation of a models predictions at the UPC level and the category level.414141Coefficient of variation is defined as As a second measure, we regress the predicted purchase rate on the actual purchase rate in the in the held-out test sample.424242The coefficients are from a regression of actual purchase rate on the predicted purchase rate (both calculated on the test set) with item/category specific fixed effects to absorb heterogeneity in the mean purchase rates across items/categories.

Table 4 shows that the Nested Factorization model has the largest variation in the predictions across households and that this variation is strongly correlated with variation in the actual purchase rates in the held-out test data. For each increase in the Nested Factorization model’s prediction of a household’s purchase for a UPC, the household’s actual purchase rate in the test set increases by .

| Coef. of Variation | Regression Coef. | |||

|---|---|---|---|---|

| Model | UPC | Category | UPC | Category |

| Nested Factorization | 3.2546 | 1.7756 | 0.9955 | 1.0023 |

| Mixed Logit with Random Price and HPF Controls | 2.0747 | 1.6085 | 0.6861 | 0.7007 |

| Mixed Logit with Random Price and Demographics | 1.3869 | 1.5724 | 0.4718 | 0.5968 |

| Multinomial Logit with HPF Controls | 1.2590 | 0.7276 | 0.8402 | 0.8893 |

| Nested Logit with HPF Controls | 1.2368 | 0.7520 | 0.8417 | 0.8725 |

| Mixed Logit with Random Price and Random Intercepts | 1.0834 | 1.0446 | 0.4666 | 0.6959 |

| Nested Logit with Demographic Controls | 0.4465 | 0.2967 | 0.8947 | 0.9314 |

| Multinomial Logit with Demographic Controls | 0.4337 | 0.2756 | 0.9077 | 0.9411 |

6.3.1 Predicting Preference for Products a Household has Not Yet Purchased