On the Convergence of SARAH and Beyond

Abstract

The main theme of this work is a unifying algorithm, LoopLess SARAH (L2S) for problems formulated as summation of individual loss functions. L2S broadens a recently developed variance reduction method known as SARAH. To find an -accurate solution, L2S enjoys a complexity of for strongly convex problems. For convex problems, when adopting an -dependent step size, the complexity of L2S is ; while for more frequently adopted -independent step size, the complexity is . Distinct from SARAH, our theoretical findings support an -independent step size in convex problems without extra assumptions. For nonconvex problems, the complexity of L2S is . Our numerical tests on neural networks suggest that L2S can have better generalization properties than SARAH. Along with L2S, our side results include the linear convergence of the last iteration for SARAH in strongly convex problems.

1 Introduction

Consider the frequently encountered empirical risk minimization (ERM) problem

| (1) |

where is the parameter to be learned from data; the set collects data indices; and, is the loss function corresponding to datum . Suppose that the set of minimizers is non-empty and is bounded from below.

The standard method to solve (1) is gradient descent (GD), which per iteration relies on the update

where is the step size (a.k.a learning rate). For a strongly convex , GD convergences linearly to , meaning after iterations it holds that with some constant ; while for convex it holds that , and for nonconvex one has ; see e.g., (Nesterov, 2004; Ghadimi and Lan, 2013). However, finding per iteration in the big data regime, i.e., with large , can be computationally prohibitive. To cope with this, the stochastic gradient descent (SGD) (Robbins and Monro, 1951; Bottou et al., 2016) draws uniformly at random an index per iteration, and updates via

Albeit computationally light, SGD comes with a slower convergence rate than GD (Bottou et al., 2016; Ghadimi and Lan, 2013), which is mainly due to the variance of the gradient estimate given by .

By capitalizing on the finite sum structure of ERM, a class of algorithms, variance reduction family, can be designed to solve (1) more efficiently. The idea is to judiciously (often periodically) evaluate a snapshot gradient , and use it as an anchor of the stochastic draws in subsequent iterations. As a result, compared with the simple gradient estimate in SGD, the variance of estimated gradients can be reduced. Members of the variance reduction family include SDCA (Shalev-Shwartz and Zhang, 2013), SVRG (Johnson and Zhang, 2013; Reddi et al., 2016a; Allen-Zhu and Hazan, 2016), SAG (Roux et al., 2012), SAGA (Defazio et al., 2014; Reddi et al., 2016b), MISO (Mairal, 2013), SCSG (Lei and Jordan, 2017; Lei et al., 2017), SNVRG (Zhou et al., 2018) and SARAH (Nguyen et al., 2017, 2019), and their variants (Konecnỳ and Richtárik, 2013; Kovalev et al., 2019; Qian et al., 2019; Li et al., 2019). Most of these rely on the update , where is a constant step size and is a carefully designed gradient estimator that takes advantage of the snapshot gradient. When aiming for an accurate solution, variance reduction methods are faster than SGD for convex and nonconvex problems, and remarkably they converge linearly when is strongly convex. The complexity of algorithms such as GD, SGD, and variance reduction families will be quantified by the number of incremental first-order oracle (IFO) calls that counts how many (incremental) gradients are computed (Agarwal and Bottou, 2015), as specified next using our notational conventions.

Definition 1.

An IFO is a black box with inputs and , and output the gradient .

For example, the IFO complexity to compute is . For a prescribed , a desirable algorithm obtains an -accurate solution (defined as follows) with minimal complexity111Complexity is the abbreviation for IFO complexity throughout this work..

Definition 2.

Let be a solution returned by certain algorithm. If is satisfied, is termed as an -accurate solution to (1).

Variance reduction algorithms outperform GD in terms of complexity. And when high accuracy ( small) is desired, the complexity of variance reduction methods is also lower than that of SGD. Among variance reduction algorithms, the distinct feature of SARAH (Nguyen et al., 2017, 2019) and its variants (Fang et al., 2018; Zhang et al., 2018; Wang et al., 2018; Nguyen et al., 2018a; Pham et al., 2019) is that they rely on a biased gradient estimator formed by recursively using stochastic gradients. SARAH performs comparably to SVRG/SAGA on strongly convex problems, but reduces the complexity of SVRG/SAGA for nonconvex losses. In addition, no duality (as in SDCA) or gradient table (for SAGA) is required. With SARAH’s analytical and practical merits granted, there are unexplored issues. For example, guarantees on SARAH with -independent step size for convex problems are missing since analysis in (Nguyen et al., 2017) requires an extra presumption. The last iteration convergence of SARAH is also not well studied yet. In this context, our contributions are summarized next.

-

•

Unifying algorithm and novel analysis: A new algorithm, LoopLess SARAH (L2S) is developed. It offers a unified algorithmic framework with provable convergence properties through a novel analyzing technique. To find an -accurate solution, L2S enjoys a complexity for strongly convex problems with condition number . For convex problems, the complexity of L2S is when an -related step size is used; or for an -independent step size. The complexity of L2S for nonconvex problems is .

-

•

Tale of generalization: Supported by experimental evidence, we find that L2S can have generalization merits compared with SARAH for nonconvex tasks such as training neural networks.

-

•

Last iteration convergence of SARAH: Linear convergence of the last iteration for SARAH on -strongly convex problems is established. Distinct from (Liu et al., ) with step size , our analysis enables a much larger step size, i.e., . In addition, we find that if each is strongly convex, the complexity of adopting last iteration in SARAH is lower than that of SVRG.

Notation. Bold lowercase letters denote column vectors; represents expectation (probability); stands for the -norm of a vector ; and denotes the inner product between vectors and .

2 Preliminaries

This section reviews SARAH (Nguyen et al., 2017, 2019) with emphases on the quality of gradient estimates. Before diving into SARAH, we first state the assumptions posed on and .

Assumption 1.

Each has -Lipchitz gradient, that is, .

Assumption 2.

Each is convex.

Assumption 3.

is -strongly convex, meaning there exists , so that .

Assumption 4.

Each is -strongly convex, meaning there exists , so that .

Assumptions 1 – 4 are standard in the analysis of variance reduction algorithms. Assumption 1 requires each loss function to be sufficiently smooth. In fact one can distinguish the smoothness of individual loss function and refine Assumption 1 as has -Lipchitz gradient. Clearly . With slight modifications on SARAH, such refinement can tighten the complexity bounds slightly. The detailed discussions can be found in Appendix E. In the main text, we will keep using the simpler Assumption 1 for clarity. Assumption 2 implies that is also convex. Assumption 3 only requires to be strongly convex, which is slightly weaker than Assumption 4. And it is clear when Assumption 4 is true, both Assumptions 2 and 3 hold automatically. Under Assumptions 1 and 3 (or 4), the condition number of is defined as .

2.1 Recap of SARAH

SARAH for Strongly Convex Problems: The detailed steps of SARAH are listed under Alg. 1. In a particular outer loop (lines 3 - 11) indexed by , a snapshot gradient is computed first to serve as an anchor of gradient estimates in the ensuing inner loop (lines 6 - 10). Then is updated times based on

| (2) |

SARAH’s gradient estimator is biased, since , where denotes the -algebra generated by . Albeit biased, is carefully designed to ensure the mean square error (MSE) relative to is bounded above, and stays proportional to .

This MSE bound of Lemma 1 is critical for analyzing SARAH, and instrumental in establishing its linear convergence for strongly convex . It is worth stressing that the step size of SARAH should be chosen by to ensure convergence, which can be larger than that of SVRG, whose step size should be less than .

SARAH for Convex Problems: Establishing the convergence rate of SARAH with an -independent step size remains open for convex problems. Regarding complexity, the only analysis implicitly assumes SARAH to be non-divergent, as confirmed by the following claim used to derive the complexity.

Claim: (Nguyen et al., 2017, Theorem 3) If , , , and , it holds that .

The missing piece of this claim is that for a finite or , must be bounded; or equivalently, the algorithm must be assumed non-divergent. Even if is finite, assuming it to be as in (Nguyen et al., 2017) is not reasonable. Another variant of SARAH in (Nguyen et al., 2018b) also relies on a similar assumption to guarantee convergence. We will show that the proposed algorithm can bypass this extra non-divergent assumption.

SARAH for Nonconvex Problems. SARAH also works for nonconvex problems if line 11 in Alg. 1 is modified to . The key to convergence again lies in the MSE of .

Lemma 2 states that the upper bound of MSE of is i) proportional to ; and, ii) larger when is larger. Leveraging the MSE bound, it was established that the complexity to find an -accurate solution is (Nguyen et al., 2019). Compared with SARAH, the proposed algorithm has its own merits for tasks such as training neural network, which will be clear in Section 4.

3 Loopless SARAH

This section presents the LoopLess SARAH (L2S) algorithmic framework, which is capable of dealing with (strongly) convex and nonconcex ERM problems.

L2S is summarized in Alg. 2. Besides the single loop structure, the most distinct feature of L2S is that is a probabilistically computed snapshot gradient given by

| (3) |

where is again uniformly sampled. The gradient estimator is still biased, since . In L2S, the snapshot gradient is computed every iterations in expectation, while SARAH computes the snapshot gradient once every updates. The emergent challenge is that one has to ensure a small MSE of to guarantee convergence, where the difficulty arises from the randomness of when a snapshot gradient is computed.

An equivalent manner to describe (3) is through a sequence of i.i.d. Bernoulli random variables with pmf

| (4) |

If , a snapshot gradient is computed; otherwise, the estimated gradient is used for the update. Let denote the event that at iteration the last evaluated snapshot gradient was at . In other words, is equivalent to . Note that can take values from (no snapshot gradient computed) to (corresponding to ).

The key lemma enabling our analysis is a simple probabilistic observation.

Lemma 3.

For a given , i) events and are disjoint when ; and, ii) .

The general idea is to exploit these properties of to obtain the MSE of , which is further leveraged to derive the convergence of L2S. Note that our idea for establishing the convergence of L2S is general enough to provide a parallel analysis for a loopless version of SVRG (Kovalev et al., 2019; Qian et al., 2019), without relying on the complicated Lyapunov function.

3.1 L2S for Convex Problems

The subject of this subsection is problems with smooth and convex losses such as those obeying Assumptions 1 and 2. We find that SARAH is challenged analytically because in Line 11 of Alg. 1, which necessitates SARAH’s ‘non-divergent’ assumption. A few works have identified this issue (Nguyen et al., 2019; Wang et al., 2018; Pham et al., 2019), but require an -dependent step size (e.g., ) to address it222These algorithms are designed for nonconvex problems, however, even assuming convexity we are unable to show the convergence with a step size independent with .. However, -independent step sizes are also widely adopted in practice. The key to bypassing this -dependence in step size, is removing the inner loop of SARAH and computing snapshot gradients following a random schedule as (3).

The analysis starts with the MSE of in L2S. All proofs are relegated to Appendix due to space limitations.

Lemma 4.

Comparing (5) with Lemma 1 reveals that conditioning on , in L2S is similar to the starting point of an outer loop in SARAH (i.e., ), while the following iterations mimic the behavior of SARAH’s inner loop. Taking expectation w.r.t. in (5), Lemma 4 further asserts that the MSE of depends on the exponentially moving average of the norm square of past gradients.

Theorem 1.

The constant depends on the choice of , e.g., for . Based on Theorem 1, the convergence rates as well as the complexities under different choices of and are specified in the following corollaries. Let us start with a constant step size that is irrelevant with .

Corollary 1.

Choose a constant . If , then L2S has convergence rate and requires IFO calls to find an -accurate solution.

Corollary 2.

Choose a constant . If , the convergence rate of L2S is . The complexity to ensure an -accurate solution is .

In Corollaries 1 and 2, the choice of does not depend on . Thus, relative to SARAH, L2S eliminates the non-divergence assumption and establishes the convergence rate as well. On the other hand, an -dependent step size is also supported by L2S, whose complexity is specified in the following corollary.

Corollary 3.

If we select , and , then L2S has convergence rate , and the complexity to find an -accurate solution is .

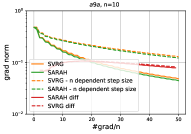

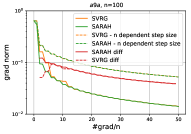

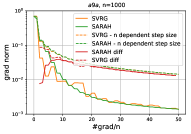

When to Adopt -dependent Step Sizes? An interesting observation is that though the complexity of using an -dependent step size is lower than those of an -independent step size in both L2S and SVRG (Reddi et al., 2016a), the numerical performances on modern datasets such as rcv1 and a9a suggest that -independent step sizes boost the convergence speed. We argue that an -dependent step size only reveals its numerical merits when is extremely large. Intuitively, a large positively correlates with the larger MSE of the gradient estimate, which in turn calls for a smaller (-dependent) step size. Our numerical results in Appendix D.3 also support this argument. We subsample aforementioned datasets with different values of . SVRG and L2S are tested on these subsampled datasets. Besides the faster convergence when using an -independent step size, it is also observed that as increases, i) the gradient norm of solutions obtained by -dependent step sizes becomes smaller; and ii) the difference on the performance gap between -dependent and -independent step sizes reduces.

3.2 L2S for Nonconvex Problems

The scope of L2S can also be broadened to nonconvex problems under Assumption 1, that is, L2S with a proper step size is guaranteed to use IFO calls to find an -accurate solution. Compared with SARAH, the merit of L2S is that the extra MSE introduced by the randomized scheduling of snapshot gradient computation can be helpful for exploring the landscape of the loss function, which will be discussed in detail in Section 4. Here we focus on the convergence properties only, starting with the MSE in nonconvex settings.

Lemma 5.

If Assumption 1 holds, L2S guarantees that for a given

| (6) |

In addition, the following inequality is true

Conditioning on , iterations are comparable to an outer loop of SARAH. Similar to Lemma 2, the MSE upper bound of in (6) is large when is large. If we take expectation w.r.t. the randomness of , the MSE of then depends on the exponentially moving average of the norm square of all past gradient estimates , which is different from Lemma 4 (for convex problems) where the MSE involves the past gradients . It turns out that such a past-estimate-based MSE is difficult to cope with using only the exponentially deceasing sequence , prompting a cautiously designed (-dependent) .

Theorem 2.

With Assumption 1 holding, and choosing , the final L2S output satisfies

An intuitive explanation of the -dependent is that with a small , L2S evaluates a snapshot gradient more frequently [cf. (3)], which translates to a relatively small MSE bound in Lemma 5. Given an accurate gradient estimate, it is thus reasonable to adopt a larger step size.

Corollary 4.

Selecting and , L2S converges with rate , and the complexity to find an -accurate solution is .

3.3 L2S for Strongly Convex Problems

In addition to convex and nonconvex problems, a modified version of L2S that we term L2S for Strongly Convex problems (L2S-SC), converges linearly under Assumptions 1 – 3. As we have seen previously, L2S is closely related to SARAH, especially when conditioned on a given . Hence, we will first state a useful property of SARAH that will guide the design and analysis of L2S-SC.

Lemma 6.

Consider SARAH (Alg. 1) with Line 11 replaced by . Choosing and large enough such that

where is defined as

| (7) |

The modified SARAH is guaranteed to converge linearly; that is,

As opposed to the random draw of (Line 11 of Alg. 1), Lemma 6 asserts that by properly choosing and , setting preserves the linear convergence of SARAH. Note that the convergence with last iteration of SARAH was also studied by (Liu et al., ) under Assumptions 1 – 3. However, their analysis requires an undesirably small step size, i.e., , while ours enables a much larger one .

Remark 1.

Through Lemma 6 one can establish the complexity of SARAH with . When Assumptions 1 - 3 hold, the complexity is , which is on the same order of SVRG with last iteration (Tan et al., 2016; Hu et al., 2018). However, when Assumptions 1 and 4 are true, the complexity of SARAH decreases to . This is the property SVRG does not exhibit.

L2S-SC is summarized in Alg. 3, where obtained in Lines 5 - 11 is a rewrite of (3) using introduced in (4) for the ease of presentation and analysis. L2S-SC differs from L2S in that when , steps back slightly as in Line 7. This "step back" is to allow for a rigorous analysis, and can be viewed as the counterpart of choosing instead of as in Lemma 6. Omitting Line 7 in practice does not deteriorate performance. In addition, the parameter required to initialize L2S is comparable to the number of outer loops of SARAH, as one can also validate through the dependence in the linear convergence rate.

The complexities of L2S-SC under different assumptions are established in the next corollaries.

Corollary 5.

4 Discussions

4.1 Comparison with SCSG

L2S can be viewed as SARAH with variable inner loop length. A variant of SVRG (abbreviated as SCSG) with randomized inner loop length has been also developed in (Lei and Jordan, 2017, 2019). A close relative of SCSG is a loopless version of SVRG (Kovalev et al., 2019; Qian et al., 2019). Unfortunately, the analysis in (Kovalev et al., 2019) is confined to strongly convex problems, while (Qian et al., 2019) relies on different analyzing schemes that are more involved. The key differences between L2S and SCSG are as follows.

d1) The random inner loop length of SCSG is assumed geometrically distributed (at least for the analysis) that could be even infinite. Thus, its total number of iterations is also random. In contrast, the total number of L2S iterations is fixed to . This is accomplished through a non-geometrically distributed equivalent inner loop length.

d2) The analyses are also different. From a high level, SCSG employs a “forward” analysis, where an iteration that computes a snapshot gradient is fixed first, and then future iterations , till the computation of the next snapshot gradient are checked; while our analysis takes the “backward” route, that is, after fixing an iteration the past iterations are checked for a snapshot gradient computation. As a consequence, our “backward” analysis leads to an exponentially moving average structure in the MSE (Lemmas 4 and 5), which is insightful, and is not provided by SCSG.

4.2 Generalization Merits of L2S

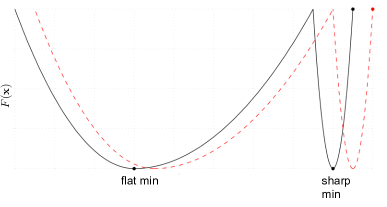

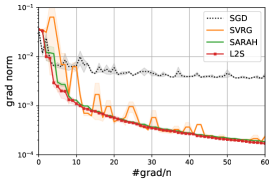

SARAH has well-documented merits for its complexity for nonconvex problems, but similar to other variance reduction algorithms, it is not as successful as expected for training neural networks. We conjecture this is related with the reduced MSE of the gradient estimates. To see this, although there is no consensus on analytical justification for this, empirical evidence points out that SGD with large mini-batch size (needed to reduce the variance of the gradient estimates) tends to converge to a sharp minimum. Sharp minima are believed to have worse generalization properties compared with flat ones (Keskar et al., 2016). Fig. 1 shows that gradient estimators with pronounced variability are more agile to explore the space and escape from a sharp minimum, while flat minima are more tolerant to larger variability. This suggests that the gradient estimator could be designed to control its exploration ability, which can in turn improve generalization. Being able to explore the loss function landscape is critical because deepening and widening a neural network does not always endow the stochastic gradient estimator with controllable exploration ability (Defazio and Bottou, 2018).

These empirical results shed light on the important role of exploration ability in the gradient estimates. A natural means of controlling this exploration in algorithms with variance reduction, is to add zero-mean noise in the gradient estimates. However, the issue is that even for convex problems, the convergence rate slows down if the noise is not carefully calibrated; see e.g. (Kulunchakov and Mairal, 2019). Carefully designed noises for escaping saddle points rather than generalization merits were studied in e.g., (Jin et al., 2017; Fang et al., 2019). But even for saddle point escaping, extra information of the loss landscape, e.g., Hessian Lipchitz constant is required for obtaining the variance of injected noise. Unfortunately, the Hessian Lipchitz constant is not always available in advance. To control the exploration ability of algorithms with variance reduction, L2S resorts to randomized snapshot gradient computation that is free of extra knowledge for the loss landscape.

With SARAH as a reference, we can see how our randomized snapshot gradient computation in L2S can benefit variability for exploration. Let denote the equivalent length of a L2S inner loop, where and are the indices of two consecutive iterations when snapshot gradients are computed. Recall from Lemma 2 that the MSE of tends to be larger as approaches . Relative to SARAH, this means that the randomized computation of the snapshot gradient increases the MSE when it so happens that .

|

|

| (a) | (b) |

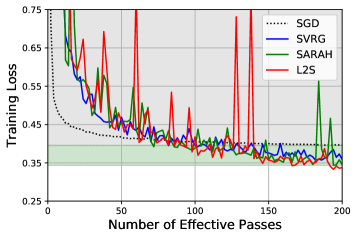

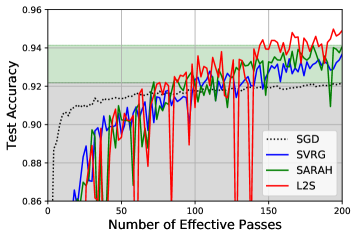

Test of L2S on Neural Networks. We perform classification on MNIST dataset333Online available at http://yann.lecun.com/exdb/mnist/ using a feedforward neural network with sigmoid activation function. The network is trained for epochs and the training loss and test accuracy are plotted in Fig. 2. The bound of gray shadowed area indicates the smallest training loss (highest test accuracy) of SGD, while the bound of green shadowed area represents the best performances for SARAH. Figs. 2 (a) and (b) share some common patterns: i) SGD converges much faster in the initial phase compared with variance reduced algorithms; ii) the fluctuate of L2S is larger than that of SARAH, implying the randomized full gradient computation indeed introduces extra chances for exploration; and, iii) when x-axis is around , L2S begins to outperform SARAH while in previous epochs their performances are comparable. Note that before L2S outperforms SARAH, there is a deep drop on its accuracy. This can be explained as that L2S explores for a local minimum with generalization merits thanks to the randomized snapshot gradient computation and the deep drop in Fig. 2 (b) indicates the transition from a local min to another.

5 Numerical Tests

Besides training neural networks, we also apply L2S to logistic regression to showcase the performances in strongly convex and convex cases. Specifically, consider the loss function

| (8) |

where is the (feature, label) pair of datum . Problem (8) can be rewritten in the format of (1) with . One can verify that in this case Assumptions 1 and 4 are satisfied. Datasets a9a, w7a and rcv1.binary444All datasets are from LIBSVM, which is online available at https://www.csie.ntu.edu.tw/~cjlin/libsvmtools/datasets/binary.html. are used in numerical tests presented. Details regarding the datasets and implementation are deferred to Appendix F.

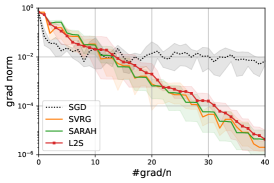

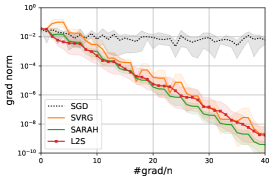

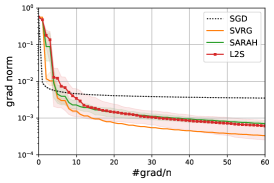

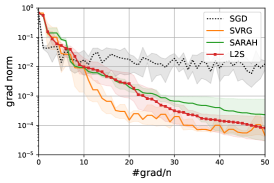

Test of L2S-SC on Strongly Convex Problems. The performance of L2S-SC is shown in the first row of Fig. 3. SVRG, SARAH and SGD are chosen as benchmarks, where SGD is with modified step size on the -th effective sample pass. For both SARAH and SVRG, the length of inner loop is chosen as . We tune step size and only report the best performance. For a fair comparison we set and for L2S the same as SARAH. It can be seen that on datasets w7a and rcv1 L2S-SC has comparable performances with SARAH, while on dataset a9a, L2S-SC has similar performance with SARAH. The simulations validate the theoretical results of L2S-SC.

Test of L2S on Convex Problems. The performances of L2S for convex problems () is listed in the second row of Fig. 3. Again SVRG, SARAH and SGD are adopted as benchmarks. We choose for SVRG, SARAH and L2S. It can be seen that on datasets w7a and rcv1 L2S performs almost the same as SARAH, while outperforms SARAH on dataset a9a. Note that the performance of SVRG improves over SARAH on certain datasets. This is because a theoretically unsupported step size () is used in SVRG for best empirical performance.

|

|

|

|

|

|

| (a) w7a | (b) a9a | (c) rcv1 |

6 Conclusions and Future Work

A unifying framework, L2S, was introduced to efficiently solve (strongly) convex and nonconvex ERM problems. The complexities to find an -accurate solution were established. Numerical tests validated our theoretical findings.

An interesting question is how to extend L2S and SARAH to stochastic optimization, i.e., solving , where is a random variable whose distribution is unknown. Such problems can be addressed using SVRG or SCSG; see e.g., (Lei et al., 2017). Works such as (Nguyen et al., 2018b) is the first attempt for solving stochastic optimization via SARAH. Though addressing certain challenges, the remaining issue is that the gradient estimate is in general not implementable on problems other than ERM. To see this, recall the SARAH based gradient estimate for stochastic optimization is , where is the -th realization of . Obtaining via a stochastic first order oracle can be impossible especially when comes from an unknown continuous probability space. To overcome this challenge is included in our research agenda.

References

- Agarwal and Bottou [2015] Alekh Agarwal and Leon Bottou. A lower bound for the optimization of finite sums. In Proc. Intl. Conf. on Machine Learning, pages 78–86, Lille, France, 2015.

- Allen-Zhu and Hazan [2016] Zeyuan Allen-Zhu and Elad Hazan. Variance reduction for faster non-convex optimization. In Proc. Intl. Conf. on Machine Learning, pages 699–707, New York City, NY, 2016.

- Bottou et al. [2016] Léon Bottou, Frank E Curtis, and Jorge Nocedal. Optimization methods for large-scale machine learning. arXiv preprint arXiv:1606.04838, 2016.

- Defazio and Bottou [2018] Aaron Defazio and Léon Bottou. On the ineffectiveness of variance reduced optimization for deep learning. arXiv preprint arXiv:1812.04529, 2018.

- Defazio et al. [2014] Aaron Defazio, Francis Bach, and Simon Lacoste-Julien. SAGA: A fast incremental gradient method with support for non-strongly convex composite objectives. In Proc. Advances in Neural Info. Process. Syst., pages 1646–1654, Montreal, Canada, 2014.

- Fang et al. [2018] Cong Fang, Chris Junchi Li, Zhouchen Lin, and Tong Zhang. Spider: Near-optimal non-convex optimization via stochastic path-integrated differential estimator. In Proc. Advances in Neural Info. Process. Syst., pages 687–697, Montreal, Canada, 2018.

- Fang et al. [2019] Cong Fang, Zhouchen Lin, and Tong Zhang. Sharp analysis for nonconvex sgd escaping from saddle points. arXiv preprint arXiv:1902.00247, 2019.

- Ghadimi and Lan [2013] Saeed Ghadimi and Guanghui Lan. Stochastic first-and zeroth-order methods for nonconvex stochastic programming. SIAM Journal on Optimization, 23(4):2341–2368, 2013.

- Gubner [2006] John A Gubner. Probability and random processes for electrical and computer engineers. Cambridge University Press, 2006.

- Hu et al. [2018] Bin Hu, Stephen Wright, and Laurent Lessard. Dissipativity theory for accelerating stochastic variance reduction: A unified analysis of svrg and katyusha using semidefinite programs. arXiv preprint arXiv:1806.03677, 2018.

- Jin et al. [2017] Chi Jin, Rong Ge, Praneeth Netrapalli, Sham M Kakade, and Michael I Jordan. How to escape saddle points efficiently. In Proc. Intl. Conf. on Machine Learning, pages 1724–1732, 2017.

- Johnson and Zhang [2013] Rie Johnson and Tong Zhang. Accelerating stochastic gradient descent using predictive variance reduction. In Proc. Advances in Neural Info. Process. Syst., pages 315–323, Lake Tahoe, Nevada, 2013.

- Keskar et al. [2016] Nitish Shirish Keskar, Dheevatsa Mudigere, Jorge Nocedal, Mikhail Smelyanskiy, and Ping Tak Peter Tang. On large-batch training for deep learning: Generalization gap and sharp minima. arXiv preprint arXiv:1609.04836, 2016.

- Konecnỳ and Richtárik [2013] Jakub Konecnỳ and Peter Richtárik. Semi-stochastic gradient descent methods. arXiv preprint arXiv:1312.1666, 2013.

- Kovalev et al. [2019] Dmitry Kovalev, Samuel Horvath, and Peter Richtarik. Don’t jump through hoops and remove those loops: SVRG and Katyusha are better without the outer loop. arXiv preprint arXiv:1901.08689, 2019.

- Kulunchakov and Mairal [2019] Andrei Kulunchakov and Julien Mairal. Estimate sequences for variance-reduced stochastic composite optimization. arXiv preprint arXiv:1905.02374, 2019.

- Lei and Jordan [2017] Lihua Lei and Michael Jordan. Less than a single pass: Stochastically controlled stochastic gradient. In Proc. Intl. Conf. on Artificial Intelligence and Statistics, pages 148–156, Fort Lauderdale, Florida, 2017.

- Lei and Jordan [2019] Lihua Lei and Michael I Jordan. On the adaptivity of stochastic gradient-based optimization. arXiv preprint arXiv:1904.04480, 2019.

- Lei et al. [2017] Lihua Lei, Cheng Ju, Jianbo Chen, and Michael I Jordan. Non-convex finite-sum optimization via scsg methods. In Proc. Advances in Neural Info. Process. Syst., pages 2348–2358, 2017.

- Li et al. [2019] Bingcong Li, Lingda Wang, and Georgios B Giannakis. Almost tune-free variance reduction. arXiv preprint arXiv:1908.09345, 2019.

- [21] Yan Liu, Congying Han, and Tiande Guo. A class of stochastic variance reduced methods with an adaptive stepsize. URL http://www.optimization-online.org/DB_FILE/2019/04/7170.pdf.

- Mairal [2013] Julien Mairal. Optimization with first-order surrogate functions. In Proc. Intl. Conf. on Machine Learning, pages 783–791, Atlanta, 2013.

- Nesterov [2004] Yurii Nesterov. Introductory lectures on convex optimization: A basic course, volume 87. Springer Science & Business Media, 2004.

- Nguyen et al. [2017] Lam M Nguyen, Jie Liu, Katya Scheinberg, and Martin Takáč. SARAH: A novel method for machine learning problems using stochastic recursive gradient. In Proc. Intl. Conf. Machine Learning, Sydney, Australia, 2017.

- Nguyen et al. [2018a] Lam M Nguyen, Katya Scheinberg, and Martin Takáč. Inexact sarah algorithm for stochastic optimization. arXiv preprint arXiv:1811.10105, 2018a.

- Nguyen et al. [2018b] Lam M Nguyen, Katya Scheinberg, and Martin Takáč. Inexact sarah algorithm for stochastic optimization. arXiv preprint arXiv:1811.10105, 2018b.

- Nguyen et al. [2019] Lam M Nguyen, Marten van Dijk, Dzung T Phan, Phuong Ha Nguyen, Tsui-Wei Weng, and Jayant R Kalagnanam. Optimal finite-sum smooth non-convex optimization with SARAH. arXiv preprint arXiv:1901.07648, 2019.

- Pham et al. [2019] Nhan H Pham, Lam M Nguyen, Dzung T Phan, and Quoc Tran-Dinh. ProxSARAH: An efficient algorithmic framework for stochastic composite nonconvex optimization. arXiv preprint arXiv:1902.05679, 2019.

- Qian et al. [2019] Xun Qian, Zheng Qu, and Peter Richtarik. L-SVRG and L-Katyusha with arbitrary sampling. arXiv preprint arXiv:1901.08689, 2019.

- Reddi et al. [2016a] Sashank J Reddi, Ahmed Hefny, Suvrit Sra, Barnabas Poczos, and Alex Smola. Stochastic variance reduction for nonconvex optimization. In Proc. Intl. Conf. on Machine Learning, pages 314–323, New York City, NY, 2016a.

- Reddi et al. [2016b] Sashank J Reddi, Suvrit Sra, Barnabás Póczos, and Alex Smola. Fast incremental method for nonconvex optimization. arXiv preprint arXiv:1603.06159, 2016b.

- Robbins and Monro [1951] Herbert Robbins and Sutton Monro. A stochastic approximation method. The annals of mathematical statistics, pages 400–407, 1951.

- Roux et al. [2012] Nicolas L Roux, Mark Schmidt, and Francis R Bach. A stochastic gradient method with an exponential convergence rate for finite training sets. In Proc. Advances in Neural Info. Process. Syst., pages 2663–2671, Lake Tahoe, Nevada, 2012.

- Shalev-Shwartz and Zhang [2013] Shai Shalev-Shwartz and Tong Zhang. Stochastic dual coordinate ascent methods for regularized loss minimization. volume 14, pages 567–599, 2013.

- Tan et al. [2016] Conghui Tan, Shiqian Ma, Yu-Hong Dai, and Yuqiu Qian. Barzilai-Borwein step size for stochastic gradient descent. In Proc. Advances in Neural Info. Process. Syst., pages 685–693, 2016.

- Wang et al. [2018] Zhe Wang, Kaiyi Ji, Yi Zhou, Yingbin Liang, and Vahid Tarokh. SpiderBoost: A class of faster variance-reduced algorithms for nonconvex optimization. arXiv preprint arXiv:1810.10690, 2018.

- Zhang et al. [2018] Jingzhao Zhang, Hongyi Zhang, and Suvrit Sra. R-spider: A fast riemannian stochastic optimization algorithm with curvature independent rate. arXiv preprint arXiv:1811.04194, 2018.

- Zhou et al. [2018] Dongruo Zhou, Pan Xu, and Quanquan Gu. Stochastic nested variance reduction for nonconvex optimization. In Proc. Advances in Neural Info. Process. Syst., pages 3925–3936, 2018.

Appendix

Appendix A Useful Lemmas and Facts

Lemma 7.

[Nesterov, 2004, Theorem 2.1.5]. If is convex and has -Lipschitz gradient, then the following inequalities are true

| (9a) | |||

| (9b) | |||

| (9c) |

Note that inequality (9a) does not require the convexity of .

Lemma 8.

[Nesterov, 2004]. If is -strongly convex and has -Lipschitz gradient, with , the following inequalities are true

| (10a) | |||

| (10b) | |||

| (10c) | |||

| (10d) |

Proof.

Proof of Lemma 3:

Proof.

If , and are disjoint by definition, since the most recent calculated snapshot gradient can only appear at either or . Since are i.i.d., one can find the probability of as

| (11) |

Hence one can verify that

which completes the proof. ∎

Appendix B Technical Proofs in Section 3.1

B.1 Proof of Lemma 4

The following lemmas are needed for the proof.

Lemma 9.

The following equation is true for

Proof.

Consider that

| (12) |

where the last equation is because . We can expand using the same argument. Note that we have , which suggests

Then taking expectation w.r.t. and expanding in (B.1), the proof is completed. ∎

Proof of Lemma 4: The implication of this Lemma 3 is that law of total probability [Gubner, 2006] holds. Specifically, for a random variable that happens in iteration , the following equation holds

| (13) |

Now we turn to prove Lemma 4. To start with, consider that when

where (a) follows from (2) and the update ; and (b) is the result of (9c). Then by choosing such that , i.e., , we have

| (14) |

Plugging (14) into Lemma 9, we have

where the last equation is because conditioning on , . Note that when , this inequality automatically holds since the LHS equals to . Because the randomness of is irrelevant to (thus ), after taking expectation w.r.t. , we have

which proves the first part of Lemma 4.

B.2 Proof of Theorem 1

Following Assumption 1, we have

| (15) |

where the last equation is because . Rearranging the terms, we arrive at

where the last inequality holds since . Taking expectation and summing over , we have

where (a) is the result of Lemma 4; (b) is by changing the order of summation, and ; and, (c) is again by . Rearranging the terms and dividing both sides by , we have

| (16) |

Finally, since , we have

| (17) |

where the last inequality follows from . Hence we have , which is applied to (B.2) to have

Now if we choose such that with being a positive constant, then we have

B.3 Proof of Corollaries 1 and 2

From Theorem 1, it is clear that upon choosing , we have . This means that iterations are needed to guarantee .

Per iteration requires IFO calls in expectation. And IFO calls are required when computing .

Combining these facts together, we have that if . And the IFO complexity is .

Similarly, if , we have . And the IFO complexity in this case becomes .

B.4 Proof of Corollary 3

From Theorem 1, it is clear that with a large , choosing leads to . Thus we have . This translates to the need of iterations to guarantee .

Choosing , we have . And the number of IFO calls is .

Appendix C Technical Proofs in Section 3.2

Using the Bernoulli random variable introduced in (4), L2S (Alg. 2) can be rewritten in an equivalent form as Alg. 4.

Recall that a known is equivalent to . Now we are ready to prove Lemma 5.

C.1 Proof of Lemma 5

It can be seen that Lemma 9 still holds for nonconvex problems, thus we have

| (18) |

where the last inequality follows from Assumption 1 and . The first part of this lemma is thus proved. Next, we have

where (a) is by Lemma 3 (or law of total probability) and ; (b) is obtained by plugging (C.1) in; (c) is established by changing the order of summation; (d) is again by Lemma 3 (or law of total probability); and (e) is because of the independence of and when , that is, . To be more precise, given , the randomness of comes from and , thus is independent with .

C.2 Proof of Theorem 2

Following the same steps of (B.2) in Theorem 1, we have

Taking expectation and summing over , we have

| (19) |

where (a) is by Lemma 5; (b) holds when ; and (c) is by exchanging the order of summation and . Upon choosing such that , i.e., , we can eliminate the last term in (C.2). Plugging in and dividing both sides by , we arrive at

where (d) is because when , which we have already seen from (B.2). The proof is thus completed.

C.3 Proof of Corollary 5

From Theorem 2, choosing , we have . This means that iterations are required to ensure .

Per iteration it takes in expectation IFO calls. And IFO calls are required for computing

Hence choosing , the IFO complexity is .

Appendix D Technical Proofs in Section 3.3

D.1 Proof of Lemma 6

We borrow the following lemmas from [Nguyen et al., 2017] and summarize them below.

Lemma 10.

Lemma 11.

Now we are ready to prove Lemma 6.

Case 1: Assumptions 1 – 3 hold. Following Assumption 1, we have

| (20) |

The derivation is exactly the same as (B.2), so we do not repeat it here. Rearranging the terms and dividing both sides with , we have

where (a) follows from the convexity of ; (b) uses Young’s inequality with to be specified later. Since , rearranging the terms we have

Choosing , we have

| (21) |

Then, taking expectation w.r.t. , applying Lemma 1 to and Lemma 10 to , with we have

Multiplying both sides by completes the proof.

D.2 Proof of Theorem 3

We will only analyze case 1 where Assumptions 1 – 3 hold. The other case where Assumptions 1 and 4 are true can be analyzed in the same manner.

For analysis, let sequence , be the iteration indices where ( is automatically contained since at the beginning of L2S-SC, is calculated). For a given sequence , it can be seen that due to the step back in Line 7 of Alg. 3, plays the role of the starting point of an inner loop of SARAH; while is analogous to of SARAH’s inner loop. Define and

| (22) |

Using similar arguments of Lemma 6, when , it is guaranteed to have

| (23) |

For convenience, let us define

Note that choosing properly we can have . Now it can be seen that

Note that this inequality is irrelevant with . Thus if we further take expectation w.r.t. , we arrive at

| (24) |

Plugging (24) into (22) we have

Note that the randomness of comes from , which is the length of the interval between the calculation of two snapshot gradient. Since for positive integers and , it can be seen are mutually independent, which further leads to the mutual independence of . Therefore, taking expectation w.r.t. on both sides of (D.2), we have

which completes the proof.

D.3 When to Use An -dependent Step Size in Convex Problems

|

|

|

|

|

|

|

|

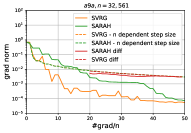

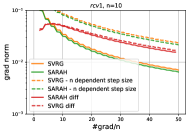

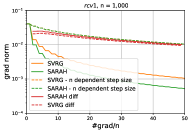

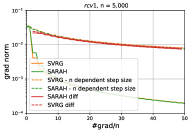

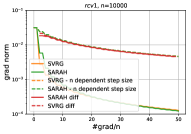

We perform SVRG and SARAH with -dependent/independent step sizes to solve logistic regression problems on subsampled rcv1 and a9a. The results can be found in Fig. 4. It can be seen that -independent step sizes perform better than those of -dependent step sizes in all the tests. In addition, as increases, i) the gradient norm of solutions obtained via -dependent step sizes becomes smaller; and ii) the performance gap between -dependent and -independent step sizes reduces. These observations suggest -dependent step sizes can reveal their merits when is extremely large (at least it should be larger than the size of a9a, which is ).

Appendix E Boosting the Practical Merits of SARAH

Assumption 5.

Each has -Lipchitz gradient, and has -Lipchitz gradient; that is, , and .

This section presents a simple yet effective variant of SARAH to enable a larger step size. The improvement stems from making use of the data dependent in Assumption 5. The resultant algorithm that we term Data Dependent SARAH (D2S) is summarized in Alg. 5. For simplicity D2S is developed based on SARAH, but it generalizes to L2S as well.

Intuitively, each provides a distinct gradient to be used in the updates. The insight here is that if one could quantify the “importance” of (or the gradient it provides), those more important ones should be used more frequently. Formally, our idea is to draw of outer loop according to a probability mass vector , where . With , D2S boils down to SARAH.

Ideally, finding should rely on the estimation error as optimality crietrion. Specifically, we wish to minimize in Lemma 1. Writing the expectation explicitly, the problem can be posed as

| (25) |

where the denotes the optimal solution. Though finding out via (25) is optimal, it is intractable to implement because and for all must be computed, which is even more expensive than computing itself. However, (25) implies that a larger probability should be assigned to those whose gradients on and change drastically. The intuition behind this observation is that a more abrupt change of the gradient suggests a larger residual to be optimized. Thus, in (25) can be approximated by its upper bound , which inaccurately captures gradient changes. The resultant problem and its optimal solution are

| (26) |

Choosing according to (26) is computationally attractive not only because it eliminates the need to compute gradients, but also because is usually cheap to obtain in practice (at least for linear and logistic regression losses). Knowing is critical for SARAH [Nguyen et al., 2017]; hence, finding only introduces negligible overhead compared to SARAH. Accounting for , the gradient estimator is also modified to an importance sampling based one to compensate for those less frequently sampled

| (27) |

Note that is still biased, since . As asserted next, with as in (26) and computed via (27), D2S indeed improves SARAH’s convergence rate.

Theorem 4.

Compared with SARAH’s linear convergence rate [Nguyen et al., 2017], the improvement on the convergence constant is twofold: i) if and are chosen the same in D2S and SARAH, it always holds that , which implies D2S converges faster than SARAH; and ii) the step size can be chosen more aggressively with , while the standard SARAH step size has to be less than . The improvements are further corroborated in terms of the number of IFO calls, especially for ERM problems that are ill-conditioned.

E.1 Optimal Solution of (25)

E.2 Proof of Theorem 4

The proof generalizes the original proof of SARAH for strongly convex problems [Nguyen et al., 2017, Theorem 2]. Notice that the importance sampling based gradient estimator enables the fact . By exploring this fact, it is not hard to see that the following lemmas hold. The proof has almost the same steps as those in [Nguyen et al., 2017], except for the expectation now is w.r.t. a nonuniform distribution .

Lemma 12.

[Nguyen et al., 2017, Lemma 1] In any outer loop , if , we have

Lemma 13.

The following equation is true

Lemma 14.

In any outer loop , if is chosen to satisfy , we have

Proof.

E.3 Proof of Corollary 7

Appendix F Numerical Experiments

Experiments for (strongly) convex cases are performed using python 3.7 on an Intel i7-4790CPU @3.60 GHz (32 GB RAM) desktop. The details of the used datasets are summarized in Table 1. The smoothness parameter can be calculated via by checking the Hessian matrix.

| Dataset | (train) | density | (test) | |||

|---|---|---|---|---|---|---|

| a9a | ||||||

| rcv1 | ||||||

| w7a |

L2S. Since we are considering the convex case, we set in (8). SVRG, SARAH and SGD are chosen as benchmarks, where SGD is modified with step size on the -th epoch. For both SARAH and SVRG, the length of inner loop is chosen as . For a fair comparison, we use the same for L2S [cf. (3)]. The step sizes of SARAH and SVRG are selected from and those with best performances are reported. Note that the SVRG theory only effects when . The step size of L2S is the same as that of SARAH for fairness.

L2S-SC. The parameters are chosen in the same manner as the test of L2S.

L2S for on Nononvex Problems We perform classification on MNIST dataset using a feedforward neural network through Pytorch. The activation function used in hidden layer is sigmoid. SGD, SVRG, and SARAH are adopted as benchmarks. In all tested algorithms the batch sizes are . The step size of SGD is , where is the index of epoch; the step size is chosen as for SVRG [Reddi et al., 2016a]; and the step sizes are for SARAH [Nguyen et al., 2019] and L2S. The inner loop lengths are selected to be for SVRG and SARAH, while the same is used for L2S.