Robustness and Tractability for Non-convex M-estimators

Abstract

We investigate two important properties of M-estimator, namely, robustness and tractability, in linear regression setting, when the observations are contaminated by some arbitrary outliers. Specifically, robustness means the statistical property that the estimator should always be close to the underlying true parameters regardless of the distribution of the outliers, and tractability indicates the computational property that the estimator can be computed efficiently, even if the objective function of the M-estimator is non-convex. In this article, by learning the landscape of the empirical risk, we show that under mild conditions, many M-estimators enjoy nice robustness and tractability properties simultaneously, when the percentage of outliers is small. We further extend our analysis to the high-dimensional setting, where the number of parameters is greater than the number of samples, , and prove that when the proportion of outliers is small, the penalized M-estimators with penalty will enjoy robustness and tractability simultaneously. Our research provides an analytic approach to see the effects of outliers and tuning parameters on the robustness and tractability for some families of M-estimators. Simulation and case study are presented to illustrate the usefulness of our theoretical results for M-estimators under Welsch’s exponential squared loss.

Keywords: computational tractability, gross error, high-dimensionality, non-convexity,robust regression, sparsity

1 Introduction

M-estimation plays an important role in linear regression due to its robustness and flexibility. From the statistical viewpoint, it has been shown that many M-estimators enjoy desirable robustness properties in the presence of outliers, as well as asymptotic normality when the data are normally distributed without outliers. Some general theoretical properties and review of robust M-estimators can be found in Bai et al., (1992); Huber and Ronchetti, (2009); Cheng et al., (2010); Hampel et al., (2011); El Karoui et al., (2013). In the high-dimensional setting, where the dimensionality is greater than the number of samples, penalized M-estimators have been widely used to tackle the challenges of outliers and have been used for sparse recovery and variable selection, see Lambert-Lacroix and Zwald, (2011); Li et al., (2011); Wang et al., (2013); Loh, (2017). However, from the computational tractability perspective, it is often not easy to compute the M-estimators, since optimization problems over non-convex loss functions are usually involved. Moreover, the tractability issue may become more challenging when the data are contaminated by some arbitrary outliers, which is essentially the situation where robust M-estimator is designed to tackle.

This paper aims to investigate two important properties of M-estimators, robustness and tractability, simultaneously under the gross error model. Specifically, we assume the data generation model is where , for , and the noise term ’s are from Huber’s gross error model (Huber,, 1964): , for . Here, denotes the probability density function (pdf) of the noise of the normal samples, which has the desirable properties, such as zero mean and finite variance; denotes the pdf of the outliers (contaminations), which may also depend on the explanatory variable , for . One thing to notice is that we do not require the mean of to be The parameter , denotes the percentage of the contaminations, which is also known as the contamination ratio in robust statistics literature. The gross error model indicates that for the sample, the residual term is generated from the pdf with probability and from the pdf with probability It is important to point out that the residual is independent of and other ’s when it is from the pdf but can be dependent with the variable when it is from the pdf

In the first part of this paper, we start with the low-dimensional case when the dimension is fixed. We consider the robust M-estimation with a constraint on the norm of . Mathematically, we study the following optimization problem:

| (1) | |||

Here, is the loss function, and is often non-convex. We consider the problem with the constraint due to three reasons: first, it is well know the constrainted optimization problem in (1) is equivalent to the unconstrained optimization problem with a regularizer. Therefore, it is related to the Ridge regression, which can alleviate multicollinearity amongst regression predictors. Second, by considering the problem of (1) in a compact ball with radius it guarantees the existence of the global optimal, which is necessary for establishing the tractability properties of the M-estimator. Finally, by working on the constrained optimization problem, we can avoid technical complications and establish the uniform convergence theorems of the empirical risk and population risk. Besides, the constrained M-estimators are widely used and studied in the literature, see Geyer et al., (1994); Mei et al., (2018); Loh, (2017) for more details. To be consistent with the assumptions used in the literature, in the current work, we assume is a constant and the true parameter is inside of the ball.

In the second part, we extend our research to the high-dimensional case, where and the true parameter is sparse. In order to achieve the sparsity in the resulting estimator, we consider the penalized M-estimator with the regularizer:

| (2) | |||

Note the corresponding penalized M-estimator with the constraint is related to the Elastic net, which overcomes the limitations of the LASSO type regularization (Zou and Hastie,, 2005).

In both parts, we will show that (in the finite sample setting,) the M-estimator obtained from (1) or (2) is robust in the sense that all stationary points of empirical risk function or are bounded in the neighborhood of the true parameter when the proportion of outliers is small. In addition, we will show that with a high probability, there is a unique stationary point of the empirical risk function, which is the global minimizer of (1) or (2) for some general (possibly nonconvex) loss functions . This implies that the M-estimator can be computed efficiently. To illustrate our general theoretical results, we study some specific M-estimators with Huber’s loss (Huber,, 1964) and Welsch’s exponential squared loss (Dennis Jr and Welsch,, 1978), and explicitly discuss how the tuning parameter and percentage of outliers affect the robustness and tractability of the corresponding M-estimators.

Our research makes several fundamental contributions on the field of robust statistics and non-convex optimization. First, we demonstrate the uniform convergence results for the gradient and Hessian of the empirical risk to the population risk under the gross error model. Second, we provide nonasymptotic upper bound of the estimation error for the general M-estimators, which nearly achieve the minimax error bound in Chen et al., (2016). Third, we investigate the computational tractability of the general non-convex M-estimators under the gross error model and show when the contamination ratio is small, there is only one unique stationary point of the empirical risk function. Therefore, efficient algorithms such as gradient descent or proximal gradient decent can be guaranteed to converge to a unique global minimizer irrespective of the initialization. Our general results also imply the following interesting and to some extent surprising statement: the percentage of outliers has an impact on the tractability of non-convex M-estimators. In a nutshell, the estimation and the corresponding optimization problem become more difficult both in terms of solution quality and computational efficiency when more outliers appear. While the former is well expected, we find the latter – that more outliers make M-estimators more difficult to numerically compute – an interesting and somewhat surprising discovery. Our simulation results and case study also verify this phenomenon.

Related works

Since Huber’s pioneer work on robust M-estimators (Huber,, 1964), many M-estimators with different choices of loss functions have been proposed, e.g., Huber’s loss (Huber,, 1964), Andrew s sine loss (Andrews et al.,, 1972), Tukey’s Bisquare loss (Beaton and Tukey,, 1974), Welsch’s exponential squared loss (Dennis Jr and Welsch,, 1978), to name a few. From the statistical perspective, much research has been done to investigate the robustness of M-estimators such as large breakdown point (Donoho and Huber,, 1983; Mizera and Müller,, 1999; Alfons et al.,, 2013), finite influent function (Hampel et al.,, 2011) and asymptotic normality (Maronna and Yohai,, 1981; Lehmann and Casella,, 2006; El Karoui et al.,, 2013). Recently, in the high-dimensional context, regularized M-estimators have received a lot of attentions. Lambert-Lacroix and Zwald, (2011) proposed a robust variable selection method by combing Huber’s loss and adaptive lasso penalty. Li et al., (2011) show the nonconcave penalized M-estimation method can perform parameter estimation and variable selection simultaneously. Welsch’s exponential squared loss combined with adaptive lasso penalty is used by Wang et al., (2013) to construct a robust estimator for sparse estimation and variable selection. Chang et al., (2018) proposed a robust estimator by combining the Tukey’s biweight loss with adaptive lasso penalty. Loh and Wainwright, (2015) proved that under mild conditions, any stationary point of the non-convex objective function will close to the underlying true parameters. However, those statistical works did not discuss the computational tractability of the M-estimators even though many of these loss functions are non-convex.

During the last several years, non-convex optimization has attracted fast growing interests due to its ubiquitous applications in machine learning and in particular deep learning, such as dictionary learning (Mairal et al.,, 2009), phase retrieval (Candes et al.,, 2015), orthogonal tensor decomposition (Anandkumar et al.,, 2014) and training deep neural networks (Bengio,, 2009). It is well known that there is no efficient algorithm that can guarantee to find the global optimal solution for general non-convex optimization.

Fortunately, in the context of estimating non-convex M-estimators for high-dimensional linear regression (without outliers), under some mild statistical assumptions, Loh, (2017) establishes the uniqueness of the stationary point of the non-convex M-estimator when using some non-convex bounded regularizers instead of regularizer. By investigating the uniform convergence of gradient and Hessian of the empirical risk, Mei et al., (2018) prove that with a high probability, there exists one unique stationary point of the regularized empirical risk function with regularizer. Thus regardless of the initial points, many computational efficient algorithm such as gradient descent or proximal gradient descent algorithm could be applied and are guaranteed to converge to the global optimizer, which implies the high tractability of the M-estimator. However, their analysis is restricted to the standard linear regression setting without outliers. In particular, they assume the distribution of the noise terms in the linear regression model should have some desirable properties such as zero mean, sub-gaussian and independent of feature vector , which might not hold when the data are contaminated with outliers. To the best of our knowledge, no research has been done on analyzing the computational tractability properties of the non-convex M-estimators when data are contaminated by arbitrary outliers, although the very reason why M-estimators are proposed is to handle outliers in linear regression in the robust statistics literature. Our research is the first to fill the significant gap on the tractability of non-convex M-estimators. We prove that under mild assumptions, many M-estimators can tolerate a small amount of arbitrary outliers in the sense of keeping the tractability, even if the loss functions are non-convex.

Notations. Given their standard inner product is defined by The norm of a vector is denoted by The by identity matrix is denoted by Given a matrix let denote the largest and the smallest eigenvalue of , respectively. The operator norm of is denoted by which is equal to when Let , be the ball in the space with center and radius Given a random variable with probability density function we denote the corresponding expectation by We will often omit the density function subscript when it is clear from the context, the expectation is taken for all variables.

Organization. The rest of this article is organized as follows. In Section 2, we present the theorems about the robustness and tractability of general M-estimators under the low-dimensional setup when dimension is fixed and less than Then in Section 3, we consider the penalized M-estimator with regularizer in the high-dimensional regression when The error bounds of the estimation and the scenario when the M-estimator has nice tractability are provided. In Section 4, we discuss two special families of robust estimator constructed by Huber’s and Welsch’s exponential loss as examples to illustrate our general theorems of robustness and tractability of M-estimators. Simulation results are presented in Section 5 and a case study is shown in Section 6 to illustrate the robustness and tractability properties when the data are contaminated by outliers. Concluding remarks are given in Section 7. We relegate all proofs to the Appendix due to space limits.

2 M-estimators in the low-dimensional regime

In this section, we investigate two key properties of M-estimators, namely robustness and tractability, in the setting of linear regression with arbitrary outliers in the low-dimensional regime where the dimension is fixed and smaller than the number of samples . In terms of robustness, we show that under some mild conditions, any stationary point of the objective function in (1) will be well bounded in a neighborhood of the true parameter Moreover, the neighborhood shrinks when the proportion of outliers decreases. In terms of tractability, we show that when the proportion of outliers is small and the sample size is large, with a high probability, there is a unique stationary point of the empirical risk function, which is the global optimum (and hence the corresponding M-estimator). Consequently, many first order methods are guaranteed to converge to the global optimum, irrespective of initialization.

Before presenting our main theorems, we make the following mild assumptions on the loss function the explanatory or feature vectors , and the idealized noise distribution We define the score function

Assumption 1.

- (a)

-

The score function is twice differentiable and odd in with for all Moreover, we assume

- (b)

-

The feature vector are i.i.d with zero mean and -sub-Gaussain, that is , for all

- (c)

-

The feature vector spans all possible directions in that is , for some

- (d)

-

The idealized noise distribution is symmetric. Define and satisfies , for all and

Assumption (a) requires the smoothness of the loss function in the objective function, which is crucial to study the tractability of the estimation problem; Assumption (b) assumes the sub-Gaussian design of the observed feature matrix; Assumption (c) assumes that the covariance matrix of the feature vector is positive semidefinite. We remark that the condition on is mild. It is not difficult to show that it is satisfied if the idealized noise distribution is strictly positive for all and decreasing for e.g., if pdf of

Before presenting our main results in this section, we first define the population risk as follows:

| (3) |

The high level idea is to analyze the population risk first, and then we build a link between the population risk and the empirical risk, which solves the original estimation problem. Theorem 1 below summarizes the results for the population risk function in (3).

Theorem 1.

Assume that Assumption 1 holds and the true parameter satisfies

- (a)

-

There exists a constant such that any stationary point of satisfies where is the contamination ratio, and is a positive constant that only depends on and the pdf , but does not depend on the outlier pdf .

- (b)

-

When is small, there exist a constant where are two positive constants that only depend on and the pdf but not depend on the outlier pdf such that

(4) for every with .

- (c)

-

There is a unique stationary point of in the ball as long as for a given contamination ratio

It is useful to add some remarks for better understanding Theorem 1. First, recall that the noise term follows the gross error model: where the outlier pdf may also depend on While the true parameter may no longer be the stationary point of the population risk function Theorem 1 implies that the stationary points of will always bounded in a neighborhood of the true parameter when the percentage of contamination is small. This indicates the robustness of M-estimators in the population case.

Second, Theorem 1 asserts that when there are no outliers, i.e., the stationary point is indeed the true parameter In addition, since the constant in (a) is an increasing function of whereas the constant in (b) is a decreasing function of stationary points of may disperse from the true parameter and the strongly convex region around will be decreasing, as the contamination ratio is increasing. This indicates the difficulty of optimization for large contamination ratio cases.

Third, part (c) is a direct result from part (a) and (b). Note that thus there exists a positive such that for any A simple lower bound on is since whenever

Our next step is to link the empirical risk function (and the corresponding M-estimator) with the population version. To this end, we need the following lemma, which shows the global uniform convergence theorem of the sample gradient and Hessian.

Lemma 1.

Under Assumption 1, for any there exists a constant depending on but independent of and such that for any the following hold:

- (a)

-

The sample gradient converges uniformly to the population gradient in Euclidean norm, i.e., if we have

(5) - (b)

-

The sample Hessian converges uniformly to the population Hessian in operator norm, i.e., if we have

(6)

We are now ready to present our main result about M-estimators by investigating the empirical risk function

Theorem 2.

Assume Assumption 1 holds and Let us use the same notation and as in Theorem 1. Then for any , there exist constant depends on but independent of and , such that as the following statements hold with probability at least

- (a)

-

for all

(7) - (b)

-

for all

(8)

Thus, as long as has a unique stationary point, which lies in the ball This is the unique global optimal solution of (1), and denote this unique stationary point by .

- (c)

-

There exists a positive constant that depends on but independent of and , such that

(9)

A few remarks are in order. First, since is independent of and Theorem 2(a) asserts that the M-estimator which minimizes is always bounded in the ball regardless of (and hence the outliers observed). This indicates the robustness of the M-estimator, i.e., the estimates are not severely skewed by a small amount of “bad” outliers. Next, when the contamination ratio is small such that there is a unique stationary point of Therefore, although the original optimization problem (1) is non-convex and the sample contains some arbitrary outliers, the optimal solution of can be computed efficiently via most off-the-shelf first-order algorithms such as gradient descent or stochastic gradient descent. This indicates the tractability of the M-estimator. Interestingly, as in the population risk case, the tractability is closely related to the amount of outliers – the problem is easier to optimize when the data contains fewer outliers. Finally, when the number of samples the estimation error bound is as the order of which nearly achieves the minimax lower bound of in Chen et al., (2016).

3 Penalized M-estimator in the high-dimensional regime

In this section, we investigate the tractability and the robustness of the penalized M-estimator in the high-dimension region where the dimension of parameter is much greater than the number of samples Specifically, we consider the same data generation model where and the noise term are from Huber’s gross error model (Huber,, 1964): Moreover, we assume and the true parameter is sparse.

We consider the -regularized M-estimation under a -constraint on :

| (10) | |||

Before presenting our main theorem, we need additional assumptions on the feature vector

Assumption 2.

The feature vector has a probability density function in In addition, there exists constant that is independent of dimension such that almost sure.

The following lemma shows the uniform convergence of gradient and Hessian under the Huber’s contamination model in the high-dimensional setting where

Lemma 2.

Now we are ready for our main theorem.

Theorem 3.

The proof of Theorem 3 is based on several lemmas, which are postponed to the appendix. We believe that some of our lemmas are of interest in their own right. Theorem 3 implies the estimation error of the penalized M-estimator is bounded as the order of which achieves the minimax estimation rate (Chen et al.,, 2016). Moreover, it implies that the penalized M-estimator has good tractability when the percentage of outliers is small.

4 Example

In this section, we use some examples to illustrate our general theoretical results about the robustness and tractability of M-estimators. In the first subsection, we consider the low-dimensional regime and study a family of M-estimators with a specific loss function known as Huber’s loss (Huber,, 1964). In the second subsection, we consider the high-dimensional regime and study the penalized M-estimator with Welsch’s exponential squared loss (Dennis Jr and Welsch,, 1978; Rey,, 2012; Wang et al.,, 2013). In both subsections, we will derive the explicit expression of the two critical radius and discuss the robustness and tractability of the corresponding M-estimators.

4.1 M-estimator via Huber’s loss

In this subsection, we illustrate the general results presented in Section 2 by studying the Huber’s loss function (Huber,, 1964)

| (14) |

where is a tuning parameter. The corresponding M-estimator is obtained by solving the optimization problem

| (15) | |||||

| subject to |

First, note the loss function in (14) is convex. Thus, the corresponding M-estimator should be tractable even though there are some outliers. Second, when goes to will converges to Thus, the least square estimator is a special case of the M-estimator obtained from (15), which is not robust to outliers. Third, for fixed are all bounded. Intuitively, this implies that the impact of outlier observations of will be controlled and thus the corresponding statistical procedure will be robust.

We now study the robustness and tractability of the M-estimator of (15) based on our framework in Theorem 2. In order to emphasize on the effects of the tuning parameter and the contamination ratio on the robustness property and tractability property, we consider a simplified assumption on the feature vector and the pdf of idealized residual

Assumption 3.

- (a)

-

The feature vector are i.i.d multivariate Gaussian distribution

- (b)

-

The idealized noise pdf has Gaussian distribution

- (c)

-

Assume the true parameter

Corollary 1.

Under Assumption 3, for any there exist two constants

| (16) | |||||

| (17) |

such that when the number of data points is large, with high probability, any stationary points of the empirical risk function in (15) belongs in the ball Moreover, the empirical risk function in (15) is strongly convex in the ball Thus, there exists a unique stationary point of which is the corresponding M-estimator.

Note which means the corresponding Huber’s estimator will be tractable, no matter there are outliers or not. This is consistent with the fact that the Huber’s loss function is convex. Moreover, it is interesting to see the special case of Corollary 1 with which reduces to the least square estimator. As we can see, with we have which implies the solution of the optimization problem in (15) can be arbitrarily in the ball even when the proportion of outliers is small. Thus it is not robust to the outliers. This recovers the well-known fact: the least square estimator is easy to compute, but is very sensitive to outliers.

Additionally, for another special case with and we have which means the true parameter is the unique stationary point of the risk function. This implies the Huber’s estimator is consistent when there are no outliers.

4.2 Penalized M-estimator via Welsch’s exponential squared loss

In this subsection, we illustrate the general results presented in Section 3 by considering a family of M-estimators with a specific nonconvex loss function known as Welsch’s exponential squared loss (Dennis Jr and Welsch,, 1978; Rey,, 2012; Wang et al.,, 2013),

| (18) |

where is a tuning parameter. The corresponding penalized M-estimator is obtained by solving the optimization problem

| (19) | |||||

| subject to |

The non-convex loss function in (18) has been used in other contexts such as robust estimation and robust hypothesis testing, see Ferrari and Yang, (2010); Qin and Priebe, (2017), as it has many nice properties. First, it is a smooth function of both and and the gradient and Hessian are well-defined. Second, when goes to will converges to Thus, the LASSO estimator is a special case of the M-estimator obtained from (19). Third, for fixed are all bounded. Intuitively, this implies that the impact of outlier observations of will be controlled and thus the corresponding statistical procedure will be robust.

We now study the robustness and tractability of the penalized M-estimator of (19) based on our framework in Theorem 3. When goes to the M-estimator reduces to the LASSO estimator, which can be computed easily. However, it is also known to be very sensitive to the outliers (Alfons et al.,, 2013). On the other hand, when increases, the estimator becomes more robust, but may lose tractability due to the highly non-convexity of the function as well as the presence of the outliers.

In order to emphasize on the relation between the tuning parameter and the contamination ratio we consider a simplified assumption on the feature vector and the pdf of idealized residual

Assumption 4.

- (a)

-

The feature vector are i.i.d multivariate uniform distribution

- (b)

-

The idealized noise pdf has Gaussian distribution

- (c)

-

The true parameter

With Assumption 4 and Theorem 3, we can get the following corollary, which characterizes the robustness and tractability of the penalized M-estimator with Welsch’s exponential squared loss in (19):

Corollary 2.

Assume that Assumption 4 holds and the true parameter satisfies for any there exist a constant such that if choose as the following hold with probability as least

- (a)

-

All stationary points of problem (19) are in

- (b)

-

The empirical risk function are strong convex in the ball

- (c)

-

As long as is large enough and the contamination ratio is small such that the problem (19) has a unique local stationary point which is also the global minimizer.

Here

| (20) | |||||

| (21) |

It is interesting to see the special case of Corollary 2 with which reduces to the LASSO estimator. On the one hand, with we have for any This means that the corresponding risk function is strongly convex in the entire region of , and hence it is always tractable. On the other hand, since the solution of the optimization problem in (19) can be arbitrarily in the ball even when the proportion of outliers is small. Thus it is not robust to the outliers. This recovers the well-known fact: the LASSO estimator is easy to compute, but is very sensitive to outliers.

Additionally, for another special case with and we have which means the true parameter is the unique stationary point of the risk function. This implies the Welsch’s estimator has nice tractability when there is no outliers. However, when the percentage of outlier is increasing, will decrease, which implies more outliers will reduce the tractability of the M-estimator.

5 Simulation results

In this section, we report the simulation results by using Welsch’s exponential loss (Dennis Jr and Welsch,, 1978) when the data are contaminated, using synthetic data setting. We first generate covariates and responses where We consider the case when the residual term have gross error model with contamination ratio , i.e., where The outlier distribution is chosen to highlight the effects of outliers when they are dependent on and has non-zero mean.

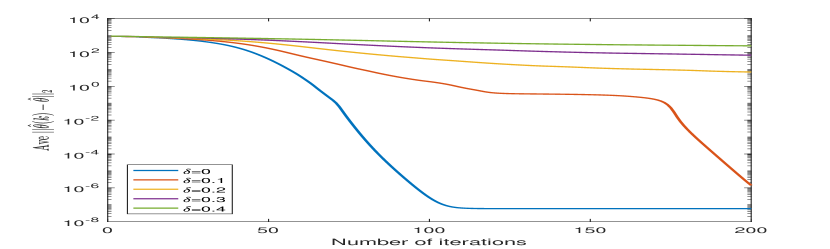

In the first part, we consider the low-dimensional case when the dimension Specifically, we generate pairs of data with dimension and with different choices of contamination ratios We use projected gradient descent to solve the optimization problem in (15) with In order to make the iteration points be inside the ball, we will project the points back into if they fall out of the ball. The step size is fixed as In order to test the tractability of the M-estimator, we run gradient descent algorithm with random initial values in the ball to see whether the gradient descent algorithm can converge to the same stationary point or not. Denote as the iteration points, Figure 2 shows the convergence of the gradient descent algorithm for the exponential loss with the choice of under the gross error model with different From Figure 2 we observe when the proportion of outliers is small (i.e., ) gradient descent could converge to the same stationary point fast. However, when the contamination ratio becomes larger, gradient descent may not converge to the same point for different initial points, indicating the loss of tractability for the same objective function with increasing proportion of outliers. Those observations are consistent to our Theorem 2, which asserts the M-estimator is tractable when the contamination ratio is small.

To illustrate the robustness of the M-estimator, we generate realizations of and run gradient descent algorithm with different initial values. The average estimation errors between the M-estimator and the true parameter are presented in Figure 2. As we can see, when all estimators have small estimation errors, which are well expected as those M-estimators are consistent without outliers (Huber,, 1964; Huber and Ronchetti,, 2009). However, for the M-estimator with i.e., the least square estimator, the estimation error will increase dramatically as the proportion of outliers increases. This confirms that the least square estimator is not robust to the outliers.

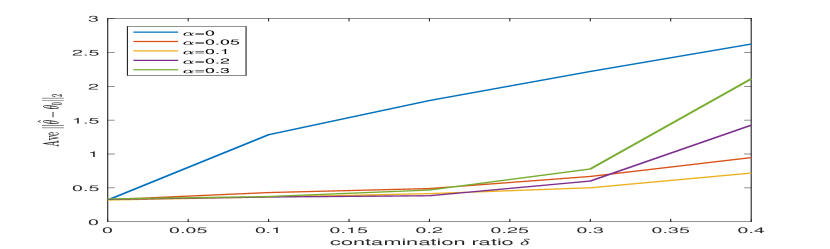

Meanwhile, when the overall estimation error does not increase much even with outliers, which clearly demonstrate the robustness of the M-estimator. Note that when is further increased from to although the estimator error is still very small for it will increase dramatically when is greater than We believe that two reasons contribute to this phenomenon: robustness starts to decrease when becomes too large; and more importantly, the algorithm fails to find the global optimum due to multiple stationary points when is large. Thus for each there exists a critical bound of such that the estimator will be robust and tractable efficiently when the proportion of outliers is smaller than that bound.

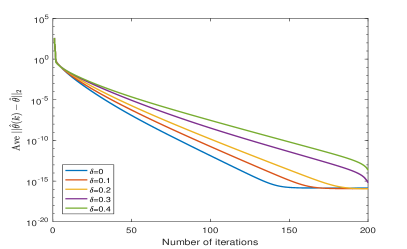

In the second part, we present our results in the high-dimensional region when . Data are generated from the same gross error model in the previous simulation study, with the true parameter a sparse vector with nonzero entries. All nonzero entries are set to be We use proximal gradient descent algorithm to solve problem (10). Similarly, we will project the points back into if they fall out of the ball. Figure 3 shows the convergence of the proximal gradient descent algorithm for the nonconvex exponential loss with the choice of and regularizer with the parameter under the gross error model with different From Figure 3 we observe when the percentage of outliers is small, the algorithm will converge to the same stationary point fast, which implies there is only one unique stationary point. When is larger, the converge rate become slower, which implies there may exist another stationary points. Those simulation results reflect our theoretical result for the tractability of the penalized M-estimator in high-dimensional regression.

6 Case study

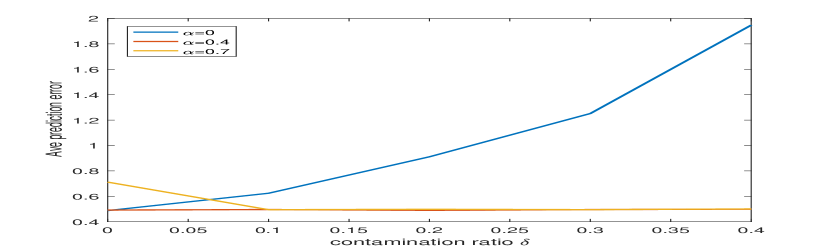

In this section, we present a case study of the robust regression problem for the Airfoil Self-Noise dataset (Brooks et al.,, 2014), which is available on UCI Machine Learning Repository. The dataset was processed by NASA and is commonly used for regression study to learn the relation between the airfoil self-noise and five explanatory variables. Specifically, the dataset contain the following explanatory variables: Frequency (in Hertzs), Angle of attack (in degrees), Chord length,(in meters), Free-stream velocity (in meters per second), and Suction side displacement thickness (in meters). There are observations in the dataset. The response variable is Scaled sound pressure level (in decibels). In this section, the five explanatory variables are scaled to have zero mean and unit variance. Then, we corrupt the response by adding noise from the same gross error model as the previous section: with

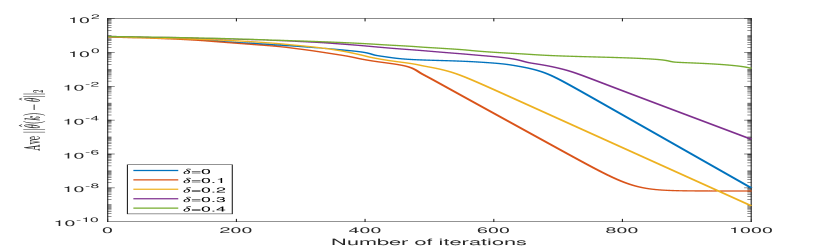

We consider the M-estimator using Welsch’s exponential loss (Dennis Jr and Welsch,, 1978) on the dataset to validate the tractability and the robustness of the corresponding M-estimator. First, we run Monte Carlo simulations. At each time, we split the dataset which consists of pairs of data into a training dataset of size and a testing dataset of size Then for the training dataset, we use gradient descent method with different initial values to update the iteration points.

Figure 5 shows the average distance between each iteration point and the optimal point with the choice of and step size . Clearly, when is smaller than gradient descent will converge to the same local minimizer, which implies the uniqueness of the stationary point. This result demonstrates the nice tractability of the M-estimator under the gross error model when the proportion of outliers is small. Then, using the optimal point as the M-estimator, we calculate the prediction error, which is the mean square error on the testing data. Figure 5 shows the average prediction error on the testing data. As we can see, the prediction error with the choice of will increase dramatically when the percentage of outliers increases. In contrast, the prediction errors of M-estimators with is stable even with a large percentage of outliers. This illustrates the robustness of M-estimators for some positive .

7 Conclusions

In this paper, we investigate the robustness and computational tractability of general (non-convex) M-estimators in both classical low-dimensional regime and modern high-dimensional regime. In terms of robustness, in the low-dimensional regime, we show the estimation error of the M-estimator is as the order of which nearly achieves the minimax lower bound of in Chen et al., (2016). In the high-dimensional regime, we show the estimation error of the penalized M-estimator has the estimation error as the order of which achieves the minimax estimation rate (Chen et al.,, 2016).

In terms of tractability, our theoretical results imply under sufficient conditions, when the percentage of arbitrary outliers is small, the general M-estimator could have good computational tractability since it has only one unique stationary point, even if the loss function is non-convex. Therefore, M-estimators can tolerate certain level of outliers by keeping both estimation accuracy and computation efficiency. Both simulation and real data case study are conducted to validate our theoretical results about the robustness and tractability of M-estimation in the presence of outliers.

8 Appendix

Proof of Lemma 1: In order to prove the uniform convergency theorem, it is suffice to verify assumption 1, 2 and 3 in Mei et al., (2018). Specifically, first, we will verify that the directional gradient of the population risk is sub-Gaussian (Assumption 1 in Mei et al., (2018)). Note the directional gradient of the population risk is given by Since and is mean zero and -sub-Gaussian by our assumption 1, due to Lemma 1 in Mei et al., (2018), there exists a universal constant such that is sub-Gaussian. Second, we will verify that the directional Hessian of the loss is sub-exponential (Assumption 2 in Mei et al., (2018)). The directional Hessian of the loss gives Since by Lemma 1 in Mei et al., (2018), is -sub-exponential. Third, let and

Then, we can show and Therefore, there exists a constant such that and which verifies the assumption 3 in Mei et al., (2018). Therefore, the uniform convergency of gradient and Hessian in theorem 1 in Mei et al., (2018) holds for our gross error model.

∎

Proof of Theorem 1: Part (a): It is suffice to show that for all Note by Assumption 1(d), we have as and Define it is easy to see that for all Then, we have

Here (i) holds from the fact that if has mean zero and is -sub-Gaussian, then for all

where is a constant (Boucheron et al.,, 2013). (ii) holds from Chebyshev’s inequality. Thus, a choice of will ensure that

| (22) |

which is greater than when

| (23) |

Therefore, there are no stationary point outside of the ball

Part(b): We first look at the minimum eigenvalue of the Hessian at For any

Therefore, we have the minimum eigenvalue of is greater than as long as

Then we look at the operator norm of For any

Hence, taking

| (24) |

guarantees that Therefore, for all we have

| (25) |

which yields there is at most one minimizer of in the ball as long as

Part (c): Note is a continuous function on Thus there exists a global minimizer, denoted by Since we have shown that there is no stationary points outside the ball should be in the ball Therefore, as long as i.e.,

| (26) |

there exists and only exists a unique stationary point of which is also the global optimum ∎

Proof of Theorem 2 Based on Lemma 1, there exists a constant such that when

| (27) | |||

| (28) |

Part (a): Note

| (29) | |||||

| (30) |

which is greater than when

| (31) |

Therefore, there are no stationary points outside of the ball

Part (b): For the least eigenvalue of the empirical Hessian in we have

| (32) | |||||

This lead to the conclusion that, is strong convex inside the ball

Part(c): When by strong convexity of in there exists a unique local minimizer, which is in We denote the unique local minimizer as

By Theorem 1, there is a unique stationary point of the population risk function in the ball Suppose is the unique stationary point of By Taylor expansion of at the point , there exists a in such that

| (33) |

Since by equation (32), the least eigenvalue of is greater than which lead to

| (34) |

which yield

| (35) |

By Theorem 1, combined with equation (35) and the uniform convergency theorem in Lemma 1 yield

| (36) |

∎

Proof of lemma 2: From the Theorem 3 in Mei et al., (2018), the uniform convergency theorem of our Lemma 2 holds if Assumption 4, 5 in Mei et al., (2018) hold under the contaminated model with outliers. Here we will show under our assumption 1 and 2, there exist constants and such that

- a

-

For all

- b

-

There exist functions and such that

(37) In addition, is - Lipschitz to its first argument and is mean-zero and -sub-Gaussian.

Part (a). The gradient of the loss is

| (38) |

By assumption 1, we have By assumption 2, we have Therefore, (a) is satisfied with parameter

Part (b). Note

| (39) |

We take and Clearly, we have and is mean and -sub-Gaussian. Furthermore, note we have

| (40) | |||||

| (41) | |||||

| (42) |

Therefore, is at most -Lipschitz in its first argument By part (a) and part (b), we can see assumption 4, 5 are satisfied under the gross error model, which prove the uniform convergency theorem in our Lemma 2. ∎

Proof of theorem 3: We decompose the proof into four technical lemmas. First, in Lemma 3, we prove there cannot be any stationary points of the regularized empirical risk in (10) outside the region which is a cone with Then in Lemma 4, we show there cannot be any stationary points outside the region where is the statistical radius which is not less than in Theorem 1. In Lemma 5, we argue that all stationary points should have support size less or equal to Finally, in Lemma 6, we show there cannot be two stationary points in Note is a continuous function, which indicates the existence of the global minimizer. Therefore, we can conclude there is and only is one unique stationary point of the regularized empirical risk as long as

To start with those lemmas, we define the subgradient of at as:

| (43) |

Therefore, the optimality condition implies that is a stationary point of if and only if To simplify notations, all constants in the following lemmas are dependent on but independent on

Lemma 3.

Let and Define a cone For any there exist constants such that letting with probability at least has no stationary points in

| (44) |

Proof.

For any it can be written as where Therefore, we have

| (45) |

Note by (22) we have

| (46) |

By lemma 2, for any there exists a constant such that

| (47) |

Letting we have

| (48) |

Plugging (46),(47),(48) into (45) yields

| (49) | |||||

| (50) |

Let we have

| (51) | |||||

Next, we will find the lower bound of under the constraint of Note by Cauchy inequality, we have

| (52) |

Therefore, under the constraint of the minimal value of is obtained when and By solving the two equations yield

| (53) | |||||

| (54) |

and Combined with (51), setting and yield which implies as long as i.e., ∎

Lemma 4.

For any there exist constants such that with probability at least

| (55) |

as long as where

| (56) |

Proof.

Lemma 5.

If for any there exist constants such that letting with probability at least any stationary points of in has support size

Proof.

Let be a stationary point of in (10). Then we have

| (61) |

where Thus, we have

| (62) |

Note and is -subgaussian with mean Then there exists an absolute constant such that is -subgaussian, see Lemma 1(d) in Mei et al., (2018). Thus we have is -subgaussian with mean Moreover, note we have for any

| (63) | |||||

Thus, we can get

| (64) | |||||

Thus, a choice of and will guarantee that

| (65) |

Let we have the event happens with the probability at least Under this event, combing with (62) yields

| (66) |

Squaring and summing over we have

| (67) | |||||

| (68) | |||||

| (69) | |||||

| (70) |

where are located on the line between and obtained by intermediate value theorem. Moreover, by Minkowski inequality and Cauchy-Schwarz inequality yield

| (71) | |||||

Due to the restricted smoothness property of the sub-Gaussian random variables Mei et al., (2018), there exists a constant depending on such that with probability at least as we have

| (72) |

Therefore, with probability at least we have

| (73) |

Moreover, by Lemma 13 in Mei et al., (2018), for any there exists constant depending on such that

| (74) |

By (65,73,74), as well as (71), at least

| (75) | |||||

| (76) |

By equation (56) we have

| (77) |

Taking gives us

| (78) | |||||

| (79) |

∎

Lemma 6.

For any positive constants and letting there exist constant such that when

| (80) |

Moreover, the regularized empirical risk in (10) cannot have two stationary points in the region

Proof.

According to (25), we have

| (81) |

By lemma 2, there exists constant such that when

| (82) |

Suppose are two distinct stationary points of in Define Since and are -sparse, is sparse, as well as for any Therefore,

| (83) | |||||

Note the regularization term is convex, we have for any subgradients

| (84) |

| (85) |

which is contradict with the assumption that and are two distinct stationary points of ∎

Proof of Theorem 3. Now we are ready to prove Theorem 3. By Lemma 3 and Lemma 4, as letting all stationary points of are in where is defined in (56), is the cone defined in Lemma 3. This proves Theorem 3(a). Moreover, by Lemma 5, Lemma 6, as cannot have two distinct stationary points in Thus, as long as there is only one unique stationary point of the regularized empirical risk function which is the corresponding regularized M-estimator of (10). This proves Theorem 3 (b).

Proof of Corollary 1: Huber’s loss function is defined by

| (88) |

the corresponding score function would be

| (91) |

Note for any all of , and are bounded. Specifically, we have Therefore, the assumptions in Theorem 1 and Theorem 2 are satisfied. It is suffice to find the explicit expression of and in equation (23) and (24). Since it is easy to see which implies the Huber’s estimator has nice computational tractability, regardless the choice of tuning parameter and the percentage of outliers Moreover, to find the explicit expression of according to Assumption 3, we have Thus, we can calculate

Therefore we have By equation (23) in the proof of Theorem 1 yields

| (92) | |||||

| (93) |

which complete the proof. ∎

Proof of Corollary 2: When the loss function is defined by the corresponding score function would be Moreover, we can get and . Note for any all of , and are bounded.

Therefore, the Assumption 1 is satisfied. It is suffice to find the explicit expression of and in equation (23) and (24). In order to have an accurate expression, we will use the individual bound of instead of the universal bound Specifically, according to Assumption 4, is -sub-Gaussian, Thus, we can calculate and By equation (23) in the proof of Theorem 1 yields

| (94) | |||||

| (95) |

Similarly, we can calculate Note by equation (24) in the proof of Theorem 1 yields

| (96) | |||||

| (97) |

According to equation (60) in the proof of Theorem 3, we have with high probability, all stationary points of the empirical risk function in (19) are inside the ball where

| (98) | |||||

| (99) |

Therefore, as we have which completes the proof. ∎

References

- Alfons et al., (2013) Alfons, A., Croux, C., and Gelper, S. (2013). Sparse least trimmed squares regression for analyzing high-dimensional large data sets. The Annals of Applied Statistics, 7(1):226–248.

- Anandkumar et al., (2014) Anandkumar, A., Ge, R., Hsu, D., Kakade, S. M., and Telgarsky, M. (2014). Tensor decompositions for learning latent variable models. The Journal of Machine Learning Research, 15(1):2773–2832.

- Andrews et al., (1972) Andrews, D. F., Bickel, P. J., Hampel, F. R., Huber, P. J., Rogers, W. H., and W.Tukey, J. (1972). Robust Estimates of Location: Survey and Advances. Princeton University Press.

- Bai et al., (1992) Bai, Z., Rao, C. R., and Wu, Y. (1992). M-estimation of multivariate linear regression parameters under a convex discrepancy function. Statistica Sinica, 2(1):237–254.

- Beaton and Tukey, (1974) Beaton, A. E. and Tukey, J. W. (1974). The fitting of power series, meaning polynomials, illustrated on band-spectroscopic data. Technometrics, 16(2):147–185.

- Bengio, (2009) Bengio, Y. (2009). Learning deep architectures for ai. Foundations and trends® in Machine Learning, 2(1):1–127.

- Boucheron et al., (2013) Boucheron, S., Lugosi, G., and Massart, P. (2013). Concentration inequalities: A nonasymptotic theory of independence. Oxford university press.

- Brooks et al., (2014) Brooks, T., Pope, S., and Marcolini, M. (2014). Uci machine learning repository.

- Candes et al., (2015) Candes, E. J., Li, X., and Soltanolkotabi, M. (2015). Phase retrieval from coded diffraction patterns. Applied and Computational Harmonic Analysis, 39(2):277–299.

- Chang et al., (2018) Chang, L., Roberts, S., and Welsh, A. (2018). Robust lasso regression using tukey’s biweight criterion. Technometrics, 60(1):36–47.

- Chen et al., (2016) Chen, M., Gao, C., and Ren, Z. (2016). A general decision theory for huber’s -contamination model. Electronic Journal of Statistics, 10(2):3752–3774.

- Cheng et al., (2010) Cheng, G., Huang, J. Z., et al. (2010). Bootstrap consistency for general semiparametric m-estimation. The Annals of Statistics, 38(5):2884–2915.

- Dennis Jr and Welsch, (1978) Dennis Jr, J. E. and Welsch, R. E. (1978). Techniques for nonlinear least squares and robust regression. Communications in Statistics-Simulation and Computation, 7(4):345–359.

- Donoho and Huber, (1983) Donoho, D. L. and Huber, P. J. (1983). The notion of breakdown point. A festschrift for Erich L. Lehmann, pages 157–184.

- El Karoui et al., (2013) El Karoui, N., Bean, D., Bickel, P. J., Lim, C., and Yu, B. (2013). On robust regression with high-dimensional predictors. Proceedings of the National Academy of Sciences, 110(36):14557–14562.

- Ferrari and Yang, (2010) Ferrari, D. and Yang, Y. (2010). Maximum lq-likelihood estimation. The Annals of Statistics, 38(2):753–783.

- Geyer et al., (1994) Geyer, C. J. et al. (1994). On the asymptotics of constrained -estimation. The Annals of Statistics, 22(4):1993–2010.

- Hampel et al., (2011) Hampel, F. R., Ronchetti, E. M., Rousseeuw, P. J., and Stahel, W. A. (2011). Robust statistics: the approach based on influence functions. John Wiley & Sons.

- Huber, (1964) Huber, P. J. (1964). Robust estimation of a location parameter. The annals of mathematical statistics, 35(1):73–101.

- Huber and Ronchetti, (2009) Huber, P. J. and Ronchetti, E. (2009). Robust statistics. New York: Wiley.

- Lambert-Lacroix and Zwald, (2011) Lambert-Lacroix, S. and Zwald, L. (2011). Robust regression through the huber’s criterion and adaptive lasso penalty. Electronic Journal of Statistics, 5:1015–1053.

- Lehmann and Casella, (2006) Lehmann, E. L. and Casella, G. (2006). Theory of point estimation. Springer Science & Business Media.

- Li et al., (2011) Li, G., Peng, H., and Zhu, L. (2011). Nonconcave penalized m-estimation with a diverging number of parameters. Statistica Sinica, 21:391–419.

- Loh, (2017) Loh, P.-L. (2017). Statistical consistency and asymptotic normality for high-dimensional robust -estimators. The Annals of Statistics, 45(2):866–896.

- Loh and Wainwright, (2015) Loh, P.-L. and Wainwright, M. J. (2015). Regularized m-estimators with nonconvexity: Statistical and algorithmic theory for local optima. Journal of Machine Learning Research, 16:559–616.

- Mairal et al., (2009) Mairal, J., Bach, F., Ponce, J., and Sapiro, G. (2009). Online dictionary learning for sparse coding. In Proceedings of the 26th annual international conference on machine learning, pages 689–696. ACM.

- Maronna and Yohai, (1981) Maronna, R. A. and Yohai, V. J. (1981). Asymptotic behavior of general m-estimates for regression and scale with random carriers. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 58(1):7–20.

- Mei et al., (2018) Mei, S., Bai, Y., Montanari, A., et al. (2018). The landscape of empirical risk for nonconvex losses. The Annals of Statistics, 46(6A):2747–2774.

- Mizera and Müller, (1999) Mizera, I. and Müller, C. H. (1999). Breakdown points and variation exponents of robust -estimators in linear models. The Annals of Statistics, 27(4):1164–1177.

- Qin and Priebe, (2017) Qin, Y. and Priebe, C. E. (2017). Robust hypothesis testing via lq-likelihood. Statistica Sinica, 27(4):1793–1813.

- Rey, (2012) Rey, W. J. (2012). Introduction to robust and quasi-robust statistical methods. Springer Science & Business Media.

- Wang et al., (2013) Wang, X., Jiang, Y., Huang, M., and Zhang, H. (2013). Robust variable selection with exponential squared loss. Journal of the American Statistical Association, 108(502):632–643.

- Zou and Hastie, (2005) Zou, H. and Hastie, T. (2005). Regularization and variable selection via the elastic net. Journal of the royal statistical society: series B (statistical methodology), 67(2):301–320.