Calibrated Surrogate Maximization of Linear-fractional Utility

in Binary Classification

Han Bao Masashi Sugiyama

The University of Tokyo RIKEN AIP tsutsumi@ms.k.u-tokyo.ac.jp RIKEN AIP The University of Tokyo sugi@k.u-tokyo.ac.jp

Abstract

Complex classification performance metrics such as the Fβ-measure and Jaccard index are often used, in order to handle class-imbalanced cases such as information retrieval and image segmentation. These performance metrics are not decomposable, that is, they cannot be expressed in a per-example manner, which hinders a straightforward application of M-estimation widely used in supervised learning. In this paper, we consider linear-fractional metrics, which are a family of classification performance metrics that encompasses many standard ones such as the Fβ-measure and Jaccard index, and propose methods to directly maximize performances under those metrics. A clue to tackle their direct optimization is a calibrated surrogate utility, which is a tractable lower bound of the true utility function representing a given metric. We characterize sufficient conditions which make the surrogate maximization coincide with the maximization of the true utility. Simulation results on benchmark datasets validate the effectiveness of our calibrated surrogate maximization especially if the sample sizes are extremely small.

1 Introduction

Binary classification, one of the main focuses in machine learning, is a problem to predict binary responses for input covariates. Classifiers are usually evaluated by the classification accuracy, which is the expected proportion of correct predictions. Since the accuracy cannot evaluate classifiers appropriately under class imbalance (Menon et al.,, 2013) or in the presence of label noises (Menon et al.,, 2015), alternative performance metrics have been employed such as the Fβ-measure (van Rijsbergen,, 1974; Joachims,, 2005; Nan et al.,, 2012; Koyejo et al.,, 2014), Jaccard index (Koyejo et al.,, 2014; Berman et al.,, 2018), and balanced error rate (BER) (Brodersen et al.,, 2010; Menon et al.,, 2013, 2015; Charoenphakdee et al.,, 2019). Once a performance metric is given, it is a natural strategy to optimize the performance of classifiers directly under the given performance metric. However, the alternative performance metrics have difficulty in direct optimization in general, because they are non-decomposable, for which per-example loss decomposition is unavailable. In other words, the M-estimation procedure (van de Geer,, 2000) cannot be applied, which makes the optimization of non-decomposable metrics hard.

One of the earliest works tackling the non-traditional metrics (Koyejo et al.,, 2014) generalized performance metrics into the linear-fractional metrics, which are the linear-fractional form of entries in the confusion matrix, and encompasses the BER, Fβ-measure, Jaccard index, Gower-Legendre index (Gower and Legendre,, 1986; Natarajan et al.,, 2016), and weighted accuracy (Koyejo et al.,, 2014). Koyejo et al., (2014) formulated the optimization problem in two ways. One is a plug-in rule (Koyejo et al.,, 2014; Narasimhan et al.,, 2014; Yan et al.,, 2018) to estimate the class-posterior probability and its optimal threshold, and the other is an iterative weighted empirical risk minimization approach (Koyejo et al.,, 2014; Parambath et al.,, 2014) to find a better cost with which the minimizer of the cost-sensitive risk (Scott,, 2012) achieves higher utilities. Although they provide statistically consistent esitmators, the former suffers from high sample complexity due to the class-posterior probability estimation, while the latter is computationally demanding because of iterative classifier training.

Our goal is to seek for computationally more efficient procedures to directly optimize the linear-fractional metrics, without sacrificing the statistical consistency. Specifically, we provide a novel calibrated surrogate utility which is a tractable lower bound of the true utility representing the metric of our interest. The surrogate maximization is formulated as the combination of concave and quasi-concave programs, which can be optimized efficiently. Then, we derive sufficient conditions on the surrogate calibration, under which the surrogate maximization implies the maximization of the true utility. In addition, we show the consistency of the empirical estimation procedure based on the theory of Z-estimation (van der Vaart,, 2000). An overview of our proposed method is illustrated in Fig. 1.

Contributions: (i) Surrogate calibration (Sec. 4): We propose a tractable lower bound of the linear-fractional metrics with calibration conditions, which guarantee that the surrogate maximization implies the maximization of the true utility. This approach is model-agnostic differently from many previous approaches (Koyejo et al.,, 2014; Narasimhan et al.,, 2014, 2015; Yan et al.,, 2018). (ii) Efficient gradient-based optimization (Secs. 3.2 and 3.3): The surrogate utility has affinity with gradient-based optimization because of its non-vanishing gradient and an unbiased estimator of the gradient direction. Even though the linear-fractional objective does not admit concavity in general, our proposed algorithm is a two-step approach combining concave and quasi-concave programs and hence computationally efficient. (iii) Consistency analysis (Sec. 5): The estimator obtained via the surrogate maximization with a finite sample is shown to be consistent to the maximizer of the expected utility.

2 Preliminaries

Throughout this work, we focus on binary classification. Let . Let if the predicate holds and otherwise. Let be a feature space and be the label space. We assume that a sample independently follows the joint distribution with a density . We often split into two independent samples and . Usually, . For a function , we write . An expectation with respect to is written as for a function , where denotes the -marginal distribution. A classifier is given as a function , where determines predictions. Here we adopt the convention . Let be a hypothesis set of classifiers. Let and be the class-prior/-posterior probabilities of , respectively. The 0/1-loss is denoted as , while denotes a surrogate loss. The norm without a subscript is the -norm. For a set , denote as the complementary set of , namely, .

The following four quantities are focal targets in binary classification: the true positives (), false negatives (), false positives (), and true negatives ().

Definition 1 (Confusion matrix).

Given a classifier and a distribution , its confusion matrix is defined as , where

and as well as and can be transformed to each other: and . They can be expressed with and , such as . The goal of binary classification is to obtain a classifier that “maximizes” and , while keeping and as “low” as possible. Classifiers are evaluated by performance metrics that trade off those four quantities. Performance metrics need to be chosen based on user’s preference on the confusion matrix (Sokolova and Lapalme,, 2009; Menon et al.,, 2015). In this work, we focus on the following family of utilities representing the linear-fractional metrics.

Definition 2 (Linear-fractional utility111 As mentioned by Dembczyński et al., (2017), there is a dichotomy in the definition of performance metrics: population utility (PU) and expected test utility (ETU). We adopt PU, which is defined as the linear-fractional transform of the population confusion matrix in this context. This is convenient to avoid estimating compared to ETU. ).

A linear-fractional utility is defined as

| (1) |

where are class-conditional score functions given as

and are constants such that ().

The class-conditional score functions correspond to a linear-transformation of and : . Examples of are shown in Tab. 1.

| Metric | Fβ-measure (van Rijsbergen,, 1974) | Jaccard index (Jaccard,, 1901) | Gower-Legendre index (Gower and Legendre,, 1986) |

|---|---|---|---|

| Definition | |||

Given a utility function , our goal is to obtain a classifier that maximizes .

| (2) |

Traditional Supervised Classification: Here, we briefly review a traditional procedure for supervised classification (Vapnik,, 1998). Our aim is to obtain a classifier with high accuracy, which corresponds to minimizing the classification risk . Since optimizing the 0/1-loss is a computationally infeasible problem (Ben-David et al.,, 2003; Feldman et al.,, 2012), it is a common practice to instead minimize a surrogate risk , where is a surrogate loss. If is a classification-calibrated loss (Bartlett et al.,, 2006), it is known that minimizing corresponds to minimizing . Eventually, what we actually minimize is the empirical (surrogate) risk . The empirical risk is an unbiased estimator of the true risk for a fixed , and the uniform law of large numbers guarantees that converges to for any in probability (Vapnik,, 1998; van de Geer,, 2000; Mohri et al.,, 2012). This strategy to minimize is called empirical risk minimization (ERM).

The traditional ERM is devoted to maximizing the accuracy, which is not necessarily suitable when another metric is used for evaluation. Our aim is to give an alternative procedure to maximize directly as in Eq. (2). In the next section, we introduce a tractable counterpart of the true utility because contains the 0/1-loss and is intractable as above.

3 Surrogate Utility and Optimization

The true utility in Eq. (1) consists of the 0/1-loss , which is difficult to optimize. In this section, we introduce a surrogate utility in order to make the optimization problem in Eq. (2) easier.

3.1 Lower Bounding True Utility

Assume that we are given a surrogate loss . We hope that the surrogate utility should lower-bound the true utility , and that / should become larger / smaller as a result of optimization, respectively. We realize these ideas by constructing surrogate class-conditional score functions and as follows:

| (3) |

We often abbreviate as if it is clear from the context. Given the surrogate class-conditional scores, define the surrogate utility as follows.

| (4) |

To construct , the 0/1-losses appearing in the true utility are replaced with the surrogate loss . The surrogate class-conditional scores in (3) are designed so that the surrogate utility in (4) bounds from below.

Lemma 3.

For all and a surrogate loss such that for all , .

Proof.

Fix and . Since , ( ). Together with ( ), we confirm . It can be confirmed that as well. Hence, is easy to see. ∎

Due to this property, maximizing is at least maximizing a lower bound of . We will discuss the goodness of this lower bound in Sec. 4, but we can immediately see for any . In the rest of this paper, we assume that is Fréchet differentiable.

3.2 Tractability of Surrogate Utility

The surrogate utility comes to have a non-vanishing gradient by using a smooth , and is guaranteed to be a lower bound of . In this subsection, we discuss how it can be maximized efficiently.

Let us consider an empirical estimator of :

| (5) |

where

A global maximizer of could be efficiently obtained if were concave. However, this is hard to achieve in our case regardless of the choice of due to its fractional form. Nonetheless, we may formulate our optimization problem as a quasi-concave program under a certain condition. First, we introduce the notion of quasi-concavity.

Definition 4 (Quasi-concavity (Boyd and Vandenberghe,, 2004)).

A function is said to be quasi-concave if the super-level set is a convex set for .

A quasi-concave function is a generalization of a concave function and has the unimodality though it is not necessarily concave, which ensures the uniqueness of the solution. Next, we have the following result, whose proof is given in App. B. Let be the numerator of .

Lemma 5.

Let . If is convex, in Eq. (5) is quasi-concave over and is concave over .

From Lemma 5, we observe the following two important facts. First, in the range of , our objective is generally neither concave nor quasi-concave, but its numerator is concave. Second, is quasi-concave over . These observations motivate us to employ Algorithm 1, which first increases the numerator only to make it positive and then maximizes the fractional form . Since the former is a concave program and the latter is a quasi-concave program within , the entire optimization can be performed computationally efficiently. For quasi-concave optimization, normalized gradient ascent (NGA) (Hazan et al.,, 2015) is applied, which is guaranteed to find a global solution of quasi-concave objectives. The behavior of Algorithm 1 is illustrated in Figure 2.

3.3 Gradient Direction Estimator

The empirical estimator in Eq. (5) is generally biased due to its fractional form. Nevertheless, its gradient is unbiased to the expected gradient up to a positive scalar multiple. Hence, we may safely use as the update direction in NGA.

Below, we state this idea formally. Under the interchangeability of the expectation and derivative, the gradient of the expected utility is expressed as

from which we can see that its gradient direction is parallel to . can be unbiasedly estimated.

Lemma 6.

Denote for simplicity. Define

| (6) |

Then, we have .

Lemma 6 can be confirmed by simple algebra, noting that two samples and are independent and identically drawn from . Since solving is identical to solving , gradient updates using is aligned to the maximization of . Hence, optimization procedures that only need gradients such as gradient ascent and quasi-Newton methods (Boyd and Vandenberghe,, 2004), e.g., the Broyden-Fletcher-Goldfarb-Shanno (BFGS) algorithm (Fletcher,, 2013) can be applied to maximize . Note that Algorithm 2 can be regarded as an extension of the traditional gradient ascent using . We plug either Algorithm 2 or BFGS using the normalized gradient to the second half of Algorithm 1.

4 Calibration Analysis: Bridging Surrogate Utility and True Utility

In Sec. 3, we formulated the tractable surrogate utility. Given the surrogate utility , a natural question arises in the same way as the classification calibration in binary classification (Zhang, 2004b, ; Bartlett et al.,, 2006): Does maximizing the surrogate utility imply maximizing the true utility ? In this section, we study sufficient conditions on the surrogate loss in order to connect the maximization of and the maximization of . All proofs in this section are deferred to App. A.

First, we define the notion of -calibration.

Definition 7 (-calibration).

The surrogate utility is said to be -calibrated if for any sequence of measurable functions and any distribution , it holds that when , where and are the suprema taken over all measurable functions.

This definition is motivated by calibration in other learning problems such as binary classification (Bartlett et al.,, 2006, Theorem 3), multi-class classification (Zhang, 2004a, , Theorem 3), structured prediction (Osokin et al.,, 2017, Theorem 2), and AUC optimization (Gao and Zhou,, 2015, Definition 1). If a surrogate utility is -calibrated, we may safely optimize the surrogate utility instead of the true utility . Note that -calibration is a concept to reduce the surrogate maximization to the maximization of within all measurable functions. The approximation error of is not the target of our analysis as in Bartlett et al., (2006).

Next, we give a property of loss functions that is needed to guarantee -calibration.

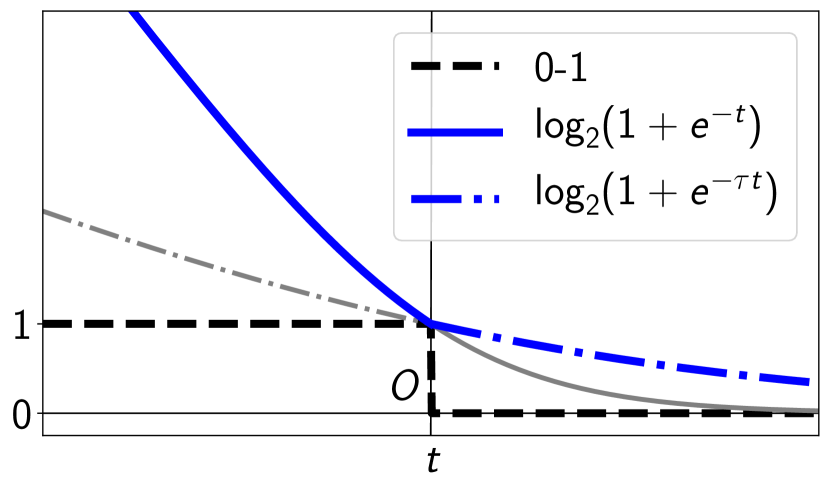

Definition 8 (-discrepant loss).

For a fixed , a convex loss function is said to be -discrepant if satisfies .

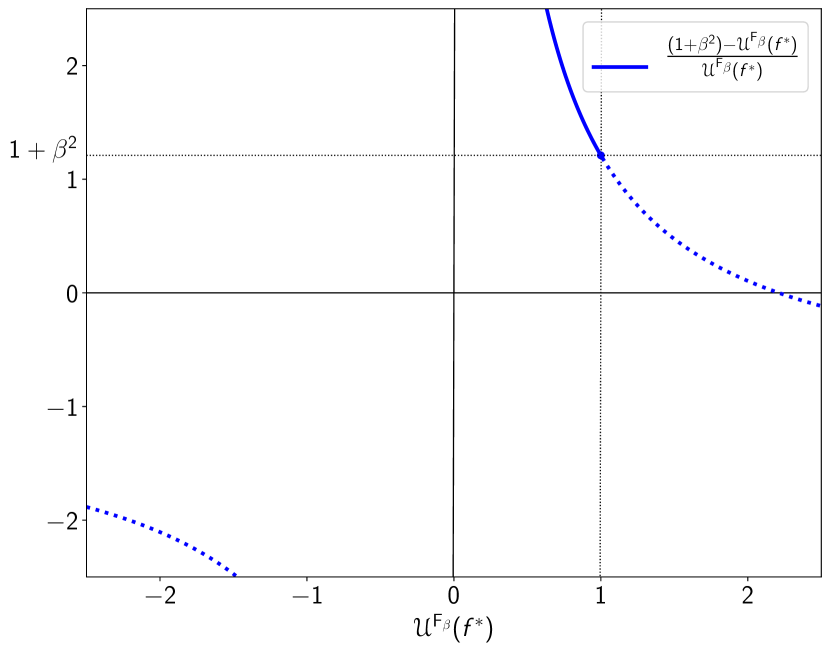

Intuitively, -discrepancy means that the gradient of around the origin is steeper in the negative domain than the positive domain (see Figure 3). The value controls steepness of the / surrogates appearing in the surrogate utility . Note that and appearing in Eqs. (3) and (4) correspond to and , respectively, by their constructions.

Below, we see calibration properties for specific linear-fractional metrics, the Fβ-measure and Jaccard index. Note that those calibration analyses can be extended to general linear-fractional utilities, which is deferred to App. A.4.

Fβ-measure: The Fβ-measure has been widely used especially in the field of information retrieval where relevant items are rare (Manning and Schütze,, 2008). Since it is defined as the weighted harmonic mean of the precision and recall (see Tab. 1), its optimization is difficult in general. Although much previous work has tried to directly optimize it in the context of the class-posterior probability estimation (Nan et al.,, 2012; Koyejo et al.,, 2014; Yan et al.,, 2018) or the iterative cost-sensitive learning (Koyejo et al.,, 2014; Parambath et al.,, 2014), we show that there exists a calibrated surrogate utility that can be used in the direct optimization as well.

For the Fβ-measure , define the true utility and the surrogate utility as

As for , we have the following Fβ-calibration guarantee. Denote .

Theorem 9 (Fβ-calibration).

Assume that a surrogate loss is differentiable almost everywhere, convex, and non-increasing, and that and is -discrepant for some constant .222Note that is non-negative and therefore such always exists. The non-negativity is discussed in App. A.5. Then, is Fβ-calibrated.

An example of the -discrepant surrogate loss is shown in Figure 3. Here is a discrepancy hyperparameter. From the fact , ranges over . We may determine by cross-validation, or fix it at by assuming .

Jaccard Index: The Jaccard index, also referred to as the intersection over union (IoU), is a metric of similarity between two sets: For two sets and , it is defined as (Jaccard,, 1901). The Jaccard index between the sets of examples predicted as positives and labeled as positives becomes , as is shown in Tab. 1. This measure is not only used for measuring the performance of binary classification (Koyejo et al.,, 2014; Narasimhan et al.,, 2015), but also for semantic segmentation (Everingham et al.,, 2010; Csurka et al.,, 2013; Ahmed et al.,, 2015; Berman et al.,, 2018).

For the Jaccard index , define the true utility and the surrogate utility as

As for , we have the following Jaccard-calibration. Denote .

Theorem 10 (Jaccard-calibration).

Assume that a surrogate loss is differentiable almost everywhere, convex, and non-increasing, and that and is -discrepant for some constant . Then, is Jaccard-calibrated.

Theorem 10 also relies on the -discrepancy as in Theorem 9. Thus, the loss shown in Figure 3 can also be used in the Jaccard case with a certain range of . In the same manner as the Fβ-measure, a hyperparameter ranges over , which we may either determine by cross-validation or fix to a certain value.

Remark: The -discrepancy is a technical assumption making stationary points of lie in the Bayes optimal set of . This is a mere sufficient condition for -calibration, while the classification-calibration (Bartlett et al.,, 2006) is the necessary and sufficient condition for the accuracy.333We give the surrogate calibration conditions for the accuracy in App. A.3. It is left as an open problem to seek for necessary conditions.

5 Consistency Analysis: Bridging Finite Sample and Asymptotics

In this section, we analyze statistical properties of the estimator in Eq. (6). To make our analysis simple, the linear-in-input model is considered throughout this section, where is a classifier parameter and is a compact parameter space. The maximization procedure introduced above can be naturally seen as Z-estimation (van der Vaart,, 2000), which is an estimation procedure to solve an estimation equation. In our case, the maximization of is reduced to a Z-estimation problem to solve the system . The first lemma shows that the derivative estimator admits the uniform convergence. Its proof is deferred to App. C.

Lemma 11 (Uniform convergence).

For simplicity, assume that . For , let . Assume that for are -Lipschitz continuous for some , and that () and () for some . Then,

| (7) |

where denotes the order in probability.

The Lipschitz continuity and smoothness assumptions in Lemma 11 can be satisfied if the surrogate loss satisfies a certain Lipschitzness and smoothness. Note that Lemma 11 still holds for -discrepant surrogates since we allow surrogates to have different smoothness parameters for both positive and negative domains. Lemma 11 is the basis for showing the consistency. Let and . Under the identifiability described below, and are roots of and , respectively. Then, we can show the consistency of .

Theorem 12 (Consistency).

Assume that is identifiable, that is, for all , and that Eq. (7) holds for . Then, .

Theorem 12 is an immediate result of van der Vaart, (2000, Theorem 5.9), given the uniform convergence (Lemma 11) and the identifiability assumption. Note that the identifiability assumes that has a unique zero , which is also usual in the M-estimation: The global optimizer is identifiable. Since Algorithm 1 is a combination of concave and quasi-concave programs, the identifiability would be reasonable to assume.

6 Related Work

In this section, we summarize the existing lines of research on the optimization of generalized performance metrics, which elucidates advantages of our approach.

(i) Surrogate optimization: One of the earliest attempts to optimize non-decomposable performance metrics dates back to Joachims, (2005), formulating the structured SVM as a surrogate objective. However, Dembczyński et al., (2013) showed that this surrogate is inconsistent, which means that the surrogate maximization does not necessarily imply the maximization of the true metric. Kar et al., (2014) showed the sublinear regret for the structural surrogate by Joachims, (2005) in online setting. Later, Yu and Blaschko, (2015), Eban et al., (2017), and Berman et al., (2018) have tried different surrogates, but their calibration has not been studied yet.

(ii) Plug-in rule: Instead of the surrogate optimization, Dembczyński et al., (2013) mentioned that a plug-in rule is consistent, where and a threshold parameter are estimated independently. We can estimate by minimizing strictly proper losses (Reid and Williamson,, 2009). The plug-in rule has been investigated in many settings (Nan et al.,, 2012; Dembczyński et al.,, 2013; Koyejo et al.,, 2014; Narasimhan et al.,, 2014; Busa-Fekete et al.,, 2015; Yan et al.,, 2018). However, one of the weaknesses of the plug-in rule is that it requires an accurate estimate of , which is less sample-efficient than the usual classification with convex surrogates (Bousquet et al.,, 2004; Tsybakov,, 2008). Moreover, estimation of the threshold parameter heavily relies on an estimate of .

(iii) Cost-sensitive risk minimization: On the other hand, Parambath et al., (2014) is a pioneering work to focus on the pseudo-linearity of the metrics, which reduces their maximization to an alternative optimization with respect to a classifier and the sublevel. This can be formulated as an iterative cost-sensitive risk minimization (Koyejo et al.,, 2014; Narasimhan et al.,, 2015, 2016; Sanyal et al.,, 2018). Though these methods are blessed with the consistency, they need to train classifiers many times, which may lead to high computational costs, especially for complex hypothesis sets.

Remark: Our proposed methods can be considered to belong to the family (i), while one of the crucial differences is the fact that we have calibration guarantee. We do not need to estimate the class-posterior probability as in (ii), or train classifiers many times as in (iii). This comparison is summarized in Tab. 2.

| Method | Consistency | Avoids to estimate | Efficient optimization |

|---|---|---|---|

| ours | ✓ | ✓ | ✓ |

| (i) | ✗ | ✓ | ✓ |

| (ii) | ✓ | ✗ | ✓ |

| (iii) | ✓ | ✓ | ✗ |

7 Experiments

In this section, we investigate empirical performances of the surrogate optimizations (Algorithm 1 with NGA and normalized BFGS). Details of datasets, baselines, and full experimental results are shown in App. D.

| (F1-measure) | Proposed | Baselines | |||

|---|---|---|---|---|---|

| Dataset | U-GD | U-BFGS | ERM | W-ERM | Plug-in |

| adult | 0.617 (101) | 0.660 (11) | 0.639 (51) | 0.676 (18) | 0.681 (9) |

| breast-cancer | 0.963 (31) | 0.960 (32) | 0.950 (37) | 0.948 (44) | 0.953 (40) |

| diabetes | 0.834 (32) | 0.828 (31) | 0.817 (50) | 0.821 (40) | 0.820 (42) |

| sonar | 0.735 (95) | 0.740 (91) | 0.706 (121) | 0.655 (189) | 0.721 (113) |

| (Jaccard index) | Proposed | Baselines | |||

|---|---|---|---|---|---|

| Dataset | U-GD | U-BFGS | ERM | W-ERM | Plug-in |

| adult | 0.499 (44) | 0.498 (11) | 0.471 (51) | 0.510 (20) | 0.516 (10) |

| breast-cancer | 0.921 (54) | 0.918 (55) | 0.905 (66) | 0.903 (78) | 0.913 (69) |

| diabetes | 0.714 (44) | 0.702 (50) | 0.692 (70) | 0.698 (56) | 0.695 (60) |

| sonar | 0.600 (125) | 0.600 (111) | 0.552 (147) | 0.495 (202) | 0.572 (134) |

Implementation Details of Proposed Methods: The linear-in-input model was used for the hypothesis set . As the initializer of , the ERM minimizer trained by SVM was used. For both NGA and BFGS, gradient updates were iterated 300 times. NGA and normalized BFGS are referred to as U-GD and U-BFGS below, respectively. The surrogate loss shown in Fig. 3 was used: when and when , where was set to in the F1-measure case and in the Jaccard index case.444 The discrepancy parameter should be chosen within and for the F1-measure and Jaccard index, respectively. Here, we fix them to the slightly small values than the upper limits of their ranges. In App. D.6, we study the relationship between performance sensitivity on . The training set was divided into 4 to 1 and the latter set was used for validation. We used a common learning rate in Algorithm 1, which was chosen from by cross validation.

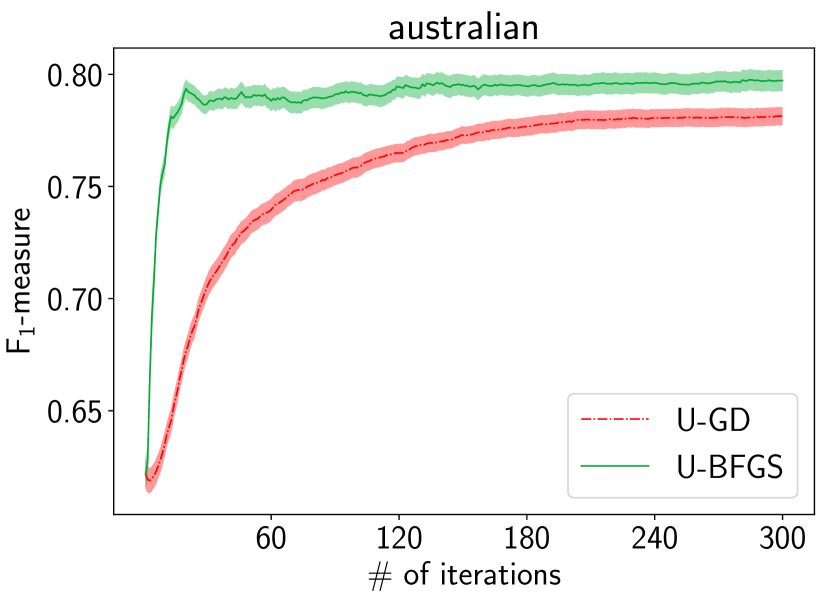

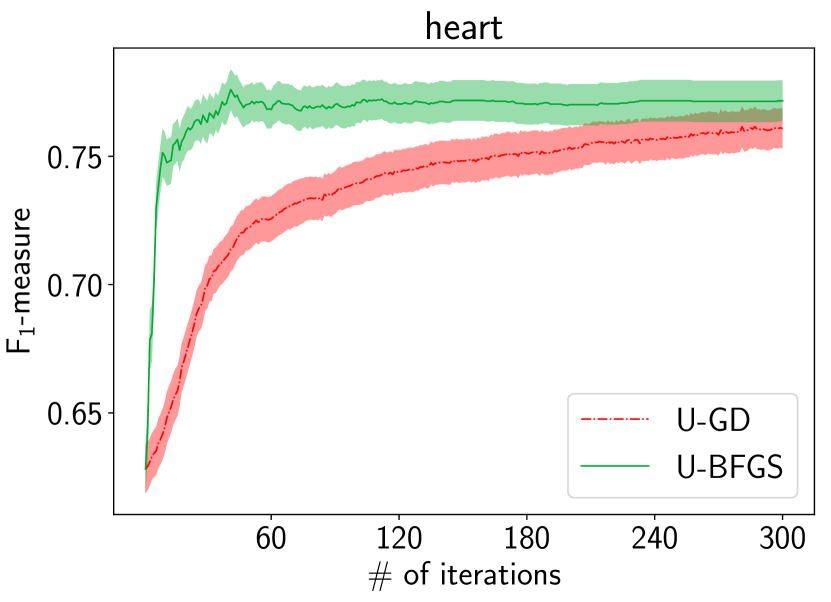

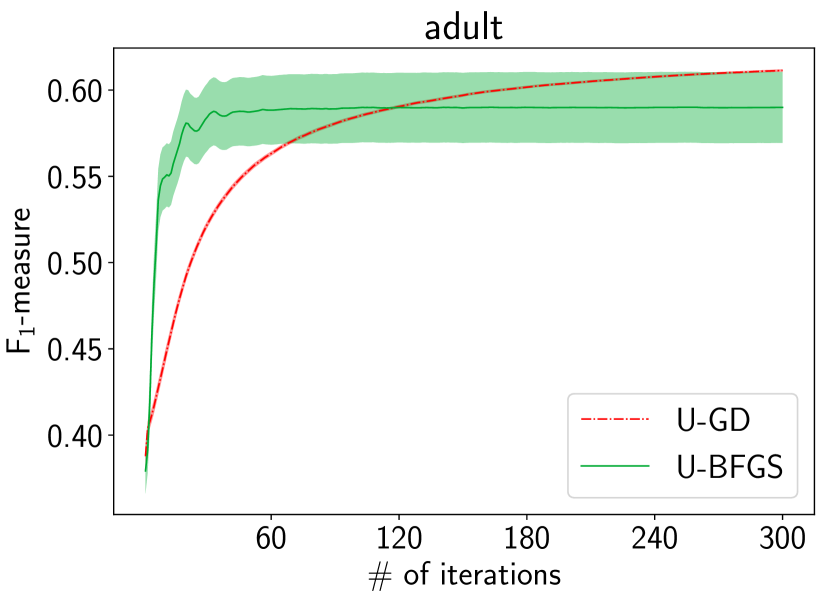

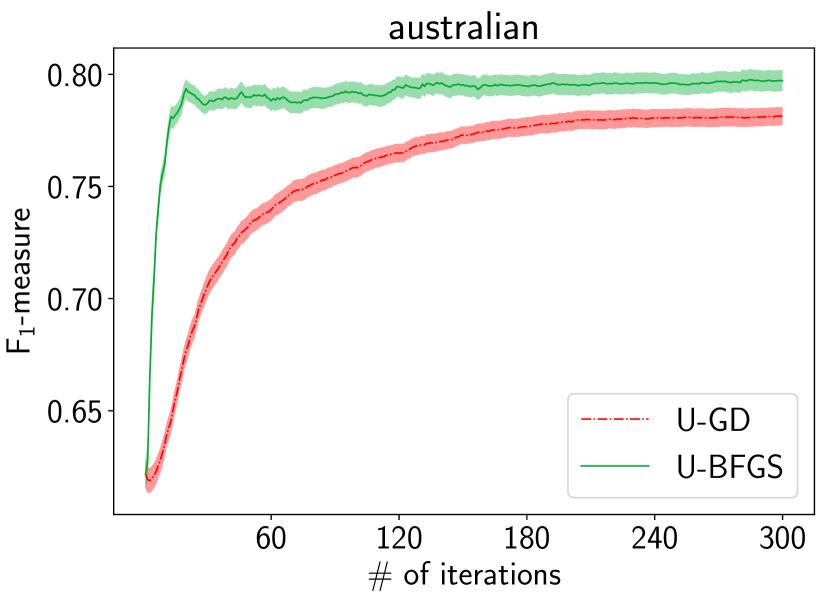

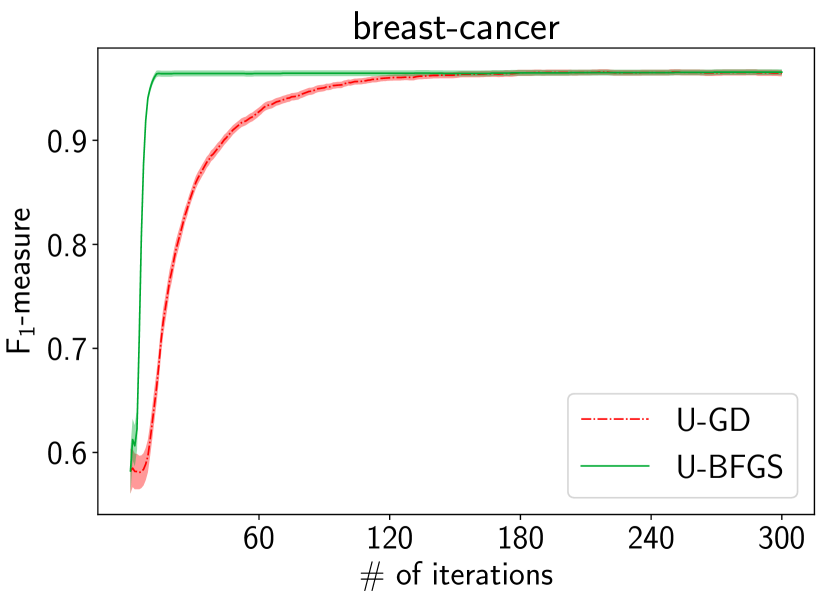

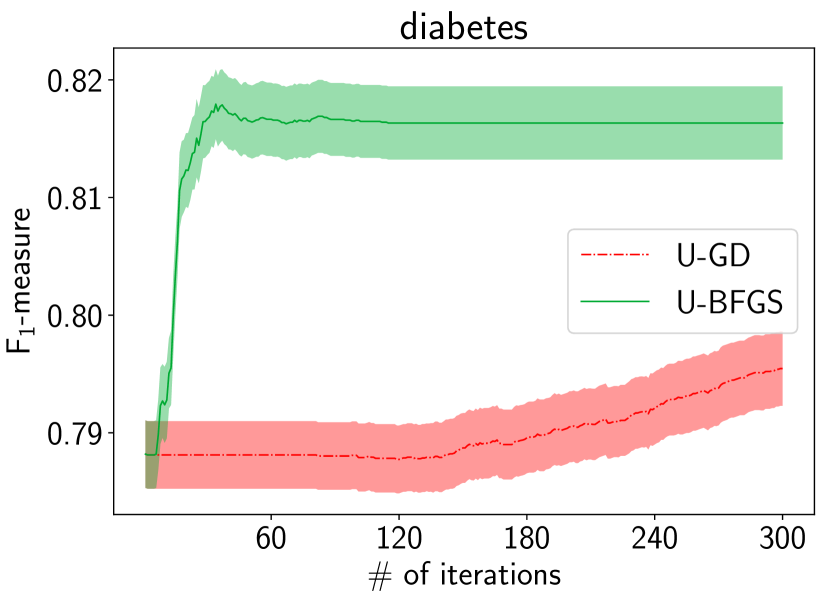

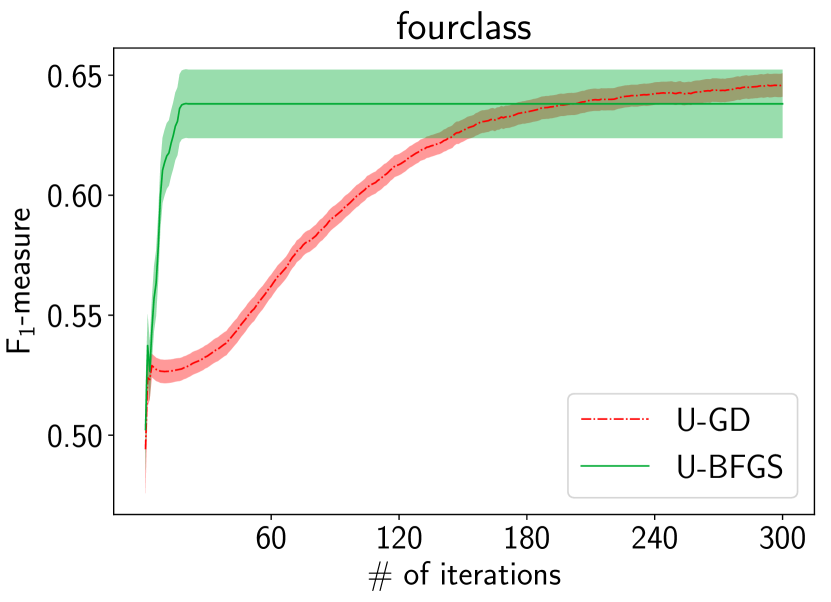

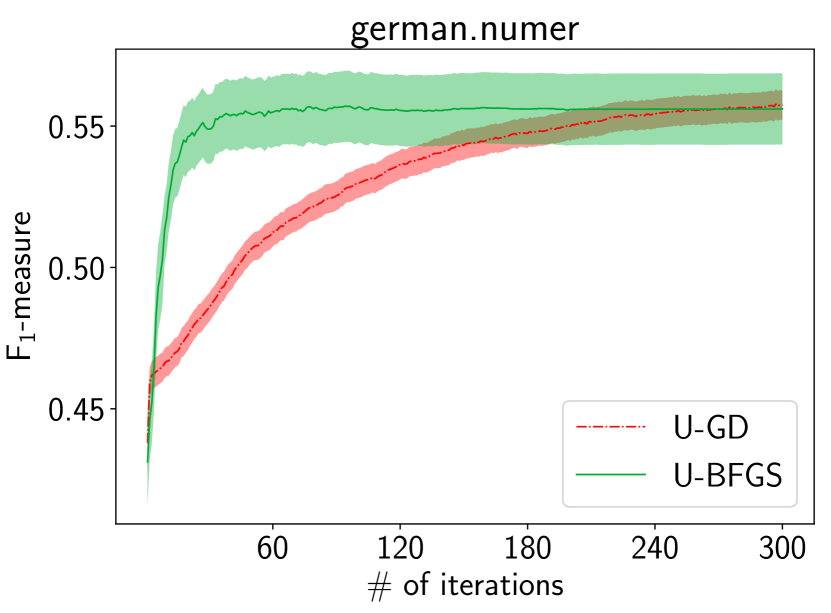

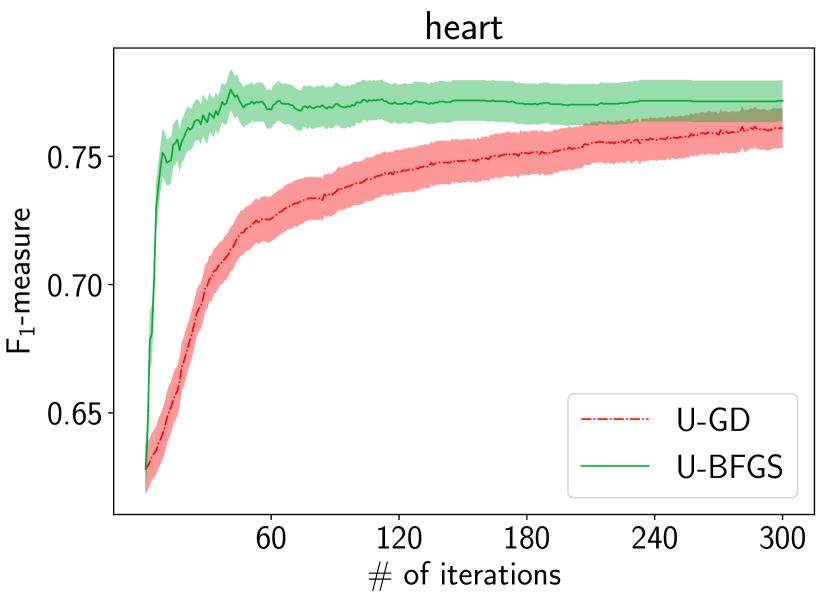

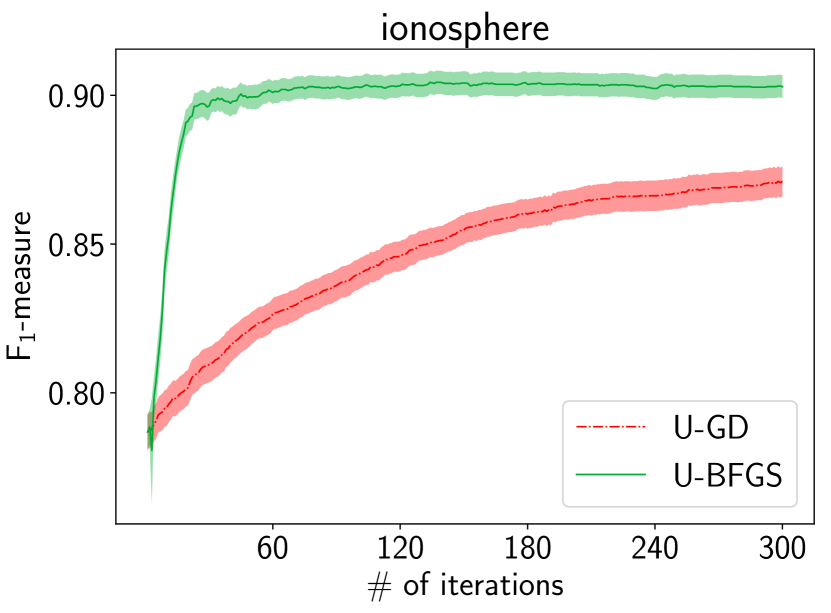

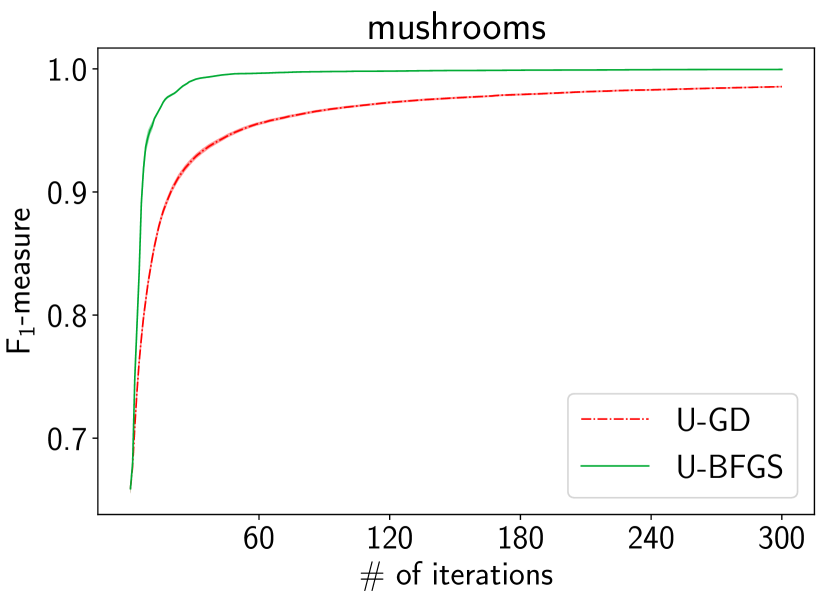

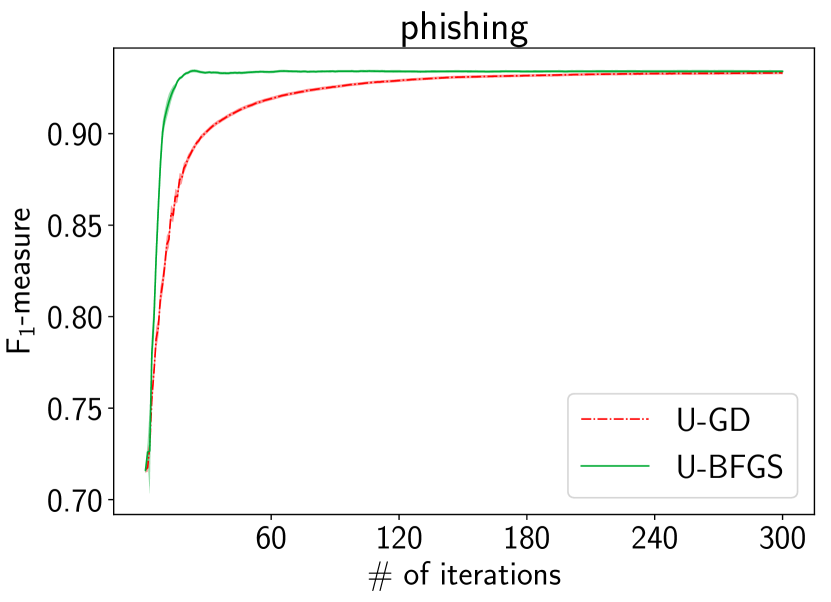

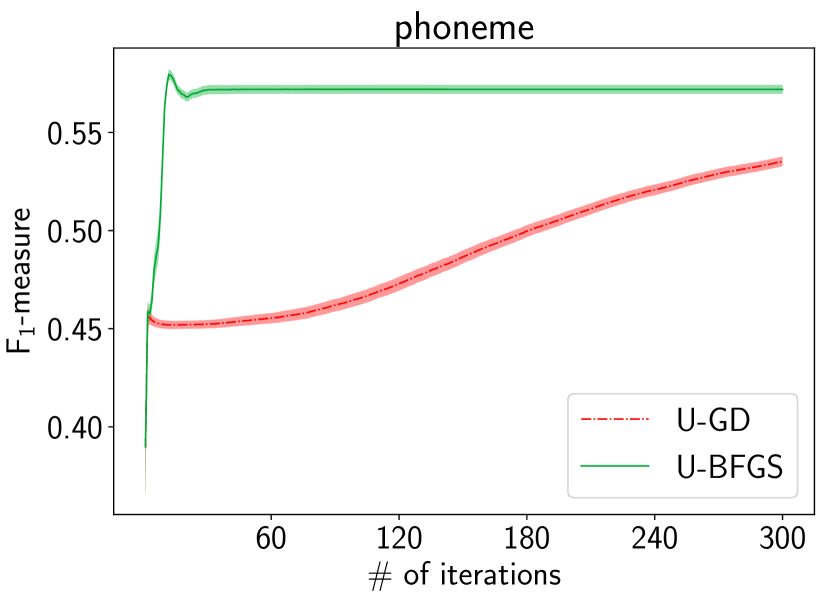

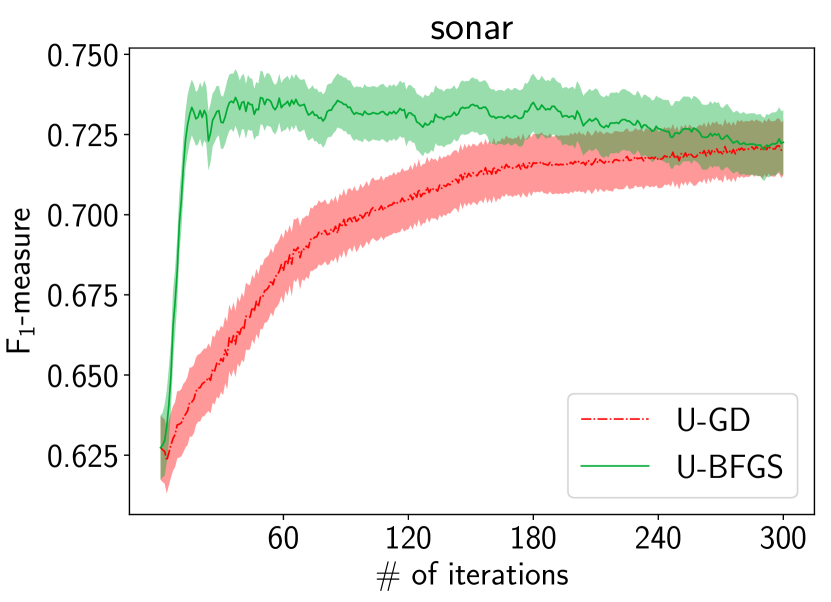

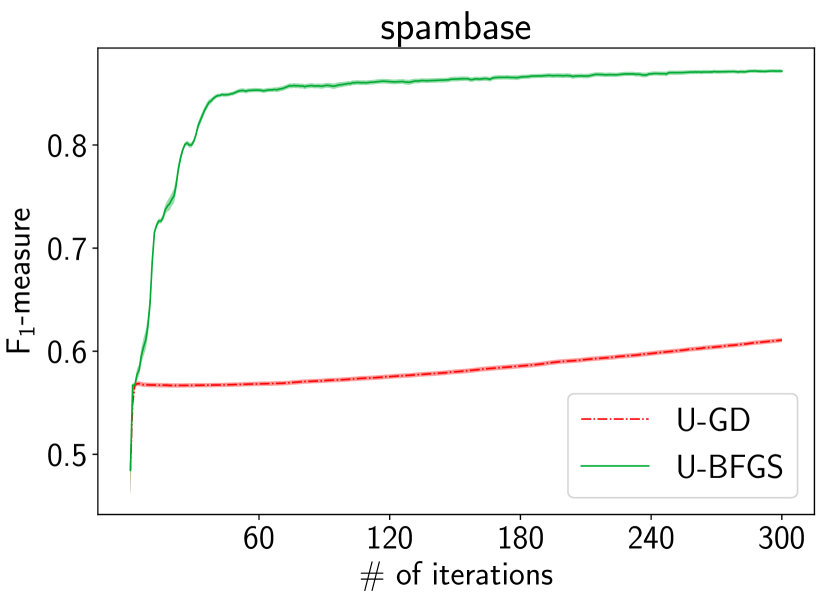

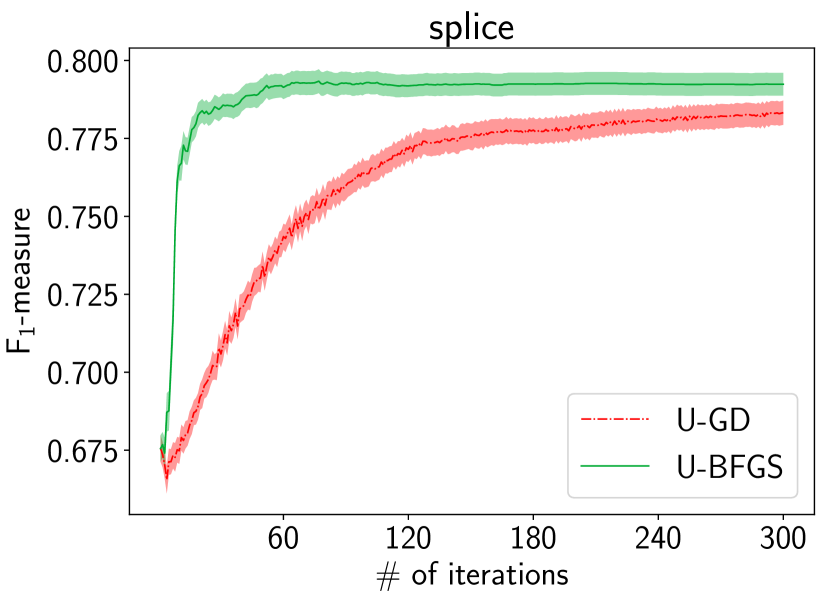

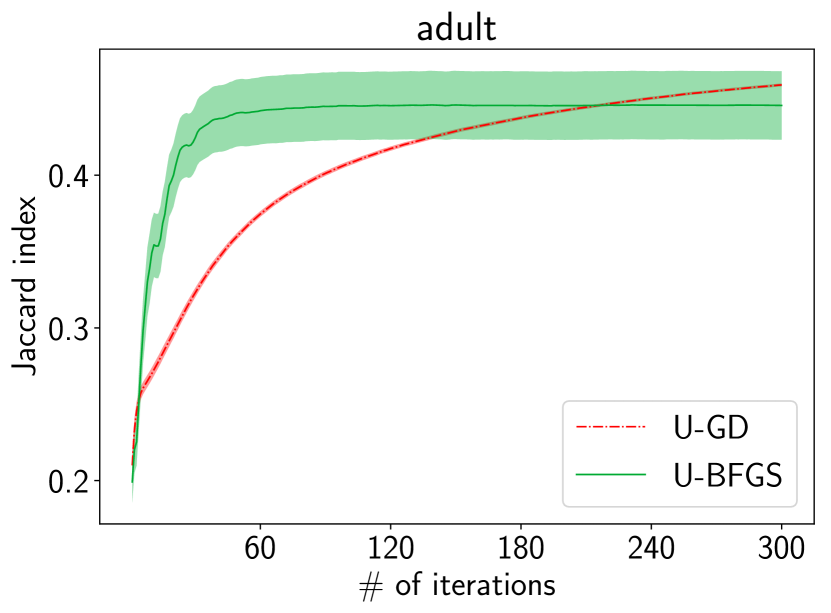

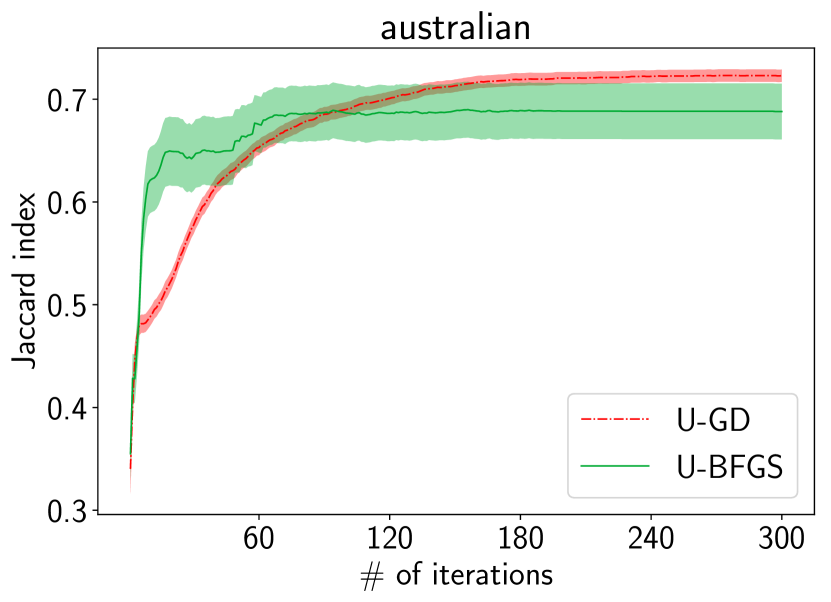

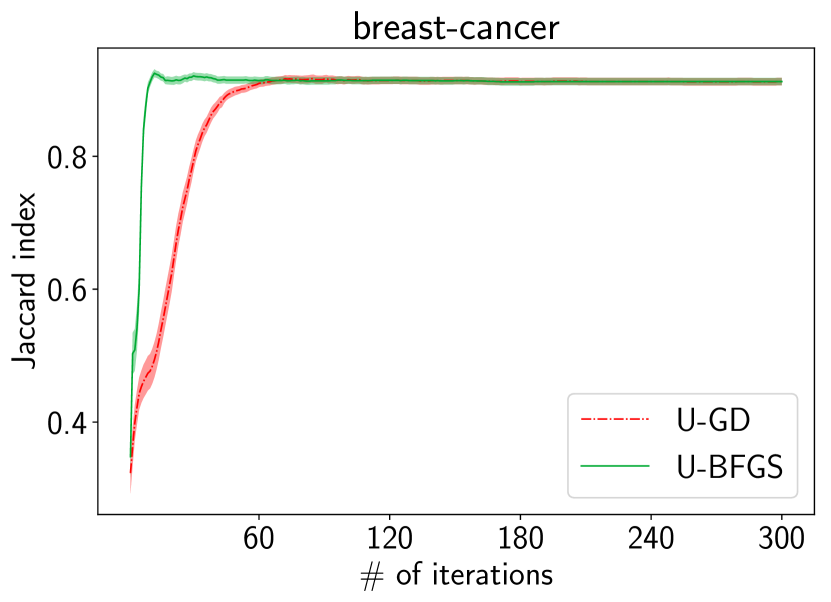

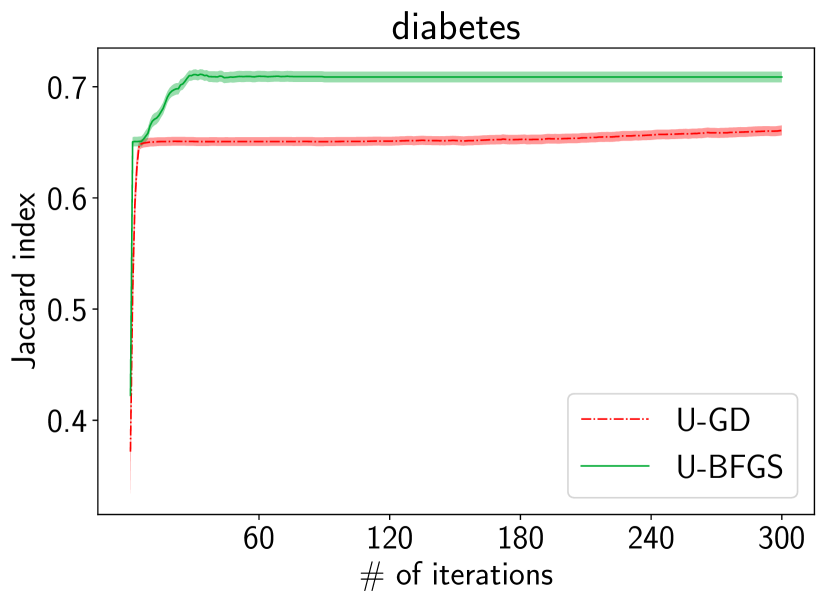

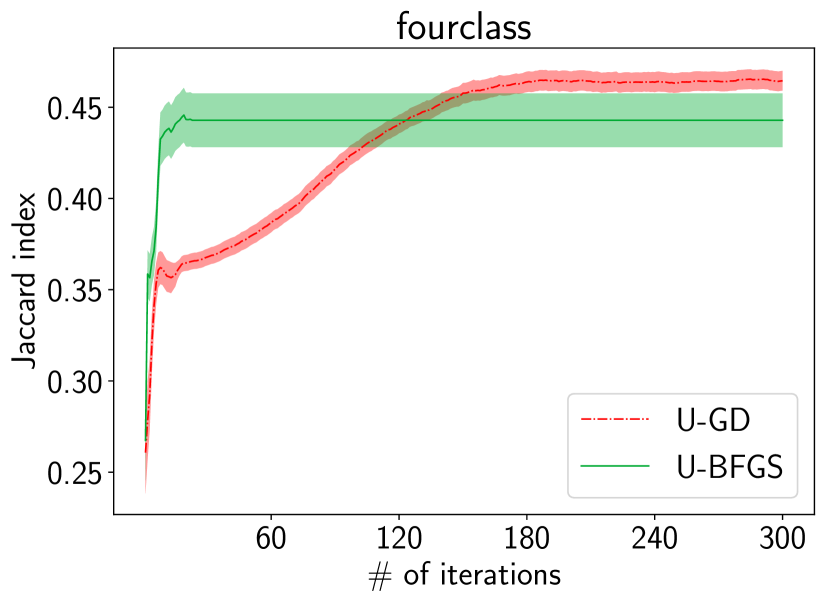

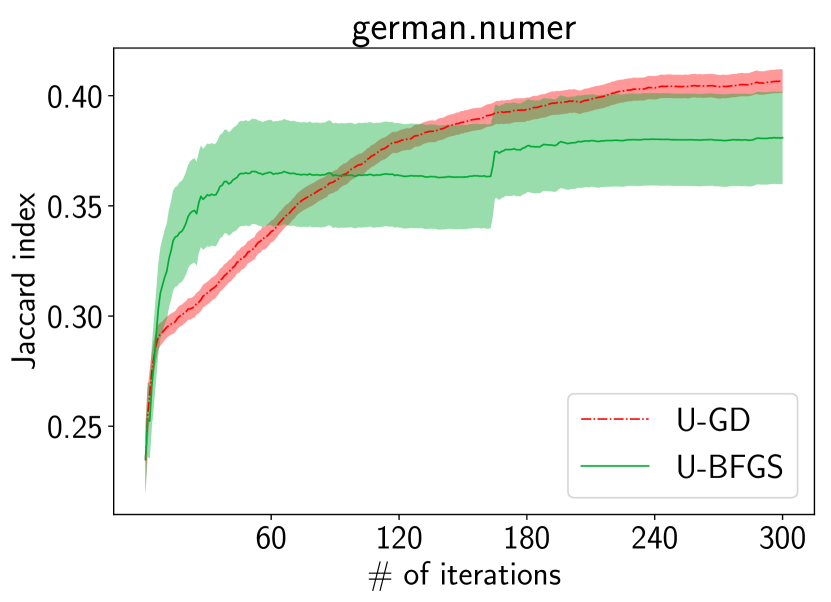

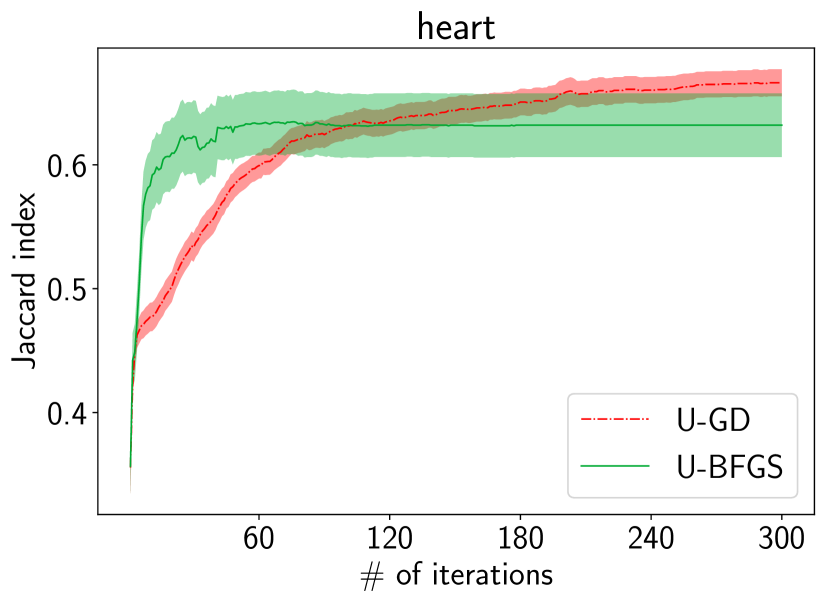

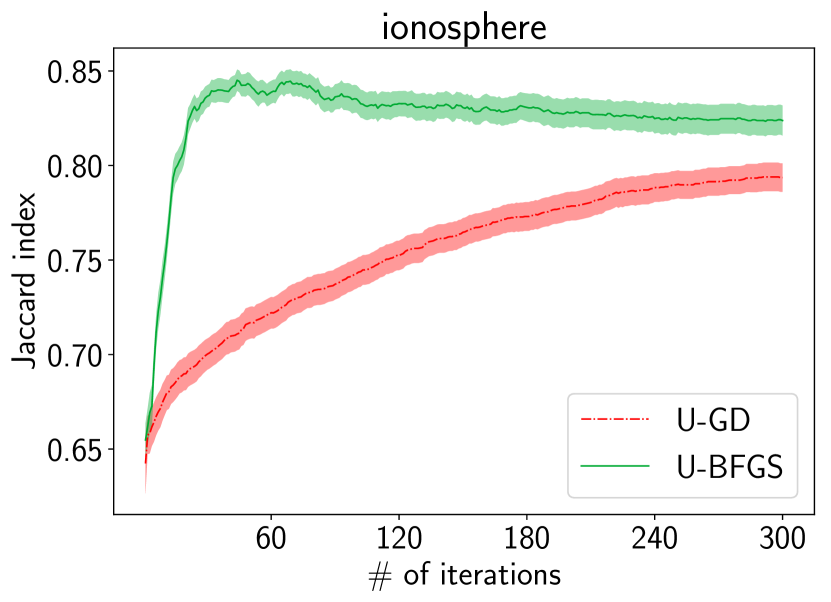

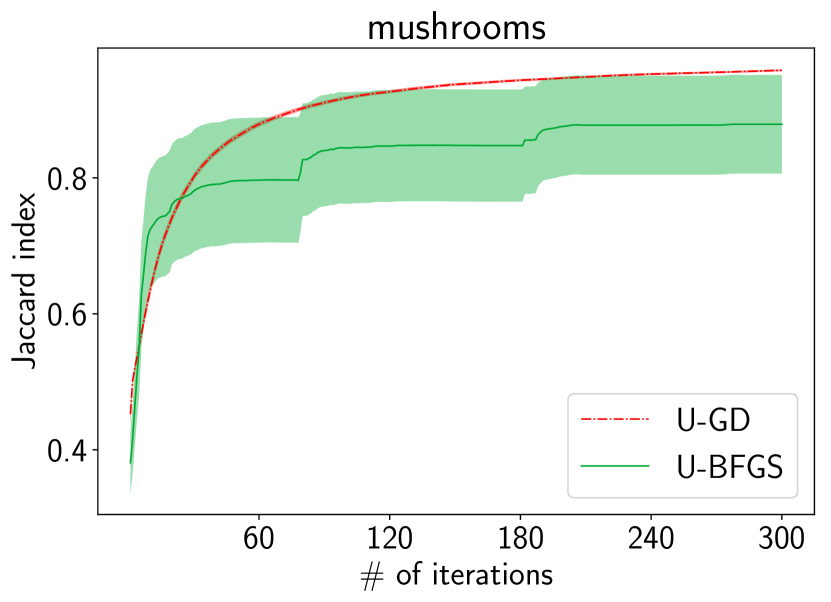

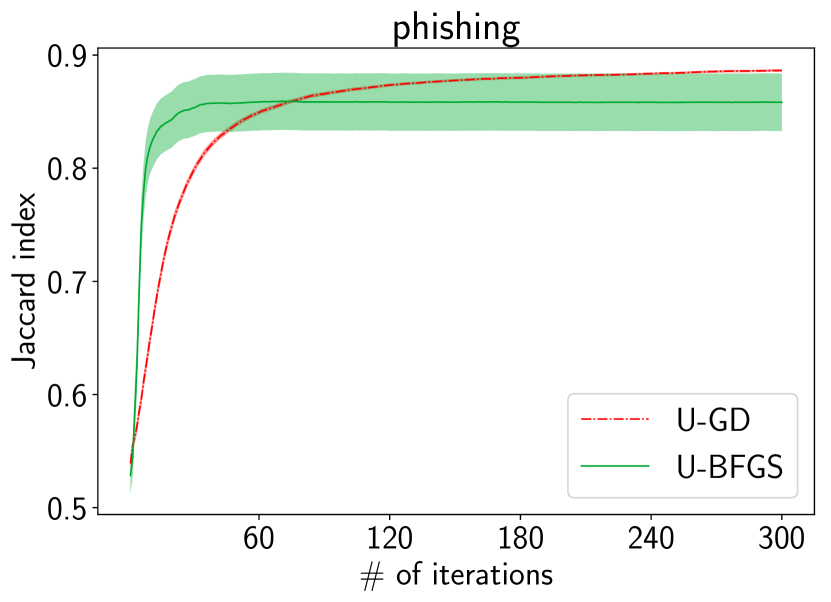

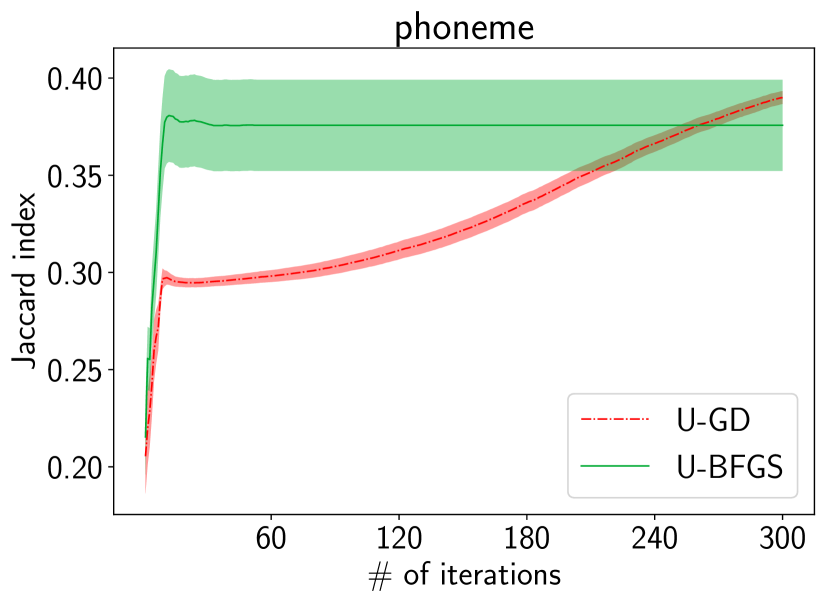

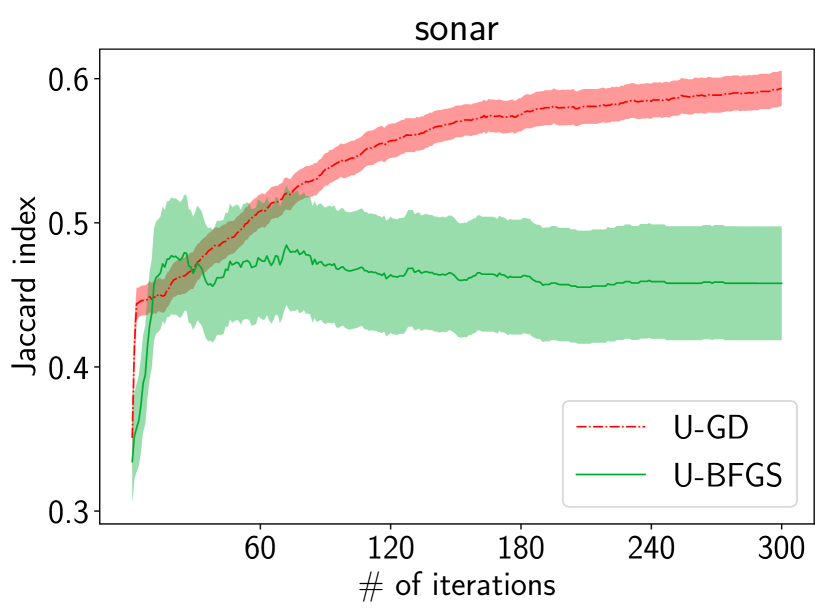

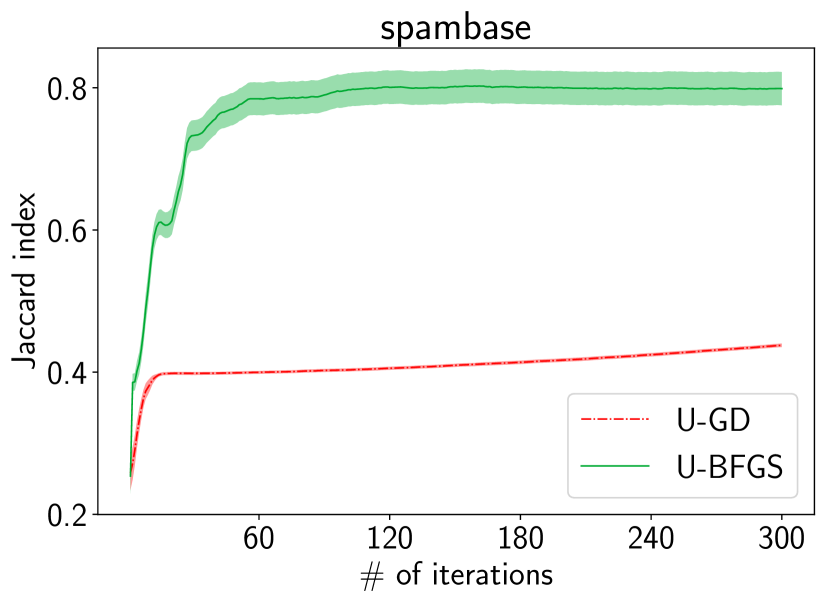

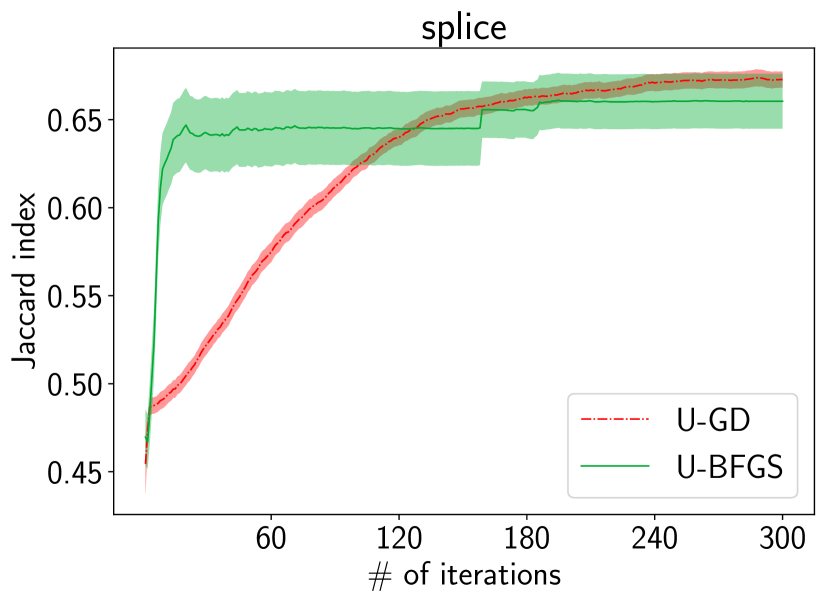

Convergence Comparison: We compare convergence behaviors of U-GD and U-BFGS. In this experiment, we ran them 300 iterations from randomly initialized parameters drawn from . The results are summarized in Fig. 4. As we expected, U-BFGS converges much faster than U-GD in most of the cases, up to 30 iterations. Note that U-BFGS and U-GD are in the trade-off relationship in that the former converges within fewer steps while the latter can update the solution faster in each step.

Performance Comparison in Benchmark: We compared the proposed methods with baselines. The results of the F1-measure and Jaccard index are summarized in Tab. 3, respectively, from which we can see the better or at least comparable performances of the proposed methods.

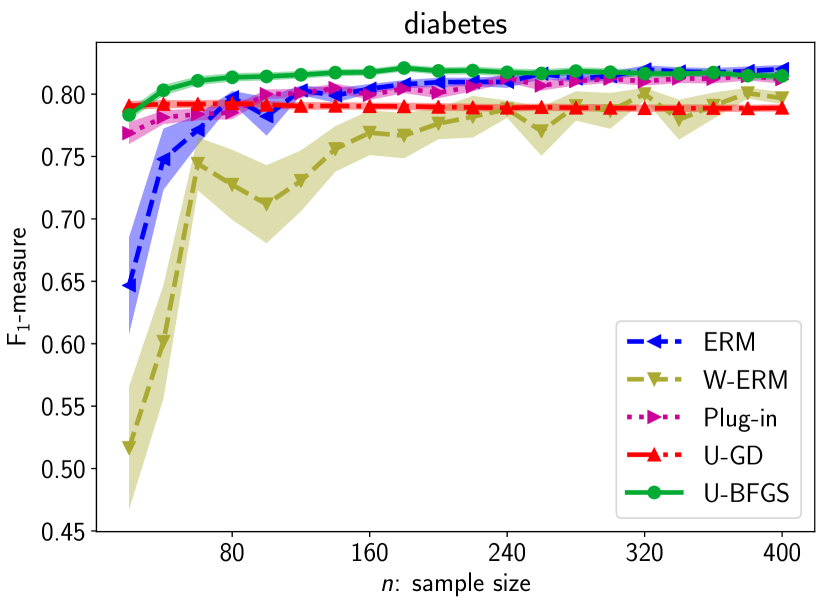

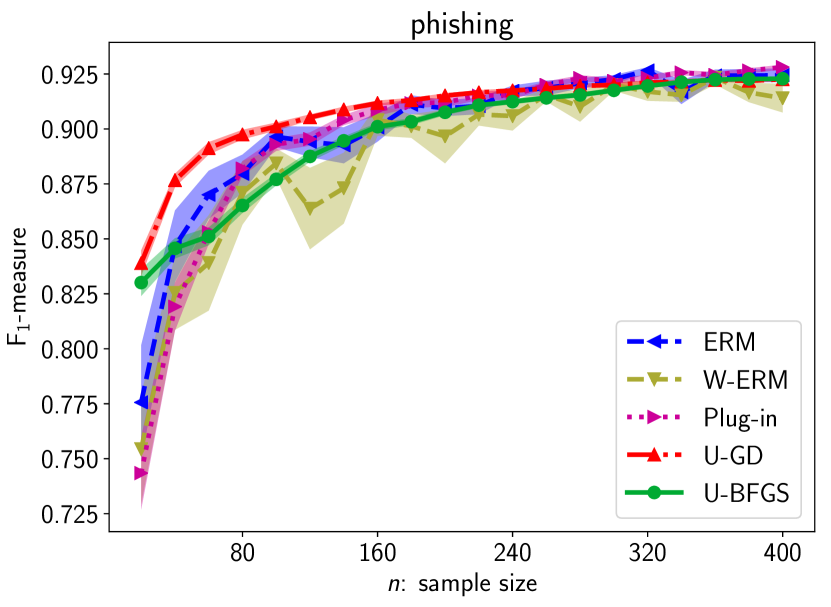

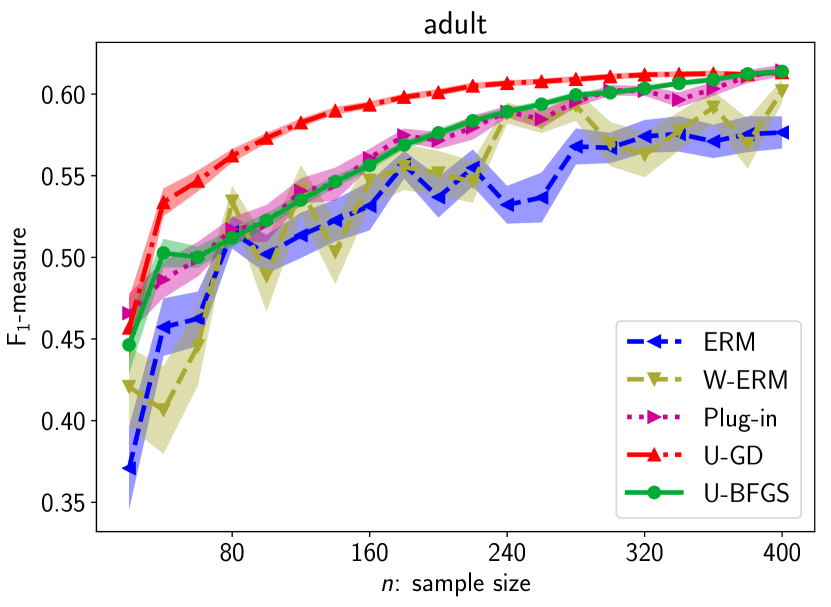

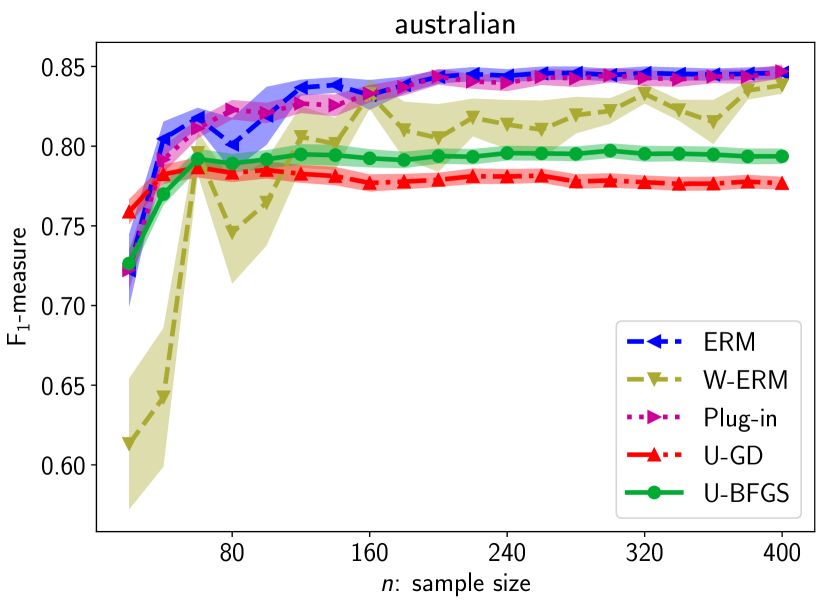

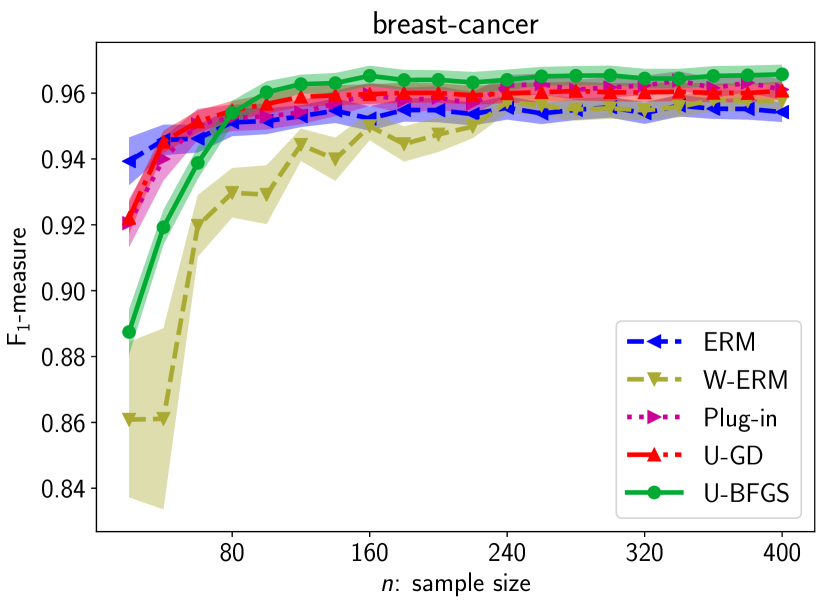

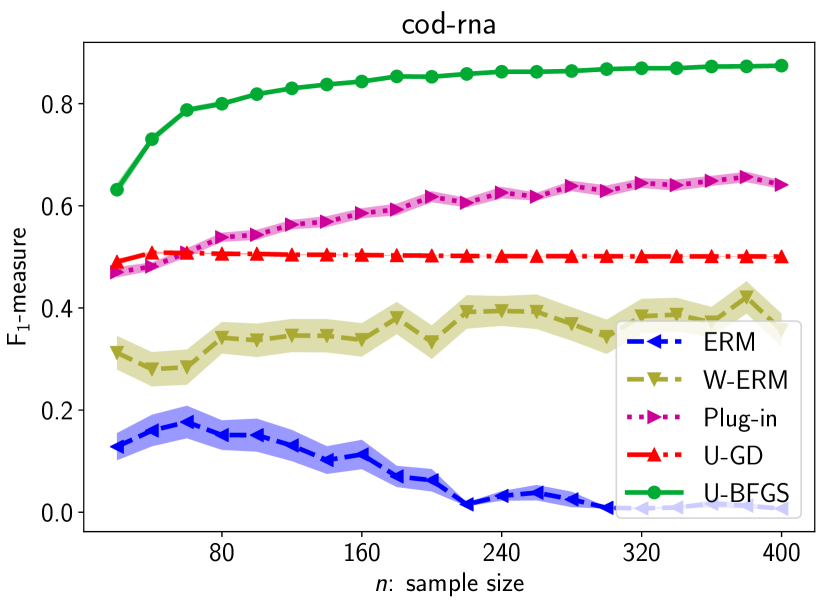

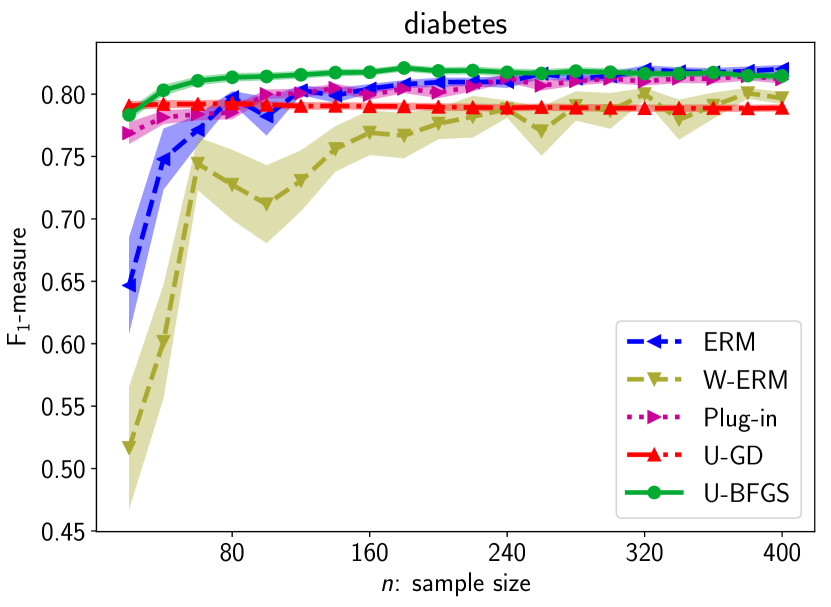

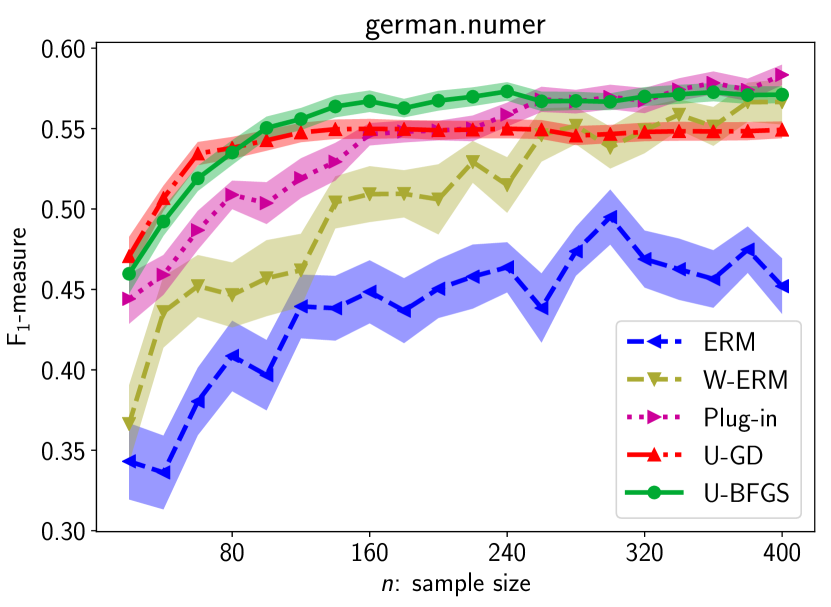

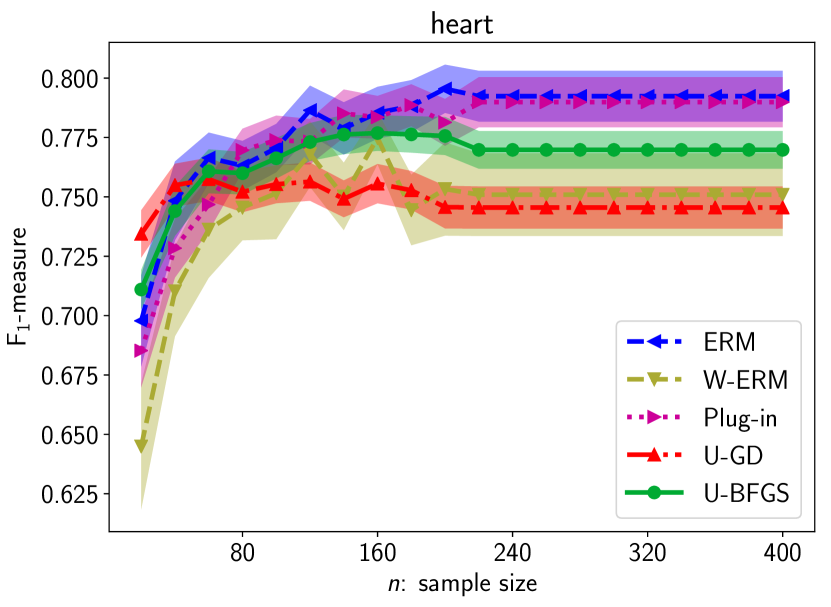

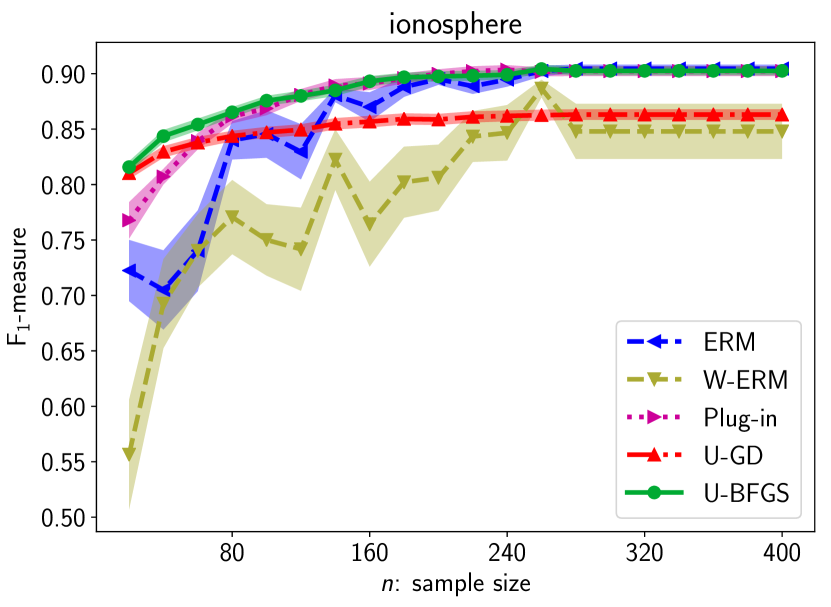

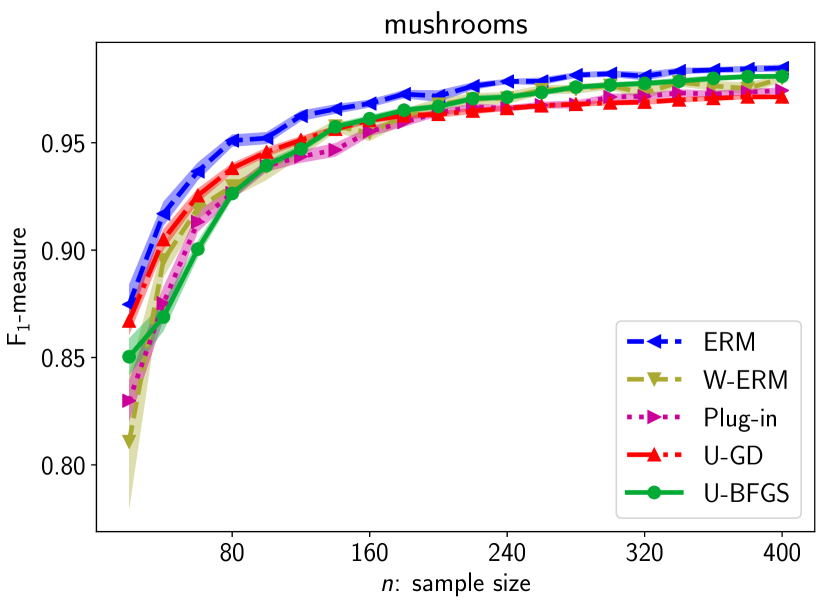

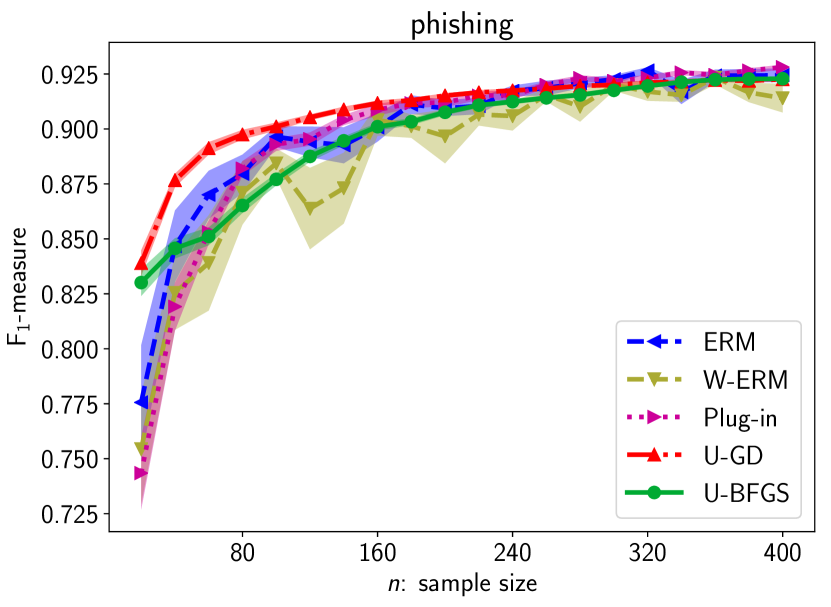

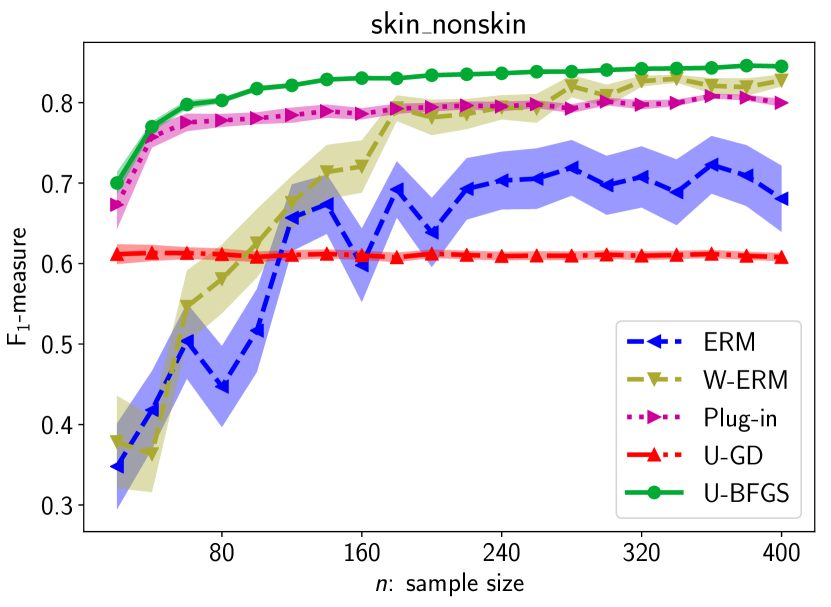

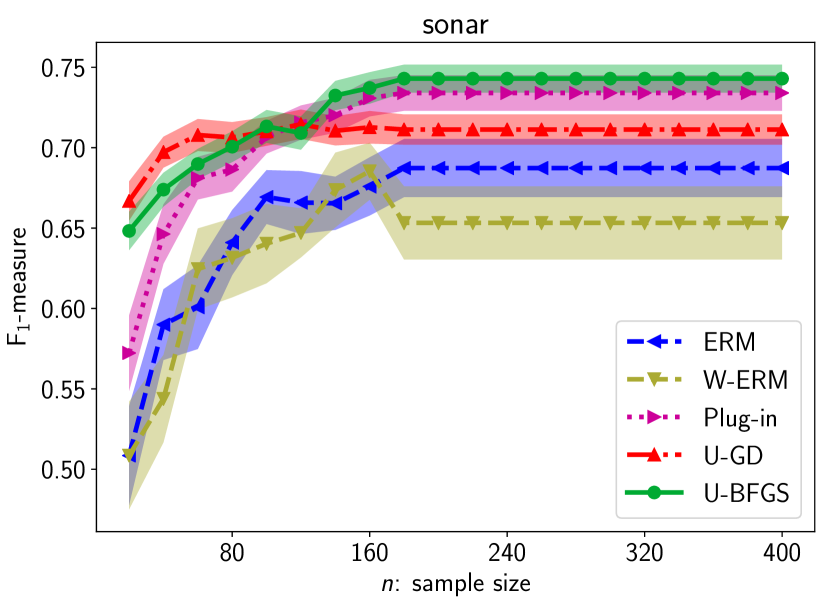

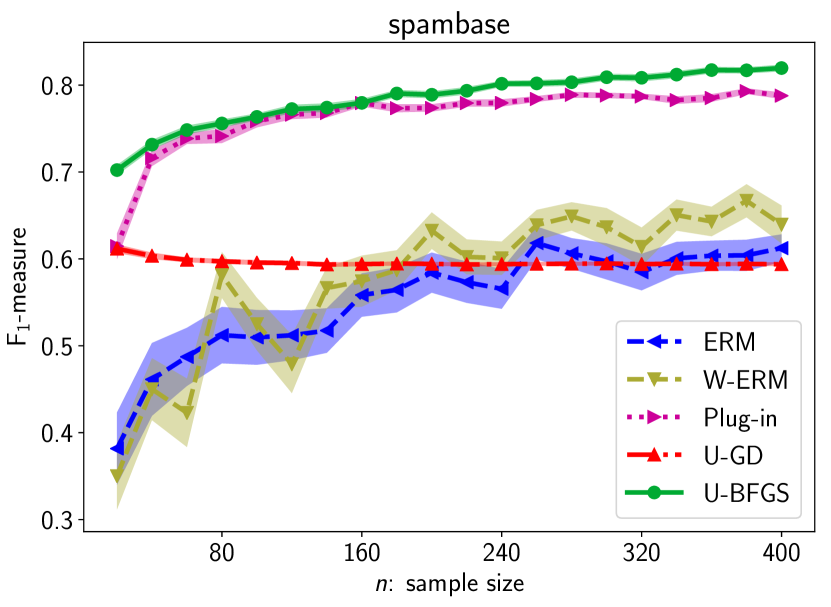

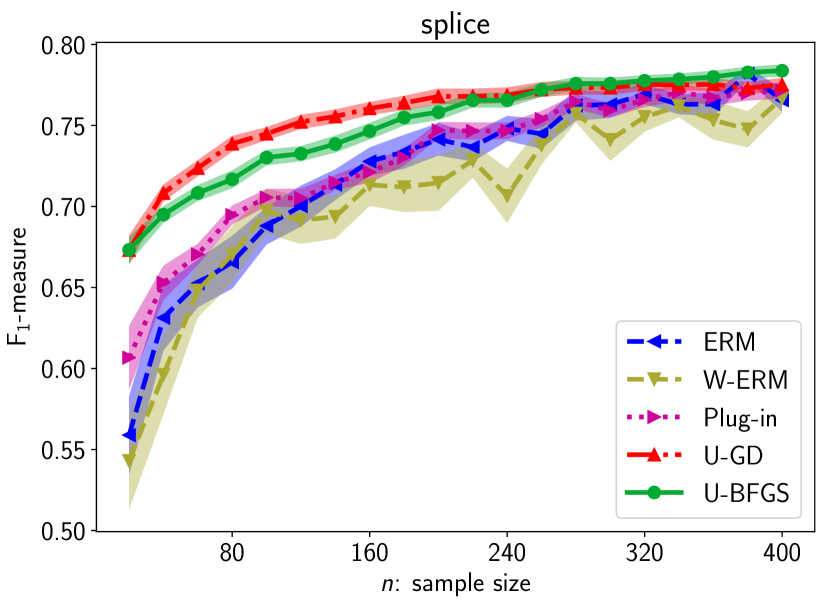

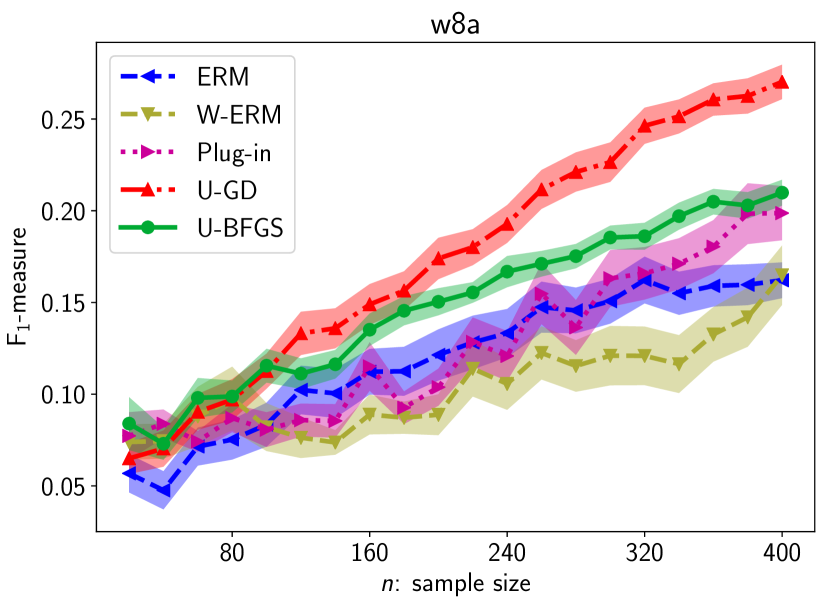

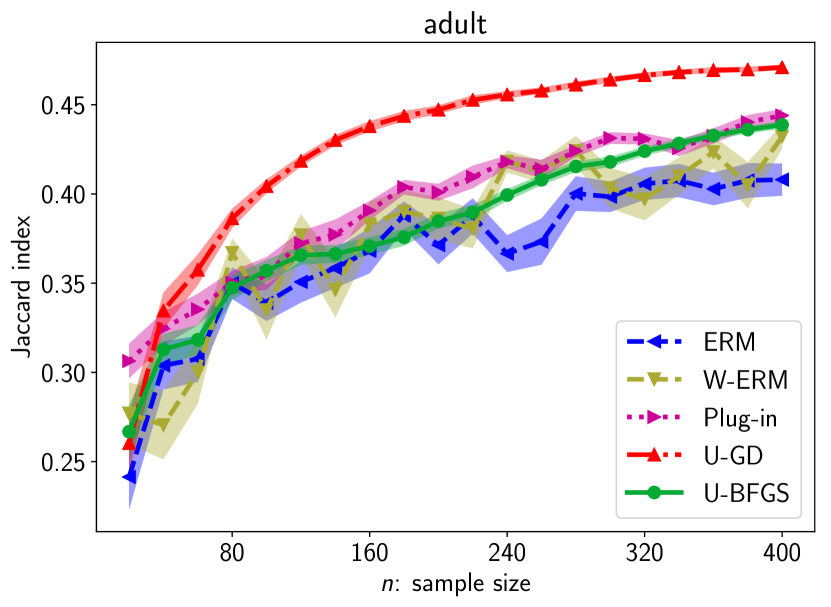

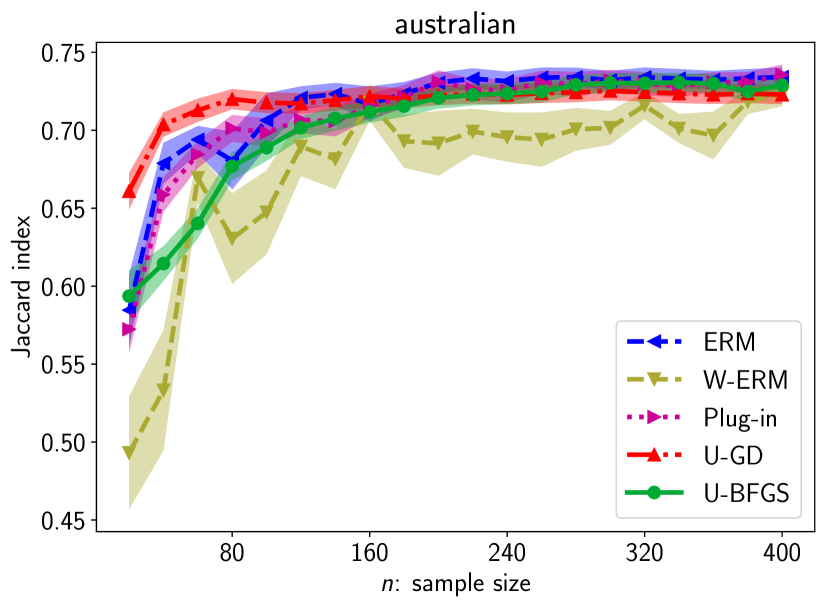

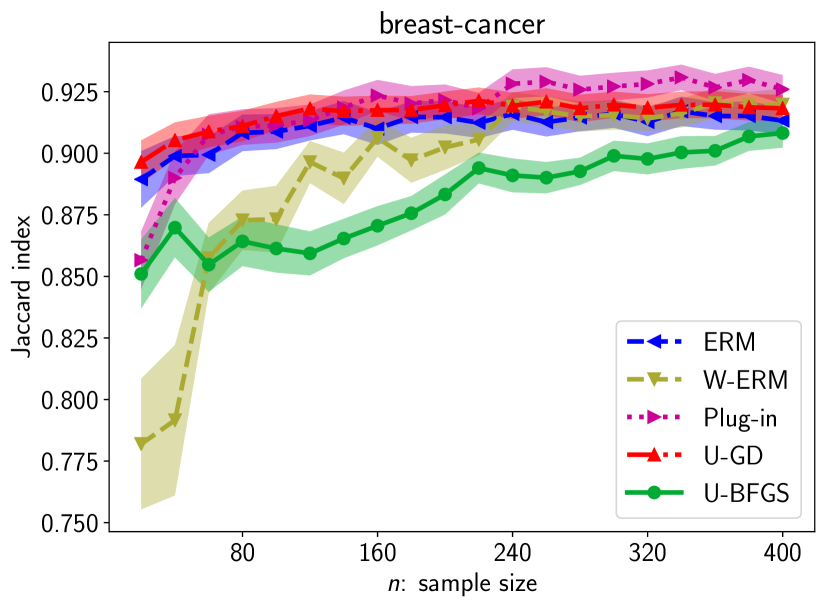

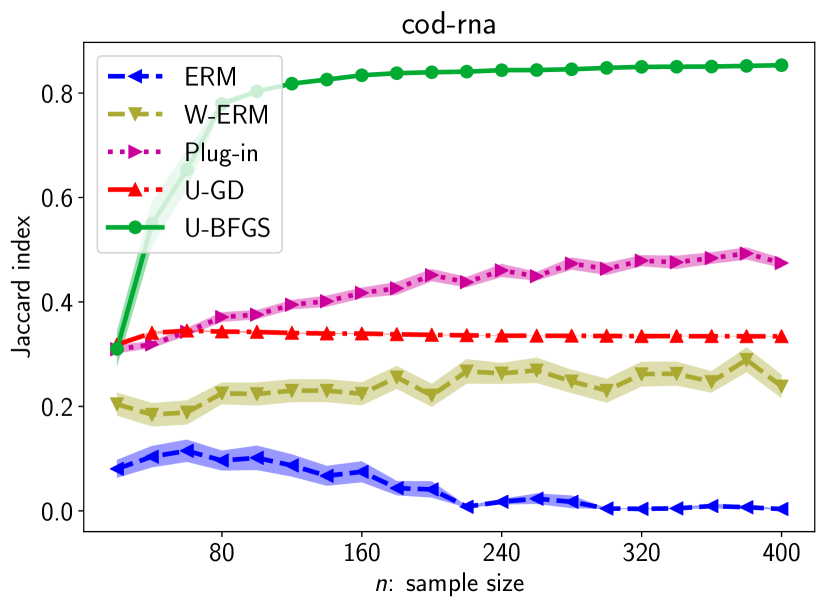

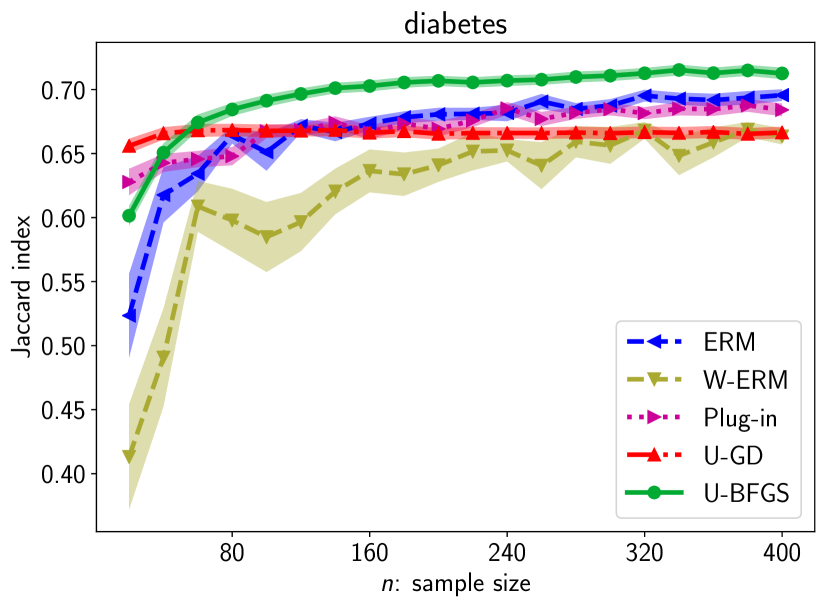

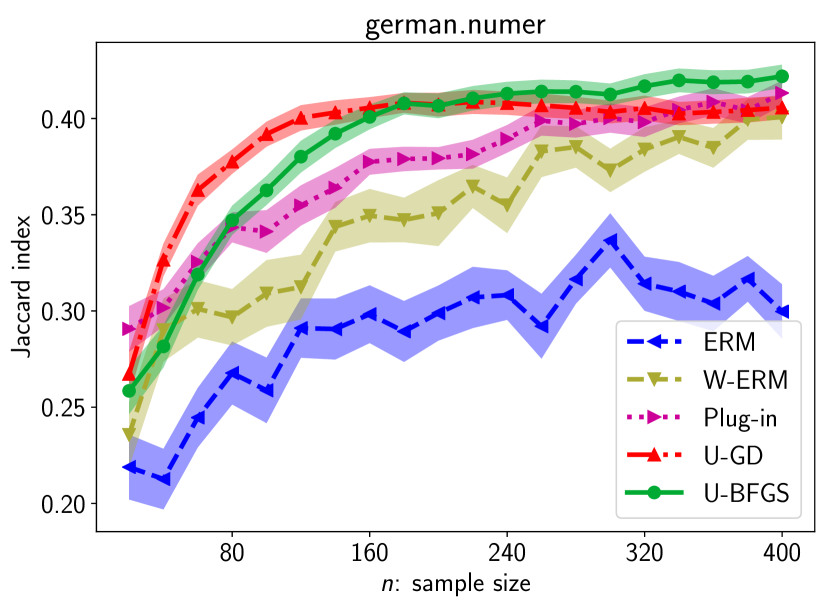

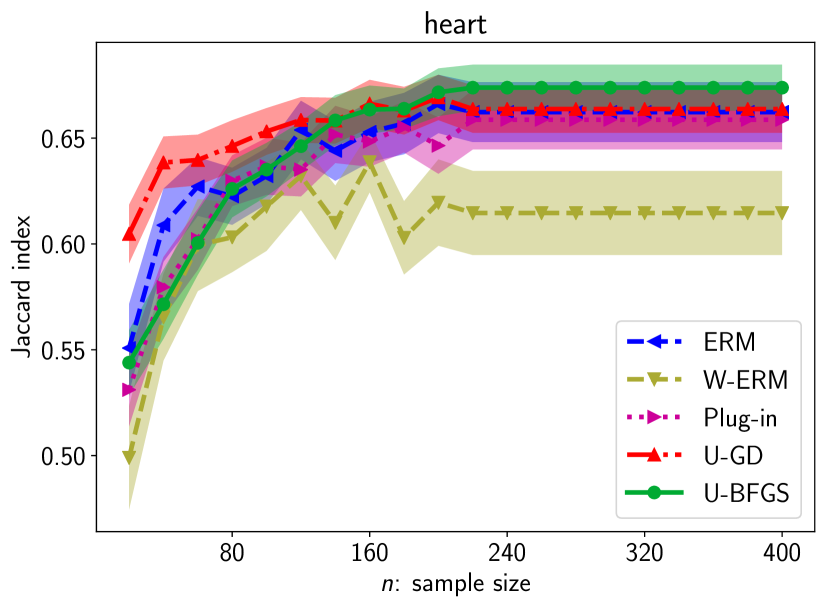

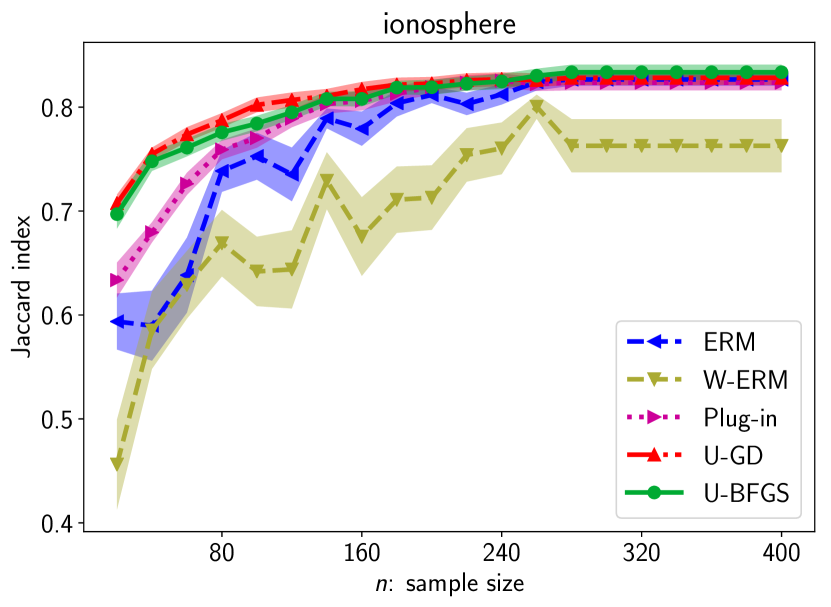

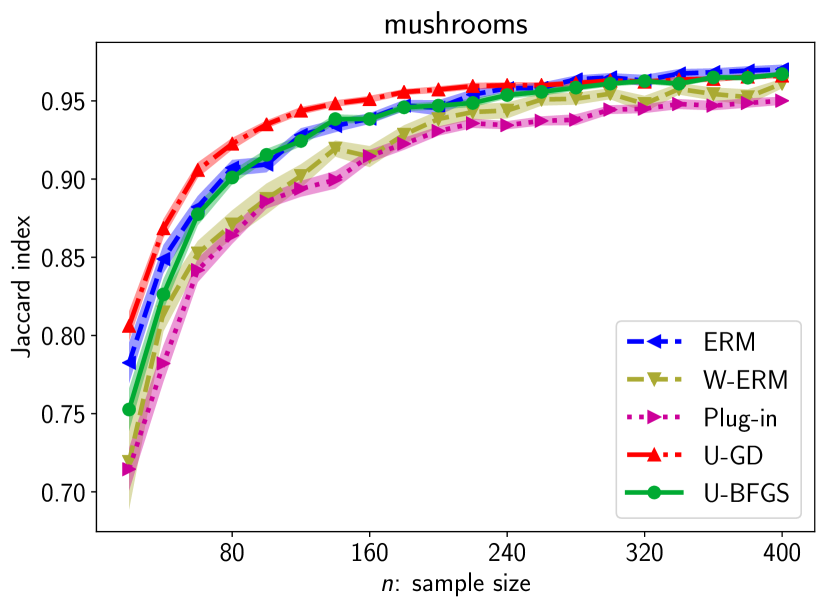

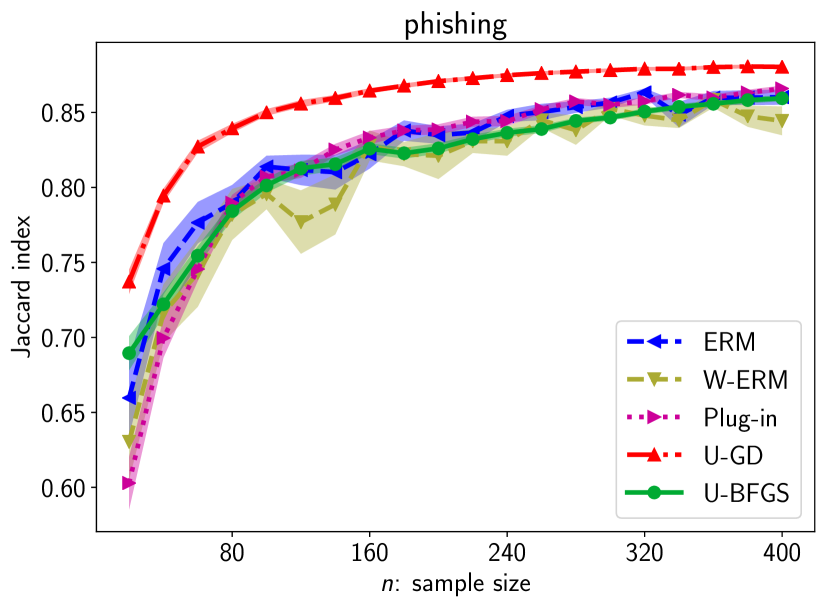

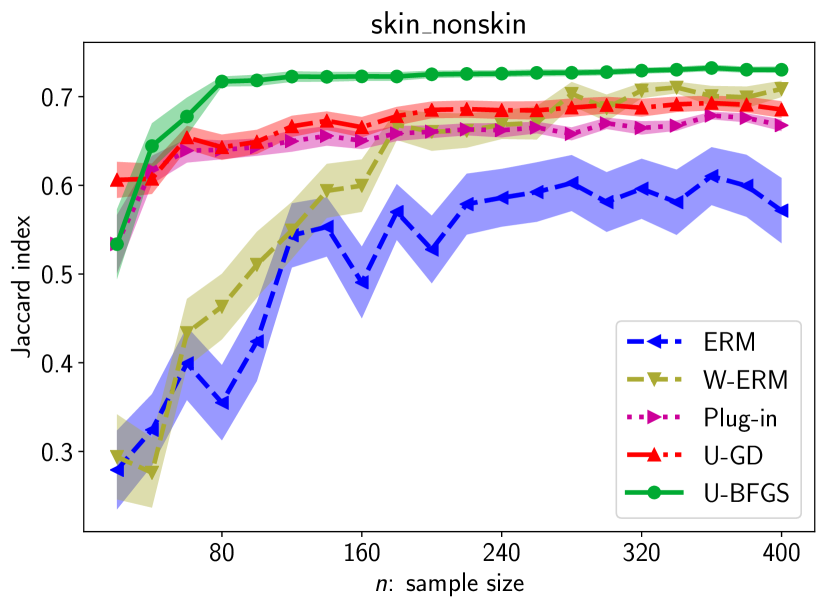

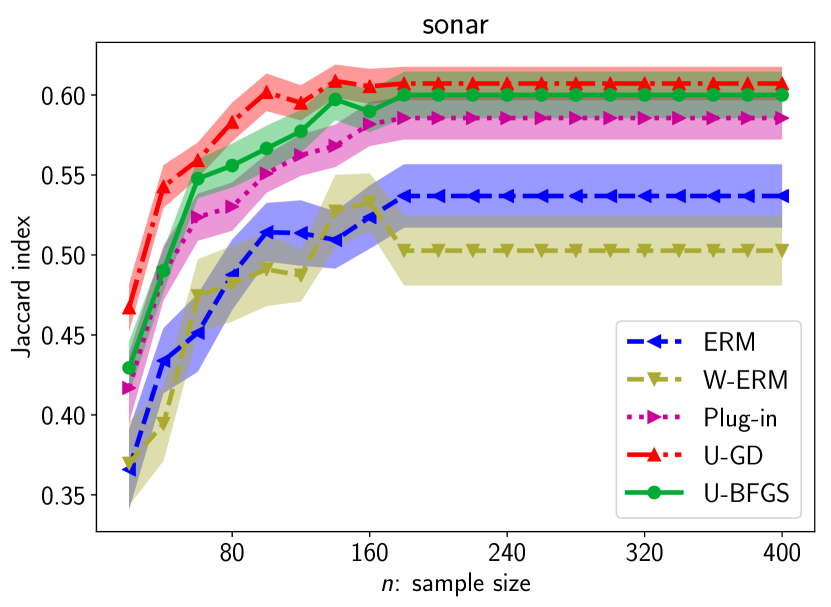

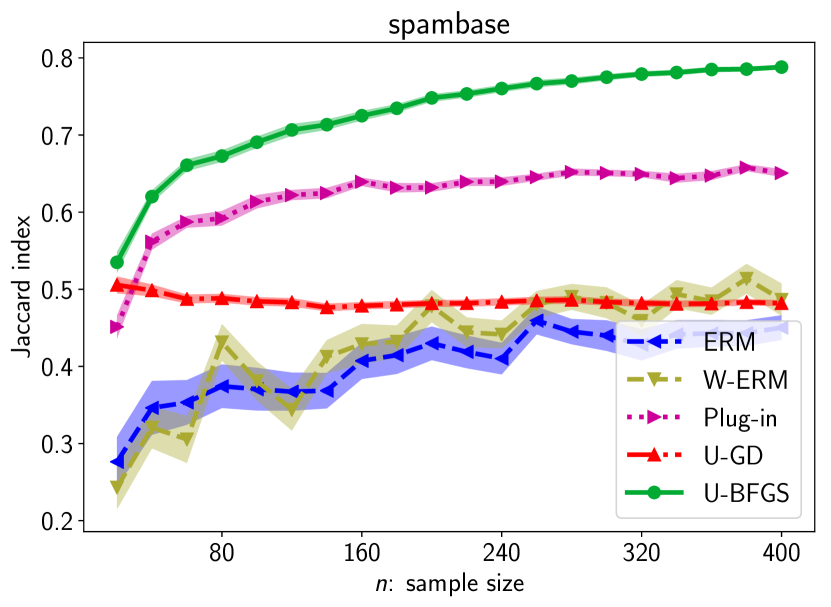

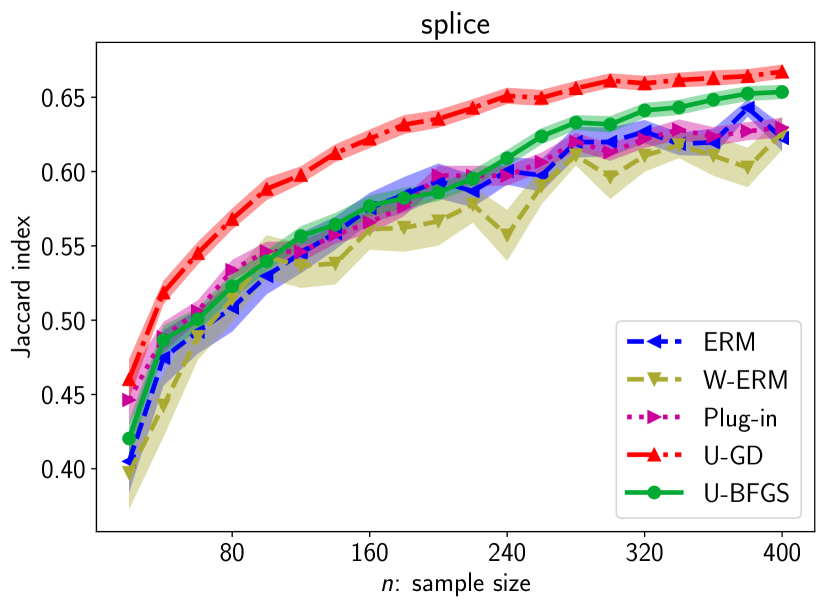

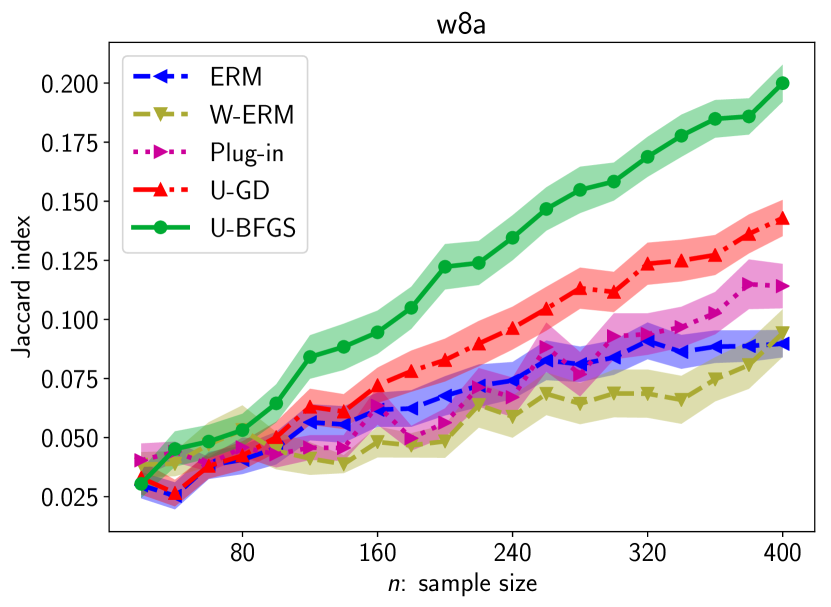

Sample Complexity: We empirically study the relationship between the performance and the sample size. We randomly subsample each original dataset to reduce the sample sizes to , and train all methods on the reduced samples. The experimental results are shown in Fig. 5. Overall, U-GD and U-BFGS outperform, which is especially significant when the sample sizes are quite small. It is worth noting that U-GD works even better than U-BFGS in some cases, though U-GD does not behave significantly better in Tab. 3. This can happen because the Hessian approximation in BFGS might not work well when the sample sizes are extremely small.

8 Conclusion

In this work, we gave a new insight into the calibrated surrogate for the linear-fractional metrics. Sufficient conditions for the surrogate calibration were stated, which is the first calibration result for the linear-fractional metrics to the best of our knowledge. The surrogate maximization can be performed by the combination of concave and quasi-concave programs, and its performance is validated via simulations.

Acknowledgement

We would like to thank Nontawat Charoenphakdee, Junya Honda, and Akiko Takeda for fruitful discussions. HB was supported by JST, ACT-I, Japan, Grant Number JPMJPR18UI. MS was supported by JST CREST Grant Number JPMJCR18A2.

References

- Ahmed et al., (2015) Ahmed, F., Tarlow, D., and Batra, D. (2015). Optimizing expected Intersection-over-Union with candidate-constrained CRFs. In CVPR, pages 1850–1858.

- Bartlett et al., (2006) Bartlett, P. L., Jordan, M. I., and McAuliffe, J. D. (2006). Convexity, classification, and risk bounds. Journal of the American Statistical Association, 101(473):138–156.

- Bartlett and Mendelson, (2002) Bartlett, P. L. and Mendelson, S. (2002). Rademacher and Gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research, 3(Nov):463–482.

- Ben-David et al., (2003) Ben-David, S., Eiron, N., and Long, P. M. (2003). On the difficulty of approximately maximizing agreements. Journal of Computer and System Sciences, 66(3):496–514.

- Berman et al., (2018) Berman, M., Triki, A. R., and Blaschko, M. B. (2018). The Lovász-Softmax loss: A tractable surrogate for the optimization of the intersection-over-union measure in neural networks. In CVPR.

- Bousquet et al., (2004) Bousquet, O., Boucheron, S., and Lugosi, G. (2004). Introduction to statistical learning theory. In Advanced Lectures on Machine Learning, pages 169–207. Springer.

- Boyd and Vandenberghe, (2004) Boyd, S. and Vandenberghe, L. (2004). Convex Optimization. Cambridge University Press.

- Brodersen et al., (2010) Brodersen, K. H., Ong, C. S., Stephan, K. E., and Buhmann, J. M. (2010). The balanced accuracy and its posterior distribution. In ICPR, pages 3121–3124.

- Busa-Fekete et al., (2015) Busa-Fekete, R., Szörényi, B., Dembczyński, K., and Hüllermeier, E. (2015). Online F-measure optimization. In NeurIPS, pages 595–603.

- Chang and Lin, (2011) Chang, C.-C. and Lin, C.-J. (2011). LIBSVM: A library for support vector machines. ACM Transactions on Intelligent Systems and Technology. Software available at http://www.csie.ntu.edu.tw/~cjlin/libsvm.

- Charoenphakdee et al., (2019) Charoenphakdee, N., Lee, J., and Sugiyama, M. (2019). On symmetric losses for learning from corrupted labels. In ICML.

- Csurka et al., (2013) Csurka, G., Larlus, D., Perronnin, F., and Meylan, F. (2013). What is a good evaluation measure for semantic segmentation? In BMVC, pages 1–11.

- Dembczyński et al., (2013) Dembczyński, K., Jachnik, A., Kotłowski, W., Waegeman, W., and Hüllermeier, E. (2013). Optimizing the F-measure in multi-label classification: Plug-in rule approach versus structured loss minimization. In ICML, pages 1130–1138.

- Dembczyński et al., (2017) Dembczyński, K., Kotłowski, W., Koyejo, O., and Natarajan, N. (2017). Consistency analysis for binary classification revisited. In ICML, pages 961–969.

- Eban et al., (2017) Eban, E., Schain, M., Mackey, A., Gordon, A., Saurous, R. A., and Elidan, G. (2017). Scalable learning of non-decomposable objectives. In AISTATS, pages 832–840.

- Everingham et al., (2010) Everingham, M., Van Gool, L., Williams, C. K., Winn, J., and Zisserman, A. (2010). The PASCAL visual object classes (VOC) challenge. International Journal of Computer Vision, 88(2):303–338.

- Feldman et al., (2012) Feldman, V., Guruswami, V., Raghavendra, P., and Wu, Y. (2012). Agnostic learning of monomials by halfspaces is hard. SIAM Journal on Computing, 41(6):1558–1590.

- Fletcher, (2013) Fletcher, R. (2013). Practical Methods of Optimization. John Wiley & Sons.

- Gao and Zhou, (2015) Gao, W. and Zhou, Z.-H. (2015). On the consistency of AUC pairwise optimization. In IJCAI, pages 939–945.

- Gower and Legendre, (1986) Gower, J. C. and Legendre, P. (1986). Metric and euclidean properties of dissimilarity coefficients. Journal of Classification, 3(1):5–48.

- Hazan et al., (2015) Hazan, E., Levy, K., and Shalev-Shwartz, S. (2015). Beyond convexity: Stochastic quasi-convex optimization. In NeurIPS, pages 1594–1602.

- Jaccard, (1901) Jaccard, P. (1901). Étude de la distribution florale dans une portion des alpes et du jura. Bulletin de la Société Vaudoise des Sciences Naturelles, 37:547–579.

- Joachims, (2005) Joachims, T. (2005). A support vector method for multivariate performance measures. In ICML, pages 377–384.

- Kar et al., (2014) Kar, P., Narasimhan, H., and Jain, P. (2014). Online and stochastic gradient methods for non-decomposable loss functions. In NeurIPS, pages 694–702.

- Koyejo et al., (2014) Koyejo, O. O., Natarajan, N., Ravikumar, P. K., and Dhillon, I. S. (2014). Consistent binary classification with generalized performance metrics. In NeurIPS, pages 2744–2752.

- Ledoux and Talagrand, (1991) Ledoux, M. and Talagrand, M. (1991). Probability in Banach Spaces: Isoperimetry and Processes. Springer.

- Lichman, (2013) Lichman, M. (2013). UCI machine learning repository.

- Manning and Schütze, (2008) Manning, R. P. C. and Schütze, H. (2008). Introduction to Information Retrieval. Cambridge University Press.

- McDiarmid, (1989) McDiarmid, C. (1989). On the method of bounded differences. Surveys in Combinatorics, 141(1):148–188.

- Menon et al., (2013) Menon, A., Narasimhan, H., Agarwal, S., and Chawla, S. (2013). On the statistical consistency of algorithms for binary classification under class imbalance. In ICML, pages 603–611.

- Menon et al., (2015) Menon, A., van Rooyen, B., Ong, C. S., and Williamson, R. (2015). Learning from corrupted binary labels via class-probability estimation. In ICML, pages 125–134.

- Mohri et al., (2012) Mohri, M., Rostamizadeh, A., and Talkwalkar, A. (2012). Foundation of Machine learning. MIT Press.

- Nan et al., (2012) Nan, Y., Chai, K. M., Lee, W. S., and Chieu, H. L. (2012). Optimizing F-measure: A tale of two approaches. In ICML, pages 289–296.

- Narasimhan et al., (2015) Narasimhan, H., Kar, P., and Jain, P. (2015). Optimizing non-decomposable performance measures: a tale of two classes. In ICML, pages 199–208.

- Narasimhan et al., (2016) Narasimhan, H., Pan, W., Kar, P., Protopapas, P., and Ramaswamy, H. G. (2016). Optimizing the multiclass F-measure via biconcave programming. In ICDM, pages 1101–1106.

- Narasimhan et al., (2014) Narasimhan, H., Vaish, R., and Agarwal, S. (2014). On the statistical consistency of plug-in classifiers for non-decomposable performance measures. In NeurIPS, pages 1493–1501.

- Natarajan et al., (2016) Natarajan, N., Koyejo, O., Ravikumar, P., and Dhillon, I. (2016). Optimal classification with multivariate losses. In NeurIPS, pages 1530–1538.

- Osokin et al., (2017) Osokin, A., Bach, F., and Lacoste-Julien, S. (2017). On structured prediction theory with calibrated convex surrogate losses. In NeurIPS, pages 302–313.

- Parambath et al., (2014) Parambath, S. P., Usunier, N., and Grandvalet, Y. (2014). Optimizing F-measures by cost-sensitive classification. In NeurIPS, pages 2123–2131.

- Reid and Williamson, (2009) Reid, M. D. and Williamson, R. C. (2009). Surrogate regret bounds for proper losses. In ICML, pages 897–904.

- Sanyal et al., (2018) Sanyal, A., Kumar, P., Kar, P., Chawla, S., and Sebastiani, F. (2018). Optimizing non-decomposable measures with deep networks. Machine Learning, 107(8-10):1597–1620.

- Scott, (2012) Scott, C. (2012). Calibrated asymmetric surrogate losses. Electronic Journal of Statistics, 6:958–992.

- Sokolova and Lapalme, (2009) Sokolova, M. and Lapalme, G. (2009). A systematic analysis of performance measures for classification tasks. Information Processing & Management, 45(4):427–437.

- Steinwart, (2007) Steinwart, I. (2007). How to compare different loss functions and their risks. Constructive Approximation, 26(2):225–287.

- Tsybakov, (2008) Tsybakov, A. B. (2008). Introduction to Nonparametric Estimation. Springer.

- van de Geer, (2000) van de Geer, S. (2000). Empirical Processes in M-estimation. Cambridge University Press.

- van der Vaart, (2000) van der Vaart, A. W. (2000). Asymptotic Statistics. Cambridge University Press.

- van Rijsbergen, (1974) van Rijsbergen, C. J. (1974). Foundation of Evaluation. Number 4.

- Vapnik, (1998) Vapnik, V. (1998). Statistical Learning Theory. Wiley, New York.

- Yan et al., (2018) Yan, B., Koyejo, O., Zhong, K., and Ravikumar, P. (2018). Binary classification with Karmic, threshold-quasi-concave metrics. In ICML, pages 5531–5540.

- Yu and Blaschko, (2015) Yu, J. and Blaschko, M. (2015). Learning submodular losses with the Lovász hinge. In ICML, pages 1623–1631.

- (52) Zhang, T. (2004a). Statistical analysis of some multi-category large margin classification methods. Journal of Machine Learning Research, 5(Oct):1225–1251.

- (53) Zhang, T. (2004b). Statistical behavior and consistency of classification methods based on convex risk minimization. The Annals of Statistics, 32(1):56–85.

Supplementary Material for “Calibrated Surrogate Maximization of Linear-fractional Utility in Binary Classification”

Appendix A Calibration Analysis and Deferred Proofs from Section 4

In this section, we analyze calibration of the surrogate utility. Before proceeding, we need to describe Bayes optimal classifier for a given metric.

Definition 13.

Given a linear-fractional utility , Bayes optimal set is a set of functions that achieve the supremum of , that is, .

Classifiers in are referred to as Bayes optimal classifiers. Note that they are not necessarily unique. In this work, we assume that . First, we characterize Bayes optimal set .

Proposition 14.

Proof.

The maximization problem in Eq. (2) can be restated as follows.

where . First, the Fréchet derivative of evaluated at is obtained as follows.

Let be a function that maximizes , and . Then, maximizes , and it satisfies (Koyejo et al.,, 2014, lemma 12)

Thus, the necessary condition for local optimality is that for all .555 This can be confirmed in a similar manner to the proof of Yan et al., (2018, Theorem 3.1). Since , the above condition is for all , which is equivalent to the condition for all . This concludes the proof. Note that is a positive value, and . ∎

You may confirm that Proposition 14 is consistent with Bayes optimal classifier in the classical case, accuracy (Bartlett et al.,, 2006): a Bayes optimal classifier should satisfy for all , since , , .

Next, we state a proposition which gives a direction to prove the surrogate calibration of a surrogate utility. This proposition follows a latter half of Gao and Zhou, (2015, Theorem 2).

Proposition 15.

Fix a true utility , a surrogate utility , and let a Bayes optimal set corresponding to the utility . Assume that

| (8) |

Then, the surrogate utility is -calibrated.

Proof.

Remind that and let

and be any sequence such that . Then, for any , there exists such that for . Here we set : for . If we assume that , this contradicts with the following facts: for a function ,

Thus, it holds that for , that is, , which indicates -calibration. ∎

Thus, the proof of -calibration of is reduced to show the condition (8). Below, we show the surrogate calibration for the Fβ-measure and Jaccard index utilizing Propositions 14 and 15. The proofs are based on the above propositions, Gao and Zhou, (2015, Lemma 6) and Charoenphakdee et al., (2019, Theorem 11).

Throughout the proofs, we assume that for the critical set , , where is the classifier attaining the supremum of . For example, this holds for any -continuous distribution (Yan et al.,, 2018, Assumption 2).

A.1 Proof of Theorem 9

.

As a surrogate utility of the Fβ-measure following Eq. (4), we have

where

From Proposition 14, the Bayes optimal set for the Fβ-measure is

We will show Fβ-calibration by utilizing Proposition 15, which casts our proof target into showing Eq. (8). We prove it by contradiction. Assume that

This implies that there exists an optimal function that achieves , that is, and for some .

Let us describe the stationary condition of . We introduce a function :

Let . Since is Gâteaux differentiable666Fréchet differentiability implies Gâteaux differentiability. and its Gâteaux derivative at must be zero in any direction, we claim that , where corresponds to Gâteaux derivative of at in the direction of . Here, is computed as

where and . Thus, the stationary condition is

| (9) |

Since , we have . Thus, the condition (9) becomes

| (10) |

From now on, we divide the cases to take care of the Bayes optimal condition .

-

1)

If and : We show

(11) Take the difference of the left-hand side and the right-hand side:

where the denominator is always negative, which reduces to show the numerator is always negative, too:

where the first inequality holds because when (see Figure 8) and when (see Figure 8). Note that . The second inequality holds because of the assumption that and is convex, which implies for every .

Thus, the inequality (11) holds, which implies the following contradiction.

-

2)

If and : As well as the previous case, we begin from the stationary condition (10). If ,

where the first inequality holds because for every and , and the second inequality holds because () implies when (see Figure 8).

If , it is easy to see the contradiction.

Combining the above cases, it follows that

Eventually, we claim that is Fβ-calibrated by using Proposition 15. ∎

A.2 Proof of Theorem 10

.

As a surrogate utility of the Jaccard index following Eq. (4), we have

and we have the Bayes optimal set for the Jaccard index such as

utilizing Proposition 14. We follow the same proof technique, proof by contradiction, as we use in the proof of Theorem 9. Assume that

which implies that there exits an optimal function that achieves , that is, and for some .

-

1)

If and : We show

First, take the difference of the left-hand side and the right-hand side.

where the denominator is always negative, which reduces to show the numerator is always negative, too. If ,

( ) ( ) where the second inequality holds because of the assumption that for every , and is convex. Thus, we admit the contradiction.

If , then from the assumption , which immediately results in the contradiction.

-

2)

If and : We begin from the stationary condition in Eq. (12). If ,

(contradiction) where the second inequality follows because () and a function () is monotonically increasing (see Figure 9).

It is easy to see contradiction in case of .

Combining the above cases, it follows that

Eventually, we claim that is Jaccard-calibrated by using Proposition 15. ∎

A.3 Analysis of Accuracy-Calibration

In this subsection, we show accuracy-calibration conditions in the same manners as the Fβ-measure and Jaccard index, and confirm that the -discrepancy is not necessary in this case. As the true and a surrogate utility of the accuracy following Eq. (4), define

Proposition 16 (Accuracy-calibration).

Assume that a surrogate loss is convex, differentiable almost everywhere, and . Then, is accuracy-calibrated.

Proof.

We have the Bayes optimal set for the accuracy such as

utilizing Proposition 14. In the same manner as the proofs of Theorems 9 and 10, assume that

and we prove by contradiction. The above assumption implies that there exists an optimal function such that , that is, and for some .

The stationary condition of around can be stated in the same way as Eq. (9):

| (13) |

We divide the cases based on the sign of .

-

1)

and : Since because of the convexity of ,

which contradicts with . Note that when .

-

2)

and : Since because of the convexity of ,

which contradicts with . Note that when .

-

3)

: Since , the stationary condition (13) reduces to , which contradicts with .

Thus, it follows that . Eventually, we claim that is accuracy-calibrated by using Proposition 15. ∎

As we can see from Proposition 16, our surrogate calibration analysis can also be applied to the classification accuracy. In addition, the -discrepancy condition disappears from assumptions in the accuracy case, which recovers the conditions Theorem 6 in Bartlett et al., (2006). Even so, our analysis still remains to be sufficient conditions. Further analysis towards the necessary and sufficient conditions in the general calibration analysis is left as an future work.

A.4 Calibration Analysis of General Linear-fractional Metrics

So far, we analyze the surrogate calibration for the Fβ-measure in Theorem 9, and Jaccard index in Theorem 10. In addition, we take a look at how our analysis goes for the classification accuracy in Theorem 16. Now, we move on to the generalized result of the surrogate calibration which encompasses the entire linear-fractional metrics. Let us consider the maximization of the true utility in Eq. (1), and the maximization of the corresponding surrogate utility in Eq. (4).

Theorem 17 (-calibration in general case).

Let be a measurable function that achieves . Assume that a surrogate loss is convex, non-increasing, and differentiable almost everywhere. On the true utility, we assume the following conditions.

-

(1)

.

-

(2)

.

-

(3)

or .

-

(4)

.

-

(5)

.

-

(6)

If , then .

Moreover, assume that there exists such that satisfies the following conditions.

-

(a)

is -discrepant.

-

(b)

satisfies

-

(c)

and satisfy

Then, the surrogate utility is -calibrated.

The conditions (1), (2), (3), (4), and (5) exclude pathological true utilities which cannot be handled by the Bayes optimal analysis. For instance, the Bayes optimal rule would be a classifier that always outputs positive values without the conditions (1) and (2); on the other hand, the Bayes optimal rule would be a classifier that always outputs negative values without the condition (3). The conditions (6), (a), (b), and (c) force the surrogate utility to be calibrated to .

Below, we give the proof of Theorem 17.

Proof of Theorem 17.

We focus on the following surrogate utility as in Eq. (4):

where

Proposition 14 tells us that the Bayes optimal set for the utility is

We prove -calibration by contradiction. Assume that

This implies that there exists such that .

Let us describe the stationary condition of at in the same manner as the proof of Theorem 9. We introduce a function :

Let , then the stationary condition is . Here, is computed as

where and . Thus, the stationary condition is

which is equivalent to

| (14) |

From now on, we divide the cases to take care of the Bayes optimal condition . Since due to and , the Bayes optimal condition can be rewritten as .

-

1)

If and :

Let . Note that and since , , and either or is non-zero (condition (3)). We show the contradiction , which can be transformed as follows.

(15) If , we have

Since , is monotonically decreasing on . Together with the assumption , we have .

If , , noting that either or is non-zero (condition (3)). Here, we have as well since is a decreasing linear function.

-

2)

If and :

Combining the above cases, it follows that

Eventually, we claim that is -calibrated using Proposition 14. ∎

A.5 Non-negativity of Optimal Surrogate Utilities

Here, we briefly discuss that the optimal surrogate utilities are non-negative even though the numerator can be negative. Let us focus on the Fβ case:

and let and be suprema of and in within all measurable functions, respectively. Then,

where . The equality (a) holds under a certain regularity condition (Steinwart,, 2007, Lemma 2.5). Hence, we confirm that the optimal value of is non-negative.

The same discussion holds for the Jaccard case.

Appendix B Proof of Quasi-concavity of the Surrogate Utility

Proof of Lemma 5.

Define an -super-level set of restricted in as . It is enough to show is a convex set for any owing to .

Fix any . Then,

Here, is concave in since it is a non-negative sum of concave functions. Note that is concave in for any due to the definition of in Eq. (3) and the assumption is convex. Similarly, is convex as well. Thus, is concave in , which means that is a convex set since any super-level sets of a concave function is convex.

Hence, we confirm that is convex for any . ∎

Appendix C Proof of Uniform Convergence

First, we need carefully analyze our non-smooth surrogate loss to take handle of the Rademacher complexity (Bartlett and Mendelson,, 2002), which is defined as follows.

Definition 18 (Rademacher complexity).

Let be a sample with size . Let be a class of measurable functions, and be the Rademacher variables, that is, random variables taking and with even probabilities. Then, the Rademacher complexity of of the sample size is defined as

Usually, we analyze the Rademacher complexity of the composite function class by using the Ledoux-Talagrand’s contraction inequality (Ledoux and Talagrand,, 1991) when the surrogate is Lipschitz continuous: , where is the Lipschitz norm of . On the other hand, we need to deal with the case of the uniform convergence of gradients, which requires smoothness of the surrogate, while -discrepant loss is non-smooth surrogates. Thus, we need an alternative analysis.

Lemma 19.

Assume that is -discrepant and can be decomposed as . For , denote . Then,

Proof.

First, we prove for . Note that , and that , thus, .

| ( and are distributed in the same way for a fixed ) | ||

where the last inequality is just the triangular inequality. For (A), let if , and . Since

the Lipschitz norm of can be computed as

Note that the Lipschitz norm of is because is -smooth. Then, we further bound (A) by using the fact .

| (A) | |||

| ( triangular inequality) | |||

where the inequality is the result of the Ledoux-Talagrand’s contraction inequality (Ledoux and Talagrand,, 1991, Theorem 4.12). Note that both and are -Lipschitz. We can prove that (B) is bounded by from the above as well. Therefore, the claim is supported. We can prove the case in the same manner. ∎

Now, we move on to the proof of Lemma 11.

Proof of Lemma 11.

We write as . If we explicit note for which sample we take the empirical average in , let us write . Let . For simplicity, we write and . First, we observe admits the bounded difference property (McDiarmid,, 1989).

Denote that and . If ,

where the second inequality also holds due to the triangular inequality, and the last inequality follows from the fact that and are -/-Lipschitz and bounded by and , respectively. The same holds for the case .

Thus, is the bounded difference with a constant for each index, and we can obtain the following inequality by McDiarmid’s inequality (McDiarmid,, 1989):

which is equivalent to

with probability at least .

Next, we bound by the symmetrization device (Ledoux and Talagrand,, 1991, Lemma 6.3).

| (17) |

where the second line is the result of the triangular inequality, and

where the first inequality is the triangular inequality. Now we introduce the Rademacher random variables that are independently and uniformly distributed on .

-

•

For (A’), we can bound it from the above by the symmetrization device and the fact that .

(A’) () (symmetrization device) () ( ) where the last inequality uses Lemma 19.

-

•

For (A”), we can bound it from the above by the symmetrization device.

(A”) (symmetrization device) (contraction inequality) where the second inequality uses the Ledoux-Talagrand’s contraction inequality (Ledoux and Talagrand,, 1991, Theorem 4.12), together with the fact that is -Lipschitz continuous.

Thus, Eq. (17) can be bounded as follows.

where the last inequality comes from Mohri et al., (2012, Theorem 4.3), which results in .

After all, we obtain the desired uniform bound: with probability at least ,

∎

Appendix D Experimental Results

D.1 Details of Datasets

Datasets that we use throughout this section are obtained from the UCI Machine Learning Repository (Lichman,, 2013) and the LIBSVM (Chang and Lin,, 2011). For those which have independent training data, validation data, and test data, all of them are merged into one dataset. We randomly split the original data with the ratio , and the former is used for training while the latter is used for evaluation. Each feature value is scaled between zero and one.

| Dataset | dimension | sample size | class-prior |

|---|---|---|---|

| adult | 123 | 48842 | 0.239 |

| australian | 14 | 690 | 0.445 |

| breast-cancer | 10 | 683 | 0.350 |

| cod-rna | 8 | 331152 | 0.333 |

| diabetes | 8 | 768 | 0.651 |

| german.numer | 24 | 1000 | 0.300 |

| heart | 13 | 270 | 0.444 |

| ionosphere | 34 | 351 | 0.641 |

| mushrooms | 112 | 8124 | 0.482 |

| phishing | 68 | 11055 | 0.557 |

| phoneme | 5 | 5404 | 0.293 |

| skin_nonskin | 3 | 245057 | 0.208 |

| sonar | 60 | 208 | 0.394 |

| spambase | 57 | 4601 | 0.394 |

| splice | 60 | 1000 | 0.517 |

| w8a | 300 | 64700 | 0.030 |

D.2 Details of Baseline Methods

We describe the details of baseline methods. Baselines 2 and 3 are also mentioned in Sec. 6.

Baseline 1 (ERM): The first baseline is the vanilla empirical risk minimization, which does not optimize the metric of our interest but accuracy. The hinge loss and -regularization are employed with the regularization parameter .

Baseline 2 (W-ERM): Weighted empirical risk minimization, or cost-sensitive empirical risk minimization, is often used to optimize non-linear performance metrics (Koyejo et al.,, 2014; Narasimhan et al.,, 2014; Parambath et al.,, 2014). Here, we applied a simple approach: Find a cost parameter from a given cost parameter space, which gives the maximum validation performance of a classifier trained by the cost-sensitive empirical risk minimization (Scott,, 2012). The training dataset is split to 4 to 1 at random, and the latter is saved for validation of a regularization parameter. The former set is further split to 9 to 1 at random, and the former 90% is used for training the base classifier, while the latter 10% is used for the validation. As the base cost-sensitive learner, we use the hinge loss minimizer with -regularization (a regularization parameter is chosen from by cross validation). The cost parameter is chosen from the range evenly split to 20 ranges, that is, .

Baseline 3 (Plug-in): Plug-in estimator is one of the other common methods to optimize the non-linear performance metrics (Koyejo et al.,, 2014; Yan et al.,, 2018), which is the two-step method: To estimate the class posterior probability first, and then to decide the optimal threshold . The classifier is constructed as . The training dataset is split to 4 to 1 at random, and the latter is saved for validation of a regularization parameter. The former set is further split to 9 to 1 at random, and they are independently used for the first and second step. For estimating (the first step), the logistic regression is used (Reid and Williamson,, 2009), with -regularization (a regularization parameter is chosen from by cross validation). For deciding , we pick a threshold with the highest validation metric from .

D.3 Convergence Comparison

Figures 10 and 11 are the full version of the convergence comparison of U-GD and U-BFGS. Figure 10 shows the result of F1-measure, and Figure 11 shows the result of Jaccard index. The vertical axes show test metric values, where the higher the better. Note that both F1-measure and Jaccard index ranges over zero to one. The horizontal axes show the number of iterations. For each dataset, metric, and method, we ran 300 iterations to see their convergence behaviors.

Overall, U-BFGS shows faster convergence than U-GD in terms of the number of iterations. In almost all cases, U-BFGS converges within 30 iterations, except german.numer and mushrooms in Jaccard case. Moreover, it usually achieves higher performance than U-GD. U-GD convergences require at least around 100 iterations (mushrooms and phishing in F1 case), and sometimes it does not converge even within 300 iterations such as heart and ionosphere in F1 and Jaccard cases.

D.4 Performance Comparison with Benchmark Data

Benchmark results are shown in Tabs. 5 and 6. Each entry shows its final metric value for either F1-measure or Jaccard index. For each dataset, we first picked the method with the highest test performance as a outperforming method within that dataset, then conducted one-sided t-test with the significant level 5%, and they are also regarded as outperforming methods if the performance differences are not significant as a result of hypothesis tests. Outperforming methods are indicated in bold-faces.

As general tendencies, we observe that U-BFGS and Plug-in work well for both F1-measure and Jaccard index. As for F1-measure, their performances are competitive, while U-BFGS is better as for Jaccard index. In practice, both U-BFGS and Plug-in are worth being tried.

As for other methods: ERM does not work good as we expect, because it does not optimize the metrics of our interests, F1-measure and Jaccard index, at all. W-ERM does not work as well as Plug-in even though both of them are known to be consistent to the linear-fractional utilities. We may need more finer split of the threshold search space, or try a binary-search-type algorithm provided by recent work (Yan et al.,, 2018). U-GD does not work as well as U-BFGS contrary to our expectation. We may need more iterations to make U-GD converge, as we see in Figures 10 and 11. Note that we ran 100 iterations for both U-GD and U-BFGS for the results shown in Tabs. 5 and 6.

| (F1-measure) | Proposed | Baselines | |||

|---|---|---|---|---|---|

| Dataset | U-GD | U-BFGS | ERM | W-ERM | Plug-in |

| adult | 0.617 (101) | 0.660 (11) | 0.639 (51) | 0.676 (18) | 0.681 (9) |

| australian | 0.843 (41) | 0.844 (45) | 0.820 (123) | 0.814 (116) | 0.827 (51) |

| breast-cancer | 0.963 (31) | 0.960 (32) | 0.950 (37) | 0.948 (44) | 0.953 (40) |

| cod-rna | 0.802 (231) | 0.594 (4) | 0.927 (7) | 0.927 (6) | 0.930 (2) |

| diabetes | 0.834 (32) | 0.828 (31) | 0.817 (50) | 0.821 (40) | 0.820 (42) |

| fourclass | 0.638 (70) | 0.638 (64) | 0.601 (124) | 0.591 (212) | 0.618 (64) |

| german.numer | 0.561 (102) | 0.580 (74) | 0.492 (188) | 0.560 (107) | 0.589 (73) |

| heart | 0.796 (101) | 0.802 (99) | 0.792 (80) | 0.764 (151) | 0.764 (137) |

| ionosphere | 0.908 (49) | 0.901 (43) | 0.883 (104) | 0.842 (217) | 0.897 (54) |

| madelon | 0.666 (19) | 0.632 (67) | 0.491 (293) | 0.639 (110) | 0.663 (24) |

| mushrooms | 1.000 (1) | 0.997 (7) | 1.000 (1) | 1.000 (2) | 0.999 (4) |

| phishing | 0.937 (29) | 0.943 (7) | 0.944 (8) | 0.940 (12) | 0.944 (8) |

| phoneme | 0.648 (27) | 0.559 (22) | 0.530 (201) | 0.616 (135) | 0.633 (35) |

| skin_nonskin | 0.870 (3) | 0.856 (4) | 0.854 (7) | 0.877 (8) | 0.838 (5) |

| sonar | 0.735 (95) | 0.740 (91) | 0.706 (121) | 0.655 (189) | 0.721 (113) |

| spambase | 0.876 (27) | 0.756 (61) | 0.887 (42) | 0.881 (58) | 0.903 (18) |

| splice | 0.785 (49) | 0.799 (46) | 0.785 (55) | 0.771 (67) | 0.801 (45) |

| w8a | 0.297 (80) | 0.284 (96) | 0.735 (35) | 0.742 (29) | 0.745 (26) |

| (Jaccard index) | Proposed | Baselines | |||

|---|---|---|---|---|---|

| Dataset | U-GD | U-BFGS | ERM | W-ERM | Plug-in |

| adult | 0.499 (44) | 0.498 (11) | 0.471 (51) | 0.510 (20) | 0.516 (10) |

| australian | 0.735 (63) | 0.733 (59) | 0.702 (144) | 0.693 (143) | 0.707 (76) |

| breast-cancer | 0.921 (54) | 0.918 (55) | 0.905 (66) | 0.903 (78) | 0.913 (69) |

| cod-rna | 0.854 (3) | 0.785 (8) | 0.864 (11) | 0.865 (9) | 0.869 (3) |

| diabetes | 0.714 (44) | 0.702 (50) | 0.692 (70) | 0.698 (56) | 0.695 (60) |

| fourclass | 0.469 (69) | 0.457 (68) | 0.436 (112) | 0.434 (171) | 0.449 (66) |

| german.numer | 0.433 (64) | 0.429 (69) | 0.335 (153) | 0.391 (98) | 0.418 (71) |

| heart | 0.665 (135) | 0.675 (135) | 0.664 (102) | 0.629 (178) | 0.626 (163) |

| ionosphere | 0.826 (76) | 0.829 (65) | 0.796 (134) | 0.749 (245) | 0.815 (87) |

| madelon | 0.495 (31) | 0.459 (69) | 0.346 (225) | 0.474 (100) | 0.496 (27) |

| mushrooms | 0.999 (2) | 0.995 (4) | 1.000 (1) | 0.999 (4) | 0.997 (7) |

| phishing | 0.883 (43) | 0.893 (11) | 0.894 (14) | 0.888 (22) | 0.894 (15) |

| phoneme | 0.435 (51) | 0.436 (24) | 0.371 (160) | 0.450 (104) | 0.461 (34) |

| skin_nonskin | 0.744 (5) | 0.751 (5) | 0.746 (10) | 0.780 (13) | 0.722 (7) |

| sonar | 0.600 (125) | 0.600 (111) | 0.552 (147) | 0.495 (202) | 0.572 (134) |

| spambase | 0.827 (22) | 0.708 (22) | 0.798 (67) | 0.790 (86) | 0.824 (31) |

| splice | 0.670 (60) | 0.672 (56) | 0.646 (71) | 0.629 (84) | 0.672 (57) |

| w8a | 0.496 (151) | 0.452 (28) | 0.580 (44) | 0.590 (35) | 0.595 (33) |

D.5 Sample Complexity

It is interesting to study the relationship between the metric performances and the size of samples, because we expect Plug-in, which requires to estimate probabilities accurately, does not work well when the size of samples is quite small. Figures 12 and 13 show the sample complexity results. Even though learning is not stable for small samples (e.g., heart and w8a), we can observe clear differences in some cases such as cod-rna, diabetes, german.numer, ionosphere, sonar, and splice in F1-measure, and australian, cod-rna, diabetes, ionosphere, phishing, sonar, and spambase in Jaccard index, where either U-GD or U-BFGS works better than Plug-in even if sample sizes are quite small around 20 to 40. In addition, Plug-in seldom works significantly better than the gradient-based methods in the cases where sample sizes range around 100 to 400 as investigated in this section. This is contrary to the behavior shown in Tabs. 5 and 6, where the full-size datasets are used to train classifiers.

As a conclusion, it can be a good option to consider using the gradient-based methods where sample sizes are very small.

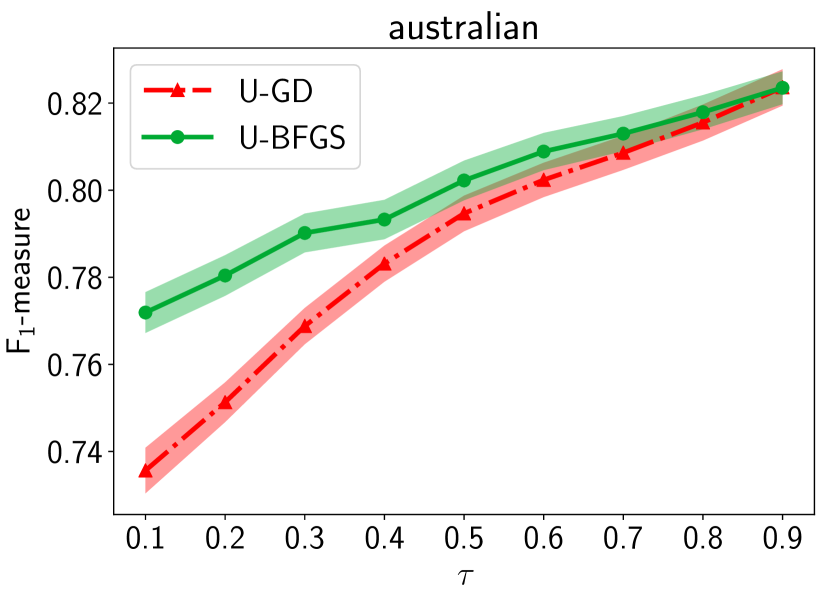

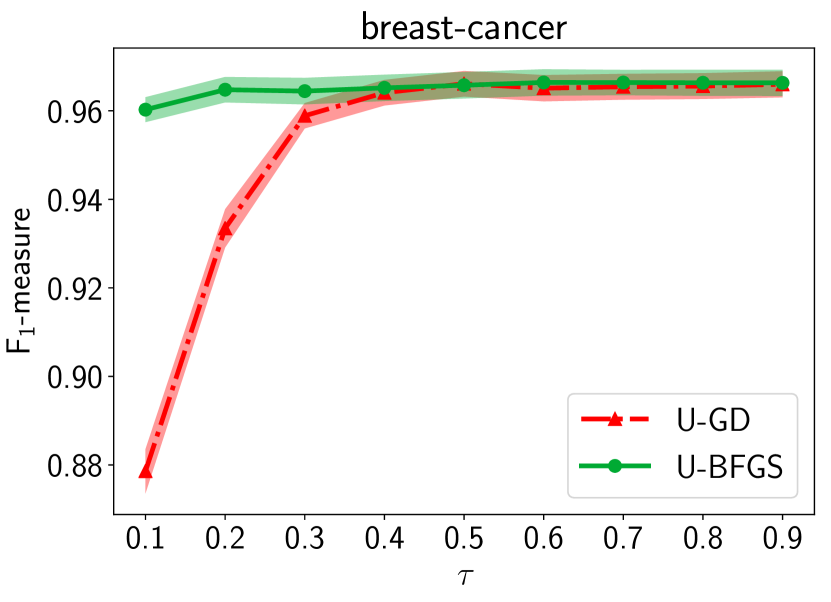

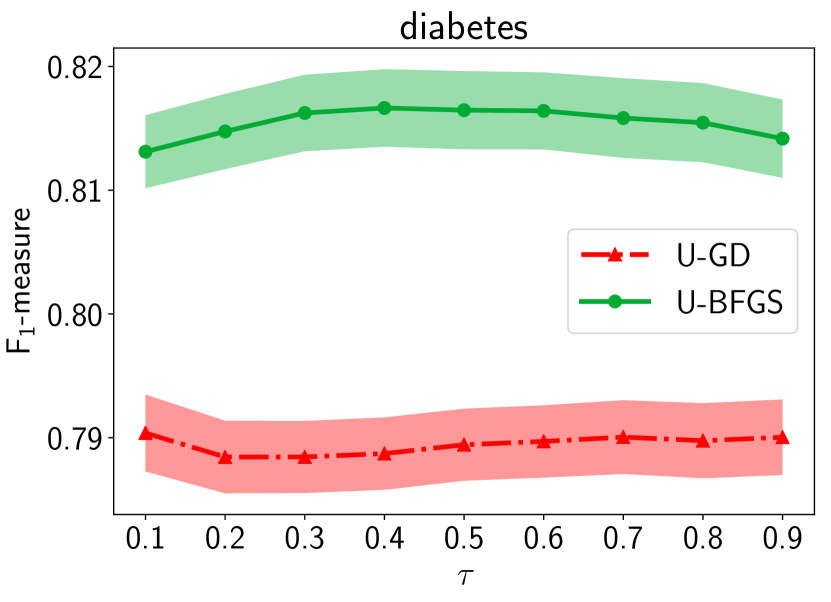

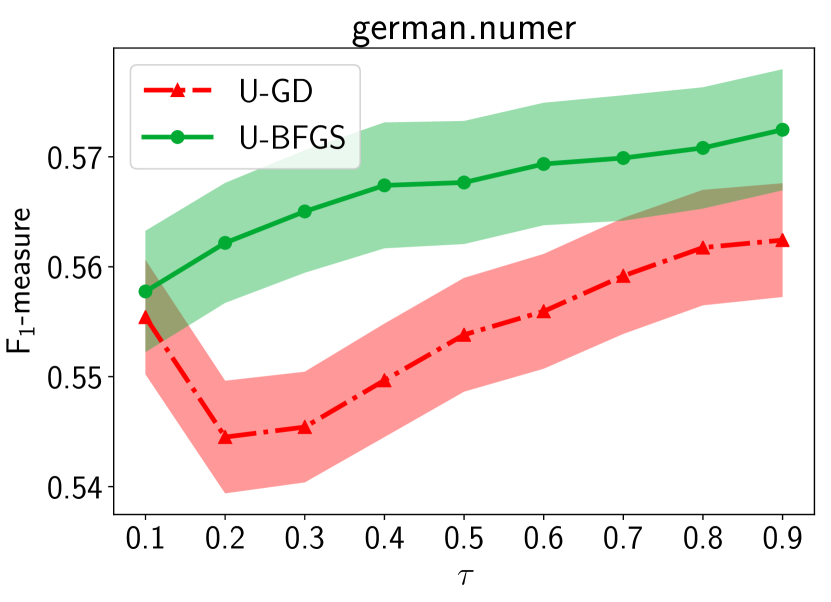

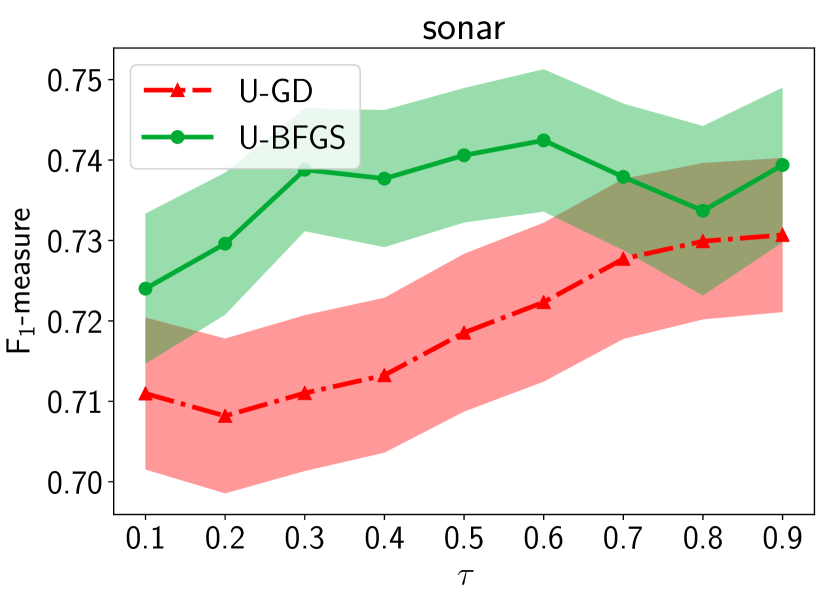

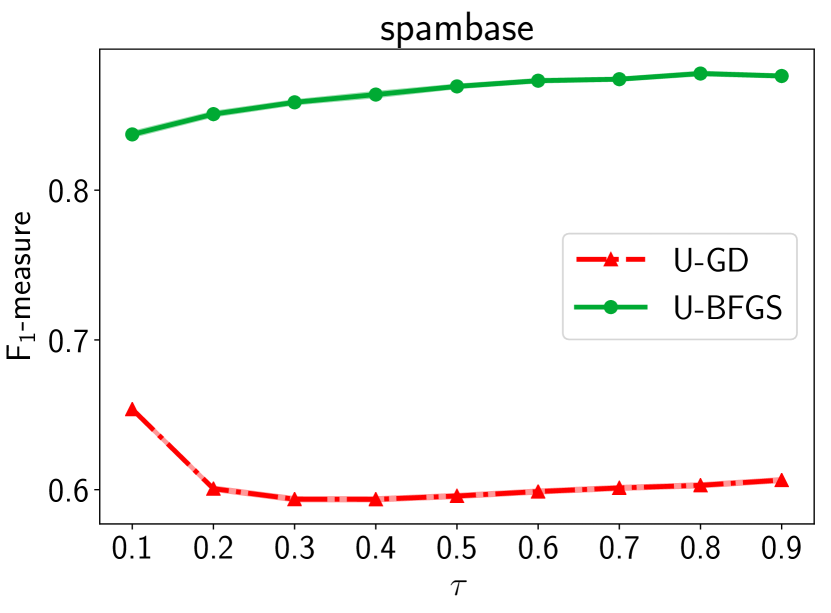

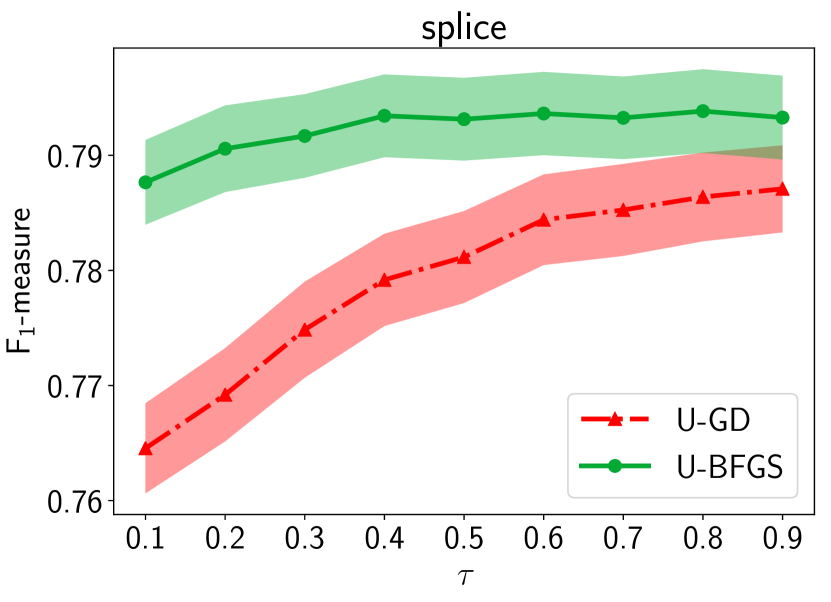

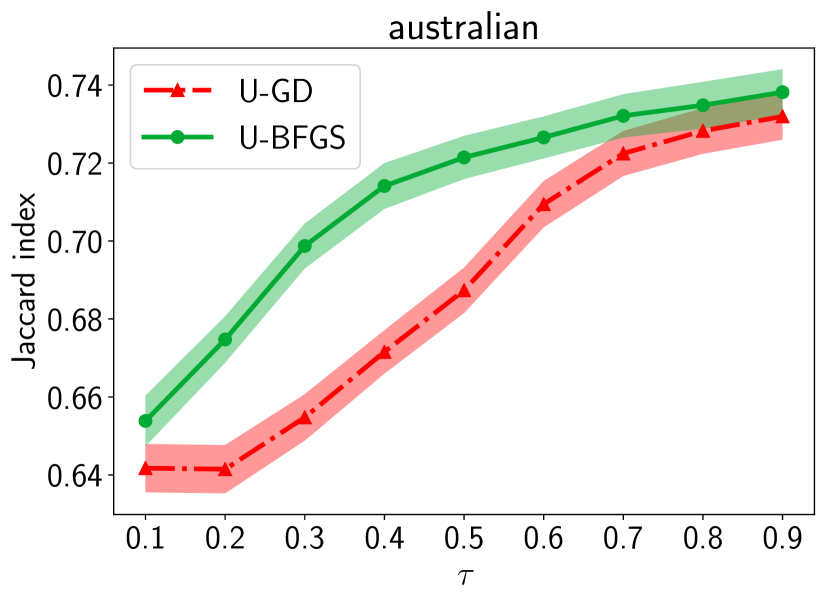

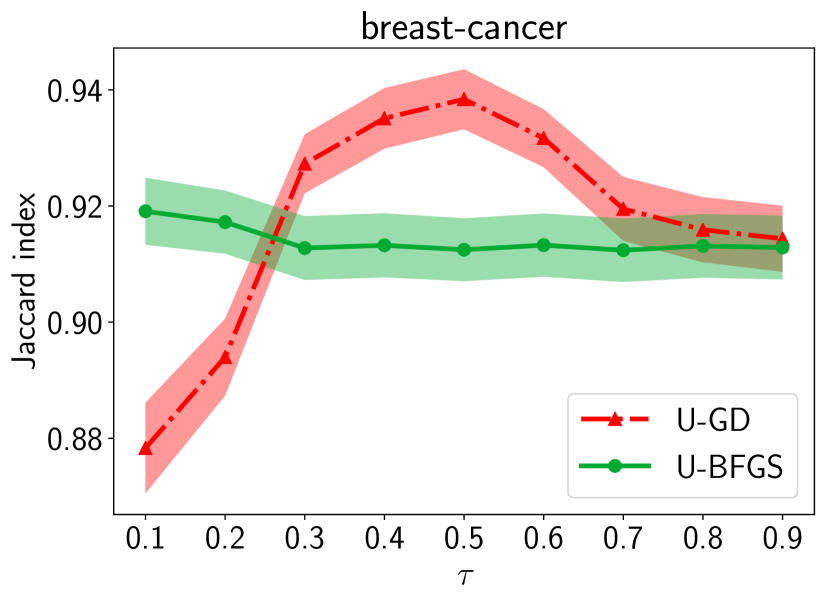

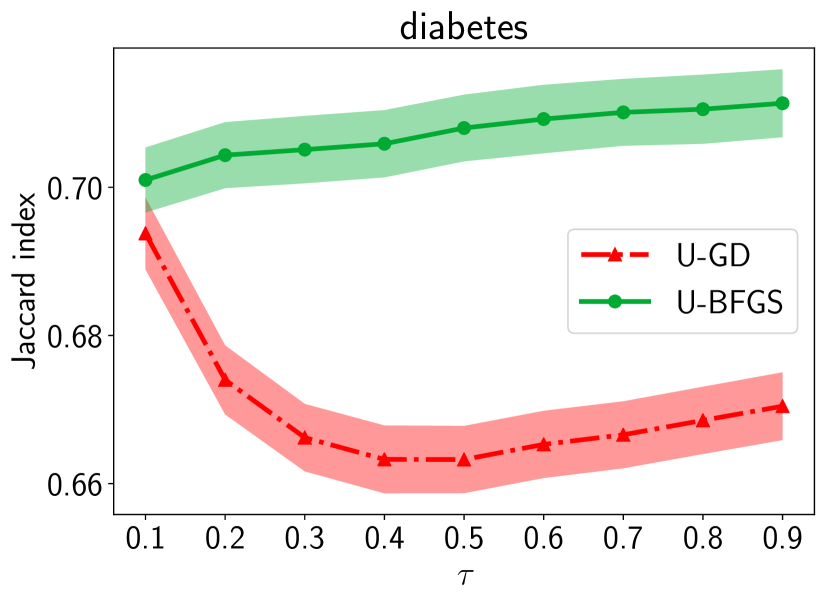

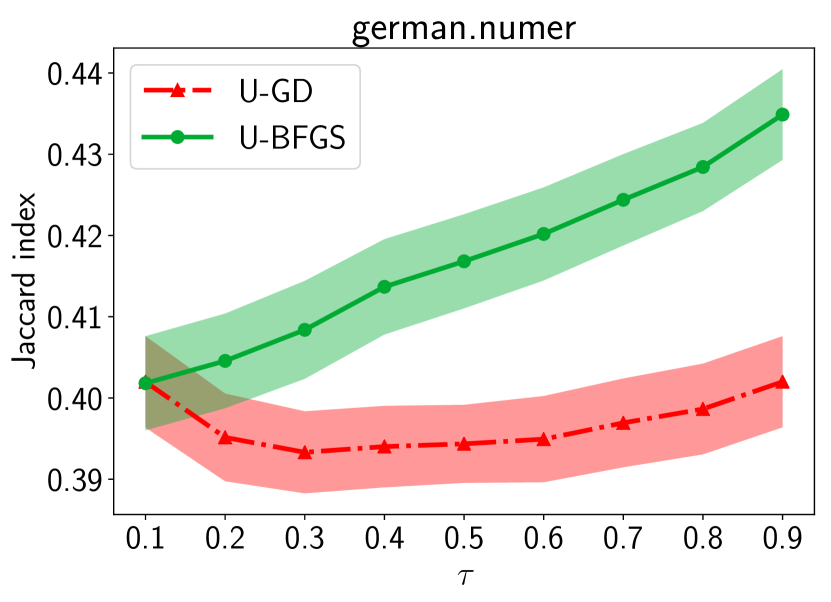

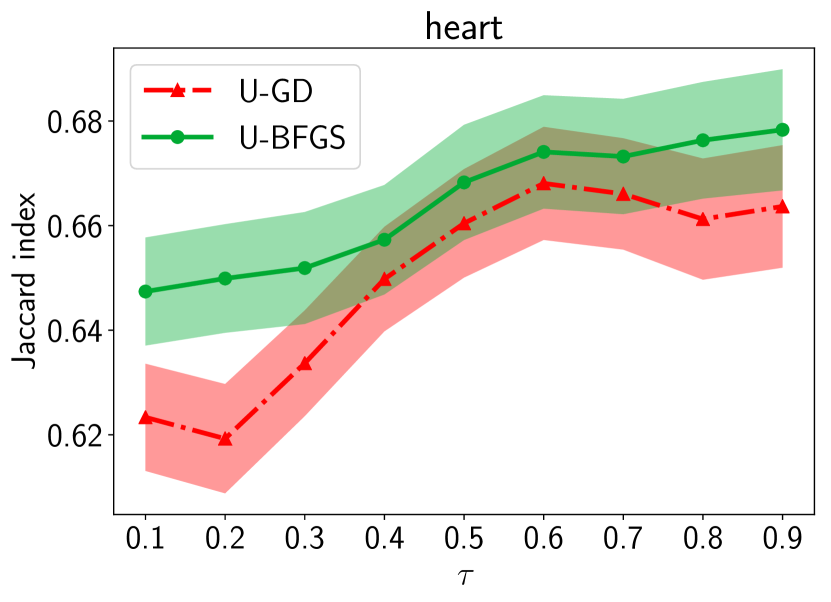

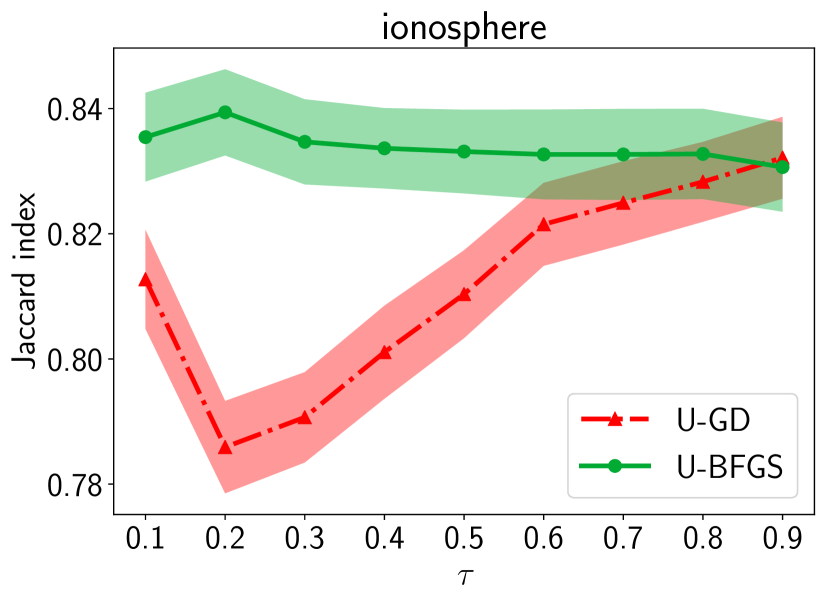

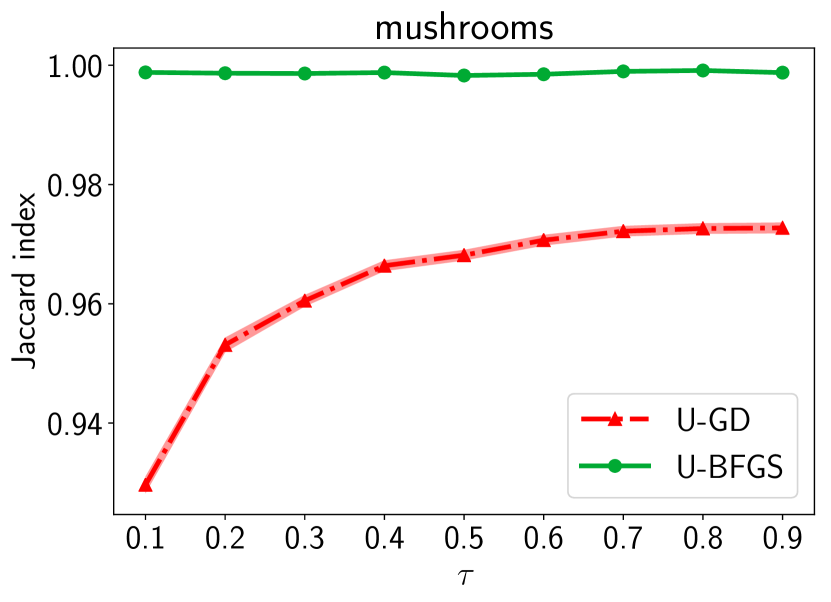

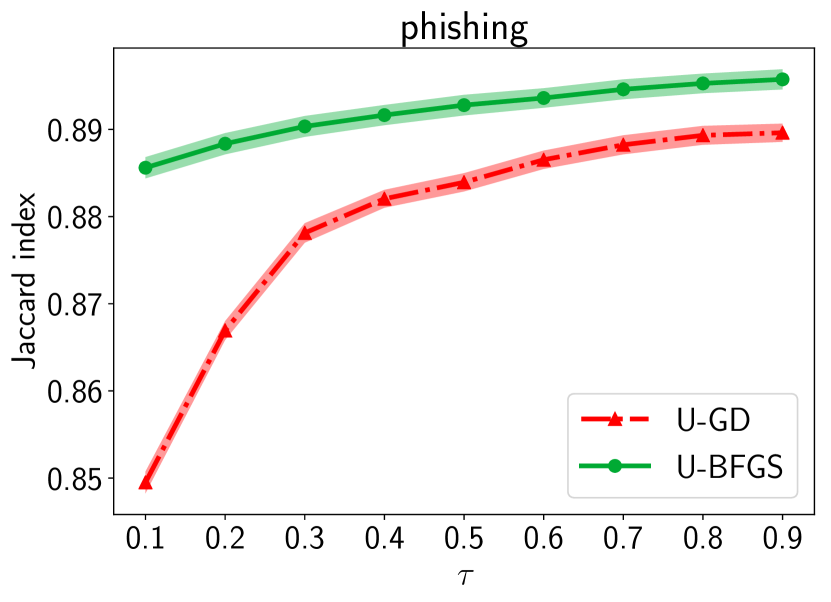

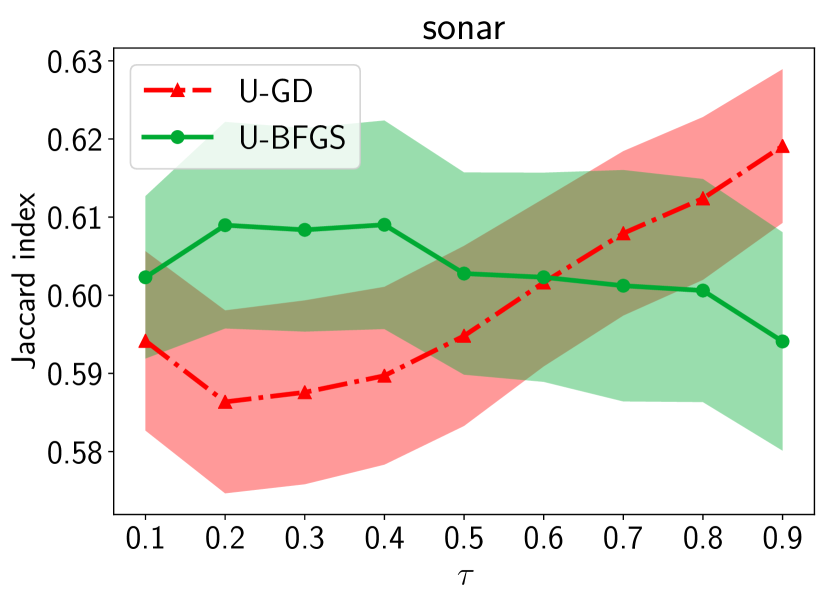

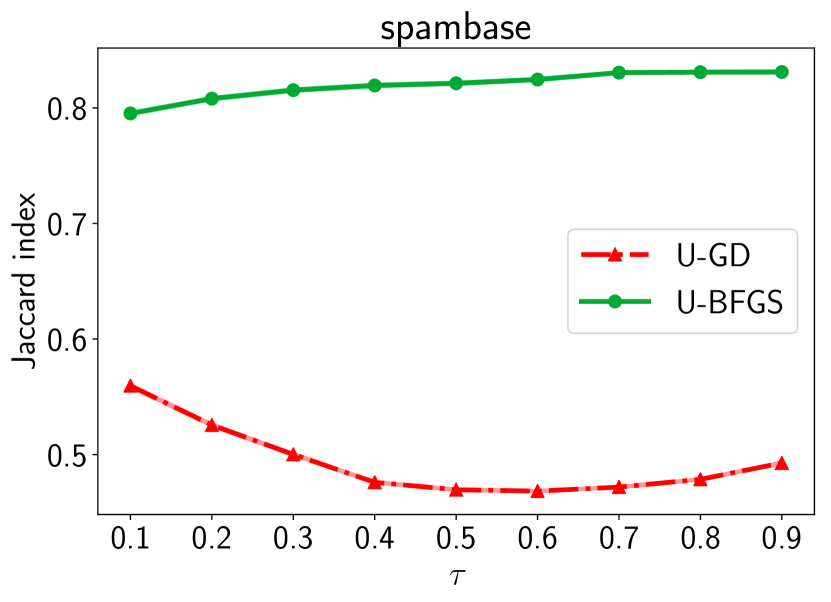

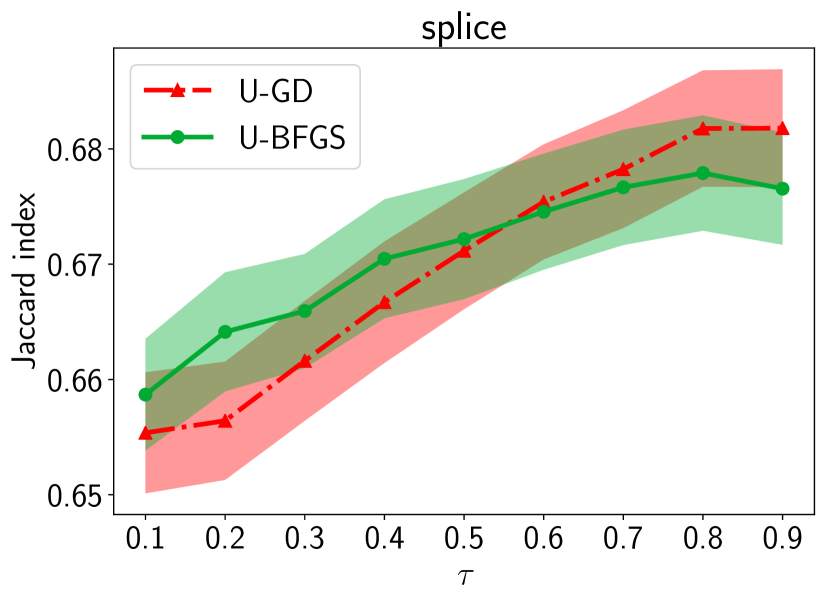

D.6 Performance Sensitivity on

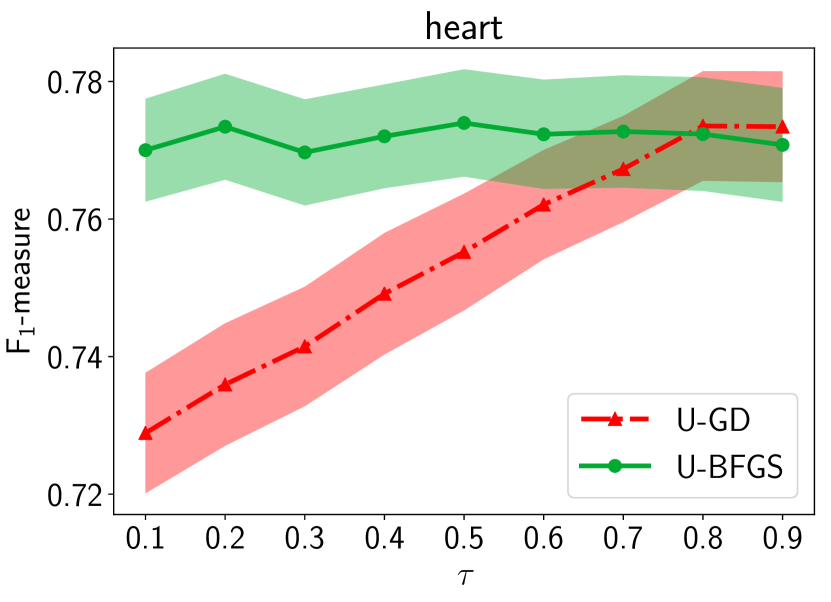

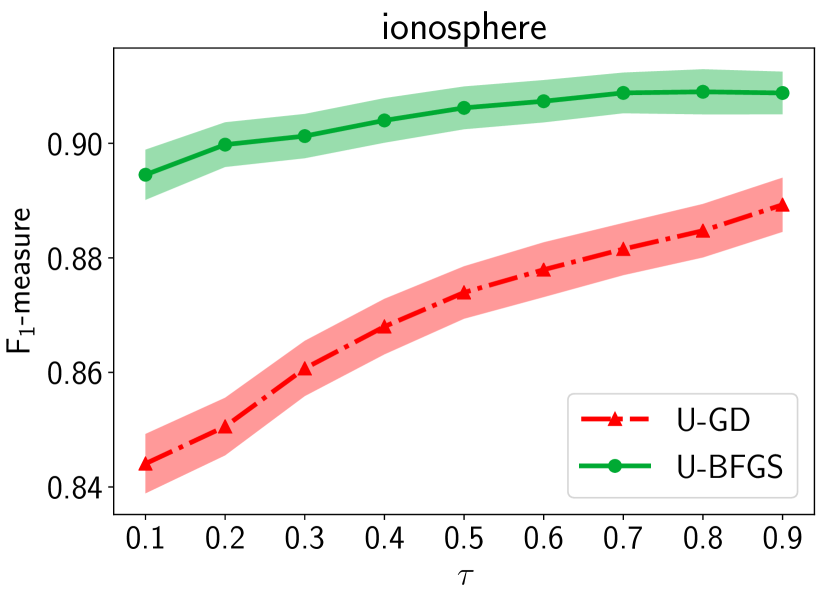

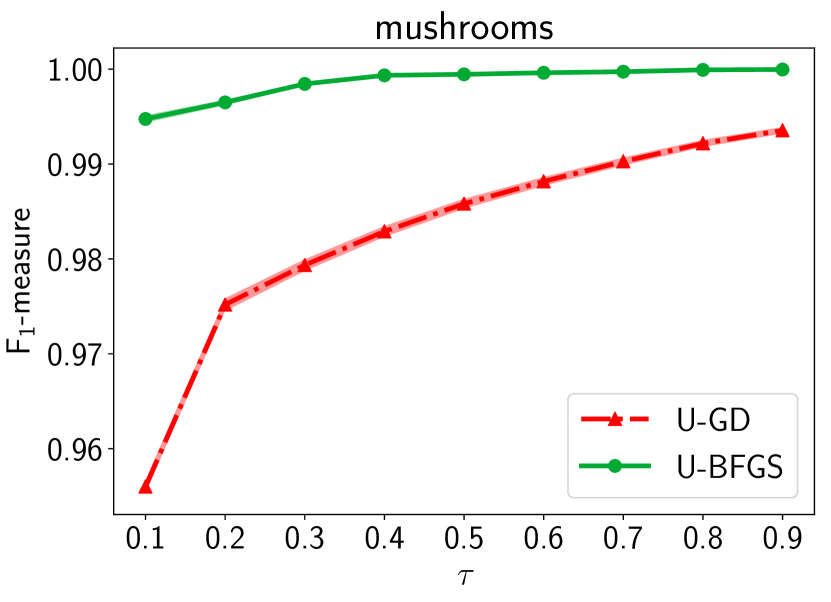

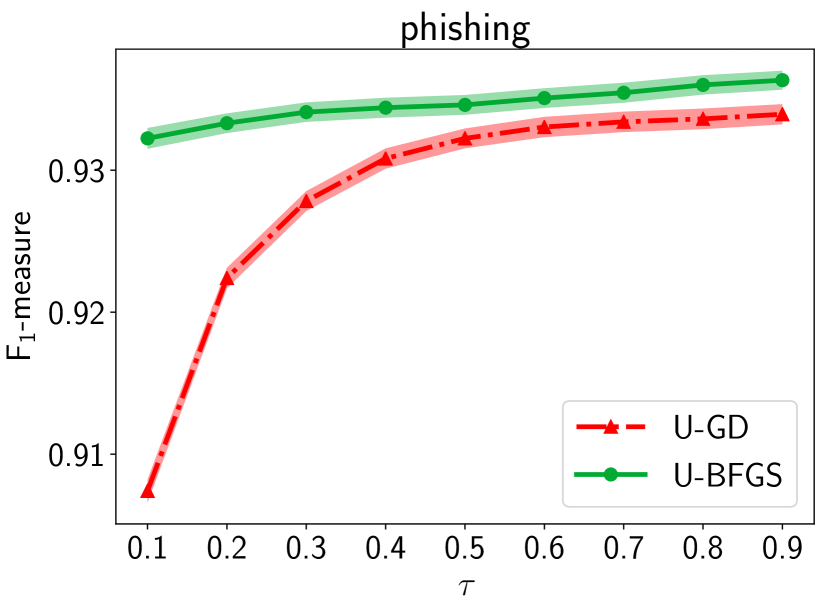

Lastly, we see the performance sensitivity on the choices of . We change and run U-GD and U-BFGS for both the F1-measure and Jaccard index. The results are summarized in Figures 14 and 15. From these figure, we can say there is a tendency that the performance becomes better as becomes closer to . For example, the below combinations of the datasets and metrics have such a tendency.

-

•

australian, breast-cancer, german.numer, heart, ionosphere, mushrooms, phishing, and splice in the Fβ-measure,

-

•

australian, mushrooms, phishing, and splice in the Jaccard index.

However, there are also other cases where there exist extrema of the performance with respect to the choices of . For example, the below combinations of the datasets and metrics have such a tendency.

-

•

german.numer and sonar in the Fβ-measure,

-

•

breast-cancer, heart, ionosphere and sonar in the Jaccard index.

From our theoretical results in Theorems 9 and 10, we cannot determine whether the surrogate utility is calibrated or not if exceeds about for the Fβ-measure, and becomes closer to for the Jaccard index. These thresholds are not so clear in Figures 14 and 15 since the conditions on is merely sufficient conditions, as we explain in Sec. 4. Further analyses on the discrepancy parameter are left for future work.