Bayesian Dynamic Fused LASSO

Abstract

The new class of Markov processes is proposed to realize the flexible shrinkage effects for the dynamic models. The transition density of the new process consists of two penalty functions, similarly to Bayesian fused LASSO in its functional form, that shrink the current state variable to its previous value and zero. The normalizing constant of the density, which is not ignorable in the posterior computation, is shown to be essentially the log-geometric mixture of double-exponential densities. This process comprises the state equation of the dynamic regression models, which is shown to be conditionally Gaussian and linear in state variables and utilize the forward filtering and backward sampling in posterior computation by Gibbs sampler. The problem of overshrinkage that is inherent in lasso is moderated by considering the hierarchical extension, which can even realize the shrinkage of horseshoe priors marginally. The new prior is compared with the standard double-exponential prior in the estimation of and prediction by the dynamic linear models for illustration. It is also applied to the time-varying vector autoregressive models for the US macroeconomic data, where we examine the (dis)similarity of the additional shrinkage effect to dynamic variable selection or, specifically, the latent threshold models.

Key words and phrases: Dynamic shrinkage, fused LASSO, dynamic linear models, forward filtering and backward sampling, scale mixture of normals, synthetic likelihoods.

1 Introduction

The univariate dynamic linear models (DLMs) in practice are frequently over-parametrized because of the massive amount of predictors, most of which are believed to be noises. For example, the time-varying vector autoregressive models are typically decomposed into the multiple univariate sub-models for the computational feasibility (e.g., Zhao et al. 2016 and Gruber and West 2016), but this approach results in the excess amount of predictors in those sub-models even for the moderate dimensional observations. This research contributes to the appropriate modeling of sparsity in the univariate DLMs with many predictors by defining a new shrinkage prior on the dynamic coefficients, and its application to the modeling of multivariate time series.

Specifically, for the univariate state variable , which is the time-varying regression coefficient in the context of DLMs, we consider the new Markov process defined by its transition density,

| (1) |

where weights and are positive. The two penalty functions in the exponential realize the shrinkage effects conditional on the latest state . By using this process as the prior in DLMs, we shrink the state variable at time toward zero by the first penalty function, while shrinking it to the previous state variable at as well to penalize the excess dynamics by the second penalty. The technical difficulty in using this prior in statistical analysis is the unknown normalizing constant abbreviated in equation (1) that involves state variable and is not ignorable in the posterior analysis. The objective of this research is to compute this normalizing constant explicitly and to provide the computational methodology for the efficient posterior analysis by Markov chain Monte Carlo methods.

The prior in (1) is named dynamic fused LASSO (DFL) prior for its similarity to Bayesian fused LASSO models (e.g., Kyung et al. 2010 and Betancourt et al. 2017). The Bayesian fused LASSO has rarely been applied to the time series analysis and, consequently, the problem of unknown normalizing constant has not been discussed. This is because, in Bayesian fused LASSO, the state variables are modeled jointly, not conditionally as in (1), by exponentiating the various penalty functions to define the joint density of all the state variables. By modeling the joint density directly, the normalizing constant becomes free from the state variables, which simplifies the Bayesian inference for the fused LASSO models and enables the scale mixture representation of the double exponential priors, as in the standard Bayesian LASSO models (Park and Casella, 2008). From this viewpoint, our research is clearly different from the existing fused LASSO models in modeling the conditional distribution of state variables to realize our prior belief in the dynamic modeling, which instead poses the problem of computing the normalizing constant that can be ignored (or not required to compute) in the study of the Bayesian fused LASSO. The modeling of the conditional distribution is crucial in predictive analysis; the direct application of the existing fused LASSO to the joint distribution of time-varying parameters does not define the conditional evolution of state variables coherently and, as a result, cannot be used for sequential posterior updating and forecasting.

Although the normalizing constant complicates the prior and posterior distributions of the DLMs with the DFL process, we prove the augmented model representation of the DFL prior as the conditionally dynamic linear models (CDLMs), for which the efficient posterior sampling of state variables by the forward filtering and backward sampling (FFBS) is available. Facilitating the posterior computation by FFBS with the help of the CDLM representation is the standard strategy in the literature of econometrics and forecasting, where the dynamic sparsity has been realized by the hierarchical DLMs (e.g., Frühwirth-Schnatter and Wagner 2010, Belmonte et al. 2014 and Bitto and Frühwirth-Schnatter 2019). This hierarchical version of dynamic linear models is obtained by the natural extension of DLMs with another prior on its scale parameters in the state equation. While the posterior of state variables is easily computed by FFBS, these priors penalize only the distance between the two consecutive state variables, and , which is understood as the special case of the prior of this study with in equation (1). Our approach, in contrast, integrates the additional penalty for the shrinkage toward zero explicitly into the conditional transition density of the prior process. This modeling approach reflects our prior belief that the state variable is likely to be either zero or unchanged from its previous value. The additional shrinkage effect to zero in the DFL prior can also address the problem of the shrinkage effect restricted to be uniform over time as “horizontal shrinkage” (Uribe and Lopes, 2017; Ročková and McAlinn, 2020) by localizing the shrinkage effect at each time by customized latent parameters as practiced in, but in a different way to, Kalli and Griffin (2014) and Kowal et al. (2019).

The conditional normality and linearity of the DFL prior is based on the fact that the prior process is decomposed into two parts: the synthetic likelihood and synthetic prior. These terminologies literally mean that the prior consists of two components, one of which is treated as (part of) likelihood and the other of which serves as the prior in the computation of the full conditional posterior of state variables. The synthetic prior is just the well-known scale mixture of Gaussian random walks, hence normal and linear in state variables. The synthetic likelihood part is equivalent to observing the artificial data with mean that provides the additional information to shrink the state variable to zero. The posterior of this CDLM is proportional to the full conditional of state variables up to constant, which justifies the use of FFBS for this synthetic model. The idea of synthetic likelihood and prior approach has been utilized in the studies of optimal portfolios that are sparse and less switching (e.g., Kolm and Ritter 2015 and Irie and West 2019), and this research consider the same idea in the context of statistical modeling.

The rest of the paper is structured as follows. Section 2 focuses on the DFL prior in (1) and proves its CDLM representation, followed by the comparison with the existing approaches in Section 2.5. Section 3 considers the effect of weights parameters and the extension of the DFL models with the prior on weights. Section 4 introduces the DLMs with the DFL prior and provides the MCMC algorithm by using the properties proven in the previous sections, in addition to discussing the estimation of observational variances. In Section 5, the proposed model is applied to the simulation data for illustration (Section 5.1) and to the US macroeconomic time series for the comparison with the model of the variable selection type (Section 5.2). The paper is concluded in Section 6 with the list of potential future research. All the proofs are given in the Supplementary Materials.

Notations: The density of the univariate normal distribution with mean and variance evaluated at is denoted by . The double-exponential density with parameter is denoted by . The gamma distribution with shape and rate is written as with mean . The exponential distribution with rate is . The beta distribution with positive shapes and with mean is . The generalized inverse Gaussian distribution is denoted by , the density of which is proportional to . In our study, is either or , so it is the inverse Gaussian distribution or its reciprocal.

2 Dynamic fused LASSO

2.1 Definitions

A new class of univariate, stationary Markov processes is defined by its conditional density of transition given in (1). The two conflicting -penalty functions, and , represent the shrinkage toward zero and the latest state , respectively. As discussed in the introduction, this process is expected to reflect our prior belief on the dynamic sparsity in coefficients of DLMs, for which we assume throughout the paper. With this restriction, we intend to have weight sufficiently small, because large might result in the excess shrinkage toward zero and lead to poor predictive accuracy. In this section, we study the property of this process as the prior for time-varying regression coefficients, while the likelihood of DLMs is introduced in Section 4.

We first write the two penalties as the densities of double-exponential distributions,

where and for non-negative weights and (Andrews and Mallows, 1974; West, 1987; Park and Casella, 2008). Then, the transition density of the DFL process from to is defined by

| (2) |

The analytical expression of is discussed later in Proposition 2.1.

Denote the marginal distribution of by . The condition for this process to be stationary is

and one solution of this functional equation is , with which the process also becomes reversible. In the following, we assume the marginal density of this form, hence the DFL process in this paper is stationary.

The representation by the scale mixture of normals is the key to the computational feasibility, as used in Bayesian LASSO (Park and Casella 2008). Using the latent scale parameters, and , we have

hence the normalizing function is

| (3) |

i.e., the scale mixture of normals with the convolution of and . The conditional density also has the following mixture representation,

| (4) |

i.e., the location-scale mixture of normals. The integrand is the regression of on with coefficient . Conditioned by the latest state , the current state is shrunk toward in this form. The amount of this conditional shrinkage is determined by the balance of two conflicting loss functions, or weights and .

2.2 Normalizing constant

The computation of normalizing function is straightforward.

Proposition 2.1

For , the normalizing function is,

| (5) |

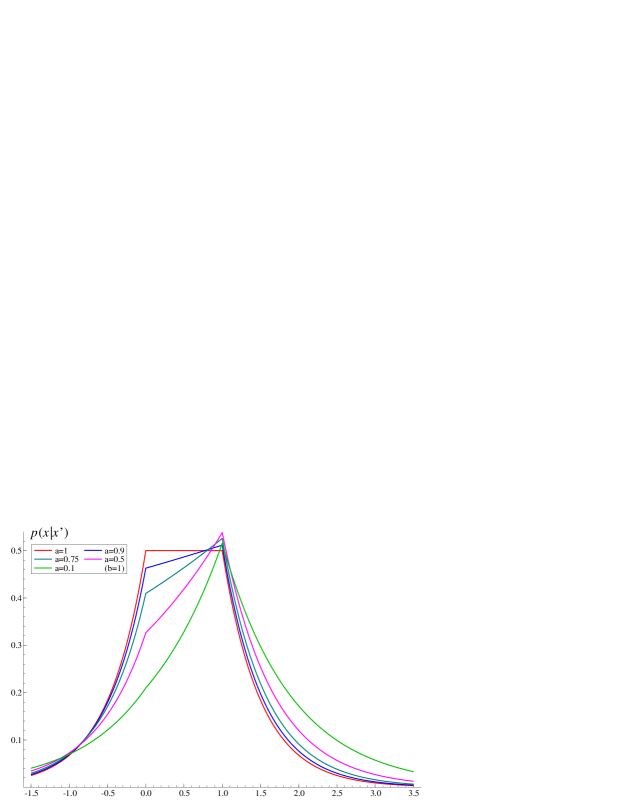

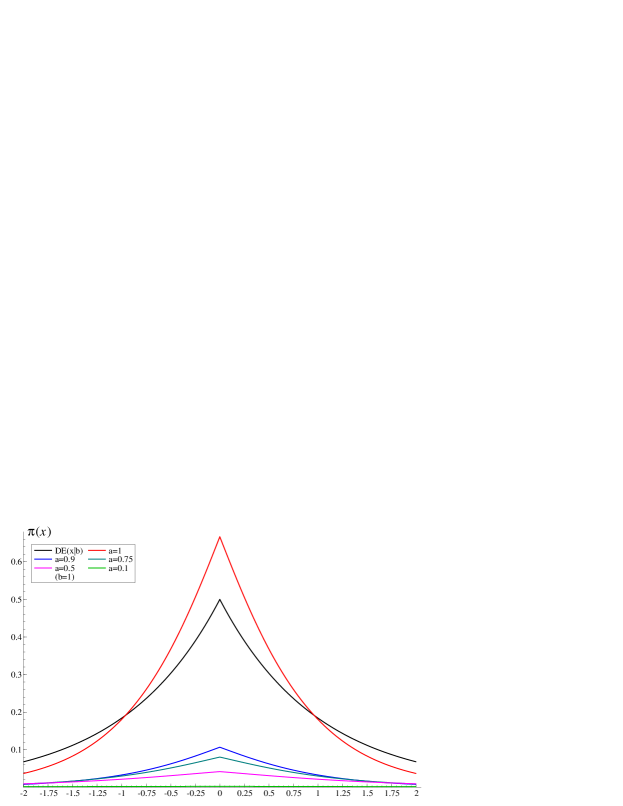

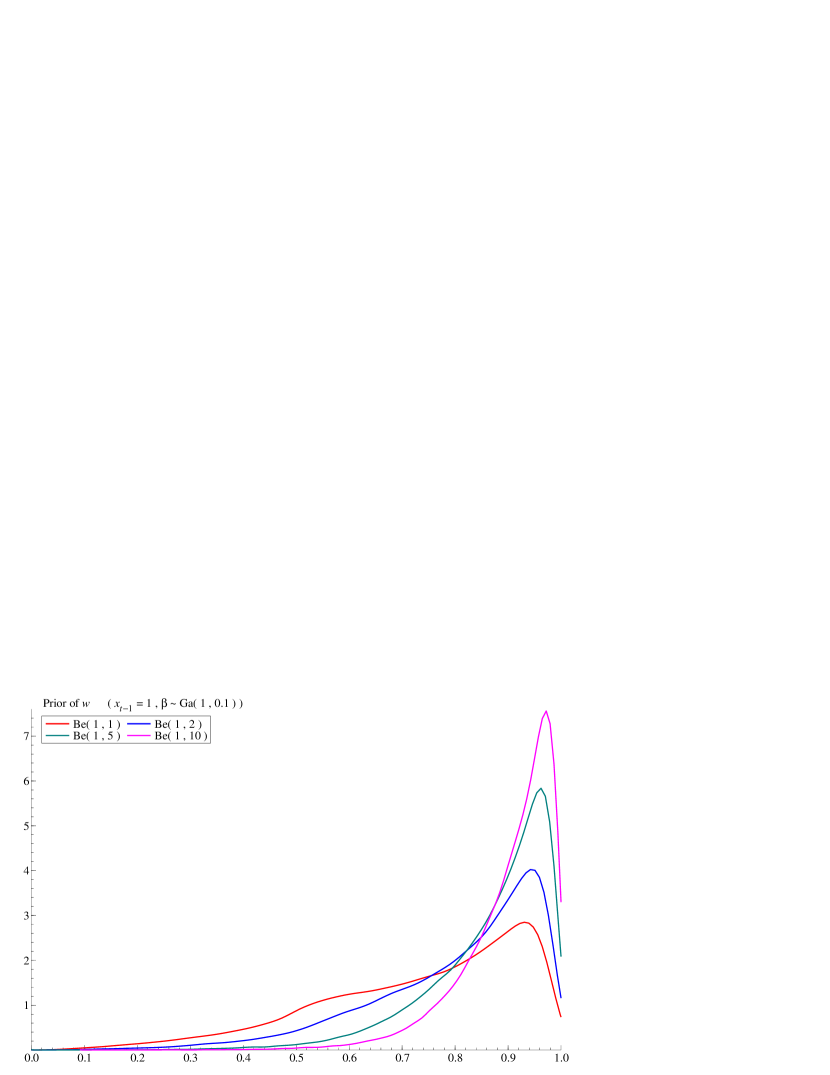

The proof is given in Section S1. This proposition enables the evaluation of densities involving , such as the conditional density and the stationary density . In Figure 1, the conditional density with and is plotted for the different choices of . As weight increases, the shrinkage effect to zero becomes visually clear. If , then the two shrinkage effects are completely balanced, which is expressed as the plateau of the density between and zero. With this density as the prior, one does not discriminate any state between these two points a priori. In practice, however, we do not want the extreme amount of shrinkage to zero when transitioning the last state to the next and, for this reason, we assume in application. Figure 2 shows the marginal, stationary density . In general, the smaller leads to the fatter tails, avoiding the shrinkage effect on the outliers. The sharp increase of density around the origin is seen even with small , so the marginal shrinkage effect to zero is preserved. For large , the density is more spiky, but clearly different from the double-exponential density. These characteristics of priors are revisited from the different viewpoints later in Section 3 to study the effect of priors on weights .

2.3 Log-geometric augmentation

In the expression of the second line of equation (5), note that because by assumption. It guarantees the absolute convergence of the series expression of the reciprocal normalizing function as

We can further rewrite this expression by using probability densities. First, the exponential function is the reciprocal of the double exponential density with parameter with the appropriate adjustment of constants. Second, in the geometric series, we can read off the mixture of double-exponential densities with the running index of series, , as the latent non-negative integer. This mixture consists of two components: (i) constant, for , which has no contribution to the posterior, and (ii) the discrete mixture of double exponential distributions with parameter for . The mixture weight is proportional to the probability function of log-geometric distribution with parameter , defined by the series representation of . We summarize this observation as a proposition.

Proposition 2.2

For , the reciprocal of normalizing function is written as

where is the mixture of a constant and the log-geometric mixture of double-exponential distributions,

| (6) |

where , and .

2.4 Joint distribution

Using the expression of normalizing constant in Proposition 2.2, we can compute the joint distribution of as follows:

The reciprocal of the normalizing constant involves the double-exponential density , which is canceled out with another in the transition from to , simplifying the joint prior to the product of two components named “prior” and “likelihood.” We can, literally, treat these components as the likelihood and prior in order to define the synthetic model whose posterior distribution is equivalent to the original joint density . This redundant expression of the prior is the key to the CDLM representation for the efficient posterior computation with the DFL prior.

The “prior” part is the Markov process defined by the initial distribution and the transition , where the explicit shrinkage of is set only toward a single point , not toward zero. This Markov process has widely been used in the state space modeling, for is the scale mixture of normals hence simplifies the posterior computation.

The rest of the density, phrased “likelihood” in the expression above, completes the synthetic model. The density is equivalent to with as the function of , where we introduce the “observation” in the synthetic model. For function , we revisit equation (6) and relabel the latent integer as

where we define for , and , and are given in Proposition 2.2. The synthetic model obtained in this way is linear in state variables, and also conditionally Gaussian by writing the double-exponential distributions as the scale mixture of normals.

Proposition 2.3

For fixed and (), the joint density of of the DFL prior is proportional to the joint posterior density of the following conditional dynamic linear model; the state evolution and the prior for the associated latent parameter are

| (7) |

with the initial distribution at ,

| (8) |

The synthetic observation is defined as, at ,

| (9) |

For , the latent count follows the discrete distribution,

| (10) |

where here is the point mass on and is the discrete distribution on positive integers whose probability function is . The quantities , and are defined in Proposition 2.2. Conditional on , and if , we additionally have observational equations defined by,

| (11) |

If , we have no additional observation equation at time .

See Section S3 for the proof. In this synthetic model, the shrinkage effects of the new Markov process gains new interpretation. If is sampled at time , then the model has no synthetic observation at , or is “missing.” If is sampled, then is observed, providing the additional information that encourages the shrinkage to zero at time . This is exactly the local (vertical) shrinkage effect, that is different from the global (horizontal) shrinkage that is uniformly applied to the state variables at all the time points, as pointed out by Uribe and Lopes (2017). The amount of this shrinkage is indirectly controlled by weights and ; the larger is, the more likely it is that , having less shrinkage effect to zero, which is consistent with the interpretation of weights in the loss function.

2.5 Other possible approach to dynamic shrinkage

The DFL prior is characterized by the two conflicting shrinkage effects that are not seen in the other continuous shrinkage priors used in the time series analysis. Proposition 2.3 gives the new interpretation to treat these shrinkage effects separately; the shrinkage to is based on the state equation (7), while the shrinkage to zero is achieved by the synthetic observations in (11). The former has been seen in the literature of state space modeling with sparsity, where the state transition is defined by

If scale follows the exponential distribution, then this is the special case of DFL prior with . Another example is the case where for all , and follows the half-Cauchy or scaled-beta priors (Frühwirth-Schnatter and Wagner 2010, Belmonte et al. 2014, Feldkircher et al. 2017 and Bitto and Frühwirth-Schnatter 2019). As discussed already, the shrinkage effect of this prior is limited for its constant scale ; the dynamic scale (or the equivalent concept) is discussed in Kalli and Griffin (2014) and Kowal et al. (2019). The DFL prior is different from these approaches in adding the new shrinkage effect to zero.

The concept of simultaneous shrinkage to two points has been discussed as variable selection, or the finite mixture of point mass on zero and (conditionally) Gaussian AR(1) process (dynamic spike-and-slab priors, Uribe and Lopes 2017 and Ročková and McAlinn 2020). The exact shrinkage to zero achieved by this approach comes at the cost of the other shrinkage directed not to the previous state but its discounted value with , in addition to the slow convergence of Markov chains that is inevitable in variable selection. Alternatively, the point mass distribution on zero can be replaced by the thresholding the latent state variables. Nakajima and West (2013a) considers the thresholding the state variables to zero, while Eisenstat et al. (2016) and Huber et al. (2019) model the thresholding of dynamics. The similarity and difference of the former approach and the DFL model is discussed in Section 5.2.

From the viewpoint of the use of multiple penalty functions, another alternative that could achieve the same objective is the existing fused LASSO prior in Kyung et al. (2010) that directly models the joint distribution of state variables (the joint fused LASSO prior, or JFL). The joint distribution of all the states variables is defined as

| (12) |

This density has the similar, but simpler, synthetic model representation as

where for all . The CDLM representation is available for this model with the scale mixture augmentation of the double-exponential distributions. However, the JFL model lacks several desired properties that the proposed DFL possesses. First, the flexibility of the JFL prior in shrinkage effect is limited. This is indicated in the difference of the DFL/JFL priors in the synthetic likelihood. The DFL prior allows for the possibility of missing the synthetic observation and the shrinkage effect to zero can vary across time based on the value of , but the latent in the JFL model is always observed, and its shrinkage effects are equally controlled by parameter at any time point. In this sense, the flexibility of the local shrinkage is limited in the JFL models. Second, the normalizing constant of the JFL prior in (12) is unknown. This involves none of the state variables, but weight parameters , so the the posterior analysis on weights is extremely difficult. At last, but most importantly, predictive analysis is not available with the JFL prior. The joint density of the JFL prior does not specify the evolution of state variables, and does not cover the existence of state variables after in the model. If one defines the joint distributions of and by (12) individually, then

and the conditional density is not coherently defined after . This concludes that the JFL prior is not suitable for the formal sequential and predictive analysis.

3 Estimation of weight parameters

3.1 Effect on marginal distribution of

The weights and determine the structure of sparsity in the prior. As the hyperparameters, these weights must be carefully chosen so that the prior appropriately reflects one’s belief on the dynamics and sparsity of the state variables. For the aim of prior elicitation, one should consider the value of the conditional mean of the state transition in (4), , and the density of shrinkage effect . They are analytically available and provide further information on the prior belief we structure by using the DFL prior. For their functional forms and graphical examples, see Section S4, S5 and S6.

3.2 Conjugate priors on weights

In practice, tuning the weight parameters of all the state variables is not realistic. It is desirable if the automated adjustment of those hyperparameters is fully or partially available. The formal approach to this goal is the Bayesian posterior analysis by placing the prior distribution on the hyperparameters. Consider the re-parametrization by , where , to allow that the inequality, , always holds. Then, we apply the gamma prior that is conditionally conjugate. For , we consider the beta distribution ; the conditional posterior density of is analytically available, from which we can easily sample by discretizing the prior on interval . For the details including the derivation of the full conditionals, see Section S7.

3.3 Horseshoe as hierarchical Bayesian LASSO

The use of -penalty is often criticized for its undesirable pattern of shrinkage, as clearly demonstrated by Carvalho et al. (2010). Partly for this reason, it is common, as in the literature mentioned in Section 2.5, to consider the scale mixture of normals by gamma distributions whose shape is not necessarily unity, but frequently to induce the strong shrinkage effect as the horseshoe prior. Naturally, the extension of the DFL to the dynamic fused horseshoe prior is desired, but the normalizing constant of such prior, and its mixture representation for computational feasibility, have been unknown.

In fact, we can bypass such mathematical difficulty to the extension by considering another type of hyperprior on weights under the DFL prior. As proven in Section S8, if and , then the marginal of with is the horseshoe prior, i.e., the scale mixture of normals by the half-Cauchy distribution. We name the hierarchical DFL prior with this set of priors for the weight parameters as dynamic fused horseshoe prior, or DFHS prior.

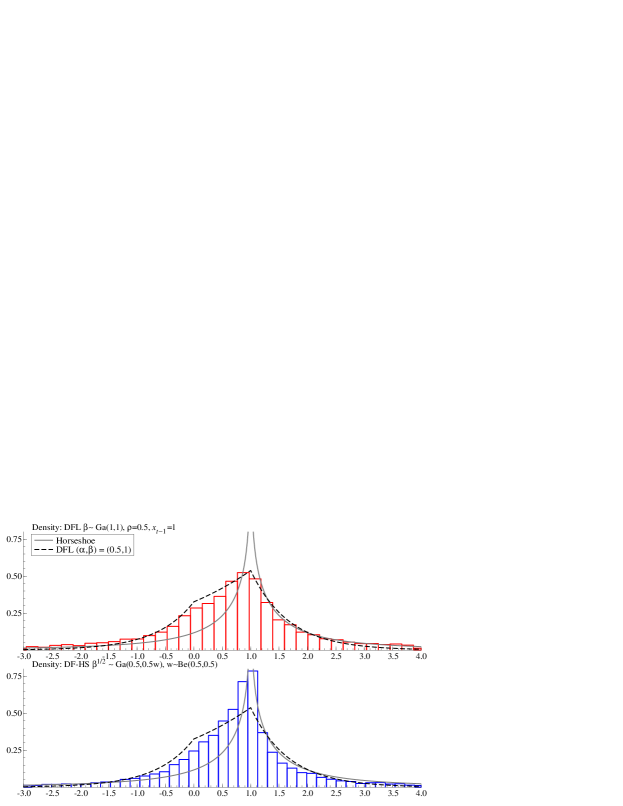

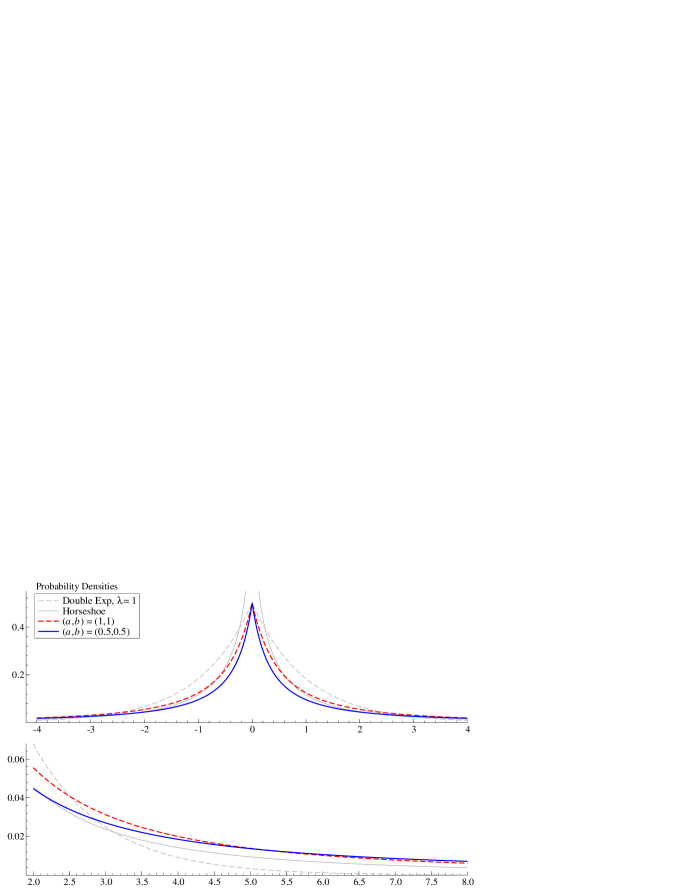

Figure 3 shows the conditional distribution of , where the weight parameters follow the priors introduced here and the conjugate priors in Section 3.2, with . The DFL prior with the fixed weights has the thinner tails and overshrink the significant change of coefficients, while the conjugate priors in Section 3.2 has the heavier tails than the horseshoe prior to integrate such observations into posteriors. The spike around , which reflects the strength in shrinking the dynamics of states, is not seen in the case of the hierarchical DFL model with the conjugate priors. In contrast, as the theory predicts, the DFHS prior exhibits the same spike of the density at , and also the same heaviness of its tails as that of the horseshoe prior.

The conditional posteriors of and for Gibbs sampler are the known class of distributions. The full conditional of is, after the appropriate re-parametrization, a special case of extended gamma distributions. We customize the rejection sampling from this distribution, based on the discussions by Finegold and Drton (2011) and Liu et al. (2012). The full conditional of belongs to the class of Kummer-beta distribution (Gordy, 1998), for which the method of random number generation is not trivial. We simply approximate the prior by the discrete distribution on the girds of , whose probabilities are propositional to the densities of , as we treat parameter in Section 3.2. The approximation bias, or the deviation from the original prior by this discretization, is negligible. See Section S8 for the derivation and more discussions.

3.4 Baseline of prior process

The marginal prior mean of states is set to be zero in order that the additional shrinkage is directed to zero. The direction of shrinkage can be changed from zero to any value (baseline) and, in fact, estimated with some prior. Denote this baseline by , and modify the transition density of the DFL process as

The parameter augmentation proved in Section 2 is still valid for this prior. The only difference from the original DFL prior is that the value of the synthetic observation is now the baseline, i.e., . The baseline is also the location parameter in the synthetic prior at , . We use the normal prior for the baseline that is conditionally conjugate in the synthetic model. Alternatively, one can choose the scale mixture of normals to introduce the shrinkage effect on the baseline. Furthermore, although not pursued in our study, the modeling of baseline as the function of time, , could be considered under the specific applied context, where the concept of shrinkage is extended and directed to the pre-specified “function,” or .

4 Application to state-space modeling

4.1 Estimation by Markov chain Monte Carlo

Consider the Gaussian and linear observational equation given by

| (13) |

where is vector of predictors known at time , is the vector of state variables, and is the observational variance parameter and modeled later in Section 4.2. Each state variable independently follows the DFL process,

| (14) |

where the baseline and weights are customized for each predictor and denoted by and . The CDLM representation of the prior given in Proposition 2.3 is now combined with the “real” likelihood in (13). Following the notation in Proposition 2.3, the set of all the latent variables introduced for this state variable for the -th state is denoted by and . The algorithm of Gibbs sampler for the posterior inference can be derived easily from the CDLM representation, where the forward filtering and backward sampling (FFBS) is utilized in sampling the state variables from the full conditionals (Carter and Kohn, 1994; Frühwirth-Schnatter, 1994).

Gibbs sampler for the Bayesian dynamic fused LASSO models

-

1.

Sampling by forward filtering and backward sampling (FFBS).

The conditional posterior of is equivalent to the posterior of the conditionally dynamic linear model with “real” likelihood in (13) and the following “synthetic” likelihoods and prior. For each , if , then the model has the synthetic likelihood,

At , the model always has the synthetic likelihood,

The state evolution of the CDLM is defined by the synthetic prior; for ,

and, for ,

By FFBS, one can sample from the full posterior of of this CDLM (e.g., West 1984, Chap. 4.8).

-

2.

Sampling .

The components of are independently sampled from the full conditionals below: for ,

-

•

Sample from for and .

-

•

Sample from for if .

-

•

Sample from for .

-

•

-

3.

Sampling .

The sampling of is based on the conditional posterior with marginalized out. For and , the latent counts, ’s, are independently sampled from

where means the geometric distribution; the probability function of random variable is for .

-

4.

Sampling .

-

5.

Sampling variances : see the next subsection.

Note that the latent scales, , are marginalized out when sampling the latent counts and weights to work on the double-exponential densities directly. This marginalization not only simplifies the sampling procedure but also facilitates the mixing of Markov chains (partially collapsed Gibbs sampler, van Dyk and Park 2008).

4.2 Modeling of stochastic volatility

The modeling of observational variance , or stochastic volatility, can be discussed independently of the use of the DFL priors; one can import an arbitrary model and computational method for . In our study, we consider the following two models. For details, see also Section S9.

The first example is the constant variance, for all , in the “scale-free” DLMs that also includes in the state equation to scale the observational and state variances simultaneously. The conjugate prior for in the DLMs of this type is the inverse gamma gamma prior, (West and Harrison 1997, Chap. 4.5). The DFL process in equation (1) is applied to the scaled state variable ; this affects the variance of the synthetic likelihood and prior but not the other parts of the model. Consequently, variance parameter appears in the synthetic likelihoods and prior of the CDLM representation in Section 4.1 as their scales, for which the FFBS is available to sample from the conditional joint posterior of states and observational variance. We consider this model in the simulation study, Section 2.

In contrast, if the stochastic volatility appears only in observational equation (13), the MCMC algorithm in Section 4.1 is easily extended by incorporating the sampling of this parameter. We consider the model of this type as the second example and, specifically, chose the log-Gaussian models for the empirical study in Section 5.2; log-volatility follows the Gaussian AR(1) process as,

with the normal, beta and inverse-gamma priors for AR(1) parameters . The posterior computation is a challenge in computational statistics. In Section 5.2, we used multi-move sampler (Shephard and Pitt, 1997; Watanabe and Omori, 2004) that is also used in the existing literature, but we would like to note that there has been continuing advancement in this area (e.g., Kastner and Frühwirth-Schnatter 2014).

Although not discussed in this research, the conjugate inverse gamma-scaled beta process can also be considered as a simpler alternative for the computational ease (West and Harrison 1997, Chap. 10.8).

5 Illustration via data analysis

The posterior analysis by the DLM with the DFL/DFHS priors is conducted for the simulated and real datasets. In the simulation study, the proposed model is compared with the standard dynamic models with double-exponential/horseshoe priors to clarify the difference in their shrinkage effects. In the analysis of real macroeconomic data, the patterns of shrinkage under the DFL priors is highlighted in comparison with the dynamic variable selection by the latent threshold models.

All computations are implemented by Ox (Doornik, 2007).

5.1 Simulated dataset

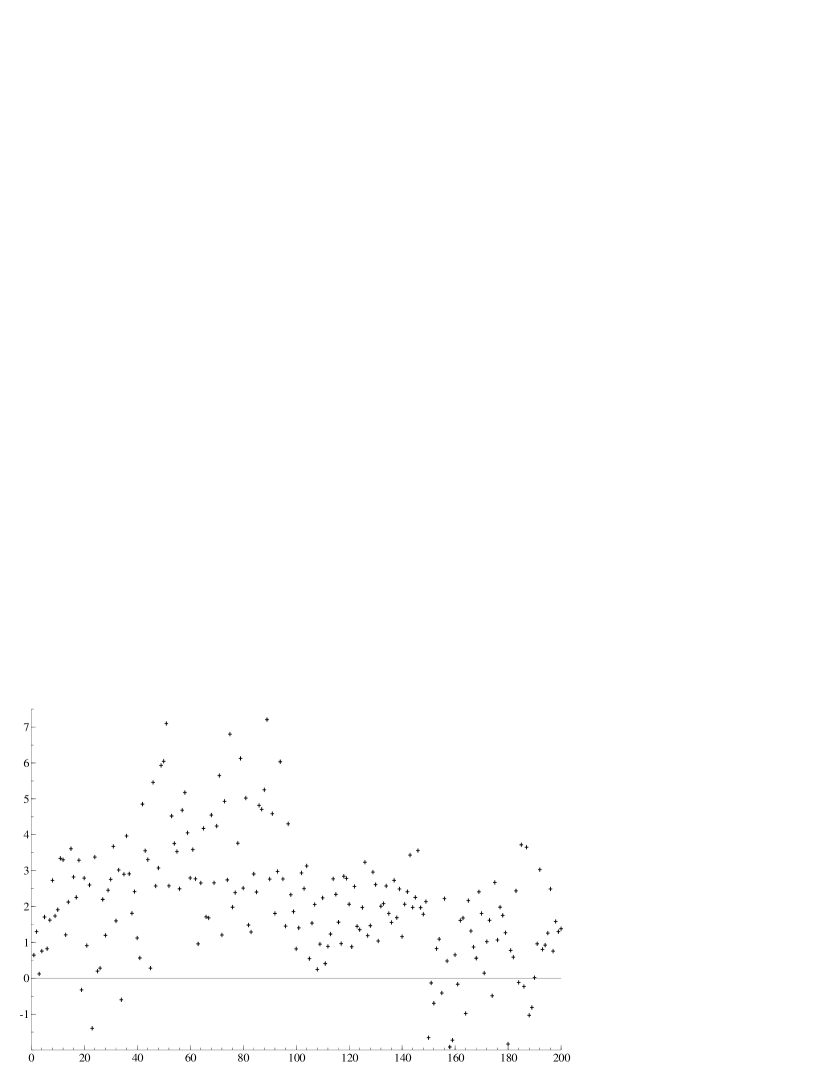

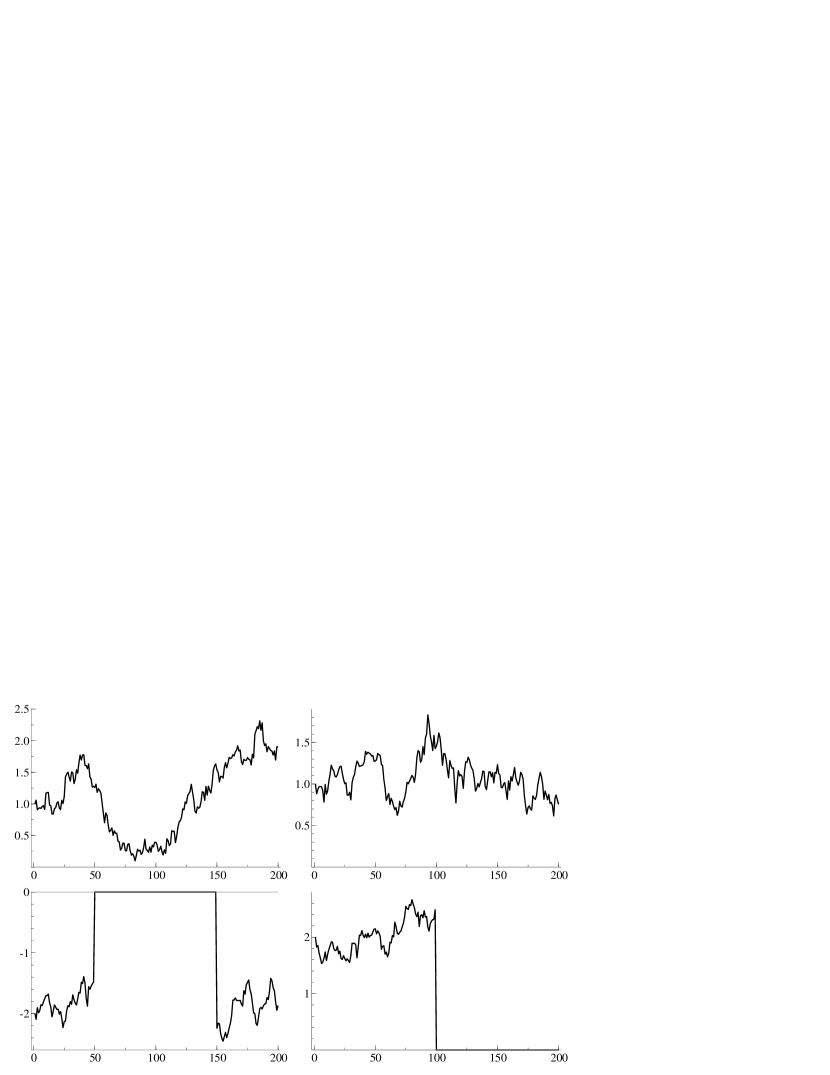

The purpose of the study in this subsection is the illustration and comparative analysis of the proposed and existing models. The univariate time series is generated from (13), based on the predictors and the true values of the parameters specified below. Twelve predictors are generated from the uniform distribution on , except for the first predictor that is constant as the intercept. The first four predictors are “active” and the others are “inactive,” in the sense that the coefficients of the former are non-zeros for all/some and the others are always zero, creating the situation suitable for the over-parametrized but sparse linear model. The data process is plotted in Figure 4(a), with the coefficients of the four active predictors, , in 4(b). The true value of the observational variance is for all .

For comparison, in addition to the DFL and DFHS priors, we also consider the double-exponential (DE) and horseshoe (HS) priors, i.e., the DFL/DFHS with . For clarity, we explicitly indicate the type of prior in the name of models, as in “DFL-DLMs.” These dynamic models have the same likelihood in (13) and differ in the modeling of state evolution. The observational variance is assumed to be constant over time, for all , and to follow inverse gamma prior ; see Section 4.2 (and S9.1). We set and in all the models. For baseline , we set or . The weight parameters ’s follow the independent gamma priors as in all models. For the parameter in the DFL-DLMs and DFHS-DLMs, we consider (i) , (ii) and (iii) . In the DE-DLMs and HS-DLMs, the initial state at is modeled by for the fair comparison with the DLF-DLMs. The three sets of hyperparameters are used: (i) , (ii) and (iii) . The posteriors are computed based on 3,000 iterations after 300 burn-in period. In predictive analysis, the posterior computation by the MCMC method is repeated for the dataset for each , including the estimation of the model parameters , to generate from the one-step ahead predictive distribution during the iterations of MCMC and compute the point forecast . To sample from the predictive distributions, it is necessary to simulate from prior ; see Section S6 for the technical details.

Posterior and predictive results

In Table 1, the posterior analyses of all the twelve models with various DFL/DE priors are summarized by the averages of the mean squared errors (MSEs) of the Bayes estimates (posterior means) for the dynamic coefficients and one-step ahead predictions. The computation of MSEs starts at , because the posteriors of DE-DLM with baseline zero are strongly biased to zero due to the prior of the initial state variable, as seen later in Figure 7(a). Among the models listed in the table, the DFL-DLMs with baseline zero perform better in almost all of the MSE measures, especially in the estimation of dynamically sparse coefficients, , and those of noises, for , supported by the newly-added shrinkage. In contrast, the MSEs of the active state variables for DE-DLMs are large due to the strong penalty on the dynamics assumed in the prior. The exception is the estimation of coefficient , where the shrinkage to zero is not coherent with the true values of and, probably for this reason, the DE-DLMs are more successful. The introduction of baselines, which is expected to improve the fitting of the models, increases the uncertainty in estimation and prediction under the DFL-DLMs, which could also explain their disproved predictive performance. This is because the baselines are redundant parameters for inactive predictors, in addition to the inefficiency for the estimation of the volatile state variables; see the discussions in Section S10.2 and Figure S7. In the following, we focus on the DFL-DLM with the mild shrinkage to zero, , the best DE-DLM in predictions, , to investigate their posterior and predictive distributions.

| No. | Model | or | Baseline | CIs | CRs | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| DFL | i | 0 | 250.93 | 136.80 | 199.95 | 189.68 | 0.08 | 250.08 | 1.64 | 0.94 | |

| ii | 0 | 249.38 | 134.22 | 198.34 | 190.97 | 0.16 | 246.35 | 1.65 | 0.94 | ||

| iii | 0 | 241.12 | 130.19 | 192.59 | 186.73 | 0.53 | 247.59 | 1.64 | 0.94 | ||

| i | 275.11 | 154.23 | 219.91 | 212.66 | 20.45 | 344.09 | 1.75 | 0.91 | |||

| ii | 293.88 | 147.81 | 208.71 | 215.10 | 16.52 | 289.69 | 1.75 | 0.93 | |||

| iii | 290.35 | 139.77 | 207.66 | 206.17 | 13.84 | 301.74 | 1.75 | 0.92 | |||

| DE | i | 0 | 312.76 | 129.69 | 207.31 | 226.57 | 14.61 | 278.45 | 2.38 | 0.97 | |

| ii | 0 | 284.38 | 134.92 | 202.55 | 224.75 | 12.64 | 277.71 | 2.43 | 0.97 | ||

| iii | 0 | 277.77 | 137.32 | 202.06 | 225.57 | 10.05 | 275.67 | 2.47 | 0.98 | ||

| i | 337.10 | 129.38 | 199.84 | 223.88 | 18.12 | 304.78 | 1.96 | 0.95 | |||

| ii | 345.93 | 122.63 | 205.24 | 214.07 | 18.07 | 304.05 | 1.96 | 0.96 | |||

| iii | 333.70 | 129.71 | 200.33 | 222.79 | 17.86 | 304.85 | 1.96 | 0.95 |

| No. | Model | or | Baseline | CIs | CRs | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| DFHS | i | 0 | 233.08 | 132.30 | 197.08 | 194.20 | 1.10 | 248.47 | 1.82 | 0.95 | |

| ii | 0 | 243.96 | 130.55 | 196.14 | 207.46 | 1.72 | 251.31 | 1.89 | 0.95 | ||

| iii | 0 | 259.61 | 127.47 | 191.68 | 208.54 | 3.34 | 257.21 | 1.95 | 0.97 | ||

| i | 355.53 | 142.04 | 215.38 | 219.99 | 16.58 | 320.10 | 1.93 | 0.94 | |||

| ii | 341.35 | 142.37 | 208.04 | 229.33 | 19.11 | 309.38 | 2.03 | 0.95 | |||

| iii | 385.78 | 139.92 | 205.93 | 222.58 | 17.56 | 301.53 | 2.13 | 0.96 | |||

| HS | i | 0 | 260.62 | 138.17 | 199.10 | 216.92 | 11.66 | 272.37 | 2.43 | 0.98 | |

| ii | 0 | 274.58 | 136.65 | 201.25 | 213.32 | 9.93 | 274.60 | 2.43 | 0.98 | ||

| iii | 0 | 266.22 | 135.74 | 201.99 | 226.11 | 9.40 | 272.69 | 2.42 | 0.98 | ||

| i | 319.69 | 128.58 | 201.88 | 221.49 | 17.26 | 308.28 | 2.00 | 0.96 | |||

| ii | 329.86 | 130.62 | 198.41 | 218.08 | 18.32 | 310.41 | 1.98 | 0.96 | |||

| iii | 326.85 | 129.95 | 200.13 | 216.51 | 17.57 | 302.03 | 1.97 | 0.97 |

The same posterior and predictive summaries for the DFHS-DLMs and HS-DLMs are given in Table 2. The DFHS-DLMs are as competitive as, or slightly improved from, the DFL-DLMs in the estimation of the non-zero coefficients, while the MSEs for zero coefficients and predictions slightly increase under the DFHS-DLMs due to the strengthened shrinkage on dynamics. One notable observation here is that the best DFHS-DLM in terms of predictive performance is with the strongest shrinkage to zero, unlike the case of DFL-DLMs. It could be explained as that the balance of two conflicting shrinkage effects is affected by the use of horseshoe prior, which change the optimal amount of shrinkage to zero.

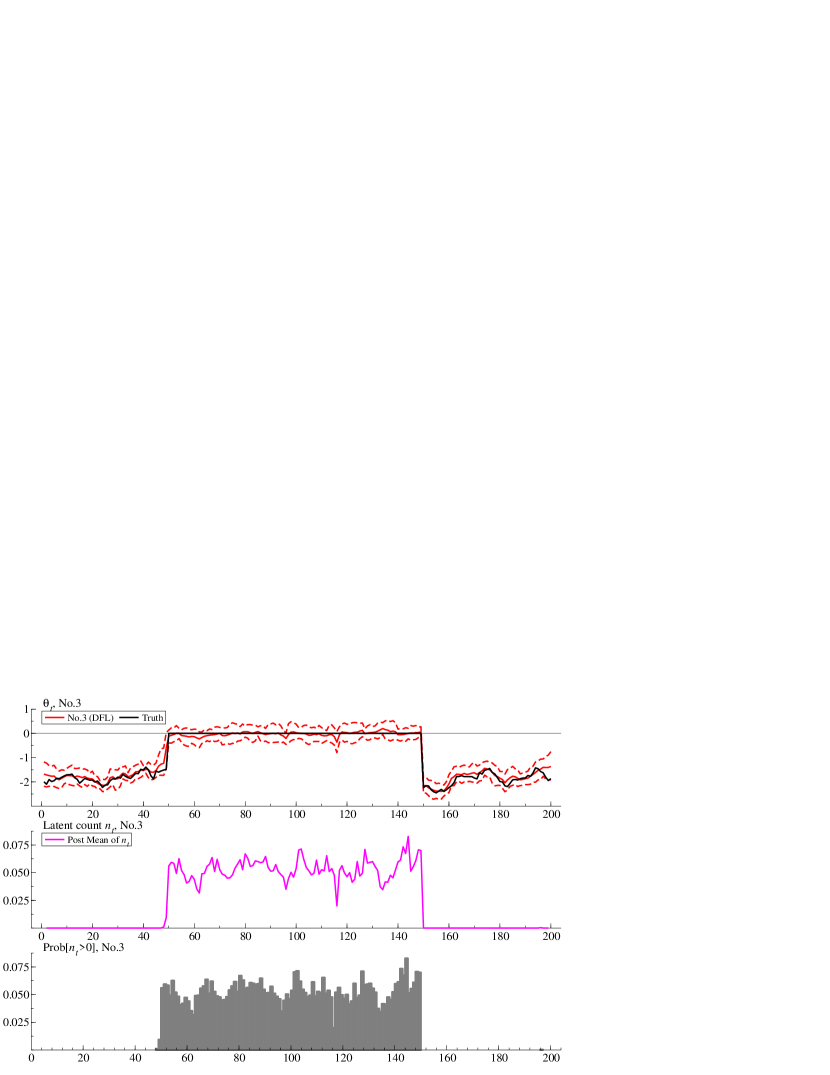

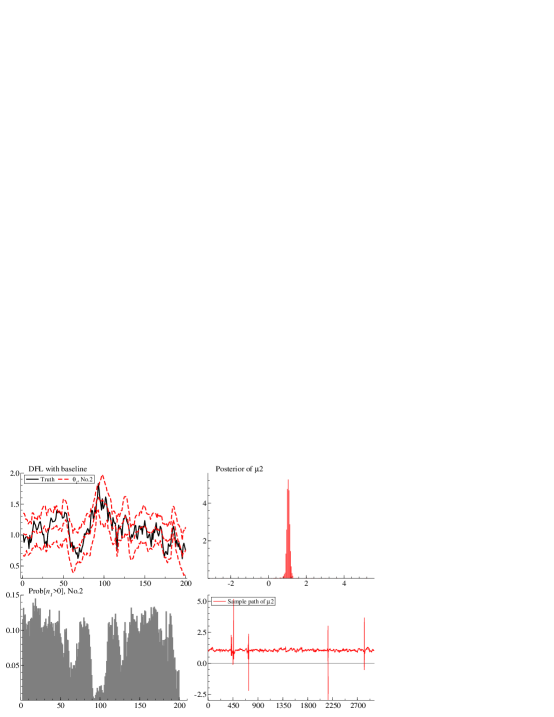

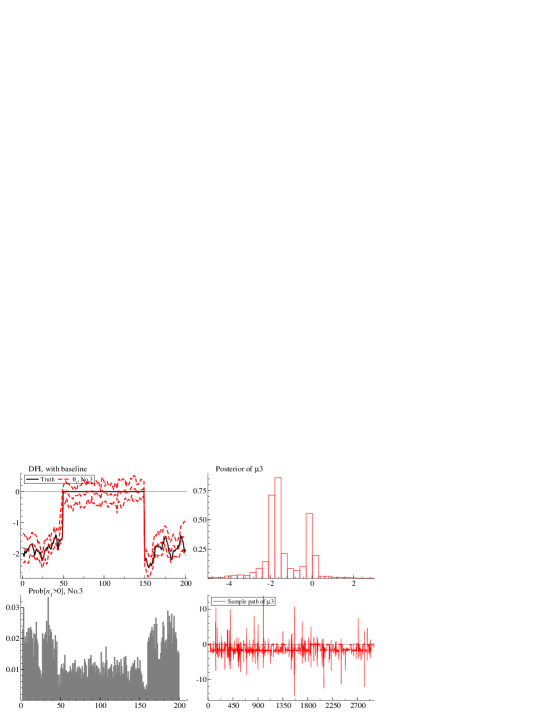

In the estimation of dynamic coefficients, the third predictor is of the special interest for its dynamic “significance.” The posterior of computed by model is shown in Figure 5 with its true values, the posterior means of the latent count , and the posterior probabilities of positive count . In addition to the success of the posterior of in tracking the true values in the top panel of this figure, we can confirm in the middle and bottom panels that the latent count is more likely to be positive in the period when the predictor is inactive. This result is easily expected from the structure of the augmented model; if the positive count is sampled, then we have the additional observational equation of in the synthetic model, whose information helps to shrink the state variable to zero in the posterior. This clear correspondence between the sparsity in state variables and the values of latent counts is not assumed a priori but the result of posterior learning (Section S10.1), hence implies the potential interpretation of the posterior of as the indicator of “insignificance” of state variables. This point is further examined in the next subsection through the application to the real macroeconomic dataset.

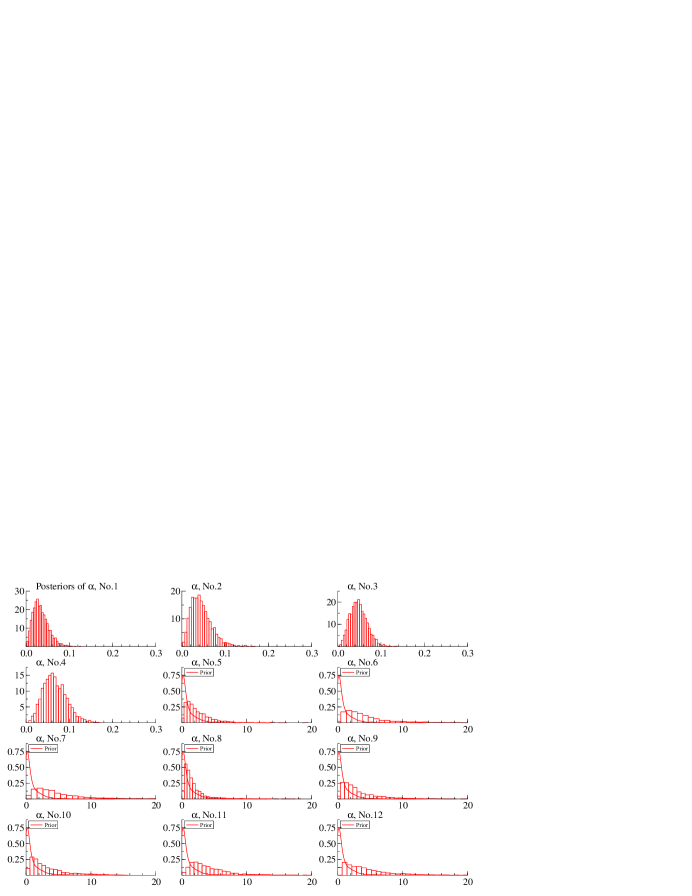

The posteriors of ’s are listed in Figure 6. It is clear in this figure that the values of these weights become extremely small for the active predictors, while being sufficiently large for the inactive predictors. The extremely small value of weight indicates that the first penalty, or the shrinkage effect to zero, is almost negligible. The large value of weight forces the model to shrink the state variable to zero more aggressively, which is the appropriate treatment for the zero coefficients.

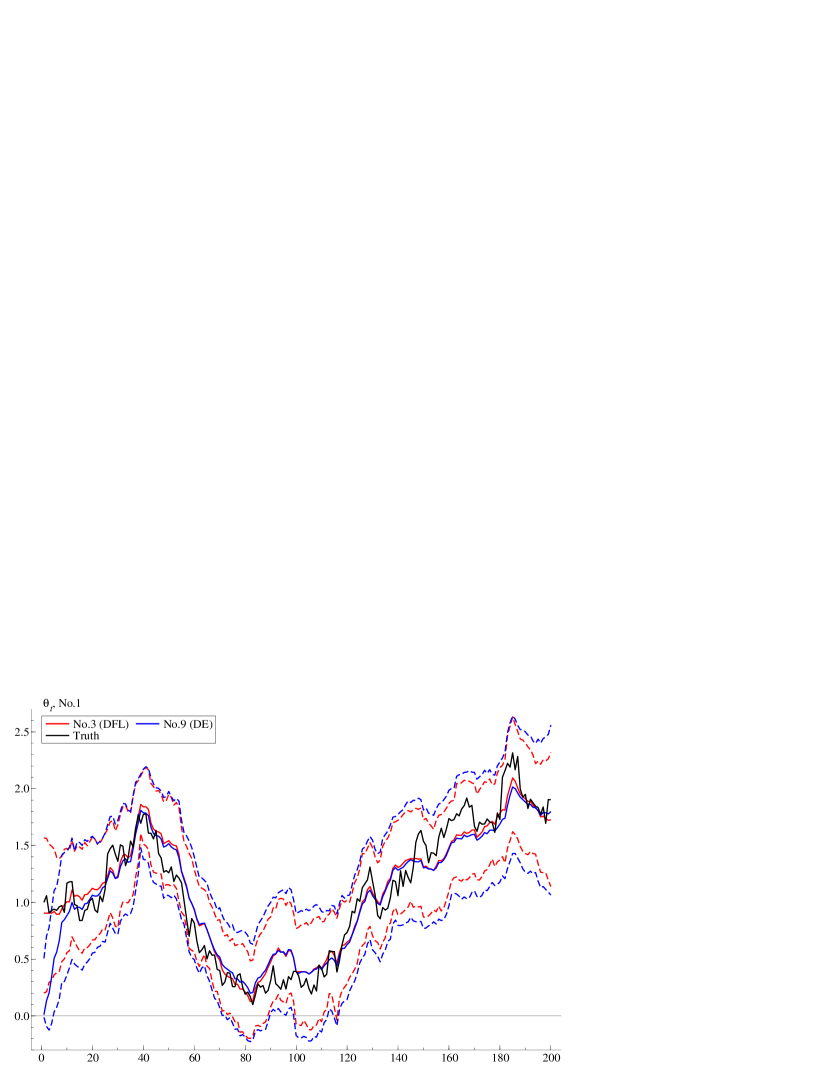

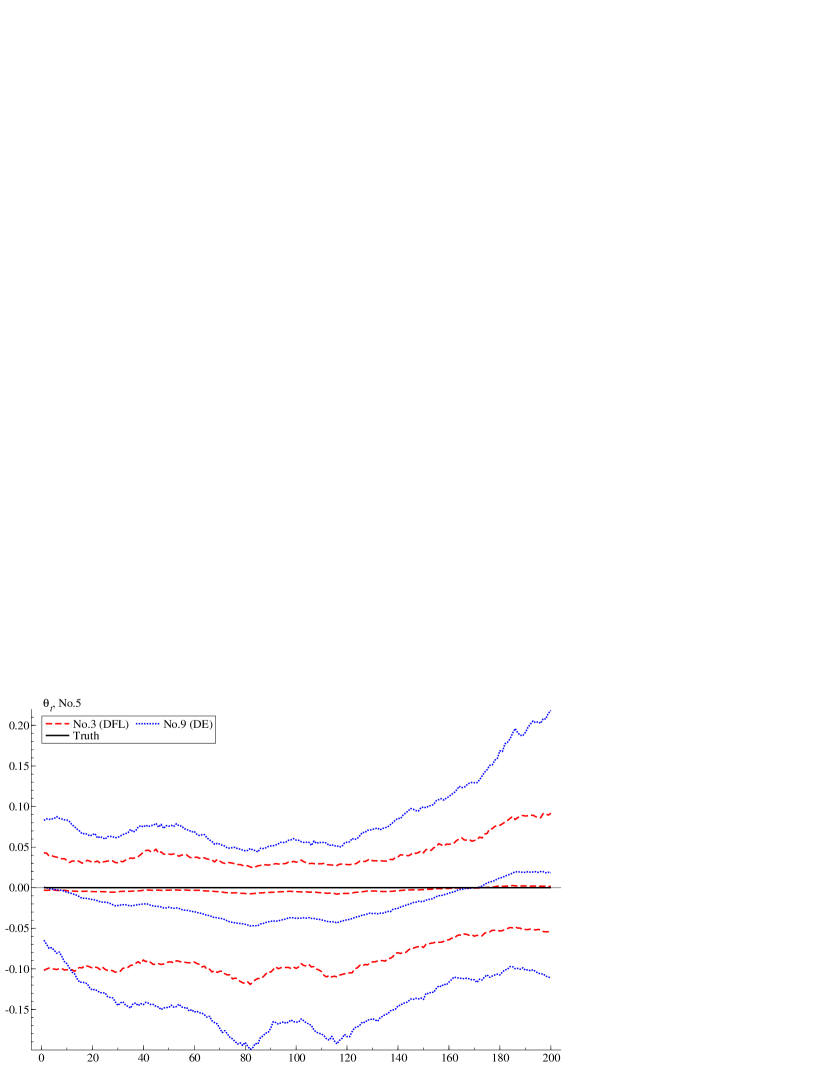

Figure 7(a) and 7(b) show the superimposed posterior trajectories of the state variables, and , of the DFL-DLM and DE-DLM . For the active predictor, as seen in the example of , the posterior means and 95% credible intervals of both models almost overlap one another all the time. This result is consistent with our observation in Figure 6 that the posterior of weight concentrates around small values and the DFL prior reduces to the DE prior. In contrast, the difference of the two models is clear in the uncertainty of state variables for the inactive predictors. The large weight on the first penalty induces the strong shrinkage to zero, shrinking the posterior locations to zero and narrowing the credible intervals. Consequently, those noise predictors do not contribute to the variation of observation in the predictive analysis.

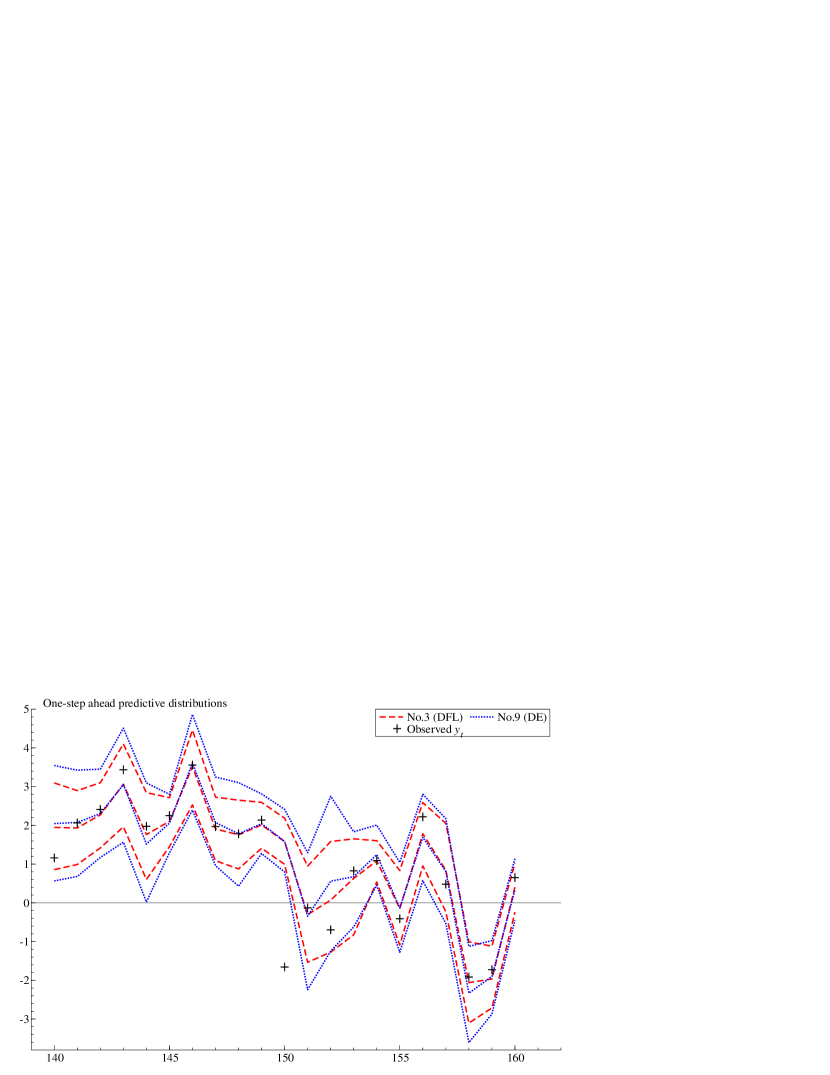

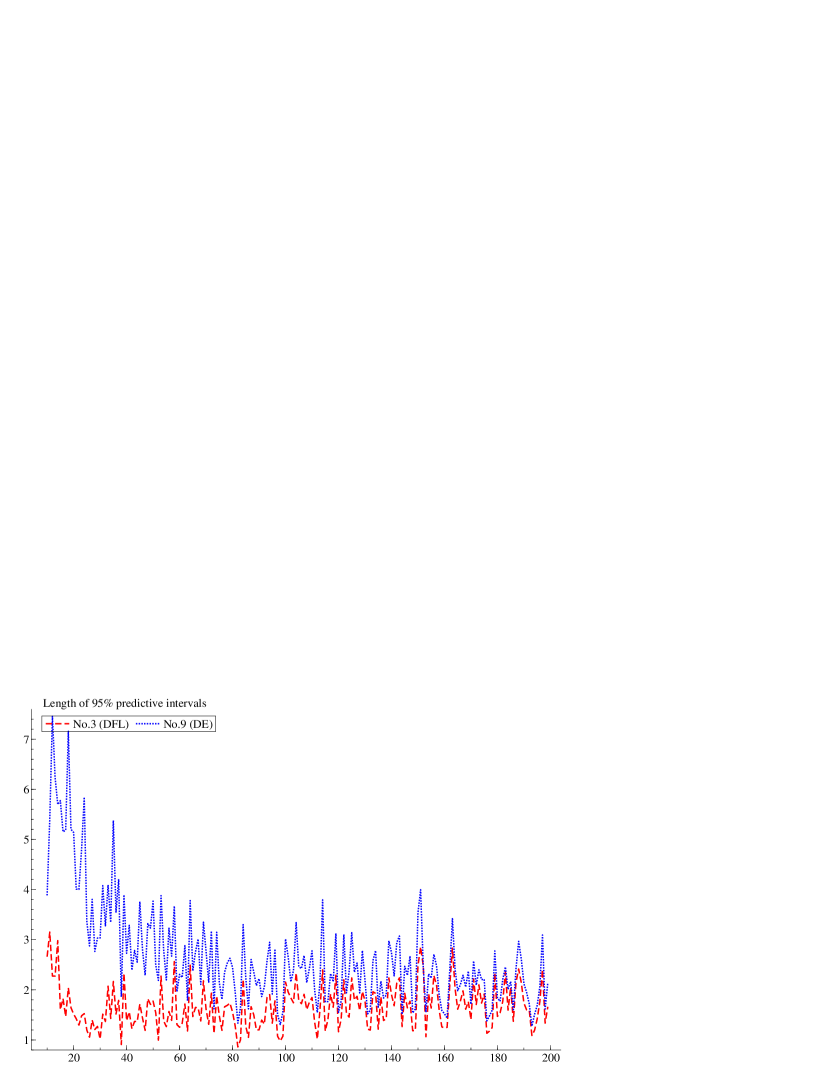

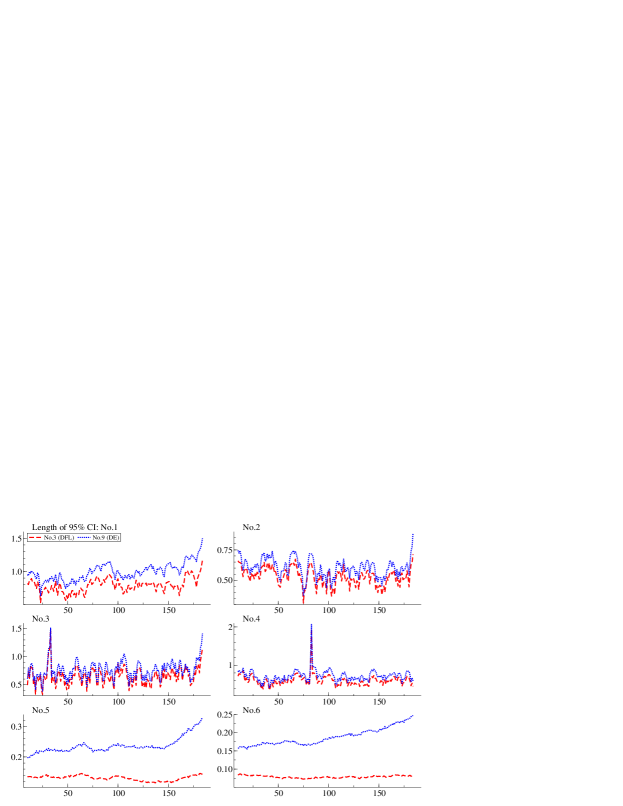

The twelve models are repeatedly estimated by the MCMC method in the sequential way, starting at time , to provide the one-step ahead forecast distributions. In addition to the summary of predictive performances in Table 1, we here focus on and and their predictions at each time point. Figure 8(a) shows the predictive means and 95% credible intervals of and with the actual observations at . Notably, the predictive uncertainty under is smaller than more clearly before . This is exactly the change-point for to becomes non-zero again and, before , model benefits the shrinkage to zero and could improve the predictive performance. The dynamics of the lengths of 95% credible intervals, which are summarized into the averages in Table 1, are shown in Figure 8(b), where we confirm that the predictive intervals of is narrower than not just on average, but at all .

5.2 Macroeconomic data and latent threshold models

The posterior plot of latent counts ’s in Figure 5 suggests, informally but empirically, the potential use of this quantity as the indicator of “(in)significance” of coefficients. In this section, we further examine this aspect of the DFL prior– the (dis)similarity of shrinkage to zero and variable selection– through the comparison with the latent threshold models (LTMs), that are the more formal approach to the dynamic variable selection (e.g., Nakajima and West 2013b, 2015). The LTMs explicitly distinguish the latent and realized state variables, and for -th coefficient, and connect them by the indicator function as,

| (15) |

where latent state variable follows a Gaussian AR(1) process and is some positive, non-dynamic threshold. The probability that this coefficient is thresholded to zero at time is parametrized by and can be computed explicitly in the posterior analysis. The posterior analysis of the LTMs by the MCMC method is feasible, but computationally costly both in coding and computational time, as typical in the models of variable selection.

The example of the analysis of the US macroeconomic variables by the LTMs are taken from Nakajima and West (2013a). The vector of the inflation, unemployment and nominal interest rates is denoted by and observed quarterly between 1977 and 2007. The base model is the time-varying vector autoregressive model with order 3, the likelihood of which is

where is the diagonal matrix of log-Gaussian stochastic volatilities and is the lower-triangular matrix with diagonal zeros. Each entry of , and follows the Gaussian, stationary AR(1) process with latent threshold in (15). The parameters of interest are and , that determine the lagged/simultaneous correlation between variables. The graphical, conditional dependence structure of the three macroeconomic variables captured by , or , is of great importance in the macroeconomic studies. We followed the computational procedure and used the same hyperparameter settings in Nakajima and West (2013a).

In this study, our interest is in whether the time-varying vector autoregressive models with the DFL prior produces the same patterns of sparse structure in and as the LTM does. We replace the prior processes for , and by the DFL priors, and compute the posterior of the latent counts , or , that are compared with the posterior exclusion probability of the LTM. To make the DFL prior compatible with the prior processes used in Nakajima and West (2013a) for state variable that are very persistent over time, we adjust the hyperparameters in the DFL prior as and for all the entries of and , and and for . For this choice of priors, we confirmed that the posteriors of error variances, or stochastic volatilities, become almost identical in both DFL-DLM and LTM (Section S11.1). The posteriors are computed by the MCMC method of 50,000 iterations after 5,000 burn-in. The chain is set relatively long, due to the slow convergence of the regression coefficients in the LTM that are sampled by the single-move sampler, not by FFBS, as reported in Nakajima and West (2013a).

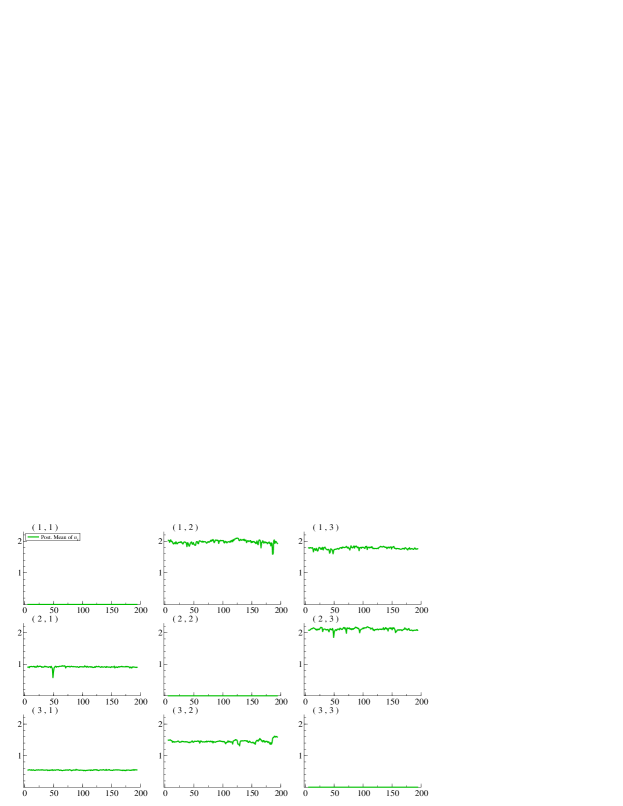

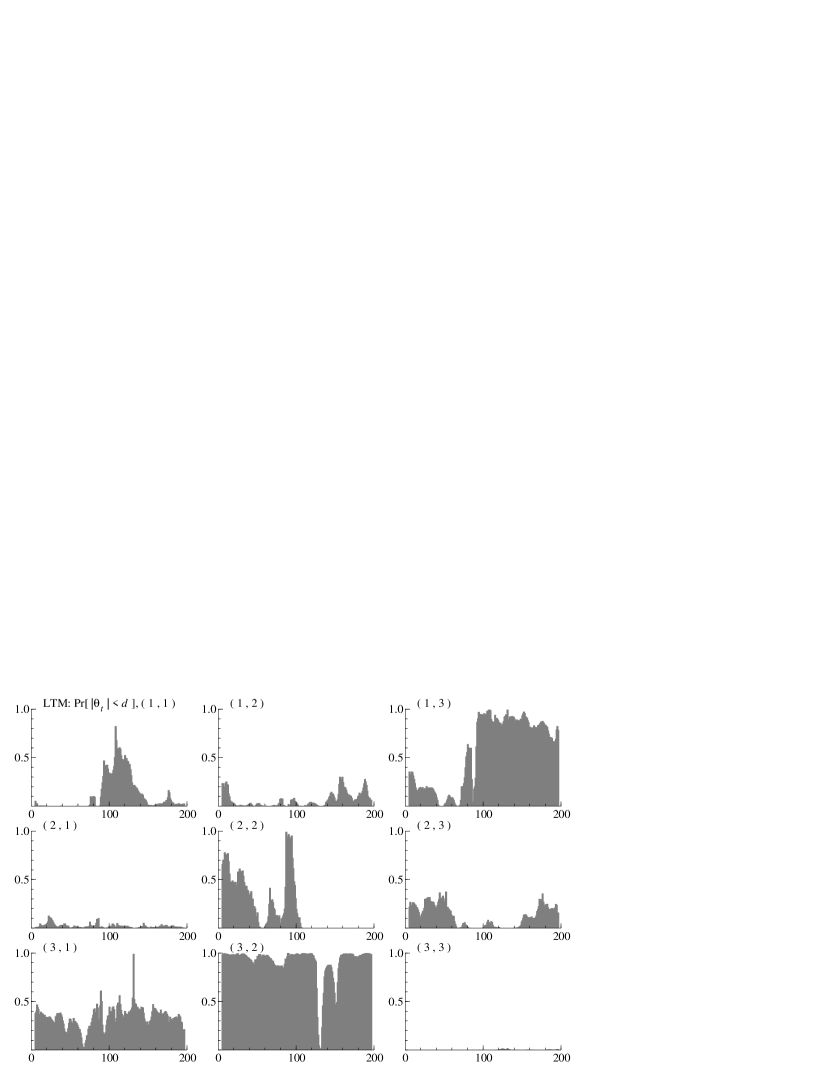

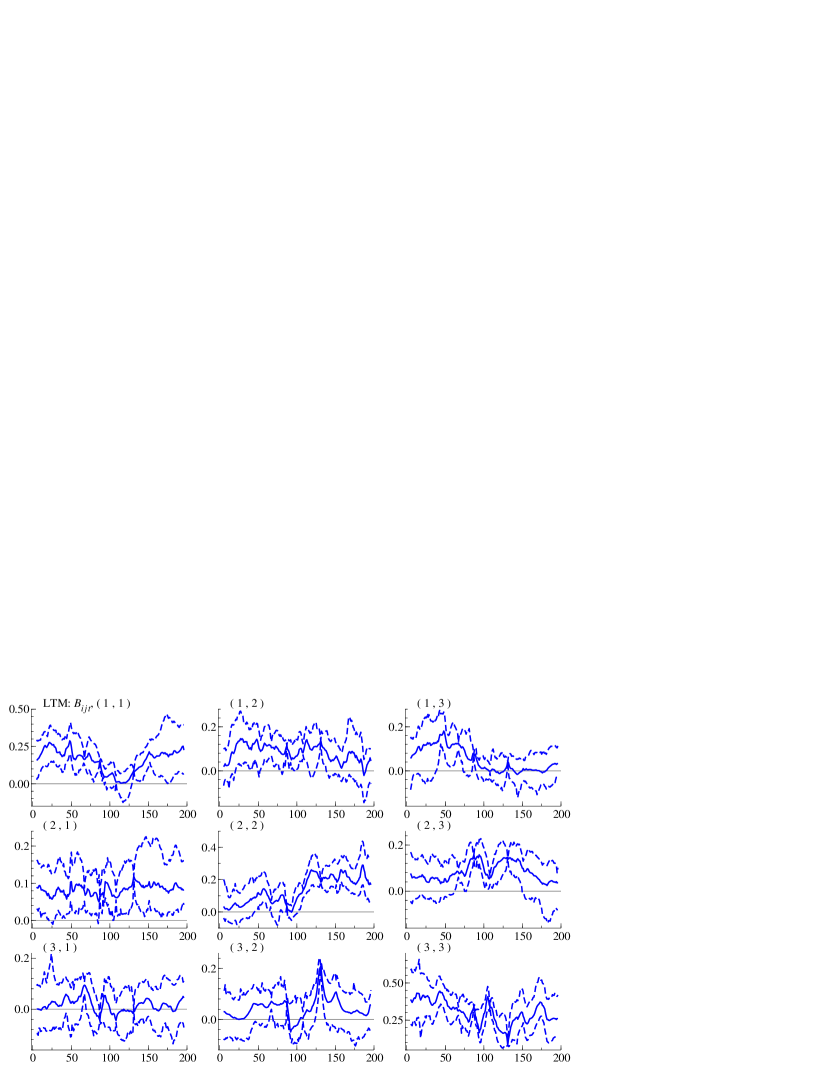

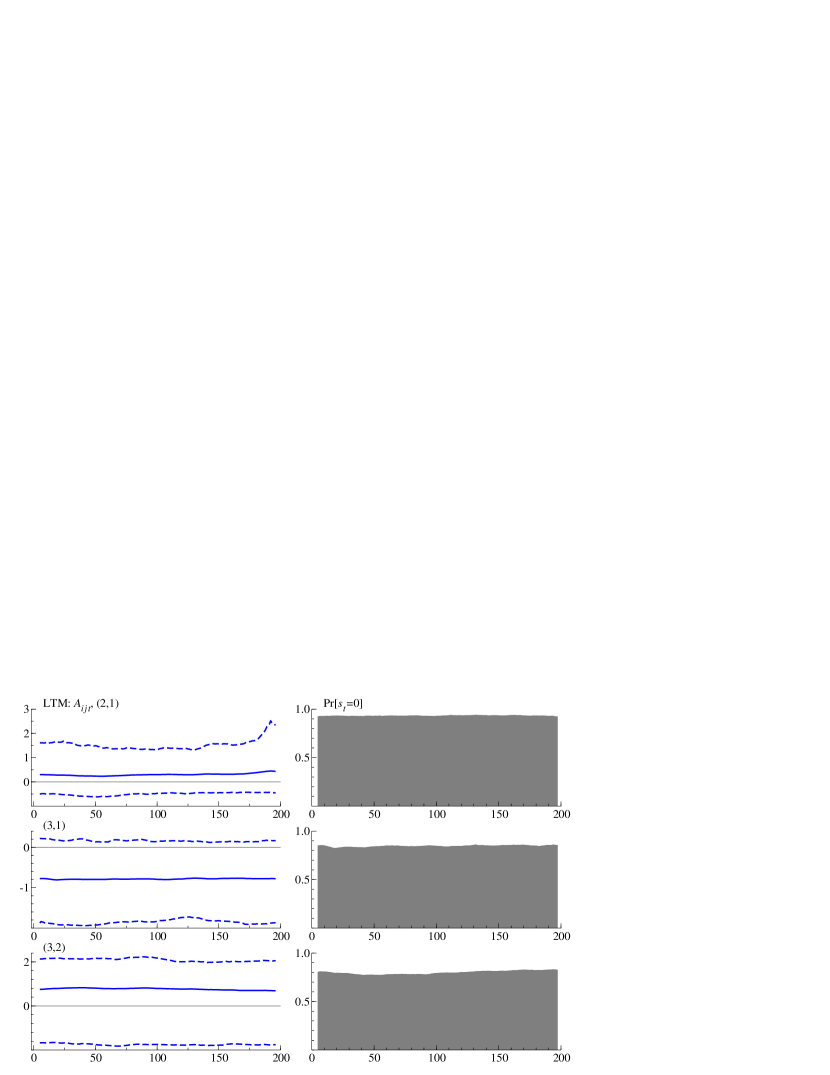

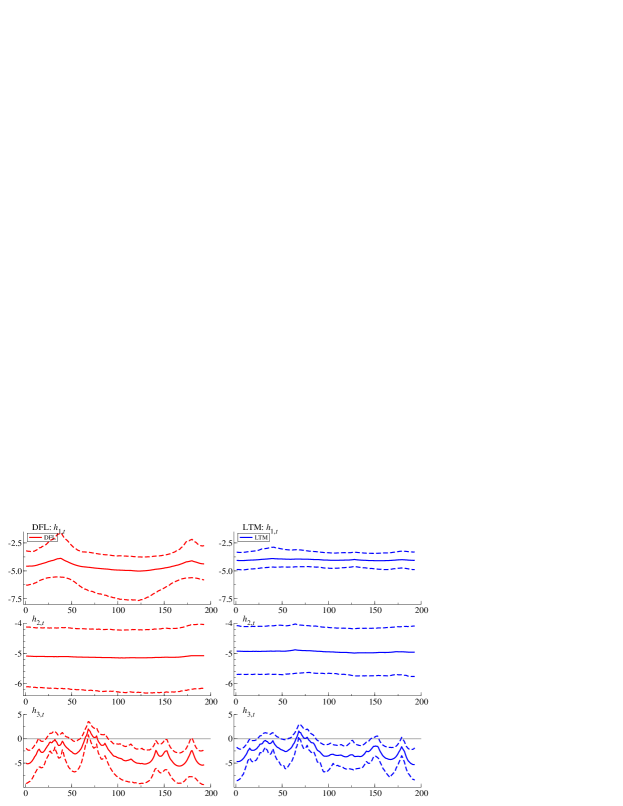

For the nine state variables of lag-1 coefficient matrix , the posterior probability of positive counts for the DFL-DLM and the posterior exclusion probabilities for the LTM are displayed in Figure 9(a) and 9(b), respectively. The estimates of diagonal entries in the DFL-DLM are least affected by shrinkage, while most of the off-diagonal entries are subject to the strong shrink to zero. The LTM, in contrast, shows the dynamic pattern of thresholding, even in the diagonal entries (e.g., (3,1)-entry). This pattern is sensitively affected by the choice of priors, while we observed the similar posterior results of the DFL-DLMs for different choices of priors and stochastic volatilities. We also double-checked the less-dynamic shrinkage under the DFL-DLM in the posterior expectation of latent counts (Section S11.2).

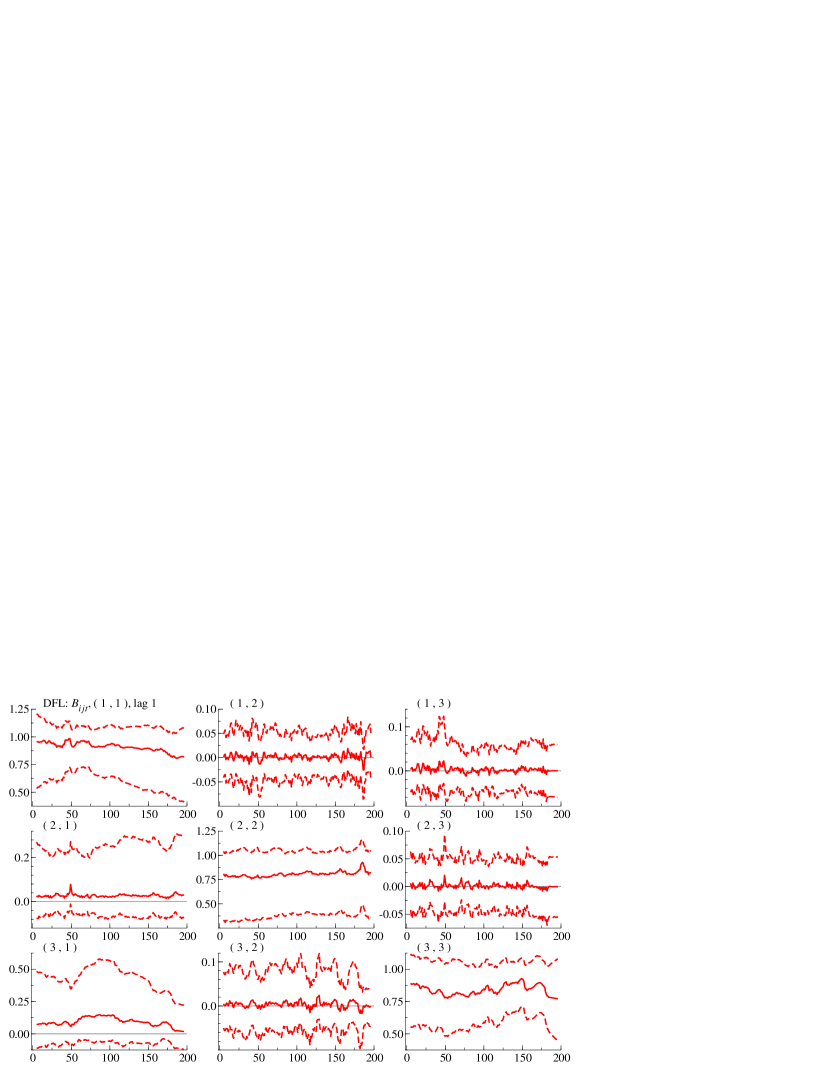

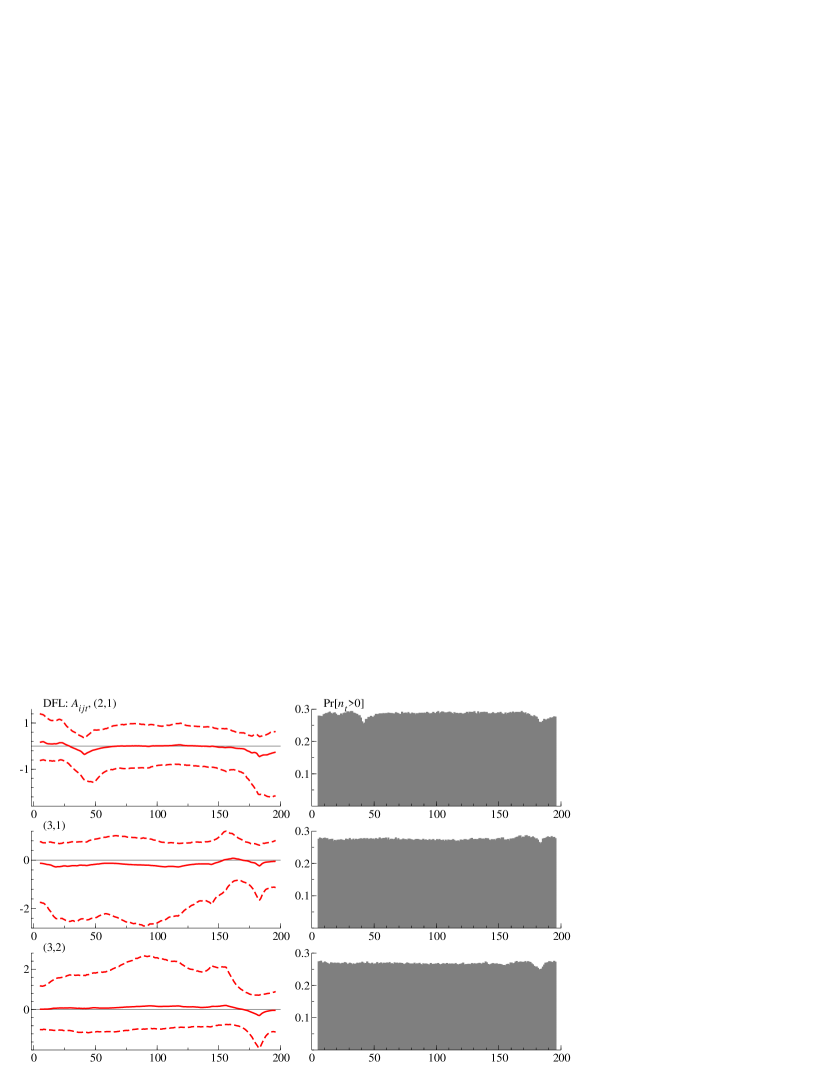

The same outputs of the posterior analysis for simultaneous correlation are shown in Figure 11(a) and 11(b). Both models deny the activeness of simultaneous correlations, but not completely. For example, the LTM leaves about 20% posterior probability of including the third parameter, i.e., the necessity of the simultaneous regression of the interest rate on the unemployment rate. In the DFL-DLM, the posterior probabilities of positive counts in the DFL are much smaller than those of , and the estimates of coefficients are not the exact zero at many points. We may conclude that both models agree that the information on the graphical structure in this dataset is limited.

Overall, in contrast to the study of simulated data, the posterior probabilities of positive counts are less dynamic, both for and . One may inflate the dynamics of shrinkage in the posteriors by choosing another set of hyperparameters that makes the DLF prior more volatile, but the overall trend of posterior results, such as the significance of the diagonal elements of , remains unchanged.

6 Concluding Remark

This research on the DFL process is the formal Bayesian attempt at the introduction of the multiple, conflicting shrinkage effects. The additional shrinkage newly introduced in the DLF process is separated from the existing shrinkage on dynamics and comprises the synthetic likelihood, with which the model becomes the CDLM and allows the posterior computation by FFBS. Although the posterior computation is limited to the MCMC method in this study, the CDLM representation could be useful potentially in deriving other computational methodologies, such as the customized version of sequential Monte Carlo methods.

The research of this type can be further developed in several directions. For example, the concept of fusing two penalty functions into the prior is generalized for arbitrary loss functions, and , as

with the integrability condition to make a proper density. This “translation” of loss functions to statistical models has been well studied in decision making problems in general (Müller, 1999) and developed particularly in the context of shrinkage priors (Fahrmeir et al., 2010; Polson and Sokolov, 2019). The DFL prior belongs to this class of priors by setting and . The important examples include; the dynamic version of Bayesian elastic net as the combination of and loss functions (Hans, 2011); the Bayesian bridge with loss functions for (Polson et al., 2014); and the loss functions induced by horseshoe density, where (Carvalho et al., 2009, 2010). In those examples, the representation of the scale mixture of normals for are available, for which the augment in Section 2.1 is valid even for this general class. Yet, it has not been known for those models, especially for the horseshoe ones, whether the latent augmentation of normalizing constant is available to enable the fast posterior computation by FFBS as in the DFL prior.

The vector-autoregressive models in Section 5.2 can be, as mentioned in the introduction, an important application of the proposed shrinkage priors. The problem of increased number of parameters has been raised at the early stage of development (Primiceri, 2005; Del Negro and Primiceri, 2015), and the use of shrinkage prior for such problem is actively investigated (Kastner, 2019; Kastner and Huber, 2020). It is worth revisiting the problem of sparse estimation of these econometric models from the viewpoint of the priors of fused penalties for the time-varying parameters.

References

-

Abramowitz and Stegun (1964)

Abramowitz, M. and Stegun, I. (1964).

“Handbook of Mathematical Functions.”

Washington, DC: National Bureau of Standards.

URL http://www.math.sfu.ca/ cbm/aands/ - Andrews and Mallows (1974) Andrews, D. F. and Mallows, C. L. (1974). “Scale mixtures of normal distributions.” Journal of the Royal Statistical Society (Series B: Methodological), 36: 99–102.

- Belmonte et al. (2014) Belmonte, M. A., Koop, G., and Korobilis, D. (2014). “Hierarchical shrinkage in time-varying parameter models.” Journal of Forecasting, 33(1): 80–94.

- Betancourt et al. (2017) Betancourt, B., Rodríguez, A., and Boyd, N. (2017). “Bayesian Fused Lasso regression for dynamic binary networks.” Journal of Computational and Graphical Statistics, 26(4): 840–850.

- Bitto and Frühwirth-Schnatter (2019) Bitto, A. and Frühwirth-Schnatter, S. (2019). “Achieving shrinkage in a time-varying parameter model framework.” Journal of Econometrics, 210(1): 75–97.

- Carter and Kohn (1994) Carter, C. K. and Kohn, R. (1994). “On Gibbs sampling for state space models.” Biometrika, 81(3): 541–553.

- Carvalho et al. (2009) Carvalho, C. M., Polson, N. G., and Scott, J. G. (2009). “Handling Sparsity via the Horseshoe.” In AISTATS, volume 5, 73–80.

- Carvalho et al. (2010) — (2010). “The horseshoe estimator for sparse signals.” Biometrika, 97(2): 465–480.

- Del Negro and Primiceri (2015) Del Negro, M. and Primiceri, G. E. (2015). “Time varying structural vector autoregressions and monetary policy: a corrigendum.” The review of economic studies, 82(4): 1342–1345.

- Doornik (2007) Doornik, J. A. (2007). Object-Oriented Matrix Programming Using Ox, 3rd ed.. London: Timberlake Consultants Press and Oxford, 3rd edition.

- Eisenstat et al. (2016) Eisenstat, E., Chan, J. C., and Strachan, R. W. (2016). “Stochastic model specification search for time-varying parameter VARs.” Econometric Reviews, 35(8-10): 1638–1665.

- Fahrmeir et al. (2010) Fahrmeir, L., Kneib, T., and Konrath, S. (2010). “Bayesian regularisation in structured additive regression: a unifying perspective on shrinkage, smoothing and predictor selection.” Statistics and Computing, 20(2): 203–219.

- Feldkircher et al. (2017) Feldkircher, M., Huber, F., and Kastner, G. (2017). “Sophisticated and small versus simple and sizeable: When does it pay off to introduce drifting coefficients in Bayesian VARs?” arXiv preprint arXiv:1711.00564.

- Finegold and Drton (2011) Finegold, M. and Drton, M. (2011). “Robust graphical modeling of gene networks using classical and alternative t-distributions.” The Annals of Applied Statistics, 1057–1080.

- Frühwirth-Schnatter (1994) Frühwirth-Schnatter, S. (1994). “Data augmentation and dynamic linear models.” Journal of time series analysis, 15(2): 183–202.

- Frühwirth-Schnatter and Wagner (2010) Frühwirth-Schnatter, S. and Wagner, H. (2010). “Stochastic model specification search for Gaussian and partial non-Gaussian state space models.” Journal of Econometrics, 154(1): 85–100.

- Gordy (1998) Gordy, M. B. (1998). “A generalization of generalized beta distributions.” Finance and Economics Discussion Series, Federal Reserve Board.

- Gruber and West (2016) Gruber, L. and West, M. (2016). “GPU-accelerated Bayesian learning in simultaneous graphical dynamic linear models.” Bayesian Analysis, 11(1): 125–149.

- Hans (2011) Hans, C. (2011). “Elastic net regression modeling with the orthant normal prior.” Journal of the American Statistical Association, 106(496): 1383–1393.

- Huber et al. (2019) Huber, F., Kastner, G., and Feldkircher, M. (2019). “Should I stay or should I go? A latent threshold approach to large-scale mixture innovation models.” Journal of Applied Econometrics, 34(5): 621–640.

- Irie and West (2019) Irie, K. and West, M. (2019). “Bayesian Emulation for Multi-Step Optimization in Decision Problems.” Bayesian Analysis, 14(1): 137–160.

- Jacquier et al. (1994) Jacquier, E., Polson, N. G., and Rossi, P. E. (1994). “Bayesian analysis of stochastic volatility models.” Journal of Business & Economic Statistics, 12(4): 371–389.

- Kalli and Griffin (2014) Kalli, M. and Griffin, J. E. (2014). “Time-varying sparsity in dynamic regression models.” Journal of Econometrics, 178(2): 779–793.

- Kastner (2019) Kastner, G. (2019). “Sparse Bayesian time-varying covariance estimation in many dimensions.” Journal of Econometrics, 210(1): 98–115.

- Kastner and Frühwirth-Schnatter (2014) Kastner, G. and Frühwirth-Schnatter, S. (2014). “Ancillarity-sufficiency interweaving strategy (ASIS) for boosting MCMC estimation of stochastic volatility models.” Computational Statistics & Data Analysis, 76: 408–423.

- Kastner and Huber (2020) Kastner, G. and Huber, F. (2020). “Sparse Bayesian vector autoregressions in huge dimensions.” Journal of Forecasting.

- Kolm and Ritter (2015) Kolm, P. N. and Ritter, G. (2015). “Multiperiod portfolio selection and Bayesian dynamic models.” Risk, 28: 50–54.

- Kowal et al. (2019) Kowal, D. R., Matteson, D. S., and Ruppert, D. (2019). “Dynamic shrinkage processes.” Journal of Royal Statistical Society, forthcoming.

- Kyung et al. (2010) Kyung, M., Gill, J., Ghosh, M., and Casella, G. (2010). “Penalized regression, standard errors, and Bayesian lassos.” Bayesian Analysis, 5(2): 369–411.

-

Liu et al. (2012)

Liu, Y., Wichura, M. J., and Drton, M. (2012).

“Rejection sampling for an extended Gamma distribution.”

Unpublished Manuscript.

URL http://www.columbia.edu/ yl2802/extgamma.pdf - Müller (1999) Müller, P. (1999). “Simulation based optimal design.” In Bernardo, J. M., Berger, J. O., Dawid, A. P., and Smith, A. F. M. (eds.), Bayesian Statistics 6, 459–474. Oxford University Press.

- Nakajima and West (2013a) Nakajima, J. and West, M. (2013a). “Bayesian analysis of latent threshold dynamic models.” Journal of Business and Economic Statistics, 31: 151–164.

- Nakajima and West (2013b) — (2013b). “Bayesian dynamic factor models: Latent threshold approach.” Journal of Financial Econometrics, 11: 116–153.

- Nakajima and West (2015) — (2015). “Dynamic network signal processing using latent threshold models.” Digital Signal Processing, 47: 6–15.

- Park and Casella (2008) Park, T. and Casella, G. (2008). “The Bayesian lasso.” Journal of the American Statistical Association, 103: 681–686.

- Polson et al. (2014) Polson, N. G., Scott, J. G., and Windle, J. (2014). “The bayesian bridge.” Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(4): 713–733.

- Polson and Sokolov (2019) Polson, N. G. and Sokolov, V. (2019). “Bayesian regularization: From Tikhonov to horseshoe.” Wiley Interdisciplinary Reviews: Computational Statistics, 11(4): e1463.

- Primiceri (2005) Primiceri, G. E. (2005). “Time varying structural vector autoregressions and monetary policy.” The Review of Economic Studies, 72(3): 821–852.

- Ročková and McAlinn (2020) Ročková, V. and McAlinn, K. (2020). “Dynamic variable selection with spike-and-slab process priors.” Bayesian Analysis.

- Shephard and Pitt (1997) Shephard, N. and Pitt, M. K. (1997). “Likelihood analysis of non-Gaussian measurement time series.” Biometrika, 84(3): 653–667.

-

Uribe and Lopes (2017)

Uribe, P. V. and Lopes, H. F. (2017).

“Dynamic sparsity on dynamic regression models.”

Unpublished Manuscript.

URL http://hedibert.org/wpcontent/uploads/2018/06/uribe-lopes-Sep2017.pdf - van Dyk and Park (2008) van Dyk, D. A. and Park, T. (2008). “Partially collapsed Gibbs samplers: Theory and methods.” Journal of the American Statistical Association, 103(482): 790–796.

- Watanabe and Omori (2004) Watanabe, T. and Omori, Y. (2004). “A multi-move sampler for estimating non-Gaussian time series models: Comments on Shephard & Pitt (1997).” Biometrika, 246–248.

- West (1984) West, M. (1984). “Outlier models and prior distributions in Bayesian linear regression.” Journal of the Royal Statistical Society (Series B: Methodological), 46: 431–439.

- West (1987) — (1987). “On scale mixtures of normal distributions.” Biometrika, 74: 646–648.

- West and Harrison (1997) West, M. and Harrison, P. J. (1997). Bayesian Forecasting and Dynamic Models. Springer Verlag, 2nd edition.

- Zhao et al. (2016) Zhao, Z. Y., Xie, M., and West, M. (2016). “Dynamic dependence networks: Financial time series forecasting and portfolio decisions.” Applied Stochastic Models in Business and Industry, 32(3): 311–332.

Supplemental Materials for “Bayesian Dynamic Fused LASSO”

Kaoru Irie

Faculty of Economics, The University of Tokyo

Overviews

The contents covered in this document are summarized as follows:

-

•

Section S1 proves Proposition 2.1 in the main text and provides the closed form of normalizing constant .

-

•

Section S2 also computes when . This result is used in drawing the density function in Figure 1 of the main text.

-

•

Section S3 proves Proposition 2.3 and writes down the augmented joint densities of in which we read off the synthetic state space model.

-

•

Section S4 gives the explicit form of the expectation and distribution of conditional shrinkage effect, and . The examples of such expectations and densities are drawn and discussed from the viewpoint of subjective elicitation of the prior, while the proof will be given in the later sections.

-

•

Section S5 computes .

-

•

Section S6 derives , and also explains the procedure of simulating from . This is an essential step in forecasting.

-

•

Section S7 is for the discussion and details of estimation of weight parameters and baseline . In each subsection, we discuss,

-

–

the conjugate priors for and the simulation from the full conditionals.

-

–

the prior of half-Cauchy type for and the simulation from the full conditionals.

-

–

the prior for baseline and its full conditional.

-

–

-

•

Section S8 proves that the horseshoe prior can be expressed as the hierarchical Bayesian LASSO.

-

•

Section S9 provides the details of variance model : the scaled version of DFL-DLMs with variance and the log-Gaussian stochastic volatility .

-

•

Section S10 stores the additional results in the simulation study in Section 5.1.

-

•

Section S11 records some posterior plots in the application to the macroeconomic study in Section 5.2.

Appendix S1 Proof of Proposition 2.1

Equation (3) in the main text provides the mixture representation of the normalizing constant as

where and independently. Set and . Then, by change of variable, we have

Then, the marginal of is

The normalizing constant is the mixture of normals with scale . That is,

which is the expression of the proposition.

Appendix S2 Normalizing constant for

Throughout our research, the inequality is assumed to represent our prior belief on the structure of sparseness in the dynamic coefficients. However, the same argument can be applied to the other cases: and . Here, we provide the functional form of normalizing constant when , which is used in drawing the density function of the DFL prior in Figure 1 in the main text.

Proposition S2.1

If , the normalizing function of the DFL prior is

Proof. The same scale mixture representation of Proposition 2.1 applies to this one. When , the marginal of is obtained by

Then, we have

where we read-off the density kernel of in the integral in the second line, and is the modified Bessel function of the second kind with order . The expression of can be found, for example, Abramowitz and Stegun (1964), Section 10.2.17.

Appendix S3 Proof of Proposition 2.3

Propositions 2.1 and 2.2 prove the geometric series representation of the transition density as

where is the discrete mixture given in Proposition 2.2 with the running index of the series denoted by . By interpreting as the latent variable in the mixture representation, the transition density is understood as the marginal of . As the marginal distribution of , we have with probability , and with probability . Jointly, for ,

and, for ,

For notational convenience, we define by

In the joint density of state and auxiliary variable , observe that appears both in the numerator and denominator for and cancels out one another as

where we write to mean that the product is taken only for that satisfies . Using the scale mixture representation of double exponential distributions, we can read off the conditional distribution in the joint density above, as

where for all , and is the set of all the latent variables up to time , i.e., . The densities in the first parenthesis imply the linear and Gaussian likelihood, and those in the second parenthesis are the Gaussian AR(1) prior. This is exactly a dynamic linear model conditional on all the latent variables, the joint density of which is given by

As a whole, this is exactly the CDLM of the proposition.

Appendix S4 Subjective elicitation of weight parameters

In this subsection, the conditional expectation and prior density of , where and , are investigated for the better understanding of weight parameters . The details of derivation are given in the next subsection.

Recall the expression of the conditional density given in Equation (4) in the main text, which is the location-scale mixture of the Gaussian AR(1) process,

| (S1) |

where the mixing distribution is

| (S2) |

which is obtained by change of variables with and . The conditional expectation is one of the useful information that statisticians can interpret as “conditional shrinkage effect” and elicit their prior belief based on this quantity. The distribution itself is analytically available as well and provides further information on one’s prior belief.

Proposition S4.1

For DFL prior with , the conditional transition density in equation (S1) has the mean , where

| (S3) |

Proposition S4.2

The joint distribution in equation (S2) is decomposed into the compositional form. The conditional distribution of is and the marginal density of is

| (S4) |

See the Section S5 and S6 for the computation of equations (S3) and (S4), respectively. Here, we focus on the implication of this form on the prior specification.

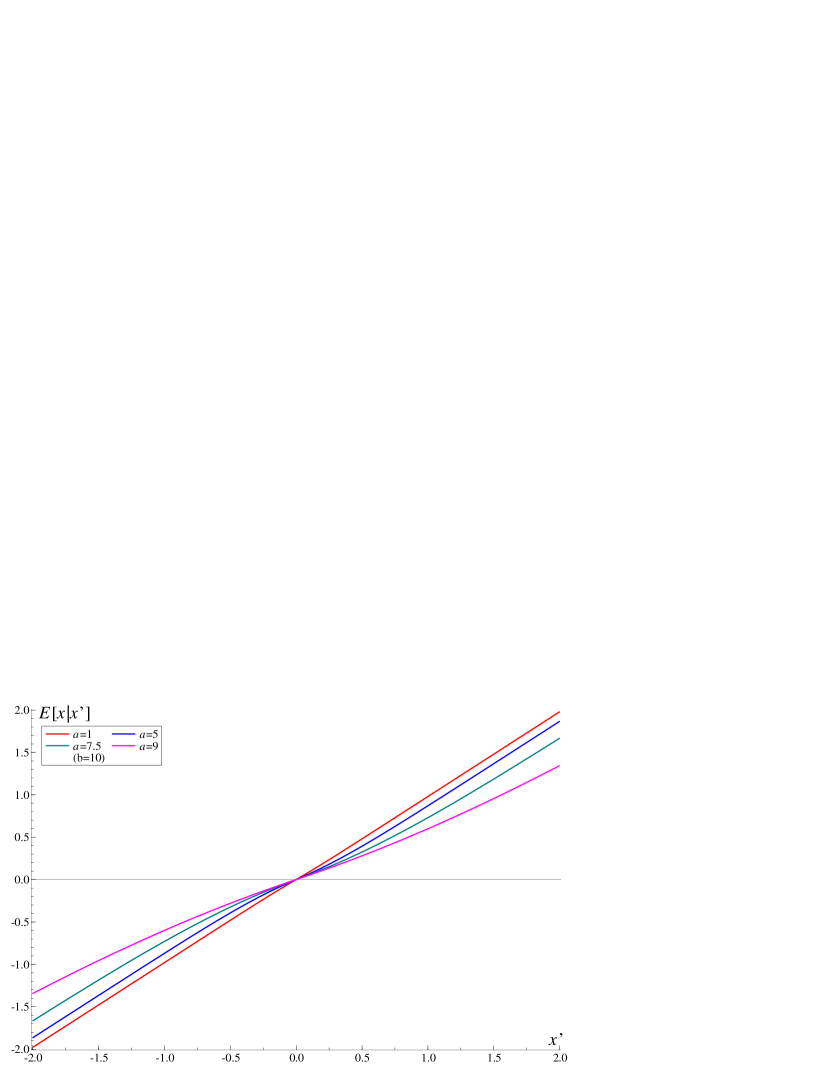

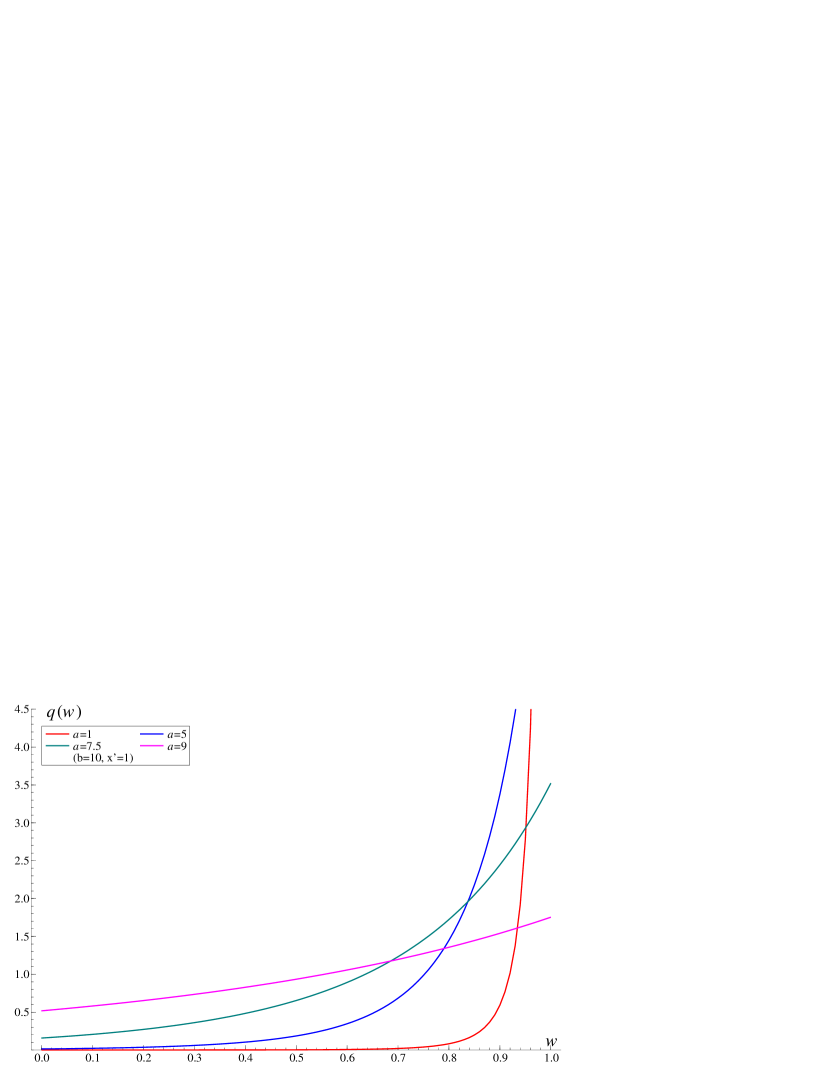

The conditional mean in equation (S1) is plotted against in Figure 1(a). When is small, the conditional means are almost on the diagonal line, showing more shrinkage effect to as in the random walk models. In contrast, for large , the shrinkage effect to zero becomes strong, making the conditional means off the diagonal line in the figure. The conditional mean is the non-linear function of as shown in equation (S3), and this non-linearity is also visually confirmed in the figure. Figure 1(b) depicts the density of shrinkage effect in equation (S4), conditional on , with marginalized out. For all the values of examined here, the prior mass concentrates around , implying the dominating conditional shrinkage effect is directed to , not to zero. For smaller , however, the more probability mass is placed on the smaller values of as well.

These two figures are just one aspect of the prior structure; for different choices of , the conditional prior mean and density look completely different, and it is difficult to summarize those differences in a simple manner. This might be the potential difficulty in subjectively specifying the prior, which motivates the estimation of hyperparameters. The automatic adjustment of hyperparameters via posterior analysis is discussed later in Section S7, but the choice of hyperparameters based on the discussion here still remains important.

Appendix S5 Computation for Proposition S4.1

In deriving the expectation , the other way of decomposition of the joint density of , i.e., , is useful. By reading off the conditional density of in equation (S2), observe that , whose normalizing constant is

Next, the marginal of is

This is the difference of two GIG densities, not the mixture, hence not suitable for the random number generation that we will discuss in the next Section. This form is rather useful in computing the moments.

Appendix S6 Simulation from the prior

Simulating the random variable from the conditional distribution is an important step at the one-step and multi-step ahead predictions. The location-scale mixture representation in equation (S1) enables the simulation from the normal distribution , given that is sampled from . Proposition S4.1 provides the compositional form of this joint density, in which is the generalized inverse Gaussian distribution and relatively easy to sample from.

The problem remains in the sampling of from marginal in equation (S4). We first verify this expression.

Proof of Proposition S4.2. The joint density of is

where we read off the conditional/marginal densities, or . In the former, given , we see . Marginalizing out, we have

which proves Proposition S4.2.

It is immediate from this expression that the density of is transformed into the relatively simple form by re-scaling.

Proposition S6.1

The marginal density of in the scale of is

| (S5) |

where . The distribution function is

| (S6) |

Proof. Apply the change of variable by to obtain equation (S5). To see equation (S6), compute the integral of (S5) based on the equality

that is obtained by integral by parts.

The explicit formula of distribution function helps computing the inverse distribution function numerically, thus allows the inverse sampling.

Sampling from .

-

1.

Sample .

-

2.

Given , set .

Recover by .

-

3.

Given , sample .

-

4.

Given , sample .

For the computation of the inverse of the distribution function , the simple Newton method can be applied and satisfactorily efficient. To compute for given , one must solve the equality

or, equivalently,

in . Further, by taking and , we have

The Newton method for solving this equation is defined by the update rule of the sequence as

until the increment is less than the tolerance level.

Appendix S7 Estimation of hyperparameters

S7.1 Likelihood and conjugate priors

To consider the hierarchical version of the DFL priors, where we assume the prior for weights and , we need to consider the “likelihood,” or the joint distribution of state variables as the function of . As stated in the main text, we re-parametrize the weights by with to guarantee the restriction . The joint density of state variables as the function of is

where, by writing , we take the product/summation of those that satisfies for . For this “likelihood,” the conditionally conjugate prior for is the gamma distribution. If , then the conditional posterior of is , where

The full conditional posterior density of is given by, with the prior density ,

In this research, we pursue the simplicity of computation by using the discrete prior on the interval . For some positive integer and (), the grid is defined by and the prior support of is . In practice, it is advised to avoid the value not too close to 1, e.g., , for the numerical issue. In our analysis, (), and follows the discrete uniform distribution on . The prior probabilities on those points are proportional to the beta density evaluated on the grids.

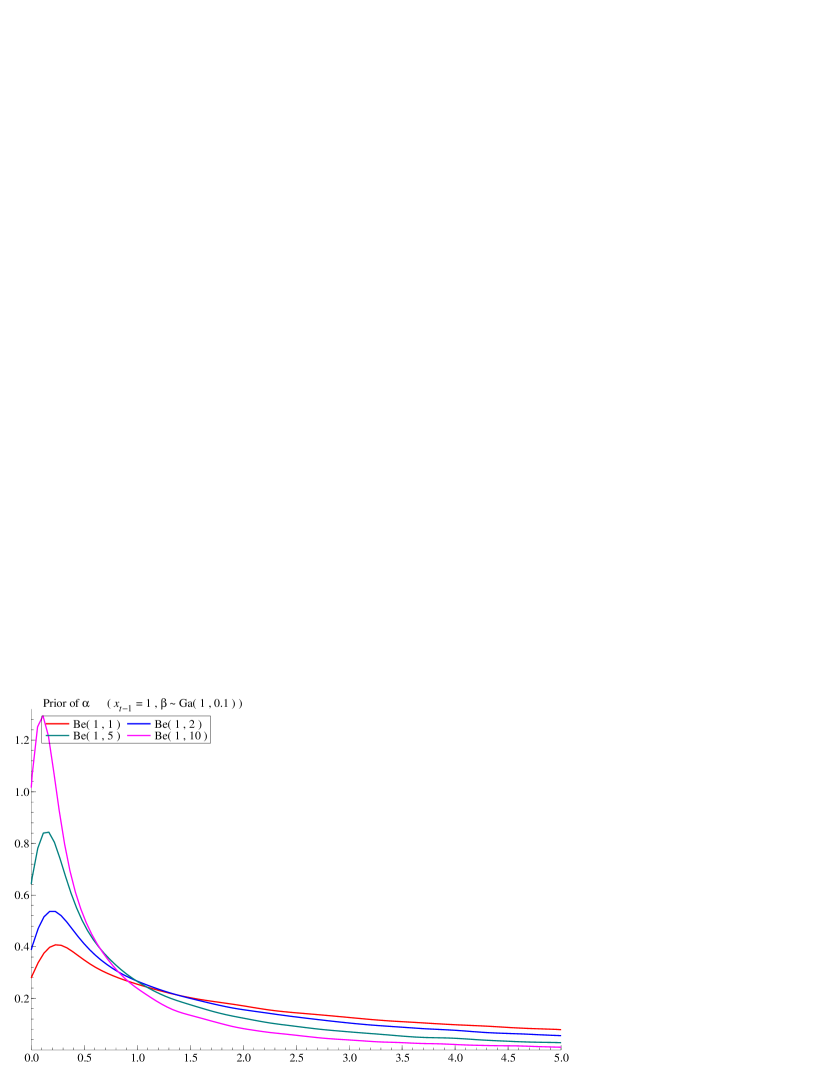

The careful, subjective choice of hyperparameters in the prior of is still unavoidable for the appropriate representation of one’s prior belief. To see this point, the marginal prior densities of and are drawn in Figure 2(a) and 2(b), respectively, for different choices of hyperparameters , while the other parameters are fixed as , and . As clearly seen in the prior of in Figure 2(a), the larger is, the less weight is placed on the shrinkage effect toward zero. The difference of those hyperparameters is emphasized in the density of – the conditional shrinkage effect to defined in the location-scale mixture representation in (S1). In Figure 2(b), the density with shows the heavier tail in smaller values of , implying the excess shrinkage effect to zero, even though the strong signal is assumed by . From this viewpoint, although this choice means follows the uniform distribution and is seemingly “less informative” prior, it is in fact regarded an extreme choice for its strong shrinkage effect applied to even large value of .

S7.2 Marginal distribution implied by hyperprior

The implied marginal distribution of state variable under the DFL prior with the conjugate prior on is illustrated in the top panel of Figure 3 in the main text by simulation. Here, we confirm the property of the marginal density analytically by studying the simpler model with . That is, consider and . Then, the marginal of is

In this form of the density function, we observe the heavier tails of the polynomial order that accommodate the sudden change of state variables. On the other hand, the density evaluated at is finite, which contrasts the density of the horseshoe prior whose density is divergent at the origin. Figure S3 shows the two examples of the marginal densities of . The hyperprior can realize the heavier tails than those of the horseshoe priors, but little change can be seen in the behavior around the original from that of the double-exponential distribution. From this figure, in addition to the observation in Figure 3 in the main text, the hierarchical DFL prior is expected to react to the dynamics of state variables and shift the posterior locations accordingly, but lacks the strong shrinkage effect toward the previous state.

S7.3 Prior of half-Cauchy type

As verified in the next section, the DFL prior can yield the horseshoe distribution as the marginal distribution of state variable if the hyperprior of is modified as

The conditional posteriors of is, after the reparametrization by , the extended gamma distribution, whose density is given by

where and

The acceptance-rejection algorithm for sampling from the general class of extended gamma distributions has been discussed in the literature (Finegold and Drton, 2011; Liu et al., 2012). We utilize the fact that the “rate” parameter is always positive in our model to devise the sampling algorithm based on Algorithm 3 in Liu et al. (2012).

Sampling from the extended gamma distribution with positive parameter and .

-

1.

Generate , where .

-

2.

Accept with probability . Otherwise, reject and return to Step 1.

The full conditional of is

which is the special case of Kummer-beta distributions. Despite the amount of works on this class of distributions (e.g., Gordy 1998), the methodology for random number generation has not been fully developed. For this problem, as discussed in the main text, we simply replace the beta prior of by the discrete distribution on grids for and . The probability on each grid is proportional to the original beta density, i.e.,

for . The posterior of is the discrete distribution defined by

S7.4 Estimation of baselines

The baseline is the location parameter of the synthetic likelihoods and the prior of initial state . The normal prior for is conditionally conjugate; for , the conditional posterior of is , where

Shrinkage on this baseline can be introduced by another hierarchical prior on .

Appendix S8 Hierarchical LASSO and its marginal

Consider the univariate following the scale mixture of normals, i.e., . If , then . In this subsection, we prove the hierarchical double-exponential distribution can be expressed as the three-parameter-beta distribution,

where and are all positive, in addition that we assume . The special case of is the half-Cauchy prior that induces the horseshoe distribution as the marginal of . In our research, we also assume .

Proposition S8.1

The three-parameter-beta distribution is expressed as the marginal of the following hierarchical model:

Importantly, the conditional distribution of is the exponential distribution which implies the double-exponential marginal as . This means that the introduction of the appropriate prior distribution on weight leads to the strong shrinkage and robustness of the horseshoe-type.

Proof. For any positive and , we have

as the integral of density function of . By applying this augmentation to the three-parameter-beta distribution, we obtain

The integrand is further computed as

Plug-in the obtained expression in the integral and observe that the desired mixture representation is obtained.

The special case of half-Cauchy distribution, where and , is stated as the following corollary.

Corollary S8.1

The half-Cauchy distribution, , is expressed as the marginal of the following hierarchical model:

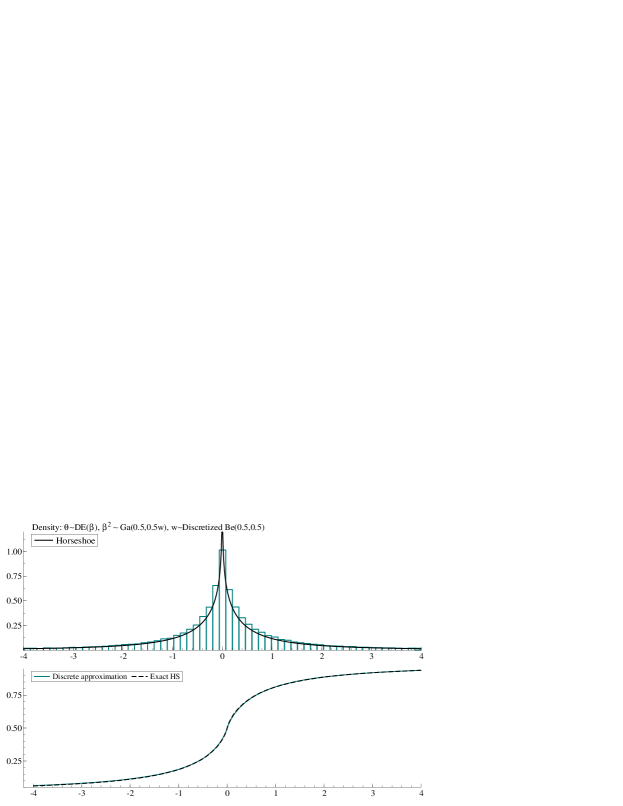

In the main text, for the convenience in posterior computation, the beta distribution of is replaced by the discrete distribution on the girds of with probability proportional to the density of the beta distribution. This modification potentially affects the marginal distribution of , which might deviate from the original half-Cauchy distribution. We examine this potential discrepancy by generating the random variables from the hierarchical model in Corollary S8.1 with the discrete distribution on in Figure S4. Both in the density form and empirical distribution function, the difference from the target horseshoe distribution is negligible.

Appendix S9 Modeling of observational variance

S9.1 Constant variance for scale-free DLMs

The scale-free DLM with the DFL prior has the CDLM form as follows;

| (S7) |

where for all and . The MCMC algorithm is modified by replacing the sampling of state variables as follows;

Gibbs sampler for scale-free models: replace Step 1 of the algorithm in Section 4 by the following.

-

1.

Sampling and .

-

(i)

Forward filtering.

For the DLM in equation (S7), implement the forward filtering to compute the one-step ahead predictive density for , where is the collection of observed ( if ). Specifically, compute the one-step ahead predictive mean and variance, and , defined by

-

(ii)

Sampling of .

Generate from its posterior , where the sufficient statistics can be computed by

-

(iii)

Sampling of .

Given , implement the forward filtering and backward sampling for the model in equation (S7) to generate .

The sampling of the other parameters remain the same for the scaled state variable .

S9.2 Stochastic volatility of log-Gaussian type

In the macroeconomic application in Section 5.2, we consider the model in Nakajima and West (2013a) where the observational variance, or stochastic volatility, is the time-varying parameter. The log-volatility, is modeled by the Gaussian AR(1) process,

with parameters to be estimated with the specific priors Jacquier et al. (1994). The priors for the set of ’s in the time-varying VAR models are taken from Nakajima and West (2013a). Likewise, the posterior sampling of is based on the multi-move sampler (Shephard and Pitt 1997; Watanabe and Omori 2004). While the efficiency of this sampling procedure is sufficient for our purpose as reported in Nakajima and West (2013a), there has been many methodological updates on the posterior computation of the stochastic volatility models; readers who seek for the better practice should refer to, for example, Kastner and Frühwirth-Schnatter (2014).

Appendix S10 Supplemental results for the simulation study

S10.1 Posterior udpate of latent count

It is of interest here how much one can learn about the latent count, , from data. We evaluate the change from prior to posterior of in the simulation study.

The prior of is given in Proposition 2.3 and 2.3 as the mixture of the point mass on zero and the log-geometric distribution. The prior probability of having is

where and . By parameterizing with , we have and . The prior probability of positive is

In practice, we also place priors on and . The prior on is the discrete distribution, so it is easy to integrate out in the above expression. To compute the expectation with respective to , we simply use the Monte Carlo integration.

The prior mean of is,

where the conditional expectation in the right is the mean of log-geometric distribution with parameter . It is shown that

Hence, in terms of and , the target expectation is computed as

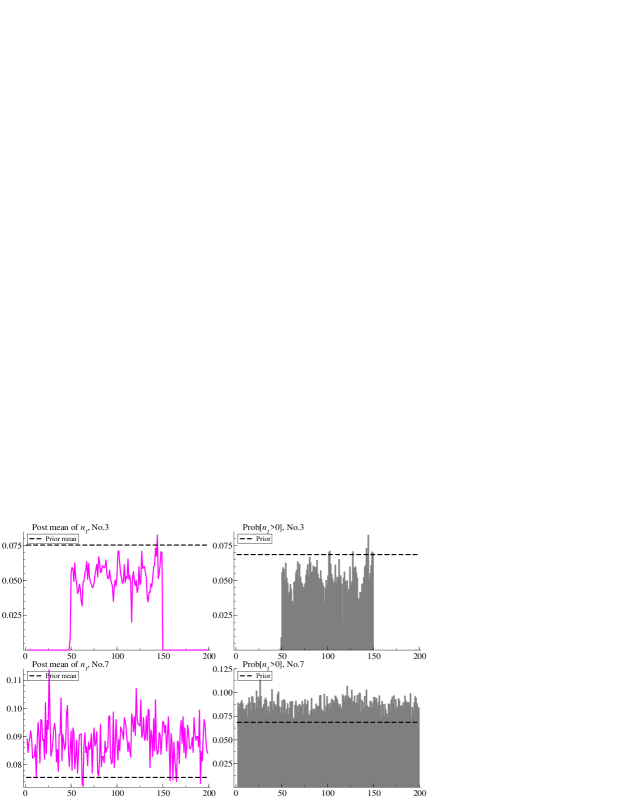

Figure S5 shows the prior and posterior mean and probability of positive for (dynamically significant predictor) and (noise predictor) under the model . The posterior probability of here is identical to the one shown in Figure 5 of the main text. For the active predictor , the probability of positive is lowered from that of the prior. This change in posterior distribution is local; the probability of positive is not completely zero when the coefficient is non-zero. For noise predictor , the posterior probability of positive and the posterior mean of are slightly larger than those of the prior, reflecting the belief on the “insignificance” of the predictor enhanced by the observed data.

S10.2 Posterior plots for baselines