Nonparametric Heterogeneous Treatment Effect Estimation in Repeated Cross Sectional Designs

Xinkun Nie

xinkun@stanford.eduChen Lu

chenl819@mit.eduStefan Wager

swager@stanford.edu

(Draft version March 2024 )

Abstract

Identifying heterogeneity in a population’s response to a health or policy intervention is crucial for evaluating and informing policy decisions. We propose a novel heterogeneous treatment effect estimator in the difference-in-differences design with repeated cross sectional data, where we observe different samples of a population at two time periods separated by the onset of a policy intervention, as well as samples of a population that serves as the control. Our estimator has orthogonality properties that enable fast rates on learning the treatment effect while allowing slower rates for estimating nuisance components. Our proposal shows promising empirical performance across a variety of simulation setups.

1 Introduction

Difference-in-differences is an increasingly popular observational study design for estimating causal effects from repeated

cross sections (e.g., Angrist and Pischke, 2008; Bertrand et al., 2004; Card and Krueger, 1994; Lechner, 2011; Obenauer and von der Nienburg, 1915). For an overview of applying difference-in-differences method in public health, see Dimick and Ryan (2014), Gertler et al. (2011) and Wing et al. (2018) for a review. Recently, several authors have employed it to study public health policy and implications due to COVID-19 (Brodeur et al., 2021; Goodman-Bacon and Marcus, 2020).

A standard design with cross sectional data is as follows: we conduct a survey or draw a sample for some outcome (e.g., medical expediture) from two comparable states

(or cities, regions, etc.). The first state later enacts some health policy of interest (e.g., encouragement of Medicare enrollment) and the second state doesn’t. We then draw another sample from both states at a time after the health policy has been implemented in the first state. The simplest difference-in-differences estimator assumes global parallel trends: if neither state had enacted the policy, then their trends would have evolved in the same way. It would then attribute any difference in trends between the two states to the effect of the policy change.

In this paper, we focus on flexibly estimating treatment effect heterogeneity in the above design. There are two main challenges. The first challenge involves representing and targeting heterogeneity effectively without assuming specific functional forms. The second challenge involves relaxing the classic assumption of “global parallel trends,” which is unlikely to hold when there is heterogeneity explained by covariates. In particular, states may have changing subgroups of people that exhibit markedly different trends on their own. For example, when studying the effect of enrollment in Medicare on

medical expenditure, we may find that there are subgroups within states (e.g., based on age, income or gender) that have different

baseline trends; then, if the two states under comparison have different proportions of these subgroups, the global parallel trends

assumption immediately becomes questionable. Instead, we may want to control for these covariates, and only assume parallel

trends once we have conditioned on them

(e.g., Abadie, 2005; Acemoglu and Angrist, 2001; Blundell et al., 2004; Heckman et al., 1998).

Throughout the paper, we work in the following formal setup. We observe independent samples

, where the state indicator denotes whether the -th individual is in the control or exposed state,

denotes the time of the observation (pre- vs. post-intervention), is a set of potential confounders

and is the outcome of interest. Only samples in the “exposed” state and “post” time period

get treated, i.e., we can write the treatment or exposure indicator as . Following the potential outcomes framework (Imbens and Rubin, 2015), let

and denote the control and treated potential outcomes and suppose we observe .

We are interested in estimating the heterogeneous treatment effect , defined as the expected treatment effect

conditional on covariates and on treated:

(1)

Because is not observed, we impose a parallel trends assumption conditional on covariates, so that

(2)

which then allows us to identify the conditional average treatment effect on the treated as follows,

(3)

As discussed in Abadie (2005), (2) may be more credible

than the standard parallel trends assumption that holds without conditioning on as it enables

us to control for known sources of confounding.

A classical approach to estimating would be to employ flexible nonparametric modeling of the treatment effect function. A common practice is to employ a two-way fixed effect linear model with interactions for in terms of of the form

(4)

then

interpreting as the treatment effect (e.g., Anzia and Berry, 2011).

However, the estimator (4) is not

justified by a nonparametric version of the assumption (2) due to the assumed linear functional forms on and on any confounding effects of

that affect the outcome (Angrist and Pischke, 2008; Ding and Li, 2019; Keele and Minozzi, 2013; Lechner, 2011). These constraining assumptions can be difficult to satisfy in practice.

In this paper, we aim to flexibly estimate the treatment effect function given only the assumption (2)

along with a relevant form of overlap. As a direct consequence of (2), the data generating process can be written as the following generic

specification:

(5)

where the joint distribution of may be arbitrary and

(6)

are the conditional effect of alone and alone, and . We note that all the conditional effect function can be nonparametric funcitons.

One naive way to estimate in this model is as follows. Recall our expression for in (2). From that expression, one might attempt to estimate

(7)

for the four pairs of and on the corresponding subsets of the data, and then estimate . However, this approach is often not robust. As an example where this method might fail, consider a high dimensional linear model, , with , and . We might consider fitting the Lasso (Tibshirani, 1996) for each separately, and estimate . However, the lasso regularizes each towards separately, which might result in being regularized away from , even when everywhere. See Künzel et al. (2019) and Nie and Wager (2021) for a similar discussion on the -Learner for the CATE.

We seek to build a robust estimator for . To this end, we start by considering the case where the underlying treatment effect is constant and the only challenge is to eliminate confounding. We start by developing an orthogonal transformation of (5)

that generalizes the transformation of Robinson (1988) for the conditionally linear model.

This representation allows us to build

a transformed regression estimator (TR) to estimate the constant treatment effect. Our TR estimator achieves the parametric

rate of convergence while allowing for slower estimation rates on all nuisance components. The rate of convergence in the TR estimator allows valid asymptotic confidence interval construction, while we still enable flexible nonparametric estimation on the nuisance components (e.g., without linearity assumptions). We further discuss the properties of the transformed regression estimator when the underlying linearity assumption is misspecified. We then build upon the transformed regression construction and propose a heterogeneous treatment effect estimator for and show empirically the proposal is advantageous comparing to exisitng baselines.

Compared to the standard difference-in-differences design, we do not assume the panel setting where every individual is observed both before and after the treatment. In that particular case, one could apply any of the existing heterogeneous treatment effect estimators (e.g., Athey et al., 2019; Hill, 2011; Künzel et al., 2019; Nie and Wager, 2021) by taking the difference between the outcomes from the two time periods as the new outcome variable. In our setting, we make the less stringent assumption of conditional parallel trends, and allow covariate shifts for the two time periods which makes the setting significantly more challenging. Adapting advances in semiparametric efficiency theory and leveraging flexible nonparametric machine learning methods for this task is our main methodological contribution.

2 Related Work

The difference-in-differences approach to treatment effect estimation was popularized by

Card and Krueger (1994), and has since become ubiquitous in the social sciences.

Angrist and Pischke (2008) and Lechner (2011) provide a textbook treatment

and a broad literature review. Building on Abadie (2005), we are here most interested

in extensions of classical difference-in-differences methods that leverage covariate information

to make the parallel trends assumption more plausible. Several authors have also recently

extended difference-in-differences analyses in other complementary directions.

Arkhangelsky (2018) and Athey and Imbens (2006) consider difference-in-differences

type designs where there may be non-additive treatment effects. Abadie et al. (2010), Arkhangelsky et al. (2018),

Athey et al. (2018), Ben-Michael et al. (2018), Xu (2017) and Li and Li (2019) develop methods that

can be applied in the panel setting in which the same individuals are observed in both the pre- and post-periods, whereas in our setting we observe separate cross-sectional data in each period.

Most of the existing literature with repeated cross sections, including Abadie (2005), Li and Li (2019), Sant’Anna and Zhao (2018), Chang (2020), assume that there is no covariate shift across cross-sections from the same

state: they require that the joint distribution of does not vary with , i.e., that .

Our approach does not require this assumption (see Proposition 1 and the following comment), as this assumption may be hard to justify with cross-sectional data where we are not able to survey exactly the same people in the pre- and post- periods.

For example, in a ride-sharing application, Lu et al. (2018) estimates the effects of a dynamic pricing feature on drivers’ behaviors

by leveraging a natural experiment where a software bug temporarily disables a dynamic pricing feature for certain drivers.

In this case, we may expect the distribution of the covariates for active drivers varies both with exposure and time .

Methodologically, we build on a large body of work in nonparametric estimation of heterogeneous treatment effects well. One approach is to reduce the “regularization bias” that might occur. Examples of this line of work include Athey and Imbens (2016), Hahn et al. (2017), and Shalit et al. (2016). Another approach, the one we choose to adopt, is to develop meta-learning procedures that do not depend on a specific machine learning method. Key examples of such works are Künzel et al. (2019) and Nie and Wager (2021). Our decomposition of is conceptually similar to the orthogonal moments constructions from Robinson (1988), and more broadly, from Belloni et al. (2011), Bickel et al. (1998), Newey (1994), Scharfstein et al. (1999), Van Der Laan and Rubin (2006) and others.

In the difference-in-differences design, flexible modeling and estimation that goes beyond the standard two-way fixed effects and linearity assumptions has also drawn considerable interest. Abadie (2005) considers inverse propensity stratification based methods. Another approach considers more flexible outcome models, see (e.g., Heckman et al., 1998; Meyer, 1995). Recently, Chang (2020), Sant’Anna and Zhao (2018)

and Zimmert (2018) proposed doubly robust variants of the approach of Abadie (2005)

that also allow for heterogeneity in .

3 An Orthogonal Transformation for the Repeated Cross Sections

The key orthogonality property of our proposed heterogeneous treatment effect estimator relies on a new decomposition for the outcome model (2) motivated by Robinson (1988).

The conditional

probabilities of an observation being in state or time period conditionally on

play a central role in our analysis (Rosenbaum and Rubin, 1983). We write these quantities as

(8)

We write . We also write for the conditional response function

marginalizing over and , and

(9)

for the conditional effect of marginalizing over and respectively. We write the conditional covariance of and as

(10)

Finally, for convenience, we let . Given this notation, we can verify the following (the derivation is given in the Supplementary Materials).

Proposition 1.

Suppose we have access to an independent and identically distributed sequence of tuples

and . Under the model (2), our data-generating distribution admits a representation

(11)

where , and

(12)

Furthermore, all terms in the above decomposition are orthogonal in the following sense:

(13)

The key property of this representation is the orthogonality property (13),

which will enable flexible estimation of treatment effects at parametric rates as discussed in the following section.

In the setting of Abadie (2005) and Sant’Anna and Zhao (2018), their assumption gives , which implies . As an immediate corollary to Proposition 1, this decomposition then simplifies to a functional

form closely reminiscent of Robinson’s transformation (Robinson, 1988):

(14)

More generally, we see that when is close to 0, all expressions underlying (11)

and (12) are well-conditioned, and we expect estimation using (11) to be stable.

Conversely, if and are highly correlated conditionally on , then

and (12) could become unstable;

this is as expected, because if and are highly correlated, then we do not expect their

interaction effect to be well identified.

Finally, we note that all nuisance components in the decomposition above are marginal quantities,

and thus can be estimated using all of the data. This property is desirable for empirical performance as it is

more data efficient when we need to estimate them in a small-sample regime.

4 The Transformed Regression Estimator

As a building block of our proposed heterogeneity treatment effect estimator, we first consider estimation in a setting where

the treatment effect itself is constant in the representation (11), but all other

nuisance components defined above, i.e., , , , , and ,

may vary with . The standard approach to estimating in this setting is to write a two-way fixed effect model of the form

(15)

and to interpret the coefficient on as an estimate of the treatment effect. However, as shown in our experiments,

this simple linear regression-based approach to treatment effect estimation may be severely biased in the setting where

the linear model (15) is misspecified.

Here, we propose the transformed regression (TR) estimator with cross-fitting (shown in Algorithm 1). The method is based on the decomposition (11), which is motivated by a decomposition used by Robinson (1988) to estimate parametric components in partial linear models. Robinson’s decomposition has also been used in many other recent works, such as in Athey et al. (2019) for causal forests, Robins (2004) for G-estimation, as well as in Chernozhukov et al. (2018a) and Zhao et al. (2017). The transformed regression estimator, motivated by Robinson, also has good theoretical properties. In Theorem 2, we show that the transformed regression estimator is -consistent and asymptotically normal under considerably more generality than simply running an OLS regression with the model (15). We note that cross-fitting helps avoid overfitting of the estimates and also serves as a proof technique to show -consistency on .

Having consistency on enables us to build valid asymptotic confidence intervals for , while we still allow nonparametric estimation on the nuisance components without imposing linearity assumptions such as in (15).

The proof of the theorem is in the Supplementary Materials.

1

Split the data into roughly equal folds, , , …, , with fixed, to be used for cross-fitting.

2For each fold , fit and , with data not in , using any supervised learning method for prediction accuracy (the superscript of denotes using data not in the -th fold).

3Estimate as a heterogeneous “treatment effect” of while ignoring ; and estimate as a “treatment effect” of ignoring . Both can leverage methods designed for heterogeneous treatment estimation in the single cross-section case.

4Construct , , and , where , using the estimated nuisance parameters following (12). Then, for , obtain point estimates and

(16)

5Run OLS on against to produce

(17)

Combine predictions from different folds :

(18)

Algorithm 1Transformed Regression Estimator (TR)

Theorem 2.

Under the conditions of Proposition 1, suppose furthermore that is

constant and that the following conditions hold:

1.

Overlap: the conditional probabilities are bounded away from

by some small for all values of , and .

2.

Consistency: for any estimated nuisance parameter , such as , and , we have that:

3.

Risk decay: for any estimated nuisance parameter , we have:

4.

Boundedness: all the nuisance parameters are uniformly bounded:

for some constant .

Then, writing as the transformed regression estimater obtained using Algorithm 1, and as the transformed regression estimator with oracle nuisance parameters, we have

where

(19)

and .

In the case when , and is constant, the expression for simplifies to

.

In step 3 of Algorithm 1, and can be estimated with methods for heterogeneous treatment effect estimation. In our simulations, we use causal forests (Athey et al., 2019), but we note that other estimators in the literature can also be used here

(e.g., Athey et al., 2019; Hill, 2011; Künzel et al., 2019; Nie and Wager, 2021).

If we ever want to use the transformed regression estimator which assumes a constant treatment effect, it is important to understand how it

behaves under misspecification. Interestingly, as shown in Proposition 3, even when is not constant, the transformed regression estimator converges to a weighted average of with positive weights, mirroring the findings in Crump et al. (2009)

and Li et al. (2018). The proof for Proposition 3 is found in the Supplementary Materials.

Proposition 3.

If we use the transformed regression estimator from Algorithm 1, and the conditions from Theorem 2 are satisfied, then

We also note that when in the setting of Abadie (2005),

where and so , the above simplifies to:

When is not constant, the transformed regression estimator can thus be thought of as a weighted mean of the treatment effect, where more weight is given to the data points that are likely to appear with all four pairs.

5 Estimating Treatment Heterogeneity with Repeated Cross Sectional Data

In this section, we relax the assumption from the previous section that the underlying treatment effect is constant, and aim to estimate the heterogeneous treatment effect. We propose a flexible nonparametric estimator in the difference-in-differences setup that draws inspiration from recent advances in heterogeneous treatment effect estimation in the single cross-section case.

We adapt our estimator of a constant causal parameter

into an estimator for a heterogeneous treatment function , by turning the estimation equation underlying

the former estimator into a loss function. The R-learner (Nie and Wager, 2021) follows this strategy to derive a heterogeneous treatment effect estimator from Robinson’s decomposition (Robinson, 1988) in the setting of a single cross section. We follow the same strategy here with repeated cross sectional data. Using the decomposition from

(11), we can estimate treatment effect heterogeneity with the following algorithm R-DiD:

1

Split the data into roughly-equal folds , …, for cross-fitting.

2Following steps 2 to 4 of Algorithm 1, estimate the nuisance parameters , , , , , using data not in the -th fold. Also following step 4 of Algorithm 1, produce point estimates and according to (16) for .

Estimate the cross-fitted heterogeneous treatment effect for data in as

(21)

where is some regularization term. For , use as the estimate for .

Algorithm 2Heterogeneous Treatment Effect Estimation with Cross Sectional Data (R-DiD)

Recall from the last section that when the treatment effect is contant, the transformed regression estimator achieves rate for estimating the treatment effect parameter . When is a nonparametric function, we can no longer achieve parametric rates. Instead, we aim to show a quasi-oracle result, i.e., even if estimating the nuisance components , , , , and have a slow convergence rate, we can still achieve fast nonparametric rates on the treatment effect function as if we had known these nuisnace components perfectly. See Chernozhukov et al. (2018b); Luedtke and van der Laan (2016); van der Laan and Dudoit (2003) for similar developments. In this work, we leverage the recent result from Foster and Syrgkanis (2019) that generalizes the quasi-oracle bounds in Nie and Wager (2021).

In particular, for any treatment effect function and nuisance function where the nuisance function includes , , , , and , define the loss function

(22)

Suppose in Algorithm 2, instead of leveraging cross-fitting to learn nuisance components, we use sample splitting, i.e. we split the data in half, and use the first half to learn all the nuisance components , and use the second half to estimate . The following then holds as a direct consequence of Theorem 1 in Foster and Syrgkanis (2019),

Theorem 4.

Suppose the conditional probabilities are bounded away from 0 by some constant for all values of and , and the outcome is bounded by . Suppose further that in Algorithm 2, and let be the treatment effect estimate on the first fold. Suppose there exist rate functions such that

(23)

and

(24)

then

(25)

for all nuisance parameter including , , , , and .

The theorem above shows that the required learning rate on the nuisance components is only at a 4th-order growth rate compared to the learning rate on the target parameter . Note that if the nuisance components were known, (24) would be in terms of . We refer readers to Section 4 in Foster and Syrgkanis (2019) to see that in the case of empirical risk minimization, the cost to relate these quantities gets absorbed, and the same conclusion holds. The proof of the theorem relies on the orthogonality results from Proposition 1 and is included in the Supplementary Materials.

6 Simulation Study

In this section, we test the validity of our methods in a variety of simulation setups where the true underlying treatment effect can be both constant and non-constant. In the simulations, we generate i.i.d. samples of dimension from some underlyng distribution ; the pre/post-treatment time indicator and the state indicator are generated with a multinomial distribution over the four pairs . The outcomes are generated from (5) with .

Next, we present results in the case where the underlying treatment effect is constant as well in the case where it is heterogeneous.

We compare five methods in estimating heterogeneous treatment effects, four of which serve as baselines. OLS is as shown in (4). The T-Learner runs a separate regression for each of the four conditional quantities in (2) with a regression forest, and follows (2) to build the estimate from the four separate regressions. The CF-time learner runs a causal forest to learn the time-wise treatment effect in the treated location, i.e.

and then runs another causal forest to learn the time-wise treatment effect in the control location, i.e.

and subtracts the two estimates. On the other hand, The CF-state learner runs a causal forest to learn the state-wise treatment effect in the treated time period, i.e.

and then runs another causal forest to learn the time-wise treatment effect in the control period, i.e.

and subtracts the two estimates.

We compare the above four baselines with the R-DiD estimator outlined in Algorithm 2. In particular, we note that causal forests (Athey et al., 2019) can be understood as an instantiation of the R-learner with random forests, and can be used in Step 3 of Algorithm 2.111For more discussions on the connection between the causal forests and the R-learner, see Section 1.3 in (Athey and Wager, 2019).

All regressions in all of the methods under comparison are implemented with regression forests from the package grf (Athey et al., 2019). In Algorithm 2, we take as the “outcome” and as the “treatment” in a causal forest. Along with CF-time and CF-state, they are all implemented with the package grf.

We consider the following four setups:

Setup A ; easy treatment effect ; easy conditional effects , ; easy baseline ; constant propensity for : , but constant propensity for , , and is independent from .

Setup B ; easy treatment effect ; challenging conditional effects and . There is no baseline effect, i.e. ; propensities are constant , with and independent.

Setup C ; there exists no time or state effect: , but highly correlated baseline effect and propensities, where , and , for ; .

Setup D ; easy non-constant treatment effect ; easy conditional effects , ; easy baseline ; non-constant propensity for : , and non-constant propensity for , , and is independent from . This is a well-specified setup for OLS.

setup

n

p

R-DiD

CF-time

CF-state

T

OLS

A

1000

6

1.01

3.83

3.29

7.8

15.05

A

1000

12

1.11

4.7

3.56

8.64

23.85

A

2000

6

0.61

2.53

1.93

5.09

7.75

A

2000

12

0.67

2.7

2.02

5.63

11.61

B

1000

6

2.69

14.1

15.18

40.8

38.66

B

1000

12

2.78

15.25

19.55

49.38

64.63

B

2000

6

2.07

8.8

8.71

32.56

18.19

B

2000

12

1.66

10.22

9.73

37.25

28.92

C

1000

6

0.03

0.04

0.04

0.27

0.55

C

1000

12

0.02

0.03

0.04

0.29

0.78

C

2000

6

0.02

0.02

0.02

0.22

0.36

C

2000

12

0.02

0.02

0.02

0.21

0.46

D

1000

6

1.92

1.64

2.73

2.34

0.18

D

1000

12

2.37

1.97

3.11

2.78

0.32

D

2000

6

1.17

1.01

1.94

1.65

0.09

D

2000

12

1.34

1.45

1.35

1.34

1.4

Table 1: Simulation results on mean squared error on an independent test set comparing our proposal R-DiD against four other baselines in different simulation setups, with varying training sample size and dimensions . Results are averaged across 200 independent runs.

The results of the simulations are shown in Table 1. For each of the values, we draw training data points, and another separate testing data points. We report results on this indepedent testing set. We run the experiments 200 times, and the mean squared error of each algorithm is shown below. Our proposal R-DiD performs well, while in simulation setup D, we see that OLS performs particularly well given it’s a well-specified setup. However, in practice it is less conceivable to have a well-specified setup, and our algorithm shines due to its flexibility to model nonparametrically and robustness towards estimation errors in nuisance components.

7 Application

To test our methods in practice, we revisit a study from Angrist and Kugler (2008) on the effect of import restrictions on self-employment incomes. The context is as follows: Columbia was one of the major suppliers of cocaine to North America and Europe before the s. Before , Columbia relied on coca leaf supplies from Bolivia and Peru, which it then refined to produce cocaine. Starting from , a series interdictions made by the United States and local militaries disrupted the air-bridge that brought the coca leaves to Columbian refiners. As a result, coca cultivation shifted to Columbia’s rural areas. The study from Angrist and Kugler (2008) then examines, among other things, the effect of the restriction of coca import on self-employment incomes in Columbia. The authors define self-employment income as income from individual short-term contract, from the sale of domestically produced goods, and from agricultural productions. The authors conclude that the decrease in import has a positive effect on the self-employment incomes.

The dataset includes repeated cross-section survey data and contains the following information about individuals: gender, age, number of family members, immigrant status, marital status, and whether they lived in rural or urban areas, which we use as covariates . The individuals come from one of three coca-growing regions (Bolivar, Cauca and Narino), or one of thirteen non-growing regions (Atlantico, Sucre, Cordoba, Santander, Boyaca, Caldas, Risaralda, Quindio, Tolima, Huilda, Antioquia, Choco, Valle de Cauca); see map in Angrist and Kugler (2008) for details. The dataset also includes a number of demilitarized zones, which we omit in our

analysis.222It was suggested that being a demilitarized zone may have an effect on the incomes of people from that region. Moreover, the demilitarized zones were exclusively growing regions. If we were to include the indicator of whether an individual is from a demilitarized region as one of our covariates, all such individuals will be in the treated group, hence violating overlap. Individuals from growing regions are classified as exposed, with , and those in non-growing regions classified as non-exposed, with , because the increase in coca production could only benefit those in growing regions. As for time periods, we take as the pre-treatment period, with ; because air interdictions occured throughtout , we take as the post-treatment period, with . The outcomes are the log self-employment incomes, .

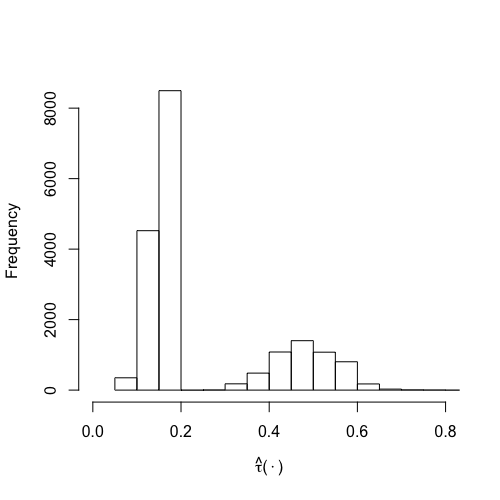

Figure 1: Histogram of fitted using Algorithm 2 on the dataset from Angrist and Kugler (2008). We see that there appears to be heterogeneity in the treatment: the treatment effects lie in two groups, one around and the other around . Our results in Table 3 suggest that these two groups are treatment effects for people living in urban and rural areas respectively.

We first fit the treatment effect function using the heterogeneous effect estimator R-DiD as in Algorithm 2. Figure 1 provides a histogram of the estimated treatment effects. We see that there appears to be heterogeneity in the treatment, as the histogram exhibits two distinct masses.

Beyond heterogeneity estimates, we compare a few different methods for the estimation of average treatment effects in this setup. In Appendix A, we describe the augmented inverse propensity estimator (AIPW) that builds upon the heterogeneous treatment effect estimates from Algorithm 2. An alternative approach is AMLE, which builds upon the Augmented Minimax Linear Estimation (AMLE) approach of Hirshberg and Wager (2021) by constructing balancing weights. See an earlier working paper (Lu et al., 2019) for details on this estimator and comparison with AIPW. We also compare our TR estimator that assumes constant treatment effects, as well as Sample Means by taking the empirical means of (3), and the standard OLS as in (15).333Note that OLS is the method used in Angrist and Kugler (2008), except we use the data in 1995 as the post-treatment period, but Angrist and Kugler (2008) use the data from 1995 up until 2000 as the post-treatment period and assumed a fixed effect for each of the year-treatment interaction. See Table 2 for result comparisons.

estimator

estimate

std. err

Sample Means

0.279

0.059

OLS

0.274

0.031

TR

0.275

0.031

AMLE

0.234

0.031

AIPW

0.258

0.031

Table 2: Average treatment effect estimates in the difference-in-differences setup with data from Angrist and Kugler (2008), where is the pre-treatment year and is the post-treatment year. The first three methods assume a constant treatment effect , and the latter two allow for treatment heterogeneity. The OLS method is most similar to the method used in Angrist and Kugler (2008). We see that AIPW and AMLE, which allow for heterogeneity in the treatment effects, both obtain a lower point estimate than the other methods, which all assume the underlying effect is constant. This may suggest that there exists heterogeneity in the treatment effects.

Table 2 shows the results for estimating average treatment effects. There exists a non-trivial difference between the estimated effect from methods that allow for heterogeneity in and those that do not, which suggests that there is a weighting effect going on when the likelihood of state and treatment time indicators vary with covariates. All the methods suggest that there is a positive effect of the air interdictions on the log self-employment income, as found in Angrist and Kugler (2008). Recall that, when the treatment effect is non-constant, TR obtains estimates of weighted average treatment effects, given by Proposition 3. Because TR is giving significantly different results from the non-constant effect methods, we suspect that in this dataset the treatment effect varies with covariates.

We also note that, in this case, the OLS estimator is fairly closely aligned with the TR estimator, suggesting that assuming linear nuisance

components did not have too big an effect on our estimation of . However, it may have been difficult to argue a-priori that

the linear specification used by OLS would be innocuous here.

As further evidence of treatment heterogeneity, Table 3 shows average

effects obtained by AMLE, separately for urban and rural regions. Thus, estimates provided by the transformed regression estimator should not necessarily be interpreted as average treatment effects, and may instead better be interpreted as targeting a weighted estimand following the discussion in Section 4.

estimand

estimate

std. err

ATE Urban

0.102

0.035

ATE Rural

0.582

0.057

Table 3: This table gives evidence that suggests the existence of heterogeneity in the treatment effect from the dataset of Angrist and Kugler (2008). The first row is obtained by running the AMLE method on only individuals who live in the urban area; the second row comes from running AMLE on individuals who live in the rural area. As shown, there seems to be a much larger treatment effect on individuals living in rural areas than on individuals in urban areas.

As a final sanity check, we also run a placebo analysis with years and as pre- and post- treatment period, and we use our methods to check if there was an effect in these years. It is encouraging that all the methods suggest there is a negligible effect on the treatment effect, as shown in Table 4.

estimator

estimate

std. err

Sample Means

-0.009

0.047

OLS

0.004

0.023

TR

0.012

0.023

AMLE

0.008

0.023

AIPW

0.007

0.023

Table 4: Treatment effect estimates with data from Angrist and Kugler (2008), where is the pretreatment year and is the post treatment year. All the methods suggest that there is negligible treatment effect.

Appendix

Appendix A Augmented IPW for cross-sectional data

Given our proposed heterogeneous treatment effect estimator, one direct way to construct an average treatment effect estimator is by building on results for doubly robust

estimation as developed in Chernozhukov et al. (2018c). In order to do so, we first note that

the average treatment parameter can be written as a weighted average of outcomes using

inverse-probability-style weights as follows: with

(26)

Recall . The result of Chernozhukov et al. (2018c) implies that if we obtain good estimates both of and the inverse-probability-style weights outlined above, then we can

obtain semiparametrically efficient estimates of using the doubly robust form such as in Augmented Inverse Propensity Weighitng (AIPW) (Robins and Rotnitzky, 1995). We will refer to this algorithm as AIPW, which takes on the following steps:

1.

Following the cross-fitting steps 2 to 4 of Algorithm 1, estimate the nuisance parameters , , , , , using data not in the , where , …, are the folds of the data. In the same way, fit nonparametric regressions for the propensities , , and .

2.

Run step 3 of Algorithm 2 to obtain cross-fitted point estimates , for each .

3.

For each , produce the cross-fitted point estimates:

(27)

and

(28)

4.

Estimate the average treatment effect as:

(29)

Abadie (2005) and Sant’Anna and Zhao (2018) explored a special case of this approach in cases where

are independent from . As a result, only the estimate of the single propensity is needed to perform a similar estimation, as opposed to the quantity .

While plug-in estimation with the doubly robust score admits for algorithmically simple estimation of the

average treatment effect, probabilities etc. may get quite small, and so inverting even slightly inaccurate propensity

estimates may result in instability.

References

Abadie [2005]

Alberto Abadie.

Semiparametric difference-in-differences estimators.

The Review of Economic Studies, 72(1):1–19, 2005.

Abadie et al. [2010]

Alberto Abadie, Alexis Diamond, and Jens Hainmueller.

Synthetic control methods for comparative case studies: Estimating

the effect of california’s tobacco control program.

Journal of the American Statistical Association, 105(490), 2010.

Acemoglu and Angrist [2001]

Daron Acemoglu and Joshua D Angrist.

Consequences of employment protection? the case of the Americans

with Disabilities Act.

Journal of Political Economy, 109(5):915–957, 2001.

Angrist and Kugler [2008]

Joshua D Angrist and Adriana D Kugler.

Rural windfall or a new resource curse? coca, income, and civil

conflict in colombia.

The Review of Economics and Statistics, 90(2):191–215, 2008.

Angrist and Pischke [2008]

Joshua D Angrist and Jörn-Steffen Pischke.

Mostly harmless econometrics: An empiricist’s companion.

Princeton university press, 2008.

Anzia and Berry [2011]

Sarah F Anzia and Christopher R Berry.

The Jackie (and Jill) Robinson effect: Why do congresswomen

outperform congressmen?

American Journal of Political Science, 55(3):478–493, 2011.

Arkhangelsky [2018]

Dmitry Arkhangelsky.

Dealing with a technological bias: The difference-in-difference

approach.

Technical report, CEMFI, 2018.

Arkhangelsky et al. [2018]

Dmitry Arkhangelsky, Susan Athey, David A Hirshberg, Guido W Imbens, and Stefan

Wager.

Synthetic difference in differences.

arXiv preprint arXiv:1812.09970, 2018.

Athey and Imbens [2016]

Susan Athey and Guido Imbens.

Recursive partitioning for heterogeneous causal effects.

Proceedings of the National Academy of Sciences, 113(27):7353–7360, 2016.

Athey and Imbens [2006]

Susan Athey and Guido W Imbens.

Identification and inference in nonlinear difference-in-differences

models.

Econometrica, 74(2):431–497, 2006.

Athey and Wager [2019]

Susan Athey and Stefan Wager.

Estimating treatment effects with causal forests: An application.

arXiv preprint arXiv:1902.07409, 2019.

Athey et al. [2018]

Susan Athey, Mohsen Bayati, Nikolay Doudchenko, Guido Imbens, and Khashayar

Khosravi.

Matrix completion methods for causal panel data models.

Technical report, National Bureau of Economic Research, 2018.

Athey et al. [2019]

Susan Athey, Julie Tibshirani, Stefan Wager, et al.

Generalized random forests.

The Annals of Statistics, 47(2):1148–1178, 2019.

Belloni et al. [2011]

Alexandre Belloni, Victor Chernozhukov, and Lie Wang.

Square-root lasso: pivotal recovery of sparse signals via conic

programming.

Biometrika, 98(4):791–806, 2011.

Ben-Michael et al. [2018]

Eli Ben-Michael, Avi Feller, and Jesse Rothstein.

The augmented synthetic control method.

arXiv preprint arXiv:1811.04170, 2018.

Bertrand et al. [2004]

Marianne Bertrand, Esther Duflo, and Sendhil Mullainathan.

How much should we trust differences-in-differences estimates?

The Quarterly Journal of Economics, 119(1):249–275, 2004.

Bickel et al. [1998]

Peter Bickel, Chris Klaassen, Yakov Ritov, and Jon Wellner.

Efficient and Adaptive Estimation for Semiparametric Models.

Springer-Verlag, 1998.

Blundell et al. [2004]

Richard Blundell, Monica Costa Dias, Costas Meghir, and John Van Reenen.

Evaluating the employment impact of a mandatory job search program.

Journal of the European economic association, 2(4):569–606, 2004.

Brodeur et al. [2021]

Abel Brodeur, Andrew E Clark, Sarah Fleche, and Nattavudh Powdthavee.

Covid-19, lockdowns and well-being: Evidence from google trends.

Journal of public economics, 193:104346, 2021.

Card and Krueger [1994]

David Card and Alan B Krueger.

Minimum wages and employment: A case study of the fast-food industry

in New Jersey and Pennsylvania.

American Economic Review, 84:772–793, 1994.

Chang [2020]

Neng-Chieh Chang.

Double/debiased machine learning for difference-in-differences

models.

The Econometrics Journal, 23(2):177–191,

2020.

Chernozhukov et al. [2018a]

Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian

Hansen, Whitney Newey, and James Robins.

Double/debiased machine learning for treatment and structural

parameters.

The Econometrics Journal, 21(1):C1–C68,

2018a.

Chernozhukov et al. [2018b]

Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian

Hansen, Whitney Newey, and James Robins.

Double/debiased machine learning for treatment and structural

parameters.

The Econometrics Journal, 21(1):C1–C68,

2018b.

Chernozhukov et al. [2018c]

Victor Chernozhukov, Juan Carlos Escanciano, Hidehiko Ichimura, Whitney K

Newey, and James M Robins.

Locally robust semiparametric estimation.

arXiv preprint arXiv:1608.00033, 2018c.

Crump et al. [2009]

Richard K Crump, V Joseph Hotz, Guido W Imbens, and Oscar A Mitnik.

Dealing with limited overlap in estimation of average treatment

effects.

Biometrika, 96(1):187–199, 2009.

Dimick and Ryan [2014]

Justin B Dimick and Andrew M Ryan.

Methods for evaluating changes in health care policy: the

difference-in-differences approach.

Jama, 312(22):2401–2402, 2014.

Ding and Li [2019]

Peng Ding and Fan Li.

A bracketing relationship between difference-in-differences and

lagged-dependent-variable adjustment.

Political Analysis, forthcoming, 2019.

Foster and Syrgkanis [2019]

Dylan J Foster and Vasilis Syrgkanis.

Orthogonal statistical learning.

arXiv preprint arXiv:1901.09036, 2019.

Gertler et al. [2011]

PJ Gertler, P Premand, and LB Rawlings.

Who-impact evaluation in practice, chapter 6.

Geneva: World Health Organization, 2011.

Goodman-Bacon and Marcus [2020]

Andrew Goodman-Bacon and Jan Marcus.

Using difference-in-differences to identify causal effects of

covid-19 policies.

2020.

Hahn et al. [2017]

P Richard Hahn, Jared S Murray, and Carlos M Carvalho.

Bayesian regression tree models for causal inference: regularization,

confounding, and heterogeneous effects.

2017.

Heckman et al. [1998]

James J Heckman, Hidehiko Ichimura, and Petra Todd.

Matching as an econometric evaluation estimator.

The Review of Economic Studies, 65(2):261–294, 1998.

Hill [2011]

Jennifer L Hill.

Bayesian nonparametric modeling for causal inference.

Journal of Computational and Graphical Statistics, 20(1), 2011.

Hirshberg and Wager [2021]

David A Hirshberg and Stefan Wager.

Augmented minimax linear estimation.

Annals of Statistics, forthcoming, 2021.

Imbens and Rubin [2015]

Guido W Imbens and Donald B Rubin.

Causal Inference in Statistics, Social, and Biomedical

Sciences.

Cambridge University Press, 2015.

Keele and Minozzi [2013]

Luke Keele and William Minozzi.

How much is minnesota like wisconsin? assumptions and counterfactuals

in causal inference with observational data.

Political Analysis, 21(2):193–216, 2013.

Künzel et al. [2019]

Sören R Künzel, Jasjeet S Sekhon, Peter J Bickel, and Bin Yu.

Metalearners for estimating heterogeneous treatment effects using

machine learning.

Proceedings of the National Academy of Sciences, 116(10):4156–4165, 2019.

Lechner [2011]

Michael Lechner.

The estimation of causal effects by difference-in-difference methods.

Foundations and Trends in Econometrics, 4(3):165–224, 2011.

Li and Li [2019]

Fan Li and Fan Li.

Double-robust estimation in difference-in-differences with an

application to traffic safety evaluation.

arXiv preprint arXiv:1901.02152, 2019.

Li et al. [2018]

Fan Li, Kari Lock Morgan, and Alan M Zaslavsky.

Balancing covariates via propensity score weighting.

Journal of the American Statistical Association, 113(521):390–400, 2018.

Lu et al. [2018]

Alice Lu, Peter I Frazier, and Oren Kislev.

Surge pricing moves Uber’s driver-partners.

In Proceedings of the 2018 ACM Conference on Economics and

Computation, page 3. ACM, 2018.

Lu et al. [2019]

Chen Lu, Xinkun Nie, and Stefan Wager.

Robust nonparametric difference-in-differences estimation.

arXiv preprint arXiv:1905.11622v1, 2019.

Luedtke and van der Laan [2016]

Alexander R Luedtke and Mark J van der Laan.

Super-learning of an optimal dynamic treatment rule.

The International Journal of Biostatistics, 12(1):305–332, 2016.

Meyer [1995]

Breed D Meyer.

Natural and quasi-experiments in economics.

Journal of business & economic statistics, 13(2):151–161, 1995.

Newey [1994]

Whitney K Newey.

The asymptotic variance of semiparametric estimators.

Econometrica: Journal of the Econometric Society, 62(6):1349–1382, 1994.

Nie and Wager [2021]

Xinkun Nie and Stefan Wager.

Quasi-oracle estimation of heterogeneous treatment effects.

Biometrika, 108(2):299–319, 2021.

Obenauer and von der Nienburg [1915]

Marie Louise Obenauer and Bertha von der Nienburg.

Effect of minimum-wage determinations in Oregon.

Bulletin of the United States Bureau of Labor Statistics, 176,

1915.

Robins and Rotnitzky [1995]

James Robins and Andrea Rotnitzky.

Semiparametric efficiency in multivariate regression models with

missing data.

Journal of the American Statistical Association, 90(1):122–129, 1995.

Robins [2004]

James M Robins.

Optimal structural nested models for optimal sequential decisions.

In Proceedings of the second seattle Symposium in

Biostatistics, pages 189–326. Springer, 2004.

Robinson [1988]

Peter M Robinson.

Root-n-consistent semiparametric regression.

Econometrica, pages 931–954, 1988.

Rosenbaum and Rubin [1983]

Paul R Rosenbaum and Donald B Rubin.

The central role of the propensity score in observational studies for

causal effects.

Biometrika, 70(1):41–55, 1983.

Sant’Anna and Zhao [2018]

Pedro HC Sant’Anna and Jun B Zhao.

Doubly robust difference-in-differences estimators.

Available at SSRN 3293315, 2018.

Scharfstein et al. [1999]

Daniel O Scharfstein, Andrea Rotnitzky, and James M Robins.

Adjusting for nonignorable drop-out using semiparametric nonresponse

models.

Journal of the American Statistical Association, 94(448):1096–1120, 1999.

Shalit et al. [2016]

Uri Shalit, Fredrik D Johansson, and David Sontag.

Estimating individual treatment effect: generalization bounds and

algorithms.

arXiv preprint arXiv:1606.03976, 2016.

Tibshirani [1996]

Robert Tibshirani.

Regression shrinkage and selection via the lasso.

Journal of the Royal Statistical Society: Series B (Statistical

Methodology), pages 267–288, 1996.

van der Laan and Dudoit [2003]

Mark J van der Laan and Sandrine Dudoit.

Unified cross-validation methodology for selection among estimators

and a general cross-validated adaptive epsilon-net estimator: Finite sample

oracle inequalities and examples.

Technical report, UC Berkeley Division of Biostatistics, Berkeley CA,

2003.

Van Der Laan and Rubin [2006]

Mark J Van Der Laan and Daniel Rubin.

Targeted maximum likelihood learning.

The International Journal of Biostatistics, 2(1),

2006.

Wing et al. [2018]

Coady Wing, Kosali Simon, and Ricardo A Bello-Gomez.

Designing difference in difference studies: best practices for public

health policy research.

Annual review of public health, 39, 2018.

Xu [2017]

Yiqing Xu.

Generalized synthetic control method: Causal inference with

interactive fixed effects models.

Political Analysis, 25(1):57–76, 2017.

Zhao et al. [2017]

Qingyuan Zhao, Dylan S Small, and Ashkan Ertefaie.

Selective inference for effect modification via the lasso.

arXiv preprint arXiv:1705.08020, 2017.

Zimmert [2018]

Michael Zimmert.

Efficient difference-in-differences estimation with high-dimensional

common trend confounding.

arXiv preprint arXiv:1809.01643, 2018.

Let us define and . The second and third equations become:

which gives us:

To obtain the expressions in (12), we just have to get rid of the conditional expectations form above, and it is easy to check that we will obtain the desired forms. Now we check (13). First, note that:

where . Because and , the above expression evaluates to zero. Similarly, we can show . For terms such as , note that

Because , the above also evaluates to zero. Similarly, we can show that and . For , note that:

Thus we have

and and can be checked similarly. To check is uncorrelated with given :

First we prove the statement , where is the transformed regression estimator, and is the transformed regression estimator with oracle nuisance parameters. From (18), we see that

(S5)

Because each is approximately , which is fixed as grows, and the number of folds is also fixed, will follow if we show that .

The proof consists of two steps. Firstly, we show that, if two nuisance parameters and , estimated by and respectively, satisfy conditions 2, 3 and 4 from above, then the estimation of their product by , and their sum by , also satisfy conditions 2, 3, and 4. As a result, the estimate of and , by sums and products of other nuisance parameters, such as and , also satisfies the conditions listed above. Secondly, we show the desired result, assuming that and satisfy the conditions above.

We start with the first step. Assume that and satisfy conditions 2 to 4. We want to estimate by , and by . Consistency and boundedness comes easily from the consistency and boundedness of and . Risk decay comes as follows:

where we used the assumption that the nuisance parameters are all bounded by . Risk decay for follows similarly. Recall we want to show the following:

(S6)

which will follow if we can show that

(S7)

and

(S8)

Because with these bounds, and noting the Taylor expansion of at some point and is given by:

we have that:

(S9)

where Slutsky’s theorem is used in the last equality. Let us first check (S7). Note that:

(S10)

(S11)

(S12)

(S13)

We check that the three terms above are small.

For (S11), we first check that has mean zero. Note that

where and and we similarly define the cross-fitted analogue and . Many terms above vanished because of (13). We will just show that

where the first line conditions on the data not in fold . Similarly, we have that

Hence we know that , and subsequently

, are all zero. Now we are ready to show that (S11) is :

(S16)

(S17)

(S18)

(S19)

where the first equality is precisely because all terms of the form have mean zero, and the bound comes from the risk decay assumption. To show (S12) is , the argument is exactly the same as the one we gave above: the only difference being we have to check that the term has mean zero. Note that:

where terms vanish in the last equality because of (13). Again we just have to show that and have mean zero, which follows exactly the same argument as we used for (S14). Thus (S12) is also . We only have to check that (S13) is , which follows by Cauchy-Schwarz and the risk decay assumption:

Thus we have finished checking (S7). We proceed to check (S8). Note that:

(S20)

(S21)

(S22)

The second term above is immediately because of the risk decay assumption. Thus we only have to check that (S21) is , which will follow exactly the same argument for (S11), once we show that has mean zero. Note then

where terms vanish in the last equality because of (13). Following the same argument for showing (S14), we can show that the two terms above are both zero. Thus

indeed has mean zero and so is , so we have finished showing .

Now we show that , where . Note that

(S23)

(S24)

(S25)

(S26)

where (S25) use Slutsky’s theorem and the central limit theorem. The desired result then follows.

The proof of Proposition 3 is essentially the same as that of Theorem 2: by exactly the same argument, we know that , where is the transformed regression estimator with oracle nuisance parameters. Then we just have to show , where , which follows from the following calculation:

(S27)

(S28)

(S29)

(S30)

where (S29) uses Slutsky’s theorem and the central limit theorem.

Following notation in Foster and Syrgkanis [2019], we first define directional derivatives: we define for a pair fo functions . We define

. Next, we check Assumptions 1-4 stated in Foster and Syrgkanis [2019].

First, we check Assumption 2 on the first order optimality.

Next, we check Assumption 1. Note that we have to check it with directional derivative with respect to all nuisance components . By symmetry, we only need to check it with .

where the last equality follows from as in Proposition 1.

Next, we check

where the last equality follows from as in Proposition 1.

Before we continue, we define

and similarly, we define .

We further define

and

We check

For the second term, we notice that from Proposition 1, and so

For the first term,

First, we note that

for some function . The upshot is that

where the second to the last equality follows from and

from Proposition 1.

Following a similar argument, we can show that

Note that

It’s immediate from the previous arguments that

and

and from Proposition 1, again we use the fact that and and

, we then conclude that

We can then conclude

An almost identical derivation can be taken to show that

We have now concluded showing Assumption 2 from Foster and Syrgkanis [2019] holds.

To show Assumption 3 holds, we have

Given and , etc., we have . Thus, and in Assumption 3.

To show Assumption 4 holds, we can check that

Finally, we can check that

and this similarly holds when we take derivative with respect to or . We conclude that in Assumption 4.

The result then directly follows from Theorem 1 in Foster and Syrgkanis [2019].