Adaptive Reduced Rank Regression

Abstract

We study the low rank regression problem , where and are and dimensional vectors respectively. We consider the extreme high-dimensional setting where the number of observations is less than . Existing algorithms are designed for settings where is typically as large as . This work provides an efficient algorithm which only involves two SVD, and establishes statistical guarantees on its performance. The algorithm decouples the problem by first estimating the precision matrix of the features, and then solving the matrix denoising problem. To complement the upper bound, we introduce new techniques for establishing lower bounds on the performance of any algorithm for this problem. Our preliminary experiments confirm that our algorithm often out-performs existing baselines, and is always at least competitive.

1 Introduction

We consider the regression problem in the high dimensional setting, where is the vector of features, is a vector of responses, are the learnable parameters, and is a noise term. High-dimensional setting refers to the case where the number of observations is insufficient for recovery and hence regularization for estimation is necessary koltchinskii2011nuclear ; negahban2011estimation ; chen2013reduced . This high-dimensional model is widely used in practice, such as identifying biomarkers zhu2017low , understanding risks associated with various diseases frank2015dietary ; batis2016using , image recognition rahim2017multi ; fan2017hyperspectral , forecasting equity returns in financial markets polk2006cross ; stock2011dynamic ; medeiros2012estimating ; bender2013foundations , and analyzing social networks wu2017generalized ; ralescu2011spectral .

We consider the “large feature size” setting, in which the number of features is excessively large and can be even larger than the number of observations . This setting frequently arises in practice because it is often straightforward to perform feature-engineering and produce a large number of potentially useful features in many machine learning problems. For example, in a typical equity forecasting model, is around 3,000 (i.e., using 10 years of market data), whereas the number of potentially relevant features can be in the order of thousands polk2006cross ; gu2018empirical ; kelly2019characteristics ; chen2019deep . In predicting the popularity of a user in an online social network, is in the order of hundreds (each day is an observation and a typical dataset contains less than three years of data) whereas the feature size can easily be more than 10k ravikumar2010high ; bamman2014gender ; sinha2013predicting .

Existing low-rank regularization techniques (e.g., koltchinskii2011nuclear ; negahban2011estimation ; ma2014adaptive ) are not optimized for the large feature size setting. These results assume that either the features possess the so-called restricted isometry property candes2008restricted , or their covariance matrix can be accurately estimated negahban2011estimation . Therefore, their sample complexity depends on either or the smallest eigenvalue value of ’s covariance matrix. For example, a mean-squared error (MSE) result that appeared in negahban2011estimation is of the form . When , this result becomes trivial because the forecast produces a comparable MSE. We design an efficient algorithm for the large feature size setting. Our algorithm is a simple two-stage algorithm. Let be a matrix that stacks together all features and be the one that stacks the responses. In the first stage, we run a principal component analysis (PCA) on to obtain a set of uncorrelated features . In the second stage, we run another PCA to obtain a low rank approximation of and use it to construct an output.

While the algorithm is operationally simple, we show a powerful and generic result on using PCA to process features, a widely used practice for “dimensionality reduction” cao2003comparison ; ghodsi2006dimensionality ; friedman2001elements . PCA is known to be effective to orthogonalize features by keeping only the subspace explaining large variations. But its performance can only be analyzed under the so-called factor model stock2002forecasting ; stock2011dynamic . We show the efficacy of PCA without the factor model assumption. Instead, PCA should be interpreted as a robust estimator of ’s covariance matrix. The empirical estimator in the high-dimensional setting cannot be directly used because , but it exhibits an interesting regularity: the leading eigenvectors of are closer to ground truth than the remaining ones. In addition, the number of reliable eigenvectors grows as the sample size grows, so our PCA procedure projects the features along reliable eigenvectors and dynamically adjusts ’s rank to maximally utilize the raw features. Under mild conditions on the ground-truth covariance matrix of , we show that it is always possible to decompose into a set of near-independent features and a set of (discarded) features that have an inconsequential impact on a model’s MSE.

When features are transformed into uncorrelated ones , our original problem becomes , which can be reduced to a matrix denoising problem donoho2014minimax and be solved by the second stage. Our algorithm guarantees that we can recover all singular vectors of whose associated singular values are larger than a certain threshold . The performance guarantee can be translated into MSE bounds parametrized by commonly used variables (though, these translations usually lead to looser bounds). For example, when ’s rank is , our result reduces the MSE from to for a suitably small constant . The improvement is most pronounced when .

We also provide a new matching lower bound. Our lower bound asserts that no algorithm can recover a fraction of singular vectors of whose associated singular values are smaller than , where is a “gap parameter”. Our lower bound contribution is twofold. First, we introduce a notion of “local minimax”, which enables us to define a lower bound parametrized by the singular values of . This is a stronger lower bound than those delivered by the standard minimax framework, which are often parametrized by the rank of koltchinskii2011nuclear . Second, we develop a new probabilistic technique for establishing lower bounds under the new local minimax framework. Roughly speaking, our techniques assemble a large collection of matrices that share the same singular values of but are far from each other, so no algorithm can successfully distinguish these matrices with identical spectra.

2 Preliminaries

Notation. Let and be data matrices with their -th rows representing the -th observation. For matrix , we denote its singular value decomposition as and is the rank approximation obtained by keeping the top singular values and the corresponding singular vectors. When the context is clear, we drop the superscript and use and (, , and ) instead. Both and are used to refer to -th singular value of . We use MATLAB notation when we refer to a specific row or column, e.g., is the first row of and is the first column. , , and are Frobenius, spectral, and nuclear norms of . In general, we use boldface upper case (e.g., ) to denote data matrices and boldface lower case (e.g., ) to denote one sample. Regular fonts denote other matrices. Let and be the empirical estimate of . Let be the eigen-decomposition of the matrix , and be the diagonal entries of . Let be an arbitrary set of column vectors, and be the subspace spanned by it. An event happens with high probability means that it happens with probability , where 5 is an arbitrarily chosen large constant and is not optimized.

\li \li; . \li\CommentGap thresholding. \li\Comment is a tunable parameter. \li, \li: diagonal matrix comprised of . \li: leading columns of and . \li \li. \li\Return.

\li. \li\CommentAbsolute value thresholding. \li\Comment is a suitable constant; is std. of the noise. \li. \li\Return {codebox} \Procname \li. \li. \li\Return

Our model. We consider the model , where is a multivariate Gaussian, , , and . We can relax the Gaussian assumptions on and for most results we develop. We assume a PAC learning framework, i.e., we observe a sequence of independent samples and our goal is to find an that minimizes the test error . We are specifically interested in the setting in which .

The key assumption we make to circumvent the issue is that the features are correlated. This assumption can be justified for the following reasons: (i) In practice, it is difficult, if not impossible, to construct completely uncorrelated features. (ii) When , it is not even possible to test whether the features are uncorrelated bai2010spectral . (iii) When we indeed know that the features are independent, there are significantly simpler methods to design models. For example, we can build multiple models such that each model regresses on an individual feature of , and then use a boosting/bagging method friedman2001elements ; schapire2013boosting to consolidate the predictions.

The correlatedness assumption implies that the eigenvalues of decays. The only (full rank) positive semidefinite matrices that have non-decaying (uniform) eigenvalues are the identity matrix (up to some scaling). In other words, when has uniform eigenvalues, has to be uncorrelated.

We aim to design an algorithm that works even when the decay is slow, such as when has a heavy tail. Specifically, our algorithm assumes ’s are bounded by a heavy-tail power law series:

Assumption 2.1.

The series satisfies for a constant and .

We do not make functional form assumptions on ’s. This assumption also covers many benign cases, such as when has low rank or its eigenvalues decay exponentially. Many empirical studies report power law distributions of data covariance matrices akemann2010universal ; nobi2013random ; urama2017analysis ; clauset2009power . Next, we make standard normalization assumptions. , , and . Remark that we assume only the spectral norm of is bounded, while its Frobenius norm can be unbounded. Also, we assume the noise is sufficiently large, which is more important in practice. The case when is small can be tackled in a similar fashion. Finally, our studies avoid examining excessively unrealistic cases, so we assume . We examine the setting where existing algorithms fail to deliver non-trivial MSE, so we assume that .

3 Upper bound

Our algorithm (see Fig. 1) consists of two steps. Step 1. Producing uncorrelated features. We run a PCA to obtain a total number of orthogonalized features. See in Fig. 1. Let the SVD of be . Let be a suitable rank chosen by inspecting the gaps of ’s singular values (Line 5 in ). is the set of transformed features output by this step. The subscript in reflects that a dimension reduction happens so the number of columns in is smaller than that in . Compared to standard PCA dimension reduction, there are two differences: (i) We use the left leading singular vectors of (with a re-scaling factor ) as the output, whereas the PCA reduction outputs . (ii) We design a specialized rule to choose whereas PCA usually uses a hard thresholding or other ad-hoc rules. Step 2. Matrix denoising. We run a second PCA on the matrix . The rank is chosen by a hard thresholding rule (Line 4 in ). Our final estimator is , where is computed in .

3.1 Intuition of the design

While the algorithm is operationally simple, its design is motivated by carefully unfolding the statistical structure of the problem. We shall realize that applying PCA on the features should not be viewed as removing noise from a factor model, or finding subspaces that maximize variations explained by the subspaces as suggested in the standard literature friedman2001elements ; stock2002forecasting ; stock2005implications . Instead, it implicitly implements a robust estimator for ’s precision matrix, and the design of the estimator needs to be coupled with our objective of forecasting , thus resulting in a new way of choosing the rank.

Design motivation: warm up. We first examine a simplified problem , where variables in are assumed to be uncorrelated. Assume in this simplified setting. Observe that

| (1) |

where is the noise term and can be approximated by a matrix with independent zero-mean noises.

Solving the matrix denoising problem. Eq. 1 implies that when we compute , the problem reduces to an extensively studied matrix denoising problem donoho2014minimax ; gavish2014optimal . We include the intuition for solving this problem for completeness. The signal is overlaid with a noise matrix . will elevate all the singular values of by an order of . We run a PCA to extract reliable signals: when the singular value of a subspace is , the subspace contains significantly more signal than noise and thus we keep the subspace. Similarly, a subspace associated a singular value mostly contains noise. This leads to a hard thresholding algorithm that sets , where is the maximum index such that for some constant . In the general setting , may not be uncorrelated. But when we set , we see that . This means knowing suffices to reduce the original problem to a simplified one. Therefore, our algorithm uses Step 1 to estimate and , and uses Step 2 to reduce the problem to a matrix denoising one and solve it by standard thresholding techniques.

Relationship between PCA and precision matrix estimation. In step 1, while we plan to estimate , our algorithm runs a PCA on . We observe that empirical covariance matrix , i.e., ’s eigenvectors coincide with ’s right singular vectors. When we use the empirical estimator to construct , we obtain . When we apply this map to every training point and assemble the new feature matrix, we exactly get . It means that using to construct is the same as running a PCA in with .

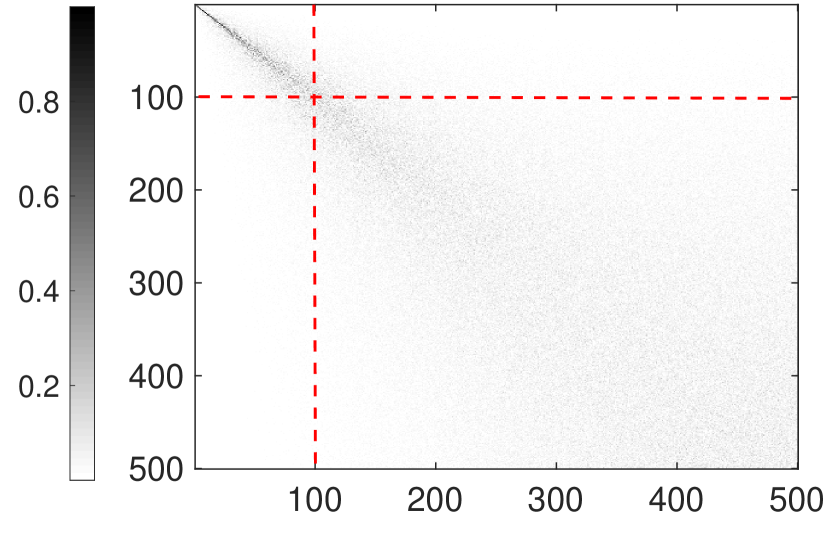

When , PCA uses a low rank approximation of as an estimator for . We now explain why this is effective. First, note that is very far from when , therefore it is dangerous to directly plug in to find . Second, an interesting regularity of exists and can be best explained by a picture. In Fig. 2, we plot the pairwise angles between eigenvectors of and those of from a synthetic dataset. Columns are sorted by the ’s eigenvalues in decreasing order. When and coincide, this plot would look like an identity matrix. When and are unrelated, then the plot behaves like a block of white Gaussian noise. We observe a pronounced pattern: the angle matrix can be roughly divided into two sub-blocks (see the red lines in Fig. 2). The upper left sub-block behaves like an identity matrix, suggesting that the leading eigenvectors of are close to those of . The lower right block behaves like a white noise matrix, suggesting that the “small” eigenvectors of are far from those of . When grows, one can observe the upper left block becomes larger and this the eigenvectors of will sequentially get stabilized. Leading eigenvectors are first stabilized, followed by smaller ones. Our algorithm leverages this regularity by keeping only a suitable number of reliable eigenvectors from while ensuring not much information is lost when we throw away those “small” eigenvectors.

Implementing the rank selection. We rely on three interacting building blocks:

1. Dimension-free matrix concentration. First, we need to find a concentration behavior of for to decouple from the MSE bound. We utilize a dimension-free matrix concentration inequality oliveira2010sums (also replicated as Lemma 3) . Roughly speaking, the concentration behaves as . This guarantees that by standard matrix perturbation results kato1987variation .

2. Davis-Kahan perturbation result. However, the pairwise closeness of the ’s does not imply the eigenvectors are also close. When and are close, the corresponding eigenvectors in can be “jammed” together. Thus, we need to identify an index , at which exhibits significant gap, and use a Davis-Kahan result to show that is close to . On the other hand, the map we aim to find depends on the square root of inverse , so we need additional manipulation to argue our estimate is close to .

3. The connection between gap and tail. Finally, the performance of our procedure is also characterized by the total volume of signals that are discarded, i.e., , where is the location that exhibits the gap. The question becomes whether it is possible to identify a that simultaneously exhibits a large gap and ensures the tail after it is well-controlled, e.g., the sum of the tail is for a constant . We develop a combinatorial analysis to show that it is always possible to find such a gap under the assumption that is bounded by a power law distribution with exponent . Combining all these three building blocks, we have:

Proposition 1.

Let and be two tunable parameters such that and . Assume that . Consider running in Fig. 1, with high probability, we have (i) Leading eigenvectors/values are close: there exists a unitary matrix and a constant such that (ii) Small tail: for a constant .

Prop. 1 implies that our estimate is sufficiently close to , up to a unitary transform. We then execute to reduce the problem to a matrix denoising one and solve it by hard-thresholding. Let us refer to , where is a standard multivariate Gaussian and as the orthogonalized form of the problem. While we do not directly observe , our performance is characterized by spectra structure of .

Theorem 1.

Consider running in Fig. 1 on independent samples from the model , where and . Let . Assume that (i) , and (ii) is a multivariate Gaussian with . In addition, and for all , for a constant , and (iii) , where .

Let , , and be a suitably large constant. Let be the orthogonalized form of the problem. Let be the largest index such that . Let be our testing forecast. With high probability over the training data:

| (2) |

The expectation is over the randomness of the test data.

Theorem 1 also implies that there exists a way to parametrize and such that for some constant . We next interpret each term in (2).

Terms are typical for solving a matrix denoising problem : we can extract signals associated with leading singular vectors of , so starts at . For each direction we extract, we need to pay a noise term of order , leading to the term . Terms come from the estimations error of produced from Prop. 1, consisting of both estimation errors of ’s leading eigenvectors and the error of cutting out a tail. We pay an exponent of on both terms (e.g., in Prop. 1 becomes ) because we used Cauchy-Schwarz (CS) twice. One is used in running matrix denoising algorithm with inaccurate ; the other one is used to bound the impact of cutting a tail. It remains open whether two CS is can be circumvented.

3.2 Analysis

We now analyze our algorithm. Our analysis consists of three steps. In step 1, we prove Proposition 1. In step 2, we relate with the product produced by our estimate . In step 3, we prove Theorem 1.

3.2.1 Step 1. PCA for the features (proof of Proposition 1)

This section proves Proposition 1. We shall first show that the algorithm always terminates. We have the following lemma.

Lemma 1.

Let be a sequence such that , for some constant , , and . Define for . Let be a sufficiently large number, and and are two suitable constants. Let be any number such that . Let be any parameter such that . There exists an such that (i) Gap is sufficiently large: , and (ii) tail sum is small: .

We remark that Lemma 1 will also be able to show part (ii) of Proposition 1 (this will be explained below). This lemma also corresponds to the “connection between gap and tail” building block referred in Section 3.1.

Proof of Lemma 1.

Define the function (by Euler–Maclaurin formula), where is a function of

Next, let us define

Roughly speaking, we want to identify an such that is smaller than but is as close to it as possible. We can interpret in a similar manner. because of the assumption .

We can verify that because . We can similarly verify that for some constant . Now using

We may use an averaging argement and show that there exists an such that

Note that because . Next, using that , we have

| (3) |

This implies one of is at least . In other words, there exists an such that Finally, we can check that

| (4) |

∎

We apply Lemma 1 by setting . There is a parameter that we can tune, such that it is always possible to find an where and . For any (a function of ), we can set . In addition, . This also proves the second part of the Proposition.

It remains to prove part (i) of Proposition 1. It consists of three steps.

Step 1. Dimension-free Chernoff bound for matrices. We first give a bound on , which characterizes the tail probability by using the first and second moments of random vectors. This is the key device enabling us to meaningfully recover signals even when .

Lemma 2.

Recall that and . For any ,

| (5) |

The exponent 10 is chosen arbitrarily and is not optimized.

Proof of Lemma 2.

We use the following specific form of Chernoff bound (oliveira2010sums )

Lemma 3.

Let , be i.i.d. random vectors such that a.s. and . Then for any ,

| (6) |

We aim to use Lemma 3 to show Lemma 2 and we set . But the -norm of ’s are unbounded so we need to use a simple coupling technique to circumvent the problem. Specifically, let be a suitable constant and define

| (7) |

By using a standard Chernoff bound, we have

| (8) |

Let us write . We set and in Lemma 3. One can see that

| (9) |

∎

Step 2. Davis-Kahan bound. The above analysis gives us that . We next show that the first a few eigenvectors of are close to those of .

Lemma 4.

Let and . Considering running in Fig. 1. Let and . When ,

Proof.

Recall that are the eigenvalues of . Let also be the eigenvalues of . Define

| (10) |

The constant 10 is chosen in an arbitrary manner. Because , we know that contains and that contains kato1987variation . Using the Davis-Kahan Theorem davis1970rotation , we get

| (11) |

∎

We also need the following building block.

Lemma 5.

tang2013universally Let and be positive semidefinite matrices with the same rank of . Let and be of full column rank such that and . Let be the smallest non-zero eigenvalue of . Then there exists a unitary matrix such that

Step 3. Commuting the unitary matrix. Roughly speaking, Lemma 4 and Lemma 5 show that there exists a unitary matrix such that is close to . Standard matrix perturbation result also shows that and are close. This gives us that and are close, whereas we need that and are close. The unitary matrix is not in the right place. This is a standard technical obstacle for analyzing PCA based techniques tang2013universally ; fan2016overview ; li2017world . We develop the following lemma to address the issue.

Lemma 6.

Let be matrices such that . Let , be diagonal matrices with strictly positive entries, and let be a unitary matrix. Then,

Proof.

Observe that,

The result then follows by taking spectral norms of both sides, the triangle inequality and the sub-multiplicativity of the spectral norm. ∎

Results from Step 1 to Step 3 suffice to prove the first part of Proposition 1. First, we use Lemma 4 and Lemma 5 (adopted from tang2013universally ) to get that

| (12) |

Next, observe that . By applying Lemma 6, with and , and , we obtain

This completes the proof of Proposition 1.

3.2.2 Step 2. Analysis of

Proposition 2.

The rest of this Section proves Proposition 2. Recall that is the orthogonalized form of our problem. Let us split , where consists of the leading columns of and consists of the remaining columns. Similarly, let , where and . Let , where and . Finally, when we refer to estimated features of an individual instance produced from Step 1, we use .

We have . We let

where and . We have

We shall let

| (13) |

where

We next analyze each term. We aim to find bounds in either spectral norm or Frobenius norm. In some cases, it suffices to use to upper bound . So we bound only ’s spectral norm. On the other hand, in the case of analyzing , we can get a tight Frobenius norm bound but we cannot get a non-trivial spectral bound.

From time to time, we will label the dimension of matrices in complex multiplication operations to enable readers to do sanity checks.

Bounding . We use the following Lemmas.

Lemma 7.

Let , where . Let each entry of be an independent standard Gaussian. We have

| (14) |

Proof of Lemma 7.

We rely on the Lemma rudelson2010non :

Lemma 8.

Let () be a random matrix so that each is an independent standard Gaussian random variable. Let be the maximum singular value of and be the minimum singular value of it. We have

| (15) |

We set . Let us start with considering the case . We have

| (16) |

and

| (17) |

The case can be analyzed in a similar fashion so that we can get

| (18) |

∎

Therefore, we have

Bounding . Observe that . Also,

Therefore,

| (19) |

We next bound .

Lemma 9.

Let be the learnable parameter in normalized form , where and , and is determined by . We have .

Proof of Lemma 9.

Recall that

We let , where and . We have . Therefore,

| (20) |

Here, we used the assumption and the last equation holds because of Proposition 1. ∎

Bounding . We have the following Lemma.

Lemma 10.

Let so that each entry in is an independent standard Gaussian and so that each entry in is an independent Gaussian . For sufficiently large , , and , where , we have

Proof of Lemma 10.

Let . By Lemma 7, with high probability . This implies that the eigenvalues of are all within the range . Note that for , if , then . This implies that the singular values of are within the range .

Let , where . We have

| (21) |

Using the fact that the columns of are orthonormal vectors, is a unitary matrix, and , we see that is a matrix with i.i.d. Gaussian entries with standard deviation .

Let and . Then, from (21), we have

| (22) |

The entries in () are all i.i.d Gaussian. By Marchenko-Pastar’s law (and the finite sample bound of it rudelson2010non ), we have with high probability . Therefore, with high probability:

∎

Lemma 10 implies that

Bounding . We have

Using a Chernoff bound, we have whp .

Bounding . Because , we have

Using a simple Chernoff bound, we have whp,

This implies

We may let

We can check that

Also, we can see that . This completes the proof for Proposition 2.

3.2.3 Step 3. Analysis of our algorithm’s MSE

Let us recall our notation:

-

1.

and .

-

2.

We let be the output of in Fig. 1.

-

3.

All singular vectors in whose associated singular values are kept.

Let be the largest index such that . One can see that our testing forecast is . Therefore, we need to bound .

By Proposition 2, we have where and whp. Let . We have

Let , , , and . We still have , and .

We next have

| (Cauchy Schwarz for random variables) | ||

We first bound (the easier term). We have

We first bound . We consider two cases.

Case 1. . In this case, we observe that . This implies that . Therefore, .

Case 2. . In this case, . This implies (i.e., the projection will not keep any subspace).

This case also implies

Next, we have .

Therefore,

Next, we move to bound

We shall construct an orthonormal basis on and use the basis to “measure the mass”. Let us describe this simple idea at high-level first. Let be a basis for and let be an arbitrary matrix. We have . The meaning of this equality is that we may apply a change of basis on the columns of and the “total mass” of should remain unchanged after the basis change. Our orthonormal basis consists of three groups of vectors.

Group 1. for , where is the number of such that .

Group 2. The subspace in that is orthogonal to . Let us refer to these vectors as and .

Group 3. An arbitrary basis that is orthogonal to vectors in group 1 and group 2. Let us refer to them as .

We have

| Term 1 | |||

| Term 2 | |||

| Term 3 | |||

To understand the reason we perform such grouping, we can imagine making a decision for an (overly) simplified problem for each direction in the basis: consider a univariate estimation problem with being the signal, being the noise, and being the observation. Let us consider the case we observe only one sample. Now when , we can use as the estimator and . This high signal-to-noise setting corresponds to the vectors in Group 1.

When , we have . On the other hand, . This means if we use as the estimator, the forecast is at least better than trivial. The median signal-to-noise setting corresponds to the vectors in group 2.

When , we can simply use as the estimator. This low signal-to-noise setting corresponds to vectors in group 3.

In other words, we expect: (i) In term 1, signals along each direction of vectors in group 1 can be extracted. Each direction also pays a term, which in our setting corresponds to . Therefore, the MSE can be bounded by . (ii) In terms 2 and 3, we do at least (almost) as well as the “trivial forecast” (). There is also an error produced by the estimator error from , and the tail error produced from cutting out features in in Fig. 1.

Now we proceed to execute this idea.

Term 1. . Let be the left singular vector of . We let have columns to include those vectors whose corresponding singular values are for the ease of calculation. We have

Term 2. . We have

On the other hand, note that

| (23) |

Note that

| (24) |

Next, we examine the term .

| (Cauchy Schwarz) | ||||

| ( | (25) | |||

Term 3. We have

This is because ’s are orthogonal to the first left singular vectors of .

We sum together all the terms:

| (26) |

In the above analysis, we used is orthogonal to . Therefore, we can collect (*) and (**) and obtain

Now the MSE is in terms of . We aim to bound the MSE in . So we next relate with . Recall that , where . The singular values of are the same as those of . By using a standard matrix perturbation result, we have

| (27) |

for some constant . We may think (27) as a constraint and maximize the difference . This is maximized when and for .

Therefore,

| (28) |

Now (26) becomes

| (29) |

Next, we assert that . Recall that . This implies for , i.e., . So we have

| (30) |

Finally, we obtain the bound for . Note that

We have

| (31) |

This completes the proof of Theorem 1.

4 Lower bound

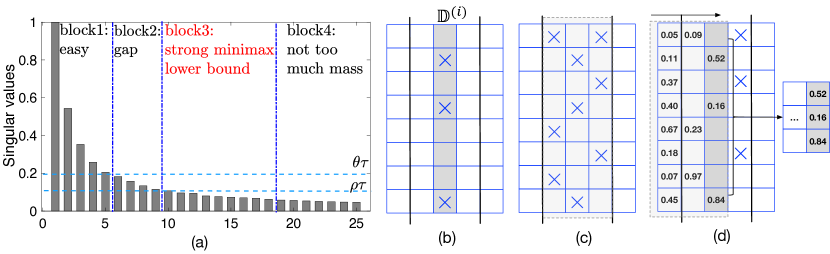

Our algorithm accurately estimates the singular vectors of that correspond to singular values above the threshold . However, it may well happen that most of the spectral ‘mass’ of lies only slightly below this threshold . In this section, we establish that no algorithm can do better than us, in a bi-criteria sense, i.e. we show that any algorithm that has a slightly smaller sample than ours can only minimally outperform ours in terms of MSE.

We establish ‘instance dependent’ lower bounds: When there is more ‘spectral mass’ below the threshold, the performance of our algorithm will be worse, and we will need to establish that no algorithm can do much better. This departs from the standard minimax framework, in which one examines the entire parameter space of , e.g. all rank matrices, and produces a large set of statistically indistinguishable ‘bad’ instances tsybakov2008introduction . These lower bounds are not sensitive to instance-specific quantities such as the spectrum of , and in particular, if prior knowledge suggests that the unknown parameter is far from these bad instances, the minimax lower bound cannot be applied.

We introduce the notion of local minimax. We partition the space into parts so that similar matrices are together. Similar matrices are those that have the same singular values and right singular vectors; we establish strong lower bounds even against algorithms that know the singular values and right singular vectors of . An equivalent view is to assume that the algorithm has oracle access to , ’s singular values, and ’s right singular vectors. This algorithm can solve the orthogonalized form as ’s singular values and right singular vectors can easily be deduced. Thus, the only reason why the algorithm needs data is to learn the left singular vectors of . The lower bound we establish is the minimax bound for this ‘unfair’ comparison, where the competing algorithm is given more information. In fact, this can be reduced further, i.e., even if the algorithm ‘knows’ that the left singular vectors of are sparse, identifying the locations of the non-zero entries is the key difficulty that leads to the lower bound.

Definition 1 (Local minimax bound).

Consider a model , where is a random vector, so represents the co-variance matrix of the data distribution, and . The relation is an equivalence relation and let the equivalence class of be

| (32) |

The local minimax bound for with independent samples and is

| (33) |

It is worth interpreting (33) in some detail. For any two , in , the algorithm has the same ‘prior knowledge’, so it can only distinguish between the two instances by using the observed data, in particular is a function only of and , and we denote it as to emphasize this. Thus, we can evaluate the performance of by looking at the worst possible and considering the MSE .

Proposition 3.

Consider the problem with normalized form . Let be a sufficient small constant. There exists a sufficiently small constant (that depends on ) and a constant such that for any , where is the smallest index such that .

Proposition 3 gives the lower bound on the MSE in expectation; it can be turned into a high probability result with suitable modifications. The proof of the lower bound uses a similar ‘trick’ to the one used in the analysis of the upper bound analysis to cut the tail. This results in an additional term which is generally smaller than the tail term in Theorem 1 and does not dominate the gap.

Gap requirement and bi-criteria approximation algorithms. Let . Theorem 1 asserts that any signal above the threshold can be detected, i.e., the MSE is at most (plus inevitable noise), whereas Proposition 3 asserts that any signal below the threshold cannot be detected, i.e., the MSE is approximately at least . There is a ‘gap’ between and , as and . See Fig. 3(a). This kind of gap is inevitable because both bounds are ‘high probability’ statements. This gap phenomenon appears naturally when the sample size is small as can be illustrated by this simple example. Consider the problem of estimating when we see one sample from . Roughly speaking, when , the estimation is feasible, and whereas , the estimation is impossible. For the region , algorithms fail with constant probability and we cannot prove a high probability lower bound either.

While many of the signals can ‘hide’ in the gap, the inability to detect signals in the gap is a transient phenomenon. When the number of samples is modestly increased, our detection threshold shrinks, and this hidden signal can be fully recovered. This observation naturally leads to a notion of bi-criteria optimization that frequently arises in approximation algorithms.

Definition 2.

An algorithm for solving the problem is -optimal if, when given an i.i.d. sample of size as input, it outputs an estimator whose MSE is at most worse than the local minimax bound, i.e.,

Corollary 1.

Let and be small constants and be a tunable parameter. Our algorithm is -optimal for

The error term consists of that is directly characterized by the signal strength and an additive term . Assuming that , i.e., the signal is not too weak, the term becomes a single multiplicative bound . This gives an easily interpretable result. For example, when our data size is , the performance gap between our algorithm and any algorithm that uses samples is at most . The improvement is significant when other baselines deliver MSE in the additive form that could be larger than in the regime .

Preview of techniques. Let be the instance (in orthogonalized form). Our goal is to construct a collection of matrices so that (i) For any , and . (ii) For any two , is large, and (iii) (cf. (tsybakov2008introduction, , Chap. 2)).

Condition (i) ensures that it suffices to construct unitary matrices ’s for , and that the resulting instances will be in the same equivalence class. Conditions (ii) and (iii) resemble standard construction of codes in information theory: we need a large ‘code rate’, corresponding to requiring a large as well as large distances between codewords, corresponding to requiring that be large. Standard approaches for constructing such collections run into difficulties. Getting a sufficiently tight concentration bound on the distance between two random unitary matrices is difficult as the matrix entries, by necessity, are correlated. On the other hand, starting with a large collection of random unit vectors and using its Cartesian product to build matrices does not necessarily yield unitary matrices.

We design a two-stage approach to decouple condition (iii) from (i) and (ii) by only generating sparse matrices . See Fig. 3(b)-(d). In the first stage (Steps 1 & 2 in Fig. 3(b)-(c)), we only specify the non-zero positions (sparsity pattern) in each . It suffices to guarantee that the sparsity patterns of the matrices and have little overlap. The existence of such objects can easily be proved using the probabilistic method. Thus, in the first stage, we can build up a large number of sparsity patterns. In the second stage (Step 3 in Fig. 3(d)), we carefully fill in values in the non-zero positions for each . When the number of non-zero entries is not too small, satisfying the unitary constraint is feasible. As the overlap of sparsity patterns of any two matrices is small, we can argue the distance between them is large. By carefully trading off the number of non-zero positions and the portion of overlap, we can simultaneously satisfy all three conditions.

4.1 Roadmap

This section describes the roadmap for executing the above idea.

Normalized form. Recall that , we have

| (34) |

We may perform an SVD on . We may also set , which is a standard multi-variate Gaussian in . Then we have

| (35) |

Let . The SVD of is exactly because is unitary. The normalized form of our problem is

| (36) |

Recall our local minimax has an oracle access interpretation. An algorithm with the oracle can reduce a problem into the normalized form on its own, and the algorithm knows . But the oracle still does not have any information on ’s left singular vectors because being able to manipulate is the same as being able to manipulate . Therefore, we can analyze the lower bound in normalized form, with the assumption that the SVD of , in which is known to the algorithm. We shall also let . Because is square, we let in the analysis below.

We make two remarks in comparison to the orthogonalized form . (i) , whereas . ’s dimension is smaller because the knowledge of and enable us to remove the directions from that are orthogonal to ’s row space. (ii) for .

We rely on the following theorem (Chapter 2 in tsybakov2008introduction ) to construct the lower bound.

Theorem 2.

Let , where . Let be distribution of the training data produced from the model . Assume that

-

•

for any .

-

•

For any and

(37) with .

Then

| (38) |

Because is fixed, this problem boils down to finding a collection of unitary matrices in such that any two elements in are sufficiently far. Then we can construct .

We next reiterate (with elaboration) the challenge we face when using existing techniques. Then we describe our approach. We shall first examine a simple case, in which we need only design vectors for one column. Then we explain the difficulties of using an existing technique to generalize the design. Finally, we explain our solution.

Recall that , where we can roughly view as a matrix that consists of independent Gaussian . For the sake of discussion, we assume in our discussion below.

Warmup: one colume case. The problem of packing one column roughly corresponds to establishing a lower bound on the estimation problem , where . corresponds to a column in and consists of independent Gaussian . correpsonds to a column in and we require . To apply Theorem 2, we shall construct a such that is large for each pair and is also large. Specifically, we require (large distance requirement) and (large set requirement). is carefully optimized and we will defer the reasoning to the full analysis below. A standard tool to construct is to use a probabilistic method. We sample independently from the same distribution and argue that with high probability is sufficiently large. Then a union bound can be used to derive . For example, we may set for all , and the concentration quality suffices for us to sample vectors.

Multiple column case. We now move to the problem of packing multiple columns in together. is required to be much larger, e.g., for certain problem instances. A natural generalization of one-column case is to build our parameter set by taking the Cartesian product of multiple copies of . This gives us a large for free but the key issue is that vectors in are generated independently. So there is no way to guarantee they are independent to each other. In fact, it is straightforward to show that many elements in the Cartesian product are far from unitary. One may also directly sample random unitary matrices and argue that they are far from each other. But there seems to exist no tool that enables us to build up a concentration of between two random unitary matrices.

Therefore, a fundamental problem is that we need independence to build up a large set but the unitary constraint limits the independence. So we either cannot satisfy the unitary requirement (Cartesian product approach) or cannot properly use the independence to build concentrations (random unitary matrix approach).

Our approach. We develop a technique that decouples the three requirements (unitary matrices, large distance, and large ). Let us re-examine the Cartesian product approach. When the vectors for each column are completely determined, then it is remarkably difficult to build a Cartesian product that guarantees orthogonality between columns. To address this issue, our approach only “partially” specify vectors in each column. Then we take a Cartesian product of these partial specifications. So the size of the Cartesian product is sufficiently large; meanwhile an element in the product does not fully specify so we still have room to make them unitary. Thus, our final step is to transform each partial specification in the Cartesian product into a unitary matrix. Specifically, it consists of three steps (See Fig. 3)

Step 1. Partial specification of each column. For each column of interest, we build up a collection . Each specifies only the positions of non-zero entire for a vector prepared for filling in .

Step 2. Cartesian product. Then we randomly sample elements from the Cartesian product . Each element in the product specifies the non-zero entries of . We need to do another random sampling instead of using the full Cartesian product because we need to guarantee that any two matrices share a small number of non-zero entries. For example, and are two elements in but they specify two matrices with the same locations of non-zero entries for the first two columns.

Step 3. Building up unitary matrices. Finally, for each element (that specify positions of non-zero entries), we carefully fill in the values of the non-zero entries so that all our matrices are unitary and far from each other. We shall show that it is always possible to construct unitary matrices that “comply with” . In addition, our unitary matrices have few entries with large magnitude so when two matrices share few positions of non-zero entries, they are far.

4.2 Analysis

We now execute the plan outlined in the roadmap. Let and be tunable parameters. For the purpose of getting intuition, is related to the size of so it can be thought as being exponential in , whereas is a constant and we use to control the density of non-zero entries in each .

Let be a collection of random subsets in , in which each is of size . We sample the subsets without replacement. Recall that is the smallest index such that and let us also define . We let . We assume that ; otherwise Proposition 3 becomes trivial. Let be the Cartesian product of for integers . We use to denote an element in . is a -tuple so that each element corresponds to an element in . There are two ways to represent . Both are found useful in our analysis.

-

1.

Set representation. We treat as a set in .

-

2.

Index representation. We treat as an index from that specifies the index of the set that refers to.

Note that the subscript of starts at (instead of or ) for convenience.

Example 4.1.

The index of starts at . Assume that . Let and . The element . There are two ways to represent this element. (i) Set representation. , in which and . (ii) Index representation. . refers to that the third element in is selected.

We now describe our proof in detail. We remark that throughout our analysis, constants are re-used in different proofs.

4.2.1 Step 1. Partial specification for each column

This step needs only characterize the behavior of an individual .

Lemma 11.

Let be a sufficiently small variable, be a tunable parameter and let be a collection of random subsets in (sampled without replacement) such that for all . There exist constants , , and such that when , with probability , for any two distinct and , .

Proof of Lemma 11.

This can be proved by a standard probabilistic argument. Let be an arbitrary subset such that . Let be a random subset of size . We compute the probability that for a fixed .

Let us sequentially sample elements from (without replacement). Let be an indicator random variable that sets to 1 if and only if the -th random element in hits an element in . We have

| (39) |

By using a Chernoff bound, we have

| (40) |

By using a union bound, we have

| (41) |

Therefore, when we set , the failure probability is . ∎

4.2.2 Step 2. Random samples from the Cartesian product

We let . Note that each is sampled independently. We define be a random subset of . We next explain the reason we need to sample random subsets. Recall that for each , we aim to construct a unitary matrix (to be discussed in Step 3) such that the positions of non-zero entries in are specified by (i.e., only when ).

Let and be two distinct elements in . Let and be two unitary matrices generated by and . We ultimately aim to have that being large. We shall make sure (i) and share few non-zero positions (Step 2; this step), and (ii) few entries in and have excessive magnitude (Step 3). These two conditions will imply that and are far, which then implies a lower bound on and .

Because we do not want and share non-zero positions, we want to maximize the Hamming distance (in index representation) between and (i.e., implies and share all non-zero positions, which is a bad event). We sample randomly from because random sample is a known procedure that generates “code” with large Hamming distance mackay2003information .

Before proceeding, we note one catch in the above explanation, i.e., different columns are of different importance. Specifically, . When and collide for a large , it makes more impact to the Frobenius norm. Thus, we define a weighted cost function that resembles the structure of Hamming distance.

| (42) |

Note that the direction we need for is opposite to Hamming distance. One usually maximizes Hamming distance whereas we need to minimize the weighted cost.

We need to develop a specialized technique to produce concentration behavior for because is weighted.

Lemma 12.

Let and be the parameters for producting . Let be a tunable parameter. Let be a random subset of of such that

| (43) |

for some constant . With high probability at least ( a constant), for any and in , .

Proof.

Let . Let and be two different random elements in . We shall first compute that . Here, we assume that is an arbitrary fixed element and is random.

Recall that for . We shall partition into subintervals and group by these intervals. Let be the set of that are in (). Let be the largest integer such that is not empty. Let and . We call the overlapping coefficients between and .

Note that . Therefore, a necessary condition for is . Together with the requirement that , we need

| (44) |

Recall that we assume that is fixed and is random. When , we say is bad. We next partition all bad into sets indexed by . Let be all the bad such that the overlapping coefficients between and are . We have

Next also note that

where is the size of each .

The number of possible such that is at most . Therefore,

By using a union bound on all pairs of and in , we have for sufficiently small , there exists a such that

∎

4.2.3 Step 3. Building up unitary matrices

We next construct a set of unitary matrices in based on elements in . We shall refer to the procedure to generate a unitary from an element as .

Procedure : Let be the matrix aims to fill in. Let be an arbitrary set of orthonormal vectors. partitions the matrix into three regions of columns and it fills different regions with different strategies. See also three regions illustrated by matrices in Fig. 3.

Region 1: for . We set when . This means all the unitary matrices we construct share the first columns.

Region 2: for . We next fill in non-zero entries of each by for . We fill in each sequentially from left to right (from small to large ). We need to make sure that (i) it is feasible to construct that is orthogonal to all () by using only entries specified by . (ii) there is a way to fill in so that not too many entries are excessively large. (ii) is needed because for any and , and still share a small number of non-zero positions (whp , according to Lemma 11). When the mass in is large, the distance between and is harder to control.

Region 3: for . fills in the rest of the vectors arbitrarily so long as is unitary. Unlike the first columns, these columns depend on so each has a different set of ending column vectors.

Analysis for region 2. Our analysis focuses on two asserted properties for Region 2 are true. We first show (i) is true and describe a procedure to make sure (ii) happens.

For , let be the projection of onto the coordinates specified by . See Fig. 3(d) for an illustration. Note that , the dimension of the subspace spanned by is at most . Therefore, we can find a set of orthonormal vectors () that are orthogonal to (). To build a that’s orthogonal to all (), we can first find a that is a linear combination of , and then “inflate” back to , i.e., the -th non-zero coordinate of is . One can see that

for any .

We now make sure (ii) happens. We have the following Lemma.

Lemma 13.

Let () be a collection of orthonormal vectors in . Let be a small tunable parameter. There exists a set of coefficients such that is a unit vector and there exist constant , , and such that

| (45) |

where .

Proof of Lemma 13.

We use a probabilistic method to find . Let for . Let . We shall set . One can check that is a unit vector. We then examine whether (45) is satisfied for these ’s we created. If not, we re-generate a new set of ’s and ’s. We repeat this process until (45) is satisfied.

Because ’s are normalized, setting the standard deviation of is unnecessary. We nevertheless do so because will be approximately a constant, which helps us simplify the calculation.

We claim that there exists a constant such that for any ,

| (46) |

So our probabilistic method described above is guaranteed to find a that satisfies (45)

We next move to showing (46). Recall that

We also let . We can see that is a Gaussian random variable with a standard deviation . The inequality uses the fact that ’s are orthonormal to each other and therefore .

On the other hand, one can see that

Therefore, by a standard Chernoff bound, .

Next, because collectively form a spherical distribution, we have is independent to . Therefore,

| (47) |

Conditioned on , we use the fact that to get and

| (48) |

Therefore,

∎

4.2.4 Proof of Proposition 3

Now we are ready to use Theorem 2 to prove Proposition 3. Let be the set constructed from Step 1 and . Let . Let also be the distribution of generated from the model . Let be the distribution of from the normalized model when is given. Let be the product distribution when we observe samples from the model . Let be the pdf of for , be the pdf of given , and be the pdf of .

We need to show that for any (i) is large, and (ii) the KL-divergence between and is bounded.

Lemma 14.

Let , , and be generated by the parameters , and (see Steps 1 to 3). For any and in , we have

| (49) |

for some constant and .

Proof.

Let such that and ; let be that and . Also, recall that we let .

We have

Let also , i.e., the set of coordinates that and agree. Whp, we have

| (50) |

The last inequality holds because of Lemma 12. Therefore, we have .

Now we have

Next we bound when . We have

| (51) |

By Lemma 11, whp . Next, we give a bound for . The bound for can be derived in a similar manner.

For each , we check whether :

Therefore,

∎

We need two additional building blocks.

Lemma 15.

Consider the regression problem , where and the eigenvalues of the features follow a power law distribution with exponent . Consider the problem in orthogonalized form. Let be the -th singular value of . Let be an arbitrary value in . There exists a constant such that

Proof of Lemma 15.

Without loss of generality, assume that . We first split the columns of into two parts, , in which consists of the first columns of and consists of the remaining columns. Let be a zero matrix in . is a matrix of rank at most .

Let us split other matrices in a similar manner.

-

•

, where and ,

-

•

, where , and , and

-

•

, where and .

We have

∎

We next move to our second building block.

Fact 4.1.

| (52) |

Proof of Fact 4.1.

∎

We now complete the proof for Proposition 3. First, define . For any and in , we have

where recall that . Using Lemma 14, we have .

Next, we find a smallest such that

| (53) |

By Lemma 12, we have . (53) is equivalent to requiring

We may thus set . Now we may invoke Theorem 2 and get

| (Use Lemma 15 to bound ) |

We shall set be a small constant (say ), , and . This gives us

Together with the fact that , we complete the proof of Proposition 3.

5 Related work and comparison

In this section, we compare our results to other regression algorithms that make low rank constraints on . Most existing MSE results are parametrized by the rank or spectral properties of , e.g. negahban2011estimation defined a generalized notion of rank

| (54) |

i.e. characterizes the generalized rank of whereas characterizes that of . When , is the rank of the because in our setting. In their setting, the MSE is parametrized by and is shown to be . In the special case when , this reduces to . On the other hand, the MSE in our case is bounded by (cf. Thm. 1). We have When , this becomes .

The improvement here is twofold. First, our bound is directly characterized by in orthogonalized form, whereas result of negahban2011estimation needs to examine the interaction between and , so their MSE depends on both and . Second, our bound no longer depends on and pays only an additive factor , thus, when , our result is significantly better. Other works have different parameters in the upper bounds, but all of these existing results require that to obtain non-trivial upper bounds koltchinskii2011nuclear ; bunea2011optimal ; chen2013reduced ; koltchinskii2011nuclear . Unlike these prior work, we require a stochastic assumption on (the rows are i.i.d.) to ensure that the model is identifiable when , e.g. there could be two sets of disjoint features that fit the training data equally well. Our algorithm produces an adaptive model whose complexity is controlled by and , which are adjusted dynamically depending on the sample size and noise level. bunea2011optimal and chen2013reduced also point out the need for adaptivity; however they still require and make some strong assumptions. For instance, bunea2011optimal assumes that there is a gap between and for some . In comparison, our sufficient condition, the decay of , is more natural. Our work is not directly comparable to standard variable selection techniques such as LASSO tibshirani1996regression because they handle univariate . Column selection algorithms dan2015low generalize variable selection methods for vector responses, but they cannot address the identifiability concern.

5.1 Missing proof in comparison

This section proves the following corollary.

Corollary 2.

Use the notation appeared in Theorem 1. Let the ground-truth matrix for . We have whp

| (55) |

Proof.

We first prove the case as a warmup. Observe that

The last inequality uses for . Therefore, we have

Next, we prove the general case . We can again use an optimization view to give an upper bound of the MSE. We view as a constraint. We aim to maximize the uncaptured signals, i.e., solve the following optimization problem

| maximize: | |||

| subject to: | |||

The optimal solution is achieved when for , where , and for . We have

| (56) |

We can also see that

Therefore,

∎

6 Experiments

| Model | MSEout | MSEin | (bps) | (bps) | Sharpe | -statistic | |

|---|---|---|---|---|---|---|---|

| ARRR, N= 983 | 0.9935 | 1.0140 | -0.0205 | 46.3761 | 158.2564 | 2.4350 | 8.3268 |

| Lasso | 1.1158 | 0.3953 | 0.7205 | 6.6049 | 7147.0116 | 2.1462 | 0.0601 |

| Ridge | 1.2158 | 0.1667 | 1.0491 | 9.8596 | 8511.9076 | 0.6603 | -0.0497 |

| Reduced ridge | 1.0900 | 0.8687 | 0.2213 | 13.0321 | 1555.5136 | 0.3065 | -0.3275 |

| RRR | 1.2200 | 0.5867 | 0.6332 | 7.0830 | 4121.2548 | 0.3647 | -0.6626 |

| Nuclear norm | 1.2995 | 0.12078 | 1.1787 | 4.7297 | 8789.0625 | 0.6710 | 0.2340 |

| PCR | 1.0259 | 0.8456 | 0.1802 | 1.1278 | 1544.7258 | 1.8070 | 0.3947 |

| ARRR, N= 2838 | 1.0056 | 0.9050 | 0.1006 | 18.5761 | 689.0625 | 1.6239 | 15.4134 |

| Lasso | 1.0625 | 0.5286 | 0.5339 | 1.1236 | 6029.5225 | 0.5954 | 0.0179 |

| Ridge | 1.0289 | 0.6741 | 0.3548 | 0.2116 | 5342.1481 | 0.5739 | 0.0670 |

| Reduced ridge | 1.9722 | 0.7373 | 1.2349 | 1.0816 | 2416.7056 | 1.5482 | 0.0619 |

| RRR | 1.0873 | 0.61376 | 0.4735 | 4.5795 | 3844.124 | -0.477 | 0.6399 |

| Nuclear norm | 1.1086 | 0.15346 | 0.9551 | 2.2097 | 8461.2402 | -0.3698 | -0.8986 |

| PCR | 1.0263 | 0.5336 | 0.4927 | 5.233 | 4653.9684 | 1.2799 | 0.6990 |

| Model | MSEin | MSEout | MSEout-in | Corrin | Corrout |

|---|---|---|---|---|---|

| ARRR | 5.0104 0.38 | 9.4276 2.31 | 4.4172 | 0.7425 0.07 | 0.6730 0.13 |

| Lasso | 2.3755 1.95 | 14.8279 4.81 | 12.4524 | 0.9171 0.09 | 0.4754 0.15 |

| Ridge | 1.3974 0.53 | 13.6244 4.39 | 12.2270 | 0.9555 0.04 | 0.4742 0.17 |

| Reduced ridge | 4.5260 1.93 | 12.2339 2.70 | 7.7079 | 0.7905 0.09 | 0.4972 0.18 |

| RRR | 4.3456 0.47 | 13.0768 2.63 | 8.7313 | 0.7725 0.12 | 0.3820 0.22 |

| Nuclear norm | 4.9190 2.04 | 13.0532 4.38 | 8.6677 | 0.7872 0.10 | 0.4869 0.16 |

| PCR | 6.4037 1.99 | 13.0847 4.19 | 8.8892 | 0.7199 0.05 | 0.4861 0.15 |

We apply our algorithm on an equity market and a social network dataset to predict equity returns and user popularity respectively. Our baselines include ridge regression (“Ridge”), reduced rank ridge regression mukherjee2011reduced (“Reduced ridge”), LASSO (“Lasso”), nuclear norm regularized regression (“Nuclear norm”), reduced rank regression velu2013multivariate (“RRR”), and principal component regression agarwal2019robustness (“PCR”).

Predicting equity returns. We use a stock market dataset from an emerging market that consists of approximately 3600 stocks between 2011 and 2018. We focus on predicting the next 5-day returns. For each asset in the universe, we compute its past 1-day, past 5-day, and past 10-day returns as features. We use a standard approach to translate forecasts into positions ang2014asset ; zhou2014active . We examine two universes in this market: (i) Universe 1 is equivalent to SP 500 and consists of 983 stocks, and (ii) Full universe consists of all stocks except for illiquid ones.

Predicting equity returns. We use a stock market dataset from an emerging market that consists of approximately 3600 stocks between 2011 and 2018. We focus on predicting the next 5-day returns. For each asset in the universe, we compute its past 1-day, past 5-day and past 10-day returns as features. We use a standard approach to translate forecasts into positions ang2014asset ; zhou2014active . We examine two universes in this market: (i) Universe 1 is equivalent to SP 500 and consists of 983 stocks, and (ii) Full universe consists of all stocks except for illiquid ones.

Results. Table 1 reports the forecasting power and portfolio return for out-of-sample periods in two universes. We observe that (i) The data has a low signal-to-noise ratio. The out-of-sample values of all the methods are close to 0. (ii) has the highest forecasting power. (iii) has the smallest in-sample and out-of-sample gap (see column MSEout-in), suggesting that our model is better at avoiding spurious signals.

Predicting user popularity in social networks. We collected tweet data on political topics from October 2016 to December 2017. Our goal is to predict a user’s next 1-day popularity, which is defined as the sum of retweets, quotes, and replies received by the user. There are a total of 19 million distinct users, and due to the huge size, we extract the subset of 2000 users with the most interactions for evaluation. For each user in the 2000-user set, we use its past 5 days’ popularity as features. We further randomly sample 200 users and make predictions for them, i.e., setting to make of the same magnitude as .

Results. We randomly sample users for 10 times and report the average MSE and correlation (with standard deviations) for both in-sample and out-of-sample data. In Table 2 we can see results consistent with the equity returns experiment: (i) yields the best performance in out-of-sample MSE and correlation. (ii) achieves the best generalization error by having a much smaller gap between training and test metrics.

6.1 Setup of experiments

6.1.1 Equity returns

We use daily historical stock prices and volumes from an emerging market to build our model. Our license agreement prohibits us to redistribute the data so we include only a subset of samples. Full datasets can be purchased by standard vendors such as quandl or algoseek. Our dataset consists of approximately 3,600 stocks between 2011 and 2018.

Universes. We examine two different universes in this market (i) Universe 1 is equivalent to S&P 500. It consists of 800 stocks at any moment. Similar to S&P 500, the list of stocks appeared in universe 1 is updated every 6 months. A total number of 983 stocks have appeared in universe 1 at least once. (ii) Universe 2 consists of all stocks except for illiquid ones. This excludes the smallest 5% stocks in capital and the smallest 5% stocks in trading volume. Standard procedure is used to avoid universe look-ahead and survival bias zhou2014active .

Returns. We use return information to produce both features and responses. Our returns are the “log-transform” of all open-to-open returns zhou2014active . For example, the next 5-day return of stock is , where is the open price for stock on trading day . Note that all non-trading days need to be removed from the time series . Similarly, the past 1-day return is .

Model. We focus on predicting the next 5-day returns for different universes. Let , where is the next 5-day return of stock on day . Our regression model is

| (57) |

The features consist of the past 1-day, past 5-day, and past 10-day returns of all the stocks in the same universe. For example, in Universe 1, the number of responses is . The number of features is . We further optimize the hyperparameters and by using a validation set because our theoretical results are asymptotic ones (with unoptimized constants). Baseline models use the same set of features and the same hyper-parameter tuning procedure.

We use three years of data for training, one year for validation, and one year for testing. The model is re-trained every test year. For example, the first training period is May 1, 2011 to May 1, 2014. The corresponding validation period is from June 1, 2014 to June 1, 2015. We use the validation set to determine the hyperparameters and build the model, and then we use the trained model to forecast returns of equity in the same universe from July 1, 2015 to July 1, 2016. Then the model is retrained by using data in the second training period (May 1, 2012 to May 1, 2015). This workflow repeats. To avoid looking-ahead, there is a gap of one month between training and validation periods, and between validation and test periods.

We use standard approach to translate forecasts into positions grinold2000active ; prigent2007portfolio ; ang2014asset ; zhou2014active . Roughly speaking, the position is proportional to the product of forecasts and a function of average dollar volume. We allow short-selling. We do not consider transaction cost and market impact. We use Newey-West estimator to produce -statistics of our forecasts.

6.1.2 User popularity

We use Twitter dataset to build models for predicting a user’s next 1-day popularity, which is defined as the sum of retweets, quotes, and replies received by the user.

Data collection. We collected 15 months Twitter data from October 01, 2016 to December 31, 2017, using the Twitter streaming API. We tracked the tweets with topics related to politics with keywords “trump”, “clinton”, “kaine”, “pence”, and “election2016”. There are a total of 804 million tweets and 19 million distinct users. User has one interaction if and only if he or she is retweeted/replied/quoted by another user . Due to the huge size, we extract the subset of 2000 users with the most interactions for evaluation.

Model. Our goal is to forecast the popularity of a random subset of 200 users. Let , where and is the popularity of user at time . Our regression model is

| (58) |

Features. For each user, we compute his/her daily popularity for 5 days prior to day . Therefore, the total number of features is .

We remark that there are observations. This setup follows our assumption .

Training and hyper-parameters. We use the period from October 01, 2016 to June 30, 2017 as the training dataset, the period from July 01, 2017 to October 30 as validation dataset to optimize the hyper-parameters, and the rest of the period, from September 10, 2017 to December 31, 2017, is used for the performance evaluation.

7 Conclusion

This paper examines the low-rank regression problem under the high-dimensional setting. We design the first learning algorithm with provable statistical guarantees under a mild condition on the features’ covariance matrix. Our algorithm is simple and computationally more efficient than low rank methods based on optimizing nuclear norms. Our theoretical analysis of the upper bound and lower bound can be of independent interest. Our preliminary experimental results demonstrate the efficacy of our algorithm. The full version explains why our (algorithm) result is unlikely to be known or trivial.

Broader Impact

The main contribution of this work is theoretical. Productionizing downstream applications stated in the paper may need to take six months or more so there is no immediate societal impact from this project.

Acknowledgement

We thank anonymous reviewers for helpful comments and suggestions. Varun Kanade is supported in part by the Alan Turing Institute under the EPSRC grant EP/N510129/1. Yanhua Li was supported in part by NSF grants IIS-1942680 (CAREER), CNS-1952085, CMMI-1831140, and DGE-2021871. Qiong Wu and Zhenming Liu are supported by NSF grants NSF-2008557, NSF-1835821, and NSF-1755769. The authors acknowledge William & Mary Research Computing for providing computational resources and technical support that have contributed to the results reported within this paper.

References

- [1] Anish Agarwal, Devavrat Shah, Dennis Shen, and Dogyoon Song. On robustness of principal component regression. In Advances in Neural Information Processing Systems, pages 9889–9900, 2019.

- [2] Gernot Akemann, Jonit Fischmann, and Pierpaolo Vivo. Universal correlations and power-law tails in financial covariance matrices. Physica A: Statistical Mechanics and its Applications, 389(13):2566–2579, 2010.

- [3] Andrew Ang. Asset management: A systematic approach to factor investing. Oxford University Press, 2014.

- [4] Zhidong Bai and Jack W Silverstein. Spectral analysis of large dimensional random matrices, volume 20. Springer, 2010.

- [5] David Bamman, Jacob Eisenstein, and Tyler Schnoebelen. Gender identity and lexical variation in social media. Journal of Sociolinguistics, 18(2):135–160, 2014.

- [6] Carolina Batis, Michelle A Mendez, Penny Gordon-Larsen, Daniela Sotres-Alvarez, Linda Adair, and Barry Popkin. Using both principal component analysis and reduced rank regression to study dietary patterns and diabetes in chinese adults. Public health nutrition, 19(2):195–203, 2016.

- [7] Jennifer Bender, Remy Briand, Dimitris Melas, and Raman Aylur Subramanian. Foundations of factor investing. Available at SSRN 2543990, 2013.

- [8] Florentina Bunea, Yiyuan She, and Marten H Wegkamp. Optimal selection of reduced rank estimators of high-dimensional matrices. The Annals of Statistics, pages 1282–1309, 2011.

- [9] Emmanuel J Candes et al. The restricted isometry property and its implications for compressed sensing. Comptes rendus mathematique, 346(9-10):589–592, 2008.

- [10] LJ Cao, Kok Seng Chua, WK Chong, HP Lee, and QM Gu. A comparison of pca, kpca and ica for dimensionality reduction in support vector machine. Neurocomputing, 55(1-2):321–336, 2003.

- [11] Kun Chen, Hongbo Dong, and Kung-Sik Chan. Reduced rank regression via adaptive nuclear norm penalization. Biometrika, 100(4):901–920, 2013.

- [12] Luyang Chen, Markus Pelger, and Jason Zhu. Deep learning in asset pricing. Available at SSRN 3350138, 2019.

- [13] Aaron Clauset, Cosma Rohilla Shalizi, and Mark EJ Newman. Power-law distributions in empirical data. SIAM review, 51(4):661–703, 2009.

- [14] Chen Dan, Kristoffer Arnsfelt Hansen, He Jiang, Liwei Wang, and Yuchen Zhou. Low rank approximation of binary matrices: Column subset selection and generalizations. arXiv preprint arXiv:1511.01699, 2015.

- [15] Chandler Davis and William Morton Kahan. The rotation of eigenvectors by a perturbation. iii. SIAM Journal on Numerical Analysis, 7(1):1–46, 1970.

- [16] David Donoho, Matan Gavish, et al. Minimax risk of matrix denoising by singular value thresholding. The Annals of Statistics, 42(6):2413–2440, 2014.

- [17] Fan Fan, Yong Ma, Chang Li, Xiaoguang Mei, Jun Huang, and Jiayi Ma. Hyperspectral image denoising with superpixel segmentation and low-rank representation. Information Sciences, 397:48–68, 2017.

- [18] Jianqing Fan, Yuan Liao, and Han Liu. An overview of the estimation of large covariance and precision matrices. The Econometrics Journal, 19(1):C1–C32, 2016.

- [19] Laura Frank, Franziska Jannasch, Janine Kröger, George Bedu-Addo, Frank Mockenhaupt, Matthias Schulze, and Ina Danquah. A dietary pattern derived by reduced rank regression is associated with type 2 diabetes in an urban ghanaian population. Nutrients, 7(7):5497–5514, 2015.

- [20] Jerome Friedman, Trevor Hastie, and Robert Tibshirani. The elements of statistical learning, volume 1. Springer series in statistics New York, 2001.

- [21] Matan Gavish and David L Donoho. The optimal hard threshold for singular values is 4/sqrt(3). IEEE Transactions on Information Theory, 60(8):5040–5053, 2014.

- [22] Ali Ghodsi. Dimensionality reduction a short tutorial. Department of Statistics and Actuarial Science, Univ. of Waterloo, Ontario, Canada, 37:38, 2006.

- [23] Richard C Grinold and Ronald N Kahn. Active portfolio management. 2000.

- [24] Shihao Gu, Bryan Kelly, and Dacheng Xiu. Empirical asset pricing via machine learning. Technical report, National Bureau of Economic Research, 2018.

- [25] Tosio Kato. Variation of discrete spectra. Communications in Mathematical Physics, 111(3):501–504, 1987.

- [26] Bryan T Kelly, Seth Pruitt, and Yinan Su. Characteristics are covariances: A unified model of risk and return. Journal of Financial Economics, 134(3):501–524, 2019.

- [27] Vladimir Koltchinskii, Karim Lounici, Alexandre B Tsybakov, et al. Nuclear-norm penalization and optimal rates for noisy low-rank matrix completion. The Annals of Statistics, 39(5):2302–2329, 2011.

- [28] Cheng Li, Felix MF Wong, Zhenming Liu, and Varun Kanade. From which world is your graph. In Advances in Neural Information Processing Systems, pages 1468–1478, 2017.

- [29] Zongming Ma and Tingni Sun. Adaptive sparse reduced-rank regression. arXiv, 1403, 2014.

- [30] David JC MacKay. Information theory, inference and learning algorithms. Cambridge university press, 2003.

- [31] Marcelo C Medeiros and Eduardo F Mendes. Estimating high-dimensional time series models. Technical report, Texto para discussão, 2012.

- [32] Ashin Mukherjee and Ji Zhu. Reduced rank ridge regression and its kernel extensions. Statistical analysis and data mining: the ASA data science journal, 4(6):612–622, 2011.

- [33] Sahand Negahban and Martin J Wainwright. Estimation of (near) low-rank matrices with noise and high-dimensional scaling. The Annals of Statistics, pages 1069–1097, 2011.

- [34] Ashadun Nobi, Seong Eun Maeng, Gyeong Gyun Ha, and Jae Woo Lee. Random matrix theory and cross-correlations in global financial indices and local stock market indices. Journal of the Korean Physical Society, 62(4):569–574, 2013.

- [35] Roberto Oliveira et al. Sums of random hermitian matrices and an inequality by rudelson. Electronic Communications in Probability, 15:203–212, 2010.

- [36] Christopher Polk, Samuel Thompson, and Tuomo Vuolteenaho. Cross-sectional forecasts of the equity premium. Journal of Financial Economics, 81(1):101–141, 2006.

- [37] Jean-Luc Prigent. Portfolio optimization and performance analysis. CRC Press, 2007.

- [38] Mehdi Rahim, Bertrand Thirion, and Gaël Varoquaux. Multi-output predictions from neuroimaging: assessing reduced-rank linear models. In 2017 International Workshop on Pattern Recognition in Neuroimaging (PRNI), pages 1–4. IEEE, 2017.

- [39] Anca Ralescu, Mojtaba Kohram, et al. Spectral regression with low-rank approximation for dynamic graph link prediction. IEEE intelligent systems, 26(4):48–53, 2011.

- [40] Pradeep Ravikumar, Martin J Wainwright, John D Lafferty, et al. High-dimensional ising model selection using l1-regularized logistic regression. The Annals of Statistics, 38(3):1287–1319, 2010.

- [41] Mark Rudelson and Roman Vershynin. Non-asymptotic theory of random matrices: extreme singular values. In Proceedings of the International Congress of Mathematicians 2010 (ICM 2010) (In 4 Volumes) Vol. I: Plenary Lectures and Ceremonies Vols. II–IV: Invited Lectures, pages 1576–1602. World Scientific, 2010.

- [42] Robert E Schapire and Yoav Freund. Boosting: Foundations and algorithms. Kybernetes, 2013.

- [43] Shiladitya Sinha, Chris Dyer, Kevin Gimpel, and Noah A Smith. Predicting the nfl using twitter. arXiv preprint arXiv:1310.6998, 2013.

- [44] James H Stock and Mark Watson. Dynamic factor models. Oxford handbook on economic forecasting, 2011.

- [45] James H Stock and Mark W Watson. Forecasting using principal components from a large number of predictors. Journal of the American statistical association, 97(460):1167–1179, 2002.

- [46] James H Stock and Mark W Watson. Implications of dynamic factor models for var analysis. Technical report, National Bureau of Economic Research, 2005.

- [47] Minh Tang, Daniel L Sussman, Carey E Priebe, et al. Universally consistent vertex classification for latent positions graphs. The Annals of Statistics, 41(3):1406–1430, 2013.

- [48] Robert Tibshirani. Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological), 58(1):267–288, 1996.

- [49] Alexandre B Tsybakov. Introduction to nonparametric estimation. Springer Science & Business Media, 2008.

- [50] Thomas Chinwe Urama, Patrick Oseloka Ezepue, and Chimezie Peters Nnanwa. Analysis of cross-correlations in emerging markets using random matrix theory. In International Conference on Computational Mathematics, Computational Geometry & Statistics (CMCGS). Proceedings, page 89. Global Science and Technology Forum, 2017.

- [51] Raja Velu and Gregory C Reinsel. Multivariate reduced-rank regression: theory and applications, volume 136. Springer Science & Business Media, 2013.

- [52] Yun-Jhong Wu, Elizaveta Levina, and Ji Zhu. Generalized linear models with low rank effects for network data. arXiv preprint arXiv:1705.06772, 2017.

- [53] Xinfeng Zhou and Sameer Jain. Active equity management. Self-published, 2014.

- [54] Xiaofeng Zhu, Heung-Il Suk, Heng Huang, and Dinggang Shen. Low-rank graph-regularized structured sparse regression for identifying genetic biomarkers. IEEE transactions on big data, 3(4):405–414, 2017.