Capacity Games with Supply Function Competition

Abstract

This paper studies a setting in which multiple suppliers compete for a buyer’s procurement business. The buyer faces uncertain demand and there is a requirement to reserve capacity in advance of knowing the demand. Each supplier has costs that are two dimensional, with some costs incurred before demand is realized in order to reserve capacity and some costs incurred after demand is realized at the time of delivery. A distinctive feature of our model is that the marginal costs may not be constants, and this naturally leads us to a supply function competition framework in which each supplier offers a schedule of prices and quantities. We treat this problem as an example of a general class of capacity games and show that, when the optimal supply chain profit is submodular, in equilibrium the buyer makes a reservation choice that maximizes the overall supply chain profit, each supplier makes a profit equal to their marginal contribution to the supply chain, and the buyer takes the remaining profit. We further prove that this submodularity property holds under two commonly studied settings: (1) there are only two suppliers; and (2) in the case of more than two suppliers, the marginal two-dimension costs of each supplier are non-decreasing and constant, respectively.

Keywords: capacity game, supply function, option contract, submodularity, Nash equilibrium

1 Introduction

When demand is uncertain, the characteristics of the supply chain and the contract arrangements will determine investment decisions. In capital-intensive industries, such as petrochemical, electronics and semiconductors, manufacturers need to invest heavily in building capacity and the lead times are long (Kleindorfer and Wu, 2003), so that it remains a critical challenge to incentivize and manage capacity investment. When manufacturers are competing against each other and a buying firm may switch to a different manufacturer, the problems are intensified. If the financial risks from investment are carried by the firms who build capacity, it is difficult to find good solutions as there is no certainty on how much capacity will be required in the future (Wu et al., 2005a). The result may be that capacity is only built for the part of the demand that can be more or less guaranteed: this conservative approach will reduce the buyer’s ability to meet customers’ demand. From a supply chain perspective, it is usually preferable for buyers to reserve capacity from suppliers in advance, with a payment made to the suppliers associated with this capacity reservation. Then the buyer also shares the risk that demand is low and not all the purchased capacity is required.

We model capacity reservation in a supply option framework. In the first stage, before knowing the actual demand, a buyer reserves a certain amount of capacity by paying a reservation price. In the second stage, after discovering the actual demand, the buyer asks for supply up to the lesser of the reserved amount and the observed demand. At this stage, the buyer pays an execution price only for the amount of capacity that is used. The underlying assumption of this model is that suppliers have to install capacity, or place orders with their own suppliers, before demand materializes because of the lead times involved.

A distinctive feature of our model is that marginal costs (of capacity and production) may depend on the volume, which is often the case in practical situations. For example, capacity investment often involves a one-off setup cost (Luss, 1982; Van Mieghem, 2003), there may be (dis)economies of scale in production (Haldi and Whitcomb, 1967; Ha et al., 2011), or in cases where a supplier manages a portfolio of facilities with heterogeneous technologies the overall cost is far from being linear (especially in the electricity industry). In our model, each supplier has a total reservation cost (incurred before demand realization), which is an arbitrary increasing function of the capacity reserved, and also a total execution cost (incurred after demand realization), which is an arbitrary increasing function of the amount actually supplied. This framework includes constant marginal costs as a special case, so our model is flexible enough to capture many practical settings in terms of cost modelling. We believe this is an important theoretical advancement as most literature on supply chain contracts assumes constant marginal costs (Cachon, 2003). The linear treatment may help simplify the analysis and develop high-level intuitions especially for competitive models, but may not align with real-world practices.

With constant marginal costs, it is plausible to focus on simple contract forms, but with general cost functions, more sophisticated contract formats may be worthwhile, such as bids which specify a schedule of different prices for different quantities (i.e., a supply function). This type of supply function bid often occurs in practice through the application of some form of quantity discount contract.

In this paper, we consider a supply chain with a single buyer and multiple suppliers, who supply a homogeneous item to the buyer. The suppliers compete by offering price functions for both reservation and execution. Given the suppliers’ bids, the buyer first reserves capacity before knowing the actual demand, and then decides how much capacity to use after observing the demand. The buyer may choose not to enter into a contract with a specific supplier in which case no costs are incurred by that supplier. Competition with function bids fits well with the situation where a buyer does not stipulate the specific bidding format in its Request for Quote (RFQ), so that suppliers can bid in whatever format they like.

We suppose that the buyer faces a random demand, with a known distribution. There are suppliers, and each has a total reservation cost, which is expressed as a general increasing function of the amount reserved, as well as a total execution cost which is a general increasing function of the amount supplied. We model this game in a Stackelberg framework, where the suppliers are leaders and the buyer is a follower. Each supplier has complete information about the buyer’s demand distribution and all supplier costs, but the buyer may not know the suppliers’ costs. This assumption has been widely used in supplier competition models and is appropriate for industries where the operating environments are more transparent and/or the production technologies are more mature such as electricity, electronics and semiconductors (Wu and Kleindorfer, 2005; Martínez-de Albéniz and Simchi-Levi, 2009; Anderson et al., 2017).

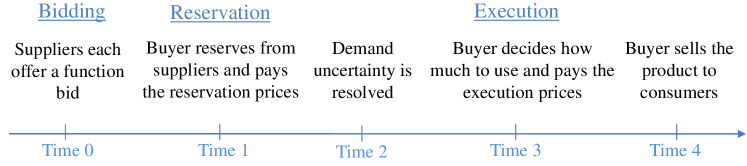

The sequence of events is depicted in Figure 1. First each supplier, with the aim of maximizing their own expected profits, offers a function bid consisting of a (marginal) reservation price function and a (marginal) execution price function to the buyer. Second, prior to knowing the actual demand, the buyer determines how much to reserve from each supplier and pays the reservation price. After demand is observed, the buyer chooses what capacity to use and pays the execution price for the amount of capacity that is used. If the demand exceeds the total amount of reserved capacity, there will be lost sales. Finally, the buyer sells the product to the consumer market at the retail price . We will call this the capacity game with function bids. This game can be considered as a special case of a general capacity game setting, in which a first stage choice by the buyer implies a constraint on the decisions to be made by the buyer at a second stage when demand information becomes known. Thus, our discussion will be carried out for the general capacity game, which in turn provides a theoretical foundation for the capacity game with function bids.

The framework we consider also applies to capacity mechanisms in electricity markets. In this context the buyer and customers are replaced by a set of consumers and a system operator who aims to maximize system welfare. Problems of this form are usually formulated with a value of lost load (VoLL). In the case where demand is stochastic but independent of price, the system operator’s problem, of minimizing the expected cost of procurement less VoLL for demand not met, becomes equivalent to maximizing VoLL times (demand met) minus the cost of procurement, which is the same as the buyer’s problem in our supply chain setting when we set the retail price to be VoLL.

It is not uncommon to have a supply chain where multiple suppliers act as Stackelberg leaders and a buyer must select amongst the available suppliers on the basis of contracts that the suppliers offer. This framework will lead to suppliers setting as high a price as they can while still being chosen. The consequence is that each supplier makes a bid that leads to the buyer being indifferent between choosing or not choosing the supplier. From this it can be shown that the profit available to each supplier is simply its contribution to the overall supply chain profit, i.e., the difference in the supply chain profits when it is chosen and when it is not.

A major contribution of this paper is to study submodularity in this setting. We will demonstrate that a natural sufficient condition for a well-behaved equilibrium is that the supply chain profits are submodular in terms of the set of suppliers available. This property is equivalent to a requirement that the profit available to a supplier cannot increase if a new supplier is added to those available. We are therefore led to considering whether or not the supply chain profits achieved are submodular. This is not always the case, but can be established in commonly studied settings. Specifically, the property holds if either: (i) there are only two suppliers; or (ii) each supplier’s marginal reservation cost is non-decreasing and marginal execution cost is constant.

A second contribution of this paper is to study how suppliers compete with each other by using supply functions rather than scalar prices. In other words, the strategy space of each supplier is extended to a function space, and as a result, the suppliers have more flexibility in their bidding decisions. On the other hand, the buyer can determine how much to reserve from each supplier (i.e., pick any point from a supply function) rather than being restricted to a fixed quantity-payment contract. Our aim is to develop an understanding of the players’ strategic behavior in such a market setting. Previous models have focused on competition problems when suppliers are restricted to a simple strategy space (i.e., scalar decision variables, including prices, quantities, lead times, quality, or specific contract types). To the best of our knowledge, this paper is among the first to study supply function competition in a capacity reservation setting.

We find that given knowledge of the other suppliers’ bids, it is optimal for each supplier to set execution prices at execution costs and make profits only through the buyer’s reservation payment. Our findings also show that, under some reasonable assumptions, there exists a continuum of equilibria in which the suppliers charge costs only for the execution prices but add a margin to the reservation costs. Despite the multiplicity of equilibrium bidding strategies, the equilibrium outcome is essentially unique: in equilibrium the buyer makes a reservation choice that maximizes the overall supply chain profit, each supplier makes a profit that is equal to their marginal contribution to the supply chain, and the buyer takes the remaining profit.

The rest of this paper is organized as follows. After a review of the relevant literature in Section 2, we present our general capacity game model in Section 3, and study the best response and equilibrium strategies for suppliers in Sections 4. Then we show how these results apply to the more specific case we have introduced above in Section 5. We discuss in Section 6 two commonly studied settings and show that the supply chain optimal profit is submodular in a broad class of capacity games with function bids. Finally, we conclude in Section 7. All technical proofs are presented in the appendix.

2 Literature review

Supply options have been extensively studied in the operations management literature (see, e.g., Barnes-Schuster et al., 2002; Burnetas and Ritchken, 2005; Wu et al., 2005b; Fu et al., 2010; Secomandi and Wang, 2012). An initial step is to investigate a buyer’s optimal purchasing decision given a fixed set of supply options (see, e.g., Martínez-de Albéniz and Simchi-Levi, 2005). As an extension of this, several papers examine option contract design problems in a Stackelberg game between a buyer and a supplier with a focus on the interaction between option markets and spot markets (see, e.g., Wu et al., 2002; Pei et al., 2011). Further extensions have been made to consider supplier competition in an option market (Wu and Kleindorfer, 2005; Martínez-de Albéniz and Simchi-Levi, 2009; Anderson et al., 2017). Wu and Kleindorfer (2005) study a commodity procurement problem where an industrial buyer purchases supply options from a small set of suppliers, while having access to an open spot market. No reservation cost at the suppliers is considered, and the buyer’s downward-sloping demand (arising from utilization maximization) is determined by the spot price and the execution prices. Such a demand modelling approach allows the buyer to rank suppliers by using a single price index combining the reservation and execution price of supply options, which leads to a Bertrand type of equilibrium for the suppliers. We study a similar situation but consider suppliers having a two-dimensional cost and a newsvendor type buyer facing uncertain demand.

The closest papers to ours within this literature are Martínez-de Albéniz and Simchi-Levi (2009) (hereafter, “MS”) and Anderson et al. (2017) (hereafter, “ACS”). MS studies a setting where marginal costs are constants and each supplier chooses a reservation price and an execution price for their limitless capacity. They show that there may be efficiency loss in equilibrium, which is up to of the overall supply chain optimal profit. Our paper differs from MS by considering general cost functions and allowing suppliers to submit function bids. By enlarging the strategy space of suppliers, we find a relatively clean and intuitive result as discussed earlier. In particular, when the supply chain optimal profit is submodular, there is no efficiency loss in equilibrium and each supplier makes a profit equal to their marginal contributions. We further show that this condition is not restrictive as it holds under some commonly studied settings. Comparing with MS, we also find that allowing suppliers to offer a function bid makes the buyer worse off, thereby highlighting the significant impact of the strategy space on equilibrium outcomes.

ACS studies a similar problem where each supplier owns a block of capacity with the same size and the buyer must reserve all of a block or none. Our general framework of capacity games covers the model by ACS as a special case since we can recover ACS by restricting the buyer’s capacity choice from each supplier to be either zero or the block size. In this respect, our paper generalizes ACS by studying a situation where the buyer can reserve any amount from each supplier and suppliers can charge different prices for different quantities.

This paper studies a situation where suppliers compete with each other by offering a function bid, and this resembles what is studied in the supply function equilibrium (SFE) literature (Klemperer and Meyer, 1989; Anderson and Philpott, 2002; Anderson and Hu, 2008; Johari and Tsitsiklis, 2011). However, the game type is different. Our model is a Stackelberg game with multiple leaders (i.e., suppliers) and one follower (i.e., buyer), and the buyer strategically responds to the supplier offers. In contrast, the SFE literature focuses on Nash games that aim to study the strategic interaction between multiple firms, and this literature does not involve a profit-maximizing buyer. In other words, we examine the buyer’s optimization problem explicitly; while in the SFE literature, the buyer’s problem is to choose a clearing price to equate the total supply with the demand, and each supplier’s best response is characterized by a differential equation. In addition, our capacity games involve the buyer making a two-stage decision and each supplier submits a two-dimensional bid consisting of a reservation price function and execution price function, which is not considered in the SFE literature.

This work is also related to the multi-unit auction literature. Problems of decentralized resource allocation (Klagnanam and Parkes, 2004) are central to auctions. A subset of this literature examines the efficiency and profit allocation of a given type of auction, for example, share auction (Wilson, 1979), menu auction (Bernheim and Whinston, 1986), split award auction (Anton and Yao, 1989, 1992), discriminatory price auction (Menezes and Monteiro, 1995), and uniform price auction (Bresky, 2013). Those papers generally assume that the total purchase amount of a buyer is exogenously given, while in our model it is endogenously determined by the buyer based on the supplier bids. Furthermore, we study capacity reservation games where the buyer’s capacity reservation problem is a two-stage stochastic program, which is new to this literature.

Finally, the equilibrium profit allocation obtained in this paper is of Vickrey-Clarke-Groves (VCG) style, so it is instructive to discuss the key point of departure from VCG models (Vickrey, 1961; Rothkopf et al., 1990). Those models study profit allocation from a mechanism design perspective: the VCG profit allocation is an outcome that arises from the payment rule. In essence the VCG approach selects bids that maximize system welfare, and pays according to each bidder’s contribution (i.e., the difference between system welfare with and without that bidder). With this setup the equilibrium result is for bidders to bid truthfully and the auction result is efficient. The model we propose uses the same bid selection approach, but pays as bid. It is then an equilibrium (in the case with submodularity) for the bidders to mark up by the exact VCG amounts. We still get an efficient auction result, but without truthful bids. This is a different approach and has some advantages over the usual VCG mechanism. Hobbs et al. (2000) and Rothkopf (2007) amongst others have discussed some of the difficulties of using a VCG auction in practice. Many of these problems are resolved with pay-as-bid prices. For example, in the auction format we discuss, there is not the same incentive for the buyer to encourage bids that will not be accepted with the aim of reducing the payments to the successful bidders. Note that a submodularity condition has also been discussed in the VCG framework by Ausubel and Milgrom (2006), who show that this condition reduces the problems ordinarily associated with VCG. Within the mechanism design literature, several papers study multi-dimensional bidding environments in an electricity context, where the focus is on designing scoring and payment rules that incentivize bidders to truthfully reveal their costs (Bushnell and Oren, 1994; Chao and Wilson, 2002; Schummer and Vohra, 2003).

3 Model setup

The problem we study is an example of a broader class of capacity games, in which the suppliers offer bids, then a buyer selects a capacity amount to buy from each supplier, then depending on the outcome of a random variable (the demand) in the second stage, the choice of amounts to buy is made by the buyer (with amounts constrained by the capacity already bought). The revenue to the buyer is a function of demand and the amounts bought. We are not considering risk aversion, so we can use the expected payoff as the objective for the buyer and the suppliers. Supplier faces costs that are the sum of a capacity cost and an execution cost. We will establish our results in this general framework and then apply this to the model described in the introduction section.

The buyer makes capacity decisions , where capacity is restricted to lie in a set , and hence . We assume that each is compact containing and is specified as part of the capacity game. Typically, is a closed interval or , which corresponds to the case where the buyer either does not use this supplier, or uses the full amount of the supplier.

The capacity payment to be made by the buyer to each supplier can depend on the complete set of capacity decisions , which may occur in practice, for example, when the suppliers have some exclusivity clauses. Note that, we are making our model as general as possible, although in the specific applications of our model considered in Section 5, the capacity payment made to a supplier depends only on the buyer’s choice from that supplier. In the second stage, after demand becomes known, there is a set of amounts (execution quantities) chosen by the buyer, where depends on the observed demand and satisfies constraints imposed by the capacity decisions of the first stage. Thus we have for some set . We require that if then . The case that is most natural is to allow any selection at the second stage that is no more than the capacity purchase at the first stage, so that and . In general, however, we only assume is compact. Then supplier decides on two payment functions and that the buyer will be offered, where is the payment made to supplier when the buyer makes a capacity reservation of , and is the payment made to supplier given execution amounts . In the formulation of the game there may be restrictions on the bids allowed, which we capture by specifying an allowed set of functions , , and restrict the supplier’s choice to and . Since the buyer can decide not to include supplier , in which case no payment is made, the feasible bids have the property that for all , whenever (similarly for ). For maximal generality of our model, we specify only the minimal further restrictions on at the end of this section.

Besides payments made by the buyer to the suppliers, we also have costs and incurred by supplier that may depend on the complete set of capacities purchased and amounts executed. This occurs when competing players can partially collaborate (e.g., they share warehouse facilities or transport links). However, in the capacity game, a supplier’s costs may be independent of other suppliers’ quantities, as in our specific applications considered in Section 5. We assume that these costs are zero if supplier is not used at either stage and hence when , and when .

Finally, we have the expected revenue to the buyer from an external source, which depends on the demand and the execution amounts . Rather than include a restriction that the total execution amounts are no more than the demand (i.e., ), we will assume that this is achieved through setting appropriate values for the revenue function .

Example 1.

We consider an example that illustrates the range of modelling applications for the general capacity game. Consider a buyer facing uncertain demand: with probability and with probability . There are two suppliers with identical cost structures who produce products that are fully substitutable. We take . Each supplier has costs of reservation for an amount of capacity given by with an additional fixed cost of $20 associated with building a transport link. This fixed cost is split between any suppliers who have capacity reserved, so it is $20 if just one supplier is used, and otherwise $10 each. Thus the reservation costs are

where the indicator function if , and otherwise. Execution costs are $1 per unit so that . Customers pay an amount $3 per unit and in addition there are fixed costs at the buyer of for each product that apply only if that product is supplied. Thus, . We have the standard form for so there is a restriction that .

Since execution amounts will depend on , we can write a policy for the buyer as , where and is a function from the demand set to , taking the value at . For simplicity, we will write for hereafter. The total expected buyer profit with this policy choice is

given a set of supplier bids . The buyer’s problem is to maximize her expected profit by choosing an optimal reservation choice and a set of execution amounts for each possible demand , i.e., to solve

| (1) |

With these bids and buyer choice , supplier has a profit of

| (2) |

The supply chain profit is

| (3) |

which is independent of the bids made.

We write for the support of a vector . We use , , to denote the optimal supply chain profit when the capacity reserved is restricted to be zero outside the set . Thus

| (4) |

Similarly, given a set of supplier bids , we use , , to denote the optimal buyer profit when the capacity reserved is restricted to be zero outside the set . Thus

The maximizations above are taken over (a vector) and (a function). To ensure that the maxima exist and are attained, we make the following (additional) assumptions: (a) the set-valued function is upper hemi-continuous; (b) the revenue function is upper semi-continuous in both arguments; and (c) the set of possible bids is such that are lower semi-continuous.

4 Best response and equilibrium behavior

We now look at each supplier’s best response problem. As a Stackelberg leader, each supplier is able to anticipate the buyer’s reservation choice provided that the competitors’ bids are observed. Since the buyer’s optimization problem is embedded in the suppliers’ best responses, we need to specify the buyer’s choice when there are different options with the same expected value to the buyer. We say that supplier has preferred status when a solution with is chosen by the buyer even if other options give the same value.

Theorem 1 (Best Response).

For any fixed supplier , we have the following statements for the supplier’s best response:

-

(a)

Given bids , the profit for supplier is no more than

where .

-

(b)

If and supplier has preferred status, then the profit is achieved by the offer defined by:

-

(c)

If , then for any , an offer of will achieve within of the maximum possible supplier profit, where .

Theorem 1 shows the maximum profit for a supplier , which is the increase in profit available to the buyer from including the bids of supplier when these are made at cost. Moreover, when optimizing for the supplier, it is sufficient to consider supplier bids that are at cost for the execution component and make money only from the reservation payments. However, we should note that the expected profit to the supplier is unaffected by parts of the function bids that are never selected by the buyer whatever demand occurs. The consequence is that there are a continuum of other best response function offers available.

Now let us consider the equilibrium strategies for suppliers. In general, the optimal solution to the buyer’s maximization problem (1) is not unique at an equilibrium as we shall show later. Since our focus is on supplier competition, and each supplier’s payoff depends on the buyer’s reservation choice, we need a tie-breaking rule to pin down the buyer’s optimal choice in case of multiple solutions. The suppliers have an interest in raising prices to the point where the buyer is about to drop them from consideration. Therefore, a tie-breaking assumption is critical, otherwise, we can have a difficulty in defining optimal behavior for the suppliers, as a type of -optimality could occur when a supplier sets his price just below a benchmark value at which the buyer no longer wishes to select the supplier. Consequently, we make the following assumption.

Assumption 1 (Tie-Breaking Rule).

In case of multiple optimal solutions, the buyer will select the one that gives the largest supply chain profit.

This assumption is in line with that for the classic Bertrand competition model, where the firm with the lowest cost wins when all the firms charge the same price. The rationale of this assumption is as follows: if the buyer selects an alternative that gives a lower supply chain profit, then keeping the other suppliers’ bids unchanged, any supplier in the supply chain optimal set (with respect to the buyer’s equally good choices) will have incentives to raise his price by an amount that is smaller than the difference between the supply chain optimal profit and the one corresponding to the buyer’s choice. This would make both the buyer and the supplier better off.

We need to rule out cases where two suppliers are identical and the optimal supply chain solution can use either one or the other, so we introduce the following assumption.

Assumption 2 (Uniqueness of Support).

All the supply chain optimal capacity choices use the same set of suppliers.

We will write to denote an optimal solution to the supply chain optimization problem (4). So Assumption 2 amounts to a statement that the support of the supply chain optimal capacity choices is unique. Let us identify the suppliers who make a contribution to the optimal supply chain profit by defining

It is easy to observe that, under Assumption 2, we have

| (5) |

To establish an equilibrium, we will need to make use of submodularity of the optimal supply chain profit as a set function of the suppliers available, where the submodularity property states that, for any and ,

| (6) |

Inequalities (6) are satisfied for a large class of problems of interest, as we shall discuss in detail in Section 6. It is convenient to make this property an assumption:

Assumption 3 (Submodularity).

The supply chain optimal profit is submodular as a function of the set of available suppliers.

This submodularity assumption implies two properties of the set function , which are established in the following two lemmas.

Lemma 1.

Under the Submodularity Assumption, the following inequality holds for any :

| (7) |

The following result shows that all the suppliers in will still be included in the optimal supply chain choice when supplier is unavailable.

Lemma 2.

Under the Submodularity Assumption, for any , we have .

We will consider the possibility of varying the offers that a supplier makes in a way that does not change the supply chain optimal solutions. We say that a set of functions from to is consistent with the cost functions if adding to the cost does not change the optimal solution or the optimal value, i.e., for every ,

| (8) |

and the maximization is attained at . It is easy to see that this is equivalent to the conditions of (a) and (b) if and for all , then

| (9) |

Note that when is zero for any , then it is trivially consistent with the costs. Now we are ready to characterize the equilibrium that occurs when is submodular as a function of .

Theorem 2 (Nash Equilibrium).

We can see immediately from Theorem 2 that the following set of bids is a Nash equilibrium (by setting all ):

and when .

Several points about this theorem are worth mentioning. First, the profit allocation in equilibrium is a VCG result. However, this is not from a mechanism design that sets prices paid in a particular way, but arises as an equilibrium from our pay-as-bid capacity game. It is straightforward that each supplier makes a nonnegative profit. Suppliers in each make a strictly positive profit while the other suppliers each make zero profits. On the buyer’s side, the profit is nonnegative, which is a direct result of the submodularity property of and can also be implied by the fact that the buyer will not purchase from any supplier should it make a negative profit.

The profit allocation is primarily driven by the level of competition between suppliers. In the extreme case where there is a perfectly competitive market, then each supplier’s contribution is zero, since in an individual supplier’s absence another supplier will step in with no overall reduction in supply chain profits. Thus the entire supply chain profit will go to the buyer.

Another property of the equilibrium is that the buyer’s profit will remain the same if any single supplier is dropped from the set of available suppliers. We establish this in the proof of Theorem 2 (see equation (A-3)). The intuition is that if the buyer makes a lower profit when any supplier is removed, then this supplier would have an incentive to increase its bid by a positive amount while still ensuring it is chosen by the buyer.

Finally, in equilibrium the buyer makes a choice that maximizes the supply chain profit, i.e., the supply chain is coordinated in equilibrium. It is instructive to relate our findings with those of the supply chain coordination literature (Cachon, 2003). In general, this literature focuses on designing sophisticated contracts (e.g., revenue sharing or buy back) to achieve the chain optimal profit in a dyadic supply chain. In contrast, we have a different supply chain structure (i.e., many to one), and the supply chain optimality arises as a result of supplier competition (rather than by way of design).

Example 1 (continued).

Let us consider again the capacity game given in Example 1. If just one of the suppliers, say , is available, then it can be shown that the optimal reservation amount for the supply chain as a whole is and the supply chain profit is . In this case, the amount supplied is less than the demand in the high demand case. On the other hand, if both suppliers are available, then it is optimal (to the supply chain) to reserve from each, so . In this case no demand is lost, but the buyer finds it worthwhile to purchase from only one of the suppliers in the event that demand is low (thus saving the additional $20 cost in this case). The supply chain profit is . Thus the supply chain profits are submodular and there is an equilibrium where each supplier offers and for and otherwise, where .

5 Application to capacity games with function bids

We will apply our results for the general capacity game to the specific case we described in the introduction section. The buyer faces a random demand , which follows a probability distribution with density over where . For each unit of items sold, the buyer collects a revenue . Supplier has a reservation cost, which is expressed as a general increasing function of the amount reserved, with a marginal reservation cost for an amount given by (so that total reservation costs are given by ). In addition supplier has an execution cost which is a general increasing function of the amount supplied, with a marginal execution cost of . We have switched to lower case letters here as an indication that these are marginal costs rather than the total costs as occur in the general capacity game. Note that and could be constants. Suppliers each maximize their own expected profits by offering a function bid consisting of a (marginal) reservation price function and a (marginal) execution price function for . Without loss of generality, we assume since the buyer will never reserve more than units. In addition, if a supplier does not want to offer that much, he may simply set a very high price for the quantities beyond the desired amount so that the buyer will never choose to reserve more than the supplier wishes to offer.

Suppose the bids offered by suppliers are , where the functions and are defined on and may be constants. The buyer makes a reservation decision in the first stage and makes an execution decision in the second stage. Since the reservation payment becomes sunk at the time when the buyer makes the execution decision, with any realized demand, the buyer simply chooses the cheapest way to meet the demand based on execution prices up to the amount reserved from each supplier. If prices are continuous and less than , then it is not hard to see that the buyer will meet the demand through choosing amounts from supplier where and the prices are all equal so that we may write , , except where is the reserved capacity for , in which case . However in the general case, when prices can decrease, there may be more than one solution having these properties even with continuous prices. In this case the buyer will select the solution with the lowest total payment.

To avoid these complications and allow us to develop explicit expressions for and , we make the following simplifying assumption.

Assumption 4.

The execution price function is non-decreasing for every .

In order to put this problem into the general form of a capacity game, we need to switch from marginal costs to the full costs given by their integrals. Also we note that for the capacity game with function bids, , , and only have dependence on and and not on the full vectors and (so that we need to capture the restriction that bids and are of this form through the specification of the sets ). Thus by setting , , , , , we obtain the problem in the required form.

For the capacity game with function bids we can write the vector of second stage choices explicitly in terms of by recognising that the optimal choice for the buyer will use the low cost suppliers first. As we will demonstrate below, this allows an explicit expression for

where and we write for the th component of . Similarly we define . Let

| (10) |

Then is the amount purchased from supplier if an amount is purchased from supplier . When is strictly increasing and continuous, then . In the special case where marginal execution costs are constant (i.e., for all where is a constant), we have if , and if .

Let denote the vector of reservation choices from suppliers other than . We now write the cumulative amount of capacity with execution prices less than as follows,

| (11) |

where is defined in (10), the term indicates the dispatched amount from supplier , and the second term represents the dispatched amount from suppliers other than . If the buyer chooses optimally then this is the total amount that the buyer purchases conditional on her purchasing amount from supplier . Hence with optimal buyer choices, the amount purchased from supplier is greater than if and only if the demand is greater than .

Thus, with the reservation choice , the buyer’s optimal expected profit is

| (12) |

where , is given in (11) and . We know that represents the probability that the buyer will use the th unit of the reserved capacity from supplier , and thus each term within the summation gives the buyer’s profit of reserving from supplier . Similarly for the supply chain as a whole we define

| (13) |

and we have

| (14) |

Now we apply Theorem 1 to get the following corollary in this case.

Corollary 1.

Given bids of the other suppliers, if supplier has preferred status, then it is optimal for supplier to set for and choose the function such that

where and provided is chosen in such a way that the optimal buyer choice is . An optimal choice for supplier is to choose for all and in addition charge a fixed amount of for any non-zero amount reserved. In the case where supplier does not have preferred status, then it is possible for supplier to achieve within of the best profit by choosing the same bid of and a bid of that is reduced by .

This result shows that for the capacity game with function bids there is an optimal solution with for the supplier ’s best response problem, but there will be multiple possible solutions for such that the buyer’s optimal choice is and the supplier makes a profit of (which will imply that the buyer makes the same profit as ). In all of these solutions, the optimal buyer choice is , which maximizes the buyer’s profit when supplier charges only his costs.

For the capacity game with function bids we also have the following immediate corollary from Theorem 2.

Corollary 2 (Nash equilibrium with a lump sum payment).

One property of the equilibrium involving a lump sum payment is that it cannot be represented simply by defining marginal prices for capacity: to do so would require an infinite price for the first of capacity. However, we can use the functions occurring in Theorem 2 to construct an equilibrium solution with finite marginal costs. This is done by adjusting the capacity offer from the lump sum bid by smoothing out the beginning of the offer. We will make use of power functions to do this.

Proposition 1 (Nash equilibrium with power functions).

This construction involves adding the margin to the reservation costs, which is a decreasing function of . Choosing a high value for will imply that decreases more steeply at the beginning and becomes flatter at the end of this interval.

From Proposition 1, we see that there is a continuum of Nash equilibria with power functions, each associated with a possible set of values. We can show that when approaches positive infinity, the power function bid reduces to the lump sum bid. Thus, Corollary 2 can be considered as a limiting example of Proposition 1. Moreover, one may easily construct an equilibrium where some suppliers use lump sum bids (with infinitely large values) while others use power function bids. Despite the multiplicity of equilibrium bidding strategies, all these equilibria lead to the same profit allocation and thus the equilibrium outcome characterized in Proposition 1 is essentially unique.

Comparison with MS

As discussed earlier, existing models have focused on the case where the marginal costs are constant. As we will show in Section 6, the supply chain optimal profit is submodular for this special case, and hence the equilibria characterized in Corollary 2 and Proposition 1 apply. It is interesting to draw a parallel between our model and the existing ones for this case. To this end, we draw on an example from MS to demonstrate the difference in equilibrium outcomes.

Example 2 (Example 1 in MS).

The buyer’s demand is uniformly distributed over , so for . There are two suppliers and their marginal costs are and . The retail price is . We now examine the supply chain optimal problems.

If the buyer reserves from two suppliers, the supply chain problem is:

The optimal solution is . The supply chain optimal profit is .

If the buyer chooses supplier only, the supply chain problem is:

The optimal solution is and the supply chain optimal profit is .

If the buyer chooses supplier only, the supply chain problem is:

The optimal solution is and the supply chain optimal profit is .

If suppliers are restricted to each offering a pair of reservation price and execution price, in equilibrium these two suppliers bid infinitesimally close to each other. MS show that the following is a continuum of -equilibria, which are parameterized with :

In equilibria, the buyer’s reservation choice is

The profit split amongst players is given by

| (15) |

and the supply chain profit is given by

Note that all the above equilibria are inefficient (i.e., not supply chain optimal) except the one with . At this efficient equilibrium, each supplier offers a bid which is identical to the supplier ’s cost. The supplier ’s profit is , the supplier ’s profit is , and the buyer’s profit equals .

We now demonstrate that the above strategies do not form an equilibrium if we allow suppliers to offer function bids. Suppose supplier chooses the proposed bid , and we now examine supplier ’s best response in choosing a function bid.

First, if supplier is the sole supplier, the buyer’s reserved amount will be the sum of the two components of , and the buyer’s profit is equal to . Therefore, we have

Second, we show that the following strategy for supplier improves his profit: setting prices to be costs and charging a lump-sum payment of . Given this offer (and the supplier ’s offer ), we can show that the solution for the buyer’s problem is

and the buyer’s profit from choosing is equal to . Also if the buyer purchases from only supplier , the buyer makes a profit of as well. According to the tie-breaking rule, the buyer will select . Then supplier 2’s profit becomes

which is strictly greater than for any . This shows that the equilibria in MS do not hold if we allow suppliers to offer a function bid.

Under our model setup, the problem is well behaved and there is an equilibrium with lump-sum payments (and there is also an equilibrium with power functions). The following bids form a Nash equilibrium (where and are lump sum payments):

At this equilibria, the buyer’s optimal reservation choice is . The profit split amongst players is given by

| (16) |

In this equilibria, each supplier’s profit equals his contribution to the supply chain system and the buyer takes the remaining profit. Moreover, the reservation choice by the buyer is supply chain optimal (in distinction to the case with constant prices).

The key message of Example 2 is that imposing the restriction that each supplier submits a pair of reservation price and an execution price rather than a function bid leads to a higher buyer profit. On the other hand, the suppliers are better off if they submit function bids. This can be easily seen by comparing the profit splits at (15) and (16).

Comparison with ACS

In our setting, each supplier offers a function bid with a marginal reservation price function and a marginal execution price function, and the buyer has the freedom to reserve whatever amount she likes. This setting resembles the two extensions to the setting with blocks of capacity discussed in Anderson et al. (2017). The two extensions they discussed were:

(a) Partial Reservation, in which the buyer is not restricted to reserving a whole block. Each supplier owns a single block and the blocks can be of different sizes. Every supplier chooses an execution price and a reservation price that apply to all elements of his block.

(b) Multiple Blocks with Common Owner, in which each supplier owns multiple unit-blocks and can choose different prices for different unit blocks. The buyer can freely choose among the offered blocks.

In both extensions, the authors demonstrate that one of their key results in the baseline model, for supplier ’s best response, does not hold. In contrast, we show that the result holds in our setting as shown in Corollary 1.

The key differences are as follows. In the case (a) of partial reservation, the buyer can freely reserve any amount as in our setting. However, suppliers are restricted to offering just two scalar prices rather than general function bids. In the case (b) of multiple blocks with common owner, each supplier can choose different prices for different blocks of capacity as in our setting. However, the buyer can freely choose any of the blocks, whereas in our function bidding setting, the buyer does not have as much flexibility, because the buyer will need to accept the prices for the earlier blocks in order to enjoy the prices for the next blocks. These differences in results highlight the importance of each player’s choice flexibility on the equilibrium outcomes.

6 Discussion of submodularity assumption

In this section we examine two commonly studied settings in supply chains: (a) there are only two suppliers competing for the buyer’s procurement business, and (b) there are more than two suppliers and the marginal execution costs are constants. In each case we are interested in establishing conditions that will ensure submodularity of .

6.1 Case with two suppliers

When there are only two suppliers (denoted by and ) we can find conditions that are enough to ensure that submodularity occurs, and it turns out that in the special case of the capacity game with function bids submodularity will hold without any further restrictions.

Proposition 2 (Subadditivity).

If is subadditive in and the cost functions are defined separately on each component, so is determined by the -th component of , and is determined by the -th component of , then is submodular in . In the case of the capacity game with function bids, these conditions will hold.

6.2 Case with constant marginal execution costs

In the case of more than two suppliers, the submodularity of supply chain profit may not hold in general, as we show in Example 4 below. The following theorem identifies some sufficient conditions for the submodularity property and these conditions are satisfied for a large class of the capacity games with function bids. The notion of laminar convexity stated in the theorem is defined in the Appendix.

Theorem 3 (Submodularity).

Let and for . If is laminar concave in and each cost function () is a convex function of (only) the -th component of , then is submodular in . In the case of the capacity game with function bids, these conditions are satisfied if for each supplier the marginal execution cost is constant and the marginal reservation cost is non-decreasing.

The complexity of the analysis arises from the fact that the supply chain profit function cannot be easily decomposed into components related to individual suppliers. The profit made from supplier is related to the capacity reservations from all the suppliers with lower execution prices.

Theorem 3 implies that, in settings considered by the existing studies where the marginal costs are constant, the supply chain optimal profit is submodular. We use the following example to illustrate this point.

Example 3.

Suppose the buyer demand follows a uniform distribution over . There are three suppliers whose costs are: ; ; and . The retail price is . We know from Theorem 3 that the problem is submodular, and we can carry out the detailed calculations to find the supply chain optimal solutions for different sets of available suppliers. One way to do these calculations is to use the screening curve approach that is common in calculation of optimal generation mix in electricity markets (see Green, 2005). We summarize the optimal reservation choices and profits in Table 1.

| Available Suppliers | ||||

|---|---|---|---|---|

Using the results in the table, we can easily check the submodularity of . We can now construct an equilibrium set of offers where the suppliers offer at cost and in addition require a lump sum reservation payment of , which then becomes the supplier profit. Here these amounts are for supplier 1, for supplier 2, and for supplier 3. In this equilibrium the buyer receives the remainder of the total supply chain profit: .

The submodularity property may not hold when suppliers have decreasing marginal costs as we demonstrate with the following example.

Example 4.

Suppose the demand is fixed with and the retail price is . There are three suppliers with . Supplier and supplier have the same costs with , for (and an infinite cost for any larger amount). Supplier ’s costs are and for . So both supplier and supplier have the capacity of and supplier ’s capacity is .

We now look at the supply chain optimal problems. If all the three suppliers are available, the buyer will choose units from each of supplier and supplier . The supply chain optimal profit is . If only suppliers and (or ) are available, the buyer will choose units from each of and (or ). The supply chain optimal profit is . If supplier is the sole supplier, the buyer will choose units from supplier and the supply chain optimal profit is . Therefore, we have which contradicts the submodularity property.

We can also show that the proposed equilibrium structure will not apply in this case. If each of suppliers 1 and 2 asks for a lump-sum payment of , and the buyer makes the supply chain optimal choice of selecting these two suppliers, then the buyer profit is . However, this is less than the profit available to the buyer from selecting supplier 3 alone, which gives the buyer as profit. So this is not an equilibrium. We can check that an equilibrium exists where both suppliers 1 and 2 ask for a lump-sum payment of , and the buyer chooses both of these offers.

7 Discussion and conclusions

In this paper, we have developed a general framework to study a broad class of capacity games. This framework allows us to examine supplier competition in an option market where suppliers’ costs may be nonlinear. In this setting, suppliers each submit a function bid consisting of a reservation price function and an execution price function. The buyer decides how much capacity to reserve from each supplier before knowing the actual demand.

When the competitors’ bids are observed, we have shown that an optimal strategy for each supplier is to set the execution price to be the execution cost and add a margin on the reservation cost. This implies that suppliers make profits only from the buyer’s reservation payments. This result does not hold in the case of bids of constant marginal costs (considered by MS).

We have also shown that, under the assumption that the supply chain optimal profit is submodular in the set of available suppliers, there is a class of equilibria in which the buyer’s reservation choice is first best, each supplier’s profit equals his marginal contribution to the supply chain and the buyer takes the remaining profit. The implication is that by allowing suppliers to compete using function bids, the supply chain is coordinated.

To demonstrate the generality of the submodularity assumption, we have shown that the supply chain optimal profit is indeed submodular when each supplier’s marginal execution cost is constant, a setting that has been studied extensively in the existing literature, or when there are only two suppliers.

From an electricity market perspective, the profits for the buyer correspond to the overall consumer welfare. In this context the capacity mechanism we have described combines the capacity auction and the market for energy into a single pay-as-bid auction, rather than having separate uniform price auctions. This achieves an efficient outcome at equilibrium, even in the case where generators can exercise market power. In the special case of a competitive environment when no single generator has a significant impact on overall system welfare when removed, we have found that each generator bids at cost and we retain the property of an efficient set of capacity and generation choices. The result we obtain on best response is interesting from the perspective of electricity capacity mechanisms since it demonstrates that when generators are required to specify their energy bids in advance with pay-as-bid in the spot, then there is no incentive to use market power in the energy component of the bids, with profits being made entirely from the capacity payments. This result applies without an assumption of monotone prices and allows quite general dispatch mechanisms. This has relevance to the issues of uplift payments that occur in US wholesale markets because of no-load and start-up costs (see, for example, Hogan, 2014).

This paper can be extended in several directions. First we assume, as in other supplier competition models, that supplier costs are known to the other suppliers. This assumption fits some settings better than others. For example, in the electricity market, generators tend to know each other’s generation technologies; thus it is prudent to assume complete cost information. However, in other settings a model that considers cost uncertainties may be more appropriate; see supply function equilibrium models with private information (Vives, 2011). In addition, our model focuses on the contract market only, and incorporation of a spot market would be another interesting direction. Our equilibrium analysis builds on the submodularity condition. Even though in Example 4 we demonstrate that, when the submodularity property fails, the VCG strategies are not a Nash equilibrium, it would be interesting to investigate further what the equilibrium looks like when the supply chain optimal profit is not submodular. Finally, we should note that our assumption is that the random demand is exogenous. An important extension that we do not consider is the case where the buyer can influence demand through setting a price.

References

- Anderson et al. (2017) Anderson, E. J., Chen, B., and Shao, L. (2017). Supplier competition with option contracts for discrete blocks of capacity. Operations Research, 65(4):952–967.

- Anderson and Hu (2008) Anderson, E. J. and Hu, X. (2008). Finding supply function equilibria with asymmetric firms. Operations Research, 56(3):697–711.

- Anderson and Philpott (2002) Anderson, E. J. and Philpott, A. B. (2002). Optimal offer construction in electricity markets. Mathematics of Operations Research, 27(1):82–100.

- Anton and Yao (1989) Anton, J. J. and Yao, D. A. (1989). Split awards, procurement, and innovation. The RAND Journal of Economics, 20(4):538–552.

- Anton and Yao (1992) Anton, J. J. and Yao, D. A. (1992). Coordination in split award auctions. The Quarterly Journal of Economics, 107(2):681–707.

- Ausubel and Milgrom (2006) Ausubel, L. and Milgrom, P. (2006). The lovely but lonely Vickrey auction. Combinatorial Auctions, 17:22–26.

- Barnes-Schuster et al. (2002) Barnes-Schuster, D., Yehuda, B., and Anupindi, R. (2002). Coordination and flexibility in supply contracts with options. Manufacturing & Service Operations Management, 4(3):171–207.

- Bernheim and Whinston (1986) Bernheim, B. D. and Whinston, M. D. (1986). Menu auctions, resource allocation, and economic influence. The Quarterly Journal of Economics, 101(1):1–32.

- Bresky (2013) Bresky, M. (2013). Revenue and efficiency in multi-unit uniform-price auctions. Games and Economic Behavior, 82:205–217.

- Burnetas and Ritchken (2005) Burnetas, A. and Ritchken, P. (2005). Option pricing with downward-sloping demand curves: The case of supply chain options. Management Science, 51(4):566–580.

- Bushnell and Oren (1994) Bushnell, J. and Oren, S. (1994). Bidder cost revelation in electric power auctions. Journal of regulatory economics, 6(1):5–26.

- Cachon (2003) Cachon, G. P. (2003). Supply chain coordination with contracts. In Graves, S. C. and de Kok, A. G., editors, Handbooks in operations research and management science: Supply chain management, chapter 7, pages 229–339. North Holland, Amsterdam, The Netherlands.

- Chao and Wilson (2002) Chao, H. and Wilson, R. (2002). Multi-dimensional procurement auctions for power reserves: Robust incentive-compatible scoring and settlement rules. Journal of Regulatory Economics, 22(2):161–183.

- Fu et al. (2010) Fu, Q., Lee, C.-Y., and Teo, C.-P. (2010). Procurement management using option contracts: Random spot price and the portfolio effect. IIE Transactions, 42(11):793–811.

- Green (2005) Green, R. (2005). Electricity and markets. Oxford Review of Economic Policy, 21(1):67–87.

- Ha et al. (2011) Ha, A. Y., Tong, S., and Zhang, H. (2011). Sharing demand information in competing supply chains with production diseconomies. Management Science, 57(3):566–581.

- Haldi and Whitcomb (1967) Haldi, J. and Whitcomb, D. (1967). Economies of scale in industrial plants: Part 1. Journal of Political Economy, 75(4):373–385.

- Hobbs et al. (2000) Hobbs, B. F., Rothkopf, M. H., Hyde, L. C., and O’Neill, R. P. (2000). Evaluation of a truthful revelation auction in the context of energy markets with nonconcave benefits. Journal of Regulatory Economics, 18(1):5–32.

- Hogan (2014) Hogan, W. (2014). Electricity market design and efficient pricing: Applications for New England and beyond. The Electricity Journal, 27(7):23–49.

- Johari and Tsitsiklis (2011) Johari, R. and Tsitsiklis, J. N. (2011). Parameterized supply function bidding: Equilibrium and efficiency. Operations Research, 59(5):1079–1089.

- Klagnanam and Parkes (2004) Klagnanam, J. and Parkes, D. C. (2004). Auctions, bidding and exchange design. In Simchi-Levi, D., Wu, S. D., and Shen, Z. M., editors, Handbook of Quantitative Supply Chain Analysis: Modeling in the E-Business Era, chapter 5, pages 143–212. Springer, Boston, MA., USA.

- Kleindorfer and Wu (2003) Kleindorfer, P. R. and Wu, D. J. (2003). Integrating long- and short-term contracting via business-to-business exchanges for capital-intensive industries. Management Science, 49(11):1597–1615.

- Klemperer and Meyer (1989) Klemperer, P. D. and Meyer, M. A. (1989). Supply function equilibria in oligopoly under uncertainty. Econometrica, 57(6):1243–77.

- Luss (1982) Luss, H. (1982). Operations research and capacity expansion problems: A survey. Operations Research, 30:907–947.

- Martínez-de Albéniz and Simchi-Levi (2005) Martínez-de Albéniz, V. and Simchi-Levi, D. (2005). A portfolio approach to procurement contracts. Production and Operations Management, 14(1):90–114.

- Martínez-de Albéniz and Simchi-Levi (2009) Martínez-de Albéniz, V. and Simchi-Levi, D. (2009). Competition in the supply option market. Operations Research, 57(5):1082–1097.

- Menezes and Monteiro (1995) Menezes, F. M. and Monteiro, P. K. (1995). Existence of equilibrium in a discriminatory price auction. Mathematical Social Sciences, 30(3):285–292.

- Murota (2003) Murota, K. (2003). Discrete Convex Analysis. SIAM.

- Murota (2009) Murota, K. (2009). Recent developments in discrete convex analysis. In Cook, W., Lovász, L., and Vygen, J., editors, Research Trends in Combinatorial Optimization, chapter 11, pages 219–260. Springer Berlin Heidelberg.

- Murota and Shioura (2004) Murota, K. and Shioura, A. (2004). Conjugacy relationship between m-convex and l-convex functions in continuous variables. Mathematical Programming, 101(3):415–433.

- Pei et al. (2011) Pei, P. P.-E., Simchi-Levi, D., and Tunca, T. I. (2011). Sourcing flexibility, spot trading, and procurement contract structure. Operations Research, 59(3):578–601.

- Rothkopf (2007) Rothkopf, M. (2007). Thirteen reasons why the Vickrey-Clarke-Groves process is not practical. Operations Research, 55(2):191–197.

- Rothkopf et al. (1990) Rothkopf, M., Teisberg, T., and Kahn, E. (1990). Why are Vickrey auctions rare? Journal of Political Economy, 98:94–109.

- Schummer and Vohra (2003) Schummer, J. and Vohra, R. (2003). Auctions for procuring options. Operations Research, 51(1):41–51.

- Secomandi and Wang (2012) Secomandi, N. and Wang, M. X. (2012). A computational approach to the real option management of network contracts for natural gas pipeline transport capacity. Manufacturing & Service Operations Management, 14(3):441–454.

- Van Mieghem (2003) Van Mieghem, J. A. (2003). Commissioned paper: Capacity management, investment, and hedging: Review and recent developments. Manufacturing and Service Operations Management, 5(4):269–302.

- Vickrey (1961) Vickrey, W. (1961). Counterspeculation, auctions, and competitive sealed tenders. Journal of Finance, 16:8–37.

- Vives (2011) Vives, X. (2011). Strategic supply function competition with private information. Econometrica, 79(6):1919–1966.

- Wilson (1979) Wilson, R. (1979). Auctions of shares. The Quarterly Journal of Economics, 93(4):675–689.

- Wu et al. (2005a) Wu, D., Erkoc, M., and Karabuk, S. (2005a). Managing capacity in the high-tech industry: A review of literature. The Engineering Economist, 50(2):125–158.

- Wu and Kleindorfer (2005) Wu, D. J. and Kleindorfer, P. R. (2005). Competitive options, supply contracting, and electronic markets. Management Science, 51(3):452–466.

- Wu et al. (2005b) Wu, D. J., Kleindorfer, P. R., and Sun, Y. (2005b). Optimal capacity expansion in the presence of capacity options. Decision Support Systems, 40(3-4):553–561.

- Wu et al. (2002) Wu, D. J., Kleindorfer, P. R., and Zhang, J. E. (2002). Optimal bidding and contracting strategies for capital-intensive goods. European Journal of Operational Research, 137(3):657–676.

Appendix

In this section, we prove the results derived in this paper and also give some basic definitions from Murota (2003) for Section 6.

A.1 Some definitions

The set of real numbers is denoted by , and and . The set of integers is denoted by , and and . We use to denote either or . Denote for any positive number . The characteristic vector of is denoted by . For , we write for , which is the th unit vector, and (zero vector).

-convexity

For a function : , the set

is called the effective domain of . For a vector , define the positive and negative supports of as

A function : is said -convex if for any and any , there exists such that the following exchange property is satisfied:

Similarly, a function : is said -convex if for any and any , there exist and such that

for all with . A function : is said -concave if is -convex.

Laminar convexity

A non-empty set is called a laminar family if for any , we have , or , or . A function : is said laminar convex if it can be represented as

where are univariate convex functions, is a laminar family, and . A function : is said laminar concave if is laminar convex.

A.2 Proof of Theorem 1

(a) We consider any feasible offer from supplier , giving a set of bids

The buyer can obtain a profit of through restricting consideration to choices with (which also implies ), and so we have a lower bound on buyer profit:

| (A-1) |

Taking as an optimal choice by the buyer given bids , we have

Hence

Using and (A-1), with a complete set of bids , we can calculate the profit for supplier as follows:

as required.

(b) Since , we know that , which implies that the optimal choice for the buyer given bids has , otherwise these two would be the same. We need to show that when the offer of is made the buyer will choose supplier (i.e., have ), which will then automatically give a profit of for supplier from (2). We will show that is optimal for the buyer given bids

and this suffices since is preferred. Now by definition

Now

since . Now consider an arbitrary choice for the buyer with . This has

and, moreover, any choice with has

Thus we have shown the optimality we needed.

(c) In this case with the bid the profit for supplier is provided . Given this offer, the buyer by choosing , defined in part (b), will achieve a profit of , which is therefore greater than any buyer profit available when . Hence the buyer’s optimal choice must have and this completes the proof.

A.3 Proof of Lemma 1

We prove the lemma by induction. It is trivial when , so we begin with , and we suppose that . From (6), we obtain

which can be rearranged to obtain the result required. Suppose (7) holds for any with . Then for , we have

where the first inequality follows from the inductive hypothesis and the second inequality follows from the submodularity property as assumed. Hence, we establish that the result holds for , which completes the proof.

A.4 Proof of Lemma 2

We prove the lemma by contradiction. Suppose otherwise and there exists and such that . By definition, . Moreover, inequality (6) implies . Thus, , which contradicts the fact that .

A.5 Proof of Theorem 2

We establish that with these bids the profit for supplier is , and then that given the bids of the other players, no improvement on this is possible for supplier . We consider two cases. First suppose that then and with bids supplier makes zero profit. In the second case and . This implies that any optimal solution for must have .

Next we show that the buyer has an optimal choice when facing bids . Now for any feasible ,

where the inequality follows from Lemma 1 and we have used for . Since , using (9) we obtain

Substitution into the inequality for leads to

| (A-2) |

We will show that with the choice the buyer can achieve this bound. Since , we have

Here we have used the fact that and also that when . Hence we have established that is an optimal choice for the buyer. By Assumption 1 the buyer choice that achieves supply chain optimality is preferred and hence we have , from which it follows that the profit for supplier when bids are is . Now we evaluate . For any feasible , the bound (A-2) still applies and hence

Since and each is non-negative we have for each . Thus

where the last equality is based on Lemma 2. Hence, as for , we have

and so is also optimal for the buyer faced with bids . Thus

| (A-3) |

and there is no loss to the buyer from a restriction that one of the values is zero.

Now suppose that there is a different offer by one of the suppliers , giving a set of bids

The buyer can obtain a profit of through restricting consideration to choices with . This follows because when . We can write this lower bound on buyer profit as

Suppose that is an optimal choice by the buyer given bids , so

Given bids , the profit for supplier is

Since and , the above quantity is at most

where the first inequality is from the fact that functions are consistent with the costs, while the second inequality is from Lemma 1. We can use (A-3) and cancel terms to obtain

The final step is to consider an offer by one of the suppliers . For these suppliers there is no profit under the set of bids . We will show that there is no chance to make a profit with a different bid. It is clear that any choice that has will give the buyer less than if the same choice was used with the bids , and we have seen that for an optimal choice is given by . Thus this choice that has (and gives preference to those in the supply chain optimal choice) gives the buyer at least the same profit as any other and is therefore chosen by the buyer. Hence the profit made by supplier with the new offer can never be greater than zero. Thus we have established that in both cases no other bid can achieve a higher profit for supplier , establishing that the bids given in the theorem are indeed a Nash equilibrium.

A.6 Proof of Corollary 1

This is immediate, since Theorem 1 part (a) establishes that supplier can make no more than , which by construction is the supplier profit under the conditions of the Corollary. Moreover the example of an optimal choice for the supplier corresponds to part (b) of Theorem 1. Finally, the statement on -optimality follows from part (c) of Theorem 1.

A.7 Proof of Proposition 1

First we want to show that , for . Assumption 1 is enough (from uniqueness of the support of supply chain capacity choices) to show , as we observed in (5). Then use of submodularity and repeated application of Lemma 2 with decreasing in size shows that for .

It suffices to show that the execution and reservation payments induced by and satisfy the conditions given in Theorem 2. It is straightforward that the execution payment is for . For , and thus . For , we obtain the reservation payment as follows:

Thus,

Next we show that when all s are large enough, the set of derived from the power function bids is consistent with the costs. There are two requirements for consistency, first we need . This follows because for , and hence independent of the choice of . The second requirement is that for any with ,

The right hand side of this expression is also a sum over the non zero elements of from (14). Thus we can look at this inequality on a component by component basis, and we want to find values of large enough that, for every

where

| (A-4) |

and is optimal for . We note that

where , i.e., it consists of with the ’th component set to zero. The first inequality here comes from submodularity and the second from the optimality of . Now we observe that for the buyer’s profit from supplier , which is

is increased by taking out the capacity from supplier (i.e., moving from to ) since is reduced. Hence

Thus,

where

We need to show that . Observe from (A.7) that if . Moreover is zero when , and hence at , with equality in the case that .

Since gives the optimal solution for we know that

Looking at the second derivative:

from our assumptions on the functions and . The strict inequality here can be established from observing that is decreasing and is increasing in . Now for

which are both zero at . Hence a Taylor series expansion shows that for close enough to but below it, we will have . The multiplier decreases as increases and has limit zero for any . Note that decreases towards at as increases, and so is less than for large enough. Hence we can set large enough that for all . Therefore, we have established that the set of is consistent with the costs.

A.8 Proof of Proposition 2

For submodularity we simply need to show that . Let be the optimal supply chain choice when both suppliers are available. Then

where for any vector we define and . Using subadditivity of and the restriction on and functions we have

The final stage is simply to observe that for the capacity game with function bids, we have and this is a subadditive function, since

A.9 Proof of Theorem 3

Note that the supply chain optimal profit as a set function can be expressed as follows:

According to (3), with the conditions of the theorem, is laminar concave and hence -concave in (see the Appendix for definition) according to Murota (2003), which implies that is -concave in . For any , let

We show that is -concave over . To this end, consider the informal convolution function

where and , with if and the indicator function of set (i.e., if and otherwise). It is clear that both and are -concave over . According to Murota (2009, Section 4.2), is -concave over . Note that the restriction of on is exactly , which therefore is -concave over with straightforward direct verification according to the definition of -concavity. We then conclude that is submodular over (Murota and Shioura, 2004), which implies that , as the restriction of to , is submodular over , as desired.

On the second part of the theorem for the case of the capacity game with function bids, we assume that, for each supplier , the marginal execution cost is constant and the marginal reservation cost is non-decreasing. Let . We will show that as defined in (14) is laminar concave in . With constant in (13) we have , . Denote and define

We can write

where

and . Denote for . Then

which leads to

Therefore,

Noticing that both and () are convex in , we conclude that is laminar concave with the corresponding laminar family .