Bid Optimization by Multivariable Control in Display Advertising

Abstract.

Real-Time Bidding (RTB) is an important paradigm in display advertising, where advertisers utilize extended information and algorithms served by Demand Side Platforms (DSPs) to improve advertising performance. A common problem for DSPs is to help advertisers gain as much value as possible with budget constraints. However, advertisers would routinely add certain key performance indicator (KPI) constraints that the advertising campaign must meet due to practical reasons. In this paper, we study the common case where advertisers aim to maximize the quantity of conversions, and set cost-per-click (CPC) as a KPI constraint. We convert such a problem into a linear programming problem and leverage the primal-dual method to derive the optimal bidding strategy. To address the applicability issue, we propose a feedback control-based solution and devise the multivariable control system. The empirical study based on real-word data from Taobao.com verifies the effectiveness and superiority of our approach compared with the state of the art in the industry practices.

1. Introduction

Online display advertising has been an increasely significant business. According to the Internet Advertising Bureau (IAB) report, internet advertising revenues for the full year of 2017 increased 21.4% over 2016 and totaled $88.0 billion in the United States, with display advertising111Display-related ad formats include: Banner and Video accounting for approximately $39.4 billion (iab, 2017). In online display advertising, advertisers pay a certain price for the ad opportunity to show their ads. Real-Time Bidding (RTB)(Wang and Yuan, 2015) is the most popular paradigm in display advertising. RTB enables advertisers to bid for the ad opportunity at the impression level, and the bidder with the highest price wins the opportunity to show its ad. Specifically, the bid price for each ad opportunity could be individually different based on its utility and cost, which allows advertisers to leverage extended information and algorithms served by DSPs(Yuan et al., 2013).

A common problem for DSPs is to help advertisers gain as much value as possible within the budget(Wu et al., 2018a). There has been some bidding strategies and algorithms(Wu et al., 2018a; Cai et al., 2017) proposed to maximize the value from advertising with the budget constraint. Therefore, advertisers could simply set the budget of the campaign, and DSPs would calculate the bid price on behalf of advertisers.

However, apart from the budget constraint, advertisers would routinely add certain key performance indicator (KPI) constraints that the advertising campaign must meet(Kitts et al., 2017). Advertisers set such KPI constraints because the campaign with a single budget constraint may suffer from huge changes of the traffic caused by the volatilities of the bidding environment. For example, the ad opportunities of certain days could become so expensive that the advertiser cannot afford to spend all budget on them. One solution is constantly adjusting the daily budget to control the investment, which is costly and even impractical for advertisers. Another solution is to set certain KPI constraints. Some KPI constraints, such as the cost-per-mille (CPM) and cost-per-click (CPC) constraints, have strong influence on the total cost of a campaign. By setting such KPI constraints, advertisers could cast a restriction on the total cost and avoid spending all budget when the ad opportunities are not worthwhile, which frees advertisers from heavy labor on frequently adjusting campaign settings. Furthermore, KPI constraints also serve as a real-time proxy to regulate the advertising performance. In most cases, advertisers ultimately want conversions. However, the conversion is sparse and delayed, which prohibits advertisers to evaluate the advertising performance in real time. As a result, advertisers use the KPI exposed by DSPs to evaluate the expected value from advertising and set it as a constraint to ensure that the performance of advertising is under control.

In this paper, we focus on the CPC constraint, which is one of the most common KPI constraints(Zhang et al., 2014, 2016). We propose the optimal bidding strategy that maximizes the quantity of conversions from advertising under the budget and CPC constraints. In this work, bid optimization is formulated as a linear programming problem, and the primal-dual method is leveraged to derive the optimal bidding strategy. Our methodology could be generalised to other cost-related KPI constraints such as the CPM constraint.

Furthermore, we propose the multivariable control system based on the optimal bidding strategy to address the applicability issue, particularly the dynamic environment, as we apply the bidding strategy in the industrial situation. Based on the analysis of the hyper parameters in the bidding strategy, we claim that the hyper parameters have strong control capabilities on achieving corresponding constraints, and devise the independent PID control system. Taking into consideration the coupling effect, we further improve the performance of the system by proposing the model predictive control system.

Moreover, the proposed systems are implemented and evaluated on real industrial datasets. Experiments on the real datasets from Taobao.com show that the systems have strong control capability on achieving the constraints. We also compare our approach with the state of the art in the industry practices, and the result reveals the superiority of our method. The main contributions of our work can be summarized as follows:

-

(1)

We propose the optimal bidding strategy that maximizes the quantity of conversions under the budget and CPC constraints.

-

(2)

We devise the multivariable control system to deal with the dynamic environment when applying the bidding strategy in the industrial situation.

-

(3)

Extensive experiments are conducted and the results demonstrate the advantage of our approach.

The rest of this paper is organized as follows: we formulate the problem and derive the optimal bidding strategy in Section 2. Section 3 addresses the applicability issue and presents the multivariable control system. Experiments and evaluations are conducted in Section 4, followed by the related work in Section 5. We conclude our work in Section 6.

2. Bidding Strategy

In this section, we firstly review some preliminary knowledge of the RTB eco-system, and afterwards formulate the bid optimization problem. Then we derive the optimal bidding strategy, and take a discussion on the characteristics of the bidding strategy.

2.1. RTB Eco-system

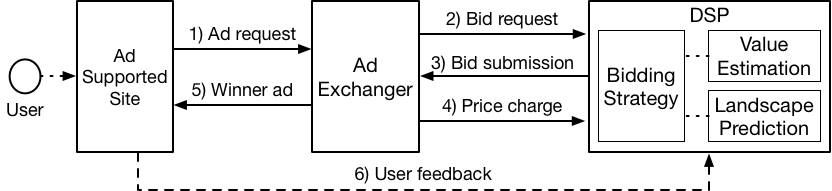

To make this paper self-contained, we briefly introduce RTB eco-system and its related techniques. The work flow of RTB is illustrated as Fig. 1, and each step is as follows: 1) A user visits an ad-supported site, and the site sends an ad request to the ad exchanger. 2) The ad exchanger initiates an auction and requests bids from DSPs. 3) DSPs submit the bid price along with the ad to the ad exchanger on behalf of advertisers. 4) The ad exchanger holds the auction and charges the winner DSP for the ad opportunity. 5)The winner’s ad is sent to the site. 6) User feedback afterwards would be sent back to the corresponding DSP. To avoid redundancy, we focus on step 3), 4) and 6), which are highly related to our work.

A DSP calculates a bid price for the advertiser by its bidding strategy when it receives a bid request from the ad exchanger. Since conversions are the target event of most advertisers, almost all bidding strategies (including ours) rely heavily on the ability of learned models to estimate ad click-through rate (CTR) (McMahan et al., 2013) and conversion rate222The conversion rate is conditioned on the click (CVR) (Lee et al., 2012). In addition, some DSPs may also base their bidding strategies on the prediction of the winning price (bid landscape prediction). CTR/CVR estimation and landscape prediction by themselves are heavily studied problems (Zhou et al., 2018; Yang, 2017; Wang et al., 2016), which is beyond our scope. Therefore, we just assume the estimation and prediction problems have been solved, and the expected probability of the click and conversion could be quantified by CTR and CVR respectively.

When a DSP wins the opportunity to show the ad in an auction, it is charged a price. The price is equal to the second highest bid price under the generalized second price (GSP) auction mechanism (Edelman et al., 2007), which is widely adopted in industrial platforms. There are also some other auction mechanisms such as Vickrey-Clarke-Groves auction mecahnism (VCG) (Nisan et al., 2007). In this paper, without loss of generality, we base the discussion and formulation on the most common GSP auction mechanism.

Any feedback on the ad from the user, such as clicks and conversions, would be sent back to the corresponding DSP. The DSP could utilize such feedbacks to train the prediction models, and timely adjust its bidding strategy. In addition, such feedbacks would be integrated and exposed to advertisers by the DSP. In our proposed system, we take advantage of such feedbacks and continuously fine tune the bidding strategy across the lifetime of the advertising campaign.

2.2. Problem Formulation

Suppose there are ad opportunities in a day, and we index each ad opportunity by their generated order as . Each ad opportunity has different value for the advertiser, and we use to represent the value of for the advertiser. Based on , the bid price is calculated and submitted to the ad exchanger. Each ad opportunity has a winning price . From the perspective of the advertiser, equals to the highest bid price of other advertisers. If is higher than , which means that the advertiser would win the ad opportunity and be charged under the GSP auction mechanism, we set to be 1, and 0 otherwise. The total and of the advertising campaign is formulated as Eq. (1) and Eq. (2).

| (1) |

| (2) |

We formulate CPC in Eq. (3). It is worth noting that we replace the real click with CTR, which provides us with a more concise formulation. Such a replacement could largely facilitate our theoretical analysis, and has trivial influence in the following practical system design.

| (3) |

The conversion is what advertisers ultimately want. Therefore, we quantify by . Please note that must be considered since conversions could only be generated after a click and CVR is conditioned on a click. We summarize the problem as follows and formulate it as (LP1).

-

•

We maximize the quantity of conversions with the budget , and guarantee that CPC does not exceed a given value .

(LP1) (4) s.t. (5) where

2.3. Optimal Bidding Strategy

The problem (LP1) is actually a linear programming problem(Schrijver, 1998), which is to find the optimal to maximize the target function with the linear constraints. There has been many algorithms proposed to directly solve such a problem, however, we aim to derive the optimal bidding strategy instead of the allocation strategy. In other words, we do not essentially care about the value of , but the underlying bidding strategy that intrinsically affects . With such a consideration, we creatively resort to the primal-dual method. Every linear programming problem, referred to as a primal problem, can be converted into a dual problem(Dantzig, 1983). In addition, the optimal primal solution can be obtained by the corresponding dual solution according to the duality theorem(Boyd and Vandenberghe, 2004). Such mathematics characteristics shell some insights on us, and we integrate the primal space and the dual space to derive the following theorem:

Theorem 2.1.

The optimal bidding strategy formulation is:

| (6) |

The optimal bidding strategy is stated in Eq. 6, where and are hyper parameters incorporated from the dual space, and correspond to the optimal dual solution. We will investigate the properties of and in later sections. For now, we give the proof for Thm. 2.1.

Proof.

(LP1) is converted to the dual problem:

| (LP2) | ||||

| (7) | s.t. | |||

| where | ||||

Assume the optimal solution for the primal problem (LP1) is , and the optimal solution of the corresponding dual problem (LP2) is , , . According the theorem of complementary slackness, we obtain:

| (8) |

| (9) |

-

•

According to Eq. (10), if the campaign wins , i.e. , then . Meanwhile, , so .

- •

To sum up, for any , the bidding strategy would guarantee that the is optimal, which leads to the optimal solution of (LP1). That is to say, when the optimal is 1 (the campaign should win ), the bid price based on the optimal bidding strategy is higher than , which would guarantee that the campaign wins . The reasoning is the same when the optimal is 0. Therefore, the campaign needs just to bid following the optimal bidding strategy in Eq. (6), and the total advertising value would be maximized with the constraints. ∎

It is worth noting that Eq. (6) does not explicitly tell the value of and . Actually, it is easy to derive the optimal and by solving the dual problem with well developed linear programming algorithms. Such work does not contribute to the comprehension of our work, so we do not discuss how to calculate the value of and here.

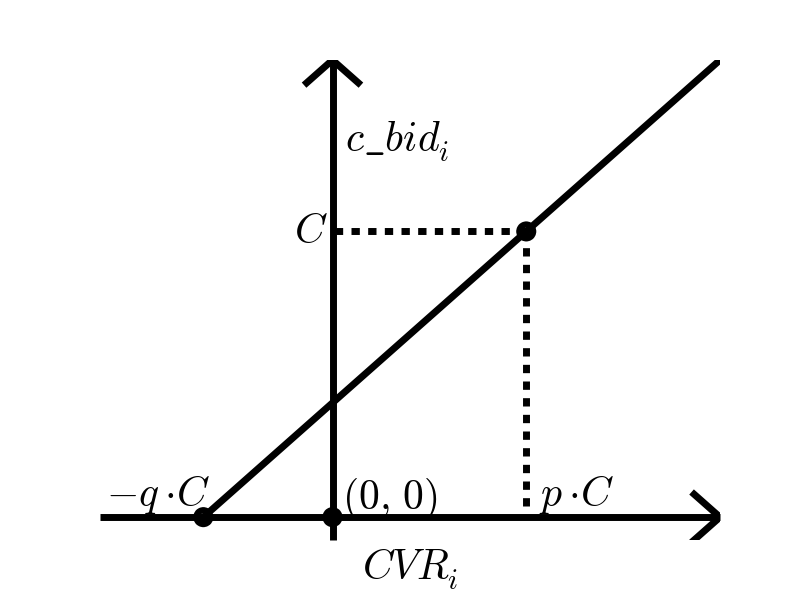

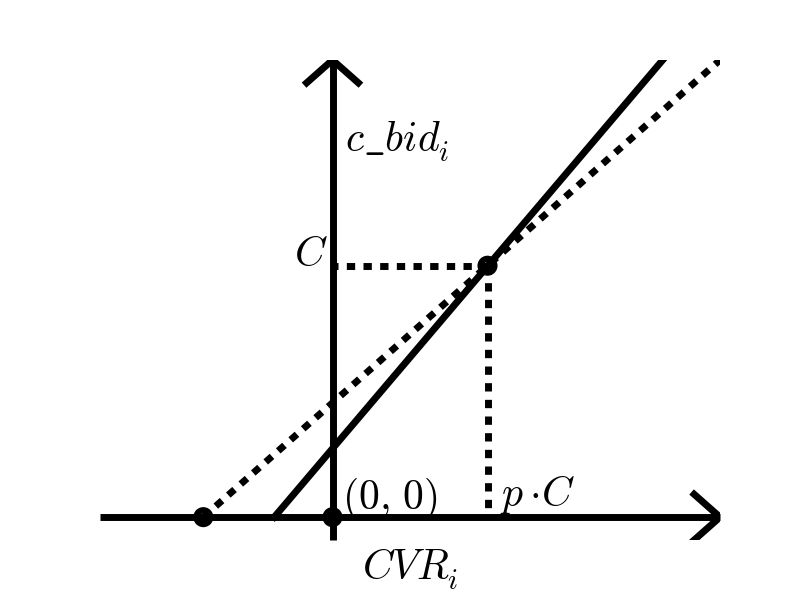

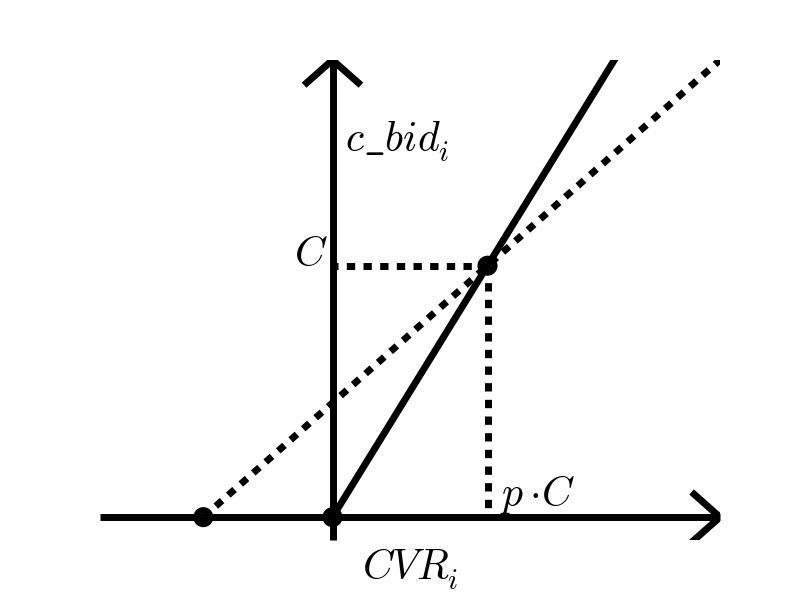

We reformulate the optimal bidding strategy for (LP1) into two stages as shown in Eq. (11), Eq. (12) and Fig. 2, where could be regarded as the bid price for a click. As an ad opportunity comes, we first determine the bid price for a click, i.e. . After we determine , the final bid price is calculated by multiplying with , which could be automatically completed and is omitted in the following discussion. In addition, the cost for a click is naturally no higher than the bid price for a click under the GSP auction mechanism(Edelman et al., 2007), so that is directly related to CPC. Therefore, we focus the discussion on the bid price for a click () instead of the final bid price to facilitate our demonstrations.

| (11) | ||||

| (12) | ||||

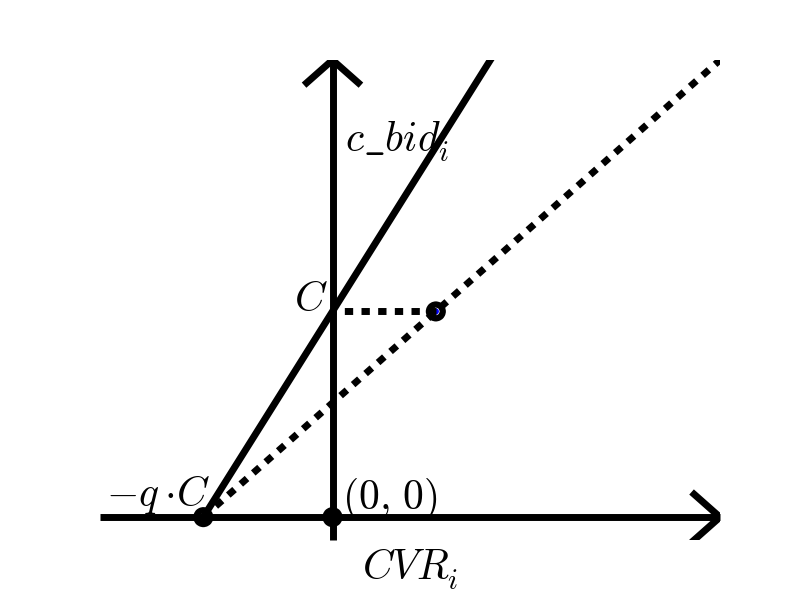

We start the discussion on the optimal bidding strategy with some obvious facts as illustrated in Fig. 2(a). Firstly, the bid price for a click is strictly positive related to . It does make sense that we should give a higher bid price for a more valuable click, and a lower price for a less valuable click. Secondly, the bid price is linear against . It is a natural result since we are maximizing the sum of the value, which is a linear function against itself. Thirdly, the bidding strategy would definitely cross two points as emphasized in the figure. We shall discuss it in details in later analysis. However, there is an unusual fact: unlike the widely adopted bidding strategies (Zhang et al., 2016; Perlich et al., 2012), the function does not necessarily get through the origin. Specifically, the bid price would be non-zero even though the ad opportunity has no value for the advertiser. It is a little bit unintuitive that we bid a non-zero price for an ad opportunity without value. We state the reason as follows: considering a CPC constraint is given, the bidding strategy tries to win some cheap ad opportunity, even without any value, to lower the overall CPC, and thus to win some valuable ad opportunity with high CPC.

3. System Design

In this section, we address the applicability issue of the bidding strategy in the industrial scenario, and propose the feedback control-based solution. Based on the analysis of the hyper parameters in the optimal bidding strategy, we present the multivariable control system.

3.1. Applicability Issue

As shown in (LP2), in order to solve the linear programming problem and obtain the optimal bidding strategy, we need to know exactly the information of every ad opportunity of the day, including the winning price, CTR and CVR. Such information, however, could not be obtained in real world until the end of the day, while the optimal bidding strategy need to be determined before the campaign starts. Apart from the fact that it is difficult to estimate all of them in the impression level precisely before the campaign starts(Wang et al., 2016; Zhou et al., 2018; Yang, 2017), how to predict the ad opportunity itself of the day is still an open question due to the dynamic environment(Snoddy and Els, 2018). One may argue that there are many statistical algorithms proposed to solve such a problem: the optimal solution could be derived from sufficient historical data and be applied in the future. One strong assumption made in such algorithms is that the distribution of the variables are stationary. However, the distribution of not only the ad opportunities, but also other factors such as the winning price, CTR and CVR are not stationary in the dynamic RTB environment. Therefore, the optimal bidding strategy derived on historical data becomes no longer optimal for future, and may even break the CPC constraint.

3.2. Feedback Control-based Solution

As discussed in the last section, due to the dynamic bidding environment, the bidding strategy we derive on the historical data may be unreliable. Therefore, we need to leverage the real-time information to adjust the bidding strategy. Feedback control, which deals with the dynamic systems from feedback and outside noise(Kumar et al., 2014), is widely adopted in the industry because of its robustness and effectiveness. A feedback control system is to achieve desirable performance by adjusting the system input based on the feedback of the system output. In our scenario, we could naturally integrate the bidding strategy and the RTB environment as a dynamic system, and regard the hyper parameters of the bidding strategy and as the input of the system. By doing so, the problem is transformed into a feedback control problem. There is still one problem: what is the desirable performance, and consequently what feedback of the output should we care about? Firstly, we aim to maximize the advertising value and control CPC. Secondly, in order to maximize the advertising value, we should pace the budget spending to win the valuable ad opportunities scattered across time(Song et al., 2017). Therefore, we need to pace the budget spending, and control CPC simultaneously. We propose the feedback solution as follows: to improve the advertising performance, we pace the budget spending and control CPC based on their real-time feedback.

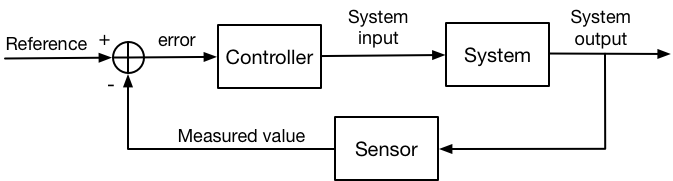

We briefly introduce the standard feedback control system. A block diagram of the feedback control system is illustrated as Fig. 3. The desired value of the ouput is called the reference, which is pre-set depending on the specific task. The sensor measures the actual value of the variable from the system output, and transmit it to the controller. Comparing the measured value and the reference, the controller would adjust the input of the system by its pre-defined algorithms or strategies to diminish the difference between them. Proportional-Integral-Derivative (PID) controller(Bennett, 1993) is the most widely adopted feedback controller in the industry. It is known that a PID controller delivers best performance in the absence of knowledge of the underlying process (Benner, 1993). A PID controller continuously calculates the error between the measured value and the reference at every time step , and produce the control signal based on the combination of proportional, integral, and derivative terms of . The control signal is then sent to adjust the system input by the actuator model . It is practical and common to use discrete time step () in online advertising scenario, so the process of PID could be formulated as following equations, where , , and are the weight parameters of a PID controller.

| (13) |

| (14) |

| (15) |

3.3. Analysis on Hyper Parameters

We have transformed the problem into a feedback control problem, and determined the dynamic system (the bidding strategy and RTB), the input parameters ( and ), and the output variables (budget spending and CPC) in last sections. The challenge is how to control the budget spending and CPC simultaneously by adjusting and . Due to the multiple input parameters and the multiple output variables, we cannot directly apply the PID controllers in our scenario since such controllers are designed for the system with a single input parameter and a single output variable. There has been some multivariable control methods such as model predictive control (Rawlings and Mayne, 2009) proposed to deal with such a system, and we shall leverage their underlying idea in our design in the next section. In this section, we revisit the optimal bidding strategy in Eq. (11) and share our ideas to design the multivariable control system.

We analyse how the hyper parameters and contribute to the bidding strategy in Eq. (11). Please recall that and are dual variables incorporated by the constraint (4) and (5) respectively, and we explore their relationship with the corresponding constraint.

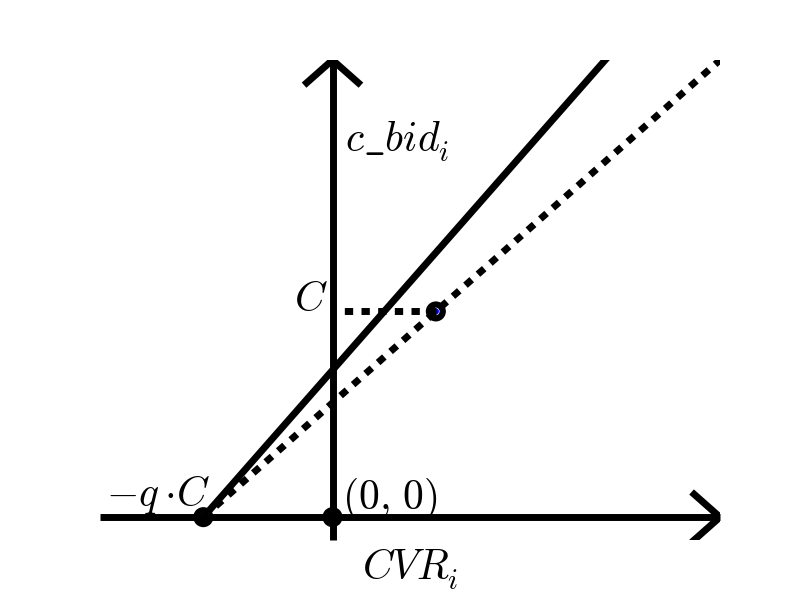

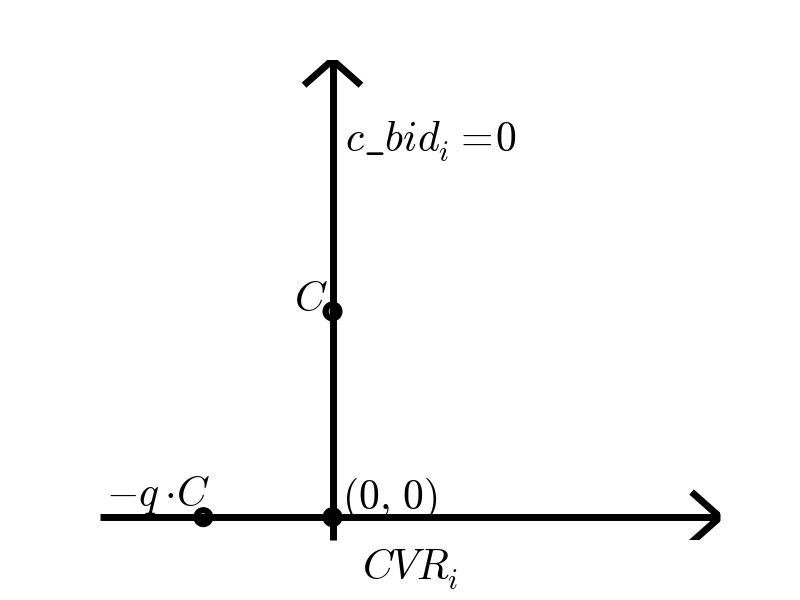

Fig. 4 shows the optimal bidding strategy with fixed and respectively decreased, increased, equal to and equal to . It is worth noting that the bidding price would exactly influence the expected cost: the higher bidding price leads to more cost since the campaign may win more ad opportunities. As illustrated in Fig. 4, the bidding price would be generally lowered or lifted as increases or decreases. When we increase , the bidding strategy would rotate clockwise around the point . The resulting fact is that: the bidding price that is above zero would be lowered, and the bidding price that is below zero333Although the bidding price would never be a negative value, the analytic continuation would help to comprehend the mathematics property. would be lifted, and thus the expected cost would be lessened. Please take and as the extreme examples. The advertising campaign would never be charged when its bid price constantly equals to zero with . When , the budget becomes no longer a constraint. The bidding price does not become infinitely high because there is still a CPC constraint and the slope of the bidding strategy is controlled completely by . If we simultaneously set to be 0, which means the CPC constraint also is removed, the bidding price would be infinitely high and the campaign would win all ad opportunities. According to the illustrations, we claim that has a direct and effective control capability on the budget spending, and could definitely lower the budget spending speed.

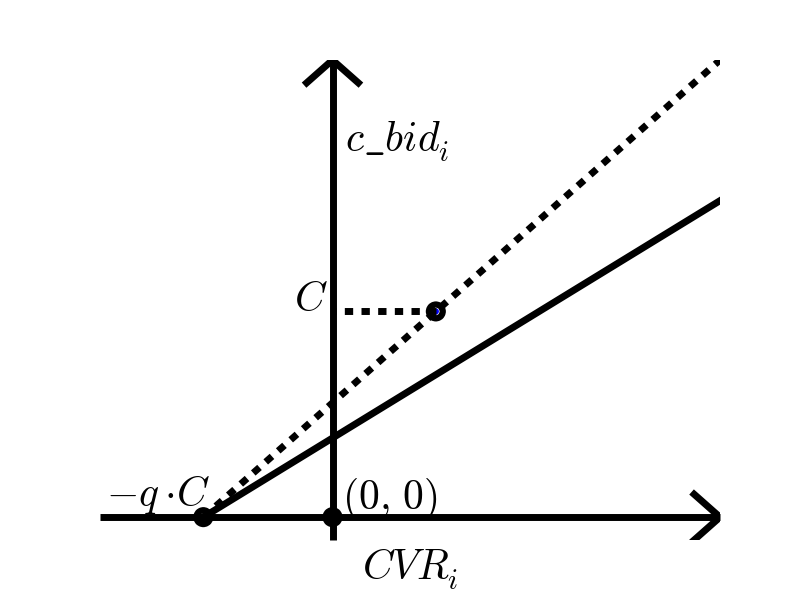

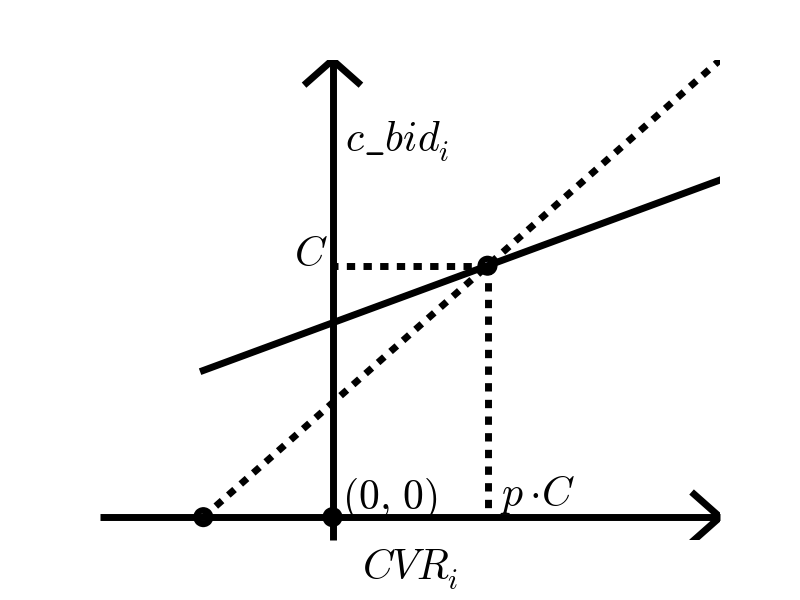

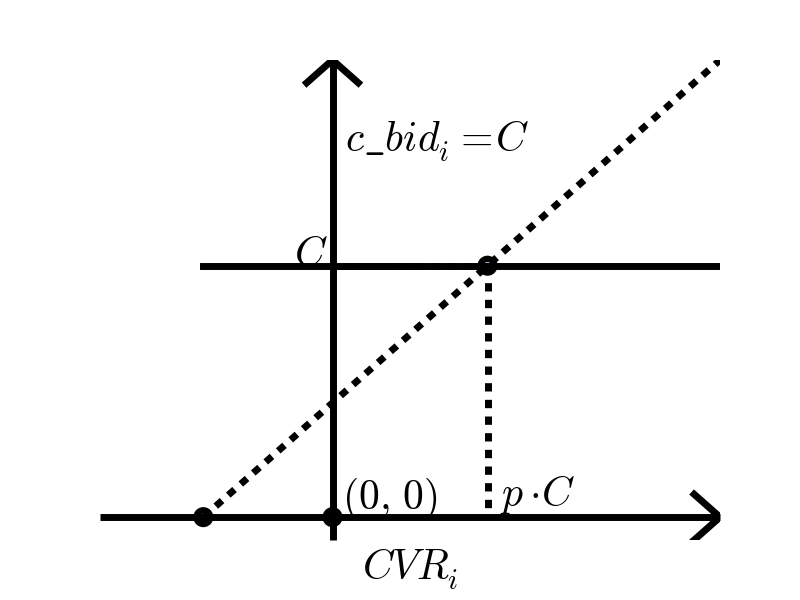

In a similar way, we fix and set to be respectively decreased, increased, equal to 0, and equal to . As illustrated in Fig. 5, ’s effects on the optimal bidding strategy is notably different to that of . When we increase or decrease , the bidding strategy would rotate clockwise or counter-clockwise around the the point . Taking increasing for example, the bid price above would be lowered, and that below would be lifted. Thus the campaign would win more ad opportunities whose CPC is below , and less ad opportunities whose CPC is above . The composite result is that the CPC is more likely to be below . In the extreme cases, CPC would be guaranteed below when . When is set to be zero, which means the CPC constraint is removed, the bidding strategy is determined by and degenerates to the optimal budget-constrained bidding strategy in (Wu et al., 2018a; Zhang et al., 2016; Perlich et al., 2012). Based on the analysis, we claim that CPC could be definitely controlled by . We propose the following two statements:

-

(1)

Hyper parameter has a direct and effective control capability on the budget spending, and the budget spending speed could be definitely lowered by given whatever value of .

-

(2)

Hyper parameter has a direct and effective control capability on CPC, and the CPC constraint could be definitely achieved by adjusting given whatever value of .

3.4. Multivariable Control

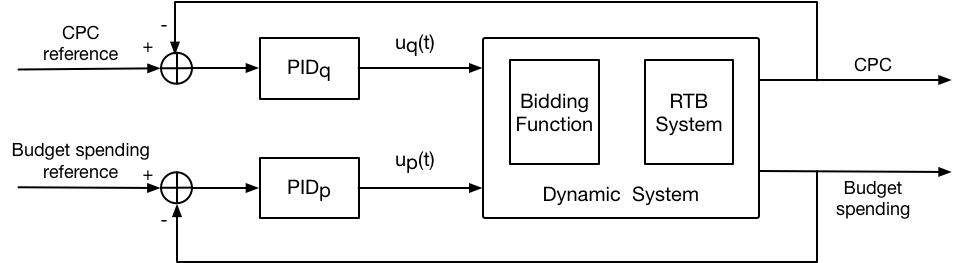

As we state in the last section, the budget spending and CPC could be definitely controlled by and respectively. In other words, and could be used to control the budget spending and CPC independently, and regard each other as outside noise. Therefore, we could decompose the multivariable feedback control problem into two single-variable feedback control problem. By doing so, PID controllers could be easily deployed, and we propose the independent PID design in Fig. 6, where and afterwards we slightly abuse the subscript and to differentiate the two controllers.

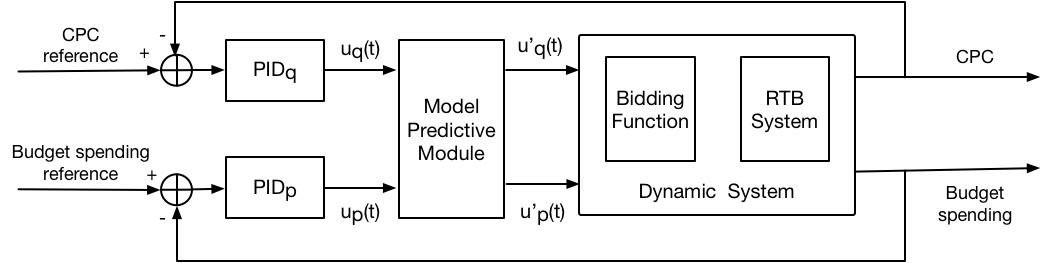

To make a further step, we revisit the analysis in Section 3.3. As illustrated in Fig. 4, increasing would generally lower the bidding price and reduce the budget spending speed. Another non-trivial effect caused by increasing is that the expected CPC would also be lowered. According to such observations, adjusting actually casts influence on CPC. Similarly, adjusting also casts influence on budget spending. Although our independent PID control system could deal with such coupling effect, which is treated as outside noise by controllers, it is possible to further improve the performance of the system by addressing such an issue. However, such coupling effect is hard to be quantified and compensated since we have no explicit knowledge of the dynamic system. In order to address such a problem, we leverage the underlying idea of model predictive control (MPC)(Rawlings and Mayne, 2009) to predict and compensate the coupling effect. It is worth mentioning that we do not directly apply MPC in our control system since modelling the highly non-linear RTB environment is costly and even impractical. In our design, combined with the human knowledge, the model predictive module needs only to predict the coupling effect, which could be approximated by a linear model. As illustrated in Fig. 7, a model predictive module is deployed after PID controllers to regulate the control signal by addressing the coupling effect.

One of the most important components of MPC is a model to represent the behaviour of the dynamic system. In our case, we model the bidding environment with respect to the cost and CPC as shown in Eq. (16), where X is a matrix and b is a matrix. After we obtain the expected and from the feedback, we could adjust and by solving the equation in Eq. (17), and derive the result as shown in Eq. (18). The formulation in Eq. (18) demonstrates that the control signal of and should be a linear combination of the changes of cost and CPC. Therefore, we define the model predictive module by Eq. (19), where and are quantified by and respectively, and is approximated by a matrix determined by and . By approximating , we could simply regard and as two weight parameters and search their best value in the training set. Although such an approximation undermines the capability to represent the system, it makes the controller more robust and stable against the changing environment. It is worth mentioning that we propose the matrix X and b to model the dynamic system, however, the exactly value of such matrices is not explicitly required. As shown in Eq. (19), we take advantage of such matrices to address the coupling effect, and obtain the approximated function determined by only and .

| (16) |

| (17) |

| (18) |

| (19) |

4. Empirical Study

In this section, we conduct comprehensive experiments to demonstrate our statements and the advantage of our multivariable control systems. After describing the real dataset and related metrics, we present the implementation details. Experiments are conducted on the example campaigns to prove the the claimed control capability of the hyper parameters. To show the superiority of our system, we compare our methods with the state of the art in the industry practices on a large group of campaigns.

4.1. Experiment Setup

4.1.1. Dataset

We base the experiments on the real dataset from Taobao.com. The dataset consists of 40 advertising campaigns across continuous days and totally bid logs. It is split according to the date as training dataset and test dataset. The key information of the dataset from the perspective of a specific advertising campaign could be summarized as Tab. 1. We mainly use the information of the winning price, and . The winning price of each ad opportunity corresponding to the specific campaign is recorded after each online auction ends. Since Taobao.com is also a publisher, the winning price could be observed even the advertiser missed the ad opportunity in the online auction. and are estimated by the online deployed models, which leverage extensive realtime and historical information of the user and ads. Please refer to (Zhou et al., 2018) for details of the online deployed estimation models.

| Key | Description |

|---|---|

| identity of the ad opportunity | |

| arriving time of | |

| winning price of | |

| estimated click-through rate of | |

| estimated conversion rate of |

4.1.2. Metrics

The goal of the bidding strategy and system is to maximize the total value of the winning ad opportunities, and control CPC under the given threshold. We quantify the advertising value by the sum of , which corresponds to the expected outcomes of the conversion. It is worth mentioning that we regard as the value, instead of the actual conversion event, to exclude the inaccuracy caused by the estimation models. Even though some previous work evaluates the bidding strategy by the actual conversions, we argue that the estimation error actually cast non-trivial influence on the results. A campaign with a fixed bidding strategy may gain more clicks/conversions just by optimizing the estimation models, so we regard as the true conversion to diminish such influence.

-

(1)

represents the advertising value of the campaign.

-

(2)

represents the maximum advertising value the campaign could achieve with the budget and CPC constraints.

-

(3)

could be used to evaluate how close the advertising performance is to the ideal result.

-

(4)

is the proportion of the campaigns that satisfy the CPC constraint (overshoot within is allowed), which could be used to evaluate the CPC control capability when comparing different methods with each other on a large group of campaigns.

-

(5)

is the average on the campaigns whose CPC constraint holds, which is to evaluate the advertising value achievement. As for those campaigns that break the CPC constraint, we exclude their when we calculate since wining more value by breaking the CPC constraint is not allowed in our scenario.

4.1.3. Implementation Details

We adopt the actuator shown in Eq. (20) in the PID controllers and the baseline strategies, where the sign of depends on the relationship between the input parameter and the output variable. In addition, it needs to be noted that we actually care about the accumulated CPC when the campaign ends, and the real-time CPC of each time step contributes differently to the accumulated CPC because the quantity of clicks in each time step is different. The traditional PID error could not address the different weight in our scenario, so we weigh the error by the quantity of clicks and modify the control signal for as shown in Eq. (21) and Eq. (22), where is calculated by Eq. (14) and represents the quantity of clicks in the time step . By such a modification, the PID controller would constantly increase its attention on the accumulated CPC, and give each time step different weights.

To determine the weight parameters of a PID controller, as well as the weight parameters and , we grid-search the best setting on the training dataset, and apply it on the test dataset. We regard every one hour as a time step, so the maximum time step equals to .

| (20) |

| (21) |

| (22) |

As we discussed in last sections, the PID controllers need a reference. In our experiments, CPC given by the advertiser is set as the constant reference to control . Considering the ad opportunity and winning price, which have an immediate impact on the cost, show different statistical characteristics across time steps, the cost reference should be customized with respect to the time step. We calculate the cost distribution on the training dataset, which is the ideal cost of each time step normalized by the total cost of the day, as the cost reference. Our experiment flow steps are as follows: 1) optimal and are calculated on the training dataset; 2) the bidding process is simulated on the test dataset, where the calculated and are applied as the initial hyper parameters; 3) the simulation would finish when the campaign runs out of budget or there is no more ad opportunity.

4.2. Control Capability

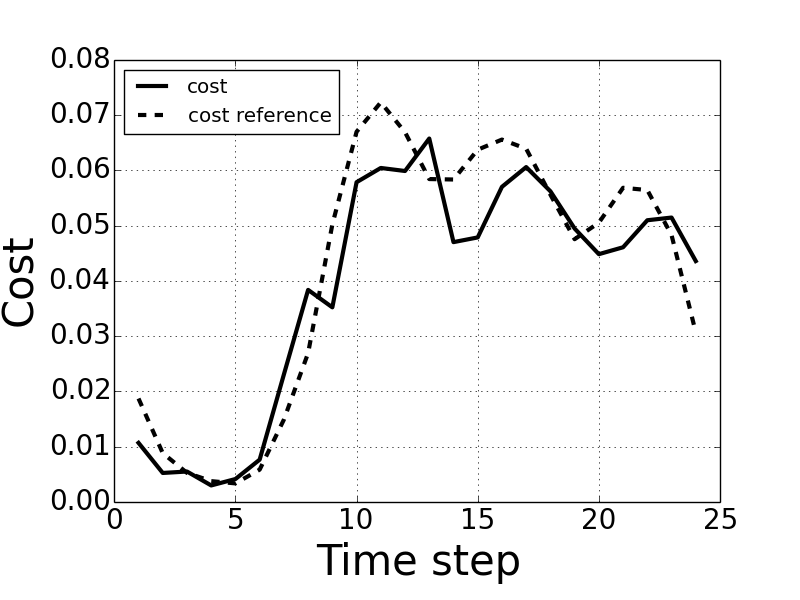

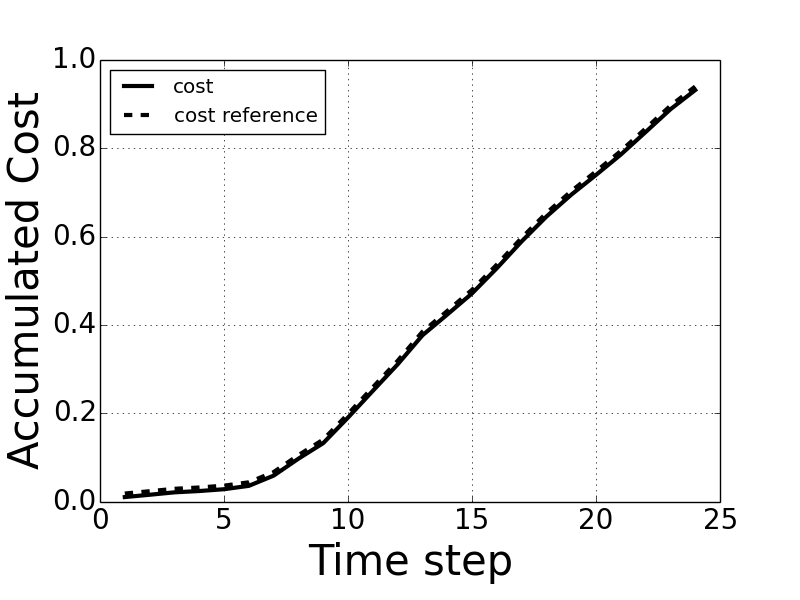

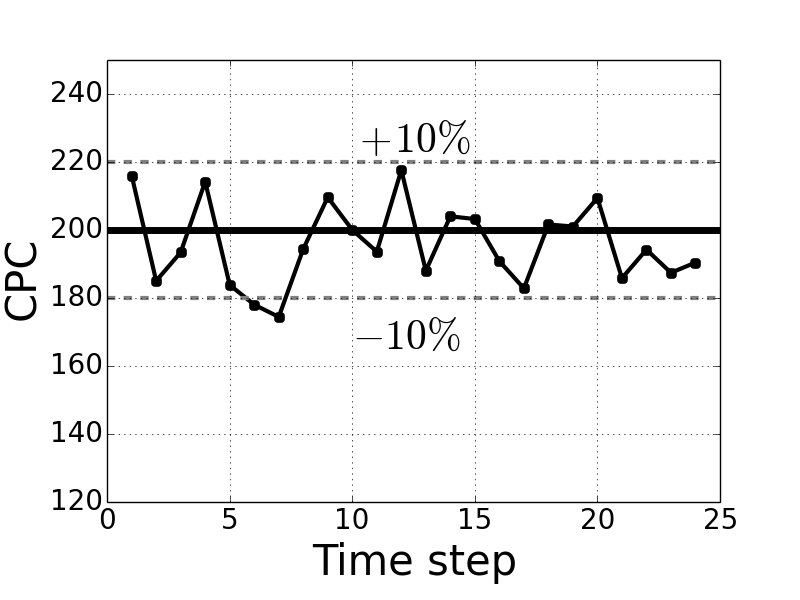

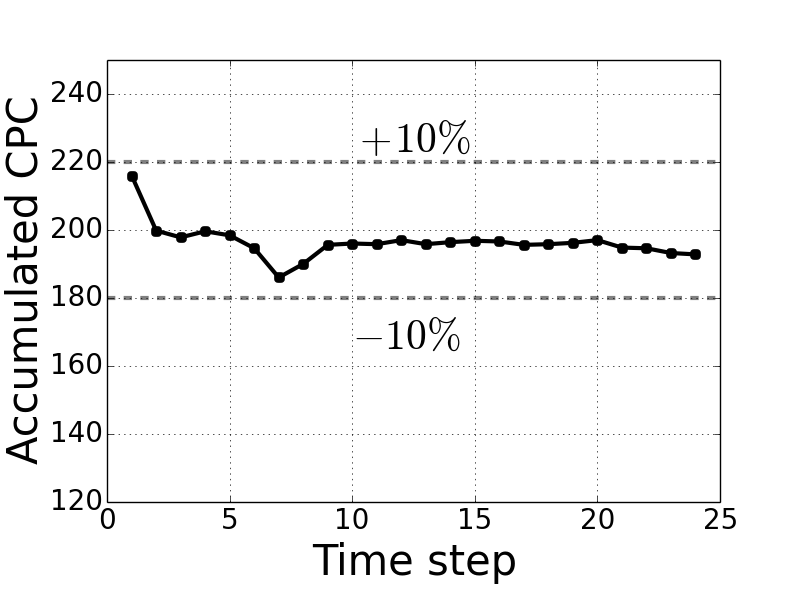

In this section, we do experiments to demonstrate our statements that budget spending and CPC could be independently controlled by and . We adjust both hyper parameters simultaneously without the model predictive module and illustrate the control performance in terms of budget spending and CPC respectively on the example campaign. The controlling performance is illustrated in Fig. 8 and Fig. 9

As illustrated in Fig. 8, the cost of each time step controlled by fluctuates around the cost reference, and the accumulated cost is well controlled referring to the accumulated cost reference. As Fig. 9 shows, CPC of each time step gets quickly confined within the tolerable margin, and the accumulated CPC is successfully controlled under the given reference. It is worth mentioning that the real-time CPC shows observable fluctuation across time steps since the attention on the real-time CPC is gradually decreased in our design. Compared with the real-time CPC, the accumulated CPC delivers stable performance as illustrated in Fig. 9(b). According to the experiments, although and have interference with each other, they could be independently adjusted to control the corresponding output variables.

4.3. Performance Evaluation

In this section, we compare our approach with the state of the art in the industry. We first introduce our baseline strategies, and evaluate all of them on the real-world dataset.

4.3.1. Baseline Strategies

-

(1)

Cost-min: Cost-min(Kitts et al., 2017) is a generic algorithm to address multiple constraints in advertising scenario, and could be applied in our scenario as follows. The bidding strategy Eq. (23) is adopted. We adjust by a PID controller according to the cost reference, and set the upper bound of to be . The CPC constraint of the advertising campaign would always hold with Cost-min because of the truncated bid price. We divide the given CPC by the averaged CVR on all bid logs of the campaign to initialize .

-

(2)

Fb-Control: Zhang et al. proposed a feedback control mechanism that dynamically adjusts the bids to control CPC(Zhang et al., 2016). In their work, they adopted the generalised bidding strategy, which is shown in Eq. (24), and constantly adjust by a PID controller according to the feedback of CPC. The given CPC is set as the initial value of . For simplicity, we reference their method as Fb-Control.

-

(3)

Fb-Control-M: Fb-Control does not consider the value of a click (i.e. ), which is important to improve the advertising performance. Therefore, we modify their bidding strategy to better fit into our scenario as shown in Eq. (23), where is adjusted by a PID controller according to our cost reference, and the upper bound of is controlled by an independent PID controller according to the feedback of CPC. The upper bound, initialized by the given CPC, would truncate every time exceeds the value, and is initialized in the same way with Cost-min. We reference the modified method as Fb-Control-M.

| (23) |

| (24) |

4.3.2. Experimental Results

We reference our independent PID control system as I-PID, and the model predictive PID control system as M-PID for simplicity. We compare I-PID and M-PID with strategies introduced in the last section on the real-word dataset, and the result on 40 test campaigns is shown in Tab. 2.

| Method | ||

|---|---|---|

| Cost-min | 1.0 | 0.362 |

| Fb-Control | 1.0 | 0.549 |

| Fb-Control-M | 1.0 | 0.709 |

| I-PID | 1.0 | 0.892 |

| M-PID | 1.0 | 0.928 |

As illustrated in Tab. 2, all methods could guarantee the CPC constraint, while Cost-min achieves the least advertising value. It is because Cost-min controls CPC greedily and excessively by simply truncating the price, which would lose many valuable ad opportunities. Fb-Control and its modified version, as well as our approaches, also show excellent control capability on achieving the CPC constraint. However, Fb-Control and Fb-Control-M achieved generally lower value than I-PID and M-PID. The key reason is that their generalised bidding strategy is not optimal to address the budget spending and CPC constraint simultaneously. Fb-Control-M obtains a better result than Fb-Control, and justifies our modification. Our approach I-PID outperforms all baseline strategies. M-PID performs even better than I-PID, since the coupling effect is addressed in M-PID and thus the controllers could behave in a more coordinated way. To sum up, compared with the state of the art in the industry practices, our multivariable feedback control systems deliver excellent control capability on the CPC and superior advertising performance in our scenario.

5. Related Work

The bid optimization problem is a very actively studied problem in real-time bidding(Zhang et al., 2012; Ren et al., 2018; Maehara et al., 2018; Zhou et al., 2008), and several formulations and algorithms have been proposed in the display advertising scenario. Authors of work (Zhang et al., 2014; Cai et al., 2017; Wu et al., 2018a) proposed models to maximize advertising value within the budget, where the KPI constraint is not considered. Some work has been proposed to specifically address the KPI constraint such as (Zhang et al., 2016; Ghosh et al., 2009). Little work in diaplay advertising focuses on advertising value and KPI constraints simultaneously. Kitts et al. introduced a generic bidding framework to take into consideration of the advertising value and multiple KPI constraints in (Kitts et al., 2017). Our work is similar to (Kitts et al., 2017), however, we focused on the specific KPI constraint and proposed a more delicate strategy. In our work, we abstracted our problem as a linear programming problem and leveraged the primal-dual method. Such an approach is generally applied in the ad allocation scenario (Chen et al., 2011; Goel et al., 2010; Agrawal et al., 2014). Different from their work, our work adopted this approach to derive the optimal bidding strategy instead of the allocation strategy. To address the dynamic environment, we took advantage of the feedback control theory, which has been proved effective in many scenarios by work of (Zhang et al., 2016; Jambor et al., 2012; Karlsson and Zhang, 2013). Other related work includes click-through rate estimation(Zhou et al., 2018; McMahan et al., 2013), conversion rate estimation(Yang, 2017; Lee et al., 2012), winning price prediction (Wu et al., 2018b; Wang et al., 2016) and budget pacing(Xu et al., 2015; Lee et al., 2013).

6. Conclusion

In this paper, we focus on the bidding strategy to maximize the advertising value with the budget and the KPI constraint. We convert such a problem into a linear programming problem and leverage the primal-dual method to derive the optimal bidding strategy. The hyper parameters of the bidding strategy is investigated and their relationship with the corresponding constraint is illustrated. It is demonstrated that the hyper parameters have strong control capability on achieving the constraints. Based on our analysis, we propose a feedback control-based solution and design the independent PID control system to address the dynamic environment. To compensate the coupling effect among variables, we further devise the model predictive PID control system by deploying a model predictive module. Extensive experiments are conducted, and our approach is compared with the state of the art in the industry on real-world dataset. The results show that our multivariable control systems deliver superior advertising performance with the KPI constraint holding.

References

- (1)

- iab (2017) 2017. IAB internet advertising revenue report. https://www.iab.com/wp-content/uploads/2018/05/IAB-2017-Full-Year-Internet-Advertising-Revenue-Report.REV_.pdf.

- Agrawal et al. (2014) Shipra Agrawal, Zizhuo Wang, and Yinyu Ye. 2014. A dynamic near-optimal algorithm for online linear programming. Operations Research 62, 4 (2014), 876–890.

- Benner (1993) S Benner. 1993. A History of Control Engineering.

- Bennett (1993) Stuart Bennett. 1993. Development of the PID controller. IEEE control systems 13, 6 (1993), 58–62.

- Boyd and Vandenberghe (2004) Stephen Boyd and Lieven Vandenberghe. 2004. Convex optimization. Cambridge university press.

- Cai et al. (2017) Han Cai, Kan Ren, Weinan Zhang, Kleanthis Malialis, Jun Wang, Yong Yu, and Defeng Guo. 2017. Real-time bidding by reinforcement learning in display advertising. In Proceedings of the Tenth ACM International Conference on Web Search and Data Mining. ACM, 661–670.

- Chen et al. (2011) Ye Chen, Pavel Berkhin, Bo Anderson, and Nikhil R Devanur. 2011. Real-time bidding algorithms for performance-based display ad allocation. In Proceedings of the 17th ACM SIGKDD international conference on Knowledge discovery and data mining. ACM, 1307–1315.

- Dantzig (1983) George Bernard Dantzig. 1983. Reminiscences about the origins of linear programming. In Mathematical Programming The State of the Art. Springer, 78–86.

- Edelman et al. (2007) Benjamin Edelman, Michael Ostrovsky, and Michael Schwarz. 2007. Internet advertising and the generalized second-price auction: Selling billions of dollars worth of keywords. American economic review 97, 1 (2007), 242–259.

- Ghosh et al. (2009) Arpita Ghosh, Benjamin IP Rubinstein, Sergei Vassilvitskii, and Martin Zinkevich. 2009. Adaptive bidding for display advertising. In Proceedings of the 18th international conference on World wide web. ACM, 251–260.

- Goel et al. (2010) Ashish Goel, Mohammad Mahdian, Hamid Nazerzadeh, and Amin Saberi. 2010. Advertisement allocation for generalized second-pricing schemes. Operations Research Letters 38, 6 (2010), 571–576.

- Jambor et al. (2012) Tamas Jambor, Jun Wang, and Neal Lathia. 2012. Using control theory for stable and efficient recommender systems. In Proceedings of the 21st international conference on World Wide Web. ACM, 11–20.

- Karlsson and Zhang (2013) Niklas Karlsson and Jianlong Zhang. 2013. Applications of feedback control in online advertising. In American Control Conference (ACC), 2013. IEEE, 6008–6013.

- Kitts et al. (2017) Brendan Kitts, Michael Krishnan, Ishadutta Yadav, Yongbo Zeng, Garrett Badeau, Andrew Potter, Sergey Tolkachov, Ethan Thornburg, and Satyanarayana Reddy Janga. 2017. Ad Serving with Multiple KPIs. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining. ACM, 1853–1861.

- Kumar et al. (2014) PR Kumar et al. 2014. Control: A perspective. Automatica 50, 1 (2014), 3–43.

- Lee et al. (2013) Kuang-Chih Lee, Ali Jalali, and Ali Dasdan. 2013. Real time bid optimization with smooth budget delivery in online advertising. In Proceedings of the Seventh International Workshop on Data Mining for Online Advertising. ACM, 1.

- Lee et al. (2012) Kuang-chih Lee, Burkay Orten, Ali Dasdan, and Wentong Li. 2012. Estimating conversion rate in display advertising from past erformance data. In Proceedings of the 18th ACM SIGKDD international conference on Knowledge discovery and data mining. ACM, 768–776.

- Maehara et al. (2018) Takanori Maehara, Atsuhiro Narita, Jun Baba, and Takayuki Kawabata. 2018. Optimal Bidding Strategy for Brand Advertising.. In IJCAI. 424–432.

- McMahan et al. (2013) H Brendan McMahan, Gary Holt, David Sculley, Michael Young, Dietmar Ebner, Julian Grady, Lan Nie, Todd Phillips, Eugene Davydov, Daniel Golovin, et al. 2013. Ad click prediction: a view from the trenches. In Proceedings of the 19th ACM SIGKDD international conference on Knowledge discovery and data mining. ACM, 1222–1230.

- Nisan et al. (2007) Noam Nisan, Tim Roughgarden, Eva Tardos, and Vijay V Vazirani. 2007. Algorithmic game theory. Cambridge University Press.

- Perlich et al. (2012) Claudia Perlich, Brian Dalessandro, Rod Hook, Ori Stitelman, Troy Raeder, and Foster Provost. 2012. Bid optimizing and inventory scoring in targeted online advertising. In Proceedings of the 18th ACM SIGKDD international conference on Knowledge discovery and data mining. ACM, 804–812.

- Rawlings and Mayne (2009) James B Rawlings and David Q Mayne. 2009. Model predictive control: Theory and design. (2009).

- Ren et al. (2018) Kan Ren, Weinan Zhang, Ke Chang, Yifei Rong, Yong Yu, and Jun Wang. 2018. Bidding Machine: Learning to Bid for Directly Optimizing Profits in Display Advertising. IEEE Transactions on Knowledge and Data Engineering 30, 4 (2018), 645–659.

- Schrijver (1998) Alexander Schrijver. 1998. Theory of linear and integer programming. John Wiley & Sons.

- Snoddy and Els (2018) Laura Snoddy and Michael Els. 2018. System and method for advertisement impression volume estimation. US Patent 9,865,004.

- Song et al. (2017) Yuxuan Song, Kan Ren, Han Cai, Weinan Zhang, and Yong Yu. 2017. Volume Ranking and Sequential Selection in Programmatic Display Advertising. In Proceedings of the 2017 ACM on Conference on Information and Knowledge Management. ACM, 1099–1107.

- Wang and Yuan (2015) Jun Wang and Shuai Yuan. 2015. Real-time bidding: A new frontier of computational advertising research. In Proceedings of the Eighth ACM International Conference on Web Search and Data Mining. ACM, 415–416.

- Wang et al. (2016) Yuchen Wang, Kan Ren, Weinan Zhang, Jun Wang, and Yong Yu. 2016. Functional bid landscape forecasting for display advertising. In Joint European Conference on Machine Learning and Knowledge Discovery in Databases. Springer, 115–131.

- Wu et al. (2018a) Di Wu, Xiujun Chen, Xun Yang, Hao Wang, Qing Tan, Xiaoxun Zhang, Jian Xu, and Kun Gai. 2018a. Budget constrained bidding by model-free reinforcement learning in display advertising. In Proceedings of the 27th ACM International Conference on Information and Knowledge Management. ACM, 1443–1451.

- Wu et al. (2018b) Wush Wu, Mi-Yen Yeh, and Ming-Syan Chen. 2018b. Deep Censored Learning of the Winning Price in the Real Time Bidding. In Proceedings of the 24th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining. ACM, 2526–2535.

- Xu et al. (2015) Jian Xu, Kuang-chih Lee, Wentong Li, Hang Qi, and Quan Lu. 2015. Smart pacing for effective online ad campaign optimization. In Proceedings of the 21th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining. ACM, 2217–2226.

- Yang (2017) Hongxia Yang. 2017. Bayesian Heteroscedastic Matrix Factorization for Conversion Rate Prediction. In Proceedings of the 2017 ACM on Conference on Information and Knowledge Management. ACM, 2407–2410.

- Yuan et al. (2013) Shuai Yuan, Jun Wang, and Xiaoxue Zhao. 2013. Real-time bidding for online advertising: measurement and analysis. In Proceedings of the Seventh International Workshop on Data Mining for Online Advertising. ACM, 3.

- Zhang et al. (2016) Weinan Zhang, Yifei Rong, Jun Wang, Tianchi Zhu, and Xiaofan Wang. 2016. Feedback control of real-time display advertising. In Proceedings of the Ninth ACM International Conference on Web Search and Data Mining. ACM, 407–416.

- Zhang et al. (2014) Weinan Zhang, Shuai Yuan, and Jun Wang. 2014. Optimal real-time bidding for display advertising. In Proceedings of the 20th ACM SIGKDD international conference on Knowledge discovery and data mining. ACM, 1077–1086.

- Zhang et al. (2012) Weinan Zhang, Ying Zhang, Bin Gao, Yong Yu, Xiaojie Yuan, and Tie-Yan Liu. 2012. Joint optimization of bid and budget allocation in sponsored search. In Proceedings of the 18th ACM SIGKDD international conference on Knowledge discovery and data mining. ACM, 1177–1185.

- Zhou et al. (2018) Guorui Zhou, Xiaoqiang Zhu, Chenru Song, Ying Fan, Han Zhu, Xiao Ma, Yanghui Yan, Junqi Jin, Han Li, and Kun Gai. 2018. Deep interest network for click-through rate prediction. In Proceedings of the 24th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining. ACM, 1059–1068.

- Zhou et al. (2008) Yunhong Zhou, Deeparnab Chakrabarty, and Rajan Lukose. 2008. Budget constrained bidding in keyword auctions and online knapsack problems. In International Workshop on Internet and Network Economics. Springer, 566–576.