Driver Surge Pricing

Abstract

Ride-hailing marketplaces like Uber and Lyft use dynamic pricing, often called surge, to balance the supply of available drivers with the demand for rides. We study driver-side payment mechanisms for such marketplaces, presenting the theoretical foundation that has informed the design of Uber’s new additive driver surge mechanism. We present a dynamic stochastic model to capture the impact of surge pricing on driver earnings and their strategies to maximize such earnings. In this setting, some time periods (surge) are more valuable than others (non-surge), and so trips of different time lengths vary in the induced driver opportunity cost. First, we show that multiplicative surge, historically the standard on ride-hailing platforms, is not incentive compatible in a dynamic setting. We then propose a structured, incentive-compatible pricing mechanism. This closed-form mechanism has a simple form and is well-approximated by Uber’s new additive surge mechanism. Finally, through both numerical analysis and real data from a ride-hailing marketplace, we show that additive surge is more incentive compatible in practice than is multiplicative surge. †† We would like to thank Uber’s driver pricing data science team, in particular Carter Mundell, Jake Edison, Alice Lu, Michael Sheldon, Margaret Tian, Qitang Wang, Peter Cohen, Kane Sweeney, and Jonathan Hall for their support and suggestions without which this work would have not been possible. We also thank Leighton Barnes, Ashish Goel, Ramesh Johari, Vijay Kamble, Anurag Komanduri, Hannah Li, Virag Shah, and anonymous reviewers. This work was funded in part by the Stanford Cyber Initiative, the Office of Naval Research grant N00014-15-1-2786, and National Science Foundation grants 1544548 and 1839229.

1 Introduction

Ride-hailing marketplaces like Uber, Lyft, and Didi match millions of riders and drivers every day. A key component of these marketplaces is a surge (dynamic) pricing mechanism. On the rider side of the market, surge pricing reduces the demand to match the level of available drivers and maintains the reliability of the marketplace, cf., Hall et al. (2015), and so allocates the rides to the riders with the highest valuations. On the driver side, surge encourages drivers to drive during certain hours and locations, as drivers earn more during surge (Lu et al., 2018; Hall et al., 2017; Chen and Sheldon, 2016). Castillo et al. (2017) show that surge balances both sides of this spatial market by moderating the demand and the density of available drivers, hence avoiding so called “Wild Goose Chase” equilibria in which drivers spend much of their time on long distance pick ups. Surge pricing – along with centralized matching technologies – is often considered the primary reason that ride-hailing marketplaces outperform traditional taxi services on metrics such as driver utilization and overall welfare (Cramer and Krueger, 2016; Buchholz, 2017; Ata et al., 2019).

However, variable pricing (across space and time) must be carefully designed, since it can create incentives for “cherry-picking” and rejecting certain trip requests. Such behavior increases earnings of strategic drivers at the expense of other drivers, who may then disproportionately receive such trip requests after they are rejected by others, cf., Cook et al. (2018). It also reduces overall platform reliability, inconveniencing riders who may have to wait longer before receiving a ride.

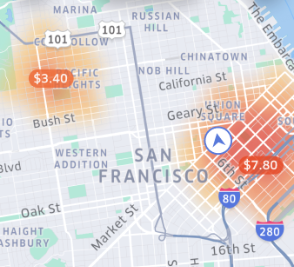

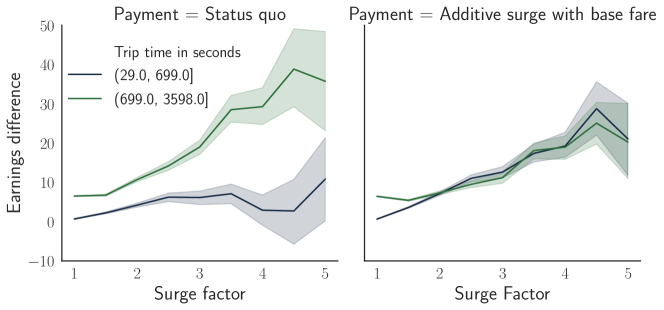

Uber recently revamped its driver surge mechanism, to improve the driver experience and make earnings more dependable (Uber, 2019b). The main change is making surge “additive” instead of “multiplicative.” Under multiplicative surge, the driver payout from a surged trip scales with the length of the trip. In contrast, under additive surge, the payout surge component is constant (independent of trip length), with some adjustment for very long trips (Uber, 2019c). Figure 1 depicts the driver app surge heat-map for each type of surge. We show that the change directly addresses a primary reason that drivers who strategically reject trip requests may earn more than others, even as total payments remain the same.

1.1 Contributions

We consider the design of incentive compatible (IC) pricing mechanisms in the presence of surge. Trips differ by their length , and the platform sets the payout for each trip in each world state (i.e., surge vs non-surge). Drivers decide which trip requests to accept in each world state, in response to the payout function .111Drivers’ level of sophistication and experience varies, cf. Cook et al. (2018). An IC mechanism aligns the incentives of drivers to accept all trips, for any level of strategic response to pricing strategies. The technical challenge is to design an IC pricing mechanism , for which accepting all trips is an earning maximizing strategy for drivers over a long horizon, i.e., where in each world state maximizes driver earnings.

We first study a continuous-time, infinite horizon single-state model, where trip requests arrive over time according to a stationary Poisson process. We show that in this model, multiplicative pricing – where the payout of a trip is proportional to the length of that trip – is incentive compatible. To obtain this result, we show in Theorem 1 that the best response strategy of a driver to function , to maximize earnings, is a threshold strategy where the driver accepts all trips with payout rate above some threshold. Hence, a mechanism that equalizes the payout rate of all trips is incentive compatible.

We then present a model where the world state stochastically transitions over time between surge and non-surge states, with trip payments, distributions, and intensity varying between states. In such a dynamic system, completing a given trip affects a driver’s earnings beyond just the length of the trip, i.e., it imposes a future-time externality on the driver that is a function of the trip length. The driver’s trip opportunity cost thus includes both what occurs during a trip, and a continuation value. This externality causes multiplicative pricing to not be incentive compatible in the presence of surge (Theorem 2), in contrast to the single-state model. Namely, drivers can benefit from rejecting long trips in a non-surge state, and short trips in the surge state.

In Theorem 3, our main result, we propose a class of incentive compatible pricing functions described in closed form of the model primitives. The prices incorporate driver temporal externalities: during surge, short trips pay more per unit time than do long trips.

Next, we study surge pricing in our model numerically, showing that additive surge is incentive compatible in more regimes of interest than is multiplicative surge. Finally, using RideAustin data, we show that our theoretical insights extend to practice: additive surge correctly values trips amid temporal externalities, unlike multiplicative surge.

To our knowledge, ours is the first ride-hailing pricing work to incorporate dynamic (non-constant), stochastic demand and pricing. This component is essential to uncover how a particular trip imposes substantial temporal externalities on a driver’s future earnings.

1.2 Related Work

We discussed some of the related work on surge pricing above. Here, we briefly review the lines of research closest to ours. We refer the reader to a recent survey by Korolko et al. (2018) for a broader overview of the growing literature on ride-hailing markets.

Driver spatio-temporal strategic behavior. Several works model strategic driver behavior in a spatial network structure, and across time in a single-state. Ma et al. (2018) develop spatially and temporally smooth prices that are welfare-optimal and incentive compatible in a deterministic model. Their prices form a competitive equilibrium and are the output of a linear program with integer solutions. We similarly seek to develop incentive compatible pricing schemes, and both works broadly construct VCG-like prices that account for driver opportunity costs. Our focus is on structural aspects (e.g., multiplicative in trip length) in a non-deterministic model.

Bimpikis et al. (2016) show how the platform would price trips between locations, taking into account strategic driver re-location decisions, in a stationary model with discrete locations. They show that pricing trips based on the origin location substantially improves surplus, as well as the benefits of “balanced” demand patterns. Besbes et al. (2018b) consider a continuous state space setting and show how a platform may optimally set prices across the space in reaction to a localized demand shock to encourage drivers to relocate; their model has driver cost to re-locate, but no explicit time dimension. They find that localized prices have a global impact, and, e.g., the optimal pricing solution incentivizes some drivers to move away from a demand shock. Afèche et al. (2018) consider a two state model with demand imbalances and compare platform levers such as limiting ride requests and directing drivers to relocate, in a two-state fluid model with strategic drivers. They upper-bound performance under these policies, and find that it may be optimal for the platform to reject rider demand even in over-supplied areas, to encourage driver movement. A similar insight is developed by Guda and Subramanian (2019) who explicitly model market response to surge pricing. Finally, Yang et al. (2018) analyze a mean-field system in which agents compete for a location-dependent, time-varying resource, and decide when to leave a given location. They leverage structural results—agents’ equilibrium strategies depend just on the current resource level and number of agents—to numerically study driver relocation decisions as a function of the platform commission structure.

Pricing in ride-sharing and service systems. There is a growing literature on queuing and service systems motivated in part by the ride-sharing market. For example, Besbes et al. (2018a) revisit the classic square root safety staffing rule in spatial settings, cf., Bertsimas and van Ryzin (1991, 1993). Much of the focus of this line of work is how pricing affects the arrival rate of (potentially heterogeneous) customers, and thus the trade-off between the price and rate of customers served in maximizing revenue.

Banerjee et al. (2015) consider a network of queues in which long-lived drivers enter the system based on their expected earnings but cannot reject specific trip requests. Under their model, dynamic pricing cannot outperform the optimal static policy in terms of throughput and revenue, but is more robust. Cachon et al. (2017) argue in contrast that surge pricing and payments are welfare increasing for all market participants when drivers decide when to work. Chen and Hu (2018) consider a marketplace with forward-looking buyers and sellers who arrive sequentially and can wait for better prices in the future. They develop strategy-proof prices whose variation over time matches the participants’ expected utility loss incurred by waiting. Lei and Jasin (2016) consider a model where customers arrive over time and utilize a capacity constrained resource for a certain amount of time. They develop an asymptotically revenue-maximizing, dynamic, customer-side pricing policy, even when service times may be heterogeneous. Glazer and Hassin (1983) consider taxi-driver strategic responses to multiplicative and affine pricing, as we do, focusing on deviations in which a driver can take a circuitous route in order to increase the length of a trip.

One of the most related to our work in modeling approach, Kamble (2019) studies how a freelancer can maximize long-term earnings with job-length-specific prices, balancing on-job payments and utilization time. In his model, a freelancer sets their own prices for a discrete number of jobs of different lengths and, with assumptions similar to our single-state model, it is optimal for the freelancer to set the same price per hour for all jobs. We further discuss the relationship of this work to our single-state model below.

Organization.

The rest of the paper is organized as follows. Section 2 contains our model; we derive driver earnings as it depends on their strategy, and formalize the platform objective. In Section 3, we formulate a driver’s best response strategy to affine pricing functions in each model. In Section 4, we present incentive compatible pricing functions for our surge model. In Section 5, we numerically compare the IC properties of additive and multiplicative surge. Finally, in Section 6, we empirically compare additive and multiplicative surge using data from the RideAustin marketplace.

2 Model, driver earnings, and platform objective

We consider a large ride-hailing market with decoupled pricing, from the perspective of a single driver. This driver receives trip requests of various lengths. The trips’ rate, distribution, and payment are known to the driver and determined exogeneously to decisions to accept or decline requests. We do not consider spatial heterogeneity, to focus on the temporal opportunity cost and continuation value based on a length of the trip.222We believe our insight can be extended to a spatial setting where the price can be decomposed to a time-based component, based on the length of the trip, and a spatial component based on the destination of the trip. However, this would be beyond the scope of this work, cf., Bimpikis et al. (2016).

In this section, we first in Section 2.1 present the primitives of our two models, a single-state model and a dynamic model with surge pricing. Then in Section 2.2 we describe the driver’s strategy space and derive the driver reward in each model. Next, in Section 2.3, we formalize the platform objective and technical challenge solved in this work. We conclude with a short discussion on our model’s relationship to practice in Section 2.4.

2.1 Model primitives

We start with the model primitives in each model.

2.1.1 Single-state model

We start with a model where there is a single world state, i.e., all model components are constant over time. Time is continuous and indexed by . At each time , the driver is either open, or busy. While open, the driver receives job (trip) requests from riders according to a Poisson process at rate , i.e., the time between requests is exponential with mean . Job lengths, denoted by , are drawn independently and identically from a continuous distribution .

If the driver accepts a job request of length at time (as discussed below), they receive a payout of at time , at which time they become open again. Otherwise, the driver remains open. Except where specified, the only assumptions on are that it is continuous and asymptotically (sub)-linear: , which ensures that the driver reward is also bounded.333These restrictions are innocuous. With continuity, similar trips pay similarly. Asymptotic sub-linearity means that the marginal value of additional length of a trip remains bounded; it trivially holds if the domain of is bounded.

2.1.2 Dynamic model with surge pricing

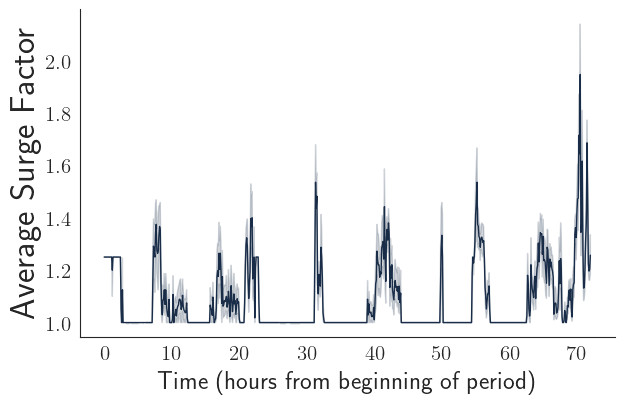

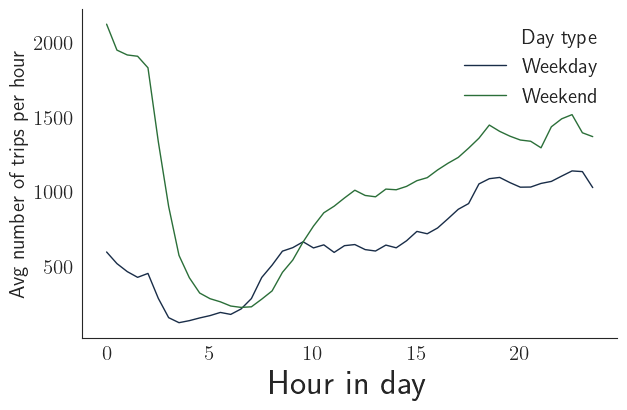

A model with fixed pricing and arrival rates of jobs is not a realistic representation of ride-hailing platforms. In particular, rider demand (both in intensity and in distribution) may vary substantially over time, even within a day (cf. Appendix Figure 9(c)). To study how this dynamic nature affects driver decisions, we consider a model with two states, , where denotes the surge state. (At a high level, the surge state provides a higher earnings rate to the driver. The precise definition is in Section 2.2.2, after we formulate the driver’s earnings rate in each state).

The world evolves stochastically between the two states, as a Continuous Time Markov Chain (CTMC). When the world is in state , the state changes to according to a fixed exponential clock that ticks at rate , independently of other randomness.

When open in state , the driver receives job requests at rate with lengths , and collects payout according to payment function , which is presumed to have the same properties as in the single-state model. The state of the world may change while a driver is on trip. Crucially, the driver receives payments according to the state of the world when the trip begins. We will use to denote the overall pricing mechanism.

2.2 Driver strategies and earnings

In our model, the driver can decide whether to accept the trip request, with no penalty.444This assumption follows Uber’s current practice. We further discuss the driver’s information set in Section 2.4.

In the single-state model, let denote the driver’s (fixed) strategy, where implies that a driver accepts job requests of length . In the dynamic model, the driver follows policy , where indicates the jobs accepted in state . We assume that driver policies are measurable with respect to (corresponding in dynamic model); for technical reasons, in the dynamic model we also assume that consist of a union of open intervals, i.e., are open subsets of . When we write equalities with policies , we mean equality up to changes of measure 0.

The driver is long-lived and aims to maximize their own lifetime average hourly earnings on the platform, including both open and busy times. Let denote the (random) total earnings from jobs accepted from time up to time if the driver follows policy and the payout function is . Then, the driver’s lifetime earnings rate is

This earnings rate is a deterministic (non-random) quantity, and is a function of the driver policy , pricing function , and the primitives.

A driver policy is optimal (best-response) with respect to pricing function if it maximizes the lifetime earnings rate of the driver among all policies: , for all valid policies (i.e., measurable with respect to or , with open sets). Then, pricing function is incentive compatible (IC) if accepting all job requests is optimal with respect to , i.e., in the single-state model or in the dynamic model is optimal with respect to . In other words, payment function is incentive compatible if an earnings-maximizing driver (who knows all the primitives, , and the trip length at request time) accepts every trip request.

We now analyze the driver’s lifetime earnings rate for each model.

2.2.1 Driver earnings in the single state model

In the single-state model, the primitives directly induce a renewal reward process, where a given renewal cycle is the time a driver is newly open to the time they are open again after completing a job. Let be the mean earnings on trips , i.e., the expected earning in a renewal cycle; let be the sum of the expected wait time to an accepted trip and the expected length of a trip, and thus the expected renewal cycle length; let be the probability the driver receives a request in . Then, the lifetime driver mean hourly earnings (earnings rate) is

The first equality follows from the renewal reward theorem, and holds with probability 1.

2.2.2 Driver earnings in the dynamic model

For the dynamic model, on the other hand, we cannot directly use the renewal reward theorem with a renewal cycle containing just a single trip. The driver’s earning on a given trip is no longer independent of earnings on other trips: given a job that starts in the surge state, the driver’s next job is more likely to also start in surge. Given whether each job started in the surge state, however, job earnings are independent. We can use this property to prove our next lemma, which gives the driver earnings rate in the dynamic model. Let be the fraction of time the driver spends either open state or on a trip that starts in state .

Lemma 1.

In the dynamic model, the earnings rate can be decomposed into each state earnings rate and fraction of time spent in state :

As in the single-state model, where

We prove the result by defining a new renewal process, in which a single reward renewal cycle is: the time between the driver is open in state 1 to the next time the driver is open in state 1 after being open in state 2 at least once. In other words, each renewal cycle is composed of some number (potentially zero) of sub-cycles in which the driver is open in state 1 and then is open in state 1 again after a completed trip; one sub-cycle starting with the driver open in state 1 and ending with being open in state 2 (either after a completed trip or a state transition while open); some number (potentially zero) of sub-cycles in which the driver is open in state 2 and then is open in state 2 again after a completed trip; and finally one sub-cycle starting in state 2 and ending with the driver open in state .

Given the number of such renewal reward cycles completed up to time , the total earnings on trips starting in each state (earnings in each sub-cycle) are independent of each other, and then we use Wald’s identity (Wald, 1973) to separate and .

Note that is not exactly the expected length of time in a single sub-cycle in a state given , but rather is proportional to it; the multiplicative constant cancels out with the same constant in the expected earnings in a single sub-cycle in a state given . This constant emerges from the primitives: when the driver is open in state , there are two competing exponential clocks (with rates and , respectively) that determine whether the driver will accept a request before the world state changes.

What does look like? We defer showing the exact form to Section 4.1 in advance of developing incentive compatible pricing. Here, we provide some intuition: the trips that a driver accepts in each state determines the portion of their time spent on trips started in each state. If a driver never accepts trips in the non-surge state, they will be open and thus available for a trip as soon as surge begins. Inversely, if a driver accepts a long surge trip immediately before surge ends, they will be paid according to the surge payment function even though surge has ended. Surprisingly, given the complex formulation of the reward as it depends on , we find the structure of optimal policies as they depend on the pricing , as well as incentive compatible pricing functions.

Finally, we can now precisely define what it means for to be the surge state: it has a higher potential earning rate than state . There exists some policy such that , for all . In other words, suppose that instead we were in the single-state setting, where the primitives were set as either or . Then the latter set of primitives would yield a higher maximum earnings.555 This assumption is different than the statement that each surge trip pays more than an equivalent non-surge trip, , and neither statement implies the other. Under this definition, surge may be characterized as higher per-trip payments. Alternatively, if request arrival rate is high due to a demand shock, , then the driver waits less time between trip requests and so has a higher earnings rate – even without higher per-trip payments. While a less common scenario in practice, our model further allows surge to be characterized by a more lucrative distribution of trips compared to , even if the intensity of trips and on-trip payments conditional on trip length are identical. More generally, surge may be characterized by a combination of such scenarios.

2.3 Platform objective and constraints

Having derived the driver reward, we now describe the platform objective, setting up the technical challenge we solve in the rest of the work. Recall that our model is decoupled: rider and driver prices are determined separately. Under decoupled pricing, the platform has under its control both the price charged to the rider and the payment paid to the driver for a trip of length —and the proportion of these two values may vary across trips. This modeling assumption follows the current practice (Uber, 2019e) and allows us to focus on the drivers’ perspective, without further complicating the analysis.666Coupled pricing imposes more constraints. Bai et al. (2018) and Bikhchandani (2020) both find that the platform should adjust its payout ratio with demand—an example of decoupling—to maximize profit or overall welfare.

What should be the role of driver payments with decoupled pricing? In practice, the platform quotes the rider a price and ‘guarantees’ fulfillment if a ride is requested; driver payments should thus primarily ensure that all requested rides are fulfilled, motivating our goal of designing incentive compatible prices. In Appendix Section A.1, we formalize this intuition by considering driver payments as a sub-problem of the comprehensive platform challenge, involving jointly setting both rider prices and driver payments to maximize an objective (e.g., profit or welfare). We establish that – with decoupled pricing and an earnings-maximizing driver within our model – this joint problem can be decomposed into one in which the rider pricing (not considered in this work) determines the objective value, subject to finding a driver payment policy that satisfies incentive compatibility and a driver participation constraint: that the driver earnings rate is higher than an outside option earnings rate (denoted ), i.e., .

In the dynamic model, we additionally consider per-state driver earnings constraints, , for some exogenous . This constraint comes from practice, via features not directly captured in our model. As detailed in Appendix Section A.2, following the current practice, in our model platforms impose a business constraint to approximately pass on rider revenue in each world state to the driver, i.e., the constraints are determined by per-state revenue, a function of latent demand and rider prices.

If the platform has more flexibility, may also be optimized, for example to induce drivers to position themselves in areas with more frequent surges. Lu et al. (2018) find empirically that drivers do re-position to higher surge areas. Ong et al. (2020) describe how Lyft manages an incentive budget over time and space to incentivize driver re-positioning, and in a coupled pricing setting Besbes et al. (2018b) show theoretically how to set prices to induce driver movement. More broadly, the revenue during one spatio-temporal period may be used to smooth out driver payments in another period, cf. Asadpour et al. (2019); Bai et al. (2018). In this work, we do not directly consider how the platform should set (or ); how to do so over space and time is an interesting avenue for future work. Instead, we establish our results for a range of for which incentive compatible prices can be constructed. This decomposition reflects how decoupled surge pricing is set in practice, and for the rest of this work we seek a payment policy that satisfies these conditions.

2.4 Practical considerations

Our model is stylized in several important respects, and ride-hailing practice is not consistent across marketplaces, time, or geography. Our theoretical model reflects our view on the most relevant components from practice.

Driver heat-maps and affine pricing We are especially interested in affine pricing schemes, where , with (in the single-state model: , with ; we refer to the case with ( as positive (negative) affine pricing). Such pricing functions can be communicated as time and distance rates (see, e.g., Uber (2019d)), and the surge component displayed on a heat-map. This simplicity is an important desiderata from practice, where payments should be clear to drivers.

Driver information structure: trip time and time to the rider. We assume that the platform reveals the total trip length to the driver at the time of request, and that the driver can freely reject it without penalty. Drivers often cannot see the rider’s destination or the trip length until they pick up the rider (but they can reject a request based on the pick-up time to the rider, without penalty).777This practice is not consistent across marketplaces and locations. For example, in California as of January 2020, Uber shows the driver the destination and payment estimate at request time. Incentive compatible pricing is an important stepping stone to showing this information. Some drivers call ahead to find out the rider’s destination or even cancel the trip at the pick-up location, creating negative experiences for both the rider and the driver.888We note that destination discrimination is against Uber’s guidelines and could lead to deactivation (Uber, 2019a). Our notion of incentive compatibility is ex-post, in which drivers would accept all trips even knowing the trip length. This notion is stronger than an ex-ante setting in which the trip length is not revealed to drivers. Furthermore, in practice, jobs have two components: the time it takes to pick up the rider, and the time while the rider is in the driver’s vehicle – and the former component is typically unpaid.999Lyft has recently experimented with paying drivers for the time it takes to pick up the rider (Auerbach, 2019). Our model combines these two components into an overall trip length, which determines payments.

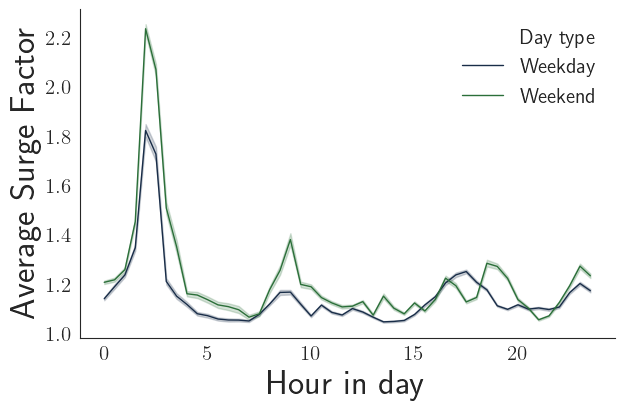

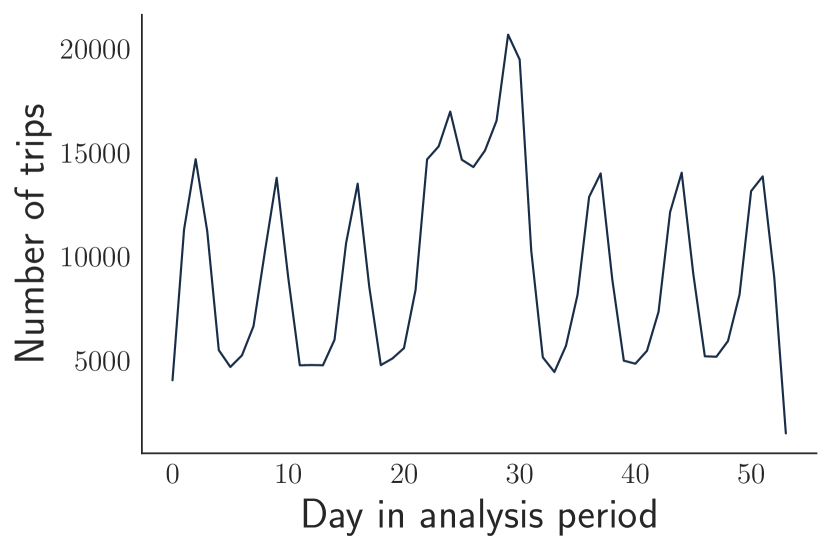

Markovian surge and model limitations. In practice, surge has strong intra-day patterns – for example, rush hours have higher average surge values, cf. Appendix Figure 9(b). However, evolution of surge on finer time scales, on the level of drivers’ individual trip decisions, is more volatile and believably Markovian, cf. Appendix Figure 9(c). Our theoretical model assumes that surge is Markovian and binary and the response of a single driver, and further ignores spatial effects. We discuss such issues in Sections A.3 and B.1, and our empirical analysis in Section 6 provides evidence that our insights extend to practice despite these theoretical limitations.

3 Incentive compatibility with affine pricing

In this section, we study the incentive compatibility of affine pricing. In Section 3.1, we first characterize the driver’s best-response strategy with respect to any pricing function in the single-state model. We then observe that multiplicative pricing, a special case of affine pricing where , is incentive compatible. In contrast, in Section 3.2, we show that in the dynamic model, multiplicative pricing may no longer be incentive compatible. We further derive the structure of optimal driver policies in each state with respect to affine or multiplicative pricing, which will enable numerical study of the incentive compatibility properties of additive and multiplicative surge in Section 5. Section 3.3 discusses the key differences in the two models, setting up Section 4 where we derive incentive compatible pricing functions for the dynamic model.

3.1 Single-state model: multiplicative pricing is incentive compatible

Our first result is a simple optimal driver policy in the single-state model.

Theorem 1.

With a single state, for each there exists a constant such that the policy is optimal for the driver with respect to .

Theorem 1 establishes that, in a single-state model with Poisson job arrivals, the length of the job is not important, only the hourly rate while busy on the job. The optimal in the policy is not necessarily : drivers must trade off the earnings rate while on a trip with their utilization rate; the more trips that a driver rejects, the longer the wait for an acceptable trip. In the appendix we prove the result by, starting at an arbitrary policy , making changes to the policy that increase the earnings rate while on a job without decreasing the utilization rate. Thus, each such change improves the reward , and the sequence of changes results in a policy of the above form, for some threshold . Then, this threshold can be optimized, leading to an optimal policy of this form.

An immediate corollary of Theorem 1 is that , for , is IC. In other words, if the platform pays a constant rate to busy drivers, then in the single-state model it is in the driver’s best interest to accept every trip. This result is driven by the following insight for Poisson arrivals: while receiving long trip requests is more beneficial to drivers in the single-state setting as they increase one’s utilization rate (the driver is busy for a longer time until the next open period), rejecting short trips to cherry-pick long trips decreases utilization by the same amount.101010This insight is similar to a result of Kamble (2019); however, in our setting the driver’s strategy is a subset of denoting the job requests accepted, as opposed to a discrete set of prices charged. Further, in our settings the driver responds to the platform’s prices instead of setting prices, enabling a wider range of IC pricing mechanisms. Further note that, given an earnings rate target , calculating the multiplier and thus an IC pricing policy is trivial.

On the other hand, affine pricing may not be incentive compatible because short trips are worth more per unit time than are long trips: . The optimal policy may thus be to accept trips in for some . However, our next proposition establishes that affine pricing is incentive compatible if the additive component stays small enough as a function of the request arrival rate:

[] With a single state, is incentive compatible if .

The sufficient condition has a simple intuition: when open, the expected amount of time the driver must wait for the next request is ; if on-trip time is valued at per unit-time, then with the additive component can be interpreted as paying for the driver’s expected waiting time. Thus, while a driver may earn more per hour for a short trip than a long trip with affine pricing, such a short trip is not worth the time the driver must wait for the next trip request. We further note that the condition in the proposition is not a necessary one; however, deriving necessary and sufficient conditions in closed form requires specifying the trip distribution .

As we’ll see in the next sub-section, the structure of optimal driver policies in reaction to affine pricing differs sharply in the dynamic model.

3.2 Dynamic model: multiplicative pricing is not incentive compatible

In the single-state model, multiplicative pricing is incentive compatible; a driver cannot benefit in the future by rejecting certain trips if all trips have the same on-trip earning rate. In contrast, we now show that the same insight does not hold for the dynamic model, as a driver can influence future trips through the decision to accept or reject certain trips.

Theorem 2.

If , there exists an optimal policy i.e., that maximizes , defined with parameters , such that

-

•

Non-surge state driver optimal policy :

-

–

If is multiplicative or positive affine, rejects long trips, i.e., .

-

–

If is negative affine, rejects short and long trips, i.e., .

-

–

-

•

Surge state driver optimal policy :

-

–

If is multiplicative or negative affine, rejects short trips, i.e., .

-

–

If is positive affine, rejects medium length trips, i.e., .

-

–

Furthermore, there exist settings where ’s take positive finite values, and in which multiplicative pricing is not incentive compatible in either state. Finally, only policies of the appropriate form as indicated (up to differences of measure 0) can be optimal.

We discuss the intuition in the next section. In the appendix, we prove the result for each case as follows: fixing for , we start with an arbitrary open set , recalling that open sets can be written as a countable union of such disjoint intervals. Then, we find , the derivative of the set function with respect to one of the interval upper end-points of , i.e., . This derivative is the infinitesimal change in the overall reward if is expanded by increasing , and it has useful properties. In the surge state with multiplicative pricing, for example, has the same sign as a function that is increasing in , for each fixed . With affine pricing, it has the same sign as a quasi-convex (positive affine in the surge state) or quasi-concave (negative affine in the non-surge state) function in , for a fixed . Such properties enable constructing a sequence of changes to that each do not decrease the reward , with the limit being a policy of the appropriate form. In particular, we can show that any policy that is not of the appropriate form above has for some , allowing local improvements until adjacent intervals can be combined or expanded to infinity. The numerics in Section 5 provide examples in which multiplicative pricing is not incentive compatible, i.e., where policies of the form above with positive finite constants strictly increase driver earnings over the driver policy that accepts all trip requests.

The results of rejecting long trips in non-surge (and short trips in surge) extend to arbitrary functions where is non-increasing (respectively, is non-decreasing). The other two results do not hold with such generality, as the behavior of the derivative may be arbitrarily complex.

3.3 Why is multiplicative surge pricing not incentive compatible?

| “I thoroughly dislike short trips ESPECIALLY when I’m picking up in a waning surge zone” |

| Anonymous driver |

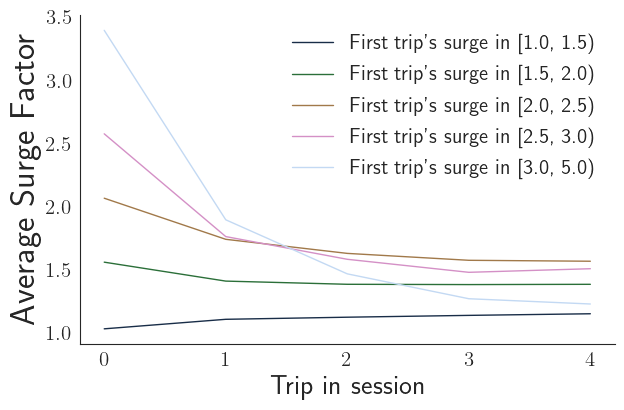

What explains the difference between multiplicative pricing being incentive compatible in the single-state model but not in the dynamic model? In the latter, a driver’s policy affects not just their earnings while they are busy, but also the fraction of time during which they are busy during the lucrative surge state. In particular, it turns out, accepting short trips during surge may reduce the amount of time that a driver is on a surge trip! Appendix Figure 7 shows in an example how the fraction of time in the surge state changes as a function of how many short trips the driver rejects.

The anonymous driver we quote above identifies the key effect: when surge is short-lived, a driver may only have the chance to complete one surge trip before it ends. Thus, the driver may be better off waiting to receive a longer trip request, as with multiplicative surge they are paid a higher rate for the full duration of the longer trip. (Of course, there is a trade-off as rejecting too many trip requests risks not receiving any acceptable request before surge ends). In the surge state, then, multiplicative pricing does not compensate drivers enough to accept short trips that may reduce their future surge earnings. In the non-surge state, analogously, multiplicative pricing under-values long trips that may prevent taking advantage of a future surge.

Affine pricing is a first, reasonable attempt at fixing these issues. In the surge state, the additive value makes the previously under-valued short trips comparatively more valuable, as the earnings per unit time (with ) are now higher for short trips. Unfortunately, with such pricing the structure for the surge optimal policy becomes – if the values are not balanced correctly, the additive value is enough to make accepting extremely short trips profitable; for medium-length trips , however, the additive value is not large enough to make up for the fact that accepting the trip prevents accepting another surged trip before surge ends. Similarly, negative affine pricing in the non-surge state, , (with ) is now too harsh on very short trips but potentially not enticing enough for long trips.

Next, we fix these issues and construct incentive compatible pricing schemes for our dynamic model. Then, in Section 5 we leverage structural results derived here to numerically compare the incentive compatibility of additive and multiplicative surge.

4 Incentive Compatible Surge Pricing

We now present our main result, regarding the structure of incentive compatible pricing in the dynamic model. To this aim, in Section 4.1, we characterize , how much time the driver spends in each state. In Section 4.2, we present incentive compatible prices, under a condition on the ratio of per-state earning rate constraints, . Section 4.3 discusses an intuition of the IC pricing structure in terms of the driver’s opportunity cost.

4.1 Transition probabilities and expected time spent in each state

The expected fraction of time spent in each state, , depends both on the evolution of the world state and the trips a driver accepts. To quantify the effects previewed in Section 3.3, we first analyze the evolution of the world state CTMC.

Lemma 2.

Suppose the world is in state at time . Let denote the probability that the world will be in state at time . Then,

Note that is not just the probability that the world state transitions once during time , but the probability that it transitions an odd number of times. This formulation emerges through a standard analysis of two-state CTMCs, in which this probability can be found through the inverse of the Laplace transform of the inverse of the resolvent of the Q-matrix for the system. Incorporating this value in closed form is the main hurdle in extending our results to general systems with more than two states. Using this formulation, the following lemma shows .

Lemma 3.

Let be as defined in Lemma 1. The fraction of time a driver following strategy spends either open in state or on a trip started in state is

We prove this lemma by finding the expected number of sub-cycles in each state , i.e., within a larger renewal reward cycle as defined, the expected number of sub-cycles that start with the driver being open in state . This expectation is the mean of a geometric random variable parameterized by the probability that the driver will next be open in state , given the driver is currently open in state . is proportional to this probability. (As with , there is a normalizing constant ); the larger it is, the fewer sub-cycles spent in state . It has two components: the first is the probability that the state changes before the driver accepts a trip request; the second is the probability that the world state is when the driver completes a trip. Thus, the numerator in is proportional to the length of a sub-cycle in state , times the fraction of sub-cycles that are started in state . The larger or , the more time the driver spends in state .

4.2 Incentive Compatible pricing in the dynamic model

How can the platform create incentive compatible pricing given the previously described effects? Our main result establishes when such IC prices exist, and reveals their form.

Theorem 3.

Let be target earning rates during non-surged and surge states, respectively. There exist prices of the form

where but may be either positive or negative, such that the optimal driver policy is to accept every trip in the surge state and all trips up to a certain length in the non-surge state. Furthermore, for , there exist fully incentive compatible prices of this form, where

and , and . For such prices, the driver policy to accept all requests is the unique optimal driver policy (up to differences of measure 0).

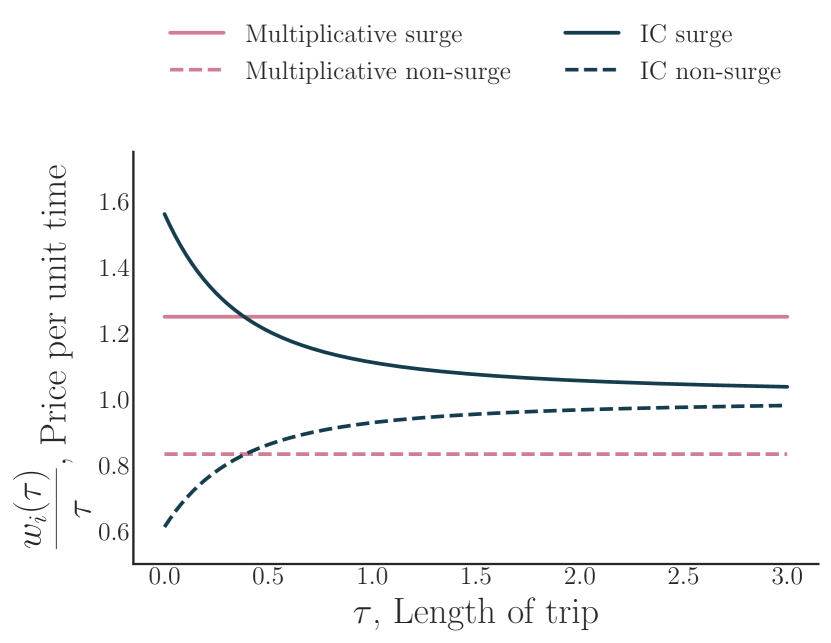

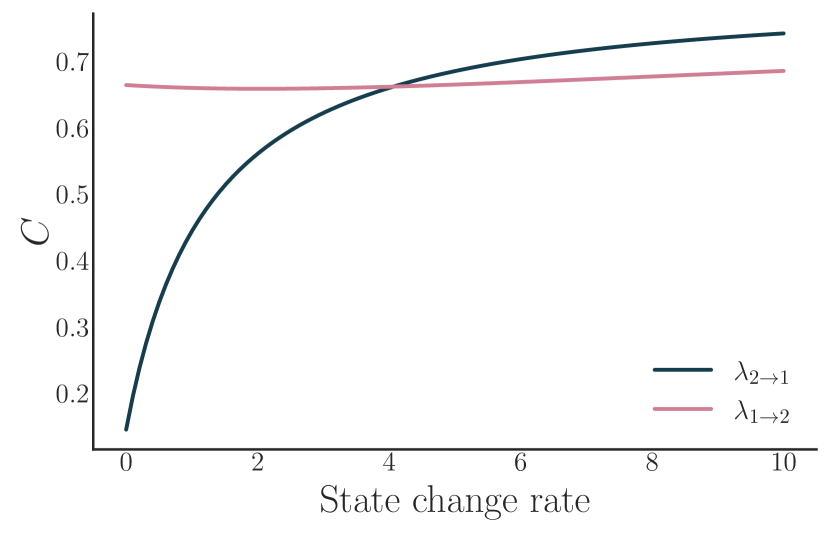

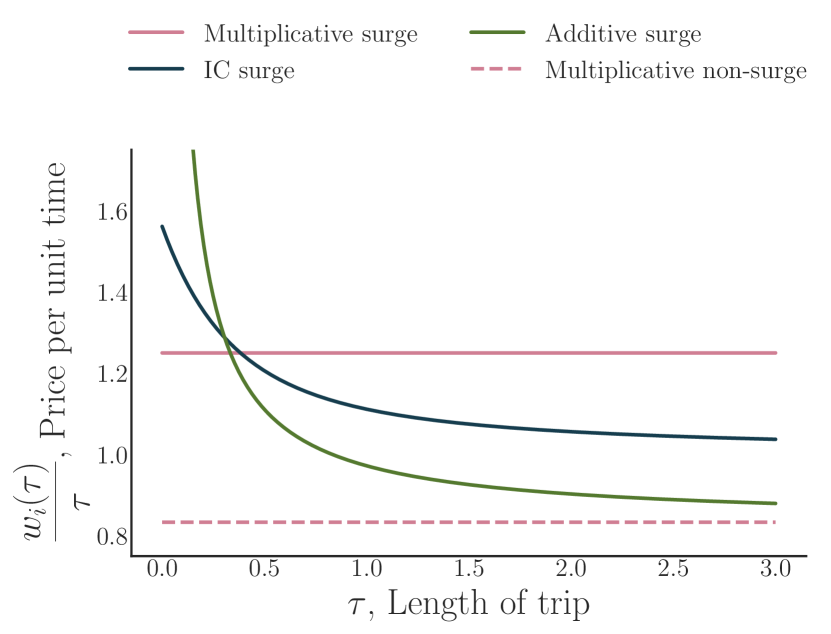

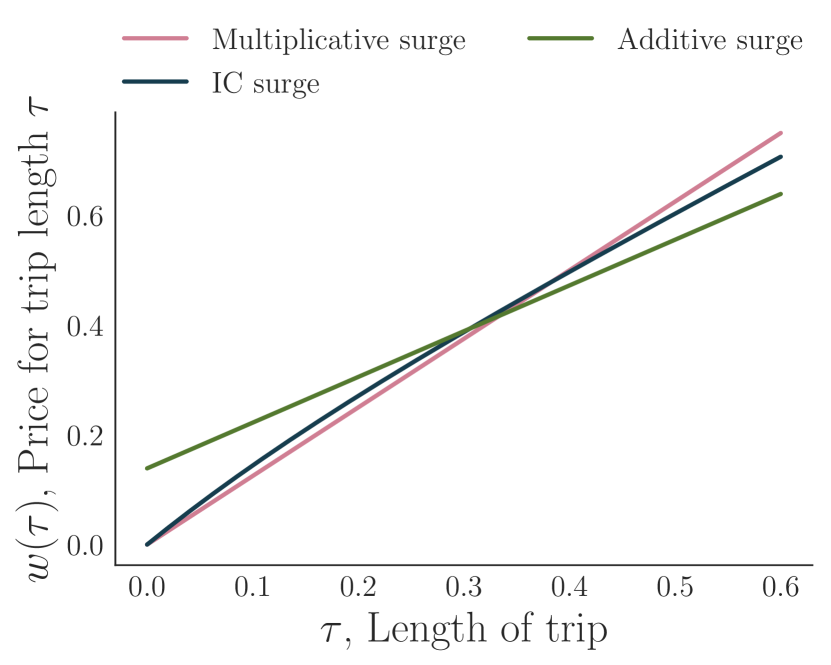

Section 4.4 contains a proof sketch. To convey intuition, Figure 2(a) shows pricing functions in each state, plotting against . Compared to multiplicative pricing with constant , IC surge pricing pays more for short trips and less for long trips. Inversely, IC non-surge pricing pays more for long trips than it does for short trips. Further, as increases, approaches , reflecting the fact that the opportunity cost for long trips does not depend as strongly on the state in which it started (as discussed in Section 4.3). Next, observe that IC surge pricing is approximately affine, as (plotted in Figure 2(b)) is upper bounded by . The two components of pricing, and , thus balance the comparative benefit of long and short trips. We give further intuition for the form of payment scheme and the range in Section 4.3, showing how they emerge from the driver’s opportunity cost.

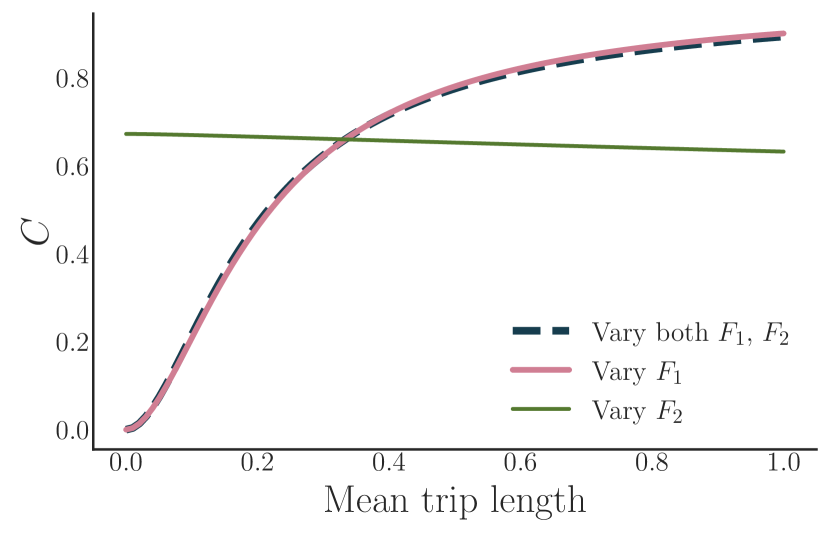

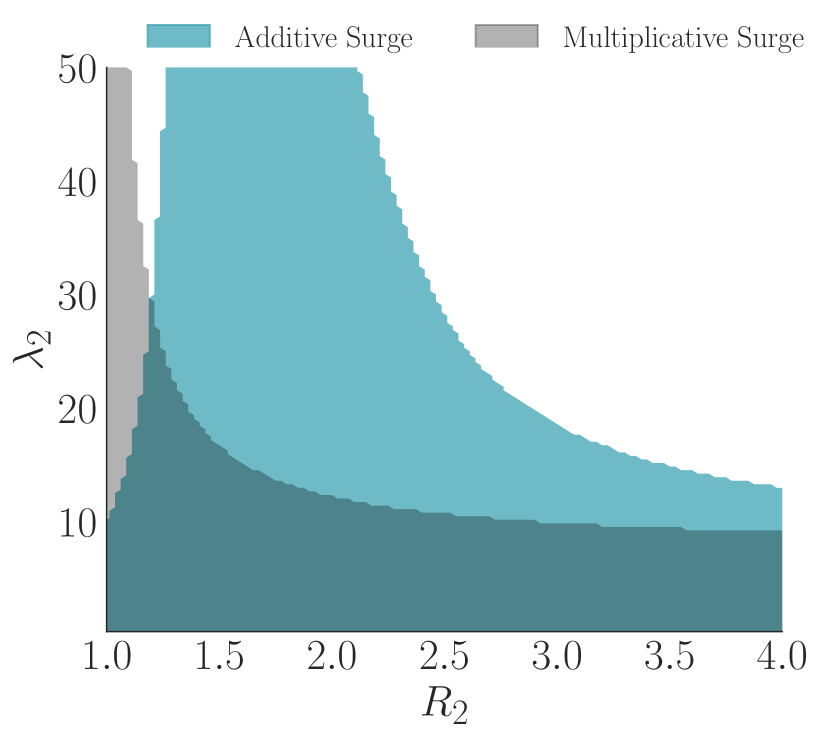

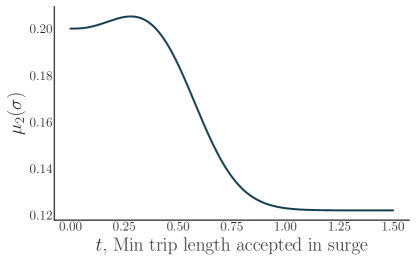

Rather surprisingly and contrary to platform design focus, the non-surge state is difficult to make incentive compatible. Our result establishes that there always exist payments, for any target driver earning rates , such that accepting every trip in the surge state is driver optimal; the same is not true for the non-surge state.111111For small enough, no pricing function can be incentive compatible in non-surge periods. A driver would rather wait for the far more lucrative surge state. Figure 3 shows how changes with the primitives.

Finally, for a given feasible , there is a range of that form an incentive compatible pricing scheme. Why? A driver who rejects a trip request waits to receive another request, during which time they do not earn money. This wait time tilts the driver toward accepting any trip request to maximize earnings. Thus, there is flexibility in the balance between short and long trip earnings. The same insight drives Proposition 1; even in the single-state model, trips do not have to have the same earnings per unit time, , as long as they meet some minimum threshold, .

4.3 Opportunity cost intuition for incentive compatible pricing

We now present some intuition to understand Theorem 3 and our incentive compatible pricing scheme. The payment must account for the driver’s opportunity cost (in a VCG-like manner), i.e., how much the driver can expect to earn if they instead reject the trip request. Of course, this opportunity cost itself depends on the pricing scheme . We now break down parts of this opportunity cost.

On-trip opportunity cost.

While the driver is on-trip, the world state continues to evolve: surge might end or start, affecting the opportunity cost.

Let be the expected amount of time that the world is in state during time , given that it is in state at time . Then, by integrating from to :

Several insights emerge:

One. As trip length , the first summand of each of dominates, and this component does not depend on starting state . As , we have , . The stationary distribution of a positive recurrent CTMC does not depend on the starting state. We cannot always construct incentive compatible prices, for any : as , the opportunity cost does not depend on the starting state , and so payments must be similar, . When all non-surge trips are long, i.e., is concentrated around large values, the earnings rate in each state must be similar, .

encodes such constraints, as shown in Figure 3. As the mean of goes to , then and so , and so the range of feasible expands. Similarly, also plays an important role. When small, the surge state is long. Thus, a driver will receive many trips during surge regardless of how long their last non-surge trip is—and so long trips during non-surge are no longer constrained to be highly paid compared to short trips.

Two. The expected time spent in each state has the form, , matching the form of our IC scheme. Thus, we can expect the “network minutes” on-trip opportunity cost – the expected earnings during the time the driver would otherwise be on the given trip – to have the same form as well.

Continuation value opportunity cost

It is not sufficient to consider just the opportunity cost for the duration of the trip: the driver’s counter-factual earnings by rejecting the trip depends on future trips accepted. Such counter-factual trips both (1) pay the driver according to their starting state even after a world state transition, i.e., the difference between and above; and (2) potentially are still in progress past time , when the current trip ends. This second complication is illustrated in Figure 7, where a driver can extend the time spent on trips starting in the surge state by rejecting short surge trips. The effect depends on the lengths of future potential trips, i.e., , and state transitions during those trips, , and is incorporated in both and the pricing scheme.

4.4 Proof sketch of Theorem 3

The result is shown in the appendix by manipulating the derivative of the reward function with respect to the policy . In particular, when the pricing function is of the given form with the appropriate constants , then any policy can be locally improved by adding more trips to it, i.e., the overall reward is increasing as the driver accepts more trips: . This result follows from , for all , given the constraints, where is an upper endpoint of the policy in a state, .

The key step is finding sufficient constraints for this derivative to be positive with a pricing function of the given form, given any , as opposed to just . This difficulty emerges because incentive compatibility is a global condition on the set function . In particular, we need to express these constraints simply—e.g., as a function of just , instead of the values . The presented in the theorem statement results from such a set of constraints on .

5 Numerics: Incentive Compatibility with Additive Surge

We now analyze surge policies that reflect practice at ride-hailing platforms today. Non-surge pricing is typically approximately multiplicative, i.e., , where is the base time (and distance) rate for a ride. We consider two types of affine surge pricing , which differ in their relationship to through a single parameter:

| Multiplicative surge: | ||||

| Additive surge: |

Multiplicative surge uses a multiplier larger than the base fare , and is reported on the heat-map as in Figure 1(a); additive surge uses the same base fare multiplier but adds a factor that is reported on the heat-map as in Figure 1(b). These functions are trivial to calculate, given fixed primitives and target earnings rate in the surge state.

Figure 8 in the Appendix shows these types of pricing, compared to the incentive compatible pricing function. Multiplicative surge has constant and so under-pays short trips and over-pays long-trips compared to IC pricing. Additive surge asymptotically (for large ) pays the same as multiplicative non-surge pricing, i.e. . As a result, it over-pays short trips and under-pays long trips compared to IC surge pricing.

Uber has recently started a transition from multiplicative to additive surge. In this section, we argue that the additive component is more important than the multiplicative component for incentive compatibility in parameter regimes of interest.

5.1 Computing optimal driver policies

Theorem 2 establishes that multiplicative pricing (and, more generally, affine pricing) may not be incentive compatible in general. However, we still wish to compare the various types of surge pricing, and to analyze the regimes under which each is incentive compatible.

However, to do this comparison, one needs to calculate optimal driver policies with respect to a pricing function. Recall that the optimal driver policy in each state is some subset of . Finding such optimal subsets for general pricing functions is intractable, and so Theorem 2 is particularly important for computational reasons. It establishes that, for any affine pricing structure in the surge state, all driver optimal policies are of the form , for some . We only need to find the values for these parameters that maximize the driver reward among sets of this form, and the resulting policy is optimal; this search is tractable with grid search and numeric integration. Note that the proposition does not establish uniqueness of driver optimal policies; we thus choose the policy that maximizes the fraction of trips accepted in our computations.

5.2 Results

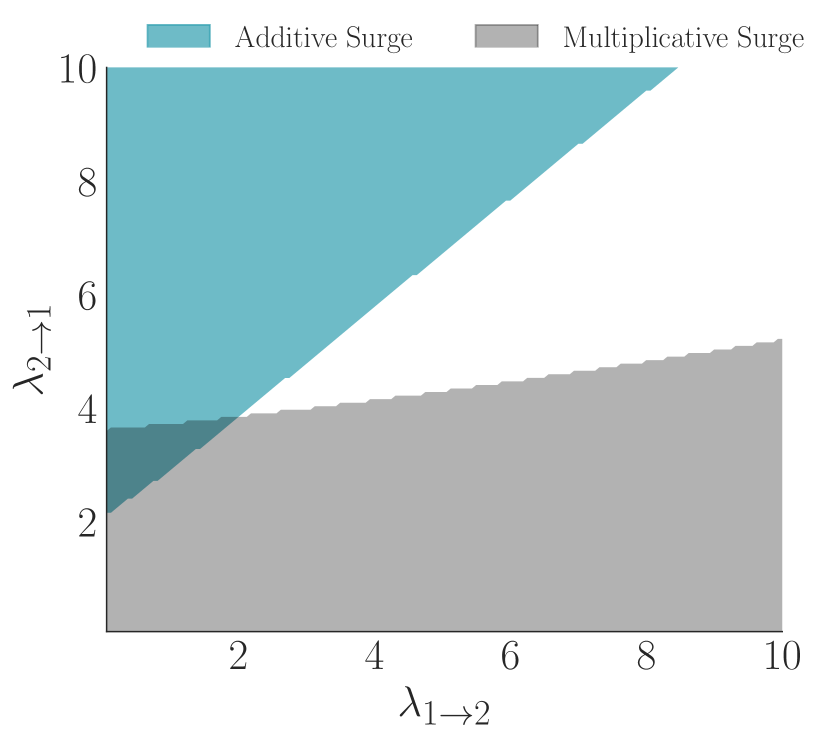

We now study the regimes in which each surge mechanism is incentive compatible. The shaded regions in Figure 4 correspond to areas where the surge pricing function is fully incentive compatible in the surge state ( is optimal). For example, when , additive surge is incentive compatible, but multiplicative surge is not.

As illustrated in Appendix B with data from the RideAustin marketplace, ride-hailing platforms most often operate in the following parameter regimes: (1) surge is between and times more valuable than non-surge; (2) surge is short-lived compared to non-surge periods (); (3) and in a typical surge the driver receives several trip requests (, but small) but only completes one or two such trips ( mean trip length). Additive surge is incentive compatible in much more of this regime than is multiplicative surge, supporting Uber’s recent shift from multiplicative to additive surge.

We can also draw qualitative insights in terms of sensitivity to the primitives, similar in spirit to effects in the form of in Theorem 3. Figure 4(a) shows the sensitivity with respect to and . As the arrival rate of jobs in the surge state, , increases, it becomes optimal for the driver to reject some trips: “cherry-picking” becomes easier, as the driver is likely to receive many more trip requests before surge ends. Similarly, as surge becomes increasingly more valuable compared to non-surge ( increases), the incentive to reject non-valuable trips in the surge state increases.

Additive surge contains an interesting non-monotonicity: when , the effect above dominates, and long trips are rejected. When the surge state is moderately more valuable than non-surge, additive surge effectively balances the payments for different trip lengths and so is incentive compatible. When the two states are nearly equally valuable, again the optimal driver policy rejects long trips: our single-state model approximates the system, and so additive surge may not be incentive compatible, cf. Theorem 1.

Figure 4(b) shows the effects of the relative lengths of surge and non-surge. Here, the two types of surge are incentive compatible in opposing regimes. When is large, surge is comparatively rare and short, and so short trips are naturally under-valued – accepting them decreases the time spent in the surge state – and additive surge is incentive compatible. With long-lasting surge (small ), on the other hand, the world almost seems unchanging during surge, and so multiplicative surge becomes incentive compatible.

The short, in-frequent surge setting – in which additive surge is preferable – is pre-dominant in the RideAustin data used in Section 6. Nevertheless, our analysis suggests that when surge is expected to last throughout the day, such as with a predictable demand shock, multiplicative surge may be preferable. (However, switching between different payment functions may be undesirable for transparency and communication reasons).

6 Empirical Comparison of Surge Mechanisms

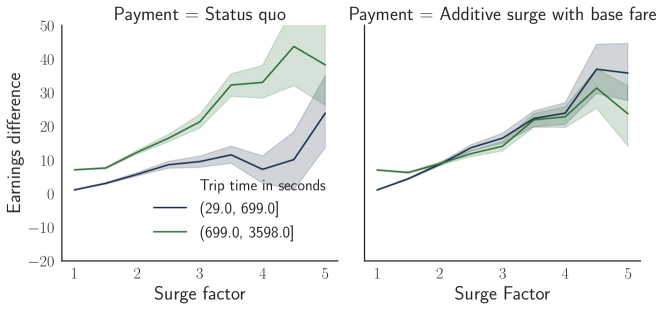

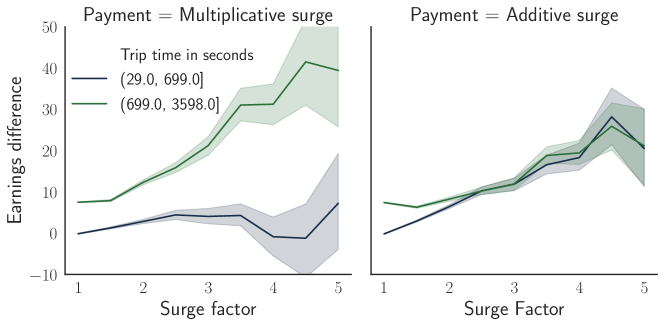

We now study how the various surge mechanisms affect driver earnings in practice using publicly available trips data from RideAustin, a nonprofit ride-hailing company based and operating in Austin, Texas. We show that additive surge effectively balances the relative value of short and long surged trips, in contrast to the multiplicative surge pricing scheme used in practice by the platform, which comparatively undervalues short surged trips.

After reverse-engineering the functional form of the actual driver payments, we calculate both status quo (with multiplicative surge) and simulated (with additive surge) driver earnings. For each payment scheme, we estimate the driver’s value in receiving and accepting a given trip request, as a function of the trip—where “value” is the increase (or decrease) in the driver’s earnings over the next 90 minutes as a result of accepting the given request.

We note that this data is not the result of an experiment with additive surge, and thus our analysis describes what changes would occur in driver earnings with the new pricing function if driver behavior does not change.121212We are not concerned with rider behavior changing, as with decoupled pricing the rider pricing can remain the same even as the driver payments change. Thus, the additive surge exercise is a calibrated simulation for such pricing functions in a realistic setting: such as when surge has more than two levels and may not evolve in a Markovian manner, the driver is not paid for the time it takes to drive to the rider, and where location plays a role. Furthermore, as the data observed is at the completed trip level (i.e., requests which the driver accepted), results showing that the driver would be better off accepting the same trip in the counter-factual world should directionally hold even as driver behavior changes.

This section is organized as follows: Section 6.1 describes the data, context, and analysis, and Section 6.2 contains results. Appendix Section B contains supporting details, and both the data (RideAustin, 2017) and our replication code is available online.131313https://github.com/nikhgarg/driver_surge_rideaustin

6.1 Data setting and analysis description

This analysis is enabled by the rich dataset, spanning from June 2016 to April 2017, during which RideAustin experienced tremendous growth and was one of the largest ride-hailing marketplaces serving the area. The data is at the completed trip level. Komanduri et al. (2018) study the same dataset and provide useful statistics about driver earnings, platform growth, and the service’s relationship to public transportation.

We consider the period from February 16, 2017, to April 10, 2017, as (1) we can reliably reverse engineer the platform’s payment function during this period, and (2), the underlying marketplace was fairly stable during this period, except for one week of high, atypical demand and surge, corresponding to the SXSW Music Festival held in Austin. (Figure 10(a) in the Appendix shows the trips per day during this period). We discard trips longer than 1 hour or shorter than 30 seconds and other trips with data errors; such trips were discarded. We analyze completed trips by drivers. (For analyses aggregating multiple trips, such as driver earnings in a given time period, we discard aggregations that include a discarded trip). The full pre-processing sequence is described in the appendix.

Several dataset features make it attractive for our analysis when compared to other publicly available ride-hailing datasets. Most importantly, there are consistent driver IDs attached to each trip. Second, for each trip, there is a value for the total fare paid by the rider, along with terms that contribute to this calculated fare: trip duration (in time and distance), payment rate (in time and distance), surge factor, standard additive fare (Pickup), and trip class (Regular vs Luxury vs SUV).141414Our results include trips from all trip classes, as a given driver may be cross-dispatched across trip classes. These features allow us to track a driver’s trajectory and earnings over a day and the entire year, reverse engineer how RideAustin calculates payments, and simulate additive surge payments.

6.1.1 Constructing payment functions

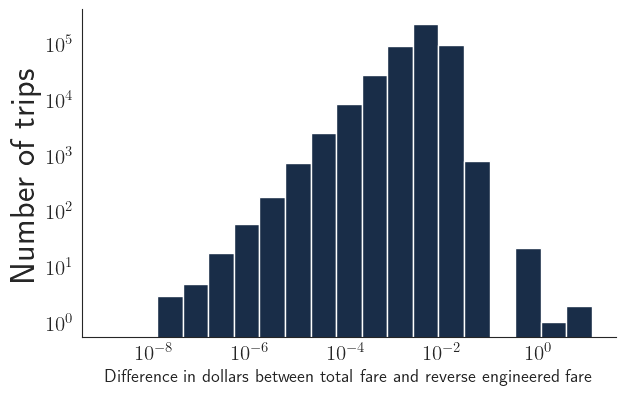

To simulate driver earnings with additive surge, we must first reverse engineer how the platform’s actual total fare was calculated, a non-trivial task as the calculation changes over time in the dataset and is not documented. We find that this status quo fare is approximately:151515The payment includes a multiplier of 1.01 and an additive value of 2.02. From publicly available information, we assume that the platform takes a fixed commission independent of trip length, and so the driver receies everything but the (RideAustin, 2019). On average, this reversed engineered fare differs from total fare by less than cent.

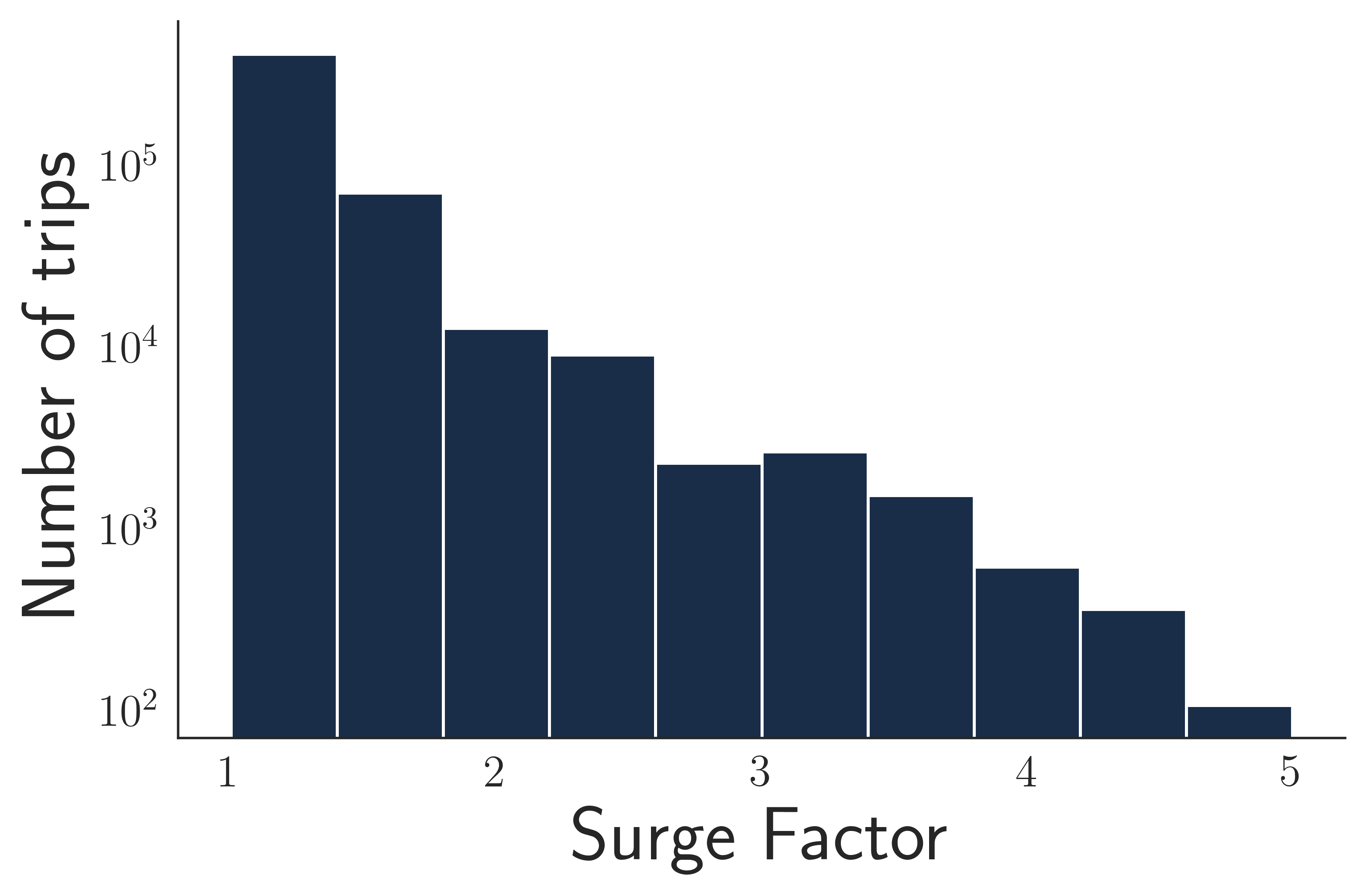

is the trip time and distance fare, only counting when the rider is in the car (recall that current practice deviates from the theory in that driving to the rider is typically unpaid). MinFareForClass is for Regular trips and otherwise. SurgeFactor of indicates no surge, comprising of trips. It increments in multiples of , and of surged trips have a factor of at most . Each of the above payment components are given as columns in the dataset.

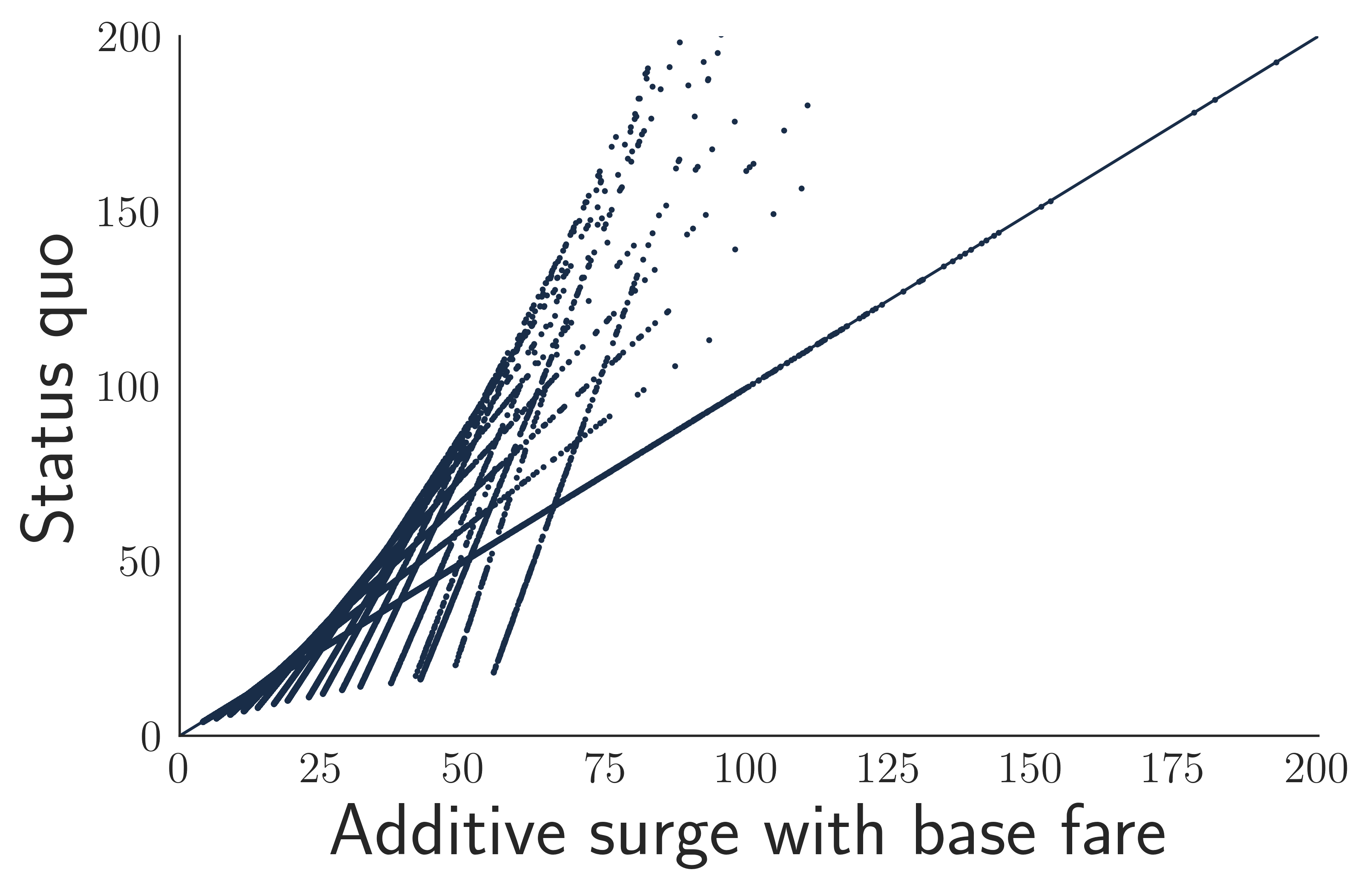

Then, we construct the following payment for each trip, to simulate how the driver would be paid with additive surge, i.e., Additive surge with base fare:

are (calculated) surge factor dependent constants that are set such that this alternative payment function spends the same amount of money overall for each surge factor as does the status quo fare. In other words, the alternative payment does not change the mean trip payment conditional on the surge factor, but does change how money is allocated to various trips within that surge. This choice reflects our theory in assuming an exogenous and removes any degrees of freedom in setting . If instead we used a single constant across surge factors, Additive surge with base fare may pay different amounts on average for the same surge factor than does the status quo fare.

6.1.2 Matching open drivers

We are interested in the value of a trip request to a driver ; to calculate this value, we need a measure of the counter-factual: what would have happened if the driver does not accept (or does not receive) a trip of length . We match the focal driver of each given completed trip to a nearby driver who is also open to receive a trip request at the time of the request. Driver ’s earnings then serve as a counter-factual for focal driver ’s earnings had driver rejected the request.

We estimate matches for each focal driver as follows. We observe trip start and end times and locations but not driver locations when they are not on a trip or even whether they still have their app open. We also observe the time at which a driver received a given trip request but not their location at this time, due to what seems like a data export bug.

This data does not allow us to simply query for other open drivers nearby who could have (but did not) receive a given trip request, as we do not directly observe drivers’ movements while they are not on a trip. Instead, we leverage recent, nearby completed trips to identify drivers who must still be nearby, as follows.

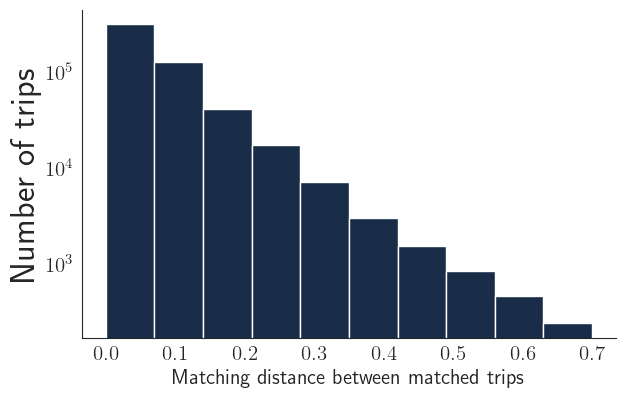

First, we define a “matching distance” between pairs of (date-time, location) tuples. Events with small matching distances occur nearby and at similar times. The exact function with how time and geographic distance are weighted is specified in the appendix. For driver’s ’s time and location, we use the trip’s start location (where the rider was) and the dispatch time (when the rider’s request was accepted). Then, we find a driver who recently completed a trip nearby and has yet to start another trip. We do so by calculating the matching distance between driver and each recent completed trips’ destination time and location. We choose the closest match, filtering out drivers who are the same as the given trip’s driver, who have started another trip before the given trip’s start time, or who ended their session (did not start any trip in the next hour).

In the appendix, we provide results from a different but complementary matching method, as well as additional information about the matches and their quality.

6.1.3 Calculating the value of a trip to a driver

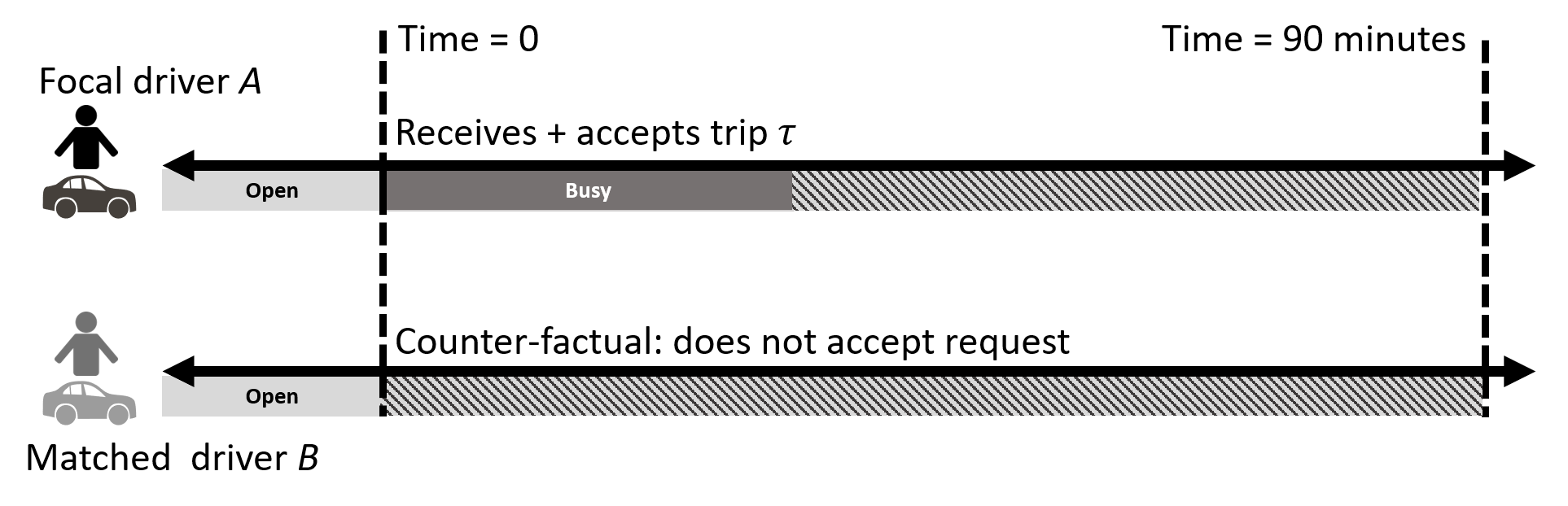

We now measure how valuable a trip is to a driver, through a notion we call trip indifference: given a specific trip request length , in expectation the driver is at least as well off accepting the request as rejecting it, assuming some future behavior. Given focal driver with trip request and a matched driver , we estimate this measure as illustrated in Figure 5: we compare the two drivers’ future earnings over the 90 minutes after the accepted trip begins—the higher driver ’s earnings over that of matched driver , the more valuable the given trip request . If there is no difference, i.e., the matched driver in expectation earns the same amount, then the given driver should be “indifferent” between accepting or rejecting the request.161616Trip indifference is related to our theoretical notion of incentive compatibility as follows. Suppose the given driver accepts all future requests over the next 90 minutes. Then, if a payment scheme is incentive compatible, the earnings difference between the given driver who accepts trip and the matched driver will be at least for all .

Suppose trips are mis-priced and do not fully incorporate the drivers’ temporal externalities. Then, trips of different lengths would vary in the value delivered to drivers. We would expect to see the average earnings differential, conditional on trip length, to vary as a function of the trip length; i.e., receiving a long trip during surge may be more valuable to a driver than is receiving a short trip.171717Bias in the matching process may shift the expected earnings difference, but should not differentially affect the measurement for each payment function: the same matches are used for each. As robustness checks, in the appendix we vary both the matching function and the length of time over which we calculate the two drivers’ earnings.

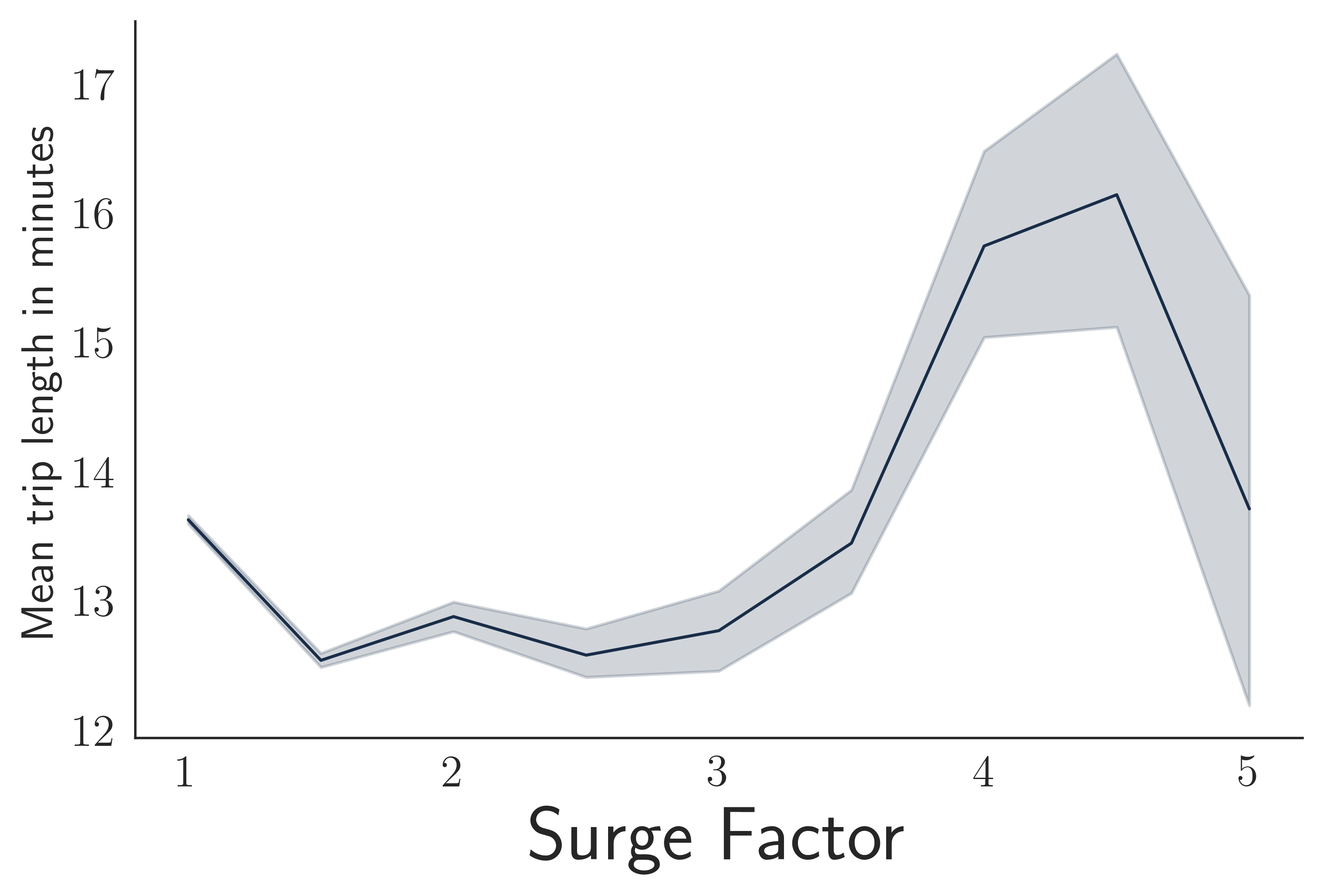

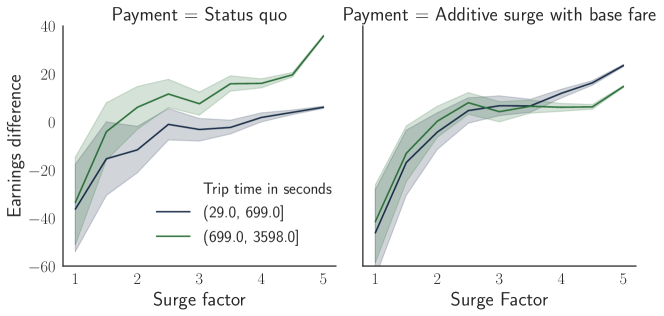

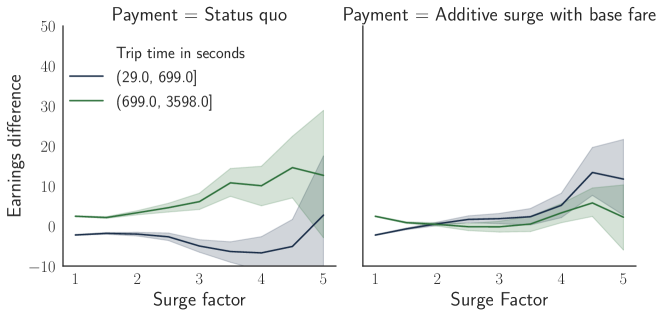

6.2 Results: value of short versus long trips

Figure 6 shows the difference in value between short (below the median trip length) and long (above the median) trips, as it changes with surge. As expected, it is more beneficial for drivers to receive trips with higher surge factors. However, with the platform’s existing multiplicative surge payment function, only long trips become more valuable as the surge factor increases; even at high surge factors, drivers would have often had higher earnings had they rejected short trip requests. With additive surge, in contrast, trips of all lengths become more beneficial on average as surge increases. During high surge times, additive surge increases the value of short trips by about per hour.

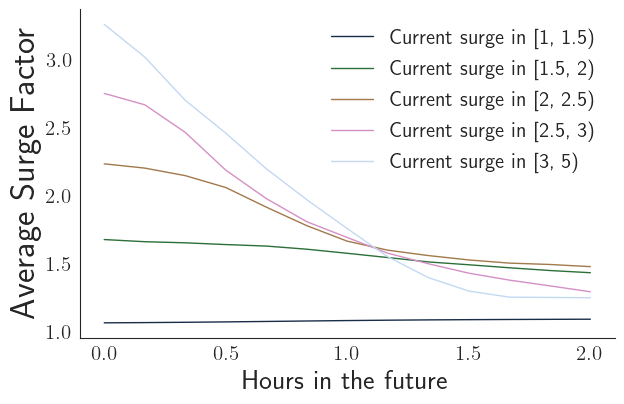

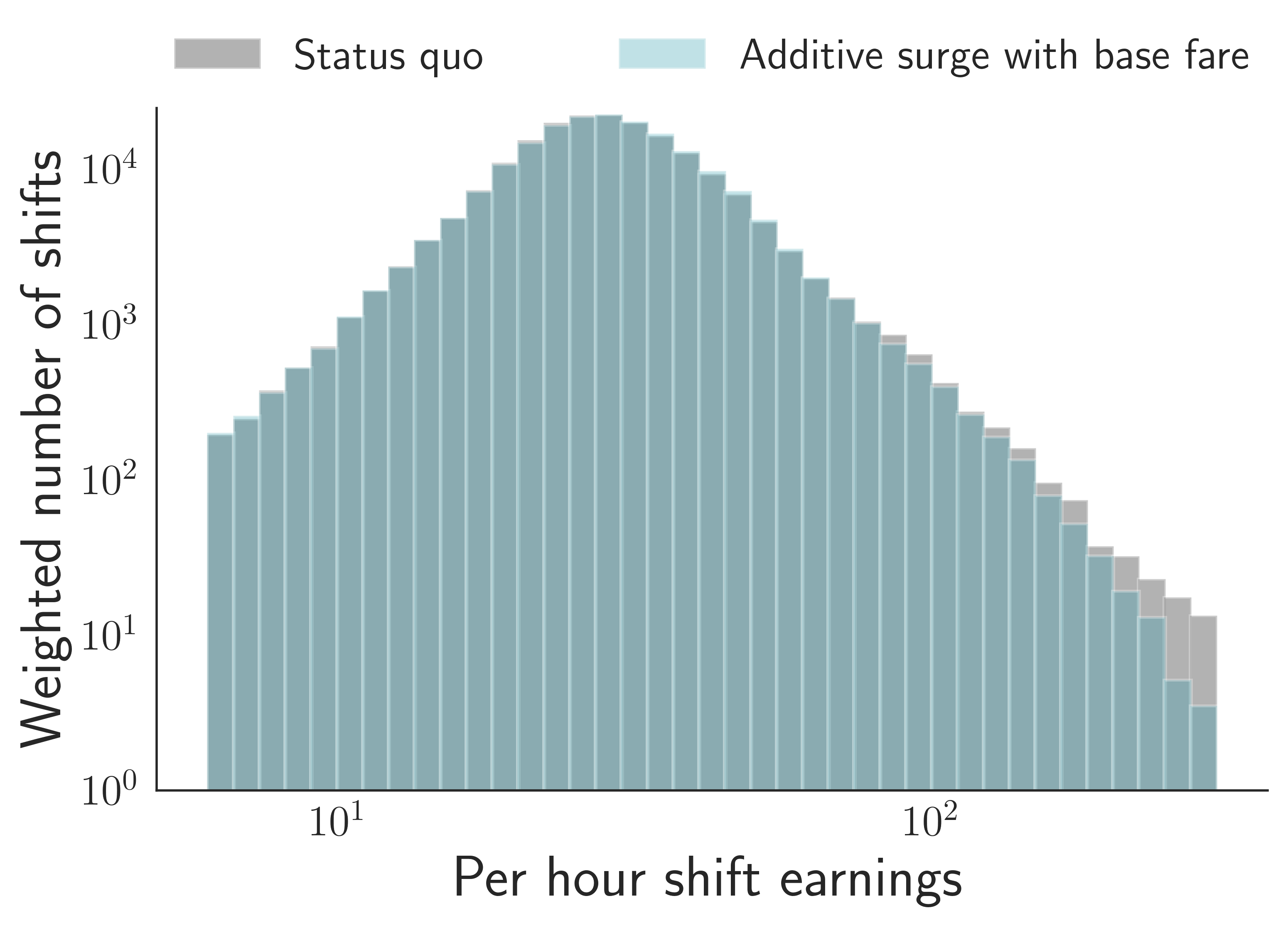

In the appendix, we further simulate a world with the RideAustin data, but with surge being common and extremely valuable (we “flip” the surge factor). This analysis illustrates that our other insights also extend to practice, with there being settings where non-surge periods cannot be made incentive compatible, and where neither multiplicative nor additive surge correctly balance the value of short and long trips. We also show how hourly driver earnings during a single “shift” change with additive and multiplicative surge, and how the former leads to more stable earnings. Overall, this analysis suggests the substantial difference that changing the structure of payments can make, and the comparative benefits of additive surge in practice under common regimes in ride-hailing.

7 Conclusion

In this work, we studied the problem of designing incentive compatible mechanisms for ride-hailing marketplaces. We presented a dynamic model to capture essential features of these environments. Even-though our model is simple and stylized, it highlights how driver incentives and subsequently dynamic pricing strategies would change in the presence of stochasticity. Our numeric and empirical analysis suggests the importance of such components in practice. We hope our work inspires other researchers in this area to incorporate such uncertainty in their models, as it is one of the biggest challenges faced in practice.

An important direction for extending our work is studying matching and pricing polices jointly, i.e., how to best match open drivers to riders in the presence of such effects, cf. (Özkan and Ward, 2016; Banerjee et al., 2017a, b; Feng et al., 2017; Zhang et al., 2017; Banerjee et al., 2018; Hu and Zhou, 2018; Korolko et al., 2018; Özkan, 2018; Ashlagi et al., 2018; Kanoria and Qian, 2019). In this work, we look at incentive compatible pricing. The platform, in addition to pricing, can use matching policies to align incentives.

References

- Afèche et al. (2018) Philipp Afèche, Zhe Liu, and Costis Maglaras. Ride-Hailing Networks with Strategic Drivers: The Impact of Platform Control Capabilities on Performance. SSRN Electronic Journal, 2018. ISSN 1556-5068. doi: 10.2139/ssrn.3120544. URL https://www.ssrn.com/abstract=3120544.

- Asadpour et al. (2019) Arash Asadpour, Daniel Freund, and Garrett J. van Ryzin. Escrow Payments: A Smoother Driver Pay Mechanism, October 2019. URL https://www.abstractsonline.com/pp8/#!/6818/presentation/7365.

- Ashlagi et al. (2018) Itai Ashlagi, Maximilien Burq, Patrick Jaillet, and Amin Saberi. Maximizing efficiency in dynamic matching markets. arXiv preprint arXiv:1803.01285, 2018. URL https://arxiv.org/pdf/1803.01285.pdf.

- Ata et al. (2019) Baris Ata, Nasser Barjesteh, and Sunil Kumar. Spatial Pricing: An Empirical Analysis of Taxi Rides in New York City. Working Paper, 2019.

- Auerbach (2019) Shane Auerbach. Paying Rideshare Drivers for Pickups, October 2019. URL https://simons.berkeley.edu/talks/tbd-78.

- Bai et al. (2018) Jiaru Bai, Kut C. So, Christopher S. Tang, Xiqun (Michael) Chen, and Hai Wang. Coordinating Supply and Demand on an On-Demand Service Platform with Impatient Customers. Manufacturing & Service Operations Management, June 2018.

- Banerjee et al. (2015) Siddhartha Banerjee, Carlos Riquelme, and Ramesh Johari. Pricing in Ride-Share Platforms: A Queueing-Theoretic Approach. SSRN Electronic Journal, 2015. ISSN 1556-5068. doi: 10.2139/ssrn.2568258. URL http://www.ssrn.com/abstract=2568258.

- Banerjee et al. (2017a) Siddhartha Banerjee, Daniel Freund, and Thodoris Lykouris. Pricing and optimization in shared vehicle systems: An approximation framework. In Proceedings of the 2017 ACM Conference on Economics and Computation, pages 517–517. ACM, 2017a.

- Banerjee et al. (2017b) Siddhartha Banerjee, Sreenivas Gollapudi, Kostas Kollias, and Kamesh Munagala. Segmenting two-sided markets. In Proceedings of the 26th International Conference on World Wide Web, pages 63–72, 2017b.

- Banerjee et al. (2018) Siddhartha Banerjee, Yash Kanoria, and Pengyu Qian. State Dependent Control of Closed Queueing Networks with Application to Ride-Hailing. March 2018. URL http://arxiv.org/abs/1803.04959.

- Bertsimas and van Ryzin (1991) Dimitris J. Bertsimas and Garrett van Ryzin. A Stochastic and Dynamic Vehicle Routing Problem in the Euclidean Plane. Operations Research, 39(4):601–615, August 1991. ISSN 0030-364X, 1526-5463.

- Bertsimas and van Ryzin (1993) Dimitris J. Bertsimas and Garrett van Ryzin. Stochastic and Dynamic Vehicle Routing in the Euclidean Plane with Multiple Capacitated Vehicles. Operations Research, 41(1):60–76, February 1993. ISSN 0030-364X, 1526-5463.

- Besbes et al. (2018a) Omar Besbes, Francisco Castro, and Ilan Lobel. Spatial Capacity Planning. SSRN Electronic Journal, 2018a. ISSN 1556-5068. doi: 10.2139/ssrn.3292651. URL https://www.ssrn.com/abstract=3292651.

- Besbes et al. (2018b) Omar Besbes, Francisco Castro, and Ilan Lobel. Surge Pricing and Its Spatial Supply Response. SSRN Electronic Journal, 2018b. ISSN 1556-5068. doi: 10.2139/ssrn.3124571. URL https://www.ssrn.com/abstract=3124571.

- Bikhchandani (2020) Sushil Bikhchandani. Intermediated surge pricing. Journal of Economics & Management Strategy, 29(1):31–50, 2020.

- Bimpikis et al. (2016) Kostas Bimpikis, Ozan Candogan, and Daniela Saban. Spatial Pricing in Ride-Sharing Networks. (ID 2868080), November 2016. URL https://papers.ssrn.com/abstract=2868080.

- Buchholz (2017) Nicholas Buchholz. Spatial Equilibrium, Search Frictions and Efficient Regulation in the Taxi Industry. 2017. URL https://scholar.princeton.edu/sites/default/files/nbuchholz/files/taxi_draft.pdf.

- Cachon et al. (2017) Gérard P. Cachon, Kaitlin M. Daniels, and Ruben Lobel. The Role of Surge Pricing on a Service Platform with Self-Scheduling Capacity. Manufacturing & Service Operations Management, 19(3):368–384, June 2017. ISSN 1523-4614.

- Castillo et al. (2017) Juan Camilo Castillo, Dan Knoepfle, and Glen Weyl. Surge Pricing Solves the Wild Goose Chase. pages 241–242. ACM Press, 2017. ISBN 978-1-4503-4527-9. doi: 10.1145/3033274.3085098. URL http://dl.acm.org/citation.cfm?doid=3033274.3085098.

- Chen and Sheldon (2016) M Keith Chen and Michael Sheldon. Dynamic Pricing in a Labor Market: Surge Pricing and Flexible Work on the Uber Platform. 2016. doi: 10.1145/2940716.2940798.

- Chen and Hu (2018) Yiwei Chen and Ming Hu. Pricing and Matching with Forward-Looking Buyers and Sellers. SSRN Scholarly Paper ID 2859864, Social Science Research Network, Rochester, NY, July 2018. URL https://papers.ssrn.com/abstract=2859864.

- Cook et al. (2018) Cody Cook, Rebecca Diamond, Jonathan Hall, John List, and Paul Oyer. The Gender Earnings Gap in the Gig Economy: Evidence from over a Million Rideshare Drivers. June 2018. doi: 10.3386/w24732. URL https://www.nber.org/papers/w24732.

- Cramer and Krueger (2016) Judd Cramer and Alan B. Krueger. Disruptive Change in the Taxi Business: The Case of Uber. American Economic Review, 106(5):177–182, May 2016. ISSN 0002-8282. doi: 10.1257/aer.p20161002.

- Feng et al. (2017) Guiyun Feng, Guangwen Kong, and Zizhuo Wang. We are on the way: Analysis of on-demand ride-hailing systems. 2017.

- Glazer and Hassin (1983) Amihai Glazer and Refael Hassin. The economics of cheating in the taxi market. Transportation Research Part A, 17(1):25–31, 1983.

- Guda and Subramanian (2019) Harish Guda and Upender Subramanian. Your uber is arriving: Managing on-demand workers through surge pricing, forecast communication, and worker incentives. Management Science, 65(5):1995–2014, 2019. doi: 10.1287/mnsc.2018.3050. URL https://doi.org/10.1287/mnsc.2018.3050.

- Hall et al. (2015) Jonathan V. Hall, Cory Kendrick, and Chris Nosko. The effects of Uber’s surge pricing: A case study. 2015. URL https://eng.uber.com/research/the-effects-of-ubers-surge-pricing-a-case-study/.

- Hall et al. (2017) Jonathan V. Hall, John J. Horton, and Daniel T. Knoepfle. Labor Market Equilibration: Evidence from Uber. 2017. URL https://eng.uber.com/research/labor-market-equilibration-evidence-from-uber/.

- Hu and Zhou (2018) Ming Hu and Yun Zhou. Dynamic type matching. Rotman School of Management Working Paper, (2592622), 2018.

- Kamble (2019) Vijay Kamble. Revenue Management on an On-Demand Service Platform. Operations Research Letters, 47(5):377–385, 2019.

- Kanoria and Qian (2019) Yash Kanoria and Pengyu Qian. Near Optimal Control of a Ride-Hailing Platform via Mirror Backpressure. March 2019. URL http://arxiv.org/abs/1903.02764.

- Komanduri et al. (2018) Anurag Komanduri, Zeina Wafa, Kimon Proussaloglou, and Simon Jacobs. Assessing the impact of app-based ride share systems in an urban context: Findings from austin. Transportation Research Record, 2672(7):34–46, 2018.

- Korolko et al. (2018) Nikita Korolko, Dawn Woodard, Chiwei Yan, and Helin Zhu. Dynamic Pricing and Matching in Ride-Hailing Platforms. SSRN Electronic Journal, page 40, 2018. ISSN 1556-5068. doi: 10.2139/ssrn.3258234. URL https://www.ssrn.com/abstract=3258234.

- Lei and Jasin (2016) Yanzhe Lei and Stefanus Jasin. Real-time dynamic pricing for revenue management with reusable resources and deterministic service time requirements. 2016.

- Lu et al. (2018) Alice Lu, Peter I. Frazier, and Oren Kislev. Surge Pricing Moves Uber’s Driver-Partners. In Proceedings of the 2018 ACM Conference on Economics and Computation, EC ’18, pages 3–3, New York, NY, USA, 2018. ACM. ISBN 978-1-4503-5829-3. doi: 10.1145/3219166.3219192.

- Ma et al. (2018) Hongyao Ma, Fei Fang, and David C. Parkes. Spatio-Temporal Pricing for Ridesharing Platforms. January 2018. URL http://arxiv.org/abs/1801.04015.

- Ong et al. (2020) Hao Yi Ong, Daniel Freund, and Davide Crapis. Driver positioning and incentive budgeting with an escrow mechanism for ridesharing platforms, 2020.

- Özkan (2018) Erhun Özkan. Joint pricing and matching in ridesharing systems. 2018.

- Özkan and Ward (2016) Erhun Özkan and Amy Ward. Dynamic Matching for Real-Time Ridesharing. SSRN Electronic Journal, 2016. ISSN 1556-5068. doi: 10.2139/ssrn.2844451. URL http://www.ssrn.com/abstract=2844451.

- RideAustin (2017) RideAustin. Dataset, 2017. URL https://data.world/ride-austin.

- RideAustin (2019) RideAustin. Driver rates, 2019. URL {http://www.rideaustin.com/drivers/rates}.

- Uber (2019a) Uber. Community Guidelines, 2019a. URL https://www.uber.com/legal/community-guidelines/us-en/.

- Uber (2019b) Uber. Dependable Earnings, 2019b. URL https://www.uber.com/drive/resources/dependable-earnings/.

- Uber (2019c) Uber. New Driver Surge, 2019c. URL https://www.uber.com/blog/your-questions-about-the-new-surge-answered/.

- Uber (2019d) Uber. How are fares calculated, 2019d. URL https://help.uber.com/riders/article/how-are-fares-calculated?nodeId=d2d43bbc-f4bb-4882-b8bb-4bd8acf03a9d.

- Uber (2019e) Uber. Service Fee, 2019e. URL https://marketplace.uber.com/pricing/service-fee.

- Wald (1973) Abraham Wald. Sequential Analysis. Courier Corporation, 1973.

- Yang et al. (2018) Pu Yang, Krishnamurthy Iyer, and Peter Frazier. Mean field equilibria for resource competition in spatial settings. Stochastic Systems, 8(4):307–334, 2018.

- Zhang et al. (2017) Lingyu Zhang, Tao Hu, Yue Min, Guobin Wu, Junying Zhang, Pengcheng Feng, Pinghua Gong, and Jieping Ye. A taxi order dispatch model based on combinatorial optimization. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 2151–2159. ACM, 2017.

APPENDIX TABLE OF CONTENTS

Appendix A Additional discussion and information

Appendix B More empirics

Appendix C Proofs of single state model results

Appendix D Proofs of dynamic model results

Appendix A Additional discussion and information

A.1 Platform objective

Our focus in this work is on designing incentive compatible payment functions for drivers. Here, we establish that this task is a sub-problem of the comprehensive platform pricing problem—one that can be studied separately given the components we considered exogenous in our model description. We work with the dynamic model, and suppose that the platform’s primary objective is profit (our argument also trivially holds for revenue, trips served, welfare, or other objectives). With our assumption of a single, earnings-maximizing driver, the platform’s overall challenge is as follows.

On the rider side, we suppose that the two world state periods, , are induced by latent demand shocks. The platform’s design lever is the pricing policy , where indicates the rider price for trip length in world state . Rider demand depends on the prices, inducing request rates and distributions through a standard demand model for each trip: a rider with latent demand for trip requests a ride if the price is no more than their valuation for the trip (without substituting for trips of different lengths).

On the driver side, as detailed in our model formulation, the driver chooses a strategy to maximize earnings rate , where the additional arguments emphasize that earnings depend on rider prices through induced demand. Further, the driver has an outside option earnings rate of , and will participate in the system only if it is possible to achieve earnings rate with some strategy .

The set of rides served by the platform are those that are both requested by riders (as induced by pricing and denoted by ) and accepted by the driver (denoted by driver strategy ):