Simultaneous Inference for Pairwise Graphical Models with Generalized Score Matching

Abstract

Probabilistic graphical models provide a flexible yet parsimonious framework for modeling dependencies among nodes in networks. There is a vast literature on parameter estimation and consistent model selection for graphical models. However, in many of the applications, scientists are also interested in quantifying the uncertainty associated with the estimated parameters and selected models, which current literature has not addressed thoroughly. In this paper, we propose a novel estimator for statistical inference on edge parameters in pairwise graphical models based on generalized Hyvärinen scoring rule. Hyvärinen scoring rule is especially useful in cases where the normalizing constant cannot be obtained efficiently in a closed form, which is a common problem for graphical models, including Ising models and truncated Gaussian graphical models. Our estimator allows us to perform statistical inference for general graphical models whereas the existing works mostly focus on statistical inference for Gaussian graphical models where finding normalizing constant is computationally tractable. Under mild conditions that are typically assumed in the literature for consistent estimation, we prove that our proposed estimator is -consistent and asymptotically normal, which allows us to construct confidence intervals and build hypothesis tests for edge parameters. Moreover, we show how our proposed method can be applied to test hypotheses that involve a large number of model parameters simultaneously. We illustrate validity of our estimator through extensive simulation studies on a diverse collection of data-generating processes.

Keywords: generalized score matching, high-dimensional inference, probabilistic graphical models, simultaneous inference

1 Introduction

Undirected probabilistic graphical models are widely used to explore and represent dependencies between random variables (Lauritzen, 1996). They have been used in areas ranging from computational biology to neuroscience and finance. An undirected probabilistic graphical model consists of an undirected graph , where is the vertex set and is the edge set, and a random vector . Each coordinate of the random vector is associated with a vertex in and the graph structure encodes the conditional independence assumptions underlying the distribution of . In particular, and are conditionally independent given all the other variables if and only if , that is, the nodes and are not adjacent in . One of the fundamental problems in statistics is that of learning the structure of from i.i.d. samples from and quantifying the uncertainty of the estimated structure. Drton and Maathuis (2017) provides a recent review of algorithms for learning the structure, while Janková and van de Geer (2019) provides an overview of statistical inference in Gaussian graphical models.

Gaussian graphical models are a special case of undirected probabilistic graphical models and have been widely studied in the machine learning literature. Suppose that . In this case, the conditional independence graph is determined by the pattern of non-zero elements of the inverse of the covariance matrix . In particular, and are conditionally independent given all the other variables in if and only if and are both zero. This simple relationship has been fundamental for the development of rich literature on Gaussian graphical models and has facilitated the development of fast algorithms and inferential procedures (see, for example, Dempster, 1972; Drton and Perlman, 2004; Meinshausen and Bühlmann, 2006; Yuan and Lin, 2007; Friedman et al., 2008; Rothman et al., 2008; Yuan, 2010; Sun and Zhang, 2013; Cai et al., 2011).

In this paper, we consider a more general, but still tractable, class of pairwise interaction graphical models with densities belonging to an exponential family with natural parameter space :

| (1) |

The functions , are the sufficient statistics and is the log-partition function. We assume throughout the paper that the support of the densities is either or and is dominated by Lebesgue measure on . To simplify the notation, for a log-density of the form given in (1) we will write

where and with . The natural parameter space has the form . Under the model in (1), there is no edge between and in the corresponding conditional independence graph if and only if . The model in (1) encompasses a large number of graphical models studied in the literature as we discuss in Section 1.2. Lin et al. (2016) studied estimation of parameters in model (1), however, the focus of this paper, as we discuss next, is on performing statistical inference—constructing honest confidence intervals and statistical tests—for parameters in (1).

The focus of the paper is on the inferential analysis about parameters in the model given in (1), as well as the Markov dependencies between observed variables. Our inference procedure does not rely on the oracle support recovery properties of the estimator and is therefore uniformly valid in a high-dimensional regime and robust to model selection mistakes, which commonly occur in ultra-high dimensional setting. Our approach is based on Hyvärinen generalized scoring rule estimate of in (1). The same procedure was used in Lin et al. (2016), however, rather than focusing on consistent model selection, we use the initial estimator to construct a regular linear estimator (van der Vaart, 1998). We establish Bahadur type representation for our final regular estimator that is robust to model selection mistakes and valid for a big class of data generating distributions. The purpose of establishing a Bahadur representation is to approximate an estimate by a sum of independent random variables, and hence prove the asymptotic normality of the estimator for (1), allowing us to conduct statistical inference on the model parameters (see Bahadur, 1966). In particular, we show how to construct confidence intervals for a parameter in the model that have nominal coverage and also propose a statistical test for existence of edges in the graphical model with nominal size. These results complement existing literature, which is focused on consistent model selection and parameter recovery, as we review in the next section. Furthermore, we develop a methodology for constructing simultaneous confidence intervals for all the parameters in the model (1) and apply this methodology for testing the parameters in the differential network111We adopt the notion used in Li et al. (2007) and Danaher et al. (2014) and define the differential network as a difference between parameters of two graphical models.. The main idea here is to use the Gaussian multiplier bootstrap to approximate the distribution of the maximum coordinate of the linear part in the Bahadur representation. Appropriate quantile obtained from the bootstrap distribution is used to approximate the width of the simultaneous confidence intervals and the cutoff values for the tests for the parameters of the differential network.

1.1 Main Contribution

This paper makes two major contributions to the literature on statistical inference for graphical models. First, compared to previous work on high-dimensional inference in graphical models (Ren et al., 2015; Barber and Kolar, 2018; Wang and Kolar, 2016; Janková and van de Geer, 2015), this is the first work on statistical inference in models where computing the log-partition function is intractable. Existing works mostly focus on Gaussian graphical models with a tractable normalizing constant, whereas our method can be applied to more general models, as we discuss in Section 2.1. Second, we apply our proposed method to simultaneous inference on all edges connected to a specific node. Our simultaneous inference procedure can be used to

-

1.

test whether a node is isolated in a graph; that is, whether it is conditionally independent with all the other nodes;

-

2.

estimate the support of the graph by setting an appropriate threshold on the proposed estimators; and

-

3.

test for the difference between graphical models where we have observations of two graphical models with the same nodes and we would like to test whether the local connectivity pattern for a specific node is the same in the two graphs.

Once again, the existing approaches cannot deal with simultaneous testing with an intractable normalizing constant. Moreover, most of the existing work impose a sparsity condition on the inverse of Hessian and focus on only. Here we relax the sparsity condition on the inverse Hessian and show how to perform inference for a general .

1.2 Related Work

Our work straddles two areas of statistical learning which have attracted significant research of late: model selection and estimation in high-dimensional graphical models, and high-dimensional inference. We briefly review the literature most relevant to our work, and refer the reader to two recent review articles for a comprehensive overview (Drton and Maathuis, 2017; Janková and van de Geer, 2019). Drton and Maathuis (2017) focuses on structure learning in graphical models, while Janková and van de Geer (2019) reviews inference in Gaussian graphical models.

We start by reviewing the literature on learning structure of probabilistic graphical models. Much of the research effort has focused on learning structure of Gaussian graphical models where the edge set of the graph is encoded by the non-zero elements of the precision matrix . The literature here roughly splits into two categories: global and local methods. Global methods typically estimate the precision matrix by maximizing regularized Gaussian log-likelihood (Yuan and Lin, 2007; Rothman et al., 2008; Friedman et al., 2008; d’Aspremont et al., 2008; Ravikumar et al., 2011; Fan et al., 2009; Lam and Fan, 2009), while local methods estimate the graph structure by learning the neighborhood or Markov blanket of each node separately (Meinshausen and Bühlmann, 2006; Yuan, 2010; Cai et al., 2011; Liu and Wang, 2017; Zhao and Liu, 2014). Extensions to more general distributions in Gaussian and elliptical families are possible using copulas, as the graph structure within these families is again determined by the inverse of the latent correlation matrix (Liu et al., 2009, 2012a; Xue and Zou, 2012; Liu et al., 2012b; Fan et al., 2017).

Once we depart from the Gaussian distribution and related families, learning the conditional independence structure becomes more difficult, primarily owing to computational intractability of evaluating the log-partition function. A computationally tractable alternative to regularized maximum likelihood estimation is regularized pseudo-likelihood which was studied in the context of learning structure of Ising models in Höfling and Tibshirani (2009), Ravikumar et al. (2010), and Xue et al. (2012). Similar methods were developed in the study of mixed exponential family graphical models, where a node’s conditional distribution is a member of an exponential family distribution, such as Bernoulli, Gaussian, Poisson or exponential. See Guo et al. (2011a), Guo et al. (2011b), Lee and Hastie (2015), Cheng et al. (2013), Yang et al. (2012), and Yang et al. (2014) for more details.

More recently, score matching estimators have been investigated for learning the structure of graphical models in high-dimensions when the normalizing constant is not available in a closed-form (Lin et al., 2016; Yu et al., 2018). Score matching was first proposed in Hyvärinen (2005) and subsequently extended for binary models and models with non-negative data in Hyvärinen (2007). It offers a computational advantage when the normalization constant is not available in a closed-form, making likelihood based approaches intractable, and is particularly appealing for estimation in exponential families as the objective function is quadratic in the parameters of interest. Sun et al. (2015) develop a method based on score matching for learning conditional independence graphs underlying structured infinite-dimensional exponential families. Forbes and Lauritzen (2015) investigated the use of score matching for the inference of Gaussian linear models in low-dimensional settings. However, despite its power, there have not been results on inference in high-dimensional models using score matching. As one of our contributions in this paper, we build on the prior work on estimation using generalized score matching and develop an approach to statistical inference for high-dimensional graphical models. In particular, we construct a novel -consistent estimator of parameters in (1). This is the first procedure that can obtain a parametric rate of convergence for an edge parameter in a graphical model where computing the normalizing constant is intractable.

Next, we review the literature on high-dimensional inference, focusing on work related to high-dimensional undirected graphical models. Liu (2013) developed a procedure that estimates conditional independence graph from Gaussian observations and controls false discovery rates asymptotically. Wasserman et al. (2014) develop confidence guarantees for undirected graphs under minimal assumptions by developing Berry-Esseen bounds on the accuracy of Normal approximation. Ren et al. (2015), Janková and van de Geer (2015), and Janková and van de Geer (2017) develop methods for constructing confidence intervals for edge parameters in Gaussian graphical models, based on the idea of debiasing the regularized estimator developed in (Zhang and Zhang, 2013; van de Geer et al., 2014; Javanmard and Montanari, 2014). A related approach was developed for edge parameters in mixed graphical models whose node conditional distributions belong to an exponential family in Wang and Kolar (2016). Wang and Kolar (2014) develop methodology for performing statistical inference in time-varying and conditional Gaussian graphical models, while Barber and Kolar (2018) and Lu et al. (2018) develop methods for semi-parametric copula models. We contribute to the literature on high dimensional inference by demonstrating how to construct regular estimators for probabilistic Graphical models whose normalizing constant is intractable. Our estimators are robust to model selection mistakes and allows us to perform valid statistical inference for edge parameters in a large family of data generating distributions.

Finally, we contribute to the literature on simultaneous inference in high-dimensional models. Zhang and Cheng (2017) and Dezeure et al. (2017) develop methods for performing simultaneous inference on all the coefficients in a high-dimensional linear regression. In the same setting, Zhao et al. (2014) use a multiplier bootstrap approach to construct robust simultaneous confidence intervals. Chang et al. (2018) applies it to the simultaneous inference of Gaussian graphical models. These procedures allow for the dimensionality of the vector to be exponential in the sample size and rely on bootstrap to approximate the quantile of the test statistic. We extend these ideas to the high dimensional graphical model setting and show how we can build simultaneous hypothesis tests on the neighbors of a specific node.

A conference version of this paper was presented in the Annual Conference on Neural Information Processing Systems 2016 (Yu et al., 2016). Compared to the conference version, in this paper we extend the results in the following ways. First, we extend the results to include the generalized score matching method (Yu et al., 2018, 2019) in place of the original score matching method. This generalized form of the score matching method allows us to improve the estimation accuracy and obtain better inference results for non-negative data. In the conference version, we made an assumption that the inverse of the population Hessian matrix, see Section 4, is (approximately) sparse. We relax this sparsity condition and develop an inference procedure that is valid even if the sparsity condition is violated, but the inverse of the Hessian matrix has bounded columns in the norm. Moreover, instead of focusing on a single edge as in the conference version, in this work we propose a procedure for simultaneous inference for all edges connected to a specific node. This allows us to build hypothesis tests for a broad class of applications, including testing of isolated nodes, support recovery, and testing the difference between two graphical models. Furthermore, while the conference version focused on the case where in (1), here we extend the results to a general choice of . Lastly, we run additional experiments to demonstrate the effectiveness of our proposed method.

1.3 Notation

We use to denote the set . For a vector , we let be the support set (with an analogous definition for matrices ), , , the -norm defined as with the usual extensions for , that is, and . For a vector , is a sub-vector of with components corresponding to the set , and is the sub-vector with component corresponding to edge omitted. For a matrix , denote as the induced norm. In particular, . We also use to denote the maximum component of . We define as the empirical mean of samples: . For two sequences of numbers and , we use , or to denote that for some finite positive constant , and for all large enough. We use to denote that happens with high probability. The notation is used to denote that . We denote as convergence in distribution to a fixed distribution and as convergence in probability to a constant . We denote for . For any function , we use to denote the gradient, and to denote the Laplacian operator on . Note that both the gradient and the Laplacian are with respect to .

1.4 Organization of the Paper

The remainder of this paper is structured as follows. We begin in Section 2 with background on exponential family pairwise graphical model, score matching method, and a brief review of statistical inference in high dimensional models. In Section 3 we describe the construction of our novel estimator for a single edge parameter based on a three-step procedure, for . Section 4 provides theoretical results and Section 5 discusses the relaxation of sparsity condition on the inverse of population Hessian matrix. Section 6 extends the procedure to simultaneous inference for all edges connected to some specific node. In Section 7 we extend our results to general . We provide experimental results for synthetic datasets and a real dataset in Sections 8 and 9 respectively. Section 10 provides conclusion and discussion.

2 Background

We begin with reviewing exponential family pairwise graphical models in Section 2.1, and then introduce the score matching and generalized score matching methods in Section 2.2. Finally we provide a brief overview of statistical inference for high dimensional models in Section 2.3.

2.1 Exponential Family Pairwise Graphical Models

Throughout the paper we focus on the case where

is an exponential family with log-densities given in (1), which frequently appear in graphical modeling. There are sets of sufficient statistics for each that depend on the individual nodes and sets of sufficient statistics for each that allow for pairwise interactions of different types. Conditional independence graph underlying a distribution has no edge between vertices and if and only if . A special case of the model given in (1) are pairwise interaction models with log-densities

| (2) |

where are sufficient statistics that depend only on and . In what follows, we will consider models that either has the form given in (2) or the more general form given in (1).

A number of well-studied distributions have the above discussed form. We provide some examples below, including examples where the normalizing constant cannot be obtained in closed-form.

Gaussian graphical models.

The most studied example of a probabilistic graphical model is the case of the Gaussian graphical model. Suppose that the random variable follows the centered multivariate Gaussian distribution with covariance and precision matrix . The log-density is given as

| (3) |

the support of the density is and the sufficient statistics take the form .

Non-negative Gaussian.

Our second example of a distribution with the log-density of the form in (2) is that of a non-negative Gaussian random vector. The probability density function of a non-negative Gaussian random vector is proportional to that of the corresponding Gaussian vector given in (3), but restricted to the non-negative orthant. Here the support of the density is . The conditional independence graph is determined the same way as in the Gaussian graphical model case through the non-zero pattern of the elements in the precision matrix . The normalizing constant in this family has no closed-form and hence maximum likelihood estimation of is intractable.

Normal conditionals.

Our third example is taken from Lin et al. (2016). See also Gelman and Meng (1991) and Arnold et al. (1999). Consider the family of distributions with densities of the form

where the matrices are symmetric interaction matrices with a zero diagonal. Members of this family have Normal conditionals, but the densities themselves need not be unimodal. The conditional independence graph does not contain an edge between vertices and if and only if both and are equal to zero. In contrast to the Gaussian graphical models, the conditional dependence may also express itself in the variances.

Conditionally specified mixed graphical models.

In general, specifying multivariate distributions is difficult, since in a given problem it might not be clear what class of graphical models to use. On the other hand, specifying univariate distributions is an easier task. Chen et al. (2015) and Yang et al. (2015) explored ways of specifying multivariate joint distributions via univariate exponential families. Consider a conditional density of the form

| (4) |

where and are known functions for each . Suppose that for a random vector , each coordinate follows the conditional density of the form in (4) with for all . Then Chen et al. (2015) and Yang et al. (2015) showed that there exists a joint distribution of compatible with the conditional densities and that it is of the form

In particular, the joint density above is of the form given in (1), with pairwise interaction sufficient statistics given as . When the support of the distribution is or , the parameters of the distribution can be efficiently estimated using score matching. In the case of unknown function , Suggala et al. (2017) explored nonparametric estimation via basis expansion and fitted parameters using pseudo-likelihood. Developing a valid statistical inference procedure for this nonparametric setting is beyond the scope of the current work.

As an example of a conditionally specified model, that we will return to later in the paper, consider exponential graphical models where the node-conditional distributions follow an exponential distribution. For a random vector described by an exponential graphical model, the density function is given by

Note that the variable takes only non-negative values. To ensure that the distribution is valid and normalizable, the natural parameter space consists of matrices whose elements are positive. Therefore, one can only model negative dependencies via the exponential graphical model.

Exponential square-root graphical model.

As our last example, consider the exponential square-root graphical model (Inouye et al., 2016) with density function given by

This square-root graphical model is a multivariate generalizations of univariate exponential family distributions that can capture the positive dependency among nodes. Specifically, it assumes only a mild condition on the parameter matrix, but allows for almost arbitrary negative and positive dependencies. We refer to Inouye et al. (2016) for details on parameter estimation with nodewise regressions and likelihood approximation methods.

2.2 Score Matching

In this section we briefly review the score matching method proposed in Hyvärinen (2005, 2007) and the generalized score matching for non-negative data proposed in Yu et al. (2018).

2.2.1 Score Matching

A scoring rule is a real-valued function that quantifies the accuracy of being the distribution from which an observed realization may have been sampled. There are a large number of scoring rules that correspond to different decision problems Parry et al. (2012). Given independent realizations of , , one finds optimal score estimator that minimizes the empirical score

| (5) |

When and consists of twice differentiable densities with respect to Lebesgue measure, the Hyvärinen scoring rule (Hyvärinen, 2005) is given as

| (6) |

where is the density of with respect to Lebesgue measure on . We would like to emphasize that this gradient and Laplacian are with respect to . In this way we get rid of the normalizing constant which does not depend on . This scoring rule is convenient for learning models that are specified in an unnormalized fashion or whose normalizing constant is difficult to compute. The score matching rule is proper (Dawid, 2007), that is, is minimized over at . Suppose the density of is twice continuously differentiable and satisfies

and

Then the Fisher divergence between ,

where is the density of , is induced by the score matching rule (Hyvärinen, 2005). The gradients in the equation above can be thought of as gradients with respect to a hypothetical location parameter, evaluated at the origin (Hyvärinen, 2005).

For a parametric exponential family with densities given in (1), minimizing (5) with the scoring rule in (6) can be done in a closed form (Hyvärinen, 2005; Forbes and Lauritzen, 2015). An estimator obtained in this way can be shown to be asymptotically consistent (Hyvärinen, 2005), however, in general it will not be efficient (Forbes and Lauritzen, 2015).

2.2.2 Generalized Score Matching for Non-Negative Data

The score matching method in Section 2.2.1 does not work for non-negative data, since the assumption that and tend to 0 at the boundary breaks down. To solve this problem, Hyvärinen (2007) proposed a generalization of the score matching approach to the case of non-negative data.

When the non-negative score matching loss (analogous to the Fisher divergence ) is defined as

The scoring rule for non-negative data that induces is given as

| (7) |

For exponential families, the non-negative score matching loss again can be obtained in a closed form and the estimator is consistent and asymptotically normal under suitable conditions (Hyvärinen, 2007).

Yu et al. (2018) proposed the generalized score matching for non-negative data to improve the estimation efficiency of the procedure based on the scoring rule in (7). Let be positive and differentiable functions and set

The generalized -score matching loss is defined as

where . Suppose the following regularity conditions are satisfied

| (8) | |||

Under the condition (8), the scoring rule corresponding to the generalized -score matching loss is given as

The regularity condition (8) is required for applying integration by parts and Fubini-Tonelli theorem in order to show consistency of the score-matching estimator.

Note that by choosing , for all , one recovers the original score matching formulas for non-negative data in (7). The advantage of this generalized score matching rule is that by choosing an increasing, but slowly growing (for example, ), one does not need to estimate high moments of the underlying distribution, which leads to better practical performance and improved theoretical guarantees. See Yu et al. (2018) for details.

2.2.3 Score matching for probabilistic graphical models

Score matching has been successfully applied in the context of probabilistic graphical models. Forbes and Lauritzen (2015) studied score matching to learn Gaussian graphical models with symmetry constraints. Lin et al. (2016) proposed a regularized score matching procedure to learn conditional independence graph in a high-dimensional setting by minimizing

where the loss function is either defined in (6) or defined in (7). For Gaussian models, -norm regularized score matching is a simple, yet efficient method, which coincides with the method in Liu and Luo (2015). Yu et al. (2018) improved on the approach of Lin et al. (2016) and studied regularized generalized -score matching of the form

Applied to data generated from a multivariate truncated normal distribution, the conditional independence graph can be recovered with the same number of samples that are needed for recovery of the structure of a Gaussian graphical model. Sun et al. (2015) develop a score matching estimator for learning the structure of nonparametric probabilistic graphical models, extending the work on estimation of infinite-dimensional exponential families (Sriperumbudur et al., 2017). In Section 3, we present a new estimator for components of in (1) that is consistent and asymptotically normal, building on Lin et al. (2016) and Yu et al. (2018).

2.3 Statistical Inference

We briefly review how to perform statistical inference for low dimensional parameters in a high-dimensional model. In many statistical problems, the unknown parameter can be partitioned as , where is a scalar of interest and is a dimensional nuisance parameter. Let denote the true unknown parameter. In a high-dimensional setting, where the sample size is much smaller than the dimensionality of the parameter , it is common to impose structural assumptions on . For example in several applications, it is common to assume that the true parameter is sparse. Indeed, we will work under this assumption as well.

Let us denote the empirical negative log-likelihood by

where is the negative log-likelihood for the observation. Let denote the information matrix and denote the partition of corresponding to as

| (9) |

The partial information matrix of is denoted as .

Consider for the moment a low-dimensional setting. In order to perform statistical inference about , one can use the profile partial score function defined as

where is the maximum partial likelihood estimator for with a fixed parameter . Under the null hypothesis that , we have that (van der Vaart, 1998)

Therefore, one can reject the null hypothesis for large values of . However, in a high-dimensional setting, the estimator is no longer -consistent and we have to modify the approach above. In particular, we will show how to modify the profile partial score function to allow for valid inference in a high-dimensional setting based on a sparse estimator of .

Without loss of generality, assume that . For any estimator , Taylor’s expansion theorem gives

| (10) |

where rem is the remainder term. The first term in (10) converges to a normal distribution under suitable assumptions using the central limit theorem (CLT). The distribution of the second term, however, is in general intractable to obtain. This is due to the fact that the distribution of depends on the selected model. Unless we are willing to assume stringent and untestable conditions under which it is possible to show that the true model can be selected, the limiting distribution of cannot be estimated even asymptotically (Leeb and Pötscher, 2007). To overcome this issue, one needs to modify the profile partial score function, so that its limiting distribution does not depend on the way the nuisance parameter is estimated.

Ning and Liu (2017) introduced the following decorrelated score function

where . The decorrelated score function is uncorrelated with the nuisance score functions and, therefore, its limiting distribution will not depend on the model selection mistakes incurred while estimating . In particular, is indeed asymptotically normally distributed under the null hypothesis, as long as is a good enough estimator of , but not necessarily -consistent estimator. Based on the asymptotic normality of the decorrelated score function, we can then build confidence intervals for and perform hypothesis testing.

In practice, the vector is unknown and needs to be estimated. A number of methods have been proposed for its estimation in the literature. For example, Ning and Liu (2017) use a Dantzig selector-like method, Belloni et al. (2013) proposed the double selection method, while Zhang and Zhang (2013), van de Geer et al. (2014), and Javanmard and Montanari (2014) use a lasso based estimator. See also Dezeure et al. (2017), Zhang and Cheng (2017) for simultaneous inference, Taylor et al. (2014), Yang et al. (2016) for post selective inference, Li (2019), Cao and Dowd (2019), and Cao and Lu (2019) for for synthetic control, etc. In this paper, we adopt the double selection procedure of Belloni et al. (2013). Details will be given in Section 3.

3 Methodology

In this section, we present a new procedure that constructs a -consistent estimator of an element of . Our procedure involves three steps that we detail below. We start by introducing some additional notation and then describe the procedure for the case where . Extension to non-negative data is given at the end of the section. Throughout this section we consider only, so that the parameter of interest is a scalar. Extensions to general is discussed later in Section 7.

For fixed indices , let

be the conditional density of given . In particular,

| (11) |

where , with , is the part of the vector corresponding to , , and ; and is the corresponding vector of sufficient statistics , , and . Here is the log-partition function of the conditional distribution and . Let and be the gradient and Laplacian operators, respectively, with respect to and defined as:

With this notation, we introduce the following scoring rule

| (12) |

where the constant term , and

with , , , and .

This scoring rule is related to the one in (6), however, rather than using the density in evaluating the parameter vector, we only consider the conditional density . We will use this conditional scoring rule to create an asymptotically normal estimator of an element . Our motivation for using this estimator comes from the fact that the parameter can be identified from the conditional distribution of where

is the Markov blanket of . Furthermore, the optimization problems arising in steps 1-3 below can be solved much more efficiently, as the scoring rule in (12) involves fewer parameters.

We are now ready to describe our procedure for estimating , which proceeds in three steps.

Step 1:

We find a pilot estimator of by solving the following program

| (13) |

where is a tuning parameter. Let .

Since we are after an asymptotically normal estimator of , one may think that it is sufficient to find and appeal to results of Portnoy (1988), who has established asymptotic normality for -estimators with increasing number of parameters. Unfortunately, this is not the case. Since is obtained via a model selection procedure, it is irregular and its asymptotic distribution cannot be estimated (Leeb and Pötscher, 2007; Pötscher, 2009). Therefore, we proceed to create a regular estimator of in steps 2 and 3. The idea is to create an estimator that is insensitive to first-order perturbations of other components of , which we consider as nuisance components. The idea of creating an estimator that is robust to perturbations of nuisance has been recently used in Belloni et al. (2013), however, the approach goes back to the work of Neyman (1959).

Step 2:

Let be a minimizer of

| (14) |

where is a tuning parameter. Let . The intuition here is that the vector approximately computes a row, up to a constant, of the inverse of the Hessian in (13).

Step 3:

Let . We obtain our estimator as a solution to the following program

| (15) |

Our estimator of is the coordinate of —which we denote as . Motivation for this procedure will be clear from the proof of Theorem 2 given in the next section.

Extension to non-negative data.

For non-negative data, the procedure is similar. In place of the score rule in (12), we will use a conditional score rule based on the generalized -score rule. We define the following scoring rule

| (16) |

with

and

Here , and . Now we can define

| (17) |

Then , which is of the same form as (12) with and replacing and , respectively. Thus our three-step procedure for non-negative data can be written as follows. For notation consistency, we omit the subscript on the estimator and support .

Step 1:

We find a pilot estimator of by solving

| (18) |

where is a tuning parameter and is defined in (16). Let .

Step 2:

Step 3:

Let . We obtain our estimator as a solution to the following program

| (20) |

Our estimator of is the coordinate of —which we denote as .

4 Asymptotic Normality of the Estimator

In this section, we outline the main theoretical properties of our estimator. We start by providing high-level conditions that allow us to establish properties of each step in the procedure.

Assumption M.

We are given i.i.d. samples from of the form in (1). Let

| (21) |

and

We assume that the parameter vector is sparse with ; and the vector is sparse with .

Let . The assumption M supposes that the parameter to be estimated is sparse, which makes estimation in the high-dimensional setting feasible. An extension to the approximately sparse parameter is possible but technically cumbersome, and does not provide additional insights into the problem. One of the benefits of using the conditional score to learn parameters of the model is that the sample size will only depend on the size of and not on the sparsity of the whole vector as in Lin et al. (2016). The second part of the assumption states that the inverse of the population Hessian is approximately sparse, which is a reasonable assumption for a number of models, since the Markov blanket of is small under the sparsity assumption on . We relax the sparsity assumption in Section 5.

The vector is determined by the model (11) and parameter , and is therefore not a free parameter. For the Gaussian graphical model, it can be shown that the sparsity of implies the sparsity of . That is, assumption M holds when the columns of the precision matrix are sparse. For a general model, it may not be easy to explicitly verify the exact sparsity of , since the calculation of involves calculation of possibly intractable moments, especially when using generalized score matching with for non-negative data. For normal conditionals and exponential graphical model, we verify numerically (in Section 8) that the sample version of behaves approximately like a sparse vector when is large enough. These indicate that assumption M is reasonable, at least in an approximately sparse version. For general models, the sparsity condition on could be violated and, therefore, we discuss how to relax it in Section 5.

Assumption SE.

Let

and

denote the minimal and maximal -sparse eigenvalues of a semi-definite matrix , respectively. We assume

where .

Assumption SE imposes the sparse eigenvalue condition on the population quantity. A lower bound on the population Hessian is required even in a low dimensional setting in order to prove asymptotic normality of an estimator. See, for example, Forbes and Lauritzen (2015) where the population Hessian is assumed to be invertible. An upper bound on the Hessian matrix is also commonly assumed in the literature on graphical models and high-dimensional inference (see, for example, Yang et al., 2015; Belloni and Chernozhukov, 2013). We use the upper bound on the Hessian to control the size of the estimated support in steps 1 and 2 of the procedure.

For Gaussian graphical model, assumption SE is satisfied with non-degenerate covariance matrix. For general models, assumption SE puts restrictions on the model parameter in a way that is hard to handle explicitly. Note that related work imposes stronger assumption on the sample Fisher information matrix directly. See, for example, conditions (C1) and (C2) in Yang et al. (2015).

For the upper bound of the sparse eigenvalue, we remark that the mean of could be non-zero. For the Gaussian graphical model, if there is a non-zero mean , then the components of and would instead be . Therefore the sparse eigenvalue would not explode. In practice, we subtract the empirical mean and only need to consider the centered case. For other models, existing works assume boundedness of the first and second order moments of all the components of . See Condition (C3) in Yang et al. (2015).

With assumption SE on the population quantity, the following lemma, adopted from Corollary 4 in Belloni and Chernozhukov (2013), quantifies the sparse eigenvalues of the sample quantity .

Lemma 1

Suppose assumption SE is satisfied. Suppose there exist such that and are bounded: and a.s. If the sample size satisfies

then the event

holds with probability at least .

Lemma 1 ensures that the sparse eigenvalues of the sample quantity are well-behaved provided that and can be upper bounded, and the sample size is reasonably large. The scale of the upper bound depends on the sufficient statistics , and can be verified for concrete models. For example, for the Gaussian graphical model, a standard result on the Gaussian tail bound gives with high probability. As another example, Proposition 4 in Yang et al. (2015) shows that, under mild conditions, with high probability when the sufficient statistics of the conditional density are given by and , which includes a wide range of applications, such as exponential graphical model, and Poisson graphical model. For models with more general sufficient statistics, we can modify the proof of Proposition 4 in Yang et al. (2015) to obtain the corresponding rate on , under suitable assumptions.

Let and , for , be the rates of estimation in steps 1 and 2, respectively. Under the assumption SE, on the event

we have that and . Similarly, on the event

we have that and , using results of Negahban et al. (2012). In order to ensure that and hold with high-probability, one needs to choose appropriate and . This calculation is specific to the model at hand. For example, if the vectors

| (22) |

have sub-Gaussian components, then by taking , the events and hold with probability at least (Yang et al., 2015; Negahban et al., 2012). For other distributions, we may need to choose larger and . See also Lemma 9 in Yang et al. (2015).

The following result establishes a Bahadur representation for .

Theorem 2

Suppose that assumptions M and SE hold. Define with and , where is given in the assumption M. On the event , we have that

| (23) |

where .

Theorem 2 is deterministic in nature. It establishes a representation that holds on the event , which in many cases holds with overwhelming probability. We will show that under suitable conditions the first term converges to a normal distribution. The following assumption is a regularity condition needed even in a low dimensional setting for asymptotic normality of the score matching estimator (Forbes and Lauritzen, 2015).

Assumption R.

and are finite for all values of in the domain.

Corollary 3

When the vectors in (22) are sub-Gaussian, we choose , so that the sample complexity is given by . For other distributions, we may need a larger sample size to bound the error term in (23). We see that the variance depends on the true and , which are unknown. In practice, we estimate using the following consistent estimator ,

| (24) |

with

and being a canonical vector with in the position of element and elsewhere. The consistency of this variance estimator is provided in the appendix. Using this estimate, we can construct a confidence interval with asymptotically nominal coverage. In particular,

In the next section, we outline the proof of Theorem 2. Proofs of other technical results are relegated to appendix.

4.1 Proof of Theorem 2

We first introduce some auxiliary estimates. Let be a minimizer of the following constrained problem

| (25) | ||||

where is defined in the step 3 of the procedure. Essentially, is the refitted estimator from step 2 constrained to have the support on . Let with , and zero elsewhere. The solution satisfies the first order optimality condition . Multiplying by , it follows that

| (26) | ||||

From Lemma 12 and Lemma 13 (Appendix A), we have that

Using Lemma 14, the term can be written as

Putting all the pieces together, we can rewrite (26) as

with . This completes the proof.

4.2 Theoretical Results for Non-negative Data

In this section we provide the theoretical results for non-negative data obtained by modifying the assumptions according to the scoring rule for non-negative data.

Assumption M’.

The parameter vector is sparse, with . Let

| (27) |

with defined in (17). Let and , for . The vector is sparse with . Let .

Assumption SE’.

We have

where .

Assumption R’.

and are finite for all values of in the domain.

Denote the modified events as

and

We have the asymptotic normality for the estimator on non-negative data.

Corollary 4

Suppose that assumptions M’, SE’, and R’ hold. Define with and , where is given in the assumption M’. In addition, suppose and where

Then we have

with the variance term

where .

5 Relaxing the Sparsity Assumption on the Inverse of Hessian

For general models, the sparsity condition on could be violated. For example, for the non-negative Gaussian graphical model with , by direct calculation we obtain that almost all the components of take the same value, which is approximately . Therefore is neither sparse, nor approximately sparse (see Section 8 for details). Instead, it only satisfies a weaker condition . This constant norm condition is studied in Ma et al. (2017). Since is dense, we cannot select sparse support in Step 2; and therefore Step 3 is no longer valid when .

We relax the sparsity condition on to a constant condition, and modify our procedure. We apply the debias method in Ma et al. (2017). Specifically, recall that the scoring rule is

| (28) |

and the gradient with respect to is

| (29) |

We obtain an estimator using Step 1, which satisfies

| (30) |

Multiplying by some matrix on both sides and rearranging terms, we obtain

| (31) |

The empirical version of (31) is

| (32) |

Rather than using Step 3 in the procedure described in Section 3, we define the left hand side as the proposed estimator:

| (33) |

Notice that the first term in the right hand side of (32) is the true value. Suppose is an approximate inverse of , then the third term in the right hand side of (32) would be negligible. For the second term, we see that is an average of i.i.d. samples. If it is independent of , then this second term is asymptotically normal, and the coordinate of is the desired estimator, similar to the three-step procedure described in Section 3. We construct following the procedure in Ma et al. (2017). We first split the data into two parts and estimate on the first part, while is estimated on the second part. For notation simplicity, let denote observations on the first part and on the second part. We estimate by solving the following convex program:

| (34) | ||||

By selecting appropriate , the solution will be an approximate inverse of and, hence, an approximate inverse of . On the other hand, since we estimate based on second part of the data, , it is independent of . Let be the population version of . We see that the column of (denoted as ) corresponds to up to a constant, where is defined in Theorem 2 with and . For non-negative Gaussian graphical model with , a simple calculation shows that for large , we have . We then see that the bounded norm condition on is satisfied.

To establish asymptotic normality of the modified procedure, we define the following event

For example, when and are sub-Gaussian vectors, modification of Lemma D.1 in Ma et al. (2017) gives us that if , then . By the proof of Lemma 10, we have that . This shows that the third term of (32) is of order . Suppose , we then obtain a similar result as in Corollary 3. It is also straightforward to see that the variance given by (32) is asymptotically the same as in Corollary 3. We conclude with the following Corollary for sub-Gaussian distribution.

Corollary 5

Suppose that assumptions SE and R hold. Furthermore, suppose . If and , then the estimator in (33) satisfies

where .

6 Simultaneous Inference

In the last two sections, we have developed a procedure for constructing a consistent and asymptotically normal estimate of a single edge parameter. In this section, we develop a procedure for simultaneous hypothesis testing of all edges connected to a specific node. We adopt the Gaussian multiplier bootstrap (Chernozhukov et al., 2013) to our setting. In this section we focus on the case where . The analysis can be straightforwardly extended to non-negative data.

For a fixed node , we would like to test the null hypothesis

| (35) |

for some values versus the alternative

| (36) |

We propose the following test statistic

| (37) |

where is obtained by the three step procedure described in Section 3. The null hypothesis will be rejected for large values of the test statistic. Using the statistics will allow us to have power against alternatives that change few of the coordinates of . In order to use the test statistic in practice, we need to be able to accurately compute the critical value of the test statistic in a high-dimensional setting. To that end, we describe a multiplier bootstrap method that will allow us to obtain an accurate critical value to the test statistic in (37).

For each and , denote

| (38) |

where as defined in Theorem 2. We use the subscript to highlight that all of these terms depend on the node and . Let , , be a sequence of independent standard Gaussian random variables and independent of data. We define the multiplier bootstrap statistic as

| (39) |

and compute the bootstrap critical value as the quantile of

Importantly, note that the quantile of the multiplier bootstrap statistic can be estimated using a Monte-Carlo method. We will show that the quantiles of approximate the quantiles of our test statistic.

Define

| (40) |

as the counterpart to , where . In order to establish our main theoretical result on simultaneous inference, we need the following regularity condition.

Assumption RR.

Define . There exist and , such that for any , we have and with probability at least . Moreover, uniformly for , we have for some .

The assumption RR imposes very mild technical conditions and is standard for a large number of models when the sample size is large enough. Part of the conditions are adopted from Chernozhukov et al. (2013) in order to apply the theoretical results on the Gaussian multiplier bootstrap.

Theorem 6

Suppose the assumptions M, SE, R and RR are satisfied, and the events hold for each . Furthermore, suppose there exists a constant , such that

| (41) |

Then, under the null hypothesis, we have

| (42) |

The proof of Theorem 6 is provided in the appendix. Since

it is straightforward to obtain the following corollary for the test statistic in (37).

Corollary 7

Suppose the conditions in Theorem 6 are satisfied. Then, under the null hypothesis, we have

| (43) |

where

| (44) |

and the bootstrap critical value is defined as

We remark that we are not aiming for a tight bound on the sample complexity. For commonly used models, we always have that in Assumption RR converges to 0 at a model specific rate. Theorem 6 is valid as long as the sample size is large enough, so that the sample complexity condition in (41) is satisfied.

6.1 Applications of Simultaneous Testing

In this section, we show three concrete applications of our proposed procedure. Specifically, we consider

-

1.

testing for isolated node;

-

2.

support recovery;

-

3.

testing for difference between graphical models.

Testing for isolated node.

For a specific node , we would like to test whether it is isolated in the graph. This specific structural question translates into whether the variable is conditionally independent with all the other nodes. In this case, we would like to test the null hypothesis

| (45) |

versus the alternative

| (46) |

We can directly apply our simultaneous inference procedure with .

Support recovery.

For a specific node , we would like to estimate the support of defined as . Let be the true support and we focus on distributions with sub-Gaussian components. For each node , let be a threshold that we set as

where is the variance estimator defined in (24). We can estimate the support by thresholding the values that are smaller than . In particular, the support recovery procedure return the following support set

| (47) |

We have the following result on the support recovery.

Corollary 8

Suppose that the values on the true support are bounded from below as

Then

| (48) |

where the infimum is taken over all data generating procedures that satisfy the minimum signal strength condition.

The proof follows in a similar way to the proof of Proposition 3.1 in Zhang and Cheng (2017) and is omitted here. The result shows that we are able to consistently recover the support of any node with overwhelming probability.

Testing the difference between graphical models.

We consider a two-sample problem in which we wish to test whether the parameters of two graphical models, with the same set of nodes and belonging to the same exponential family of the form in (2), are the same. For example, we may have the data for the same set of nodes collected in different time periods, and we want to test whether the graph structure changes over time. As another example, consider functional brain connectivity. It is of interest to test whether brain connectivity is the same for the healthy subjects and people with a certain disorder.

Formally, suppose there are two densities and of the form in (2), indexed by parameter vectors and . Given i.i.d. samples from and i.i.d. samples from , we would like to test the null hypothesis

| (49) |

versus the alternative

| (50) |

In order to create a test statistic for the difference, we first apply the three step procedure on each group of observations. That is, we obtain the estimators , and estimates of their variances . According to the Bahadur representation (23) in Theorem 2, we have

| (51) |

and

| (52) |

We propose to use the following test statistic

| (53) |

which will allow us to identify sparse changes in parameter values. We reject the null hypothesis for large values of the test statistic above. Next, we describe how to estimate the quantiles of the test statistic using the multiplier bootstrap.

Denote

| (54) |

and

| (55) |

We generate two sequences of independent standard Gaussian random variables

that are independent of data as well. The multiplier bootstrap statistic is defined as

| (56) |

and

is the bootstrap critical value.

Similar to Corollary 7, under the null hypothesis, we have

| (57) |

This gives us a valid procedure for testing whether the parameters of two graphical models are the same or not.

A recent paper (Kim et al., 2019) proposed a different inference procedure that directly estimates the parameters of the differential network. Xia et al. (2015) studied the two sample problem in the context of Gaussian graphical models and proposed the following test statistic

| (58) |

and showed that under the null hypothesis the limiting distribution of the test statistic satisfies

| (59) |

Unfortunately, the convergence to the extreme value distribution is rather slow and, as a result, the critical values based on the limiting approximation are not accurate for finite samples. In comparison, our multiplier bootstrap procedure provides non-asymptotic approximation to quantiles of the test statistic. Furthermore, the approximation quality improves polynomially with the sample size and, as a result, provides a good performance for small and moderate sample sizes.

7 Extension to General

So far we have assumed that the number of parameters corresponding to an edge is . In this section we extend our results to general . Throughout the section, we treat as a fixed quantity. Recall that , , represent sufficient statistics.

Inference for a fixed edge.

For a fixed index , the parameter of interest is the dimensional vector, . There is no edge between and in the corresponding conditional independence graph if and only if . Following the same procedure as in Section 3, we have the logarithm of conditional density as

where , with , is the part of the vector corresponding to , , and ; and is the corresponding vector of sufficient statistics

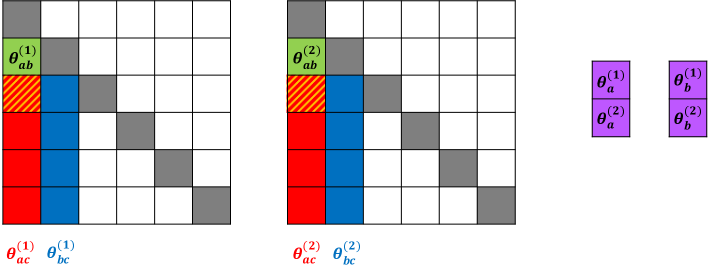

For notation simplicity, for a given node , denote as the stack of for ; similarly, denote as the stack of . Let denote the stack of and , which are the parameters in without group structure. We define , , and similarly. Let denote the index set of the parameters corresponding to the edge . Figure 1 presents an illustrative example with , , and .

We modify the three step procedure in Section 3 as follow.

Step 1:

We find a pilot estimator of by solving the following program

| (60) |

where

| (61) |

and is a tuning parameter. Since , we use the group Lasso penalty to estimate . Let be the support of :

| (62) |

Step 2:

For , let be a minimizer of

| (63) |

where is a tuning parameter. Let be the union of the support of :

| (64) |

Step 3:

Let . We obtain our estimator as a solution to the following program

| (65) |

Our estimator of is , a block of .

Asymptotic Normality.

For each , define with and , where is the population version of . Define

| (66) |

and

| (67) |

Let and as the stack of : . Similar to Theorem 2, we obtain the Bahadur representation for as:

| (68) |

where . Furthermore, under similar conditions as in Section 4, we obtain

| (69) |

where is the covariance matrix defined as . From (69) we can construct a multivariate confidence interval with asymptotically nominal coverage as before.

Simultaneous inference.

For simultaneous inference, with a fixed node , we would like to test the null hypothesis

| (70) |

for some fixed versus the alternative

| (71) |

Again, the test involves a large number of parameters, .

First, note that we can directly apply the procedure developed in Section 6. By ignoring the covariance structure of , we can directly use the Gaussian multiplier bootstrap. Specifically, for each , we obtain the Bahadur representation in (68). Next, we stack the resulting vectors into a dimensional vector and perform the Gaussian multiplier bootstrap method to calculate the test statistic and critical values. Since is an absolute constant, all the analysis in Section 6 remains valid. However, such a procedure disregards the group structure on parameters and ignores the off-diagonal elements of the covariance matrix when constructing the test and computing the critical values.

An alternative approach is based on the moderate deviation result for the -test developed in Liu and Shao (2013). Here, we outline the procedure and refer to Liu and Shao (2013) for technical details. First, for each , we define

| (72) |

It follows from (69) that the limiting distribution of is . Under mild conditions, Theorem 2.2 of Liu and Shao (2013) shows that

uniformly for . This motivates the following test statistic

| (73) |

We obtain the critical value that satisfies

The null hypothesis is rejected if . We can prove that the asymptotic Type I error is under the null only when the dependency among is weak. We refer to Liu and Shao (2013) for technical details. The disadvantage of this approach is that, the terms are correlated across , which is ignored when computing the critical value. Despite ignoring the group structure, the approach based on multiplier bootstrap can control the Type I error better with small sample sizes. See Section 8 for experimental results.

8 Simulations

In this section, we illustrate the finite sample properties of our inference procedure on several synthetic data sets. We generate data from four different Exponential family distributions that were introduced in Section 2.1. The first and third example involve Gaussian node-conditional distributions, for which we use regularized score matching. For the second and fourth setting where the node-conditional distributions follow Truncated Gaussian and Exponential distribution, respectively, we use regularized non-negative score matching procedure. Following the recommendation in Yu et al. (2018), we set for the non-negative settings. In each example, we report the mean coverage rate of 95% confidence intervals for several coefficients averaged over 500 independent simulation runs.

Gaussian graphical model.

For the Gaussian setting, we have with precision matrix . Without loss of generality, say we are interested in . We have

where for the second ‘’ is at location . Now we have

We can see that can be partitioned into first elements and last elements: . The two parts can be optimized separately. Moreover, both the population quantity and are the covariance matrix after rearranging terms and ignoring zero components. Assumption SE is satisfied with most of the commonly used covariance matrices with full rank. Moreover, we can verify that and are proportional to the second and first column of the precision matrix . Therefore, assumption M is satisfied when the columns of the precision matrix are sparse.

For the experiment, we set diagonal entries of as . The sparsity pattern of the precision matrix corresponds to the the 4-nearest neighbor graph and the non-zero coefficients are set as and . We set the sample size and vary the number of nodes . Table 1 shows the empirical coverage rate for different values of for four chosen coefficients. As is evident from the table, the coverage probabilities for the unknown coefficient is remarkably close to nominal.

| 95.4% | 92.4% | 93.8% | 93.2% | |

| 94.6% | 92.4% | 92.6% | 94.0% | |

| 94.6% | 94.8% | 92.6% | 93.8% |

Non-negative Gaussian.

For simplicity we first consider score matching for non-negative Gaussian model with . Following the setting and notation in the previous paragraph, we have

As before, is separable into two parts; we focus on one to obtain

We can see that it contains expectations, such as , which are hard to calculate explicitly, in addition to the matrix inversion. To the best of our knowledge, this calculation is intractable. If we instead use generalized score matching with , the calculation would be more complicated.

One exception is when the precision matrix , which means follows i.i.d. non-negative standard normal distribution. Using the moments , , , , we can calculate explicitly. It turns out that the two parts in are the same. All their components take the same value at approximately , except for one component that takes the value approximately . Therefore, we can see that the sparsity assumption on is violated. It instead only satisfies a weaker condition that for large . Similarly, we can calculate that for large . We then follow the debias method in Section 5 to construct confidence intervals.

For the simulation, we use the same setting as for the Gaussian graphical model with and . We set , and use the minimax tilting method to generate the data (Botev, 2017). We first support the bounded norm condition of through experiments with a small and large . Here we focus on the edge ; results for other edges are similar, and are therefore omitted. Since we have enough samples, we estimate as the exact inverse of the empirical quantity . Table 2 shows the average mean and maximum of the norm of on column , based on 500 independent simulation runs with different sample sizes. This shows that the norm of the column of would be bounded from above. These experimental results indicate that the bounded norm condition of is reasonable.

Table 3 shows the empirical coverage rate for various choices of and . Note that since we are doing sample splitting, the real sample size is . We observe that by using the debias method, we can obtain nominal coverage rate even for relatively large with small .

| averaged mean, | 13.01 | 11.42 | 11.16 | 11.10 |

|---|---|---|---|---|

| averaged max, | 17.84 | 13.46 | 11.95 | 11.52 |

| averaged mean, | 24.71 | 15.19 | 12.90 | 12.72 |

| averaged max, | 32.65 | 17.86 | 14.13 | 13.17 |

| 94.2% | 93.8% | 95.0% | 92.4% | |

| 95.2% | 96.6% | 94.8% | 94.6% | |

| 94.8% | 95.8% | 95.0% | 94.4% |

Normal conditionals.

For the experiment, we consider a special case of normal conditionals with parameter matrix, whose density is

| (74) |

This distribution is also considered in Lin et al. (2016). We set , , and we use a 4 nearest neighbor lattice dependence graph with interaction matrix: and . Since the univariate marginal distributions are all Gaussian, we generate the data using a Gibbs sampler. The first 500 samples were discarded as ‘burn in’ step, and of the remaining samples, we keep one in three.

We first support the assumption M through experiments with a small and large . Here we focus on the edge ; results for other edges are similar, and are therefore omitted. We estimate as in Step 2, but without the regularization term since we have enough samples. For normal conditionals, we have . There are five components in with relatively large non-zero values (not decreasing with ), and we calculate the mean and maximum absolute value of the remaining 35 components. Table 4 shows the average mean and maximum absolute values of these 35 components, based on 500 independent simulation runs with different sample sizes. This suggests that the population quantity would be close to a sparse vector, with an infinite amount of samples. These experimental results indicate that assumption M is reasonable, at least in an approximately sparse version.

We then set the number of samples , and follow the proposed three-step procedure to calculate the coverage rate. Table 5 shows the empirical coverage rate for and nodes. Again, we see that our inference algorithm behaves well on the above Normal Conditionals Model.

| average mean | ||||

|---|---|---|---|---|

| average max |

| 93.2% | 93.4% | 94.6% | 95.0% | |

| 93.2% | 93.0% | 92.6% | 93.0% |

Exponential graphical model.

We choose , and a 2 nearest neighbor dependence graph with . We again first support the assumption M through experiment with a small and large , where we focus on the edge and use a Gibbs sampler to generate data. For exponential graphical model, we have . There are four components in with relatively large non-zero values (not decreasing with ), and we calculate the mean and maximum absolute value of the remaining 34 components. Table 6 shows the average mean and maximum absolute values of these 34 components, based on 500 independent simulation runs with different sample sizes. This suggests that the population quantity would be close to a sparse vector, with an infinite amount of samples. Once again, this experiment results indicate that assumption M is reasonable, at least in an approximately sparse version.

We then set and the empirical coverage rate and histograms of estimates of four selected coefficients are presented in Table 7 and Figures 2 for and , respectively.

| average mean | ||||

|---|---|---|---|---|

| average max |

| 94.2% | 91.6% | 92.6% | 92.4% | |

| 92.6% | 92.0% | 92.2% | 92.4% |

We can see from the simulations here that we need more samples for inference based on non-negative score matching to be valid, compared to regular score matching. The results are still impressive as the sample size is small relative to the total number of parameters in the model. Moreover, by using the generalized score matching with , we get more accurate empirical coverage compared to the original score matching, which uses . The histograms in Figures 2 show that the fitting is quite good, but to get a better estimation and hence better coverage, we would need more samples.

Simultaneous inference.

We then apply the simultaneous inference procedure to test for all the edges connected to some node . Since the sample complexity (41) for simultaneous inference is large, we set . For hypothesis testing, we focus on the first node and we would like to test the null hypothesis

| (75) |

versus the alternative

| (76) |

We set the designed Type I error as and we consider Gaussian and Non-negative Gaussian settings as before. Table 8 shows the empirical Type I error under the null with different choices of sample size. We see that our procedure works well as long as we have enough data.

| Gaussian | 0.082 | 0.074 | 0.042 | 0.052 | 0.048 |

| Non-negative Gaussian | 0.072 | 0.062 | 0.054 | 0.040 | 0.046 |

Simultaneous inference with general .

We finally consider the simultaneous inference with general . We consider the normal conditionals model with density

This corresponds to . We apply the two methods in Section 7 to test for all the edges connected to some node . We set and the designed Type I error . For hypothesis testing, we focus on the first node (i.e., ). Table 9 shows the empirical Type I error under the null with different choices of sample sizes. We see that both methods work well as long as we have enough data.

| Gaussian multiplier bootstrap | 0.076 | 0.058 | 0.054 | 0.048 |

| Moderate deviation method | 0.182 | 0.092 | 0.068 | 0.056 |

9 Protein Signaling Dataset

In this section we apply our algorithm to a protein signaling flow cytometry data set, which contains the presence of proteins in cells (Sachs et al., 2005). Yang et al. (2015) fit exponential and Gaussian graphical models to the data set.

Figure 3 shows the network structure after applying our method to the data using an Exponential Graphical Model. We learn the structure directly from the data as well as provide confidence intervals using the Exponential Graphical Model, rather than log-transforming the data and fitting Gaussian graphical model as was done in Yang et al. (2015). To infer the network structure, we calculate the -value for each pair of nodes, and keep the edges with -values smaller than 0.01. Estimated negative conditional dependencies are shown via red edges. Recall that the exponential graphical model restricts the edge weights to be non-negative, hence only negative dependencies can be estimated. From the figure we see that PKA is a major protein inhibitor in cell signaling networks. This result is consistent with the estimated graph structure in Yang et al. (2015), as well as in the Bayesian network of Sachs et al. (2005). In addition, we find significant dependency between PKC and PIP3.

10 Conclusion

Motivated by applications in Biology and Social Networks, much progress has been made in statistical learning models and methods for networks with a large number of nodes. Graphical models provide a powerful and flexible modeling framework for such networks to uncover the dependency among nodes. As a result, there is a vast literature on estimation and inference algorithms for high dimensional Gaussian graphical models, as well as more general graphical models in the exponential family. As a disadvantage of most of these works, the normalizing constant (partition function) of the conditional densities is usually computationally intractable and without closed-form formula. Score matching estimators provide a way to address this issue, but so far all the existing works on score matching focus on estimation problem for high-dimensional graphical models without statistical inference. In this paper, we fill this gap by proposing a novel estimator using the score matching method that is asymptotically normal, which allows us to build statistical inference for a single edge of the graph. Moreover, we propose the procedure on simultaneous testing on all the edges connected to some specific node in the graph, using the Gaussian multiplier bootstrap method. This procedure can be used to test if certain nodes are isolated or not, recover the support of the graph, and test the difference between two graphical models. There are a number of interesting and important directions that will be explored in future. For example, developing inferential techniques based on score matching for multi-attribute graphical models (Kolar et al., 2013, 2014), graphical models with confounders (Geng et al., 2019, 2018), time-varying graphical models (Zhou et al., 2010; Kolar et al., 2010b; Kolar and Xing, 2011), networks with jumps (Kolar and Xing, 2012) and conditional graphical models (Kolar et al., 2010a), as well as data with missing values (Kolar et al., 2010a). It is also of interest to incorporate constraints in the model and perform constrained inference (Yu et al., 2020). Finally, our method is developed for continuous data and developing results for discrete valued data is also of interest.

Acknowledgments

We are extremely grateful to the associate editor, Jie Peng, and two anonymous reviewers for their insightful comments that helped improve this paper. This work is partially supported by an IBM Corporation Faculty Research Fund and the William S. Fishman Faculty Research Fund at the University of Chicago Booth School of Business. This work was completed in part with resources provided by the University of Chicago Research Computing Center.

A Technical proofs

We first establish a bound on the size of and in the following lemma.

Lemma 9

Assume the conditions of Theorem 2 are satisfied. Then

Proof From the KKT conditions we have that satisfies

where . Restricted to , we have (elementwise)

Computing the norm on both sides,

For the first term we have that

using Negahban et al. (2012). For the second term, we have that

Combining the two bounds, we obtain

Now, proceeding as in the proof of Theorem 3 in Belloni and Chernozhukov (2013), we establish that

The proof for is similar.

Our next result establishes bounds on .

Lemma 10

Assume the conditions of Theorem 2 are satisfied. Then

Proof From the KKT conditions we have that satisfies

while satisfies

Combining these two equations we have

and

Therefore, using Negahban et al. (2012),

Combining with Lemma 9, we obtain

A similar result can be established for , which we state without proof, as it is analogous to the proof of Lemma 10.

Lemma 11

Assume the conditions of Theorem 2 are satisfied. Then

To simplify notation later, let and , for .

Lemma 12

Under the conditions of Theorem 2, we have

Proof Let be the set of -sparse vectors in the unit ball,

Abusing the notation, let denote the sparse spectral norm for matrices, that is,

Using Lemma 4.9 of Barber and Kolar (2018),

for any fixed matrix and vectors , and any . With this, we have

where the second line follows from the assumption SE, and

Lemma 10 and Lemma 11.

Lemma 13

Under the conditions of Theorem 2, we have

Proof Using Hölder’s inequality, we have

On the event , we have . Finally, using Lemma 11, we conclude that

Lemma 14

Under the conditions of Theorem 2, we have

Proof We have that

For the second term, we have

since we are working on the event . Since

, combining with the

display above, the proof is complete.

Lemma 15

Under the assumptions M and R, we have that

where .

Proof Let . Then

| (77) |

From Forbes and Lauritzen (2015), we have that and

is finite. An application of the central limit theorem

completes the proof.

Lemma 16

The variance estimator is consistent, .

Proof The variance estimator is obtained by using the second sample moment, and replacing true with . We show the consistency of by showing the consistency of the estimator for and , respectively.

Step 1.

We can write

Let denote the population version of and the sample version. With high probability we have that

Step 2.

We estimate the variance of . Since

we can use the second sample moment to estimate the variance. As above, we plug in and , to obtain that

Combining the results of the two steps, completes the proof.

Proof of Theorem 6

Denote

| (78) |

as the counterpart to . Let

| (79) |

Denote

| (80) |

where is defined in assumption RR. In order to apply Theorem 3.2 in Chernozhukov et al. (2013), we check the following conditions:

-

1.

.

-

2.

.

-

3.

With probability at least , . Here denotes the probability with respect to , conditionally on the observed data.

We verify the first condition by applying Lemma A.1 in van de Geer (2008). By the definition of , clearly we have . Together with assumption RR, we apply Lemma A.1 in van de Geer (2008) and obtain

According to (41), for sufficiently large , we have , for some . By Markov inequality,

which verifies the first condition.

Next, we verify the second condition. For a fixed , under the null, we have

with probability at least , where the second inequality comes from the consistency of , Lemma 13, and Lemma 15. We then have

which verifies the second condition.

Finally, we verify the third condition. We have

| (81) |

Denote . Under the null we have

According to Lemma A.1 in Chernozhukov et al. (2013), we have

uniformly for each , where

| (82) |

and

| (83) |

We then have