Computational Socioeconomics

Abstract

Uncovering the structure of socioeconomic systems and timely estimation of socioeconomic status are significant for economic development. The understanding of socioeconomic processes provides foundations to quantify global economic development, to map regional industrial structure, and to infer individual socioeconomic status. In this review, we will make a brief manifesto about a new interdisciplinary research field named Computational Socioeconomics, followed by detailed introduction about data resources, computational tools, data-driven methods, theoretical models and novel applications at multiple resolutions, including the quantification of global economic inequality and complexity, the map of regional industrial structure and urban perception, the estimation of individual socioeconomic status and demographic, and the real-time monitoring of emergent events. This review, together with pioneering works we have highlighted, will draw increasing interdisciplinary attentions and induce a methodological shift in future socioeconomic studies.

keywords:

Socioeconomics; network science; data mining; machine learning1 Introduction

Many branches of science have experienced the paradigm shift from qualitative to quantitative studies. Even the most representative one for quantitative sciences, physical science, has undergone a long period for qualitative explorations in its early stages. For example, more than two thousand years ago, Aristotle raised the famous four elements theory, which claims that the four classical elements, namely earth, water, air and fire, are the material basis of the physical world. At almost the same time, some Chinese ancient philosophers proposed the Wu Xing theory (i.e., the Chinese five elements theory), which is a fivefold conceptual scheme that uses the proportion of ingredients and movements of the five elements (i.e., metal, wood, water, fire and earth) to explain a wide array of phenomena, from the cosmic cycles to the validity of a dynasty. For about two thousand years, the ancient Greek system, contributed by Aristotle and some others, represents the most advanced understanding of the world, which is indeed one of the most influential theory in human history. Up to the end of the middle ages, thanks to the quantitative analyses and experimental verifications, these ancient theories, such as Aristotle’s four elements theory and kinetic theory, were progressively replaced by modern scientific theories like the Atomic theory and the Newton’s laws.

In contrast to physical science that concentrates on the study of matter and its motion through space and time, social science investigates the social structure based on the activities of and relations between human beings, including sociology, economics, politics, linguistics, jurisprudence, and many other branches. In comparison with physical science, the way from qualitative to quantitative studies is more difficult for social science. On the one hand, the objects under social science study are much more complex than those under physical science study. An individual person is one of the most important units for social science study, playing an analogous role to an atom in physical science [1]. However, human behaviors exhibit heterogeneity and burstiness: different people have much different behavioral patterns and even the same person shows far different behaviors in different spaces and times [2]. Therefore, except a certain success in analyzing the flow of human crowds [3, 4], to treat human beings as atoms will kill many interesting social phenomena. Some other objects under study are naturally not easy to be characterized numerically, such as policies and legal provisions. On the other hand, social science study inevitably suffers from uncertainty and incompleteness. The factors affecting social development are countless, and thus any seemingly coverall theory cannot include all relevant factors and be self-contained. In addition, every single factor is unstable and not independent, being affected by other factors and the external environment. The above intrinsic complexity makes it infeasible to quantitatively test and verify any social theory through controllable repeated experiments in a closed environment, while such experimental verification is indeed the methodological cornerstone that pushes forward physical science and other branches of natural science [5]. At the same time, social science is not good at quantitative predictions to the future, with many predictions from experts and complicated theories being no better than wild guesses [6]. What a pity is that such incorrect predictions cannot subvert the corresponding social theories (much different from physical science) since the mistakes are attributed to the unknow/undetected factors or emergent events [7], instead of the flaws of the theories themselves.

Up to now, along with the development of quantitative methods, social science has successfully learned how to be wise after the event. That is to say, we can always find some theoretical models (possibly together with some cosmetic changes) to provide qualitatively correct or even quantitatively accurate explanations after the event. However, these theories are usually powerless in predicting the future. Confronting such straits, social scientists should not turn back to the qualitative description, but insist on quantitative explanation and prediction, and evaluate the validity of a theory based on its explanatory power and prediction accuracy before the event. In fact, social science study recently shows higher and higher level of quantification and becomes increasingly dependent on real data [8, 9]. However, the traditional way to obtain real data has many limitations. For example, survey data from questionnaires and self-reports usually contains a small number of samples and suffers from social desirability bias (i.e., subjects tend to give socially acceptable answers, instead of the real facts) [10]. Larger-scale and more precise data, such as data from economic census, usually consumes huge resources and lacks timeliness. In many poor countries and regions, population-scale economic census is not feasible. Fortunately, thanks to the digital wave that sweeps across the whole world [11], social scientists have an unprecedented opportunity to develop a quantitative methodology. Indeed, it is for the first time in history, data in the processes of social and economic development, as well as the data of human activities, are recorded by more and more sensing devices, online platforms and other data acquisition terminals. However, these data are not well-structured and are different from the normally handled data in social science. Typical examples include satellite remote sensing data, mobile phone data, social media data, and so on. On the one hand, to understand and analyze these data asks for advanced techniques in data mining and machine learning, which is a considerable challenge to traditional social scientists. On the other hand, these data are of larger size, almost in real time and with higher resolution, which can reduce the sparsity and bias in small-size data, and reduce the invisible parts in the developing processes (e.g., data points in two consecutive censuses are usually across a few years, and the changes in between are not visible). Therefore, based on these large-scale novel data, we can in principle make great progress in perceiving socioeconomic situations, evaluating and amending known theories, enlightening and creating new theories, detecting abnormal events, predicting future trends, and so on.

The above-mentioned challenges and corresponding attempts have led to the emergence of a new scientific branch, which studies various phenomena in socioeconomic development by using quantitative methods that based on large-scale real data, with particular attention to the economic development problems related to social processes and the social problems related to economic development. We name it as Computational Socioeconomics, which is immature, but future-pointing and burgeoning. The computational socioeconomics can be considered as a new branch of socioeconomics resulted from the transformation of methodology, or as a new branch of computational social science by emphasizing on socioeconomic problems.

In the above definition, three keywords are worth paying close attention to. The first one is “quantitative methods”, which emphasizes the usage of numerical values, rather than qualitative description, in characterizing problems and presenting results. In the 5th century BC, the ancient Greek doctor Hippocrates (who is often referred to as the “Father of Medicine”) proposed the four temperaments theory, which suggests that there are four fundamental personality types: sanguine, choleric, melancholic, and phlegmatic, and the personality type of an individual is determined by the excess or lack of four body fluids: blood, yellow bile, black bile, and phlegm [12]. Such a qualitative theory, analogous to the impacts of the four elements theory on physical science, has ruled social psychology (in particular the studies on personality) for more than two thousand years. In despite of some reasonable ingredients, the four temperaments theory has stayed on the level of qualitative description, and thus failed to accumulate scientifically solid achievements in its long-time development. Only after modern psychologists obtained quantitative evaluations of the Big Five personality traits via standard scales, personality analysis became an important research domain that plays central roles in many issues of social psychology [13]. Such example show the importance and necessity of the development of quantitative methods. The second one is “real data”, which emphasizes that any theoretical model should respect real data and use the explanatory power and prediction accuracy for real data as the evaluation criteria for its validity. Economics shows a high level of quantification, with most theoretical models being precisely described by a group of elegant equations. Accordingly, given the values of necessary parameters, many targeted economic variables are calculable. However, the majority of economic theories have cocooned themselves in a quantitative fantasyland consisted of ideal assumptions while largely ignored real data. It eventually makes the classical economic theories beautiful rather than practical. For the short term, it cannot predict the upcoming economic crisis [14] (but it can always find out graceful and reasonable theoretical explanations after the crisis [15]). For a long time, it failed to provide effective strategies on economic development for more than a hundred of developing countries over the world [16]. The third one is “large-scale”, which emphasizes the importance of population-scale data (i.e., the data that can directly reflect the entire population under study, instead of a small sample). A very small data set may not only bring statistical bias, but result in completely wrong conclusions. For example, a widely accepted theory by academic community, which has also been validated by various experiments on small-scale social networks, is that the interacting strength between two connected individuals (which can be measured by the frequency and duration of mobile communication or the number of comments, replies and mentions on a social platform, and so on) decays as the increase of the range of their link (the range of a link is defined as the shortest distance between its two endpoints after the removal of this link, and a large link range indicates that the two corresponding endpoints locate in two distant communities with few overlapping nodes) [17, 18]. A very recent experiment on 11 population-scale social networks, however, shows that the interacting strengths through very long-range links are not weaker than those through short-range links [19], which fundamentally challenges our traditional understanding of social network organization.

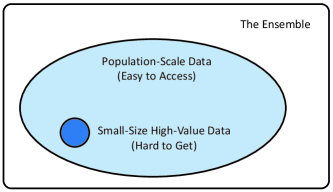

In comparison with routine methods in social science, the increasing diversity and volume of data lead to methodological changes in two aspects. Firstly, simple statistical tools are not suitable for analyzing unstructured data, such as remote sensing images, street views, social networks, textual content, and so on. Therefore, researchers are badly in need of artificial intelligence, in particular advanced techniques of data mining and machine learning, such as deep learning [20]. Secondly, with population-scale data, sampling is not a necessary method to estimate the statistical properties of the whole population. Instead, one can concentrate on a small-size subset sampled from the original data in hand, and add new dimensions of data. These new data dimensions are usually of high values, which can be obtained from traditional ways like manual labelling and questionnaire survey. Using such a small sample as the training data, one can learn a model to infer new dimensions of data from the original dimensions. Applying such model to the whole data set, new dimensions of data for all individuals appeared in the original dataset can be obtained in principle. Such method integrates some routine methods like sampling, labelling and surveying, while it is much more powerful. For example, it is relatively easy to obtain the population-scale data on mobile communication and mobility (all can be obtained from mobile phones), in contrast, it is very hard to know the household income of every family since a poor country cannot support a population-scale economic census and such data is usually treated as official secrets that are not open for public or research institutions. Under the circumstances, we can obtain household incomes of a certain number of families (what we need is just a tiny fraction of all families) via routine questionnaires. These much smaller data set can be used as training data, based on which we can apply machine learning techniques to build a model that can predict household income of a family from the mobile phone data of the family members [21]. Although the inferred data is not perfect, it can be very close to the real data under a certain well-designed algorithm. Notice that, a significant advantage is that the high-value data for almost every individual can be obtained at a very low cost. As shown in Figure 1, combining the accessible population-scale data, a small sample of high-value but hard-to-get data, and a properly selected or well-designed algorithm to infer the high-value data for individuals other than the sample is a novel and representative method in the computational socioeconomics study, showing the deep integration of social science and computer science methods.

Long-term speaking, no matter computational socioeconomics will become a mature branch of science with distinct borderlines or it will completely integrate into the framework of traditional social science, the above-mentioned novel perspective and methodology, driven by big data and artificial intelligence, will definitely become the mainstream in the future and change the landscape of science research in a profound and irrevocable way. Inspired by this positive judgment, we decide to present this review article. In addition, there are three technical reasons for us to write this review. Firstly, computational socioeconomics is an emerging research domain with research findings published in disparate journals and conference proceedings across many disciplines. Therefore, it is necessary to collect these results together. Secondly, we would like to sort and classify representative results according to the objects and data sets under study, so that it is easy for readers to see the landscapes of both methods and achievements. A proper taxonomy can largely reduce the difficulty to master the related knowledge and methods. Although the presented one is built just according to the current progresses of this field, it will evolve to be a more systematic and reasonable one along with further studies. Thirdly, in the nascent stage of computational socioeconomics, different research articles used different expressions to describe essentially the same problems and methods, and thus it is valuable to unify the problem description and the symbolic system. In a word, we hope this review will become a handbook for researchers who are willing to contribute to the development of computational socioeconomics. Furthermore, the paradigm shift in methodology, as presented in this review, is not only relevant to socioeconomics, but also to most branches of social science and to many other qualitative disciplines beyond social science.

The remainder of this review article is organized as follows. The second section will discuss some important problems at the macroscopic scale, such as the world economic development, the competitive powers of countries, the inequality problem, and so on. The third section will mainly concentrate on the urban scale and introduce some novel ways to solve problems related to the regional economic development, such as how to precisely perceive regional socioeconomic status and how to choose the suitable development paths and strategies for a city. The fourth section will focus on individual level, discussing how to make use of some unobtrusive data to estimate the individual socioeconomic status, including income, employment situation, and even health condition. The fifth section will go a little beyond the scope of computational socioeconomics, and to discuss how the frequently-used data in the previous sections can be utilized to benefit the emergency management and disaster assistance. We cover such issue because the emergency management is an increasingly important social problem and the reported methods are consistent to the methods introduced in the previous sections. In this review, many different data resources have played important roles, among which the following three are the most important: remote sensing satellites, mobile phones and social media platforms. For each of the three data resources, there are some certain representative analytics tools and methods, so it is very effective to sort the results according to the data resources and corresponding methods. Finally, in the last section, we will summarize representative progresses, explore the tendency of the development of computational socioeconomics, discuss the challenges and opportunities in this emerging field, and outline some potentially interesting and significant open issues.

2 Global development, inequality and complexity

2.1 World development and poverty mapping

Revealing the status of economic development is one of the long-standing problems in socioeconomics [22, 23]. Recently, data with improved quantity and quality have been used to map nations’ economic characteristics such as poverty, which comes with economic development and is a major cause of societal instability. Based on an international poverty line at USD 1.25 a day in 2008 [24], 1.2 billion people (21%) lived in poverty in 2012 [25]. Reducing poverty is thus a key target of the Millennium Development Goals (MDGs). To approach this goal, the first step is to accurately map the spatial distribution of poverty [26]. New data and tools have been utilized to better reveal, explain and predict global poverty and economic inequality. In this section, we will briefly introduce literature that map poverty from satellite imagery, infer socioeconomic status from mobile phone (MP) data and fight against poverty with combined data.

2.1.1 Remote sensing observes poverty

Remote sensing (RS) is the acquisition of information by using sensor technologies to detect objects on earth, which is originally used in earth science disciplines [27]. In recent years, high resolution data from RS, for example, nighttime lights (NTLs) satellite imagery, has been used to supply information about economic activity, especially in developing countries where traditional economic census data are insufficient [28]. With a great potential for recording the presence of humanity on the surface of earth, NTLs data can provide an unambiguous indication of the spatial distribution of economic development. Indeed, NTLs have been found to be a powerful predictor of ambient population density and economic activity. Nightsat [29] is a concept for a satellite system, which is capable of global observation. The Nightsat can capture the location and density of lighted infrastructures within human settlement.

One of the pioneering works by Elvidge et al. [30] suggested that NTLs data can be used as a proxy for socioeconomic development in developing countries. Lighted area has a high correlation with the gross domestic product (GDP) and electric power consumption. Moreover, lighted area is strongly correlated with GDP for 21 countries. Latter, by combing lighted area with ancillary statistical information of a city, Doll et al. [31] investigated the potential of NTLs data for quantitative estimation of global socioeconomic parameters. They found that the country-level total lighted area exhibits significantly high correlations with GDP and emission. Sutton and Costanza [32] estimated the amount of light energy (LE) from satellite images with global coverage at a high spatial resolution. They found that LE is correlated with GDP at the national level and can serve as a more accurate indicator of economic activity. That is because LE is more spatially explicit and can be directly observed and easily updated almost in real time.

Together with census and survey data, NTLs data have been applied in mapping poverty. Ebener et al. [33] applied regression methods using NTLs imagery to model the distribution of wealth within 171 countries at the national level and 26 countries at the subnational level. They showed that NTLs data is correlated with GDP per capita and other socioeconomic indicators. Noor et al. [34] computed asset-based poverty by applying the principal component analysis (PCA) to NTLs data and household survey data of 37 countries in Africa. They found that the mean brightness of NTLs data can offer a robust and inexpensive alternative to asset-based poverty indices derived from survey data, suggesting that it is possible to explore and track economic inequity at subnational levels by leveraging NTLs data. For Uganda, Rogers et al. [35] presented a discriminant analysis model to predict poverty after combining satellite imagery and household survey data. They estimated the poverty index by the likelihood of each pixel falling within a specified poverty class. They found that external and independent data have descriptive power for poverty mapping. These novel data sources are likely to outperform socioeconomic datasets that are internally correlated and exploited by small area methods.

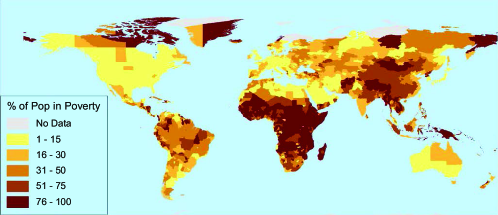

A spatially disaggregated global poverty map of 233 countries was produced by Elvidge et al. [36]. The poverty levels were estimated by dividing the LandScan population count data [37] by the brightness from NTLs data (see Figure 2). The produced poverty indices correlate very strongly with other widely accepted measures, suggesting that satellite imagery can enhance the knowledge of socioeconomic conditions around the world at a fine spatial resolution. Later, Ghosh et al. [38] proposed a model to estimate the world-wide economic activity. In their model, a grid of nonagricultural economic activity was created according to the NTLs, while a grid of agricultural activity was created according to the LandScan population grid. Then, by integrating the two grids, a disaggregated map of total economic activity was produced, which can provide an alternative means for measuring global economic activity and predicting future socioeconomic trends.

To better estimate true income growth from NTLs, Henderson et al. [39] developed a statistical framework to estimate two parameters. One is a coefficient that maps NTLs growth into a proxy for GDP growth, and the other is an optimal weight to combine this proxy with national account data. After applying the method to countries with very low-quality national account data, Henderson et al. [39] demonstrated the key role of NTLs data in analyzing growth at the subnational and supranational levels. With the NTLs data, income data and papulation data of 748 regions across 54 countries in Africa, Mveyange [40] estimated the regional income inequality by calculate two standard measures of inequality, the Gini index and the mean log deviation (MLD) measure [41]. After presenting the empirical model, they showed that the estimated inequality index has significant and positive correlations with income-based regional inequality indicators, suggesting that NTLs are good proxies to estimate regional inequality. These results are especially meaningful in the lack of reliable and consistent subnational income data.

Cauwels et al. [42] explored the dynamics and spatial distribution of global NTLs for 160 different countries. They found that the center of light moves eastwards about 60 km per year, and there is a tendency of global centralization of light. After introducing spatial light Gini coefficients, they found a universal pattern of human settlements across different countries. Ghosh et al. [28] summarized literature that leveraged NTLs to develop a variety of alternative measures of human well-being. They introduced the application of NTLs to estimate various human well-being indicators (e.g., GDP, poverty, informal economic activity and remittances), develop the night light development index (NLDI), map the human ecological footprint, measure the electrification rates and estimate the ICT Development Index (IDI). Recently, Bennett et al. [43] summarized the methods to correlate NTLs with socioeconomic parameters including urbanization, economic activity and population. They highlighted the value of NTLs for detecting, estimating and monitoring socioeconomic dynamics.

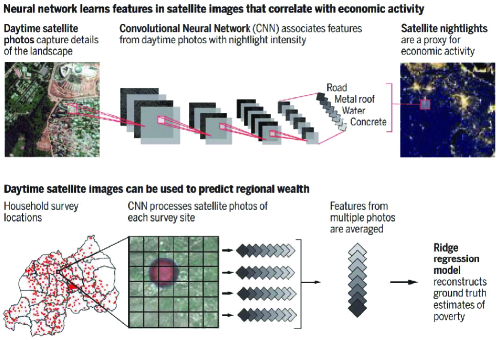

NTLs data are successful in revealing economic activity, however, it is not effective for less developed areas due to the uniformly dark of satellite imagery in these areas. To this point, Jean et al. [44] applied deep learning algorithms to learn the relationship between NTLs and daytime satellite imagery. The former can predict the wealth distribution while the latter contains rich information about landscape features. They employed a multi-step transfer learning approach [45] to train a convolutional neural network (CNN) [46]. In particular, a linear chain transfer learning graph was constructed. First, they transferred knowledge from the object recognition on the ImageNet (Problem 1) [47], an object classification image dataset of over 14 million images from 1000 different categories, to the prediction of NTL intensity from daytime satellite imagery (Problem 2). They chose the model trained on ImageNet as the starting CNN model [48], and then constructed the fully convolutional model. Formally, given an unrolled -dimensional input , the fully connected layers perform a matrix-vector product,

| (1) |

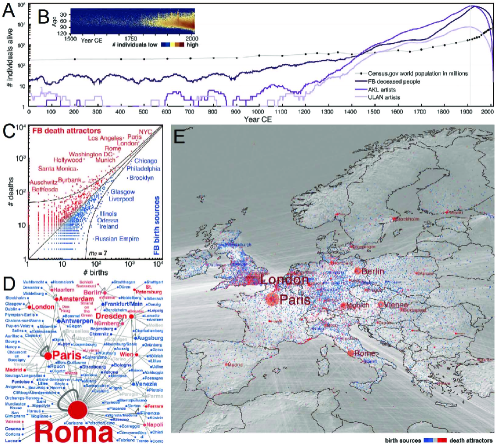

where is a weight matrix, is a bias term, is a nonlinear function, and is the output. Then, they transferred knowledge from Problem 2 to the prediction of poverty from daytime satellite imagery (Problem 3), for which the amount of training data is limited. The illustration of the method is summarized by Blumenstock [21] (see Figure 3), and technical details are presented in the early work by Xie et al. [46]. The image features extracted from the daytime imagery can explain up to 75% of the variation in the average household asset across five African countries. Moreover, the method is able to reconstruct survey-based indicators of regional poverty with high accuracy. Using only publicly available data, the method has broad potential applications in tracking and targeting poverty in developing countries.

Other RS data and machine learning approaches can also be used in quantifying poverty-environment relationships. By applying the principal component analysis (PCA) and spatial models in the field of geostatistics, Sedda et al. [49] demonstrated the correlations between the normalized difference vegetation index (NDVI, a measure of vegetation greenness in RS [50]), intensity of poverty, and health for a large area of West Africa. They found that high NDVI is associated with low poverty and child mortality. Their results highlight the utility of satellite-based metrics for poverty analysis. With high-resolution daytime satellite imagery, the UN Global Pulse Lab Kampala built a proxy indicator for poverty based on the household’s roof counting. The research project entitled “Measuring Poverty with Machine Roof Counting” [51] developed image processing software to count the roofs and identify the type of roof that a house has. Watmough et al. [52] applied a random forests approach to study the relationships between welfare and geographic metrics for over 14,000 villages in India. They found that geographic metrics account for 61% and 57% of the variation in the lowest and highest welfare quintile, respectively. These methods help estimate socioeconomic status in less developed countries where household surveys remain lacking.

2.1.2 Mobile phones reveal socioeconomic status

Mobile phones (MPs), serving as ubiquitous sensors, are increasingly common in developing economies. Compared to coarse-grained remote sensing, MPs are able to capture an enormous information and provide cost-effective data at the individual level, such as the frequency and timing of communication events [18, 53, 54], the traveling patterns [55], the histories of consumption and expenditure [56], and so on. With MP logs that are related to housing, education, health, etc., socioeconomic status can be inferred by employing regression models and machine learning approaches at the aggregated subnational and national levels.

To explore the relationship between MP usages and wealth in developing countries, Blumenstock et al. [56] presented a novel method that contains three steps: (1) modeling the relationship between assets and expenditures using Demographic and Health Survey (DHS) data; (2) conducting a phone-survey with a small subset of MP users to collect information on asset ownership; (3) obtaining call detail records (CDRs) for the individuals in the phone survey and creating a single dataset that use call histories to predict annual expenditures. By analyzing the data from Rwanda, they found that household expenditures are positively correlated with MP usages, mainly with the numbers of international calls, the number of different districts contacted, and the average airtime credit purchase. Airtime credit is money in MP number account, ready to spend on texts, calls and data. These results suggest that the annual expenditures of MP users can be predicted only using their anonymous phone usage data. Blumenstock and Eagle [57] later found that MP usages in Rwanda are not uniform. They provided a quantitative description about the demographic and socioeconomic structure of MP usages, for example, phone owners are considerably richer and predominantly male. Moreover, Blumenstock et al. [58] showed that Rwandans use MP network to transfer their airtime credit to those affected by disasters. In particular, transfers tend to be sent to rich individuals and between pairs of individuals with a strong history of reciprocal.

Individual MP data can be aggregated to estimate socioeconomic status at the national level. By analyzing CDRs and airtime credit purchase histories, Gutierrez et al. [59] mapped the relative income of individuals, the diversity and inequality of income, and the socioeconomic segregation for fine-grained regions in Côte d’Ivoire. In particular, they quantified the variation in purchase amounts of each user by using the Coefficient of Variation (CV),

| (2) |

where and are the standard deviation and the mean of the purchase amounts. They found that urban areas clearly stand out in diversity, showing the opportunity to obtain real-time and low-cost socioeconomic statistics. Also for Côte d’Ivoire, Smith et al. [60] demonstrated how aggregated CDRs can be mined to derive proxies of socioeconomic indicators. They found strongly negative correlations between the communication activity within a region and the multidimensional poverty index (MPI) [61], a survey-based indicator that measures a region’s actual poverty. Further, they derived a linear model to estimate the poverty level using the diversity of communication. Their work suggests CDRs as an invaluable source for poverty estimation, even without the knowledge of individual behavior.

MP data from Côte d’Ivoire has also been used to explore the relations between national communication network and socioeconomic dynamics. Mao et al. [62] introduced the CallRank indicator–the PageRank centrality [63] calculated over the MP communication network–to quantify the relative importance of an area and tested the correlation between network features and socioeconomic indicators. They found that the outgoing call ratio consistently correlates with local socioeconomic statistics such as low poverty rate and high annual income. Moreover, the Gini index exhibits significant correlations with CallRank and other CDRs-based indicators. Further, to quantify the strength of the rich-club effect [64, 65], they measured the weighted rich-club coefficient of the MP communication network,

| (3) |

where , and corresponds to the null model generated by randomizing the original MP network while preserving its degree distribution. Here, each node has a richness parameter as the average annual income of the region, is the total number of links, is the number of links to the region, is the sum of the weights attached to these links, and with are the ranked weights of links on the network. If , network shows the rich-club effect in comparison with the null model. The extent to which is larger than 1 indicates the strongness of the rich-club effect. After analyzing the CDRs, Mao et al. [62] found that rich areas form rich club in MP communication, where rich areas communicate more frequently with each other.

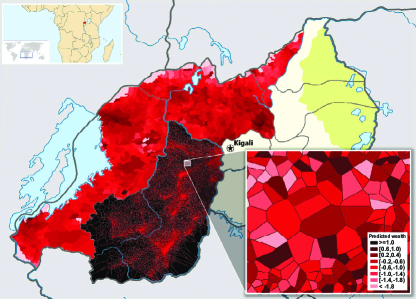

By analyzing anonymized records of interactions on Rwanda’s MP network and the follow-up phone surveys of some individual subscribers, Blumenstock et al. [66] predicted the wealth of MP users. They demonstrated that the predicted attributes of individuals can accurately reconstruct the distribution of the entire nation’s wealth. Specifically, they used a two-step approach in feature engineering and model selection, where the first step generates a thousand metrics from the MP data, and the second step eliminates irrelevant metrics and selects a parsimonious model using the elastic net regularization [67]. After applying this machine learning approach to analyze the survey data, they found that individual wealth can be well predicted and individuals in relative poverty can be accurately identified. Then, they generated out-of-sample predictions for 1.5 million MP users and produced the wealth map of Rwanda at a very high resolution (see Figure 4). Further, they found a strong correlation between the government “ground truth” data and the predicted wealth data after aggregating them to the district level. Their method is promising to map the distribution of wealth and other socioeconomic indicators for the full national population. Other works that leveraged MP data to infer socioeconomic status at the regional or urban levels will be introduced in the following sections.

2.1.3 Combined data for better inference

Novel sources of data with a high spatial resolution have been used to provide an up-to-date indication of living conditions. For example, remote sensing (RS) data capture information about physical properties of the land, which are cost-effective but relatively coarse in urban areas. By contrast, call detail records (CDRs) from mobile phones (MPs) have high spatial resolution in urban areas but the resolution is usually insufficient in rural areas due to the sparsity of towers. Therefore, some recent works estimate socioeconomic status by combining data from different domains such as LandScan population [37], RS and MPs.

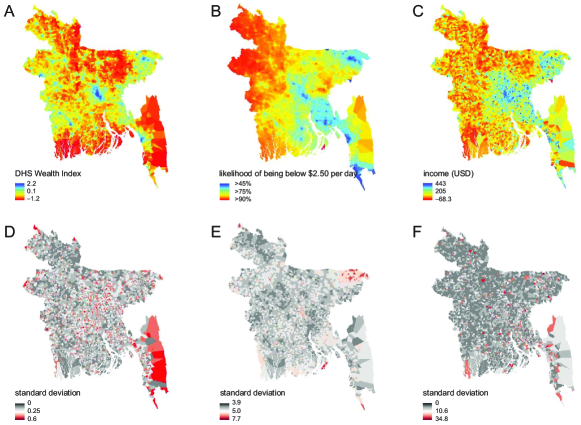

While RS-only and CDRs-only models perform comparably in mapping poverty, Steele et al. [68] demonstrated that their combination can produce better predictive maps of socioeconomic status in Bangladesh. Specifically, they employed hierarchical Bayesian geostatistical models (BGMs) [69] that combine RS data, CDRs and traditional survey-based data to map three commonly used indicators of living standards, namely, Wealth Index (WI), Progress out of Poverty Index (PPI) and reported household income (Income). The BGMs are built on the scale of the Voronoi polygons, which approximate the mobile tower coverage areas using Voronoi tessellation [70]. They applied BGMs to predict the poverty metrics (WI, PPI and Income) for each Voronoi polygon as a posterior distribution with completely modeled uncertainty around estimates. Then, they generated prediction maps with associated uncertainty using the posterior mean and standard deviation (see Figure 5). Their method using combined CDRs CRS data exhibits a better predictive power (highest ) for the observed data than RS-only method () and CDRs-only method (). Similarly, Njuguna and McSharry [71] built a linear model to predict MPI based on the combination of CDRs, RS and LandScan datasets in Rwanda. They extracted four meaningful features that proxy socioeconomic status from the combine dataset, specifically, nighttime lights (NTLs) per capita from RS data, mobile ownership per capita from CDRs, average daily call volume per phone from CDRs, and population density from LandScan data. They proposed a simple linear regression model using the four features to predict MPI, as

| (4) |

where stands for the value of the corresponding feature. This model can explain 76% of the variance in MPI across 295 sectors in Rwanda. These results suggest that combination of multiple data sources can yield socioeconomic estimates at a high spatial resolution.

Exhaust from digital and physical commodities can provide rich information about socioeconomic status, and thus proxy indicators can be built by leveraging these novel data sources. For example, United Nation Global Pulse launched the project entitled “Building Proxy Indicators of National Wellbeing with Postal Data” [72], which investigates the potential of using the international postal flow network to approximate indicators of countries’ socioeconomic profiles. The project collected 14 million electronic postal records of 187 countries from 2010 to 2014. The dataset covers 680,000 post offices and forms the world’s largest postal network. Results show that indicators gathered from the postal network correlate well with fourteen widely used socioeconomic indicators such as GDP and Human Development Index (HDI). This work demonstrates that structural features of world flow networks can be used to produce proxy indicators of socioeconomic status.

Meanwhile, Hristova et al. [73] examined how digital traces and the network structure can reveal the socioeconomic profiles of different countries. They measured the position of each country in six different global networks (trade, postal, migration, international flights, IP and digital communications) and built proxies for a number of socioeconomic indicators including GDP per capita and HDI ranking and other twelve indicators. In particular, they applied the multilayer network model [74] to characterize the strength of these international ties, where six networks representing six types of international ties are considered as six layers of the multiplex network with each pair of nodes possibly having one relationship in each layer. Formally, the multiplex network [75] is denoted as

| (5) |

where each layer contains a set of edges and a set of nodes , and is the total number of networks. The multiplex neighborhood of a node is defined as the union of its neighborhoods on each layer:

| (6) |

where is the neighbourhood of node in layer . The global multiplex degree of node is defined as , and the weighted global multiplex degree is defined as

| (7) |

where is the total number of nodes. The network metrics have predictability to several socioeconomic indicators. The global multiplex degree is the best-performing degree in terms of consistently high performance across all fourteen indicators. In particular, the global degree exhibits the most highly negative correlation with the HDI ranking (Spearman’s rank correlation ). These results show that a nation’s socioeconomic proxy indicators can be constructed based on different global networks after combining the data from multiple sources.

2.2 Economic complexity and fitness of nations

Understanding how economies develop to prosperity is a long-standing challenge in economics. In traditional literature, as an aggregated monetary indicator, GDP has been widely used to identify the stages of economic development of countries. Recently, a novel index named economic complexity has been proposed as the root in the gaps of economic development. In particular, the new steam of literature introduce a variety of non-monetary metrics based on international trade networks to quantitatively assess a country’s potential for future economic growth. In this section, we will briefly introduce recent works on economic complexity index, fitness index, and some variant indices, as well as their applications to predict world economic development.

2.2.1 Product space and economic complexity

Economic development has been traditionally measured by aggregated variables like GDP, however, such averages can not capture the increasing diversity that is associated with economic development. An insight raised recently is that the mix and diversity of products and industries are highly suggestive to economic growth. Hausmann et al. [76] introduced the level of sophistication–the income level of a country’s exports–to the characterization of products and demonstrated that it can predict subsequent economic growth. Specifically, they first construct an index called PRODY, which represents the income level associated with a product. The PRODY index for product is given by

| (8) |

where is the total export of product by county , is the total export of country , and is the GDP per capita of country . Indeed, the PRODY index is a weighted average of the per capita GDPs of countries exporting a given product. Then, they construct the PRODY index, which represents the income level associated with a country’s export basket. The PRODY index for country is given by

| (9) |

Indeed, the PRODY index is a weighted average of the PRODY for the country, where the weights are the shares of the products in the total exports of the country. After analyzing the international trade data covering over 5,000 products and 124 countries, Hausmann et al. [76] found that countries with high initial sophistication of export baskets (EXPY) tend to perform better in subsequent economic growth. These results suggest that countries have economically meaningful differences in the specialization patterns of exporting baskets, and countries export more sophistication products are likely to grow more rapidly.

Later, Hidalgo et al. [77] illuminated this viewpoint through analyzing the network of relatedness between products, named product space, which is built based on the international trade data. Products are considered to have high relatedness if they have a high probability to be co-exported by many countries in the international trade. Formally, the proximity between products and is defined as

| (10) |

where is the conditional probability that country is a significant exporter of product given that it has been a significant exporter of product . The significant exporter of a product is identified by the revealed comparative advantage (RCA) [78]. The RCA value is defined as the share of product in the export basket of country to the share of product in the world trade. Specifically, the of country in product is defined by

| (11) |

where is the total export of product by country . If , country is a significant exporter of product . Larger proximity means higher relatedness between products and . Based on the proximity measure, the product space is generated and visualized (see Figure 6). It can be seen that the product space has a core-periphery structure with more-sophisticated products locating in the core and less-sophisticated products occupying the periphery (see Ref. [79, 80] for the definition of core-periphery structure in networks). Richer and poorer countries tend to export products that are located in the core and periphery, respectively. More significantly, countries move through the “product space” by developing products that are related to what they currently have. These results provide explanations to the fact that economic development a path-dependent process [81] and not all countries face the same opportunities in development.

In particular, it is hard for poor countries to move toward new products with high sophistication since these countries tend to occupy the peripheries of the product space with current exports of less-sophisticated products. Using the concept of product space to explore the international trade data, Abdon and Felipe [82] studied the opportunity for economic growth and structural transformation of Sub-Saharan Africa (SSA) countries. They found that the majority of SSA countries are trapped in the export of products that are unsophisticated, standard and poorly connected in the product space. This makes the structural transformation of a region being particularly difficult, because the nearby products are in the periphery and the current capabilities are not enough to jump into more sophisticated products. To solve this problem, governments must implement policies and provide public inputs that can give incentives for the private sector to invest in the more sophisticated activities.

Further, Hidalgo and Hausmann [83] quantified the economic complexity of nations based on international trade data and demonstrated its central role in a country’s economic development. In particular, they proposed the Method of Reflections (MR) to characterize the structure of “country-product” bipartite network and showed that the variables produced by the MR method can be interpreted as indicators of economic complexity. Formally, the bipartite network can be represented by an adjacency matrix , where if country is a significant exporter () of product , and if otherwise. The economic complexity index (ECI) of country is then defined as

| (12) |

where is the number of countries, and are functions of mean and stand deviation that operate on the elements of vector , and is the eigenvector associated with the 2nd largest eigenvalue of the matrix

| (13) |

Indeed, the matrix is defined through a set of linear iterative equations by connecting countries who have similar products, weighted by the inverse of the ubiquity of product () and normalized by the diversity of country (). Formally, putting the equation (the average ubiquity of product) into the equation (the average diversity of country) can generate the equation

| (14) |

where is the number of iteration. The economic complexity of country is given by , where is country ’s complexity in the previous iteration step. For more mathematical details, readers are encouraged to read the book on economic complexity wrote by Hausmann et al. [84]. Empirical results showed that countries’ ECIs are highly correlated with their income levels are predictive of their future growth. Indeed, economic development is a process that requires acquiring more complex sets of capabilities to move towards new activities associated with higher levels of productivity. Therefore, efforts should focus on generating the conditions that allow complexity to emerge, so that sustained growth and prosperity in economic development will appear.

From a network perspective, uncovering the characteristics of the “country-product” bipartite network is very important for understanding economic development. Hausmann and Hidalgo [85] proposed an analytic framework to account for the nature of the bipartite network structure. They found that countries differ in their product diversification and in the ubiquity of their exported products. Countries with more capabilities are able to produce less ubiquitous products. This logic explains the negative relationship between the diversification of countries and the average ubiquity of the products that they produce. Later, Bustos et al. [86] studied the presence and absence of industries in international and domestic economies. They found that “country-product” bipartite networks are significantly nested [87], and the dynamics of nestedness can predict the evolution of industrial ecosystems (see Refs. [88, 89] for details on nestedness in networks). Moreover, the nestedness tends to be constant over time, making the pattern of industrial appearances predictable. Felipe et al. [90] applied MR to rank 5107 products and 124 countries in the international trade. They found that countries’ export shares of products of different complexity vary with the level of their income per capita. Specifically, export shares of the most complex products increase with income, while the export share of the less complex products decrease with income. Moreover, MR can distinguish products that require more complex or simpler capabilities, and the complexity rankings of countries exhibit a high correlation with their technological capabilities.

2.2.2 Fitness index and economic dynamics

The Fitness index employs a statistical approach to define a new set of metrics to quantify the fitness of countries and the complexity of products through coupled nonlinear maps. Based on the analysis of the “country-product” bipartite networks of international trade, Caldarelli et al. [91] proposed a new method based on biased Markov chain process to rank countries in a more conceptually consistent way, where a two-parameter bias is used to account for the bipartite network structure. Formally, the Markov process is given by

| (15) |

where is the fitness of country , is the complexity of product , is the interaction step, and is the Markov transition matrix given by

| (16) |

where and are free parameters. In a vectorial formalism, country ’s fitness is , where the ergodic stochastic matrix is defined as . The complexity of product is , where the ergodic stochastic matrix is (see Ref. [91] for mathematical details). After analyzing these equations, Caldarelli et al. [91] revealed a strongly nonlinear entanglement between the diversification of a country and the ubiquity of its products in determining the competitiveness of countries and the complexity of products. In particular, having more-sophisticated products in the portfolio contributes more to the competitiveness of a country than having many less-sophisticated products.

Moving forward, Tacchella et al. [92] developed a so-called Fitness-Complexity Method (FCM) using coupled nonlinear maps, whose fixed point can define new metrics for the fitness of countries and the complexity of products. In their iterative algorithm, fitness of countries and complexity of products interact in a nonlinear and self-consistent mathematical way. Specifically, the fitness of a country is proportional to the number of its products weighted by their complexity. In turn, the complexity of a product is inversely proportional to the number of countries exporting it weighted by the inverse of their fitness (similar methods have also been proposed for search engine [93] and online reputation systems [94]). Formally, the coupling between the fitness of country and the complexity of product is given by the nonlinear iterative scheme:

| (17) |

where and are respectively normalized in each step by and , given the initial condition and . The nonlinear iteration goes until the stationary state is reached (see Ref. [95] for the convergence property), in which reflects the fitness of countries and reflects the complexity of products. Indeed, FCM is based on the idea that (i) a diversified country gives limited information on the complexity of products, and (ii) a poorly diversified country tends to have a specific product of a low level sophistication. Therefore, a nonlinear iteration is needed to bound the complexity of industries by the fitness of the less competitive provinces having them. After applied to the international trade data, FCM performs better than MR in capturing the bipartite network structure, in defining an effective non-monetary matric for economic complexity, and in quantifying a country’s potential for growth.

Meanwhile, Cristelli et al. [96] argued that nonlinear dependence is the fundamental element and the nonlinear approach is consistent with the structure of the unweighted “country-product” bipartite network. Moreover, they analyzed the case of including weights in the matrix through , where is the total export of product by country . After comparing MR and FCM in both economic and mathematical aspects, they found that FCM is more conceptually consistent and well-grounded from an economic point of view. Taking into account the triangular structure of the bipartite network, Tacchella et al. [97] discussed how to define suitable non-monetary metrics for both the complexity of products and the diversification of countries. In particular, they argued the conceptual flaws of MR by using three toy models and demonstrated that FCM is able to grasp the level of competitiveness of a country by defining the simplest metrics that seem to be consistent with the triangular-like pattern.

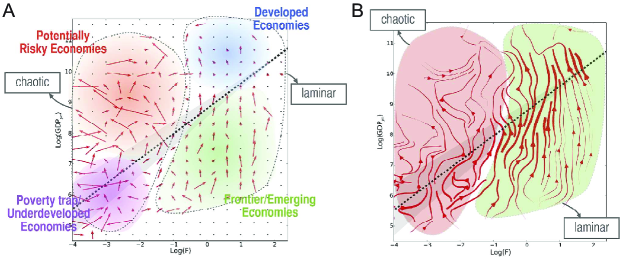

This branch of studies has provided new perspectives to cast economic prediction into the conceptual scheme of forecasting the evolution of a dynamical system, for example, weather dynamics. Cristelli et al. [98] compared the non-monetary metrics, in particular the fitness of countries, with their monetary figures, say GDPpc. They showed that FCM is able to quantify the hidden growth potential of countries. More interestingly, they demonstrated that the pattern of countries’ evolution in the Fitness-GDPpc plane is strongly heterogeneous with two regimes of very different predictability features (see Figure 7). Specifically, there is a strongly predictable area of economic development, named the laminar regime, while the predictability is low in the so-called chaotic regime. Two kinds of evolution patterns can be observed in the laminar regime, where emerging economies develop rapidly and developed economies enjoy stable growth. In the chaotic regime, the dynamics of countries are highly diverse and unstable, leading to the difficulty in predicting the economic development. In this case, tools like regressions are no more appropriate in developing a predictive scheme.

To address this issue, Cristelli et al. [98] defined a selective predictability scheme to assess future evolution of countries by resembling the method of analogues [99], which was developed to predict the evolution of a dynamical system given the knowledge of the past but without the laws of motion. The framework provides insights to the regime-dependent economic predictability and opens new paths to economic forecasting. Recently, Tacchella et al. [100] applied this scheme to predict the five-year GDP growth. In the Fitness-GDPpc plane, they repeatedly sampled analogues with a Gaussian kernel (centred on the present state of a country) and performed a bootstrap of previously observed evolution (weighted by the distance of the analogues starting points), resulting in the global distribution of possible outcomes. They further refined the forecast by taking into account the strong self-correlation of GDP growth. Specifically, the forecast based on the global distribution is combined with the forecast that assumes a past five-year growth by a certain weighted averaging. This scheme outperforms the International Monetary Fund (IMF) five-year GDPpc forecast [101] by more than 25% in accuracy. Moreover, the method’s forecasting errors are predictable and not correlated with IMF errors, showing its complementarity to traditional approaches.

2.2.3 Variant indices and development analysis

Many recent studies have highlighted the importance of complexity and capabilities in economic development. The pioneering work by Hidalgo and Hausmann [83] introduced MR to extract the competitiveness of countries and the complexity of product from the “country-product” bipartite networks with the assumption that there are linear interactions between the two metrics. Tacchella et al. [92, 97] proposed FCM and emphasized the necessary of nonlinear coupling between the fitness of countries and the complexity of products. Mariani et al. [102] quantitatively compared the ability of MR and FCM in ranking countries and products by their importance in networks. Based on the international trade data of 132 countries and 723 products, they found that FCM outperforms MR in ranking both products and countries. In particular, FCM captures the nestedness of the bipartite network and ranks nodes better by their importance.

Mariani et al. [102] proposed a modified FCM (MFCM for short), in which the nonlinear coupling is governed by a tunable parameter. By adjusting the parameter, we can find a better tradeoff between the favor on countries with diversified exports and the penalization on products with a large number of exporting countries. Formally, MFCM is defined by the equations

| (18) |

where is the tunable parameter. When , MFCM degenerates to FCM. The correlation between the product complexity and the product ubiquity decreases with the increase of . When , the ranking of product complexity by MFCM is perfectly correlated with that by FCM, however the ranking is volatile (very sensitive to noise). For this reason, MFCM with larger can only be applied to high-quality data instead of noisy data. When input data is reliable, MFCM is able to produce better rankings of countries and products.

Wu et al. [103] showed some rigorous mathematical properties of the fitness-complexity metric for nested networks. They introduced a simpler variant of FCM, named Minimal Extremal Metric (MEM), where the complexity of a product is equal to the fitness of the least-fit country that exports it. Formally, MEM defines the fitness of country and the complexity of product by

| (19) |

Obviously, in MEM, only the fitness of the least-fit country contributes to the product complexity . In the limit , MEM is a special case of MFCM. Results based on the analysis of the international trade data show that MEM can reproduce the nested structure of the “country-product” bipartite network but it is highly sensitive to noise in data.

Morrison et al. [104] provided both theoretical and numerical evidence for the intrinsic instability in the nonlinear map employed by FCM. Using the preferential attachment model (see Refs. [105, 106]) and two real-world datasets (trade and patent), they showed that FCM is unstable to even small perturbations in the network, while MR does not suffer from this problem. That is because the nonlinear iterative approach in FCM amplifies the effects of countries with low fitness on the complexity of a product and highlights economies producing exclusive niche products, which are produced by a very few countries but not necessarily the most sophisticated. Adding a product exported by only a single country may lead to a global reorganization of the fitness landscape. Therefore, FCM has a serious problem when applied to dynamic economical systems with new products entering markets.

With new methodologies, attentions have been paid to better understand economic development, innovation and industrialization. Based on the international trade data, Zaccaria et al. [107] built a hierarchically directed network by measuring the taxonomy of products through computing the excess frequency of co-occurrence of two products comparing to the random binomial case. Formally, the taxonomy between products and is defined by projecting the “country-product” matrix to a unipartite space as (similar to [108])

| (20) |

The taxonomy network presents the temporal connections between products and suggests the most relevant products for the development of countries. Indeed, the structure of the taxonomy network is suggestive to the potential growth of countries. Later, Saracco et al. [109] proposed a dynamical network approach to model the process of country’s innovation and competition on the evolution of the export baskets. Their dynamical model can accurately reproduce the main features observed in the evolution of the “country-product” bipartite network. Moreover, their model suggests that countries can follow different paths in the “product space” [77, 107] to gradually diversify their export baskets.

Focusing on the time evolution of trade volume, average complexity and competitiveness, Zaccaria et al. [110] compared the exports of different sectors in Netherlands. They found that high-tech related sectors have high average complexity but low competitiveness, while sectors heavily relying on raw materials have a low complexity but high competitiveness such as Energy and Horticulture sectors. Indeed, not only products but also services are important in explaining economic stability and predicting future growth. Stojkoski et al. [111] found that services have in general higher economic complexity than products. The sophistication and diversification of service exports can provide an additional route for economic growth in both developing and developed countries. Countries that are not able to diversify service portfolio may face diminishing growth prospects.

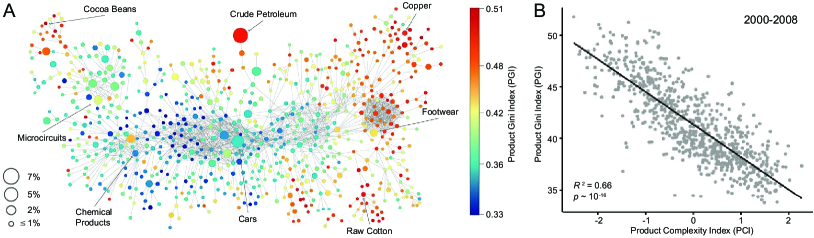

Hartmann et al. [112] found that countries exporting more complex products have lower levels of income inequality. In particular, economic complexity index (ECI) outperforms GDP in explaining income inequality. Based on the international trade data, they calculated the Product Complexity Index (PCI) using the method proposed by Hidalgo and Hausmann [83]. Further, they estimated the level of income inequality associated with products by introducing the Product Gini Index (PGI), which is a weighted average of the Gini coefficients of the countries that export a product (see Figure 8A for the PGIs of products in the product space). There is a strong and negative correlation between PCI and PGI, showing that sophisticated products tend to have low levels of inequality (see Figure 8B). Moreover, countries with high (low) level of ECI are more likely to specialize in high-PCI (low-PCI) products, suggesting that the productive structure of a country may condition its range of income inequality. Recently, Mealy et al. [113] interpreted economic complexity metrics by showing that ECI and PCI are equivalent to a spectral clustering algorithm, which divides a similarity network into two parts. Moreover, these measures are closely related to many dimensionality reduction methods such as correspondence analysis and diffusion maps. Their findings shed some new light on the empirical success of ECI and PCI in explaining specialization patterns of countries in economic growth.

Pugliese et al. [114] analyzed the role of complexity in economic development and found that economies with differentiated products face a lower barrier in the transition towards industrialization. They extended the concept of poverty trap to include the two factors of economic complexity and GPDpc (see also Ref. [98]). They defined an index of development and industrialization, named Complex Index of Relative Development (CIRD), by the equation:

| (21) |

where is the fitness of country at time , is the GDPpc of country at time , and is a tunable parameter. The use of the CIRD index allows to study development as a monodimensional process. In particular, is a threshold for countries to exit the poverty trap, and the increase of the input growth reaches its maximum at this critical point. The CIRD index facilitates our understanding of industrialization dynamics and is helpful for development analysis. Sbardella et al. [115] analyzed the relationship between wage inequality and industrialization using fitness and GDPpc. They found that movement of wage inequality along with the industrialization follows a longitudinally persistent pattern. This finding is comparable to theories proposed by Kuznets [22], who hypothesized that countries with an average level of development suffer the highest levels of wage inequality.

Along with the literature, some online platforms have been developed and launched to help understand the evolution of countries’ productive structures and economic development. For example, Simoes and Hidalgo [116] launched a data visualization site, named Observatory of Economic Complexity (OEC) (https://atlas.media.mit.edu). The OEC combines a number of international trade datasets and serves more than millions of interactive visualizations including imports and exports, origins and destinations, product space, economic complexity rankings based on MR, income inequality, and so on. Meanwhile, the GROWTHCOM Project launched a data platform (http://www.growthcom.eu), which provides visualization tools of the product network [107] and the countries’ trajectories in the fitness-GDPpc plane [98].

2.3 Spatial demography and culture evolution

High resolution and near real-time data from new sources like remote sensing (RS), mobile phone (MP) and social media (SM) are complementary to traditional costly data with a long-time delay in inferring population distributions and demographics. Moreover, these so-called socioeconomic big data, together with methods from interdisciplinary fields including statistical physics and computer sciences, have been used to predict international migration and quantify world culture evolution. In this subsection, we will briefly introduce some methods using new data sources to map world population, estimate international migration and study culture evolution.

2.3.1 World population distribution

Knowing the spatial distribution of population on earth is critical for many socioeconomic applications such as accurate environmental impact assessments, human health adaptive strategies and disease burden estimation [117]. Developed countries have substantial resources to create accurate and contemporary population datasets with high spatial resolution [118], however, relevant data are often scarce, outdated and unreliable in low-income countries due to economic constrains. In addition, acquiring census data in a timely and accurate manner is very difficult due to the rapid change of population and some administrative challenges. As a results, our knowledge of population distribution in many areas of the world remains poor thus far. Fortunately, technologies developed during the past decades have opened new ways for us to estimate and map world population distribution in a more timely manner and with a relatively lower cost.

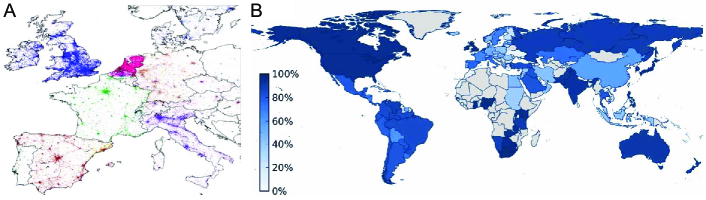

Some large-area gridded world population distribution datasets have been built based on multiple data resources. Tobler et al. [119] developed the first version of Gridded Population of the World (GPW) database by transforming population counts from census units to a grid. The Global Rural Urban Mapping Project (GRUMP) utilizes higher resolution inputs and renders outputs at a 30 arc-second resolution (approximately 1km). In addition to census data, spatial covariate datasets are also used to estimate populations. For example, the LandScan Global Population Project [37] produced the world-wide 1998 LandScan population database at a 30 arc-second resolution based on the land cover database derived from satellite imagery and urban area vector data [120]. Tatem et al. [121] produced the 100m gridded population map by combining land cover information and census data under the Malaria Atlas Project. The semi-automated population distribution mapping at unprecedented spatial resolution produces more accurate results at a spatial resolution of about 100m in East Africa.

Cheriyadat et al. [122] generated human settlement maps based on high-resolution satellite imagery. Their algorithm employed gray level co-occurrence matrices [123] to generate texture and edge patterns from satellite imagery that are useful in urban land cover classification. Liao et al. [124] presented a high-accuracy population mapping method that integrates genetic programming (GP) [125] and genetic algorithms (GA) [126] with geographic information systems (GIS). Specifically, they applied GIS to identify relevant factors (e.g., land-cover types and transport infrastructure) and use GP and GA to transform census data to population grids. Deng et al. [127] estimated small-area population by incorporating GIS, remote sensing (RS) and demographic data into a popular demographic model. They demonstrated that the derived spatial factors can significantly improve the accuracy of small-area population estimation.

Gaughan et al. [128] constructed an accurate and high-resolution population distribution dataset for Southeast Asia. They modeled population distributions for 2010 and 2015 by combining satellite-derived settlement maps, land cover information, and ancillary datasets on infrastructure. Stevens et al. [129] presented a new semi-automated dasymetric modeling approach, where RS and geospatial data are combined to model the dasymetric weights and the random forest model is used to generate a gridded prediction of population density at about 100m resolution. Patel et al. [130] presented a novel method to map multitemporal settlement and population from Landsat imagery using Google Earth Engine, which is an online environmental data monitoring platform that provides analysis capabilities on Landsat data by leveraging cloud computing services. They demonstrated that the integration of GEE-derived urban extents improves the quality of population mapping.

Spatial covariates derived from satellite imagery and land cover are typically static in nature and are not direct measures of people’s presence on earth [118]. Thanks to the rapid adoption of Internet and mobile devices in developing countries, there is a great potential of using digital records to do population mapping. For example, call detail records (CDRs) can overcome many limitations of census-based data since MPs have a high penetration rate across the world. For urban areas, Pulselli et al. [131] developed a technique to monitor population density in real time based on MP chatting, given that the intensity of activity in the area covered by an antenna is proportional to the number of MP users. Based on MP location data, Dan and He [132] proposed a dynamic distribution model to estimate urban population density using an improved K-means clustering algorithm [133]. Kang et al. [134] discussed several fundamental issues on using CDRs to estimate population distributions. After analyzing the CDRs of nearly two million MP subscribers, they found that the number of calls other than the total daily call volume serves as a good estimator of population distribution.

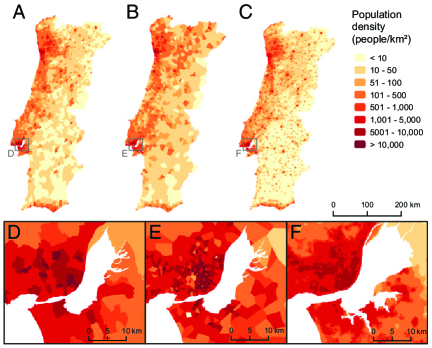

Recently, using both RS and MP data, Deville et al. [135] produced spatially and temporarily explicit estimations of population densities at national scales (see Figure 9). Based on over one billion CDRs from Portugal and France, they estimated the population density of an administrative unit using a two-step method that relies on the density of MP users, where is the Voronoi polygon [70] associated with tower . The nighttime density for unit is calculated by

| (22) |

where is the area of unit , and is the intersection area of unit and the Voronoi polygon . The density is compared with the census-derived population densities through

| (23) |

where and . By transforming Eq. (23) to , the two parameters and can be fitted by a linear regression on training data. Further, they combined the MP method with the RS method proposed by Stevens et al. [129], who used the random forest model to generate gridded predictions of population density. Formally, the population density in pixel is estimated by

| (24) |

where is the weight assigned to pixel and is the total population. Combining MP and RS data can produce population datasets with a high spatial and temporal resolution.

Douglass et al. [136] created high-resolution maps of population distribution by combing telecommunications data, satellite imagery and census data in Milan, Italy. They fitted population and call data by applying an elementary model that is similar to Eq. (23). They found that the total out-call volume has the strongest correlation (about 0.68) with the grid-level population. Further, they employed a random forest regression to predict population using features of land cover measures, call activity measures and their combinations. They found that building land cover and calls made out at 10am are the top-two predictors that are sufficient to provide accurate predictions. Lulli et al. [137] proposed a function to capture similarities between individual call profiles (ICPs). The similarity of ICPs is captured by combining the Euclidean similarity and the Jaccard similarity. Then, they built a clustering algorithm to provide clusters of individuals based on the similarity between ICPs. Using an automatic classifier to label the clusters, their method can estimate the number of residents, commuters and visitors in a given region. At the urban scale, Khodabandelou et al. [138] estimated population density by applying Eq. (22) and Eq. (23) based on the mobile network traffic metadata. Their method can estimate both static and dynamic populations across different cities.

Calling activities are powerful in mapping populations, however, it is usually not easy to obtain due to privacy concerns [139]. For example, some highly sensitive traits and attributes can be inferred from digital records of human behavior [140]. The increasingly available social media data presents alternative opportunities in estimating population distribution. Twitter has gained worldwide popularity, making the geotagged tweets show detailed depictions of human activity. Leetaru et al. [141] explored over 1.5 billion tweets posted by over 70 million users. They found a high correlation (0.79) between geotagged tweets and the NASA City Lights imagery. The most accurate feature is the self-reported user location field, exhibiting a correlation 0.72 with the geotagged baseline. Their work demonstrates the potential of geotagged tweets in world population mapping.

Very recently, volunteered geographic information (VGI) collected from the Internet (e.g., check-in data [142]) has been used to estimate population at a fine scale. Yao et al. [143] presented a framework to map population distribution at the building level by integrating national census data with two geospatial data sources. One is the points-of-interest (POIs) provided by Baidu Map Services, and the other is the real-time Tencent user densities (RTUD). They employed the random forest algorithm [144] to analyze the two geospatial datasets and downscale the street-level population distribution to the grid level. Then, they proposed an iterative gravity model that can efficiently estimates the population density in each building and study area. Their method achieves a high correlation to the official census data.

The WorldPop collection recently brings together publications describing detailed and open-access spatial demographic datasets built using transparent approaches [145]. For the Latin America and the Caribbean region, Sorichetta et al. [146] opened an archive of high-resolution gridded population datasets for 2010, 2015 and 2020 based on the most recent official population count data for 28 countries. Gaughan et al. [147] opened mainland China population maps for 1990, 2000 and 2010 after analyzing temporally-explicit census data using an ensemble prediction model. Lloyd et al. [148] described the datasets and production methodology for the 3 and 30 arc-second resolution global gridded population data. The basis of the archive contains four tiled raster datasets and other layers.

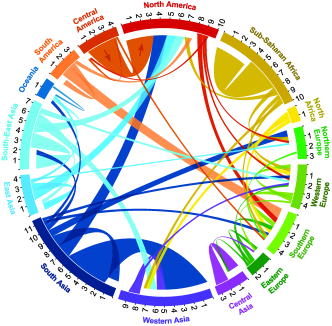

2.3.2 International migration

International migration is one of the major reasons of demographic, economic and political changes. Literature suggested some determinants of migration such as family and personal networks [149] and revealed the impact of immigrants on the host country’s economy [150]. There are some bottlenecks in studying migration such as data availability, data quality, data collection rules, and inconsistencies in measurement. For example, a person may involve multiple migrations during a given year, but most systems considered the number of migrations instead of migrants, resulting in the overestimate of the amount of immigrants. Moreover, “migration” defined by different countries may differ substantially, which results in the inconsistencies among international data. In addition, which country is reporting the data will lead to significant different patterns of migration [151]. Census and registered migration data are helpful for the estimation of international migrations. By combining census migration data and patient registration data, Raymer et al. [152] developed a log-linear model to estimate elderly migration flows in England and Wales. Their model extends the spatial interaction model (see Ref. [153] for details) by adding a third variable of interest, such as health status in migration data. Formally, the log-linear model with an offset is given by

| (25) |

where is the expected migration flow from origin to destination for level of the third variable, and are respectively related to the origin and destination’s characteristics, and is the auxiliary information on migration flows.