section[3em]2em1pc \dottedcontentssubsection[5em]2.4em1pc

Finite-time ruin probabilities under large-claim reinsurance treaties for heavy-tailed claim sizes

Abstract

We investigate the probability that an insurance portfolio gets ruined within a finite time period under the assumption that the largest claims are (partly) reinsured. We show that for regularly varying claim sizes the probability of ruin after reinsurance is also regularly varying in terms of the initial capital, and derive an explicit asymptotic expression for the latter. We establish this result by leveraging recent developments on sample/path large deviations for heavy tails. Our results allow, on the asymptotic level, for an explicit comparison between two well/known large/claim reinsurance contracts, namely LCR and ECOMOR. We finally assess the accuracy of the resulting approximations using state/of/the/art rare event simulation techniques.

1 Introduction

We consider the following ruin problem of the classical Cramér/Lundberg model in risk theory; see e.g. [4]. Let be a sequence of i.i.d. positive random variables representing successive claim sizes that arrive according to a homogeneous Poisson process , , with rate . Premiums are received continuously at a constant rate . We assume that there is also a reinsurance agreement in place, where is the reinsured amount at time . More precisely, if is the aggregate claim amount at time and is the remaining premium for the insurer after reinsurance has been purchased, then the aggregate loss minus premiums at time for the insurer is equal to . If is the initial capital, then the probability of ruin before time is defined as

| (1) |

We will restrict our attention to two forms of large claims reinsurance, namely LCR and ECOMOR. In an LCR (largest claim reinsurance) contract (see e.g. [3] for an early reference), the reinsurer agrees to cover the largest claims, where is a fixed number, while in an ECOMOR (excédent du coût moyen relatif) contract [19], the reinsurer covers the excess of the largest claims over the st largest claim; see [2] for more details on this type of reinsurance contracts.

We assume that the distribution of the claim sizes belongs to a class of distributions with a regularly varying tail, which is valid for many applications [11]. It is well known that the principle of one big jump holds in the heavy/tailed claim setting, i.e. ruin is typically caused by a single large claim. However, under the presence of large claim reinsurance contracts, ruin probabilities are typically harder to analyse because the largest claims are covered by the reinsurer and thus multiple claims may be responsible for the event of ruin.

Several papers have studied properties of large claim reinsurance contracts. For example, when claim sizes are light/tailed, the asymptotic tail behavior of the reinsured amounts is considered in [12, 13] and their joint tail behavior in [17]. For asymptotic properties of the reinsured amounts when the claim size distribution is heavy/tailed, see [1, 15]. For dependence between claim sizes and interarrival times in this context, see [16]. An interesting recent link between large claim treaties and risk measures is given in [8]. However, none of these contributions deal with the ruin probability, which is considered here.

In this paper, we suggest to leverage recent new tools developed in the context of sample/path large deviations for heavy/tailed stochastic processes for the study of ruin problems under LCR and ECOMOR treaties. Concretely, for a centered Lévy process , , with regularly varying Lévy measure , sample/path large deviations were developed in [18]. Consider the process , where , . Then, asymptotic estimates of for a large collection of sets were derived. For Lévy processes with only positive jumps that are regularly varying with index , , these results take the form

| (2) |

where and are the interior and closure of , is interpreted as the minimum number of jumps in the Lévy process that are needed to cause the event , and is a measure. We will show how the reinsurance problem fits in the above framework. For this, we resolve several technical challenges such as showing how ruin probabilities in the reinsurance setting can be written as continuous maps of the input process in a suitable Skorokhod space.

Apart from the fact that reinsurance contracts are an interesting object of study in their own right, the present application seems to be the first example for which it is possible to compute the pre/factors in the asymptotics (2) explicitly. More precisely, we show for both the LCR and ECOMOR treaty that and we provide an explicit expression for this value.

The rest of the paper is organised as follows. In Section 2, we provide some preliminary results and introduce the necessary notation. Section 3 develops the main result, i.e. the tail asymptotics for finite time ruin probabilities. For this, we are inquired to write (1) in terms of (2). This leads to the need to show continuity of certain mappings, as well as several additional technical requirements. In Section 4, we validate our asymptotic results with numerical experiments.

2 Model description and preliminaries

Following the notation and terminology used in Section 1, let denote the distribution function of the claim sizes and be their expectation. We assume that is regularly varying with index , i.e. there exists a slowly varying function such that , with . Let further denote the order statistics of .

In an LCR treaty, the reinsured amount is equal to

| (3) |

i.e. the largest claims are paid by the reinsurer. On the other hand, the reinsured amount in an ECOMOR treaty takes the form

| (4) |

That is, the ECOMOR constitutes an excess/of/loss treaty with a random retention, and the latter is the -largest claim. For more details and background on such reinsurance contracts, see [2]. In either treaty, the number of reinsured claims is equal to .

Assumption 1.

If , we set , for . This means that in case there are less than claims, the reinsurer pays all the claims in the ECOMOR treaty.

Another modeling assumption is concerned with the way the reinsurance is affecting the capital position of the insurance company under consideration.

Assumption 2.

We assume that at each time , the currently applicable reinsured amount is considered in the determination of the available surplus. In particular, this means that before the arrival of the -st claim, the random retention in the ECOMOR treaty is considered to be zero. As a consequence in the ECOMOR treaty, the arrival of a new claim can lead to a modification of of either sign, as the excess over the -st claim may also decrease.

Note also that the setup we study here is that the duration of the reinsurance contract is , and the implied premium for the reinsurance contract over the period is uniformly spread over this time interval. We will study the asymptotic behavior of the finite time ruin probabilities (1) utilizing (2). Therefore, we formulate in the next section the large deviation problem that arises in our reinsurance context.

2.1 Large deviations in reinsurance

In [18], the large deviations results (2) were derived in the Skorokhod topology. Correspondingly, we let be a Skorokhod space, i.e. a space of real/valued càdlàg (right continuous with left limits) functions on , equipped with the -metric defined by

| (5) |

where denotes the set of all strictly increasing continuous bijections from to itself, denotes the identity mapping, and denotes the uniform (sup) norm on . Thus, and in (2) are a measurable set and a measure on , respectively. Furthermore, if is a continuous functional on and is a Borel set such that , where stands for the inverse of , it holds that

| (6) |

The above relation portrays how it is possible to use the result (2) to study continuous functionals of . To connect this to our ruin problem, we define as the centred and scaled process

| (7) |

Moreover, we assume that the capital increases linearly in , i.e. there exists an such that . We now formulate the large deviations problem to estimate the probabilities

| (8) |

where . As a next step, we must identify a continuous functional such that

| (9) |

so that we can write

| (10) |

However, it is not immediately obvious from Equation 9 what the functional looks like because is not expressed in terms of . We focus first on the LCR treaty and observe that

i.e. can be expressed as the sum of the biggest jumps of the process . For every and , we define

| (11) |

as the supremum of the sum of the largest jumps of the function . Naturally, . Consequently, the functional we are looking for is a mapping defined for every as

| (12) |

Moreover, we denote the pre/image of under as where

| (13) |

By comparing Equations 3 and 4, we observe that the relation between the reinsured amounts of the two treaties is

Thus, in the ECOMOR treaty, the functional in (10) is the mapping defined for every as

| (14) |

while the pre/image of under , i.e. , is defined as

| (15) |

2.2 Preliminaries on the Skorokhod topology and notation

Consider the complete metric space . The functional defined in (11) will play a significant role in the forthcoming analysis. Thus, it is important to confirm that it is well/defined. For this reason, let be the set of discontinuities of , i.e.

| (16) |

and let be the set of discontinuities of magnitude at least , i.e.

| (17) |

The following result is standard.

Lemma 2.1 (Theorem 12.2.1 & Corollary 12.2.1 of [20]).

For any and , is a finite subset of . In particular, is either finite or countably infinite.

Consequently, the supremum in Equation 11 is attained because only finitely many jumps can exceed a given positive number. As a result, is well defined.

Some important subspaces of for our analysis are those restricted to step functions. We let be the set of all non/decreasing step functions vanishing at the origin. Furthermore, is the subspace of consisting of non/decreasing step functions, vanishing at the origin, with exactly steps, and similarly, consists of non/decreasing step functions, vanishing at the origin, with at most steps. Finally, if denotes the number of discontinuities of , we can then formally define the integer/valued set function appearing in Equation 2 by:

| (18) |

which we call the rate function. Observe that every is determined by the pair of jump sizes and jump times , i.e. , where is the indicator function on the set . For and , we define the sets

| (19) | ||||

| and | ||||

| (20) | ||||

where the ’s are not following the ordering of the ’s, i.e. . Thus, we can formally define the mapping by .

Furthermore, let (i.e. the pure power decay part of the regularly varying claim sizes), and let denote the restriction to of the /fold product measure of . We define for each the measure concentrated on as

| (21) |

where the random variables , , are i.i.d. uniform on .

Finally, we say that a set is bounded away from another set if . Additionally, we let for any .

3 Main result

Note that the parameter introduced in Section 2.1 can be either positive or negative. However, for , the rare event probability in Equation 10 converges to one by the functional law of large numbers. For this reason, we focus only on the case . Letting be the hypergeometric function, with denoting the Pochhammer symbol, we have the following theorem.

Theorem 3.1.

For , , and , it holds that

| (22) |

where

The proof of Theorem 3.1 is based on sample/path large/deviations results developed in [18]. Specifically, Theorems 3.1–3.2 in [18] provide the conditions under which the result (2) holds, and in addition the and are equal. Thus, to achieve our goal, we must verify that these conditions are satisfied for and (LCR) or (ECOMOR) defined in Equations 13 and 15, respectively. However, their verification is rather involved. Hence, to make the proof of Theorem 3.1 more accessible, we split it in various steps after the aforementioned conditions and we provide additional explanations for each step.

Note that all of the forthcoming results are similar in the two treaties with possible deviations in small details. Therefore, we will first prove them for the LCR treaty and then show briefly how they can be extended to the ECOMOR treaty.

3.1 Proof of Theorem 3.1

The first step is to show that both mappings from Equations 12 and 14, respectively, are Lipschitz continuous. Due to their continuity, Equation 10 will hold and, consequently, we will be able to write and . For this, we need the following intermediate result.

Lemma 3.2.

For every , , and , it holds that

| (23) |

Proof.

By the definition of , there exists with for all , such that

| (24) |

In addition, we have that

| (25) |

Subtracting now Equations 24 and 25, we obtain

Following similar arguments, we can also show that , which completes the proof. ∎

We are now ready to establish the desired continuity.

Lemma 3.3 (Lipschitz continuity of the mapping).

The mappings defined by Equations 12 and 14, respectively, are Lipschitz continuous w.r.t. . More precisely, there exist and such that and , for all .

Proof.

W.l.o.g. we assume that , otherwise we switch the roles of and . For every , there exists such that

| (26) |

On the other hand, by the definition of , there exists so that

| (27) |

Furthermore, using the fact that is a homeomorphism on , we obtain

| (28) |

Subtracting (28) from (26) yields

where we have also used (27) and by applying Lemma 3.2 with and . Letting , we conclude that , i.e. is Lipschitz continuous. The Lipschitz continuity for the mapping can be shown in an analogous manner. More precisely, for every , there exists such that

| (29) |

For a homeomorphism on satisfying Equation 27, we have

| (30) |

We assume now w.l.o.g. that and we subtract (30) from (29) to attain

where we have also used (27) and twice Lemma 3.2 with and . Letting , the result is immediate. ∎

As a next step, we calculate the rate functions and that appear in Equation 2 and are formally defined in (18). We set for simplicity and .

Lemma 3.4 (Evaluation of the rate function).

The rate function defined by Equation 18 is equal to in both treaties, i.e.

Proof.

We need to show first that cannot take any value smaller than or equal to . Let us assume on the contrary that such that . This means that , with and all distinct. By taking into account Assumptions 1 and 2, we calculate

which states that because . As a result, , .

Let us assume now that such that , i.e. , with and all distinct. To calculate , observe first that

| (31) |

because all the claims are “absorbed” according to Assumption 2 before the arrival of the ()st claim, which happens at time . Thus, we can write

since remains fixed at the value from onward, while decreases or increases depending on the value of . Due to the fact that , we get

i.e. but contains all step functions with steps such that the ()st largest step satisfies: . Thus, .

The proof for in the ECOMOR treaty is similar. More precisely, it can easily be shown that with . Consequently, , . Let us assume next that such that , i.e. , with and all distinct. It holds that

| (32) |

due to Assumption 1. By combining now Equations 31 and 32, we calculate

Since , we get , i.e. but contains all step functions with steps such that the ()st largest step satisfies: . Thus, , and the proof is complete. ∎

Remark 3.5.

The above lemma does not only give the value of the rate function, but it also provides the form of the minimal that belongs to the sets and , i.e. all step functions with steps such that their ()st greatest step is greater than or equal to the value in the LCR treaty and the value in the ECOMOR treaty.

An essential condition of Theorem 3.2 in [18] is that the sets and are bounded away from and , respectively. Verifying this condition allows us then to derive the result (2) for both treaties. We can directly use the value of the rate function in the following result due to Lemma 3.4.

Lemma 3.6 (Bounded away property).

The sets and are bounded away from for some .

Proof.

To simplify the notation in the proof, we write instead of and instead of , while the notation , follows naturally.

We start by showing that is bounded away from for some . Thanks to Lemma 3.2, we have that , where . Hence, it suffices to show that is bounded away from . Let . Since , we can write with , for which it holds that according to the proof of Lemma 3.4. Furthermore, . Combining the two inequalities, we obtain that , for . In other words, for , with jump sizes bounded from below by , which implies that is bounded away from .

In a similar manner, it suffices to show that is bounded away from , where . Let . Since , we can write with , for which it holds that . Furthermore, . Combining the two inequalities, we obtain that , for . In other words, the jump sizes of are bounded from below by , which implies that is bounded away from for , and the proof is complete. ∎

Let := and := . According to Section 3.1 in [18], the and in Equation 2 yield the same result when

However, the above equality holds when the set is -continuous, i.e. , where the boundary of a set is the closure of without its interior. We prove in the next lemma that the sets and are both -continuous.

Lemma 3.7 (Equality of the limits).

The sets and are -continuous, i.e. .

Proof.

To simplify the notation in the proof, we write again instead of and instead of , while the notation , , , follows naturally.

We start by showing the -continuity of . In compliance with the notation introduced in Section 2.2, we consider the function such that

Obviously, the set has zero Lebesgue measure. Combining this with and being a continuous function, we conclude that , i.e. is -continuous. To prove the -continuity of , it suffices to observe that the set has zero Lebesgue measure, where

which follows by the same reasoning. ∎

We calculate now the pre/constants and .

Lemma 3.8 (Calculation of the pre-constant).

The constants and are given by

Proof.

Recall that := and := . To calculate these constants, we use the definition of the measure in Equation 21. We start with . It is known that for , the distribution of the r.v. is given by the formula . Furthermore, by using that with , we calculate recursively the following multiple integrals for and positive ’s

Consequently, in case , we obtain by virtue of Remark 3.5

Analogously, we find

In case , the coefficients simplify to

∎

Remark 3.9.

When , the coefficients and can be equivalently expressed in terms of finite sums involving the Gamma function. More precisely, by applying times integration by parts, we calculate for that

where is again the Pochhammer symbol. Thus,

Remark 3.10.

4 Numerical implementations

Our primary goal in this section is to verify our asymptotic approximations in Theorem 3.1 via numerical illustration. For this purpose, we employ an importance sampling scheme that was developed in [9] and it is proved to be strongly efficient in the current setting. We provide a short description of this scheme in Appendix A.

We use a shifted Pareto distribution for the claim sizes, i.e. , , and . In addition, we calculate the net premiums and of the insurer after purchasing an LCR or ECOMOR reinsurance for a premium and , respectively.

We assume here that the reinsurance premiums are determined according to an expected value principle, see e.g. [2]. Hence, we need to determine . As the Pareto claims arrive according to a Poisson process with rate , we follow [7] to obtain

where is the lower incomplete gamma function. Thus, if are the relative safety loadings imposed by the insurer and reinsurer, respectively, we calculate the annual retained premium over a period of years via the formula . Correspondingly,

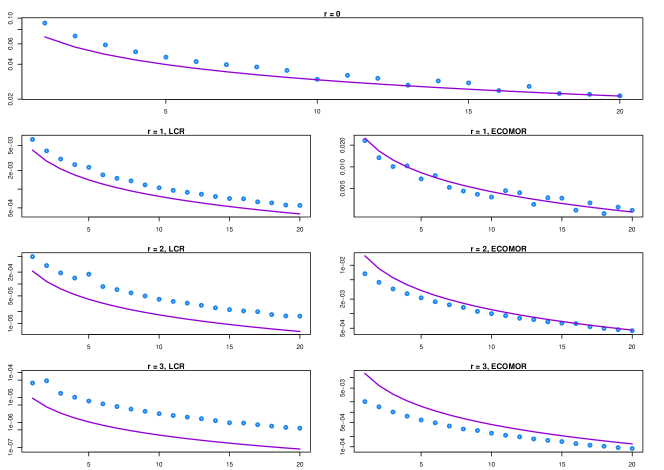

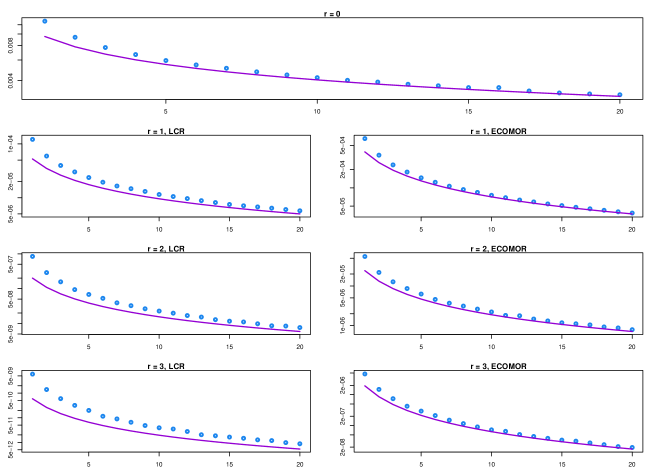

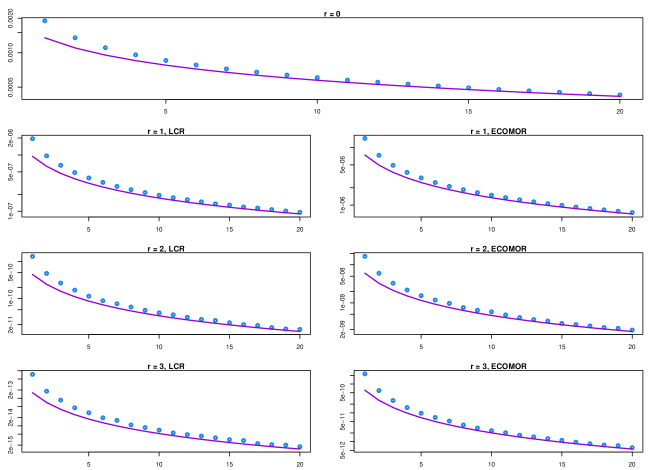

We fix now , , , , (safety loadings for reinsurance are typically larger than for primary insurance, see [2]) to obtain the following figures:

0 0 0 24 24 4 4 1 4.5309 3.0539 18.1098 20.0299 -1.8902 0.0298 2 6.0078 4.0719 16.1897 18.7065 -3.8102 -1.2935 3 6.9758 4.7505 14.9314 17.8242 -5.0686 -2.1757

Finally, we choose the values of such that the asymptotic approximations for LCR and ECOMOR are simultaneously defined. In other words, it should hold that , where , . It is clear from Table 1 that . Therefore, both approximations are simultaneously valid for .

The results under both LCR and ECOMOR treaties for different combinations of and are presented in Figures 1, 2 and 3. We plot the simulation estimates (circles) together with the large deviation approximation (line) of the rare event probabilities as a function of . Note that the results for can be considered as a sanity check for our simulation study.

We observe that the large deviation results become accurate as grows, in line with Theorem 3.1. It is quite remarkable that in most cases the resulting approximation is already excellent for . This corresponds to a time horizon of 20 years for the present insurance application. For fixed , the quality of the asymptotic approximation improves as increases. Finally, we recognize that LCR always leads to lower ruin probabilities than ECOMOR, which is intuitively expected. However, the explicit expression given in Theorem 3.1, allows for the first time to quantitatively assess the effects of the model parameters on the resulting ruin probabilities.

Appendix A Appendix: Short description of the simulation technique

Our simulation estimator is based on an importance sampling strategy; see e.g. Chapter V of [5]. To be precise, for , we define the auxiliary set

where is given in (17). We propose an importance distribution that is determined by

where and . Note that is the conditional distribution given the event has at least discontinuities of magnitude . The proposed importance distribution has the following interpretation. We flip a coin at the beginning of each simulation. We generate with probability the sample path of under the original measure and with probability , we sample under the measure . To compensate for the bias introduced by the importance distribution, a likelihood ratio – that is the Radon/Nikodym derivative between and – must be included in the estimator. In our case, the estimator for is then given by

The output analysis is performed similarly to the Monte Carlo method, i.e. we generate i.i.d. replicates of from and we estimate as the arithmentic mean of the replicates. From Theorem 1 in [9], there exists such that the simulation estimator has a bounded relative error. Hence, the number of simulation runs required to achieve a given accuracy is bounded as goes to infinity. For more details of the estimator, we refer the readers to [9].

Acknowledgements

H.A. and E.V. acknowledge financial support from the Swiss National Science Foundation Project 200021_168993. B.C. and B.Z. are supported by NWO VICI grant # 639.033.413 of the Dutch Science Foundation.

References

- [1] H. Albrecher, C. Robert, and J. Teugels. Joint asymptotic distributions of smallest and largest insurance claims. Risks, 2(3):289–314, 2014.

- [2] H. Albrecher, J. L. Teugels, and J. Beirlant. Reinsurance: Actuarial and Statistical Aspects. John Wiley & Sons, 2017.

- [3] H. Ammeter. The rating of “Largest Claim” reinsurance covers. Quarterly letter from the Algemeene Reinsurance Companies Jubilee, (2):5–17, 1964.

- [4] S. Asmussen and H. Albrecher. Ruin Probabilities. Advanced Series on Statistical Science & Applied Probability, 14. World Scientific, Second edition, 2010.

- [5] S. Asmussen and P. Glynn. Stochastic Simulation: Algorithms and Analysis, volume 57 of Stochastic Modelling and Applied Probability. Springer-Verlag New York, 2007.

- [6] S. Asmussen and C. Klüppelberg. Large deviations results for subexponential tails, with applications to insurance risk. Stochastic processes and their applications, 64(1):103–125, 1996.

- [7] B. Berliner. Correlations between excess of loss reinsurance covers and reinsurance of the largest claims. ASTIN Bulletin: The Journal of the IAA, 6(3):260–275, 1972.

- [8] A. Castaño-Martìnez, G. Pigueiras, and M. Sordo. On a family of risk measures based on largest claims. Insurance: Mathematics and Economics, 2019.

- [9] B. Chen, J. Blanchet, C.-H. Rhee, and B. Zwart. Efficient rare-event simulation for multiple jump events in regularly varying random walks and compound poisson processes. arXiv:1706.03981v1.

- [10] P. Embrechts, C. M. Goldie, and N. Veraverbeke. Subexponentiality and infinite divisibility. Probability Theory and Related Fields, 49(3):335–347, 1979.

- [11] P. Embrechts, C. Klüppelberg, and T. Mikosch. Modelling Extremal Events: for Insurance and Finance, volume 33 of Applications of Mathematics. Springer-Verlag, 1997.

- [12] E. Hashorva and J. Li. Ecomor and lcr reinsurance with gamma-like claims. Insurance: Mathematics and Economics, 53(1):206–215, 2013.

- [13] J. Jiang and Q. Tang. Reinsurance under the lcr and ecomor treaties with emphasis on light-tailed claims. Insurance: Mathematics and Economics, 43(3):431–436, 2008.

- [14] A. E. Kyprianou. Introductory Lectures on Fluctuations of Lévy Processes with Applications. Universitext. Springer-Verlag, Berlin, 2006.

- [15] S. A. Ladoucette and J. L. Teugels. Reinsurance of large claims. Journal of Computational and Applied Mathematics, 186(1):163–190, 2006.

- [16] J. Li. Asymptotics for large claims reinsurance in a time-dependent renewal risk model. Scandinavian Actuarial Journal, 2015(2):172–183, 2015.

- [17] L. Peng. Joint tail of ecomor and lcr reinsurance treaties. Insurance: Mathematics and Economics, 58:116–120, 2014.

- [18] C.-H. Rhee, J. Blanchet, and B. Zwart. Sample path large deviations for lévy processes and random walks with regularly varying increments. arXiv: 1606.02795v3.

- [19] A. Thépaut. Une nouvelle forme de réassurance: Le traité d’excédent du coût moyen relatif (ecomor). Bulletin Trimestriel de l’Institut des Actuaires Français, (49):273–343, 1950.

- [20] W. Whitt. Stochastic-Process Limits: An introduction to stochastic-process limits and their application to queues. Springer Series in Operations Research. Springer-Verlag, 2002.