2 Underlying Dynamics and Problem Setting

Let be an ordinary two-dimensional Brownian motion under the measure and assume that the underlying processes follow under the measure the stochastic dynamics characterized by the stochastic differential equations

|

|

|

|

(2.1) |

|

|

|

|

(2.2) |

where and are known constants.

As usually in models subject to Knightian uncertainty, let the degree of ambiguity be given and denote by the set of all probability measures, that are equivalent to with density process of the form

|

|

|

for a progressively measurable process with for all and . Under the measure defined by the likelihood ratio

|

|

|

we naturally have that

|

|

|

|

|

|

|

|

is an ordinary 2-dimensional -Brownian motion. Thus, we notice that under a measure the dynamics of the underlying processes read as

|

|

|

|

(2.3) |

|

|

|

|

(2.4) |

where denotes a two-dimensional -Brownian motion.

Given the underlying processes and the class of equivalent measures generated by the density process , we now plan to investigate the following optimal stopping problem

|

|

|

(2.5) |

where is a known non-negative and measurable function which is assumed to be positively homogeneous of degree one in the following unless otherwise stated. For the sake of comparison, denote the value of the optimal timing policy in the absence of ambiguity by (cf. Alvarez E. and Virtanen, (2005) and Christensen and Irle, (2011))

|

|

|

(2.6) |

Before stating our main results on the optimal timing policy and its value we first establish the following result characterizing the impact of ambiguity on the optimal stopping strategy and its value in a general setting.

Lemma 2.1.

Ambiguity decreases the value of the optimal stopping policy and accelerates optimal timing by shrinking the continuation region where waiting is optimal. More precisely, for a general measurable and non-negative reward function it holds that

for all and , where and .

Proof.

Inequality follows directly from the definition of the value of the optimal stopping policy in the presence of ambiguity. Denote the continuation regions associated to the considered stopping problems by and . It is clear that if then

implying that as well and, consequently, that .

∎

Lemma 2.1 demonstrates that ambiguity accelerates optimal exercise by shrinking the continuation set at which waiting is optimal. As intuitively is clear higher ambiguity also decreases the value of the optimal policy. It is worth emphasizing that the negativity of the impact of ambiguity on the value and the incentives to wait is more generally valid than just within the considered class of problems, since the proof can be directly extended to a higher-dimensional setting where the underlying processes are more general than just geometric Brownian motions.

3 Optimal Timing Policy

Our objective is now to develop our main results on the considered class of optimal stopping problems. We can now make the following useful observation summarizing a set of conditions under which the worst case prior can be straightforwardly identified and, consequently, under which both the value as well as the optimal stopping policy can be determined from a standard stopping problem.

Lemma 3.1.

For a general measurable and non-negative reward function the following holds true:

(A) Assume that is monotonically increasing as a function of and monotonically decreasing as a function of . Then

the worst case measure is generated by the choice .

(B) Assume that is monotonically increasing as a function of and . Then

the worst case measure is generated by the choice .

(C) Assume that is monotonically decreasing as a function of and monotonically increasing as a function of . Then

the worst case measure is generated by the choice .

(D) Assume that is monotonically decreasing as a function of and . Then

the worst case measure is generated by the choice .

In all cases stated above we have

|

|

|

Proof.

We only prove part (A), since proving the rest of the claims is completely analogous. It is now clear by definition of the value that

|

|

|

In order to reverse this inequality, we notice that since

|

|

|

the alleged claim follows directly from standard comparison results after invoking the a.s.-bounds

|

|

|

|

|

|

|

|

the strong uniqueness of the solutions, and the assumed monotonicity of the exercise payoff.

∎

Lemma 3.1 characterizes the worst case measures in the case where the reward function is strictly monotonic as a function of the underlying state variables.

This simplifies the analysis since it delineates circumstances under which the worst case measure can be determined solely based on the monotonicity properties of the reward

without having to solve simultaneously the worst case density generators and the value of the optimal policy. Since the measure is in the cases treated in Lemma 3.1 independent of the prevailing state, we notice that

under the conditions of Lemma 3.1 the value of the optimal policy preserves the homogeneity of the exercise payoff (cf. Olsen and Stensland, (1992) for a general treatment in the absence of ambiguity; see also McDonald and Siegel, (1986) and Hu and Øksendal, (1998)).

Having stated the cases associated with the monotone cases, we now plan to proceed into the analysis of the more general cases resulting into endogenous state dependent switching of the density generators determining the worst case measure. In order to characterize the worst case measure in the considered class of problems, let us first consider the determination of the optimal density generators by relying on standard dynamic programming arguments. To this end, we denote by

|

|

|

the differential operator associated with the underlying processes under the measure and

assume now that the function is twice continuously differentiable on .

A standard application of the Itô-Döblin theorem then yields

|

|

|

(3.1) |

It is then clear from this expression that the density generators associated with the worst case scenario are of the form

and

Thus, if the function is chosen so that it satisfies the partial differential equation

on some open subset with compact closure in , then we have

|

|

|

(3.2) |

for all admissible density generators , , and .

Noticing that and for all admissible

and then shows that

|

|

|

with equality only when . Even though this observation is interesting as a

characterization for the optimal policy and its value, it has at least two weaknesses from the perspective of the considered class of problems.

First of all, it is not beforehand clear whether the value of the optimal policy is actually smooth enough for the utilization of the

Itô-Döblin theorem. Fortunately, there are extensions which do not require as much smoothness (see, for example, pp. 315 – 318 in Øksendal, (2003) or Section IV.7 in Protter, (2005)) which could be utilized in the determination of the value and worst case measure. Second, the characterization of the value on the continuation region as

a solution of a partial differential equation overlooks the homogeneity properties of the considered class of problems and, therefore, does not make use of the possibility to reduce the dimensionality of the considered problem by focusing on the ratio process instead of the two-dimensional process .

Given the observations above, let us now follow the approach originally developed in Christensen, (2013) and investigate if we can identify a set of minimal harmonic functions which can be utilized in the determination of the value of an optimal timing policy. We also refer to Beibel and Lerche, (1997) (see also Lerche and Urusov, (2007), Christensen and Irle, (2011), and Gapeev and Lerche, (2011)) for related considerations for usual optimal stopping problems.

Put formally, our objective is to identify a twice continuously differentiable function such that , where . In order to achieve this we plan to utilize the positive homogeneity of the exercise payoff and investigate if it is possible to find homogeneous solutions for the partial differential equation characterizing the value on the continuation region. In the present setting

|

|

|

indicating that the density generators resulting into a worst case measure are now

and . Consequently, if then

we necessarily have

|

|

|

for ,

|

|

|

for , and

|

|

|

for . Moreover, for , for , and for .

In order to determine the harmonic mappings needed for the determination of the value and its optimal policy, we first notice that if condition is satisfied then

the quadratic equation

|

|

|

(3.3) |

has two roots

|

|

|

|

|

|

|

|

In that case we can define the monotonically decreasing, twice continuously differentiable, and strictly convex function

On the other hand, condition also guarantees that

the quadratic equation

|

|

|

(3.4) |

has two roots

|

|

|

|

|

|

|

|

In this case we can define the monotonically increasing and twice continuously differentiable function when and

when . Notice that condition implies that guaranteeing that is strictly convex in that case. Finally, in order to capture the potential cases appearing in multiple boundary problems, we again assume that condition is satisfied and define the twice continuously differentiable function as

|

|

|

(3.5) |

when . If, however, then

|

|

|

(3.6) |

where

|

|

|

Since

|

|

|

|

|

|

|

|

we notice that is again twice continuously differentiable on ,

monotonically decreasing on , and monotonically increasing on . Moreover, condition guarantees that is strictly convex on as well, and satisfies the condition on .

It is worth noticing that if , then the function admits the representation

, where

|

|

|

|

|

|

|

|

|

|

|

|

Note that since as the function reduces to

when .

Having characterized the key harmonic functions needed in the characterization of the value of the optimal timing policy, we now investigate the behavior of the ratio

|

|

|

for all and . A set of auxiliary results characterizing the key role of the harmonic functions in the determination of the worst case measure as well as the value of the optimal policy is now summarized in the following (see Lemma 1 in Christensen, (2013)).

Lemma 3.2.

Assume that and denote by the measure induced by the density generators , where . Then,

|

|

|

|

(3.7) |

|

|

|

|

(3.8) |

and

|

|

|

(3.9) |

where is a 2-dimensional Brownian motion under the measure . Moreover, for any stopping time , admissible density generator , and we have

|

|

|

Proof.

We first observe that under our assumptions is strictly convex and twice continuously differentiable on . Consequently, the standard Itô-Döblin theorem applies.

Given this observation and utilizing the identity (3.2) in the homogeneous case yields

|

|

|

where . Assume that is an open subset with compact closure in and let denote the first exit time of the process from . The smoothness of the function and behavior of the ratio process (it can be sandwiched between two geometric Brownian motions) then guarantees that all the functional forms are bounded on open subsets with compact closure on . Since and for all and admissible density generators we notice that

|

|

|

demonstrating that the stopped process

is a bounded positive -submartingale. For we have

|

|

|

proving that the process is a bounded positive local -martingale. Analogous computations demonstrate that the process is actually a positive -martingale and, therefore, a supermartingale. Finally, it is clear that under the measure the underlying processes as well as their ratio evolve according to the random dynamics characterized by the stochastic differential equations (3.7), (3.8), and (3.9).

∎

Lemma 3.2 essentially shows how the function induces an appropriate class of worst case supermartingales for the considered class of processes. A first result of this type is given in the next proposition.

Proposition 3.3.

If

|

|

|

then .

Proof.

Assume that the set and let

It is then clear that (see part (i) of Theorem 3 in Christensen, (2013))

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

for all , , and . Hence, we have found that .

Since for all we notice that

|

|

|

proving that as claimed.

Interestingly, the

ratio process (3.9) is an ordinary linear diffusion with known infinitesimal characteristics which helps us in the determination of the expected first exit times from bounded open intervals in

. This is formally summarized in our next lemma.

Lemma 3.4.

Assume that so that . For all we have

|

|

|

where

|

|

|

,

|

|

|

, , , and .

Proof.

constitutes the density of the scale function and the density of the speed measure of the diffusion characterized by

(3.9). The result then follows from the analysis in, for example, Chapter 4 in Itô and McKean, (1974).

∎

Lemma 3.4 essentially guarantees that the first exit times of from bounded open intervals in

is -a.s. finite. This observation as well as the properties of the function plays a central role in the characterization of the optimal timing policy and its value as summarized in our next theorem.

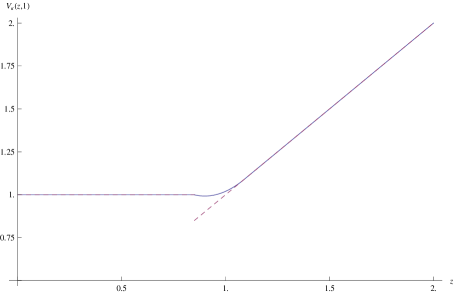

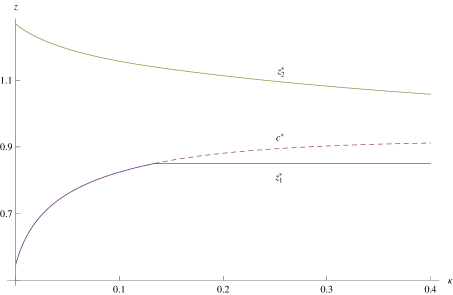

Theorem 3.5 (Two-sided case).

Assume that there are two points , , for some such that . Then

-

(A)

-

(B)

If for all , then

|

|

|

-

(C)

Let be such that -a.s. for all initial points with . Then, is an equilibrium in the sense that for all initial points with it holds that

|

|

|

|

|

|

|

|

Proof.

First note that the process

|

|

|

is a positive -martingale by Lemma 3.2. Using this, it holds that for all and all initial points with

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

It furthermore holds that as given in (C) is -a.s. finite by Lemma 3.4 for all initial points with

and hence . Moreover, by optional sampling,

|

|

|

This yields that for both inequalities in the calculations above are indeed equations, i.e.

|

|

|

|

Since we notice that

|

|

|

implying that for all , i.e., the first inequality in (A). The calculations furthermore prove the second equilibrium condition in (C).

To prove the opposite inequality in (A) and the first equilibrium condition in (C) we obtain – using again that the admissible stopping policy is -a.s. finite and on the set as well as Lemma 3.2 –

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

for all , proving (A). Now, (A) together with the last inequalities im Lemma 3.2, yields the first part of (C).

Finally, noticing that for all we have

|

|

|

showing that , viz. (B).

∎

According to Proposition 3.3 the points belonging to the set are part of the stopping set where waiting is suboptimal independently of the reference point . This is an interesting finding since it provides a straightforward technique for identifying elements in the stopping region. Theorem 3.5 delineates a set of conditions under which the optimal stopping strategy constitutes a two boundary policy and the value can be expressed in terms of the function .

As in the case of a general reference point we again notice that the functions and

can be utilized in the analysis of the optimal timing policy and the associated worst case measure for the one-sided boundary situation. This is summarized in the following two theorems.

Theorem 3.6 (lower-boundary case).

Assume that condition is met and that there exists a point . Then

-

(A)

whenever .

-

(B)

If for all , then

|

|

|

-

(C)

Let be such that -a.s. for all initial points with . Then, is an equilibrium in the sense that for all initial points with it holds that

|

|

|

|

|

|

|

|

Proof.

Noticing that condition yields that is -a.s. finite is met for all initial points with ,

the statement holds by a straightforward modification of the arguments in the proof of Theorem 3.5.

∎

Not surprisingly, we obtain analogously

Theorem 3.7 (upper-boundary case).

Assume that condition

is met and that there exists a point . Then

-

(A)

whenever .

-

(B)

If for all , then

|

|

|

-

(C)

Let be such that -a.s. for all initial points with . Then, is an equilibrium in the sense that for all initial points with it holds that

|

|

|

|

|

|

|

|

Remark

3.8.

Proposition 3.3 together with the previous three theorems leads to a procedure for solving general versions of our stopping problem (2.5) as follows:

-

1.

Determine the maximum points of the real functions for all to find

|

|

|

-

2.

The complement of forms a partition of into subcones. For each such cone , , find a parameter such that Theorem 3.5, 3.6, or 3.7 is applicable. Then, is a worst case prior for the corresponding subcone, defines the value function on it, and the first entrance time into is a (global) optimal stopping time for (2.5). For last claim, note that the underlying processes do not have jumps and therefore, the different connected components of the complement of do not communicate with each other.

The question arises whether this procedure can always be applied. In other words: Is one of the Theorem 3.5, 3.6, or 3.7 always applicable in Step 2?

– The answer is yes under some mild assumptions. To see that this is indeed the case, assume that condition holds and consider, for fixed , , the functions and as functions of .

It is clear that

|

|

|

|

|

|

|

|

Since, for example,

|

|

|

we observe now by utilizing the fact that the pointwise infimum of an affine function is concave and, thus, continuous, that is continuous as a function of . Since the maximum of continuous functions is continuous, we notice that is continuous as a function of too. The same argument is naturally valid for as well. Consequently, the difference

|

|

|

is continuous as a function of . Now, there are three possible cases:

-

1.

. Then there exists such that Theorem 3.6 is applicable whenever is a maximum (which is the case under standard continuity- and growths-assumptions on the reward function ).

-

2.

. Then, whenever is a maximum, there exists such that Theorem 3.7 is applicable.

-

3.

By continuity, there exists such that . Assuming again that the suprema are maxima, there exist two points such that Theorem 3.5 is applicable.

It is at this point worth emphasizing that our findings indicate that the representation of the value as the smallest element of an appropriately chosen function space developed in Christensen, (2013) applies in some cases in the present setting as well.

In that case we have

|

|

|

for all .

It is clear from the description above that the minimal harmonic functions in the present case differ from the ones appearing in the one-dimensional setting. There are two main reasons for this. First, the presence of two driving random factor dynamics implies that the underlying density generators may separately switch from one extreme to another at different states as is clear from the form of the sets and . Second, the assumed homogeneity of the exercise payoff implies that both the growth rate as well as the density generator associated with the numeraire variable affect the rate at which the problem is discounted. This mechanism where nature also selects the rate at which the problem is discounted cannot naturally appear in a one-dimensional setting where discounting is not affected by the characteristics of the underlying factor dynamics.