Partially Specified Space Time Autoregressive Model with Artificial Neural Network

Wenqian Wang

Beth Andrews

Department of Statistics

Northwestern University

1 Introduction

In Chapter 1, we proposed a PSAR model enhanced by a neural network component which aims at explaining the spatial dependence through a nonlinear approach. However, sometimes we may collect data across time as well as space. For this type of data, we want to construct a model with dependence over time taken into consideration which has a broad application especially in environmental sciences. One interesting application is forecasting the weather. For example, in a fixed location, the everyday temperature will change from time to time but in the meanwhile, it would also be affected by temperatures in the neighboring locations.

A class of such linear models known as space-time autoregressive (STAR) and space-time autoregressive moving average (STARMA) models was introduced by Cliff and Ord (1973) and Martin and Oeppen (1975) in 1970s. In general, STAR models contain a hierarchical ordering of “neighbors” of each site. For instance, on a regular grid, one can categorize neighbors of a site as first-order and second-order neighborhoods and so on. An observation at each site is then modeled as a linear function of the previous time observations at the same site and of the weighted previous observations at the neighboring sites of each order. Let be a multivariate time series of location components. Weights are incorporated in weight matrices for order . An STAR model with autoregressive order and spatial order considerded in Borovkova et.al (2008) is defined as

where is the spatial order of the th autoregressive term, is the autoregressive parameter at time lag and spatial lag . Similarly an STAR model with space locations and exogenous variables is given by Stoffer (1985) as, for ,

where values of the exogenous variables are covariate matrices containing values of exogenous variables for all locations at time . and . is the autoregressive order for and is a model parameter.

STAR models have been widely applied in many areas of science. In genomics, Epperson (1993) analyzed population gene frequencies using STAR models where he assumed genes may vary over space and time. This model is also well known in economics (Giacomini and Granger, 2004) and has been applied to forecasting regional employment (Hernandez and Owyang, 2004) as well as traffic flow (Garrido 2000; Kamarianakis and Prastacos, 2004). For instance, the traffic flow of a road network observed at different fixed locations can be simultaneously modelled as a linear combination of past observations and current observations at neighboring sites. Through weight matrices, an STAR model assumes that near sites exert more influence on each other than distant ones.

In this chapter, we want to extend an STAR model to a semi-parametric model such that this new model can capture nonlinear dependence between covariates and the spatial observations of interest.

2 PSTAR-ANN model

We define a Partially Specified Space-Time Autoregressive model with Artificial Neural Network (PSTAR-ANN) as follows.

| (1) |

where contains observations of dependent variables at locations and at time . The independent variable matrix is the covariate matrix at time , where is a vector containing exogenous regressors at location and time , . denote a vector of noise terms which are independent identically distributed across and with density function , mean and variance .

Exogenous parameters and scalars , the spatial/space-time autoregressive parameters, are assumed to be the same over all regions. is a known spatial weight matrix which characterizes the connection between neighboring regions. For the ease of illustration, we define some notations. Given a function continuous in , we define a new matrix map as s.t. .

Using the notation defined above, the artificial neural network component (Medeiros et al. [14]) can be written as

represents two layer NN component where the first layer has -neurons with the sigmoid activation function and the second layer has only one neuron with an identity activation function. In the first layer, the input is and weights are where is the weights in the th neuron. is the sigmoid activation function in this layer.

In the second layer, the inputs are and the weights are . So final output is for each .

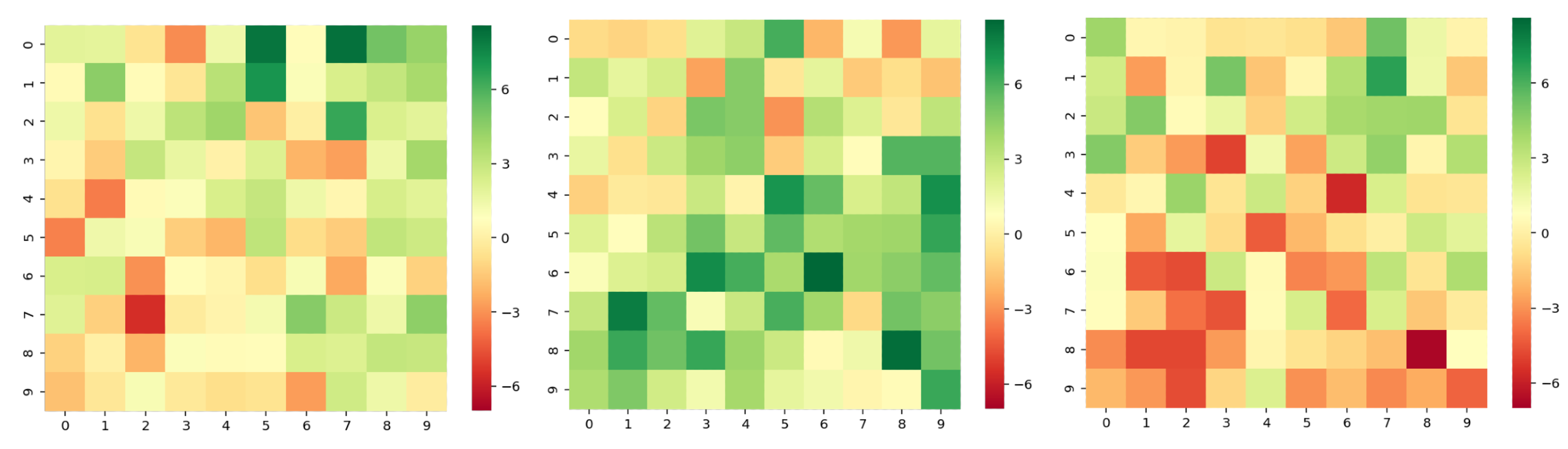

The weight matrix is a measure of distance between the spatial units, and in our application, we begin by using a square symmetric matrix with element equals to 1 if regions and are neighbors and otherwise. The diagonal elements of the matrix are set to zero. Then we row standardize this matrix denoted by . For more details on construction of the weight matrix, you can refer to the previous chapter or LeSage [12]. The following plot provides a preview of the data we are working with. This data is generated from a PSTAR-ANN model in a 10 by 10 lattice. The model equation is shown below:

| (2) |

, with are generated i.i.d from , and the error is from . Figure 1 shows the heatmaps of simulated at using (2).

The color scale represents the value in each cell. We can observe colors in cells changing gradually with the spatial and time dependence (, there is a little flip in cell color comparing the left figure with the middle one).

3 The Model and the Likelihood Function

3.1 The Model

Let

Suppose is invertible, then model (1) can be rewritten as:

Let be the usual backshift operator such that , . Assuming that exists, we can rewrite as

| (3) |

In order to derive asymptotic properties, we also need to be a causal spatial temporal process. Referring to the definition in Brockwell and Davis [5], the process is causal if there exists matrices with absolutely summable components such that . Let be a matrix-valued polynomial. Causality is equivalent to the condition for all such that .

The matrices can be found recursively from the equations

| (4) |

where we define , for , for and for . Therefore, this gives us

Then

| (5) |

With this expansion, we need few assumptions on and will be discussed later.

3.2 Likelihood Function

Denote . Since has an identical density function , the conditional joint density of conditioned on a finite number of past values and is

Since

we have

Hence, the log-likelihood function of is given by [2, p. 63],

| (6) |

where for .

For the analysis of identification and estimation of the PSTAR-ANN model, we adopt the following assumptions:

Assumption 1.

The parameter vector , where is a subset of the dimensional Euclidean space, . is a closed and bounded compact set and contains the true parameter value as an interior point.

Assumption 2.

The spatial correlation coefficient satisfies and , where , are eigenvalues of spatial weight matrix . To avoid the non-stationarity issue when approaches to 1, we assume .

Assumption 3.

We assume is defined by queen contiguity and is uniformly bounded in row and column sums in absolute value as so is also uniformly bounded in both column and row sums as .

Assumption 4.

We assume a causal spatial process which means that every which solves

lie inside a unit circle. So the operator is causal [16].

Assumption 5.

is stationary, ergodic satisfying and is full column rank for .

Assumption 6.

The error terms , , are independent and identically distributed with density function , zero mean and unit variance . The moment exists for some and .

Assumption 2 defines the parameter space for such that is strictly diagonally dominant. By the Levy-Desplanques theorem [19], it follows that exists for any values in . In real applications, since is row standardized, one just searches over a parameter space on to find the optimizer [7, p. 749-754].

It is natural to consider the neighborhood by connections and in many practical studies, since entries scaled to sum up to 1, each row of sums up to 1, which guarantees that all nonzero weights are in . For simplicity, we define the weight matrix using the queen criterion and do row standardization. Assumption 3 is originated by Kelejian and Prucha [9, 10] and is also used in Lee [11]. With to be uniformly bounded, we can prove that is also uniformly bounded in row and column sums for and , by Lemma A.4 in Lee[11]. This result is a necessary condition for Assumption 4.

From Assumption 2 and 3, we can decompose by its eigenvalue and eigenvector pairs : , where is a diagonal matrix with eigenvalues on its diagonals and (we assume ’s are normalized eigenvectors). So

| (7) |

It is trivial that .

Assumption 4 guarantees that is a causal operator and there exists a casual solution to the system of the model equation (1). Then is absolutely summable. This requirement serves to determine a region of possible values that will result in a stationary process .

Assumption 5 is a trivial one when exogenous variables are included in a space time model. Similar to previous chapter, the stationarity of is necessary in the ergodic theorem in later proofs.

Assumption 6 imposes restrictions for the random error. In this paper we mainly consider the heavy tailed density functions such scaled distributions and Laplace distributions. When the degrees of freedom goes to infinity, the scaled distribution would approximate a standard normal distribution. So we would like to concentrate more on the scaled distribution with lower degrees of freedom.

4 Model Identification

In the previous section, we have some restrictions on the weight matrices and ’s to guarantee the identification of a classical spatial time autoregressive model. We now investigate the conditions under which PSTAR(p)-ANN model is identified. By Rothenberg [17], a parameter is globally identified if there is no other in that observationally equivalent to such that ; or the parameter is locally identified if there is no such in an open neighborhood of in . The model (1), in principle, is neither globally nor locally identified due to the neural network component. The lack of identification of neural network models has been discussed in many papers (Hwang and Ding [8]; Medeiros et al. [14]). Here we extend the discussion to our proposed PSTAR(p)-ANN model. Three characteristics imply non-identification of our model: (a) the interchangeable property: the value of the likelihood function may remain unchanged if we permute the hidden units. For a model with neurons, this will result in different models that are indistinguishable from each other and have equal local maximums of the log-likelihood function; (b) the “symmetry” property: for a logistic function, allows two equivalent parametrization for each hidden unit; (c) the reducible property: the presence of irrelevant neurons in model (1) happens when for at least one and parameters remain unidentified. Conversely, if , is a constant and can take any value without affecting the value of likelihood functions.

The problem of interchangeability (as mentioned in (a)) can be solved by imposing the following restriction, as in Medeiros et al. [14]:

Restriction 1. parameters are restricted such that: .

And to tackle (b) and (c), we can apply another restriction:

Restriction 2. The parameters and should satisfy:

(1) , ; and

(2) , .

To guarantee the non-singularity of model matrices and the uniqueness of parameters, we impose the following basic assumption:

Assumption 7.

The true parameter vector satisfies Restrictions 1-2.

Referring to the section 4.3 by Medeiros et al. [14], we can conclude the identifiability of the PSAR-ANN model.

5 Asymptotic Results

Let the true parameter vector as and the solution which maximizes the log-likelihood function (6) as . Hence, should satisfy

Suppose as is large enough, goes to infinity, is equivalent to maximizing the average of the likelihood function shown as follows:

At specific time , suppose we have a lattice where we consider asymptotic properties of when . Write the location as the coordinate in the lattice space. The distance between two locations is defined as . So if observations at locations are neighbors (by queen criterion), their coordinates should satisfy or .

In a spatial context, we should notice that the functional form of is not identical for all the locations due to values of the weights . For example, in a lattice, units at edges, vertexes or in the interior have different density functions due to different neighborhood structures (Figure 2). Denote as a neighborhood set for location . For an interior point (Figure 2(c)), its neighborhood set contains eight neighbors where if otherwise , for . Similarly, an edge point (Figure 2(b)) has five neighboring units with for and the weight of a vertex neighborhood is because a vertex unit has only three neighbors. This is known as an edge effect in spatial problems.

To deal with this, referring to Yao and Brockwell [23], we construct an edge effect correction scheme based on the way that the sample size tends to infinity. In a space , we consider its interior area as , where satisfying that and other locations belong to the boundary areas . Therefore the set contains interior locations while the set contains boundary locations. Then and can be split into a sum of two parts (interior and boundary parts):

where and is the row of .

Therefore, given that , vanishes a.s. as tends to infinity for any . Therefore,

In this equation, every location has eight neighboring units under the queen criterion with nonzero weights . Hence for an interior unit , . And the log likelihood function is approximately

| (8) |

So the maximum likelihood estimator approximately maximizes

5.1 Consistency Results

To establish the consistency of , the heuristic insight is that because maximizes , it approximately maximizes . By equation (8), can generally be shown tending to a real function with maximizer as under mild conditions on the data generating process, then should tend to almost surely. Before the formal proof of the consistency, we need the following assumptions on the density function satisfied (similar assumptions are made in White [22], Andrews, Davis and Breidt [1], Lii and Rosenblatt [13]).

Assumption 8.

For all , and is twice continuously differentiable with respect to .

Assumption 9.

The density should satisfy the following equations:

Assumption 10.

The density should follow the following dominance conditions:

, , , , and are dominated by , where , , are non-negative constants and .

Assumption 11.

If in previous assumption, we further assume .

Discussed in Breidt, Davis, Lii and Rosenblatt [4] and Andrews, Davis and Breidt [1, p. 1642-1645], these assumptions on the density are satisfied by the t-distribution case when and by a mixture of Gaussian distributions. The assumption (see Assumption 6) is also checked satisfied by the normal and t distributions (). The Laplace distribution does not strictly satisfy the Assumptions 8-10, since it is not differentiable at 0 but it satisfies these boundedness conditions almost everywhere so we believe the consistency and asymptotic normality results remain valid for parameter estimates. This will be shown in the simulation section. Assumption 11 is a necessary to boundedness conditions in later proof.

Proof.

is the joint density function of for .

Denote . By Jensen’s inequality,

So . By Lemma 1, the PSTAR(p)-ANN model is globally identified and therefore is uniquely maximized at for all . Since the parameter vector does not depend on and , it is equivalent to say that . ∎

We define a Hadamard product denoted by , s.t. for vectors , a matrix ,

And let

To facilitate the proof later on, we provide a lemma as follows.

Proof.

As illustrated in equation (8), in a lattice with size ,

Therefore, to prove (9) is equivalent to show that

| (10) |

where denotes the interior units mentioned before. Since the interior units have the same neighboring structure, the space process for them is stationary when go to infinity. We first show for fixed .

To prove this, we want to show that . Expanding around with respect to ,

where is between and . Under the true parameter values, (denoted as or as its vector form in the following) is independent and identically distributed. From Assumption 6, . For , can be expressed as

| (11) | ||||

where . Function . Consider ,

Denote is a polynomial about with highest order . Since we have assumed that existed and the expansion is absolutely summable so is finite. By Assumption 10-11, and are dominated by , . Let , then,

So also . With Cauchy–Schwarz inequality [18] and the finite second moment of , we can have,

| (12) | ||||

| (13) | ||||

| (14) | ||||

| (15) | ||||

| (16) | ||||

| (17) |

Because is well defined and is stationary with finite second moment, so component (17) is finite. (16) is dominated by so with the dominance assumption, (16) is finite. Hence, with (12)-(17) finite, , we can conclude that . Then by ergodic theorem [3],

To complete the proof of uniform convergence, we also need to show is equicontinuous for , i.e., for all ,

| (18) |

Applying the mean value theorem to the left side in (18):

where is some value between and . Since is in a compact set , we show in (5.1) that, for all , is bounded by some function of not depending on .

| (19) | ||||

Similarly, referring to (5.1), it is easy to show that is bounded by some function about and . Therefore, due to the dominance of (see Assumption 10) and stationarity of , for between and , there exists a constant such that

| (20) |

Hence, for

So is equicontinuous for . With the pointwise convergence and equicontinuity, we can conclude the uniform convergence in (10) and furthermore (9) follows. ∎

Similar to Chapter 1, we now give a formal statement of the consistency results.

Proof.

Similar to the proof by Lung-fei Lee [11], we need to show the stochastic equicontinuity of to have the uniform convergence of the log likelihood function . Applying the mean value theorem,

where is between and . By Assumption 2 and 3, , is bounded in both rows and column sums uniformly and using (7),

where is a constant not depending on . So and with Lemma 3 we can conclude the uniform convergence that

With the assumptions 1-10, the parameter space is compact; is continuous in and is a measurable of for all . is continuous on and by Lemma 2, has a unique maximum at . Referring to Theorem 3.5 in White [21] with the uniform convergence in (9), we can conclude that as . ∎

5.2 Asymptotic Distribution

Assumption 12.

The limit is nonsingular.

Assumption 13.

The limit is nonsingular.

These assumptions are to guarantee the existence of the covariance matrix of the limiting distribution of parameters in a PSTAR(p)-ANN model. We now give the asymptotic distribution of the maximum likelihood estimator .

Proof.

Since maximizes , . By the mean value theorem, expand around with respect to ,

where is between and . Therefore, we can have the following equation:

| (22) |

From (5.1), denote as and .

Recall that so the first order derivatives can be expressed as

| (23) |

By Lemma 2, the true parameter values maximize , so . In (12)-(17) and (5.1), we showed that is dominated by some function not related to and (20) indicates that is bounded for interior units in . Hence,, it follows that, with , we can have,

Therefore, with Assumption 13,

And under this . Since is the sum of identical and ergodic random variables, by the central limit theorem for stationary ergodic processes [15], the limiting distribution of is .

Next we would like to show that . Following the results in (23), define , and write so the second order derivatives are given below

| (24) |

Since is between and , so also converges to in probability as . By Assumption 10, and are continuous and are bounded by so are continuous. With , is also a continuous function of .

Therefore elements in are continuous functions for in . Then by the continuity,

| (25) |

Finally we will prove that . Since can be decomposed as , to show is equivalent to show

| (26) |

We first discuss the second derivative with respect to component in (26). By triangular inequality, where is the true value of . Consider , under stationarity, it can be simplified as

| (27) |

Define and by assumptions, is uniformly bounded in row and column. Suppose the row sum or column sum of is bounded by a constant . We know . So we only need to show .

By simple linear algebra,

So . Therefore is the component of and we expand

| (28) | ||||

| (29) | ||||

| (30) |

From assumptions 3 and 4, we know that is uniformly bounded and is absolute summable so under the stationary condition of . Hence, .

Therefore combining all these components together, . So equation (27) is finite.

Because in (26) only relates to , this term goes away when taken second derivative with respect to other parameters. Similar to the proof of , we can show that for and , i.e.,

Other elements in the matrix (26) equal to those in and they are also finite.

| (31) | ||||

| (32) | ||||

| (33) | ||||

| (34) | ||||

| (35) | ||||

| (36) | ||||

| (37) | ||||

| (38) | ||||

| (39) | ||||

| (40) |

Then we can apply the ergodic theorem [3] and conclude that

| (41) |

Recall the equation (22), we have proved that has the limiting distribution . With (41), for between and , so we can conclude that , where . ∎

6 Numerical Results

6.1 Simulation Study

In this section, we conduct simulation experiments to examine the estimators’ behavior for finite samples. We look at two PSTAR-ANN models with one and two neurons with model parameters specified below:

| (42) | |||

| (43) | |||

Simulations are conducted in a 30 by 30 lattice grid, so and , . Random errors are sampled respectively from three distributions (standard normal, rescaled t-distribution and Laplace distribution) with variance 1. We generated data for two exogenous variables, observed at different time points and location . Let . Usually we would like to normalize predictors before fitting a neural network model to avoid the computation overflow [14] so values of , were generated independently from normal distributions and respectively. The log-likelihood function is given in (44) and we use L-BFGS-B method [6, 24] (recommended for bound constrained optimization) to find the parameter estimates which maximize (44).

| (44) | ||||

| for model (42): | ||||

| for model (43): |

For the models under consideration, we estimated the covariance of the asymptotic normal distribution equation (21). Since matrices and involve expected values with respect to the true parameter , given merely observations, in practice they can be estimated as follows:

where

Using (23) and (24), we can calculate to assess the asymptotic properties of parameter estimates. Note that the derivative of the log-likelihood with respect to cannot be calculated directly because it requires taking derivative with respect to a log-determinant of . For small sample sizes, we can compute the determinant directly and get the corresponding derivatives; but for large sample sizes, for example a dataset with observations, is a weight matrix which makes it impossible to calculate the derivative directly. Since is a square matrix, we can apply the spectral decomposition such that can be expressed in terms of its eigenvalue-eigenvector pairs in (7). So we can apply the following approach to calculate the derivative of , which greatly reduces the burden of computations (Viton [20]).

Further the derivatives of the log-likelihood function with respect to is

Finally we can estimate the covariance matrix by equation (45).

| (45) |

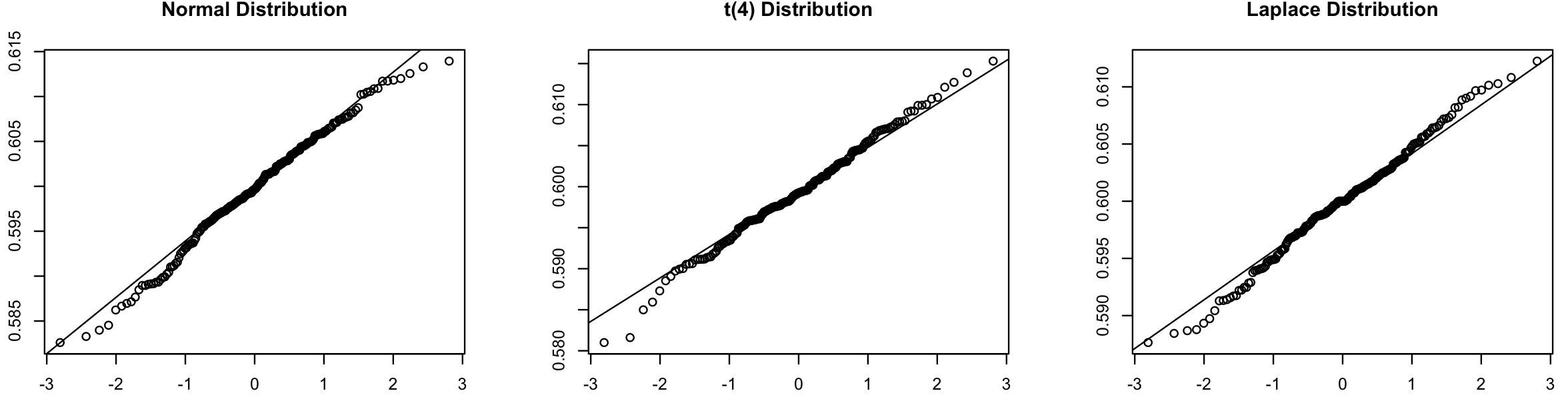

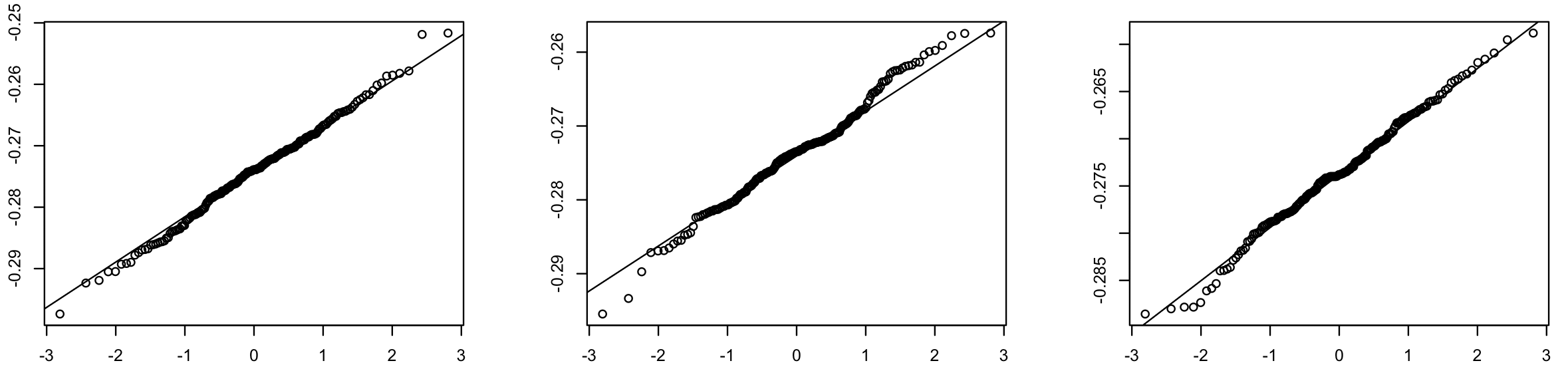

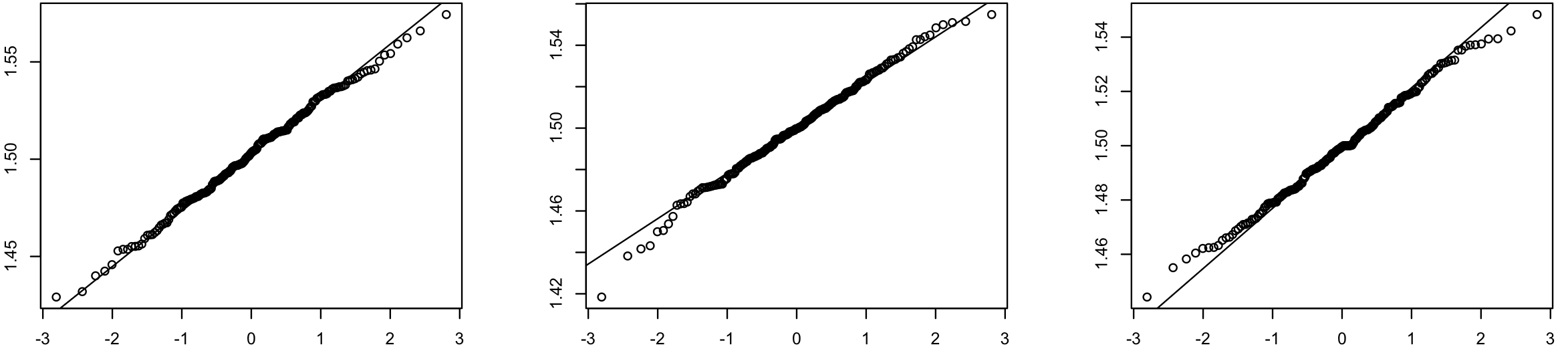

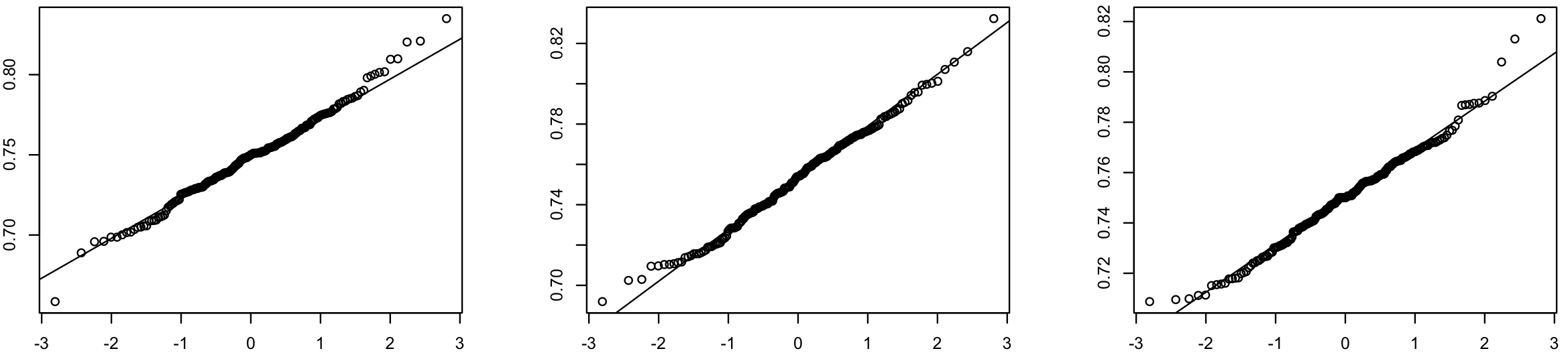

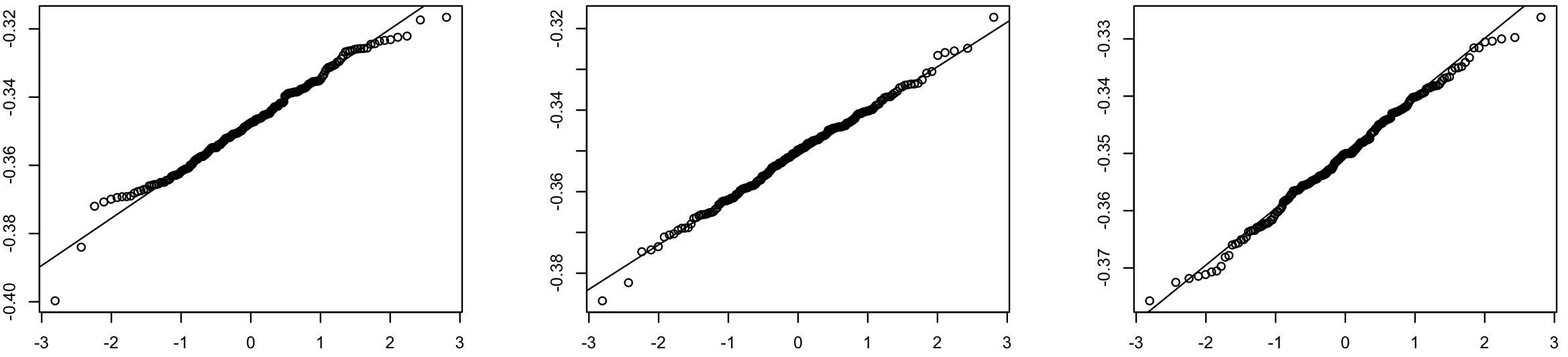

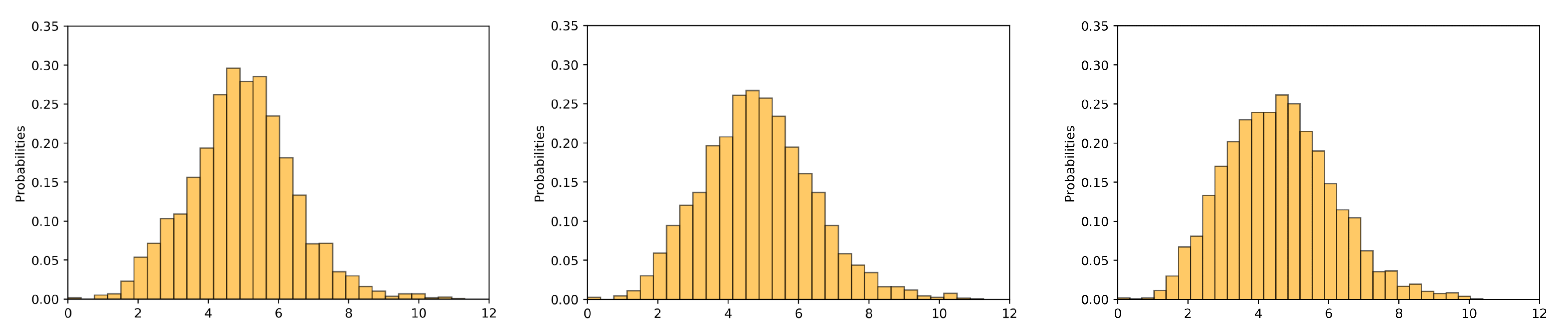

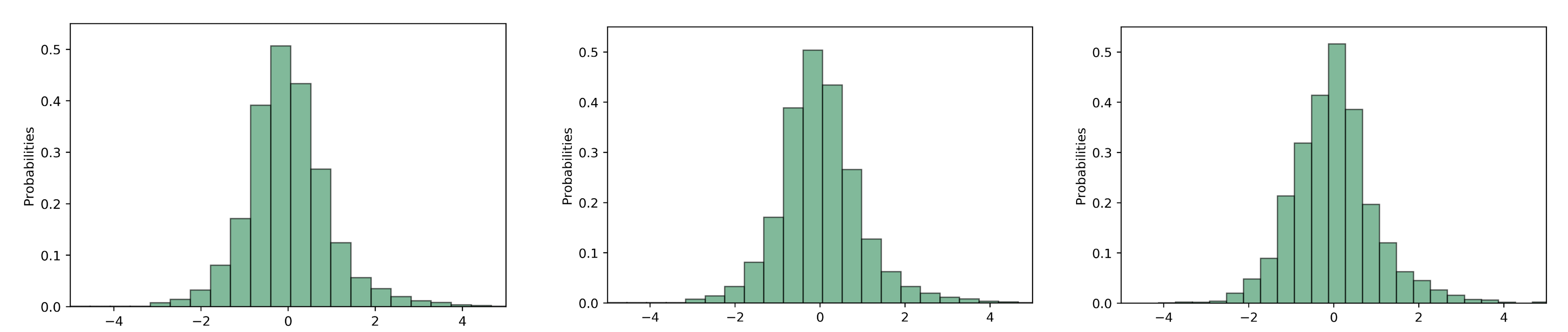

In each simulation study, we compute for each of 200 replicates. The estimated of the asymptotic covariance matrix is computed based on a sample with simulated observations. Table 1 compares the empirical mean and standard errors (in parentheses) of with the true value and their estimated asymptotic standard deviations. From simulation results of the two models, the empirical standard deviations of are close to the asymptotic standard deviations, which implies that the estimators’ large finite sample behavior roughly matches their asymptotic distributions. Note that when is sampled from a Laplace distribution, this covariance matrix cannot be computed because its second order derivative is not differentiable at . But the simulated ’s still exhibit normal properties. Normal plots for parameter estimates are shown in Figure 3 and give a strong indication of normality.

| Model 1: | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| true value | ||||||||||

| 0.5997 | -0.2743 | 1.5025 | 0.7485 | -0.3476 | ||||||

| (0.0065) | (0.0079) | (0.0274) | (0.0269) | (0.0134) | ||||||

| [0.0079] | [0.0085] | [0.0308] | [0.0310] | [0.0147] | ||||||

| 0.5994 | -0.2737 | 1.5000 | 0.7531 | -0.3507 | ||||||

| (0.0059) | (0.0069) | (0.0236) | (0.0249) | (0.0112) | ||||||

| [0.0068] | [0.0071] | [0.0259] | [0.0258] | [0.0122] | ||||||

| 0.5999 | -0.2736 | 1.4992 | 0.7501 | -0.3504 | ||||||

| (0.0048) | (0.0058) | (0.0199) | (0.0196) | (0.0097) | ||||||

| Model 2: | ||||||||||

| 0.6000 | -0.2748 | 0.2402 | -0.6985 | 1.9927 | 0.7503 | 0.7030 | 0.8076 | 0.3577 | -1.0159 | |

| (0.0039) | (0.0046) | (0.0137) | (0.0140) | (0.0928) | (0.0962) | (0.0369) | (0.0450) | (0.0899) | (0.1209) | |

| [0.0040] | [0.0044] | [0.0135] | [0.0141] | [0.0921] | [0.0920] | [0.0390] | [0.0449] | [0.0835] | [0.1243] | |

| 0.5999 | -0.2740 | 0.2402 | -0.7005 | 2.0008 | 0.7496 | 0.7016 | 0.7989 | 0.3521 | -1.0078 | |

| (0.0036) | (0.0034) | (0.0130) | (0.0106) | (0.0727) | (0.0714) | (0.0332) | (0.0392) | (0.0749) | (0.0972) | |

| [0.0035] | [0.0036] | [0.0116] | [0.0113] | [0.0759] | [0.0324] | [0.0371] | [0.0758] | [0.0697] | [0.1026] | |

| 0.6006 | -0.2743 | 0.2408 | -0.6997 | 1.9983 | 0.7509 | 0.7026 | 0.8034 | 0.3477 | -1.0089 | |

| (0.0030) | (0.0030) | (0.0100) | (0.00995) | (0.0638) | (0.0624) | (0.0256) | (0.0293) | (0.0621) | (0.0873) | |

6.2 Real Data Example

Spatial models have a lot of applications in understanding spatial interactions in cross-sectional data. In our first chapter we applied a partially specified spatial autoregressive model to understand the relationships between vote choices and social factors. In this chapter, we want to use a partially specified space time autoregressive model to further analyze the time influence in the electoral dynamics.

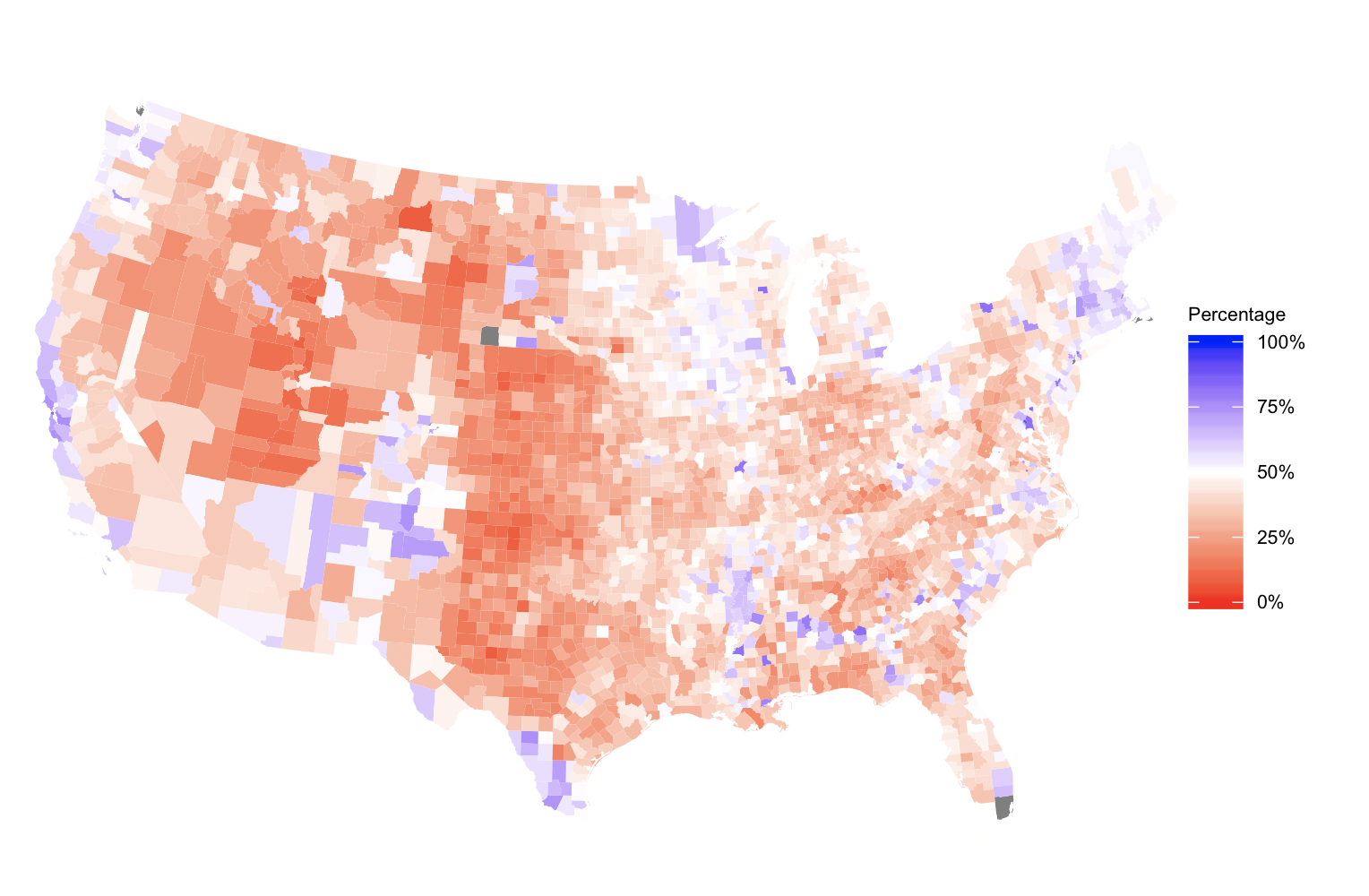

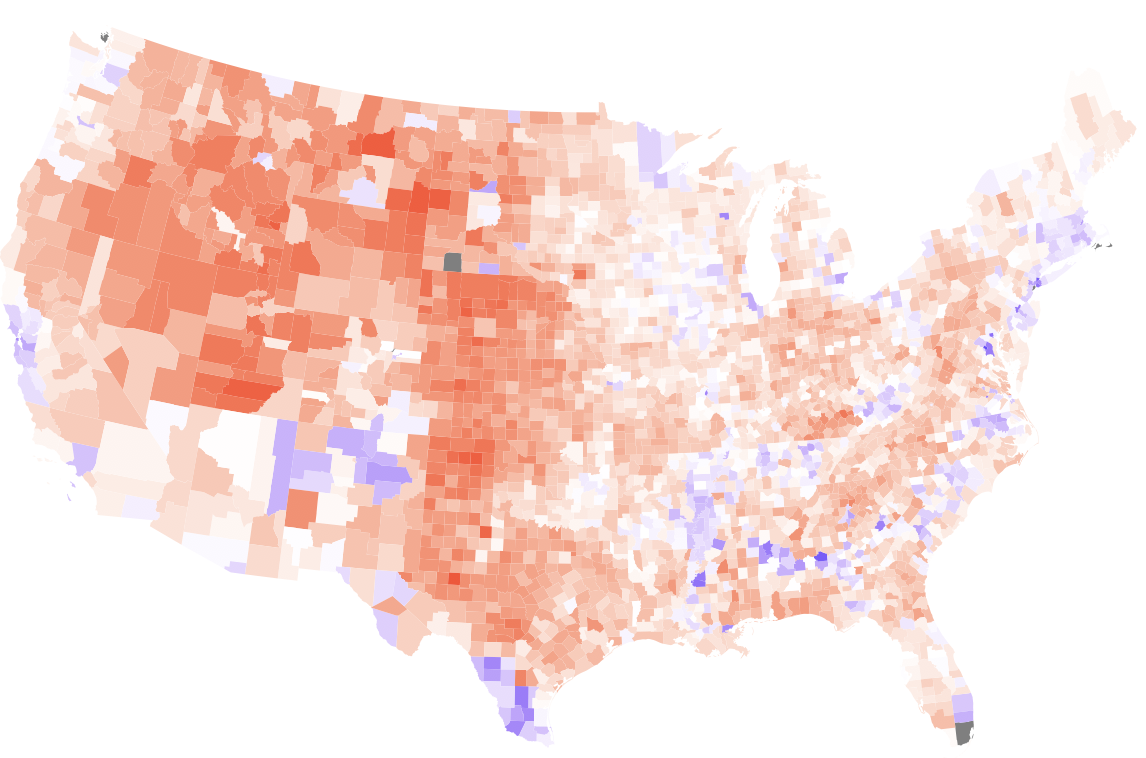

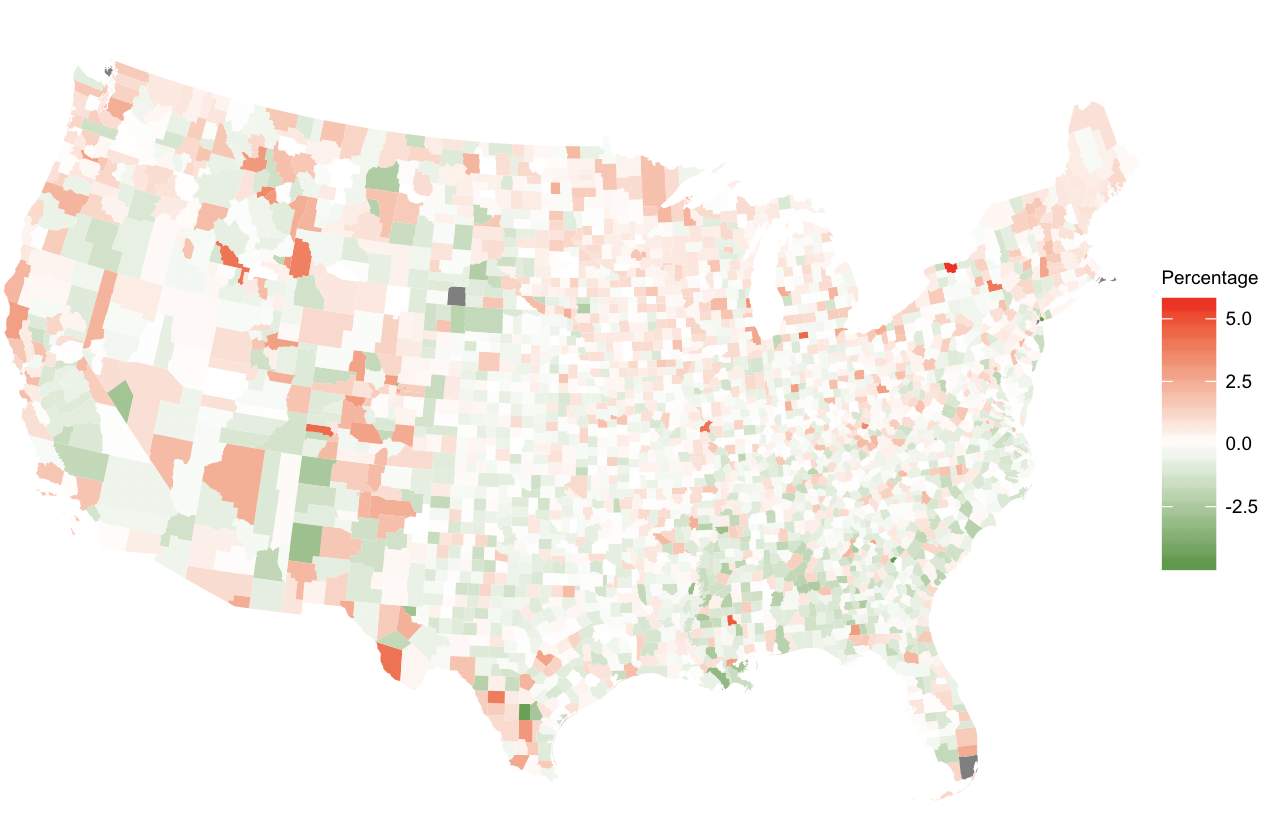

We focus on the proportion of votes cast for U.S. presidential candidates at the county level in 2004. Counties are grouped by state, and let (so , i.e., observe and ) be the corresponding fraction of votes (vote-share) in a county for the Democratic candidate in 2004 and 2000. Predictors are chosen from economic and social factors covering the living standard, economy development and racial distribution.

Figure 4 shows the observed values of for 2004 and for 2000 in a US map. Despite the strong spatial correlation (by Moran’s Test on test statistic = , P-value ), these heat maps also exhibit the correlation across time since the two heat maps look rather similar. This indicates that , the fraction of vote-share for Democratic candidate, is not independently distributed across the space or time. Therefore we consider fitting a space time model to the data.

In our analysis, we exclude the four U.S. counties with no neighbors (San Juan, Dukes, Nantucket, Richmond) to avoid the non-singularity of our spatial weight matrix in the modeling, so the total number of observations is . Continuing our analysis in the first chapter, the selected explanatory variables are percent residents under 18 years in 2004 (UNDER18), percent white residents in 2004 (WHITE), percent residents below poverty line in 2004 (pctpoor).

We also assume the random error follows a scaled distribution and, similar to previous chapter, perform variable transformations as follows:

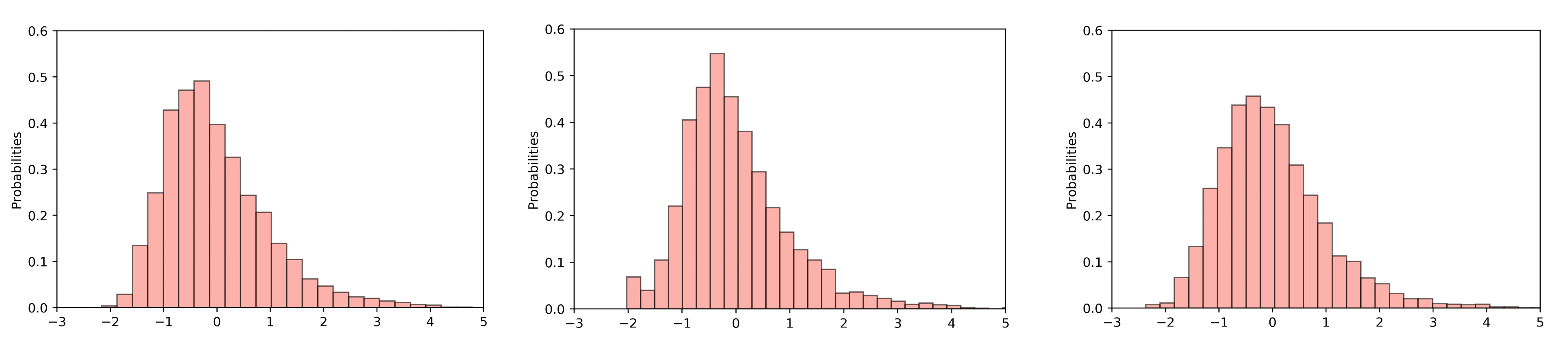

Figure 5 illustrates histograms of (first row) and histograms of exogenous variables when ( represents the year 2008) respectively. Comparing their histograms at different years, we can observe that the distributions look similar so we may consider and as stationary processes across time.

The estimated PSAR-ANN model in chapter 1 is:

| (46) |

In this chapter we would like to add time into the model and we fit two PSTAR-ANN models with one and two neurons respectively. Similarly we find the parameter estimates by maximizing the corresponding log-likelihood functions and use the L-BFGS-B algorithm to search for the optimum. Detailed optimization steps are similar to those in chapter 1. The model fits are shown below. One is the PSTAR-ANN with one neuron:

| (47) |

Another is the PSTAR-ANN with two neurons:

| (48) | ||||

Comparing the three models (6.2), (6.2) and (6.2), the coefficients estimates are all positive so it is apparent that there exist a positive space correlation, between and its neighbors, and also a positive time correlation between and . The P-values of Moran’s test statistic of PSTAR-ANN model residuals (residuals of model (6.2) and (6.2)) are higher than that of model (6.2), which indicates that PSTAR-ANN models are able to describe more spatial correlations than the PSAR-ANN model.

For the preliminary comparison purpose, we compare the AICs (AIC ) of the three models (See table 2). For likelihood ratio test (: Model (6.2) is adequate, : model (6.2) is adequate), the test statistic with , P-value , so we rejected and conclude that the PSTAR-ANN model with one neuron is a better fit. Similarly we apply the same method to compare the two PSTAR-ANN models and conclude that the model with two neurons is better (the test statistic with , P-value ).

| Models | PSAR-ANN | PSTAR-ANN | PSTAR-ANN |

|---|---|---|---|

| (one neuron) | (one neuron) | (two neurons) | |

| Parameters | |||

| Moran’s Test | |||

The covariance matrices for the parameter estimates of model (6.2) and (6.2) are calculated and the confidence intervals for the model parameters are shown in Tables 3 and 4.

| Parameter | Estimate | Std. | C.I. |

|---|---|---|---|

| 0.425 | 0.0086 | ||

| 0.464 | 0.0182 | ||

| -1.173 | 0.3283 | ||

| 0.148 | 0.0697 | ||

| -1.177 | 0.1638 | ||

| -0.153 | 0.1079 | ||

| 3.056 | 0.6397 | ||

| -0.722 | 0.1278 | ||

| 1.689 | 0.1762 | ||

| 0.248 | 0.1890 |

From Table 3, all the parameters, except (pctpoor), are significant at 0.05 significance level. Table 4 shows the level of parameter estimates in model (6.2).

| Parameter | Estimate | Std. | C.I. |

|---|---|---|---|

| 0.417 | 0.0086 | ||

| 0.467 | 0.0178 | ||

| -1.576 | 0.3063 | ||

| 0.203 | 0.0731 | ||

| -1.222 | 0.1507 | ||

| -0.057 | 0.0926 | ||

| 3.180 | 1.2624 | ||

| -0.621 | 0.1193 | ||

| 1.621 | 0.1521 | ||

| 0.495 | 0.1063 | ||

| 0.699 | 0.2397 | ||

| -1.294 | 0.6060 | ||

| 0.084 | 0.4859 | ||

| -3.247 | 0.3570 |

From Table 3 and 4, we can see that values of are positively spatially correlated in both space and time. Looking at the signs of parameter estimates of coefficients, we can see that the sign of variable UNDER18 in model (6.2) is negative while positive in model (6.2) and (6.2). Considering its parameter estimate significant in all models, this indicates that age and vote-shares for Democratic candidates can be dependent but the percent residents under 18 may not be a good measurement for this social factor. We should consider using other age related variables to predict such as the percent young voters between 18 and 30 years old. Variable WHITE is negatively correlated with in all three fitted models and this negative correlation accords with our common sense that white voters tend to support the Republican candidate. The last variable pctpoor is bit tricky because it is not significant in model (6.2) but is significant in the neural network component in model (6.2). Regarding to this, it needs further assessment to decide if pctpoor should be included in the model. In chapter 3, we will further discuss the model selection in detail. To conclude, our proposed model PSTAR-ANN appears to successfully capture some presidential election dynamics over both space and time. It allows for non-Gaussian random errors and is flexible in learning nonlinear relationships between the response and exogenous variables.

References

- Andrews et al. [2006] Beth Andrews, Richard A Davis, and F Jay Breidt. Maximum likelihood estimation for all-pass time series models. Journal of Multivariate Analysis, 97(7):1638–1659, 2006.

- Anselin [2013] Luc Anselin. Spatial econometrics: methods and models, volume 4. Springer Science & Business Media, 2013.

- Birkhoff [1931] George D Birkhoff. Proof of the ergodic theorem. Proceedings of the National Academy of Sciences, 17(12):656–660, 1931.

- Breid et al. [1991] F Jay Breid, Richard A Davis, Keh-Shin Lh, and Murray Rosenblatt. Maximum likelihood estimation for noncausal autoregressive processes. Journal of Multivariate Analysis, 36(2):175–198, 1991.

- Brockwell et al. [2002] Peter J Brockwell, Richard A Davis, and Matthew V Calder. Introduction to time series and forecasting, volume 2. Springer, 2002.

- Byrd et al. [1995] Richard H Byrd, Peihuang Lu, Jorge Nocedal, and Ciyou Zhu. A limited memory algorithm for bound constrained optimization. SIAM Journal on Scientific Computing, 16(5):1190–1208, 1995.

- Gershgorin [1931] Semyon Aranovich Gershgorin. Uber die abgrenzung der eigenwerte einer matrix. Bulletin de l’Académie des Sciences de l’URSS. Classe des sciences mathématiques et na, (6):749–754, 1931.

- Hwang and Ding [1997] JT Gene Hwang and A Adam Ding. Prediction intervals for artificial neural networks. Journal of the American Statistical Association, 92(438):748–757, 1997.

- Kelejian and Prucha [1998] Harry H Kelejian and Ingmar R Prucha. A generalized spatial two-stage least squares procedure for estimating a spatial autoregressive model with autoregressive disturbances. The Journal of Real Estate Finance and Economics, 17(1):99–121, 1998.

- Kelejian and Prucha [1999] Harry H Kelejian and Ingmar R Prucha. A generalized moments estimator for the autoregressive parameter in a spatial model. International economic review, 40(2):509–533, 1999.

- Lee [2004] Lung-Fei Lee. Asymptotic distributions of quasi-maximum likelihood estimators for spatial autoregressive models. Econometrica, 72(6):1899–1925, 2004.

- LeSage et al. [1999] James P LeSage et al. Spatial econometrics, 1999.

- Lii and Rosenblatt [1992] Keh-Shin Lii and Murray Rosenblatt. An approximate maximum likelihood estimation for non-gaussian non-minimum phase moving average processes. Journal of Multivariate Analysis, 43(2):272–299, 1992.

- Medeiros et al. [2006] Marcelo C Medeiros, Timo Teräsvirta, and Gianluigi Rech. Building neural network models for time series: a statistical approach. Journal of Forecasting, 25(1):49–75, 2006.

- M.I.Gordin [1969] M.I.Gordin. The central limit theorem for stationary processes. Soviet. Math. Dokl., 10:1174–1176, 1969.

- Pfeifer and Deutrch [1980] Phillip E Pfeifer and Stuart Jay Deutrch. A three-stage iterative procedure for space-time modeling phillip. Technometrics, 22(1):35–47, 1980.

- Rothenberg [1971] Thomas J Rothenberg. Identification in parametric models. Econometrica: Journal of the Econometric Society, pages 577–591, 1971.

- Steele [2004] J Michael Steele. The Cauchy-Schwarz master class: an introduction to the art of mathematical inequalities. Cambridge University Press, 2004.

- Taussky [1949] Olga Taussky. A recurring theorem on determinants. The American Mathematical Monthly, 56(10P1):672–676, 1949.

- Viton [2010] Philip A Viton. Notes on spatial econometric models. City and regional planning, 870(03):9–10, 2010.

- White [1994] Halbert White. Parametric statistical estimation with artificial neural networks: A condensed discussion. From statistics to neural networks: theory and pattern recognition applications, 136:127, 1994.

- White [1996] Halbert White. Estimation, inference and specification analysis. Number 22. Cambridge university press, 1996.

- Yao et al. [2006] Qiwei Yao, Peter J Brockwell, et al. Gaussian maximum likelihood estimation for arma models ii: spatial processes. Bernoulli, 12(3):403–429, 2006.

- Zhu et al. [1997] Ciyou Zhu, Richard H Byrd, Peihuang Lu, and Jorge Nocedal. Algorithm 778: L-bfgs-b: Fortran subroutines for large-scale bound-constrained optimization. ACM Transactions on Mathematical Software (TOMS), 23(4):550–560, 1997.