Is Volatility Rough ?111This work was supported by JSPS KAKENHI Grant Number JP17J04605.

Abstract

Rough volatility models are continuous time stochastic volatility models where the volatility process is driven by a fractional Brownian motion with the Hurst parameter smaller than half, and have attracted much attention since a seminal paper titled “Volatility is rough” was posted on SSRN in 2014 showing that the log realized volatility time series of major stock indices have the same scaling property as such a rough fractional Brownian motion has. We however find by simulations that the impressive approach tends to suggest the same roughness irrespectively whether the volatility is actually rough or not; an overlooked estimation error of latent volatility often results in an illusive scaling property. Motivated by this preliminary finding, here we develop a statistical theory for a continuous time fractional stochastic volatility model to examine whether the Hurst parameter is indeed estimated smaller than half, that is, whether the volatility is really rough. We construct a quasi-likelihood estimator and apply it to realized volatility time series. Our quasi-likelihood is based on the error distribution of the realized volatility and a Whittle-type approximation to the auto-covariance of the log-volatility process. We prove the consistency of our estimator under high frequency asymptotics, and examine by simulations its finite sample performance. Our empirical study suggests that the volatility is indeed rough; actually it is even rougher than considered in the literature.

Keywords Rough volatility, Stochastic volatility, Fractional Brownian motion, Realized variance, Whittle estimator, High frequency data analysis

1 Introduction

Nowadays it is widely recognized that the volatility of an asset price is not a constant but a stochastic process. The property of the process is, however, not very clear because it is not a directly observable process. Even in a simple continuous framework where the volatility process defined through

| (1) |

with an asset price process and a Brownian motion , one can only examine indirectly its properties via a statistic like the realized variance

where is a piecewise constant process which jumps at every sampling time of to the observed value of at the time. In a hypothetical situation where sampling frequency goes to infinity without any measurement error,

| (2) |

in probability; one therefore expects to work as a proxy of the unobservable quantity. Since the high frequency asymptotics does not require any ergodicity or stationarity assumption, it particularly fits the analysis of recent financial market data, where the sampling frequency is really high. The two remarkable empirical properties of daily realized variance time series that were already documented in the earliest work by Andersen et al. [1] are that their unconditional distributions are approximately log Gaussian, and that their auto-covariances decay slowly. Various modifications of the realized variance taking into account market microstructure noise and asset price jumps have been proposed and associated limit theorems have been proven in the literature; see Aït-Sahalia and Jacod [2] for an overview.

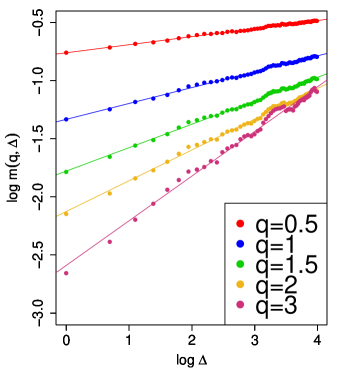

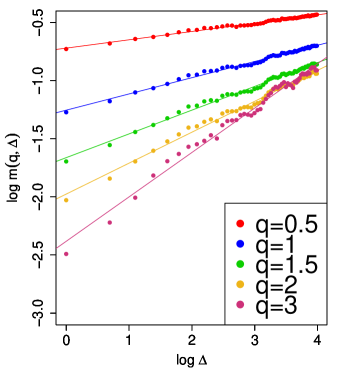

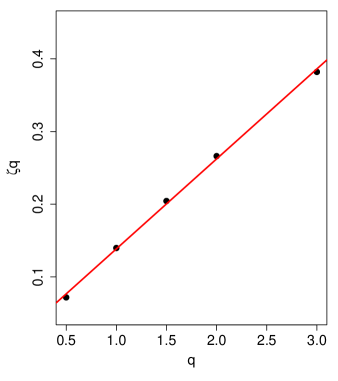

In 2014, an interesting paper, Gatheral et al. [21] titled “Volatility is rough” was posted on SSRN. Since then, it has been so influential in the community of Mathematical Finance that a number of papers777 Antoine Jacquier established and has maintained a website https://sites.google.com/site/roughvol/home as a reference point for the fast growing literature of rough volatility. have already appeared dealing with the so-called rough volatility models. In that paper, the authors looked at the historical volatility proxy data including those from the Oxford-Man realized library888 The Oxford-Man Institute provides daily nonparametric volatility estimates at https://realized.oxford-man.ox.ac.uk . Let be such a volatility proxy as the realized volatility

for a day computed from intraday asset price data, where corresponds to the length of one day. They did a linear regression to find an impressive fit

| (3) |

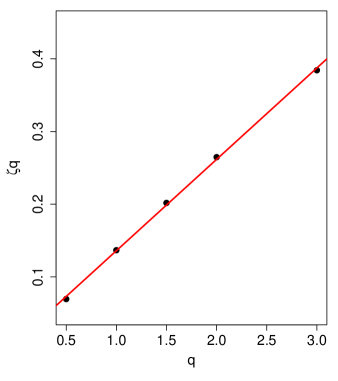

for various values of ; see Figure 1 (left). Then, for the regression coefficients , they did another linear regression to find another impressive fit with ; see Figure 1 (right).

Naively, this scaling property together with the above mentioned stylized fact that the realized variance is approximately log Gaussian suggests a simple dynamics

| (4) |

where is a constant and is a fractional Brownian motion999A fractional Brownian motion is characterized as a continuous centered Gaussian process with a.s., stationary increments and for any , where is the absolute th moment of the standard normal distribution. See Mishura [26] for further detail. The fractional Brownian motion in volatility dynamics does not imply an arbitrage opportunity because the asset price process (1) is a local martingale. with the Hurst parameter . Note that the estimate is not consistent to a widespread belief that the volatility is a process of long memory. Gatheral et al. [21] showed by some simulations that such a “short memory” process pretends to be of long memory. They demonstrated also a good prediction performance of this simple model. The analysis is extended by Bennedsen et al. [5] to a wider set of assets. The estimate means that the volatility path is rougher than semimartingales, and is consistent to a power law for the term structure of implied volatility skew empirically observed in option markets; see [3, 16, 4, 17, 11, 20, 10]. A market microstructural foundation of a rough volatility model is given by El Euch et al. [9].

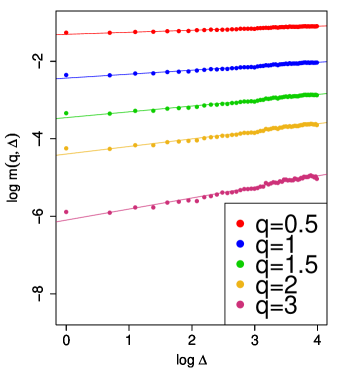

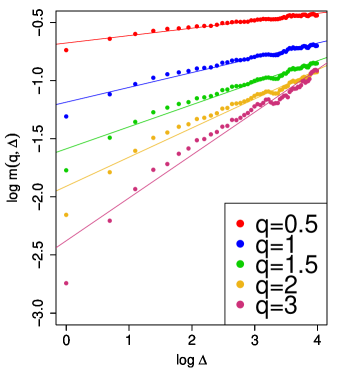

The statement by Gatheral et al. [21] should be, however, understood not as a statistical estimate but as the proposal of a model which is consistent to a number of empirical evidences. In fact, as noted in that paper itself, what they “show here is that we cannot find any evidence against the RFSV 101010Rough Fractional Stochastic Volatility. It is a special case of our model (5) below. model”. Our numerical experiments show that when using 5-minute realized volatility, the linear regression methods in Gatheral et al. [21] or in Bennedsen et al. [5] often give almost perfect fit with irrespectively to the true value of used to simulate paths; see Figure 2 just for one example, and see Westphal [33] for more extensive simulation results.

Figure 2 indicates also that this striking phenomenon is due to the use of a volatility proxy; the approximation error of to results in an illusive scaling property. These observations from simple numerical experiments bring us a question whether the volatility is really rough, which the present paper aims at providing the first step to answer.

This is a question about the smoothness of a hidden process. Therefore any nonparametric spot volatility estimation method or filtering approach in the literature is not helpful here; such an estimator is not meant to preserve the regularity of the hidden path. Further, notice that for continuous time models like (1), most of theoretical studies in the high frequency data analysis so far have assumed that the volatility process is an Itô semimartingale. This is an indispensable assumption because the analysis is typically based on a piecewise constant approximation of , and the path regularity of determines the convergence rate of the approximation error; we refer again to Aït-Sahalia and Jacod [2]. There is a work by Rosenbaum [30] about fractional volatility models including (4); this however assumes a priori and so, is not helpful here to study whether (rough) or not. Other results from high frequency statistics for the model (1) that do not require to be an Itô semimartingale include the most primitive convergence (2), associated central limit theorems by Jacod and Protter [22] and Fukasawa [14, 15], and some limit theorems for the so-called two-scales, or multi-scales realized volatility that takes the market microstructure noise into account; see Aït-Sahalia and Jacod [2].

This paper proposes a novel estimator of the Hurst and diffusion parameters under a fractional volatility model extending (4). Taking the difference between and its proxy into account, we derive an estimation function combining the three ideas: (1) a normal approximation of the log-realized volatility estimation error based on the above mentioned central limit theorem, (2) a local Gaussian approximation of the log-realized variance time series, and (3) a Whittle-type estimation for high frequency self-similar Gaussian models developed in Fukasawa and Takabatake [18]. The asymptotic results in this previous work are, however, not directly applicable here because the observed sequence is not Gaussian but only ”locally Gaussian”. The local Gaussian approximation error causes several technical difficulties in proving the consistency of our estimator. The consistency result in this paper is the first to show that a Whittle-type estimation function is effective to a non-Gaussian model under high frequency asymptotics.

Our empirical study for major stock indices indicates that is even smaller than ; so our tentative answer to the question is affirmative. It is tentative because constructing statistical tests still remains for future research. We remark that a model with formally corresponds to a Gaussian multiplicative chaos [24], or a multifractal process [27, 29]. A framework including those is also a topic for future research.

The paper is organized as follows. We propose a model, construct an estimator and state a consistency theorem in Section 2, examine the finite sample performance of our estimator by simulations in Section 3, and then apply it to the Oxford-Man realized library data to get an estimate of in Section 4. The proofs are deferred to Appendix.

2 Model, Quasi-likelihood Estimator, and its Consistency

2.1 Model

Denote by , , a filtered probability space satisfying the usual condition on which an asset price process and its volatility process are defined. Extending the simplest rough volatility model (4) and a fractional volatility model of Comte and Renault [8], we assume the volatility process to satisfy

| (5) |

where is an unknown -adapted càdlàg (or càglàd) process and is a fractional Brownian motion which is also -adapted. The parameter to be estimated is , where is a compact set of the form and . The true value is denoted by and assumed to be an interior point of . The process is not directly observed and so needs to be estimated from discrete observations of the asset price . As a proxy of the unobservable , we adopt the realized variance with equidistant sampling

and model directly the law of the proxy error for the log realized variance

| (6) |

as an i.i.d. sequence independent of and normally distributed with mean and variance , where is the size of intraday price data used to compute . This specification of the law of is motivated by the following limit theorem.

Theorem 2.1.

Consider a positive sequence and a sequence of natural numbers satisfying and as , and . Assume that a log-asset price process given by

| (7) |

where is a -adapted locally bounded left-continuous process, is a standard -Brownian motion and the volatility process is given in (5). Then we have

where is an i.i.d. standard Gaussian sequence independent of .

Remark 2.2.

We model the volatility dynamics (5) in the business time scale, which means that the time variable in the model evolves only when a market of the asset is open. Therefore, the volatility is freezing when markets are closed. Including volatility jumps remains for future research.

Remark 2.3.

In Theorem 2.1 and in the sequel, we consider the double high frequency limits . For example, corresponding to the 1 day length in a year consisting of 250 business days. For the 5-minute realized variance of market data with 6 opening hours, .

Remark 2.4.

Daily volatility proxy data including the 5-minute realized variance are readily available thanks to the Oxford-Man Institute, while high frequency price data (tick data) are not easily accessible. This motivates us to include a proxy as a model element. Among many volatility proxies, we adopt the realized variance by the following 4 reasons: i) As mentioned in Introduction, the high frequency limit theorems for the realized variance are valid without assuming the volatility to be an Itô semimartingale while those for others are not in general. ii) The asymptotic theory of two-scales and multi-scales realized volatilities assumes the market microstructure noise to be independent of the price and the volatility processes. While this is a popular assumption in the literature, the authors do not consider it enough realistic. iii) The realized variance with modest frequency like 5 minutes, for which the market microstructure noises are negligible but still high frequency limit theorems are valid, is easy to compute from modest frequency price data that are nowadays easily obtained online for free. iv) As shown in Theorem 2.1 above, the realized variance with equidistant sampling admits a particularly simple limit law. Note that the limit law is different for a different proxy and even so for the realized variance with a different sampling scheme; see [14, 15]. It is remarkable that the limit law in Theorem 2.1 does not depend on , which enables us to quantify the size of the approximation error to without knowing the exact value of .

Remark 2.5.

In view of Theorem 2.1, for our model (6), more plausible would be a weaker assumption that the law of is not exactly but only asymptotically i.i.d. Gaussian with mean and variance . We believe that the same quasi-likelihood estimator given below enjoys the same consistency property also under this weaker assumption plus a suitable uniform integrability condition; we however refrain from increasing the complexity of this already technical and lengthy paper.

2.2 Construction of Adapted Whittle Estimator

Here, for a sequence of integers and a positive sequence , we define a quasi-likelihood estimator of the unknown parameter based on the log-realized variance increments

Firstly, we define an estimator of a reparametrized parameter , where , by

| (8) |

where , and and are a periodogram of and an approximate spectral density of with respect to the reparametrized parameter respectively given by

| (9) | |||

where and are given in Appendix D. Note that, for each , the estimator always exists because is compact. Then we define an estimator of the parameter by substituting and into the relation , i.e. an estimator of the original unknown parameter is defined by

| (10) |

We call the estimator as the adapted Whittle estimator through this paper.

Now the idea for (8) is summarized in the following remark.

Remark 2.6.

Our idea to derive the approximate likelihood function (8) is based on a local approximation of by a certain Gaussian vector and the Whittle likelihood of a sequence of the approximate Gaussian vectors. Indeed, the Taylor and the Euler-Maruyama approximations of yield

| (11) |

as , where is an i.i.d. sequence independent of and normally distributed with mean and variance . See Appendix B for a precise statement of the above approximation. Furthermore, we can show that a covariance function of the approximate Gaussian vector is characterized by a spectral density given by

See Appendix D for more detail. Finally, we adopt the Whittle likelihood of the Gaussian vector , which was investigated in Fukasawa and Takabatake [18] under high frequency observations without the noise , as an approximate likelihood of .

Remark 2.7 (Why we need to reparametrize ?).

Under high frequency observations, due to a self-similarity property of fractional Gaussian noises, the effects of and fuse in the limit and the asymptotic Fisher information matrix becomes singular. As a result, it is necessary to reparametrize the parameter in order to obtain a limit theorem of estimator. See Brouste and Fukasawa [7] and Fukasawa and Takabatake [18] for more details.

2.3 Main Theorem

We state our main theorem in this paper.

Theorem 2.8.

Assume the true value is an interior point of and the following three conditions hold:

-

(H.)

and .

-

(H.)

, where .

-

(H.)

.

Then a sequence of estimators is weakly consistent, i.e. in probability as .

The proof of Theorem 2.8 is deferred to Appendix. Here we make comments on technical difficulties for the proof in the following remark.

Remark 2.9.

One of the difficulties is that the parameter space where the estimation function is minimized depends on the asymptotic parameter and . As a result, fails to satisfy the identifiability condition of the parameter in the limit as . In order to circumvent this difficulty, we appropriately rescale the estimator and its estimation function , and attempt to find a function which can identify a rescaled parameter in the limit. Actually, we can find a function , where , which satisfies

| (12) |

where

| (13) | |||

| (14) |

with . Indeed, and are connected by the relation so that the estimator also minimizes

As a result, (12) follows from the one-to-one correspondence between and . Then we can show that and converge to a certain function which can identify the rescaled parameter and to the true value , where denote and , respectively when, at least, the proxy error rapidly vanishes in the sense of (H.3). Furthermore, we can also show that the estimator converges to by using the convergence to . Note that is not a true estimation function because the true value is used in its definition. It plays, however, the similar role to the usual estimation function due to (12). The final remark is that a sequence of rescaled parameter spaces converges to the unbounded set so that several additional cares in the proof are necessary.

3 Numerical Study

In this section, we examine the finite sample performance of the adapted Whittle estimator proposed in Section 2.2 when the log-volatility dynamics is given by a fractional Ornstein-Uhlenbeck process with mean-reverting property. We explain how to simulate a sample path of an asset price process following the fractional volatility model in Section 3.1 and how to implement the adapted Whittle estimation in Section 3.2. We summarize several numerical results in Section 3.3.

3.1 Simulation Method for Asset Price Process

In our numerical studies, we simulate an asset price process whose log-volatility process is given by the fractional Ornstein-Uhlenbeck process, i.e.

| (15) |

by using the Euler-Maruyama approximation, where is a Brownian motion independent of . Here we generate the fractional Brownian motion by using the R-function ”SimulateFGN” given in the R-package ”FGN”. We consider the case of and . For the size of the price data used to compute the realized volatility, we consider three cases: and of which the values are corresponding to those of 5-minute and 1-minute realized volatilities respectively. Moreover, our model parameters are given by , , , and . We generate 100 paths to have 100 samples of the estimator.

3.2 Implementation of Adapted Whittle Estimator

Denote by and for notational simplicity. In order to implement the adapted Whittle estimator, we evaluate the estimation function by

| (16) |

for sufficiently small , where the above integral is calculated using the R-function ”integrate” and additional correction terms and are respectively given by

with and given by

for a sufficiently large and each . The derivation (16) is given in Appendix I. Note that the auto-covariance function can be effectively computed using the fast Fourier transform algorithm. Moreover, we adopt the Paxson approximation of spectral densities for the spectral density used in (16), i.e. is approximated by

with a sufficiently large , where

for and ; see Fukasawa and Takabatake [19] for more detail. We fix , and in our numerical studies.

Finally, we briefly explain how to numerically evaluate the minimizer of the estimation function . In our numerical studies, we use the R-function ”optim” in order to obtain the minimizer and select the option ”L-BFGS-B” as the optimization method of . Then we consider the parameter space and take the true value , where , as the initial value of the optimization for .

3.3 The numerical results

In Table LABEL:Table.Mean.H and Table LABEL:Table.Mean.eta, we give the mean and variance of and respectively. The tables show that when the Hurst parameter is greater than , both of the Hurst and diffusion parameters are estimated reasonably well even with 5-minute realized volatility. In the case of , positive and negative estimation biases are observed for the estimator and respectively. There would be, however, no problem in examining whether the volatility is rough ( or not) because there are few estimation biases in the case of and the size of them in the case of would not be too large. Thus, we conclude that the adapted Whittle estimator gives a reliable answer to our question with data analysis using 5-minute realized volatility. \ctable[botcap,caption=The mean and variance of the adapted Whittle estimator of the Hurst parameter.,label=Table.Mean.H,pos=H,]lrrcrrcrr\FL = 1 = 2 = 3 \NN Mean Variance Mean Variance Mean Variance \ML=0.01\NN 1 min \NN 5 min\ML=0.05\NN 1 min \NN 5 min\ML=0.1\NN 1 min \NN 5 min\ML=0.3\NN 1 min \NN 5 min\ML=0.5\NN 1 min \NN 5 min\ML=0.7\NN 1 min \NN 5 min\LL \ctable[botcap,caption=The mean and variance of the adapted Whittle estimator of the diffusion parameter.,label=Table.Mean.eta,pos=H,]lrrcrrcrr\FL = 1 = 2 = 3 \NN Mean Variance Mean Variance Mean Variance \ML=0.01\NN 1 min \NN 5 min\ML=0.05\NN 1 min \NN 5 min\ML=0.1\NN 1 min \NN 5 min\ML=0.3\NN 1 min \NN 5 min\ML=0.5\NN 1 min \NN 5 min\ML=0.7\NN 1 min \NN 5 min\LL

4 Application to Daily Realized Volatility Data of Stock Indices

In this section, we apply the adapted Whittle estimator to the 5-minute daily realized volatility data for several major stock indices provided by the Oxford-Man realized library. We give the estimated values in Section 4.1 and give an additional discussion in Section 4.2.

4.1 Estimation Results

First of all, we make several remarks on the optimization of the estimation function. In our data analysis, we use the same implementation and optimization methods of the estimation function and the same parameter space mentioned in Section 3.2. Then we calculate the optimal value in the candidates of the estimated values each of which is obtained from the optimization method starting at each initial value with and .

Next, we briefly explain how to compute the value of which is the size of price data used to compute the 5-minute daily realized volatility for each stock index. In our data analysis below, we consider the following 5 stock indices: S&P 500, FTSE 100, Nikkei 225, DAX, Russell 3000. Then we can easily calculate the value of for each stock index since we know the opening hours of the markets are from 9:30 to 16:00 for S&P 500, from 8:00 to 16:30 for FTSE 100, from 9:00 to 11:30 and from 12:30 to 15:00 for Nikkei 225, from 9:00 to 17:40 for DAX, from 9:30 to 16:00 for Russell 3000, see Remark 2.3 for an example of computation of . In the first row of Table LABEL:Table.Data, we summarize the values of for the stock indices. We give the estimated values in Table LABEL:Table.Data. For all indices, the Hurst parameter is estimated between 0.02 and 0.06. Our data analysis suggests , that is, the volatility is indeed rough; it is even rougher than claimed in Gatheral et al. [21] and Bennedsen et al. [5]. It is noteworthy that the estimate is consistent to the calibrated parameters from the option market data in Bayer et al. [4]. \ctable[botcap,caption=Estimated value of the adapted Whittle estimator of major stock indices for the period: 02/01/2008-29/12/2017.,label=Table.Data,pos=H,]lcccccrrcrrcrr\FL SPX 500 FTSE 1000 Nikkei 225 DAX Russell 3000 \ML\NN\NN\LL

4.2 Additional Discussion

In this subsection, we check whether the estimated values given in Section 4.1 are adequate from another aspect. More specifically, we apply the linear regression method of Gatheral et al. [21] to simulated 5-minute realized volatility data for which the Hurst and diffusion parameters are chosen to be the estimated values.

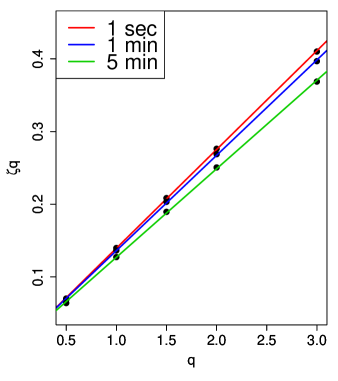

In Figure 3, we compare the linear regression results of SPX and simulated data for the same period of the estimation results given in Table LABEL:Table.Data. Taking into account the estimation bias of the adapted Whittle estimator mentioned in Section 3.3, we used slightly smaller value of the Hurst parameter than its estimated value given in Section 4.1. We obtained similar figures and linear regression coefficients of against from the SPX and simulated 5-minute realized volatilities. In particular, we confirm that the linear regression method of Gatheral et al. [21] does not give a proper estimate of and our estimated value of does not contradict the analysis in Gatheral et al. [21].

5 Conclusion

We have questioned whether the volatility is really rough, that is, whether the Hurst index of the fractional Brownian motion driving the volatility process is smaller than 0.5 or not. We have proposed an estimator for the Hurst and diffusion parameters under a fractional stochastic volatility model (5). We have proved its consistency under high frequency asymptotics. We have also confirmed by numerical simulations its reasonably good performance with finite samples. The estimated Hurst parameters for various stock indices and periods are all smaller than 0.06, indicating that the volatility is rough. This is however a tentative answer to our question; in particular constructing statistical tests remains for future research.

|

|

|

|

References

- [1] Andersen, T.G., Bollerslev, T., Diebold, F.X. and Labys, P. (2001): The Distribution of Realized Exchange Rate Volatility, Journal of the American Statistical Association, 96, 42-55.

- [2] Aït-Sahalia, Y. and Jacod, J. (2014): High-Frequency Financial Econometrics, Princeton University Press.

- [3] Alòs, E., León, J.A., Vives, J. (2007): On the short-time behavior of the implied volatility for jump-diffusion models with stochastic volatility. Finance Stoch. 11, 571-589.

- [4] Bayer, C., Friz, P. and Gatheral, J. (2016): Pricing under rough volatility, Quant. Finance. 16(6), 887-904.

- [5] Bennedsen, M., Lunde, A. and Pakkanen, M. S. (2017): Decoupling the Short- and Long-Term Behavior of Stochastic Volatility, arXiv.

- [6] Billingsley, P. (1968): Convergence of probability measures, John Wiley.

- [7] Brouste, A. and Fukasawa, M. (2018): Local asymptotic normality property for fractional Gaussian noise under high-frequency observations, Ann. Statist. 46, 2045-2061.

- [8] Comte, F. and Renault, E. (1998): Long Memory in Continuous-Time Stochastic Volatility Models, Math. Finance 8(4), 291-323.

- [9] El Euch, O., Fukasawa, M. and Rosenbaum, M. (2018): The microstructual foundations of leverage effect and rough volatility, Finance Stoch. 22, 241-280.

- [10] El Euch,O., Fukasawa, M., Gatheral, J. and Rosenbaum, M. (2019): Short-term at-the-money asymptotics under stochastic volatility models, SIAM J. Finan. Math. 10, 491-511.

- [11] Forde, M. and Zhang, H.(2017): Asymptotics for rough stochastic volatility models, SIAM J. Financial Math. 8, 114-145.

- [12] Fox, R. and Taqqu, M. S. (1986): Large-Sample Properties of Parameter Estimates for Strongly Dependent Stationary Gaussian Time Series, Ann. Statist. 14(2), 517-532.

- [13] Fox, R. and Taqqu, M. S. (1987): Central Limit Theorems for Quadratic Forms in Random Variables having Long-Range Dependence, Probab. Theory Relat. Fields 74(2), 213-240.

- [14] Fukasawa, M. (2010): Realized volatility with stochastic sampling, Stochastic Process. Appl. 120, 829-852.

- [15] Fukasawa, M. (2011): Discretization error of stochastic integrals, Ann. Appl. Probab. 21, 1436-1465.

- [16] Fukasawa, M. (2011): Asymptotic analysis for stochastic volatility: martingale expansion, Finance Stoch. 15, 635-654.

- [17] Fukasawa, M. (2017): Short-time at-the-money skew and rough fractional volatility, Quant. Finance. 17(2), 189-198.

- [18] Fukasawa, M. and Takabatake, T. (2019): Asymptotically efficient estimators for self-similar stationary Gaussian noises under high frequency observations, Bernoulli, forthcoming.

- [19] Fukasawa, M. and Takabatake, T. (2019): Supplement to ”Asymptotically efficient estimators for self-similar stationary Gaussian noises under high frequency observations”, Bernoulli, forthcoming.

- [20] Garnier, J. and Solna, K. (2017): Correction to Black-Scholes formula due to fractional stochastic volatility, SIAM J. Financial Math. 8, 560-588.

- [21] Gatheral, J., Jaisson, T. and Rosenbaum, M. (2018): Volatility is rough, Quant. Finance. 18(6), 933-949.

- [22] Jacod, J. and Protter, P. (1998): Asymptotic error distributions for the Euler methods for stochastic differential equations, Ann. Probab. 26(1), 267-307.

- [23] Jacod, J. and Shiryaev, A. N. (2003): Limit Theorems for Stochastic Processes, 2nd ed., Springer, Berlin.

- [24] Kahane, J.P. (1985): Sur le chaos multiplicatif, Ann. Sci. Math. Québec, 9, no.2, 105-150.

- [25] Karatzas, I. and Shreve, S. E. (1998): Brownian Motion and Stochastic Calculus, second edition, Springer.

- [26] Mishura, Y. (2008): Stochastic Calculus for Fractional Brownian Motion and Related Processes, Springer-Verlag Berlin Heidelberg.

- [27] Muzy, J.F., Delour, J. and Bacry, E. (2000): Modelling fluctuations of financial time series: from cascade process to stochastic volatility model, Eur. Phys. J. B, 17:537.

- [28] Nourdin and Peccati (2012): Normal approximations with Malliavin calculus: From Stein’s method to universality, Cambridge university press, New York.

- [29] Pochart, B. and Bouchaud, J.P. (2002): The skewed multifractal random walk with applications to option smiles, Quantitative Finance, vol. 2, issue 4, 303-314.

- [30] Rosenbaum, M. (2008): Estimation of the volatility persistence in a discretely observed diffusion model, Stochastic Process. Appl. 118, 1434-1462.

- [31] Tudor, C. A. (2013): Analysis of Variations for Self-similar Processes, Springer.

- [32] Velasco, C. and Robinson, P. M. (2000): Whittle Pseudo-Maximum Likelihood Estimation for Nonstationary Time Series, J. Amer. Statist. Assoc. 95(452), 1229-1243.

- [33] Westphal, R. (2017): Empirical Analysis of High-Frequency Financial Data under the Rough Fractional Stochastic Volatility Model, Master thesis, ETH Zurich.

Appendix A Notation

In this section, we summarize notation used throughout the appendix in this paper.

A.1 Notation of Bilinear Form

Denote by the set of the Lebesgue integrable functions on . Let and be an even function. We define a symmetric bilinear form of and with a certain symmetric -matrix by

where denotes the transpose of vector and denotes a symmetric matrix whose -element is given by the th Fourier coefficient of , denoted by , for each , i.e.

In particular, we denote by . Note that

holds, where the periodogram is defined in (9).

A.2 Notation of Stochastic Sequences

Set . Denote by a probability space on which the sequence of observations is defined and by , , the -norm on the probability space. Furthermore, we denote for a discrete-time stochastic process and , and

Recall that

where is an i.i.d. sequence independent of and normally distributed with mean and variance . For each and , denote by , and

where

Note that for each , -a.s. ,

| (17) |

follows from the change of variables and Fubini’s theorem. Moreover, the Hölder continuity of the fractional Brownian motion and yield that for any ,

| (18) |

Appendix B Approximation of Data

The following proposition gives a precise statement of the approximation (11) in Remark 2.6, which follows from a Taylor expansion of around the Gaussian vector under high frequency observations, i.e. .

Proposition B.1.

For any and , there exists a positive random variable , which is independent of the asymptotic parameter , such that

| (19) |

holds -a.s. for sufficiently small .

Note that the lhs of the inequality in Proposition B.1 is dominated as follows:

| (20) | ||||

In the rest of this section, we evaluate the asymptotic order of the three terms in the rhs of (20) when . At first, we treat the first term in (20) in the following lemma.

Lemma B.2.

For any and , there exists a positive random variable , which is independent of the asymptotic parameter , such that

holds -a.s. for sufficiently small .

Proof.

At first, Taylor’s theorem yields that any infinitely differentiable function on an -open ball at the point of is expanded by

for each and . Moreover, if the function and its derivatives of any order are also continuous on , then it holds that

| (21) |

Therefore, using the Hölder continuity of , we can derive the following Taylor’s expansion:

| (22) |

Note that the Hölder continuity property also implies that all reminder terms in the above equality are independent of and if is sufficiently small, see also (21). Therefore, the conclusion follows from taking a difference of both sides of (22). ∎

The second term is also negligible because the following inequality holds.

Lemma B.3.

The following inequality holds:

Finally, we show the negligibility of the third term. In order to achieve this purpose, it suffices to prove that the error between and is negligible for each by using the triangle inequality of . Therefore, we show the following result.

Lemma B.4.

For each with , the following relation holds for any ,

where given by

Proof.

At first, consider the case where , i.e. with . Note that the binomial theorem yields that the integrand of is given by

Then is represented by

where

Therefore, the conclusion when follows from the Hölder continuity of the fractional Brownian motion . Next, we consider the case where . Then the multinomial theorem yield that

where the last sum is taken over all satisfying that there exists such that . As a result, the conclusion when follows from (18) and the conclusion when . ∎

Appendix C Asymptotic Decay of Covariance Function for Stationary Process Associated with Some Functionals of Fractional Brownian Motion

In this section, we will show an asymptotic decay of covariance function for the stationary process appeared in the reminder terms of the Taylor approximation given in Proposition B.1. This result plays a key role in order to prove that the reminder terms are asymptotically negligible in the case where the consistency of the adapted Whittle estimator holds. We will state the key result in Section C.1, several preliminary results used in its proof are summarized in Section C.2 and its proof is given in Section C.3.

C.1 Notation and Statement of Key Result

At first, we prepare notation in order to state a general result for Proposition C.1. Denote by a set of real-valued continuous functions on and by a Borel -algebra on generated by a topology associated with the compact convergence. Let be the distribution of the two-sided standard fractional Brownian motion with the Hurst parameter on , and a continuous shift operator be defined by for . Note that is -invariant, i.e. for each since the fractional Brownian motion enjoys the stationary increments property. Moreover, denotes the canonical process on , i.e. for each . Furthermore, for each , , and compact set , we define a functional by

for , and set a stochastic process for .

Next, let us recall the following definition, e.g. see Tudor [31], p.172.

Definition C.1.

A filter of length and order is a -dimensional vector such that for any with ,

| (23) |

where we use for convenience, and

| (24) |

Moreover, we also call as a filter of length and order if it satisfies (24) for .

Remark C.2.

For any filter of order , the property (23) yield that for any with ,

| (25) |

For a filter and a stochastic process , we define

| (26) |

For example, if we set with , , then is a filter of length and order , and .

Finally, we will state a main result in this section.

Proposition C.3.

Let be a filter of length and order . Then for any with , the stochastic process is stationary and for any , with and ,

| (27) |

As a corollary of Proposition C.3, we can obtain the following result from the self-similarity property of the fractional Brownian motion.

Proposition C.4.

For any , with , the stochastic process is stationary for each and the following relation holds for any :

C.2 Preliminary Results

We summarize several preliminary results used in the proof of Proposition C.3 in this subsection. The first result is proven in the similar way to that in Billingsley [6], p.230-231.

Proposition C.5.

Let with and be a measurable function on . For , we define a functional by

| (28) |

Then the functional is -measurable if is integrable on . Furthermore, if is compact and is continuous, then is also continuous.

Since the shift operator is continuous and is -invariant, we can obtain the following result using Proposition C.5.

Corollary C.6.

Let us consider a functional of the form (28) with a continuous function and a compact set . Then a stochastic process defined by for is continuous and strong stationary on the probability space .

The following result is a consequence of the well-know Wick formula which expresses the higher moments of centered multivariate Gaussian vectors in terms of its second moments, e.g. see Nourdin and Peccati [28]. Given a finite set the number of which is even, we denote by the class of all partitions of such that each block of a partition contains exactly two elements, and recall .

Lemma C.7.

For any and -dimensional centered Gaussian vector ,

where and denotes the subset of whose elements are partitions such that there exists satisfying .

Proof.

Let us consider only the case that both and are even since the other cases are trivial from the Wick formula. Since and are even, the Wick formula yields that

Therefore, the conclusion follows. ∎

C.3 Proof of Proposition C.3

Before proving Proposition C.3, we will show the following two lemmas. Denote by for .

Lemma C.8.

For each , is infinitely differentiable a.e. and, for any and compact set , its th derivative satisfies

Proof.

Fix and a compact set . Since is a distribution of the two-sided standard fractional Brownian motion with the Hurst parameter , we have

As a result, the first assertion is obvious and for any , we obtain

| (29) |

if is sufficiently large, where denotes the sign function defined by

Then the second assertion follows from (29) because Taylor’s theorem yields that for any ,

as uniformly in and for . ∎

Lemma C.9.

Let be a filter of length and order . For any compact set and , with ,

Proof.

By using Lemma C.7 in the case that , and -dimensional centered Gaussian vector given by

it suffices to prove that for any compact set and ,

| (30) |

since the stationary increments property of the fractional Brownian motion implies

for any .

Fix a compact set and recall . Since Taylor’s theorem and Lemma C.8 yield that for any ,

| (31) |

(30) in the case of follows from (25) if we take satisfying . Moreover, the Taylor approximation (31), the multinomial theorem and Lemma C.8 yield that

| (32) |

as , and (25) and Lemma C.8 yield that

| (33) | ||||

Then (30) in the case of follows from (32) and (33) if we take satisfying . Therefore, we finish the proof. ∎

Appendix D Approximating Spectral Density of Data

D.1 Spectral Density of Stationary Gaussian Sequence

Recall that a spectral density of the stationary Gaussian sequence , which is obtained by [18], is characterized by

where

with . The following Lemma shows that the stationary Gaussian sequence satisfies Assumption 1 in [18], see Section 4.2 in [18].

Lemma D.1.

The spectral density satisfies the following relations.

-

For any , , , is a non-negative integrable even function with -periodicity. Moreover, it satisfies that

-

If and are distinct elements of , a set has a positive Lebesgue measure.

-

Let with . There exist constants and for any , there exists a constant , which only depends on , such that the following conditions hold for every .

-

.

-

For any ,

-

D.2 Spectral Density of Stationary Gaussian Sequence

We derive a spectral density of the stationary sequence in this subsection. Since is an i.i.d. sequence, is a MA(1) process and its auto-covariance function is given by

Then its spectral density is given by the Fourier series

Since and are independent, the covariance function of is characterized by

where the spectral density is given by

Appendix E Extension of Some Results in Fox and Taqqu [12, 13]

We will show several extended lemmas and theorem developed in Fox and Taqqu [12, 13] in the case where functions appeared in their results depend on the asymptotic parameter . They can be easily proven in the similar way to the corresponding results in Fox and Taqqu [12, 13]; we will however give their concise proofs in Section E.1 and Section E.2 for convenience. The following two results are extensions of Lemma 4 and Lemma 5 in [12] which show an asymptotic decay of the Fourier coefficient.

Lemma E.1 (cf.Lemma 4 and Lemma 5 in [12]).

Let and . Suppose a sequence of -periodic functions , , satisfies the following conditions:

-

If , is continuously differentiable on for each and

-

If , is integrable and twice continuously differentiable on for each and

Then the sequence of the Fourier coefficients , , satisfies

Lemma E.2.

Suppose a sequence of -periodic functions , , is continuously differentiable on for each and

Then the sequence of the Fourier coefficients , , satisfies

The following result is an extension of Theorem 1 in [13] in the case where functions appeared in Theorem 1 in [13] depend on the asymptotic parameter ; they however have the same asymptotic behavior at the origin as that assumed in Theorem 1 in [13] uniformly to the asymptotic parameter and they uniformly converge to some functions almost everywhere as .

Theorem E.3 (cf. Theorem 1 in [13]).

Let and . Suppose sequences of even functions satisfy the following two conditions:

-

The following relations hold:

-

There exist functions such that

Moreover, the discontinuities of and have the Lebesgue measure .

Under the above conditions, we have

-

If ,

-

If , then for any ,

E.1 Proof of Lemma E.1 and Lemma E.2

Proof of Lemma E.1 in Case (1).

Consider the case of . Let . Since is -periodic, we have

As a result, we obtain

| (34) |

The assumption implies that

By the mean value theorem,

as . Note that is necessary to obtain the last asymptotic behavior. A similar argument shows that

We also have

This completes the proof in the case of . ∎

Proof of Lemma E.1 in Case (2).

Consider the case of . Let . Since the continuity of on implies , the integration by parts formula yields

Moreover, since the derivative is also -periodic from the assumption, the argument in the case (1) can be applied so that we obtain

This completes the proof in the case of . ∎

Proof of Lemma E.2.

The same argument in Lemma E.1 shows the inequality (34). The assumption implies that

By the mean value theorem, the similar argument in Lemma E.1 yields

as . A similar argument shows that

Since is bounded a.e. from the assumption, the same argument in Lemma E.1 yields

This completes the proof of Lemma E.2. ∎

E.2 Proof of Theorem E.3

E.2.1 Outline of Proof of Theorem E.3

Fix and note that

where for and

Following the arguments of Fox and Taqqu [13], we divide into three disjoint sets , , given by

where and

Note that we use the notation for simplicity.

In order to prove the first result of Theorem E.3, it suffices to prove that implies the following three results:

| (35) | |||

| (36) | |||

| (37) |

Remark E.4.

In order to prove (36), we will show that implies

| (38) |

Remark E.5.

In conclusion, the first result of Theorem E.3 will be proven if we show that implies (35), (38) and (40). Moreover, the second result of Theorem E.3 will be proven if we show that implies

| (41) |

These results will be proven in Section E.2.3. In the next subsection, we summarize several preliminaries used in the proof of Theorem E.3 following with Fox and Taqqu [13].

E.2.2 Preliminaries

To state the lemma, introduce the diagonal

Let be the measure on which is concentrated on and satisfies for all . Thus is Lebesgue measure on , normalized so that .

Lemma E.6 (cf. Lemma 7.1. in [13]).

Define a measure on by

| (42) |

for each measurable set . Then converges weakly to as .

For each , define the function

and the function by

where .

Lemma E.7.

There exists a constant such that for each and ,

Proof.

As shown in [13], p.237, we have

for each and . Therefore, the conclusion follows from the assumption. ∎

Proposition E.8 (cf. Proposition 6.1. in [13]).

Let and .

-

a)

If , then for any ,

-

b)

If , then for any ,

Proposition E.9 (cf. Proposition 6.2. in [13]).

Let .

-

a)

If , then

-

b)

If , then for any ,

E.2.3 Proof of Theorem E.3

As mentioned in Fox and Taqqu [13], p.237-238, the results (38), (40) and (41) immediately follow from Proposition 6.1., Proposition 6.2. in [13] in addition to Lemma E.7. In the rest of this section, we will prove (35). Note that

where is given in (42), and set

Since the assumptions imply

and the limit function is continuous a.e. and bounded on for each , see Fox and Taqqu [13], p.237, for more detail, Lemma 7.1. in Fox and Taqqu [13] yields

Therefore, the conclusion follows.

Appendix F Limit Theorems of Quadratic Forms

In this section, we derive several limit theorems of the quadratic form of random sequence which are used in the proof of Proposition G.1 and Proposition G.2 under the following assumptions.

Assumption F.1.

Recall is a compact set of the form and . Let us consider a function , denoted by , be even and integrable on for each and and assume there exist monotonically increasing continuous functions such that the function satisfies the conditions (C.1)-(C.3) below on a restricted parameter space , where be a compact interval of and

Here denotes the true value of , the function is given in Lemma D.1 and we only consider sufficiently small such that , where is the set of all interior points of .

-

(C.)

For each , there exists a function such that

and the discontinuities of has the Lebesgue measure for each .

-

(C.)

For each , the following relations hold:

-

(C.)

For each , is differentiable with respect to and its partial derivatives satisfy

F.1 Basic Properties of Bilinear and Quadratic Forms

At first, we summarize several basic properties of the bilinear form and the quadratic form as functionals on without proofs.

Lemma F.2.

Let . The functionals and on satisfy the following properties.

-

For each , the functional is linear on .

-

For each , the functional is non-decreasing on , i.e. for each ,

where means for a.e. .

-

For each , if satisfies .

-

For each with , if satisfies and the set has a positive Lebesgue measure.

Next lemma is useful to evaluate asymptotic behaviors of bilinear forms.

Lemma F.3.

Proof.

Define a function by

Then it is obvious that the function satisfies all conditions mentioned at the beginning. Moreover, the first inequality immediately follows from Lemma F.2 (2). In the rest of this proof, we will prove the second inequality. Decompose into the following two non-negative functions:

Note that both of and are even functions and satisfy the condition (C.2) from the assumptions of . At first, consider the case where both of and are positive almost everywhere. Since Lemma F.2 (4) yields the matrix is positive definite, Lemma F.2 (1), Schwartz’s inequality of bilinear forms and (43) yield that for each ,

Note that the above inequalities also follows even if or . Therefore, the conclusion follows. ∎

F.2 Pointwise Convergence of Gaussian Quadratic Form

Denote by . In the next lemma, we show a pointwise convergence of the quadratic form of the stationary Gaussian sequence , .

Lemma F.5.

Proof.

The following result is easily proven in the similar way to the proof of Lemma F.5.

F.3 Pointwise Convergence of Quadratic Form of Observation

Denote by . Our goal in this subsection is to prove that the quadratic form of the rescaled observation and that of the Gaussian vector are asymptotically equivalent as . Namely, we show the following result.

Proposition F.7.

Proof.

From Proposition B.1, Corollary F.4 and Lemma F.5, it suffices to prove the following two results for the non-negative function given in Lemma F.3 and each :

-

(R.1)

For any and , the following relation holds:

-

(R.2)

Assume that there exists a positive random variable , which is independent of the asymptotic parameter , such that a random vector satisfies

(46) Then there exists a constant such that the following relation holds:

In the rest of this proof section, we prove (R.1) and (R.2). ∎

Proof of (R.1).

Fix . At first, Chebyshev’s inequality and Lemma F.2 (3) yield that the following inequality holds for any :

| (47) |

where the stationarity property of is used in the last equality, see Proposition C.4. Since the function satisfies the all assumptions in Lemma E.1 and Lemma E.2 with respect to , we obtain

| (48) |

As a result, (48) and Proposition C.4 yield that there exists a constant such that the last quantity of (47) is dominated by

| (49) |

Note that the series in (49) converges because implies . Since the last quantity of (49) is independent of the asymptotic parameter , the conclusion follows as . ∎

Proof of (R.2).

F.4 Uniform Convergence of Quadratic Form of Observations

In this subsection, we prove a uniform convergence of the quadratic form of which is an extension of Corollary F.8 given in the previous subsection.

Proposition F.9.

Proof.

Fix . At first, the compactness of yields that for each , there exists and a finite open covering given by

Then we obtain the following inequality:

| (52) |

Here Corollary F.8 yields that for each , the first term of the last quantity of (52) converges to as . Moreover, the second term of it also converges to as because is uniformly continuous on under the condition (C.3). As a result, it suffices to show that the third term of it is negligible for sufficiently small and large .

Without loss of generality, we assume and

since is uniformly continuous on . Here the condition (C.3) implies

Then the mean value theorem and Schwartz’s inequality yield that for any , and ,

| (53) |

where and is determined by the relation with . Since implies , Lemma F.2 and (53) yield that the third term of the last quantity of (52) is dominated by

| (54) |

where

Moreover, Lemma D.1 and , , yield that there exists a constant , which is independent of , such that the first term of the last quantity of (54) is dominated by

As a result, the first term of the last quantity of (54) converges to as irrespectively to the asymptotic parameter . Moreover, Corollary F.8 yields that for each , the second term of the last quantity of (54) converges to as . Therefore, the conclusion follows. ∎

Appendix G Proof of Theorem 2.8

Main purpose in this section is to give a proof of Theorem 2.8. We prepare notation used in its proof in Section G.1 and several limit theorems of estimation and its score functions are summarized in Section G.2. A key proposition and Theorem 2.8 are proven in Section G.3.

G.1 Notation of Parameter Space and Estimation Function

Recall is a compact set of the form , and with . Following the argument in Velasco and Robinson [32], we divide the parameter space into the following two subsets:

where and . Moreover, we also divide the rescaled parameter space into the following four subsets:

for and , where

Denote by , defined in Section 2.2, and

Note that and for any and , we can show that satisfies the identifiability condition with respect to the parameter on , i.e. for any ,

| (55) |

by using Lemma D.1 (2) and the elementary inequality for any that is actually an equality only when .

G.2 Convergence of Estimation and Its Score Functions

Proposition G.1.

Let be a compact interval of and be an interior point of . Under the conditions , the following uniform convergences on hold for any :

Proof.

Let us consider only the first claim because the second one is proven in the similar way. Here we have

| (56) | ||||

where is defined in (45). Under the assumption and , we obtain

so that the first term of rhs of (56) is negligible as . Note that we have

for any . Let us fix sufficiently small . Then we can show that the second term of rhs of (56) is also negligible as by using Proposition F.9 in the case of the function , and . Therefore, the conclusion follows. ∎

Proposition G.2.

Let be an interior point of . Under the conditions , the score function has the following asymptotic behavior at the point : there exists a constant such that

Proof.

At first, we decompose with into the following three parts:

where

and . Note that Lemma D.1 (3) yields that for any ,

Let us fix sufficiently small . Then we can show that as and as for a certain constant by using Corollary F.6 and Proposition F.7 in the case of the function and respectively. As a result, it suffices to prove that as . Our proof is similar to that of Theorem 2 in Fox and Taqqu [12]. At first, we obtain

| (57) |

Since the functions are -periodic, it is well-known that is the th Fourier coefficient of the convolution defined by

where we use the property that is an even function in the above equality. Moreover, we have

| (58) |

for any from Lemma E.1 and Lemma E.2. As a result, for each , is expanded as the following Fourier series for a.e. :

| (59) |

Note that the continuity of the function on implies the Fourier series expansion (59) also holds for all . In particular, we obtain

| (60) | ||||

From the equalities (57) and (60), we obtain

| (61) |

Then we can show that both terms of (61) are negligible as in the similar way to the proof of Theorem 2 in Fox and Taqqu [12] by using the relation (58). Therefore, the conclusion follows. ∎

G.3 Proof of Theorem 2.8

Before proving Theorem 2.8, we show the following result.

Proposition G.3.

Let be an interior point of . Under the conditions ,

Following the argument of Velasco and Robinson [32], we divide the proof of Proposition G.3 into the following two steps.

Step 1.

Let and . Define a random variable by

Then, for each and , in probability as .

Proof of Step 1.

Step 2.

There exist constants and such that for any and , in probability as .

Proof of Step 2.

Without loss of generality, we can assume and , , are non-empty sets for each and . Note that for any , we have

| (62) |

Since we can show that

the rhs of (62) is dominated by

| (63) |

for any . Then the first term of (63) is negligible as from Proposition G.1 and Step 1. Therefore, it suffices to prove that the other terms are negligible as if we take sufficiently large and small respectively. We divide the proof into the following three lemmas.

Lemma G.4.

For any , there exists a constant such that for any ,

Proof.

Fix . Note that Lemma D.1 and the assumption (H.3) yield that there exist constants , which are independent of and , such that

holds for any and , where is given in (14). Then for any and satisfying , we obtain

| (64) |

where we use the elementary inequality for any in the second inequality. Let , where denotes the boundary of the set . Since the relation holds for any , we can obtain the following inequality from (64):

| (65) |

Moreover, Corollary F.8 in the case of and yields that the third term of the rhs of (65) converges to

in probability as and we obtain the following inequality:

| (66) |

Note that we can make the rhs of (66) arbitrarily large if we take sufficiently small. In particular, if we take such that

holds, then we can obtain the following convergence from (65), (66) and Corollary F.8 again:

| (67) |

Therefore, the conclusion follows from (67). ∎

Lemma G.5.

For any , there exists a constant such that for any ,

Proof.

Fix . Since the inequality

| (68) |

holds for each and we can make the rhs of (68) arbitrarily large if we take sufficiently large, the conclusion immediately follows. ∎

Lemma G.6.

For any , there exists a constant such that for any ,

Proof.

Fix . Without loss of generality, we can assume . At first, we can show that for any ,

| (69) |

where

Then it suffices to prove that there exist a constant such that

| (70) |

Indeed, if we take sufficiently large , the inequality (69) and (70) imply

in the similar way to the proof of Lemma G.4. Therefore, the conclusion immediately follows. Since Lemma D.1 and the assumption (H.3) yield that there exists a constant such that for any , and ,

the similar argument in the proof of Lemma G.4 implies that it suffices to prove that there exist constants and such that

| (71) |

instead of (70). In the rest of this proof, we will show (71). Since Proposition F.9 in the case of the function and yields that

as and we can take sufficiently small satisfying

the convergence (71) follows. Therefore, we finish the proof. ∎

In the rest of this section, we prove the consistency of the estimator as .

Proof of Theorem 2.8.

Note that the following equality holds:

Therefore, it suffices to prove that as from the above equality and the delta method. In the rest of this proof, we attempt to prove the following convergence:

| (72) |

in probability, where . At first, Taylor’s theorem yields that

| (73) |

Here as for any because is a minimizer of and Proposition G.3 yields that converges to the interior point as . Moreover, Proposition G.2 yields that as for a certain constant . As a result, the following convergence holds from (73):

| (74) |

Since is invertible, the convergence (72) follows from (74), Proposition G.1, Proposition G.3 and Slutsky’s theorem. ∎

Appendix H Proof of Theorem 2.1

In this appendix, we give a proof of Theorem 2.1. Actually, we will show the following limit theorem that is a stronger version of Theorem 2.1.

Theorem H.1.

Under the same assumption in Theorem 2.1, a sequence of càdlàg processes

converges in law to a continuous Gaussian process given by , , as , where is a standard Brownian motion independent of .

We recall the martingale functional central limit theorem in Section H.1, a preliminary result used in the proof of Theorem H.1 is summarized in Section H.2 and we prove Theorem H.1 in Section H.3.

H.1 Summary of Martingale Functional Central Limit Theorem

In this subsection, we recall the well-known martingale functional central limit theorem and give its concise proof in the case where local martingales are continuous.

Theorem H.2 (Martingale Functional Central Limit Theorem).

Let be a probability space, be a sequence of filtrations on satisfying the usual conditions and be a sequence of continuous -local martingales. If there exists a continuous function such that for any ,

| (75) |

then a sequence of the -valued random variables converges in law to the time-changed Brownian motion , where is a standard Brownian motion.

Proof.

At first, Dambis-Dubins-Schwarz’s theorem, see Karatzas and Shreve [25], Theorem 3.4.6, yields that there exists a sequence of standard Brownian motions such that for each ,

Note that, since is non-negative and non-decreasing and is continuous, the assumption (75) implies that for any ,

| (76) |

by using Theorem VI.2.15 in Jacod and Shiryaev [23]. Moreover, (76) and the Slutsky’s theorem yield that -valued process converges in law to as , where is a standard Brownian motion. Therefore, the conclusion follows from the above convergence in law and the continuous mapping theorem since defined by is continuous in the similar argument to Billingsley [6], p.145. ∎

Remark H.3.

In Theorem H.2, it is always possible to take a standard Brownian motion independent of .

H.2 Notation and Preliminaries

In this subsection, we summarize notation and a preliminary result used in the proof of Theorem H.1. In the rest of this section, we consider a sequence of filtrations and sequences of -martingales and defined by

Moreover, we set for and for . In the following lemma, we will show that the assumption of the asset price process introduced in Section 2.1 in the original article implies the similar conditions introduced in Fukasawa [14]. Note that, by localization argument, we can also assume without loss of generality that is bounded and so the volatility process is the Hölder-continuous.

Lemma H.4.

For any and , as ,

Proof.

Since we have

the binomial theorem yields that for any ,

| (77) |

Since the Brownian motion enjoys stationary and independent increments properties, we have

| (78) |

for any . Moreover, the Burkholder-Davis-Gundy inequality and the Hölder-continuity of yield that for any , there exists a constant such that for each ,

| (79) | ||||

as . Then the conclusion follows from (78) and (79) by using Cauchy-Schwarz’s inequality to the rhs of (77). ∎

H.3 Proof of Theorem H.1

Before proving Theorem H.1, we will show the following theorem.

Theorem H.5.

Consider sequences of continuous -local martingales and continuous stochastic processes respectively given by

Then a sequence of the -valued random variables given by , , converges in law to the continuous Gaussian process defined in Theorem H.1.

Proof.

Since we have

Itô’s formula yields that

Since Taylor’s theorem yields that

we can decompose into the following three parts:

| (80) |

for each , where a sequence of continuous -local martingales and continuous process are given by

First of all, we will show that

| (81) |

Then Theorem H.2 yields that, in order to prove (81), it suffices to prove that for each ,

| (82) |

By Itô’s formula, we have

where

Since Lemma H.4 and the Burkholder-Davis-Gundy inequality yield that as ,

hold, the convergence (82) follows from Lemma 2.3. in [14] and the above two convergences. Therefore, the convergence (81) follows.

In the rest of this proof, we would like to show that the second and third terms of (80) are negligible as . Namely, we will prove the following three convergences: for any and ,

| (83) | |||

| (84) | |||

| (85) |

Indeed, if (83), (84) and (85) hold, then the continuous processes appeared in the second and third terms of (80) converge in probability to the function that is identically zero as so that the convergence of follows from (81) and the continuous mapping theorem.

At first, (83) immediately follows from the Hölder-continuity of the volatility process . Next, we will prove (84). In the similar argument to the first term of (80), we can show that

| (86) |

Then (84) follows from (86) and Doob’s inequality. Finally, we will prove (85). By Itô’s formula, we have

where

Since Lemma H.4 and the Burkholder-Davis-Gundy inequality yield

the convergence (85) follows from an easy modification of Lemma 2.3. in [14] and the above two convergences. Therefore, we finish the proof. ∎

Let us embed the realized variance into a continuous-time stochastic process

Then we can obtain the following limit theorem.

Theorem H.6.

A sequence of càdlàg processes given by

converges in law to the continuous Gaussian process defined in Theorem H.1.

Proof.

Note that we have

where , . By using Lemma H.4, we can show that

uniformly in for any in the similar way to the proof of Lemma 3.9. and Theorem 3.10. in [14] respectively. Then we obtain

as uniformly in for any . Therefore, the conclusion follows from Theorem H.5 and the continuous mapping theorem since as uniformly in for any . ∎

Appendix I Approximate Formula of Estimation Function

In this appendix, we derive the approximate formula of the estimation function (15) in the original article. Since the spectral density and the periodogram are symmetric with respect to , we have

for any , where

In the rest of this subsection, we will show and as . At first, we consider the first approximation. Note that the Taylor expansion yields that

| (87) |

Then we obtain the first approximation from the Taylor expansion as as follows:

Next we consider the second approximation. Since is an even function, is represented by

where

Since the Taylor expansion as yields that

| (88) | ||||

| (89) |

we obtain the second approximation when the series in (89) is truncated after finite terms. Note that the truncation error of the Taylor expansion in (88) is dominated as follows:

for any and . As a result, for fixed , we can make the truncation error arbitrary small uniformly with respect to as is taken sufficiently large even in the case of the finite sample.