OPRE-2017-09-472.R1

Ma and Simchi-Levi

Tight Weight-dependent Competitive Ratios for Online Matching, Assortment, and Pricing

Algorithms for Online Matching, Assortment, and Pricing with Tight Weight-dependent Competitive Ratios

Will Ma \AFFOperations Research Center, Massachusetts Institute of Technology, Cambridge, MA 02139, \EMAILwillma@mit.edu \AUTHORDavid Simchi-Levi \AFFInstitute for Data, Systems, and Society, Department of Civil and Environmental Engineering, and Operations Research Center, Massachusetts Institute of Technology, Cambridge, MA 02139, \EMAILdslevi@mit.edu \ABSTRACT

Motivated by the dynamic assortment offerings and item pricings occurring in e-commerce, we study a general problem of allocating finite inventories to heterogeneous customers arriving sequentially. We analyze this problem under the framework of competitive analysis, where the sequence of customers is unknown and does not necessarily follow any pattern. Previous work in this area, studying online matching, advertising, and assortment problems, has focused on the case where each item can only be sold at a single price, resulting in algorithms which achieve the best-possible competitive ratio of 1-1/e.

In this paper, we extend all of these results to allow for items having multiple feasible prices. Our algorithms achieve the best-possible weight-dependent competitive ratios, which depend on the sets of feasible prices given in advance. Our algorithms are also simple and intuitive; they are based on constructing a class of universal “value functions” which integrate the selection of items and prices offered.

Finally, we test our algorithms on the publicly-available hotel data set of Bodea et al. (2009), where there are multiple items (hotel rooms) each with multiple prices (fares at which the room could be sold). We find that applying our algorithms, as a “hybrid” with algorithms which attempt to forecast and learn the future transactions, results in the best performance.

1 Introduction

In this paper we study a general online resource allocation problem, motivated by dynamic assortment and pricing in revenue management. Consider an airline website selling parallel flights, i.e. different flights which depart from the same origin to the same destination around the same time. Each flight corresponds to an item which could be sold, and its seat capacity corresponds to the unreplenishable starting inventory of that item. Each flight has multiple fare classes (e.g. Economy, Basic Economy) which correspond to prices at which that item could be sold. We will refer to this collection of initial information (items, inventories, prices) as the setup.

Over the booking horizon, heterogeneous customers sequentially arrive to the airline’s website. We assume that the airline can reliably estimate each customer’s choice probabilities from historical data. That is, upon a customer’s arrival, for any combination of items and prices that could be shown, the stochastic distribution of how the customer would choose among those items/prices is given. The customer is assumed to choose at most one item and one price, as the flights are parallel. The customer could also choose to make no purchase. Given the choice probabilities, the airline selects an assortment of items and corresponding prices to show the customer, where items with zero remaining inventory cannot be shown. The customer’s decision is realized immediately afterward, and if she makes a purchase, then the airline earns the corresponding price as revenue, and depletes one unit of inventory of the corresponding item. The airline wants to maximize its cumulative revenue earned before the booking horizon is over (or all the flights are full).

We study this problem under the framework of competitive analysis, where the sequence of customers to arrive over the booking horizon is unknown and does not necessarily follow any pattern. Instead, the airline seeks to have a good relative performance on all possible sequences. It offers assortments and pricings using a (possibly randomized) online algorithm, which can make decisions based on only the setup and the arrival sequence/purchase realizations seen so far. For , the online algorithm is said to be -competitive, or achieve a competitive ratio of , if

| (1) |

where denotes the algorithm’s expected revenue on arrival sequence , and denotes the value of an optimum which knows the entirety of in advance. In this paper, we will allow the competitive ratio guarantee to be setup-dependent; that is, the value of in (1) can be a function of the items, their starting inventories, and prices. We are interested in online algorithms which achieve the best-possible competitive ratios for various families of setups.

1.1 Overview of Result, and Relation to Previous Results

For setups where each item has a single fare class, the competitive ratio of the above problem has been analyzed extensively under many streams of literature, which we review below.

-

1.

Online Assortment: If each item has a single price, then the above problem formulation is exactly the online assortment problem of Golrezaei et al. (2014). The authors use an algorithm which judiciously “balances” between offering different items, based on their remaining inventory levels. They show, among other results, that their algorithm is -competitive in the asymptotic regime. That is, their value of in (1) depends on the smallest starting inventory amount in the setup, and approaches as all starting inventories approach . Without large starting inventories, this problem has also been studied in the special case where all offered assortments must have size 1, in which case it becomes the online matching with stochastic rewards problem (Mehta and Panigrahi 2012, Mehta et al. 2014).

-

2.

Online Vertex-weighted Matching: Consider the special case of the problem where the outcome of any assortment offering is deterministic, and given upon the customer’s arrival. In this case, we know the maximum (possibly 0) a customer is willing to pay for each item, and our decision can be reduced to selecting an item to offer to the customer at her maximum-willingness-to-pay (we can also offer no item). We will refer to this problem as the deterministic case; it can be viewed as an online weighted matching problem.

If each item is restricted to have a single price, then we get the online vertex-weighted matching problem of Aggarwal et al. (2011). The authors develop an algorithm which randomly “ranks” the items and matches higher-ranked items first, and show that it is -competitive. Their result generalizes the classical result of Karp et al. (1990) for the unweighted online bipartite matching problem (where all items have the same price).

-

3.

Adwords: The Adwords problem of Mehta et al. (2007) is central to online advertising and features budget-constrained bidders instead of inventory-constrained items. It also uses the idea of “balancing”, between the bidders’ budgets in this case, to achieve -competitiveness in an asymptotic small bids regime. Although its budget constraints are not directly captured by our model, we show that in this asymptotic regime, the Adwords problem corresponds to a version of our problem where each item has a single price (despite each bidder having multiple bid values—we explain the reduction in Section 6).

Our main contribution, motivated by the parallel flights problem, is extending all of the preceding results to setups where items could have multiple prices, that are known in advance. Note that such a setup also arises naturally from models where the customers have been classified into “types”, and there is a “match quality” score between each item and each type—in that case, the price set of an item consists of the item’s possible match scores.

However, allowing for multiple prices per item runs into a known impossibility result: even in the deterministic case, which corresponds to the aforementioned online weighted matching problem, it is not possible to provide a non-zero competitive ratio guarantee which holds for every multi-price setup (the way was a constant guarantee for every single-price setup). This is because the moment we commit to a match, unboundedly larger edge weights can arrive afterward—see Mehta (2013, Ch. 7). Therefore, previous work in online weighted matching has assumed that matches can be freely disposed if larger weights arrive later (Feldman et al. 2009), or that arrivals appear in a random order (Kesselheim et al. 2013).

In our paper, we instead assume that the price sets (i.e., the possible edge weights) are known in advance, and derive weight-dependent competitive ratio guarantees, where our value of in (1) will depend on the setup; specifically, the price sets of the items. Our algorithms also make use of the knowledge of the price sets. Our competitive ratio results are based on establishing a universal mapping from price sets to ratios in , such that:

-

1.

Our Multi-price Balance algorithm, which extends the existing “inventory balancing” algorithms, is -competitive in the asymptotic regime;

-

2.

Our Multi-price Ranking algorithm, which extends the existing “randomized ranking” algorithm, is -competitive in the deterministic case;

-

3.

Any (deterministic or randomized) algorithm can be at most -competitive for the family of setups with price sets chosen from , even if we restrict the setups to have asymptotic starting inventories and/or deterministic arrival sequences.

For any singleton price set , , and hence if , then our results recover existing results: the -competitiveness of inventory balancing in the asymptotic regime, the -competitiveness of randomized ranking in the deterministic case, and a single counterexample which shows that both of these algorithms are tight. approaches 0 if contains both a large number of prices and large ratios between its prices, so our statement 3 also recovers the known impossibility result.

1.2 A Bid Price Algorithm when Items have Multiple Prices

We illustrate the necessity for our new algorithms by comparing Multi-price Balance to the existing inventory balancing algorithm of Golrezaei et al. (2014); similar arguments can be made in comparisons to the existing online vertex-weighted matching and Adwords algorithms.

Suppose there are parallel flights, whose seats have the same two fare classes: a lower price of , and a higher price of . At any point in time, for each flight , let denote the fraction its starting inventory which has been sold. The algorithm of Golrezaei et al. (2014) would associate each fare class of each flight with a “pseudorevenue” equal to

| (2) |

where is a decreasing function that penalizes the revenues associated with flights which are almost full. The algorithm then offers, to each customer, the assortment which maximizes the expected pseudorevenue of the (flight, fare)-combination that the customer would choose.

In (2), although will disincentivize the offering of a flight whose is large, the algorithm has no way of setting a “booking limit”—preventing sales at the lower price while still allowing sales at price . Given a stream of customers who are only interested in the lower price, the algorithm would sell all the seats at price , without realizing the opportunity cost of it gave up. Since this could happen to every flight , the algorithm’s competitiveness is at most .

To improve upon this, our algorithm must implement some notion of “booking limits”. As a result, we define the pseudorevenue associated with fare class of flight to be

| (3) |

where is an increasing function that sets a cost to selling flights which are almost full. Multi-price Balance uses the same idea of maximizing expected pseudorevenue, with the modification that it rejects the customer outright if the maximum expected pseudorevenue is non-positive.

The exact form of function for this example is shown in Figure 1. Note that for a flight , if the fraction sold is between and 1, then the pseudorevenue (3) will be negative for the lower price of 150 and positive for the higher price 450, producing a desirable “booking limit” at . Other than that, still produces a continuously-increasing cost as increases from 0 to 1, allowing us to trade off between offering the different flights based on their values of .

In (3), can be interpreted as a bid price, or the value placed on one unit of item ’s inventory. Optimizing based on bid prices is a classical idea in revenue management (see Talluri and Van Ryzin (2006), Liu and Van Ryzin (2008)), where typically the bid prices are computed using a large LP which encompasses both the inventories and the forecasted distribution of future customers. However, since we make no assumptions about future customers, our bid prices are based on only the remaining inventories, like the balance algorithms from competitive analysis.

1.3 Our Competitive Ratio Guarantees

In general, for any price set we define a construction which we call a value function. In a setup, if denotes the price sets of the items, then Multi-price Balance defines the pseudorevenues of each item using value function in expression (3). Our Multi-price Ranking algorithm uses the same value functions, but applies them to a “random seed” instead.

Note that for each item , the construction of from is universal in that it does not depend on other parameters in the setup, e.g. the price sets of the other items. Our mapping from price sets to ratios was also universal. The fact that separately determining the value function for each item leads to the best-possible competitive ratio of is, in our opinion, very surprising—see also the discussions in Devanur and Jain (2012), Devanur et al. (2013). For any , our exact derivation of and comes from the solution of a differential equation, which arises from a primal-dual analysis based on Buchbinder et al. (2007).

When , with , value function , and hence our notion of pseudorevenue in (3) coincides with the existing notion in (2). If each item has a single price, then our algorithms will coincide with the existing ones.

We now give a flavor of our new results with . Let , where is the ratio from high price to low price. The value function depends on (see Figure 1 for an example with ). For any , equals

| (4) |

and the booking limit implied by (i.e. the corresponding value of in Figure 1) equals . We note that this is different from the booking limit of derived by Ball and Queyranne (2009), which is optimal for selling a single item whose price set is . For any value of , the booking limit implied by our function is greater than , which means that our algorithm is willing to sell a greater fraction of units at the lower price. The intuitive explanation of this is that with multiple items, there is less upside to reserving inventory for higher prices, because the reserved units still have to compete with other items to be sold.

The smallest guarantee of in this diagram is also implied by the results of Chen et al. (2016).

If every item has two prices and denotes the maximum ratio of an item’s high price to low price, then equals because is decreasing. Also letting denote the minimum starting inventory among the items, we plot, in Figure 2, our competitive ratio guarantees for Multi-price Balance and Multi-price Ranking as both and range over . This guarantee equals in the asymptotic regime or deterministic case, which is tight.

The lower bound on the competitive ratio guarantee when each item has at most two prices occurs as , in which case . This is greater than the naive bound of , which would arise from randomly choosing between 2 prices and then using a -competitive algorithm on the chosen prices. Thus, using a function like to integrate the selection of prices with the allocation across items is necessary for achieving the optimal competitive ratio.

Our guarantees may not be tight in the non-asymptotic, non-deterministic setting, which is an important open problem even in the single-price case (Devanur et al. 2013). Nonetheless, as increases, our bounds sharply approach the tight guarantee from the asymptotic regime. In the single-price case, our bound is a factor of from the tight guarantee of , improving the previous-best-known dependence on from Golrezaei et al. (2014).

1.4 Simulations on Hotel Data Set of Bodea et al. (2009)

We first summarize the general benefits of applying the algorithms from competitive analysis. In contrast to traditional algorithms, which optimize based on a forecast of future demand, or attempt to learn the demand, competitive algorithms guarantee some performance ratio under the worst case, and operate without any demand information. Most immediately, they are useful for products with highly unpredictable demand (Ball and Queyranne 2009, Lan et al. 2008), or for initializing new products with no historical sales data (Van Ryzin and McGill 2000). Second, by eschewing stochastic processes for generating demand, competitive algorithms are usually simple and flexible, leading to clean insights about the problem (Borodin and El-Yaniv 2005). Third, past research has reported on cases where competitive algorithms perform well in practice (Feldman et al. 2010), or on average in numerical experiments (Golrezaei et al. 2014, Chen et al. 2016).

In Section 7, we run simulations on the publicly-accessible hotel data set of Bodea et al. (2009). We use the product availability information to estimate customer choice models, and use the sequence of transactions as the sequence of arrivals. This leads to an online assortment problem like in Golrezaei et al. (2014), but with multiple prices (advance-purchase rate, rack rate, etc.) for each item (King room, Two-double room, etc.). We compare the performance of our Multi-price Balance algorithm to various benchmarks and forecasting algorithms.

The main conclusion from our simulations is that the best performance is achieved by hybrid algorithms (see Golrezaei et al. (2014)). These are forecasting-based algorithms which continuously reference our forecast-independent value functions , and adjust their decisions accordingly. Although this only changes a small fraction () of decisions, these tend to be the decisions where the forecast is being most overconfident. Therefore, not only does this boost average performance, it drastically reduces the variance in performance caused when the forecast is wrong.

1.5 Other Related Work

We briefly mention some papers which study online resource allocation problems under other arrival models or performance metrics.

When a stochastic process generating the arrivals is given as input, the resulting optimization problem is generally still computationally intractable. Nonetheless, many effective heuristics have been proposed under various models of online resource allocation (Zhang and Cooper 2005, Jasin and Kumar 2012, Ciocan and Farias 2012, Chen and Farias 2013). These heuristics can earn of the LP optimum in general settings (Chan and Farias 2009, Wang et al. 2015). Manshadi et al. (2012) derive an improved performance ratio when the stochastic process is IID.

Competitive/approximation ratios both analyze the fraction of optimum achieved by an algorithm, but online resource allocation problems are also often analyzed under the regret metric, which measures the difference from optimum. This work often focuses on learning some unknown underlying stochastic model (Badanidiyuru et al. 2013, Ferreira et al. 2016). On the other hand, queueing-theoretic analyses have also been performed given a known stochastic model (Reiman and Wang 2008). Unlike in competitive analysis, all of these papers tend to focus on asymptotic performance as the number of customers grows to infinity. Finally, a recent metric which has been introduced is regret ratio (Zhang et al. 2016). For a comprehensive review of different metrics under different models of demand (for a single item), we refer to Araman and Caldentey (2011).

1.6 Organization of Paper

Throughout Sections 2–5 of this paper, we analyze a simplified model where each customer is offered a single item at a single price (but her purchase decision is still stochastic). This avoids the complexities of assortment optimization while still capturing our main techniques. In Section 6, we discuss the generalizations to the assortment and Adwords settings. In Section 7, we display the results of our simulations on the hotel data set.

2 Problem Definition, Algorithm Sketch, and Theorem Statements

A firm is selling different items. Each item 111For a general positive integer , let denote the set . starts with a fixed inventory of units, and could be offered at any price in its price set . Throughout most of this paper, we assume that each consists of discrete prices satisfying . We will refer to as “price of item ”, and define . We extend to the case where is a continuum of prices in Appendix 13.1.

There are customers arriving sequentially. Upon the arrival of customer , the firm is given , the probability222 If is a continuum of prices, then we need to assume that the purchase probabilities can be input compactly. There are many parametric models for doing so, e.g. linear demand, where the purchase probability is for prices lying in an interval . that customer would buy item at price , for all and .333 These probabilities can be 0 for items the customer is not interested in, or prices that are too high. The firm chooses up to one of the items with remaining inventory and offers it to customer , at any price . The customer accepts the offer with probability , in which case the firm earns revenue , and the inventory of item is decremented by 1.

We divide the elements defined above into:

-

1.

The Setup , consisting of parameters known at the start: ; and

-

2.

The Arrival sequence , consisting of parameters revealed over time: .

An online algorithm must decide, on any setup , what to offer to each customer . This decision can be based on only the setup , the past arrivals/purchase realizations, and the purchase probabilities of the present customer ; the online algorithm does not know the purchase probabilities associated with future customers. For an online algorithm, let denote the revenue earned on a run on setup with arrival sequence , which is a random variable with respect to the customers’ purchase decisions as well, as any randomness in the algorithm’s decisions.

Meanwhile, we can write the following LP for setup with arrival sequence :

| (5a) | |||||

| (5b) | |||||

| (5c) | |||||

| (5d) | |||||

LP (5) encapsulates the execution of any algorithm, which could make full use of the arrival sequence at the start, on setup — represents the unconditional probability of the algorithm offering item at price to customer ; (5b) enforces that starting inventories are respected; (5c) enforces that at most one combination of item and price is offered to each customer; and objective function (5a) represents the expected revenue earned by the algorithm. Let denote its optimal objective value. Note that although knows the arrival sequence in advance, it does not know the outcomes of the customers’ potential purchase decisions.

For a fixed online algorithm and any setup , the online algorithm is said to achieve a competitive ratio of on , if

| (6) |

In this paper, we will allow the competitive ratio guarantee to depend on parameters in the setup , and derive results that hold for any .

Definition (6) provides a guarantee on relative to any algorithm which could have been possible, due to the following standard result.

Lemma 2.1

is an upper bound on the expected revenue of any algorithm, which could make full use of the arrival information at the start, on setup with arrival sequence .

The proof of Lemma 2.1 is deferred to Appendix 9. The definition of based on the LP is standard in problems with both stochastic purchase realizations and arbitrary customer arrivals—we refer to Mehta and Panigrahi (2012), Golrezaei et al. (2014) for its justification.

In the deterministic case of our problem, every is 0 or 1. The problem can be simplified by letting , with if the set is empty, for all and . We say that item is assigned to customer to indicate that is offered to customer at price , which results in a sale; there is no reason to offer any other price. Customer can also be rejected, e.g. if is low for every . In the deterministic case, the LP (5) is integral, so is equal to the revenue of the best algorithm knowing the arrival sequence at the start.

2.1 Construction of Value Function for a Price Set

In this section, we specify a value function and a number , for any price set consisting of discrete prices with . The derivation of and , as well as the case where is a continuum of prices, are deferred to Appendix 13.

Consider an item with price set . Following the description from Section 1.2, we will interpret to be a function of , which is the fraction of the item’s starting inventory which has been sold. specifies the value that should be placed on one unit of the item’s inventory, when its fraction sold is .

First we define “booking limits” , which are the fractions of starting inventory “reserved” for the respective fares , via the following proposition.

Proposition 2.2

Let be any numbers satisfying . Then there is a unique set of positive values which sum to 1 and satisfy

| (7) |

There is also a different, unique set of positive values which sum to 1 and satisfy

| (8) |

The proof of Proposition 2.2 is elementary and deferred to Appendix 9. While finding the exact solution to (7) requires finding the roots of a degree- polynomial, a numerical solution can easily be found via bisection search.

Proposition 2.2 contrasts in (7) with the booking limits in (8) originally derived by Ball and Queyranne (2009), which are optimal for selling a single item with price set . With , we can now complete the definition of .

Definition 2.3

Define the following, based on the values of from Proposition 2.2:

-

•

: the sum , defined for all (note that and );

-

•

: a function on , where is the unique for which (note that for ; we define to be ).

The value function for price set is then defined over by:

| (9) |

An example of for was plotted in the Introduction, in Figure 1. In general, is continuously increasing and piecewise-convex over segments of lengths , separated by segment borders . For each , reaches the value of at .

Definition 2.4

For price set , let and , where and are the values from Proposition 2.2.

Our competitive ratio guarantees will be based on the functions and . It can be checked that maps a price set to and maps the price set to , where is the number of prices in . When , our value function is , which can be related back to the existing multiplicative “penalty functions” from the single-price case.

2.2 Sketch of our MULTI-PRICE BALANCE and MULTI-PRICE RANKING Algorithms

Having defined the value function for an arbitrary price set , we now sketch our algorithms.

We start with Multi-price Ranking, which is simpler. It assumes that for all , which does not lose generality since an item that starts with multiple units of inventory can be transformed into multiple disparate items. At the start, the algorithm fixes for each item a random seed , drawn independently and uniformly from . It then treats as the bid price for the single unit of item : it offers to each customer the available item and price maximizing the expected pseudorevenue, .

Multi-price Ranking hedges against the ambiguity in customer arrivals using randomness, which is standard in competitive analysis. The random seed determines the random minimum price at which the algorithm is willing to sell item , as well as a random priority for selling when the algorithm is choosing between multiple items.

We now sketch Multi-price Balance, which updates the bid price of each item based on the fraction of its units which has been sold. However, the algorithm does not directly use as the bid price of item , because would always be a multiple of , while the booking limits and segment borders which is based on may not be multiples of . Instead, the algorithm first uses a randomized procedure for rounding the booking limits in to multiples of .

Specifically, at the start, the algorithm fixes for each item random segment borders , which are multiples of satisfying . We note that having is possible (and guaranteed to happen if ), in which case the ’th segment has length zero. In either case, the realizations of imply a random value function for item , which is a perturbation of . Function is defined on , since the fraction sold is always a multiple of , and also satisfies . At any point in time, Multi-price Balance treats as the bid price for item : it offers to each customer the item and price maximizing

| (10) |

In (10), the definition of pseudorevenue at price is instead of . This is because we want the expected pseudorevenue to be 0 when . In general, the realized will be close to , so that . In the asymptotic regime with , is deterministically initialized to . However, for small , optimizing a randomized procedure for initializing (based on as well as ) instead of having the deterministic (which is based on only ) allows us to achieve a greater competitive ratio.

2.3 Statements of Our Results

Our competitive ratio results are based on the universal functions and from Definition 2.4, which assign a number to every price set .

Theorem 2.5

For any setup, with price sets denoted by and starting inventories denoted by , Multi-price Balance achieves a competitive ratio of , where for each item , is lower-bounded by all of: (i) ; (ii) ; and (iii) if .

Corollary 2.6

Multi-price Balance achieves a competitive ratio approaching as each starting inventory approaches .

Corollary 2.7

Suppose that each item has at most discrete prices and at least units of starting inventory. Then the competitive ratio achieved by Multi-price Balance is lower-bounded by , which approaches as approaches .

Theorem 2.5 is our general result, where for each , is determined by the randomized procedure used to initialize the value function for item .

Lower bound (i) on is attained by a randomized procedure which perturbs the “ideal” value function to define . This perturbation loses a factor of in the denominator, which decreases to 1 as , resulting in Corollary 2.6. Corollary 2.7 is a further simplification of the bound presented, using the fact that . Meanwhile, lower bound (ii) is attained by solving an optimization problem for the best randomized procedure to define when ; this procedure is not based on perturbing and the bound is based on instead of . Finally, lower bound (iii) is an improvement of (i) in the single-price case, where we have gained a factor of in the denominator. It simplifies and improves the dependence on from Golrezaei et al. (2014).

Multi-price Balance is formalized and Theorem 2.5 is proven in Section 3. We explain the ideas behind our primal-dual analysis, why we need random value functions, and how to overcome the ensuing analytical challenges.

Theorem 2.8

For any setup in the deterministic case, Multi-price Ranking achieves a competitive ratio of .

Multi-price Ranking is formalized and Theorem 2.8 is proven in Section 4. Our analysis builds upon the framework of Devanur et al. (2013) and extends it to handle multiple prices.

Theorem 2.9

Let be any positive integer. Let be any price set consisting of prices with . Then there exists a setup where each item has starting inventory and price set , along with a distribution over arrival sequences falling in the deterministic case, for which no online algorithm can have expected revenue greater than .

Theorem 2.9 is proven in Section 5. Since the starting inventory can be made arbitrarily large and the arrival sequences fall in the deterministic case, Theorem 2.9 implies that the competitive ratio guarantees in Corollary 2.6 and Theorem 2.8 are tight, via Yao’s minimax principle (Yao 1977).

Our counterexample is based on those from Karp et al. (1990), Mehta et al. (2007), Golrezaei et al. (2014), where a large number of customers arrive according to a random permutation chosen uniformly from all possible permutations. In our case however, the customers are further split into “phases”, where the customers in phase are willing to pay for any of the items they are interested in. The phases lengths are optimized by an adversary to minimize the competitive ratio.

Interestingly, on the existing counterexamples, the random permutation implies that all (reasonable) algorithms are indifferent and have the same performance. By contrast, on our counterexample with the adversarially-optimized phase lengths, there is a unique optimal algorithm given the distribution over arrival sequences . When , this unique algorithms turns out to be our Multi-price Balance and Multi-price Ranking algorithms, which coalesce to the same algorithm in the asymptotic regime. This coalescence phenomenon has been noted in the single-price case as well by Aggarwal et al. (2011).

Proposition 2.10

For prices satisfying , from which and are defined according to Proposition 2.2, the following inequalities hold:

| (11) | |||

| (12) | |||

| (13) |

Finally, Proposition 2.10, which is proven in Appendix 9, puts our tight competitive ratio of into perspective. is the existing tight competitive ratio for a single item, while is the existing tight competitive ratio for multiple items with one price each. (11) shows that our competitive ratio for multiple items with multiple prices is not a naive combination of the existing competitive ratios; our algorithms also cannot be obtained by naively combining existing algorithms.

With a single item whose price can take any value in the continuum , the tight competitive ratio is (Ball and Queyranne 2009). (12) says that if the prices are restricted to a discrete subset of , then the competitive ratio of can only be larger.

We have a corresponding relationship in the multi-price setting. , with as defined444 can be solved to equal , where is the inverse of the function , and —see Appendix 13.1. in (13), is our competitive ratio when there are multiple items whose price sets are . (13) says that if the prices are restricted to a discrete subset of , then the competitive ratio of can only be larger.

3 MULTI-PRICE BALANCE and the Proof of Theorem 2.5

Multi-price Balance, as sketched in Subsection 2.2, is formalized in Algorithm 1. For now, we consider a generic randomized procedure for initializing and in Step 1, where the realized initializations always satisfy the following monotonicity conditions:

| (14) | |||

| (15) |

Since is non-decreasing, the expression in (16) is non-positive once the number sold reaches . Therefore, Algorithm 1 never tries to offer an item which has stocked out.

| (16) |

Theorem 3.1

Theorem 3.1 identifies conditions which, when satisfied by the randomized procedure for each , yields a competitive ratio of . Note that (17) needs to hold for every potential initialization of , while (18) only needs to hold in expectation over the initializations. We prove Theorem 3.1 in Appendix 10, but outline its proof here and provide some intuition.

First, we take the dual of the LP (5):

| (19a) | |||||

| (19b) | |||||

| (19c) | |||||

By weak duality, is upper-bounded by the objective value of any feasible dual solution.

During the (random) execution of Algorithm 1, it maintains a dual variable for each . At each time , only if a sale is realized, does the algorithm set to a non-zero value (Line 8) and increment the -variables by incrementing (Line 9). We prove three claims:

-

1.

During each time , the gain in the dual objective is at most some multiple of the revenue earned by the algorithm;

-

2.

During each time , the conditional expectation of over the random purchase decision of customer , combined with the current value of , make the LHS of (19b) at least , for all and ;

-

3.

The expectation of , over the random segment borders and value function initially chosen by the algorithm, is at least , for all and .

Claim 1 follows from condition (17), while Claim 3 follows from condition (18). Claims 2 and 3 can be combined to show that the dual variables and maintained by the algorithm are feasible, after taking an expectation over all sample paths.

We explain the intuition behind our idea of a random value function, and the resulting analysis. Even for a single item, with a small starting inventory and a large ratio from its highest to lowest price, in order to achieve a constant competitive ratio which does not scale with , one must use random booking limits (Ball and Queyranne 2009). With multiple items, our equivalent is to have the configuration of segment borders be random, and define an arbitrary value function corresponding to each one. In order to “average” over these configurations in the analysis, we relax dual feasibility to only hold in expectation. The idea of feasibility in expectation has been previously seen, but in different contexts: in Devanur et al. (2013), over a random seed, and in Golrezaei et al. (2014), over a random purchase decision (similar to our Claim 2).

3.1 Optimizing the Randomized Procedures

Theorem 3.1 reduces the problem of deriving a competitive algorithm to that of finding a randomized procedure for initializing satisfying (17)–(18). We can consider this problem separately for each , based on and , and omit the subscript .

A randomized procedure consists of a distribution over the all of the configurations satisfying (14), and for each configuration, values for satisfying (15). We would like to find a randomized procedure which satisfies (17)–(18) with a maximal value of . While this optimization problem is intractable in general, we can use the intuition behind the definitions of and from Subsection 2.1 to specify a near-optimal randomized procedure.

Definition 3.2

Define the following randomized procedure for initializing :

-

1.

Draw a random seed uniformly from ;

-

2.

For each , set if , and otherwise;

-

3.

For , let be the unique such that (note that for ; we define to be ).

The value function is then defined over by

| (20) |

increases over the (possibly empty) “segments” of its domain , which are “bordered” by . (20) is similar to definition (9) for , except the sum in (20) does not telescope, since equals only in expectation.

Note that in Step 2 above, the random segment borders are rounded comonotonically (in a perfectly positively correlated fashion) using a single seed. This ensures that the borders are increasing as required in (14), as well as the following properties.

Proposition 3.3

The random values of from Definition 3.2 satisfy:

| (21) | |||||

| (22) |

(22) is the key property derived from comonotonicity: although the rounding could move each by up to in either direction, the distance between two different never changes by more than from . Proposition 3.3 is then used to prove our main result about the randomized procedure from Definition 3.2.

Theorem 3.4

Theorem 3.4 is proven in Appendix 10. It, in conjunction with Theorem 3.1, establishes bounds (i) and (iii) from our main result for Multi-price Balance, Theorem 2.5. In Appendix 10, we state the complete proof of Theorem 2.5, including bound (ii), which involves explicitly formulating the optimization problem over randomized procedures and solving it when .

4 MULTI-PRICE RANKING and the Proof of Theorem 2.8

In Subsection 2.2, we sketched Multi-price Ranking for our general problem. In Algorithm 2, we formalize it specifically for the deterministic case, which is the case analyzed in Theorem 2.8. Note that we have assumed, without loss of generality, that for each item .

| (23) |

Our analysis extends the framework of Devanur et al. (2013) to incorporate multiple prices. It uses the dual LP defined in (19), where every is 0 or 1.

If Algorithm 2 assigns item to customer (charging price ), then we set dual variables and , where is the fixed function defined in Subsection 2.1 (we ignore the measure-zero set where is undefined). All dual variables not set during a time period are defined to be zero. The following lemmas are proven in Appendix 11:

Lemma 4.1

If Algorithm 2 assigns item to customer , then w.p.1.

Lemma 4.2

Setting for all forms a feasible solution to the dual LP (19).

The proof of Theorem 2.8 is then easy given these lemmas:

5 Randomized Counterexample and the Proof of Theorem 2.9

We first formalize the setup and randomized arrival sequence described in Subsection 2.3.

There are items, indexed by , which all have , for all , and for some . We think of as going to , while is arbitrary. Throughout this example, we often express quantities as portions of . We abuse notation and write to refer to an integer, even if is irrational, since the error from rounding to the nearest integer is negligible as .

The arrival sequence is randomized following the classical construction of Karp et al. (1990). There are customers, split into “groups” of identical customers each. Uniformly draw a random permutation of from the possibilities. For , all customers in group would deterministically buy any item in . Our construction differs from existing ones in that the groups of customers are further split into “phases”. Let be positive numbers summing to 1, corresponding to the fraction of groups in each phase, whose values we specify later. For all , the customers in groups are willing to pay for any of the items in their interest set.

Definition 5.1

Define the following shorthand notation for all :

-

•

(note that and );

-

•

(note that and ).

Proposition 5.2

Given , , and as defined in Proposition 2.2, there exists a unique solution to the following system of equations in variables :

| (24) |

with .

We define according to Proposition 5.2. This implies definitions for , which are strictly positive and sum to 1.

Now, regardless of the permutation , the optimal algorithm allocates the copies of item to the customers in group , for each , successfully serving all customers and earning revenue . This is also the optimal objective value of the LP (5). Therefore, regardless of the realized arrival sequence , which we can rewrite as

| (25) |

5.1 Upper Bound on Performance of Online Algorithms

Lemma 5.3

The expected revenue of an online algorithm with this randomized is upper-bounded by the maximum value of

| (26) |

subject to for , , and .

Lemma 5.3 drastically simplifies the analysis of the online algorithm, because it restricts to algorithms which are indifferent to the realized permutation , allowing for a deterministic analysis. However, our analysis differs from existing ones (e.g. (Golrezaei et al. 2014, Lem. 6)) in that despite the item symmetry, the online algorithm has a decision—how many customers in each phase to serve, as opposed to reserving inventory for customers in future phases.

This is controlled by the -variables, where denotes the expected fraction of item ’s inventory sold to phase- customers. The expected number of groups served during phase is then at most , resulting in the upper bound (26). Constraint comes from the fact that must not exceed the total number of groups in phase , .

Lemma 5.4

Let and . The maximum value of

| (27) |

subject to for all as well as is

| (28) |

Lemma 5.4 establishes the optimal objective value of the optimization problem from Lemma 5.3. The upper bound of on for turns out to not be binding. With both lemmas, the proof of Theorem 2.9 is easy.

Proof 5.5

Proof of Theorem 2.9. The value of (28) with and is

| (29) |

where we have used (7) to derive the equality. Combining Lemmas 5.3–5.4, we get that the RHS of (29) is an upper bound on , for any online algorithm. Meanwhile, is equal to (25) regardless of , which is exactly the RHS of (29) divided by . We have established that , completing the proof of the theorem. \Halmos

Remark 5.6

Suppose that . It can be seen that our algorithm (either Multi-price Balance or Multi-price Ranking, which behave identically when —see Aggarwal et al. (2011)), with booking limits , is the unique optimal algorithm given this distribution over arrival sequences. Indeed, the proof of Lemma 5.3 shows that given , the dominant strategy for the online algorithm is to deplete the inventories of items evenly (which is possible since ), in which case upper bound (26) is attained. The proof of Lemma 5.4 shows that the unique optimal values for are . It only remains to show that is feasible, namely for . Applying (24), this is equivalent to showing , or , which follows from (7) since .

6 Extending our Techniques

We explain how our techniques can be extended to allow for fractional inventory consumption like in the Adwords problem (Mehta et al. 2007), or offering multiple items like in the online assortment problem (Golrezaei et al. 2014).

Consider the following modification of our problem from Section 2: when customer is offered item at price , she deterministically pays and consumes a fractional amount of item ’s inventory, instead of paying and consuming 1 unit with probability . We assume that . This generalizes the Adwords problem under the small bids assumption, by allowing each budget to be depleted at different rates .

For this problem, we use Multi-price Balance, except since we are taking , we can deterministically set each . The three claims used to establish Theorem 3.1 are simpler: Claim 2 now holds deterministically instead of requiring a conditional expectation over , while Claim 3 also holds deterministically since is always . In Theorem 3.4, condition (17) is now only satisfied under an additional error term , since is no longer a discrete integer. Nonetheless, the rounding error approaches 0 as , so the optimal competitive ratio is still achieved.

For online assortment, we use the term product to refer to an (item, price)-combination . Consider the following modification of our problem from Section 2: upon the arrival of customer , for any subset (assortment) of products and , we are given , the probability that customer would pick product when offered the choice from . After being given these probabilities, we must offer an assortment to customer . This generalizes the original online assortment problem of Golrezaei et al. (2014), by allowing each item be offered at different prices. We note that the assortment offered can be constrained to lie in an arbitrary downward-closed family of subsets of ; for example, we could disallow assortments where an item is simultaneously offered at multiple prices. The execution of an algorithm can be encapsulated by the following modification of the LP (5):

| (30a) | |||||

| (30b) | |||||

| (30c) | |||||

| (30d) | |||||

Multi-price Balance can be directly applied to this problem, with the change that it offers the assortment maximizing expected pseudorevenue, , to each customer . We assume the existence of an oracle for solving this single-shot assortment optimization problem, which admits an efficient algorithm under many commonly-used choice models (see Cheung and Simchi-Levi (2016) for a summary). In the analysis, dual constraints (19b) now require for all and , which is still implied by the conditions of Theorem 3.1 as long as the choice probabilities for customers satisfy a mild substitutability assumption (see Golrezaei et al. (2014) for details).

7 Simulations on Hotel Data Set of Bodea et al. (2009)

We test our algorithms on the publicly-accessible hotel data set collected by Bodea et al. (2009). Based on the data, we consider a multi-price online assortment problem, as defined in Section 6.

7.1 Experimental Setup

We consider Hotel 1 from the data set, which has more transactions than the other four hotels. For each transaction, we use booking to refer to the date the transaction occurred, and occupancy to refer to the dates the customer will stay in the hotel. We consider occupancies spanning the 5-week period from Sunday, March 11th, 2007 to Sunday, April 15th, 2007. Although the data contains occupancies for a couple of weeks outside this range, such transactions are sparse.

We merge the different rooms into 4 categories: King rooms, Queen rooms, Suites, and Two-double rooms. Rooms under the same category draw from the same inventory. We merge the different fare classes into two: discounted advance-purchase fares and regular rack rates. We use product to refer to any of the 8 combinations formed by the 4 room categories and 2 fares.

We estimate a Multinomial Logit (MNL) choice model on these 8 products, for each of 8 customer types. The customer types are based on the booking channel, party size, and VIP status (if any) associated with a transaction. These types capture preference heterogeneity (for example, party sizes greater than 1 tend to prefer Suites and Two-double rooms). The details of our choice estimation are deferred to Appendix 14.

We should point out that more sophisticated segmentation and estimation techniques have been employed on this data set (van Ryzin and Vulcano 2014, Newman et al. 2014). Nonetheless, MNL has been reported to perform relatively well (van Ryzin and Vulcano 2014, sec. 5.2). The MNL choice model is convenient for our purposes because under it, both the assortment optimization problem, as well as the choice-based LP (30) with exponentially many variables, can be solved efficiently (Talluri and Van Ryzin 2004, Liu and Van Ryzin 2008, Cheung and Simchi-Levi 2016).

We treat each occupancy date as a separate instance of the problem, for which we define a sequence of arrivals, with one arrival for each transaction which occupies that date. The choice probabilities for each arrival are determined by the customer type associated with the corresponding transaction.555The choice realized in that transaction was used for choice model estimation, but is not used in defining the arrival. The number of days in advance of occupancy that each arrival occurred is also recorded, but this information is only relevant for algorithms which attempt to forecast the remaining number of arrivals based on the remaining length of time.

Before we proceed, we discuss the limitations of our analysis and the data set:

-

1.

In the data set, 55% of the transactions occupy multiple, consecutive days. However, we treat such a transaction as a separate arrival in the instances for each of those occupancy dates. While this is a simplifying assumption, the focus of our paper is on the basic allocation problem without complementarity effects across consecutive days, and our goal in using the data set is to extract an arrival pattern over time.

-

2.

It is not possible to deduce from the data the fixed capacity for each category of room. To compensate, we consider a wide range of starting capacities in our tests.

-

3.

Estimating the number of customers who do not make a purchase is a standard challenge in choice modeling, which is exacerbated in this data set by the fact that the arrivals are rather non-stationary. We test various assumptions on the weight of the no-purchase option in the MNL model for each customer type. In general, we assume that this weight is large, which causes the revenue-maximizing assortments to be large, allowing for tension between offering large assortments which maximize immediate revenue, and offering small assortments which regulate inventory consumption (details in Appendix 14).

7.2 Instance Definition

A test instance corresponds to a specific occupancy date, which has a finite inventory of each room category. Each customer interested in that occupancy date arrives in sequence, after which her characteristics (channel, party size, VIP status) are revealed. The problem is to show a personalized assortment of (room, fare)-options to each customer. The instances we test are described below.

-

•

Arrival sequence: 35 possibilities, one for each day in the 5-week occupancy period. We multiply the arrivals by 10 (i.e. instead of a type-1 customer followed by a type-2 customer, we have 10 type-1 customers followed by 10 type-2 customers), being interested in the high-inventory regime. After multiplication, the average number of arrivals per day is 1340, peaking on Sundays and Mondays, although the number and breakdown of customers varies by day.

-

•

Number of products: 8 (room, fare)-combinations, identical for all instances.

-

•

Prices of products: displayed in Table 7.2, identical for all instances. These prices were determined by taking the average price of that (room, fare)-combination over all transactions.

-

•

Starting inventories: 3 possibilities, where we set the starting inventories to yield a desired loading factor. The loading factor is defined by the average (over all 35 days) number of customers per unit of starting inventory, and we use the same loading factors (1.4, 1.6, 1.8) as Golrezaei et al. (2014). For a fixed loading factor, all 35 instances have the same starting inventories. The fraction of total starting inventory corresponding to each room type is based on the relative frequency with which that type is booked over all transactions (see Table 7.2).

We test additional synthetic instances, where we increase the high fares and consider a greater range of loading factors, in Subsection 7.5.

Details on Room Categories and Fares \updownRoom Category Low Fare High Fare Fraction of Rooms \upKing $307 $361 52% Queen $304 $361 15% Suite $384 $496 13% \downTwo Double $306 $342 20%

7.3 Algorithms Compared

We compare the performances of 10 algorithms on each instance.

First we describe the forecast-independent algorithms we test.

-

1.

Myopic: offer each customer the assortment maximizing immediate expected revenue, from the items that have not stocked out.

-

2.

Conservative: only offer items at their maximum prices.666This algorithm selects between the items (at their high prices) using the algorithm of Golrezaei et al. (2014).

- 3.

-

4.

Our Algorithm: offer to each customer the assortment maximizing

(31) where is the fraction of item sold. This is essentially Multi-price Balance, except we have used the fixed value function instead of the random value function to define the bid price of each item , which is a simplifying approximation for the high-inventory regime.

The Myopic and Conservative algorithms represent two extremes, where the former extracts the maximum in expectation from every customer and is optimal as the loading factor approaches 0, while the latter extracts the maximum from every unit of inventory and is optimal as the loading factor approaches . In-between these extremes, our algorithm attempts to balance revenue-per-customer and revenue-per-item as it selects items and prices to put in the assortment.

Next we describe the forecasting-based algorithms we test. These algorithms all estimate the number of each type of customer yet to arrive, and then incorporate this information into the LP (30) to set bid prices. They differ in how they perform the forecasting, and how frequently they update the bid prices by re-solving the LP. Further details about these algorithms, as well as discussion of alternative algorithms, are deferred to Appendix 14.1.

-

5.

One-shot LP: solve the LP only once, at the start, using the average number of customers of each type to appear on a given day.

-

6.

LP Resolving: re-solve the LP every 100 arrivals, using updated forecasts and inventory counts. During each re-solve, the estimated number of remaining customers is updated, taking into account the length of time remaining until occupancy, and the number of customers that have arrived. The estimated type breakdown is fixed, based on the aggregate distribution.

-

7.

LP Learning: same as LP Resolving, except the estimated type breakdown is also updated, based on the empirical distribution observed thus far.

-

8.

LP Clairvoyant: same as LP Resolving, but given the true number of customers of each type remaining.

Finally, we describe the hybrid algorithms we test. These algorithms combine a forecasting algorithm with “Our Algorithm” as described above, based on a parameter . For each customer , the hybrid algorithm considers the expected pseudorevenue (as defined in (31)) of the assortment suggested by the forecasting algorithm. If this is at least of the maximum value of (31) over all assortments , then the hybrid algorithm offers . Otherwise, the hybrid algorithm offers the assortment suggested by our algorithm, which maximizes (31) by definition.

-

9.

Resolve-1.5: hybrid algorithm based on LP Resolving and parameter .

-

10.

Learn-1.5: hybrid algorithm based on LP Learning and parameter .

We selected above by taking the better of the two values tested in Golrezaei et al. (2014). We did not search over for the best , as the reported performance of such a hybrid algorithm would be greatly inflated, since would be chosen after seeing the performance.

7.4 Results

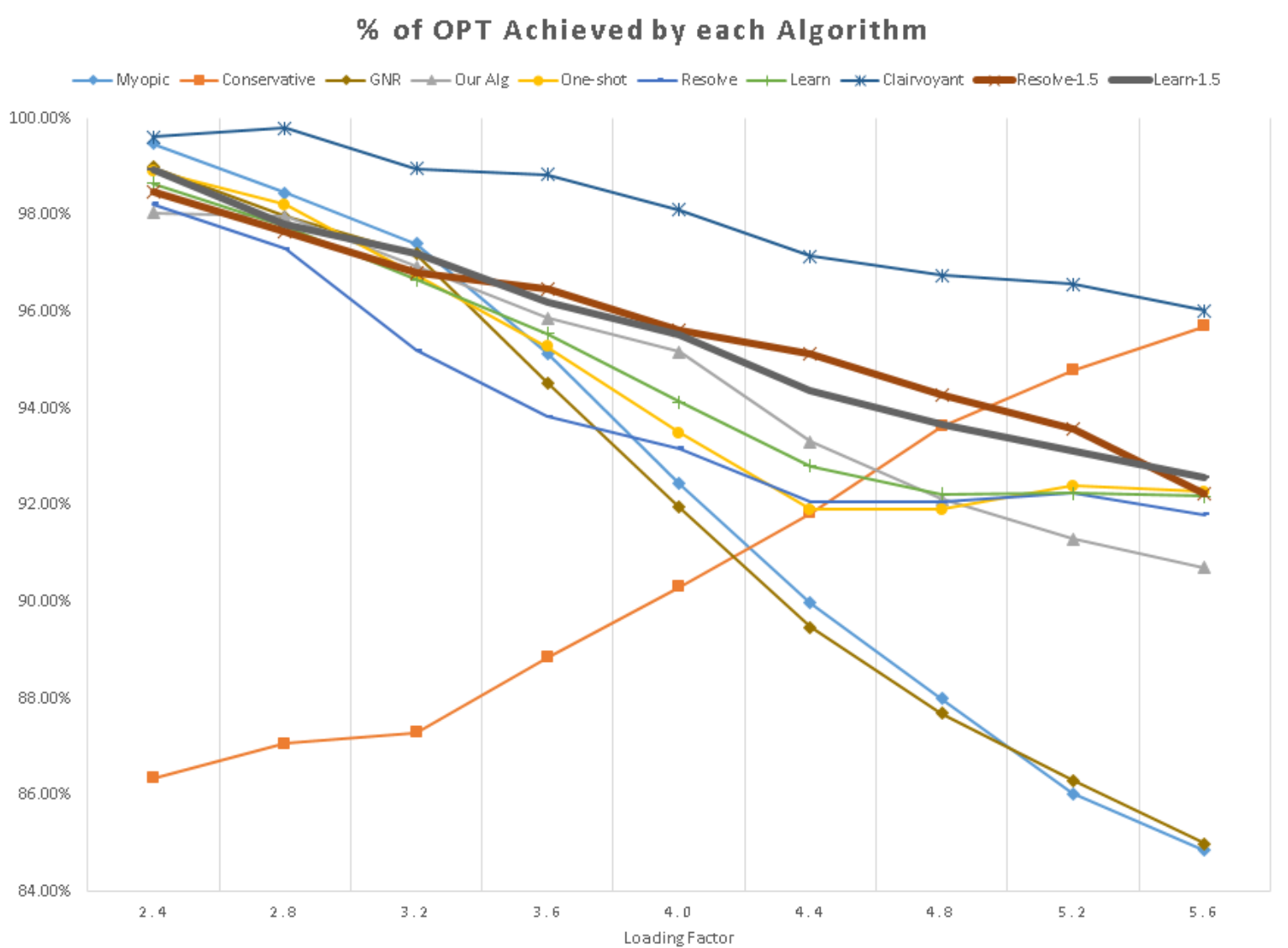

On every instance, we express the performance of each algorithm as a percentage of the LP upper bound. That is, we take the expected revenue of the algorithm (approximated over 10 runs), and divide it by the optimal objective value of the LP (30) with the true arrival sequence. In Table 7.4, we report the mean and standard deviation of each algorithm’s percentages over the 35 arrival sequences, for each loading factor.

The percentages of optimum achieved by different algorithms. The 3 highest percentages in each row are bolded. The 3 lowest standard deviations in each row are italicized. \updownLoading Forecast-independent Forecast-dependent Hybrid \updownFactor Myopic Conservative GNR OurAlg One-shot Resolve Learn Clairvoyant Resolve-1.5 Learn-1.5 \up1.4 Mean 0.974 0.940 0.973 0.976 0.973 0.962 0.958 0.991 0.977 0.977 \down Stdev 0.023 0.034 0.020 0.013 0.016 0.039 0.041 0.008 0.018 0.020 \up1.6 Mean 0.965 0.960 0.964 0.971 0.964 0.961 0.963 0.990 0.977 0.978 \down Stdev 0.025 0.036 0.020 0.014 0.021 0.031 0.030 0.008 0.008 0.010 \up1.8 Mean 0.957 0.972 0.960 0.968 0.808 0.962 0.968 0.990 0.977 0.977 \down Stdev 0.020 0.036 0.017 0.012 0.100 0.029 0.023 0.009 0.008 0.007

In general, our Multi-price Balance algorithm is the most profitable and consistent among the forecast-independent algorithms, while the forecast-dependent algorithms have much greater fluctuation in their performance for different occupancy days, depending on how accurate their forecasts were for that day. LP Learning is slightly better than the others, but is most prone to overfitting in its forecasts. We note that although the forecast-independent algorithms do not make use of information about the remaining time horizon (which can be used to estimate the remaining number of customers), they perform comparably well to the forecasting algorithms. Nonetheless, by combining the forecasting algorithms with Multi-price Balance, the hybrid algorithms are able to correct for forecast overconfidence and achieve the best performance overall (aside from the Clairvoyant algorithm, which has a perfect forecast of the future). We find that although the hybrid algorithm only changes a small fraction () of the forecasting algorithm’s decisions, this drastically improves the profitability and consistency.

7.5 Results under Greater Fare Differentiation

The instances tested in Subsection 7.4 were “easy” in that there was not so much difference between selling rooms at their low or high fares. In this subsection, we synthetically modify the higher fare for each room category to be twice its lower fare. We also increase the utility of the no-purchase option in the MNL model for each customer type (see Appendix 14), to maintain the tension between low fares which maximize expected revenue, and high fares which limit inventory consumption.

Furthermore, we test a complete range of loading factors, including both the extreme where the Myopic algorithm is optimal, and the extreme where the Conservative algorithm is optimal. In Figure 3, we plot the average percentages of optimum attained by each algorithm over the 35 arrival sequences, for each loading factor.

The conclusion again is that our two hybrid algorithms, which use forecasts but continuously reference our forecast-independent value functions, are the most profitable and consistent. Note that our Multi-price Balance algorithm comes third, and performs significantly better than the inventory-balancing algorithm of Golrezaei et al. (2014), which is similar to the Myopic algorithm as it does not take the two different prices of the same item into account.

However, it is important to note that overall, our methodology is only relevant in scenarios where the loading factor is in-between the extremes where there is a non-trivial tradeoff. If the loading factor is very low, and the hotel does not even get close to full on any day, then it would be best to always use the Myopic algorithm; similarly, if the loading factor is very high, and the hotel gets full every day, then it would be best to always use the Conservative algorithm. Nonetheless, we argue that most hotels do lie in-between the extremes, where it is sometimes full and sometimes empty depending on sudden local events. Otherwise, the hotel either over-built or under-built in an higher-order decision.

8 Conclusion

Competitive analysis is a well-established methodology in sequential decision-making problems, providing a baseline decision in the absence of a reliable forecast of the future. Previously, online resource allocation algorithms based on competitive analysis have assumed that each resource can only be converted to reward at a fixed rate. We extend these results and derive algorithms which jointly consider the tradeoffs between different resources and different reward rates. This broadly expands the applicability of competitive analysis in areas such as online matching, online advertising, personalized e-commerce, and appointment scheduling.

Acknowledgments

The authors would like to thank Rong Jin of Alibaba for pointing out a detailed technical error in an earlier version of the appendix. The authors would also like to thank Ozan Candogan and James Orlin for asking questions which led to the simpler bound presented in Corollary 2.7. A preliminary version of this article appeared in the 20th ACM Conference on Economics and Computation (EC), whose anonymous reviewers helped clarify the manuscript in several places.

References

- Aggarwal et al. (2011) Aggarwal G, Goel G, Karande C, Mehta A (2011) Online vertex-weighted bipartite matching and single-bid budgeted allocations. Proceedings of the twenty-second annual ACM-SIAM symposium on Discrete Algorithms, 1253–1264 (Society for Industrial and Applied Mathematics).

- Araman and Caldentey (2011) Araman VF, Caldentey R (2011) Revenue management with incomplete demand information. Wiley Encyclopedia of Operations Research and Management Science .

- Badanidiyuru et al. (2013) Badanidiyuru A, Kleinberg R, Slivkins A (2013) Bandits with knapsacks. Foundations of Computer Science (FOCS), 2013 IEEE 54th Annual Symposium on, 207–216 (IEEE).

- Ball and Queyranne (2009) Ball MO, Queyranne M (2009) Toward robust revenue management: Competitive analysis of online booking. Operations Research 57(4):950–963.

- Bodea et al. (2009) Bodea T, Ferguson M, Garrow L (2009) Data set—choice-based revenue management: Data from a major hotel chain. Manufacturing & Service Operations Management 11(2):356–361.

- Borodin and El-Yaniv (2005) Borodin A, El-Yaniv R (2005) Online computation and competitive analysis (cambridge university press).

- Buchbinder et al. (2007) Buchbinder N, Jain K, Naor JS (2007) Online primal-dual algorithms for maximizing ad-auctions revenue. European Symposium on Algorithms, 253–264 (Springer).

- Chan and Farias (2009) Chan CW, Farias VF (2009) Stochastic depletion problems: Effective myopic policies for a class of dynamic optimization problems. Mathematics of Operations Research 34(2):333–350.

- Chen et al. (2016) Chen X, Ma W, Simchi-Levi D, Xin L (2016) Dynamic recommendation at checkout under inventory constraint. manuscript on SSRN .

- Chen and Farias (2013) Chen Y, Farias VF (2013) Simple policies for dynamic pricing with imperfect forecasts. Operations Research 61(3):612–624.

- Cheung and Simchi-Levi (2016) Cheung WC, Simchi-Levi D (2016) Efficiency and performance guarantees for choice-based network revenue management problems with flexible products. available on SSRN .

- Ciocan and Farias (2012) Ciocan DF, Farias V (2012) Model predictive control for dynamic resource allocation. Mathematics of Operations Research 37(3):501–525.

- Devanur and Jain (2012) Devanur NR, Jain K (2012) Online matching with concave returns. Proceedings of the forty-fourth annual ACM symposium on Theory of computing, 137–144 (ACM).

- Devanur et al. (2013) Devanur NR, Jain K, Kleinberg RD (2013) Randomized primal-dual analysis of ranking for online bipartite matching. Proceedings of the Twenty-Fourth Annual ACM-SIAM Symposium on Discrete Algorithms, 101–107 (SIAM).

- Feldman et al. (2010) Feldman J, Henzinger M, Korula N, Mirrokni V, Stein C (2010) Online stochastic packing applied to display ad allocation. Algorithms–ESA 2010 182–194.

- Feldman et al. (2009) Feldman J, Korula N, Mirrokni V, Muthukrishnan S, Pál M (2009) Online ad assignment with free disposal. International Workshop on Internet and Network Economics, 374–385 (Springer).

- Ferreira et al. (2016) Ferreira KJ, Simchi-Levi D, Wang H (2016) Online network revenue management using thompson sampling. manuscript on SSRN .

- Golrezaei et al. (2014) Golrezaei N, Nazerzadeh H, Rusmevichientong P (2014) Real-time optimization of personalized assortments. Management Science 60(6):1532–1551.

- Jasin and Kumar (2012) Jasin S, Kumar S (2012) A re-solving heuristic with bounded revenue loss for network revenue management with customer choice. Mathematics of Operations Research 37(2):313–345.

- Karp et al. (1990) Karp RM, Vazirani UV, Vazirani VV (1990) An optimal algorithm for on-line bipartite matching. Proceedings of the twenty-second annual ACM symposium on Theory of computing, 352–358 (ACM).

- Kesselheim et al. (2013) Kesselheim T, Radke K, Tönnis A, Vöcking B (2013) An optimal online algorithm for weighted bipartite matching and extensions to combinatorial auctions. European Symposium on Algorithms, 589–600 (Springer).

- Lan et al. (2008) Lan Y, Gao H, Ball MO, Karaesmen I (2008) Revenue management with limited demand information. Management Science 54(9):1594–1609.

- Liu and Van Ryzin (2008) Liu Q, Van Ryzin G (2008) On the choice-based linear programming model for network revenue management. Manufacturing & Service Operations Management 10(2):288–310.

- Manshadi et al. (2012) Manshadi VH, Gharan SO, Saberi A (2012) Online stochastic matching: Online actions based on offline statistics. Mathematics of Operations Research 37(4):559–573.

- Mehta (2013) Mehta A (2013) Online matching and ad allocation. Foundations and Trends® in Theoretical Computer Science 8(4):265–368.

- Mehta and Panigrahi (2012) Mehta A, Panigrahi D (2012) Online matching with stochastic rewards. Foundations of Computer Science (FOCS), 2012 IEEE 53rd Annual Symposium on, 728–737 (IEEE).

- Mehta et al. (2007) Mehta A, Saberi A, Vazirani U, Vazirani V (2007) Adwords and generalized online matching. Journal of the ACM (JACM) 54(5):22.

- Mehta et al. (2014) Mehta A, Waggoner B, Zadimoghaddam M (2014) Online stochastic matching with unequal probabilities. Proceedings of the Twenty-Sixth Annual ACM-SIAM Symposium on Discrete Algorithms, 1388–1404 (SIAM).

- Newman et al. (2014) Newman JP, Ferguson ME, Garrow LA, Jacobs TL (2014) Estimation of choice-based models using sales data from a single firm. Manufacturing & Service Operations Management 16(2):184–197.

- Reiman and Wang (2008) Reiman MI, Wang Q (2008) An asymptotically optimal policy for a quantity-based network revenue management problem. Mathematics of Operations Research 33(2):257–282.

- Talluri and Van Ryzin (2004) Talluri K, Van Ryzin G (2004) Revenue management under a general discrete choice model of consumer behavior. Management Science 50(1):15–33.

- Talluri and Van Ryzin (2006) Talluri KT, Van Ryzin GJ (2006) The theory and practice of revenue management, volume 68 (Springer Science & Business Media).

- Van Ryzin and McGill (2000) Van Ryzin G, McGill J (2000) Revenue management without forecasting or optimization: An adaptive algorithm for determining airline seat protection levels. Management Science 46(6):760–775.

- van Ryzin and Vulcano (2014) van Ryzin G, Vulcano G (2014) A market discovery algorithm to estimate a general class of nonparametric choice models. Management Science 61(2):281–300.

- Wang et al. (2015) Wang X, Truong V, Bank D (2015) Online advance admission scheduling for services, with customer preferences. Working paper.

- Yao (1977) Yao ACC (1977) Probabilistic computations: Toward a unified measure of complexity. Foundations of Computer Science, 1977., 18th Annual Symposium on, 222–227 (IEEE).

- Zhang and Cooper (2005) Zhang D, Cooper WL (2005) Revenue management for parallel flights with customer-choice behavior. Operations Research 53(3):415–431.

- Zhang et al. (2016) Zhang H, Shi C, Qin C, Hua C (2016) Stochastic regret minimization for revenue management problems with nonstationary demands. Naval Research Logistics (NRL) 63(6):433–448.

9 Deferred Proofs from Section 2

Proof 9.1

Proof of Lemma 2.1. Fix any adaptive algorithm (which knows the arrival sequence, but not the realizations of the customers’ purchase decisions, at the start) and consider its execution on setup with arrival sequence . Let be the indicator random variable (0 or 1) for the algorithm offering item at price to customer , and be the indicator random variable for customer accepting when item is offered to her at price . On a given run, the constraints and are satisfied. Therefore, they are still satisfied after taking an expectation over all runs, and furthermore we can use independence to show that . Therefore, the algorithm must satisfy constraints (5b) and (5c) of the LP. Since its revenue on a given run is , taking an expectation over it yields (5a), completing the proof. \Halmos

Proof 9.2

Proof of Proposition 2.2. The statement for is immediate from the fact that the explicit value of is , for all . To prove the statement for , we show that the solution to the system of equations formed by (7) and is unique and strictly positive.

Let for all . Then the constraint can be rewritten as . Furthermore, we derive from (7) that for all , . Therefore,

| (32) |

Consider the LHS of (32) as a function of on . This is a continuous, strictly increasing function which is at most when and when . Therefore, there is a unique solution with , and the resulting value of is positive. For , since can also be written as , it can be seen that , hence the unique value for is positive as well. \Halmos

Proof 9.3

Proof of Proposition 2.10. For the first inequality in (11), observe that is a strictly increasing function on . Since , , which is the desired result.

For the second inequality in (11), we show , by showing that for all , is a smaller multiple of than is of . This suffices because both the fractions and must sum to 1. For a given , we must establish that . By definition, . Therefore, is suffices to show that , or . This follows from the fact that the function is strictly increasing.

To prove (12), note that , while . Therefore, it suffices to show that for any , . Letting , the desired inequality becomes , which is immediate.

For (13), we would like to prove that . Note that is the unique solution to

| (33) |

while is the unique solution to

| (34) |

The LHS of (33), as a function of , is increasing over ; the same can be said about the LHS of (34) as a function of . Therefore, it suffices to show that if , then the LHS of (33) is strictly less than the LHS of (34), for all .

Let and consider any . Let . It suffices to show that , which can be rearranged as . For the final inequality, note that is a strictly concave function on , since . Therefore, , because the LHS is the slope of the secant line through and , while the RHS is the slope of the tangent line through . \Halmos

10 Supplement to Section 3

The first subsection contains the deferred proofs from Section 3. In the second subsection, we explain how to optimize the randomized procedure for generating a single value function. In the third subsection, we put together the proof of Theorem 2.5.

The following inequality will be useful throughout the paper. For all , (7) says that , where we have used the fact that . Therefore, for all , we can derive that

| (35) |

10.1 Deferred Proofs

Proof 10.1

Proof of Theorem 3.1. Define to be the algorithm’s value for at the end of time ( is understood to be 0), for all and . For all , define and if a sale was made during time ; define otherwise.

Consider the solution to the dual LP (19) formed by setting for all , and for all . We claim that this solution is feasible. The non-negativity constraint (19c) can be verified directly from the definitions.

Now, consider constraint (19b) for a fixed . Given the initializations of and the value of , the algorithm will always make a decision during time which earns pseudorevenue whose conditional expectation is at least , by definition (16). Formally,

for all values of . By the tower property of conditional expectation, . Meanwhile, has been set to . Since and is increasing, . Therefore, the LHS of (19b), , is at least . By (18), this is at least , completing the proof of feasibility.

Applying weak duality, we obtain

| (36) |

We now analyze the term inside the expectation,

| (37) |

for every . We would like to argue that it is at most , on every sample path.

There are two cases. If an item was sold at price during time , then (37) equals

| (38) |

Indeed, , for all , and by definition. Furthermore, since is positive, must by less than . Therefore, we can invoke (17) to get that (38) is at most , which is equal to by definition. In the other case, if no item was sold during time , then (38) is 0, while too, so (38) is still at most .

Proof 10.2

Proof of Proposition 3.3.

For (21), note that .

For (22), note that . We will prove that ; the inequality that follows by symmetry. The maximum value of is while the minimum value of is , hence the result is immediate unless , i.e. . However, in this case, if , then and hence is rounded up as well. Similarly, if is rounded down, then must be rounded down as well. If and are rounded in the same direction, then (iii) holds. \Halmos

Proof 10.3

Proof of Theorem 3.4. First we prove (18), the claim that , inductively. Clearly . Now consider and suppose we have established (18) for the case. We can compare expression (20) with and to obtain . Therefore,

where the first inequality uses the induction hypothesis, and the second inequality uses Jensen’s inequality (the exponential function is convex). The equality follows from (21) and the definition that , completing the induction.

Now we prove (17) for an arbitrary and . Let and . Note that , and . Substituting into the LHS of (17), we get . Adding and subtracting and rearranging, we get

| (39) |

The following upper bound can be derived for expression (39):

| (40) |

The inequality holds because for all , and is at most .

It suffices to show that expression (40) is bounded from above by

| (41) |

To assist in this task, we would like to establish the following for all and :

| (42) |

But due to the definition of in (7), and due to (35). Substituting back into inequality (42), it suffices to prove

where we have used Definition 2.3 to rewrite the first exponent. Now,

since and . Thus it remains to prove that

| (43) |

We consider two cases. First suppose , i.e. . Then the LHS of (43) equals , which equals the RHS of (43) by the assumption that . In the second case, suppose , i.e. . Then inequality (43) can be rearranged as

The first bracket is positive by the assumption that and the second bracket is non-negative since . This finishes the proof of (43), and hence (42).

Equipped with (42), we return the task of proving that expression (40) is at most expression (41). If we inductively apply inequality (42) to expression (40) for (when , ; when , if we arrived at case two during iteration and otherwise,…), we conclude that expression (40) is bounded from above by

for some . The fact that , due to (7), and the fact that , due to (22), complete the proof of expression (40) being at most expression (41), and thus the proof of Theorem 3.4 for general .

10.2 Optimizing the Randomized Procedure

We can explicitly formulate the optimization problem over randomized procedures for a single item with starting inventory and prices . Using the “balls in bins” counting argument, the number of configurations satisfying (14) is .

We refer to these configurations in an arbitrary order using the index , where we let denote the probability of choosing configuration , denote the value function for , and denote the value of under configuration for all . The optimization problem of satisfying (17)–(18) with a maximal value of can be formulated as follows:

| (44a) | |||||

| (44b) | |||||

| (44c) | |||||

| (44d) | |||||

| (44e) | |||||

| (44f) | |||||