On singular control problems, the time-stretching method, and the weak-M1 topology

Abstract.

We consider a general class of singular control problems with state constraints. Budhiraja and Ross [8] established the existence of optimal controls for a relaxed version of this class of problems by using the so-called ‘time-stretching’ method and the J1-topology. We show that the weak-M1 topology is better suited for establishing existence, since it allows to bypass the time-transformations, without any additional effort. Furthermore, we reveal how the time-scaling feature in the definition of the weak-M1 distance embeds the time-stretching method’s scheme. This case study suggests that one can benefit from working with the weak-M1 topology in other singular control frameworks, such as queueing control problems under heavy traffic.

AMS Classification: Primary: 93E20, 60J60, 60F99, 60K25.

Keywords: weak-M1 topology, singular control, time-stretching, optimal controls.

1. Introduction

In this paper, we revisit the problem of proving the existence of optimal controls for a class of singular control problems with state (and control) constraints. The paper includes two main theorems. Theorem 2.1 argues that there exist optimal singular controls for the problem. Our proof for this theorem uses weak convergence arguments under the Skorokhod’s weak-M1 (WM1) topology defined on the space of functions that are right-continuous with left limits (RCLL). This problem was analyzed by Budhiraja and Ross [8] using the standard Skorokhod’s J1 topology and the time-stretching method, which provides tightness of some time-scaled processes and uses rescaling of time in the limit. We on the other hand, show that, under the WM1 topology, tightness can be obtained directly for the original sequence. This leads to a simpler proof. Furthermore, in the second main theorem, Theorem 3.1, we shed light on the relationship between the time-stretching method and the WM1 topology.

1.1. Singular control problems

In singular control problems the control is allowed to be singular with respect to the Lebesgue measure . Such problems have been studied in various fields such as queueing systems, mathematical finance, actuarial science, manufacturing systems, etc. State constraints for singular controlled diffusion processes are natural in many practical problems. For example in queueing systems, the diffusion scaled queueing problem is often approximated by the so-called Brownian control problems (see, [22, 20]). In this case, buffers cannot be negative and in case they have bounded capacity, further restrictions are imposed, see e.g., [24]. In the area of mathematical finance and actuarial sciences the prices of assets are often modeled by diffusion processes and the singular controls are restricted (e.g., non decreasing processes).

We consider the following multi-dimensional problem. Fix a finite horizon . Let be a process whose increments belong to a closed cone that is contained in an open half-space (for example the nonnegative orthant. This is the case in optimal dividend payouts [1, Section 3], portfolio selection with transaction costs [15, Section 3], and the reduced Brownian network in [24, Section 5]). Specifically, the state process is given by

such that belongs to a closed and convex set, where is a Wiener process. The decision maker aims to minimize a cost that accounts for the state process and the singular control. This is a generalization of the model considered in [8] since the coefficients in the state dynamics that we consider are not constants and the state process is not restricted to live in a cone. Another minor difference is that we consider a finite horizon problem instead of an infinite horizon discounted one. Nevertheless, this is only due to a personal taste of the author. The techniques in this paper can be transferred to the discounted case without any difficulty. We comment on this in Remark 3.4.

Optimal solutions in such problems, in dimension one, are often defined using Skorokhod’s reflection mapping, see e.g., [5] and [21]. The latter paper’s approach works in higher dimensions as well. The technique is to study the regularity of relevant solutions of a free boundary differential equation. The smoothness is necessary for verifying that the candidate reflected control is optimal, see e.g., [43, 41]. The difficulty with this approach is that regularity is not always available. Hence, in the general case, the value function is characterized as the unique viscosity solution to the associated differential equation, see [2]. Another approach is the time-stretching method on which we now detail.

1.2. The time-stretching method

The time-stretching method was introduced by Meyer and Zheng in [34] and studied in the same framework by Kurtz in [29]. Kurtz further used it for constrained Markov processes in [27, 28]. The results of these papers are used to contruct reflecting diffusions and prove convergence results. In the context of stochastic control, the method was first used by Kushner and Martins in [33, 31] and was adopted in [7, 8, 9, 10]. Kurtz and Stockbridge [30] used this method to characterize stationary solutions for controlled and singular martingale problems. More recently, Costantini and Kurtz [12, 13] used this method to establish existence and uniqueness of some constrained Markov processes.

We now sketch the basic idea of the proof of the existence of optimal singular controls using the time-stretching method. First, one chooses a sequence of asymptotic optimal controls . In case of absolutely continuous controls with a bounded control set, compactness and tightness arguments yield the existence of optimal control. This is not the case with singular controls under the J1 topology, in which case the oscillation can be very big. However, it is possible to scale time in such a way so that the time-scaled controls (and other relevant processes) are uniformly Lipschitz. The scaled processes are therefore tight and one may consider a limit point of these processes. Rescaling back to the original time-scale, any of the limit points are shown to be optimal by proving the convergence of the costs, passing through the time-scaled processes. These time-rescaled limit points may have jumps.

1.3. The advantage of the WM1 topology over the J1 topology

Before introducing the WM1 topology, we remind the reader that under the J1 topology, the distance between two functions with (time-)unmatched jumps (say, both of size 1) is not negligible. This is in contrast to the WM1 topology. Hence, it suggests that the WM1 topology is more appropriate for singular control problems. Another nice feature that makes the WM1 topology so useful in the context of singular controls is that the WM1 oscillation of any nondecreasing (component-wise) function is zero, see (3.11) for the definition of the WM1-oscillation. This is in contrast to the J1 oscillation, which can be very big, especially in the existence of jumps. Therefore, in case that the singular controls have nondecreasing increments in each of its components, the proof of the existence of optimal controls is fairly easy and only requires probabilistic growth bounds to attain tightness and convergence of the costs. The assumption that the increments are nondecreasing is not restrictive since the increments take values in a closed cone, strictly contained in an open half space. Such a cone can be linearly transformed into the nonnegative orthant and the problem can be reformulated accordingly. This is rigorously established at the beginning of Section 4.

The simplicity of the proof of the existence of optimal singular control demonstrates the advantage of the WM1 topology for singular control problems in any dimension. This suggests that one can benefit from working with this topology in other singular control problems, such as the general approximation of the Brownian control problem to queueing control problems presented in the seminal work of Budhiraja and Ghosh [7], the integral transformation used by Atar and Shifrin [3, Section 3], the Knightian uncertainty model given in [11, 10], and in other queueing models as well. At this point, one may wonder how come the simplicity of the proof using the WM1 topology does not violate the principle that there is no such thing as a free lunch. The reason is that part of the complexity is embedded in the properties of the WM1 topology, established in [46, Section 12]. Hence, one can think of the WM1 topology framework as a ready-made lunch. In the next subsection we explain how the time-stretching method’s scheme is embedded in the definition of the WM1 topology.

1.4. The WM1 topology and its relationship with the time-stretching method

In his seminal paper [42], Skorokhod introduced four ways to evaluate distances in the space of RCLL functions, known as J1, J2, M1, and M2. The associated topologies are named the same. Later, Whitt [46, Section12] presented strong and weak versions of the M1 and the M2 topologies, which, in each case, coincide in dimension one. The strong topology agrees with the standard topology introduced by Skorokhod and the weak topology coincides with the product topology. While the J1 topology is the most commonly used, over the years, several works have been done under the M1 topology, see e.g., [44, 47, 26, 32, 38, 39, 40, 45, 36, 16, 18, 35]. These works often consider one-dimensional processes, hence the terms weak and strong topologies coincide. The WM1 topology is much less common, yet is still found to be useful, see e.g., [23, 46, 4, 19, 17].

The strong- and weak-topologies over the time interval are defined by the following distance

where the infimum is taken over all possible continuous nondecreasing functions , , satisfying and , when traces out the graph according to the natural order of the graph, see Section 3.1 for a rigorous definition. Such a mapping is called a weak parametric representation of . Loosely speaking, is a time scaled version of with respect to the time scaling function . The difference between the strong- and weak-topologies lies in the way the graph is defined at discontinuity points of . The exact definition of the graph under the WM1 topology appears in Section 3 below.

In Theorem 3.1 we show that the WM1-convergence of functions embeds the time-stretching scheme through the definition of the weak parametric representations. Specifically, we consider a sequence of RCLL functions that converges in the WM1 topology to an RCLL function . Then, for every we construct a weak parametric representation , using the same structure used in the time-stretching method, where recall that the function is the time-scaling function and is the time-scaled function. These functions are uniformly Lipschitz over , hence a limit point exists. We show that, in some sense, is a weak parametric representation of . More accurately, we show that , where is the right-inverse of . That is, brings the limit of the time-scaled functions back to the scale of . This is the same procedure done in the time-stretching method, only that now it is built-in the definition of the WM1 topology.

1.5. Preliminaries and notation

We use the following notation. The sets of natural and real numbers are respectively denoted by and . For any , and , denotes the dot product between and , and is the Euclidean norm; for , . For , set and . The interval is denoted by . For any interval and any , denotes the space of valued functions that are RCLL defined on . For and , . For any event , is the indicator of the event , that is, if holds and otherwise. We use the convention that the infimum of the empty set is .

1.6. Organization

The rest of the paper is organized as follows. In Section 2 we present the singular control problem, state Theorem 2.1 that establishes the existence of an optimal singular control, and explicitly introduce the steps of the time-stretching method given in [8]. Section 3 is dedicated to the WM1 topology, where we also establish its relationship with the time-stretching method in Theorem 3.1. Finally, in Section 4 we prove Theorem 2.1.

2. The control problem and the main result

Throughout the paper we fix a finite horizon and dimensions . Let be a closed and convex cone in and let be a closed and convex subset of , both with nonempty interiors. Let be a continuous mapping and denote its image by . Denote and impose the following assumption.

Assumption 2.1.

() For any there exists such that, for every , there exists such that , where the latter is the interior of . Moreover, there are vectors and and a parameter such that, for all and ,

| (2.1) |

The first part of the assumption guarantees that the set of admissible controls, which is defined below, is not empty. The geometric interpretation of the second part is that both and are subsets of open half-spaces. One generic example for a non-constant function satisfying the first part of the assumption is that for any , is a cone and also is a cone, and there exists such that, for every , there exists for which . A more concrete example is , where is continuous and . In this case, for any , , so .

Definition 2.1.

An admissible singular control for any is a tuple

where is a filtered probability space satisfying the usual conditions and supporting the processes and that satisfy the following conditions.

-

•

is a -dimensional -measurable Wiener process ;

-

•

is an RCLL -progressively measurable process whose increments take values in ;

-

•

is the state process whose dynamics are given by

(2.2) and for every , where and are measurable functions satisfying further properties given in Assumption 2.2 below.

Throughout the paper we fix and denote by the collection of all admissible singular controls. More than often we abuse notation and refer to as the control, denoting instead of . By convention we assume and .

The cost function associated with the admissible control , is given by

where , , and are measurable functions that satisfy further properties, given in Assumption 2.2 below. The associated value is

A control is called an optimal control if its associated cost attains the value, that is, .

The following assumption is needed for the main result of this section to hold:

Assumption 2.2.

-

()

The functions and are continuous on their domains. Hence, and are bounded.

-

()

There exists a constant such that for all .

-

()

The functions and are uniformly bounded and Lipschitz continuous in , uniformly in .

-

()

At least one of the following three conditions hold:

-

(a)

There exist positive constants and and such that

(2.3) and

(2.4) - (b)

-

(c)

There exist positive constants and such that for any , and . Moreover, there exists positive such that for any and , . In this case, we allow for and to be unbounded from above.

-

(a)

Remark 2.1.

Notice that the conditions in the present paper are more general than the ones imposed in [8] as we now list.

- (i)

-

(ii)

The dynamics of the state process in our case follow a general diffusion process plus a singular control component, where the coefficients are not necessarily constants as in [8]. At this point it is worth mentioning that the Lipschitz continuity of and are required for the existence of a solution to (2.2).

Aside these generalizations there is another small difference between the models. We study a finite horizon problem with terminal cost and not a discounted one. Therefore, we impose condition (2.3) on the terminal cost and not on the running cost.

The proof of the theorem is provided in Section 4.

2.1. Solving the problem using the time-stretching scheme

We now shortly review the scheme of the time-stretching method used in [8] to prove the existence of optimal controls. The reason for this introduction is two-fold. First, in order to compare between our proof of existence using the WM1 topology (Section 4) and the proof using the time-stretching scheme we need to introduce the scheme; and second, we need the notion of time-stretching in order to tie between it and the WM1 topology. The latter is done in Section 3.2.

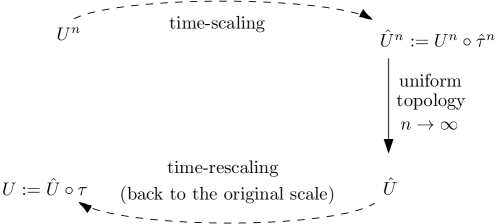

The idea of the scheme is to consider a sequence of singular controls , whose associated payoff converges to the value function. A limiting control (if exists) is a candidate for an optimal control. The problem is that an arbitrary sequence of singular controls is not necessarily relatively compact under the J1 topology since the J1-oscillation can be very big. To deal with this problem, one follows the next five-step scheme, which is also illustrated in Figure 1.

- (i)

-

(ii)

For each define the process

(2.5) It is strictly increasing and continuous by (2.1) and since is continuous. Hence, the left inverse is continuous and strictly increasing.

-

(iii)

Define the time-stretched process

(2.6) and similarly set and . The paths of the sequence are uniformly Lipschitz, hence, under the J1 topology, their -tightness is attained. Moreover, the tighness of follows from tightness of , and finally, the tightness of follows from the tightness of . As a consequence, one can consider a limit point , along a converging subsequence labeled .

-

(iv)

Define the time-inverse process , and set up the rescaled process

(2.7) and similarly for and .

-

(v)

Show that is an optimal control for the original problem by proving convergence of the costs, passing through the time-stretched and rescaled processes.

Note that the approximating continuous controls from the first step imply that is continuous in addition to increasing, and hence is strictly increasing. This property is very convenient when going back to the original scale. However, as mentioned in [8] (without a proof), this approximation is not necessary.111Cohen [10] managed to bypass the continuous approximation this issue because in the queueing model considered there, the singular control process has small jumps, by nature. Hence, in the limit, the oscillation of the time-stretched process is small even though it is not continuous. Also, it is possible that the process may have jumps even though are continuous.

3. The WM1 topology

We now set up the WM1 topology on and state a few results that serve us in the sequel. For additional reading about this topology and the other Skorokhod topologies, the reader is referred to [46]. Please note that Whitt also sets up the strong M1 topology, which we ignore in this manuscript. The reason is that our framework involves multidimensional processes for which the strong-M1 topology is not useful and in the one-dimensional case the weak- and strong-M1 topologies coincide. In this regard, see Footnote 3.

3.1. The weak parametric representation

Fix . For any define the product segment

where . For any define the thick graph of by

| (3.1) | ||||

where . A weak (partial) order relation is defined on the graph as follows: if either or and for all , .

The WM1 topology is defined by a semi-metric (does not satisfy the triangle inequality, see [46, Example 12.3.2]). To set it up, define the weak parametric representation of to be a continuous nondecreasing (with respect to the weak order defined above) function222The hat notation is consistent with the one given in Section 2.1. mapping into such that and . The component scales the time interval to and time-scales . Let be the set of all the weak parametric representations of and define,

| (3.2) |

Notice that the parametric representations bring and to the same time-scale . Hence, the parametric representations are ‘comparable’. A nice observation that serves us in the sequel is that if one sets the right-inverse of , , then

| (3.3) |

Indeed, for every , there is such that . If then (3.3) is obvious. Otherwise, by the definition of , for any , . Therefore, by the monotonicity of and the definition of the weak parametric representation, for any and , and , which leads to . By the continuity of one obtains (3.3).

Remark 3.1.

(A general construction of a parametric representation, [46, Remark 12.3.3]) The basic idea for the parametrization is to ‘stretch’ time in a way that for every jump of we associate a subinterval of on which the scaled time component stays constant and increases (with respect to the partial order defined above) to match the values of at the endpoints of the chosen subinterval. Explicitly, let be the set of all the discontinuities of . For each pick a subinterval , . For every set and let be nondecreasing with respect to the partial order, such that and , (for example, Whitt suggested to take to be defined via a linear interpolation between and ). Do this in a way that holds if and only if . Let be a continuity point of . If is a limit of a subsequence of discontinuity points , set up and , where and . Finally, we are left with a collection of open intervals of the form on which is not defined. We use linear interpolation and set up

| (3.4) |

Note that whenever a jump occurs, time is stretched. This is the first hint for the connection we aim to establish in the next section.

3.2. The relationship between WM1 and the time-stretching

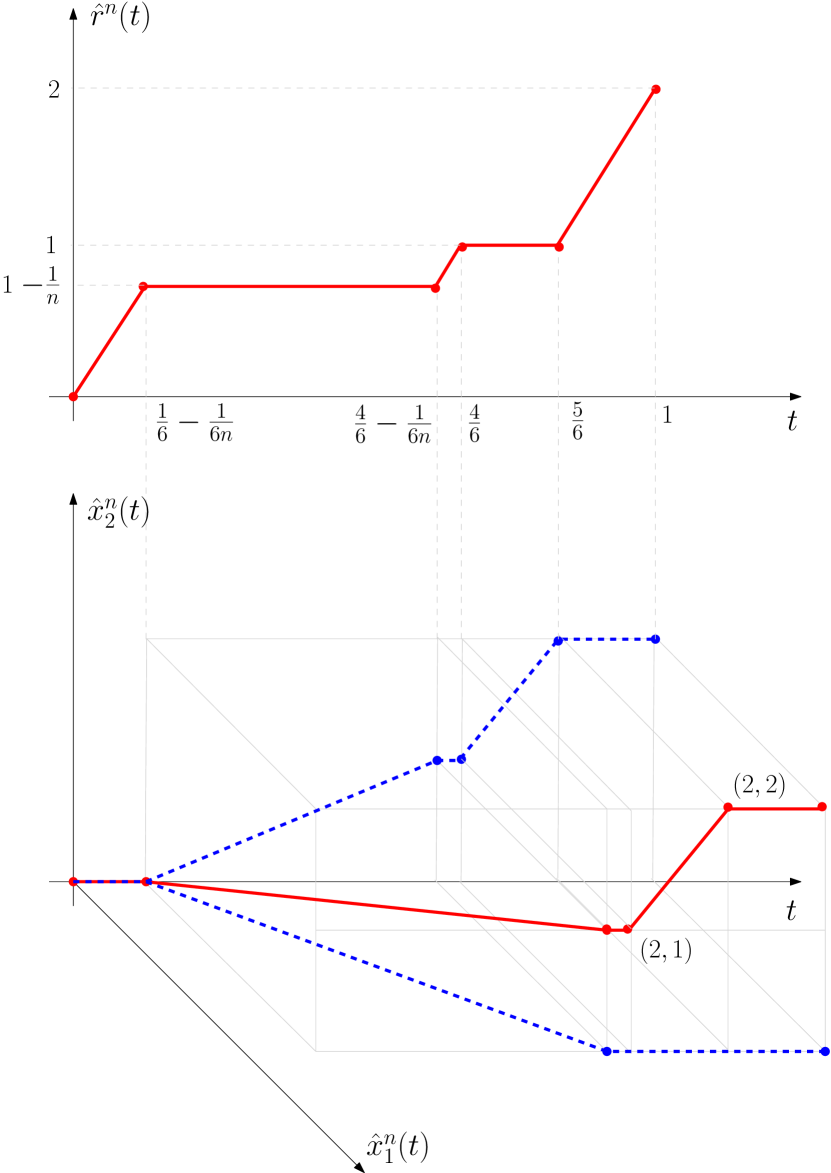

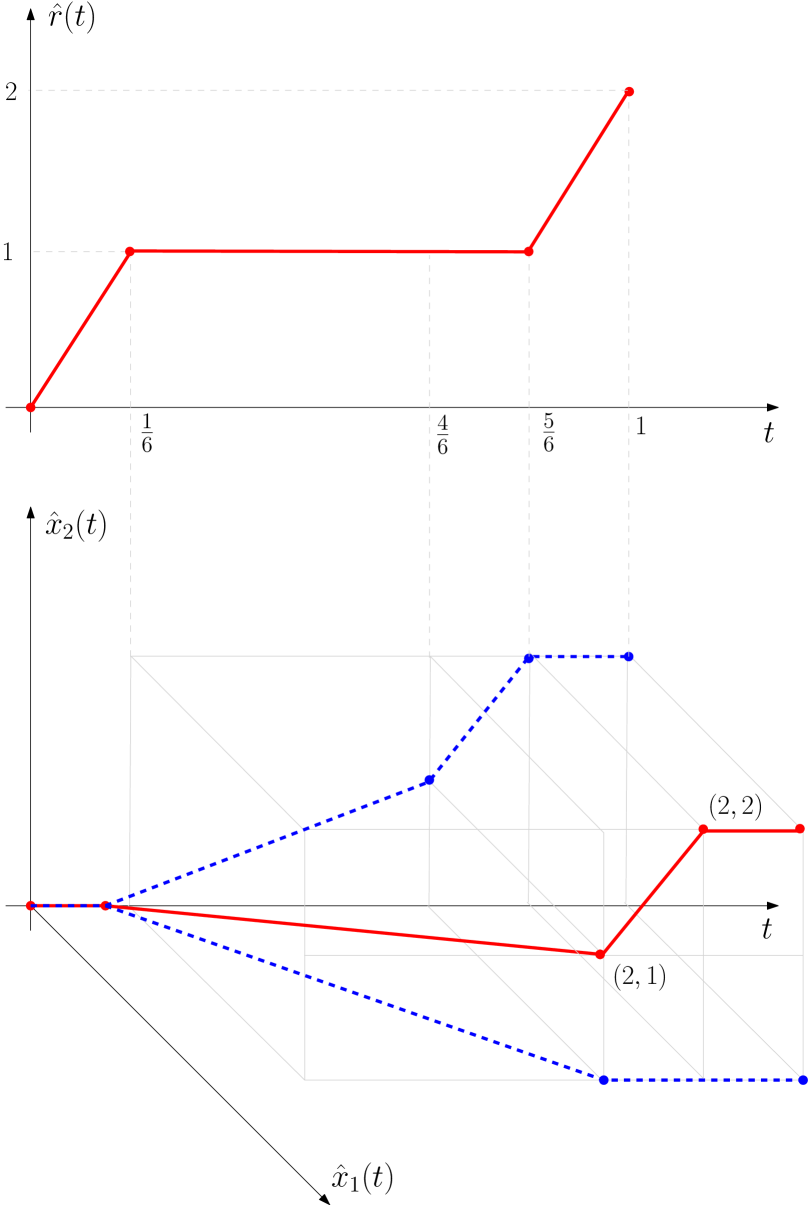

Before establishing the relationship in the general case, we provide an example for WM1 convergence in . This example also clarifies the weak parametric representation. The numbers are taken from [46, Example 12.3.1], where it is also shown that the convergence does not hold under the strong-M1 topology (on which we comment in Footnote 3). The weak parametric representations that we choose to work with are different than the ones Whitt used. The reason is that our constructionfollows the same way time is scaled in the time-stretching scheme, given in Section 2.1.

3.2.1. An illuminating example

Let be given by

The first observation is that . Hence, weak parametric representations only need to satisfy the continuity and monotonicity condition for and , with the initial-terminal conditions and . To this end we construct the representation by stretching time whenever a jump occurs in the same manner done in the time-stretching scheme, given in Section 2.1. The connection between this scheme and the parametric representation is discussed extensively immediately after the example. Following (2.5), define the function by

Next, define the left inverse of by

Also, set as follows.

Notice that and increase only when is flat. The structure of is consistent with the scheme given in Remark 3.1.

Now, the elements of the sequence are uniformly Lipschitz and uniformly converge to , given by,

This is indeed a weak parametric representation of . Observe that it is merely pathwise linear along the interval , on which is constant. The pathwise linearity is allowed of course by the definition of the thick graph. As can be seen from Figure 2, the form of is inherited by the forms of .333This is in fact what distinguishes the weak- from the strong-topology. In the strong topology, the thick graph is replaced by a thin graph (see the definition in [46, 12.(3.3)]) and our cannot be a part of a strong parametric representation. The reason is that under the strong topology, it must be linear along connecting and . The gap between these two functions indicate that the convergence holds only under WM1.

We now discuss about the connection between the weak parametric representation and the time-stretching scheme, which is given in Section 2.1.

Remark 3.2.

The functions and are equivalent versions of , , , , , , and , respectively. Indeed, for any , , hence (2.1) holds with and . However, there are some differences that follow one after the other. The first one is that we construct a weak parametric representation for the noncontinuous function itself and not for an approximating continuous function. This yields the second difference: the functions are not strictly increasing, unlike . This in turn leads to the third difference: the function is defined by a linear interpolation on intervals on which is constant as described in Remark 3.1, and not by as done in the stochastic problem when setting up . Nevertheless, when going back to the original scale both methods work in the same way. In point (iv) in Section 2.1 one defines , where and in our setting as well , where , see (3.3). The minimum with comes since we consider a finite time-horizon, unlike [8].

This comparison confirms that, indeed, in the stochastic model, one may avoid the continuous controls approximation (Step (i) in Section 2.1) and define the time-stretched processes using linear interpolation on intervals where is constant. Clearly, the notation becomes heavier in this case and this procedure is less favorable than the one that asserts Step (i).

3.2.2. Establishing the relationship in the general case

The arguments for the general case are similar and are now explicitly provided. We choose to work with RCLL functions whose increments are not restricted to the cone . Thus, we work with the total variation , see Remark 3.3 for more details. Consider a relatively compact sequence under the WM1 topology, which is also uniformly bounded in total variation. By reducing to a subsequence, which is relabeled by , consider such that as . We now set up a weak representation in the same way done in the last example, which is consistent with the definitions of and from (2.5). Denote by the total variations of between and , and set

| (3.5) |

Define its left-inverse

| (3.6) |

The decision of working with the total variation and is justified in Remark 3.3 below. The first observation is that , and is nondecreasing. Next, observe that jumps together with . Each jump of then leads to a corresponding interval on which is constant. Hence, one can set up by a linear interpolation as suggested in Remark 3.1 so that is a weak-representation parameterization of . By the right continuity of and the continuity of , the following identity holds . Hence, by (3.3),

| (3.7) |

This is the equivalence of (2.6). Indeed, the continuity of there, implies that , hence .

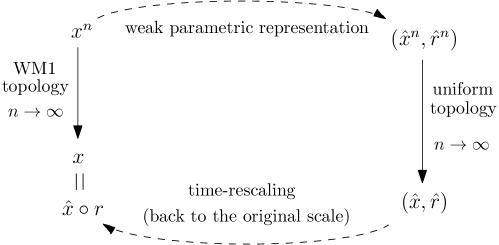

In the next theorem we show that in the limit , one obtains the equivalence of (2.7). Hence, establishing the desired connection. This is illustrated in Figure 3. Compare it with Figure 1.

Theorem 3.1.

Fix which are uniformly bounded in total variation. For any , let and be given by (3.5)–(3.6). Also, set according to the scheme given in Remark 3.1 with respect to . Then the sequence is relatively compact under the uniform topology. Consider a limit point attained via the subsequence and set , . Then,

-

(1)

for , implies that ;

-

(2)

if in addition each is nondecreasing component-wise, then is a parametric representation of and consequently, .

Remark 3.3.

-

(1)

Comparing with (2.5), we choose to work here with the total variation, which is nondecreasing in time. The rationale behind this choice is that for any function with increments in , satisfying , and for any , the following holds

(3.8) So setting up with the total variation is equivalent to the setting with . The first inequality follows from (2.1) since for any partition , one has

Taking the supremum over all the partitions, one obtains the desired inequality.

-

(2)

The uniform bound of the total variations assumed in the theorem is essential to attain uniform Lipschitzity of and as a result relatively compactness. In light of (3.8), this property holds with high probability in the time-stretching method used in the stochastic model [8]. This leads to relatively compactness of the stretched processes.

-

(3)

The main goal of Theorem 3.1 is to show that the time-stretching scheme is embedded within the definition of the WM1 topology. A careful look at the first part of the theorem reveals that we do not claim that is a parametric representation of . To obtain such a result one needs to account for the sensitivity of the WM1 topology with respect to the order on the thick graph. Hence, it is not sufficient to only have the uniform convergence . The second part confirms that this is the case for monotonic functions. The general case is outside the scope of this paper and is left for future research.

-

(4)

Theorem 3.1 is analogous to [29, Theorem 1.1]. Indeed, and there can be taken to be and . As a result there, would be . The reader is also referred to Remark 1.2 in the same paper, which states (in an infinite horizon setup):

“It is tempting to define a notion of convergence which states that if there exist and nondecreasing, continuous RCLL functions with and such that and in the Skorokhod (J1) topology. Unfortunately, this notion of convergence does not correspond to a metric.”

The definition of , using the weak parametric representation, is more conservative since it uses the uniform norm instead of the J1 topology and since the weak parametric representation is defined using a weak order defined on the thick graph. Yet, as mentioned earlier, is not a metric. However, as will be discussed in Section 3.2 there is a metric that induces the same topology.

Proof of Theorem 3.1.

1. The uniform bound of the total variations leads to the following inequality, which holds for any and ,

This in turn implies that are uniformly Lipschitz. Hence, this sequence is tight under the uniform topology, and as a consequence, it has a convergence subsequence. Take a limit point along a subsequence, which we relabel by . In order to show that the RCLL functions and are equal, it is sufficient to show that for any bounded and continuous ,

From (3.3), , . Hence, to this end, it is sufficient to show that

| (3.9) |

and

| (3.10) |

Fix a bounded and continuous . The definition of implies that for every which is a continuity point of , the convergence holds444This is explicitly stated in Proposition 3.1 (iii) below. and by the continuity of , also . Since the set of discontinuity points is at most countable, we get by the bounded convergence theorem that (3.9) holds.

Next, [37, Theorem IV.45] implies that

By [14, Lemma 2.4] the r.h.s. of the above converges to , which by [37, Theorem IV.45] again equals . This proves (3.10) and finishes the proof.

2. Now we assume in addition that each is nondecreasing component-wise. Then, so are , and by definition, also . As a consequence is nondecreasing, and clearly also . Finally, the composition is nondecreasing. To verify that is a weak parametric representation of we need to show that for any and , the followin two conditions hold:

By the definition of , . The monotonicity of implies that

where the equality follows by the definition of . Similarly, by the monotonicity of and the inequality it follows that

This establishes the two requirements and as a consequence is a parametric representation of . Finally, as ,

∎

3.3. Oscillation and compactness

In this section we set up some oscillation functions and use them in order to establish compactness results, which are necessary for the proof of Theorem 2.1. Some of the results in [46], e.g., Theorem 12.12.2, require that the functions in are continuous at the boundary points and . This is not part of the requirements for (thus nor for as well) mentioned in Definition 2.1, hence should be avoided. Furthermore, recall that we assumed and . To this end, we slightly modify some of the definitions given in [46] and work on a closed interval whose interior contains , for simplicity we consider the interval . Set up555In Remark 3.4 below we mention cases where the continuity at time is not required and comment about the infinite horizon and discounted problem.

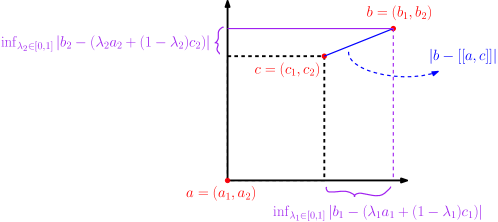

Now, for any , , and define, respectively, the oscillation function and the WM1-oscillation of around by

where is the Euclidean distance between the point and a subset in . Also, set up

| (3.11) |

Define also the set of discontinuities of by Disc. Finally, define the metric on , by

where is given by (3.2) with the dimension . This is the metric that induces the product topology. From the second representation in (3.1) it follows that . That is, the product topology is not stronger than the weak topology. The next theorem claims that the two topologies coincide. As a byproduct, we obtain that the weak topology is metrizable. The next proposition provides equivalent characterizations for the WM1 convergence.

Proposition 3.1.

(Theorem 12.5.2 in [46]) The following are equivalent characterizations of as in the WM1 topology of .

-

(i)

as .

-

(ii)

as .

-

(iii)

as for every and

-

(iv)

as ; for every

and for every

Corollary 3.1.

Let . If and converges to in the uniform norm, then .

Proof.

Part (iv) of the previous proposition holds true for and . From the uniform convergence of to we clearly have and for every ,

Moreover, using that is continuous, one gets that for every ,

where . Hence,

and part (iv) of the previous proposition holds true for and , hence, as .

∎

Next, we provide a characterization of compactness.

Proposition 3.2.

An important observation is that for every function with nondecreasing components in the sense that is nondecreasing for each , one has . Hence for compactness, it is sufficient to verify only (3.12). This is summarized in the next corollary.

Corollary 3.2.

Fix . The set

is compact under the WM1 topology.

We end this section by establishing the connection to probability. For this, we claim that WM1 is a polish space. Indeed, the WM1 topology of is:

-

(i)

metrizable by ;

-

(ii)

separable, since under the J1 topology is separable and is a richer topology than M1;

-

(iii)

complete. To this end, recall that is complete under the strong-M1 topology, see [46, Theorem 12.8.1], and that the strong- and weak-M1 topologies coincide in dimension one. Hence, by the definition of given above, the product topology on is complete. By the equivalence of the product topology and the WM1 topology for the multidimensional case, one obtains the completeness of WM1.

Hence, Prohorov’s theorem applies and tightness is equivalent to relatively compactness, see [6, Theorems 5.1 and 5.2]

Proposition 3.3.

(Theorem 12.12.3 in [46]) A sequence of probability measures on is tight under the WM1 topology if and only if

| (3.13) |

and for every ,

| (3.14) |

Remark 3.4.

If we restrict the admissible controls to ones for which , that is, there is no jump at the terminal time , or alternatively, if the cost function does not depend on the time instant and equals

then one may work with the space

Now, for an infinite horizon and discounted control problem, one may use the metric

where and are the restrictions of and to the interval , and is the metric given by (3.2) adjusted to .

4. Proof of Theorem 2.1 using the WM1 topology

From Corollary 3.2 it follows that the WM1 topology can handle quite easily nondecreasing processes (component-wise). Hence, in case that the processes and are nondecreasing then (3.14) holds trivially. So, in order to establish compactness we only need to verify (3.13). These monotone properties follow if and lie in the nonnegative orthants. The first observation is that, without loss of generality, we may assume the latter. Indeed, the conditions imposed in (2.1) imply that and are subsets of convex polyhedral cones with and faces, respectively, which can be linearly transformed into the nonnegative orthant. Hence, and can be mapped, by a linear and invertible map into the nonnegative orthant. Identify this linear transformation by an invertible matrix and denote . Then the process can be expressed by for some process with increments in the nonnegative orthant of . Similarly, there is a regular matrix , with finite norm , such that lies in the nonnegative orthant, where . Set,

All together, the new state process satisfies

Similarly, set up the new cost components

and . Assumption 2.1 clearly holds now with , , and . Assumption 2.2 holds for the new components, where the Lipschitz continuity follows since has a finite norm. The invertibility of and enables to go back from the new problem to the original one. Also, the conditions (b) and (c) in Assumption (), regarding the function , are translated now to .

Another geometric way to look at it is that there are at most vectors in such that any point in the cone is a linear combination of these vectors with nonnegative coefficients. These vectors point to ‘extreme’ directions (being at the boundary of the cone) of the jumps, and the coefficients, being nonnegative, mean that jumps always go in the same directions component-wise. For illustration, consider the cone from Figure 4. Each point in this cone is indeed a nonnegative combination of the (extreme) vectors and .

Following the discussion above, in the rest of the proof we assume without loss of generality that

| (4.1) |

Hence,

In order to establish the existence of an optimal control, we start with a sequence of asymptotic optimal controls. Then we show that this sequence is relatively compact under the WM1 topology, hence has a converging subsequence and that any of its limit points is an optimal control (Proposition 4.1). Specifically, we consider a sequence of admissible singular controls such that

| (4.2) |

Before arguing its tightness (under WM1), we prove that the control and the state processes have finite moments. These bounds serve us in the proofs of the next three Propositions.Let be the expectation with respect to the measure .

Lemma 4.1.

Proof.

First, note that in all three cases (a)–(c), the first bound in (4.3) implies the second one. This follows by (2.2), the boundedness of and , the BDG inequality applied to , the monotonicity of , and the first bound in (4.3). Hence, it remains to prove the first bound and we do it case by case.

Throughout the proof refers to a positive constant, independent of and , and which can change from one line to the next. We start with case (a). Recall Assumptions () and (). Burkholder–Davis–Gundy (BDG) inequality applied to implies that

| (4.4) |

Then, the conditions in (a) and both parts of (4.4) imply the following two inequalities, respectively,

| (4.5) | ||||

Isolating in the above, one gets that

where the first inequality follows since is nondecreasing, and the second inequality follows since by (4.2), and since . By Young’s inequality and since , it follows that (4.3) holds.

The proof in case (b) is similar only that in (4.5) on the second and third lines the term is replaced by 0. This is true, since in case (b), . The rest of the proof follows the same lines.

Set the processes

Proposition 4.1.

The sequence is relatively compact under the WM1 topology.666In fact, one can establish -tightness of under the J1 topology.

Proof.

Recall that WM1 is metrizable (see Section 3.3). Hence Prohorov’s theorem holds and relatively compactness is equivalent to tightness. Now, . Hence, in order to establish the tightness of it is sufficient to show that each of the components in this sequence is tight. We start with establishing the tightness of the sequence of measures . To this end, it follows from Proposition 3.3 that it is sufficient to show that

and that for every ,

| (4.6) |

The first limit holds by Markov inequality and the second bound in (4.3). In order to establish (4.6) observe first that the monotonicity of implies that for any , and satisfying , one has

where the first inequality follows by the definition of the product segment and the distance between a point and a set; this is illustrated in Figure 5. The second inequality follows by the triangle inequality, and the last inequality follows by the monotonicity of . Again, the boundedness of and and the BDG inequality imply that

for some constant , independent of and . Markov inequality implies (4.6). The tightness of follows by the same arguments.

We now identify the limit points of . Let , be a limit point. By Skorokhod’s representation theorem and by reducing to a subsequence, which we relabel by , we may consider a probability space that supports a sequence of processes and the processes , such that

| (4.7) | ||||

and

| (4.8) |

Specifically, -almost surely (a.s), for every , , where

| (4.9) |

Also, set the filtration

At this point it is worth pointing out that the processes , and consequently , may have jumps, which may occur in different times than the ones of and , respectively.

Proposition 4.2.

The processes , , ,and satisfy -a.s., for every ,

| (4.10) | ||||

| (4.11) | ||||

| (4.12) |

where is a -Wiener process. Furthermore, -a.s., has increments in , and for all .

Proof.

The convergence (4.8) implies the convergence of each of the components under the metric . The next observation is that by Proposition 3.1(iii) the convergence implies the convergence of for any continuity point of and . Therefore, the Portmanteau theorem [6, Theorem 2.1] implies that (4.10) holds.

To prove (4.11) we use martingale arguments. For every twice continuously differentiable function , set

where and are, respectively, the gradient and the Hessian of . Also, set the processes

Once we show that is a -martingale for , , where and it follows by the same arguments given in the proof of Proposition 5.4.6 in [25], that there exists a -Wiener process, , such that, , -a.s.

We show that is a -martingale, providing the details for for arbitrary . The proof for the case is simpler, hence omitted. Denote and let be a sequence of twice continuously differentiable functions satisfying:

-

•

for any , , and , ;

-

•

for any , together with its first and second order derivatives are bounded;

-

•

there is a constant such that for any and ,

(4.13)

Recall that is bounded. Hence, by [25, Proposition 5.4.2], for any , is a martingale with respect to the filtration

Thus,

Fix a continuous and bounded mapping , where the spaces and are endowed with the Borel -algebras, generated by the metrics and the Euclidean metric, respectively. Denote by , and the restrictions of , , , , , , and to the time interval . Then the above implies,

The first equality follows because the first term within the expectation is measurable with respect to . Taking expectations on both sides, we get

Take the limit on both sides, the bounded convergence theorem then implies that

From the above, together with (4.13) and the boundedness of , and , it follows that there is a constant , which may change from one line to the next, such that for any ,

| (4.14) | ||||

Fatou’s lemma implies that

where the last inequality follows by the boundedness of and and Cauchy–Schwartz and BDG’s inequalities. Taking on both sides and plugging in (4.14), one obtains that

We now show that since this equality holds for every bounded and continuous function , it follows that for any ,

which in turn implies that is a -martingale. To this end, note that for any there is a Borel set such that . Hence, it is sufficient to verify that , where is the Borel -algebra of with respect to the metric , and

Now, by Lemma A.1, for any open set , the indicator can be approximated by continuous functions. Therefore, contains the -system , where is the collection of all the open sets of . One can easily verify that is a -system. Hence, by the - theorem, .

The next proposition points out an optimal control, hence establishing Theorem 2.1.

Proposition 4.3.

The control is optimal.

Proof.

From Proposition 4.2 it follows that is admissible. Hence, we only need to show that its associated cost equals . By (4.2) and (4.7) it is sufficient to show that

| (4.15) |

and

| (4.16) |

The analysis is different for each of the conditions (a), (b), and (c) in Assumption ().

We start with showing that under condition (a), (4.15) holds. By Proposition 3.1(iii) the convergence implies the convergence of for any continuity point of and . The Portmanteau theorem [6, Theorem 2.1] together with (4.1) imply that

| (4.17) |

Since is continuous and bounded (see Assumption ()), the bounded convergence theorem implies that

Since is nondecreasing and is bounded it follows from Lemma 4.1 that

Since , -a.s., we have that and therefore,

Combining the last three limits, we obtain (4.15).

We now prove (4.15) in cases (b) and (c). As before, (4.17) holds. Using the nonnegativity of the integral, we get that

Fatou’s lemma implies

Taking , it follows by the monotone convergence theorem together with the nonnegativity of and the increments of that (4.15) holds.

We now turn to proving (4.16). Recall the growth assumptions on and in cases (a) and (b) and their continuity. Repeating the same arguments leading to (4.15) in case that (a) holds, where now using the -a.s. convergence , (3.9), the second bound in (4.3), and truncating by , we get that

In case that (c) holds, we may repeat the same arguments leading to (4.15) given under cases (b) and (c) in order to establish (4.16). ∎

Appendix A An auxiliary lemma

Lemma A.1.

Let be a metric space and let be the Borel -algebra endowed with the metric . Let be an open set. Then, there exists a sequence of continuous functions satisfying and pointwise, as .

Proof.

If or , then is continuous and the approximation is trivial.

Fix a nonempty open set and set , , where . Clearly, and . For sufficiently large , is not empty. For such ’s the following functions are well defined:

In particular, for and for . Then, and pointwise. The rest of the proof is dedicated to showing that each is continuous. Fix . The continuity at each point is verified separately for , , and .

-

•

Case 1: , which implies . Fix in a -neighborhood of . That is, . Then, , and therefore,

Note that implies . Together, with the continuity of at , it follows that as .

-

•

Case 2: , which implies . Fix again in a -neighborhood of . That is, . In this case, , and therefore,

Note that implies , and so .

-

•

Case 3: . Denote . Fix in an -neighborhood of . That is, . In this case, , and therefore,

In conclusion, is continuous at . ∎

Acknowledgments

The author is thankful to the anonymous referees and the AE for their valuable suggestions, which greatly helped him to improve the presentation of the paper. One of the referees pointed out several errors in a previous version of the paper and the author is gratitude for that.

References

- [1] S. Asmussen and M. Taksar. Controlled diffusion models for optimal dividend pay-out. Insurance Math. Econom., 20(1):1–15, 1997.

- [2] R. Atar and A. Budhiraja. Singular control with state constraints on unbounded domain. Ann. Probab., 34(5):1864–1909, 2006.

- [3] R. Atar and M. Shifrin. An asymptotic optimality result for the multiclass queue with finite buffers in heavy traffic. Stoch. Syst., 4(2):556–603, 2014.

- [4] B. Basrak and D. Krizmanić. A multivariate functional limit theorem in weak m1 topology. J. Theoret. Probab., 28(1):119–136, Mar 2015.

- [5] J. Bather and H. Chernoff. Sequential decisions in the control of a spaceship. In Fifth Berkeley Symposium on Mathematical Statistics and Probability, volume 3, pages 181–207, 1967.

- [6] P. Billingsley. Convergence of Probability Measures. Wiley Series in Probability and Statistics: Probability and Statistics. John Wiley & Sons Inc., New York, second edition, 1999. A Wiley-Interscience Publication.

- [7] A. Budhiraja and A. P. Ghosh. Diffusion approximations for controlled stochastic networks: an asymptotic bound for the value function. Ann. Appl. Probab., 16(4):1962–2006, 2006.

- [8] A. Budhiraja and K. Ross. Existence of optimal controls for singular control problems with state constraints. Ann. Appl. Probab., 16(4):2235–2255, 2006.

- [9] A. Budhiraja and K. Ross. Convergent numerical scheme for singular stochastic control with state constraints in a portfolio selection problem. SIAM J. Control Optim., 45(6):2169–2206, Jan. 2007.

- [10] A. Cohen. Asymptotic analysis of a multiclass queueing control problem under heavy traffic with model uncertainty. Stoch. Syst., 9(4):359–391, 2019.

- [11] A. Cohen. Brownian control problems for a multiclass M/M/1 queueing problem with model uncertainty. Math. Oper. Res., 44(2):739–766, 2019.

- [12] C. Costantini and T. G. Kurtz. Existence and uniqueness of reflecting diffusions in cusps. Electron. J. Probab., 23:Paper No. 84, 21, 2018.

- [13] C. Costantini and T. G. Kurtz. Markov selection for constrained martingale problems. Electron. J. Probab., 24:Paper No. 135, 31, 2019.

- [14] J. G. Dai and R. J. Williams. Existence and uniqueness of semimartingale reflecting brownian motions in convex polyhedrons. Theory Probab. Appl., 40(1):1–40, 1996.

- [15] M. H. Davis and A. R. Norman. Portfolio selection with transaction costs. Math. Oper. Res., 15(4):676–713, 1990.

- [16] F. Delarue, J. Inglis, S. Rubenthaler, and E. Tanré. Particle systems with a singular mean-field self-excitation. application to neuronal networks. Stochastic Process. Appl., 125(6):2451 – 2492, 2015.

- [17] G. Fu. Extended mean field games with singular controls. arXiv e-prints, page arXiv:1909.04154, Sep 2019.

- [18] G. Fu and U. Horst. Mean field games with singular controls. SIAM J. Control Optim., 55(6):3833–3868, 2017.

- [19] G. Fu and U. Horst. Multi-dimensional mean field games with singular controls. Technical note, 2017.

- [20] J. M. Harrison. Brownian models of queueing networks with heterogeneous customer populations. In Stochastic differential systems, stochastic control theory and applications (Minneapolis, Minn., 1986), volume 10 of IMA Vol. Math. Appl., pages 147–186. Springer, New York, 1988.

- [21] J. M. Harrison and M. I. Taksar. Instantaneous control of Brownian motion. Math. Oper. Res., 8(3):439–453, 1983.

- [22] J. M. Harrison and J. A. Van Mieghem. Dynamic control of Brownian networks: state space collapse and equivalent workload formulations. Ann. Appl. Probab., 7(3):747–771, 1997.

- [23] J. M. Harrison and R. J. Williams. A multiclass closed queueing network with unconventional heavy traffic behavior. Ann. Appl. Probab., 6(1):1–47, 1996.

- [24] J. M. Harrison and R. J. Williams. Workload reduction of a generalized Brownian network. Ann. Appl. Probab., 15(4):2255–2295, 2005.

- [25] I. Karatzas and S. E. Shreve. Brownian motion and stochastic calculus, volume 113 of Graduate Texts in Mathematics. Springer-Verlag, New York, second edition, 1991.

- [26] O. Kella and W. Whitt. Diffusion approximations for queues with server vacations. Adv. in Appl. Probab., 22(3):706–729, 1990.

- [27] T. G. Kurtz. Martingale problems for constrained Markov problems. In Recent advances in stochastic calculus (College Park, MD, 1987), Progr. Automat. Info. Systems, pages 151–168. Springer, New York, 1990.

- [28] T. G. Kurtz. A control formulation for constrained Markov processes. In Mathematics of random media (Blacksburg, VA, 1989), volume 27 of Lectures in Appl. Math., pages 139–150. Amer. Math. Soc., Providence, RI, 1991.

- [29] T. G. Kurtz. Random time changes and convergence in distribution under the Meyer-Zheng conditions. Ann. Probab., 19(3):1010–1034, 1991.

- [30] T. G. Kurtz and R. H. Stockbridge. Stationary solutions and forward equations for controlled and singular martingale problems. Electron. J. Probab., 6:no. 17, 52, 2001.

- [31] H. J. Kushner and L. F. Martins. Numerical methods for stochastic singular control problems. SIAM J. Control Optim., 29(6):1443–1475, 1991.

- [32] A. Mandelbaum and W. A. Massey. Strong approximations for time-dependent queues. Math. Oper. Res., 20(1):33–64, 1995.

- [33] L. F. Martins and H. J. Kushner. Routing and singular control for queueing networks in heavy traffic. SIAM J. Control Optim., 28(5):1209–1233, 1990.

- [34] P.-A. Meyer and W. A. Zheng. Tightness criteria for laws of semimartingales. Ann. Inst. H. Poincaré Probab. Statist., 20(4):353–372, 1984.

- [35] S. Nadtochiy and M. Shkolnikov. Particle systems with singular interaction through hitting times: Application in systemic risk modeling. Ann. Appl. Probab., 29(1):89–129, 02 2019.

- [36] G. Pang and W. Whitt. Continuity of a queueing integral representation in the m1 topology. Ann. Appl. Probab., 20(1):214–237, 2010.

- [37] P. E. Protter. Stochastic integration and differential equations, volume 21 of Applications of Mathematics (New York). Springer-Verlag, Berlin, second edition, 2004. Stochastic Modelling and Applied Probability.

- [38] A. A. Puhalskii and W. Whitt. Functional large deviation principles for first-passage-time processes. Ann. Appl. Probab., 7(2):362–381, 1997.

- [39] A. A. Puhalskii and W. Whitt. Functional large deviation principles for waiting and departure processes. Probab. Engrg. Inform. Sci., 12(4):479–507, 1998.

- [40] S. Resnick and E. van den Berg. Weak convergence of high-speed network traffic models. J. Appl. Probability, 37(2):575–597, 2000.

- [41] S. E. Shreve and H. M. Soner. A free boundary problem related to singular stochastic control. In Proceedings of Imperial College Workshop on Applied Stochastic Analysis. Citeseer, 1990.

- [42] A. V. Skorokhod. Limit theorems for stochastic processes. Theory Probab. Appl., 1(3):261–290, 1956.

- [43] H. M. Soner and S. E. Shreve. Regularity of the value function for a two-dimensional singular stochastic control problem. SIAM J. Control Optim., 27(4):876–907, 1989.

- [44] W. Whitt. Weak convergence of first passage time processes. J. Appl. Probability, 8(2):417–422, 1971.

- [45] W. Whitt. Limits for cumulative input processes to queues. Probab. Engrg. Inform. Sci., 14(2):123–150, 2000.

- [46] W. Whitt. Stochastic-process limits. Springer Series in Operations Research. Springer-Verlag, New York, 2002. An introduction to stochastic-process limits and their application to queues.

- [47] M. J. Wichura. Functional laws of the iterated logarithm for the partial sums of iid random variables in the domain of attraction of a completely asymmetric stable law. Ann. Probab., 2(6):1108–1138, 1974.