Uniform minimum risk equivariant estimates for moment condition models

Michel Broniatowski1, Jana Jurečková2 and Amor KEZIOU31 LPSM, Sorbonne-Université, Paris, France

michel.broniatowski@upmc.fr

2The Czech Academy of Sciences, Institute of Information

Theory and Automation, Prague, Czech Republic

jureckova@karlin.mff.cuni.cz

3Laboratoire de Mathématiques de Reims, France

amor.keziou@univ-reims.fr

(Date: April, 2019)

Abstract.

We consider semiparametric moment condition models invariant to

transformation groups. The parameter of interest is estimated by minimum

empirical divergence approach, introduced by Broniatowski and Keziou (2012). It is

shown that the minimum empirical divergence estimates, including the

empirical likelihood one, are equivariants. The minimum risk equivariant

estimate is then identified to be any one of the minimum empirical

divergence estimates minus its expectation conditionally to maximal

invariant statistic of the considered group of transformations. An

asymptotic approximation to the conditional expectation, is obtained, using

the result of Jurečková and Picek (2009).

AMS Subject Classifications:62F10, 62F30, 62F99 Keywords : Pitman estimator, semiparametric

model, equivariant estimator

1. Introduction

The semiparametric moment condition models are defined through

estimating equations

where denotes the mathematical expectation, is a random vector, is the unknown true value of the parameter

of interest which is assumed to be unique, and is some specified

measurable -valued function defined on . Such models are popular in statistics and econometrics, see e.g.,

Qin and Lawless (1994), Haberman (1984), Sheehy (1987),

McCullagh and Nelder (1983), Owen (2001) and the references therein.

Denoting the probability distribution of the

random vector , then the above estimating equations can be

written as

Let be the collection of all signed finite measures (s.f.m.) on

the Borel -field such

that . The submodel ,

associated to a given value , consists of all

s.f.m.’s satisfying linear constraints induced by the

vector valued function ,

namely,

with . The statistical model which we consider can be written as

(1)

Let be an i.i.d.

sample of the random vector with unknown

probability distribution . The problems of

testing the model ,

confidence region and point estimations of , have

been widely investigated in the literature. Hansen (1982) considered

generalized method of moments (GMM) in order to estimate . Hansen et al. (1996) introduced the continuous updating (CU)

estimate. Asymptotic confidence regions for the parameter have been obtained by Owen (1988) and Owen (1990), introducing

the empirical likelihood (EL) approach. It has been used, in the context of

model (1), by Qin and Lawless (1994) and Imbens (1997)

introducing the EL estimate for the parameter . The

recent literature in econometrics focusses on such models; Smith (1997),

Newey and Smith (2004) provided a class of estimates called generalized

empirical likelihood (GEL) estimates which contains the EL and the CU ones.

Among other results pertaining to EL, Newey and Smith (2004) stated that EL

estimate enjoys asymptotic optimality properties in term of efficiency when

bias corrected among all GEL estimates including the GMM one. Broniatowski and Keziou (2012) proposed a general approach through empirical

divergences and duality technique which includes the above methods in the

general context of signed finite measures under moment condition models (1). These approach allows the asymptotic study of the estimates

and associated test statistics both under the model and under

misspecification, leading to new results, in particular, for the EL

approach. Note that all the proposed estimates including the EL one are

generally biased, and that the problem of their finite sample efficiency, at

our knowledge, have not yet been studied.

The aim of the present paper is to investigate the finite-sample optimality

property estimation in the context of semiparametric model (1). We will discuss the problem of constructing minimum risk equivariant

estimates (MRE) for the parameter , as well as the

problem of the numerical calculation of these estimates.

We recall in the following lines, for the above estimation problem, the

notions of group transformations on the random vector space, model

invariance and the induced group of transformations on the parameter space,

loss invariance and equivariance estimation; we refer to the unpublished

preprint of Hoff (2012) for an excellent presentation of the

above notions, and the book of Lehmann and Casella (1998).

Let be a collection, of one-to-one transformations from the

vector space in , which we assume to be a

“group”, in the sense that, it should be closed under both composition and

inversion, namely,

The group can be extended to a group of transformations on the

sample space, onto , which will be denoted , as follows

We will consider two kinds of transformation groups,

“additive”

(2)

where is some subset of ,

or

“multiplicative”

(3)

where is diagonal matrix, with

entries or with possibly some entries equal to one.

We assume that the model given in (1) is

invariant under the considered group of transformations , in

the sense that,

(4)

The induced group of transformations on the parameter space, onto , denoted hereafter, will be defined as

follows. Let be any transformation belonging to , and

consider any random vector such that . Then, by identifiability assumption, there exists a unique

such that . By invariance assumption (4), of the model to the group , the distribution belongs to . Therefore, there exists a

unique (by indentifiability) such

that .

Denote then by the bijection induced by on the parameter

space onto , defined by

The induced group on the parameter space, onto , is then

defined to be

Two points are said

equivalent iff

for some The orbit , of a point , is

defined to be the set of equivalent points:

We will assume that there is only one orbit of , i.e.,

(5)

which means that the group of transformation is

rich enough allowing to go from any point in to another via some

transformation . In such case, the

group is said to be “transitive” over .

We give here some examples for illustration. In all the examples below, we

can see that the group is transitive over .

Example 1.

Sometimes we have information relating the first and

second moments of a random variable (see e.g. Godambe and Thompson (1989) and McCullagh and Nelder (1983)). Let be an i.i.d. sample of a random variable

with mean , and assume that , where is a known function. Our aim is to estimate . The information about the distribution of can be

expressed in the form of (1) by taking If we take the

parameter space to be , then it is straightforward to see

that the model is invariant to the additive group of

transformations

if for some , and invariant to the

multiplicative group

if for some .The induced groups on the

parameter space are, respectively,

and

Example 2.

Let be an i.i.d. sample of a bivariate

random vector with . In this case, we can take If we consider ,

then the model is invariant with respect to the groups

or

The induced groups on are, respectively,

and

A some what similar problem is when is known, and is to be estimated, by taking Such problems are common in survey

sampling (see e.g. Kuk and Mak (1989) and Chen and Qin (1993)). Taking , the model is then invariant with respect

to the groups

or

The induced groups on are, respectively,

and

Example 3.

Let be an i.i.d. sample of a random

variable with distribution such that , where , . The known intervals may be bounded or unbounded, and are known

nonnegative numbers. The information about can be written under the

form of model (1) taking and .

The model in this case is invariant to the groups

or

and the induced groups on the parameter space are, respectively,

and

Example 4.

Let be an i.i.d. sample of a random

variable with continuous distribution such that , and , where is known and is to be estimated. Note that is the quantile of order of the variable , and that the variance of is assumed to be

known and equal to one. This problem can be written under the form of model (1) taking and . The model in this case is invariant with respect to the additive group

and the induced group on is

Example 5.

Let be an i.i.d. sample of a random

variable with continuous distribution such that and , where is known and is to be

estimated. Note that is the quantile of order of the

variable . This problem can be written under the form of model (1) taking and . The

model in this case is invariant with respect to the

multiplicative group

and the induced group on is

Example 6.

Let be an

i.i.d. sample of a random vector with

continuous distribution such that , where is some specified measurable function, and is to be estimated. We can consider also the

case where some components of are known and that the

other components are to be estimated. It is clear that the corresponding

model defined in (1), taking and , is invariant to the additive group

and the induced group on the parameter is

Likewise, if the data are such that , where is some specified measurable function, and is to be estimated, then the

corresponding model , taking , is invariant to the multiplicative group

and the induced group on the parameter is

In all the sequel, without loss of generality, we assume that the model and the group of transformation are such

that

(6)

Note that this assumption implies the condition (4)

that the model is invariant under .

In all the following, when estimating by an estimate

, we consider the quadratic loss function

(7)

if the model is invariant with respect to additive group, and the loss

function is taken to be relative quadratic

(8)

if the model is invariant with respect to the multiplicative group.

Definition 7.

(invariant loss under a group of transformations). A loss function , where denotes

the set of the parameter estimates (called decision space), is invariant

under a transformation iff for any estimate ,

there exists a unique such that We denote then by

the bijection, from onto , such that . Hence, we have

We denote by the induced group on the decision

space .

Definition 8.

Assume that the estimation problem is invariant under

the group . Let and be, respectively, the induced groups on the parameter space and the decision space . An estimate is said to be

equivariant iff

We will see, under condition (6), that the empirical

minimum divergence estimates, introduced in Broniatowski and Keziou (2012), are

equivariant for the above models, using results on the existence and

characterization of the distribution ont the sets . First, we recall the definition of -divergences and some of their properties. Let be a

convex function from onto with ,

and such that its domain, is an interval, with

endpoints satisfying , which may be bounded or unbounded, open or

not. We assume that is closed; the closedness of means

that if or are finite then when , and when . Note that,

this is equivalent to the fact that the level sets , , are closed in endowed with the usual topology. For any s.f.m. , the -divergence between and a probability distribution , when is absolutely continuous with respect to (a.c.w.r.t) , is defined

through

(9)

where is the Radon-Nikodym derivative of w.r.t. . When is not a.c.w.r.t. , we set . For

any probability distribution , the mapping is convex and takes nonnegative values. When then . Furthermore, if the function is

strictly convex on a neighborhood of , then we have

(10)

All the above properties are presented in Csiszár (1963), Csiszár (1967) and in Chapter 1 of Liese and Vajda (1987), for divergences defined on the set of all probability distributions .

When the -divergences are extended to , then the same

arguments as developed on hold. When defined on , the

Kullback-Leibler , modified Kullback-Leibler , ,

modified , Hellinger , and

divergences are respectively associated to the convex functions , , , , and . All these divergences

except the one, belong to the class of the so-called power

divergences introduced in Cressie and Read (1984) (see also Liese and Vajda (1987) and Pardo (2006)). They are defined through the

class of convex functions

(11)

if , and . So, the divergence is associated to , the to ,

the to , the to and

the Hellinger distance to . We extend the definition of the

power divergences functions

onto the whole set of signed finite measures as follows. When the

function is not defined on or

when is defined on but is not convex (for

instance if ), we extend the definition of as

follows

(12)

Note that for -divergence, the corresponding function is convex and defined on whole .

In this paper, for technical considerations, we assume that the functions are strictly convex on their domain , twice continuously

differentiable on , the interior of their domain. Hence, , and for all , . Here, and are used

to denote respectively the first and the second derivative functions of . Note that the above assumptions on are not restrictive,

and that all the power functions , see (12), satisfy the above conditions, including all standard

divergences.

2. Minimum empirical divergence estimates

Let denote an i.i.d.

sample of a random vector with probability

distribution . Let be the associated

empirical measure, namely,

where denotes the Dirac measure at point , for all . For a given ,

the “plug-in” estimate of is

(13)

If the projection of on exists, then it is clear that is a s.f.m. (or possibly a probability distribution) a.c.w.r.t. ; this means that the support of must be

included in the set . So, define the set

(14)

which may be seen as a subset of . Then, the plug-in estimate (13) can be written as

(15)

In the same way,

can be estimated by

(16)

By uniqueness of and since the infimum

is reached in , we estimate through

(17)

The expression of the estimate , given in (15), is

the solution of a convex optimization problem under convex constrained

subset in . In order to transform this problem to an

unconstrained one, we will make use of the Fenchel-Lengendre transform,

denoted , of the convex function , as well

as some other duality arguments. It is defined by

(18)

For convenience, we recall some properties of the convex conjugate

of . For the proofs we can refer to Section 26 in Rockafellar (1970). Theses properties will be used to determine the convex

conjugates of some standard divergence functions ; see

Table 1 below. The function in turn

is convex and closed, its domain is an interval with endpoints

(19)

satisfying with . Note that the interval

can be different from , the real domain of given by (19). This holds when or is finite and or is finite, respectively. For

example, for the convex function

we have and , and

we can see that the domain of the corresponding -function is which is different from The two

intervals and coincide if the

function is “essentially smooth”, i.e., differentiable with

(20)

The strict convexity of on its domain is equivalent to the

condition that its conjugate is essentially smooth, i.e.,

differentiable with

(21)

Conversely, is essentially smooth on its domain if and

only if is strictly convex on its domain .

In all the sequel, we assume additionally that is

essentially smooth. Hence, is strictly convex on its domain , and it holds that

and

(22)

where denotes the inverse of the derivative

function of . It holds also that is

twice continuously differentiable on with

(23)

In particular, and . Obviously, since is assumed to be closed, we have

which may be finite or infinite. Hence, by closedness of ,

likewise we have

Finally, the first and second derivatives of in and are

defined to be the limits of and when and when . The first and

second derivatives of in and are defined in a

similar way. In Table 1, using the above

properties, we give the convex conjugates of some standard

divergence functions , associated to standard divergences. We

determine also their domains, respectively, and .

Table 1. Convex conjugates of some standard divergence

functions .

Using some duality arguments, see Broniatowski and Keziou (2012), we can

show that, for any , if there exists in such that

(24)

then

(25)

with dual attainment. Conversely, if there exists some dual optimal solution

such that

(26)

then the equality (25) holds, and the unique optimal

solution of the primal problem

namely, the projection of on , is given by

(27)

where is solution of the system of equations

(28)

In view of the last results, using the notations

and

we obtain the following equivalent expressions to the estimates , and , see (13), (16) and (17),

(29)

(30)

(31)

(32)

and

(33)

Remark 9.

The empirical likelihood estimate is obtained for

the particular choice of the modified Kullback-Leibler divergence ,

namely, when . Moreover,

straightforward computation shows that , . Therefore, can be

omitted, and the above expression can be simplified to

and

We will show that for any divergence , the estimate is invariant with respect to

loss for the additive group, and invariant with respect to loss for

the multiplicative group. First, we expose the asymptotic counterpart of the

estimates (29), (31) and (33). In particular, we give results about existence and characterization

of the projection of on the model . The characterization

of the projection will be of great importance in computing the minimum risk

equivariant estimate. We have; see Theorem 1 in Broniatowski and Keziou (2006):

Proposition 10.

Let be

a given value in . Assume that for all , and that there exists in such that and111The strict inequalities mean that

(34)

Then, we have

(35)

with dual attainment. Conversely, if there exists a dual optimal solution

belonging to the interior (in ) of the set

(36)

then the dual equality (35) holds, and the unique optimal

solution of the primal problem ,

namely, the projection of on , is given by

where is the solution of the system of

equations

(37)

Furthermore, the solution

is unique if the functions are linearly independent

in the sense that for all with

Remark 11.

By minimizing , upon , , we obtain the

semiparametric model of densities

where is the solution of the system of

equations (37). For the particular case of the -divergence,

namely, when , can be explicitly computed, and the obtained model is the semiparametric

exponential family of probability densities

(38)

where, for all , is the solution in of

the system of equations

(39)

or equivalently

Proposition 12.

Assume that condition (6) holds. Then, the minimum

empirical -divergence estimates are

equivariant

-

to the additive group of transformations with respect to the

loss;

-

to the multiplicative group of transformations with respect to the loss.

Moreover, in both cases, the induced group of transformations on the space of estimates is equal to , the group of transformations on the parameter space , in the sense

that

Corollary 13.

For any estimate , the

corresponding loss function is constant.

In view of the above corollary, for the additive group, in order to obtain

the uniform minimum risk estimate, we can compute the risk of any estimate under the particular value , and then select the estimate that minimizes the risk.

Likewise, if a multiplicative group is considered, to obtain the uniform

minimum risk estimate, we can compute the risk of any estimate under the particular value ,

and then select the estimate that minimizes the risk. To do this, we will

first characterize the equivariant estimates.

Definition 14.

A functional is “invariant” iff

Definition 15.

A functional is a “maximal invariant” iff it is

invariant and satisfies

Remark 16.

For the additive group, we have that a functional , a

function of , is maximal invariant. Likewise, for the

multiplicative groupe, a functional , a function of , is maximal invariant.

Proposition 17.

Assume that the estimation problem is invariant under

the group . Let and be, respectively, the induced groups on the parameter space and the decision space . Let be any equivariant estimate.

Then, an estimate is equivariant iff

for some invariant functional , i.e.,

Proposition 18.

(Hoff (2012), Theorem 3). A functional is invariant iff it is

a function of a maximal invariant functional .

Combining the above results, we obtain

Proposition 19.

Let be any equivariant estimate. Then is equivariant iff

where is some function of the maximal

invariant functional

Remark 20.

Notice that acts additively for additive group, and multiplicatively for

multiplicative group, i.e.,

when an additive group is considered, and

for multiplicative group.

3. UMRE estimate for additive group

Let be any one of the

equivariant estimates , and assume

that . Consider the loss. In view of the above

statements, the UMRE estimate of is then given by

(40)

where , and is the

conditional expectation of given , under the assumption that . We give in the following an asymptotic approximation to the

conditional expectation

using the result of Jurečková and Picek (2009). Straightforward

calculs, shows that the score function, of the semiparametric exponential

family (38), can be written as

(42)

where and are, respectively, the

derivative w.r.t. , of and

the solution of the system (39). The derivative

can be derived by the

implicit function theorem. Denote with

Let

Then, by the implicit function theorem, we have

(43)

Notice that, for true value ,

since , we obtain for

the true value the more simpler expression

(44)

Let

(45)

Under some integrability assumptions, by dominated convergence theorem, we

obtain

(46)

which is the opposite of the Fisher information matrix.

Theorem 21.

Under some regularity conditions, we have

(47)

(48)

which gives the following approximation of the UMRE estimate

(49)

where is the

empirical estimate of the Fisher information matrix , given by

with

(50)

is the solution of the

empirical version of the system (39), i.e., the

solution in of

(51)

and is the

gradient of at the point given by

(52)

where

and

4. UMRE estimate for multiplicative group

Let be any one of

the equivariant estimates of , and assume that .

Consider the loss. In view of the above statements, the UMRE

estimate of is given by

(53)

where , and is the conditional expectation given , under the assumption that .

5. Simulation results

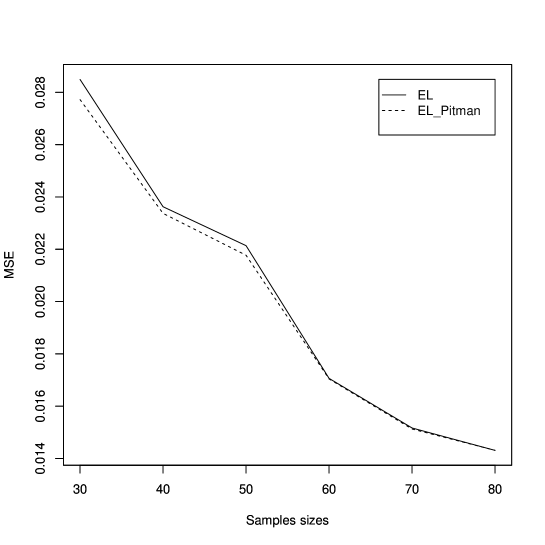

Example 22.

Consider the model

where . Let be a random

variable with distribution with . The model is invariant to the additive group. We compare the mean

square errors (MSE) of the EL estimate and the proposed UMRE estimate using

the approximation (49), for the sample sizes , with runs. We can see, from figure 1,

that the proposed estimate improves the EL one for moderate sample sizes.

Figure 1. MSE v.s. sample sizes

References

Broniatowski and Keziou (2006) Broniatowski,

M. and Keziou, A. (2006).

Minimization of -divergences on

sets of signed measures.

Studia Sci. Math. Hungar.;

arXiv:1003.5457, 43(4), 403–442.

Broniatowski and Keziou (2012) Broniatowski, M.

and Keziou, A. (2012).

Divergences and duality for estimation and

test under moment condition models.

J. Statist. Plann.

Inference, 142(9), 2554–2573.

Chen and Qin (1993) Chen, J. H. and Qin, J. (1993).

Empirical likelihood estimation for finite populations and the

effective usage of auxiliary information.

Biometrika,

80(1), 107–116.

Cressie and Read (1984) Cressie, N. and Read, T.

R. C. (1984).

Multinomial goodness-of-fit tests.

J.

Roy. Statist. Soc. Ser. B, 46(3), 440–464.

Csiszár (1963) Csiszár, I. (1963).

Eine informationstheoretische Ungleichung und ihre Anwendung auf den Beweis der Ergodizität von Markoffschen Ketten.

Magyar

Tud. Akad. Mat. Kutató Int. Közl., 8, 85–108.

Csiszár (1967) Csiszár, I. (1967).

On topology properties of -divergences.

Studia Sci.

Math. Hungar., 2, 329–339.

Godambe and Thompson (1989) Godambe, V. P.

and Thompson, M. E. (1989).

An extension of quasi-likelihood

estimation.

J. Statist. Plann. Inference, 22(2),

137–172.

With discussion and a reply by the authors.

Haberman (1984) Haberman, S. J. (1984).

Adjustment by minimum discriminant information.

Ann. Statist., 12(3), 971–988.

Hansen et al. (1996) Hansen, L.,

Heaton, J., and Yaron, A. (1996).

Finite-sample properties of some

alternative gmm estimators.

Journal of Business and Economic

Statistics, 14, 462–2800.

Hansen (1982) Hansen, L. P. (1982).

Large

sample properties of generalized method of moments estimators.

Econometrica, 50(4), 1029–1054.

Hoff (2012) Hoff, P. D. (2012).

Equivariant estimation.

Preprint.

Imbens (1997) Imbens, G. W. (1997).

One-step

estimators for over-identified generalized method of moments models.

Rev. Econom. Stud., 64(3), 359–383.

Jurečková and Picek (2009) Jurečková, J. and Picek, J. (2009).

Minimum risk

equivariant estimator in linear regression model.

Statist.

Decisions, 27(1), 37–54.

Kuk and Mak (1989) Kuk, A. Y. C. and Mak, T. K.

(1989).

Median estimation in the presence of auxiliary

information.

J. Roy. Statist. Soc. Ser. B, 51(2),

261–269.

Lehmann and Casella (1998) Lehmann, E. L. and

Casella, G. (1998).

Theory of point estimation.

Springer Texts in Statistics. Springer-Verlag, New York, second edition.

Liese and Vajda (1987) Liese, F. and Vajda, I.

(1987).

Convex statistical distances, volume 95.

BSB B. G. Teubner Verlagsgesellschaft, Leipzig.

McCullagh and Nelder (1983) McCullagh, P. and

Nelder, J. A. (1983).

Generalized linear models.

Monographs on Statistics and Applied Probability. Chapman & Hall, London.

Newey and Smith (2004) Newey, W. K. and Smith,

R. J. (2004).

Higher order properties of GMM and generalized

empirical likelihood estimators.

Econometrica, 72(1), 219–255.

Owen (1990) Owen, A. (1990).

Empirical

likelihood ratio confidence regions.

Ann. Statist., 18(1), 90–120.

Owen (1988) Owen, A. B. (1988).

Empirical

likelihood ratio confidence intervals for a single functional.

Biometrika, 75(2), 237–249.

Owen (2001) Owen, A. B. (2001).

Empirical

Likelihood.

Chapman and Hall, New York.

Pardo (2006) Pardo, L. (2006).

Statistical inference based on divergence measures, volume 185 of Statistics: Textbooks and Monographs.

Chapman & Hall/CRC, Boca

Raton, FL.

Qin and Lawless (1994) Qin, J. and Lawless, J.

(1994).

Empirical likelihood and general estimating equations.

Ann. Statist., 22(1), 300–325.

Rockafellar (1970) Rockafellar, R. T. (1970).

Convex analysis.

Princeton University Press,

Princeton, N.J.

Sheehy (1987) Sheehy, A. (1987).

Kullback-Leibler constrained estimation of probability measures.

Report, Dept. Statistics, Stanford Univ.

Smith (1997) Smith, R. J. (1997).

Alternative

semi-parametric likelihood approches to generalized method of moments

estimation.

Economic Journal, 107, 503–519.