∎

22email: dbertsim@mit.edu 33institutetext: C. McCord 44institutetext: Operations Research Center, Massachusetts Institute of Technology, Cambridge, MA 02139

44email: mccord@mit.edu

From Predictions to Prescriptions in Multistage Optimization Problems

Abstract

In this paper, we introduce a framework for solving finite-horizon multistage optimization problems under uncertainty in the presence of auxiliary data. We assume the joint distribution of the uncertain quantities is unknown, but noisy observations, along with observations of auxiliary covariates, are available. We utilize effective predictive methods from machine learning (ML), including -nearest neighbors regression (NN), classification and regression trees (CART), and random forests (RF), to develop specific methods that are applicable to a wide variety of problems. We demonstrate that our solution methods are asymptotically optimal under mild conditions. Additionally, we establish finite sample guarantees for the optimality of our method with NN weight functions. Finally, we demonstrate the practicality of our approach with computational examples. We see a significant decrease in cost by taking into account the auxiliary data in the multistage setting.

Keywords:

Data-driven optimization Multistage optimization1 Introduction

Many fundamental problems in operations research (OR) involve making decisions, dynamically, subject to uncertainty. A decision maker seeks a sequence of actions that minimize the cost of operating a system. Each action is followed by a stochastic event, and future actions are functions of the outcomes of these stochastic events. This type of problem has garnered much attention and has been studied extensively by different communities and under various names (dynamic programming, multistage stochastic optimization, Markov decision process, etc.). Much of this work, dating back to Bellman (1952), has focused on the setting in which the distribution of the uncertain quantities is known a priori.

In practice, it is rare to know the joint distribution of the uncertain quantities. However, in today’s data-rich world, we often have historical observations of the uncertain quantities of interest. Some existing methods work with independent and identically distributed (i.i.d.) observations of the uncertainties (cf. Swamy and Shmoys (2005), Shapiro (2006)). However, in general, auxiliary data has been ignored in modeling multistage problems, and this can lead to inadequate solutions.

In practice, we often have data, , on uncertain quantities of interest, . In addition, we also have data, , on auxiliary covariates, , which can be used to predict the uncertainty, . For example, may be the unknown demand for a product in the coming weeks, and may include data about the characteristics of the particular product and data about the volume of Google searches for the product.

The machine learning (ML) community has developed many methods (cf. Bishop (2006)) that enable the prediction of an uncertain quantity () given covariates (). These methods have been quite effective in generating predictions of quantities of interest in OR applications (Goel et al (2010), Gruhl et al (2005)). However, turning good predictions into good decisions can be challenging. One naive approach is to solve the multistage optimization problem of interest as a deterministic problem, using the predicted values of the uncertainties. However, this ignores the uncertainty by using point predictions and can lead to inadequate decisions.

In this paper we combine ideas from the OR and ML communities to develop a data-driven decision-making framework that incorporates auxiliary data into multistage stochastic optimization problems.

1.1 Multistage Optimization and Sample Average Approximation

Before proceeding, we first review the formulation of a multistage optimization problem with uncertainty. The problem is characterized by five components:

-

•

The state at time , , contains all relevant information about the system at the start of time period .

-

•

The uncertainty, , is a stochastic quantity that is revealed prior to the decision at time . Throughout this paper, we assume the distribution of the uncertainty at time does not depend on the current state or past decisions.

-

•

The decision at time , , which is chosen after the uncertainty, , is revealed.

-

•

The immediate cost incurred at time , , which is a function of the decision at time .

-

•

The dynamics of the system, which are captured by a known transition function that specifies how the state evolves, .

We note that it is without loss of generality that the cost and transition functions only depend on the decision variable because the feasible set is allowed to depend on and . To summarize, the system evolves in the following manner: at time , the system is known to be in state , when the previously unknown value, , is observed. Then the decision is determined, resulting in immediate cost, , and the system evolves to state .

Consider a finite horizon, stage problem, in which the initial state, , is known. We formulate the problem as follows:

| (1) |

where

for , and . The function is often called the value function or cost-to-go function. It represents the expected future cost that an optimal policy will incur, starting with a system in state with realized uncertainty . Of course, in practice it is impossible to solve this problem because the distributions of are unknown. All that we know about the distribution of comes from the available data.

A popular data-driven method for solving this problem is sample average approximation (SAA) (Shapiro and Ruszczynski, 2014). In SAA, it is assumed that we have access to independent, identically distributed (i.i.d.) training samples of , for . The key idea of SAA is to replace the expectations over the unknown distributions of with empirical expectations. That is, we replace with . With these known, finite distributions of the uncertain quantities, the problem can be solved exactly or approximately by various dynamic programming techniques. Additionally, under certain conditions, the decisions obtained by solving the SAA problem are asymptotically optimal for (1) (Shapiro, 2003). The basic SAA method does not incorporate auxiliary data. In practice, this can be accounted for by training a generative, parametric model and applying SAA with samples from this model conditioned on the observed auxiliary data. However, this approach does not necessarily lead to asymptotically optimal decisions, so we instead focus on a variant of SAA that starts directly with the data.

1.2 Related Work

Multistage optimization under uncertainty has attracted significant interest from various research communities. Bellman (1952) studied these problems under the name dynamic programming. For reference, see Bertsekas (2017). These problems quickly become intractable as the state and action space grow, with a few exceptions that admit closed form solutions, like linear quadratic control (Dorato et al, 1994). However, there exists a large body of literature on approximate solution methods (see, e.g., Powell (2007)).

When the distribution of the uncertainties is unknown, but data is available, SAA is a common approach (Shapiro, 2006). Alternative approaches include robust dynamic programming (Iyengar, 2005) and distributionally robust multistage optimization (Goh and Sim, 2010). Another alternative approach is adaptive, or adjustable, robust optimization (cf. Ben-Tal et al (2004), Bertsimas et al (2011)). In this approach, the later stage decisions are typically constrained to be affine or piecewise constant functions of past uncertainties, usually resulting in highly tractable formulations.

In the artificial intelligence community, reinforcement learning (RL) studies a similar problem in which an agent tries to learn an optimal policy by intelligently trying different actions (cf. Sutton and Barto (1998)). RL methods typically work very well when the exact dynamics of the system are unknown. However, they struggle to incorporate complex constraints that are common in OR problems. A vast literature also exists on bandit problems, which seek to find a series of decisions that balance exploration and exploitation (cf. Berry and Fristedt (1985)). Of particular relevance is the contextual bandit problem (cf. Chapelle and Li (2011), Chu et al (2011)), in which the agent has access to auxiliary data on the particular context in which it is operating. These methods have been very effective in online advertising and recommender systems (Li et al, 2010).

Recently, the single stage optimization problem with auxiliary data has attracted interest in the OR community. Rudin and Vahn (2014) studied a news-vendor problem in the presence of auxiliary data. Cohen et al (2016) used a contextual bandit approach in a dynamic pricing problem with auxiliary data. Ferreira et al (2015) used data on the sales of past products, along with auxiliary data about the products, to solve a price optimization problem for never before sold products. Bertsimas and Kallus (2014) developed a framework for integrating predictive machine learning methods in a single-stage stochastic optimization problem. Recently, Ban et al (2018) developed a method to solve a multistage dynamic procurement problem with auxiliary data. They used linear or sparse linear regression to build a different scenario tree for each realization of auxiliary covariates. Their approach assumes the uncertainty is a linear function of the auxiliary covariates with additive noise. Our approach is more general because we do not assume a parametric form of the uncertainty.

Statistical decision theory and ML have been more interested in the problems of estimation and prediction than the problem of prescription (cf. Berger (2013)). However, of integral importance to our work are several highly effective, yet simple, nonparametric regression methods. These include -nearest neighbor regression (Altman, 1992), CART (Breiman et al, 1984), and random forests (Breiman, 2001).

1.3 Contributions and Structure

In this paper, we consider the analogue of (1) in the presence of auxilliary data. For each , before the decision is made, we observe auxiliary covariates . Therefore, our training data consists of and . By saying training data is i.i.d., we mean observation , , was sampled independently of all other observations from the same joint distribution on .

We assume throughout that the auxiliary covariates evolve according to a Markov process, independently of , i.e., is conditionally independent of given . This framework can model more complex dependencies because we are able to choose the auxiliary covariate space. We could for example, append to the auxiliary covariates observed at time . In addition, we assume is conditionally independent of all past observations given .

The problem we seek to solve is defined:

| (2) |

where

for , with

and . We summarize our key contributions here.

-

1.

In Section 2, we extend the framework introduced by Bertsimas and Kallus (2014) to the multistage setting. Similarly to SAA, we replace the expectations in (2) with sums over the value functions, evaluated at observations of . However, unlike SAA, we weight the observations according to their relevance to the current problem’s auxiliary data, using weight functions inspired by popular machine learning methods.

-

2.

In Section 3, we prove the asymptotic optimality and consistency of our method with -nearest neighbor, CART, and random forest weight functions, under fairly mild conditions, for the multistage problem. (We formalize these definitions in that section.) The result for the -nearest neighbor weight function is new for the multistage setting, and the results for the CART and random forest weight functions are new for both the single-stage and multistage settings.

-

3.

In Section 4, we establish finite sample guarantees for our method with -nearest neighbor weight functions. These guarantees are new for both the single-stage and multistage problems.

-

4.

In Section 5, we demonstrate the practical tractability of our method with several computational examples using synthetic data. In addition, our results show that accounting for auxiliary data can have significant value.

2 Approach

In this section, we introduce our framework for solving multistage optimization problems under uncertainty in the presence of auxiliary covariates (2). Motivated by the framework developed by Bertsimas and Kallus (2014), and analogous to SAA, we replace the expectations over an unknown distribution with finite weighted sums of the value functions evaluated at the observations in the data. The weights we use are obtained from ML methods.

First, we use our training data to learn weight functions, , which quantify the similarity of a new observation, , to each of the training examples, . We then replace the conditional expectations in (2) with weighted sums. In particular,

| (3) |

where

for , with

and .

We note that this is analogous to the sample average approximation method, which can be represented in this framework with the weight functions equal to . The weight functions can be computed from various predictive machine learning methods. We list here a few examples that we find effective in practice.

Definition 1

Motivated by -nearest neighbor regression (Altman, 1992), the NN weight function is given by

Definition 2

Motivated by classification and regression trees (Breiman et al, 1984), the CART weight function is given by

where is the set of training points in the same partition as in the CART model.

Definition 3

Motivated by random forests (Breiman, 2001), the random forests weight function is given by

where is the set of training points in the same partition as in tree of the random forest.

We offer two observations on the formulation in (3) before proceeding.

-

1.

In SAA, we are justified in replacing by by the strong law of large numbers. We will see in Section 3 that a conditional strong law of large numbers holds under certain conditions, and this justifies replacing with .

-

2.

If the weight functions are nonnegative and sum to one (as is the case with those presented here), then we can think of this formulation as defining a dynamic programming problem in which the uncertain quantities have a known, finite distribution. This means we can readily apply exact and approximate dynamic programming algorithms to solve (3). For the reader’s convenience, we provide a decomposition algorithm, tailored to our approach, in Appendix B, which can be used to exactly solve small to moderately sized problems.

2.1 Notation

We summarize the relevant notation we use in Table 1. We use lower case letters for and to denote observed quantities in the data and capital letters, and , to denote random quantities. When we discuss the asymptotic optimality of solutions in Definitions 4 and 5, the data are random quantities, and thus solutions to (3) are also random. For notational convenience, we sometimes write even though does not depend on (because the auxiliary data observed after the last decision is made is irrelevant to the problem).

| Auxiliary data observed at time , | |

| State of the system at the beginning of time period , | |

| Decision made at time , | |

| Uncertain quantity observed after the decision at time , | |

| Transition function that gives the evolution of the state to | |

| Cost of decision at time | |

| Weight function for stage , gives weighting for training sample | |

| Value function in full information problem (2) | |

| Value function in approximate problem (3) | |

| Optimal objective value of full information problem (2) | |

| Optimal objective value of approximate problem (3) |

3 Asymptotic Optimality

In the setting without auxiliary covariates, under certain conditions, the SAA estimator is strongly asymptotically optimal (Shapiro, 2003). Here, we provide similar results for the multistage setting with auxiliary data.

Definition 4

We say , a sequence of optimal solutions to (3), is strongly asymptotically optimal if, for almost everywhere (a.e.),

-

1.

The estimated cost of converges to the true optimal cost:

(4) almost surely.

-

2.

The true cost of converges to the true optimal cost:

almost surely.

-

3.

The limit points of are contained in the set of true optimal solutions:

almost surely, where denotes the limit points of the set .

Definition 5

We say , a sequence of optimal solutions to (3), is weakly asymptotically optimal if, for almost everywhere (a.e.),

-

1.

The estimated cost of converges to the true optimal cost in probability:

(5) -

2.

The true cost of converges to the true optimal cost in probability:

3.1 -Nearest Neighbor Weight Functions

We begin by defining some assumptions under which asymptotic optimality will hold for (3) with the -nearest neighbor weight functions.

Assumption 1 (Regularity)

For each , there exists a closed and bounded set such that for any and , the feasible region, , is contained in .

Assumption 2 (Existence)

The full information problem (2) is well defined for all stages, : for all and is nonempty for all and .

Assumption 3 (Continuity)

The function is equicontinuous in at all stages. That is, for , , such that

for all . Additionally, the final cost function, is continuous.

Assumption 4 (Distribution of Uncertainties)

The following hold:

-

1.

The stochastic process satisfies the Markov property.

-

2.

For each , is conditionally independent of and given .

-

3.

For each , the support of , , is compact.

-

4.

The noise terms have uniformly bounded tails, i.e., defining , there exists such that

-

5.

For all and , is a continuous function of .

We remark that Assumption 3 does not preclude the possibility of integral constraints on . In fact, if is a finite discrete set, the assumption is automatically satisfied (choose ). Condition 4 of Assumption 4 can be satisfied if are uniformly bounded random variables, are subgaussian random variables with uniformly bounded subgaussian norms, or are subexponential random variables with uniformly bounded subexponential norms. With these assumptions, we have the following result regarding the asymptotic optimality of (3) with the -nearest neighbor weight functions.

Theorem 3.1

Comparing the result with that of Bertsimas and Kallus (2014) for the single-stage problem, we see it is quite similar. Both theorems assume regularity, existence, and continuity. The difference in the multistage setting is that these assumptions must hold for the value function at each stage. We also note that Bertsimas and Kallus (2014) listed several sets of regularity assumptions that could hold, whereas we only list one for clarity. However, the extension of the other sets of regularity assumptions to the multistage setting is straightforward.

To prove this result, we rely on several technical lemmas. Lemmas 1,3, and 4 are refined versions of results originally stated in Bertsimas and Kallus (2014).

Lemma 1

Suppose for each , and are equicontinuous functions, i.e., and , s.t. , and likewise for . If for every ,

then the convergence is uniform over any compact subset of .

Proof

Let be a sequence that converges to . For any , by assumption, such that for all . By the convergence of , there exists an such that , . This implies, , for all . Additionally, by assumption, s.t. , . Therefore,

Therefore, for any convergent sequence in , , .

Given a compact subset , suppose that . This implies and a sequence such that occurs infinitely often. Define to be the subsequence for which this event occurs. Since is compact, by the Bolzano-Weirestrass theorem, has a convergent subsequence in . If we define to be this subsubsequence, we have that and for all . We have . The first term converges to 0 because of what we showed above. The second term converges to 0 by the equicontinuity assumption. This is a contradiction, so it must be that for any compact set .

This lemma shows that, given an equicontinuity assumption, pointwise convergence of a function implies uniform convergence over a compact set. We will apply this with . The following two lemmas establish that strong asymptotic optimality follows from the uniform convergence of the objective of (3) to that of (2).

Lemma 2

Suppose is a compact set and and are two continuous functions. If and , then

and

Proof

First, because of the optimality of and ,

Second,

Lemma 3

Fix and suppose as and is a continuous function of . In addition, suppose constraint set is nonempty, closed, and bounded. Any sequence for has all of its limit points contained in .

Proof

Suppose there is a subsequence , converging to . (We must still have that because is compact.) Let . By the continuity assumption, such that for all . Additionally, by assumption, we can find a such that , This implies that for any ,

From lemma 2, we know that

which goes to 0 as , and is thus a contradiction. Therefore, all limit points of must be contained in .

Lemma 4 shows that, given an equicontinuity assumption, if a function indexed by converges almost surely for each in a compact set, then the convergence holds almost surely for all .

Lemma 4

Suppose for each , and are equicontinuous functions: i.e., and , s.t. , and likewise for . In addition, suppose that for each , almost surely ( is a random quantity). Furthermore, assume is compact. Then, almost surely, for all .

Proof

Let . Because is countable, for almost everywhere, by the continuity of probability measures. For any sample path for which this occurs, consider any . We have, for any ,

By equicontinuity and the density of , we can pick such that each of the first two terms is less for any . By assumption, we can also find an such that the third term is bounded by for all , so we have for all . This is true for any for this particular sample path. Since the set of sample paths for which this is true constitutes a measure 1 event, we have the desired result.

We also restate a result from Biau and Devroye (2015) (Theorem 12.1) regarding the uniform consistency of the -nearest neighbor regression estimator.

Lemma 5

Let be i.i.d. observations of random variables . Assume has support on a compact set and there exists such that

In addition, assume is a continuous function. For some , let . If is the nearest neighbor regression estimator for and , then

almost surely.

From these lemmas, the proof of Theorem 3.1 follows.

Proof (Theorem 3.1)

We need to show that

a.s. for a.e. The desired result then follows from lemmas 2 and 3. To begin, we have:

Expanding the second term on the right hand side, and using the fact that and , we have:

where we have used lemma 2. Therefore, we have:

Repeating the above argument for , we have:

To see that each term on the right hand side goes to 0 a.s., we first apply lemma 5 to each term. This shows that each term (without the supremums over ) goes to 0 a.s. for each . Next we apply lemma 4 to each term to show that the convergence holds simultaneously for all with probability 1. Finally, we apply lemma 1 to show the convergence of each term is uniform over a.s. To do so, we let and . We can verify the equicontinuity assumption holds for each of these functions because of Assumption 3 and Jensen’s inequality (because define a probability distribution). This completes the proof.

3.2 CART Weight Functions

In order to study the asymptotic properties of (3) with the CART and random forest weight functions, we need to consider modified versions of the original algorithms of Breiman et al (1984) and Breiman (2001). Since greedy decision trees have proven difficult to analyze theoretically, we instead consider a modified tree learner introduced by Wager and Athey (2015). Formally, a regression tree is defined as

where identifies the region of the tree containing , and is an auxiliary source of randomness. Trees are built by recursively partitioning the feature space. At each step of the training process, for each region, a feature is selected and a cutoff is chosen to define an axis-aligned hyperplane to partition the region into two smaller regions. This is repeated until every region contains some minimum number of training points. In order to guarantee consistency, we place several restrictions on how the trees are built. We use the following definitions from Wager and Athey (2015).

Definition 6 (Random-split, regular, and honest trees)

Let the regression tree be the type defined above.

-

1.

is a random-split tree if at each step in the training procedure, the probability that the next split occurs in the th feature is at least for all , with some . This source of this randomness is .

-

2.

is a regular tree if at each split leaves at least a fraction of the available training examples on each side of the split. Additionally, the tree is grown to full depth , meaning there are between and training examples in each region of the feature space.

-

3.

is an honest tree if the splits are made independently of the response variables . This can be achieved by ignoring the response variable entirely when making splits or by splitting the training data into two halves, one for making splits and one for making predictions. (If the latter is used, the tree is regular if at least a fraction of the available prediction examples are on each side of the split.)

The standard implementation of the CART algorithm does not satisfy these definitions, but it is straightforward to modify the original algorithm so that it does. It involves modifying how splits are chosen. If we learn weight functions using trees that do satisfy these definitions, we can guarantee the solutions to (3) are weakly asymptotically optimal. We first introduce two additional assumptions. We note that these assumptions are strengthened versions of Assumptions 3 and 4.

Assumption 5 (Distribution of Auxiliary Covariates)

The distribution of the auxiliary data, , is uniform on (independent in each feature)111The result holds under more general distributional assumptions, but uniformity is assumed for simplicity. For example, we could assume has a continuous density function on , bounded away from 0 and . See Wager and Athey (2015) for a further discussion..

Assumption 6 (Continuity)

For each , there exists an such that and ,

Furthermore, for each , is -Lipschitz continuous in , for all .

Theorem 3.2

Suppose Assumptions 1-6 hold, and the training data is i.i.d. Let be the CART weight functions for , and assume the trees are honest, random split, and regular with , the minimum number of training examples in each leaf, equal to for . Then , a sequence of optimal solutions to (3), is weakly asymptotically optimal.

The proof of this result follows closely the proof of Theorem 3.1. To begin, we prove a result regarding the bias of tree based predictors. It relies on the same argument Wager and Athey (2015) used in proving their Lemma 2.

Lemma 6

Suppose is a regular, random-split tree as in Definition 6, and the training covariates are i.i.d. uniform() random variables. If denotes the partition of containing , and as , then

Proof

As in the proof of Lemma 2 in Wager and Athey (2015), we define to be the number of splits leading to the leaf and to be the number of these splits that are on the th coordinate. Following the same arguments as Wager and Athey (2015), we have, conditional on ,

where . In addition, for sufficiently large, with probability at least (over the training data),

We call this event . From here, we have, for any ,

for sufficiently large, where is a constant that does not depend on or . The second inequality follows from the union bound since there are a maximum of total partitions in the tree, and the fourth inequality follows from Hoeffding’s inequality. Putting everything together, we have:

It is easy to verify that the final expression goes to 0 as , so the proof is complete.

Next, we establish the uniform consistency of the CART regression estimator.

Lemma 7

Suppose is a regular, random-split, honest tree as in Definition 6, the training data are i.i.d. with uniform on , and is -Lipschitz continuous. In addition, assume there exists such that the uniform noise condition is satisfied: . Finally, suppose and as . If denotes the prediction of at and , then

Proof

To begin, we have

where is the CART weight function corresponding to tree . In the third and fourth inequalities we used Jensen’s inequality and the Lipschitz continuity assumption. By lemma 6, the latter term goes to 0 in probability. For the former, we define to be the number of training examples in the leaf containing . For fixed , if , then by Lemma 12.1 of Biau and Devroye (2015), we have, for any ,

Because there are a maximum of leaves in the tree, there are a maximum of values of the weight function . Therefore, we can use the union bound to show:

where the second inequality follows because by assumption. Taking the expectation of both sides and the limit as completes the proof.

We prove one more intermediate result, and the proof of Theorem 3.2 will follow.

Lemma 8

Suppose is an Lipschitz continuous function for all (with respect to ), and is nonempty, closed, and bounded with diameter . It follows that

where is a constant that depends only on .

Proof

This result follows from a standard covering number argument. We can construct a -net of , with . That is, , there exists such that . If we define to be the function that returns this index, then, for all ,

Taking the supremum of both sides over , we have

Next, we select , and we have:

where the final inequality follows from the union bound.

Proof (Theorem 3.2)

The proof follows the same outline as the proof of Theorem 3.1. We need to show

for a.e. The desired result then follows from lemma 2. Following the same steps as in the proof of Theorem 3.1, we have:

Next, we have, for all ,

Rearranging, and taking the supremum over both sides, we have

which demonstrates

is Lipschitz. We now apply lemma 8 to get:

By lemma 7, the right hand side goes to 0 in probability. Repeating this argument for all completes the result.

3.3 Random Forest Weight Functions

A random forest is an ensemble method that aggregates regression trees as base learners in order to make predictions. To aggregate the trees into a random forest, Breiman suggested training each tree on a bootstrapped sample of the training examples. In order to facilitate the theoretical analysis, we instead build a forest by training trees on subsamples of size of the training data. The random forest estimator is given by:

| (6) |

where denotes a random subset of training examples of size . Given this definition of a random forest, we have the following asymptotic optimality result for random forest weight functions.

Theorem 3.3

Suppose Assumptions 1-6 hold, and the training data is i.i.d. Let be the random forest weight functions for . Assume the trees that make up the forest are honest, random split, and regular and , the minimum number of training examples in each leaf, equals for . Furthermore, assume , the subsample size, equals for . Then , a sequence of optimal solutions to (3), is weakly asymptotically optimal.

Proof

This theorem shows it is possible to obtain asymptotically optimal solutions to (3) with random forest weight functions. The random forest model we use is slightly different than Breiman’s original algorithm, which is implemented in common machine learning libraries. For example, we require that , the minimum number of training examples in each leaf, grows with , whereas the original algorithm has fixed at 1. We include an additional theorem in the appendix which proves the strong asymptotic optimality of random forest weight functions with fixed for the single stage version of the problem. However, the proof does not extend to the multistage problem we consider here. The proof of Theorem 3.3 uses the following lemma.

Lemma 9

Suppose is a random forest consisting of regular, random-split, honest trees, each trained on a random subset of the training data of size . Assume the training data are i.i.d. with uniform on , is -Lipschitz continuous, and there exists such that the uniform noise condition is satisfied: . Finally, suppose and as . If denotes the prediction of at and , then

Proof

We define the prediction of the th tree in the ensemble to equal , so we have, by Jensen’s inequality,

By lemma 7, we immediately have that each term on the right hand side goes to 0 in probability. Because does not depend on , this completes the result.

4 Finite Sample Guarantees

In this section, we establish finite sample, probabilistic guarantees for the difference between the cost of a solution to (3) and the true optimal cost. We focus on -nearest neighbor weight functions. To the best of our knowledge, this is the first finite sample bound for either the single-stage or multistage setting with auxiliary data.

To facilitate the presentation of our result, we begin by discussing convergence rate results for the single stage setting. Without auxiliary data, the problem we want to solve is given by

If represents the SAA approach applied to this problem, then, under appropriate conditions, the regret, , is , where the notation suppresses logarithmic dependencies (see, for example, (Shapiro and Ruszczynski, 2014)). This implies that for any confidence level, , we know that the regret is bounded by a term of order with probability at least . We contrast this with the setting in which we have auxiliary data,

If represents a solution to this problem using the approach of Bertsimas and Kallus (2014) with the -nearest neighbor weight functions, then the regret, is for , where is the dimension of the auxiliary covariate space. The problem with auxiliary data is clearly harder. The baseline with respect to which we compute the regret is smaller because it takes into account the value of the auxiliary covariates. Furthermore, many of the s in the training data will be very different from the we are concerned with. In fact, with the -nearest neighbor weight functions, we effectively throw out all but the most relevant training examples. Because of this, we pay a penalty that depends on the dimension of the auxiliary covariate space.

To formalize the above discussion for the multistage setting, we add two additional assumptions.

Assumption 7 (Distribution of auxiliary covariates)

For each , has its support contained in and and , with , where .

This assumption is satisfied, for example, if is uniformly distributed or has finite support and, thus, is more general than Assumption 5.

Assumption 8 (Subgaussian noise terms)

The noise terms are uniformly subgaussian, i.e., defining , there exists such that

for all .

This assumption implies condition 4 of Assumption 4. With these additional assumptions, we have the following theorem.

Theorem 4.1

Suppose Assumptions 1-4 and Assumptions 6-8 hold, the training data, , is i.i.d., and are the nearest neighbor weight functions with for and . We define

where is an optimal solution to (3). For any , with probability at least ,

for , for almost everywhere. (Here, .) , , , , and are constants that may depend only logarithmically on and and are defined in (7) in the proof.

represents the regret of the solution to (3), i.e., the difference between the cost of the solution and the true optimal cost, . We can optimize the bound by choosing and restate the result more prosaically:

As before, this result is best understood in comparison with the multistage SAA problem without any auxiliary covariates. For this problem, regret is (Shapiro and Ruszczynski, 2014, ch. 5). We pay a penalty that depends on , the maximum dimension of the auxiliary covariate spaces, .

To prove this result, we rely on the following lemma, which provides a finite sample guarantee on the error of the NN regression estimator.

Lemma 10

Suppose has support , for all , and is conditionally subgaussian given with variance proxy , uniformly for all . Assume the training data, is i.i.d. and that is -Lipschitz. If denotes the NN regression estimator at and , then

for any and .

Proof (Lemma 10)

We decompose into a sum of two terms: and . For the latter term, we utilize the Lipschitz assumption to show

where denotes the th nearest neighbor of out of , as measured by Euclidean distance. Next, we note that . This gives:

Next, we construct an -net for , , with . For any , there exists a such that . Therefore, we can upper bound the above expression by

where . Applying Hoeffding’s bound, we have:

for any .

For the second part, we use Theorem 12.2 of Biau and Devroye (2015), which says the number of possible distinct orderings of neighbors of is less than or equal to for all . Therefore,

where denotes the observation corresponding to . It is easy to verify, see Proposition 8.1 of Biau and Devroye (2015) for example, that are conditionally independent given . Therefore, we apply Hoeffding’s bound for sums of subgaussian random variables to get, for any ,

Taking the expectation of both sides and combining with the previous part completes the result.

Now, we can prove the main result.

Proof (Theorem 4.1)

By lemma 2, the regret is bounded by

Following the same steps as in the proof of Theorem 3.1, we have:

We next apply lemma 8, as in the proof of Theorem 3.2, to see, for each ,

Next, we use lemma 10 to upper bound this expression by

for any and . Combining the results for with the union bound, and plugging in for the definitions of , , , , , and , we have:

for all and . From this we deduce that for any ,

is implied by the following system of inequalities:

Following some algebraic manipulations, we see the above system of inequalities is implied by:

where

| (7) | ||||

5 Computational Examples

In this section, we illustrate the practical applicability of our approach with two examples using synthetic data. These examples also serve to demonstrate the value of accounting for auxiliary data.

5.1 Multistage Inventory Control

First, we consider a multistage inventory control problem (Bertsimas and Georghiou, 2015), in which we manage the inventory level of a single product subject to periods of uncertain demand. At each time step, we observe auxiliary data, which may include data about the product as well as data on time-varying external factors that may be used to predict demand, such as the season of the year, the price of the S&P 500 index, or the demand for a similar product during the previous time period. We also have historical data of the demand for products we’ve sold in the past as well as the corresponding auxiliary data for each of these products.

At the beginning of time period , we observe the demand and the new auxiliary covariates . Demand can be served by ordering units at price for immediate delivery or by ordering units at price for delivery at the beginning of the next time period. If there is a shortfall in the inventory, orders can be backlogged, incurring a cost of per unit. If there is excess inventory at the end of a time period, we pay a holding cost of per unit. In addition, there is an ordering budget, so the cumulative advance orders () must not exceed at any time . We assume all ordering and inventory quantities are continuous, and we represent the amount of inventory at the end of time period by (with and ). If demand is known, we have the following deterministic formulation of the problem.

| s.t. | |||||

We used the parameters , , , and . We assumed the initial inventory to be 0 and set . To generate training data, we sampled independently from a 3 dimensional AR(1) process such that , where is a sample of a random variable. We used a factor model for the demand.

where are drawn independently from a 3 dimensional standard Gaussian and are drawn independently from a 1 dimensional standard Gaussian. At each time step, the factor loadings, and , are permutations of and , respectively (held constant for all samples). The results we present here show the average cost of policies based on out-of-sample testing as a function of the amount of training observations, . All results are averaged over one hundred realizations of training sets.

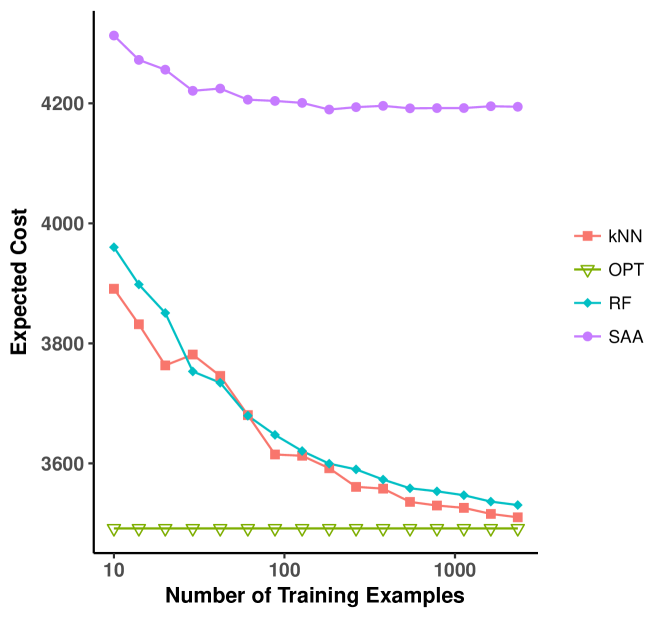

Figure 1 shows the expected cost of policies learned using our method versus the number of training samples. We see that the SAA approach, which ignores the auxiliary data, is suboptimal. Our method, using the -nearest neighbor and random forest weight functions, is asymptotically optimal. We obtain a reduction in cost of over 15% by accounting for auxiliary data.

5.2 Multistage Lot Sizing

For our second computational example, we consider a multistage lot sizing problem (Bertsimas and Georghiou, 2015). This problem is similar to the multistage inventory control problem, but it includes binary decision variables. The continuous ordering decision for immediate delivery, , is replaced with binary ordering decisions, , . Each of these decisions corresponds to a quantity, , which is delivered immediately for cost per unit. Additionally, there is no longer the option to backorder demand. All demand must be satisfied immediately. These restrictions make the problem more realistic because it is often not feasible to produce an arbitrary amount of a product immediately, and it is difficult to estimate the cost of lost customer goodwill due to backordering. Instead, in order to meet demand, the decision maker must buy from another supplier a fixed quantity of product at a higher price.

If demand is known, we have the following deterministic formulation (where we assume , and ).

| s.t. | |||||

We used the same parameters and data generating procedure as in the multistage inventory control example. The only differences were that we capped at 200 (to ensure feasibility) and we drew independently from a uniform distribution on for each .

To solve the problem, we use an approximate DP algorithm. To develop the algorithm, we recall that basestock policies are optimal for a wide variety of inventory control problems. A basestock policy is one in which there is some ideal amount of inventory, , which we desire at the start of time period . If we have less than , we place advanced orders (if available) to have this amount. If we have more than , we order nothing in advance. We then serve the remaining demand with immediate orders. A basestock policy will not be optimal for the lot sizing problem because of the nonconvexity of the value function, but it does provide a reasonable approximation. To account for auxiliary data, we have different basestock amounts for each time period. Therefore, denotes the target basestock at time when the observed axuiliary data is . Parametrizing the policy space with parameters greatly reduces the amount of computation required to solve the problem and allows us to solve much larger problem instances than we could otherwise.

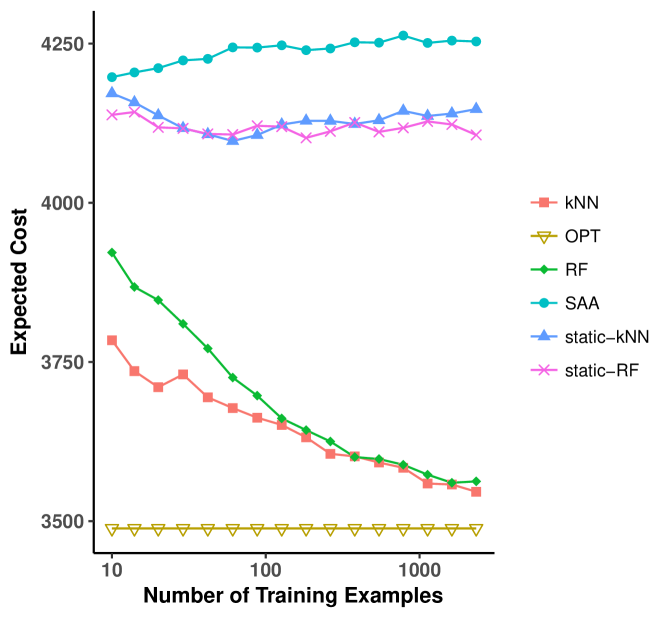

Figure 2 shows the results of our method for the SAA, -nearest neighbor, and random forest weight functions on a twelve stage lot sizing problem. The SAA method is again clearly suboptimal. We see that the static NN and static RF methods, which only use the auxiliary covariates at time 0, offer a significant improvement over the SAA method. However, the NN and RF methods which take into account the auxiliary data that arrives over time outperforms all of the above methods, again illustrating the value of auxiliary data. With very little additional computational cost, we are able to obtain an improvement in cost of nearly 15%.

6 Conclusion

In this paper, we introduced a data-driven framework for solving multistage optimization problems under uncertainty with auxiliary covariates. We demonstrated how to develop specific methods by integrating predictive machine learning methods such as NN, CART, and random forests. Our approach is well suited for multistage optimization problems in which the distribution of the uncertainties is unknown, but samples of the uncertainty and auxiliary data are available.

We demonstrated that our method with the -nearest neighbor, CART, and random forest weight functions are asymptotically optimal. We also provided finite sample guarantees for the method with NN weight functions. Additionally, we showed how to apply the framework with two computational examples. Because we can think of (3) as a dynamic programming problem, we have at our disposal a variety of exact and approximate solution techniques. The problem is often tractable in practice and can lead to significant improvements over methods that ignore auxiliary data.

We leave for future work the extension in which the decision affects the distribution of the uncertainty. This type of problem appears in applications such as pricing where the choice of price affects the distribution of the demand. We also leave for future research the development of efficient variants of our methods for specific applications. In a world in which the availability of data continues to grow, our proposed approach utilizes this data efficiently and has the potential to make a significant impact in OR applications.

References

- Altman (1992) Altman NS (1992) An introduction to kernel and nearest-neighbor nonparametric regression. The American Statistician 46(3):175–185

- Ban et al (2018) Ban GY, Gallien J, Mersereau A (2018) Dynamic procurement of new products with covariate information: The residual tree method. Forthcoming in Manufacturing and Service Operations Management

- Bellman (1952) Bellman R (1952) On the theory of dynamic programming. Proceedings of the National Academy of Sciences 38(8):716–719

- Ben-Tal et al (2004) Ben-Tal A, Goryashko A, Guslitzer E, Nemirovski A (2004) Adjustable robust solutions of uncertain linear programs. Mathematical Programming 99(2):351–376

- Benders (1962) Benders JF (1962) Partitioning procedures for solving mixed-variables programming problems. Numerische mathematik 4(1):238–252

- Berger (2013) Berger JO (2013) Statistical decision theory and Bayesian analysis. Springer Science & Business Media

- Berry and Fristedt (1985) Berry DA, Fristedt B (1985) Bandit problems: sequential allocation of experiments (Monographs on statistics and applied probability). Springer

- Bertsekas (2017) Bertsekas DP (2017) Dynamic programming and optimal control, vol 1. Athena Scientific Belmont, MA

- Bertsimas and Georghiou (2015) Bertsimas D, Georghiou A (2015) Design of near optimal decision rules in multistage adaptive mixed-integer optimization. Operations Research 63(3):610–627

- Bertsimas and Kallus (2014) Bertsimas D, Kallus N (2014) From predictive to prescriptive analytics. arXiv preprint arXiv:14025481

- Bertsimas et al (2011) Bertsimas D, Brown DB, Caramanis C (2011) Theory and applications of robust optimization. SIAM review 53(3):464–501

- Biau and Devroye (2015) Biau G, Devroye L (2015) Lectures on the nearest neighbor method. Springer

- Bishop (2006) Bishop CM (2006) Pattern recognition and machine learning. Springer

- Breiman (2001) Breiman L (2001) Random forests. Machine learning 45(1):5–32

- Breiman et al (1984) Breiman L, Friedman J, Stone CJ, Olshen RA (1984) Classification and regression trees. CRC press

- Chapelle and Li (2011) Chapelle O, Li L (2011) An empirical evaluation of thompson sampling. In: Advances in neural information processing systems, pp 2249–2257

- Chu et al (2011) Chu W, Li L, Reyzin L, Schapire RE (2011) Contextual bandits with linear payoff functions. In: AISTATS, vol 15, pp 208–214

- Cohen et al (2016) Cohen MC, Lobel I, Paes Leme R (2016) Feature-based dynamic pricing

- Dorato et al (1994) Dorato P, Cerone V, Abdallah C (1994) Linear-quadratic control: an introduction. Simon & Schuster

- Ferreira et al (2015) Ferreira KJ, Lee BHA, Simchi-Levi D (2015) Analytics for an online retailer: Demand forecasting and price optimization. Manufacturing & Service Operations Management 18(1):69–88

- Goel et al (2010) Goel S, Hofman JM, Lahaie S, Pennock DM, Watts DJ (2010) Predicting consumer behavior with web search. Proceedings of the National academy of sciences 107(41):17,486–17,490

- Goh and Sim (2010) Goh J, Sim M (2010) Distributionally robust optimization and its tractable approximations. Operations research 58(4-part-1):902–917

- Gruhl et al (2005) Gruhl D, Guha R, Kumar R, Novak J, Tomkins A (2005) The predictive power of online chatter. In: Proceedings of the eleventh ACM SIGKDD international conference on Knowledge discovery in data mining, ACM, pp 78–87

- Iyengar (2005) Iyengar GN (2005) Robust dynamic programming. Mathematics of Operations Research 30(2):257–280

- Li et al (2010) Li L, Chu W, Langford J, Schapire RE (2010) A contextual-bandit approach to personalized news article recommendation. In: Proceedings of the 19th international conference on World wide web, ACM, pp 661–670

- Murphy (2013) Murphy J (2013) Benders, nested benders and stochastic programming: An intuitive introduction. arXiv preprint arXiv:13123158

- Powell (2007) Powell WB (2007) Approximate Dynamic Programming: Solving the curses of dimensionality, vol 703. John Wiley & Sons

- Rudin and Vahn (2014) Rudin C, Vahn GY (2014) The big data newsvendor: Practical insights from machine learning

- Shapiro (2003) Shapiro A (2003) Inference of statistical bounds for multistage stochastic programming problems. Mathematical Methods of Operations Research 58(1):57–68

- Shapiro (2006) Shapiro A (2006) On complexity of multistage stochastic programs. Operations Research Letters 34(1):1–8

- Shapiro (2011) Shapiro A (2011) Analysis of stochastic dual dynamic programming method. European Journal of Operational Research 209(1):63–72

- Shapiro and Ruszczynski (2014) Shapiro DD Alexander, Ruszczynski A (2014) Lectures on stochastic programming: modeling and theory, vol 16. Siam

- Sutton and Barto (1998) Sutton RS, Barto AG (1998) Reinforcement learning: An introduction, vol 1. MIT press Cambridge

- Swamy and Shmoys (2005) Swamy C, Shmoys DB (2005) Sampling-based approximation algorithms for multi-stage stochastic optimization. In: Foundations of Computer Science, 2005. FOCS 2005. 46th Annual IEEE Symposium on, IEEE, pp 357–366

- Wager and Athey (2015) Wager S, Athey S (2015) Estimation and inference of heterogeneous treatment effects using random forests. arXiv preprint arXiv:151004342

- Zou et al (2016) Zou J, Ahmed S, Sun XA (2016) Nested decomposition of multistage stochastic integer programs with binary state variables. Optimization Online

Appendix A Additional Results on Random Forest Weight Functions

Here we provide an additional result on the strong asymptotic optimality of the method with random forest weight functions in the single stage setting. Here, we consider random forests as defined in Wager and Athey (2015). The random forest consists of an ensemble of trees, each trained on a subsample of the data of size . Each of the trees in the forest is a regular, random-split, and honest regression tree as in Definition 6. The prediction of the random forest at is given by

| (8) |

In practice, this is estimated by training trees on random subsamples of the data and random draws of .

Assumption 9 (Random Forest Specification)

The random forest, as defined in (8), has random-split, regular, and honest regression trees as its base learners. In addition, , and the subsample size, , scales with . That is, with and .

This assumption ensures the forest consists of diverse trees, each with low bias, so they can be aggregated into a consistent regressor.

Theorem A.1

Suppose is nonempty and compact, and the training data is i.i.d. In addition, suppose , for all , , and that is a well-defined -Lipschitz continuous function of for all . Finally, suppose is uniformly distributed on and is an -Lipschitz continuous function of for all . Let be the random forest weight function, satisfying assumption 9. Then , a sequence of optimal solutions to

is strongly asymptotically optimal with respect to the true problem, .

This result shows that our method can be strongly asymptotically optimal for the single stage problem with random forest weight functions. Some of the assumptions are slightly stronger than in Theorem 3.3. For example, we require that the value functions are bounded and the random forests are slightly different. However, we do not require that the minimum number of training samples per leaf, , grows with as we do for Theorem 3.3. This is consistent with Breiman’s original random forest algorithm in which is fixed at 1. To prove this theorem, we first prove a result on the strong consistency of the random forest estimator.

Lemma 11

Suppose are i.i.d. samples, the distribution of uniform on , and , a.s. Let be a Lipschitz continuous function. Define to be the prediction of a random forest that satisfies Assumption 9. Then, almost surely,

for a.e.

Proof

We first note that the bias of the predictions goes to 0, , for a.e. by Theorem 3 from Wager and Athey (2015). (The assumptions are satisfied by Assumption 9.) Next, we define , where . We note that for any ,

This is due to the assumption that . Since each tree predicts at by averaging the s corresponding to training samples in the same partition of the feature space as , the prediction of any tree is bounded between -1 and 1. Changing a single training sample only affects the trees trained on subsets of the data including that example. This only affects a fraction of the trees in the forest. Since the prediction of the random forest is the average of the predictions of all the trees, the most the prediction can be changed by altering a single training sample is . Applying McDiarmid’s inequality, we have, for ,

By our assumption, this can be rewritten

where . From this we see , so, by the Borel Cantelli lemma, a.s. Combining the two results with the triangle inequality completes the proof.

Proof (Theorem A.1)

We need to show

a.s. for a.e. The desired result then follows from lemmas 2 and 3. If we ignore the supremum, we can apply lemma 11 to see it goes to 0 a.s. Next, we apply lemma 4 to see that the convergence holds simultaneously for all with probability 1. Finally, we apply lemma 1 to show the convergence is uniform over a.s.

Appendix B Decomposition Algorithm

For the reader’s convenience, we present a decomposition algorithm, similar to that of Shapiro (2011), tailored for use with our methods. Given weight functions, which we compute from an appropriate machine learning algorithm, our goal is to solve (3). If the decisions spaces and state spaces are finite sets with small cardinality, it may be possible to solve the problem exactly using the classical dynamic programming algorithm (see, for example, Bertsekas (2017)). However, in many OR problems, this is not the case, and we need to deal with continuous decision and state spaces.

We note that it is possible to formulate (3) as a large, but finite sized, single stage optimization problem. To do so, we create copies of , copies of , etc. These copies of the decision variables represent our contingency plan. For each potential realization of , we have a distinct copy of . If the and functions are linear and the sets are polyhedral, the resulting problem will be a linear optimization problem, which can be solved in time that is polynomial in the size of the formulation. However, the number of variables in the formulation is , and this formulation becomes impractical for moderately sized and . In order to solve larger problems, we resort to a Benders-like decomposition approach. (For a review of Benders decomposition methods, see, for example, Murphy (2013).)

Algorithm 1 describes the approach. The main idea is that we maintain a piecewise linear, convex lower bound, , on for each . We have the relaxed problems:

| (9) |

(For , there is no dependence on .) If and are linear functions and is a polyhedral set, then the relaxed problem can be reformulated as a linear optimization problem because is the maximum of a finite set of linear functions.

The algorithm consists of two main steps, which are repeated until convergence. First, sample paths for and are sampled (with replacement) from the training data. Then, in the forward step, for each of these sample paths, trial states are computed by solving the relaxed problems from to , assuming the system evolves according to the corresponding sample path. Using the costs of each of these sample paths, we can compute a statistical upper bound on the optimal value of (3) (assuming and are such that a central limit theorem is a reasonable approximation).

In the backward step, we update the functions. We proceed backwards, starting with , and solve for each of the trial states. We compute the cut coefficients (which we will discuss in more detail next), and then average them across all possible realizations and , according to the distribution . We then update with this new cut. Finally, we update the lower bound on the optimal value of the problem by solving .

There are several possible stopping criteria we can use. One is to stop when the statistical upper bound (line 1 in Algorithm 1) is within a specified of the lower bound (line 1). This will give us an -optimal solution with probability at least (assuming is sufficiently large and is much larger than so that the central limit theorem is a reasonable approximation). Alternatively, we can stop when the lower bound stabilizes or after a fixed number of iterations. All three of these can allow the algorithm to construct lower bounds, , that are reasonable approximations to the value functions.

/* Forward step */

/* Statistical upper bound */

/* Backward Step */

/* Lower bound update */

The crucial component required for this algorithm to work is the cuts. We begin with a definition from Zou et al (2016).

Definition 7 (Valid, tight, and finite cut)

Let be the stage cut coefficients computed in the backward step of Algorithm 1. We say that the cut is:

-

1.

Valid if

-

2.

Tight if

where represents the optimal value of (9), is the trial state computed during the corresponding forward pass of the algorithm, and is the auxiliary covariate from the forward pass of the algorithm.

-

3.

Finite if solving (9) for fixed can only generate finitely many possible cuts.

Under the conditions that and are linear functions, are polyhedral sets, and at every stage, (9) is feasible with finite optimal value, it is shown in Shapiro (2011) that the SDDP algorithm will converge to an optimal solution in a finite number of iterations with probability 1, provided the cuts used are valid, tight, and finite. Zou et al (2016) showed that this result also holds if the state variables are purely binary, instead of continuous.

The validity of the cuts ensures that the functions maintain lower bounds on the value functions at each stage. Next, we describe several classes of valid cuts that can be used within the SDDP algorithm.

Benders’ Cut

A well known class of cuts is the Bender’s cut (Benders, 1962). These cuts are valid for linear problems, even with integer constraints, and are tight for linear optimization problems (or more generally convex optimization problems) in which strong duality holds. To compute the cuts for stage in the SDDP algorithm we solve the following form of :

| s.t. | |||||

We then let be the optimal dual solution (of the LO relaxation if there are integer variables) corresponding to the indicated constraint and set , where is the optimal value of the above problem. In order for these cuts to be finite, we should always use basic solutions for .

Integer Optimality Cut

If the state space is binary, the SDDP algorithm with Benders’ cuts is not guaranteed to produce an optimal solution. This is because they are not guaranteed to be tight. Instead, we can solve the above integer optimization problem to optimality and choose cuts defined by the linear expression:

These cuts are valid, tight, and finite when the state space is binary. However, they tend to be very ineffective in practice.

Lagrangian Cut

The third class of cut we describe was introduced by Zou et al (2016) and shown to be valid and tight when the state space is binary. They are much more effective than the integer optimality cuts in practice. These cuts are computed by solving the Lagrangian dual problem:

where

| s.t. | |||||

We then use the cut with equal to the optimal solution of the Lagrangian dual problem and equal to the optimal value of .

These three classes of cuts allow us to solve problems where the state space is continuous or pure binary with the SDDP algorithm. When the state space is a mixed integer set, we can perform a binary expansion to desired accuracy on the continuous variable to convert the problem to the pure binary case. Of course, we can also combine different classes of cuts, and this can speed convergence.