A rectangular additive convolution for polynomials

Abstract

Motivated by the study of singular values of random rectangular matrices, we define and study the rectangular additive convolution of polynomials with nonnegative real roots. Our definition directly generalizes the asymmetric additive convolution introduced by Marcus, Spielman and Srivastava (2015), and our main theorem gives the corresponding generalization of the bound on the largest root from that paper. The main tool used in the analysis is a differential operator derived from the “rectangular Cauchy transform” introduced by Benaych-Georges (2009). The proof is inductive, with the base case requiring a new nonasymptotic bound on the Cauchy transform of Gegenbauer polynomials which may be of independent interest.

1 Introduction

This paper introduces the rectangular additive convolution to the theory of finite free probability. The motivation for a finite analogue of free probability came from a series of works that used expected characteristic polynomials to study certain combinatorial problems in linear algebra [14, 16, 17]. It is well known that the characteristic polynomial of a Hermitian matrix is the real-rooted polynomial , and in [16] the authors showed that one could analyze the effect of certain random perturbations on by studying the effect of certain differential operators applied to . In particular, they showed that any valid bounds on the largest root of the transformed polynomials could be translated into statements about the randomly perturbed matrix. In [14], the same authors showed that these differential operators were actually a special case of a more general class of “polynomial convolutions” and they introduced a technique for deriving bounds on the largest root under certain convolutions. One interesting property of the bounds that came from this technique was that they had quite similar form to known identities from free probability. This idea was strengthened by the realization that the major tools used in proving these bounds had striking similarities to tools in free probability.

The connection was formalized in [13], where it was shown that the inequalities derived for two of the convolutions studied in [14] — the symmetric additive and multiplicative convolutions — converge to the - and -transform identities of free probability (respectively). Since the release of [13], a number of advances have been made in understanding the relationship between free probability and polynomial convolutions, most notably the work of Arizmendi and Perales [1] in developing a combinatorial framework for finite free probability using finite free cumulants (the approach in [13] is primarily analytic).

The purpose of this paper is to introduce a convolution on polynomials that generalizes the third convolution studied in [14] — what is there called the asymmetric additive convolution — and to prove the corresponding bound on the largest root. The method of proof will be similar to the one used in [14], however there will be a number of added complications. Those familiar with [14] may recall that all of the inequalities proved there utilized various levels of induction to reduce to a small set of “base cases.” One of the difficulties in dealing with the asymmetric additive convolution (as opposed to the other two convolutions) was the fact that the corresponding base case was highly nontrivial. Rather, it required a bound on the Cauchy transform of Chebyshev polynomials that was both unknown at the time and not particularly easy to derive.

We will encounter the same issue: replacing the analysis on Chebyshev polynomials will be an analysis on (the more general) Gegenbauer polynomials. To establish the bound, we will prove a number of inequalities relating nonasymptotic properties of Gegenbauer polynomials (which appear to be unknown) with the corresponding asymptotic properties (many of which are known) and these could be of interest in their own right (see Section 1.2 for the location of results).

Many of the ideas required in generalizing the various constructs in [14] to the ones used in this paper were inspired by the work of Florent Benaych-Georges, in particular [3] where the appropriate transforms for calculating the rectangular additive convolution of two freely independent rectangular operators were introduced (hence the name of our convolution). We remark on this connection briefly in Section 1.3, but in general have written the paper in a way that assumes no previous knowledge of free probability.

1.1 Previous work

The primary predecessors of this work are [14], where other polynomial convolutions were introduced, and [3], where the free probability version of the rectangular additive convolution was introduced (see 1.3 for more discussion on the relation to [3]). The original purpose of [14] was to develop a generic way to bound the largest root of a real-rooted polynomial when certain differential operators were applied. Such bounds are useful in tandem with the “method of interlacing polynomials” first introduced in [15]. One of the main inequalities in [14] is the following:

Theorem 1.1 (Marcus, Spielman, Srivastava).

Let and be real rooted polynomials of degree at most . Then

The operator here is what is called the symmetric additive convolution in [14] and is the differential operator . The acts to smoothen the roots of the polynomials, making the convolution more predictable. Theorem 1.1 is used in [16] to prove an asymptotically tight version of restricted invertibility, a theorem first introduced by Bourgain and Tzafriri that has seen a wide variety of uses in mathematics (see [19]).

A considerably more difficult inequality in [14] concerned what the authors called the asymmetric additive convolution. In the notation of this paper — see (2) and (4) — this inequality reads

Theorem 1.2 (Marcus, Spielman, Srivastava).

Let and be polynomials of degree at most with nonnegative real roots. Then

for all . Furthermore, equality holds if and only if or .

Theorem 1.2 was then used in [17] to prove the existence of bipartite Ramanujan graphs of all degrees and all sizes. The main theorem of this paper (Theorem 1.3) is a generalization of Theorem 1.2. In particular, we show that the generalized convolution (defined in Section 2) satisfies a similar inequality:

Theorem 1.3.

Let and be polynomials of degree at most with nonnegative real roots. Then

| (1) |

for all and , where

Furthermore, equality holds if and only if or .

One obvious difference between the two theorems is the replacement of the operator with the more general operator, defined in Section 3 (the differences between the two are discussed in Remark 3.1). Much of the added difficulty in the proof of Theorem 1.3 (with respect to the proof of Theorem 1.2) is the quadratic nature of the operator.

The other obvious difference is that the bound in (1) no longer relates the of the convolution to that of the original polynomials in a linear way (unless ) We have yet to come up with an intuitive explanation of why this is the correct form, apart from it coming up naturally in the work of Benaych-Georges (see Section 1.3). However, it was worth noting that the form of (and ) only plays a significant role in Section 5 (the base cases). The inductive steps in Section 4 can be adapted to work with a much larger family of operators (and quantities) with the appropriate monotonicity properties (as was pointed out by an anonymous referee). One corollary of the results in Section 3, however is that, for fixed , the quantity is increasing in . Given that , this will provide the type of bound we are hoping. quantitatively bound the effects of on the largest root (with respect to the input polynomials).

In a different direction, Leake and Ryder showed that Theorem 1.1 was actually a special case of a more general submodularity inequality [10] (note that they use the notation as opposed to the notation introduced in [14]).

Theorem 1.4 (Leake, Ryder).

For any real rooted polynomials of degree at most , one has

1.2 Structure

The paper is structured as follows: in the remaining introductory sections, we attempt to provide some concrete motivation for studying the rectangular additive convolution. In Section 2, we define the rectangular additive convolution and prove some of the basic properties that it satisfies. Of particular importance in application is Theorem 2.3, which shows that preserves nonnegative rootedness. In Section 3, we introduce two equivalent methods — the -transform and operator — that we will use to measure the effect of on the largest root (with respect to the input polynomials).

The proof of Theorem 1.3 will be presented in Section 5, however it will require a number of lemmas and simplifications that will need to be proved along the way. Section 4 contains two “induction” lemmas that will allow us to reduce the proof of Theorem 1.3 to a subset of polynomials we call basic polynomials (see Section 2 for definitions). One of the main ingredients in the inductions is a “pinching” technique similar to the one used in [14] which is introduced in Section 4.1.

Given these induction lemmas, the primary difficulty remaining will be in proving various “base cases” of Theorem 1.3. These will be addressed in Section 5 modulo one major assumption: a bound on the Cauchy transform of a certain class of orthogonal polynomials (the Gegenbauer polynomials). The missing bound will then be proved in Section 6, along with a number of other nonasymptotic inequalities concerning Gegenbauer polynomials that may be of independent interest. Section 6 has been (to a large extent) quarantined from the rest of the paper in an attempt to allow readers with a primary interest in orthogonal polynomials to find it accessible without needing to read other parts of the paper.

1.3 Motivation for this work

Before beginning, we would like to give some motivation for the study of this particular convolution. In particular, Section 1.3.2 and Section 1.3.3 will discuss the relationship to a field first initiated by Voiculescu known as “free probability” [22]. The discussion of free probability will be restricted to these sections, and the remainder of the paper should be accessible to those unfamiliar with this area. However, for those interested in (or at least aware of) the connections of polynomial convolutions to linear algebra (in particular, expected characteristic polynomials) may find these sections useful for understanding the motivations for some of what will appear. For those interesting in learning more about this subject (and, in particular, the large role that combinatorics plays), we suggest starting with [18].

1.3.1 As an operation on singular values

We start by recalling the relationship between the symmetric additive convolution from [14] and eigenvalues of matrices. There is a natural correspondence between any degree real-rooted polynomial and the class of Hermitian matrices for which

It was shown in [14] that the symmetric additive convolution of two degree real-rooted polynomials is (again) a degree real-rooted polynomial. Hence the symmetric additive convolution can be viewed as a binary operation on these classes of matrices. This may seem coincidental, but it was shown in [13] that the symmetric additive convolution can be reproduced by the actual addition of matrices; that is, for all Hermitian and , there exists a unitary matrix for which

Hence, for example, the symmetric additive convolution must satisfy Horn’s inequalities [8] (precisely where in the Horn polytope the convolution lies is an interesting open question).

In a similar spirit, a polynomial in can be written as for some matrix (where we are free to choose ). In Theorem 2.3, we show that the rectangular additive convolution of two polynomials in is another polynomial in . Hence, similar to above, the rectangular additive convolution can be seen as a binary operation on the classes of matrices with a given set of singular values. The one small issue in that the roots of the polynomial are actually the squares of the singular values of , and one can view the appearance of the operator in the definition of as a correction to this issue (see Remark 3.1).

While this relationship to matrices is a primary motivation for defining (and studying) this particular convolution, we will see that (similar to [14]) that it is beneficial to ignore this relationship when proving bounds. In particular, one part of the induction we will use requires us to be able to apply the rectangular additive convolution to polynomials of different degrees, which would correspond to adding matrices of different sizes in the view discussed above. Hence we will refrain from using this view for the majority of this paper, instead working strictly in the realm of polynomials. The two exceptions to this are Remark 3.1 and Section 7, where we will use the connection to matrices to help explain certain aspects of our analysis that may not obvious when viewing the rectangular additive convolution completely in terms of polynomials. In particular, none of the main results will require any previous knowledge of free probability (or finite free probability).

1.3.2 Inspiration from free probability

Much of the connection between polynomial convolutions and free probability stems from Remark 3.1; in many ways, both theories consist of the only reasonable way to define a unitarily invariant binary operations on matrices. Hence the fact that polynomial convolutions turn into free convolutions (in the appropriate limit) is not surprising (proving that this is the case is less straight-forward [13]). While the concepts in [14, 16, 17] were developed without any knowledge of this connection, more recent work (including this paper) has benefited greatly from this relationship.

The connection is perhaps best seen by recalling that the primary tool used in [14] to understand the behavior of the symmetric additive convolution was the differential transform

for . This is nothing more than a more “polynomial friendly” version of the Cauchy transform (of the uniform distribution on the roots of ):

where denote the roots of . In particular, one can check that

and so many of the properties of can be derived directly from well known properties of the Cauchy transform. One the other hand, has the advantage of remaining in the realm of real rooted polynomials (it is well known that the operator preserves real rootedness, see for example [4]) and this turns out to be useful in the analysis done in [14].

In order to understand the behavior of the rectangular convolution, we will do something similar. Instead of relating to the Cauchy transform, however, we will use a construction inspired by the work of Benaych-Georges [3]. The -transform defined in this paper is a slight modification of what Benaych-Georges calls a rectangular Cauchy transform with much of the modification coming from the fact that the objects of interest in [3] are infinite dimensional operators, and so one must view the relationship between and as a ratio. Some a posteriori explanations of the differences between and are discussed in Remark 3.1, but this is not intended to obscure the fact that all of our a priori inspiration came directly from [3].

1.3.3 Finite free probability

The original inspiration for [14, 13] came from the study of expected characteristic polynomials of matrices. In fact the definition of the rectangular additive convolution in Section 2 was originally derived from the following observation [12]:

Theorem 1.5.

Let and be rectangular matrices, with (singular value) characteristic polynomials

Let and denote Haar invariant measures over and (the spaces of unitary matrices of size and , respectively). Then the coefficients of the polynomial

are multilinear functions of the coefficients of and .

One can check that the exact formula for in terms of and derived in [12], is given by the rectangular additive convolution. In this respect, this paper can be viewed as the continuation of an investigation into the correspondence between expected characteristic polynomials and free probability that has become known as “finite free probability.”

Finite free probability has played an important role in some recent results in computer science [17, 25], and while we will not discuss any applications in this paper, we should mention that this paper is the first in a series of three papers. The second will be an extension of [17] (which showed the existence of bipartite Ramanujan graphs for any number of vertices and degree ) to the case of biregular, bipartite graphs [6]. The third will be an analogue of the analysis done in [13], showing that the inequality in Theorem 1.3 becomes an equality in the appropriate limit by showing that the individual terms converge to Benaych-Georges’ rectangular -transform [7]. The third paper, in particular, suggests that the rectangular additive convolution can be viewed as a finite version of the addition of freely independent rectangular matrices. In this respect, the bounds given in this paper show that the roots of lie inside the support of the free convolution, a property which we will combine with the “method of interlacing polynomials” introduced in [15] to build Ramanujan graphs.

2 The Convolution

For , we define to be the collection of degree polynomials with real coefficients that have

-

1.

All nonnegative roots

-

2.

At least one root positive

-

3.

The coefficient of positive

and set to be the (constant) polynomial for all . Note that the second property only serves to eliminate the polynomial and that this is the only polynomial that is added by the closure:

We will use to denote the union . Note that this does not include the polynomial.

We will call a polynomial basic if it has the form for some real numbers . Otherwise we call it nonbasic. Note that, trivially, every polynomial in is basic.

We define a binary operation on polynomials as follows:

Definition 2.1.

For and , we define the rectangular additive convolution to be the linear extension of the operation

| (2) |

In particular, if we write

then we have

| (3) |

There are two special cases worth mentioning: for any polynomial , we have

-

1.

, and

-

2.

.

One property that can be derived directly from the definition is the following:

Lemma 2.2.

Let and . Then

Proof.

2.1 Preservation of nonnegative real roots

The main property that we will need in this paper is the fact that the rectangular additive convolution (with the appropriate parameters) preserves the property of having all nonnegative roots.

Theorem 2.3.

Let . Then for any and , we have .

The proof of this theorem will rely on a result of Lieb and Sokal [11]. Recall that a polynomial is called stable if whenever for all . If (in addition) the coefficients of are real numbers, then is called real stable. A degree univariate polynomial is stable if and only if it has real roots. A multivariate polynomial is called multiaffine if it has degree at most in each of its variables.

Theorem 2.4 (Lieb–Sokal).

If and are multiaffine real stable polynomials, then

is either the polynomial or is multiaffine real stable.

We will also need the following well-known lemma:

Lemma 2.5.

For any degree univariate polynomial with positive leading coefficient, we have if and only if is real stable.

Proof.

Assume is not real stable; that is, for some with and . Without loss of generality, we can set and where . Hence is a root of , and since

this root is not a nonnegative real, so .

In the other direction, if then has a non-real root. Since has real coefficients, the roots come in conjugate pairs so one such root must be in the upper half plane. Setting and to be that root shows that is not real stable. ∎

We will write to denote the map

where is the elementary symmetric polynomial on the inputs (and is undefined when ). The linear extension of the map to polynomials is known as the polarization operator. It should be clear that is multiaffine for any polynomial and any integer . A theorem of Borcea and Brändën shows that polarization preserves the property of being real stable [4]:

Theorem 2.6.

If is a real stable polynomial then is real stable as well.

Proof of Theorem 2.3.

We first note that it suffices to consider the case when . To see why, we can proceed by induction on . Since is the only possibility when , the base case will be covered. Now for , if or , then we can use Lemma 2.2 to write the same polynomial using a convolution with parameter , and this is real rooted by the induction hypothesis.

To ease notation, we will write

and

Given polynomials , with and , set

and

Both and are multiaffine (by definition of polarization) and real stable (by a combination of Lemma 2.5 and Theorem 2.6). Hence Theorem 2.4 implies that

is either or real stable. If it is , then we are done, so assume not. Since substitution of variables preserves real stability, the bivariate polynomial formed by substituting and into is also real stable. We claim that

which, by Lemma 2.5, would complete the proof.

The main observation that we will need to compute is that for any ,

which can easily be checked by hand. In particular, this gives

when (and otherwise). Applying this to our formula for , we get

Plugging in and , we then get

∎

3 The measuring stick

In this section, we define the operator that will be used to measure the effects of the rectangular additive convolution on the largest root of a polynomial. Rather than define it directly, however, it will be useful to first introduce a modification of the -transform from [3], which will then have as its corresponding differential operator. To state the two succinctly, it will help to introduce two other operators:

| (4) |

Given a polynomial with nonnegative roots, we define the -transform of (with parameter ) as

| (5) |

and the corresponding differential operator

| (6) |

Note that the parameter is intended to be the same as the parameter in (2). One could consider and for general value of , but we will only be using these transforms to directly measure the effect of and so there is no reason to consider this more general case.

Remark 3.1.

For those familiar with the operator from [14], we would like to point out that there is a natural way to understand the differences between that operator and the defined here using the relationship to characteristic polynomials mentioned in Section 1.3.1. As discussed there, the symmetric additive convolution can be viewed as a binary operation on eigenvalues (technically, classes of Hermitian matrices with the same eigenvalues) and, in a similar spirit, the rectangular additive convolution can be viewed as a binary operation on singular values (technically, classes of matrices with the same dimensions and singular values). This correspondence goes via the characteristic polynomials with Hermitian (in the eigenvalue case) and with a matrix with (in the singular value case). The second correspondence is not perfect, however, in that the roots of the polynomial are actually the squares of the singular values of .

The first main difference between the and operators — the appearance of the operator — can be viewed as a necessary compensation for this issue. One concern one might have is that this “correction” effectively creates two copies of each singular value (a positive one and a negative one). Fortunately, our primary interest is in understanding the largest singular value (that is, the largest root of ), and so the addition of extra negative roots will prove to be irrelevant in our analysis.

The remaining differences between the and operators — the quadratic nature and appearance of the operator (and the parameter in general) — can likewise be seen as a necessary compensation for a different issue. Given the polynomial , there is no way to know the number of columns in the underlying matrix . One might hope that this is irrelevant, but the analysis in [3] shows that this is not the case. One obvious attempt to correct this would be to instead consider the polynomial , but one runs into the same problem concerning the number of rows (and therefore the value of ). The operator compensates for this by using both polynomials

to be used. The one case where the operator would not need both polynomials is of course when . In this case, becomes a difference of squares (which can then be factored):

This is the reason that the analysis of the asymmetric convolution in [14] could be done using the simpler operator (despite being a special case of the results in this paper).

As in [14], we would like to be able to associate the function with the largest root of the polynomial but for this to be well-defined, we first need to show that has real roots. Our proof will use a classical result in real rooted polynomials [4]:

Theorem 3.2 (Hermite–Biehler).

Let and be polynomials with real coefficients. Then the following are equivalent:

-

1.

Every root of satisfies (here denotes the imaginary part)

-

2.

and are real rooted and the polynomial at any point .

Using this, it is easy to show the following lemma, which will immediately imply what we need:

Lemma 3.3.

Let and be real rooted polynomials. Then

is real rooted.

Proof.

It is an easy consequence of Rolle’s theorem that is real rooted whenever is, and then one can check that

for all by noticing

Hermite–Biehler then implies that the polynomials

have no roots in the upper half plane. Hence their product

has no roots in the upper half plane as well. So Hermite–Biehler (in the opposite direction) gives that is real rooted. ∎

We therefore have the following correspondence, which amounts to nothing more than algebraic manipulation:

Corollary 3.4.

3.1 Monotonicity Properties

One of the most important properties of the function when is real rooted is that it is strictly monotone decreasing on the interval (something that can be seen directly from the definition). Our new functions will inherit that property:

Lemma 3.5.

For all polynomials with nonnegative roots, the function is strictly decreasing at any .

Proof.

Let . Since has nonnegative roots, both and are real rooted with

Hence both and are strictly decreasing for and so the product is strictly decreasing as well. ∎

This then implies two “inverse” properties for the differential operators:

Corollary 3.6.

Let be a polynomial with nonnegative roots. Then for any , the quantity

is strictly increasing.

Proof.

The one disadvantage of these new differential operators is their quadratic nature. In the case where we will only need qualitative information about two polynomials, we will be able to reduce to the simpler case:

Lemma 3.7.

Let be polynomials with nonnegative roots. Then for any , we have

Proof.

Let

| (7) |

and similarly for . By definition, we therefore have

and so the difference is

where for we have . Hence

have the same sign. But by (7), we can write

and since , the lemma follows. ∎

Using Lemma 3.7, the primary inequality that we will need becomes a simple calculation.

Lemma 3.8.

Let be polynomials with nonnegative roots and positive leading coefficients such that . Furthermore, assume each has at least one positive root. Then for all and all , we have

whenever . Furthermore, equality holds in one direction if and only if it holds in the other direction.

Proof.

By Lemma 3.7, it suffices to show that

for any which is greater than . Now notice that

where and are both positive at (since is larger than the maximum root of each polynomial, and each polynomial has a positive leading coefficient). So setting , we have

for some . The lemma then follows. ∎

Of particular importance will be the case when .

Corollary 3.9.

Let satisfy the conditions of Lemma 3.8 with

Assume further that . Then

with two of the equal if and only if all three of the are equal.

4 Inductions

The goal of this section is to prove two “induction steps” that will be useful in the proof of Theorem 1.3. Let

| (9) |

where

Notice that Theorem 1.3 can be restated as saying that . Our first induction will be on the degree .

Lemma 4.1.

Let . Assume that, for some fixed and , we have

-

(i)

for all

-

(ii)

for all

Then for all .

Our second induction will be on the number of distinct roots in the polynomial.

Lemma 4.2.

Let . Assume that, for a fixed and , we have

-

(i)

for all polynomials

-

(ii)

for all basic polynomials

Then for all polynomials .

The proofs of both lemmas are given in Section 4.2. The proof of Lemma 4.2 will utilize a decomposition of a nonbasic polynomial into two “simpler” polynomials that is proved in Section 4.1. By “simpler”, we mean that one of the polynomial will have lower degree (allowing for induction) and the other polynomial will have two of its roots moved closer together (an operation that is referred to in [14] as “pinching”). Obviously one can always pinch a nonbasic polynomial — the goal will be to find a pinch that decreases , as this would imply that any minimum of (if it exists) must be a basic polynomial.

Because basic polynomials feature prominently in the computations moving forward, it will be useful to have calculated the following quantity beforehand:

Lemma 4.3.

Let with and . Then

Proof.

For as given, we have

where . Hence

| (10) |

and so

∎

4.1 The Pinch

The main goal of this subsection is to prove Lemma 4.4, which provides the existence of a pinch with the properties that will be useful in the proof of Lemma 4.2.

Lemma 4.4.

Fix , , and let be nonbasic. Then there exist and so that

-

a.

,

-

b.

,

-

c.

-

d.

.

The proof of Lemma 4.4 will occur in two steps. First we will prove a pinching lemma for a “linearized” version of the -transform (by removing the operator), and then we will show how the existence of a linearized pinch implies Lemma 4.4. Note that this is the only section where these linearized operators will appear.

We define the “linearized” versions of the -transform as:

and note that for two polynomials , implies . Corresponding to this is the “linearized” version of the -transform

which by Lemma 3.3 is real-rooted as long as is real rooted. Hence we can say

| (11) |

Lemma 4.5 (Linearized pinching).

Let , , and let be a monic polynomial with . Then there exist real numbers and so that the polynomials

satisfy

-

a.

and (in particular, )

-

b.

-

c.

-

d.

Proof.

Let . Since , we have by Lemma 3.6 that , so there is no issue in setting

or (rearranging slightly)

| (12) |

Note that (12) gives as the harmonic average of and (where ). Using the fact that , this implies that or (equivalently) . Furthermore,

so (12) also shows that .

Now define . Since and have the same leading coefficient, it should be clear that has degree . Furthermore, we can now write

Evaluating at the point , we get that

for some , so since we must have

As is mentioned above, this implies

and so by (11)

The fact that shows that , and so it remains to show that and that . We first multiply out the equation and equate coefficients to get

| (13) |

Now to see that , recall that (12) expresses as the harmonic average of two postive numbers. The inequality between the arithmetic and harmonic means therefore implies

which, after rearranging, gives that .

To move from the “linearized” pinch to the “quadratic” pinch that we need, we will use the following observation:

Lemma 4.6.

Fix , , and let . Then

Proof.

By definition, we have

and so is some root of ; we wish to show it is the largest one. Assume (for contradiction) that there exists some for which . This would imply that

However this is impossible, since is strictly decreasing whenever and we have assumed that . The reverse direction (once we have fixed the value of ) is essentially the same. ∎

Lemma 4.4 then follows easily:

4.2 The Lemmas

We now give proofs of the two main lemmas stated at the beginning of the section (the lemmas are restated here for convenience).

Lemma 4.1.

Let . Assume that, for some fixed and , we have

-

(i)

for all

-

(ii)

for all

Then for all .

Proof.

Lemma 4.2.

Let . Assume that, for a fixed and , we have

-

(i)

for all polynomials

-

(ii)

for all basic polynomials

Then for all polynomials .

Proof.

Fix and and assume (for contradiction) that there exists a polynomial for which . Since has a finite number of roots, we can find a constant for which all of the roots of lie in the interval , and then consider the collection of all polynomials in whose roots lie in the interval . This collection is compact, and so (a continuous function in the roots of ) achieves its minimum. Let be a polynomial achieving this minimum; in particular, note that , which means (by hypothesis ) must be nonbasic.

Since is nonbasic, it has a decomposition with the properties of Lemma 4.4. In particular, note that

-

a.

implies (by the linearity of ) that

-

b.

implies that has all of its roots in , so the choice of as a minimizer ensures that .

-

c.

implies (by plugging in to the definition of )

Hence Properties b. and c. combine to give and so

| (14) |

5 Base Cases

Our proof of Theorem 1.3 is inductive and utilizes both Lemma 4.1 and Lemma 4.2. Each of these lemmas will require its own “base case”.

Neither of these lemmas is particularly simple (despite being the “base cases” of an induction). We prove Corollary 5.3 using a separate induction, first considering the case when is a basic polynomial (Lemma 5.2) and then using Lemma 4.2 to extend this to all polynomials. While the proof of Lemma 5.2 is mostly calculus, the functions that one needs to consider become complicated enough that we were forced to appeal to the aid of a computer in order to calculate them. Section 5.1 is dedicated to this case.

Lemma 5.8, on the other hand, will require an entire investigation of its own. Corollary 5.6 will relate the rectangular additive convolution of two basic polynomials a well-studied class of orthogonal polynomials and we will utilize a number of well-known properties of these polynomials to prove the necessary inequalities. To simplify the presentation, the proof of Lemma 5.8 given in Section 5.2 will be contingent upon a bound on the Cauchy transform of Gegenbauer polynomials that will be proved in Section 6.

Assuming these two base cases, the proof of Theorem 1.3 is then straightforward:

Theorem 1.3.

For and , we have .

Proof.

We proceed by induction on . The base case (when ) is covered by Lemma 5.8, since degree polynomials are (by definition) basic.

In order to make the presentation of the two lemmas more readable, we first show that the parameter can be effectively scaled out of statements pertaining to . Note that the transformation in Lemma 5.1 preserves basic polynomials, so statements that are restricted to basic polynomials can be scaled out as well.

Lemma 5.1.

For a fixed and polynomials with nonnegative roots, let and . Then

Proof.

5.1 The case of

As mentioned earlier, we start by proving the case when is a basic polynomial.

Lemma 5.2.

Let , , and let be a basic polynomial. Then .

Proof.

By Lemma 5.1, it suffices to prove the lemma when . To simplify notation slightly, we will sometimes write . Note that for and , Lemma 4.3 implies that

Letting

it then suffices to show that

or, squaring both sides and rearranging,

| (16) |

Furthermore, we can calculate

where has coefficients that depend on . Hence

and so (16) is equivalent to having . Our approach to proving this will be to show that for all . Consider the Taylor series of the function

around . With the help of a computer, one can calculate that and that

and

where

So for , we have , and for , all other terms in are trivially nonnegative. Hence for all .

Now note that, because the leading coefficient of is positive, the fact that implies that the number of roots of that are larger than is even. On the other hand, when ,

and so has three roots at and one at . As is real rooted for all and the roots of are continuous functions of its coefficients (and thus of ) we can conclude that for small all but one of the roots of must be near ; in other words, the function

is positive for sufficiently small . Hence it suffices to show that for any .

Assume (for contradiction) that there exists for which . In other words, which (in particular) means that . But this is a contradiction, since we have shown to be strictly positive for . Hence must remain strictly positive for all , finishing the proof. ∎

Corollary 5.3.

Let , , and let be an (arbitrary) polynomial. Then .

Proof.

Let be the statement

Our goal is then to prove for all , and we will proceed by induction on . The base case is when , which we will consider below. Now assume to hold whenever and consider a polynomial with degree for which . We split into two cases:

-

1.

:

-

2.

:

Hence in both cases we have reduced the statement to one that we know (by the inductive hypothesis) is true, so is true as well.

To finish the proof, we then need to consider only the base case: . For , set

and note that

is independent of . Hence we have

where by Lemma 5.2, and so it suffices to show that

| (17) |

By Corollary 3.4 and Lemma 3.7, this is equivalent to showing that

for all . However, it is easy to check that

which is negative for . ∎

5.2 The case of basic polynomials

We start by finding a generating function for the rectangular convolution of two basic polynomials. The derivation will use the following well known generalization of the binomial theorem (see, for example, [24]).

Theorem 5.4.

The function has the formal power series expansion

Lemma 5.5.

For all and , the polynomials

satisfy the formal power series identity

Proof.

Using (3), we can write explicitly. Letting

we have

Hence we have the formal power series identity

∎

This provides an easy link between the rectangular convolution of basic polynomials and the Gegenbauer polynomials studied in Section 6:

Corollary 5.6.

For all we have

Bounding the -transform of the convolution of two basic polynomials can therefore be reduced to bounding the Cauchy transform of Gegenbauer polynomials. We prove the necessary bound in Section 6, but reproduce the theorem here for continuity.

Theorem 6.11.

Consider the bivariate polynomial

and assume that for a given and that . Then

The proof of Lemma 5.8 will require a number of identities that are not, by themselves, important to understanding the overall proof. In order to keep the continuity of ideas in the proof, we have separated these identities out into a separate lemma:

Lemma 5.7.

For , let

and also let

Then the following identities hold:

-

1.

.

-

2.

Proof.

For real numbers , it is easy to check that is a root of the polynomial by simple substitution. Hence , or (rearranging slightly),

| (18) |

By definition of , however, we have

| (19) |

Equating (18) and (19) and then rearranging gives

| (20) |

which clearly implies 1. Now note that if we multiply out 2., we get

which, after canceling the terms and dividing out matches (20). ∎

Finally, we are able to prove the lemma:

Lemma 5.8.

Let , , and let be basic polynomials. Then .

Proof.

Again by Lemma 5.1 it suffices to consider the case . We set

and note that Corollary 5.6 and Theorem 6.11 show that

| (21) |

Also set ; substituting this and Lemma 4.3 into the definition of , we get that it suffices to show

| (22) |

Next define the quantities

noting that the string of inferences

show that is well defined. Then to prove (22), it suffices to show (after squaring both sides, and substituting) the inequality .

Finally, define

and notice that the identity in Lemma 5.7.2 implies that . Then if , we are done, so we are left to consider the case when .

For , we then have by (21) that

so Lemma 3.5 implies that the inequality holds if and only if

| (23) |

By definition, we have

and so we can rewrite (23) as

We now bound by noting that the identity in Lemma 5.7.1 allows us to apply Theorem 6.11 to the ordered pair

By Corollary 5.6, we then get the inequality

Hence

as required. ∎

6 Gegenbauer polynomials

The Gegenbauer (or ultraspherical) polynomials are a collection of polynomials which are orthogonal with respect to the weight function on the interval . They can be computed explicitly using a generating function

| (24) |

or by the three-term recurrence given in Lemma 6.1. They are a special case of the more general Jacobi polynomials:

and are themselves a generalization of two other well-studied families of orthogonal polynomials:

-

1.

Chebyshev polynomials of the second kind (), and

-

2.

Legendre polynomials ().

We will use the following identities, which can be derived directly from (24) or taken as a specialization of known identities for Jacobi polynomials (see, for example, [21]). Note that the appearing in the second identity is the usual Gamma function

Lemma 6.1.

The following hold for all real numbers and all integers .

-

1.

Recurrence relation, with convexity coefficients:

-

2.

Value(s) at 1:

-

3.

Differential equation:

Our goal will be to derive bounds on the Cauchy transform of at values greater than its roots. Fortunately, much is known about the largest roots of Gegenbauer polynomials; in particular, the following bound from [5] provides a useful starting point:

Lemma 6.2 (Elbert, Laforgia).

For fixed , the roots of lie in the interval where

Remark 6.3.

Note that is decreasing in , and so decreasing the degree or increasing the parameter will cause the interval to shrink. This coincides with the well known fact that all of the positive roots of are increasing as grows and decreasing as grows [21].

The bound we will derive differs from Lemma 6.2 (and all other known bounds, as far as we can tell) in that it requires us to compare the largest roots of as and grow together in a linear way. Specifically, we will be interested in understanding the largest root of for a generic constant . The intuition above tells us that the growth in and the growth in should push the roots in opposite directions, and so it should not be surprising that the computations become somewhat delicate.

It should be noted that the asymptotic behavior of these polynomials has been studied, and it is well known that the density of the roots of these polynomials converges to a fixed distribution that will depend on the parameter . The distribution can be computed using a result of Kuijlaars and Van Assche regarding the asymptotic root distributions of Jacobi polynomials [9]. The following is a reformulated version of the theorem specific to our polynomials:

Theorem 6.4 (Kuijlaars, Van Assche).

For all , the density of the roots of converges (as ) to the function

An asymptotic bound on the Cauchy transform can then be derived from Theorem 6.4:

Corollary 6.5.

For all , and all , we have

| (25) |

We give a brief sketch of the computation in an Appendix for the benefit of the reader. Note that for the specific case of , the formula in Theorem 6.4 simplifies greatly to a well-known bound on the Cauchy transform of Chebyshev polynomials:

for all .

The rest of this section will be devoted to showing that the bound in Corollary 6.5 holds for the individual polynomials as well. In particular, we will show that the the sequence is increasing in for all and all where we define

One part of this will be to show that the sequence is an increasing function of (for fixed ). For the moment, however, we will find it convenient to consider the following “two-step” maximum root:

6.1 Nonasymptotic bounds

To simplify notation slightly, we will fix and normalize the polynomials of interest (in a manner that is common when deriving such inequalities — see [2], for example). For nonnegative integers, we will set

Definition 6.6.

We will say that a polynomial is -orthogonal-fit if

-

1.

in , and

-

2.

in .

It is easy to check that -orthogonal-fitness is closed under nonnegative linear combinations (a fact that will be used in Lemma 6.8) and that Remark 6.3 implies that any polynomial which is -orthogonal-fit is also -orthogonal-fit whenever .

The following lemma reduces the monotonicity statement we are interested in to one regarding certain polynomials being -orthogonal-fit.

Lemma 6.7.

The following statements are equivalent:

-

1.

For any fixed , we have

-

2.

The polynomial

(26) is -orthogonal-fit.

Proof.

We start by rewriting the first statement as

and notice that the third identity in Lemma 6.1 implies that

and

Plugging these in and canceling the like terms, we get the equivalent statement

Plugging in the second identity in Lemma 6.1 and simplifying, we see that this is equivalent to having on the interval and on the interval , which is the definition of being -orthogonal-fit. ∎

Before proving anything with the polynomials , it will be worthwhile to note the translation of the first identity in Lemma 6.1 into these polynomials:

| (27) |

where (for our fixed )

We will use the following fact (that comes from direct calculation):

| (28) |

Lemma 6.8.

The polynomial

| (29) |

is -orthogonal-fit for all .

Proof.

The fact that is a root follows from the definition of , and so it would suffice to show that has at most one root in the desired interval, a fact that we will prove by induction (on ). The base case can be computed explicitly:

which is clearly -orthogonal-fit. For the inductive step, let and . By (27), we have

and so

Plugging in

then gives

The induction hypothesis gives that is -orthogonal-fit and (28) shows that . Since -orthogonal-fitness is closed under nonnegative combinations, it would then suffice to show that the polynomial is -orthogonal-fit for any . Again, is obviously a root, and so the theorem would follow by showing that there is at most one real root in the desired interval.

However, this follows easily from interlacing properties: it is well known that consecutive orthogonal polynomial have interlacing roots, and one can show that a polynomial interlaces a polynomial if and only if there exist nonnegative constants such that

where the are the roots of (see, for example, [23]). In particular, this ratio is nonnegative and monotone decreasing at any . Hence interlaces and interlaces and the product

is nonnegative and monotone decreasing for (recall that the monotonicity mentioned in Remark 6.3 implies that has the largest root of these polynomials). Hence

can have at most one solution in the interval . But for , we have

implying that has a single root in and proving the theorem. ∎

Note that, even though we were forced to consider the possibility that in the proof of Lemma 6.8, one direct implication of the lemma is that such a scenario is impossible.

Corollary 6.9.

Proof.

For our purposes, we will need a similar statement about the Cauchy transform:

Corollary 6.10.

For and , we have

-

1.

-

2.

for all , we have

where .

Proof.

Note that while the form of Corollary 6.10.2 is the more popular one in the literature, it has a downside when appearing in inequalities (the false appearance of a sign change at ). It is easy to check by cross multiplication that an equivalent way to write this inequality is

| (31) |

and this will be the form we use in our proof of Theorem 6.10.

Theorem 6.11.

Consider the bivariate polynomial

and assume that for a given and that . Then

Proof.

Fix and let . By Corollary 6.10 and (31), we have

Since both sides are positive, we can square them, to get

Using the fact that , we can then simplify to get

Hence for any , we have that

| (32) |

Now let and satisfy . It is well known that the range of the Cauchy transform is the positive reals, so there exists some for which . It then suffices to show that , since (due to the fact that the Cauchy transform is decreasing) that would imply

as required.

To see that , we consider two cases. If , then trivially. Otherwise, we have , so by (32), we must have . However it is easy to check that

| (33) |

whenever , implying in this case as well. ∎

7 Illustrative Examples

In this section we hope to give some intuition as to how one can view the operator and (in particular) the role that the parameter plays. We then give computational examples that show the relative accuracy of Theorem 1.3. All plots and computations in this section were done using Mathematica 12.

7.1 Singular values of rectangular matrices

Before discussing polynomials directly, it will be informative to recall the connection with the singular values of matrices that was mentioned Section 1.3.3. That is, let and be matrices with

so that the roots of are

(and similar for and ). One (important) consequence of Theorem 2.3 is that there exists a matrix for which

Thus if we define to be the class of matrices which have the same dimensions and same singular values as , then the rectangular additive convolution can be viewed as a binary operation on these classes. Coupled with the observation made in Section 1.3.3 that we have the explicit formula

| (34) |

when and are Haar-uniform random unitary matrices of the appropriate size, one could feel justified in writing this binary relation as

An obvious question, then, is to what extent and have similar behavior. In general, they cannot be the same because the singular values of will depend on the singular vectors of and , whereas is independent of the singular vectors. However, if we were to interpret as some sort of “unitarily invariant” way of “adding” two matrices together, then Theorem 1.3 would be a statement about the behavior of the largest singular value under this operation.

The first relevant observation in this direction is that Theorem 1.3 simplifies greatly when , in that

Hence in this case, Theorem 1.3 reduces to

which, when written in the matrix context, becomes the inequality

| (35) |

That is, satisfies a triangle inequality similar to normal matrix addition (and in fact this triangle inequality can be derived from the normal one using (34)).

The shortcoming of (35) is that it neglects much of the information we have concerning the singular values of the original matrices. If we are to accept the interpretation that is some sort of a “unitarily invariant” version of addition, then we should suspect that the true answer will depend on all of the singular values of and . This is the case, and the purpose of is to try to obtain better bounds by accessing this extra information.

7.2 The role of

For the purpose of illustration, let us consider the matrix classes and with:

versus

It should be clear that the triangle inequality (35) would treat all of the sums involving and similarly:

However, the interpretation of as a “unitarily invariant” version of addition suggests that should be significantly larger than , since many of the rotations in (34) will result in

The goal then is to improve this bound by taking into account the positions of the other singular values (of both matrices). However, it is important for applications that we incorporate this information in a way that can be easily iterated, as we will often find ourselves wanting to apply knowledge we have gained about to gain knowledge about (for example). The upshot of Theorem 1.3 is that we can accomplish this using the transformation.

The intuition behind the action of that we find the most illuminating is inspired by a model from [20]. If one were to view the roots of as particles, then the application of can be seen as a gust of wind (with total strength parametrized by ) pushing the particles forward. In theory, one would expect any such wind to divide its force evenly between the particles (pushing them the same amount). However the operator has the property that the positive roots of and those of will always interlace111We will not prove this here, but it is a direct consequence of Theorem 2.3 — see [4].. That is, if

are the roots of and (respectively), then one will always have the inequality

As a result, the force of the wind treats the particles like “billiard balls” with polynomials like (that have many roots close to the largest root) transferring much of the energy onto the largest root. In comparison, will see a lot of its energy transferred onto its second-largest root, but as long as is not too big, there will not be much energy transferred on to the largest root.

Hence the distance that the operator pushes the root of a polynomial, when viewed as a function of , encodes different levels of information about the locations of the other roots. Values of that are too large will result in most of the energy being transferred onto the largest root (independent of the initial configuration). Similarly, small values of will result in very little of the energy being transferred on to the largest root (also independent of the initial configuration). Intuitively, the optimal will be one that allows as much initial force as possible while still avoiding too much transfer onto the largest particle.

7.3 Example computations

Let use consider the examples from the previous section in the case where and are matrices (so ). Hence

and the resulting convolutions are (where we have replaced with to aid readability):

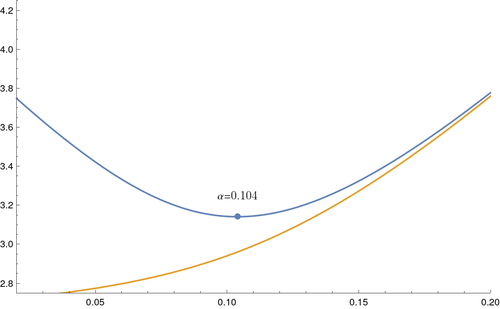

Figure 1 shows two functions of , plotted for each of the convolutions above: the true value of (in yellow) plotted against the bound given by Theorem 1.3 (in blue). In particular, the blue curve in each case will have value when (as dictated by the triangle inequality), while the value we are trying to bound will be the value of the yellow curve at . Unfortunately, we were forced to cut off the values at in the graphs due to precision issues, so we have listed the relevant values in Table 1.

8 Further Research

One possible direction of research comes from an observation in [3] concerning a degeneration in the rectangular convolution in the case ( in [3]) that allows one to compute singular value distributions of square matrices using the additive convolution. In particular, if the asymptotic singular laws of two independent (left and right unitarily invariant) matrices converge to and , then the asymptotic singular law of their sum is the unique probability measure on which, when symmetrized, is equal to the free convolution of the symmetrizations of and . In terms of polynomial convolutions, this would mean that

which is not true (in general). It is true that they share the same bounds; by Theorem 1.1,

and by Theorem 1.2,

One might then ask whether there is an inequality between the two, and we conjecture that, in fact, there is:

Conjecture 8.1.

For all in , we have

It is not hard to show that Conjecture 8.1 is true for basic polynomials in . Recall from Corollary 5.6 that for basic polynomials and that

Using a similar method, one can show that for these polynomials

As was noted in Remark 6.3, the positive roots of are decreasing with , which will result in the roots of majorizing the roots of . Since the function is convex for , the Cauchy transform is Schur convex on that range, and this implies Conjecture 8.1 (for this particular and ). In particular, it may be possible to prove Conjecture 8.1 using an inductive method like the one developed in Section 4.

Later versions of [14] use a similar argument on basic polynomials to prove the “base case” for Theorem 1.2 from Theorem 1.1 and, if true in general, Conjecture 8.1 would imply Theorem 1.2 directly from Theorem 1.1. It would be interesting to know whether Theorem 1.3 can be proved as a corollary of Theorem 1.1, as this would imply new identities in free probability. However, this seems unlikely; as was noted in Section 1.1, the only reason Theorem 1.2 can be stated using the operator is due to a degeneration at that does not hold for any other and there is no reason to believe that and can be compared in an asymptotically tight way for general .

References

- [1] O. Arizmendi, D. Perales, Cumulants for finite free convolution, Journal of Combinatorial Theory, Series A, 155 (2018), 244–266.

- [2] R. Askey, G. Gasper, Positive Jacobi polynomial sums. II, Amer. J. of Math. (1976), 98 (3), 709–737.

- [3] F. Benaych-Georges, Rectangular random matrices, related convolution, Probab. Theory Relat. Field (2009) 144:471-515. arXiv:math/0507336

- [4] J. Borcea, P. Brändën, The Lee-Yang and Pólya-Schur programs, II: theory of stable polynomials and applications, Comm. on Pure and Appl. Math., 62(12):1595–1631, 2009.

- [5] A. Elbert, A. Laforgia, On the zeros of associated polynomials of classical orthogonal polynomials, Differential and Integral Equations 6 (1993), 1137–1143.

- [6] A. Gribinski, A. W. Marcus, Biregular, bipartite Ramanujan graphs of arbitrary size and degree (in polynomial time), preprint. arXiv:2108.02534

- [7] A. Gribinski, A. W. Marcus, A theory of singular values for finite free probability, in preparation.

- [8] A. Knutson, T. Tao, The honeycomb model of tensor products I: Proof of the saturation conjecture. Jour. of the Amer. Math. Soc. 12.4 (1999): 1055-1090.

- [9] A. B. J. Kuijlaars, W. Van Assche, The asymptotic zero distribution of orthogonal polynomials with varying recurrence coefficients. J. of Approx. Theory 99.1 (1999): 167-197.

- [10] J. Leake, N. Ryder, On the further structure of the finite free convolutions, preprint. arXiv:1811.06382

- [11] E. H. Lieb, A. D. Sokal, A general Lee-Yang theorem for one-component and multicomponent ferromagnets. Comm. Math. Phys. 80 (1981), no. 2, 153–179.

- [12] A. W. Marcus, Discrete unitary invariance, preprint. arXiv:1607.06679

- [13] A. W. Marcus, Polynomial convolutions and (finite) free probability, preprint. arXiv:2108.07054

- [14] A. W. Marcus, D. A. Spielman, N. Srivastava, Finite free convolutions of polynomials, preprint. arXiv:1504.00350

- [15] A. W. Marcus, D. A. Spielman, N. Srivastava, Interlacing families I: bipartite Ramanujan graphs of all degrees, Ann. of Math. 182-1 (2015), 307-325. arXiv:1304.4132

- [16] A. W. Marcus, D. A. Spielman, N. Srivastava, Interlacing families III: improved bounds for restricted invertibility, to appear (Isr. Jour. of Math.) arXiv:1712.07766

- [17] A. W. Marcus, D. A. Spielman, N. Srivastava, Interlacing families IV: bipartite Ramanujan graphs of all sizes, FOCS (2015). arXiv:1505.08010

- [18] J. A. Mingo, R. Speicher. Free probability and random matrices. Vol. 35. New York, NY, USA: Springer, 2017.

- [19] A. Naor and P. Youssef, Restricted invertibility revisited, preprint. arXiv:1601.00948.

- [20] N. Srivastava. Spectral Sparsification and Restricted Invertibility Ph.D. Thesis, Yale University. https://math.berkeley.edu/ nikhil/dissertation.pdf

- [21] G. Szegö. Orthogonal polynomials. AMS, Providence, RI MR 51 (1975): 8724.

- [22] D. V. Voiculescu, Limit laws for random matrices and free products, D. Invent. math. (1991) 104: 201.

- [23] D. Wagner, Multivariate stable polynomials: theory and applications. Bull. of the Amer. Math. Soc. 48.1 (2011): 53-84.

- [24] H. Wilf, generatingfunctionology. AK Peters/CRC Press (2005).

- [25] Xie, J., Xu, Z. (2020). Subset selection for matrices with fixed blocks. To appear, Israel J. Math. arXiv:1903.06350

Appendix

In this appendix, we give a brief sketch of the computation leading from Theorem 6.4 to Corollary 6.5. We have seen such a calculation referred to as “standard” in various places in the literature, but wanted to give some indication as to how the proof goes for those who, like the authors, might be less familiar with such computations.

Lemma 8.2.

For and , let be a sequence of compact distributions for which

where . Then for all , we have

Proof.

Since all of the distributions are compact, we can interchange the limit with the integral defining the Cauchy transform. That is,

We then make a change of variable from to , using the Euler substitution:

yielding

| (36) |

We can then rewrite the integrand using partial fractions:

where we have defined

For , these integrals can be computed explicitly using the trigonometric substitution . This gives

since for all . The result follows by plugging these into (36) and simplifying. ∎