Change Point Estimation in Panel Data with Temporal and Cross-sectional Dependence

Abstract

We study the problem of detecting a common change point in large panel data based on a mean shift model, wherein the errors exhibit both temporal and cross-sectional dependence. A least squares based procedure is used to estimate the location of the change point. Further, we establish the convergence rate and obtain the asymptotic distribution of the least squares estimator. The form of the distribution is determined by the behavior of the norm difference of the means before and after the change point. Since the behavior of this norm difference is, a priori, unknown to the practitioner, we also develop a novel data driven adaptive procedure that provides valid confidence intervals for the common change point, without requiring any such knowledge. Numerical work based on synthetic data illustrates the performance of the estimator in finite samples under different settings of temporal and cross-sectional dependence, sample size and number of panels. Finally, we examine an application to financial stock data and discuss the identified change points.

Key words and phrases. adaptive estimation, autocovariance matrices, change point, estimation, least squares, panel data,

JEL Classification. C23, C33, C51

1 Introduction

The change point problem for univariate data has a long history in the econometrics and statistics literatures. A broad overview of the technical aspects of the problem is provided in Basseville and Nikiforov (1993); Csörgö and Horváth (1997). The problem has a wide range of applications in economics (Baltagi et al., 2016; Liangjun and Qian, 2015; Li et al., 2016) and finance (Frisén, 2008), while other standard areas include quality monitoring and control (Qiu, 2013), as well as newer ones, like genetics and medicine (Chen and Gupta, 2011) and neuroscience (Koepcke et al., 2016).

In many of these applications, the multivariate (panel) data streams exhibit both temporal, as well as cross-sectional dependence, since they reflect different facets of coordinated activity -e.g. stock price co-movements, cross-talk amongst brain regions and co-expression of members of genetic regions.

The rather limited technical literature on change point analysis for panel data focuses on the common break signal plus noise model given by

| (1.1) | |||||

where represents a common break fraction for all series (streams), the difference represents the magnitude of the shift for each series, and are random error processes. The primary objective is to estimate the location of change point , as well as the levels of the series before and after it.

Literature review: Different aspects of change point analysis have been studied in the literature for the aforementioned model, wherein the random process exhibits only temporal dependence (assumed cross-sectionally independent). Bai (2010) employed a least squares criterion to estimate the common change point and established its asymptotic distribution, while Horváth and Hušková (2012) developed tests for the presence of a change point during the observation period. Peštová and Pešta (2017) and Bardwell et al. (2018) provided a method to detect a common break point even when the change happens immediately after the first time point or just before the last epoch for panels with limited number of time points. Cho and Fryzlewicz (2015) segmented the second-order structure of a high-dimensional time series and used the CUSUM statistic to detect multiple change points. Further, Kim (2014); Baltagi et al. (2016); Barigozzi et al. (2018); Westerlund (2018) investigated estimation of the change point in panel data, wherein the cross-sectional dependence is modeled by a common factor model, which effectively makes the cross-sectional dependence low-dimensional.

However, as previously argued, often both temporal and cross-sectional dependence is present in panel data under the signal plus noise model. To the best of our knowledge, Cho (2016) represents the only work on change point analysis in such a setting and investigates both single and multiple change-point detection. The nature of the cross-sectional dependence is general, while geometrically decaying -mixing is assumed across time, and the number of series can grow at a polynomial rate in the number of time points . Another work that considers both temporal and cross-sectional dependence is by Safikhani and Shojaie (2017), that examines change point analysis for sparse high-dimensional vector autoregressive models.

Key contributions: In this paper, we consider the problem of single change point detection in high-dimensional panel data using a least squares criterion, where the temporal and cross-sectional dependence are captured through an infinite order moving average process (MA()). We establish the convergence rate (Theorem 2.1) and derive the asymptotic distribution (Theorem 2.2) for the least squares estimator of the change point. Further, since there are multiple regimes for the asymptotic distribution of the change point estimate determined by the underlying unknown signal-to-noise ratio, we also provide a self-adaptive, data driven method for computing confidence intervals of the change point that does not require us to know the specific regime.

Note that this work extends the analysis in (Bai, 2010) to the case where the multivariate MA() error process is correlated across its coordinates. Such correlations introduce a number of technical challenges that are successfully resolved in Theorems 2.1 and 2.2. Another broadly related work is that of Cho (2016). For the single change point analysis that is the focus of this paper, we note that our rate result is obtained under weaker detectability conditions for a much larger class of error processes and allowing faster growth of the time series as a function of the number of time points . Further, the obtained rate of the change point is sharper and in addition we derive its asymptotic distribution - a more detailed discussion of these points are provided in Remark 2.2 and Section 4. On the other hand, the latter paper develops methodology for detection of multiple change points, which is outside the scope of the current work.

The remainder of the paper is organized as follows. In Section 1.1, we describe the signal-plus-noise model exhibiting a single change point in its mean structure, with temporal and cross-sectional dependence introduced through a vector moving average process. In Section 2, we define the least squares estimator for the change point and establish its convergence rate and asymptotic distribution in Theorems 2.1 and 2.2, respectively. Further, we discuss that the assumptions required for these theorems hold under very mild conditions for certain illustrative examples considered in Section 2.2 which are employed often in practice. In Section 3, we propose a data based adaptive inference scheme for obtaining the asymptotic distribution of the change point estimate in practice which does not require prior knowledge on the signal-to-noise regime. Performance evaluation results based on synthetic data are presented in Section 4. Finally, an application of the proposed methodology to financial data is discussed in Section 5. Additional technical details and all proofs are delegated to an Appendix - Sections 6 and 7, respectively.

1.1 Modeling Framework

We observe (dimension depends on sample size ) from the following model:

| (1.2) | |||||

Here, is the change point and , are -dimensional mean vectors before and after the change point. All processes , , and correspond to -dimensional random vectors. Notation-wise we often write instead of , when there is no room for confusion. Further, are i.i.d. mean , variance random variables with finite 4th moments; i.e. . Finally, the coefficient matrices correspond to deterministic matrices. We assume for all and , are nested. That means the first components of is . Clearly, and are not nested, but they form triangular sequences. We consider as . For expository clarity, we shall use for , , , , , , , , , , , respectively.

The objective is to estimate the change point , together with all other model parameters .

In the above model, the data stream process exhibits dependence across both time and co-ordinates. Since is a stationary process, the covariance between and depends only on lag . Further, the population autocovariance matrix of order is given by

Note that are all matrices. If then and we have independence across time. On the other hand, if are all diagonal matrices, then so are the ones, which in turn implies component-wise independence. In this paper, we assume that the coefficient matrices have a general form.

This model for has attracted much attention in the literature and various aspects of it have been studied, including estimating the autocovariance matrices (Bhattacharjee and Bose (2014)), studying properties of the spectrum of the sample autocovariance matrices (Liu et al. (2015), Bhattacharjee and Bose (2016), Wang et al. (2017)), testing for the presence of trends (Chen and Wu (2018)) and so forth. Further, Bai (2010) and Bhattacharjee et al. (2017) obtained a consistent estimator of the change point when all are diagonal matrices. In this work, we extend the analysis to general coefficient matrices.

2 The change point estimator and its asymptotic properties

Next, we propose an estimator of the change point and study its asymptotic properties. Since the change point in the model is driven by changes in the mean structure, we employ a least squares criterion for the task at hand. Specifically, the estimate is obtained by

| (2.1) | |||||

The first result established is that of the rate of convergence of in Theorem 2.1. To that end, let denote the spectral norm of a matrix. Further, define . Note that time dependence in is characterized by the variation of the coefficient matrices across . Hence, the aggregate provides a measure of cross-sectional dependence in , but not of temporal dependence. We need the following signal-to-noise (SNR) condition for establishing the convergence rate of .

(SNR)

Note that is the average signal per model parameter, which drives the occurrence of the change point. The SNR condition intuitively states that the average signal needs to grow faster than . If the coefficient matrices satisfy , then the SNR condition reduces to

(SNR*) ;

i.e., the average signal needs to grow faster than ,

which is similar to the identifiability conditions in other change point problems that exhibit independence both across

time and across coordinates (see e.g. Bhattacharjee et al. (2017)). Examples of coefficient matrices satisfying are discussed in Sections 6.1.1, 6.1.2 and Example 2.3(ii). Often may not hold, as shown in Examples 2.3(i), 2.1 and 2.1. In the latter case, the SNR condition is required, which is stronger than the SNR*. Finally, note that the SNR condition depends only on the total number of time points observed, but not on the nature of the temporal dependence of .

Theorem 2.1.

Suppose (SNR) holds. Then .

If , then the convergence rate of is the same as that under independence across both time and panels. For details see Section 6.1.2. However, if grows with , the the convergence rate in Theorem 2.1 is compromised: this is the price paid for growing cross-sectional dependence.

Remark 2.1.

It is easy to see from the proof of Theorem 2.1 and Remark 7.1 that under cross-sectional independence -i.e. when - in SNR can be replaced by a smaller quantity . As a consequence, when , the conclusion of Theorem 2.1 continues to hold under the weaker (SNR′) condition . Further, if , then SNR′ reduces to SNR*.

Remark 2.2.

As mentioned in the Introduction, Cho (2016) considered the problem of single, as well as multiple change-point detection in high dimensional panel data under general cross-sectional dependence, but for processes that exhibit geometrically decaying -mixing across time. In general, a multivariate MA() process is not a geometrically decaying -mixing process (e.g. consider the case of polynomially decaying coefficients). Thus, there are many linear processes which are eligible under our setting, but can not be accommodated by Cho (2016).

Focusing on the results pertaining to a single change point, note that if the coefficients of the MA() process are geometrically decaying -e.g. autoregressive (AR) or autoregressive moving average (ARMA) processes-, then it becomes a geometrically decaying -mixing process. Although AR and ARMA processes can be considered as special cases of the model in Cho (2016), our results do not follow from those in that paper. The reason is that we employ a least squares based estimator, while that paper considers an estimator derived from a CUSUM statistic. The latter estimator requires the following identifiability condition which is stronger than the posited (SNR) above. In addition, the obtained convergence rate for the change point estimator is , which is also slower than the convergence rate of the least squares estimator for . Moreover, Cho (2016) assumed that all moments of are finite, whereas we only require finite -th order moments of . Finally, we allow the dimension of the data stream to grow as for , vis-a-vis the for some fixed required in the aforementioned paper.

2.1 Asymptotic distribution of the least squares estimator

Unlike the convergence rate result that can be established under the SNR condition, the derivation of the asymptotic distribution for is significantly more involved, as presented next. We start by noting that in the panel data setting, the asymptotic distribution of differs, depending on the following regimes: (I) , (II) and (III) (see Bai (2010)).

Recall that

in the presence of a single panel (univariate case), the following two results have been established in the literature: (i) if (Regime (II)) at an appropriate rate as a function of the sample size , then the asymptotic distribution of the change point is given by the maximizer of a Brownian motion with triangular drift (for details see Bhattacharya (1994)); and (ii) if (Regime (III)), then the

asymptotic distribution of the change point, in the random design setting, is given by the maximizer of a two-sided compound Poisson process (for details see Chapter 14 of the book by Kosorok (2008)). As previously mentioned and will be established rigorously next, in the panel data setting analogous regimes emerge, with the modification that in the case of (ii) since we are dealing with a fixed design (equispaced time points), the limit process becomes a two-sided generalized random walk. In addition, there exists a third one (Regime (I)), where the asymptotic distribution of the change point becomes degenerate at the true value.

Next, we introduce assumptions needed to establish these results. As we deal with dependence across both time and panels, we have the following modified regimes — (a) , (b) and (c) . If , then (a)-(c) coincide with (I)-(III) above. In Regime (a), the asymptotic distribution of the change point can be derived under the same assumptions as in Theorem 2.1. On the other hand, in the second and third regimes, a non-degenerate limit distribution can be obtained under the following additional assumptions. Detailed comments on these assumptions will be provided after stating the results.

Regime (b): , assumptions.

For all , define

| (2.2) |

We require, (A1) exists for all . (A2) is positive definite for all and . (A3) . If we have independence across time and panels -i.e. - condition (A3) is satisfied automatically. If we have independence across both time and panels, then further simplification of is possible. For more details, see Sections 6.1.1 and 6.1.2. Regime (c): , assumptions:. Consider the following disjoint and exhaustive subsets of :

| (2.3) | ||||

We make the following assumptions. (A4) does not vary with . (A5) For some , .

Define,

| (2.4) | |||||

(A6) , exists for all and . (A7) is positive definite for all , and . (A8) and , . (A9) .

Given the previously posited assumptions, we next state the following theorem that describes the limiting distribution of , whose proof is given in Section 7.3.

Theorem 2.2.

Suppose (SNR) holds. (a) If , then . (b) If and (A1), (A2) and (A3) hold, then for all and ,

where is a tight Gaussian process on with continuous sample paths.

(c) If and (A4)-(A9) hold, then

where for each , and

Discussion of Theorem 2.2. We now provide detailed comments on the assumptions and how they relate to the three regimes established in Theorem 2.2.

In the first regime, the signal for is high and therefore the difference

becomes a point

mass at . On the other hand, in the second and third regimes, the total signal is weak and moderate, respectively, and a non-degenerate limit distribution can be obtained under additional assumptions.

Under the last two regimes, the results are based on the weak convergence of the process

| (2.5) |

Under appropriate conditions (as mentioned in Theorem 2.2), converges weakly to the unique maximizer of the limiting process. For more details see Lemma 7.2.

Regime (b): . In the second regime, the asymptotic covariance of is proportional to for all , and hence the need for assumption (A1). Discussion of conditions under which (A1) is satisfied are given in Proposition 2.3. Assumption (A2) is required for establishing the non-degeneracy of the asymptotic distribution. Finally, the asymptotic normality of requires (A3). If -i.e. if we have independence across time- then (A3) is satisfied automatically.

Regime (c): . Under the third regime, the limiting process has two components based on the partition of into sets and , defined in (2.3). Observe that is the collection of all such indices whose corresponding variables eventually have the same mean before and after the change point. In the second regime, is the empty set. On the other hand, under the third regime, may not be empty, but can be at most a finite set. Hence, is necessarily an infinite set.

These two sets in the partition contribute differently to the limit. Let ,

Note that

| (2.6) |

Limit of : Conditions (A4) and (A5) are required to establish the limit of the random part involving . The asymptotic covariance between and is given by for all and . Existence of these covariances and non-degeneracy of the corresponding asymptotic distributions are guaranteed by (A6) and (A7) for and . Condition (A8) is a technical condition and is required for establishing the asymptotic normality of for all and . As is a finite set, by (A4)-(A8), converges weakly to the process , described in Theorem 2.2(c). Limit of : The limit of the random part involving is an appropriately scaled Gaussian process on with a triangular drift, as given by in Theorem 2.2(c) and can be established using similar arguments given in Regime (b). Analogous to Assumptions (A1), (A2) and (A3) in Regime (b) are conditions (A6), (A7) for and and (A9). Discussion of conditions under which Assumption (A6) is satisfied are given in Proposition 2.4. Dependence between and : Moreover, the limits coming from and are correlated and their covariances are given by , where and . Thus, we require Assumptions (A6) and (A7) for all and . (A9) is a technical assumption. Following the proof of Theorem 2.2(c), at some point we need to establish the asymptotic normality of

| (2.7) |

Note that for , is a collection of infinitely many centered random variables. To apply Lyapunov’s central limit theorem to (2.7), we require

| (2.8) |

By (A6) and (A7), the left side of (2.8) is dominated by

| (2.9) | |||||

for some . (A9) is a natural sufficient condition for (2.9) to converge to . Similarly we need (A8) for the asymptotic normality of for all and .

Remark 2.3.

The asymptotic distributions obtained in Theorem 2.2 can be simplified further for some special cases such as independence across panels and independence across both panels and time.

Independence across panels: Then, for all , and . This implies that the limits of are independent across . Moreover, the limits coming from and are also independent. For more details, see Section 6.1.1. Independence across time and panels: Then, the population autocovariance matrix and consequently , only when and . More details are given in Section 6.1.2.

Sufficient conditions for (A1) and (A6). Next, we further elaborate on Assumptions (A1) and (A6) that ensure the existence of certain limits, which are not trivially satisfied. We need some restrictions on the means and and on the coefficient matrices in the panel data model (1.2) for satisfying (A1) and (A6). Propositions 2.3 and 2.4, given below, provide sufficient conditions for (A1) and (A6) to hold. Their proofs are given in Section 7.4.

Define for any sequence of matrices ,

Proposition 2.3.

Suppose the following conditions hold. (a) , (b) , (c) , (d) , (e) , (f) . Then, under , exists for all .

Proposition 2.4.

Proposition 2.3 needs Conditions (a)-(f) for satisfying (A1). Next we explain these conditions. For a sequence , the first order differences of grow slower than if holds. Conditions (a)-(d) in Proposition 2.3 assume that the first order differences of sequences , , and grow at a slower rate than these sequences respectively. Conditions (e) and (f) in Proposition 2.3 respectively ensure that, uniformly over and , the first order differences of and the sequence decay faster than and respectively.

In Proposition 2.4, we divide Assumption (A6) into three parts — (I) exists for all , (II) exists for all and and (III) exists for all and . For (I), Proposition 2.4 needs (a)-(c) given in Proposition 2.3 and two additional Conditions (g) and (h) which are same as (e) and (f) respectively except is replaced by and the rate of decay for (g) and for (h) (as ). Proposition 2.4 also states that (II) holds if (a)-(c) in Proposition 2.3 are satisfied along with Conditions (i) and (j) which are similar to (g) and (h) except here the rates of decay are and respectively. Moreover, (III) is satisfied if (a) and (c) in Proposition 2.3 hold.

Consider the following simplified conditions. (k) and . That is uniformly over and , the first order differences of and the sequence decay faster than . (l) and . That is uniformly over and , the first order differences of and the sequence decay faster than . Suppose (a)-(d) in Proposition 2.3 hold and (e.g. and ). Then it is easy to see that (A1) and (A6) are satisfied under (k) and (l) respectively.

If and , then (g)-(j) in Proposition 2.4 reduce to (l1), given below. (l1) and . That is uniformly over and , the first order differences of and the sequence decay faster than .

Following the proof of Propositions 2.3 and 2.4, it is easy to see that, under cross-sectional independence i.e. when , and both can be replaced by smaller quantity throughout the propositions. In this case also, (e), (f) in Proposition 2.3 are implied by (k) and (g)-(j) in Proposition 2.4 are implied by (l). Moreover if , then it can be replaced by and (l) reduces to (l1).

Sufficient conditions for (A2) and (A7). It is easy to see that and are positive definite, if is positive definite for all . Using similar arguments as in the univariate case in Brockwell and Davis (2009), if is positive definite then so is for all . Therefore, a sufficient condition for (A2) and (A7) is positive definiteness of uniformly over i.e., where denotes its smallest eigenvalue.

2.2 Illustrative Examples

Next, we provide some examples of coefficient matrices which satisfy the assumptions required for Theorems 2.1 and 2.2. Note that Assumptions (A1), (A2), (A6), (A7) and the first condition of (A8) relate to the coefficient matrices and, as previously discussed, are rather technical in nature. The following examples and ensuing discussion provide additional insight into the nature of these assumptions.

For any matrix , define .

For all examples given below, suppose the first order differences of sequences and grow at a slower rate than these sequences respectively, i.e., suppose (c) and (d) in Proposition 2.3 are satisfied.

Example 2.1.

Banded coefficient matrices: A matrix is said to be -banded, if for . It is known that the -th order population auocovariance matrix can be consistently estimated, if are -banded (see e.g. Bhattacharjee and Bose (2014)). The -banded structure of implies that and are uncorrelated for . For all , suppose is symmetric and if . Also assume , and the smallest eigenvalue of is bounded away from for at least one . Then, and they are bounded away from . Hence, (A2), (A7) and the first condition of (A8) hold. The SNR condition becomes . Finally, (A1) and (A6) are satisfied if (a)-(j) in Propositions 2.3 and 2.4 hold with replaced by . For more explanation, suppose the first order differences of sequences and grow at a slower rate than these sequences respectively. Then (A1) holds if uniformly over and , the first order differences of and the sequence decay faster than and respectively. Moreover (A6) is satisfied if uniformly over and , the first order differences of and the sequence decay faster than and respectively.

Example 2.2.

VARMA process: Suppose follows a VARMA process given by

| (2.10) |

where , the smallest eigenvalue of and are bounded away from with respect to both and , and is as described after Model (1.2). Then, (2.10) can be expressed as Model (1.2) under the causality condition , for some . For details, see Brockwell and Davis (2009) and Bhattacharjee and Bose (2014). We assume these causality conditions hold. Then, and decays exponentially with . Hence, and they are also bounded away from . Therefore, (A2), (A7) and the first condition of (A8) are met. In addition, (SNR) becomes . Finally, (A1) and (A6) are satisfied if conditions (k) and (l1), stated after Propositions 2.3 and 2.4, hold respectively.

Example 2.3.

(Separable cross-sectional and time dependence) Often, dependence among panels and dependence across time can be separated. For example, let for all and for some , matrix , where is a sequence of nested matrices. It is easily observed that the time dependence is controlled by whereas cross-sectional dependence is absorbed into . As these two types of dependency are controlled by two different parameters, this model is said to exhibit separable cross-sectional and time dependence. Here, and . Therefore, and . Thus, and are of orders and respectively and they characterize only cross-sectional dependence. The following statements hold: (a) (SNR) is satisfied if . (b) (A1) and (A6) hold if (a)-(j) in Propositions 2.3 and 2.4 are satisfied after replacing and by and respectively. More simplification is given in (i) and (ii) below. (c) (A2) and (A7) hold if the smallest singular value of is bounded away from and . (d) The first condition in (A8) is satisfied if . The above statements provide simplified assumptions for Theorems 2.1 and 2.2 to hold. Next, we discuss some special choices for which often arise in practice. (i) Coefficient matrices with equal off-diagonal elements. Coefficient matrices with equal off-diagonal entries arise whenever the covariances between and , , do not depend on and ; i.e., when these covariances are all equal. Suppose where , is the identity matrix of order and is the matrix with all elements . Then . Thus, (SNR) becomes . In Propositions 2.3 and 2.4, condition (c) implies conditions (a) and (b). Also as , (A1) and (A6) hold if (k) and (l), stated after Propositions 2.3 and 2.4, are satisfied respectively. As is positive definite with smallest eigenvalue , Assumptions (A2) and (A7) hold if . Moreover, the condition of (A8) is satisfied, since and . (ii) Toeplitz coefficient matrices. Toeplitz matrices have a wide range of applications in many fields, including engineering, economics and biology for modeling and analysis of stationary stochastic processes. A Toeplitz structure in coefficient matrices can arise naturally, when the covariances between and depends only on and . Suppose where and the smallest eigenvalue of is bounded away from . Then, . Thus, , and they are bounded away from . Hence, (SNR) becomes , which is the same SNR required for independence across both time and panels. (A1) and (A6) holds if (k) and (l1), stated after Propositions 2.3 and 2.4, are satisfied respectively. As the smallest eigenvalue of is bounded away from , (A2) and (A7) also hold if . Moreover, this choice of satisfies (A8).

Example 2.4.

One may think that the structures in Examples 2.3 and 2.4 are restrictive. In Example 6.3, we consider a significantly wider class of coefficient matrices which are dominated by separable cross-sectional and time dependence structure.

Example 2.5.

Independence across panels and dependence across time. All previous examples deal with correlated panels. In this example, we consider the case where panels are independent, but dependence across time is present. As cross-sectional dependence is absorbed into the off-diagonal entries of the coefficient matrices, independence across panels can be modeled with diagonal coefficient matrices . Suppose . Then, by Remarks 2.1 and 2.3, the conclusions of Theorems 2.1 and 2.2 continue to hold for this case if instead of (SNR), condition (SNR*) is satisfied. Moreover, (A1) and (A6) holds if (k) and (l1), stated after Propositions 2.3 and 2.4, are satisfied respectively. Further, suppose . Then, (A2), (A7) and the first condition of (A8) hold. In this model, a weaker assumption (A8*) (instead of (A8)) stated in Section 6.1.1 also serves our purpose: the expressions for , defined in (2.2) and (2.4) can be simplified further and the processes and in Theorem 2.2(c) turn out to be independent. A detailed discussion of this model is given in Section 6.1.1.

Some more examples are deferred to Section 6.2.

Corollary 2.1.

Connections to the results presented in Bai (2010). (A) We next compare our results previously with those in the paper by Bai (2010) that posited that data streams are generated according to the model in Example 2.5 (elaborated in Section 6.1.1) and considered the following assumptions:

-

1.

-

2.

-

3.

The key result in that paper is that under assumptions (1)-(3) . Details are presented in Theorems and in Bai (2010).

In comparison, we assume in Example 2.5 (elaborated in Section 6.1.1) that , which is clearly weaker than (1). Further, observe that assumptions (SNR*) and (2) above indicate two different regimes, since none of them implies the other. Moreover, note that assumption (3) above is stronger than the posited (SNR*). Therefore, Example 2.5 (elaborated in Section 6.1.1(a)) implies Bai (2010)’s result under assumptions (1) and (3).

(B) Suppose are uncorrelated. Then, for all . Thus in (2.4) becomes . Let denote the standard Brownian motion.

Suppose that are uncorrelated, , and that exists. Then, Bai (2010) also established in Theorem that

| (2.11) |

To derive (2.11), one needs to establish the asymptotic normality of , presented at the end of the first column on page in Bai (2010). To that end, further assumptions need to be imposed on and in addition to , as has been previously discussed around (2.7)-(2.9). However, such assumptions appear to be missing in Bai (2010).

Finally, consider all the assumptions stated before (2.11) in (B). Further, assume the weaker condition instead of . Recall the sets and from (2.3). We additionally need (A9) and as the empty set for (2.11) to hold. Section 6.1.1(c) provides a more general result for the model in Example 2.5 when are not necessarily uncorrelated.

3 Data Driven Adaptive Inference

The results in Theorem 2.2 identify three different limiting regimes for the least squares estimator that are determined by the norm difference of the model parameters before and after the change point. The latter norm difference is a priori unknown, thus posing a dilemma for the practitioner of which regime to use for construction of confidence intervals for the change point. Next, we present a data driven adaptive procedure to determine the quantiles of the asymptotic distribution of the change point, irrespective of the specific regime pertaining to the data at hand. Let

Define the sample autocovariance matrix of order by

For any matrix of order and , the banded version of is

It is known in the literature that is not consistent for in . However, a suitable banded version of is consistent when the coefficient matrices belong to an appropriate parameter space. See Bhattacharjee and Bose (2014) for a detailed discussion on the estimation of autocovariance matrices. A discussion of the parameter space for consistency is provided after stating the required SNR condition for adaptive inference (SNR-ADAP), later in this section.

For -dimensional vectors , let be the vector of dimension , built by stacking ; is a matrix, comprising of -many block matrices, with the -th block being . Generate data from the process that satisfies

Irrespective of the probability distribution of the originally observed data , we always generate data from the above Gaussian process in the proposed adaptive inference procedure. Define and write . Obtain

The following theorem states the asymptotic distribution of under a stronger identifiability condition (SNR-ADAP) together with consistency of . (SNR-ADAP) We first define the appropriate parameter spaces for where consistency of can be achieved. To impose restrictions on the parameter space, define for any nested sequence of matrices ,

is said to have polynomially decaying corner if for some and for all large . Let We define the following class of for some and ,

which ensures that the dependence between and decreases with the lag . Note that summability implies that the decay rate of cannot be slower than a polynomial rate. In case of a finite order moving average process, as we have a finite number of norm bounded parameter matrices, will automatically belong to for all and .

For any , let be the -th coordinate of the vector . Next, we ensure that for any and , the dependence between and becomes weaker for larger lag . We achieve this by putting restrictions over for all . Consider the following class for some and as

Though the conditions in are very technical, but they are satisfied if ’s are decaying exponentially fast and for all , has polynomially decaying corner. For VAR and VARMA processes, if all parameter matrices have polynomially decaying corner, then they satisfy the condition of . For details see Bhattacharjee and Bose (2014).

To establish the result, we introduce next the following assumptions. (C1) for some and . Let be the -th coordinate of . (C2) and for some . (C3) . By Theorem of Bhattacharjee and Bose (2014), if (C1), (C2) and (C3) hold, then

| (3.1) |

The following theorem provides the limiting distribution of . Its proof is given in Section 7.5.

Theorem 3.1.

Suppose SNR-ADAP, (C1), (C2) and (C3) hold. (a) If , then . (b) If and (A1), (A2) and (A3) hold, then converges in distribution to the same limit as does in Theorem 2.2(b).

(c) If and (A4)-(A9) hold, then converges in distribution to the same limit as does in Theorem 2.2(c).

Note that the asymptotic distribution of is identical to the asymptotic distribution of . Therefore, in practice we can simulate for a large number of replicates and calculate the quantiles of the resulting empirical distribution. The above Theorem guarantees that the empirical quantiles will be accurate estimates of the quantiles of the limiting distribution under the true regime. Note that the proposed procedure is trivially parallelizable, which controls its computational cost. However, the procedure requires a stronger (SNR-ADAP) condition, together with assumptions (C1), (C2) and (C3), which represents the price we pay for not knowing the exact regime.

4 Performance Evaluation

Next, we investigate the performance of the least squares estimator on synthetic data, and also undertake a comparison with the one introduced in Cho (2016), henceforth denoted by DCn.

Models considered: Model (1.2) is examined with the following two choices for the error process . Model 1: ARMA process. Let , where and . It is easy to see that and hence the process is causal. Therefore, it can be represented as an MA process with exponentially decaying spectral norm of the coefficient matrices. Moreover, this process is also a geometrically decaying -mixing process. Model 2: MA process with polynomially decaying coefficient. Let . We consider two choices for — Model 2a: and Model 2b: , where denotes the identity matrix of order and is a matrix with all entries equal to . In both models, the coefficient matrices are polynomially decaying. In addition, is bounded away from , bounded above for Model 2a and of order for Model 2b. It is then easy to see that they are not geometrically decaying -mixing processes, and therefore, are not amenable to the procedure in Cho (2016). Although no theoretical results are established for this model in the latter paper, the ensuing simulation results render support to the empirical fact that the change point estimator in Cho (2016) behaves similarly to the least squares estimator introduced in this study. Define

| (4.1) |

Note that Cho (2016) requires , while the least squares estimator requires . Throughout this section we consider . The choices for and the probability distribution of are specified in the ensuing subsections, depending on the objective under consideration. To better understand the performance of the change point estimators, we also mention the value of SNR ( for DCn and for ) and the signal . Consistency of the change point estimators needs the SNR to go to infinity. Moreover, asymptotic distribution of the change point estimators depends on .

(A) Effect of the (SNR) condition: We simulate from , with . Further, we consider the following two choices for and . (i) and . In this case, is bounded and therefore the identifiablity condition of Cho (2016) is not satisfied. Moreover, , which implies (SNR) holds for Models 1 and 2a. However, since for some , (SNR) is not satisfied for Model 2b.

(ii) and . In this case, and . Therefore, both the identifiablity condition in Cho (2016) and (SNR) hold.

Tables 4.1 and 4.2 depict the performance of the change point estimators in Cases (i) and (ii), respectively. In Table 4.1, performs badly in Model 2b and DCn does not perform well either, since the required SNR condition is not satisfied in either case. On other cells in Table 4.1, (SNR) is satisfied and consequently exhibits good performance. In Table 4.2 for Models 1 and 2a, and DCn estimate very well and fairly accurately in the presence of a very high signal. In Table 4.2 for Model 2b, the magnitude of the signal is moderate and therefore and DCn do not perform as accurately as for Models 1 and 2a, but their performance is overall satisfactory.

| , | , | , | , | |||||

|---|---|---|---|---|---|---|---|---|

| Model 1 | 0.59 (0.074) | 0.78 (0.44) | 0.536 (0.039) | 0.85 (0.36) | 0.4936 (0.0068) | 0.67 (0.42) | 0.5024 (0.0028) | 0.83 (0.44) |

| SNR (Model 1) | 22.36 | 0.6 | 31.62 | 0.588 | 70.71 | 0.569 | 100 | 0.563 |

| (Model 1) | 1.602 | 1.602 | 1.614 | 1.614 | 1.631 | 1.631 | 1.635 | 1.635 |

| Model 2a | 0.584 (0.083) | 0.68 (0.37) | 0.461 (0.037) | 0.82 (0.41) | 0.5068 (0.0072) | 0.75 (0.33) | 0.4974 (0.0031) | 0.79 (0.39) |

| SNR (Model 2a) | 22.36 | 0.6 | 31.62 | 0.588 | 70.71 | 0.569 | 100 | 0.563 |

| (Model 2a) | 1.602 | 1.602 | 1.614 | 1.614 | 1.631 | 1.631 | 1.635 | 1.635 |

| Model 2b | 0.83 (0.46) | 0.69 (0.34) | 0.64 (0.38) | 0.78 (0.42) | 0.72 (0.47) | 0.67 (0.32) | 0.81 (0.41) | 0.84 (0.48) |

| SNR (Model 2b) | 0.0447 | 0.6 | 0.0316 | 0.588 | 0.01414 | 0.569 | 0.01 | 0.563 |

| (Model 2b) | ||||||||

| , | , | , | , | |||||

|---|---|---|---|---|---|---|---|---|

| Model 1 | 0.4985 () | 0.5018 () | 0.5012 () | 0.5016 () | 0.5008 () | 0.499 () | 0.5002 () | 0.5002 () |

| SNR (Model 1) | 17.014 | 25.743 | 69.812 | 108.574 | ||||

| (Model 1) | 500 | 500 | 1000 | 1000 | 5000 | 5000 | 10000 | 10000 |

| Model 2a | 0.5011 () | 0.5015 () | 0.501 () | 0.5014 () | 0.5006 () | 0.4992 () | 0.5001 () | 0.5002 () |

| SNR (Model 2a) | 17.014 | 25.743 | 69.812 | 108.574 | ||||

| (Model 2a) | 500 | 500 | 1000 | 1000 | 5000 | 5000 | 10000 | 10000 |

| Model 2b | 0.405 (0.123) | 0.62 (0.1) | 0.552 (0.058) | 0.43 (0.072) | 0.4911 (0.013) | 0.5107 (0.0538) | 0.5042 (0.007) | 0.5088 (0.0489) |

| SNR (Model 2b) | 22.36 | 17.014 | 31.62 | 25.743 | 70.71 | 69.812 | 100 | 108.574 |

| (Model 2b) | 0.95 | 0.95 | 0.98 | 0.98 | 0.99 | 0.99 | 1 | 1 |

(B) Effect of dimension and sample size : Next, we simulate from the same setup as in (A)(ii) and consider . Clearly, both and go to . However, the DC estimator additionally requires for some , which is not satisfied when . Nevertheless, the results in Table 4.3 suggest that DCn performs as well as when .

| , | , | , | , | |||||

|---|---|---|---|---|---|---|---|---|

| Model 1 | 0.5016 () | 0.5016 () | 0.4988 () | 0.5014 () | 0.5006 () | 0.5006 () | 0.4999 () | 0.5002 () |

| SNR (Model 1) | 38.045 | 75.709 | 621.007 | 1961.925 | ||||

| (Model 1) | 5590.17 | 5590.17 | 25436 | 25436 | ||||

| Model 2a | 0.5014 () | 0.5012 () | 0.5014 () | 0.5015 () | 0.5007 () | 0.4994 () | 0.5001 () | 0.5001 () |

| SNR (Model 2a) | 38.045 | 75.709 | 621.007 | 1961.925 | ||||

| (Model 2a) | 5590.17 | 5590.17 | 25436 | 25436 | ||||

| Model 2b | 0.578 (0.074) | 0.594 (0.084) | 0.468 (0.028) | 0.538 (0.038) | 0.5044 (0.0052) | 0.4952 (0.0048) | 0.5017 (0.0012) | 0.4985 (0.0018) |

| SNR (Model 2b) | 22.36 | 38.045 | 31.62 | 75.709 | 70.71 | 621.007 | 100 | 1961.925 |

| (Model 2b) | 2.24 | 2.24 | 2.94 | 2.94 | 8.895 | 8.895 | 18.07 | 18.07 |

(C) Effect of moments: Next, we simulate from and consider , , and to be as in settings (A)(ii) and (B). Recall that the DC estimator requires finite moments of all orders, whereas only requires a -th order moment. The above choice for has finite moments up to order . Tables 4.4 and 4.5 illustrate the performance of both change point estimators. As expected, DCn exhibits an inferior performance, whereas estimates the change point very well, as seen in both Tables 4.4 and 4.5.

| , | , | , | , | |||||

|---|---|---|---|---|---|---|---|---|

| Model 1 | 0.5017 () | 0.59 (0.132) | 0.5011 () | 0.62 (0.072) | 0.5008 () | 0.69 (0.0494) | 0.5001 () | 0.39 (0.0457) |

| Model 2a | 0.5014 () | 0.63 (0.112) | 0.4987 () | 0.42 (0.069) | 0.5007 () | 0.42 (0.0516) | 0.5002 () | 0.64 (0.0439) |

| Model 2b | 0.612 (0.126) | 0.58 (0.119) | 0.559 (0.046) | 0.41 (0.072) | 0.4932 (0.009) | 0.67 (0.0513) | 0.4965 (0.0056) | 0.62 (0.0445) |

| , | , | , | , | |||||

|---|---|---|---|---|---|---|---|---|

| Model 1 | 0.5018 () | 0.62 (0.115) | 0.5014 () | 0.66 (0.069) | 0.5006 () | 0.61 (0.0491) | 0.4998 () | 0.42 (0.0457) |

| Model 2a | 0.5014 () | 0.58 (0.119) | 0.5011 () | 0.56 (0.063) | 0.4992 () | 0.38 (0.0501) | 0.5001 () | 0.64 (0.0442) |

| Model 2b | 0.474 (0.077) | 0.64 (0.121) | 0.557 (0.019) | 0.44 (0.071) | 0.4933 (0.0047) | 0.42 (0.0515) | 0.5012 (0.0018) | 0.38 (0.0437) |

(D) Performance of the Asymptotic distribution of : We consider the same , , and probability distribution of as in setting (A). Consider the following two choices for : (i) for Models 1 and 2a, and for Model 2b. Therefore, , but . (ii) for Models 1 and 2a, and for Model 2b. Therefore, , but . In Tables 4.6-4.9, we present 95% confidence intervals assuming knowledge of the true limiting regime, as well as their adaptive counterparts, along with the proportion of containing based on replications. Tables 4.6 and 4.8 report theoretical confidence intervals (TCI) which are obtained by simulating observations from the asymptotic distribution given in Theorem 2.2 assuming knowledge of the true limiting regime and then computing the sample quantiles. Tables 4.7 and 4.9 present adaptive confidence intervals (ACI) obtained by the method discussed in Section 3. The simulation results show tighter confidence intervals as the sample size increases. This is due to the fact . Finally, the performance of ACI is as good as TCI, which demonstrates the utility of the data-driven adaptive procedure.

| , | , | , | , | |||||

|---|---|---|---|---|---|---|---|---|

| 95% TCI | EP | 95% TCI | EP | 95% TCI | EP | 95% TCI | EP | |

| Model 1 | 0.2601, 0.7426 | 95.2 | 0.3483, 0.6294 | 94.8 | 0.4552, 0.5381 | 94.8 | 0.4736, 0.5230 | 95 |

| Model 2a | 0.2667, 0.7273 | 94.6 | 0.3592, 0.6444 | 95.4 | 0.4568, 0.5406 | 95.2 | 0.4730, 0.5243 | 94.8 |

| Model 2b | 0.2689, 0.7411 | 94.6 | 0.3527, 0.6345 | 94.8 | 0.4558, 0.5385 | 95.2 | 0.4731, 0.5244 | 94.9 |

| SNR | 4.73 | 5.62 | 8.41 | 10 | ||||

| 0.211 | 0.178 | 0.119 | 0.1 | |||||

| , | , | , | , | |||||

|---|---|---|---|---|---|---|---|---|

| 95% TCI | EP | 95% TCI | EP | 95% TCI | EP | 95% TCI | EP | |

| Model 1 | 0.342, 0.650 | 95.4 | 0.423, 0.576 | 95.2 | 0.4844, 0.5152 | 94.8 | 0.4921, 0.5077 | 95.2 |

| Model 2a | 0.346, 0.652 | 94.4 | 0.422, 0.577 | 94.4 | 0.4844, 0.515 | 94.8 | 0.4923, 0.5075 | 95 |

| Model 2b | 0.344, 0.646 | 95.4 | 0.422, 0.573 | 94.8 | 0.4846, 0.5148 | 95.2 | 0.4924, 0.5075 | 94.8 |

| SNR | 22.36 | 31.62 | 70.71 | 100 | ||||

| 1 | 1 | 1 | 1 | |||||

| , | , | , | , | |||||

|---|---|---|---|---|---|---|---|---|

| 95% ACI | EP | 95% ACI | EP | 95% ACI | EP | 95% ACI | EP | |

| Model 1 | 0.2729, 0.7472 | 93.2 | 0.3631, 0.6589 | 93.8 | 0.4602, 0.5439 | 94.4 | 0.4766, 0.5257 | 94.8 |

| Model 2a | 0.2777, 0.7472 | 94.2 | 0.3707, 0.6592 | 95.8 | 0.4585, 0.5445 | 94.6 | 0.4759, 0.5271 | 95 |

| Model 2b | 0.2763, 0.7563 | 93.8 | 0.3709, 0.6489 | 94.6 | 0.4568, 0.5443 | 95.6 | 0.4744, 0.5271 | 95.2 |

| SNR | 4.73 | 5.62 | 8.41 | 10 | ||||

| 0.211 | 0.178 | 0.119 | 0.1 | |||||

| , | , | , | , | |||||

|---|---|---|---|---|---|---|---|---|

| 95% ACI | EP | 95% ACI | EP | 95% ACI | EP | 95% ACI | EP | |

| Model 1 | 0.348, 0.648 | 93.8 | 0.423, 0.573 | 94.4 | 0.4844, 0.5152 | 94.6 | 0.4924, 0.5076 | 95.4 |

| Model 2a | 0.346, 0.652 | 94.2 | 0.422, 0.573 | 94.4 | 0.4848, 0.5152 | 95.4 | 0.4921, 0.5073 | 94.8 |

| Model 2b | 0.346, 0.648 | 95.4 | 0.422, 0.574 | 94.4 | 0.4846, 0.5150 | 95.2 | 0.4924, 0.5075 | 95.2 |

| SNR | 22.36 | 31.62 | 70.71 | 100 | ||||

| 1 | 1 | 1 | 1 | |||||

5 Application to Financial Asset Prices

The data set comprises of weakly stock prices for 75 financial US firms - banks, insurance companies and broker-dealers covering the period from 1/2/2001 to 12/27/2016, containing in total time points. The data were retrieved from Wharton’s Research Data Service (WRDS). First, log-returns were calculated, where denotes the stock price at time for firm . The final number of firms analyzed is 66 that had sufficient data throughout the time period considered.

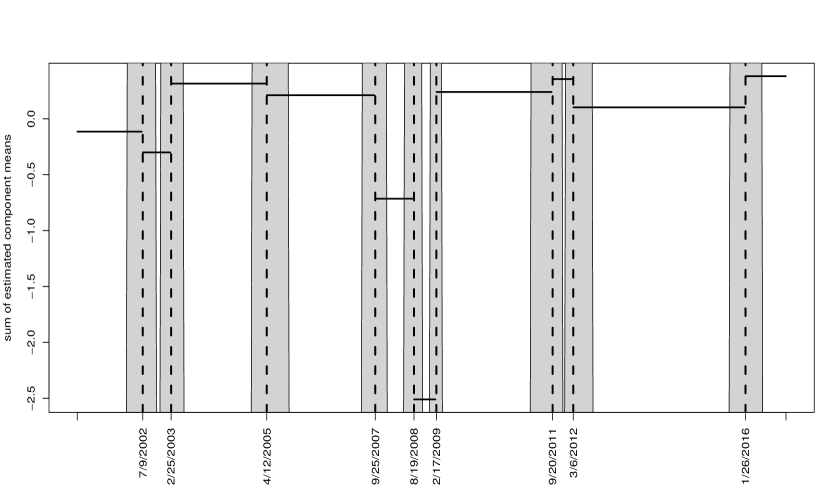

Since the developed methodology focuses on a single change point, we considered the following strategy, also employed in Billio et al. (2012). We consider 24-month-long rolling-windows, separated by 3 months, thus applying the procedure 60 times. For each window containing 104 time points, we compute the minimizer of the least squares criterion function given in (2.1). The minimizers that appear at least twice among these 60 potential minimizers, are declared to be candidate change points and reported in Table 5.1. There are 9 such change points. To calculate confidence intervals, we partition the time axis into 9 windows, starting from the mid-point of the interval contain the -th and -th change points to the mid-point of the -th and -th change points. For each of these 9 windows, we employ the adaptive method given in Section 3 for computing confidence intervals and present these intervals in Table 5.1.

The identified nine change points together with their calculated confidence intervals cover time periods where major shocks occurred, thus providing evidence of the validity of the proposed methodology. Specifically, the 2002 coincides with the popping of the Internet bubble, while the 2003 marks the turning point for the broader market; the 2005 change point and its confidence interval cover a period of rapid consecutive interest increases from 2.5% to 4% by the Fed; the 2007 is a few weeks after the August market turmoil induced by global credit fears and a liquidity crunch that led the Fed to shore up substantially liquidity of the US Banking system; the 2008 change point is a few weeks before the collapse of Lehman Brothers on 9/15/2008; the 2009 one is a couple of weeks off the bottom of the stock market following the Great Recession; the 2011 change point is a the center of the time period that led to significant downgrades of various European Union countries sovereign debt including Italy, Spain, Portugal and Greece; the 2012 one is related to the finalization of the second bailout package for Greece that provide a respite from market turmoil; finally, the 2016 change point is associated with a crash in oil prices and concerns about the Chinese economy that led to a sharp correction in the SP500 index of more than 5% during January of that year.

| CP | 7/9/2002 | 2/25/2003 | 4/12/2005 | 9/25/2007 | 8/19/2008 | 2/17/2009 |

|---|---|---|---|---|---|---|

| LCI | 2/26/2002 | 12/3/2002 | 12/14/2004 | 6/12/2007 | 6/3/2008 | 12/30/2008 |

| UCI | 11/5/2002 | 6/17/2003 | 10/18/2005 | 1/22/2008 | 11/4/2008 | 4/14/2009 |

| CP | 9/20/2011 | 3/6/2012 | 1/26/2016 |

|---|---|---|---|

| LCI | 3/29/2011 | 1/3/2012 | 9/22/2015 |

| UCI | 12/20/2011 | 8/21/2012 | 6/21/2016 |

Further, we used the methodology based on double CUSUM statistics introduced in Cho (2016) and the resulting candidate change points are given in Table 5.2. Note that the there is a certain degree of concordance between the results in Table 5.1 and those in Table 5.2. For example, the 2nd, 4th, 6th, 8th, 10th and 11th change points in Table 5.2 are very close to first 6 change points in Table 5.1. However, the latter method does not declare any change points after 2009, which is surprising given the turmoil in world financial markets induced by the sovereign debt crisis in Europe (2011-2012) and the significant market correction in January 2016 due to a crash in oil prices and concerns about China’s economy that resulted in a 23% decline in the major stock indices in China.

| 10/2/2001 | 10/2/2001 | 10/1/2002 | 3/4/2003 | 7/15/2003 | 10/11/2005 |

| 2/13/2007 | 7/10/2007 | 2/19/2008 | 9/23/2008 | 1/27/2009 | 8/18/2009 |

References

- Bai [2010] J. Bai. Common breaks in means and variances for panel data. Journal of Econometrics, 157(1):78–92, 2010.

- Baltagi et al. [2016] B. H. Baltagi, Q. Feng, and C. Kao. Estimation of heterogeneous panels with structural breaks. Journal of Econometrics, 191(1):176–195, 2016.

- Bardwell et al. [2018] L. Bardwell, P. Fearnhead, I. A. Eckley, S. Smith, and M. Spott. Most recent changepoint detection in panel data. Technometrics, (just-accepted):1–28, 2018.

- Barigozzi et al. [2018] M. Barigozzi, H. Cho, and P. Fryzlewicz. Simultaneous multiple change-point and factor analysis for high-dimensional time series. Journal of Econometrics, (206):187–225, 2018.

- Basseville and Nikiforov [1993] M. Basseville and I. V. Nikiforov. Detection of Abrupt Changes: Theory and Application. Prentice-Hall, Inc., Upper Saddle River, NJ, USA, 1993. ISBN 0-13-126780-9.

- Bhattacharjee and Bose [2014] M. Bhattacharjee and A. Bose. Estimation of autocovariance matrices for infinite dimensional vector linear process. J. Time Series Anal., 35(3):262–281, 2014.

- Bhattacharjee and Bose [2016] M. Bhattacharjee and A. Bose. Large sample behaviour of high dimensional autocovariance matrices. The Annals of Statistics, 44(2):598–628, 2016.

- Bhattacharjee et al. [2017] M. Bhattacharjee, M. Banerjee, and G. Michailidis. Common change point estimation in panel data from the least squares and maximum likelihood viewpoints. arXiv preprint arXiv:1708.05836, 2017.

- Bhattacharya [1994] P. Bhattacharya. Some aspects of change-point analysis. Lecture Notes-Monograph Series, pages 28–56, 1994.

- Billio et al. [2012] M. Billio, M. Getmansky, A. W. Lo, and L. Pelizzon. Econometric measures of connectedness and systemic risk in the finance and insurance sectors. Journal of financial economics, 104(3):535–559, 2012.

- Brockwell and Davis [2009] P. J. Brockwell and R. A. Davis. Time series: theory and methods. Springer, 2009.

- Chen and Gupta [2011] J. Chen and A. K. Gupta. Parametric statistical change point analysis: with applications to genetics, medicine, and finance. Springer Science & Business Media, 2011.

- Chen and Wu [2018] L. Chen and W. B. Wu. Testing for trends in high-dimensional time series. Journal of the American Statistical Association, (just-accepted):1–37, 2018.

- Cho [2016] H. Cho. Change-point detection in panel data via double cusum statistic. Electronic Journal of Statistics, 10(2):2000–2038, 2016.

- Cho and Fryzlewicz [2015] H. Cho and P. Fryzlewicz. Multiple-change-point detection for high dimensional time series via sparsified binary segmentation. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 77(2):475–507, 2015.

- Csörgö and Horváth [1997] M. Csörgö and L. Horváth. Limit theorems in change-point analysis. John Wiley & Sons Inc, 1997.

- Frisén [2008] M. Frisén. Financial surveillance, volume 71. John Wiley & Sons, 2008.

- Horváth and Hušková [2012] L. Horváth and M. Hušková. Change-point detection in panel data. Journal of Time Series Analysis, 33(4):631–648, 2012.

- Hsu et al. [2012] D. Hsu, S. Kakade, and T. Zhang. A tail inequality for quadratic forms of subgaussian random vectors. Electronic Communications in Probability, 17, 2012.

- Kim [2014] D. Kim. Common breaks in time trends for large panel data with a factor structure. The Econometrics Journal, 17(3):301–337, 2014.

- Koepcke et al. [2016] L. Koepcke, G. Ashida, and J. Kretzberg. Single and multiple change point detection in spike trains: Comparison of different cusum methods. Frontiers in systems neuroscience, 10, 2016.

- Kosorok [2008] M. R. Kosorok. Introduction to Empirical Processes and Semiparametric Inference. Springer, 2008.

- Li et al. [2016] D. Li, J. Qian, and L. Su. Panel data models with interactive fixed effects and multiple structural breaks. Journal of the American Statistical Association, 111(516):1804–1819, 2016. doi: 10.1080/01621459.2015.1119696.

- Liangjun and Qian [2015] S. Liangjun and J. Qian. Shrinkage Estimation of Common Breaks in Panel Data Models via Adaptive Group Fused Lasso. Working Papers 07-2015, Singapore Management University, School of Economics, Sept. 2015. URL https://ideas.repec.org/p/siu/wpaper/07-2015.html.

- Liu et al. [2015] H. Liu, A. Aue, and D. Paul. On the marčenko–pastur law for linear time series. The Annals of Statistics, 43(2):675–712, 2015.

- Peštová and Pešta [2017] B. Peštová and M. Pešta. Change point estimation in panel data without boundary issue. Risks, 5(1):7, 2017.

- Qiu [2013] P. Qiu. Introduction to statistical process control. CRC Press, 2013.

- Safikhani and Shojaie [2017] A. Safikhani and A. Shojaie. Joint structural break detection and parameter estimation in high-dimensional non-stationary var models. arXiv preprint arXiv:1711.07357, 2017.

- van der Vaart and Wellner [1996] A. W. van der Vaart and J. A. Wellner. Weak convergence and empirical processes: with applications to statistics. Springer, 1996.

- Wang et al. [2017] L. Wang, A. Aue, and D. Paul. Spectral analysis of sample autocovariance matrices of a class of linear time series in moderately high dimensions. Bernoulli, 23(4A):2181–2209, 2017.

- Westerlund [2018] J. Westerlund. Common breaks in means for cross-correlated fixed-t panel data. Journal of Time Series Analysis, 2018.

6 Appendix: Additional technical details

6.1 Some consequences of Theorems 2.1 and 2.2

In this section, we provide some immediate consequences of Theorems 2.1 and 2.2 in special cases such as independence across time and/or component-wise.

6.1.1 Independence across panels and dependence across time

Consider the model in (1.2) with independence across and

| (6.1) |

Then holds under (SNR*) . Note that SNR* is weaker than (SNR). (a) Moreover, if (SNR*) holds and , then . Note that in Model (6.1), population autocovariance of order is

Thus the quadratic form

Hence, becomes

In Model (6.1), is asymptotic variance-covariance matrix of a finite dimensional distribution of the limiting Gaussian process when . Therefore the following statement is true (b) Suppose (SNR*) and (A3) hold, , exists and is positive definite for all and . Then the conclusion of Theorem 2.2(b) holds with replaced by .

Recall the partition of into and from (2.3). In Regime , as discussed after (2.3), we need to treat and separately. Clearly, is a finite set. Moreover, in Model (6.1), . As are independent across both and , are also independent across and converge weakly if (A4), (A5) given before Theorem 2.2 and (A8*) stated below hold. (A8*) , and . , . As we have independence across components, and are independent. In this case, , and reduces to

Limit of the random part involving is a Gaussian process on with covariances . Existence of this limits and non-degeneracy of the Gaussian process are guaranteed by (A6*) and (A7*) stated below. (A6*) , exists for all . (A7*) is positive definite for all and . (A9*) is the analogue of (A9) and is required to establish asymptotic normality of the random part involving . (A9*) . Now the following statement is true. (c) Suppose (SNR*) and (A4), (A5), (A6*)-(A9*) hold and , then

where for each and ,

Remark 6.1.

Assumption (A8*) is weaker than (A8). If further holds in Model (6.1), then (A8) satisfies, and are Gaussian. This implies are independent across and for all , .

6.1.2 Independence across panels and time

Consider the model in (1.2) with independence across and

That is

| (6.2) |

Further suppose there is such that . Then . Recall SNR* in Section 6.1.1. Then holds under SNR*. (a) Moreover, if SNR* holds and , then . Now consider regime . In this case, population autocovariance

The quadratic form becomes

Define

Thus for all and the following statement is true. (b) If (SNR*) holds, , exists, then

where is the standard Brownian motion.

Now consider the regime . Recall that and Assumptions (A4), (A5) and (A9*). Note that Model (6.2) is a special case of Model (6.1). Thus reason of considering these assumptions are same as discussed in Section 6.1.1. As are independent across both and , (A8*) in Section 6.1.1 reduces to (A8**) stated below. (A8**) , for all and . , . Define,

Thus for Model (6.1), , for all and . Hence (A7*) holds automatically and (A6*) reduces to (A6**) as stated below. (A6**) and exists. Thus the following statement is true. (c) Suppose (SNR*) and (A4), (A5), (A6**), (A8**) and (A9*) hold and , then

where and

6.2 Other examples

Example 6.1.

Diagonally dominant coefficient matrices. A symmetric matrix is said to be diagonally dominant if . If the coefficient matrices are sparse, diagonally dominance can often be a reasonable assumption. In this case, for all , the covariances between and are much smaller for compared to . Suppose are all symmetric and diagonally dominant matrices. We know that . Now . Thus, and are of the same order. Suppose (a)-(d) in Proposition 2.3 holds. For such choices of coefficient matrices, (A1) and (A6) are satisfied if (k) and (l), stated after Propositions 2.3 and 2.4, are satisfied respectively. For this example, no other simplification is possible for (SNR), (A2), (A7) and for the first condition of (A8).

Example 6.2.

VAR process: A Vector Autoregressive process of order (VAR) is given by

where the nested matrices are the model parameter matrices and are as described after (1.2). Moreover, if for some ,

| (6.3) |

then (6.2) can be represented as (1.2) with , . Further, suppose . Then, one can easily show that for some and . This implies . Also, as , is bounded away from . Hence, for Theorems 2.1 and 2.2, we need (SNR*) , instead of (SNR). Also, (A1) and (A6) hold if (k) and (l1), stated after Propositions 2.3 and 2.4, are satisfied respectively. Again, suppose the smallest eigenvalues of , , are bounded away from with respect to both and . This implies that the smallest eigenvalue of is bounded away from and (A2), (A7) and the first condition of (A8) hold.

Example 6.3.

Coefficient matrices dominated by separable cross-sectional and time dependence structure. One may think that the structures in Examples 2.3 and 2.4 are restrictive. In this example, we consider a significantly wider class of coefficient matrices which are dominated by separable cross-sectional and time dependence structure. In other words, where be the -th element of . Define a sequence of nested matrices such that . Then (a) and (d) in Example 2.3 hold. Also suppose that for at least one . This implies that is bounded away from . Therefore, in Propositions 2.3 and 2.4, we need to replace and by and , respectively. Consequently, (A1) and (A6) hold if (b)-(j) in Propositions 2.3 and 2.4 are satisfied after replacing and by and , respectively. Finally, (A2) and (A7) are satisfied if the smallest singular value of is bounded away from and for atleast one .

7 Supplementary material: Proofs

7.1 Useful lemmas

Following two lemmas quoted from van der Vaart and Wellner [1996] are needed to prove Theorems 2.1 and 2.2.

Lemma 7.1.

For each , let and be stochastic processes indexed by a set . Let and be a map (possibly random) from to . Suppose that for every large and

| (7.1) | |||

| (7.2) |

for some and for function such that is decreasing in on for some . Let satisfy

| (7.3) |

Further, suppose that the sequence takes its values in and satisfies for large enough . Then, .

Lemma 7.2.

Let and be two stochastic processes indexed by a metric space , such that in for every compact set i.e.,

| (7.4) |

Suppose that almost all sample paths are upper semi-continuous and possess a unique maximum at a (random) point , which as a random map in is tight. If the sequence is uniformly tight and satisfies , then in .

Following lemma is useful to proof Theorem 3.1. Define,

Lemma 7.3.

Suppose SNR-ADAP, (C1), (C2) and (C3) hold. Then the following statements are true.

(a) for all , and for some .

(b)

(c)

(d)

(e)

(f) when .

(g) for all and

(h) for all , and .

Proof.

(a) It is easy to see that

where .

Hence, by independence of and (C1), (C2), for all ,

Similar arguments hold for . This completes the proof of Lemma 7.3(a). (b) With out loss of generality, assume . Note that

Now By Theorem 2.1, Assumption (C1)-(C3) and Theorem of Hsu et al. [2012], we have

This completes the proof of Lemma 7.3(b) for . Similar arguments also work for . Proof of Lemma 7.3(c)-(f) is similar to the proof of Lemma 7.3(b). Hence we omit it. (g) Note that

This completes the proof of Lemma 7.3(g). Proof of Lemma 7.3(h) is similar to the proof of Lemma 7.3(g). This completes the proof of Lemma 7.3. ∎

7.2 Proof of Theorem 2.1

Recall that

| (7.5) | |||||

Here we prove . To prove Theorem 2.1, we need Lemma 7.1 quoted from van der Vaart and Wellner [1996]. For our purpose, we make use of the above lemma with , , , , , , , . Thus, to prove Theorem 2.1, it is enough to establish that for some ,

| (7.6) | |||

| (7.7) |

Note that the left hand side of (7.7) is dominated by

| (7.8) |

By Doob’s martingale inequality, (7.8) is further dominated by

| (7.9) |

Thus, to prove Theorem 2.1, it is enough to show that for some ,

| (7.10) |

Hence, it is enough to prove (7.6) and (7.10) to establish Theorem 2.1. We shall prove these for . Similar arguments work when .

Let , say. We write for .

| (7.11) | |||||

First we calculate expectation and variance of . Let . Now,

| (7.12) | |||||

Note that

Next,

Also,

Thus

| (7.13) |

Now we compute variance of .

Note that,

Let . Therefore,

Hence,

Finally,

Similarly,

Therefore,

| (7.14) |

Next consider . For ,

Let,

Thus

| (7.15) | |||||

Now,

| (7.16) | |||||

Similarly,

| (7.17) |

Also, , . Thus,

| (7.18) |

Now, using similar calculations as in , we have

Moreover, and

Similarly, .

Thus

| (7.19) | |||||

Next, for , we have

Thus

Note that

Therefore,

Now, using similar calculations as in , we have

Thus

| (7.20) |

Moreover, using similarly calculations as in ,

| (7.21) |

Remark 7.1.

It is easy to observe from the proof of Theorem 2.1 that serves as an upper bound of or of similar quantities. Now under cross-sectional independence i.e. when , then is turned out to be an smaller upper bound and can be replaced by throughout the proof. As a consequence the conclusion of Theorem 2.1 continues to hold under weaker (SNR′) compared to SNR.

7.3 Proof of Theorem 2.2

Proof of (a). Note that since and by Theorem 2.1, . For Theorem 2.2(b) and (c), we use Lemma 7.2. To employ Lemma 7.2, we consider where and . We shall find weak limit of when or . We assume . Similar arguments work when .

From the previous calculations, it is easy to see that

where

Thus taking , where or , we have

for some compact set . Proof of (b). To prove Theorem 2.2(b), by Lemma 7.2, it is enough to establish

as , and for all compact subsets of .

It is easy to see that

as , and for all compact subsets of .

Now note that

Therefore, by (A3) and Lyapunov’s Central Limit Theorem,

| (7.22) |

where for all and ,

This completes the proof of Theorem 2.2(b). Proof of (c). It is easy to see that

Note that

Moreover, by (A4)-(A8),

Also by (A6), (A7) and (A9)

This completes the proof of Theorem 2.2(c). Hence, Theorem 2.2 is proved.

7.4 Proof of Propositions 2.3 and 2.4

Here we prove only Proposition 2.4. Similar proof works for Proposition 2.3. (I) Note that

Thus

This completes the proof of Proposition 2.4(I). Proof of Proposition 2.4(II) follows from similar arguments in the proof of Proposition 2.4(I). (III) It is easy to see that

Hence, by (a) and (c), we have

This proves Proposition 2.4(III). This completes the proof of Proposition 2.4.

7.5 Proof of Theorem 3.1

Without loss of generality, assume . Note that

Let and . Therefore,

Hence by Lemma 7.1 and similar arguments at the beginning of Section 7.2, we have

Now by Lemma 7.3(c),

This implies Theorem 3.1(a). Now,

Note that are Gaussian. Hence Theorem 3.1(b) follows from Lemma 7.2 and Lemma 7.3(a)-(d) and (g). A similar argument as in the proof of Theorem 2.2(c) and similar approximations as in the proof of Theorem 3.1(b) also work for Theorem 3.1(c) and hence we omit them. Hence, Theorem 3.1 is established.