Copula estimation for nonsynchronous financial data

Abstract.

Copula is a powerful tool to model multivariate data. We propose the modelling of intraday financial returns of multiple assets through copula. The problem originates due to the asynchronous nature of intraday financial data. We propose a consistent estimator of the correlation coefficient in case of Elliptical copula and show that the plug-in copula estimator is uniformly convergent. For non-elliptical copulas, we capture the dependence through Kendall’s Tau. We demonstrate underestimation of the copula parameter and use a quadratic model to propose an improved estimator. In simulations, the proposed estimator reduces the bias significantly for a general class of copulas. We apply the proposed methods to real data of several stock prices.

Keywords: Copula, Correlation, Kendall’s Tau, Asynchronicity, Dependence structure.

1. Introduction

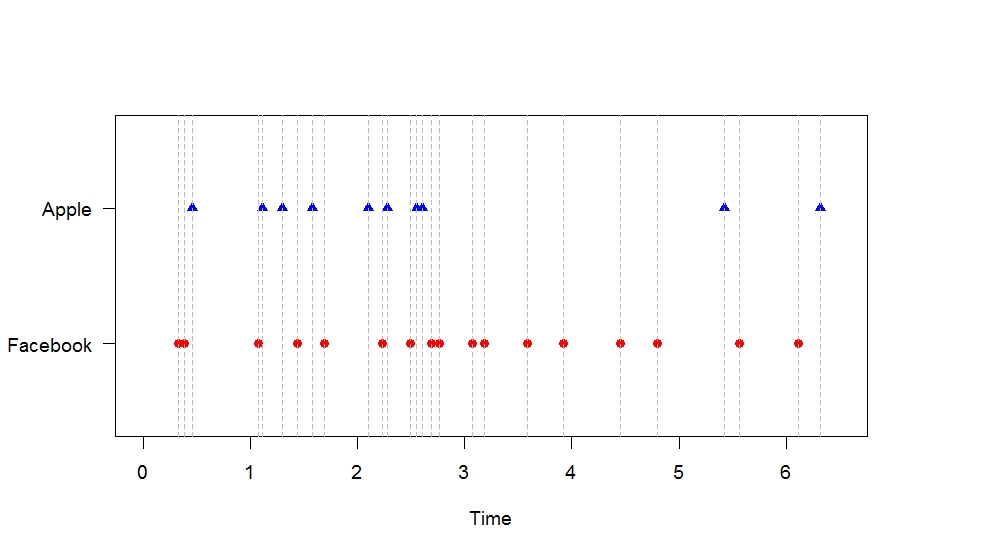

A very rich collection of market risk models have been developed and thoroughly investigated for intraday financial data. Although univariate modeling is important for addressing certain kinds of problems, it is not enough to unveil the nature and dynamics of the financial market. Interactions between different financial instruments are left out of univariate studies. If the companies belong to related business sectors or are owed by the same business house then such interactions can arise. High dependence between several constituent stocks of a portfolio can increase the probability of a large loss. So accurate estimation of the dependence between assets is of paramount importance. Correlation dynamics models, therefore, have become an important aspect of the theory and practice in finance. Correlation trading, which is a trading activity to exploit the changes in dependence structure of financial assets, and correlation risk that capture the exposure to losses due to changes in correlation, have attracted the attention of many practitioners, see Krishnan et al. (2009). Accurate modelling of dependence is also important in a range of practical scenarios. For example, basket options are widely used although their accurate pricing is challenging. The primary reason is that they are cheaper to use for portfolio insurance. The cost-saving relies on the dependence structure between the assets, see Salmon et al. (2006). In the actuarial world, as shown in Embrechts et al. (2002), some Monte Carlo-based approach to joint modelling of risks, like Dynamic Financial Analysis, depends heavily on the dependence structure. Frey and McNeil (2002) and Breymann et al. (2003) showed that the choice of model and correlation have a significant impact on the tail of the loss distribution and measures of extreme risks. It follows from the above discussion that we need accurate multivariate modeling and analysis. In order to perform multivariate analysis, we need multivariate data. This means that we need to have data for all variables on (sufficiently large) time points. For example, in case of daily financial data we would expect to observe the price of all stocks on a particular day. This kind of data is called synchronously observed data. On the other hand, if we don’t have observations for one or several variables (or stocks) on a particular time point then we call it nonsynchronous /asynchronous data. An example of such data is intraday stock price data. Within a particular day we can not expect to observe transactions in all stocks simultaneously. In Figure 1, we have shown the transaction/arrival times of two stocks within a small time interval.

The effect of asynchronicity can be quite serious on the estimation of model parameters. One of such phenomenon, reported by Epps (1979), is called Epps effect. Empirical results reported in that paper showed that the realized covariance between stock returns decreases as sampling frequency increases. Later the same phenomenon has been reported in several other studies on different stock markets, see Zebedee and Kasch-Haroutounian (2009) and foreign exchange market, see Muthuswamy et al. (2001). It is also empirically shown , see Renò (2003), that taking into account only the synchronous, or nearly synchronous, alleviates this underestimation problem.

Several studies have been devoted to the estimation of the covariance from intraday data. Mancino and Sanfelici (2011) analysed the performance of the Fourier estimator originally proposed by Malliavin et al. (2009). Peluso et al. (2014) adopted a Bayesian Dynamic Linear model and treated asynchronous trading as missing observations in an otherwise synchronous series. Corsi and Audrino (2012) proposed two covariance estimators, adapted to the case of rounding in the price time stamps, which can be seen as a general way of computing the Hayashi-Yoshida estimator (see Hayashi et al. (2005)) at a lower frequency. Zhang (2011) proposed a method called two-scale realized covariance estimator (TSCV) which combines two-scale sub-sampling and previous tick method that can simultaneously remove the bias due to microstructure noise and asynchronicity. Fan et al. (2012) studies TSCV under high-dimensional setting. Aït-Sahalia et al. (2010) proposed quasi–maximum likelihood estimator of the quadratic covariance.

The correlation coefficient only captures the linear dependence. In this work, we aspire to focus on estimation of non-linear dependence structure through copula. Apart from modelling the complete dependence structure, one of many other advantages of copula is the flexibility it offers to model the complex relationship between variables in a rather simple manner. It allows us to model the marginal distributions as necessary and takes care of the dependence structure separately. It is also one of the most important tools to model tail dependence, which is the probability of extremely large or small return on one asset given that the other asset yielded an extremely large or small return, see Xu (2008). For this reason, copula is also a useful tool for modelling the joint distribution of default times. Therefore it is important for pricing Credit Spread Basket, Credit Debt Obligation, First to Default, -to Default and other Credit derivative baskets, see Malgrat (2013). They also shows how copula helps to correlate the systematic risk to idiosyncratic risk. Zhang and Zhu (2016) developed a class of copula structured multivariate maxima and moving maxima processes which is a flexible and statistically workable model to characterize joint extremes.

In this paper, we will elaborately discuss the impact of asynchronicity on several measures of association in a general class of copulas. We explain why there is a serious underestimation of the measures of association unless treated carefully. We propose an alternative method for the estimation of correlation. Moreover we prescribed methods for accurate estimation of the associated copula. It is also shown that the estimation of some commonly used measures of associations, like Kendall’s tau, is challenging unless the underlying copula is determined. The rest of the paper is organized as follows. In section 2 we deal with the elliptical copula parameter estimation for nonsynchronous data and prove the main theorems. Section 3 deals with a more general class of copulas. In section 4 and 5 the results of simulation and real data analysis are shown. We present the conclusions in section 6. All the proofs are given in appendix A.

2. Estimation of Elliptical Copula

Suppose there are two stocks and their log-prices at time are denoted by and . By and we denote the corresponding log-returns. Although in the ideal world of the Black-Scholes model, the log returns are assumed to follow a Gaussian distribution, the stylized facts about financial market suggest that a distribution with a heavier tail needs to be considered. In the multivariate scenario, the search for such a model is challenging. In such situations copula appears to be a central tool at our disposal.

In Section 4, the results of a simulation study are reported where the effect of asynchronicity on the estimation of the correlation coefficient has been shown. The simulation results display severe underestimation. Before attempting to understand the problem and propose a remedy, we will present an algorithm to synchronize the data to make it suitable for standard multivariate analysis. We should note that some studies (see Hayashi et al. (2005), Buccheri et al. (2020)) attempt to calculate integrated covariance without synchronizing the data.

2.1. Pairing Method

The prices of the stocks are observed at random times when transactions take place. As a transaction in one stock wouldn’t influence the transaction time in the other, it is reasonable to assume that the observation times of the two stocks are independent Point processes. Therefore, if we have log prices of the first stock along with its time of occurrence as and that of the second stock as , then s and s are independent. Here and are the number of observations of first and second stock respectively, available on a particular day.

Before fitting a copula model, the observations of two stock prices need to be paired such that they can be treated as synchronously observed. The conventional synchronizing methods require a set (or sample) of time points at which we would like to observe a synchronized pair. For each stock, the tick information observed just previous to each such sampled time point is chosen to construct the synchronized pair (), yielding such pairs.

It is evident from the above discussion that the number of synchronized pairs is less than both and , unless we allow repetition. This means many observations in each stock will be removed and not to be used for further analysis. Generalized sampling times are defined as the following.

Definition 1.

Suppose we have stocks. is the -th arrival time of the -th asset. Then : , are called generalized sampling times Ait-Sahalia et al. (2005) if

a) .

b) for some .

c) in probability, where .

If , then it is called Previous tick sampling. In the above-mentioned method, an observation is uprooted from its original time point and assigned to a sampled time point , for some . In contrast, we want to retain the actual times of the prices that are chosen to be paired. In other words, instead of having a pair like , we want to have a pair where are the times at which the -th pair of stock-prices were observed. To emphasise this, we call the algorithm as the ‘pairing method’ (in contrast to ‘synchronizing method’). The pairing method, to be followed throughout in this paper, is described through the following algorithm ():

Algorithm (): 1. Take and 2. While and : • If then find . The th pair will be . Modify . • If then find . The th pair will be . Modify • Modify . and .

The pairs created by this algorithm are identical to the pairs created by ”refresh time sampling” (see Barndorff-Nielsen et al. (2011)) but accommodates more information by retaining the transaction times. Instead of writing we shall henceforth write .

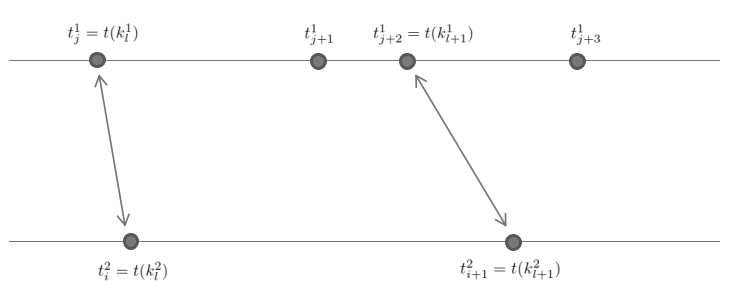

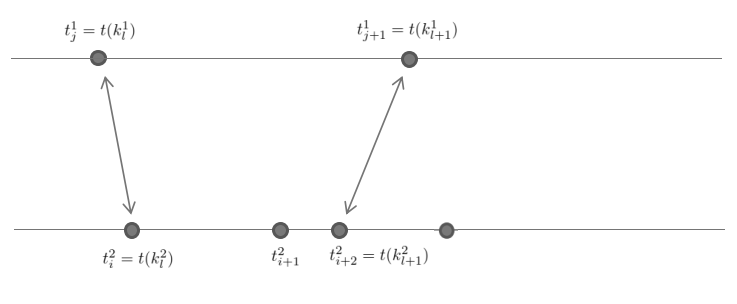

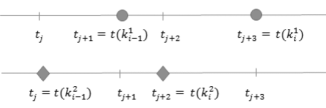

In Figure 2 and 3, and are paired together as (). The figures illustrate how the next pair is going to be chosen using the algorithm. In figure 2, . So and is chosen to be the largest of the arrival times in the first stock that are less than . In figure 3, . So and is chosen to be the largest of the arrival times in the first stock that are less than . The pairs are represented by the arrows.

2.2. Estimation of Correlation coefficient

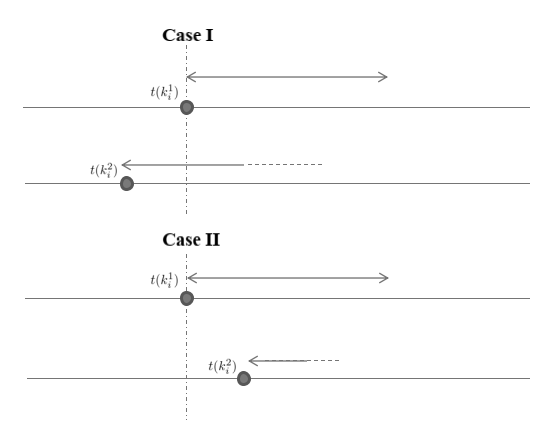

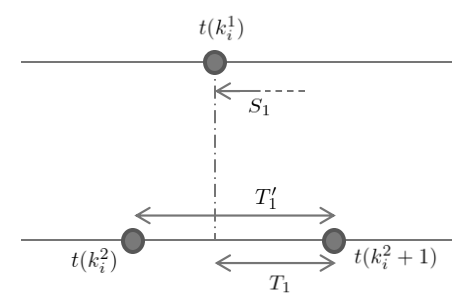

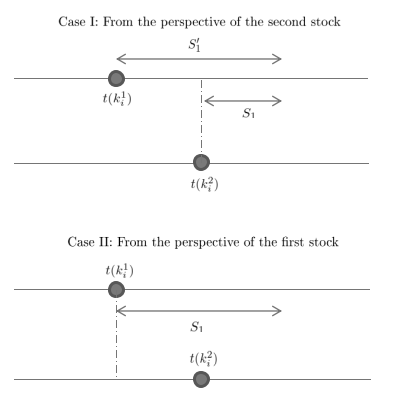

Once we have paired observations, we can proceed to calculate the correlation coefficient. We denote as a bivariate rv with mean , variances and correlation . is independent of the arrival processes. Since the log returns and are calculated over two nonidentical time-intervals, namely and , the correlation between the returns is heavily dependent on the length of overlapping and non-overlapping portions of these two time-intervals. To see this, first suppose for some and . Here is the set of combined (ordered) time points at which a transaction (in any of the stocks) is noted. Then one of these four configurations is true:

| (1) |

See Figure 4 and 5 for illustrations of the first two configurations where two consecutive pairs of log-prices are and with their corresponding transaction times , .

We define a random variable , denoting the overlapping time interval of th interarrivals corresponding to and

First consider Figure 4. Define with , where , are the number of observations in the two stocks. The conditional expectation:

These examples lead us to our first theorem.

We consider the following assumptions ():

: The log return process follows independent and stationary increment property

: The observation times (arrival process) of two stocks are independent Renewal processes and as

: Estimation is based on paired data obtained by algorithm

Theorem 1.

Under the assumptions defined below is a consistent estimator of the true correlation coefficient

where for and being the sample mean and sample correlation coefficient based on the pairs.

Moreover,

where and and

According to this theorem in order to get a consistent estimator, we need to multiply the usual sample correlation coefficient, based on the paired observations (by algorithm ), by a correction factor. The correction factor is a function of only and for i.e. it is only dependent on the arrival process and not on the copula.

2.3. Nonlinear dependence and Elliptical copula

So far we were dealing with linear dependence through the correlation coefficient. In this section we will deal with nonlinear dependence through copula. We will restrict our attention to elliptical copula. The Gaussian copula is the most widely used elliptical copula which mimics the dependence structure of a multivariate Gaussian distribution. But it does not capture the nonlinear dependence. It is well-known that a Gaussian copula with correlation coefficient zero reduces to independent copula. But this is not true in general. For example in case of another common elliptical copula, namely the t copula, the parameter captures the linear dependence but the form of the copula function accommodates for nonlinear dependence. We will now discuss the effect of asynchronicity on copula estimation.

By Sklar’s theorem (see Nelsen (2007)), the distribution function of the log returns and can be expressed as , where is the unique copula associated with . Asynchronicity not only affects the estimation of , but also the estimation of the copula function because and are assumed to be observed synchronously. The convergence of ,

where and are empirical distribution functions of and , needs more than the convergence of . The next theorem tries to address this concern. Before stating the theorem we will make an additional assumption which ensures that the probability of both the missing value of return at and observed value of return at lying in an interval of length is in the order of for . Define, and for .

for where

with and being a positive real number.

Theorem 2.

If the true underlying copula is an elliptical copula then under , is uniformly convergent to the true copula, where and are the empirical distribution functions of the marginals of and computed from the paired data and is defined as in Theorem 1.

2.4. Expected loss of data and :

Recall that the correction factor in Theorem 1 is a function of the arrival process only. It is worthwhile to express in terms of the underlying parameters of the arrival processes. In the next theorem, we will try to do so. But the implication of the theorem goes beyond this purpose. Remember that all the synchronization methods we discussed have one problem. It results in loss of data, which is evident from Figure 2. The second observation of the first stock will not be included in any of the pairs and therefore will be wasted. So one can ask the question that what proportion of observations (of each stock) will be wasted by using our pairing method (). This can be answered if we can compare average interarrival length in a stock (for example for the first stock) and average interarrival length formed by the pairs ( for the first stock). One important point to note here is that even if the two initial point processes and are independent, the point processes after pairing the observations- and - are not independent. This is due to the fact that the pairing method () involves arrivals of both the stocks. Due to that fact, we will see in the next theorem both and involves , the parameters of the two point processes.

Theorem 3.

Suppose the two underlying point processes are Poisson processes with parameters and and for then,

-

(a)

-

(b)

-

(c)

where

and for i=1,2

As a consequence of this theorem we have-

| (2) |

3. Extension to general copula

In this section, we will deal with a more general class of copulas. As the argument in Section 2 is entirely based on the correlation coefficient it can not be directly extended to a larger class of copulas. This is precisely because for a general copula there is no direct relation between the Pearson’s correlation coefficient and the copula parameter.

We propose to use Kendall’s Tau to capture the copula dependence. The definition of Kendall’s tau is

where and are identical but independent copies of and . The relation between Kendall’s Tau and the copula is captured through the following equation.

| (3) |

If and be random variables with an Archimedean copula generated by in then

| (4) |

For the elliptical copulas a simplified form can be derived,

| (5) |

So we can study how Kendall’s tau is affected by asynchronicity. Thereupon we will gauge the impact on the copula parameter using the above mentioned relation.

3.1. Underestimation of Kendall’s tau

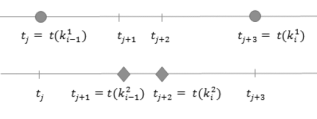

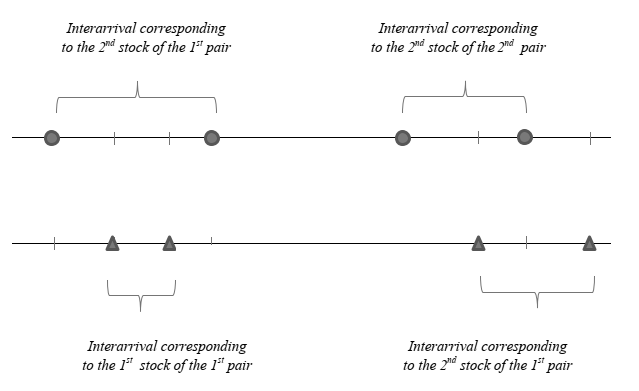

The problem with nonsynchronous data is that any two independent pairs of returns can not be taken as identical copies of each other. To see this, consider figure 6, where arrival times of the 1st stock are denoted by triangles and arrival times of the second stock are denoted by circles. After applying the pairing method, suppose the first circle and first triangle represent the location of the first pair of prices. Similarly, the second circle and the second triangle represent the next pair. From the figure, it is evident that these two pairs are forming an example of the second configuration (see eq. 1). Similarly, the 3rd and 4th pair constitutes an example of the 4th configuration. So the corresponding returns may not be considered as identically distributed. In this subsection, we will measure the Kendall’s tau using only the returns with same configuration. Figure 7 represents the arrival times of two pairs of the same configuration.

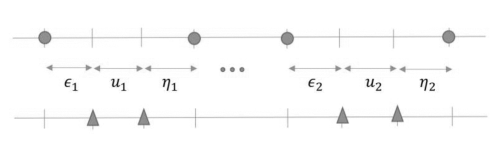

As illustrated in Figure 7, suppose we have two non-overlapping inter-arrivals and for the first stock and and for the second stock, with arrival times denoted by the triangles and circles respectively. The log returns corresponding to the inter-arrivals of the first stock are given by and . Similarly, the log returns corresponding to the intervals of the second stock are denoted by (due to independent increment property) and . In the following section, we will focus on the two specific configurations (eq. (1)).

Define,

and

where and are respectively overlapping and non-overlapping regions of the th pair of returns. In the above example, , , and . Note that for the first and fourth configurations, gives us true Kendall’s tau. We cannot calculate because and are not observed. Instead, we observe and . Therefore the observed Kendall’s Tau is . In this section, we will try to find out the relation between and .

In order to establish our result, we need some assumptions. Suppose and are positively associated random variables. Let and be two identical copies of . Then, given the information that , we would expect that is more likely to be positive than negative. Intuitively, positive association would also suggest that given the information , is more likely to be positive. This notion is not in general captured by any known measure of association. For each of the following we define and as two identical copies of , and .

Assumptions() stated below, try to capture the above idea:

: If

then for all ,

and

.

: If then for all ,

and

Before stating the main theorems, we will first state some Lemmas which will help us to prove the theorems.

Lemma 1.

.

Lemma 2.

This is a straightforward consequence of Lemma 1 and the independence of and .

Theorem 4.

Under the Assumption , for the pairs with 1st and 4th configuration,

where is the Kendall’s tau calculated on the paired data with 1st and 4th configurations, i.e. , where and are independent pairs of the same configurations.

Theorem 5.

For the pairs with 1st and 4th configuration,

where is the Kendall’s tau calculated on the paired data with 1st and 4th configurations, i.e. , where and are independent pairs of the same configurations.

3.2. Corrected Estimator

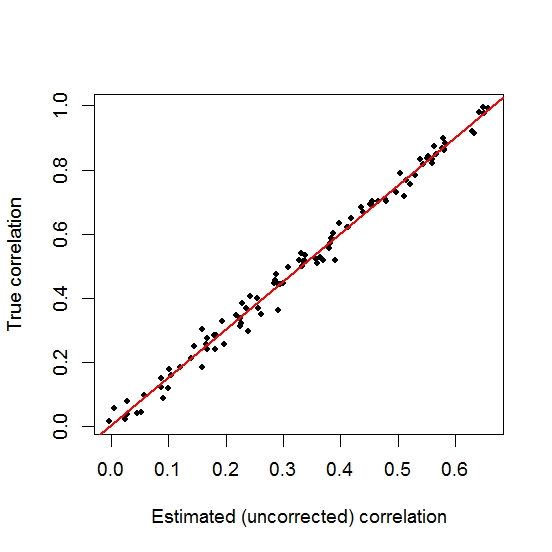

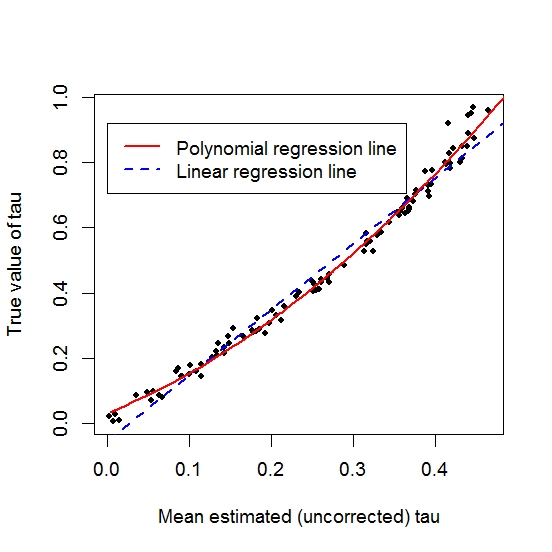

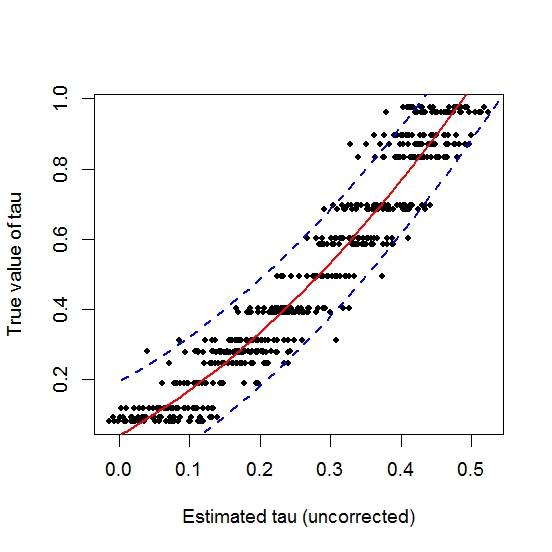

Similar to section 2, we would like to find a correction factor, that only depends on the arrival times, for a more general class of copula. For Elliptical copula, the value of the correction factor is not dependent on the value of the parameter. This is evident from Fig. 8 (left panel), showing the true and uncorrected mean estimated parameter of Gaussian copula for simulated nonsynchronous data. We generated the arrival times according to a pre-specified Poisson process. We can see that the true and estimated parameters lie along the regression line where the intercept term of the regression line is insignificant. This suggests that the corrected estimator should be a constant times the uncorrected one. This constant was the correction factor derived in Theorem 1.

On the other hand in the figure for Clayton copula (right panel, Fig. 8), we can see that a straight line would not be a good candidate to model the relation between the true and uncorrected estimated Kendall’s tau. This means we should not aspire to find a simple multiplicative correction factor that would give us the value of the true parameter. On inspection, a second degree polynomial seems to be a good model. Bu the same procedure, a second-degree polynomial seems to be appropriate for the Gumbel copula as well. We therefore, use a quadratic model to obtain the corrected estimator. The detailed steps are outlined below:

-

(1)

From the observed data, estimate the two arrival processes independently.

-

(2)

Estimate the univariate marginal distributions.

-

(3)

Using the pairing algorithm described in section 2.2, pair the observations.

-

(4)

With paired data, we can now see which copula fits best to the data. It can be obtained through AIC or BIC criterion.

-

(5)

Estimate the Kendall’s tau (uncorrected) from this paired data.

-

(6)

Prefix copula parameters (or equivalently Kendall’s tau). For each parameter, with the information of the underlying copula, arrival processes, and marginals, we now simulate nonsynchronous samples (the technique of generating nonsynchronous data is discussed in section 4).

-

(7)

For each sample, calculate uncorrected estimate and plot the estimates and the true Kendall’s tau in a plot like Fig. 10 (right panel).

-

(8)

Fit a suitable quadratic regression for such a plot.

-

(9)

From the regression equation, find the corrected Kendall’s tau corresponding to the estimated value of the Kendall’s tau (obtained from step 5).

Note that the above procedure yields an interval estimator for Kendall’s tau by considering the prediction interval in the regression. In section 4 we study the coverage probability of such intervals through simulations and compare them to other interval estimates.

4. Simulation

We simulated data of synchronized log-returns of two stocks for time points. The time points are generated by a Poisson Process. Corresponding returns are drawn randomly from a bivariate distribution determined by a pre-specified copula and margins. These pairs are then transformed appropriately to represent log-prices on the corresponding interarrivals. Now from the first stock, we randomly delete time points and their corresponding prices. The remaining data points constitute the data for the first stock. For the second stock, we keep the time points which were deleted from the first stock and delete rest of the time points. These time points, along with their corresponding log-prices, constitute data for the second stock. So now we have nonsynchronous data for the two stocks.

4.1. Estimation of copula parameter of Elliptical copulas

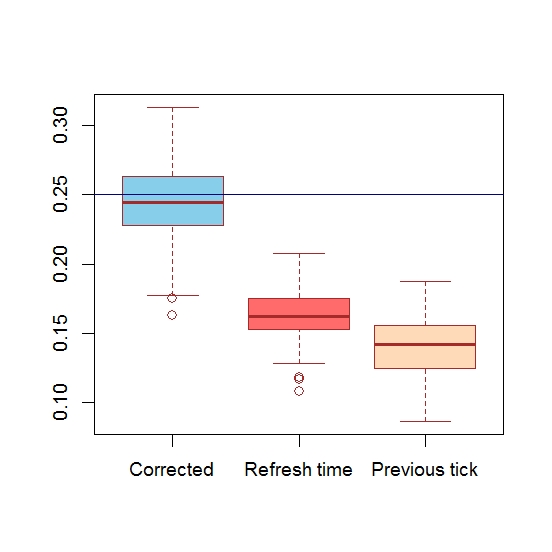

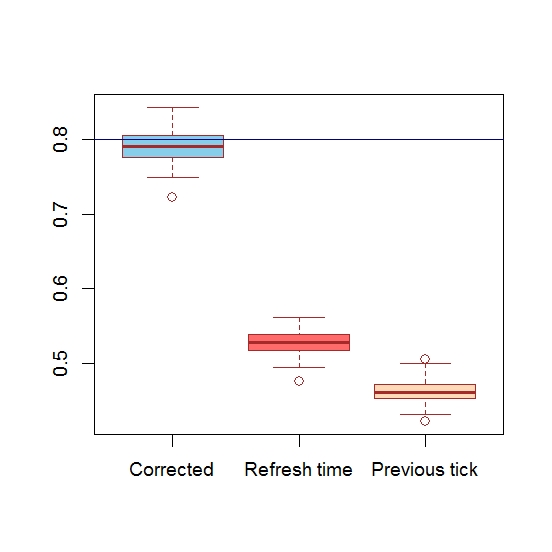

In the following simulation study, we test the performance of the method, prescribed in Theorem 1, to estimate the copula parameter. To do so, we first choose a Gaussian copula and generate 100 instances of nonsynchronous data by the method mentioned above. Initially, both and are taken to be the same. The mean, variance and Mean Square Error of the 100 estimates are reported in Table 1 and Table 2. In Figure 9, we show the boxplots for . The boxplot on the left corresponds to the corrected estimate and those on the middle and right corresponds to uncorrected estimates obtained from refresh time sampling and previous tick sampling respectively. The horizontal line suggests the true parameter.

| Estimate from | Estimates from | Corrected | ||

|---|---|---|---|---|

| previous tick sampling | refresh time sampling | estimate | ||

| -0.4 | 800 | -0.2316 | -0.2680 | -0.4022 |

| (0.049) | (0.046) | (0.069) | ||

| 0.1 | 800 | 0.061 | 0.069 | 0.1049 |

| (0.043) | (0.042) | (0.063) | ||

| 0.2 | 800 | 0.1205 | 0.1237 | 0.1853 |

| (0.049) | (0.045) | (0.067) | ||

| 0.8 | 800 | 0.4675 | 0.5255 | 0.7885 |

| (0.038) | (0.035) | (0.051) | ||

| -0.4 | 2000 | -0.2325 | -0.2682 | -0.4022 |

| (0.034) | (0.025) | (0.039) | ||

| 0.1 | 2000 | 0.056 | 0.065 | 0.098 |

| (0.033) | (0.026) | (0.039) | ||

| 0.2 | 2000 | 0.1115 | 0.1274 | 0.1911 |

| (0.027) | (0.031) | (0.046) | ||

| 0.8 | 2000 | 0.4613 | 0.5258 | 0.7888 |

| (0.028) | (0.019) | (0.029) | ||

| -0.4 | 5000 | -0.2289 | -0.2637 | -0.3956 |

| (0.018) | (0.017) | (0.026) | ||

| 0.1 | 5000 | -0.061 | 0.065 | 0.099 |

| (0.049) | (0.019) | (0.029) | ||

| 0.2 | 5000 | 0.1165 | 0.1357 | 0.2036 |

| (0.019) | (0.015) | (0.023) | ||

| 0.8 | 5000 | 0.4582 | 0.5224 | 0.7844 |

| (0.016) | (0.013) | (0.019) |

| MSE (previous tick) | MSE (refresh time) | MSE (corrected) | ||

|---|---|---|---|---|

| -0.4 | 800 | 0.0307 | 0.0195 | 0.0047 |

| 0.2 | 800 | 0.0087 | 0.0078 | 0.0047 |

| 0.8 | 800 | 0.112 | 0.0765 | 0.0027 |

| -0.4 | 2000 | 0.029 | 0.0179 | 0.0015 |

| 0.2 | 2000 | 0.0085 | 0.0062 | 0.0021 |

| 0.8 | 2000 | 0.1155 | 0.0755 | 0.0009 |

| -0.4 | 5000 | 0.0296 | 0.018 | 0.0006 |

| 0.2 | 5000 | 0.007 | 0.004 | 0.0003 |

| 0.8 | 5000 | 0.1117 | 0.077 | 0.0006 |

From the table, we see that both previous tick and refresh time sampling fail to capture the magnitude of true dependence. In fact the previous tick method is the worst choice for synchronization.

We carried out the same analysis with the copula, with different marginal distributions with different degrees of freedom, which is a more realistic scenario for intraday financial data. The result is similar i.e. not only does our prescribed correction give a good estimate but also the uncorrected method returns a biased estimate and the bias is significant. The result of 100 simulations with parameter -0.4 is summarized in Table 3.

| t copula (df 8) | mean | sd | mean | sd |

|---|---|---|---|---|

| marginals | uncorrected estimate | uncorrected estimate | corrected estimate | corrected estimate |

| (t(5), t(7)) | -0.2623 | 0.036 | -0.3932 | 0.054 |

| (N(0,2), N(0,4)) | -0.264 | 0.038 | -0.3961 | 0.055 |

| (t(4), N(0,3)) | -0.2532 | 0.039 | -0.3801 | 0.059 |

4.2. Interval estimation of Kendall’s Tau in non-Elliptical copula

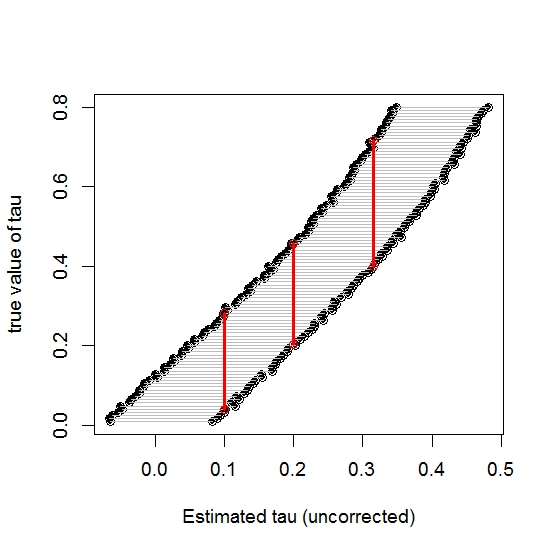

: We take three approaches to interval estimation of the true Kendall’s tau and applied those on simulated data from several Archimedean copulas. In the first approach, we follow the method described above and get the 95% prediction interval. The blue dotted lines in the right panel of Figure. 10 show the prediction intervals for Clayton copula.

The second approach is similar to the first one, but we don’t fit a regression line. Instead, for each true Kendall’s tau, we plot the interval that contains the (under)estimated Kendall’s tau 95% of times. In the left panel of Fig. 10, we plot the intervals (horizontal) against the true Kendall’s tau. Now we calculate the confidence interval for true Kendall’s tau as the vertical interval corresponding to the estimated Kendall’s tau (see the red vertical lines corresponding to 0.1, 0.2 and 0.32 in the figure).

In the third approach, we deliberately mis-specify the underlying copula as a Gaussian copula and use Theorem 1 to calculate the confidence interval (using the relation between correlation coefficient and Kendall’s tau for elliptical copula, see eq. 5). The results of these three approaches to interval estimation are given in Table 4 in section 4.

The coverage probability and interval lengths from the three methods of interval estimation, described in section 4.2, are shown in Table 4. An important takeaway from this table comes from the last column which demonstrates that the effect of model misspecification can be quite serious. Note that the second method, being completely non-parametric, does not assume anything about the shape of the dependence function between the true parameter and the uncorrected estimate. The first method assumes a quadratic model. This assumption reduces computations by a huge amount. From the table we see that the coverage probability of the first method is always at least the target value of 95%. So the assumption of a quadratic model does not compromise the coverage probability. The intervals are a little larger than the second method, so the first method is more conservative. Another observation is that the length of the intervals do not depend much on the value of the underlying parameter.

| Copula | True Kendall’s tau | 1st Method | 2nd Method | 3rd Method |

|---|---|---|---|---|

| (CP, IL) | (CP, IL) | (CP, IL) | ||

| Clayton | 0.1 | (.98,0.30) | (.95,0.19) | (.84,0.1) |

| Clayton | 0.2 | (.98,0.31) | (.96,0.24) | (.77,0.3) |

| Clayton | 0.3 | (.97,0.31) | (.97,0.25) | (.56,.29) |

| Clayton | 0.5 | (.95,0.31) | (.97,0.29) | (.29,.26) |

| Gumbel | 0.1 | (.98,0.30) | (.98,0.21) | (0.8,0.2) |

| Gumbel | 0.2 | (.99,0.31) | (.94,0.24) | (.72,0.3) |

| Gumbel | 0.3 | (.99,0.31) | (.95,0.25) | (.55,.29) |

| Gumbel | 0.5 | (.95,0.31) | (.93,0.27) | (.23,.26) |

5. Real data analysis

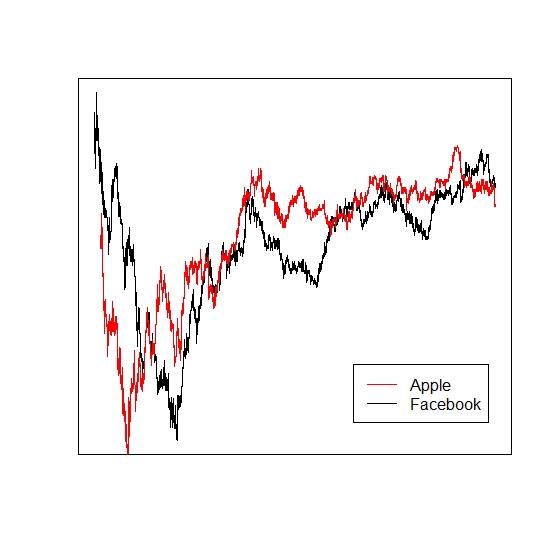

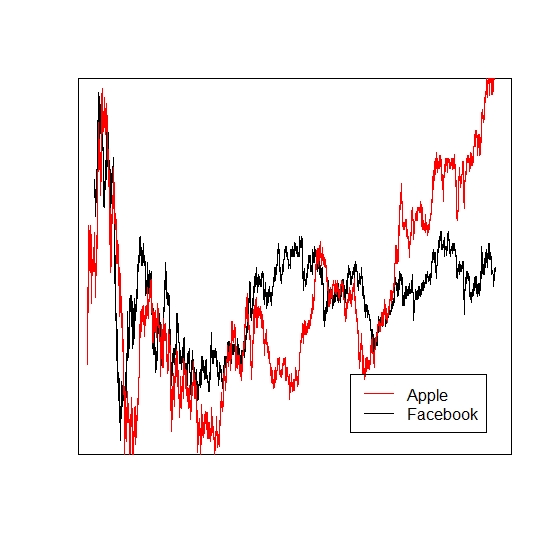

We analyze real financial intraday data to see which kind of copula is most likely to be encountered in practice. We use AIC to compare and select the best copula. In many of the cases, we find that the t-copula is a good choice to model bivariate intraday data. To see the impact of asynchronicity for real data we record the relative extent of correction to be undertaken. The intraday data for Apple and Facebook stocks are plotted in Figure 11. These have been modelled by bivariate copula for three consecutive days. For all three days both the uncorrected and the corrected estimates are evaluated in Table 5. The percentage change in values of uncorrected and corrected estimates is reported in the third column. We notice that almost 30 to 35% of data being lost or deleted after constructing the pairs by algorithm .

| uncorrected | corrected | percentage change | |

|---|---|---|---|

| biased estimate | unbiased estimate | () | |

| Day 1 | 0.098 | 0.141 | 43.87% |

| Day 2 | 0.129 | 0.186 | 44.18% |

| Day 3 | 0.111 | 0.159 | 43.24% |

We also perform the same analysis for a couple of other stocks and the results we obtained are very similar. For example, when we consider Amazon and Netflix on three nearly consecutive days, the percentage changes in copula parameter with copula are 41.75%, 39.84%, 42.76% respectively.

6. Conclusion and Future directions

Both simulations and real data analysis clearly show that the impact of asynchronicity can be very serious if not tackled properly. We discuss some of the methods to circumvent the problem. Careful pre-processing of intraday data is necessary to model or infer about the underlying realities. We propose a consistent estimator of the correlation coefficient and more generally of elliptical copula function. For a more general class of copulas, where there is a one-one relation between the Kendall’s tau and the copula, we suggest a way of estimating the copula parameter. Alongside the point estimates, three ways of interval estimation is discussed and compared. From the results it is evident that the impact of asynchronicity can be quite serious under model mis-specification. The real data analysis corroborates our findings. For the two chosen stocks, as the correlation is very less, the absolute change in the value after the correction is not much. But the relative change is significantly high, as we expected.

There are several directions in which one can extend this work. Firstly, we didn’t assume the presence of microstructure noise. In the presence of noisy observations, the estimator may demand further modifications. The estimation procedure can be further challenging if the parameter is time-dependent. As time-dependent copula modelling is gaining popularity in financial data analysis, it is worthwhile to investigate the effect of asynchronicity in time-varying parameter estimation. Another question one can look into is that how asynchronicity affect the estimation of popular risk measures like Value at Risk (VaR).

References

- (1)

- Aït-Sahalia et al. (2010) Aït-Sahalia, Y., Fan, J. and Xiu, D. (2010), ‘High-frequency covariance estimates with noisy and asynchronous financial data’, Journal of the American Statistical Association 105(492), 1504–1517.

- Ait-Sahalia et al. (2005) Ait-Sahalia, Y., Mykland, P. A. and Zhang, L. (2005), ‘How often to sample a continuous-time process in the presence of market microstructure noise’, The Review of Financial Studies 18(2), 351–416.

- Barndorff-Nielsen et al. (2011) Barndorff-Nielsen, O. E., Hansen, P. R., Lunde, A. and Shephard, N. (2011), ‘Multivariate realised kernels: consistent positive semi-definite estimators of the covariation of equity prices with noise and non-synchronous trading’, Journal of Econometrics 162(2), 149–169.

- Breymann et al. (2003) Breymann, W., Dias, A. and Embrechts, P. (2003), ‘Dependence structures for multivariate high-frequency data in finance’, Quantitative Finance 3(1), 1–14.

- Buccheri et al. (2020) Buccheri, G., Bormetti, G., Corsi, F. and Lillo, F. (2020), ‘A score-driven conditional correlation model for noisy and asynchronous data: An application to high-frequency covariance dynamics’, Journal of Business & Economic Statistics pp. 1–17.

- Corsi and Audrino (2012) Corsi, F. and Audrino, F. (2012), ‘Realized covariance tick-by-tick in presence of rounded time stamps and general microstructure effects’, Journal of Financial Econometrics 10(4), 591–616.

- Embrechts et al. (2002) Embrechts, P., McNeil, A. and Straumann, D. (2002), ‘Correlation and dependence in risk management: properties and pitfalls’, Risk management: value at risk and beyond 1, 176–223.

- Epps (1979) Epps, T. W. (1979), ‘Comovements in stock prices in the very short run’, Journal of the American Statistical Association 74(366a), 291–298.

- Fan et al. (2012) Fan, J., Li, Y. and Yu, K. (2012), ‘Vast volatility matrix estimation using high-frequency data for portfolio selection’, Journal of the American Statistical Association 107(497), 412–428.

- Frey and McNeil (2002) Frey, R. and McNeil, A. J. (2002), ‘Var and expected shortfall in portfolios of dependent credit risks: conceptual and practical insights’, Journal of banking & finance 26(7), 1317–1334.

- Hayashi et al. (2005) Hayashi, T., Yoshida, N. et al. (2005), ‘On covariance estimation of non-synchronously observed diffusion processes’, Bernoulli 11(2), 359–379.

- Krishnan et al. (2009) Krishnan, C., Petkova, R. and Ritchken, P. (2009), ‘Correlation risk’, Journal of Empirical Finance 16(3), 353–367.

- Malgrat (2013) Malgrat, M. (2013), Pricing of a “worst of” option using a Copula method, PhD thesis, KTH.

- Malliavin et al. (2009) Malliavin, P., Mancino, M. E. et al. (2009), ‘A fourier transform method for nonparametric estimation of multivariate volatility’, The Annals of Statistics 37(4), 1983–2010.

- Mancino and Sanfelici (2011) Mancino, M. E. and Sanfelici, S. (2011), ‘Estimating covariance via fourier method in the presence of asynchronous trading and microstructure noise’, Journal of Financial Econometrics 9(2), 367–408.

- Muthuswamy et al. (2001) Muthuswamy, J., Sarkar, S., Low, A. and Terry, E. (2001), ‘Time variation in the correlation structure of exchange rates: high-frequency analyses’, Journal of Futures Markets: Futures, Options, and Other Derivative Products 21(2), 127–144.

- Nelsen (2007) Nelsen, R. B. (2007), An introduction to copulas, Springer Science & Business Media.

- Peluso et al. (2014) Peluso, S., Corsi, F. and Mira, A. (2014), ‘A bayesian high-frequency estimator of the multivariate covariance of noisy and asynchronous returns’, Journal of Financial Econometrics 13(3), 665–697.

- Renò (2003) Renò, R. (2003), ‘A closer look at the epps effect’, International Journal of theoretical and applied finance 6(01), 87–102.

- Salmon et al. (2006) Salmon, M., Schleicher, C. et al. (2006), ‘Pricing multivariate currency options with copulas’, Copulas: From Theory to Application in Finance, Risk Books, London .

- Xu (2008) Xu, Q. (2008), Estimating and evaluating the Archimedean-copula-based models in financial risk management: a dissertation submitted in fulfillment of the requirements for the degree of Doctor of Philosophy in Financial Economics, Massey University, Auckland, New Zealand, PhD thesis, Massey University.

- Zebedee and Kasch-Haroutounian (2009) Zebedee, A. A. and Kasch-Haroutounian, M. (2009), ‘A closer look at co-movements among stock returns’, Journal of Economics and Business 61(4), 279–294.

- Zhang (2011) Zhang, L. (2011), ‘Estimating covariation: Epps effect and microstructure noise’, Journal of Econometrics 160(1), 33–47.

- Zhang and Zhu (2016) Zhang, Z. and Zhu, B. (2016), ‘Copula structured m4 processes with application to high-frequency financial data’, Journal of Econometrics 194(2), 231–241.

Appendix A Proofs

A.1. Proof of Theorem 1:

Proof.

The conditional expectation:

This is a consequence of the assumption (as illustrated in the examples in section 2.2).

Similarly,

Then we have, and

.

Therefore,

Note that the estimate is defined as

where .

Let us define the correction factor: .

Now,

and

and

Therefore, , where

As is sample correlation coefficient, we know that

By Slutsky’s theorem we get,

Using we then have,

Now we need to stabilize the variance.

Note that,

Define, Then,

Therefore a simple application of delta method implies that

This completes the proof. ∎

A.2. Proof of Theorem 2.

Proof.

Note that .

So

is a consistent estimator for the copula . But ’s

are unobserved, where ’s are actually observed.

Let us use the notation and

for the empirical distribution function of based on the observations

and

respectively. Therefore to claim that the estimated copula based

on the paired data (observed) is consistent, we have to show that-

a.s.

Suppose

. Note that by Assumption , .

Then,

This implies that

The second inequality is due to Chebyshev’s inequality and the last equality is due to . The third inequality is a consequence of asynchronicity as for each , there are at most two ’s (the preceding and the next) for which and are dependent.

Hence by Borel Cantelli Lemma, . Again as we have that, .

Now we have to show that uniform convergence will hold in this case. That is, we want to show . For any given we have a finite partition of the real line such that . This can be achieved

by taking and .

Then, . Because if

then by right continuity there exists a such that ,

hence contradicting the definition of . So between and

, jumps at least . This can happen at most

finite number of times, so . By our definition of ,

we have . Hence

.

If

then we have,

Now using properties of copula we can clearly see that

As both and are uniformly convergent to and respectively, the result follows. ∎

A.3. Proof of Theorem 3

Proof.

(a) If you fix the point then there can be two situations depending on the position of as illustrated in Figure 12.

Firstly consider case 1. We are interested in the overlapping interval. As illustrated in Figure 13, define as the first interarrival of the first stock after , as the first interarrival of the 2nd stock after and as the first interarrival of the 2nd stock after i.e. if we start observing the process only from then the first arrival time for the second stock. As the arrival processes are Poisson processes, distributions of and are same (due to memory-less property). Denote all the subsequent interarrivals as and .

Now (for case 1),

Therefore (for case 1),

Now, and .

Define

and .

So,

Note that and . Therefore,

where Thereffore,

Similarly,

Similarly we can derive for case 2 by interchanging the role of and . See Figure 14. Hence for case 2 we have,

Now two cases are equally likely, .

Therefore combining both the cases we have, .

(b) Now we have to calculate .

For case 1:

Define,

Then, , where

For case 2 the derivation is similar.

(c) Following similar derivation as part (b) ,

where is the mean of defined below,

A similar derivation will establish-

∎

A.4. Proof of Lemma 1

Proof.

As is independent of and symmetric around , clearly

So, . ∎

A.5. Proof of Theorem 4

Proof.

Due to symmetry of two configurations, it is enough to prove the theorem for one configuration. Let us consider the 4th configuration. Here , , and .

The Kendall’s tau for this nonsynchronous configuration, as defined in section 1, is:

According to our notation, and . So, and . Let us denote the region, where , by i.e. .

A.6. Proof of Theorem 5

Proof.

Due to symmetry of two configurations, it is enough to prove the theorem for one configuration. We consider the case of Figure 7 (4th configuration). Here , , and .

The Kendall’s tau for this nonsynchronous configuration, as defined in section 1, is:

According to our notation, and . So,

and

where is the true Kendall’s tau and .

Therefore,

| (6) |

Now we have to calculate the probability .

The 3rd step of the above derivation is justified because and are clearly independent. Also independence of and is self evident which results in step 4. Note that and will depend on and . Due to independent increment property, and are independent. Therefore .

Let us denote the events and . Note that as condition on the event does not influence the expected value of .

Inserting this to 6 we get

Hence we proved the result. ∎

Appendix B Positive and negative connection

Suppose and are positively associated. And and are two identical pairs. Then bigger the value of from , bigger the probability of would expected to be. This good expectation is formalized in the following definition.

Definition 2.

is said to be positively connected to if ,

is said to be negatively connected to if , the signs of the above inequalities are reversed.

Note that, the definition is not symmetric for and . is positively connected to does not mean that is positively connected to .

Definition: If is positively (or negatively) connected to and is positively (or negatively) connected to , then we call- there is a positive (or negative) connection between and .

It is easy to see that if and have positive (/negative) connection, then assumption 1, assumption 2 and assumption 2’ are satisfied. This is because .

Therefore this stronger but reasonable assumption unifies the previous assumptions and enable us to state the following theorem.

Theorem 6.

Under the assumption that returns of two stocks have positive (/negative) connection, for the pairs with 1st and 4th configuration,

and

where is the Kendall’s tau calculated on the paired data with 1st and 4th configurations, i.e. , where and are independent pairs of the same configurations.