Horizon-unbiased Investment with Ambiguity111 We are grateful for the funding from the NSF of China (11501425 and 71801226).

Abstract

In the presence of ambiguity on the driving force of market randomness, we consider the dynamic portfolio choice without any predetermined investment horizon. The investment criteria is formulated as a robust forward performance process, reflecting an investor’s dynamic preference. We show that the market risk premium and the utility risk premium jointly determine the investors’ trading direction and the worst-case scenarios of the risky asset’s mean return and volatility. The closed-form formulas for the optimal investment strategies are given in the special settings of the CRRA preference.

Keywords: Ambiguity, Forward Performance, Robust Investment, Risk Premium

1 Introduction

Dynamic portfolio choice problems usually envisage an investment setting where an investor is exogenously assigned an investment performance criteria and stochastic models for the price processes of risky assets. However, the investor may extemporaneously change the investment horizon, consistently update her preference with the market evolution, and conservatively invest due to ambiguity on the driving force of market randomness or the dynamics of the risky assets. Motivated by these investment realities, we study a robust horizon-unbiased portfolio problem in a continuous-time framework.

In the seminal work of Merton, (1969), continuous-time portfolio choice is formulated as a stochastic control problem to maximize the expected utility at a specific investment horizon by searching for the optimal strategy in an admissible strategy space. Note that if the investor has two candidate investment horizon , , , the resulting optimal strategies associated with these two horizons are generally not consistent over the common time interval , (Musiela & Zariphopoulou,, 2007). Hence, Merton’s framework is neither suitable for the case where an investor may extend or shorten her initial investment horizon, nor the case where the investor may update her preference in accordance to the accumulated market information. In these quite realistic settings, the investor needs an optimal strategy which is independent of the investment horizon and reflects her dynamic preference in time and wealth. The horizon-unbiased utility or forward performance measure, independently proposed by Choulli et al., (2007), Henderson & Hobson, (2007), Musiela & Zariphopoulou, (2007), provides a portfolio framework satisfying the aforementioned requirements. In such framework, an investor specifies initial preferences (utility function), and then propagates them forward as the financial market evolves. This striking characteristic contrasts the portfolio choice based on the forward performance measure from that in Merton’s framework, in which intertemporal preference is derived from the terminal utility function in a backward way. Musiela & Zariphopoulou, 2010b specify the generic forward performance measure as a stochastic flow , taking time and wealth as arguments. The randomness of the forward performance measure is driven by the Brownian motion which is the same as the driving force of the randomness of asset price. It implies that the driving force of market randomness is simultaneously embedded into the investor’s preference and the risky asset price process. Such modeling approach implicitly assumes that the Brownian motion represents the essential source of risk behind the financial market and the risky assets. Especially, the volatility of a forward performance measure reflects the investor’s uncertainty about her future preference due to the randomness of the financial market states. However, due to the epistemic limitation or limited information, an investor may have ambiguity about the driving force of market randomness and her future preference. Focusing on such ambiguities, we will introduce a robust forward performance measure, and investigate the corresponding portfolio selection problems.

The mean return rate and volatility are important factors characterizing the dynamics of risky assets. In the traditional portfolio theory, these two factors are usually modeled by stochastic processes, the distributions of which are known to the decision-maker at each time node before the specified investment horizon. In this case, the investor is actually assumed to have full information on the driving force of market randomness, and can accurately assigns probabilities to the various possible outcomes of investment or factors associated with the investment. However, in so complicated financial markets, it is unrealistic for investors to have accurate information on the dynamics or distributions of the risk factors, essentially due to the cognitive limitation on the driving force of market randomness. This situation is referred to as “ambiguity” in the sense of Knight, while “risk” in the former situation. Ambiguity has raised researchers’ attention in the area of asset pricing and portfolio management (see e.g. Maenhout,, 2004, Garlappi et al.,, 2007, Wang,, 2009, Bossaerts et al.,, 2010, Liu,, 2011, Chen et al.,, 2014, Luo et al.,, 2014, Guidolin & Liu,, 2016, Luo,, 2017, Zeng et al.,, 2018, Escobar et al.,, 2018). We assume that an investor has ambiguous beliefs on the paths of the risky asset price. Ambiguous beliefs are characterized by a set of probability measures defined on the canonical space , the set of continuous paths starting from the current price of the risky asset. We incorporate the investor’s ambiguity on the risky asset price into her preference, by defining the forward performance measure on the canonical space .

We first characterize ambiguity on the dynamics of risky asset in terms of ambiguity on its mean return and volatility. More specifically, we assume that the mean return and the volatility processes of the risky asset lie in a convex compact set , which then leads to the set of probability measures . This formulation is different from the stochastic models with the known distributions at each time node, and generalizes the framework defined on a probability space with only one probability measure. Within in this general setting, we investigate an ambiguity-averse investor’s investment strategy, and her conservative beliefs on the mean return and the volatility of risky assets.

We then define the robust forward performance measure, by taking the investor’s ambiguity on the deriving force of market randomness. In turn, we propose a method to construct such robust forward performance measure for a given initial preference, and derive the corresponding investment strategy and conservative beliefs on the mean return and the volatility of risky assets. We show that the sum of the market risk premium and the utility risk premium determines the trading direction. We further specify the initial preference of the constant relative risk aversion (CRRA) type, and investigate the determinants of the conservative beliefs on the mean return and the volatility of risky assets in three settings, i.e., ambiguity on the mean return rate, ambiguity on the volatility, and the structured ambiguity. When we consider ambiguity on the mean return rate, we keep the volatility as a constant, and vise versa. Such ambiguities have been investigated in Merton’s framework (see e.g. Lin & Riedel,, 2014, Luo,, 2017). The third setting is motivated by the fact that there is no consensus on the relation between the mean return and the volatility of risky assets in the empirical literature (see e.g. Omori et al.,, 2007, Bandi & Renò,, 2012, Yu,, 2012), and investigated by Epstein & Ji, (2013). We show that the sign of the total risk premium determines the conservative belief on the mean return in the first setting, while the risk attitude and the relative value of the market risk premium over the utility risk premium jointly determine the conservative belief on the volatility in the second setting. In the third setting, we would not derive the closed-form formula for the conservative beliefs, but show that the corresponding beliefs can take some intermediate value within the candidate value interval, as well as the upper and lower bounds. To our knowledge, such interesting results are new in the portfolio selection literature.

This paper contributes to the existing literature in three folds. First, we propose a generic formulation of robust forward performance accommodating an investor’s ambiguity on the dynamics of risky assets. Second, we figure out the determinants of trading direction for an investor in a market with one risk-free asset and one risky asset. From the economic point of view, it is the sum of the market risk premium and the utility risk premium that determines an investor’s trading direction. Third, we show that the market risk premium, the utility risk premium, and the risk tolerance affect an investor’s conservative belief on the mean return and volatility. Especially, if the maximum of the total risk premium is negative, an investor will take the maximum of the mean return as the worst-case value; if the minimum of the total risk premium is positive, an investor will take the minimum of the mean return as the value in the worst-case scenario; otherwise, the worst-case mean return lies between its minimum and maximum. The market risk premium, the utility risk premium, and the risk tolerance jointly determine an investor’s conservative belief on the volatility of risky assets. We emphasize that the conservative belief is related to the optimization associated with risk premiums, and these conservative beliefs may be some intermediate values within their candidate value intervals, as well as boundaries.

Related Literature. Most of the existing results on forward performance measures have so far focused on its construction and portfolio problems in the setting of risk, rather than ambiguity (Zariphopoulou & Žitković,, 2010, Musiela & Zariphopoulou, 2010a, , Alghalith,, 2012, El Karoui & Mrad,, 2013, Kohlmann et al.,, 2013, Anthropelos,, 2014, Nadtochiy & Tehranchi,, 2017, Avanesyan & May,, 2018, Shkolnikov et al.,, 2016, Angoshtari et al.,, 2018, to name a few). As one of the few exceptions, Källblad et al., (2018) investigate the robust forward performance measure in the setting of ambiguity characterized by a set of equivalent probability measures. However, this approach fails to solve the robust “forward” investment problem under ambiguous volatility, since volatility ambiguity is characterized by a set of mutually singular probability measures (Epstein & Ji,, 2013). We fill this gap by characterizing an investor’s ambiguity with a set of probability measures, which may not be equivalent with each other. Similar to our work, Chong & Liang, (2018) investigate robust forward investment under parameter uncertainty in the framework where a unique probability measure is aligned to the canonical space . Different from such model setup, we align a set of probability measures on the canonical space , accounting for an investor’s ambiguity on the future scenarios of the risky asset price. This approach is not only technically more general than the approach with a set of dynamic models under a unique probability measure (as detailed in Remark 4 by Epstein & Ji, (2013)), but also allows an investor to explicitly incorporate ambiguity on the risk source into her preference. That is the key difference between our framework and the framework of Chong & Liang, (2018). On the other hand, Chong & Liang, (2018) construct the forward performance measure based on the solution of an infinite horizon backward stochastic differential equation (BSDE). Our approach associates the forward performance measure with a stochastic partial differential equation (SPDE), which provides the analogue of the Hamilton-Jacobi-Bellman equation (HJB) in Merton’s framework. For the reason of tractability, we limit ourself to forward performance measures of some special forms, and investigate the corresponding robust investment. It is out of this paper’s scope to investigate the existence, uniqueness, and regularity of the solution of the associated SPDE in the general setting. Such simplified model setup and the corresponding results shed light on how ambiguity-aversion investors dynamically revise their preferences as the market involves.

The remainder of this paper is organized as follows. Section 2 introduces the model setup for robust forward investment. The construction of the robust forward performance measure is investigated in Section 3. In Section 4, we study the conservative belief of an ambiguity-averse investor with preference of the constant relative risk aversion (CRRA) type. Section 5 concludes.

2 Model setup

We consider a financial market with two tradable assets: the risk-free bond and the risky asset. The risk-free bond has a constant return rate , i.e.,

| (2.1) |

where is bond price with .

The risk asset price is modelled by the canonical process of , defined by

where is the current price of the risky asset and . We equip with the uniform norm and the corresponding Borel -field . denotes the canonical filtration, i.e., the natural (raw) filtration generated by . Due to the complication of financial market and the limitation of individual cognitive ability, an investor may have ambiguous belief on the risky asset price, i.e., ambiguity on the mean return or volatility in our model setup. We assume that can take any value within a convex compact set , but without additional information about their distributions for any time . That is, represents ambiguity on the return and volatility of the risky asset. More explicitly, we characterize ambiguity by , defined by

| (2.2) |

For , let be the probability measure on such that the following stochastic differential equation (SDE)

| (2.3) |

admits a unique strong solution , where is a Brownian motion under . Let denote the set of probabilities on such that the SDE (2.3) has a unique strong solution, corresponding to the ambiguity characteristic . The Brownian motion can be interpreted as the driving force of randomness behind the risky asset under the probability measure . Such model setup allows us to analyze how the investor’s belief on the risky asset affects her preference and investment strategy, especially the effect of ambiguity on the risk source.

An investor is endowed with some wealth at time , and allocates her wealth dynamically between the risky asset and the risk-free bond. For and , let be the proportion of her wealth invested in the stock at time . Due to the self-financing property, the discounted wealth is given by

| (2.4) |

where is the risk-free interest rate, is a Brownian motion under . The set of admissible strategies is defined by

The optimal investment strategy and the corresponding wealth process are usually associated with an optimization problem, such as utility maximization or risk minimization. Within Merton’s framework for portfolio theory (Merton,, 1969), the value process is formulated as

| (2.5) |

where the investment horizon is predetermined, is a utility function, is the set of admissible strategy, and is the terminal wealth corresponding to an admissible strategy . The expectation in (2.5) is taken under some probability measure , if there is no ambiguity on the deriving force of market randomness. Then, the dynamic programming principle can be applied to solve the optimal control problem (2.5), namely,

| (2.6) |

By verification arguments, is the solution of the Hamilton-Jacobi-Bellman (HJB) equation (Yong & Zhou,, 1999). The dynamic programming equation (2.6) essentially signifies that is a martingale at the optimum, and a supermartingale otherwise, associated with some probability measure . This property can be interpreted as follows: if the system is currently at an optimal state, one needs to seek for controls which preserve the same level of the average performance over all future times before the predetermined investment horizon . We refer to this property as the martingale property of the value process. On the other hand, (2.6) hints that coincides with , where represents the preference at . Note that the future utility function is specified at . However, it is not intuitive to specify the future preference at the initial time with complete isolation from the evolution of the market. Musiela & Zariphopoulou, (2007, 2008) propose the so-called forward performance measure which keeps the martingale property of for any horizon , and coincides with the initial preference, namely . In this framework, the future preference dynamically changes in accordance with the market evolution.

In the similar spirit of Musiela & Zariphopoulou, (2007, 2008), we will generalize the definition of forward performance measure by considering ambiguity on the risk source. For , we define

| (2.7) |

which facilitates the definition of the robust forward performance measure.

Definition 2.1 (Robust forward performance).

An -progressively measurable process is called a robust forward performance if for and , the following holds.

-

(i)

The mapping is strictly concave and increasing.

-

(ii)

For each , , and

-

(iii)

There exists for which

Given the dynamics of the forward performance measure , we will solve the problem for optimal investment strategy, which can be formulated as a similar problem as (2.6).

Problem 2.1 (Robust Investment Problem).

The solution of this problem provides the robust investment strategy and the worst-case scenario of under ambiguity. In turn, they will implicitly provide the corresponding probability measure . In the next section, we will introduce the construction methods for the forward performance under ambiguity, and then solve the robust investment problem.

3 Robust Investment under the Forward Performance Measures

The specification of a forward performance measure can take the market state and investor’s wealth level into account at time . Mathematically, is called stochastic flow, a stochastic process with space parameter. It can be characterized by its drift random field and diffusion random field. Under certain regularity hypotheses (El Karoui & Mrad,, 2013), it can be written in the integration form

| (3.9) |

where is the standard Brownian motion defined on some probability space, is the initial utility, and and are the so-called drift random field and the diffusion random field, respectively. To guarantee a stochastic flow satisfy the definition 2.1, its drift random filed and diffusion random field should satisfy some structure. By exploring such structure, Musiela & Zariphopoulou, 2010b constructed some examples of forward performance measures. In this framework, the driving force of market randomness is modelled by the standard Brownian motion . We will generalize such framework, and account for the ambiguity on the driving force of market randomness or the risky asset price. Different from the dynamics of the risky asset price (2.3), we give even more freedom to an investor’s preference, and propose the robust forward performance measure of the following form,

| (3.10) |

where a Brownian motion under and . The random field characterizes an investor’s attitudes toward wealth level, ambiguity, and market risk. Especially, the volatility term of the robust forward performance measure reflects the investor’s ambiguity about her preferences in the future, and is subject to her choice. The BSDE-based approach proposed by Chong & Liang, (2018) captures the investor’s concern on parameter uncertainty by the generator of the associated BSDE. Different from this BSDE-based approach, we explicitly embed such concern into the axiomatic formulation (3.10).

For any given robust forward preference of the form (3.10), the investment problem 2.1 allows an investor to maximize her utility under the worst-case scenario of . To make the investment problem tractable, the forward performance measure is assumed to be regular enough. For this reason, we introduce the notation of -smooth stochastic flow.

Definition 3.1 (-Smooth Stochastic Flow).

Let be a stochastic flow with spatial argument and local characteristics , i.e.,

where is a Brownian motion defined on a filtered probability space . is said to be -smooth or belong to , if

-

(i)

for , is continuous; for each , is a -map from to , -a.s.,

-

(ii)

and are continuous process continuous in such that

-

(a)

for each , belong to , -a.s.;

-

(b)

for each , and are -adapted.

-

(a)

For , we are ready to formulate the robust forward performance as a -smooth stochastic flow

| (3.11) |

where a Brownian motion under and . Its smoothness plays a key role to construct the robust forward performance measures by specifying the structure of .

Lemma 3.1.

For , let be a -smooth stochastic flow as defined in (3.11). Let us suppose that

-

(i)

the mapping is strictly concave and increasing;

-

(ii)

for an arbitrary , there exists , such that

and is a -supermartingale;

-

(iii)

there exists such that is a -martingale.

Then is the optimal investment strategy for Problem 2.1, associated with the worst-case scenario of .

Proof.

For each , since is a -supermartingale,

Since there exists such that is a -martingale, we have

Recalling the definition of robust forward performance (Definition 2.1), we can see that is a forward performance, and the statement of this theorem is proved. ∎

Lemma 3.1 provides a method to find the worst-case scenario of the mean return and volatility of the risky asset, and the corresponding investment strategy, as stated in Theorem 3.2.

Theorem 3.2.

Let be a -smooth stochastic flow on with and , and the mapping is strictly concave and increasing. We suppose the following holds.

-

(i)

satisfies the following equation

(3.12) -

(ii)

For any , there exists such that

Let satisfy

and satisfy

| (3.13) | |||||

Proof.

Under the regularity conditions on , we apply the Itô-Ventzell formula to for any admissible portfolio under each

We denote by .

For ,

where on , and on .

Therefore,

| (3.14) |

Theorem 3.2 provides a natural way to construct a robust forward performance measure, optimal investment strategy and the worst-case scenario of the mean return and volatility of risky assets. We summarize such results in Corollary 3.3.

Corollary 3.3.

-

(i)

If the is a robust forward performance measure and the worst-case is selected, the optimal investment strategy is given in the feedback form

(3.15) where the first and second term of the optimal strategy will be referred to as its non-myopic and myopic part, respectively (Musiela & Zariphopoulou, 2010b, ).

-

(ii)

If the is a robust forward performance measure, its characteristics should satisfy.

(3.16) for . The solution of condition (3.16) leads to the worst-case .

The constraint (3.16) on the local characteristics implies that the forward performance measure is not unique for a given initial utility function. By specifying three of them, we can calculate the fourth one. Hence, the investor in this framework has the freedom to specify her initial utility, as well as the additional characteristics of the utility field. However, in Merton’s framework, the dynamics and characteristics of the utility field are derived from the terminal utility function, which is specified by the investor at the initial time. We note that the constraint (3.16) holds in the path-wise sense.

The local characteristics actually can be used to represent the investor’s attitude through local risk tolerance , utility risk premium (El Karoui & Mrad,, 2013), and market risk premium . Actually, the optimal strategy (3.15) can be written as

| (3.17) | ||||

| (3.18) |

The first component of the investment strategy (3.17), known as myopic strategy, resembles the investment policy followed by an investor in markets in which the investment opportunity set remains constant through time. The second one is called the excess hedging demand and represents the additional (positive or negative) investment generated by the volatility process of the performance process (Musiela & Zariphopoulou, 2010b, ). Essentially, the investment strategy (3.18) reveals that it is affected by the investor’s risk tolerance, market risk premium, and utility risk premium, as well as the worst-case scenario of the mean return and the volatility of the risky asset. Obviously, it is the sum of utility risk premium and market risk premium that determines the trading direction of an investor. Such statement holds regardless of the specification of the robust forward performance measure. Note that the worst-case scenario of is characterized by (3.16). To analyze the implication of ambiguity, we restrict ourself to the robust forward performance measure of special forms, and derive the analytical solution for (3.16).

4 Robust Forward Performance of the CRRA type

Utility function of the CRRA type is one of the commonly used utility function, which is a power function of wealth. We assume an investor’s dynamic preference is characterized by utility function of the CRRA type over the time , with the initial utility function , and time-varying coefficients. More specifically, we set such forward performance of the following form

| (4.19) |

where and is a Brownian motion defined on a filtered probability space with and . Without loss of generality. Its differential form is then given by

| (4.20) |

and

| (4.21) | ||||

| (4.22) |

In this case, the utility risk premium .

We can rewrite the forward performance measure (4.34) in the form of (3.11), where

| (4.23) | ||||||

The characteristics can be substituted into the constraints (3.16), to specify the structure of the forward performance (4.19).

If there is no ambiguity on the mean return and volatility, the constraint (3.16) is reduced to

| (4.24) |

and the corresponding investment strategy is given by

| (4.25) |

The optimal investment strategy without ambiguity (4.25), as well as the optimal strategy with ambiguity (3.18), implies that the market risk premium and utility risk premium play an important role in the trading direction in both settings.

In the following sub-sections, we will consider an investor’s conservative beliefs and the forward performance of the CRRA type in different settings: ambiguity on mean return , ambiguity on the volatility , and ambiguity on both mean return and volatility. The structure of forward performance in these settings will involve optimizations with respect to and , as implied by the constraint (3.16).

4.1 Ambiguity only on the mean return

Ambiguity on the mean return is referred to as the case where the dynamics of mean return is ambiguous, with known dynamics of volatility. For the sake of simplicity, we assume is known as a constant .

Proposition 4.1.

Assume an investor’s forward preference is characterized by the initial utility function with , and propagates in the following form

| (4.26) |

where and are deterministic functions of , is the volatility of the risky asset, and is a Brownian motion defined on a filtered probability space with and .

If the investor’s ambiguity is characterized by the lower bound and upper bound of , should satisfy the following condition

| (4.27) |

where

| (4.28) |

Corresponding to the selection of worst-case mean return , the investment strategy is given by

| (4.29) |

Proof.

We can interpret the selection rule (4.28) from the premium point of view. Recalling the definition of the market risk premium and the utility risk premium , i.e.,

we can rewrite (4.28) as

| (4.33) |

It implies that the worst-case mean return and the trading direction depend on the total risk premium that the investor can achieve in the setting of ambiguity on mean return, i.e., . When is positive, an investor will take as the worst-case mean return, and take a long position . When is negative, an investor will take as the worst case, and take a short position . Otherwise, she will take as the worst-case mean return, and do not invest on the risky asset . From this point of view, it is the total risk premium that characterizes the worst-case mean return and the investor’s trading direction.

Such premium-based rule (4.28) on the conservative belief towards the mean return is consistent with the rule proposed by Chong & Liang, (2018) and Lin & Riedel, (2014). Chong & Liang, (2018) propose to select the worst-case scenario of the mean return in a feedback form associated with the position on risky assets, i.e., the long and short positions correspond to and , respectively. In the classical framework, the selection of worst-case mean return dependents on the investor’s position on the risky asset, as argued by Lin & Riedel, (2014) that nature decides for a low drift if an investor takes a long position, and for a high drift if an investor takes a long position. However, the rule (4.28) is not given in a feedback form associated with an investor’s position, but directly related to the market situations and the investor’s utility risk premium. In this new framework, we highlight the combination effect of the utility risk premium and the market risk premium on the worst-case mean return of the risky asset.

4.2 Ambiguity only on volatility

We refer to volatility ambiguity as the case where the dynamics of volatility is unknown, but constrained in the interval with . For the sake of simplicity, we suppose to be a constant over the time.

Proposition 4.2.

Assume an investor’s preference is characterized by the initial utility function with , and propagates in the following form

| (4.34) |

where and are deterministic functions of , is the volatility of the risky asset, and is a Brownian motion defined on the filtered probability space with and .

If the investor ambiguity is characterized by the lower bound and upper bound of , should satisfy the following structure

| (4.35) |

where

| (4.36) |

Correspondingly, the optimal investment strategy is

Proof.

In this setting, the constraint (3.16) is reduced to

| (4.37) |

To solve the optimization problem, we denote , and define a function by

Simply analysis can provide that reaches its maximum at , where

| (4.38) |

Due to , we have the worst-case scenario of (4.38). ∎

The conservative belief on the volatility depends on the market risk premium and the utility risk premium, as the case of the conservative belief on mean return (4.28) or (4.33). We will show that it is the relative value of these two premiums that determines the conservative belief on volatility. Note that it is the sum of these two premium determines the conservative belief on mean return, as shown by (4.28) or (4.33). In our specific setting, ambiguity on mean return only affects the market risk premium, while ambiguity on volatility affects both the market risk premium and the utility risk premium. It is then natural to consider the effects of their relative value.

Define the relative value of the utility risk premium with respect to the market price of risk as

Then, the worst-case volatility (4.38) can be rewritten as

| (4.39) |

The rule (4.39) for worst-case volatility implies that if the relative value of the utility risk premium over the market risk premium is large enough than the investor’s risk-averse attitude , the investor will take as the worst-case volatility. Alternatively, if such relative value is smaller enough than the investor’s risk-averse attitude, the investor will take as the worst-case volatility. Otherwise, the worst-case volatility depends on her attitude toward risk and ambiguity about her future preferences. Overall, an ambiguity-averse investor will take her attitude toward risk and ambiguity into account when ambiguous on the volatility of the driving force of market randomness.

4.3 Structured ambiguity on mean return and volatility

Empirical research shows that the mean return can be either positively or negatively related to the volatility of risky assets (see e.g. Omori et al.,, 2007, Bandi & Renò,, 2012, Yu,, 2012). Without a consensus of their relation, we employ a flexible model to capture the structured ambiguity on the mean return and volatility of the driving force of market randomness (Epstein & Ji,, 2013, 2014),

| (4.40) |

where and such that . implies that the return is positively related to the volatility, and vice versa. The selection of worst-case value of mean return and volatility will be reduced to the selection of , where the spread represents the size of an investor’s ambiguity on the mean return and volatility.

For any given set of the parameters , we can easily solve the problem (4.41) with respect to , and the optimal investment strategy is correspondingly given as the expression (3.15). The analytical expression for is omitted here, since it is not very expressive, in the sense that the solution for (4.41) does not provide a straightforward intuition for the determinants of the conservative beliefs. Obviously, the value of depends on the interval and the shape of (4.41). To derive more intuitional information on the conservative beliefs and its dependence on , we define

| (4.43) |

where are given in (4.42). The second order derivative of with respect to is

Since , and , we have

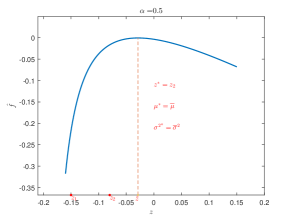

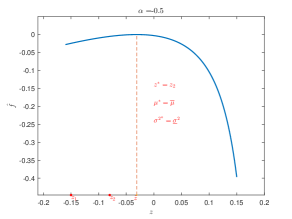

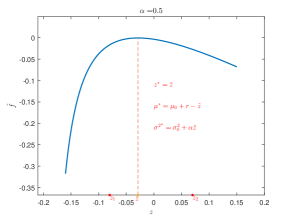

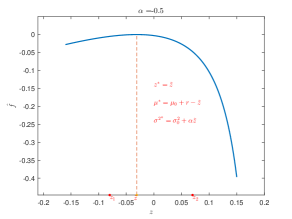

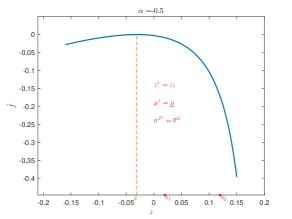

That is, is a concave function on . Such property relates to the model parameters and the concavity of , as shown in the Figure 1 with some toy examples.

These toy examples show the concavity of in the setting of and with the following common parameters

For each , we denote by the value of at which reaches its maximum. Then, we have three cases of for each , i.e., , , and . Take the case of and for example, reaches its maximum at if . Correspondingly, we have and . One can easily figure out in the other cases from Figure 1. We summarize these toy examples in Table 1. Generally speaking, may take the upper or lower bound of the interval for , or some value lying in the interval. When the mean return is positively related to the volatility of the risky asset , the worst-case scenario of these two parameters is , , or some intermediate value depending on some . When they are negatively related, the conservative belief is , , or some intermediate value depending on some .

By specifying the interval , we can not only verify the conservative belief on given in Table 1 or Figure 1, but also the relation between trading direction and total risk premium. Some alternatives for are given in Table 2. The worst-case scenario is consistent with the implications of Table 1 or Figure 1. The corresponding investment strategy and total risk premium listed in the last two columns show that the investor will take a long position on the risky assets if the total risk premium is position, and vice versa. This is consistent with our theoretical statements, as given by (3.18).

| Total Risk Premium | |||||||

|---|---|---|---|---|---|---|---|

| -0.15 | -0.08 | 0.5 | -0.0795 | ||||

| -0.08 | 0.07 | 0.5 | -0.0289 | 0.0089 | 0.0145 | -0.0059 | |

| 0.02 | 0.12 | 0.5 | 0.7727 | ||||

| -0.15 | -0.08 | -0.5 | -0.5476 | ||||

| -0.08 | 0.07 | -0.5 | -0.0311 | 0.0111 | 0.0156 | 0.0066 | |

| 0.02 | 0.12 | -0.5 | 0.9074 |

5 Conclusion

The complicated market confronts an investor to ambiguity on the driving force of market randomness. Such ambiguity may take the form of ambiguity on the mean return rate and volatility of an risky asset. It may also affect the investor’s preference when making investing decisions. That is, the investor may be ambiguous not only on the characteristics of risky assets but also on her future preference. We took these two types of ambiguity into account, and investigated the horizon-unbiased investment problem.

We proposed the robust forward performance measure by accounting for an investor’s ambiguity on the future preference, arising from the ambiguity on the driving force of market randomness. This robust forward performance measure is then applied to formulate the investment problem. The solution to such investment problem shows that the sum of the market risk premium and the utility risk premium jointly determines the optimal trading direction. If it is positive, the investor will take a long position on the risky asset. Otherwise, she will take a short position. This statement holds regardless of the specific form of the forward performance measures.

We then explored the worst-case scenarios of the mean return and volatility when the initial utility is of the CRRA type. Specifically, we investigate the worst-case mean return and volatility in three settings: ambiguity on mean return , ambiguity on the volatility , and ambiguity on both mean return and volatility. In the case of ambiguity on the mean return, it is the total value of the market risk premium and the utility risk premium that determines an investor’s conservative belief; In the case of ambiguity on the volatility, it is the relative value of these two premiums that affects an investor’s conservative belief. In the case of ambiguity on both the mean return and volatility, the conservative belief may not be directly associated with these two premiums. Note that, in all the three settings, the conservative beliefs may be the some intermediate values within their candidate value intervals, as well as boundaries.

In conclusion, the results provide explanations on the mechanism of conservative belief selection and robust portfolio choice when an investor propagates her preference in accordance with the market evolution.

References

- Alghalith, (2012) Alghalith, M. (2012). Forward Dynamic Utility Functions: A New Model and New Results. European Journal of Operational Research, 223(3), 842–845.

- Angoshtari et al., (2018) Angoshtari, B., Zariphopoulou, T., & Zhou, X. Y. B. (2018). Predictable Forward Performance Processes: The Binomial Case. working paper, (pp. 1–22).

- Anthropelos, (2014) Anthropelos, M. (2014). Forward Exponential Performances: Pricing and Optimal Risk Sharing. SIAM Journal on Financial Mathematics, 5(1), 626–655.

- Avanesyan & May, (2018) Avanesyan, L. & May, M. F. (2018). Construction of Forward Performance Processes in Stochastic Factor Models and an Extension of Widder’s Theorem. arXiv:1805.04535.

- Bandi & Renò, (2012) Bandi, F. M. & Renò, R. (2012). Time-Varying Leverage Effects. Journal of Econometrics, 169(1), 94–113.

- Bossaerts et al., (2010) Bossaerts, P., Ghirardato, P., Guarnaschelli, S., & Zame, W. (2010). Ambiguity in Asset Markets : Theory and Experiment. The Review of Financial Studies, 23(4), 1325–1359.

- Chen et al., (2014) Chen, H., Ju, N., & Miao, J. (2014). Dynamic Asset Allocation with Ambiguous Return Predictability. Review of Economic Dynamics, 17(4), 799–823.

- Chong & Liang, (2018) Chong, W. F. & Liang, G. (2018). Optimal Investment and Consumption with Forward preferences and Uncertain Parameters. working paper, (pp. 1–28).

- Choulli et al., (2007) Choulli, T., Stricker, C., & Li, J. (2007). Minimal Hellinger Martingale Measures of Order . Finance and Stochastics, 11(3), 399–427.

- El Karoui & Mrad, (2013) El Karoui, N. & Mrad, M. (2013). An Exact Connection between Two Solvable SDEs and a Non Linear Utility Stochastic PDEs. SIAM Journal on Financial Mathematics, 4, 697–736.

- Epstein & Ji, (2013) Epstein, L. G. & Ji, S. (2013). Ambiguous Volatility and Asset Pricing in Continuous Time. Review of Financial Studies, 26(7), 1740–1786.

- Epstein & Ji, (2014) Epstein, L. G. & Ji, S. (2014). Ambiguous Volatility, Possibility and Utility in Continuous Time. Journal of Mathematical Economics, 50, 269–282.

- Escobar et al., (2018) Escobar, M., Ferrando, S., & Rubtsov, A. (2018). Dynamic Derivative Strategies with Stochastic Interest Rates and Model Uncertainty. Journal of Economic Dynamics and Control, 86, 49–71.

- Garlappi et al., (2007) Garlappi, L., Uppal, R., & Wang, T. (2007). Portfolio Selection with Parameter and Model Uncertainty: A Multi-prior Approach. Review of Financial Studies, 20(1978), 41–81.

- Guidolin & Liu, (2016) Guidolin, M. & Liu, H. (2016). Ambiguity Aversion and Underdiversification. Journal of Financial and Quantitative Analysis, 51(4), 1297–1323.

- Henderson & Hobson, (2007) Henderson, V. & Hobson, D. (2007). Horizon-Unbiased Utility Functions. Stochastic Processes and their Applications, 117(11), 1621–1641.

- Källblad et al., (2018) Källblad, S., Obłój, J., & Zariphopoulou, T. (2018). Time–Consistent Investment under Model Uncertainty: The Robust Forward Criteria. Finance and Stochastics, (pp. 1–41).

- Kohlmann et al., (2013) Kohlmann, M., Siyuan, L., & Xiong, D. (2013). A Generalized Itô-Ventzell Formula to Derive Forward Utility Models in a Jump Market. Stochastic Analysis and Applications, 31(4), 632–662.

- Lin & Riedel, (2014) Lin, Q. & Riedel, F. (2014). Optimal Consumption and Portfolio Choice with Ambiguity. working paper.

- Liu, (2011) Liu, H. (2011). Dynamic Portfolio Choice under Ambiguity and Regime Switching Mean Returns. Journal of Economic Dynamics and Control, 35(4), 623–640.

- Luo, (2017) Luo, Y. (2017). Robustly strategic consumption–portfolio rules with informational frictions. Management Science, 63(12), 4158–4174.

- Luo et al., (2014) Luo, Y., Nie, J., & Young, E. R. (2014). Model Uncertainty and Intertemporal Tax Smoothing. Journal of Economic Dynamics and Control, 45, 289–314.

- Maenhout, (2004) Maenhout, P. J. (2004). Robust Portfolio Rules and Asset Pricing. Review of Financial Studies, 17(4), 951–983.

- Merton, (1969) Merton, R. C. (1969). Lifetime Portfolio Selection under Uncertainty: The Continuous-Time Case. The Review of Economics and Statistics, 51(3), 247–257.

- Musiela & Zariphopoulou, (2007) Musiela, M. & Zariphopoulou, T. (2007). Investment and Valuation Under Backward and Forward Dynamic Exponential Utilities in a Stochastic Factor Model. In Advances in Mathematical Finance (pp. 303–334). Boston, MA: Birkhäuser Boston.

- Musiela & Zariphopoulou, (2008) Musiela, M. & Zariphopoulou, T. (2008). Optimal Asset Allocation under Forward Exponential Performance Criteria. In R. H. thier, Stewart N. and Feng, Jin and Stockbridge (Ed.), Markov Processes and Related Topics: A Festschrift for Thomas G. Kurtz, volume 4 (pp. 285–300). Beachwood, Ohio, USA: Institute of Mathematical Statistics.

- (27) Musiela, M. & Zariphopoulou, T. (2010a). Portfolio Choice under Space-Time Monotone Performance Criteria. SIAM Journal on Financial Mathematics, 1, 326–365.

- (28) Musiela, M. & Zariphopoulou, T. (2010b). Stochastic Partial Differential Equations and Portfolio Choice. In C. Chiarella & A. Novikov (Eds.), Contemporary Quantitative Finance (pp. 1–24). Berlin Heidelberg: Springer-Verlag.

- Nadtochiy & Tehranchi, (2017) Nadtochiy, S. & Tehranchi, M. (2017). Optimal Investment for All Time Horizons and Martin Boundary of Space-Time Diffusions. Mathematical Finance, 27(2), 438–470.

- Omori et al., (2007) Omori, Y., Chib, S., & Shephard, N. (2007). Stochastic Volatility with Leverage : Fast and Efficient Likelihood Inference. Journal of Econometrics, 140, 425–449.

- Shkolnikov et al., (2016) Shkolnikov, M., Sircar, R., & Zariphopoulou, T. (2016). Asymptotic Analysis of Forward Performance Processes in Incomplete Markets and Their Ill-Posed HJB Equations. SIAM Journal on Financial Mathematics, 7(1), 588–618.

- Wang, (2009) Wang, N. (2009). Optimal consumption and asset allocation with unknown income growth. Journal of Monetary Economics, 56(4), 524–534.

- Yong & Zhou, (1999) Yong, J. & Zhou, X. (1999). Stochastic Controls: Hamiltonian systems and HJB equations. New York: Springer-Verlag.

- Yu, (2012) Yu, J. (2012). A Semiparametric Stochastic Volatility Model. Journal of Econometrics, 167(2), 473–482.

- Zariphopoulou & Žitković, (2010) Zariphopoulou, T. & Žitković, G. (2010). Maturity-Independent Risk Measures. SIAM Journal on Financial Mathematics, 1(1), 266–288.

- Zeng et al., (2018) Zeng, Y., Li, D., Chen, Z., & Yang, Z. (2018). Ambiguity aversion and optimal derivative-based pension investment with stochastic income and volatility. Journal of Economic Dynamics and Control, 88, 70–103.