101 \jmlryear2019 \jmlrworkshopACML 2019

-Armed Bandits: Optimizing Quantiles, CVaR and Other Risks

Abstract

We propose and analyze StoROO, an algorithm for risk optimization on stochastic black-box functions derived from StoOO. Motivated by risk-averse decision making fields like agriculture, medicine, biology or finance, we do not focus on the mean payoff but on generic functionals of the return distribution. We provide a generic regret analysis of StoROO and illustrate its applicability with two examples: the optimization of quantiles and CVaR. Inspired by the bandit literature and black-box mean optimizers, StoROO relies on the possibility to construct confidence intervals for the targeted functional based on random-size samples. We detail their construction in the case of quantiles, providing tight bounds based on Kullback-Leibler divergence. We finally present numerical experiments that show a dramatic impact of tight bounds for the optimization of quantiles and CVaR.

keywords:

Optimistic optimization; Risk-averse solutions; Quantile optimization; CVaR optimization1 Introduction

We consider an unknown function , where and denotes the probability space representing some uncontrollable variables. For any fixed is a random variable of distribution and we consider with a real-valued functional defined on probability measures. We assume that there exists at least one such that . Using a set of sequential observations , our goal is to minimizing the simple regret with the value returned after using a budget .

Different families of algorithms have been developed to treat this problem. Some are for example of Bayesian flavor (see Shahriari et al., 2016, for instance), some are inspired by the bandit literature. Here we focus our interest on the bandit framework.

In the classical -armed bandit problem, a forecaster selects repeatedly a point in the input space and receives a reward distributed according to an unknown distribution . Historically, the main goal was to minimizing the cumulative regret, i.e. the sum of the difference between his collected rewards and the ones that would have been brought by optimal actions. In the last decade, other works focused on the simple regret. These can be divided in two: algorithms that optimize an unknown function with the knowledge of the smoothness, for example StoOO (Munos et al., 2014), HOO (Bubeck et al., 2011) or Zooming (Kleinberg et al., 2008) and others focusing on the optimization of unknown functions without the knowledge of the smoothness, such as POO (Grill et al., 2015), StroquOOL (Bartlett et al., 2018), GPO (Xuedong et al., 2019), StoSOO (Valko et al., 2013) or Locatelli and Carpentier (2018).

Those algorithms focus on the optimization of the conditional expectation of . This choice is questionable in some situations. For example if the shape and variance of the reward distribution depend on the input, a forecaster may be interested in different aspects of the unknown distribution in order to modulate its risk exposure. In the literature, some measures of risk have been proposed to replace the expectation: for instance quantiles (also referred to as Value-at-Risk, see Artzner et al., 1999), the Conditional Value-at-Risk (CVaR also referred as Superquantile or Expected Shortfall, Rockafellar et al., 2000) or expectiles (Bellini and Di Bernardino, 2017). The purpose of this paper is to present a risk optimization framework of an unknown stochastic function with the knowledge of the smoothness using only pointwise sequential observations and a finite budget .

-armed bandit algorithms rely on optimistic strategies that associate with each point of the space an upper confidence bound (UCB), that is, an optimistic prediction of the outcome. Adapting the classical setting to the optimization of risk measures implies being able to create high-probability confidence bounds for that particular measure. This problem has been tackled in the multi-armed bandit setting ( when the input space is discrete and finite). For instance, Audibert et al. (2009); Sani et al. (2012) focused on the empirical variance, Galichet et al. (2013); Kolla et al. (2019); Hepworth (2017) on the CVaR while in David and Shimkin (2016); Szorenyi et al. (2015) the authors based their policies on the quantile. However, the literature is scarce in the continuous input space case.

In this paper we provide a new version of the Stochastic Optimistic Optimization (StoOO) algorithm (Munos et al., 2014), named StoROO (Stochastic Risk Optimistic Optimization), which is designed to handle any functional . In a first part, we provide an analysis of the simple regret from a generic point of view. We then particularize our analysis in two important illustrative cases: conditional quantiles and CVaR. In the case of quantiles, assuming that the output distribution has a continuous, strictly increasing cumulative distribution function, we first propose an upper bound on the simple regret using Hoeffding’s inequality, then, we derive tighter confidence intervals that take into account the order of the quantile respectively based on Bernstein’s and Chernoff’s inequalities. In the case of the CVaR, we first derive an upper bound on the regret using the deviation inequality of Brown (2007), then using the work of Thomas and Learned-Miller (2019) we derived tighter confidence bounds. Finally, we present numerical experiments that illustrate the ability of our method to optimize conditional quantiles and CVaR of a black-box function and the relevance of using tight deviation bounds.

2 Problem setup

2.1 Hierarchical partitioning

The upper confidence bounds on which optimistic algorithms are based are surrogate functions larger than the objective (in a sense detailed below) with high probability. At each round , the point having the highest UCB is sampled and a reward is collected.

In the classical multi-armed bandit problem, computing and sorting the UCB can be done without major issues. But dealing with continuous input spaces implies maximizing a UCB function over a continuous space, which can be both computational intensive and algorithmically challenging. For example, Piyavskii’s algorithm (see Bouttier, 2017, and references therein) defines using a global Lipschitz assumption on the targeted function. Because of the Lipschitz hypothesis, the UCB maximizer is at an intersection of hyperplanes, i.e. where the UCB is non-differentiable. Thus a gradient-based algorithm cannot be used, implying that finding the point with the highest UCB is a very hard problem to solve.

To overcome the computational difficulties, a popular alternative is to rely on hierarchical partitions (see Bubeck et al. (2011); Munos et al. (2014) for instance), of such that

with the number of sub-regions obtained after expanding a cell and the -th cell at depth . In the following we assume that:

Assumption : There exists a decreasing sequence , such that for any and for any cell , , with the center of .

Assumption : There exists such that every cell of depth contains a ball of radius .

Starting with and following an optimistic strategy, at time the algorithm has expanded some cells and the result is a tree that is a subset of and a partition of . In this setting is taken as a piecewise constant function. Indeed for any we define such that for all , .

In the literature of -armed bandits there are two ways to select a cell of at each round. In Bubeck et al. (2011), the algorithm follows an optimistic path from the root to the leaves. In Munos et al. (2014), StoOO selects the cell having the highest UCB among all the cells of that have not been expanded, the set of leaves of . We consider here this second alternative. Hence, to find the maximizer of at time , we only need to evaluate and sort a finite number of values .

2.2 Regularity assumptions, noise and bias

Even in the absence of noise, optimization from finite samples requires some regularity of the objective. Following Munos et al. (2014), we assume the following smoothness property:

| (1) |

Note that this condition is less restrictive than a global Hölder condition. In particular, the objective may be very irregular (even possibly discontinuous) except in the neighborhood of global maxima.

At first glance, in our stochastic setting, it may not be easy to asses that satisfies (1). Sufficient conditions can be derived from the continuity of the conditional distribution with respect to . The relevant metric on the space of distributions actually depends on the chosen risk. For conditional quantiles, the natural assumption is that satisfies (1), and a sufficient condition is that . In the case of the the conditional expectation and for the CVaR (or more generally for a large class of Optimized Certainty Equivalent Ben-Tal and Teboulle (2007)), the natural metric involved is the Wasserstein distance , as explained in Section A.1.

To create confidence bounds for , StoOO samples the leafs at their centers . Then using that all observed values are independent, deviation inequalities are used to create , a UCB for . Finally to create , a UCB over the cells, a bias term is added that takes into account how can potentially increase from the center of the cell to its edges. Because the convergence of StoOO (and StoROO) only needs to be a UCB of for the cell containing (see the proof of Proposition 3.2 (see also Munos et al. (2014)), it is enough to use the condition (1) to define a UCB as

. The algorithm also needs a quantity that bounds from below in order to provide guaranties on the value of over each cell. We thus construct a lower confidence bound, termed , for , and use it as a LCB for the maximum of on . In particular, on the cell containing the optimum , it holds that

with high probability. To summarize, the estimation of is altered by two sources of error: the local estimation error made at the center of the cell, and the bias term . Balancing those two terms naturally provides a trade-off between exploration and exploitation.

3 Stochastic Risk Optimistic Optimization

3.1 The StoROO algorithm

StoROO starts by sampling one time each sub-region of the root node. Then, at each time the algorithm selects having the highest UCB. To reduce the estimation error, StoROO can either get more samples from (to reduce the variance), or split the cell in order to reduce its diameter (to reduce the bias). The good balance between these two options is found by dividing a cell as soon as the local estimation error is smaller than the bias, that is when

| (2) |

If Condition (2) is satisfied, StoROO expands and requires a new sample at the center of each sub-region. If Condition (2) is not satisfied, then StoROO requires a new sample at the center which is used to update and .

When the budget is exhausted, several choices are possible for the return value: they have the same theoretical guarantees. Following Munos et al. (2014), one can return the deepest node among those that have been expanded. Here we propose a different, more conservative choice. Denoting by the set of nodes having the highest LCB among those that have been expanded after a budget , StoROO returns the node with the highest value (an estimator of ) among the deepest nodes of . The pseudo-code of the full algorithm is given in Algorithm 1. It requires the parameters and that satisfy Condition (1), but of course the inequality do not have to be tight.

Input: error probability ; number of children ; time horizon ; ; ;

Define: UCB and LCB

Initialization ; ;

Expand into sub-regions the root node and sample one time each child

while do

3.2 Analysis of the algorithm

In this section we provide a theoretical analysis of StoROO. It is inspired by Munos et al. (2014), but differs most notably by the fact that the analysis is suited for any and not only for the conditional expectation. The analysis relies on the possibility to construct, for any , upper- and lower-confidence bounds and such that the event

has probability at least . We defer to Section 4 their specific expression for the cases of the quantile and CVaR. Especially Section 4 shows that in our setting the size of the confidence interval associated to each node is not always explicit, by opposition of the classical case. We thus need to introduce the following definition to quantify how many times a node needs to be sampled before satisfying the expansion condition (Eq. 2).

Definition 3.1.

Let and , a vector of safe constants is composed of constants , , and such that the event

has probability at least .

For example, in the case of the conditional expectation a direct consequence of Hoeffding’s inequality provides , and (see Munos et al. (2014)).

To ensure the convergence of StoROO, we first prove (Proposition 3.2) that any point at the center of an expanded cell of depth belongs to

| (3) |

Next, Proposition 3.3 shows that using a budget , the tree reaches at least a depth . This implies the point returned by the algorithm belongs to (Proposition 3.4). Finally, using an assumption on the size of that can be formalized by the so-call near-optimality dimension, we provide an upper bound on the regret (Theorem 3.7).

Proposition 3.2.

Conditionally on , StoROO only expands cells such that .

Given the safe constants and the total budget , the deeper the algorithm builds the tree, the better are the guarantees on the final point returned. So the goal of the following proposition is to provide a lower bound on the depth of .

Proposition 3.3.

Define and define the largest such that

The deepest node expanded by StoROO is such that

Intuitively, is the budget needed to expand all the nodes in for all . It may be that some of this nodes will not be visited, but in the worst case they are and they need to be considered in order to obtain a valid bound. Putting Propositions 3.2 and 3.3 together, yields a first upper bound on the simple regret:

Proposition 3.4.

Running StoROO with budget , with probability the regret is bounded as

A more explicit bound for the regret can be obtained by quantifying the volume of for small values of . Introducing the Holderian semi-metric that is associated with its regularity constants and , the near-optimality dimension of the function is defined as follows, (see Munos et al. (2014); Bubeck et al. (2011) for more details).

Definition 3.5.

The -near optimality dimension is the smallest such that for all , there exists such that the maximal number of disjoint -balls of radius with center in is less than .

In order to evaluate , we need to bound for all . The following proposition makes the link between the near optimality dimension and .

Proposition 3.6.

Let be the -near-optimality dimension, and the corresponding constant. Then

Finally, combining Propositions 3.4 and 3.6 with an hypothesis on the decreasing sequence , it is possible to provide the speed of convergence of .

Theorem 3.7.

Assume that for some and , and assume that . Thus with probability , the regret of StoOO is bounded as

where is the near optimality dimension and the corresponding near optimality constant.

If is the conditional expectation, a vector of safe constants is (based on Hoeffding’s inequality). Thus if we plug it into the quantity defined in Theorem 3.7 we obtain

that is equivalent to what it is obtained in Munos et al. (2014).

Remark: In the particular case where each cell is a hypercube and

the sub-regions are created by the division of the parent-cell into sub-regions of equal size, then , is equal to and is equal to .

4 Optimizing quantiles

In this section, we focus on the optimization of quantiles, which are well-established tools in (risk-averse) decision theory (see Rostek, 2010, for instance). In particular, they benefit from interesting robustness properties, with respect to outliers or heavy tails. Let

be the -quantile of , where is the cumulative distribution function (CDF) of . Here we detail how to construct the UCB and LCB for quantiles. First, we provide bounds based on Hoeffding’s inequality and we use them to adapt the regret bounds of Theorem 3.7. Then we provide two more refined bounds that take into account the order of the quantile based respectively on the Bernstein’s inequality and on the Kullback-Leibler divergence.

Let us first introduce some notations. For all , , and we denote

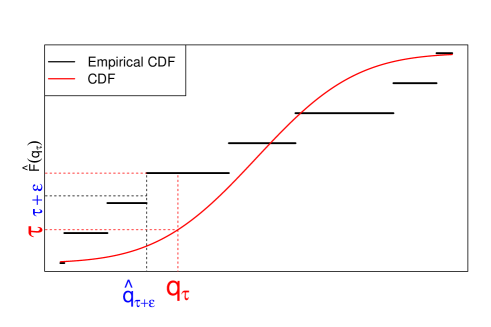

the empirical CDF of the reward inside the cell , where is the (random) number of times the cell was sampled up to time (see Definition 3.1). The generalized inverse of the piecewise constant function is defined as that is the order statistic of the sample that has been collected from the node until time .

To define confidence bounds on the conditional quantile we proceed in two steps. First we propose confidence bounds on . To do so, we simply use deviation bounds for Bernoulli distributions, since for all , for all , the random variables are independent and identically distributed with a Bernoulli law of parameter , if denotes the time when the node has been sampled for the -th time. Then we use the properties

| (4) | |||||

| (5) |

to create confidence bounds on using bounds on . Note that here we just assume that the output distribution has a continuous, striclty increasing cumulative distribution function. It is not necessary to assume something else, such as bounded support or bounded moments because here we refer to Bernouilli distributions. The first equivalence in illustrated on Figure 1.

|

4.1 Hoeffding’s bound and regret analysis

Let , and let

| (6) |

| (7) |

The next proposition motivates the choice of the above quantities as a UCB and a LCB for the quantile of order at the points .

Proposition 4.1.

Now, analyzing the regret requires a high probability bound on the number of time a node is sampled before being expanded:

Proposition 4.2.

According to the previous proposition, if we have sampled a node at depth more than

| (8) |

times, then with probability , Condition (2) is satisfied and thus the node is expanded.

Equality (8) reflects two dependencies. The smaller the minimum of the density over a neighborhood of the quantile and the closer from or , the larger the upper bound on the number of samples needed before being expanded. Indeed a small density value in a neighborhood of the targeted quantile will produce samples with few observations close to the quantile, hence the estimation error will be large. In addition from Proposition (4.1), to obtain non trivial UCB and LCB, the value has to be large enough to ensure and this value increases as comes close from or . Thus a more precise way to understand the behaviour of StoROO is that the number of time a node needs to be sampled before expansion depends on the pdf value in a neighborhood (of decreasing size with ) of the targeted quantile.

To obtain an upper bound on the simple regret, we now just need to combine Theorem 3.7 with Proposition 4.2 so as to obtain the following theorem.

Theorem 4.3.

Note that the speed of convergence is the same as the one obtained in the conditional expectation optimization setting; only the constant varies.

4.2 Tighter bounds

Using Hoeffding’s inequality is convenient because it leads to explicit lower and upper confidence bounds, which simplifies the deriviation of bounds on the regret. However, it implicitly upper-bounds the variance of all -valued random variables by , which is overly pessimistic when the inequality is applied to variables whose expectations are far from . This is in particular the case for quantile estimation, when the quantile is of order close to or . To take into account the order of the quantile, following David and Shimkin (2016), a first possibility is to derive confidence intervals from Bernstein’s inequality as presented in the following proposition.

Proposition 4.4.

For any , for all , and , define

and

with

If is the conditional quantile of order then the event has probability at least .

Although Bernstein’s inequality takes into account the order of the quantile, it is possible to do something better. In order to create tighter confidence bounds, we thus go back to Chernoff’s inequality and derive less explicit, but more accurate upper- and lower- confidence bounds on the -quantiles. We follow here Garivier and Cappé (2011), but a close inspection at the proofs shows however a difference in the order of the marginals of the KL functions. Recall that the binary relative entropy is defined for as:

with by convention, , and

Proposition 4.5.

For any , for all , and , define

Define

Then the event has probability at least .

Contrary to Bernstein’s inequality, Chernoff’s bound is always tighter than Hoeffding’s inequality, which follows from Pinsker’s inequality (see e.g. Garivier et al., 2018). It follows in particular that the regret of StoROO using confidence bounds derived from Chernoff’s inequality has, at least, the guarantees presented in Theorem 4.3.

The online setting we consider in this article induces that, after steps, the set of nodes and the number of observations in each node are random. To cope with this, we thus need deviation bounds for random size samples. The most simple way to obtain such inequalities is to use a union bound on the possible number of observations in each node, as presented above. Tighter results can be obtained from a more thorough analysis (sometimes called peeling trick): this is what is presented below.

Proposition 4.6.

For any let , and define

Define

Then the event has probability at least .

Note that for every , and thus ; hence, .

5 Optimizing CVaR

We now detail how StoROO can be applied to the optimization of another important notion of risk: the CVaR. CVaR has raised a great interest in recent years, notably because it is a coherent risk indicator (see Ben-Tal and Teboulle (2007) for instance). For the condition value at risk at level of a continuous random variable is defined as

with . Following Brown (2007), it can be estimated by

Since often stands for a loss, the CVaR is usually to be minimized. In order to stay consistent with the rest of the paper, we choose in the following to maximizing .

Assuming the random variables are bounded in an interval , the next proposition adapts the deviation inequalities presented in Brown (2007) to our sequential setting.

Proposition 5.1.

For any , for all , for all and for all , define

with

where represents the value of for the node . If the random variables are bounded in for all and have continuous distribution functions, then the event has probability at least .

Note that deviation inequalities can be established for CVaR in sub-Gaussian or light-tailed cases (see Kolla et al. (2019) for instance) but an assumption has to be made on the value of the pdf in a neighborhood of the -quantile.

From Proposition (5.1), one can see that whenever a node has been played more than times, it has been expanded. Thus a possible associated vector of safe constants is Combining with Theorem 3.7 provides the following upper bound on the regret.

Theorem 5.2.

Under the conditions required by Proposition 5.1, if for some and , then with probability , the regret of StoROO for minimizing is bounded as

with the near-optimality dimension and the near-optimality corresponding constant.

The inequalities obtained in Proposition 5.1 are convenient because they lead to explicit lower and upper confidence bounds, which simplifies the derivation of bounds on the regret. However, as they are based on Hoeffding’s inequality, they can be over-conservative. To obtain better bounds, Thomas and Learned-Miller (2019) propose data-dependent inequalities derived from the Dvoretzky-Kiefer-Wolfowitz inequality. The following proposition provides the UCB and LCB based on these inequalities.

Proposition 5.3.

Assume for all , is bounded by . For any , for all , and , define

and

with and . Then if , the event has probability at least .

Although we do not propose an analysis of the regret based on this bounds, it is immediate to state that the upper bound on the regret is always smaller than the bound obtained in Theorem 5.2 because these inequalities are strictly tighter than Brown’s inequalities. In the following section, we numerically highlight the relevance of using these tight bounds.

6 Experiments

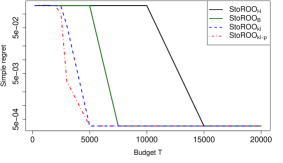

We empirically highlight the capacity of StoROO to optimize the conditional quantile and CVaR of a black-box function. Four versions of StoROO are compared for both cases.

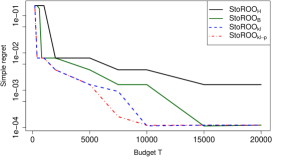

For the conditional quantile we compare StoROO using confidence bounds repectively derived from Hoeffding’s, Bernstein’s, Chernoff’s inequalities (resp. denoted , and ) and Chernoff’s inequality and the peeling trick ().

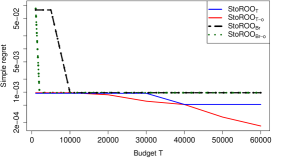

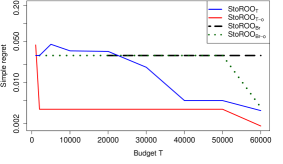

For the optimization of the conditional CVaR, we compare the use of confidence bounds derived from Brown’s inequality and from Thomas and Learned-Miller (2019). To use these inequalities we have to provide that bound the output. Hence, we compare two cases: one where we provide conservative bounds for (here ), and one where we provide their actual values ( and , the minimum and the maximum of the support of the conditional distribution). We denote the four variants (from Brown’s inequality), (from Thomas and Learned-Miller (2019)), and and for their variants with oracle bounds.

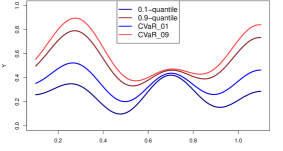

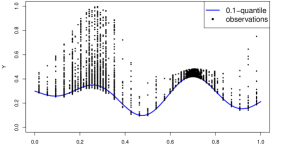

As a test-case, we chose two functions with heteroscedastic noise and local extrema. The first is where is a log-normal random variable of parameters and truncated at its -quantile (the truncated mass is uniformly reallozcated between and ). Note that to initialise StoROO not too close from a global optimum, we optimize the quantiles of on and the CVaR on . Figure 2 (left) shows the shape of the and -quantiles and -CVaR of , while Figure 2 (right) shows samples of the -quantile. The second test-case is , on with

and a random variable that follows a Cauchy distribution of parameters . Note that for all , is unbounded and it has unbounded moments. Thus we can only apply quantile optimization on based on the strategies developed in the past sections. Figure 3 (left) shows the shape of the -quantile of . The performance of each version of StoROO is evaluated for different values of and quantified according to the simple regret. In our experiments we fix the values and (resp. , and , ) for the optimization of the quantiles (resp. the CVaR of order and ) of and and for the optimization of the -quantile of . Note that these values underestimate the regularity conditions at optimum so that satisfying the condition (1). In addition we fix and we choose to expand the nodes into sub-region of equal sizes.

|

|

|

|

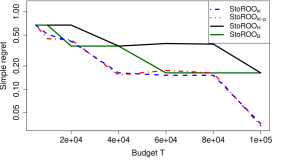

Figure 2 and 3 report the average of the simple regret over runs. For both values of all the variants of StoROO have a regret that decreases with the budget. However from our experiments a ranking can be created. For the optimization of the quantile let us firt remark that as bounds are known for , for this test case we modified Proposition (4.1-4.5-4.6) by replacing ) by . The less efficient method is . For its simple regret decreases slower than the three others methods and for does not reach the performance of the others variants. To reach a fixed accuracy, sometimes needs a much larger budget than others variants. For example, on , taking , needs a budget of to reach a simple regret of order , while and need a budget equal to . Second-to-last is . Using the maximal budget, on both experiments on , this variant reaches the same accuracy as and but its simple regret decreases slower. For some levels of performance needs a much larger budget than . For example, taking , to reach the value needs a budget of while is enough for . Finally, the most efficient methods are clearly and . The use of a peeling argument (instead of a plain union bound) in provides some additional gain over on but the effect is negligible on .

For the optimization of the CVaR, the variant based on tighter bounds is almost always better than the other and it is independent of the use of oracle bounds. The use of oracle bounds always improves the performance of StoROO and this effect is stronger if the confidence intervals are created with the inequalities of Thomas and Learned-Miller (2019). Of course, in a real problem the oracle bounds are not known. Nevertheless this result motivates the use of estimators of the minimum and the maximum to estimate the conditional support so that to accelerate convergence.

7 Conclusion

In this work, we extended StoOO to a generic algorithm applicable to any functional of the reward distribution. We proposed a tailored application to the problem of quantile optimization, with four variants: one based on the classical Hoeffding’s inequality, one based on Bernstein’s inequality, and two others based on Chernoff’s inequality. We showed that using Chernoff’s inequality to build confidence intervals resulted in a dramatic improvement, both in theory and practice. We also illustrated the ability of StoROO to optimize the CVaR and compared numerically four variants.

For simplicity, we assumed that the local regularity (or at least, an upper bound) of the target function at the optimum was known to the user. However, we believe that it might be possible to combine our results to the procedure defined in Grill et al. (2015); Xuedong et al. (2019) so as to propose an algorithm able to optimize without the knowledge of the smoothness near an optimal point: this is left for future work. A second possible extension is to leverage the results proposed here to design an algorithm for the cumulative regret, in the spirit of HOO Bubeck et al. (2011) for example.

We would like to thank Sébastien Gerchinovitz for the discussions and his useful comments.

References

- Artzner et al. (1999) Philippe Artzner, Freddy Delbaen, Jean-Marc Eber, and David Heath. Coherent measures of risk. Mathematical finance, 9(3):203–228, 1999.

- Audibert et al. (2009) Jean-Yves Audibert, Rémi Munos, and Csaba Szepesvári. Exploration-exploitation tradeoff using variance estimates in multi-armed bandits. Theoretical Computer Science, 410(19):1876–1902, 2009.

- Bartlett et al. (2018) Peter L Bartlett, Victor Gabillon, and Michal Valko. A simple parameter-free and adaptive approach to optimization under a minimal local smoothness assumption. arXiv preprint arXiv:1810.00997, 2018.

- Bellini and Di Bernardino (2017) Fabio Bellini and Elena Di Bernardino. Risk management with expectiles. The European Journal of Finance, 23(6):487–506, 2017.

- Ben-Tal and Teboulle (2007) Aharon Ben-Tal and Marc Teboulle. An Old-New Concept of Convex Risk Measures: The Optimized Certainty Equivalent. Mathematical Finance, 17(3):449–476, 2007.

- Bouttier (2017) Clément Bouttier. Optimisation globale sous incertitudes: algorithmes stochastiques et bandits continus avec application à la planification de trajectoires d’avions. 2017.

- Brown (2007) David B Brown. Large deviations bounds for estimating conditional value-at-risk. Operations Research Letters, 35(6):722–730, 2007.

- Bubeck et al. (2011) Sébastien Bubeck, Rémi Munos, Gilles Stoltz, and Csaba Szepesvári. X-armed bandits. Journal of Machine Learning Research, 12(May):1655–1695, 2011.

- David and Shimkin (2016) Yahel David and Nahum Shimkin. Pure exploration for max-quantile bandits. In Joint European Conference on Machine Learning and Knowledge Discovery in Databases, pages 556–571. Springer, 2016.

- Galichet et al. (2013) Nicolas Galichet, Michele Sebag, and Olivier Teytaud. Exploration vs exploitation vs safety: Risk-aware multi-armed bandits. In Asian Conference on Machine Learning, pages 245–260, 2013.

- Garivier and Cappé (2011) Aurélien Garivier and Olivier Cappé. The KL-UCB algorithm for bounded stochastic bandits and beyond. In Proceedings of the 24th annual conference on learning theory, pages 359–376, 2011.

- Garivier et al. (2018) Aurélien Garivier, Pierre Ménard, and Gilles Stoltz. Explore first, exploit next: The true shape of regret in bandit problems. Mathematics of Operations Research, 2018.

- Grill et al. (2015) Jean-Bastien Grill, Michal Valko, and Rémi Munos. Black-box optimization of noisy functions with unknown smoothness. In Advances in Neural Information Processing Systems, pages 667–675, 2015.

- Hepworth (2017) Adam J Hepworth. A multi-armed bandit approach to superquantile selection. PhD thesis, Monterey, California: Naval Postgraduate School, 2017.

- Kleinberg et al. (2008) Robert Kleinberg, Aleksandrs Slivkins, and Eli Upfal. Multi-armed bandits in metric spaces. In Proceedings of the fortieth annual ACM symposium on Theory of computing, pages 681–690. ACM, 2008.

- Kolla et al. (2019) Ravi Kumar Kolla, Krishna Jagannathan, et al. Risk-aware Multi-armed Bandits Using Conditional Value-at-Risk. arXiv preprint arXiv:1901.00997, 2019.

- Locatelli and Carpentier (2018) Andrea Locatelli and Alexandra Carpentier. Adaptivity to Smoothness in X-armed bandits. In Conference on Learning Theory, pages 1463–1492, 2018.

- Munos et al. (2014) Rémi Munos et al. From bandits to Monte-Carlo Tree Search: The optimistic principle applied to optimization and planning. Foundations and Trends® in Machine Learning, 7(1):1–129, 2014.

- Rockafellar et al. (2000) R Tyrrell Rockafellar, Stanislav Uryasev, et al. Optimization of conditional value-at-risk. Journal of risk, 2:21–42, 2000.

- Rostek (2010) Marzena Rostek. Quantile maximization in decision theory. The Review of Economic Studies, 77(1):339–371, 2010.

- Sani et al. (2012) Amir Sani, Alessandro Lazaric, and Rémi Munos. Risk-aversion in multi-armed bandits. In Advances in Neural Information Processing Systems, pages 3275–3283, 2012.

- Shahriari et al. (2016) Bobak Shahriari, Kevin Swersky, Ziyu Wang, Ryan P Adams, and Nando De Freitas. Taking the human out of the loop: A review of bayesian optimization. Proceedings of the IEEE, 104(1):148–175, 2016.

- Szorenyi et al. (2015) Balazs Szorenyi, Róbert Busa-Fekete, Paul Weng, and Eyke Hüllermeier. Qualitative multi-armed bandits: A quantile-based approach. In 32nd International Conference on Machine Learning, pages 1660–1668, 2015.

- Thomas and Learned-Miller (2019) Philip Thomas and Erik Learned-Miller. Concentration Inequalities for Conditional Value at Risk. In International Conference on Machine Learning, pages 6225–6233, 2019.

- Valko et al. (2013) Michal Valko, Alexandra Carpentier, and Rémi Munos. Stochastic simultaneous optimistic optimization. In International Conference on Machine Learning, pages 19–27, 2013.

- Xuedong et al. (2019) Shang Xuedong, Emilie Kaufmann, and Michal Valko. General parallel optimization a without metric. In Algorithmic Learning Theory, pages 762–787, 2019.

Appendix A Appendix

A.1 Details about the regularity hypothesis

In the classical setting the Optimized Certainty Equivalent is defined as

with a concave function. Here we assume is concave and -lipschitzian (). Let us consider two random variables and , then

Using the Kantorovich-Rubinstein representation one obtains

with the Wasserstein distance associated with . Thus if , then a sufficient condition to satisfied (1) is , for all .

To treat the case of the , we use the fact that if then we have the equality .

In the case of the conditional expectation the same kind of condition can be sufficient. Indeed we have

A.2 Proofs related to the generic analysis of StoROO

Proof of Proposition 3.2

Let us define the partition containing . Assume that the partition has been selected, thus

By definition , thus . Conditionally on , that implies

Note that the last inequality is obtained because the partition is expanded, which implies that

Finally:

thus belongs to .

Proof of Proposition 3.3

Thus so There is at least an expanded node of depth after a budget was used.

Proof of Proposition 3.4

Proposition 3.2 implies that the center of an expanded partition is in . Proposition 3.3 implies that a partition of depth at least has been expanded. Thus StoROO has expanded a node in . At the end of the budget StoROO returns the node having the highest LCB among the nodes that have been expanded and not the deepest node among those that have been expanded. But

That ensure the node having the highest LCB has the same theoretical regret as the node of maximal depth among those that have been expanded.

Proof of Proposition 3.6

According to the assumption , each cell contains a ball of radius centered in that is a -ball of radius centered in . If is the near optimality dimension then there is at most disjoint - balls of radius inside . Thus if this implies there is more than disjoint balls of radius with center in , that is a contradiction.

A.3 Proofs related to the section Optimizing quantiles

Proof of Proposition 4.1

Let us consider the event

Define the number of nodes expanded throughout the algorithm, define for , as the time when the cell has been selected for the -th time and define the reward obtained at that time at the point . Then one can write

Using this notation, we have:

By Hoeffding’s inequality, if

we obtain

Now using Equation (4) we can express this inequality directly in terms of quantiles:

Using the same scheme of proof with Inequality (5), we obtain:

and hence

Proof of Proposition 4.2

Without loss of generality let us assume . Assume the node has been sampled times, with

thus

That implies

and in particular

Then define the event

with

Using equivalences (4) and (5), one can write:

Thus

| Using the same notation as in the proof of Proposition 4.1, one can write | |||

Now by applying the Massart’s inequality to bound

one obtain . Thus with probability , we have:

| (9) |

Assuming that is differentiable in , by the mean value theorem, we deduce

Next, using (9) it is possible to write that with probability :

We define as the smallest such that

that is

A proper has to verify

To satisfy this constraint we define

To conclude the whole proof, since , we obtain .

Proof of Proposition 4.4

Let be random variables bounded by the interval . Define . For the Bernstein’s inequality gives

Let us consider the event

Using the same lines as in the proof of Proposition 4.1 we have

| then applying the Bernstein’s inequality we obtain | ||||

| (10) |

By now the goal is to find such that

Finding such can be easily done because it is a square of a second order polynomial. The result is

Plugging the value of inside (10) concludes the proof.

Proof of Proposition 4.5

Step 1: bounds on for a i.i.d sample

Let be random variables bounded by the interval . Define . For the Chernoff’s inequality gives

Let be the value such that , then for all :

Now let us define the candidate for the UCB of a i.i.d sample:

and let us remark that

| (11) |

thus

For let us introduce

one proves in the same way

Step 2: Double union bound

Let us consider the event

Following the notation of the proof of Proposition 4.1 we have

Using the equivalence (11), the probability can be reformulated as

Now using Chernoff’s inequality we obtain

By equivalence (4) this implies that, , with probability at least , Using the same lines one can show

By equivalence (5) this implies that, , with probability at least . Putting this two probabilities together prove the result.

Proof of Proposition 4.6

Define

Step 1: Martingale For every , let . Let and for ,

is a martingale relative to . In fact,

That is equivalent to

Step 2: Peeling Let us devide the interval into slices of geometric increasing size. We may assume that , since otherwise the bound is trivial. Take , let and for all , let .

Define the number of nodes expanded throughout the algorithm, thus for , it is possible to rewrite the last probability as

with

Observe that if and only if and

Define , let be the smallest integer such that ; if , then thus . Thus for all such that , we obtain . For such that , let Let be such that and let , so that Consider such that and .

Observe that

-

•

if , then

-

•

if , then as

it holds that:

Hence on the event it holds that

Step 3: Putting everything together

As is a martingale, . Thus the Doob’s inequality for martingales provides:

Finally

But as , and as long as

we obtain:

Using the same lines for the LCB concludes the proof.

A.4 Proofs related to the section Optimizing CVaR

Proof of Proposition 5.1

Let us consider the event

| (12) | ||||

| (13) |

First let us consider (12):

Thus by Brown’s inequality

Taking

provides the first part, (12).

We use the same scheme of proof to bound (13), the only difference comes from the fact that the inequality of deviation is different:

By Brown’s inequality

Taking

provides (13) .

Proof of Proposition 5.3 If are i.i.d random variables bounded by then Thomas-Learned-Miller’s inequalities provide

and

Define

and

To treat the sequential point of view, here we use a double union bound as it is done in the proof of Proposition 13, then it can be shown that

Thus by defining

we obtain

Using the same scheme of proof with

provides

Finally

and hence .