Predicting success in the worldwide start-up network

By drawing on large-scale online data we construct and analyze the time-varying worldwide network of professional relationships among start-ups. The nodes of this network represent companies, while the links model the flow of employees and the associated transfer of know-how across companies. We use network centrality measures to assess, at an early stage, the likelihood of the long-term positive performance of a start-up, showing that the start-up network has predictive power and provides valuable recommendations doubling the current state of the art performance of venture funds. Our network-based approach not only offers an effective alternative to the labour-intensive screening processes of venture capital firms, but can also enable entrepreneurs and policy-makers to conduct a more objective assessment of the long-term potentials of innovation ecosystems and to target interventions accordingly.

Recent years have witnessed an unprecedented growth of interest in start-up companies. Policy-makers have been keen to sustain young entrepreneurs’ innovative efforts with a view to injecting new driving forces into the economy and foster job creation and technological advancements (?, ?, ?, ?). Investors have been lured by the opportunity of disproportionally high returns typically associated with radical new developments and technological discontinuities. Large corporations have relied on various forms of external collaborations with newly established firms to outsource innovation processes and stay abreast of technological breakthroughs (?). Undoubtedly, knowledge-intensive ventures such as start-ups can have a large positive impact on the economy and society. Yet they typically suffer from a liability of newness (?), and cannot avoid the uncertainties and sunk costs resulting from disruptive product developments, uncharted markets and rapidly changing technological regimes (?). For these reasons, their long-term benefits are inherently difficult to predict, and their economic net present value cannot be unambiguously assessed (?).

Indeed traditional models of business evaluation, based on historical trends of data (e.g., on sales, production capacity, internal growth, and markets size) are mostly inapplicable to start-ups, chiefly because their limited history does not provide sufficient data. Venture capitalists and private investors often evaluate start-ups primarily based on the qualifications and dexterity of the entrepreneurs, on their potential to create new markets or niches and to unleash the “gales of creative destruction” (?). The process of screening and evaluating companies in their early stages is therefore a subjective and labor-intensive task, and is inevitably fraught with biases and uncertainty.

To overcoming these limitation, we propose a novel and data-driven framework for assessing the long-term economic potential of newly established start-ups. Our study draws upon the construction and analysis of the worldwide network of professional relationships among start-ups. Such network provides the backbone and the channels through which knowledge can be gained, transferred, shared, and recombined. For instance, skilled employees moving across firms in search of novel opportunities can bring with them know-how on cutting-edge technologies, advisors who gained experience in one firm can help identify the most effective strategies in another, whilst well connected investors, lenders and board members can rely on the knowledge gained in one firm to tap business and funding opportunities in another.

Previous work has investigated how knowledge transfer impacts upon the performance of start-ups; yet information flows have been simply inferred mainly through data on patents (?), interorganizational collaborations (?), co-location of firms and their proximity to universities (?). Other studies have analyzed social networks (e.g., inventor collaboration networks, interlocking directorates) to unveil the microscopic level of interactions among individuals; yet their scope has been limited mostly to specific industries or small geographic areas, and to a fairly small observation period (?, ?, ?). Owing to lack of data, what still remains to be studied is the global network underpinning knowledge exchange in the worldwide innovation ecosystem. Equally, the competitive advantage of differential information-rich network positions and their role in opening up, expediting, or obstructing pathways to firms’ long-term success have been left largely unexplored.

The world-wide network of start-ups.

Here we study the complex time-varying network (?, ?) of interactions among all start-ups in the worldwide

innovation ecosystem over a period of 26 years (1990-2015). To this end,

we collected all data on firms and people (i.e., founders, employees,

advisors, investors, and board members) available from the

www.crunchbase.com website. Drawing on the data, we

first constructed a bipartite graph in which people

are connected to start-ups according to their professional role. We

then obtained the projected one-mode time-varying graph in which

start-ups are the nodes and two companies are connected when they

share at least one individual that plays or has played a professional

role in both companies (see Supplementary Material (SM) for details).

At the micro scale, employees working in a

company can perceive the intrinsic value of new appealing

opportunities and switch companies accordingly. This mobility

creates an intel flow between companies, where those receiving

employees increase their fitness by capitalizing on the know-how the

employee is bringing with her. Such microscopic dynamics is thus

captured and modelled by the creation of new edges at the level of the

network of start-ups. As a consequence, companies which are perceived

at the micro scale as

appealing opportunities by mobile employees will likely boost their

connectivity and therefore will acquire a more central position in

the overall time-varying network.

The resulting time-varying

World Wide Start-up (WWS) network comprises

companies distributed across countries around the

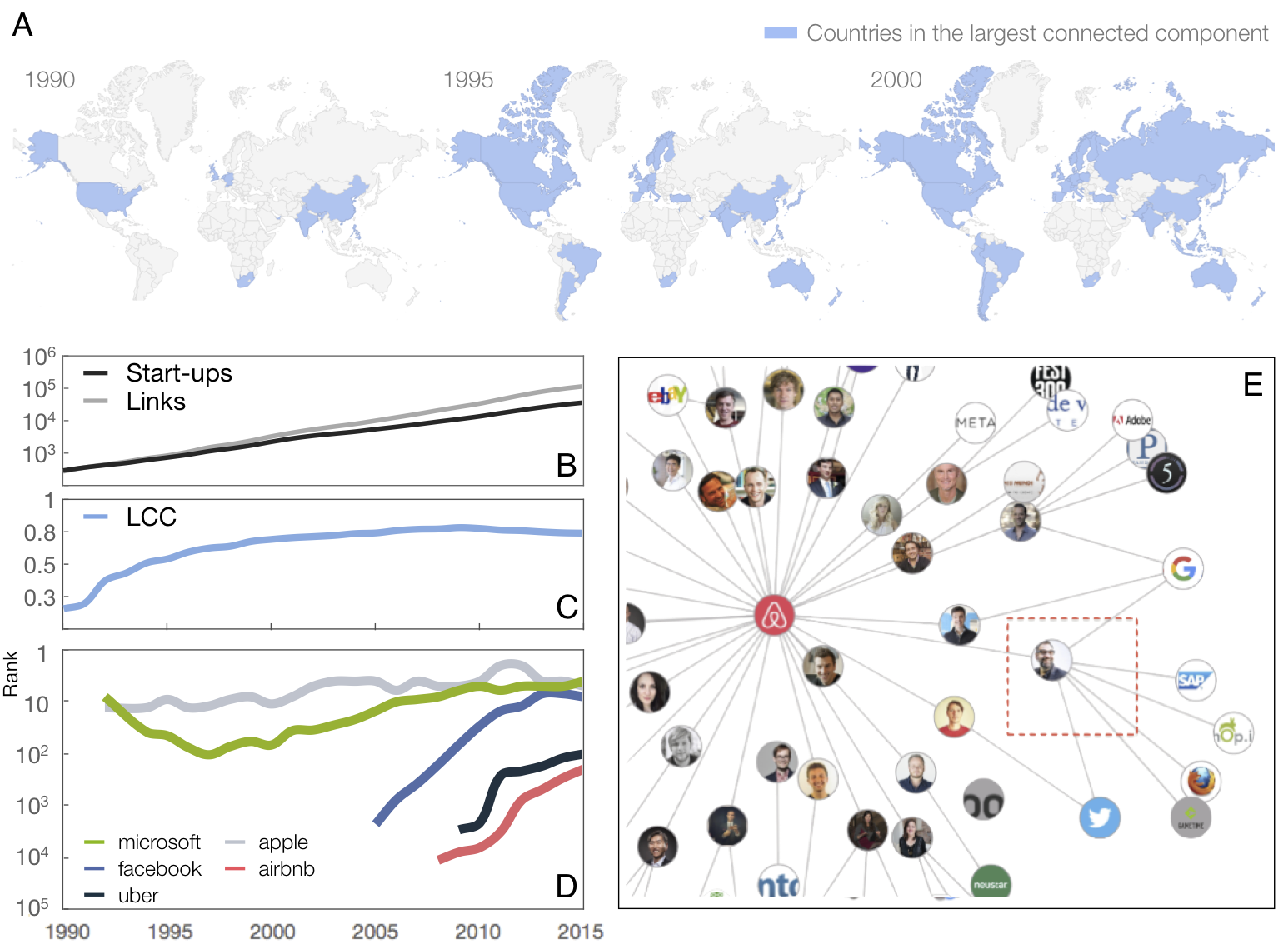

globe, and links among them (see Fig S3 and S4 in the

SM). Fig 1A highlights the countries in which start-ups have joined,

over time, the largest connected component of the network

(?, ?). Fig 1B indicates that the number of

nodes and links in the WWS network has grown exponentially over the

last 26 years.

In the same period, various communities of start-ups

around the globe have joined together to form the largest connected

component including about of the nodes of the network (Fig

1C). Currently, an average of 4,74 “degrees of separation” between

any two companies characterizes the WWS network.

At the micro scale, Fig 1E shows a snapshot of the network of interactions between Airbnb and other companies based on shared individuals. As an illustration, in 2013 Airbnb hired Mr Thomas Arend (highlighted in the red square), who had previously acted as a senior product manager in Google, as an international product leader in Twitter, and as a product manager in Mozilla. As previously pointed out, the professional network thus reveals the potential flow of knowledge between Airbnb and the three other companies in which Mr Arend had played a role. Moreover, as new links were forged over time, the topological distances from Airbnb to all other firms in the WWS network were reduced, which in turn enabled Airbnb to gain new knowledge and tap business opportunities beyond its immediate local neighborhood.

The mechanistic interpretation of employees’ mobility inducing link creation discussed above and illustrated in Fig 1E suggests that the potential exposure to knowledge of a start-up in the WWS network, and its subsequent likelihood to excel in the future, should be well captured by its network centrality over time. To test this hypothesis we have considered different measures of node centrality (?). For parsimony here we focus on the results obtained by closeness centrality as it assesses the centrality of a node in the network from its average distance from all the other nodes, although similar results has also been found by some other centrality measures, such as betweenness or degree (see SM). In each month of the observation period, we ranked companies according to their values of closeness centrality (i.e., top nodes are firms with the highest closeness). Fig 1D is an example of the large variety of observed trajectories as companies moved towards higher or lower ranks, i.e., they obtained a larger or smaller proximity to all other companies in the network. Notice that Apple has always been in the Top 10 firms over the entire period, while Microsoft exhibited an initial decline followed by a constant rise towards the central region of the network. The trajectories of once upon a time younger start-ups, such as Facebook, Airbnb, and Uber, are instead characterized by an abrupt and swift move to the highest positions of the ranking soon after their foundation, possibly as a result of the boost in activity that has characterized the venture capital industry in recent years.

Early-stage prediction of high performance.

To investigate the interplay

between the position of a given firm in the WWS network and its

long-term economic performance, from www.crunchbase.com we

collected additional data on funding rounds, acquisitions, and initial

public offerings (IPOs). For each month , we obtained the list of

firms, ranked in terms of closeness, that can be classified as

“open deals” for investors, namely: (i) they have not yet received

funding; (ii) they have not yet been acquired; and (iii) they have not

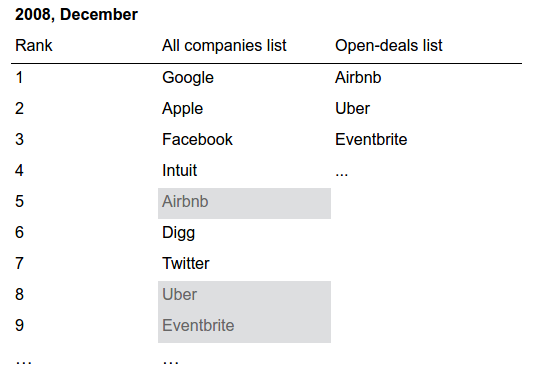

yet been listed in the stock exchange market (see Fig S5 in SM). As an

example, the company WhatsApp, which ranked 1,060th in June

2009 in the full list, occupied the 15th position in the

open-deals list in the same month. Notice that, by assessing a firm’s

network position prior to any financial acquisition or IPO, our

analysis is not subject to possible biases arising from the effects

that the capital market might have upon the firm’s expected

performance.

Furthermore, predicting the long-term economic

performance of firms in the open-deal list is arguably a challenging

task, as illustrated by the fact that the average success of

venture funds early-stage investments in similar open deals is only around

10-15% (see section S4.2 in SM).

Over the range of 26 years of the dataset, a total of different start-ups were identified as open-deals.

Our recommendation method is based on the hypothesis

that start-ups with higher values of closeness centrality at an early stage

are more likely to show signs of positive long-term economic performance.

Accordingly, we counted the total

number of firms inside the open-deal list that, within a time

window years starting at month , succeeded in

securing at least one of the following positive outcomes: (i) they

took over one or more firms; (ii) they were acquired by one or more

firms; or (iii) they underwent an IPO. To assess the accuracy of our

recommendation method in early identifying successful companies, we checked

how many of the Top companies in the closeness-based ranking of

open-deals obtained a positive outcome (see Fig S6 in SM).

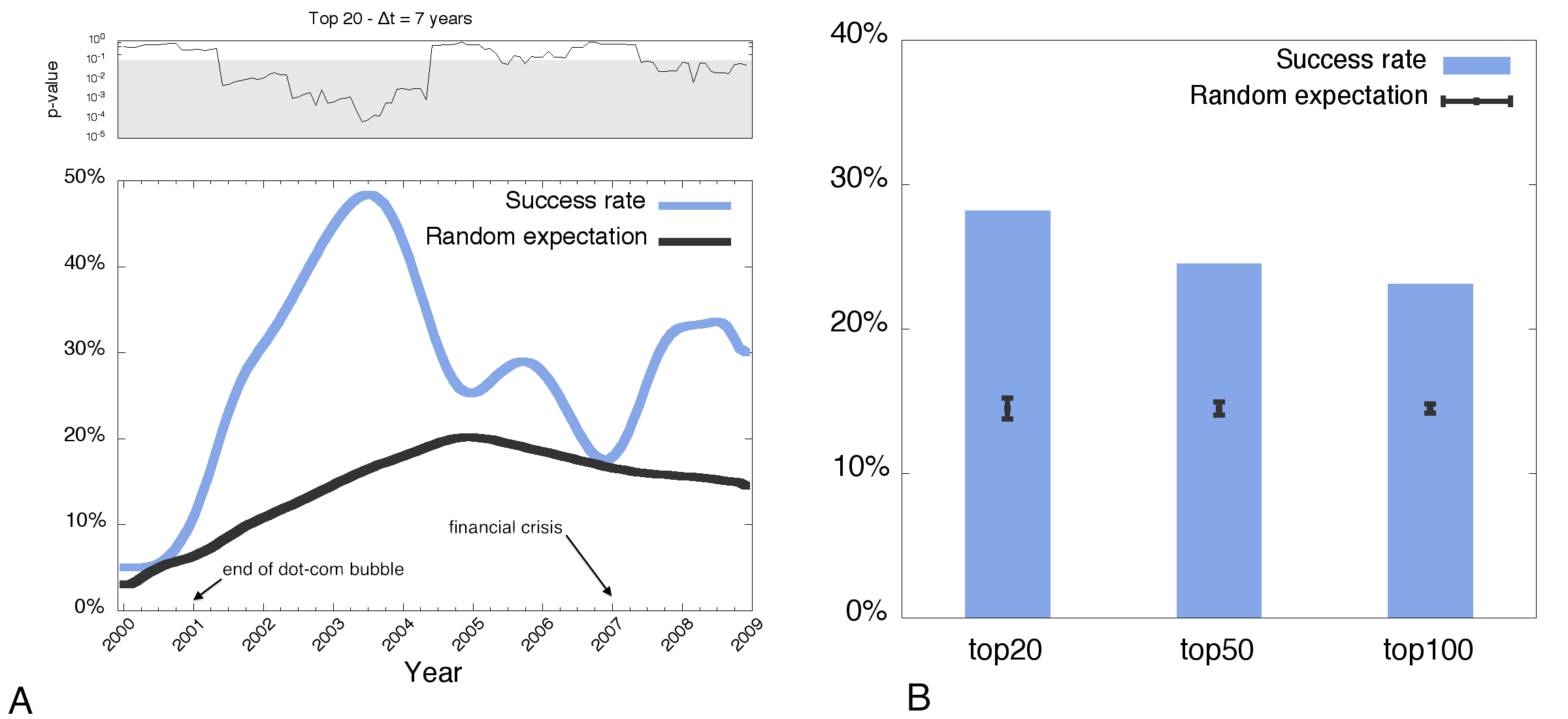

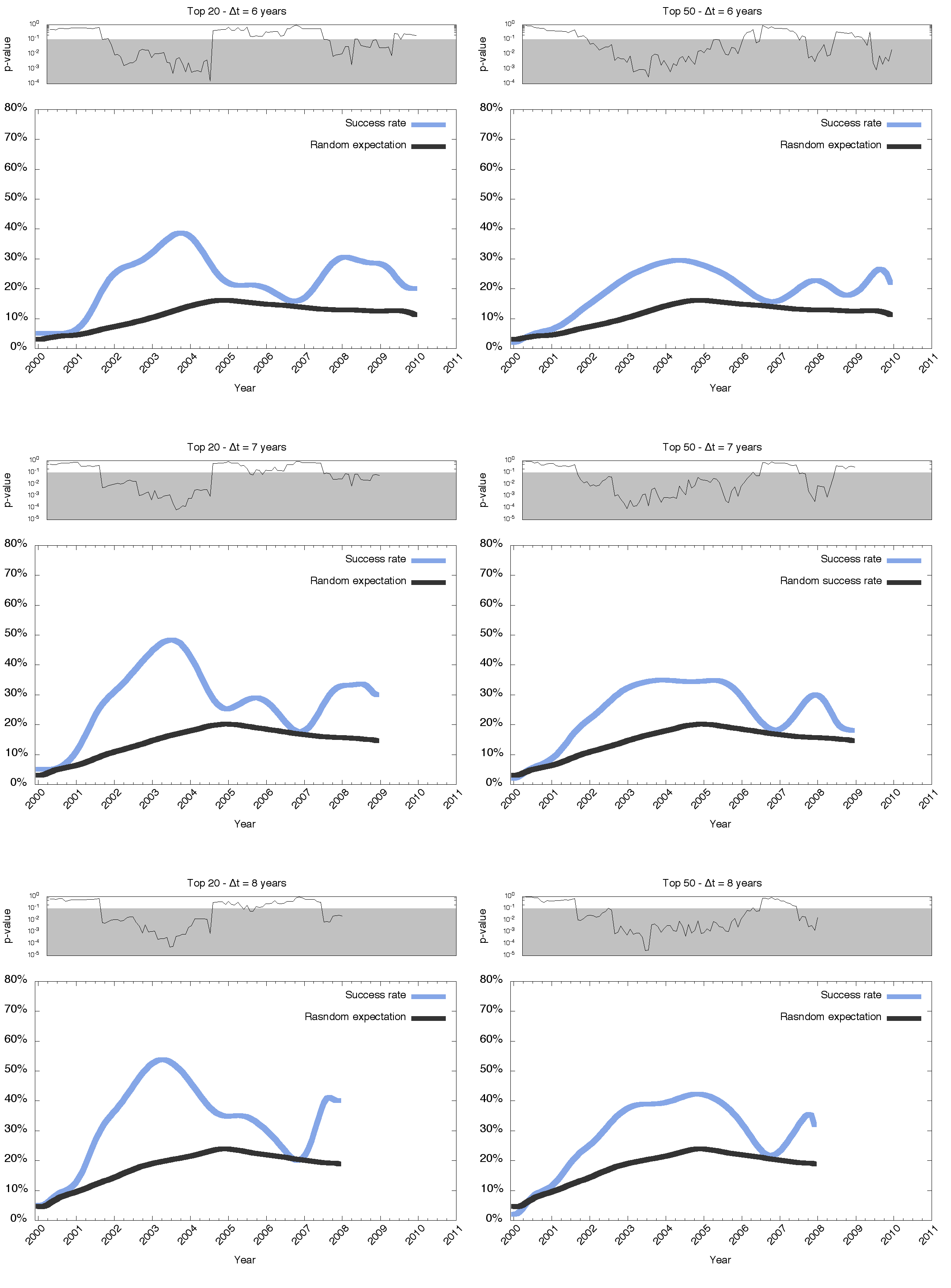

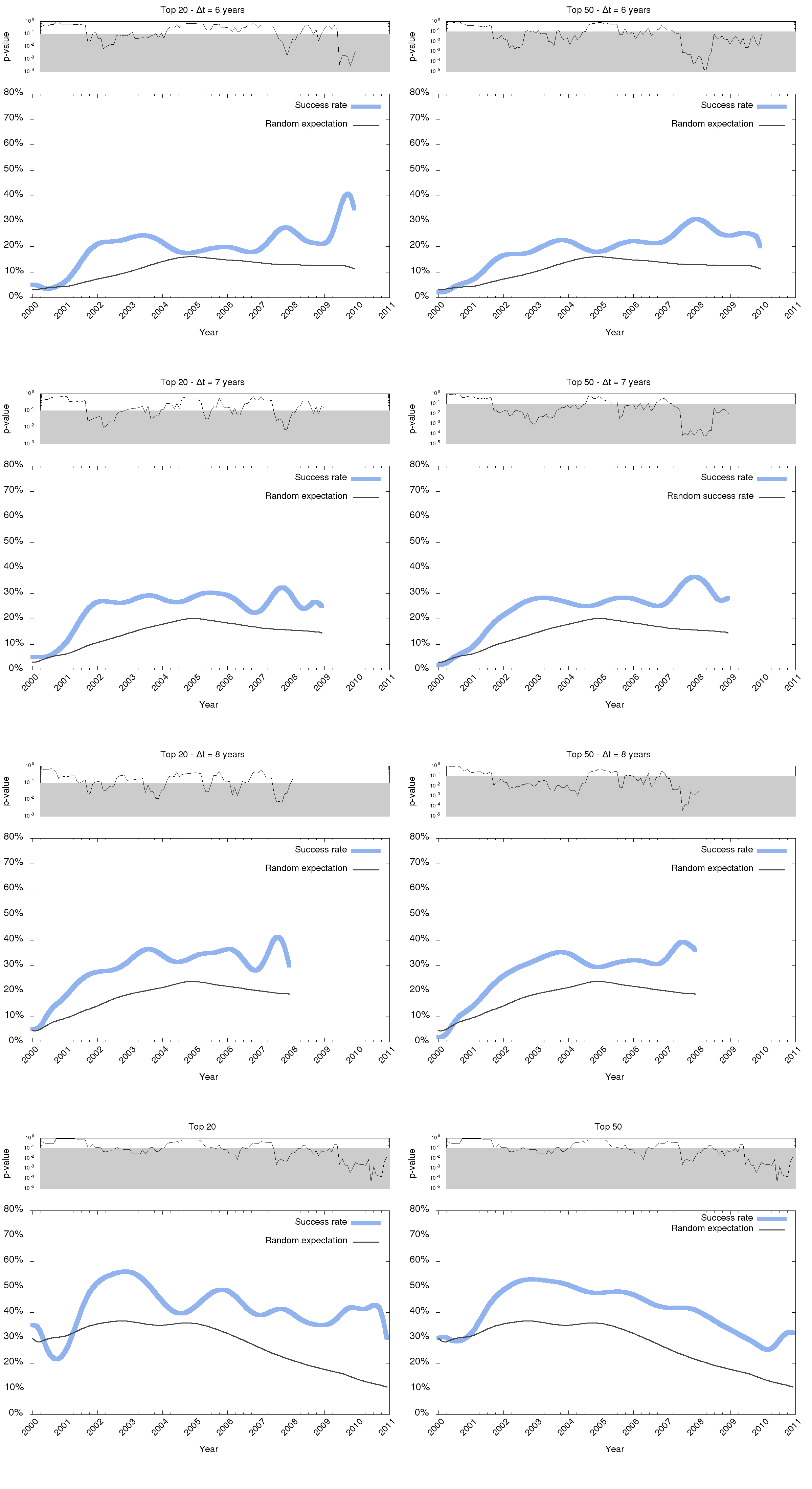

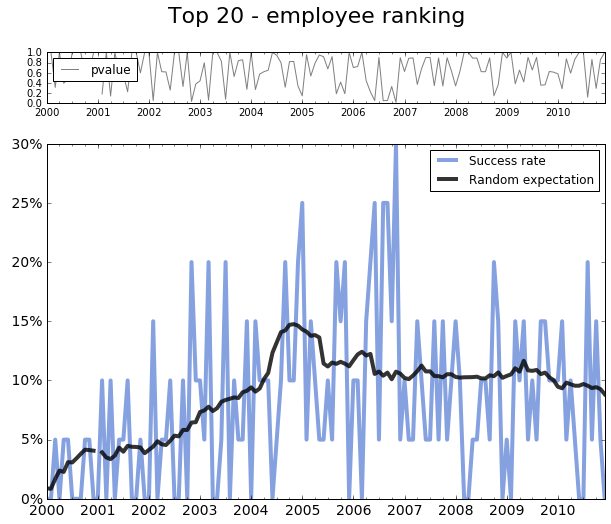

Fig 2A reports the “success rate” (blue curve) of the

recommendation method, defined as , where is the

number of firms with a positive outcome included in the Top

firms, and (black curve) is the success

rate expected in the case of random ordering of companies, i.e.

the expected success of a null model of random sampling without replacement which complies with a hypergeometric distribution (see SM section 4 for details).

The -value in the top panel of Fig 2A measures the probability of

obtaining, by chance, a success rate larger than , with low

values of (highlighted regions) indicating the time periods where

the prediction is statistically significant (-value ). From

mid 2001 to mid 2004, the success rate of our

recommendation method (blue curve) is remarkably

larger than the one based on random expectations (black curve), and

the -value is always smaller than 0.01. exhibits an

exceptional peak of in June 2003 (-value = 0.0001). From

2004 to 2007, the blue curve decreases, reaching a local minimum at a

time when a global financial crisis was triggered by the US housing

bubble. In this period (as well as during the collapse of the dot-com

bubble in 1999-2001), even though the success rate still exceeds

random expectations, the high -values indicate that the predictions

are not statistically significant. Finally, after mid 2007, the

performance of the prediction increases, and it stabilizes around

(-value = 0.01). For completeness, Fig S7 in SM reports

results based on different lengths of the recommendation list and on

different time windows. The observed dependence of

the performance of our network-based recommendation method on the level

of external financial market stress should be studied in more depth.

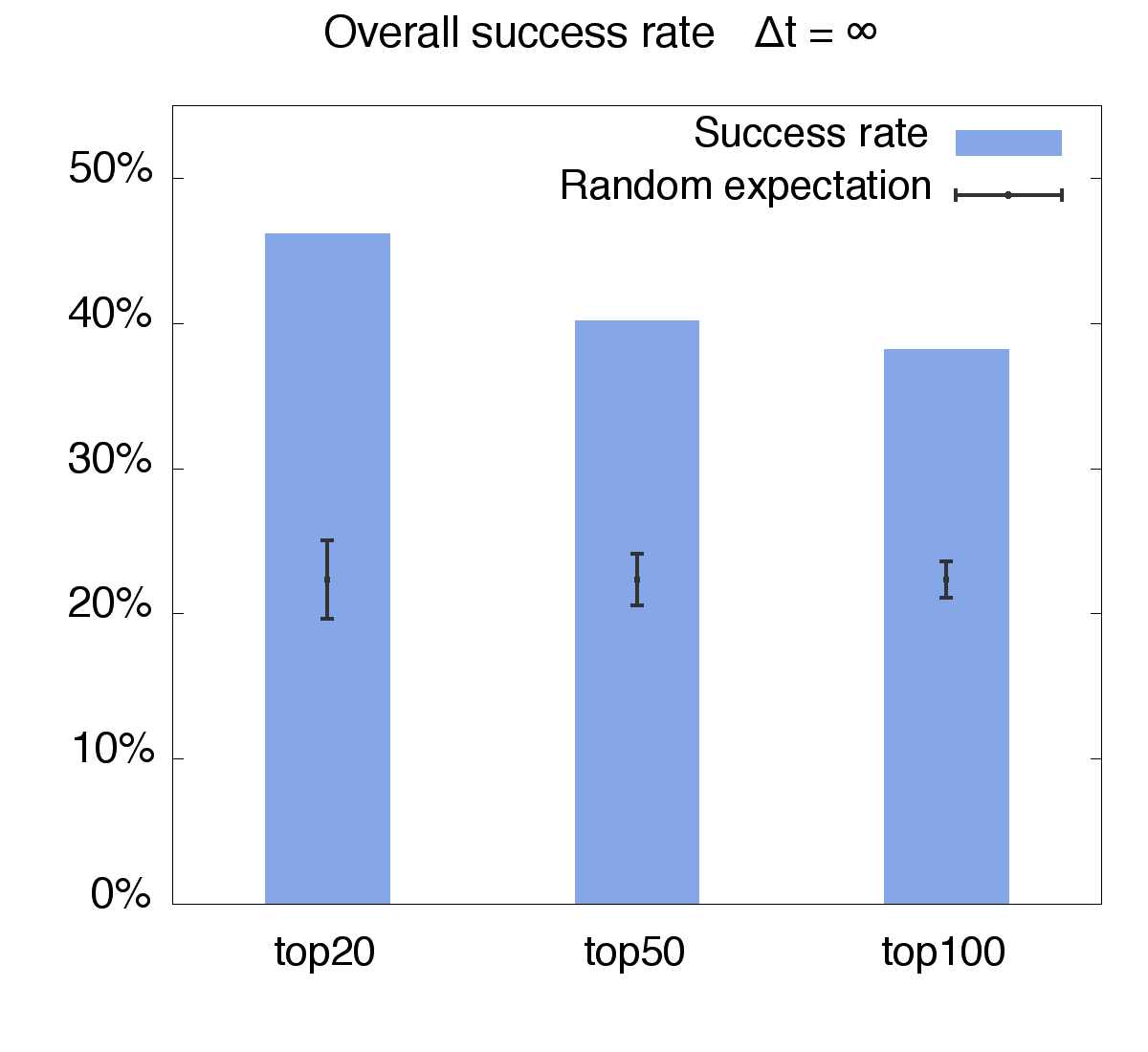

In Fig 2B, we characterize the overall performance of the

recommendation method over the entire period of observation. Results

indicate that about of the firms appearing in the Top 20 in any

month from 2000 to 2009 have indeed achieved a positive economic outcome within 7 years since the time of our recommendation. The black error

bars indicate the expected success rates and standard deviations in

the case of random ordering of companies (-values in this case are

all below ). Interestingly, the

random null model provides an expected success rate which is indeed

comparable to the actual performance that venture funds focusing on early-stage start-ups reach through costly and labour-intensive screening processes (see

section 4.2 in SM for details), while the performance of our recommendation method

is considerably superior.

We further checked the robustness of our methodology by replicating

the analysis based on the Top 50 and Top 100 (reported in Fig 2B), for two additional time windows

and years (see Fig S8 in SM) and an

alternative method of aggregation of the success rate across the

entire observation period (see Fig S9 in SM). We

also controlled for different confounding factors such as

start-up size, geographical location or structural role of venture

capital funds in the start-up network, finding that our conclusions hold (see section 5 of the SM).

Finally, notice that the method presented here

only provides a simple heuristic recommendation, i.e. it does not

quantify the probability of each start-up

in the open-deal list to show economic success in the future.

In Section 6 of the SM we further

studied this possibility by using a suite of logistic regression

methods to predict success of each and every start-up in the open-deal

list. We indeed found that a snapshot

of the closeness centrality ranking of a given start-up could predict its future economic outcome (F1 score ), in qualitative

agreement with findings in Fig 2.

Implications. As lack of data and subjective biases

inevitably impede a proper and rigorous evaluation of risky and newly

established innovative activities, our study has indicated that the

network of professional relationships among start-ups can unlock the

long-term potential of risky ventures whose economic net present value

would otherwise be difficult to measure. Our recommendation method can

help stakeholders devise and fine-tune a number of effective

strategies, simply based on the underlying network. Employees,

business consultants, board members, bankers and lenders can identify

the opportunities with the highest long-term economic

potential. Individual and institutional investors can discern

financial deals and build appropriate portfolios that most suit their

investment preferences. Entrepreneurs can hone their networking

prowess and strategies for sustaining professional inter-firm

partnering and securing a winning streak over the long run. Finally,

governmental bodies and policy-makers can concentrate their attention

and efforts on the economic activities and geographic areas with the

most promising value-generating potential (e.g., activities with the

capacity of job creation, youth employment and skill development,

educational and technological enhancement) for both the national and

local communities. Sociological and economic research has vastly

investigated the impact of knowledge spillovers (?),

involvement in inter-firm alliances (?) and network

position (?) on firms’ performance, innovation capacity,

propensity to collaborate, and growth rates. Yet, whether the

centrality in the professional network of newly established

knowledge-intensive firms can help predict their long-term economic

success has largely remained a moot question. Our work is the first

attempt to pave the way in this direction, and

represents a contribution, from a different angle, to the ongoing

discussion on the science of success (?),

complementing recent findings in different fields such as

science (?, ?, ?) and arts

(?, ?).

Acknowledgements: LL acknowledges funding from EPSRC grant EP/P01660X/1. VL acknowledges funding from EPSRC grant EP/N013492/1. Authors express their gratitude to StartupNetwork s.r.l for providing data and computational infrastructure.

References

- 1. European Commission, “Towards a job-rich recovery” (COM(2012) 173 final, 18 April 2012).

- 2. The White House, “Economic report of the President”, (US Government Printing Office, Washington, DC, 2016).

- 3. J. Haltiwanger, R. S. Jarmin, J. Miranda, Who creates jobs? Small versus large versus young. Review of Economics and Statistics, 95(2), 347-361(2013).

- 4. M. Mazzucato, The Entrepreneurial State: Debunking the Public vs. Private Myth in Risk and Innovation (Anthem, London, UK, 2013).

- 5. H. W. Chesbrough, The era of open innovation. MIT Sloan Management Review, 44(3), 35-41 (2003).

- 6. J. Freeman, G. R. Carroll, M. T. Hannan, Liability of newness: Age dependence in organizational death rates. American Sociological Review, 48(5), 692-710 (1983).

- 7. W. W. Powell, D. R. White, K. W. Koput, J. O. Smith, Network dynamics and field evolution: The growth of interorganizational collaboration in the life sciences. American Journal of Sociology, 110(4), 1132-1205 (2005).

- 8. S. A. Shane, The Illusions of Entrepreneurship: The Costly Myths that Entrepreneurs, Investors, and Policy Makers Live by (Yale Univ. Press, New Haven, CT, 2008).

- 9. J. A. Schumpeter, The Theory of Economic Development (Harvard University Press, Cambridge, MA, 1934).

- 10. J. Guzman, S. Stern, Where is Silicon Valley?, Science, 347(6222), 606-609 (2015).

- 11. W. W. Powell, K. W. Koput, L. Smith-Doerr, Interorganizational collaboration and the locus of innovation: Networks of learning in biotechnology. Administrative Science Quarterly, 41(1), 116-145 (1996).

- 12. A. Saxenian, Regional Advantage (Harvard University Press, Cambridge, MA, 1996).

- 13. O. Sorenson, J. W. Rivkin, L. Fleming, Complexity, networks and knowledge flow. Research Policy, 35(7), 994-1017 (2006).

- 14. M. Ferrary, M. Granovetter, The role of venture capital firms in Silicon Valley’s complex innovation network, Economy and Society, 38(2), 326-359 (2009).

- 15. V. Latora, V. Nicosia, G. Russo, Complex Networks: Principles, Methods and Applications (Cambridge University Press, 2017)

- 16. N. Masuda, R. Lambiotte, A Guide to Temporal Networks (World Scientific, Singapore, 2016).

- 17. S. Wasserman, K. Faust, Social Network Analysis: Methods and Applications (Cambridge University Press, Cambridge, 1994).

- 18. T. E. Stuart, O. Sorenson, Liquidity events and the geographic distribution of entrepreneurial activity. Administrative Science Quarterly, 48(2), 175-201 (2003).

- 19. R. C. Sampson, R&D alliances and firm performance: The impact of technological diversity and alliance organization on innovation. Academy of Management Journal, 50(2), 364-386 (2007).

- 20. B. Uzzi, Embeddedness in the making of financial capital: How social relations and networks benefit firms seeking financing. American Sociological Review, 64(4), 481-505 (1999).

- 21. A.-L. Barabasi, The Formula: The Universal Laws of Success (Little Brown and Company, New York, 2018)

- 22. O. Penner, R. K. Pan, A. M. Petersen, K. Kaski, S. Fortunato, On the predictability of future impact in science, Scientific Reports, 3:3052 (2013).

- 23. A. Ma, R. J. Mondragón, V. Latora, Anatomy of funded research in science, Proceedings of the National Academy of Sciences, 112(48), 14760–14765 (2015).

- 24. R. Sinatra, D. Wang, P. Deville, C. Song, A. L. Barabasi, Quantifying the evolution of individual scientific impact, Science, 354, 3612 (2016).

- 25. O. E. Williams, L. Lacasa, V. Latora, Quantifying and predicting success in show business, arXiv:1901.01392.

- 26. S. P. Fraiberger, R. Sinatra, M. Resch, C. Riedl, A. L. Barabási, Quantifying reputation and success in art, Science, 362, 6416, 825-829 (2018).

Supplementary Materials include:

Supplementary section S1) Data set: additional details

Supplementary section S2) Construction of the World Wide Start-up (WWS) network

Supplementary section S3) Analysis of the WWS network

Supplementary section S4) Open-deals recommendation method

Supplementary section S5) Additional analysis

Supplementary section S6) From recommendation to prediction of start-up success: supervised learning approaches

Supplementary Tables S1–S4

Supplementary figures Fig S3–S19

Supplementary References (27–37)

Supplementary Material

S1 Data set: additional details

Data were collected from the crunchbase.com Web API and were updated until December 2015. The data provided by the Crunchbase website are manually recorded and managed by several contributors (e.g., incubators, venture funds, individuals) affiliated with the Crunchbase platform. Moreover, the data are further enriched by Web crawlers that scrape the Web, on a daily basis, in search for news about IPOs, acquisitions, and funding rounds. To date Crunchbase is widely regarded as the world’s most comprehensive open data set about start-up companies. It contains detailed information on organizations from all over the world and belonging to four categories, namely companies, investors, schools, and groups. Among schools there are universities, including top-tier institutions such as Stanford University, the Massachusetts Institute of Technology (MIT), and many others. In addition to people’s business activity, the data track information about their educational paths, and consequently their access to academic knowledge.

The total number of organizations listed at the date of data collection amounted to . However, a large number of entries contained very limited information, no profile pictures, and no employees’ records. Accordingly, we needed to clean the data keeping only the organizations for which enough information was provided, and for which such information was reliable (see Section S2 for more details). This finally limited the number of organizations to . For this work, all these organizations were included in the construction of the network. Notice however, that only organizations belonging to the category “companies” and, at the same time, younger than two years, have been included in the recommendation list. For each organization we extracted all the people included in the team (e.g., founders, advisors, board member, employees, alumni) and additional information such as details on firms’ foundation dates, locations of the firms’ headquarters, founding rounds, acquisitions, and IPOs. Organizations and people are uniquely identified by alphanumeric IDs. All data are time-stamped, and an accurate reconstruction of historical events was made possible by the use of trust codes, i.e., numerical codes provided by Crunchbase to indicate the reliability of a certain timestamp. The timestamps indicate the dates of foundation, funding rounds, acquisitions, and IPOs, as well as the start and the end times of job roles.

S2 Construction of the World Wide Start-up (WWS) network

We constructed a bipartite time-varying graph with nodes representing organizations distributed across countries around the globe, nodes representing people, and links between people and organizations. The graph is time-varying because each node and each link have an associated timestamp, representing, respectively, the time an organization was founded and the time a person was affiliated (and held a variety of roles) with a given organization. Notice that in the construction of the time-varying graph we retained only the timestamps whose trust code guarantees the reliability of the year and month. Additionally, we cleaned the data by solving and removing inconsistencies such as an employee’s role starting at a date prior to the company’s foundation. In these cases, we retained the most reliable information according to the trust code value. Inconsistencies were removed by adopting a strong self-penalising data cleaning strategy. In particular, we did not make any assumption on dates, nor did we attempt to infer timestamps. As a result, we do not retain in the graph links whose timestamps cannot be determined in a reliable way. This approach to data cleaning strengthens the validity of our results because it ensures that companies do not gain higher positions in the closeness centrality rank score as a result of connections that were forged at subsequent dates to those incorrectly or only partially reported in the data set. In this way we avoid biases that could artificially inflate the success rate of the method, and accordingly our results can safely be seen as conservative lower bounds.

We then projected the bipartite time-varying graph onto a one-mode graph in which two companies are connected when they share at least one individual that plays or has played a professional role in both companies. Such a graph comprises companies and links among them, and is here referred to as the World Wide Start-up (WWS) network. The projected graph is time-varying like the original bipartite graph: a link between any two companies is forged as soon as one individual with a professional role in one company takes on a role in the other company. Since the creation of these links denote intel transfer between companies, we realistically assume that such intel flow generates considerable know-how for the nodes receiving new links. Once created, the links are then maintained, since the know-how of a given company is not destroyed or removed.

S3 Analysis of the WWS network

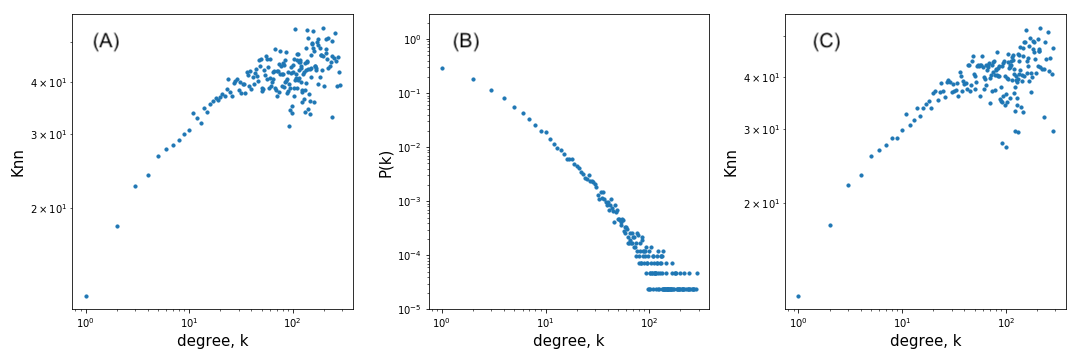

For completeness, we have calculated a variety of quantities for measuring the characteristics of the structure of the WWS network. In particular, from 1990 to 2015, for every month, we have computed the number of companies (nodes) and links, and examined the partition of the WWS network into distinct connected components. A connected component of a network is a subgraph in which any two nodes are connected to each other by at least one path [15, 16]. If the network has more than one component, one can identify the largest connected component (LCC), namely the component with the largest number of nodes. The countries highlighted in blue in Fig 1A (main text) are those that have at least one start-up that is part of the LCC of the WWS network. Fig 1C (main text) shows a rapid growth in the fraction of start-ups in the LCC, thus highlighting the tendency that companies have to establish new connections with one another and move toward the core of the network. Like many other real-world complex networks, the WWS network is characterised by a rich topological structure, a small average shortest path length (), and a high value of the average clustering coefficient, , as expected from the one-mode projection of a bipartite network [15, 16]. The value of the average shortest path length is similar to the one obtained for an equivalent Erdös-Renyi random graphs (?) with the same number of nodes and edges ( = 4.17). However, the statistical features of the WWS differ from those characterising random graphs: the degree distribution approaches a power-law with an exponent greater than (see Fig. S3, panel B), the assortativity coefficient (?) is positive, namely (see Fig. S3, panel A) and this result holds even if all venture capital firms are removed from the network (panel C). The clustering coefficient is significantly larger than the one obtained for a corresponding random network, .

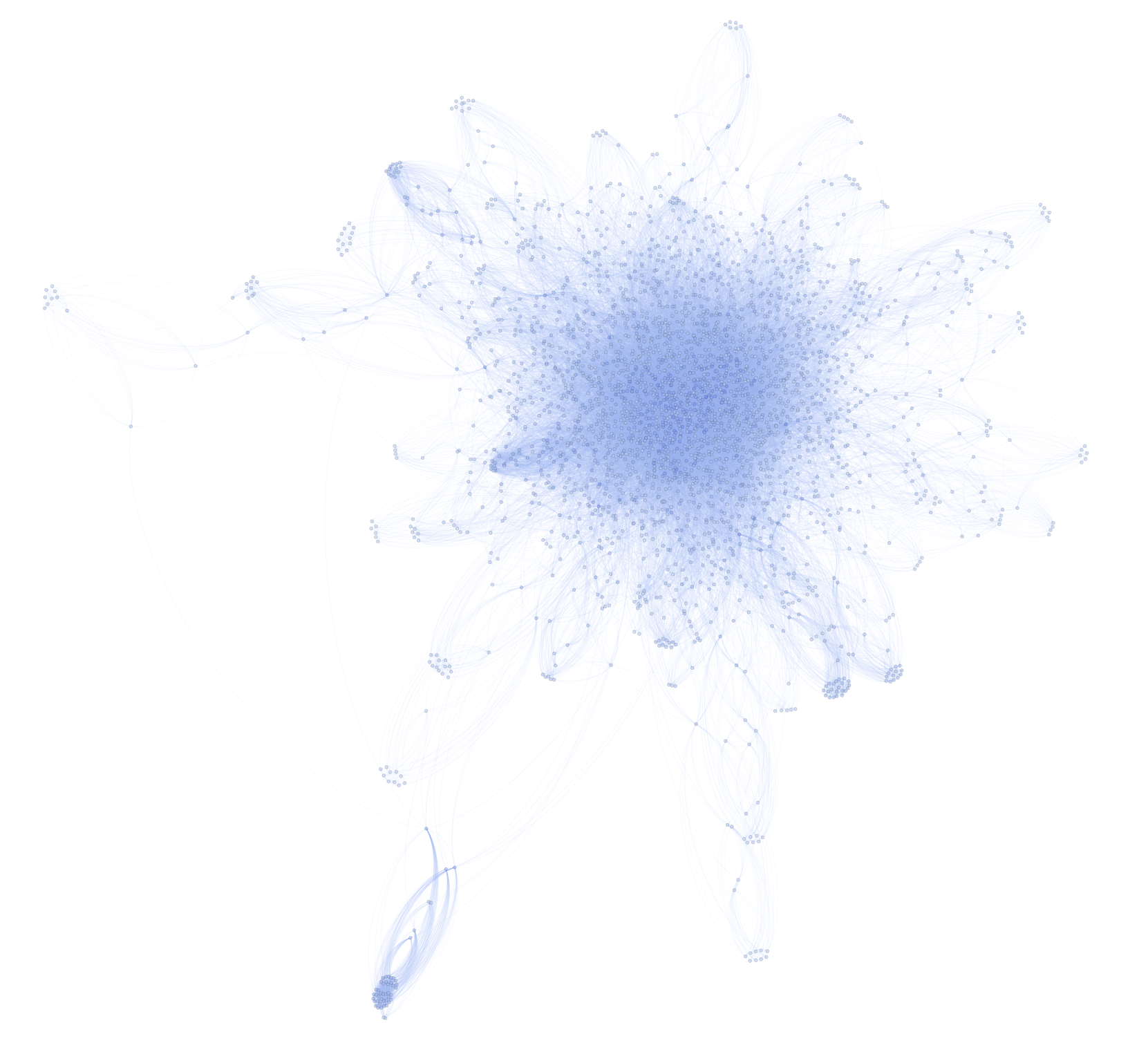

To offer a glimpse of the structure of the WWS network, in Fig. S4 we show the subgraph obtained by using the k-core decomposition technique and including only the nodes that belongs to the 10th shell. The k-core decomposition of a graph (?, ?, ?) is a technique that iteratively deletes nodes starting from the most peripheral ones (i.e., nodes with degree equal to ) and progressively unveil the most central and interconnected core of the network. Nodes are assigned to a core value equal to accordingly to the k-core subgraph to which they belong.

S4 Open-deals recommendation method

Our working hypothesis is that companies with a central position in the network have higher exposure to knowledge and easier access to resources than companies with peripheral positions. If this is the case, centrally positioned companies will be better equipped to compete and have higher chances to survive, grow and flourish than peripheral ones. We have therefore used network centrality measures [15, 16] that capture the structural centrality of a node in a graph, with a view to identifying companies with a large long-term economic potential.

The concept of centrality and the related measures were first introduced in the context of social network analysis (?). the centrality of a company we have computed, on a monthly basis, its closeness centrality in the WWS network. Several other centrality measures have also been considered, and the results are reported in Section S5. The closeness centrality quantifies the importance of a node in the graph by measuring its mean distance from all other nodes. The closeness centrality of a node , is defined as:

| (S1) |

where is the number of nodes in the graph at time , while is the graph distance between the two nodes and , measured as the number of links in the shortest path between the two companies. To account for disconnected components we used the generalisation of closeness centrality proposed in (?).

Our claim is that young start-ups with proportionally higher values of closeness centrality will have a higher likelihood to become successful in later years. This can be readily translated into several possible heuristics to provide recommendation for investing into a given start-up. Among other possibilities, we have considered the following recommendation method. For each month , we ranked all the companies according to their values of closeness centrality , such that the top nodes are those with the highest closeness. From the ranked lists we then removed the companies that can reasonably be regarded as irrelevant deals to investors, i.e., those companies that had already been acquired, had already been listed in a stock market, or had received funding from other investors. The companies retained in the analysis belong to the so-called open-deals ranked list at month . Notice that, by definition, the open-deal list considers newly-established start-ups. As a matter of fact, incubators such as 500 Startups, Y Combinator, Techstars or Wayra indeed target early-stage companies, i.e. they make risky investments on ideas and small teams without much of previous history. Their investment targets are therefore similar to the ones captured by our the definition of ‘open-deal list’, and it is easy to realize that predicting future positive outcomes of firms in such a set is more challenging than predicting future positice outcomes of more established firms.

Fig S5 shows an example of the procedure adopted. The companies highlighted in grey are those which, prior to December 2008, had not yet received funding, had not yet been acquired, or had no yet been listed in any stock market. These companies thus could be seen as investment opportunities at month . Since we want to focus on early-stage companies, we also removed any company that was more than two years old.

S4.1 Success rate in open-deals lists

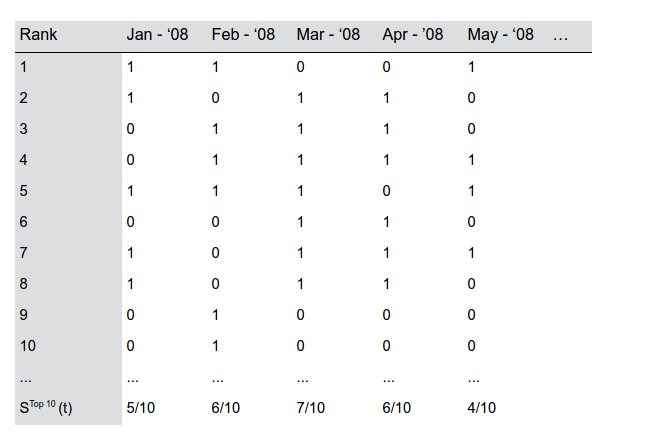

Each open-deals list in month contains successful companies (), i.e., those companies that have obtained, within a time window or years since month , a positive outcome. A positive outcome is here defined in terms of the occurrence of at least one of the following events: (i) the company makes an acquisition; (ii) the company is acquired; or (iii) the company undergoes an IPO. To each company in the open-deals list we then assigned the value of a binary variable, namely if the company has achieved a positive outcome within the chosen time windows , or otherwise. Fig S6 shows an example of the monthly open-deals lists, in which names are replaced by their associated binary values. Notice that the higher the number of ones in the top regions of the rankings, the better the performance of the recommendation method in predicting positive outcomes.

We focus on companies in the top positions of our open-deals recommendation list, and we indicate by the number of companies in the Top 20 in month that have obtained a positive outcome, i.e., the number of ones in the first entries of the list. Notice that the same procedure has been repeated for the Top 50 companies () to check for the robustness of results. The accuracy of the recommendation method is assessed by computing the success rate defined as the ratio . How does this compare to a null model where network properties are not taken into account? If the open-deals lists were randomly ordered, the expected number of successful companies in e.g. the Top 20 () would be given by the expected value of the hypergeometric distribution . In particular, the expected value of is and thus the expected success rate is . Similarly, it follows that .

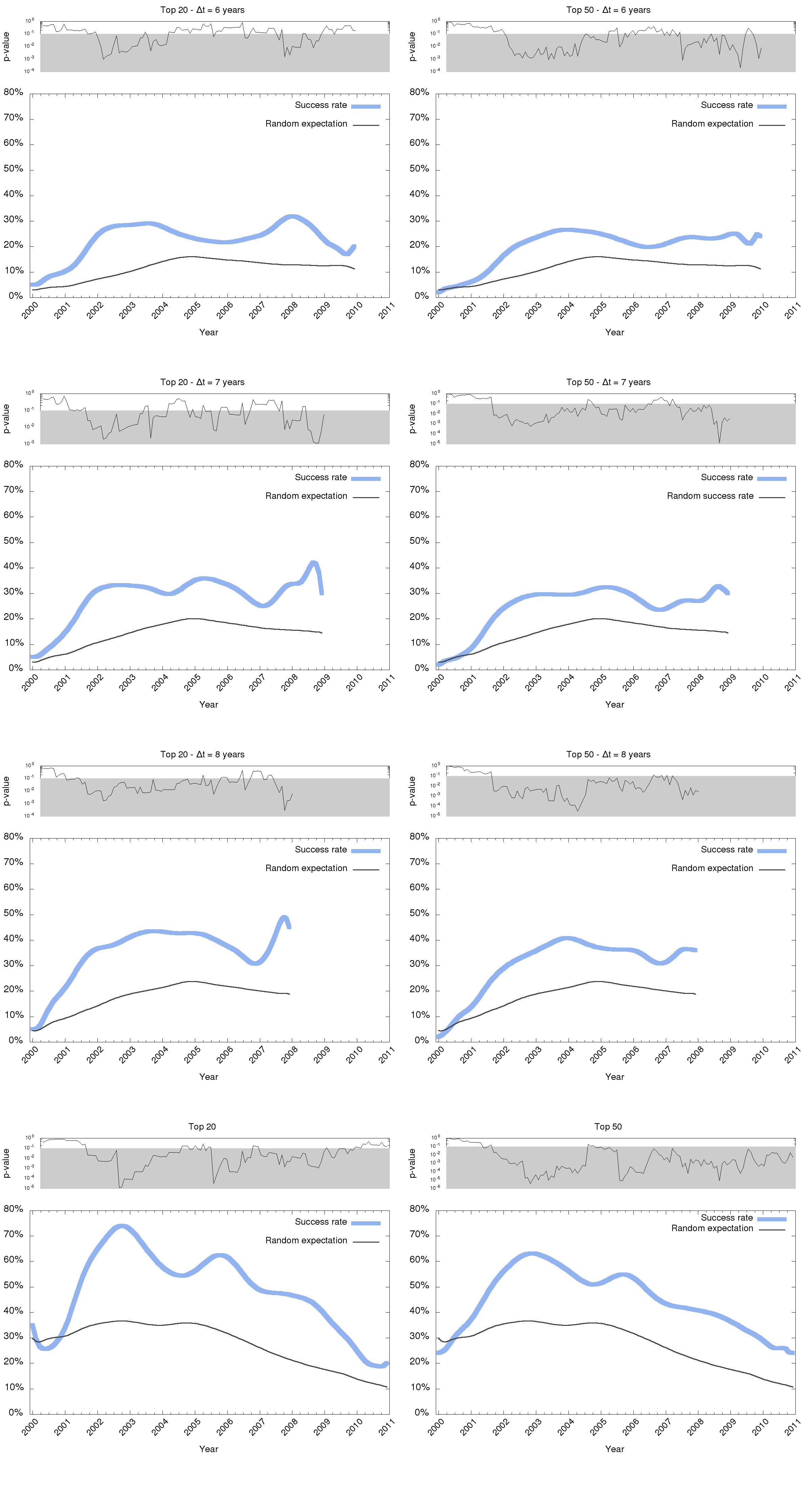

Fig 2 (main text) and Fig S7 show that (blue curve) is systematically much higher than (black curve), except during two short periods corresponding, respectively, to the dot-com bubble (1999-2001) and to the 2008 financial crisis. In both cases, the difference between and becomes narrower, yet always remains higher than . Moreover, Fig S7 shows that these findings are robust against variations in the length of the time window (i.e., ) and in the number of companies considered in the recommendation (i.e., Top 20 and Top 50).

The statistical significance of the results is assessed by computing the hypergeometric -values, which give the probability of obtaining, by chance, a success rate equal to or greater than the one obtained with real data. Denoting as the probability mass function of we can compute the -value at time as:

The top charts in Fig 2 (main text) and in each panel of Fig S7 report the evolution of the -values over time. Low -values () are observed in most parts of the observation period. This suggests that the discrepancy between the success rate of the 20 top-ranked companies selected according to our recommendation method and the success rate of the same number of companies selected at random from the open-deals list is statistically significant. Conversely, high -values are observed in correspondence of the downturns, thus indicating that in such periods the success rates predicted by our recommendation method could have been obtained also by chance.

S4.2 Real investors performance is similar to random expectation

It is important to highlight that, although the random expectation null model has mainly been introduced to assess whether our results are statistically significant, the performance of real investements is remarkably similar to the expected success rate in the null model. To illustrate this, a summary statistics of the Top 15 investors, according to the number of investments, is reported in Table S1 (data extracted from crunchbase.com). Notice that there is a great variability in investors performance, which reflects the variability in the type of investments. Highlighted in pink are those investors whose target complies with our definition of open-deal list. Incubators such as 500 Startups, Y Combinator, Techstars or Wayra focus indeed their interest on very early-stage companies, i.e. they invest on ideas and small teams of entrepreneurs without much history. They make the most risky bets in the landscape of start-ups investments and their performance lies around . Their investment target is very close to the type of companies that we have isolated in our definition of “open deals”. On the other end, large venture firms such as Intel Capital, Accel Partners, or Goldman Sachs invest in companies at later stage of maturity. They are interested in organizations with larger teams, that have already previously received funding, and they typically inject funds to boost a business that has already found a market fit and has history of revenues, customers, and other indicators of growth. The presence of quantitative indicators of growth allows large venture firms to perform a more objective evaluation of the company and its success potential, which in turn is reflected on higher investment performances.

| Investor | # investments | # successful investments | Success rate |

|---|---|---|---|

| 500 Startups | 1022 | 153 | |

| Y Combinator | 953 | 154 | |

| Intel Capital | 744 | 313 | |

| Start-up Chile | 710 | 10 | |

| Sequoia Capital | 700 | 267 | |

| New Enterprise Associates (NEA) | 672 | 272 | |

| SV Angel | 600 | 258 | |

| Techstars | 549 | 95 | |

| Brand Capital | 537 | 80 | |

| Accel Partners (Accel) | 536 | 270 | |

| Sos Ventures (SOSV) | 493 | 17 | |

| Wayra | 476 | 11 | |

| Kleiner Perkins Caufield & Byers (KPCB) | 457 | 203 | |

| Right Side Capital Management (RSCM) | 449 | 44 | |

| Goldman Sachs | 410 | 209 |

In summary, while investors decide on which start-ups to invest through costly and labour-intensive screening processes, results confirm that the percentage of real investments that were deemed ‘successful’ is consistently similar to the success rate given by our random expectation model. In other words, state-of-the-art success rate is not much better than a random expectation null model. This means that any improvement upon the null model provides valuable information. We conclude that our recommendation method based on centrality –whose success rate consistently exceeds random expectation over several periods– is a considerable improvement with respect to the state of the art.

S4.3 Details on overall success rate

To obtain an overall measure of the performance of our method, the success rate can be aggregated across the entire observation period. This can be carried out in two complementary ways leading to two different measures of the overall success, namely and . Here we discuss and provide some details with regards to both measures.

The first measure of overall success rate, , which is used in the main text, takes into account the total number of positive entries in the top positions in all open-deals lists, regardless of the specific companies that occupy those positions. In this way provides a measure of the overall goodness of the ranking across months, but it does not provide information about the number of unique companies correctly or wrongly identified as successful. As an example of the computation of , let us consider the period starting in January 2000 and ending in December 2007, and the Top 20 companies (bottom-left charts in Fig S7). Such a period includes months. The overall success rate is defined as:

where is the total number of entries in the Top 20 list across the months, and , where the sum runs over all months in the observation period. To construct a null model to which we can compare these measures, we then proceed to randomly shuffling the entries in each open-deal list independently for each month and apply the same procedure (i.e., the null model makes a random sampling of the list without replacement). Accordingly, at month we count the number of successful companies within the Top 20 and label it . The expected total number of successful companies within all the Top 20 lists in this null model is thus given by:

and the corresponding variance is given by the sum of the variances in each month

where denotes the variance associated to the random null model, i.e. the variance of the hypergeometric distribution. The expected overall success rate in the case of random ordering is then given by

and its standard deviation is

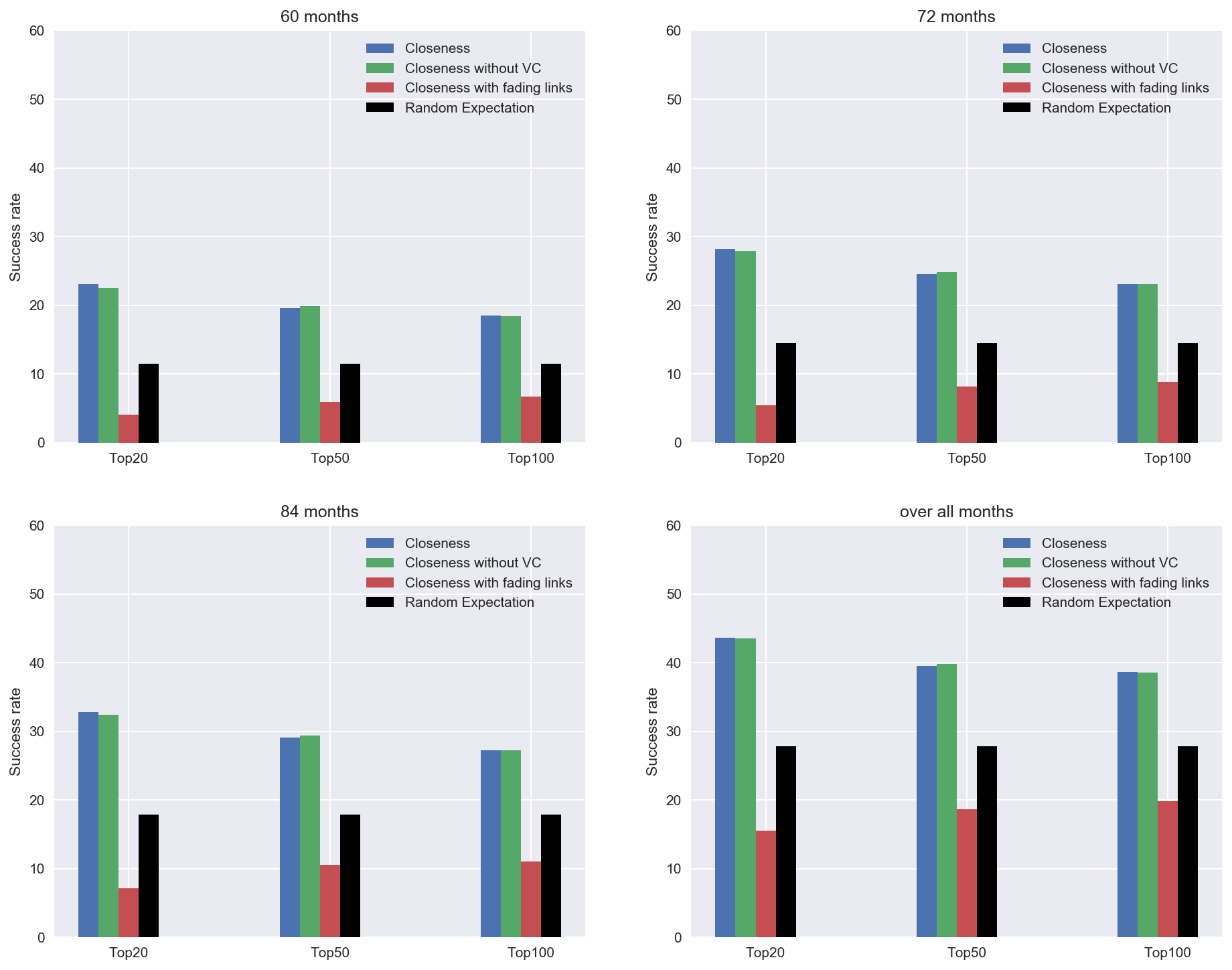

Figure S8 reports the overall success rate empirically found (blue bars), the overall success rate expected by chance (black dots), and its standard deviation (black error bars) for various values of , and for different numbers of recommended companies (i.e., Top 20, 50, and 100).

The second measure of the overall success rate, , does not simply capture the overall performance of the ranking-based recommendation method, but compares the number of unique companies in the Top 20s correctly predicted as successful by our method, across the entire observed period, against the number of successful companies that would be expected under random selection. In particular, this second measure of overall success is based on: (i) the total number of unique companies available in any month; (ii) the total number of unique companies that have achieved a positive outcome at any time since their foundation up to 2015; (iii) the number of unique companies included in all Top 20 rankings in any month; and (iv) the number of unique companies, listed in all Top 20 rankings, that have achieved a positive outcome at any time since their foundation up to 2015.

Notice that, in this way, each company contributes only once to the evaluation of the success rate. Therefore, the probability of finding exactly successful companies in any ranking of Top 20 (50, or 100) is given by the hypergeometric function . The success rate shown in Fig S9 is computed as , while the success rate in the case of the null model is given by . Fig S9 reports also the error bars of the success rate computed as the standard deviation of the hypergeometric distribution.

While the first index of overall performance assesses the average goodness of the ranking, the second index measures only the number of companies correctly identified as successful across the entire observation period. The two aggregation methods produce comparable results, and achieve a substantial success rate of about in the case of . Moreover, in both cases, the success rate found in reality and the one expected by random chance are very different, and their discrepancy is always statistically significant with -values smaller than .

S5 Additional analysis

S5.1 Closeness centrality in successful vs non-successful start-ups

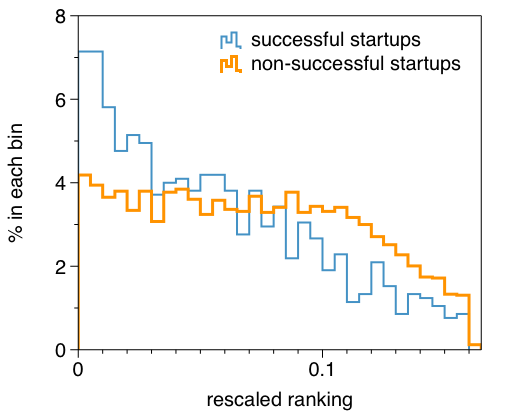

To have a better understanding of how closeness centrality is distributed among start-ups, in Fig S10 we compare the estimated frequency histograms of closeness centralities rescaled ranking. To obtain the rescaled ranking, in each calendar month we calculated the closeness centrality of each firm in the global network and ranked all firms in terms of their centrality, what gives an ‘absolute rank‘ for each firm. We then extract those firms which belong to the open-deal list, and re-rank them accordingly (so that the firm with top ranking acquires a rank in the open-deal ranking, the second acquires rank , and so on). The rescaled ranking is then defined as the ratio between the open-deal-rank and the maximum absolute-rank of open-deal companies at a given month. Thus, the firm with the highest position (i.e., zero ranking) maintained the same value (i.e., zero) in the rescaled ranking. By contrast, firms at lower positions were assigned rescaled values approaching 1 as their ranking approached the highest value (i.e., the lowest position). Such a rescaling thus enables to appropriately compare firms characterised by different values of centrality, obtained in different networks and at different calendar times. In order to smooth out the data, a binning has been performed in the x axis (bin size of ). We notice that histograms are non-overlapping, and that there is a net overabundance of start-ups with a positive outcome (successful) closer to the top of the ranking. In other words, start-ups which are higher in the centrality rankings (i.e. small values of closeness centrality ranks) have statistically a higher chance of positive economic outcomes. This confirms that rankings based on closeness centrality are indeed informative of a start-up long-term success and can then be used to inform recommendation.

S5.2 Different centrality measures are correlated

We have considered closeness centrality as our primary

measure of network centrality. Closeness centrality is based on the lengths

of shortest paths in the network. However, the structural centrality of a node

in a network can be quantified by different network metrics, either global such

as closeness and betweenness, and local as the degree centrality (?).

Closeness centrality of a node (Eq.S1) characterises the overall distance between that node and the rest of the nodes in the network, such that the lower that overall distance, the higher this measure, and hence the more central this node is.

On the other hand, the betweenness centrality of a node when the network is observed at a given time is given by

| (S2) |

where is the total number of shortest paths between nodes and whereas is the number of shortest paths between and that actually go through . This measure was introduced by Freeman to quantify the fact that communication travels just along shortest paths, and so a node is more ‘central’ the more shortest paths among pairs of nodes in the network go through it.

While both closeness and betweenness are measures of centrality based on shortest paths, one can also think of a node being central if it acquires many edges over time –i.e. acquiring intel from several other companies–. To account for this we may resort to use (normalised) degree centrality , defined as

| (S3) |

where is the degree (number of links) of node and is the largest degree in the network at that particular time snapshot.

Consequently, the centrality of a start-up

in the WWS network can be measured in many

alternative ways. In this section we will show that the choice of using

closeness centrality is not only supported by theoretical arguments based on

employees’ mobility and intel flows among companies, but it also a robust

choice as other alternative measures produce similar results.

To validate robustness, for each start-up in the open-deal list across

time we have computed additional centrality measures, namely degree

and betweeness centrality (?), and computed to which extent

all three possible measures of centrality are correlated. More

concretely, we consider all start-ups in the open-deal list for which (i) we

have data of the three centralities over at least 3 of the 24 months

forming the observation window, and for which (ii) closeness and betweeness centralities are defined. For each firm, we then compute the

Pearson correlation coefficient between the monthly sequence of each

pair of (rescaled) centrality measures. We do this for all firms and we then construct

the frequency histogram of the Pearson correlation coefficients. Results

are reported in Fig. S11. Interestingly, we find

that the three measures are in general well (pairwise)

correlated.

We conclude that the choice of a particular type of global centrality

measure, such as closenness, is a robust choice as other global

structural indicators based on a different use of shortest paths and,

to a minor extent, also local measures such as the degree are

correlated with the closeness in the case of the WWS network under

analysis in this work. Hence, focusing on closeness centrality is a

robust choice. In the next subsection we round-off this validation by

exploring results of our recommendation method using either

betweenness or degree centrality as the key network indicator, and

will show that success rates of the recommendation method are similar

in all three cases.

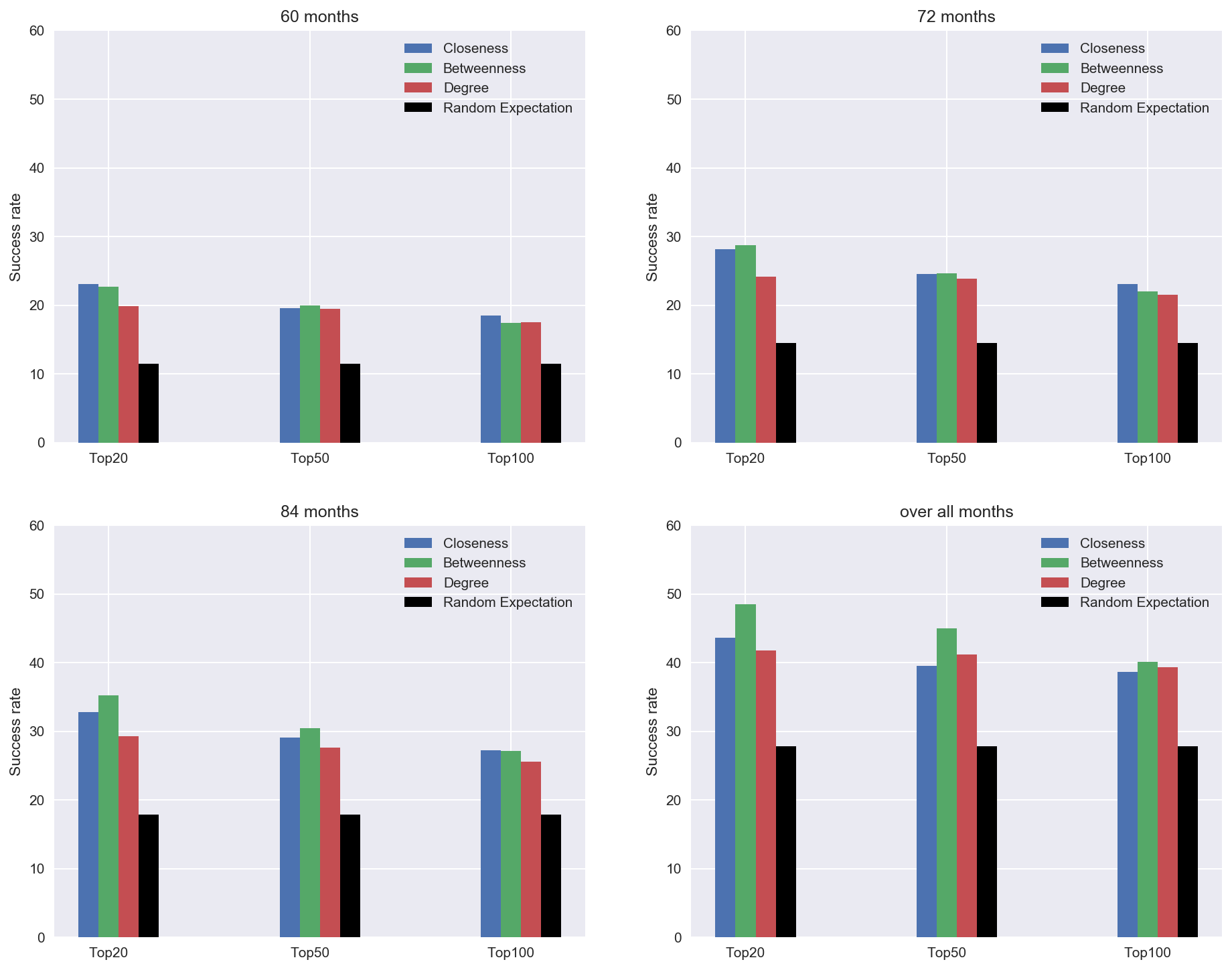

S5.3 Recommendation methods based on other centrality measures

To further complement the correlation analysis of the previous subsection, here we focus on recommendation methods based on centrality measures other than closeness. Results are summarised in Fig.S12 for averages over the entire period, and in Figs.S13 and S14 for monthly analysis. In every case we find that the results are qualitatively similar whether we use closeness, betweeness or degree centrality, with success rates systematically larger than random expectations (and therefore larger than the actual perfomance of accelerators and investors focusing on early-stage start-ups).

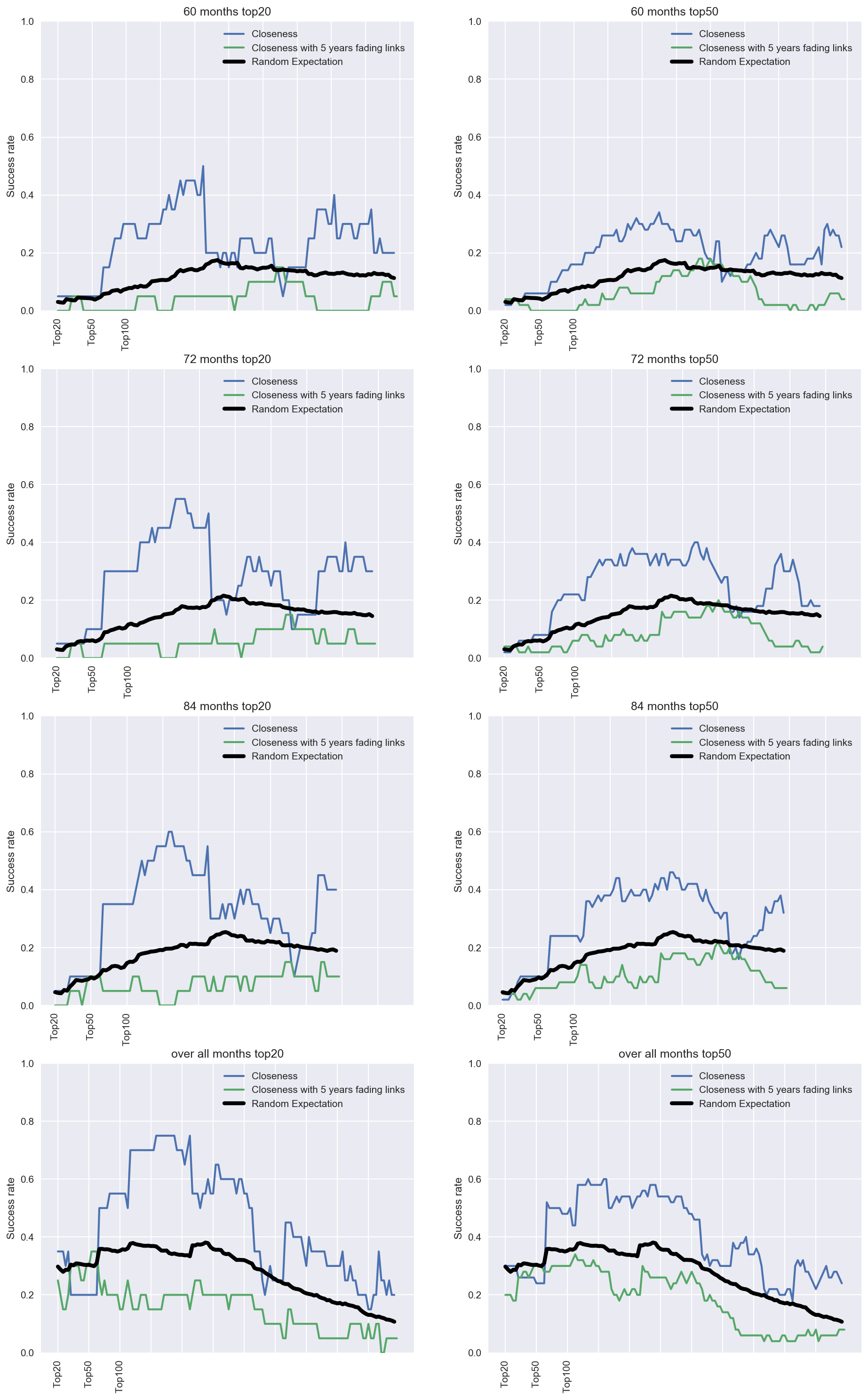

S5.4 The effect of fading links

The mobility of workers from one company to another

creates an intel flow between companies. Our working hypothesis is

that companies receiving employees increase their fitness by

capitalising on the know-how the employee is bringing with him/her.

Such microscopic dynamics is thus captured and modelled by the

creation of new edges at the level of the network of start-ups. As a

consequence, companies which are perceived at the micro scale as

appealing opportunities by mobile employees will likely boost their

connectivity and therefore will acquire a more central position in

the WWS network. An important underlying assumption is that, once a

link is created, it will remain in the network indefinitely, so that

the company that has received the intel keeps it and builds on this intel

forever.

Conversely, considering the

possibility of removing links (or actually fading their strength) some time after their creation,

would actually be equivalent to assume that companies

can lose the know-how they have acquired, something which is less

likely to occur.

Accordingly, allowing links to fade or be removed with time in the construction of

the time-varying WWS network should lead to recommendations on the positive

economic outcome with much lower success rates than those obtained

from a network where know-how is not artificially removed. To check

for this case, we have first build the WWS (for each month) from January 1990 to December 1999. Then, starting from January 2000 onwards, for each month all connections older than 10 years are removed from the network. Closeness is then evaluated each month as described in the recommendation method. A similar analysis is also performed for 5-year fading instead of 10-year fading, with very similar results.

In Fig.S15 we compare the overall success rate for the 5-year fading case (red bars) to our standard recommendation method based on a WWS network that does not allow link fading. Results show that a recommendation method with fading links systematically fails. In fact it works even worse than a random null model, in good logical agreement with our previous discussion. For completeness, a comparison of the two methods is also considered for the monthly success rates in Fig.S16. Results are consistent with those obtained for the overall success rate.

All these results strengthen our working hypothesis that the intel flow across start-ups is well captured by node centrality in the WWS network.

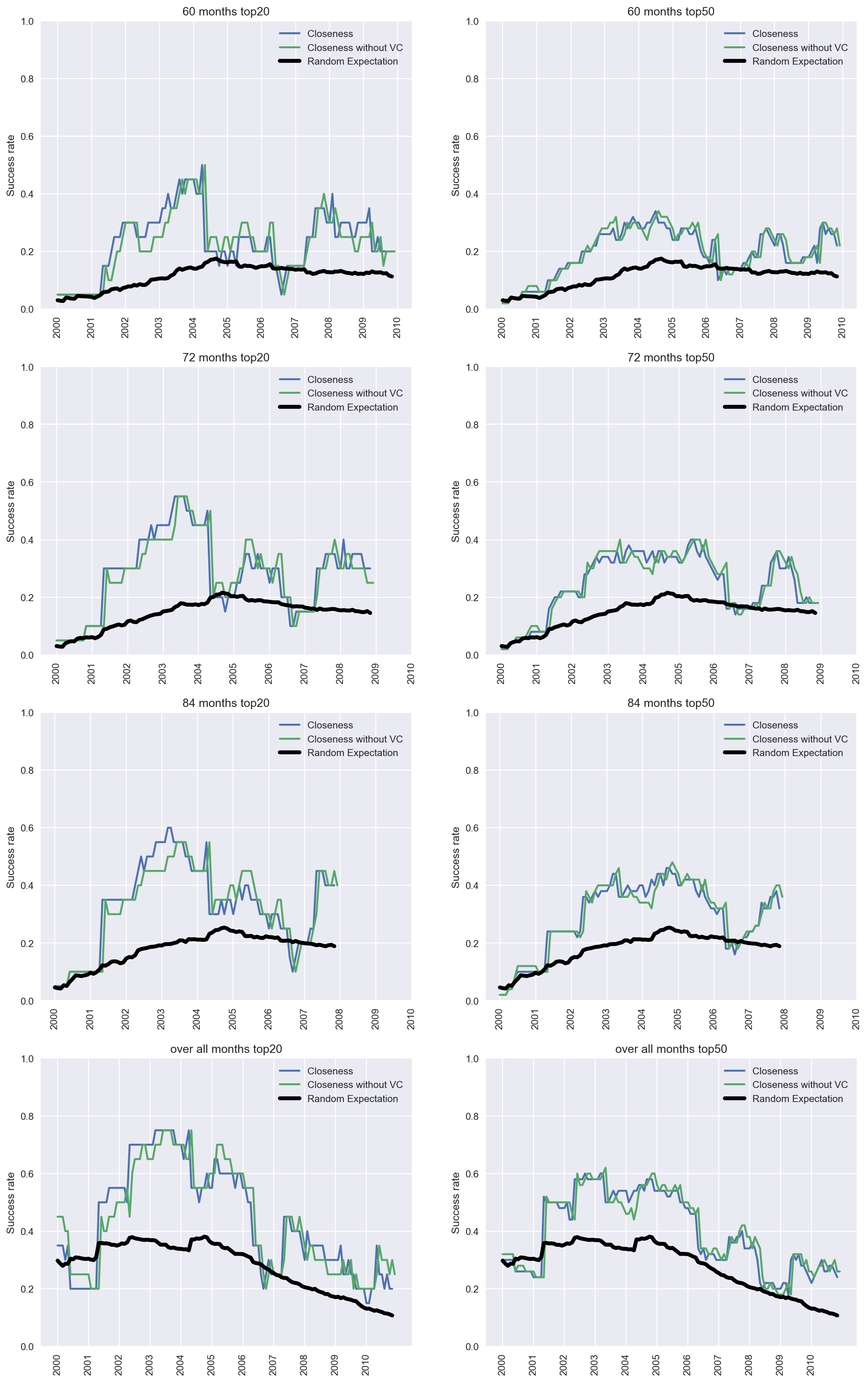

S5.5 Possible confounding factor 1: the effect of venture capital funds

A first possible confounding factor is the presence of venture capital

funds, i.e. the fact that the presence of these nodes in the network

might enhance the closeness centrality of start-ups. In order to

assess the role played by venture capital funds in the effective

centrality of different start-ups, we have performed an experiment

where we remove all venture capital funds from the world start-up

network, and subsequently have recomputed closeness centrality values

for each start-up in the open-deal list. Concretely, we extracted from

CrunchBase.com a list of companies that are labelled as

venture capital firms see Table S5 for details.

Accordingly, in this experiment we create the WWS network but not include those nodes in the network (and all the connections they bring with them). Closeness centrality is then evaluated each month as described in the recommendation method.

Results of overall success rate are shown (green bars) in Fig.S15 while monthly success rates are compared in Fig.S17. The success rate of the recommendation method based on this quantity is consistently similar to the one found in the case where venture capital funds are not removed from the original network, hence confirming that the topological presence of venture capital funds is not a confounding factor.

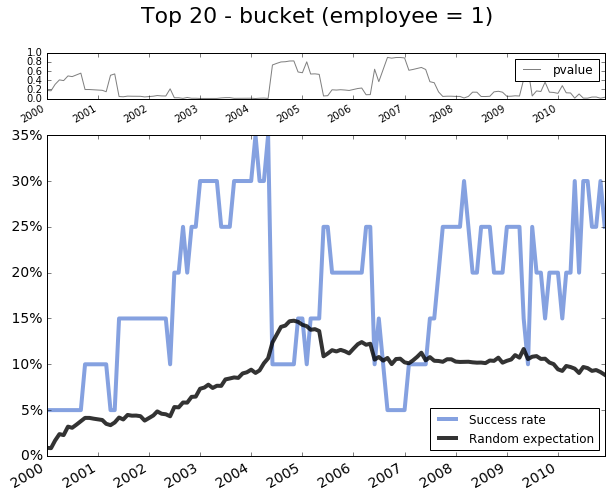

S5.6 Possible confounding factor 2: number of employees

A second possible confounding factor or hidden predictor is the start-up size (e.g., number of employees). To assess this possibility, we have conducted a number of experiments. Initially, we explored start-up size (number of employees) instead of topological network centrality as the informative predictor, and built a recommendation method based on that metric. Results are shown in the left panel of Fig.S18, confirming that number of employees is not informative of the start-up success likelihood.

Additionally, we have also checked the recommendation method (based on closeness centrality) when only the subset of open-deal start-ups with a fixed number of employees is considered. Since the most frequent size is a start-up with a single employee, we extract the subset of all start-ups with only one employee. Monthly success rates of the recommendation method are shown in the right panel of Fig.S18. These results confirm that start-up size is not a counfounding factor and that number of employees is indeed not an informative variable that determines future success.

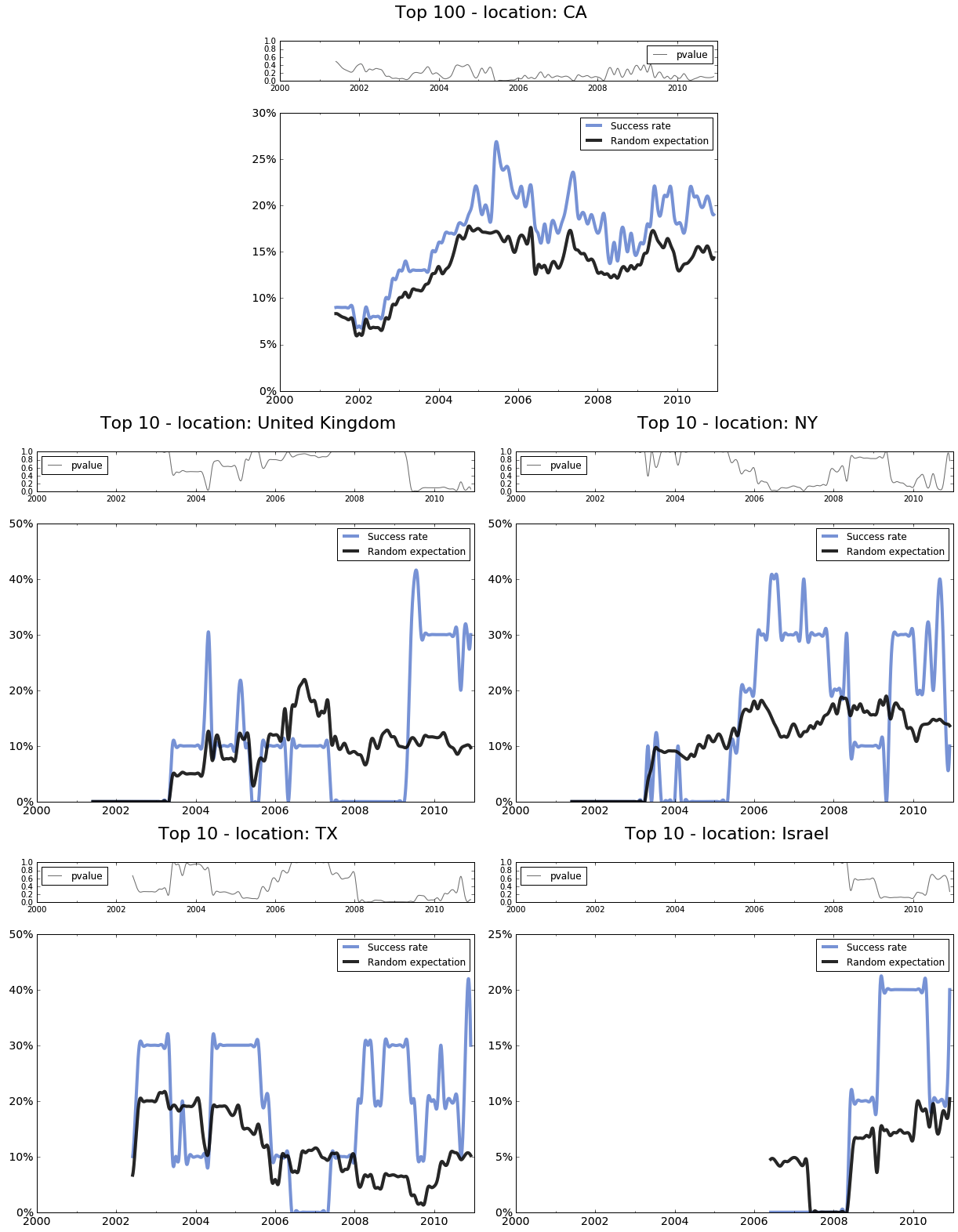

S5.7 Possible confounding factor 3: start-up geographical location

A third possible confounding factor is the geographical location of each of the start-ups. To account for this, we have replicated our analysis (originally performed at a worldwide scale) in five geographically separated regions, by dividing open-deal start-ups in five subsets: California, United Kingdom, New York, Texas and Israel. Results for the monthly success rate of our recommendation method are plotted in Fig.S19. While results are more noisy than for the worldwide setup, we can confirm that for every case the recommendation method based on closeness centrality is above the random expectation.

S6 From recommendation to prediction of start-up success: supervised learning approaches

The recommendation method proposed in the main text is based on the

working hypothesis that start-ups with higher closeness centrality

rankings are more likely to experience a economic successful outcome

in the future. We have provided theoretical foundation to our research

hypothesis at the microscopic level, and then heuristically validated

our recommendation lists on a monthly basis, obtaining results that

are significantly better than those obtained by a random expectation

model.

However, strictly speaking, a recommendation method is not a true prediction

method, as we are not predicting the outcome of each and every start-up in the

open-deal list (either to the successful or to the non-successful category).

To bridge this gap, in this section we consider different types of prediction models which can

indeed truly “predict” the positive outcome of a start-up, i.e. they can

classify whether a given start-up will have a positive outcome or not.

All models are initially based on a sample including firms.

These are the firms that have been in the open-deal list for at least

one month, and can therefore be suggested as potential investment

opportunities. Each firm is then observed over a period of months, or until when it has experienced a

“successful” event (positive economic outcome) if this event occurs

before the end of the months period.

Notice however that in the greatest majority of cases firms were

observed for 24 months. For this experiment note also that we are aggregating all the firms in open-deal list in our database: not all of them are observed in the same time, e.g. one firm can be observed for the 24 months starting in January 2000, another firm can be observed for the 24 months starting in June 2004, etc. In other words, month for a given firm does not necessarily matches the actual date of month for another firm, we are simply recording the temporal evolution of different start-ups which appear in open-deal lists at different times in the period ranging from 1990 to 2008.

Then, for each of the firms, we conclude that a firm has

experienced a “successful” event (a positive economic outcome)

at month if, within a

time window of or years since month , one of

the following events takes place: (i) the firm makes an acquisition;

(ii) the firm is acquired; or (iii) the firm undergoes an

IPO. Accordingly, each firm receives a unique class label (either successful with class label ‘1’, if at any time the start-up experiences a successful event, or not-successful with class label ’0’ otherwise).

Overall, this data set enables supervised learning

(classification), as it consists of a large number of samples (the

firms in the open-deal list), each of them described by a set of

features (a vector of centrality measures over the whole observation

window), and each of them being labelled by a class label.

We will use logistic regression as our supervised learning model. A logistic regression model links the probability of success of a start-up to a linear combination of predictors. More precisely, a logistic regression model is traditionally given by:

| (S4) |

where is the probability of success of the -th start-up, is the vector of predictors, is the (transposed) vector of parameters, which are estimated when the logistic regression model is fitted, and are the errors, which are assumed to be independent, identically-distributed Normal random variables. Rearranging terms, we have

where is a linear combination of predictors with additive noise term and is the so-called logistic function.

In essence, the term is akin to a linear regression on the predictors, and the logistic function is used to force the outcome to be equal to 0 or 1: if , the class is assigned, and for the class is assigned, where the threshold is indeed another parameter that can be trained by the algorithm. Once the parameters are estimated, logistic regression can be used to predict the probability of success of new start-ups.

In what follows we consider two scenarios. In the first case, we define prediction models that do not consider the time evolution of centrality measures for each firm and only use instantaneous values of the firm’s closeness centrality: these models will be closer in spirit to the recommendation method. In a second case, we enrich the predictor set by adding predictors summarising the time evolution of the firm’s centrality over the observation period (to assess whether this factor is informative) as well as similar quantities extracted from different centrality measures.

S6.1 Logistic regression: the unbalanced case.

Here we use the ROC (receiver operating characteristic) curve to assess the efficacy of this binary classification algorithm to choose the optimal threshold based on our tolerance for false negatives and desire for true positives. We initially have used only the last value of the (rescaled) closeness centrality of a start-up over the observed period as the single predictor, in order to try to match the conditions of our recommendation method where only instantaneous information is used. The estimation and prediction steps above have been repeated 1,000 times, leaving out 10% of the data set (Monte Carlo cross-validation). Averaging over the prediction results, we obtain the confusion matrix reported in Table S2 (left panel), together with the confusion matrix expected for a random classifier operating on the same data set (right panel).

| ACTUAL | predicted | ||

|---|---|---|---|

| failure | success | ||

| true | failure | 0.43 | 0.34 |

| success | 0.11 | 0.13 |

| RANDOM | predicted | ||

|---|---|---|---|

| failure | success | ||

| true | failure | 0.593 | 0.177 |

| success | 0.177 | 0.053 |

Classical ways to assess the prediction performance include the evaluation of accuracy, defined as the total percentage of correctly identified samples, sensitivity, defined as the percentage of successful start-ups correctly predicted by the classifier over the percentage of true successful start-ups, and precision, defined as the percentage of successful start-ups correctly predicted by the classifier over the total percentage of start-ups which are predicted as successful by the classifier. The F1 score is the harmonic average of precision and sensitivity. Depending on the context, it might be desirable for a classifier to have high sensitivity or precision, and when both quantities are relevant then the F1 score is typically used to assess model selection. In our case the sensitivity is the relevant quantity to look at if we want to maximise the detection of successful start-ups, whereas the precision is important if we want to make sure that all the start-ups classified as successful will be successful. In other words, the first performance indicator can be the one of relevance for an investment company with unlimited budget, while the precision can be of interest to an investment company with limited budget.

The values obtained for the different indicators are reported in Table S3. The F1 score –which trades off sensitivity and precision– shows that the predictions on whether any start-up in the open-deal list will have a positive outcome are systematically better than those of a benchmark given by a random classifier. Note that the problems with the accuracy are due to the fact that our two classes are unbalanced, and this can affect the usefulness of this indicator. We will come back to this point in the next subsection.

We have also experimented by including additional features of the evolution over time of the closeness centrality as predictors in the logistic regression model. Interestingly, our results did not improve significantly, suggesting that it is not necessary to use temporal evolution of centrality measures, and thus confirming the validity of the recommendation method. This observation will be further explored in the next subsection.

| Accuracy | Sensitivity | Precision | F1 score | |

| Unbalanced | 0.56 | 0.54 | 0.28 | 0.37 |

| Unbalanced (random classifier) | 0.65 | 0.31 | 0.31 | 0.31 |

| Balanced (single predictor) | 0.58 | 0.61 | 0.57 | 0.59 |

| Balanced (with temporal information) | 0.59 | 0.62 | 0.58 | 0.60 |

| Balanced (random classifier) | 0.5 | 0.5 | 0.5 | 0.5 |

S6.2 Logistic regression: the balanced case

It is well known that many binary classification algorithms suffer if the two classes are unbalanced, i.e. if the number of samples in each class is not similar. A classifier would then systematically try to fit the over-represented class and, as an outcome, the classification would be biased. Consider, e.g., the extreme case where the classifier assigns each sample to the over-represented class. In this extreme situation, the classifier would not be predicting anything, but the classification accuracy would still be very high due to class unbalance. For such a reason most classifiers do not perform well for unbalanced classes, and in unbalanced classification, accuracy can be a misleading metric. This is indeed our case, as in our data set the majority of start-ups do not end up being successful. Here, we show that, when we correct for class unbalancing, then the prediction performance substantially improves. In order to solve the issue of unbalanced classes, we downsample the over-represented class, so that the successful/non-succesful classification problem has now perfectly balanced () classes.

All over this section we use 5-fold crossvalidation. First we have considered that case where we only use the value of the closeness centrality of each start-up in the last month of our observation window, this being closer in spirit to the analysis performed in the main part of the manuscript. Again, the descriptor used is the closeness centrality rescaled ranking. The performance indicators of this logistic regression model are reported in Table S3, while the confusion matrix is shown in Table S4. Results confirm that prediction is indeed possible, and performance indicators are safely superior to random benchmarks.

| ACTUAL | predicted | ||

|---|---|---|---|

| failure | success | ||

| true | failure | 0.275 | 0.227 |

| success | 0.193 | 0.305 |

| RANDOM | predicted | ||

|---|---|---|---|

| failure | success | ||

| true | failure | 0.25 | 0.25 |

| success | 0.25 | 0.25 |

We have also considered

a second logistic regression model with predictors including various statistics

of the temporal sequence of closeness centralities in the observation

window. We have used the following 9 predictors based on

closeness centrality, namely:

maximum value, minimum value, slope of a linear interpolation and

last value of both the ranking and the rescaled ranking,

and number of months in the observation window).

The model provides an accuracy of

0.59, sensitivity 0.62 and precision 0.58, indicating that temporal

information leads to only a marginal improvement over the previous case.

Finally, we have investigated other

logistic regression models by further adding predictors related to

other centrality measures. We find that the performance is not boosted,

in agreement with the fact that in our case most of the other

centrality measures tend to be correlated to the closeness,

according to Fig.S11.

| 3i group | advanced technology ventures | accel partners |

| andreessen horowitz | atlas venture | atomico |

| august capital | austin ventures | avalon ventures |

| azure capital partners | bain capital ventures | balderton capital |

| battery ventures | benchmark | bessemer venture partners |

| binary venture partners | canvas venture fund | carmel ventures |

| charles river ventures | clearstone venture partners | columbus nova |

| costanoa venture capital | crosslink capital | crunchfund |

| data collective | digital sky technologies fo | draper fisher jurvetson |

| elevate ventures | ff venture capital | fidelity ventures |

| firstmark capital | first round capital | flybridge capital |

| foundation capital | founders fund | general catalyst partners |

| genesis partners | golden gate capital | ggv capital |

| google ventures | granite ventures | greylock partners israel |

| harris harris group | highland capital partners | idg ventures europe |

| idg ventures india | idg ventures vietnam | initial capital 2 |

| in q tel | index ventures | innovacom |

| insight venture partners | intel capital | intellectual ventures |

| institutional venture partners | inventus capital partners | jerusalem venture partners |

| jmi equity | kapor capital | kleiner perkins caufield byers |

| khosla ventures | lightspeed venture partners | lux capital |

| matrix partners | maveron | mayfield fund |

| menlo ventures | meritech capital partners | merus capital |

| morgenthaler ventures | new enterprise associates | norwest venture partners |

| oak investment partners | oregon angel fund | openview venture partners |

| polaris partners | radius ventures | redpoint ventures |

| revolution capital partners | rho ventures | finisterre capital |

| rre ventures | rothenberg ventures | sante ventures |

| scale venture partners | scottish investment bank | scottish equity partners |

| sequoia capital | seventure partners | sevin rosen funds |

| the social capital partnership | sofinnova partners | spark capital |

| tenaya capital | third rock ventures | tribeca global investments |

| union square ventures | us venture partners | vantagepoint capital partners |

| venrock | wellington partners |

Additional References

- 1.

- 2. V. Latora, V. Nicosia and G. Russo, Complex Networks: Principles, Methods and Applications (Cambridge University Press, 2017).

- 3. M. E. Newman, Mixing patterns in networks. Physical Review E, 67(2), 026126 (2003).

- 4. P. Erdös, A. Rényi, On random graphs I. Publicationes Mathematicae, 6, 290-297 (1959).

- 5. P. Erdös, A. Hajnal, On chromatic number of graphs and set-systems. Acta Mathematica Hungarica, bf 17(1), 61-99 (1966).

- 6. S. B. Seidman, Network structure and minimum degree. Social Networks, 5(3), 269-287 (1983).

- 7. S. Wasserman, K. Faust, Social Network Analysis: Methods and Applications (Cambridge University Press, Cambridge, 1994).

- 8. N. Lin 1976. Foundations of Social Research (McGraw-Hill, New York, 1976).

- 9. A. Skrondal, S. Rabe–Hesketh, Generalized Latent Variable Modeling: Multilevel, Longitudinal, and Structural Equation Models (Chapman & Hall/CRC Press, Boca Raton FL, 2004).

- 10. W. A. Thompson, On the treatment of grouped observations in life studies. Biometrics, 33, 463–470 (1977).

- 11. E. L. Kaplan, P. Meier, Nonparametric estimation from incomplete observations. Journal of the American Statistical Association, 53, 457–481 (1958).

- 12. D. R. Cox, Regression models and life-tables (with discussion). Journal of the Royal Statistical Society. Series B, 34, 187–220 (1972).