First passage time for Slepian process with linear barrier

Abstract

In this paper we extend results of L.A. Shepp by finding explicit formulas for the first passage probability , for all , where is a Gaussian process with mean 0 and covariance We then extend the results to the case of piecewise-linear barriers and outline applications to change-point detection problems. Previously, explicit formulas for were known only for the cases (constant barrier) or (short interval).

keywords:

[class=MSC]keywords:

arXiv:0000.0000 \pstVerbrealtime srand \startlocaldefs \endlocaldefs

,

1 Introduction

Let be a fixed real number and let , , be a Gaussian process with mean 0 and covariance

This process is often called Slepian process and can be expressed in terms of the standard Brownian motion by

| (1.1) |

Let and be fixed real numbers and . We are interested in an explicit formula for the first passage probability

| (1.2) |

note for .

The case of a constant barrier, when , has attracted significant attention in literature. In his seminal paper [1], D.Slepian has shown how to derive an explicit expression for in the case ; see also [2]. The case is much more complicated than the case . Explicit formulas for with general were derived by L. A. Shepp in [3]; these formulas are special cases of results formulated in Section 2.2 and 3.1. We believe our paper can be considered as a natural extension of the methodology developed in [1] and [3]; hence the title of this paper.

In the case , Slepian’s method for deriving formulas for can be easily extended to the case of a general linear barrier; see Section 7.1 for the discussion and formulas for with . For general , including the case , explicit formulas for were unknown. Derivation of these formulas is the main objective of this paper.

To do this, we generalise Shepp’s methodology of [3]. The principal distinction between Shepp’s methodology and our results is the use of an alternative way of computing coincidence probabilities. Shepp’s proofs heavily rely on the so-called Karlin-McGregor identity, see [4], but we use a different result formulated and discussed in Section 2.1.

The structure of the paper is as follows. In Section 2, we derive an expression for for integer and in Section 3 we extend the results for non-integral . In Sections 4 and 5, we extend the results to the case of piecewise-linear barriers. In Section 6, we outline an application to a change-point detection problem; this application was our main motivation for this research. In Appendix A, we discuss formulas for with and provide approximations for the ARL (average run length) in a change-point detection procedure. In Appendix B, we give two technical proofs.

2 Linear barrier with integral

In this Section, we derive an explicit formula for the first passage probability defined in (1.2) under the assumption that is a positive integer, . First, we formulate and slightly modify a general result from [5, p.40].

2.1 An important auxiliary result

Lemma 2.1.

For any and a positive integer , let , be independent Brownian Motion processes with drift parameters ; . Suppose and and let be infinitesimal intervals around . Construct the vectors , and . Then

| (2.1) | |||||

where denotes the Euclidean norm, denotes the scalar product and is the transition probability for the standard Brownian Motion with no drift,

| (2.2) |

Lemma 2.1 is an extension of the celebrated result of Karlin and McGregor on coincidence probabilities (see [4]) when applied specifically to Brownian Motion, and accommodates for different drift parameters of . Karlin-McGregor’s result can be applied to general strong Markov processes with continuous paths but no drifts. The transition probability for the process is , where is the transition density.

Corollary 2.1.

| (2.3) |

Proof. Using the relation and dividing both sides of (2.1) by , we obtain the result.

2.2 The main result

Let and be the density and the c.d.f. of the standard normal distribution. Assume that is a positive integer. Define -dimensional vectors

| (2.4) |

and let , and be -th components of vectors , a and c respectively (). Note that we start the indexation of vector components at 0.

Theorem 2.1.

In the case we obtain

2.3 An alternative representation of formula (2.5) and two particular cases

It is easier to interpret Theorem 2.1 by expressing the integrals in terms of the values of at times .

Let

For we set with .

It follows from the proof of (2.5), see Section 2.4, that have the meaning of the values of the process at times ; that is,

(). The range of the variables in (2.5) is , for . The variables are expressed via by

() with . Changing the variables, we obtain the following equivalent expression for the probability :

where is given by (2.4) but expressions for a and c change:

In a particular case of we obtain:

| (2.6) | |||||

which agrees with (7.1) in the Appendix A. For the case of we obtain:

2.4 Proof of Theorem 2.1

Using (1.1) we rewrite as

Let be the event defined as follows

and let , . Integrating out over the values , by the law of total probability we obtain:

| (2.7) | |||||

Note that , since and . For , define the processes

Then the event above can be equivalently expressed as

| (2.8) |

and under the conditioning introduced in (2.7), we have for :

Therefore (2.7) can expressed as

| (2.9) |

The region of integration for (2.4) is determined from the following chain of inequalities which ensure that the inequalities in (2.8) hold at and :

Hence, the upper limit of integration for all variables is infinity and the lower limit for the integral with respect to , , is given by the formula:

Since the conditioned Brownian Motion processes are independent, using (2.1) we can express the first term in (2.4) as

where , a and c are defined in (2.4). The second probability in the right hand side of (2.4) is simply . By noticing

and collating all terms, we obtain (2.5).

3 Linear barrier with non-integral

In this section, we shall derive an explicit formula for the first passage probability defined in (1.2) assuming is not an integer. Represent as , where is the integer part of and . Set .

3.1 The main result

Let and be as defined in (2.2). Define the - and -dimensional vectors as follows: is as defined in (2.4),

| (3.1) |

and let and be -th components of vectors and respectively (). Similarly, let and be -th components of vectors and respectively (). Recall that we start the indexation of vector components at 0.

Theorem 3.1.

For and non-integral with , we have

Proof is given below in Section 3.3.

If then the above formula for coincides with Shepp’s formula (2.25) in [3] expressed in variables and ().

3.2 Two particular cases of Theorem 3.1

Taking and hence yields the following

which agrees numerically with (7.1) in the Appendix for . Taking yields

3.3 Proof of Theorem 3.1

We are interested in an expression for the first passage probability

Using (1.1), can be equivalently expressed as follows

Let be the event

Then by integrating out over the values and of at times and , , by the law of total probability we have

| (3.3) | |||||

Note that , since and , and define the processes

Then the event can be equivalently expressed as with

Under the conditioning introduced in (3.3) we have for and :

Now under the above conditioning the processes are independent and so the conditional probability of in (3.3) becomes a product of the conditional probabilities of and . Therefore, (3.3) becomes

| (3.4) | |||||

The region of integration for the variables in (3.4) is determined from the following chain of inequalities:

Whence, the upper limit of integration with respect to is infinity and the lower limit for the integral with respect to , is given by the formula . For the variables in (3.4), we have the following chain of inequalities

Once again, the upper limit of integration with respect to is infinity and the lower limit for the integral with respect to () is . For , the upper and lower limits of integration are infinite.

4 Piecewise linear barrier with one change of slope

4.1 Formulation of the main result

In this section, we derive an explicit formula for the first passage probability for with a continuous piecewise linear barrier, where not more than one change of slope is allowed. For any non-negative and real we define the piecewise-linear barrier by

for an illustration of this barrier, see Figure 1. We are interested in finding an expression for the first passage probability

| (4.1) |

We only consider the case when both and are integers. The case of general can be treated similarly but the resulting expressions are much more complicated.

Define the -dimensional vectors as follows:

| (4.2) |

| (4.3) |

and let and be -th components of vectors and respectively ().

Theorem 4.1.

For and any positive integers and , we have

| (4.4) |

4.2 Two particular cases of Theorem 4.1

Below we consider two particular cases of Theorem 4.1; first, the barrier is with ; second, the barrier is with . See Figures 3 and 3 for a depiction of both barriers. As we shall demonstrate in Section 6, these cases are important for problems of change-point detection.

For , Theorem 4.1 provides:

| (4.6) | |||||

5 Piecewise linear barrier with two changes in slope

5.1 Formulation of the main result

Theorem 4.1 can be generalized to the case when we have more than one change in slope. In the general case, the formulas for the first-passage probability become very complicated; they are already rather heavy in the case of one change in slope.

In this section, we consider just one particular barrier with two changes in slope. For real , define the barrier as

As will be explained in Section 6, the corresponding first-passage probability

| (5.1) |

is important for some change-point detection problems.

Define the four-dimensional vectors as follows:

| (5.2) |

and let and be -th components of vectors and respectively ().

Proposition 5.1.

For and any real and

| (5.3) | |||||

5.2 A particular case of Proposition 5.1

In this section, we consider a special barrier (depicted in Figure 4), which will be used in Section 6. In the notation of Proposition 5.1, , , , and we obtain

| (5.4) |

6 Application to change-point detection

In this section, we illustrate the natural appearance of first-passage probabilities for the Slepian process for piece-wise barriers and in particular the barriers considered in Sections 4.2 and 5.2.

Suppose one can observe the stochastic process governed by the stochastic differential equation

| (6.1) |

where is the unknown (non-random) change-point and is the drift magnitude during the ‘epidemic’ period of duration with ; and may be known or unknown. The classical change-point detection problem of finding a change in drift of a Wiener process is the problem (6.1) with ; that is, when the change (if occurred) is permanent, see for example [6, 7, 8, 9].

In (6.1), under the null hypothesis , we assume meaning that the process has zero mean for all . On the other hand, under the alternative hypothesis , . In the definition of the test power, we will assume that is large. However, for the tests discussed below to be well-defined and approximations to be accurate, we only need (under ).

In this section, we only consider the case of known , in which case we can assume (otherwise we change the time-scale by and the barrier by ). The case when is unknown is more complicated and the first-passage probabilities that have to be used are more involved; even so, these probabilities can be treated by the methodology similar to the one discussed below.

We define the test statistic used to monitor the epidemic alternative as

The stopping rule for is defined as follows

| (6.2) |

where the threshold is chosen to satisfy the average run length (ARL) constraint for some (usually large) fixed . Here denote the expectation under the null hypothesis.

Under , for all and under we have

The problem of construction of accurate approximations for relies on the construction of accurate approximations for the first-passage probabilities for the Slepian process with constant barrier and large . This problem was addressed in [10], where several accurate approximations were constructed. As a result, we can derive an accurate approximation for , see Section 7.2. For example, to get we need . Since is known, for any the test with the stopping rule (6.2) is optimal in the sense of the abstract Neyman-Pearson lemma, see Theorem 2, [11, p 110].

Here we are interested in the power of the test (6.2) which can be defined as

| (6.3) |

where denotes the probability measure under the alternative hypothesis.

Define the piecewise linear barrier as follows

The barrier is visually depicted in Fig 6 below. The power of the test with the stopping rule (6.2) is then

Consider the barrier of Section 5 with . Define the conditional first-passage probability

| (6.4) |

The denominator in (6.4) is very simple to compute, see (2.6) with and . The numerator in (6.4) can be computed by (5.2). Computation of requires numerical evaluation of a two-dimensional integral, which is not difficult.

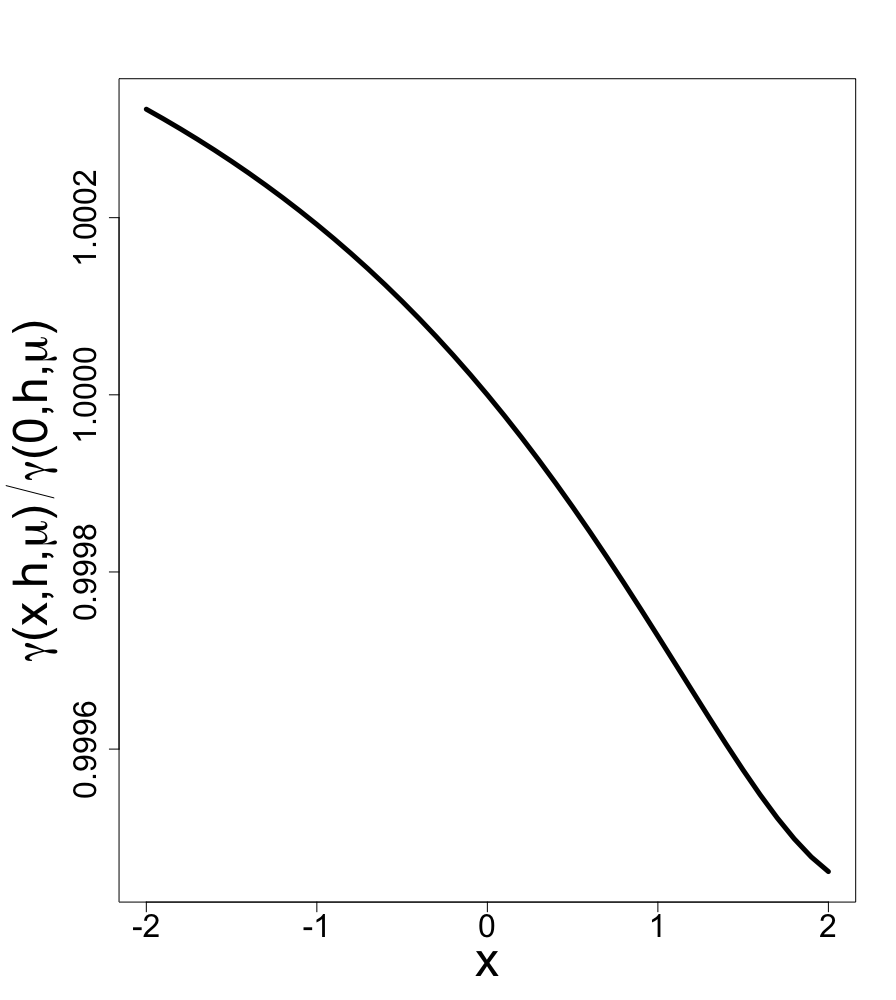

We approximate the power by . In view of (1.1) the process forgets the past after one unit of time hence quickly reaches the stationary behaviour under the condition for all . By approximating with , we assume that one unit of time is almost enough for to reach this stationary state. In Figure 6, we plot the ratio as a function of for and . Since the ratio is very close to 1 for all considered , this verifies that the probability changes very little as varies implying that the values of at have almost no effect on the probability . This allows us to claim that the accuracy of the approximation is smaller than for all . This claim agrees with discussions below in this section and extensive simulations which we have performed. This claim also agrees with Table 2 in [10] (the row corresponding to ), from where we deduce that the accuracy of approximation is smaller than for all and ; it is also intuitively clear that the accuracy of the approximation improves as grows.

In Table 1, we provide values of for different , where the values of have been chosen to satisfy for ; see (7.4) regarding computation of the ARL .

As seen from Figures 3 and 4, the barrier is the main component of the barrier . Instead of using the approximation it is therefore tempting to use a simpler approximation , where

To compute values of we only need to evaluate a one-dimensional integral. Table 2 we show some values of for different . Comparing the entries of Tables 1 and 2 we can observe that the quality of is not too bad, especially for large .

Approximation can be improved if we average values of over an appropriate distribution for . According to Section 2.4.2 in [10], one of possible appropriate distributions for has density

Define , which is a two-dimensional integral. As seen from comparison of Tables 1 and 3, the accuracy of the approximation is almost the same as the accuracy of the main approximation . Computational cost of computing is similar to the cost for .

To assess the impact the final line-segment in the barrier on power (the line-segment with gradient in Fig 6, ), in Table 4 we document the values of for different . Here

and can be computed using (4.6) with . By comparing Tables 1 and 4, one can see the expected diminishing impact which the final line-segment in has on power, as increases. However, for small the contribution of this part of the barrier to power is significant suggesting it is not be sensible to approximate the power of our test with .

| , | |

|---|---|

| 2 | 0.3052 |

| 2.25 | 0.3876 |

| 2.5 | 0.4765 |

| 2.75 | 0.5676 |

| 3 | 0.6559 |

| 3.25 | 0.7371 |

| 3.5 | 0.8075 |

| 3.75 | 0.8653 |

| 4 | 0.9101 |

| 4.25 | 0.9429 |

| 4.5 | 0.9655 |

| 4.75 | 0.9802 |

| 5 | 0.9892 |

| , | |

|---|---|

| 2 | 0.1384 |

| 2.25 | 0.1946 |

| 2.5 | 0.2638 |

| 2.75 | 0.3445 |

| 3 | 0.4338 |

| 3.25 | 0.5272 |

| 3.5 | 0.6197 |

| 3.75 | 0.7061 |

| 4 | 0.7824 |

| 4.25 | 0.8461 |

| 4.5 | 0.8961 |

| 4.75 | 0.9332 |

| 5 | 0.9592 |

| , | |

|---|---|

| 2 | 0.0956 |

| 2.25 | 0.1402 |

| 2.5 | 0.1979 |

| 2.75 | 0.2687 |

| 3 | 0.3510 |

| 3.25 | 0.4416 |

| 3.5 | 0.5358 |

| 3.75 | 0.6285 |

| 4 | 0.7146 |

| 4.25 | 0.7900 |

| 4.5 | 0.8525 |

| 4.75 | 0.9011 |

| 5 | 0.9370 |

| , | |

|---|---|

| 2 | 0.2918 |

| 2.5 | 0.4645 |

| 3 | 0.6471 |

| 3.5 | 0.8021 |

| 4 | 0.9075 |

| 4.5 | 0.9644 |

| 5 | 0.9889 |

| , | |

|---|---|

| 2 | 0.1310 |

| 2.5 | 0.2553 |

| 3 | 0.4256 |

| 3.5 | 0.6132 |

| 4 | 0.7783 |

| 4.5 | 0.8940 |

| 5 | 0.9583 |

| , | |

|---|---|

| 2 | 0.0903 |

| 2.5 | 0.1911 |

| 3 | 0.3438 |

| 3.5 | 0.5295 |

| 4 | 0.7101 |

| 4.5 | 0.8499 |

| 5 | 0.9358 |

| , | |

|---|---|

| 2 | 0.3047 |

| 2.5 | 0.4760 |

| 3 | 0.6555 |

| 3.5 | 0.8073 |

| 4 | 0.9100 |

| 4.5 | 0.9654 |

| 5 | 0.9892 |

| , | |

|---|---|

| 2 | 0.1383 |

| 2.5 | 0.2637 |

| 3 | 0.4337 |

| 3.5 | 0.6196 |

| 4 | 0.7824 |

| 4.5 | 0.8961 |

| 5 | 0.9592 |

| , | |

|---|---|

| 2 | 0.0956 |

| 2.5 | 0.1978 |

| 3 | 0.3509 |

| 3.5 | 0.5358 |

| 4 | 0.7146 |

| 4.5 | 0.8524 |

| 5 | 0.9370 |

| , | |

|---|---|

| 2 | 0.2389 |

| 2.5 | 0.4017 |

| 3 | 0.5873 |

| 3.5 | 0.7567 |

| 4 | 0.8801 |

| 4.5 | 0.9514 |

| 5 | 0.9840 |

| , | |

|---|---|

| 2 | 0.1039 |

| 2.5 | 0.2131 |

| 3 | 0.3731 |

| 3.5 | 0.5611 |

| 4 | 0.7373 |

| 4.5 | 0.8685 |

| 5 | 0.9458 |

| , | |

|---|---|

| 2 | 0.0708 |

| 2.5 | 0.1575 |

| 3 | 0.2974 |

| 3.5 | 0.4785 |

| 4 | 0.6657 |

| 4.5 | 0.8194 |

| 5 | 0.9192 |

7 Appendix A

7.1 First-passage probability for

For , the first passage probability has been well studied. An explicit formula was first derived in 1988 in [12, p.81] (published in Russian) and more than 20 years later it was independently derived in [13] and [14]. The authors of [12] and [14] also considered the case of piecewise-linear barriers.

In [12], the first passage probability for was obtained by using the fact is a conditionally Markov process on the interval . It was shown in [2] that after conditioning on , can be expressed in terms of Brownian Motion as follows

with . From this it follows that for

Noting that and using the well known barrier crossing formula for the Brownian motion (see e.g. [15])

| (7.1) |

where , and . This methodology, like many others, fails for .

7.2 An approximation for

Consider the unconditional probability (taken with respect to the standard normal distribution):

Under , the distribution of has the form:

where is the delta-measure concentrated at 0 and

is the first-passage density. This yields

| (7.2) |

There is no easy computationally convenient formula for as expressions for are very complex. For deriving approximations for we apply approximations for , discussed in [10]. One of the simplest (yet very accurate) approximation takes the following form:

| (7.3) |

with . Values of must be numerically computed; approximations and simpler forms of have been presented in [10] should one require an explicit formula. Using (7.3), we approximate the density by

Evaluation of the integral in (7.2) yields

| (7.4) |

Numerical study shows that the approximation (7.4) is very accurate for all .

8 Appendix B

8.1 Proof of (4.1)

The proof of (4.1) follows similar steps to the proof of (2.5). The event becomes

As in the proof of (2.5), let , , where . Then

| (8.1) | |||||

Define the following processes which take different forms depending on the value of :

for , with for all processes. The event can now be expressed as

| (8.2) |

Under the conditioning introduced in (8.1), depending on the size of we have: for

and for

Whence (8.1) can be expressed as

| (8.3) | |||||

The region of integration in (8.3) is determined from the following inequalities which, like in the proof of (4.1), ensure that the inequalities in (8.2) hold at and :

From this, the upper limit of integration is infinity for all . For , the lower limit for is . For , the lower limit for is .

8.2 Proof of (5.3)

Like the proof of (4.1), the proof of (5.3) is similar to the proof of (2.5). We modify the event as follows:

By the law of total probability,

| (8.4) | |||||

Define individually the following processes:

with for all processes. The event can be re-written as

| (8.5) |

The conditioning introduced in (8.4) results in:

From this, we can express (8.4) as:

| (8.6) | |||||

The region of integration for (8.6) is determined from the following inequalities (see proof of (2.5) for similar discussion):

Thus, the upper limit of integration is infinity for all . For integration with respect to , the lower limit is . For integration with respect , the lower limit is . Finally, for , the lower limit is . Now using (2.1) with we obtain

, and are given in (5.2). The second probability in the right hand side of (8.6) is . Using the fact

and collecting all results we complete the proof.

References

- [1] D. Slepian. First passage time for a particular Gaussian process. The Annals of Mathematical Statistics, 32(2):610–612, 1961.

- [2] C.B. Mehr and J.A. McFadden. Certain properties of Gaussian processes and their first-passage times. Journal of the Royal Statistical Society. Series B (Methodological), 27(3):505–522, 1965.

- [3] L. Shepp. First passage time for a particular Gaussian process. The Annals of Mathematical Statistics, 42(3):946–951, 1971.

- [4] S. Karlin and J. McGregor. Coincidence probabilities. Pacific Journal of Mathematics, 9(4):1141–1164, 1959.

- [5] M. Katori. Reciprocal time relation of noncolliding Brownian motion with drift. Journal of Statistical Physics, 148(1):38–52, 2012.

- [6] M. Pollak and D. Siegmund. A diffusion process and its applications to detecting a change in the drift of Brownian motion. Biometrika, 72(2):267–280, 1985.

- [7] G. Moustakides. Optimality of the CUSUM procedure in continuous time. The Annals of Statistics, 32(1):302–315, 2004.

- [8] A. Polunchenko. Asymptotic near-minimaxity of the randomized Shiryaev–Roberts–Pollak change-point detection procedure in continuous time. Theory of Probability & Its Applications, 62(4):617–631, 2018.

- [9] A. Polunchenko and A. Tartakovsky. On optimality of the Shiryaev–Roberts procedure for detecting a change in distribution. The Annals of Statistics, 38(6):3445–3457, 2010.

- [10] J. Noonan and A. Zhigljavsky. Approximating Shepp’s constants for the Slepian process. arXiv preprint arXiv:1812.11101, 2018.

- [11] U. Grenander. Abstract inference. John Wiley & Sons, 1981.

- [12] A. Zhigljavsky and A. Kraskovsky. Detection of abrupt changes of random processes in radiotechnics problems. St. Petersburg University Press, 1988. (in Russian).

- [13] W. Bischoff and A. Gegg. Boundary crossing probabilities for (q, d)-Slepian-processes. Statistics & Probability Letters, 118:139–144, 2016.

- [14] P. Deng. Boundary non-crossing probabilities for Slepian process. Statistics & Probability Letters, 122:28–35, 2017.

- [15] D. Siegmund. Boundary crossing probabilities and statistical applications. The Annals of Statistics, 14(2):361–404, 1986.