Pricing under Fairness Concerns

This paper proposes a theory of pricing premised upon the assumptions that customers dislike unfair prices—those marked up steeply over cost—and that firms take these concerns into account when setting prices. Since they do not observe firms’ costs, customers must extract costs from prices. The theory assumes that customers infer less than rationally: when a price rises due to a cost increase, customers partially misattribute the higher price to a higher markup—which they find unfair. Firms anticipate this response and trim their price increases, which drives the passthrough of costs into prices below one: prices are somewhat rigid. Embedded in a New Keynesian model as a replacement for the usual pricing frictions, our theory produces monetary nonneutrality: when monetary policy loosens and inflation rises, customers misperceive markups as higher and feel unfairly treated; firms mitigate this perceived unfairness by reducing their markups; in general equilibrium, employment rises. The theory also features a hybrid short-run Phillips curve, realistic impulse responses of output and employment to monetary and technology shocks, and an upward-sloping long-run Phillips curve.

Introduction

Prices are neither exactly fixed nor fully responsive to cost shocks (Carlsson and Skans 2012; De Loecker et al. 2016; Caselli, Chatterjee, and Woodland 2017; Ganapati, Shapiro, and Walker 2020). Such price rigidity has first-order importance by determining how economic shocks percolate through the economy as well as the effectiveness of different policy responses.

Asked why they show such restraint when setting prices, firm managers explain that they endeavor to avoid alienating customers, who balk at paying prices that they regard as unfair (Blinder et al. 1998). Yet theories of price rigidity never include fairness considerations (Blanchard 1990; Mankiw and Reis 2010), with the notable exception of the theory by Rotemberg (2005), which calls attention to the role of fairness in pricing.111Fairness has received more attention in other contexts: Akerlof (1982), Akerlof and Yellen (1990), and Benjamin (2015) add fairness to labor-market models; Rabin (1993), Fehr and Schmidt (1999), and Charness and Rabin (2002) to game-theoretic models; and Fehr, Klein, and Schmidt (2007) to contract-theoretic models. For surveys of the fairness literature, see Fehr and Gachter (2000), Sobel (2005), and Fehr, Goette, and Zehnder (2009). Due to its innovative nature, however, that theory is somewhat difficult to analyze or use in other frameworks (see Section 2).

This paper develops a theory of pricing that incorporates the fairness concerns exhibited by firms and their customers and uses such concerns to generate the price rigidity observed in the data. The theory permits closed-form expressions for price markups and passthroughs, as well as a set of comparative statics. It also transfers easily to other frameworks: here, we port it to a New Keynesian model to study the macroeconomic implications.

The first element of our theory is that customers dislike paying prices marked up heavily over marginal costs because they find these prices unfair, and that firms understand this. This assumption draws upon evidence from numerous surveys of consumers and firms, our own survey of French bakers, and religious and legal texts (Section 3). We formalize this assumption by weighting each unit of consumption in the utility function by a fairness factor which depends upon the markup that customers perceive firms as charging: the fairness factor decreases in the perceived markup—higher markups seem less fair—and is concave—people respond more strongly to increases in markups than to decreases.

Customers who cannot observe firms’ costs estimate these costs from prices, and then use their estimates to evaluate firms’ fairness. The second element of our theory is that customers update their beliefs about marginal costs less than rationally. First, customers underinfer marginal cost from price: their beliefs depend upon some anchor, which may be their prior expectation of marginal cost. Second, insofar as customers do update their beliefs about marginal cost from price, they engage in a form of proportional thinking by estimating a marginal cost that is proportional to price. We dub this pair of assumptions subproportional inference. They draw upon evidence that during inflationary periods people seem to underinfer increases in nominal costs, and more generally that people tend to infer less than they should about others’ private information from others’ actions (see also Section 3).

We begin our analysis by embedding these psychological elements into a model of monopoly pricing (Section 4). The monopolist’s price features a markup that decreases in the price elasticity of demand. We assume a standard utility function, with the property that customers without fairness concerns would exhibit constant price elasticity of demand.

Absent fairness concerns, the monopolist would set a constant markup that produces flexible prices, which move proportionally to marginal costs. If customers cared about fairness and rationally inverted the price to uncover the hidden marginal cost, the same pricing rule would be an equilibrium. Indeed, when price increases by , customers correctly infer that marginal cost has increased by , and therefore that the markup has not changed. Since the price change does not change the perceived markup, the price elasticity of demand does not change, and neither does the markup.

Once fairness concerns and subproportional inference come together, however, pricing changes. First, demand is more price elastic than it would be otherwise, leading the monopoly to lower its markup. Indeed, demand decreases in price not only through the standard channel, but also through a fairness channel. Customers who see a higher price attribute it partially to a higher marginal cost and partially to a higher markup—which they find unfair. Thus the higher price lowers their marginal utility of consumption, which further decreases demand.

Second, demand is more price elastic at higher perceived markups, creating price rigidity. Following a price increase spurred by a cost increase, customers underappreciate the increase in marginal cost and partially misattribute the higher price to higher markup. Since the fairness factor is decreasing and concave in the perceived markup, it is more elastic at higher perceived markups; this property translates to demand. Facing a more elastic demand after the cost increase, the monopoly reduces its markup. As a result, the price increases less than proportionally to the underlying marginal cost. This mild form of price rigidity agrees with the passthroughs of marginal-cost shocks into prices estimated in empirical studies.

Price rigidity plays a central role in many macroeconomic models. To illustrate how our theory can be embedded into such models, and to develop its implications, we substitute it for the usual pricing frictions in a New Keynesian model (Section 5). Again we assume that customers infer less than they should about marginal cost from price. In the dynamic model, subproportional inference means that in each period, customers average their previous-period beliefs about marginal costs with beliefs that are proportional to current prices.

The macroeconomic model makes several realistic predictions. First, monetary policy is nonneutral in the short run: it affects output and employment. This property arises through the same channel as in the monopoly model: expansionary monetary policy raises prices and nominal marginal costs; customers partially misattribute higher prices to higher markups, which they perceive as unfair; as a result, the price elasticities of the demands for goods rise; firms respond by reducing markups, thus stimulating the economy. Second, the New Keynesian Phillips curve is hybrid: it links current employment not only to current and to expected future inflation, but also to past inflation. The reason is that consumers form backward-looking beliefs about marginal costs, which forces firms to account for both past and future inflation when setting prices. Third, the model yields reasonable impulse responses to monetary shocks and to technology shocks when the parameters governing fairness concerns and subproportional inference are calibrated to match the microevidence on cost passthroughs. In particular, the impulse responses of employment are hump-shaped. Fourth, monetary policy is nonneutral in the long run: higher steady-state inflation leads to higher steady-state employment; that is, the long-run Phillips curve is nonvertical.

Our macroeconomic model is also consistent with survey evidence that inflation angers people—who attribute it to commercial greed—whereas deflation pleases people. In our model, because people partially misattribute higher prices to higher markups, inflation leads them to perceive transactions as less fair, generating disutility. Conversely, deflation leads people to misperceive markups as lower and deem transactions more fair, generating utility.

Related Literature

Rotemberg (2005) developed the first theory of price rigidity based on fairness considerations.222Rotemberg (2011) explores other implications of fairness for pricing, such as price discrimination. Customers in his model care about firms’ altruism, which they evaluate following every price change. They purchase a normal amount from a firm unless they can reject the hypothesis that the firm is sufficiently altruistic, in which case they withhold demand entirely to lower the firm’s profits. Profit-maximizing firms react to the discontinuity in demand by refraining from passing on small cost increases, creating price stickiness. Consumers err in equilibrium by mistaking purely selfish firms as altruistic.

We depart from Rotemberg’s discontinuous, buy-normally-or-buy-nothing formulation to one in which customers continuously reduce demand as the unfairness of the transaction increases. Our continuous formulation seems more realistic and offers greater tractability. The tractability allows for closed-form expressions for the markup and passthrough, and thus to obtain a range of comparative statics. The tractability also allows us to embed our pricing theory into a New Keynesian model, to calibrate the theory’s parameters based on microevidence, and to perform standard simulations.

More broadly, our approach to fairness differs from the popular social-preferences approach, both the intention-based model of Rabin (1993) and the distribution-based model of Fehr and Schmidt (1999). Like Rotemberg’s model, these models predict that consumers endeavor to harm firms by withholding demand to lower profits in certain circumstances—namely when the firm treats consumers unkindly (Rabin 1993), and when the firm receives a higher payoff than consumers (Fehr and Schmidt 1999). In our model, by contrast, because customers simply do not savor unfairly priced goods, they withhold demand irrespective of any harm to the firm. An advantage of our approach, which appears in its macroeconomic application, is that fairness continues to matter in general equilibrium. This is not the case with many social preferences: when people’s utility can be written as a separable function of their own and others’ allocations, social preferences do not affect general-equilibrium prices or allocations (Dufwenberg et al. 2011; Sobel 2007).

Microevidence Supporting the Assumptions

This section presents microevidence in support of the assumptions underlying our theory. First, we show that people care about the fairness of prices, and assess prices that include low markups over marginal costs as fair. Second, we document that people erroneously infer marginal costs from prices and thus misperceive markups. Finally, we show that firms account for customers’ fairness concerns when setting prices.

Customers’ Fairness Concerns

Our theory assumes that customers find a price unfair when it entails a high markup over marginal cost, and that they dislike such prices. Here we review evidence supporting this assumption.

Price Increases Due to Higher Demand

Our assumption implies that people find price increases unjustified by cost increases to be unfair. In a survey of Canadian residents, Kahneman, Knetsch, and Thaler (1986, p. 729) document this pattern. They describe the following situation: “A hardware store has been selling snow shovels for $15. The morning after a large snowstorm, the store raises the price to $20.” Among 107 respondents, only 18% regard this pricing as acceptable, whereas 82% regard it as unfair.

Subsequent studies confirm and refine Kahneman, Knetsch, and Thaler’s results. For example, in a survey of 1,750 households in Switzerland and Germany, Frey and Pommerehne (1993) confirm that customers dislike price increases that involve increased markups; so too do Shiller, Boycko, and Korobov (1991) in a comparative survey of 391 respondents in Russia and 361 in the United States.

The snow-shovel evidence leaves open the possibility that people find the price increase unfair simply because it occurs during a period of hardship. To address this question, Maxwell (1995) asks 72 students at a Florida university about price increases following an ordinary increase in demand versus those following a hardship-driven increase in demand. While more find price increases in the hardship environment unfair (86% versus 69%), a substantial majority in each case perceive the price increase as unfair.

Price Increases Due to Higher Costs

Conversely, our fairness assumption suggests that customers tolerate price increases following cost increases so long as the markup remains constant. Kahneman, Knetsch, and Thaler (1986, pp. 732–733) identify this pattern: “Suppose that, due to a transportation mixup, there is a local shortage of lettuce and the wholesale price has increased. A local grocer has bought the usual quantity of lettuce at a price that is 30 cents per head higher than normal. The grocer raises the price of lettuce to customers by 30 cents per head.” Among 101 respondents, 79% regard the pricing as acceptable, and only 21% find it unfair. In a survey of 307 Dutch individuals, Gielissen, Dutilh, and Graafland (2008, Table 2) also find that price increases following cost increases are fair, while those following demand increases are not.

Price Decreases Allowed by Lower Costs

Our assumption equally implies that it is unfair for firms not to pass along cost decreases. Kahneman, Knetsch, and Thaler (1986, p. 734) find milder support for this reaction. They describe the following situation: “A small factory produces tables and sells all that it can make at $200 each. Because of changes in the price of materials, the cost of making each table has recently decreased by $20. The factory does not change its price of tables.” Only 47% of respondents find this unfair, despite the elevated markup.

Subsequent studies, however, find that people do expect price reductions after cost reductions. Kalapurakal, Dickson, and Urbany (1991) survey 189 US business students, asking them to consider the following scenario: “A department store has been buying an oriental floor rug for $100. The standard pricing practice used by department stores is to price floor rugs at double their cost so the selling price of the rug is $200. This covers all the selling costs, overheads and includes profit. The department store can sell all of the rugs that it can buy. Suppose because of exchange rate changes the cost of the rug rises from $100 to $120 and the selling price is increased to $220. As a result of another change in currency exchange rates, the cost of the rug falls by $20 back to $100.” Then two alternative scenarios were evaluated: “The department store continues to sell the rug for $220” compared to “The department store reduces the price of the rug to $200.” The latter was judged significantly fairer: the fairness rating was instead of (where is extremely unfair and extremely fair). Similarly, in survey of US respondents, Konow (2001, Table 6) finds that if a factory that sells a table at $150 locates a supplier charging $20 less for materials, the new fair price is $138, well below $150.

Norms about Markups

Religious and legal texts written over the ages display a long history of norms regarding markups—which suggests that people deeply care about markups. For example, Talmudic law specifies that the highest fair and allowable markup when trading essential items is 20% of the production cost, or one-sixth of the final price (Friedman 1984, p. 198).

Another example comes from 18th-century France, where local authorities fixed bread prices by publishing “fair” prices in official decrees. In the city of Rouen, for instance, the official bread prices took the costs of grain, rent, milling, wood, and labor into account, and granted a “modest profit” to the baker (Miller 1999, p. 36). Thus, officials fixed the markup that bakers could charge. Even today, French bakers attach such importance to convincing their customers of fair markups that their trade union decomposes the cost of bread and the rationale for any price rise into minute detail (https://perma.cc/GQ28-JMFC).

Two more examples come from regulation in the United States. First, return-on-cost regulation for public utilities, which limits the markups charged by utilities, has been justified not only on efficiency grounds but also on fairness grounds (Zajac 1985; Jones and Mann 2001). Second, most US states have anti-price-gouging legislation that limits the prices that firms can charge in periods of upheaval (such as an epidemic). But by exempting price increases justified by higher costs, the legislation only outlaws price increases caused by higher markups (Rotemberg 2009, pp. 74–77).

Fairness and Willingness to Pay

We assume that customers who purchase a good at an unfair price derive less utility from consuming it; as a result, unfair pricing reduces willingness to pay. Substantial evidence documents that unfair prices make customers angry, and more generally that unfair outcomes trigger feelings of anger (Rotemberg 2009, pp. 60–64). A small body of evidence also suggests that customers reduce purchases when they feel unfairly treated. In a telephone survey of 40 US consumers, Urbany, Madden, and Dickson (1989) explore—by looking at a 25-cent ATM surcharge—whether a price increase justified by a cost increase is perceived as more fair than an unjustified one, and whether fairness perceptions affect customers’ propensity to buy. While 58% of respondents judge the introduction of the surcharge fair when justified by a cost increase, only 29% judge it fair when not justified (Table 1, panel B). Moreover, those people who find the surcharge unfair are indeed more likely to switch banks (52% versus 35%; see Table 1, panel C). Similarly, Piron and Fernandez (1995) present survey and laboratory evidence that customers who find a firm’s actions unfair tend to reduce their purchases with that firm.

Fixed Costs

A natural question is whether the fair price would differ from a fair markup over marginal cost for businesses that have significant fixed costs. The literature almost exclusively reports on experiments with marginal costs and without fixed costs, so we cannot say how people would incorporate fixed costs into the fair price. Anecdotal evidence, however, points towards people caring directly about marginal costs. Ride-sharers outraged by Uber’s surge pricing seldom mention that Uber has never reported a profit. Likewise, consumers deplore pharmaceutical companies for selling pills with very low marginal costs at high markups, without mention of R&D expenses. In light of the evidence, we focus on marginal costs and abstract from fixed costs in the analysis.

Subproportional Inference of Costs

Because customers do not observe firms’ marginal costs, their fairness perceptions depend upon their estimates of these costs. Since customers cannot easily learn about hidden costs, however, they are prone to develop mistaken beliefs. To describe such misperceptions, we assume subproportional inference. First, consumers underinfer marginal costs from prices: their beliefs depend too much upon some anchor. Second, insofar as consumers do update their beliefs about costs from prices, they engage in a form of proportional thinking by estimating marginal costs that are proportional to prices. We now review evidence that supports this pair of assumptions.

Underinference in General

Numerous experimental studies establish that people underinfer other people’s information from those other people’s actions (Eyster 2019). In the context of bilateral bargaining with asymmetric information, Samuelson and Bazerman (1985), Holt and Sherman (1994), Carillo and Palfrey (2011), and others show that bargainers underappreciate the adverse selection in trade. The papers collected in Kagel and Levin (2002) present evidence that bidders underattend to the winner’s curse in common-value auctions. In a metastudy of social-learning experiments, Weizsaecker (2010) finds that subjects behave as if they underinfer their predecessors’ private information from their actions. In a voting experiment, Esponda and Vespa (2014) show that people underinfer others’ private information from their votes. Subproportional inference encompasses such underinference.

Underinference from Prices

Shafir, Diamond, and Tversky (1997) report survey evidence that points at underinference in the context of pricing. They presented 362 people in New Jersey with the following thought experiment: “Changes in the economy often have an effect on people’s financial decisions. Imagine that the US experienced unusually high inflation which affected all sectors of the economy. Imagine that within a six-month period all benefits and salaries, as well as the prices of all goods and services, went up by approximately 25%. You now earn and spend 25% more than before. Six months ago, you were planning to buy a leather armchair whose price during the 6-month period went up from $400 to $500. Would you be more or less likely to buy the armchair now?” The higher prices were distinctly aversive: while 55% of respondents were as likely to buy as before and 7% were more likely, 38% of respondents were less likely to buy (p. 355). Our model makes this prediction. While consumers who update subproportionally recognize that higher prices signal higher marginal costs, they stop short of rational inference. Consequently, consumers perceive markups to be higher when prices are higher. These consumers deem today’s transaction less fair, so they have a lower willingness to pay for the armchair.

Proportional Thinking

A small body of evidence documents that people think proportionally, even in settings that do not call for proportional thinking (Bushong, Rabin, and Schwartzstein 2020). In particular, Thaler (1980) and Tversky and Kahneman (1981) demonstrate that people’s willingness to invest time in lowering the price of a good by a fixed dollar amount depends negatively upon the good’s price. Rather than care about the absolute savings, people appear to care about the proportional savings. Someone who thinks about a price discount not in absolute terms but as a proportion of the purchase price may think about marginal cost not in absolute terms but rather as a percentage of price. If so, then the simplest assumption is that, insofar as the person infers marginal cost from price, she infers a marginal cost proportional to price.

Firms’ Fairness Concerns

| Survey | Country | Period | Number of firms |

|---|---|---|---|

| Blinder et al. (1998) | United States (US) | 1990–1992 | 200 |

| Hall, Walsh, and Yates (2000) | United Kingdom (GB) | 1995 | 654 |

| Apel, Friberg, and Hallsten (2005) | Sweden (SE) | 2000 | 626 |

| Nakagawa, Hattori, and Takagawa (2000) | Japan (JP) | 2000 | 630 |

| Amirault, Kwan, and Wilkinson (2006) | Canada (CA) | 2002–2003 | 170 |

| Kwapil, Baumgartner, and Scharler (2005) | Austria (AT) | 2004 | 873 |

| Aucremanne and Druant (2005) | Belgium (BE) | 2004 | 1,979 |

| Loupias and Ricart (2004) | France (FR) | 2004 | 1,662 |

| Lunnemann and Matha (2006) | Luxembourg (LU) | 2004 | 367 |

| Hoeberichts and Stokman (2006) | Netherlands (NL) | 2004 | 1,246 |

| Martins (2005) | Portugal (PT) | 2004 | 1,370 |

| Alvarez and Hernando (2005) | Spain (ES) | 2004 | 2,008 |

| Langbraaten, Nordbo, and Wulfsberg (2008) | Norway (NO) | 2007 | 725 |

| Olafsson, Petursdottir, and Vignisdottir (2011) | Iceland (IS) | 2008 | 262 |

In our model, firms pay great attention to fairness when setting prices. This seems to hold true in the real world: firms identify fairness as a major concern in price setting.

Surveys of Firms

Following Blinder et al. (1998), researchers have surveyed more than 12,000 firms across developed economies about their pricing practices (Table 1). The typical study asks managers to evaluate the relevance of different pricing theories from the economics literature to explain their own pricing, in particular price rigidity. Amongst the theories that the managers deem most important, some version of fairness invariably appears, often called “implicit contracts” and described as follows: “firms tacitly agree to stabilize prices, perhaps out of fairness to customers.” Indeed, fairness appeals to firms more than any other theory, with a median rank of 1 and a mean rank of (Table 2). The second most popular explanation for price rigidity takes the form of nominal contracts—prices do not change because they are fixed by contracts: it has a median rank of 3 and a mean rank of . Two common macroeconomic theories of price rigidity—menu costs and information delays—do not resonate at all with firms, who rank them amongst the least popular theories, with mean and median ranks above 9.

| Country of survey | Overall rank | |||||||||||||||

| Theory | US | GB | SE | JP | CA | AT | BE | FR | LU | NL | PT | ES | NO | IS | Median | Mean |

| Implicit contracts | 4 | 5 | 1 | 1 | 2 | 1 | 1 | 4 | 1 | 2 | 1 | 1 | 2 | 1 | 1 | |

| Nominal contracts | 5 | 1 | 3 | 3 | 3 | 2 | 2 | 3 | 3 | 1 | 5 | 3 | 1 | 2 | 3 | |

| Coordination failure | 1 | 3 | 4 | 1 | 5 | 5 | 5 | 2 | 9 | 4 | 2 | 2 | 3 | 4 | ||

| Pricing points | 8 | 4 | 7 | 4 | – | 10 | 13 | 8 | 10 | 7 | 11 | 6 | 4 | 5 | 7 | |

| Menu costs | 6 | 11 | 11 | 7 | 10 | 7 | 15 | 10 | 13 | 8 | 10 | 7 | 6 | 6 | 9 | |

| Information delays | 11 | – | 13 | – | 11 | 6 | 14 | – | 15 | – | 8 | 9 | 5 | – | 11 | |

Survey respondents rated the relevance of several pricing theories to explain price rigidity at their own firm. The table ranks common theories amongst the alternatives. Blinder et al. (1998, Table 5.1) describes the theories as follows (with wording that varies slightly across surveys): “implicit contracts” stands for “firms tacitly agree to stabilize prices, perhaps out of fairness to customers”; “nominal contracts” stands for “prices are fixed by contracts”; “coordination failure” stands for two closely related theories, which are investigated in separate surveys: “firms hold back on price changes, waiting for other firms to go first” and “the price is sticky because the company loses many customers when it is raised, but gains only a few new ones when the price is reduced” (which is labeled “kinked demand curve”); “pricing points” stands for “certain prices (like $9.99) have special psychological significance”; “menu costs” stands for “firms incur costs of changing prices”; “information delays” stands for two closely related theories, which are investigated in separate surveys: “hierarchical delays slow down decisions” and “the information used to review prices is available infrequently.” The rankings of the theories are reported in Table 5.2 in Blinder et al. (1998); Table 3 in Hall, Walsh, and Yates (2000); Table 4 in Apel, Friberg, and Hallsten (2005); Chart 14 in Nakagawa, Hattori, and Takagawa (2000); Table 8 in Amirault, Kwan, and Wilkinson (2006); Table 5 in Kwapil, Baumgartner, and Scharler (2005); Table 18 in Aucremanne and Druant (2005); Table 6.1 in Loupias and Ricart (2004); Table 8 in Lunnemann and Matha (2006); Table 10 in Hoeberichts and Stokman (2006); Table 4 in Martins (2005); Table 5 in Alvarez and Hernando (2005); Chart 26 in Langbraaten, Nordbo, and Wulfsberg (2008); and Table 17 in Olafsson, Petursdottir, and Vignisdottir (2011).

Firms also understand that customers bristle at unfair markups. According to Blinder et al. (1998, pp. 153–157), 64% of firms say that customers do not tolerate price increases after demand increases, while 71% of firms say that customers do tolerate price increase after cost increases. And firms describe the norm for fair pricing as a constant markup over marginal cost. Based on a survey of businessmen in the United Kingdom, Hall and Hitch (1939, p. 19) report that the “the ‘right’ price, the one which ‘ought’ to be charged” is widely perceived to be a markup (generally, 10%) over average cost. Okun (1975, p. 362) also observes in discussions with business people that “empirically, the typical standard of fairness involves cost-oriented pricing with a markup.”

Survey of French Bakers

To better understand how firms incorporate fairness into their pricing decisions, we interviewed 31 bakers in France in 2007. The French bread market makes a good case study because the market is large; bakers set their prices freely; and French people care enormously about bread.333In 2005, bakeries employed 148,000 workers, for a yearly turnover of billion euros (https://perma.cc/V679-UFE8). Since 1978, French bakers have been free to set their own prices, except during the inflationary period 1979–1987 when price ceilings and growth caps were imposed. For centuries, bread prices caused major social upheaval in France. Miller (1999, p. 35) explains that before the French Revolution, “affordable bread prices underlay any hopes for urban tranquility.” During the Flour War of 1775, mobs chanted “if the price of bread does not go down, we will exterminate the king and the blood of the Bourbons”; following these riots, “under intense pressure from irate and nervous demonstrators, the young governor of Versailles had ceded and fixed the price ‘in the King’s name’ at two sous per pound, the mythohistoric just price inscribed in the memory of the century” (Kaplan 1996, p. 12). We sampled bakeries in Aix-en-Provence, Grenoble, Paimpol, and Paris. The interviews reveal that bakers are guided by norms of fairness when they adjust prices to preserve customer loyalty. In particular, cost-based pricing is widely used. Bakers only raise the price of bread in response to increases in the cost of flour, utilities, or wages. They refuse to increase prices in response to increased demand—during weekends, during the summer tourist season, or during the holiday absences of local competitors. Bakers explained that pricing otherwise would be unfair, and hence would anger and drive away customers.

Monopoly Model

We extend a simple model of monopoly pricing to include fairness concerns and subproportional inference, along the lines described in Section 3. In this extended model, the markup charged by the monopoly is lower. Furthermore, the markup responds to marginal-cost shocks, generating some price rigidity: prices are not fixed, but they respond less than one-for-one to marginal costs.

Assumptions

A monopoly sells a good to a representative customer. The monopoly cannot price-discriminate, so each unit of good sells at the same price . The customer cares about fairness and appraises transactional fairness by assessing the markup charged by the monopoly. Since the customer does not observe the marginal cost of production, she needs to infer it from the price. We assume that the marginal cost perceived at price is given by a belief function . For simplicity, we restrict to be deterministic. Having inferred the marginal cost, the customer deduces that the markup charged by the monopoly is

The perceived markup determines the fairness of the transaction through a fairness function . Both functions and are assumed to be twice differentiable.

A customer who buys the quantity of the good at price experiences the fairness-adjusted consumption

The customer also faces a budget constraint:

where designates initial wealth, and designates remaining money balances. Fairness-adjusted consumption and money balances enter a quasilinear utility function

where the parameter governs the concavity of the utility function. Given fairness factor and price , the customer chooses purchases and money balances to maximize utility subject to the budget constraint.

Finally, the monopoly has constant marginal cost . It chooses price and output to maximize profits subject to customers’ demand for its good.

Demand and Pricing

We begin by determining customers’ demand for the monopoly good. The customer chooses purchases to maximize utility

The maximum of the customer’s utility function is given by the following first-order condition:

This first-order condition yields the demand curve

| (1) |

The price affects demand through two channels: the typical substitution effect, captured by ; and the fairness channel, captured by . The fairness channel appears because the price influences the perceived markup and thus the fairness of the transaction; this in turn affects the marginal utility of consumption and demand.

We turn to the monopoly’s pricing. The monopoly chooses price to maximize profits . The first-order condition is

We introduce the price elasticity of demand, normalized to be positive:

The first-order condition then yields the classical result that

that is, the monopoly optimally sets its price at a markup over marginal cost.444In Appendix A, we use the assumptions on the belief and fairness functions introduced in the next sections to verify that the first-order condition always gives the maximum of the monopoly’s profit function.

To learn more about the monopoly’s markup, we compute the elasticity . Using (1), we find

| (2) |

where is the elasticity of the fairness function with respect to the perceived markup, normalized to be positive. The first term, , describes the standard substitution effect. The second term, , represents the fairness channel and splits into two subterms. The first subterm, , appears because a higher price mechanically raises the perceived markup and thus reduces fairness. The second subterm, , appears because a higher price conveys information about the marginal cost and thus influences perceived markup and fairness. We now use (2) to compute the markup in various situations.

No Fairness Concerns

Before studying the more realistic case with fairness concerns, we examine the benchmark case in which customers do not care about fairness.

Definition 1.

Customers who do not care about fairness have a fairness function .

Without fairness concerns, the fairness function is constant, so its elasticity is . According to (2), the price elasticity of demand is constant: . This implies that the optimal markup for the monopoly takes a standard value of .

Since the markup is independent of costs, changes in marginal cost are fully passed through into the price; that is, prices are flexible. Formally, the cost passthrough is

which measures the percentage change in price when the marginal cost increases by 1%. The passthrough takes the value of one because

The following lemma summarizes the results:

Lemma 1.

When customers do not care about fairness, the monopoly sets the markup to , and the cost passthrough is .

Fairness Concerns and Observable Costs

We now introduce fairness concerns. As a preliminary step to the analysis with unobservable costs, we explore pricing when costs are observable.

To describe fairness concerns, we impose some structure on the fairness function.

Definition 2.

Customers who care about fairness have a fairness function that is positive, strictly decreasing, and weakly concave on , where and .

The assumption that the fairness function strictly decreases in the perceived markup captures the pattern that customers find higher markups less fair and resent unfair transactions. The assumption that the fairness function is weakly concave means that an increase in perceived markup causes a utility loss of equal magnitude (if is linear) or of greater magnitude (if is strictly concave) than the utility gain caused by an equal-sized decrease in perceived markup. We could not find evidence on this assumption, but it seems natural that people are at least as outraged over a price increase as they are happy about a price decrease of the same magnitude.

The properties in Definition 2 lead to the following results:

Lemma 2.

When customers care about fairness, the elasticity of the fairness function

is strictly positive and strictly increasing on , with and . As an implication, the superelasticity of the fairness function

is strictly positive on .

The proof is simple algebra and relegated to Appendix A. The property that the superelasticity of the fairness function is positive plays a central role in the analysis. It means that the fairness function is more elastic at higher perceived markups. This property follows from Definition 2 because a positive, decreasing, and weakly concave function always has positive superelasticity.555The concavity of the fairness function is not a necessary condition for the results in the paper: the necessary condition is that the superelasticity of the fairness function is positive. This occurs with concave functions but also with other not-too-convex functions. For example, the logistic function with is not concave but it has a positive superelasticity: . All the results would carry over with a logistic fairness function. We limit ourselves to concave fairness functions instead of allowing for any fairness function with a positive superelasticity because we find such restriction more natural and easier to interpret.

Since the marginal cost is assumed to be observable, customers correctly perceive marginal cost (), so the perceived markup equals the true markup (). From (2), we see that the price elasticity of demand is ; therefore, the markup charged by the monopoly satisfies

| (3) |

Since is strictly increasing from to when increases from to (Lemma 2), the right-hand side of the equation is strictly decreasing from to 1 when increases from to . We infer that the fixed-point equation (3) admits a unique solution, located between 1 and ). Therefore, the markup is well-defined and .

The next lemma records the results:

Lemma 3.

When customers care about fairness and observe costs, the monopoly’s markup is implicitly defined by (3). This implies that and the cost passthrough is . Hence, the markup is lower than without fairness concerns, but the cost passthrough is identical.

Without fairness concerns, the price affects demand solely through customers’ budget sets. With fairness concerns and observable marginal costs, the price also influences the perceived fairness of the transaction: when the price is high relative to marginal cost, customers deem the transaction to be less fair, which reduces the marginal utility from consuming the good and hence demand. Consequently, the monopoly’s demand is more price elastic than without fairness concerns, which forces the monopoly to charge a lower markup.

However, (3) shows that with fairness concerns and observable costs, the markup does not depend on costs, as in the absence of fairness concerns. Since changes in marginal cost do not affect the markup, they are completely passed through into price: prices remain flexible.

Fairness Concerns and Rational Inference of Costs

Next, we combine fairness concerns with unobservable marginal costs, beginning with a final preliminary case in which customers rationally invert the price to uncover the hidden marginal cost. In this case, the model takes the form of a simple signaling game in which the monopoly learns its marginal cost and chooses a price, before customers observe the monopoly’s price—but not its marginal cost—and formulate demand.

Let be the set of all possible marginal costs for the monopoly. The monopoly knows its marginal cost , but customers do not; instead, customers have non-atomistic prior beliefs over .

A pure-strategy perfect Bayesian equilibrium (PBE) of this game comprises three elements: a pure strategy for the monopolist, which is a mapping that selects a price for every possible value of marginal cost; a belief function for customers, which is a mapping that determines a marginal cost for every possible price; and a pure strategy for customers, which is a mapping that selects a quantity purchased for every possible price.666Strictly speaking, should allow the consumer to hold probabilistic beliefs about the firm’s marginal cost given price, but we sidestep this subtlety because it does not affect our analysis.

We look for a PBE that is fully separating: the monopoly chooses different prices for different marginal costs, which allows a rational customer who knows the monopoly’s equilibrium strategy and observes the price to deduce marginal cost. We claim the existence of a PBE in which the monopolist uses the strategy ; customers believe if , and otherwise; and customers demand . In such a PBE, customers correctly infer marginal costs from prices on the equilibrium path () and infer the worst from prices off the equilibrium path (), namely that the firm has zero marginal cost and infinitely high markup.

The argument proceeds in three steps. First, given their beliefs, customers’ demand is indeed optimal, as we have shown in (1). Second, given the monopolist’s strategy, customers’ beliefs are indeed correct for any equilibrium price. Third, given customers’ beliefs and demand, the monopolist’s strategy is optimal. Indeed, given customers’ beliefs for , we have . Then, according to (2) (which is implied by customers’ strategy), the price elasticity of demand for any price on is . Hence, the monopolist optimally charges . Finally, the monopoly has no incentive to charge some price not belonging to , which would lead customers to perceive an infinite markup, bringing the fairness factor, demand, and profits to zero.

The following lemma records the findings:

Lemma 4.

When customers care about fairness and rationally infer costs, there is a PBE in which the monopoly uses the markup , and customers learn marginal cost from price. In this PBE, the cost passthrough is . Hence, in this PBE, the markup and cost passthrough are the same as without fairness concerns.

The lemma shows that when customers care about fairness and rationally infer costs, there is a PBE in which fairness does not play a role. With fairness concerns, the price affects demand not only by changing customers’ budget sets but also by changing the perceived markup. In this equilibrium, however, after observing any price chosen by the monopoly, customers perceive the same markup . The second channel through which price could affect demand closes, so the monopoly sets the standard markup . Since the markup does not depend on marginal cost, changes in marginal cost are fully passed through into prices: prices are flexible again.

Of course, there may exist other equilibria beside the one described in Lemma 4. A pooling PBE may exist in which all types of the firm charge the same price , and consumers believe that a firm who prices otherwise has zero marginal cost. However, this and other non-fully-separating PBEs fail standard signaling refinements.777Only a separating PBE satisfies the D1 Criterion from Cho and Kreps (1987). Intuitively, consumers ought to interpret a price as coming from type rather than type , which undermines the pooling equilibrium. Indeed, if consumers demand no less at than in equilibrium, then all types of firm benefit from deviating; if consumers demand less at than in equilibrium, then the highest-cost firm strictly benefits whenever any other type of firm weakly benefits. On these grounds, the D1 Criterion suggests that consumers should interpret as coming from the highest marginal-cost firm. Because the linear PBE in Lemma 4 is so simple and robust, it is more plausible than any alternative, which suggests that fairness is unlikely to matter when customers rationally infer costs.

Fairness Concerns and Subproportional Inference of Costs

We turn to the main case of interest: customers care about fairness and subproportionally infer costs from prices. In this case, the fairness function satisfies Definition 2, and the belief function takes the following form:

Definition 3.

Customers who update subproportionally use the belief-updating rule

| (4) |

where is a prior point belief about marginal cost, and governs the extent to which beliefs anchor on that prior belief.

We have seen evidence that people do not sufficiently introspect about the relationship between price and marginal cost, which leads them to underinfer the information conveyed by the price, and that they tend to think proportionally. The inference rule (4) geometrically averages no inference with proportional inference, so it encompasses these two types of error.

First, customers underinfer marginal costs from price by clinging to their prior belief . The parameter measures the degree of underinference. When , customers do not update at all about marginal cost based on price; they naively maintain their prior belief , irrespective of the price they observe. When , customers do infer something from the price, but not enough.

Moreover, insofar as they infer something, they infer that marginal cost is proportional to price, given by . Such proportional inference represents a second error: underinference pertains to how much customers infer, whereas proportional inference describes what customers infer in as much as they do infer. The updating rule has the property that in the limit as , customers infer rationally. Indeed, when , the monopoly optimally sets the markup , which makes the marginal cost at price , and proportional inference agrees with rational inference. When , however, the monopoly does not find it optimal to mark up proportionally, and proportional inference becomes an error.

Last, we impose a constraint on the parameter such that the perceived markup falls below when the firm prices at marginal cost; this is necessary for equilibrium existence.

Despite its apparent arbitrary nature, the assumption of subproportional inference has close ties to game-theoretic models of failure of contingent thinking. It is related to the concept of cursed equilibrium, developed by Eyster and Rabin (2005), and to the concept of analogy-based-expectation equilibrium, developed by Jehiel (2005) and extended to Bayesian games by Jehiel and Koessler (2008). Both concepts propose mechanisms that can be used to explain why people might fail to account for the information that equilibrium prices reveal about marginal costs.888In fact, with , the beliefs given by (4) resemble those in a fully cursed equilibrium and the coarsest analogy-based-expectation equilibrium, when recasting our model as a Bayesian game, as in Section 4.5. In these equilibrium concepts, an unsophisticated household infers nothing about marginal cost from any economic variable. Consequently, a consumer with average prior beliefs about marginal cost equal to would continue to perceive marginal costs with mean given any price. Subproportional inference is also related to the cursed-expectation equilibrium developed by Eyster, Rabin, and Vayanos (2019) as an alternative to rational-expectations equilibrium in markets.999In a cursed-expectation equilibrium of a model in which traders endowed with private information trade a risky asset, each trader forms an expectation about the value of the asset equal to a geometric average of her expectation conditional upon her private signal alone and her expectation conditional upon both her private signal and the market price. Traders’ expectations therefore take the form of a weighted average of naive beliefs and correct beliefs. The two rules differ in that consumers in our model average naive beliefs with a particular form of incorrect beliefs (proportional inference); to include rational updating as a limit case, we calibrate the updating rule to match correct equilibrium beliefs for the case in which all consumers are rational. We adopt this approach for its tractability.

Subproportional inference also draws upon several well-documented psychological biases. Customers in our model are coarse thinkers in the sense of Mullainathan, Schwartzstein, and Shleifer (2008) because they do not distinguish between scenarios where price changes reflect changes in cost and those where they reflect changes in markup. The underinference could also be a form of the anchoring heuristic documented by Tversky and Kahneman (1974): consumers understand that higher prices reflect higher marginal costs but do not adjust sufficiently their estimate of the marginal cost. Altogether, the updating rule (4) captures the well-known bias that people do not update their beliefs sufficiently from available information.

Analytical Results

Plugging the belief-updating rule (4) into gives the following:

Lemma 5.

When customers update subproportionally, they perceive the monopoly’s markup to be

which is a strictly increasing function of the observed price .

Customers appreciate that higher prices signal higher marginal costs. But by underappreciating the strength of the relationship between price and marginal cost, customers partially misattribute higher prices to higher markups. Consequently, they regard higher prices as less fair.

As the belief function and fairness function are differentiable, customers enjoy an infinitesimal price reduction as much as they dislike an infinitesimal price increase. Therefore, the monopoly’s demand curve (1) has no kinks, unlike in pricing theories based on loss aversion (Heidhues and Koszegi 2008).

Combining (2) and (4), we then find that the price elasticity of demand satisfies

| (5) |

We have seen that without fairness concerns (), or with rational inference (), the price elasticity of demand is constant, equal to . That result changes here. Since , the price elasticity of demand is always greater than . Moreover, since is increasing in and in , the price elasticity of demand is increasing in . These properties have implications for the markup charged by the monopoly, .

Proposition 1.

When customers care about fairness and update subproportionally, the monopoly’s markup is implicitly defined by

| (6) |

which implies that . Furthermore, the cost passthrough is given by

which implies that . Hence, the markup is lower than without fairness concerns or with rational inference; and unlike without fairness concerns or with rational inference, the cost passthrough is incomplete.

The proof is relegated to Appendix A, but the intuition is simple. First, when customers care about fairness but underinfer marginal costs, they become more price-sensitive. Indeed, an increase in the price increases the opportunity cost of consumption—as in the case without fairness—and also increases the perceived markup, which reduces the marginal utility of consumption and therefore demand. This heightened price-sensitivity raises the price elasticity of demand above and pushes the markup below .

Second, after an increase in marginal cost, the monopoly optimally lowers its markup. This occurs because customers underappreciate the increase in marginal cost that accompanies a higher price. Since the perceived markup increases, the price elasticity of demand increases. In response, the monopoly reduces its markup, which mitigates the price increase. Thus, our model generates incomplete passthrough of marginal cost into price—a mild form of price rigidity. Furthermore, customers err in believing that transactions are less fair when the marginal cost increases: transactions actually become more fair.

Comparison with Microevidence

The result that prices do not fully respond to marginal-cost shocks accords well with evidence on real firm behavior. First, using matched data on product prices and producers’ unit labor cost in Sweden, Carlsson and Skans (2012) find a passthrough of idiosyncratic marginal-cost changes into prices of only . Second, using production data for Indian manufacturing firms, De Loecker et al. (2016, Table 7) find that following trade liberalization in India, marginal costs fell significantly due to the import tariff reduction, yet prices failed to fall in step: they estimate passthroughs between and . Third, using production and cost data for Mexican manufacturing firms, Caselli, Chatterjee, and Woodland (2017, Table 7) also find a modest passthrough of idiosyncratic marginal-cost changes into prices: between and . Last, combining production data for US manufacturing firms with data on energy prices and consumption, Ganapati, Shapiro, and Walker (2020, Tables 5 and 6) find a moderate passthrough of marginal-cost changes caused by energy-price variations into prices: between and . Taking the midpoint estimates from the four studies, we find an average passthrough of . Such cost passthrough is well below 1.

Additionally, our theory predicts that when customers care about fairness, the passthrough of marginal costs into prices is markedly different when costs are observable and when they are not. The passthrough is one when costs are observable (Lemma 3) but is strictly below one when costs are not observable (Proposition 1). Kachelmeier, Limberg, and Schadewald (1991a), Kachelmeier, Limberg, and Schadewald (1991b), and Renner and Tyran (2004) provide experimental evidence consistent with this result: they find that after a cost shock, prices adjust more when costs are observable than when they are not.

Comparison with the Literature

Price rigidity in our model arises from a nonconstant price elasticity of demand, which creates variation in markups after cost shocks. Other models share the feature that variable price elasticity leads to price rigidity. In international economics, these models have been used to explain the behavior of exchange rates and prices (Dornbusch 1985; Bergin and Feenstra 2001; Atkeson and Burstein 2008). In macroeconomics, they have been used to create real rigidities that amplify nominal rigidities (Kimball 1995; Dotsey and King 2005; Eichenbaum and Fisher 2007). Unlike many of these models, our model does not make reduced-form assumptions about the utility function or demand curve to generate a nonconstant price elasticity of demand but instead provides a microfoundation.

Additional Analytical Results

To obtain further results, we introduce a simple fairness function that satisfies all the requirements from Definition 2:

| (7) |

where governs the intensity of fairness concerns. A higher means that a consumer grows more upset when consuming an overpriced item and more content when consuming an underpriced item. The fairness function reaches when the perceived markup equals ; then fairness-adjusted consumption coincides with actual consumption. When the perceived markup exceeds , the fairness function falls below one; and when the perceived markup lies below , the fairness function surpasses one.

Furthermore, to compare different industries or economies, we focus on a situation in which customers have acclimated to prices by coming to judge firms’ markups as acceptable: adjusts so and . Acclimation is likely to occur eventually within any industry or economy, once customers have faced the same prices for a long time.101010As noted by Kahneman, Knetsch, and Thaler (1986, p. 730), “Psychological studies of adaption suggest that any stable state of affairs tends to become accepted eventually, at least in the sense that alternatives to it no longer come to mind. Terms of exchange that are initially seen as unfair may in time acquire the status of a reference transaction…. [People] adapt their views of fairness to the norms of actual behavior.” The belief-updating rule (8) introduced in the New Keynesian model has the property that for any initial belief, people eventually become acclimated.

We then obtain the following comparative statics:

Corollary 1.

Assume that customers care about fairness according to the fairness function (7), infer subproportionally, and are acclimated. Then the monopoly’s markup is given by

The markup decreases with the competitiveness of the market (), concern for fairness (), and degree of underinference (). And the cost passthrough is given by

The passthrough increases with the competitiveness of the market (); it decreases with the concern for fairness () and degree of underinference ().

Comparison with Additional Microevidence

Our theory predicts that the cost passthrough is higher in more-competitive markets. This property echoes the finding by Carlton (1986) that prices are less rigid in less-concentrated industries. It is also consistent with the finding by Amiti, Itskhoki, and Konings (2014) that firms with higher market power have a lower passthrough of cost shocks driven by exchange-rate fluctuations.

Our theory also predicts that the passthrough is lower—so prices are more rigid—in markets that are more fairness-oriented. This property could contribute to explain the finding by Kackmeister (2007) that retail prices were more rigid in 1889–1891 than in 1997–1999. Kackmeister emphasizes that the relationship between retailers and customers was much more personal in the 19th century than today.111111Kackmeister notes: “In 1889–1891 retailing often occurred in small one- or two-person shops, retailers supplied credit to the customers, and retailers usually delivered the purchases to the customer’s home at no extra charge. Today retailing occurs in large stores, a third party supplies credit, and the customer takes his own items home. These changes decrease both the business and personal relationship between the retailer and the customer” (p. 2008). This more personal relationship could have made the retail sector more fairness-oriented, which would help explain, according to our theory, its greater historical price rigidity. This channel could also help explain the finding by Nakamura and Steinsson (2008, Table 8) that prices are more rigid in the service sector than elsewhere, since relationships between buyers and sellers are more personal in the service industry.

New Keynesian Model

We now explore the macroeconomic implications of the pricing theory developed in Section 4. To that end, we embed it into a New Keynesian model as a substitute for usual pricing frictions—either Calvo (1983) pricing or Rotemberg (1982) pricing. We find that when customers care about fairness and infer subproportionally, the price markup depends on the rate of inflation; thus, monetary policy is nonneutral in both short and long run. (Derivations are relegated to Appendix B.)

Assumptions

A continuum of firms indexed by and a continuum of households indexed by make up the economy. Firms use labor services to produce goods. Households supply labor services, consume goods, and save using riskless nominal bonds. Since goods are imperfect substitutes for one another, and labor services are also imperfect substitutes, firms exercise some monopoly power on the goods market, and households exercise some monopoly power on the labor market.

Fairness Concerns

Households cannot observe firms’ marginal costs. When a household purchases good at price in period , it infers that firm ’s marginal cost is . The model is dynamic so it provides a natural candidate for the anchor that households use when inferring costs: last period’s perception of marginal cost. Hence, instead of being given by (4) as in the monopoly model, households’ perception of firm ’s marginal cost at time is given by

| (8) |

where is last period’s perceived cost, and is the degree of underinference.

Having inferred the marginal cost, households deduce that the markup charged by firm is . This perceived markup determines the fairness of the transaction with firm , measured by . The fairness function , specific to good , satisfies the conditions listed in Definition 2. The elasticity of with respect to is .

An amount of good bought by household at a unit price yields a fairness-adjusted consumption

Household ’s fairness-adjusted consumption of the various goods aggregates into a consumption index

where is the elasticity of substitution between different goods. The price of one unit of the consumption index at time is given by the price index

Households

Household derives utility from consuming goods and disutility from working. Its expected lifetime utility is

where is the mathematical expectation conditional on time- information, is the discount factor, is its labor supply, and is the inverse of the Frisch elasticity of labor supply.

To smooth consumption over time, households trade one-period bonds. In period , household holds bonds. Bonds purchased in period have a price , mature in period , and pay one unit of money at maturity.

Household ’s consumption-savings decisions in each period must obey the constraint

where is the wage rate for labor service , and are dividends from firm ownership. In addition, household satisfies a solvency constraint that prevents Ponzi schemes.

Finally, in each period , household chooses purchases for each , labor supply , bond holdings , and wage rate . The household’s objective is to maximize its expected utility subject to the budget constraint, to the solvency constraint, and to firms’ demand for labor service . The household takes as given its initial endowment of bonds , all fairness factors , all prices and , and dividends .

Firms

Firm hires labor to produce output using the production function

| (9) |

where is output of good , is its technology level, is the extent of diminishing marginal returns to labor, and

is an employment index. In the index, is the quantity of labor service hired by firm , and is the elasticity of substitution between different labor services. The technology level is stochastic and unobservable to households—making the firm’s marginal cost unobservable.

Each period , firm chooses output , price , and employment levels for all . The firm’s objective is to maximize the expected present-discounted value of profits

where is the stochastic discount factor for period- nominal payoffs, subject to the production constraint (9), to demand for good , and to the law of motion of the perceived marginal cost (8). The firm takes as given the initial belief about its marginal cost , all wage rates , and discount factors . Its profits accrue to households as dividends.

Monetary Policy

The nominal interest rate is determined by a simple monetary-policy rule:

| (10) |

where is a stochastic exogenous component, is the inflation rate, and governs the response of the interest rate to inflation.

Symmetry

We assume a symmetric economy. All households receive the same bond endowment and same dividends . All firms share a common technology , face the same fairness function , and are believed to have the same initial cost . Hence, all households behave identically, as do all firms.

Notation

Since the equilibrium is symmetric, we drop subscripts and to denote the equilibrium values taken by the variables. We also denote the steady-state value of any variable by . And for any variable except the inflation and interest rates, we denote the logarithmic deviation from steady state by . For the inflation and interest rates, we denote the deviation from steady state by , , and .

Demand for Goods and Pricing

Households and firms behave exactly as in the textbook New Keynesian model, except that fairness concerns modify consumers’ demand and, consequently, firms’ pricing.

The demand for good from all households is

where describes the level of aggregate demand. The price of good appears twice in the demand curve: as part of the relative price ; and as part of the fairness factor . This second element leads to unconventional pricing.

As in the monopoly model, fairness affects pricing through the price elasticity of demand , which satisfies (5). Unlike in the monopoly model, however, the profit-maximizing markup is not because does not capture the effect of the current price on future beliefs and thus future demands. Instead, in equilibrium, firms set their price markup such that

| (11) |

The gap between and reflects how much today’s price affects future perceived marginal costs, demands, and profits. Conversely, if firms do not care about the future (), the equation reduces to .

The price markup plays a critical role because it directly determines employment:

| (12) |

Employment is strictly decreasing in the price markup because in equilibrium the price markup is the inverse of the real marginal cost, which is itself increasing in employment. Since a higher price markup implies a lower real marginal cost, it also implies lower employment.

Calibration

Before simulating the model, we calibrate it to US data. To set the values of the fairness-related parameters, we use new evidence on price markups and cost passthroughs. For the other parameters, we rely on standard evidence. The calibrated values of the parameters are summarized in Table 3.

Fairness Function

We set the shape of the fairness function to (7). This simple functional form has two advantages. First, it introduces only one new parameter, , which governs the concern for fairness. Second, it produces a fairness factor equal to one at the zero-inflation steady state. Indeed, in such steady state, the perceived price markup is , as shown by (8), and so the fairness factor is . Thus, with no trend inflation, customers acclimate and are neither happy nor unhappy about markups.

| Value | Description | Source or target |

| A. Common parameters | ||

| Quarterly discount factor | Annual rate of return | |

| Shape of production function | Labor share | |

| Inverse of Frisch elasticity of labor supply | Chetty et al. (2013, Table 2) | |

| Response of nominal interest rate to inflation | Gali (2008, p. 52) | |

| Persistence of monetary shock | Gali (2008, p. 52), Gali (2011, p. 26) | |

| Persistence of technology shock | Gali (2008, p. 55) | |

| B. Parameters of the New Keynesian model with fairness | ||

| Elasticity of substitution across goods | Steady-state price markup | |

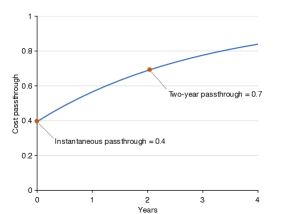

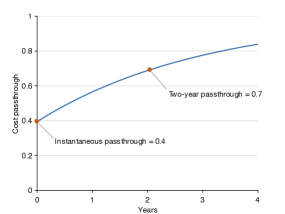

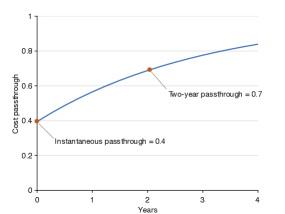

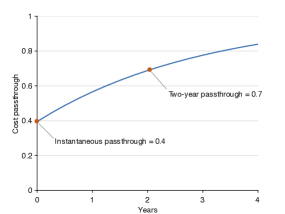

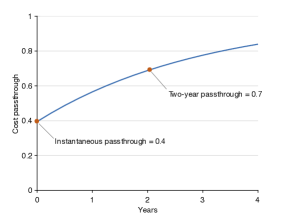

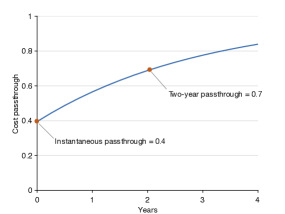

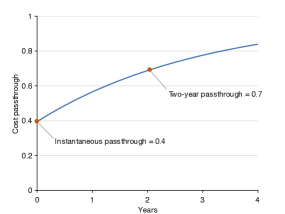

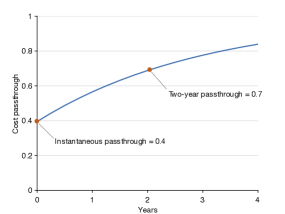

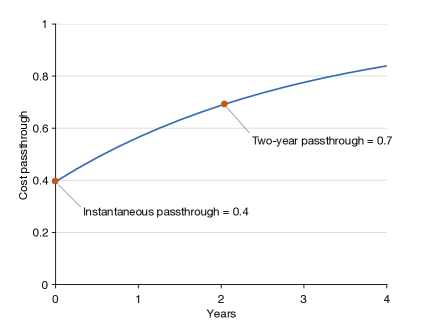

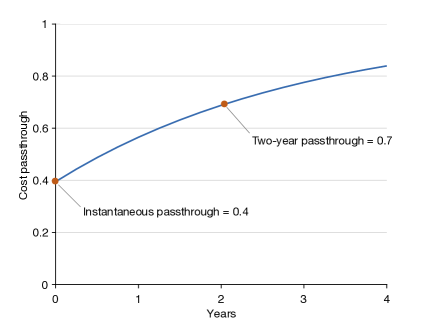

| Fairness concern | Instantaneous cost passthrough | |

| Degree of underinference | Two-year cost passthrough | |

| C. Parameters of the textbook New Keynesian model | ||

| Elasticity of substitution across goods | Steady-state price markup | |

| Share of firms keeping price unchanged | Average price duration quarters | |

The parameter values described in the table are obtained in Section 5.3.

Fairness-Related Parameters

We then calibrate the three parameters central to our theory: the fairness parameter , the inference parameter , and the elasticity of substitution across goods . These parameters jointly determine the average value of the price markup and its response to shocks—which determines the cost passthrough. Hence, for the calibration, we match evidence on price markups and cost passthroughs. We target three empirical moments: average price markup, short-run cost passthrough, and long-run cost passthrough.

First, using firm-level data, De Loecker, Eeckhout, and Unger (2020, p. 575) estimate price markups in the United States. They find that the average markup across the US economy hovers between and in the 1955–1980 period, rises from in 1980 to in 2000, remains around until 2014, before spiking to in 2016. As the markup averages between 2000 and 2016, we adopt this value as a target.121212The aggregate markup computed by De Loecker, Eeckhout, and Unger (2020) is commensurate to markups measured in specific industries and goods in the United States. In the automobile industry, Berry, Levinsohn, and Pakes (1995, p. 882) estimate that on average , which translates into a markup of . In the ready-to-eat cereal industry, Nevo (2001, Table 8) finds that a median estimate of is , which translates into a markup of . In the coffee industry, Nakamura and Zerom (2010, Table 6) also estimate a markup of . For most national-brand items retailed in supermarkets, Barsky et al. (2003, p. 166) discover that markups range between and . Finally, earlier work surveyed by Rotemberg and Woodford (1995, pp. 260–267) finds similar markups: between and in the industrial-organization literature, and around in the marketing literature.

Second, in the United States, Sweden, India, and Mexico, the short-run cost passthrough is estimated between and , with an average value of (Section 4.6). Hence, we target a short-run cost passthrough of .

Third, Burstein and Gopinath (2014, Table 7.4) provide estimates of the long-run exchange-rate passthrough for the United States and seven other countries. The exchange-rate passthrough measures the response of import prices to exchange-rate shocks. Its level may not reflect that of the cost passthrough, because marginal costs may not vary one-for-one with exchange rates, but there is no reason for the two passthroughs to have different dynamics (Amiti, Itskhoki, and Konings 2014). The immediate exchange-rate passthrough is estimated at , and the two-year exchange-rate passthrough at . Based on these dynamics, and the fact that the immediate cost passthrough is also , we target a two-year cost passthrough of .

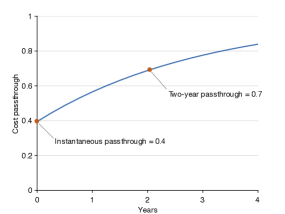

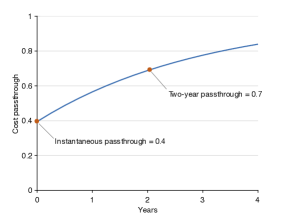

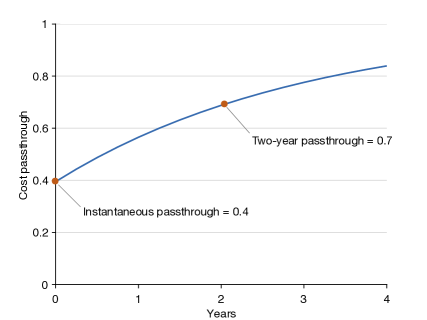

We then simulate the dynamics of a firm’s price in response to an unexpected and permanent increase in its marginal cost (see Appendix B.5). We find that the fairness parameter primarily affects the level of the cost passthrough, while the inference parameter primarily affects its persistence. Based on the simulations, we set , , and . This calibration allows us to achieve a steady-state price markup of , an instantaneous cost passthrough of , and a two-year cost passthrough of .

Other Parameters

We set the labor-supply parameter to , which gives a Frisch elasticity of labor supply of . This value is the median microestimate of the Frisch elasticity for aggregate hours (Chetty et al. 2013, Table 2). We then set the quarterly discount factor to , giving an annual rate of return on bonds of . We set the production-function parameter to . This calibration guarantees that the labor share, which equals in steady state, takes its conventional value of . Last, we calibrate the monetary-policy parameter to , which is consistent with observed variations in the federal funds rate (Gali 2008, p. 52).

Parameters of the Textbook New Keynesian Model

We also calibrate a textbook New Keynesian model (described in Appendix C), which we will use as a benchmark in simulations. For the parameters common to the two models, we use the same values—except for . In the textbook model, the steady-state price markup is , so we set to obtain a markup of .

We also need to calibrate a parameter specific to the textbook model: , which governs price rigidity. To generate price rigidity, the New Keynesian literature uses either the staggered pricing of Calvo (1983) or the price-adjustment cost of Rotemberg (1982). Both pricing assumptions lead to the same linearized Phillips curve around the zero-inflation steady state, and therefore to the same simulations (Roberts 1995). But the Calvo interpretation of is easier to map to the data, so we use it for calibration. The parameter indicates the share of firms that cannot update their price each period; it can be calibrated from microevidence on the frequency of price adjustments. If a share of firms keep their price fixed each period, the average duration of a price spell is (Gali 2008, p. 43). In the microdata underlying the US Consumer Price Index, the mean duration of price spells is about 3 quarters (Nakamura and Steinsson 2013, Table 1). Hence, we set , which implies .

Effects of Monetary Policy in the Short Run

Price rigidity is a central concept in macroeconomic theory because it is a source of monetary nonneutrality. Here we explore how our pricing theory produces monetary nonneutrality. At this stage, we focus on the short-run effects of monetary policy, tracing how an unexpected and transitory shock to monetary policy permeates through the economy.

Analytical Results

The dynamics of the textbook New Keynesian model around the steady state are governed by an IS equation, describing households’ consumption-savings decisions, and a short-run Phillips curve, describing firms’ pricing decisions. In the model with fairness, the same IS equation remains valid, but the Phillips curve is modified—because firms price differently.131313Introducing fairness concerns into the New Keynesian model improves the realism of the Phillips curve but does not modify the IS equation. Yet the IS equation is also problematic: it notably creates several anomalies at the zero lower bound. Other behavioral elements have been introduced into the New Keynesian model to improve the realism of the IS equation. For instance, Gabaix (2020) assumes that households are inattentive to unusual events. Alternatively, Michaillat and Saez (2019) assume that households derive utility from social status, which is measured by relative wealth.

The main difference is that the Phillips curve involves not only employment and inflation but also the perceived price markup, which itself obeys the following law of motion:

Lemma 6.

In the New Keynesian model with fairness, the perceived price markup evolves according to

| (13) |

Hence, the perceived price markup is a discounted sum of lagged inflation terms:

The proof appears in Appendix B.4; it is obtained by reworking the inference rule (8).

Equation (13) shows that the perceived price markup today tends to be high if inflation is high or if the past perceived markup was high. Past beliefs matter because people use them as a basis for their current beliefs. Inflation matters because people do not fully appreciate the effect of inflation on nominal marginal costs. Because of its autoregressive structure, the perceived price markup is fully determined by past inflation.

As a result, the short-run Phillips curve involves not only forward-looking elements—expected future inflation and employment—but also backward-looking elements—past inflation.

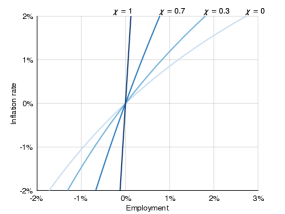

Proposition 2.

In the New Keynesian model with fairness, the short-run Phillips curve is

| (14) |

where

Accordingly, the short-run Phillips curve is hybrid, including both past and future inflation rates:

Simulation Results

Next we simulate the dynamical response of our calibrated model to an unexpected and transitory monetary shock. Following the literature, we simulate dynamics around the zero-inflation steady state.

We assume that the exogenous component of the monetary-policy rule (10) follows an AR(1) process such that

where the disturbance follows a white-noise process with mean zero, and governs the persistence of shocks. We set , which corresponds to moderate persistence (Gali 2008, p. 52; Gali 2011, p. 26). We simulate the response to an initial disturbance of , which is an expansionary monetary shock. Without any inflation response, this shock would reduce the annualized interest rate by 1 percentage point.

This figure describes the response of the New Keynesian model with fairness (solid lines) to a decrease in the exogenous component of the monetary-policy rule (10) by 1 percentage point (annualized) at time 0. The exogenous component of monetary policy and inflation rate are deviations from steady state, measured in percentage points and annualized. The other variables are percentage deviations from steady state. For comparison, the figure also displays the response of the textbook New Keynesian model (dashed lines). The log-linearized equilibrium conditions used in the simulation of the model with fairness are presented in Appendix B.4; those used in the simulation of the textbook model are in Appendix C. The calibration of the two models is described in Table 3.

Figure 1 depicts the dynamical response to the expansionary monetary shock. The exogenous component of monetary policy and inflation rate are expressed as deviations from steady-state values, measured in percentage points and annualized (by multiplying by four the variables and ); all other variables are expressed as percentage deviations from steady-state values.

Loosening monetary policy raises inflation. Observing higher prices, customers underinfer the underlying increase in nominal marginal costs and thus perceive higher price markups. Firms respond to such perceptions by cutting their actual markups. The price markup falls by , which raises output and employment by . (Output and employment respond identically because the production function is calibrated to be linear.)

Comparison with Microevidence

In our model, when consumers observe inflation, they misperceive price markups as higher and transactions as less fair, which lowers their consumption utility and triggers a feeling of displeasure. The survey responses collected by Shiller (1997) agree with these predictions. Among 120 respondents in the United States, 85% report that they dislike inflation because when they “go to the store and see that prices are higher,” they “feel a little angry at someone” (p. 21). The most common perceived culprits are “manufacturers,” “store owners,” and “businesses,” whose transgressions include “greed” and “corporate profits” (p. 25). Thus, in our model as in the real world, consumers perceive higher markups during inflationary periods and are angered by them.