Optimal excess-of-loss reinsurance for stochastic factor risk models

Abstract

We study the optimal excess-of-loss reinsurance problem when both the intensity of the claims arrival process and the claim size distribution are influenced by an exogenous stochastic factor. We assume that the insurer’s surplus is governed by a marked point process with dual-predictable projection affected by an environmental factor and that the insurance company can borrow and invest money at a constant real-valued risk-free interest rate . Our model allows for stochastic risk premia, which take into account risk fluctuations. Using stochastic control theory based on the Hamilton-Jacobi-Bellman equation, we analyze the optimal reinsurance strategy under the criterion of maximizing the expected exponential utility of the terminal wealth. A verification theorem for the value function in terms of classical solutions of a backward partial differential equation is provided. Finally, some numerical results are discussed.

Keywords: optimal reinsurance, excess-of-loss reinsurance, Hamilton-Jacobi-Bellman equation, stochastic factor model, stochastic control.

JEL Classification codes: G220, C610.

MSC Classification codes: 93E20, 91B30, 60G57, 60J75.

1. Introduction

In this paper we analyze the optimal excess-of-loss reinsurance problem from the insurer’s point of view, under the criterion of maximizing the expected utility of the terminal wealth. It is well known that the reinsurance policies are very effective tools for risk management. In fact, by means of a risk sharing agreement, they allow the insurer to reduce unexpected losses, to stabilize operating results, to increase business capacity and so on. Among the most common arrangements, the proportional and the excess-of-loss contracts are of great interest. The former was intensively studied in [Irgens and Paulsen, 2004], [Liu and Ma, 2009], [Liang et al., 2011], [Liang and Bayraktar, 2014], [Zhu et al., 2015], [Brachetta and Ceci, 2019] and references therein. The latter was investigated in these articles: in [Zhang et al., 2007] and [Meng and Zhang, 2010], the authors proved the optimality of the excess-of-loss policy under the criterion of minimizing the ruin probability, with the surplus process described by a Brownian motion with drift; in [Zhao et al., 2013] the Cramér-Lundberg model is used for the surplus process, with the possibility of investing in a financial market represented by the Heston model; in [Sheng et al., 2014] and [Li and Gu, 2013] the risky asset is described by a Constant Elasticity of Variance (CEV) model, while the surplus is modelled by the Cramér-Lundberg model and its diffusion approximation, respectively; finally, in [Li et al., 2018] the authors studied a robust optimal strategy under the diffusion approximation of the surplus process.

The common ground of the cited works is the underlying risk model, which is the Cramér-Lundberg model (or its diffusion approximation)111See [Lundberg, 1903], [Schmidli, 2018].. In the actuarial literature it is of great importance, because it is simple enough to perform calculations. In fact, the claims arrival process is described by a Poisson process with constant intensity (or a Brownian motion, in the diffusion model). Nevertheless, as noticed by many authors (e.g. [Grandell, 1991], [Hipp, 2004]), it needs generalization in order to take into account the so callled size fluctuations and risk fluctuations, i.e. variations of the number of policyholders and modifications of the underlying risk, respectively.

The main goal of our work is to extend the classical risk model by modelling the claims arrival process as a marked point process with dual-predictable projection affected by an exogenous stochastic process . More precisely, both the intensity of the claims arrival process and the claim size distribution are influenced by . Thanks to this environmental factor, we achieve a reasonably realistic description of any risk movement. For example, in automobile insurance may describe weather conditions, road conditions, traffic volume and so on. All these factors usually influence the accident probability as well as the damage size.

Some noteworthy attempts in that direction can be found in [Liang and Bayraktar, 2014] and [Brachetta and Ceci, 2019], where the authors studied the optimal proportional reinsurance. In the former, the authors considered a Markov-modulated compound Poisson process, with the (unobservable) stochastic factor described by a finite state Markov chain. In the latter, the stochastic factor follows a general diffusion. In addition, in [Brachetta and Ceci, 2019] the insurance and the reinsurance premia are not evaluated by premium calculation principles (see [Young, 2006]), because they are stochastic processes depending on . In our paper, we extend further the risk model, because the claim size distribution is influenced by the stochastic factor, which is described by a diffusion-type stochastic differential equation (SDE). In addition, we study a different reinsurance contract, which is the excess-of-loss agreement.

In our model the insurer is also allowed to lend or borrow money at a given interest rate . During the last years, negative interest rates drew the attention of many authors. For example, since June 2016 the European Central Bank (ECB) fixed a negative Deposit facility rate, which is the interest banks receive for depositing money within the ECB overnight. Nowadays, it is . As a consequence, in our framework . We point out that there is no loss of generality due to the absence of a risky asset, because as long as the insurance and the financial markets are independent (which is a standard hypothesis in non-life insurance), the optimal reinsurance strategy turns out to depend only on the risk-free asset (see [Brachetta and Ceci, 2019] and references therein). As a consequence, the optimal investment strategy can be eventually obtained using existing results in the literature.

The paper is organized as follows: in Section 2, we formulate the model assumptions and describe the maximization problem; in Section 3 we derive the Hamilton-Jacobi-Bellman (HJB) equation; in Section 4, we investigate the candidate optimal strategy, which is suggested by the HJB derivation; in Section 5, we provide the verification argument with a probabilistic representation of the value function; finally, in Section 6 we perform some numerical simulations.

2. Model formulation

Let be a complete probability space endowed with a filtration which satisfies the usual conditions, where is the insurer’s time horizon. We model the insurance losses through a marked point process with local characteristics influenced by an environment stochastic factor . Here, the sequence describes the claim arrival process and the corresponding claim sizes. Precisely, , , are stopping times such that a.s. and , , are -random variables such that , is -measurable.

The stochastic factor is defined as the unique strong solution to the following SDE:

| (2.1) |

where is a standard Brownian motion on . We assume that the following conditions hold true:

| (2.2) | |||

| (2.3) |

We will denote by the natural filtration generated by the process .

The random measure corresponding to the losses process is given by

| (2.4) |

where denotes the Dirac measure located at point . We assume that its -dual predictable projection has the form

| (2.5) |

where

-

•

is such that , is a distribution function, with ;

-

•

is a strictly positive measurable function.

In the sequel, we will assume the following integrability conditions:

| (2.6) |

and

| (2.7) |

which implies the following:

According with the definition of dual predictable projection, for every nonnegative, -predictable and -indexed process we have that222For details on marked point processes theory, see [Brémaud, 1981].

| (2.8) |

In particular, choosing with any nonnegative -predictable process

i.e. the claims arrival process is a point process with stochastic intensity .

Now we give the interpretation of as conditional distribution of the claim sizes333This result is an extension of Proposition 2.4 in [Ceci and Gerardi, 2006]..

Proposition 2.1.

and

In particular, this implies that

where is the strict past of the -algebra generated by the stopping time :

Proof.

See Appendix A. ∎

This means that in our model both the claim arrival intensity and the claim size distribution are affected by the stochastic factor . This is a reasonable assumption; for example, in automobile insurance may describe weather, road conditions, traffic volume, and so on. For a detailed discussion of this topic see also [Brachetta and Ceci, 2019].

Remark 2.1.

Let us observe that for any -predictable and -indexed process such that

the process

turns out to be an -martingale. If in addition

then is a square integrable -martingale and

Moreover, the predictable covariation process of is given by

that is is an -martingale444For these results and other related topics see e.g. [Bass, 2004]..

In this framework we define the cumulative claims up to time as follows

and the reserve process of the insurance is described by

where is the initial wealth and is a non negative -adapted process representing the gross insurance risk premium. In the sequel we assume , for a suitable function such that .

Now we allow the insurer to buy an excess-of-loss reinsurance contract. By means of this agreement, the insurer chooses a retention level and for any future claim the reinsurer is responsible for all the amount which exceeds that threshold (e.g. means full reinsurance). For any dynamic reinsurance strategy , the insurer’s surplus process is given by

where is a non negative -adapted process representing the reinsurance premium rate. In addition, we suppose that the following assumption holds true.

Assumption 2.1.

(Excess.of-loss reinsurance premium) Let us assume that for any reinsurance strategy the corresponding reinsurance premium process admits the following representation:

where is a continuous function in , with continuous partial derivatives in , such that

-

1.

for all , since the premium is increasing with respect to the protection level;

-

2.

, because the cedant is not allowed to gain a profit without risk.

In the rest of the paper, should be intended as a right derivative.

Assumption 2.1 formalizes the minimal requirements for a process to be a reinsurance premium. In the next examples we briefly recall the most famous premium calculation principles, because they are widely used in optimal reinsurance problems solving. In Appendix B the reader can find a rigorous derivation of the following formulas (2.9) and (2.10).

Example 2.1.

The most famous premium calculation principle is the expected value principle (abbr. EVP)555See [Young, 2006].. The underlying conjecture is that the reinsurer evaluates her premium in order to cover the expected losses plus a load which depends on the expected losses. In our framework, under the EVP the reinsurance premium is given by the following expression:

| (2.9) |

for some safety loading .

Example 2.2.

Another important premium calculation principle is the variance premium principle (abbr. VP). In this case, the reinsurer’s loading is proportional to the variance of the losses. More formally, the reinsurance premium admits the following representation:

| (2.10) |

for some safety loading .

From now on we assume the following condition:

| (2.11) |

Furthermore, the insurer can lend or borrow money at a fixed interest rate . More precisely, every time the surplus is positive, the insurer lends it and earns interest income if (or pays interest expense if ); on the contrary, when the surplus becomes negative, the insurer borrows money and pays interest expense (or gains interest income if ).

Under these assumptions, the total wealth dynamic associated with a given strategy is described by the following SDE:

| (2.12) |

It can be verified that the solution to (2.12) is given by the following expression:

| (2.13) |

Our aim is to find the optimal strategy in order to maximize the expected exponential utility of the terminal wealth, that is

where is the risk-aversion parameter and is the set of all admissible strategies as defined below.

Definition 2.1.

We denote by the set of all admissible strategies, that is the class of all non negative -predictable processes . With the notation we refer to the same class, restricted to the strategies starting from .

Remark 2.2.

Observe that the condition (2.11) implies . In fact we have that

As usual in stochastic control problems, we focus on the corresponding dynamic problem:

| (2.14) |

where denotes the insurer’s wealth process starting from evaluated at time .

3. HJB formulation

In order to solve the optimization problem (2.14), we introduce the value function associated with it, that is

| (3.1) |

This function is expected to solve the Hamilton-Jacobi-Bellman (HJB) equation:

| (3.2) |

where denotes the Markov generator of the couple associated with a constant control . In what follows, we denote by the class of all bounded functions , with , with bounded first order derivatives and bounded second order derivatives with respect to the spatial variables .

Lemma 3.1.

Let be a function in . The Markov generator of the stochastic process for all constant strategies is given by the following expression:

| (3.3) |

Proof.

For any , applying Itô’s formula to the stochastic process , we get the following expression:

where is defined in (3.3) and

In order to complete the proof, we have to show that is an -martingale. For the first term, we observe that

because the partial derivative is bounded and using the assumption (2.2). For the second term, it is sufficient to use the boundedness of and the condition (2.6). ∎

Remark 3.1.

Since the couple is a Markov process, any Markovian control is of the form , where denotes a suitable function. The generator associated to a general Markovian strategy can be easily obtained by replacing with in (3.3).

In order to simplify our optimization problem, we present a preliminary result.

Remark 3.2.

Let be an integrable function such that . For any , the following equation holds true:

where . In fact, by integration by parts we get that

| (3.4) |

Now let us consider the ansatz , which is motivated by the following proposition.

Proposition 3.1.

Let us suppose that there exists a function solution to the following Cauchy problem:

| (3.5) |

with final condition , , where

| (3.6) |

Then the function

| (3.7) |

solves the HJB problem given in (3.2).

Proof.

From the expression (3.7) we can easily verify that

By Remark 3.2, taking , we can rewrite the last integral in this more convenient way:

Now we define by means of the equation (3.6), obtaining the following equivalent expression:

Taking the infimum over , by (3.5) we find out the PDE in (3.2). The terminal condition in (3.2) immediately follows by definition. ∎

The previous result suggests to focus on the minimization of the function (3.6), that is the aim of the next section.

4. Optimal reinsurance strategy

In particular, we provide a complete characterization of the optimal reinsurance strategy. In the sequel we assume .

Proposition 4.1.

Let us suppose that is strictly convex in and let us define the set as follows:

| (4.2) |

If the equation

| (4.3) |

admits at least one solution in for any , denoted by , then the minimization problem (4.1) admits a unique solution given by

| (4.4) |

Proof.

The function is continuous in by definition (see Assumption 2.1) and for any its derivative is given by the following expression:

| (4.5) |

Since is convex in by hypothesis, if then , then , because the derivative is increasing in and there is no stationary point in . Else, if then , and coincides with the unique stationary point of , which is . Let us notice that it exists by hypothesis and it is unique because is strictly convex. ∎

By the previous proposition, we observe that is an important threshold for the insurer: as long as the marginal cost of the full reinsurance falls in the interval , the optimal choice is full reinsurance.

Unfortunately, it is not always easy to check whether is strictly convex in or not. In the next result such an hypothesis is relaxed, while the uniqueness of the solution to (4.3) is required.

Proposition 4.2.

Proof.

The next result deals with the existence of a solution to (4.3). In particular, it is sufficient to require that the claim size distribution is heavy-tailed, which is a relevant case in non-life insurance (see [Rolski et al., 1999, Chapter 2]), plus a technical condition for the reinsurance premium.

Proposition 4.3.

Let us assume that the reinsurance premium is such that666E.g. if is convex in .

and the claim size distribution is heavy-tailed in this sense:

Then, for any , the equation (4.3) admits at least one solution in .

Proof.

The following property of heavy-tailed distributions is a well known implication of our assumption:

Hence, by equation (4.5), for any

On the other hand, we know that

As a consequence, being continuous in , there exists such that . ∎

Now we turn the attention to the other crucial hypothesis of Proposition 4.1, which is the convexity of . The reader can easily observe that the reinsurance premium convexity plays a central role.

Proposition 4.4.

Suppose that the reinsurance premium is convex in and for some function such that . Then the function defined in (3.6) is strictly convex in .

Proof.

Recalling the expression (3.6), it is sufficient to prove the convexity of the following term:

For this purpose, let us evaluate its second order derivative:

Now the term in brackets is

The proof is complete. ∎

By Proposition 2.1, the hypothesis on the claim sizes distribution above may be read as assuming that the claims are exponentially distributed conditionally to .

4.1. Expected value principle

Now we investigate the special case of the expected value principle introduced in Example 2.1.

Proposition 4.5.

Under the EVP (see equation (2.9)), the optimal reinsurance strategy is given by

| (4.7) |

Proof.

Using Remark 3.2, we can rewrite the equation (2.9) as follows:

As a consequence, we have that

For , we have that

hence and by Proposition 4.1 the minimizer belongs to . Now we look for the stationary points, i.e. the solutions to the equation (4.3), that in this case reads as follows:

| (4.8) |

Solving this equation, we obtain the unique solution given by (4.7). In order to prove that it coincides with the unique minimizer to (4.1), it is sufficient to show that

For this purpose, observe that

The proof is complete. ∎

Remark 4.1.

Formula (4.7) was found by [Zhao et al., 2013] (see equation 3.31, page 508). We point out that it is a completely deterministic strategy. This fact is crucially related to the use of the EVP rather than the underlying model; in fact, in [Zhao et al., 2013] the authors considered the Cramér-Lundberg model under the EVP777It is not surprising, in fact in [Brachetta and Ceci, 2019] and references therein also the optimal proportional reinsurance under EVP turns out to be deterministic.

From the economic point of view, by equation (4.7) it is easy to show that the optimal retention level is decreasing with respect to the interest rate and the risk-aversion; on the contrary, it is increasing with respect to the reinsurer’s safety loading. In addition, the sensitivity with respect to the time-to-maturity depends on the sign of .

Another relevant aspect of (4.7) is that it is independent of the claim size distribution. To the authors this result seems quite unrealistic. In fact, any subscriber of an excess-of-loss contract is strongly worried about possibly extreme events, hence the claims distribution is expected to play an important role.

4.2. Variance premium principle

This subsection is devoted to derive an optimal strategy under the variance premium principle (see Example 2.2).

Proposition 4.6.

Let us suppose that is strictly convex in and

| (4.9) |

for some (eventually ).

Under the VP (see equation (2.10)) the optimal reinsurance strategy is the unique solution to the following equation:

| (4.10) |

Proof.

The proof is based on Proposition (4.1). By equation (2.10) we get its derivative:

It is clear that the set defined in (4.2) is empty, because for any

Hence the minimizer should coincide with the unique stationary point of , i.e. the solution to (4.10). In order to prove it, we need to ensure the existence of a solution to (4.10). For this purpose, we notice that on the one hand

On the other hand, for , by (4.9) we get

As a consequence, by the continuity of there exists a point such that . Such a solution is unique because is strictly convex by hypothesis. ∎

Conversely to Proposition 4.5, the optimal retention level given in Proposition 4.6 is still dependent on the stochastic factor . Such a dependence is spread through the claim size distribution.

Remark 4.2.

Now we specialize the variance premium principle to conditionally exponentially distributed claims.

Proposition 4.7.

Under the VP, suppose that for some function such that . The optimal reinsurance strategy is given by

| (4.11) |

Proof.

By the proof of Proposition 4.6, we know that under VP . Now, under our hypotheses, by equation (4.5) we readily get

The equation admits a unique solution, given by equation (4.11). At this point , the function is strictly convex, because

It follows that is the unique minimizer by Proposition 4.4. ∎

Contrary to the equation (4.7), the explicit formula (4.11) keeps the dependence on the stochastic factor . In addition, the following result holds true.

Remark 4.3.

Suppose that for some function such that . We consider two different reinsurance safety loadings , referring to the EVP and VP, respectively. Moreover, let us denote by and the optimal retention level under the EVP and VP, given in equations (4.7) and (4.11), respectively. It is easy to show that

From the practical point of view, as long as the stochastic factor fluctuations result in a rate parameter higher than the threshold , the optimal retention level evaluated through the expected value principle turns out to be larger than the variance principle.

5. Verification Theorem

Theorem 5.1 (Verification Theorem).

Proof.

By Proposition 3.1, the function defined in equation (3.7) solves the HJB problem (3.2). Hence for any

where and denote the solutions to (2.12) and (2.1) at time , starting from and , respectively.

From Itô’s formula we get

| (5.2) |

with defined by

| (5.3) |

In order to show that is an -local-martingale, we use a localization argument, taking

The reader can easily check that is a non decreasing sequence of stopping time such that . For the diffusion term of , using the assumptions (5.1) and (2.2), we notice that

where is a constant depending on . For the jump term, by the condition (2.7) and Remark 2.1, we get

with denoting a positive constant dependent on . Thus turns out to be an -local-martingale and is a localizing sequence for it. Now, taking the expectation of (5.2) with in place of , we obtain that

Let us notice that

where is a constant. As a consequence, is a sequence of uniformly integrable random variables. By classical results in probability theory, it converges almost surely. Using the monotonicity and the boundedness of , together with the non explosion of and (see (2.13) and (2.3)), taking the limit for we conclude that

As a byproduct, since given in Proposition 4.1 realizes the infimum in (4.1), we have that and, replicating the calculations above, we obtain the equality

i.e. is an optimal control. ∎

By Theorem 5.1, the value function (3.1) can be characterized as a transformation of the solution to the partial differential equation (PDE) (3.5). Nevertheless, an explicit expression is not available, except for very special cases. The following result provides a probabilistic representation by means of the Feynman-Kac theorem.

Proposition 5.1.

Proof.

The thesis immediately follows by Theorem 5.1 and the Feynman-Kac representation of . ∎

Remark 5.1.

We refer to [Heath and Schweizer, 2000] for existence and uniqueness of a solution to the PDE (3.5).

6. Numerical results

In this section we show some numerical results, mostly based on Propositions 4.5 and 4.7. We assumed the following dynamic for the stochastic factor for performing simulations:

The -dual predictable projection (see equation (2.5)) is determined by these functions:

The parameters are set according to Table 1 below.

| Parameter | Value |

|---|---|

| Y | |

The SDEs are approximated through a classical Euler’s scheme with steps length , while the expectations are evaluated by means of Monte Carlo simulations with parameter .

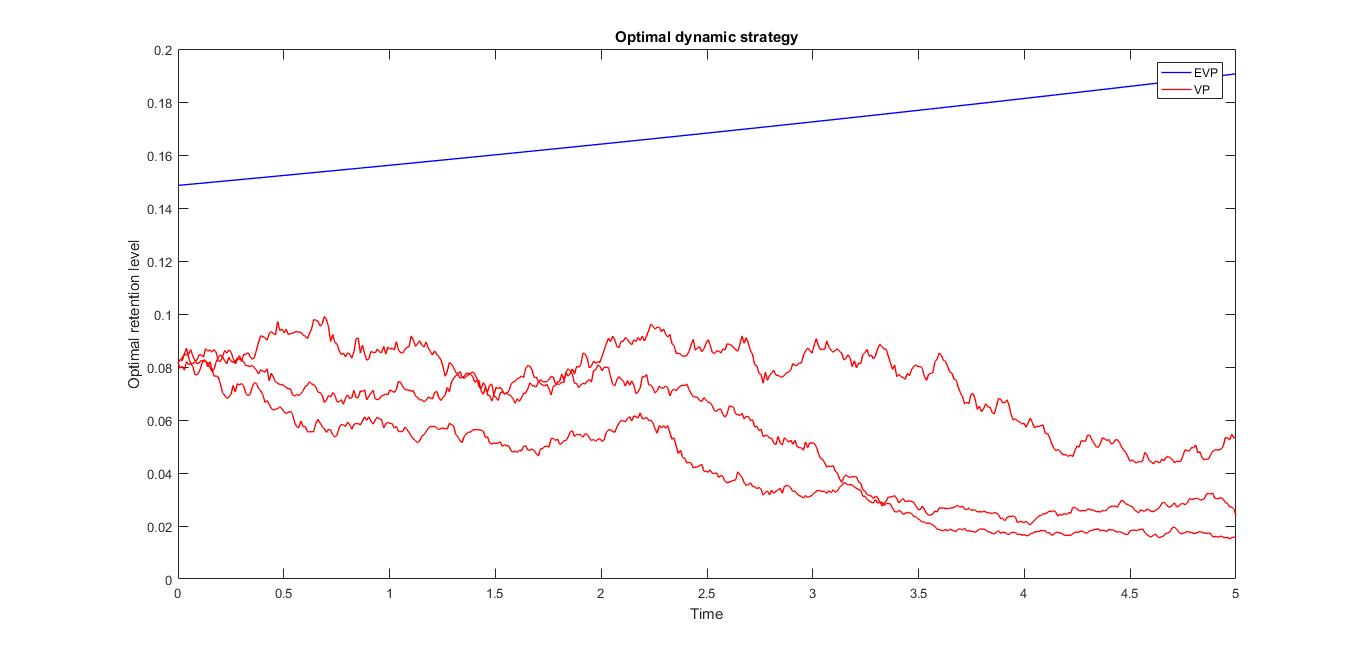

In Figure 1 we show the dynamic strategies under EVP and VP, computed by the equations (4.7) and (4.11), respectively.

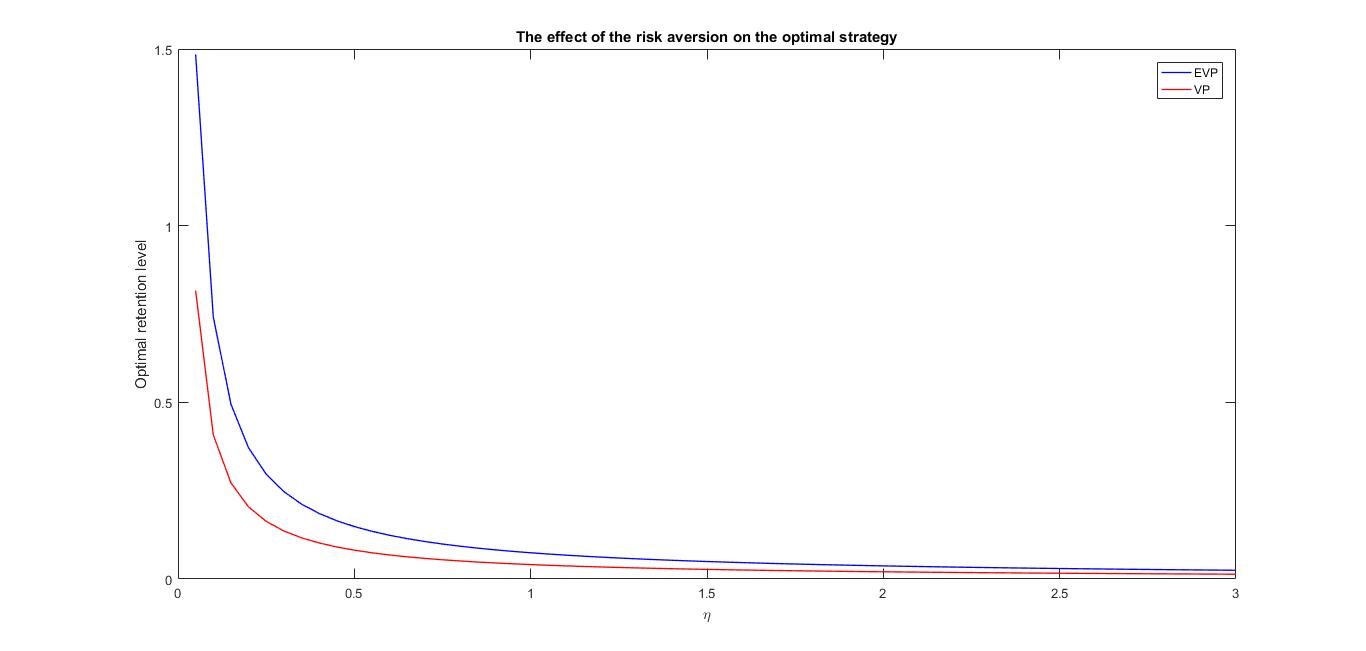

In Figure 2 we start the sensitivity analysis investigating the effect of the risk aversion parameter on the optimal strategy at time . As expected, there is an inverse relationship. Notice that for high values of the two strategies tend to the same level.

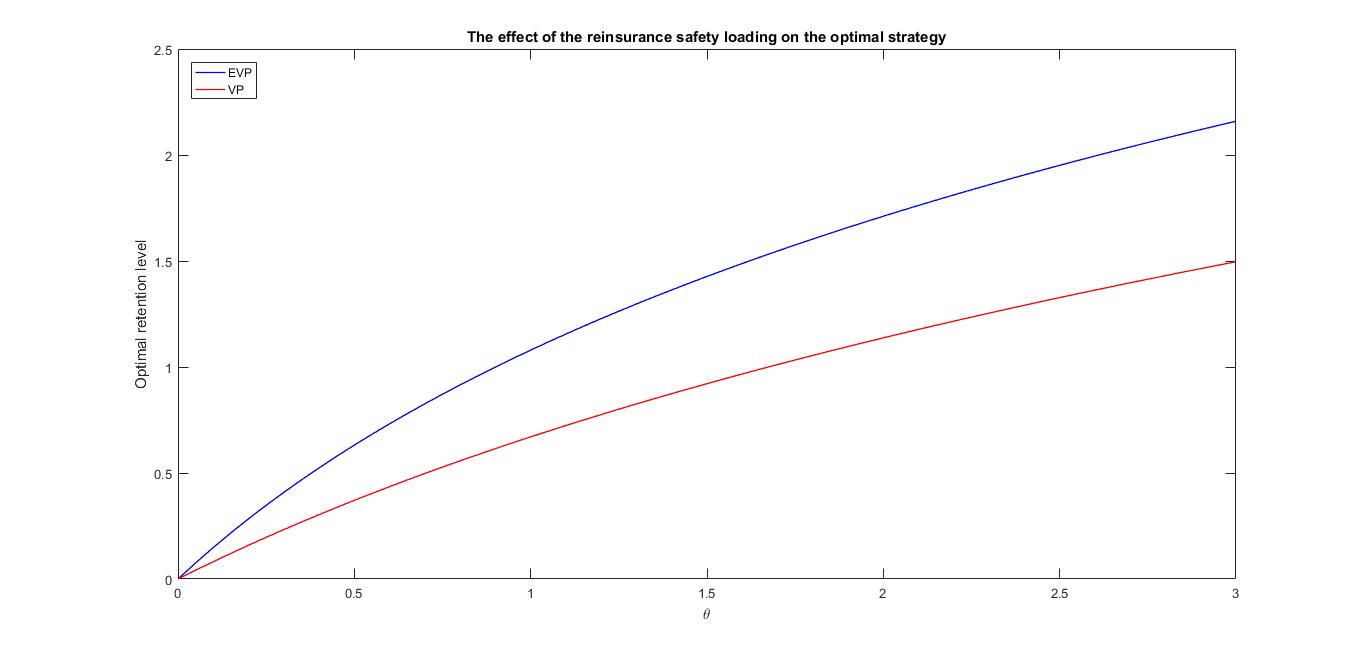

Figure 3 refers to the sensitivity analysis with respect to the reinsurance safety loading . When the strategies coincide (because the premia coincide), then they diverge for increasing values of .

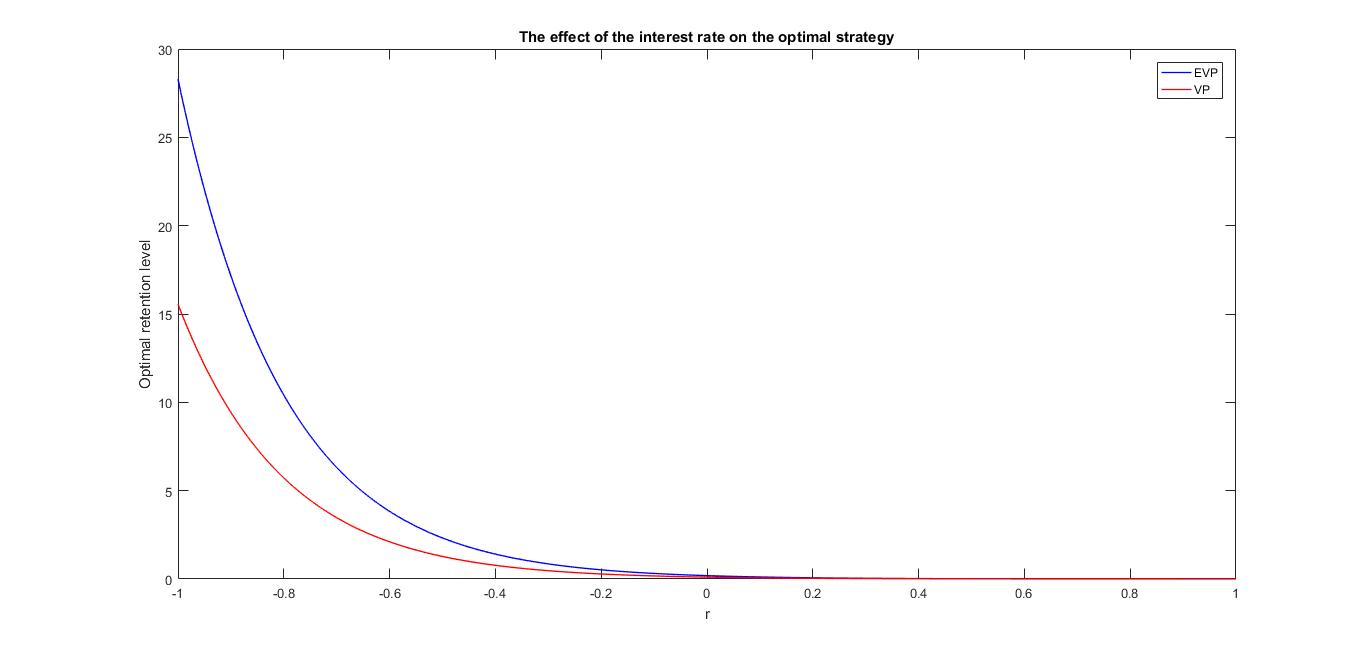

In Figure 4 we observe that the distance between the retention levels in the two cases is larger when and it decreases as long as increases. Nevertheless, even for positive values of the risk-free interest rate the distance is not negligible (see the pictures above, with ).

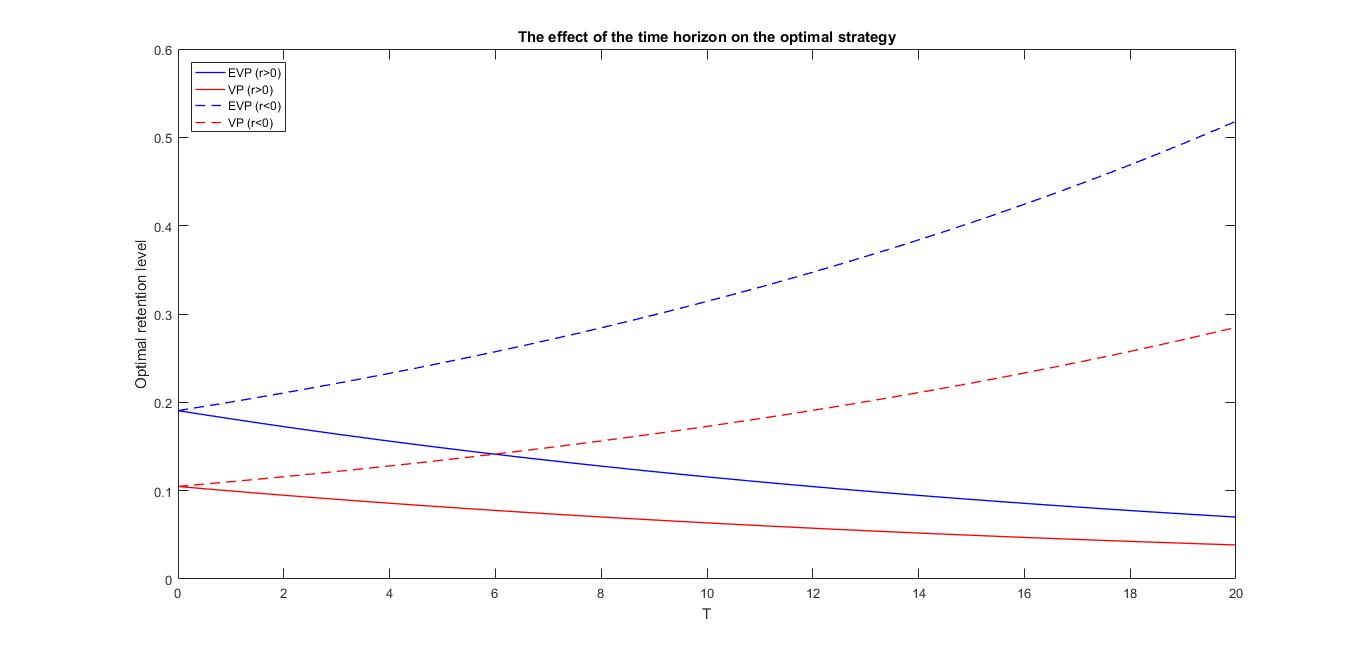

In Figure 5 we study the response of the optimal strategy to variations of the time horizon. The two cases exhibit the same behavior, which is strongly influenced by the sign of the interest rate. In fact, if the retention level increases with the time horizon, while if the optimal strategy decreases with .

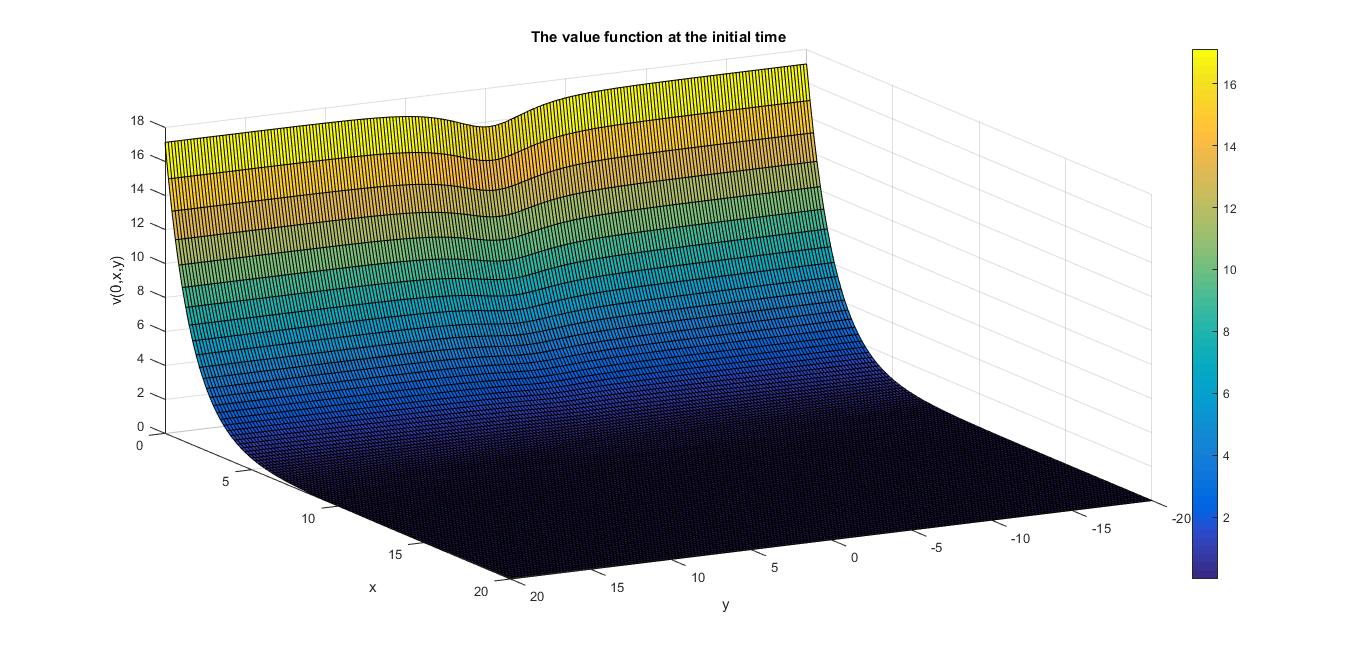

Finally, thanks to Proposition 5.1 we are able to numerically approximate the value function by simulating the trajectories of . The graphical result (under VP) is shown in Figure 6 below.

Appendix A Appendix

Proof of Proposition 2.1.

By equation (2.8), for any with any nonnegative -predictable process and we get

Since is an -measurable random variable (see Appendix 2, T4 in [Brémaud, 1981]), denoting by the conditional distribution of given , we have that

Hence the following equality holds true

and by the arbitrariness of and strictly positivity of we finally obtain that

∎

Appendix B Appendix

In this section we motivate formulas (2.9) and (2.10). Let us denote by the reinsurer’s cumulative losses at time :

Recalling (2.5), by equation (2.9) in Example 2.1 we readily check that for any strategy under the EVP

for some safety loading , i.e. for any time the expected premium covers the expected losses plus an additional (proportional) term, which is the expected net income.

Now let us focus on Example 2.2. Under the VP the reinsurance premium should satisfy the following equation:

| (B.1) |

for some safety loading . We need to evaluate the variance term. Let us introduce the following stochastic process:

denoting . We have that

Denoting by the predictable covariance process of , using Remark 2.1 we finally obtain

Under the special case and (e.g. under the Cramér-Lundberg model), for any constant strategy the previous equation reduces to

Extending this formula to the model formulated in Section 2, we obtain the expression (2.10). Of course, there will be an approximation error, because in our general model the intensity and the claim size distribution depend on the stochastic factor. Nevertheless, this is a common procedure in the actuarial literature.

References

- [Bass, 2004] Bass, R. F. (2004). Stochastic differential equations with jumps. Probab. Surveys, 1:1–19.

- [Brachetta and Ceci, 2019] Brachetta, M. and Ceci, C. (2019). Optimal proportional reinsurance and investment for stochastic factor models. Insurance: Mathematics and Economics.

- [Brémaud, 1981] Brémaud, P. (1981). Point Processes and Queues. Martingale dynamics. Springer-Verlag.

- [Ceci and Gerardi, 2006] Ceci, C. and Gerardi, A. (2006). A model for high frequency data under partial information: a filtering approach”. International Journal of Theoretical and applied Finance, 9(4):555–576.

- [Grandell, 1991] Grandell, J. (1991). Aspects of risk theory. Springer-Verlag.

- [Heath and Schweizer, 2000] Heath, D. and Schweizer, M. (2000). Martingales versus pdes in finance: An equivalence result with examples. Journal of Applied Probability, (37):947–957.

- [Hipp, 2004] Hipp, C. (2004). Stochastic control with applications in insurance. In Stochastic Methods in Finance, chapter 3, pages 127–164. Springer.

- [Irgens and Paulsen, 2004] Irgens, C. and Paulsen, J. (2004). Optimal control of risk exposure, reinsurance and investments for insurance portfolios. Insurance: Mathematics and Economics, 35:21–51.

- [Li et al., 2018] Li, D., Zeng, Y., and Yang, H. (2018). Robust optimal excess-of-loss reinsurance and investment strategy for an insurer in a model with jumps. Scandinavian Actuarial Journal, (2):145–171.

- [Li and Gu, 2013] Li, Q. and Gu, M. (2013). Optimization problems of excess-of-loss reinsurance and investment under the cev model. ISRN Mathematical Analysis, page 10.

- [Liang and Bayraktar, 2014] Liang, Z. and Bayraktar, E. (2014). Optimal reinsurance and investment with unobservable claim size and intensity. Insurance: Mathematics and Economics, 55:156–166.

- [Liang et al., 2011] Liang, Z., Yuen, K., and Guo, J. (2011). Optimal proportional reinsurance and investment in a stock market with ornstein–uhlenbeck process. Insurance: Mathematics and Economics, 49:207–215.

- [Liu and Ma, 2009] Liu, B. and Ma, J. (2009). Optimal reinsurance/investment problems for general insurance models. The Annals of Applied Probability, 19:1495–1528.

- [Lundberg, 1903] Lundberg, F. (1903). Approximerad framställning av sannolikehetsfunktionen, terförsäkering av kollektivrisker. Almqvist and Wiksell.

- [Meng and Zhang, 2010] Meng, H. and Zhang, X. (2010). Optimal risk control for the excess of loss reinsurance policies. ASTIN Bulletin, 40(1):179–197.

- [Rolski et al., 1999] Rolski, T., Schmidli, H., V., S., and Teugels, J. (1999). Stochastic processes for insurance and finance. Wiley.

- [Schmidli, 2018] Schmidli, H. (2018). Risk Theory. Springer Actuarial. Springer International Publishing.

- [Sheng et al., 2014] Sheng, D., Rong, X., and Zhao, H. (2014). Optimal control of investment-reinsurance problem for an insurer with jump-diffusion risk process: Independence of brownian motions. Abstract and Applied Analysis, pages 1–19.

- [Young, 2006] Young, V. R. (2006). Premium principles. Encyclopedia of Actuarial Science, (3).

- [Zhang et al., 2007] Zhang, X., Zhou, M., and Guo, J. (2007). Optimal combinational quota-share and excess-of-loss reinsurance policies in a dynamic setting. Applied Stochastic Models in Business and Industry, 23:63–71.

- [Zhao et al., 2013] Zhao, H., Rong, X., and Zhao, Y. (2013). Optimal excess-of-loss reinsurance and investment problem for an insurer with jump–diffusion risk process under the heston model. Insurance: Mathematics and Economics, 53(3):504 – 514.

- [Zhu et al., 2015] Zhu, H., Deng, C., Yue, S., and Deng, Y. (2015). Optimal reinsurance and investment problem for an insurer with counterparty risk. Insurance: Mathematics and Economics, 61:242–254.