Subdominant eigenvalue location and

the

robustness of Dividend Policy Irrelevance

Abstract. This paper, on subdominant eigenvalue location of a bordered diagonal matrix, is the mathematical sequel to an accounting

paper by Gao, Ohlson, Ostaszewski [7]. We explore the following

characterization of dividend-policy irrelevance (DPI) to equity valuation in

a multi-dimensional linear dynamics framework : DPI occurs under when

discounting the expected dividend stream by a constant interest rate iff

that rate is equal to the dominant eigenvalue of the canonical principal

submatrix of This is justifiably the ‘latent’ (or gross) rate of return, since

the principal submatrix relates the state variables to each other but with

dividend retention. We find that DPI reduces to the placement of the

maximum eigenvalue of between the dominant and subdominant eigenvalues

of We identify a special role, and a lower bound, for the coefficient measuring the

year-on-year dividend-on-dividend sensitivity in achieving robust equity

valuation (independence of small variations in the dividend policy).

Mathematics Subject Classification (2010): primary 91B32, 91B38; secondary 91G80, 49J55, 49K40.

Keywords: Dividend irrelevance, dominant eigenvalue,

bordered diagonal matrix, performance stability, dividend-on-dividend sensitivity.

1 Introduction and motivation

Accounting theory seeks to reconcile valuation of a firm based on historically observed variables (‘primitives’, that recognize value created to date) with its equity value, arrived at by markets in a prospective fashion. The market’s valuation is theoretically modelled as the present value of future (expected) dividends and involves discounting by the (notional) riskless interest rate in force, say per unit time. From the historic (accounting) side, various secondary composite variables have been derived from the primitives (with appropriate technical names such as ‘residual income’ – for a brief introduction see [8]), formalizing in one way or another a notion of current ‘earnings’; the latter is then intended to identify equity value directly (as a dependent variable) and to provide empirically stable time series.

To arrive at such a composite accounting variable, assumptions are needed concerning the future evolution of the primitives – at least in a hypothetical ‘steady state’ context. (For a ‘dynamic’ alternative, drawing on the value of waiting, see [5] in this same volume.) The favourite mechanism for this context is a linear state-space representation , thereby introducing subtle links – our main concern here – between accounting theory and mathematics.

It is noteworthy, though not of direct mathematical significance to this paper, that an encouraging feature for the use of a (linear) representation is its flexibility in permitting inclusion, alongside state variables that recognize historic value creation (as above), additional ‘information’ state variables; these capture the (typical) dynamics of an embedded ‘potential to create’ value, an ‘intangible’ value, currently unrecognized in the accounts but feeding through to future recognized value (a matter central to the luckless 2014 attempt by Pfizer to bid for AstraZeneca – ‘the mega-merger that never was’). This partly bridges the historic-prospective divide. (The idea was introduced into the accounting literature of linear systems by Ohlson [21], and enabled him to include the accounting of ‘goodwill’ value – see [15]; for another example of an intangible, involving product ‘image’ and its valuation, see e.g. [13].)

Returning to mathematical concerns, we note that the eigenstructure of (eigenvalue distribution) has to connect with economic consequences of an assumed ‘steady state’ – such as absence of arbitrage opportunities in equity valuation, and its relation to the notional riskless interest rate (above). A further fundamental insight, going back to Miller and Modigliani [18] in 1961, is that – under prescribed conditions (but see e.g. [4] for the effects of alternative informational assumptions) – the equity value should not depend on the distribution of value, be it impounded into the share price or placed in the share-holders’ pockets (via dividend payouts); this is properly formalized below. (This is one aspect of capital structure irrelevance: equity value should not depend on debt versus equity issuance [17, 19].) The principle of dividend policy irrelevancy also carries implications for the linear dynamics. For a recent analysis of the connections see [7], where the basic result asserts that DPI occurs iff the riskless interest rate agrees with the dominant eigenvalue of the reduced linear system (‘subsystem’) obtained by the firm withholding (retaining) dividend payouts. One may call the latter the dominant ‘latent’ rate of the system . Recall that it is the riskless rate that is used in the present-value calculation above.

This is a knife-edge characterization in regard both to the riskless interest rate and the dominant eigenvalue, so it is natural to study accounting robustness in the DPI framework. That is the principal aim of this paper, achieved by studying an eigenvalue location problem, similar but distinct from one in control theory (reviewed shortly below). The delicacy of this matter is best seen in the light of Wilkinson’s example in [28, §33] of a sparse matrix with the integers on the diagonal (its eigenvalues) and all superdiagonal entries of ; a small perturbation of in the bottom left-hand corner yields the characteristic polynomial to be , so that for the eigenvalues are these: 6 real ones which are to 1 decimal place 0.9, 2.1, 2.6, 18.4, 18.9, 20.0, and 7 conjugate complex pairs (all in mid-range values, in modulus) as follows:

Turning now to the mathematical problem, consider, granted initial conditions, the performance of the following discrete-time system:

| () |

Here is the dividend-on-dividend ‘year-on-year’ growth; its effect is particularly significant – see below and §2 (Theorem 3). So the state variables at time are – with representing the time- dividend, an ‘information’ variable (as above), subjected to ‘fading’ over time by a factor satisfying

with a real matrix (hereafter, the reduced matrix of the system, or the ‘dividend-retention’ matrix) that is constant over time. The performance of the system at time is measured by the expression

in which a discount factor is applied to the sequence generated by Here with as above (the governing riskless interest rate per unit time), and so represents an initial equity valuation of the firm – in the sense motivated above. To guarantee convergence it is sufficient to assume that all components of any solution of have growth below referring to the modulus of the dominant eigenvalue of the coefficient matrix in by this growth condition may be restated as

| (1) |

The bottom row vector in

is termed the dividend policy.

In this setting the full coefficient matrix is assumed constant, but not known to observers of the state variables (which are disclosed in the annual accounts). However, whereas and the penultimate row involve value created over time through an initial (fixed) investment, it is the final row that generates the returns (over time) to the investors. Thus the equity should be regarded as a function of and of the dividend-policy vector parameters set by the managers, that is

| (2) |

One says that the valuation exhibits Dividend Policy Irrelevancy (DPI) at if the function is unchanged as the dividend-policy vector varies. A first problem is to determine circumstances under which the system exhibits dividend irrelevancy. Up to a technical side-condition (ensuring co-dependence of dividends and value creation) the short answer is that the dominant eigenvalue of should agree with – this was first proved by Ohlson in the special case and then generalized in [7] (and also referred to in the earlier published monograph [23]).

Below we refine the notion of dividend irrelevancy in order to study the effects of a proximal sub-dominant eigenvalue. We first establish notation and some conventions. Begin by omitting hereafter explicit mention of the information variable we regard it as yet another state variable absorbed into (with then becoming an eigenvalue of the reduced matrix), and so we overlook its simple dynamics; we may now free up and for other uses below. The eigenvalues of the reduced matrix (latent relative to , below) are listed in order of decreasing modulus. As these will be required to be real, positive and (generically) distinct, this is taken to mean

Whenever convenient (e.g. in proofs) we omit the superscript The system matrix of () above, viewed as the augmented matrix of , is now given by

("-bordered"), and is regarded as a function of the real vector Its (possibly complex) eigenvalues will likewise be regarded as functions of and denoted by or more simply by so that

which distinguish them more easily (from each index here is identified through the functional conditions

| (3) |

We write

Although is not in general symmetric, we will contrive situations in which the eigenvalues of interlace with those of just as in Cauchy’s Interlace Theorem, cf. [11, Th. 4.3.17], [3, Ch.7, §8 Th. 4], [12], at least for .

Since we are mostly concerned with the characteristic polynomial and eigenvalue location, we will be working in an equivalent canonical setting in which, firstly, is diagonal and, secondly, as a further simplification, we suppose that for the dividend significance coefficients are all non-zero. Rescaling by the -th equation of the diagonalized system gives what we term the equivalent canonical system in which the resulting dividend significance coefficients are (as, of course, we may also rescale by : see Remark 2 in §2.1). Thus is replaced by

| (4) |

where for each It is preferable to subsume as (rather than as ) into the ‘canonical dividend-policy vector’ corresponding to . Our first definitions all contain growth conditions analogous to (1) and are motivated by Proposition 1 below.

Definition 1. We say that the system has dividend irrelevance at if, for all such that

with the zero vector.

Definition 2. We say that the system has local dividend irrelevance at for if there is so that, for all such that and

Here the norm is Euclidean. The local definition is weaker in that it requires merely that the equity valuation be robust in respect of the accounting system (i.e. insensitive to minor accounting variations). However, in our model setting regarded as a function of is a rational function in these variables (see Observation below in §1.2), so its local constancy for a given is equivalent to global constancy for the same . An intermediate definition permitting constant equity is the following

Definition 3. We say that the system ( has bounded dividend irrelevance at if, for some positive and all such that

The example below identifies anomalous behaviour which these definitions offer as possible.

The requirement for dividend irrelevance amounts to discovering to what extent depends only on the initial data:

In view of the role of the interest rate it will be appropriate to make the following.

Blanket assumption. The eigenvalues of are all real and positive.

Notice that if small enough variations in the dividend-policy vector will ensure that the inequality is preserved. This entails (see Proposition 1 below) that the system will have local dividend-policy irrelevance at more than one rate, namely at and Our contribution is to identify in Theorem 3 below a condition on namely that

requiring a lower bound on the dividend-on-dividend yearly growth, which ensures that and thereby achieves uniqueness of the latent rate of return in this case: dividend-policy irrelevance occurs only at the one rate .

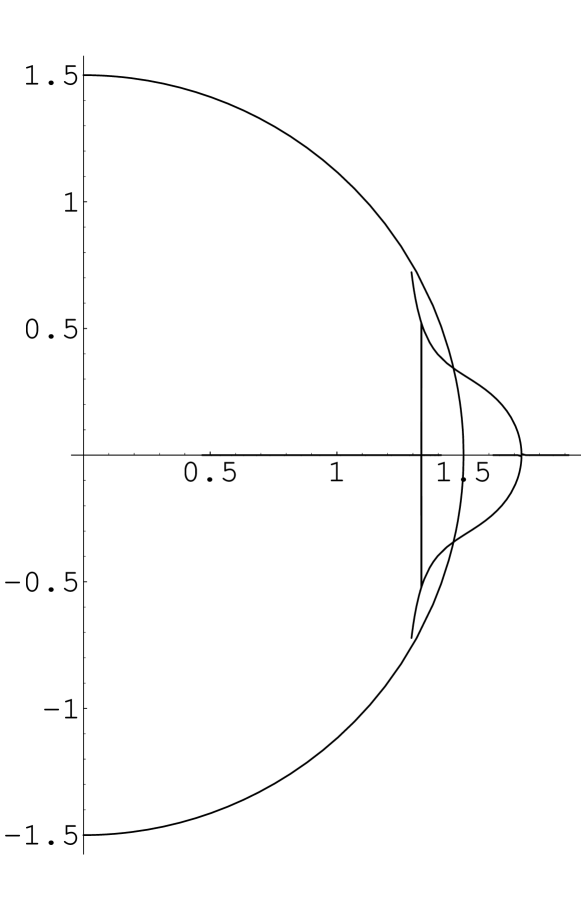

Example of Bounded-DPI at both and . We take , and Note that so

Figure 1 shows the locus of the conjugate complex root pair for running through the range 0.1 to 1.2 generated by Mathematica. The third root is below, but close to, Note that the additional vertical line appears from the numerics (the computer routine switches the identity of the two conjugates). Variations in bounding the eigenvalues to keep both equity and constant.

1.1 Continuous-time analogue

Letting denote cumulative dividends, the analogous dynamic in continuous time may be formulated as

Here is now the state vector of flow variables and and are columns in . Putting we arrive at the system

where as before is bordered by and Thus has growth rate at most the largest eigenvalue of

The equity is

which converges provided that the dividend flow is of exponential growth less than and in particular that

| (5) |

This requires therefore that

The identical format allows interpretation of results in this paper leading to valid conclusions for the continuous-time framework. In fact set

to obtain the discounted flow, i.e. the Laplace transform. We conclude that

subject to Assuming is invertible we have

whence

This formula was exploited in Ashton et al. in [1], [2] in a stochastic setting.

An identical formula can be developed for discrete time (with Laplace transform replaced by z-transform) and is the departure point for the purely algebraic argument developed in [7]. We note an important conclusion, which follows from the form of the adjugate matrix (or by invoking Cramer’s Rule).

Observation. In the framework above, the equity regarded as a function of is a rational function in these variables.

1.2 Control-theory analogies

We remark on the contextual similarities between the accounting model and two standard control-theory settings and identify the differences. For background, see e.g. [25].

The first setting is the closest. Here we regard as a state vector and as a control variable, and write the system equation as

with the control variable selected according to a non-standard (since it is in effect differential) feedback-law

In these circumstances we interpret defined by (2) as the system performance index (a discounted cost stream), and require that that it be either (i) independent of the feedback law parameters, or (ii) independent of small variations in the parameters. This is akin to performance stability, or even a ‘disturbance decoupling problem’, except that there is no modelled disturbance here. Our analysis is similar to that of the standard pole-placement problem (requiring assignment of eigenvalues through feedback-law design). Where we differ is in the inevitable presence and effect of zeros as well as poles.

The alternative view is to regard as the observation vector of the state with state equation and observation vector defined respectively by

Here is the projection matrix from to In these circumstances the performance index of the system is given by and we wish to ensure that the performance is dependent only on the evolution of observation and the initial state

1.3 The accounting context

The dividend irrelevance question (in particular whether or not dividends should be irrelevant to stockholders) has been a live issue since the 1961 paper [18] of Modigliani and Miller. See, for example, [6]. The current quest for dividend irrelevance comes from the general possibility of restating equity in terms of an identically discounted alternative series based on accounting numbers, as first pointed out in 1936 by Preinreich [24]; see the discussion in the survey paper by [23]. If () models the evolution of the firm and models its observable accounting numbers, interest focuses on whether valuations are possible at time based on the accounting numbers alone, that is to say in the absence of access to the currently unobservable information . See Proposition 2 below.

The current paper inter alia identifies circumstances under which dividend irrelevance does indeed occur at an eigenvalue of and so shows that the earlier derived equivalence is non-vacuous.

1.4 Organization of material

The paper is organized as follows. In Section 2 we give our main theorems (Theorems 1-5) and the auxiliary propositions on which they are based. Shorter proofs are included here, but longer proofs are delayed till later. The results of Sections 2 and 3 are then used in Section 4 to perform a detailed study of eigenvalue location of the augmented matrix. This is done by examining the two-pole case first, and then estimating the distortion effects when other poles are present. Some bifurcation analysis is conducted in Section 5 in circumstances corresponding to Theorem 1. Sections 6 and onwards contain longer proofs, or such details as are not required for the analysis of Section 4.

2 Main Theorems and auxiliary propositions

In [7] it is shown that dividend irrelevance at occurs iff takes the value of the dominant eigenvalue, here defined to be the largest in modulus (in the spirit of the Perron-Frobenius context – see [11, Ch. 8], [26, Ch.1,2]), of the reduced matrix which will forthwith be diagonal. Asymptotic considerations suggest this result, since for generic initial conditions, and for large the dominant eigenvalue growth of dwarfs into insignificance the other state components, both those entering the accounting state vector and those entering the dividend (provided of course that the dividend-policy vector gives the dominant growth component a non-zero coefficient). Asymptotic considerations thus turn the multi-dimensional system apparently into an essentially one-dimensional one, and it is to this that Ohlson’s Principle (initially proven in dimension one only) might apply – see Theorem 2 below. That is to say, assuming dividend and dominant state variable are inter-linked, dividend irrelevance occurs if and only if takes a unique value, that value being the dominant eigenvalue of the dividend-retention matrix (that of the dominant state). (Of course, in the long run, observation of the dividend sequence permits inference of the dividend-policy vector.)

In this paper we offer an analysis of the quoted result based on algebraic considerations, some complex analysis (including an inessential reference to Marden’s ‘Mean-Value Theorem for polynomials’), and graphical analysis. These complement a standard textbook analysis based on Gerschgorin’s circle theorem – for which see e.g. [20, Th. 13.14] or [9, Th. 7.8d].

Unsurprisingly, the eigenvalues of may be located arbitrarily, but only if no restrictions are placed on the dividend policy Evidently, Dividend Irrelevance must implicitly assume the convergence assumption as a bound on the eigenvalues of . It transpires (see Proposition 3) that the dividend-policy vector is restricted by this assumption to the interior of an appropriate polytope in .

Conditions may be placed on the vector such that, when lies in an open region of parameter space, it is the case that the dominant eigenvalue of the augmented matrix is real and lies between the first largest and the second largest eigenvalue of the reduced matrix. This is the substance of our first main result stated here and proved in Sections 4 and 6.

Theorem 1 (An Eigenvalue Dominance Theorem). Suppose that has real positive distinct eigenvalues. In the canonical setting (4) we have as follows.

(i) If sign and sign for then the open set

has non-empty intersection with the set

Moreover, the second largest eigenvalue of for small is increasing in for small Under these circumstances dividend irrelevance holds uniquely at

(ii) More generally, the open set

has non-empty intersection with the set

and again under these circumstances dividend irrelevance holds uniquely at

(iii) If and for all and has all its eigenvalues in the disc of the complex -plane, then has an eigenvalue in the annulus

(iv) If and for all then the system has a real eigenvalue in the real interval .

For a proof see Section 6.

Remark. We see therefore that for an appropriate vector there is a region of parameter space for which the eigenvalues of the augmented matrix remain strictly bounded in modulus by , the dominant eigenvalue of Note the re-emergence of the side conditions analogous to the condition in Ohlson’s Theorem for (see [23]).

We are able to provide some information about the extent of the subspace (see formula (14) of §3) where we obtain (when ) the upper bound on positive of

for the case Moreover, Proposition 4 and calculations of §4 appear to imply that, even if rises above this bound, the two particular roots of the characteristic polynomial of which are forced into coincidence remain outside the disc in the complex -plane (as they move asymptotically to a vertical towards ), provided

By contrast, we find for and the top two roots of the augmented matrix both approach from opposite sides; this again is in keeping with the expectation that dividend irrelevance occurs only at the dominant root

Our results link to work concerned with the real spectral radius of a matrix, see Hinrichsen and Kelb [10], which investigates by how much a matrix may be perturbed without moving its spectrum out of a given open set in the complex plane. In the cited work the open set of concern is usually either the unit disc or the open left half-plane, both in connection with stability issues. Our interest, however, focuses additionally on the open set described by the annulus defined by the first and second largest eigenvalues of (cf. Th. 1). We note that there is a well-established Sturmian algorithm for counting the number of zeros of a polynomial in the unit disc in the complex plane (see Marden [16, §42, p. 148]), and so in principle the issue of Dividend Irrelevance is resolvable for a given policy vector by reference to the number of zeros in the unit circle of the two polynomials

Specifically, the first should have zeros and the second no more than The Schur-Cohn criterion [16, Th. 43.1], [9, §6.8] might perhaps also be invoked to count the number of roots in the unit disc.

2.1 Preliminaries

Our analysis is based on two results embodied in Proposition 1 and in the equivalences given in Proposition 2. The arbitrary placement of the zeros, the substance of Proposition 3, is also a consequence of Proposition 2.

Proposition 1 (Under the assumption of distinct eigenvalues). In the canonical setting (4) with

for any and fixed the equity is locally or globally independent of iff provided

| (6) |

in which case

The proof is in Section 7.

Remark 1. Apparently, if the eigenvalues of all lie in the disc with radius any other eigenvalue of the Proposition permits local dividend irrelevance to occur at several rates of return. We will show below that subject to (6) such an anomalous behaviour is definitely excluded when and also for some

Remark 2. In principle we might want to allow to respect a restriction in the directional sense of a re-scaling of accounting variables (if appropriate); it transpires from the next Proposition that the sign of can be absorbed by and the choice of sign is only a matter of symbolic convenience, so that we can interpret as saying That said, it is important to realize that rescaling an accounting variable, say by requires an inverse rescaling of the corresponding dividend-policy component, that is of by (in order to preserve the definition of dividend untouched). The right-hand side of the valuation equation perforce does not refer to the eigenvalues , despite the fact that these control the growth rates of the canonical accounting variables.

The following algebraic equivalences lie at the heart of all our arguments. Below we denote by the characteristic polynomial of

Proposition 2 (Inverse relations). Put The equations below are all equivalent.

| (7) |

| (8) | ||||

Polar form for with leading quadratic term:

| (9) |

Polar form for and with for :

| (10) |

In particular, with putting

| (11) |

we obtain the equivalent equation

Proof of equivalence follows in Section 8. Each of the above identities enables a different analytic approach.

Our first conclusion regards the potentially arbitrary placement of the zeros of (7).

Proposition 3 (Zero placement). In the canonical setting of Proposition 1, for an appropriate choice of real vector the characteristic polynomial

may take the form

| (12) |

for arbitrary choice of real coefficients The transformation

is affine invertible. The roots of the characteristic polynomial may therefore be located at will, subject only to the inclusion, for each selected complex root, of its conjugate.

This result is proved in Section 9.

Proposition 3 above indicates that in principle the region of parameter space in which the boundedness assumption holds may be obtained as the transform under the above mentioned transformation of the set of vectors satisfying a criterion derived from Cauchy’s theorem on the Inclusion Radius [9, Th. 6.41], [16, Th. 27.1], namely

(Recall that the inclusion radius of the polynomial (12) is the positive root of the polynomial .) Since the set of vectors so described is the interior of a polytope, the corresponding region in parameter space is therefore likewise seen to be the interior of a polytope. Let us term this the Cauchy polytope.

Evidently is on the boundary of the Cauchy polytope, since then

An immediate corollary is the following result, first announced for the case by Ohlson at the 2003 International Conference on Advances in Accounting-based Valuation – see [23, Lemma 4.1; generalization of Lemma 4.1: Appendix 2].

Theorem 2 (Multivariate Ohlson Principle). The system has dividend irrelevance at iff

Proof. By varying we can place one eigenvalue in the interval so by Proposition 1, there cannot be dividend irrelevance at and below. Note that this means that for the chosen

The situation with general placement of eigenvalues alters if is a positive real, lies below the eigenvalues of and the dividend-policy vector of the canonical setting is non-negative in all its components. The formula (10) confines the non-real eigenvalues to an infinite strip, while the formula (8) allows us to confine all the eigenvalues still further when is itself bounded.

We refer to formula (9) as the associated polar form. This form offers a graphical approach to the analysis of the real root location, and some insight into complex root location; in particular, the leading quadratic term is responsible for unbounded root behaviour, as follows.

Proposition 4 (Unbounded roots). Fix for with

(i) Subject to we have the asymptotic expansion

(ii) For the unbounded roots as behave asymptotically as follows:

For the proof, see Section 10.

Remark 1. In the case with we are of course assuming that If moreover for all and we have Here the conjugate roots have real part approaching from the right. However, with other sign assumptions on the sign of need not be positive, in particular if for all

Remark 2. By (8) we may rewrite the characteristic polynomial in the form

For fixed with pass to the limit as to obtain the following equation of degree

Thus given the assumptions of the Proposition, only two complex roots can be unbounded.

Remark 3. Note that, by contrast, the unbounded roots for fixed and varying have the asymptotic behaviour Note also that, if then the error term -behaviour alters.

Theorem 3. With fixed for such that and with if

the unbounded root locus does not enter the disc as So the system has local dividend irrelevance at uniquely at

Proof. Under these circumstances the unbounded roots are outside the disc , since they are confined to by virtue of

By Proposition 1 the only value remaining for is thus

Notation. Below and throughout, denotes the real interval where

comprises the two circles in the plane subtending angles of on

Proposition 5 (Strip-and-two-circles theorem). Suppose that that and that

(i) All the non-real roots of the characteristic equation (7) lie in the infinite strip of the complex -plane given by

The proof is delayed to Section 11.

Remark 1. Taken together parts (i) and (ii) may operate simultaneously. These results should, however, be taken together with Gerschgorin’s Circle Theorem, which implies immediately that the eigenvalues lie in the union of the discs in the complex -plane given by and by Thus the eigenvalues are bounded, not only to the above mentioned vertical strip but also to a horizontal strip of width around the real axis.

Remark 2. It is obvious that, for and with the real roots of (7) lie in by continuity. Gerschgorin’s Circle Theorem limits the real roots to the slightly larger interval Thus the two-circle result is merely a sharpening of the bounds.

Remark 3. If less elegant improvements can be made so that extends only as far as on the left.

We can state, ahead of the proof of Proposition 5, our theorem on eigenvalue location.

Theorem 4 (Eigenvalue bounds). Suppose that and that

Non-real eigenvalues lie in the rectangle bounded by Real eigenvalues lie in the interval

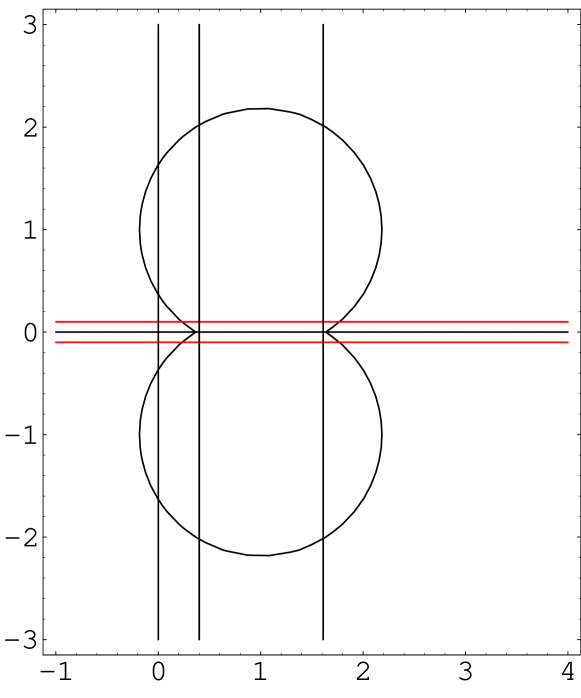

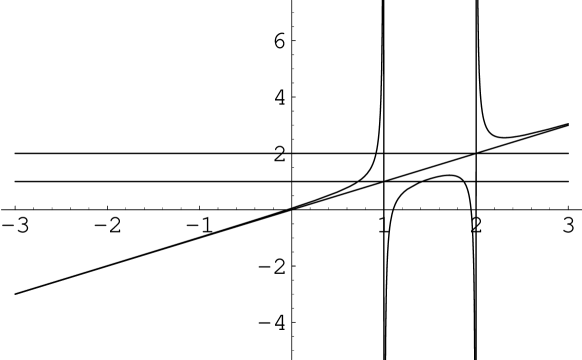

The theorem follows from Proposition 5 - see Figure 2. The two-circle result gives useful bounds only for the real roots.

Remark. The above analysis does not yet exclude the possibility of all eigenvalues being located to the left of We next offer a graphical analysis of the real-root locations in the following subsection, which shows that at least one root has to be to the right of when and for some

3 Eigenvalue location: general analysis

Our ultimate purpose (achieved in the next section) is to show that under suitable restrictions one can guarantee the existence of a real eigenvalue in the range Specifically, we show that if and there is a real eigenvalue in the range for all small enough positive . The aim of this section is to identify (i) the real-root locus of the characteristic polynomial of by examining the general features of the graph of the associated polar form of the characteristic equation given by (9), and (ii) the complex-root locus when the associated polar form has just two poles. The latter is a preliminary to our identification of (iii) an elementary estimate of the distortion effect of other poles.

In this section the real eigenvalues of (see equation(4)) are studied as functions of with the other components of fixed. Interest naturally focuses on as the link coefficient with the dominant state vector. The two-pole case arises when and is considered as a benchmark, with a view to understanding how the multi-pole situation deforms the benchmark case.

Treating as a free variable, with the remaining dividend-policy coefficient fixed, we use (9) to study the map and its local inverses. We have, with as in (11),

| (13) |

so that the graph of , or of against has vertical asymptotes from right to left at all of which are manifestly simple poles. The asymptotes break up the concave leading quadratic term (if into connected components corresponding to the intervals . The equation

is equivalent to an -degree polynomial equation so its roots contribute to at most stationary points in the graph.

In the interval the component has an even, respectively an odd, number of stationary points depending on whether the sign of is or In view of the behaviour of the leading quadratic term, not all the components can be monotone (possess a zero number of stationary points!). Thus at least one component is non-monotonic.

The components may be interpreted as graphs/loci of the eigenvalues More precisely, the differentiable local inverses of the mapping are the graphs of That is to say, each non-monotonic component must be first partitioned into monotone parts on either side of its stationary points. The labelling of these inverses from right to left respects the cyclic order on the set together with one or other of the identifications

The latter may require the point at infinity on the asymptote to be considered as the intersection of consecutive loci.

Note that from (13) and so . (This is consistent with the matrix having a first column with zeros in all but the last row.)

We will see in §4.1 from these asymptotic features of the graph that, since for all small enough positive the eigenvalue is in the range as we now demonstrate.

As a preview of the full argument of §4.2, with our assumption that and we note that we can arrange for to be large and positive in the vicinity to the right of by taking With the domain of is infinite, so that

Thus the largest real eigenvalue of remains above See Figure 3 (in §4.1 below). Of course for small enough the remaining roots even if complex, remain in an open vertical complex strip including the closed real interval

We can similarly arrange for to be large and negative in the vicinity to the right of by taking In view of the behaviour of the graph for large this implies the existence of two roots in under these circumstances. With the domain of is bounded, say by and one has

See Figure 4 (below in §4.1). As the eigenvalue remains above dividend irrelevance can occur only at An upper bound for is provided by the maximum value of the leading quadratic term

obtained by evaluation at namely

| (14) |

This gives the coefficient at the previous date’s dividend, a significant bounding role.

In order to understand the qualitative behaviour of the complex eigenvalues of the characteristic equation, we study the associated polar form on an open interval between the two adjacent poles at and for As a first step, we study the contribution to arising in (13) only from the two terms corresponding to the two adjacent poles and . In the subsequent section we identify how the presence of the other terms in (13) perturbs this simple analysis.

3.1 Root locus for two-pole case

For present purposes, by scaling and a shift of origin, as we may take and It is convenient to study the corresponding terms of by introducing and looking at the two functions

The first of these has its zero at in and maps bijectively onto the reals. The second function is more awkward; provided it has a zero outside at More information is provided in the Circle Lemma below.

Circle Lemma. For the function has a positive local minimum value at and positive local maximum value at where

The range of on omits an interval of positive values .

For the equation

| (15) |

has conjugate complex roots in the complex -plane describing a circle centred at the real number with radius

The real part moves from towards Hence for as decreases from the real part increases and for it decreases.

Note. See below for a more general analysis of the behaviour of the real part near a local minimum. For the function is symmetric about and is asymptotic to zero at infinity; a limiting version of the lemma is thus still valid, but the conjugate roots lie on the vertical line for

Proof. The conjugate roots satisfy

In view of the dependence of the real part on as given by we see that the term can be absorbed by a shift of origin on the axis. Hence the locus as varies is a circle. Reference to the extreme locations identifies the shifted centre, and the radius.

3.2 Multi-pole case: a distortion estimate

The presence of additional poles outside distorts the result obtained in the Circle Lemma above for the two-pole contribution. Provided all the eigenvalues are well-separated, i.e. the ratio of adjacent intervals does not vary greatly (see the calculation of below), the distortion is controlled by the value of . In the next subsection we take note of a third-derivative test (based on Taylor’s Theorem) which identifies bifurcation behaviour of coincident real roots. For an application see §4.5.1.

We again work in the standardized co-ordinate system with the adjacent poles at and Put then the decomposition, valid for and

yields the following bounds:

These and an amendment of the parameter in to a variable coefficient for in the closed interval enable us to account for the presence of terms other than in by absorbing their contributions into On the ‘adjusted’ inherits from boundedness, continuity and indeed two-fold differentiability. Thus we have

where for close to . Expansion round yields

so

The main point of this is to observe how perturbs the complex roots (cf. Figure 7). The equation (15) of the Circle Lemma now gives us the following.

Proposition 6 (Distortion Estimate). The equation

is equivalent to for

The equation is equivalent to

with where

We note that

3.3 Analysis of the real part via Taylor’s theorem

Proposition 7 (Third-derivative test: real part follows ). Suppose that has a local minimum/maximum at Let denote the local solution for over the complex domain of the equation for

with small and with . If then the locus satisfies initially:

For a proof see Section 12. Proposition 7 implies that the quadratic terms of the associated polar form have no effect on the local behaviour of the real part at a bifurcation.

4 Eigenvalue location: some cases

In this section we consider the case and the two cases with general when are of constant sign for as referred to in Theorem 1.

4.1 The case

This case is in fact typical, despite having the simplifying structure that one root of the cubic characteristic polynomial is always real. There may thus be two more real roots, or two conjugate complex roots.

In view of earlier comments, we need to consider only the case Interpret this as saying and

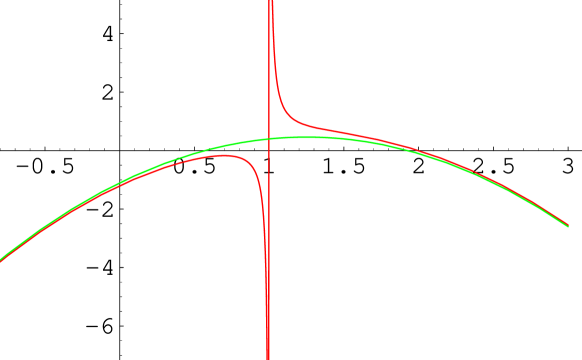

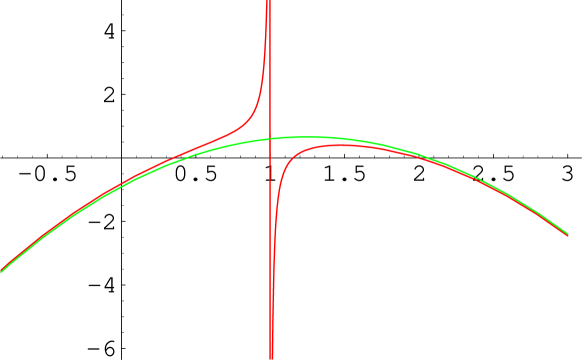

(a) For now assume (For see (b) below.) Taken together Figures 3 and 4 tell it all. They graph the implicit relation between and the eigenvalues as given by the equation treating as the independent variable and as dependent. To derive the root locus for real roots rotate the graphs, so that becomes the independent variable. Then each branch of the graph yields the as the dependent eigenvalues in decreasing magnitude.

If then for increasing as in Figure 3, the dominant root of decreases down to (in the limit).

If then for increasing as in Figure 4, the first/second root of , respectively, decrease/increase into coincidence in the interval Thereafter, the root locus of the conjugate pair behaves as illustrated below in Figure 5. That is, the real part decreases towards and the imaginary parts tend to infinity.

(b) We consider now the limiting case . As the characteristic polynomial is

this has one root at which, by Proposition 1, precludes DPI occurring at Note that the expression in square brackets corresponds to an analogous problem with reduced order (effectively the case), and this feature, of a reduction of order, occurs for general .

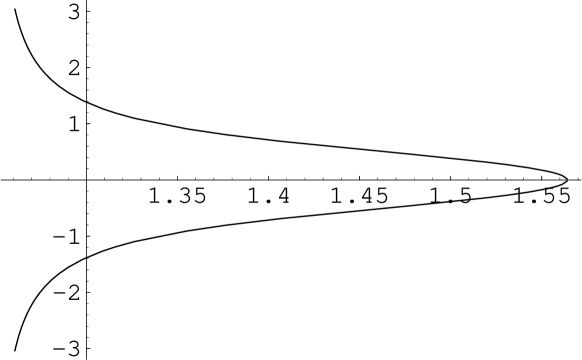

Remark. Of course, for the characteristic polynomial of for has two additional real roots in the interval for small For larger the conjugate roots lie in the complex -plane on the vertical This is because

As before, if , then and the conjugate roots do not enter the open disc ; however, if , then which means that two roots will be in the open disc for a range of values of with the third on the boundary. Eventually the conjugate pair exits the annulus (see Figure 1).

4.2 General case with for

We fix arbitrarily for . The assumption is without loss of generality interpreted as with variable The analysis now proceeds similarly. Here we have the identity connecting eigenvalue and parameter in the shape of the associated polar form (9):

We note that the quadratic term reflects the behaviour of the two equations which remain when all the variables other than the dividend and the dominant accounting variable are ignored (equivalent to taking Our analysis identifies the locations of all the real roots of in order to discuss the equation

Noting that and , by the Intermediate Value Theorem, there exist roots for of the equation which are real and satisfy

Finally, since and there exists a root

Evidently the equation similarly has roots for any in the same intervals for . Thus we have ‘interlacing’ for :

Now and with There are thus two generic possibilities.

(i) The equation has a root in . In this case, as increase from zero there are initially two real roots and of the equation which lie in and which move into coincidence. Thereafter they become complex conjugates which behave qualitatively as in the case In particular, are increasing in (under the assumptions of this case), and since

with the right-hand side constant, we see that is decreasing in As the lower bound is the complex roots certainly do not enter the disc provided i.e. (Note that

(ii) The function is negative in and the equation has its remaining root in In this case the convergence assumption is violated for small in that there are eigenvalues of outside the disc

Finally, the special case arises when has a double root at In this case as increases from zero the remaining two roots are conjugate complex and again behave as in Figures .

4.3 General case with for

This proceeds similarly. The root decreases towards as increases. Likewise the roots for decrease towards As these latter roots remain bounded, the remaining two roots and may be real, but will be the unbounded complex conjugates for large enough (indeed the remaining component of the graph is -shaped). This time the real part increases towards as increases.

4.4 General case when for some with for remaining indices

We find that in all these cases DPI cannot hold at by Proposition 1.

Clearly, if then is an eigenvalue of the system, i.e. there is an eigenvalue in the annulus and so DPI cannot hold at

In general, if for just one of then and in fact

with the matrix obtained from by omitting the -th row and column, i.e. a reduction of order occurs. But now the assumptions for agree with those made in the case of the previous subsection. It now follows that has an eigenvalue in the annulus , and so again DPI cannot hold at

Finally, if for several among and for the remaining indices , then a further reduction of order occurs, with the same conclusion that an eigenvalue exists in the annulus . So here too, DPI cannot hold at

Note that in both scenarios the locus of decreases as increases from zero.

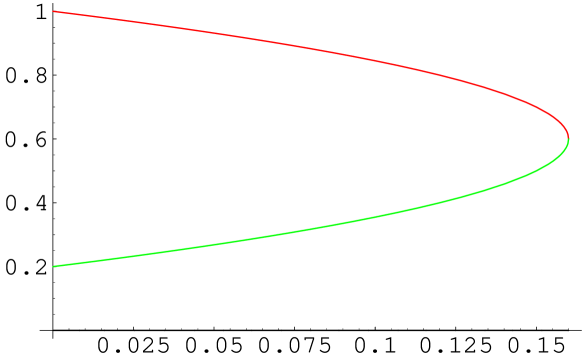

4.5 Effect of the dividend-on-dividend multiplier: a distortion example

We conclude this section by illustrating the effect of the policy parameter on the three eigenvalues in the case In the range we see in the illustrative example of Figure 6 that the root decreases whilst the root increases as increases; increases for all as might be expected, with as supremum. Intuitively speaking, the push away from the origin created by the two increasing roots and causes the location of the coincident root to execute a jump up to a new coincidence location above by way of a continuous root locus in the complex -plane (see the Remark on bifurcation in the next section). The push can in fact be physically interpreted. The partial-fraction-expansion terms in (10) may be regarded as modelling electric charges placed at the pole locations and acting according to an inverse distance law (see Marden [16, §1.3 p. 7]). Thus for large enough to ensure both and have been re-located above , we see the locus of resume its downward path towards the origin (but tending in the limit only as far as the barrier ), while resumes its upward path away from the origin. The locus dynamics are investigated more properly in the next section.

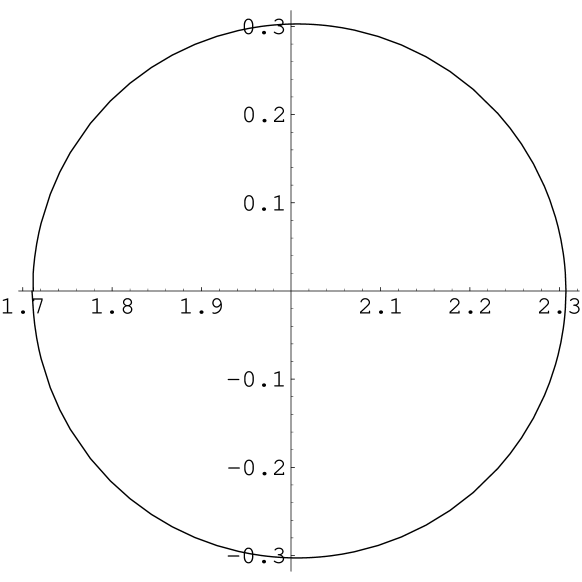

The conjugate root locus for this case is shown in Figure 7. For varying over the range corresponding to the presence of complex roots (with and fixed), the root locus of the conjugate pair appears close to being a circle as a consequence of the Circle Lemma and Proposition 6.

4.5.1 A case study: distorted circle

Since we have here

so the equation is equivalent to The essential reason for the closeness observed here is the slow variation of in the vicinity of . Indeed, by (8) we have

from which we compute that

and so

So the positive sensitivity to variation in is slight, as asserted, though in fact it is increasing.

Of course, writing in place of all the dependence on is formally lost; however, note that the remaining constant is inadequate as an explanataion of the actual radius.

4.6 Qualitative behaviour in the most general case

The picture emerging from our analysis for is that the dominant and subdominant eigenvalues remain in the annulus (of Th. 1) provided

Other eigenvalues, when real, interlace between the eigenvalues of with remaining associated with for or One pair of roots become unbounded as a complex conjugate pair and are asymptotic on one or other side of as depending on the remaining parameters of Evidently a regime change occurs with the unbounded root locus being vertical. Other conjugate pairs execute deformed circles as described by the Circle Lemma and Proposition 6 of §3.1.

5 Differential properties of eigenvalues: some bifurcation analysis

The purpose of this section is to analyse briefly the root locus in the -plane. We conduct a partial analysis mostly concentrated on the dynamics of the dominant eigenvalue as changes (with the remaining policy parameters fixed) with a view to completing the proof of the dominance theorem in the next section. Our starting point is the following proposition, which follows from (8) by implicit differentiation. It is suggested by our earlier Circle Lemma of §3.1 and Proposition 6 concerning the third derivative.

Proposition 8 (Under the assumption of distinct eigenvalues). In the canonical setting of Proposition 1, let the dividend-policy vector be represented by with The eigenvalues of the augmented matrix viewed as functions of satisfy the following differential properties expressed in terms of the constants :

(i) for

| (16) |

(ii) for

| (17) |

Proof. From the identity

we have

so that

So, for as then ,

From the identity

by implicit differentiation,

except at the critical points defined by

e.g. where the locus of crosses The result of the Proposition now follows directly from (8).

Remark. For the assumption of distinct roots to hold we must manifestly disregard the non-generic critical points, which are those points where any two of the functions agree in value; of particular importance to us are points where may cease to be the largest eigenvalue (in modulus), as for instance when it agrees in value with . The first formula when is to be read as

and note that, at we have, by (3), and for

| (18) |

and

The equation (18) implies that the choice of a value close to will accelerate the growth rate of the leading canonical variable relative to the first dividend-policy coefficient.

Technical point. In the arguments that follow, it is important to realize that when the roots and are complex conjugates, then for real the following signature property is satisfied:

just as when and were real and both below . (Since the quadratic has no real roots, it is positive definite here.)

Corollary 1 (Bifurcation behaviour near ). Assume the eigenvalues of are real and distinct and that for is real and satisfies At any bifurcation point, for small enough positive increments in the conjugate complex roots and move away from the origin if , and towards the origin if .

Remark. The corollary is thus in keeping with the intuition expressed in connection with Figures where we alluded to the push away from the origin for the root regarded as a function of

Proof. Suppose that Suppose that occurs at some point If now with , put and so that

We need to be sure which of is to be interpreted as and and whether the display above is correct. In fact, either interpretation is valid, and leads to the same conclusion; we return to this issue in a moment. Thus, since for small enough we shall have

so that

and hence that

where is small and positive. That is, the remaining ratios pull in the same direction, towards the origin. Note that if we switch the interpretation of around, then the angles change sign, making small and negative. However, the sign of also switches.

In conclusion, the conjugate complex roots and initially move closer to the origin if See Figures above for an illustration in the case where the third root of is evidently real. Note the vertical asymptote in the complex -plane for identified by Proposition 4.

Remark (Bifurcation behaviour elsewhere). Assuming that the first repeated root is not the dominant root, one may attempt to repeat the argument at the other locations to observe a tug of war between those ratios below the coincidence location pulling one way and those above it pulling the other way. (We have noted in §4.5 the electric force field interpretation.) Who wins this tug of war is determined by the geometric considerations, and so we discover that there will be a critical point a watershed, such that to the right of the complex roots move towards the origin, whereas to the left they move away from it.

Corollary 2. Assume all the eigenvalues are real and positive, at some is the maximal eigenvalue (in modulus) and is real, and further

Then

(i) for

(ii) for

and finally for

Proof. Counting the signs gives

For

| sign | ||||

Corollary 3. Suppose all the eigenvalues of are real and positive, and is small enough so that

and is real with

Then, for each with real,

where In particular, provided

Proof. Recalling for that

we compute that

and so

6 Proof of the dominance theorem

We may now put together the analysis of the last sections to deduce our main result concerning the location of the dominant eigenvalue of .

Proof of Eigenvalue Dominance Theorem. We consider the first part of the theorem only, as the more general result follows by a restatement of the same argument. By selecting the sign of as and of for as we can arrange, given (18), for the eigenvalue function identified by the condition to be decreasing in in the region

and so to remain below We have, however, to ensure that remains the maximal root. Recall that Since the remaining eigenvalues are below we may, by continuity, ensure that the eigenvalues functions of also lie strictly below and that moreover

Remark. By Corollary 3 it is possible that, following a path in parameter space, the locus of intersects that of . Note, however, that if upon intersection at we were thereafter to have for close to then provided the remaining eigenvalues remain below the signs of all the derivatives and those of would switch, i.e. both loci would turn around, a contradiction. Thus, subject to the assumption about the remaining eigenvalues, this implies that in fact is at the boundary of that region in policy-parameter space where and are both real. Moreover, according to (16) the graph has infinite slope at We illustrate this point in the following simple example with and

Example. For let

The characteristic polynomial is Here

since The roots are real for

and we have

We note that as the roots become complex the real part stays constant at i.e. the root locus bifurcates and the conjugate roots move orthogonally to the real axis; there being no poles in this simple case, there is no ‘push’ on the real part, neither away nor towards the origin. In particular, provided the roots are in the unit circle, they remain in the annulus

7 Obtaining dividend irrelevance

In this section we prove the results in Proposition 1.

After a change of accounting state variables from to, say the system becomes

where

with the new augmented matrix (with the same eigenvalues as the original augmented matrix and where are the eigenvectors of assumed presented in decreasing modulus size (with largest).

Evidently the characteristic polynomial

is the same as . We assume its eigenvalues have distinct modulus.

The force of our implicit assumptions on the dividend significance coefficients is that they are all non-zero: for all Otherwise, the eigenvalues of the augmented matrix would include all the eigenvalues of the reduced matrix. (To see this expand the characteristic determinant by the -th row.)

Henceforth we assume the canonical variables have been re-scaled by and we may therefore take for the canonical dividend significance coefficients the symbol with the additional stipulation that

As a first step we note the consequence for dividend irrelevance of the non-zero dividend significance coefficients. Writing and fixing there are coefficients such that

Now the equation

with the solution also given by the eigenvalues of the augmented matrix

must satisfy

for all Hence

We thus have, assuming for all that the dividend series converges, and

Consequently, if is permitted, then

This indeed depends only on the initial data. See Ashton [Ash] for a discussion of this formula. The earliest form of this equation is due to Ohlson in 1989, though published later in [22].

We recall that the basis of this calculation is the identity

We will thus obtain dividend irrelevance at provided all the eigenvalues are in modulus less than

8 Derivation of equivalences

We begin by expanding by the bottom row

to obtain

or

where

Similarly,

This yields the equation

Dividing by ,

or

as required.

Dividing by we obtain

9 Invertible parametrization and zero placement

This section is devoted to a proof of Proposition 3. Let us write

so that

denotes the elementary symmetric function summing the zeros of taken at a time. Thus

Hence

As a first step we compute that

and that

Similarly,

The pattern is now clear, and we shall show by induction that

Indeed,

Note that

so

Our next step is to observe that the coefficients in the polynomial on the right-hand side of identity (8) may be expanded as follows:

where

(i.e. the summation refers to the omission of from any of the components ). Note also that

We now consider for constants the identity

Comparing sides, we obtain

Now given any we select so that

For the remaining equations, we have

where i.e.

Here the coefficient matrix is given as follows:

Its determinant is equal, up to a possible sign change, to the van der Monde determinant Hence is non-singular and the equation may be solved for any given vector To see this, note that may be reduced to the alternant matrix in the variables

(taking times the first row, times the second row and so on).

It is now easy to find the inverse transformation by applying the elementary row operations just used to the original matrix equation. This leads to the following result. Putting the original equations

now transform to

where

Note that with the sign adjustment the equations specify as a convolution (taking Now we have

where the inverse is given by (see Klinger [14]) the matrix with entry

here is the elementary symmetric function as above (sum over the -fold product omitting the variable ).

10 Asymptotics of the unbounded roots

Proof of Proposition 4. Assume that for We rewrite (9) as

so that

Iterating, we obtain

and hence the assertion of the Proposition follows provided The alternative direct derivation by expanding as a geometric series is less informative about the convergence of the series.

We may in principle use the identity (10) (valid for all large enough ) recursively to obtain an asymptotic expansion (in for the unbounded roots.

To obtain the first term of the expansion, let and consider the quadratic approximation

so that is large and positive and

Hence for we have the first term of the expansion to be

Now write

With this notation, taking only one term in (10) we have with large and negative that

so to first order in

Writing and taking real and imaginary parts gives the two equations

Note that for

Now the determinant of the two equations in and above is positive and equal to

Solving for and we have

so that

The result for assumes that and further that

i.e.

11 Strip-and-two-circles theorem

We prove Proposition 5. For part (i) we argue as follows. Suppose, for all , that and Suppose satisfies

If is strictly to the right of then we may also assume that has positive imaginary part (otherwise switch to the conjugate root ). The argument of is thus positive for each and that of negative, i.e. has negative imaginary part. The right-hand side therefore sums to a complex number with negative imaginary part. However, has positive imaginary part.

If is to the left of then we may suppose it has negative imaginary part. The argument of is for each thus positive, as also for Now apply the previous reasoning to the identity

For part (ii), let be arbitrary real for We will apply Marden’s ‘Mean-Value Theorem for polynomials’ (Marden [16, §2.8 p.23]) to the polynomials for and the polynomial as defined by

We must, however, first find for each the location of the roots of the equation The roots are of course for taken together with the two real roots of

which are to the left of and the right of . The exact and approximate formulas are

and require that

Thus the roots of all the equations lie in the interval By Marden’s Theorem in the special case of real positive scalars summing to unity, the roots of

lie in the star-shaped region (cf. Prop. 5). Thus if we take small and so that

then indeed and all the roots of (7) lie in the said star-shaped region.

In fact, one may take small and and for for and leading to the restriction

i.e.

12 The third-derivative test

The result in §3.3 is a consequence of the following by specializing when

Proposition 9. For with , the solution over the complex domain of the equation

with small and subject to satisfies

The imaginary part is initially increasing and satisfies

Proof. Below we work to order . Without loss of generality we assume that (Otherwise rescale and by ) Set then, by Taylor’s Theorem, the first approximation to the equation is

with solution . So we introduce correction terms by putting

and solve a second approximation

Substitution for gives after cancellation of the term

| (24) | |||

Equate real and imaginary parts to cancelling the second by (non-zero, w.l.o.g.) gives

The roots corresponding to the imaginary part, for and sufficiently small, are

So we may neglect and in what follows, which leads to the approximation

Claim. For small enough, In particular, is the same sign as . (So, also, conversely, if is the same sign as then

Proof. The equation for the real part of (24), ignoring and cancelling by gives

Its two roots have negative product and

The root near is ruled out by the continuity of the root locus, which tends to as For the positive root is near and so as For the negative root is and again as

References

- [1] Ashton, D.: The cost of Equity Capital and a generalization of the Dividend Growth Model. Acc. Bus. Res. 26, 34–18 (1995)

- [2] Ashton, D. , Cooke, T. , Tippett, M., Wang, P.: Linear information Dynamics, Aggregation, Dividends and "Dirty Surplus", Accounting. Acc. Bus. Res. 34 , 277–299 (2004)

- [3] Bellman, R.: Introduction to Matrix Analysis. Reprint of the second (1970) edition. Classics in Applied Mathematics 19, SIAM (1997).

- [4] Bhattacharya, S.: Imperfect information, dividend policy, and "the bird in the hand" fallacy. Bell J. Econ. 10 , 259–270 (1979)

- [5] Davies, R.O., Ostaszewski, A.J.: Optimal forward contract design for inventory: a value-of-waiting analysis. This volume, chapter 4

- [6] Dybvig, P.H., Zender, J.F.: Capital Structure and Dividend Irrelevance with Asymmetric Information. Rev. Fin. Studies, 4, 201–219 (1991)

- [7] Gao, Z., Ohlson, J.A., Ostaszewski, A.J.: Dividend Policy Irrelevancy and the construct of Earnings. J. Bus. Fin. Acc. 40, 673–694 (2013)

- [8] Gietzmann, M.B., Ostaszewski, A.J.: Predicting firm value: the superiority of q-theory over residual income. Acc. Bus. Res. 34, 349–377 (2004)

- [9] Henrici, P.: Applied and Computational Complex Analysis, Vol. I: Power Series-Integration-Conformal Mapping-Location of Zeros. Wiley, (Reprinted 1988) (1974)

- [10] Hinrichsen, D., Kelb, B.: Stability radii and spectral value sets for real matrix perturbations. In: Systems and Networks: Mathematical Theory and Applications, vol. II, pp. 217–220, Invited and Contributed Papers, Akademie-Verlag, Berlin (1994)

- [11] Horn, R. A., Johnson, C. R.: Matrix Analysis. Cambridge Univ. Press (1985)

- [12] Hwang, S-K.: Cauchy’s interlace theorem for eigenvalues of Hermitian matrices. Amer. Math. Monthly 111, 157–159 (2004)

- [13] Jack, A., Johnson, T., Zervos, M.: A singular control model with application to the goodwill problem. Stochastic Process. Appl. 118, 2098–2124 (2008)

- [14] Klinger, A.: The Vandermonde matrix. Amer. Math. Monthly 74, 571–574 (1967)

- [15] Lo, K., Lys, T.: The Ohlson model: contribution to valuation theory, limitations, and empirical applications, J. Acc. Aud. Fin. 15, 337–367 (2000)

- [16] Marden, M.: The Geometry of the Zeros of a Polynomial in a Complex Variable. Amer. Math. Soc. Math. Surveys (1949)

- [17] Miller, M. H., Modigliani, F.: The Cost of Capital, Corporation Finance and the Theory of Investment. Amer. Econ. Rev. 48, 261–297 (1958)

- [18] Miller, M. H., Modigliani, F.: Dividend Policy, Growth, and the valuation of shares. J. Business 34, 411– 433 (1961)

- [19] Miller, M. H., Modigliani, F.: Corporate income taxes and the cost of capital: a correction. Amer. Econ. Rev. 53, 433–443 (1963)

- [20] Noble, B.: Applied Linear Algebra. Prentice-Hall (1969)

- [21] Ohlson, J.: Earnings, book values, and dividends in equity valuation. Contemporary Acc. Res. 11, 661–687 (1995)

- [22] Ohlson, J.: Accounting Earnings, Book Value, and Dividends: The Theory of the Clean Surplus Equation (Part I). In: (R.P. Brief and K.V. Peasnell, eds.) Clean Surplus: A Link Between Accounting and Finance, pp. 165–230, Garland Publishing (1996)

- [23] Ohlson, J.A., Gao, Z.: Earnings growth and equity value. Foundations and Trends in Accounting 1, 1–70 (1981)

- [24] Preinreich, G. : The fair value and yield of common stock. Acc. Rev. 11, 130–140 (1936)

- [25] Rugh, W. J.: Linear System Theory. Prentice-Hall (1996)

- [26] Seneta, E.: Non-negative Matrices and Markov Chains. 2nd ed. revised reprint (1st ed. 1973), Springer (1981)

- [27] Tippett, M., Warnock, T.: The Garman-Ohlson Structural System. J. Bus. Fin. Acc. 24, 1075–1099 (1997)

- [28] Wilkinson, J. H.: The Algebraic Eigenvalue Problem. Oxford Univ. Press (1965)

Mathematics Department, London School of Economics, Houghton Street, London WC2A 2AE; A.J.Ostaszewski@lse.ac.uk