A Robust Bootstrap Change Point Test for High-dimensional Location Parameter

Abstract

We consider the problem of change point detection for high-dimensional distributions in a location family when the dimension can be much larger than the sample size. In change point analysis, the widely used cumulative sum (CUSUM) statistics are sensitive to outliers and heavy-tailed distributions. In this paper, we propose a robust, tuning-free (i.e., fully data-dependent), and easy-to-implement change point test that enjoys strong theoretical guarantees. To achieve the robust purpose in a nonparametric setting, we formulate the change point detection in the multivariate -statistics framework with anti-symmetric and nonlinear kernels. Specifically, the within-sample noise is canceled out by anti-symmetry of the kernel, while the signal distortion under certain nonlinear kernels can be controlled such that the between-sample change point signal is magnitude preserving. A (half) jackknife multiplier bootstrap (JMB) tailored to the change point detection setting is proposed to calibrate the distribution of our -norm aggregated test statistic. Subject to mild moment conditions on kernels, we derive the uniform rates of convergence for the JMB to approximate the sampling distribution of the test statistic, and analyze its size and power properties. Extensions to multiple change point testing and estimation are discussed with illustration from numerical studies.

doi:

10.1214/154957804100000000keywords:

[class=MSC]keywords:

1904.03372 \startlocaldefs \endlocaldefs

and

1 Introduction

Change point detection problems are commonly seen in many statistical and scientific areas including functional data analysis [6, 3], time series inspection [7, 35, 60], panel data study [19, 51, 34, 8], with applications to fields of biomedical engineering [4, 62], genomics [58], financial revenue returns [5, 20, 8] among many others. Statistical testing and estimation of change points have long history with extensive literature [24, 7, 32, 5, 9, 43, 42]. This paper studies the problem of change point detection for high-dimensional distributions (i.e., ) from a location family with shift parameter. Let be a sequence of independent random vectors taking values in . Our goal is to test whether or not there is a location shift in the distribution functions . Precisely, let be a location family indexed by the shift parameter , where is the standard distribution in ( is arbitrary). We consider the following hypothesis testing problem:

An advantage of this model is the flexibility of whose mean parameter can be non-existing. Before highlighting the robustness from it, we shall first illustrate below the intuition of constructing a test statistic for separating and . For brevity, we denote (i.e., ) for a fixed , and . With this notation, we have that are independent and identically distributed (i.i.d.) with distribution and that are i.i.d. with distribution such that the change point detection problem boils down to the two-sample testing problem for the shift parameter with an unknown change point location . Since is unknown, we may take all possible ordered pairs in the whole sample , such that the within-sample noise (i.e., in each and samples, separately) cancels out and the between-sample signal is properly preserved under . Note that our change point hypothesis on the location family is the same as the location-shift model:

| (1.1) |

Viewing as the mean-shift, a natural choice for detecting the existence of a change point shift is to consider the noise cancellations in the empirical mean differences:

| (1.2) |

Under , we have so that there is no mean-shift signal contained in and the sampling behavior of is purely determined by the random noises . On the other hand, if is true, then . Thus, if the mean difference between the two samples is large enough to dominate the random behavior of (due to noise ) under , then the statistic would be able to distinguish between .

In practice, a main concern of using in (1.2) is its robustness. Specifically, the (empirical) mean functional is not robust in the sense that its influence function is unbounded. Further, in the high-dimensional setting, robustness is a challenging issue since information contained in the data is rather limited. To address this problem, we view the shift signal as a more general location parameter in the distribution family without referring to the means. This simple observation brings a major advantage that change point detection can be made possible even in cases where the means are undefined (such as the Cauchy distribution). To achieve the robustness purpose in a nonparametric setting, we consider a general nonlinear form of (1.2) in the -statistics framework. Let be an anti-symmetric kernel, i.e., for all . We propose the statistic

| (1.3) |

to test for against . Clearly, is a (scaled) -statistic of order two. The anti-symmetry of the kernel plays a key role in testing for the change point in terms of noise cancellations. To see this, under we have and . Observe that

Thus if is true, then , where is the change point signal through the kernel . If has a suitable lower bound, then we expect that can separate and . For instance, consider the sign kernel , where is the component-wise sign operator of (i.e., for , if , , , respectively). Then,

where is a random variable with symmetric distribution. In particular, if is the distribution in with independent components such that each component admits a continuous probability density function , then under local alternatives (i.e., ) we have , where is the convolution of the densities of and . Hence, and have the same magnitude, implying that signal distortion under the sign kernel is only up to a multiplicative constant.

The mean difference statistic in (1.2) is a special case of with the linear kernel and . The sign kernel considered above is another important anti-symmetric and bounded kernel, which is useful if the means are not robust or undefined. Specifically, for the sign kernel, component-wise median of corresponds to the Hodges-Lehmann estimator for the component-wise population median of the location difference before and after the change point [31]. In the univariate case , it is known that the Hodges-Lehmann estimator is a highly robust version of sample mean difference (with the linear kernel) against heavy-tailed distributions, and it has a much higher asymptotic relative efficiency (with respect to the mean) than the sample median at normality [55]. In addition, when the change point location is known, is also equivalent to the classical nonparametric Mann-Whitney test statistic (see e.g., Chapter 12 in [53]).

Since is a -dimensional random vector, we need to aggregate its components to make a decision rule for hypothesis testing. We construct the critical regions based on the Kolmogorov-Smirnov (i.e., the -norm) type aggregation of , namely our change point test statistic is

| (1.4) |

Then is rejected if is larger than a critical value such as the quantile of . In Section 2, we will introduce a (Gaussian) multiplier bootstrap to calibrate the distribution of , and we will establish its non-asymptotic validity in the high-dimensional setting in Section 3.

We point out that our test statistic has comparable computational and statistical properties to the widely used cumulative sum (CUSUM) procedures in literature. For a classical treatment of the CUSUM (and other change point) statistics, we refer to [21] as a monograph on the change point analysis. The CUSUM statistics are defined as a sequence of (dependent) random vectors in of the form

| (1.5) |

It is obvious that the CUSUM statistics have a sequential nature in that the left and right sample averages are examined along all possible change point locations, which is necessary to estimate the location . However, if the goal is only testing for the existence of a change point, this (local) sequential comparison strategy is not as efficient as a global test (1.3), both computationally and statistically. Consider , which is the case for the sign and linear kernels. For a general nonlinear kernel, computational cost is for (and also for ). If the kernel is linear (i.e., ), then the computational cost can be further reduced to for effortlessly. Thus we call is the global one-pass Mann-Whitney type test statistic. In contrast, the computational cost for is which can reduces to [39] via dynamic programming. Statistically, it has been shown in [61, 38] that a boundary removal procedure is needed for the (bootstrapped) CUSUM change point test to achieve the size validity since the distributions of are difficult to approximate at the boundary points. On the contrary, the test statistic proposed in this paper does not remove any boundary points because we are able to approximate the distribution of based on majority of the data points in the sample . Thus it is expected that achieves faster rate of convergence in the error-in-size for the bootstrap calibration. See Remark 2 ahead for a detailed comparison.

1.1 Literature review and our contribution

Single change point inference has been extensively studied in literature such as [21, 29, 33] for univariate or fixed multivariate setting.

Using anti-symmetric kernels in -statistics for location change can be traced back to [49], which considered a CUSUM-type sequence of two-sample Mann-Whitney statistics with the sign kernel and took the maximum absolute value along the sequence as the test statistic. Asymptotic properties of such statistic for univariate data have been studied in the settings of online and offline change point problems [22, 27, 30, 40]. To the best of our knowledge, the proposed global one-pass Mann-Whitney type change point detection procedure in (1.3) based on a general anti-symmetric kernel without using a CUSUM-type sequence is new in literature, even in the one-dimensional case.

Second, owing to increasing ability to handle large dimensional data, the focus migrates to a more challenging stage in high dimension that allows faster than . Therefore, signal aggregation across dimension becomes influential in the designing of statistics and algorithm. For instance, [38, 61, 57] dealt with sparse change (i.e. mean structure changes in a sparse subset of coordinates), while [8, 34, 25] considered -type aggregation for dense change. Taking both cases into account, [25] proposed a scan test statistic aiming at sparser change coupled with their linear statistic in inference. [19] adopted additional weighted CUSUM-type factor along coordinate to make the double-CUSUM statistic more adaptive in detection. The detection rate are also investigated in terms of sparsity and signal magnitude as well as change point location [25, 44, 59]. We show that our result achieves optimal minimax rate, cf. Remark 5. For multiple change point detection which is more challenging and essential in applications, we will discuss a backward detection (BD) algorithm without introducing external statistics. We will also discuss an extension to dependent sequence in Remark 6.

Among the change point literature, mean change are widely explored using CUSUM statistics [38, 61, 19, 20], least-square type statistics [8, 10], -statistics [56] and some other kernel based methods [48, 12, 2]. In practice, when error terms are heavy-tailed, Gaussianity assumption is beyond salvation and becomes too restrictive. This concern especially highlights the potential of robust nonparametric methodology (such as nonlinear projection) to avoid direct measure on mean or higher moments in data distributions. Note that the -statistic approach, including our method in this paper, is conducting “global” characterization (either one-sample or two-sample) via kernels to have change point signals peak. Such kernel concept is different from kernel density estimator or kernel distance measure for individual observations. Specifically, [48] proposed CUSUM variant statistic based on kernel transferred data points; [12] smoothed left and right mean function using kernel density estimation; [2] applied kernel least-squares criterion to quantify segmentation candidate and estimate change point locations. Compared to aforementioned papers, our -statistic approach starts from a pure testing point-of-view that does not rely on any tuning of bandwidth or threshold.

The rest of this paper proceeds as follows. The bootstrap calibration for the distribution of is described in Section 2. Main results for size validity and power properties of the bootstrap test are derived in Section 3. Extensions to multiple change point scenario are elaborated in Section 4. We report simulation study results in Section 5 and real data examples in Section 6. All proofs with auxiliary lemmas are given in Appendix.

1.2 Notation

For and a generic vector , we denote for the -norm of and we write . For a random variable , denote . For , let be a function defined on and be the collection of all real-valued random variables such that for some . For , define . Then, for , is an Orlicz norm and is a Banach space [41]. For , is a quasi-norm, i.e., there exists a constant such that holds for all [1]. Let be the Kolmogorov distance between two random variables and . We shall use and to denote positive and finite constants that may have different values. The symbol (or ) denotes greater than (or equal to, smaller than) some rates with constants omitted and (or ) means the maximum (or minimum) of terms.

Throughout the paper, we assume and (i.e., and ) to simplify some statements and all inference works for .

2 Bootstrap calibration

To approximate the distribution of , we propose the following bootstrap procedure. Let be i.i.d. random variables that are independent of . Define the bootstrapped -statistic and test statistic as

| (2.1) |

We reject if , where

is the quantile of the conditional distribution of given . Before presenting the rigorous validity of our bootstrap test procedure in terms of the size and power in Section 3, we shall explain the reason why it can (asymptotically) separate against .

First, suppose is true, i.e., are i.i.d. with distribution . Let and . Due to the anti-symmetry of , we have . Then the Hoeffding decomposition of is

| (2.2) |

Since is degenerate, the linear part is expected to be a leading term of , and the distribution of (denote as ) can be approximated by its Gaussian analog via matching the first and second moments [17, 13]. Since and

we expect that , where , for a large sample size . Once the Gaussian approximation result for by is established, the rest of the work is to compare the distribution of and the conditional distribution of given , both of which are mean-zero Gaussians. Since standard concentration inequalities for (one-sample) -statistics in [13] yield that . Thus we expect that , from which the size validity of the bootstrapped change point test based on follows.

Next, we suppose is true, i.e., are i.i.d. with distribution and are i.i.d. with distribution such that and . To study the power property, the main idea is to consider the two-sample Hoeffding decomposition of that is similar to (2.2). Suppose is shift-invariant in terms of location parameter. Let ,

such that . Define

which is degenerate such that . Under , we may split the -statistic sum as

where the first sum on the r.h.s. of the above equation has mean zero (again, due to the anti-symmetry of ). Thus, to study the power of (and its bootstrapped version ), it suffices to analyze the second sum on the r.h.s. of the last display above, which is a two-sample -statistic that admits the following Hoeffding decomposition:

| (2.3) |

Since the last three sums on the r.h.s. of (2.3) have mean zero, the power of the proposed test is determined by the magnitude of and the sampling distributions of other terms involving no . For the latter, all of those distributions can be well estimated and controlled as in since they do not contain the change point signal. Thus, if obeys a minimal signal size requirement, then the power of would tend to one.

Remark 1.

It is interesting to note that our bootstrapped -statistic in (2.1) is closely related to the jackknife multiplier bootstrap (JMB) proposed in [13] for high-dimensional -statistics and in [15] for infinite-dimensional -processes with symmetric kernels. In both settings, the (unobserved) Hájek projection process is estimated by the jackknife procedure and a multiplier bootstrap is applied to the jackknife estimated process. In our change point detection context, since the kernel is anti-symmetric, averaging the empirical Hájek process by jackknife would simply be an estimate of zero. Thus, we may only use half (e.g., a triangular array index subset ) of the JMB to estimate . In view of this connection, we call our bootstrap method is a JMB tailored to change point detection. ∎

3 Theoretical properties

Let be i.i.d. random vectors with distribution . Recall that and in the Hoeffding decomposition (2.2). Then and for all (i.e., is degenerate). Denote . In this section, we will characterize theoretical properties through (the dimension of ) and (the expected mean change of ) rather than (the original dimension of data) or (the original location shift parameter) since the whole procedure is constructed on top of .

3.1 Size validity

We first establish the validity of the bootstrap approximation to the distribution of under . Let be a constant and which is allowed to increase with . We make the following assumptions.

-

(A1)

for all .

-

(A2)

for all and .

-

(A3)

for all .

Condition (A1) is a non-degeneracy requirement for the kernel . Without (A1), bootstrap may approximate constant observation through a random process so that our method is not valid. Conditions (A2) and (A3) impose moment conditions on the kernel coupled with the data distribution . For instance, when the kernel is bounded, we do not explicitly impose additional assumption on the data distribution . Thus conditions (A2) and (A3) are more robust than the canonical linear kernel when the data distribution has polynomial tails. In our high-dimensional setting, we allow both and to increase with .

Theorem 3.1 (Size validity of bootstrap test under ).

Suppose is true and (A1)-(A3) hold. Let such that for some constant . Then there exists a constant depending only on and such that

| (3.1) |

holds with probability at least , where

| (3.2) |

Consequently, we have

| (3.3) |

In particular, if , then .

Theorem 3.1 constructs non-asymptotic bootstrap validity in theory and guarantees that the -th quantile of bootstrapped statistic is always close to the -th quantile of test statistic . Moreover, the error bound is uniform over . The technique for proving Theorem 3.1 extends the Gaussian approximation theory for -statistics in [13], which focuses on symmetric kernels.

Remark 2 (Comparisons with the CUSUM-based statistics).

[38] and [61] propose CUSUM-based bootstrap tests that require the removal of boundary points for detecting change points in high-dimensional mean vectors. Specifically, for the CUSUM statistics (1.5) considered in [61], the test statistic is of the form for some boundary removal parameter . Accordingly, the Gaussian multiplier bootstrap version of is defined as:

where and are the left and right sample averages at , respectively. sequentially inspects the two-sample distributions before and after all possible change point locations in the interval . Then for the special case of linear kernel and distribution satisfying the conditions (A1), (A2), and (A3), the rate of convergence for shown in [61] obeys

with probability at least . Comparing the last display with the rate of convergence for in (3.1) and (3.2), we see that the JMB method proposed here has better statistical properties than the Gaussian multiplier bootstrap without removing any boundary points in computing and . Consequently this will reduce the error-in-size (3.3) for our bootstrap calibration . Empirical evidence for our algorithm with smaller error-in-size can be found in Section 5. The main reason for the improved rate is due to the fact that we can approximate the distribution of based on the majority of the data points in the entire sample . In addition, the proposed change point detector and its JMB calibration can be viewed as a nonlinear and one-pass version of the CUSUM statistics. ∎

Remark 3 (Improved size validity of the bootstrap test).

Proof of Theorem 3.1 is based on the Gaussian and bootstrap results for linear partial sums in high dimensions [17] and the maximal inequality for degenerate -statistics [15]. Since the work of [17], there have been substantial progresses being made to improve the rate of convergence of Gaussian approximation for partial sums under various settings. For instance, [18] derived nearly optimal bound for the Gaussian approximation over hyper-rectangles. Tailored to our change point detection setting, if the correlation matrix of is strongly non-degenerate (i.e., the smallest eigenvalue of the correlation matrix of is strictly positive), then the rate of Gaussian approximation to can be sharpened to . Combining this with the maximal inequality for , we can improve the overall bound for to .

Let be the square root of the smallest eigenvalue of the correlation matrix of . We assume that

-

(A2’)

for all .

-

(A3’)

for all .

Theorem 3.2 (Improved size validity of the bootstrap test under ).

Suppose is true, , and (A1), (A2’) and (A3’) hold. Let such that for some constant . Then there exists a constant depending only on and such that

| (3.4) |

holds with probability at least , where

| (3.5) |

∎

3.2 Power analysis

Next, we analyze the power of the proposed testing under in terms of the change point signal and its location . In our -statistic framework, the test implicitly depends on through , which the signal strength characterization will relate to. As we have discussed earlier, the signal magnitudes between and can be preserved for the robust sign kernel. Under , we assume the following conditions.

-

(B1)

is shift-invariant: .

-

(B2)

for all and .

-

(B3)

for all .

Condition (B1) is a natural requirement since the within-sample noise cancellation by should be invariant under data translation in the location-shift model (1.1). Conditions (B2) and (B3) are in parallel with Condition (A2) and (A3) in the sense that they quantify the moment and tail behaviors of the centered version of the kernel (w.r.t. the distribution ). In particular, Conditions (B2) and (B3) separate the location-shift signal from the mean-zero noise, and if , Conditions (B2) and (B3) reduce to Conditions (A2) and (A3). Our next theorem characterizes the minimal signal strength for detecting the change point under the alternative hypothesis .

Theorem 3.3 (Power of bootstrap test under ).

Suppose is true and (B1)-(B3) hold in addition to (A1)-(A3). Let such that for some constant . Suppose for some large enough . If

| (3.6) |

for some constants and , then

Theorem 3.3 provides the lower bound of signal strength that is related to change point location and size level , as well as sample size and kernel dimension . Markedly, our theory derives the tail probability control on the maximum of two-sample order-two -statistics.

Remark 4 (Interpretation of Theorem 3.3).

Note the first term on the r.h.s. of (3.6) reflects the Type I error of the bootstrap test (coming from and in Theorem 3.1), while the second term reflects the connection to the Type II error under through . If the location shift happens in the middle, i.e., , then . In this case, the signal strength has to obey , which matches the power result for the bootstrap test based on the CUSUM statistics in [61] (cf. Theorem 3.3 therein). If the location shift occurs at the boundary, for instance for , then the signal has to be , which diverges to infinity. Thus, under our framework, detection is possible for local alternative when the change point location satisfies . ∎

Remark 5 (Rate optimality for sparse alternative).

In [44, Theorem 1], the authors derived the minimax rate of detection boundary for single change point case where is -dimensional Gaussian distribution with independent entries. Suppose the location shift only occurs in the first components with the same size of , i.e.

For sparse regime when , let under local alternative, then their minimax result reads as

Note that, . Hence, their result indicates that . The rate inside square root is up to a logarithm factor through (for example by plugging in ). On the other hand, our (3.6) in Theorem 3.3 requires the lower bound up to . If is bounded away from boundaries, i.e., , then our result is minimax optimal. ∎

Remark 6 (Extension of the bootstrap test to time series data).

When the noise sequence in the location-shift model (1.1) is a stationary time series, we need to modify the bootstrap test statistic to adjust for the temporal dependency because is no longer zero and there is a bias term to be calibrated in the bootstrap test. Nonetheless, if the time series is weakly dependent, then the bias term decays to zero when increases. This motivates us to consider a trimmed version of the bootstrap test by removing summands within close indices in (and thus ). Let the integer be a trimming parameter. We define a generalized -statistic as

| (3.7) |

Under , we expect behaves similarly to the i.i.d. scenario for large since the dependency between and is weak. Thus, we have for and . Under , with for and , we have

| (3.8) |

There is a natural trade-off in choosing the trimming parameter to control the effective signal strength under and . For larger values of , calibration of the distribution of would be more accurate. However, the compromise of signal strength in (6) would also be larger. Thus, it would be harder to detect change point (i.e., to separate from ) when the temporal dependence of data is stronger. Similarly as the i.i.d. noise case, we can use the -norm to construct our test statistic

| (3.9) |

which separates from when temporal dependence exists.

Let be i.i.d. random variables that are independent of . Define the bootstrapped test statistic

| (3.10) |

and . We reject if , the quantile of the conditional distribution of given .

When is an independent noise sequence, we simply set so that and reduce to and , respectively. In Section 5.6, we shall provide some empirical performance of the trimmed bootstrap test for a vector autoregressive process . ∎

4 Extensions to multiple change points scenario

4.1 Direct extension to multiple change points testing

Recall as a sequence of independent random vectors taking values in . Generally, suppose there are change points such that

Without loss of generality, we can assume . Consider the alternative hypothesis with multiple change points

| (4.1) |

Denote and due to the shift-invariant property (B1) we have

Let be the size of data segment that corresponds to the -th location shift. Then,

| (4.2) |

where the standardized signal strength is . Under the multiple change points alternative, if signal cancellation does not exist, i.e. is away from 0, then we can directly extend the theory as below.

Lemma 4.1 (Power of the bootstrap test under ).

Suppose is true and (B1)-(B3) hold in addition to (A1)-(A3). Let such that for some constant . Suppose is a constant. If

| (4.3) |

where

then for some constants and .

Remark 7 (Explanation on and connection to single change point case).

Compared to (3.6) in Theorem 3.3, there is an additional term in (4.3). It comes from controlling under the alternative hypothesis. Consider the special case of single change point where in (4.1), we may assume . Then for , i.e., is dominated by the l.h.s. of (4.3). Then our result under reads the same as (3.6). ∎

The l.h.s. of (4.3) is the overall signal strength which does not directly depend on minimum separation of change points or signal strength like or that is usually assumed under CUSUM-based approach [19, 20, 61]. Taking (1.5) for instance, our framework does not screen out any statistic by visiting each location . Therefore, we allow the product of dominates the overall change even if or is fairly small. However, it is inconvenient that signal cancellation in (4.2) cannot be characterized by or . Another drawback is that can happen even if and is large. This issue will be discussed in the next section. Before that, we discuss two special cases derived from Lemma 4.1 based on and to make the lemma more informative and instructional. Besides, we can avoid being on both sides of (4.3).

-

1.

Suppose is upper bounded, for example is the bounded sign kernel. We have , which leads to and . Since , so , which is nearly the same rate as the first part on the r.h.s. of (4.3). Therefore, can be dropped.

-

2.

Suppose are at the same magnitude and is dominated by for some pair of . Then a sufficient condition to control Type II error is to have greater than the upper bound of , namely . So we only need . This is weaker than the condition in [19, (B1)] which requires . One example of such assumption is the setup in [38] where each dimension has at most one change.

In summary, we have the following corollary.

Corollary 4.2.

In Remark 4, we have shown that local alternative is detectable when . Corollary 4.2 (ii) has a stronger requirement due to extra cost from handling the possible cancellation in analyzing the general case of multiple change points. If there is only one change point, then the interpretation of rates in Lemma 4.1 can be found in Remark 7. A real application for our global test lies in the special case of monotone signals that have order structures [45].

4.2 Modification to block testing

The direct extension of testing against depends on , which can be 0 even if each are fairly large. The global test will not help under severe signal cancellation. One solution is to localize the test such that the problem can convert to single change point scenario.

Consider performing a block testing in the following way. Divide the sample into blocks of size ( for brevity) where . Then each block contains at most 1 change point. We can apply the original test to the block-vector data , where . Let be the block version extension of :

Note that there is no signal cancellation issue. Denote . Modified theory of power will depend on signal strength as below.

Corollary 4.3.

Note that the rate now depends on rather than (except for logarithm factors). The block test sacrifices sample size to gain the single change-point structure. In practice, the block parameter (or equivalently ) needs to be selected carefully since power depends on the relevant locations of . One solution is to use that is discussed in Remark 4 or that is from Corollary 4.2 (ii).

4.3 Discussion on binary segmentation

To deal with multiple change points, binary segmentation (BS) is conceptually straightforward [19, 20, 61]. The main idea is to recursively estimate change points by screening sub-segments before and after each estimated location. However, such process starts from a “global” detection that may miss change points under unfavorable configuration of signal cancellation. To improve BS, [26] proposed wild binary segmentation (WBS) that randomly draw intervals to localize searching for change points. Recently, it has been widely adopted [57, 56] owing to its flexibility and computational efficiency. However, we will not be able to apply BS or WBS based approaches directly because there is no estimator in our framework so far.

One solution is to incorporate an external estimator. For example, consider the -statistics where is the anti-symmetric kernel used in (1.3). It can be shown that for each segment

In other word, within each segment , is monotone (). So is always attained at one change point. Therefore, the estimator

can play a role in BS type approach. Similar ideas are discussed in [49, 28, 27, 11] as applications using -statistics for estimation of change points. Though it is fascinating to investigate the consistency of a BS algorithm that combines estimation using and our bootstrapping test using , the focus and main contribution of this paper is to perform a test without visiting each point. So we leave this algorithm as an open question for future analysis.

Another solution is to adopt the randomization idea from WBS to conduct inference in the presence of multiple change points. One can independently sample intervals that are wider than a pre-specified length and obtain a set of (scaled) test statistics on each interval. Denote the set as . For a given level , we then perform the proposed bootstrap test on the interval whose corresponding (scaled) test statistic achieves the -th quantile of . If the bootstrap test rejects under level , then it implies a change point in this interval, which in turn concludes of at least one change point. The WBS-type test is summarized in Algorithm 1.

Note that the tuning parameter of bounds the length of randomly selected intervals from below. If is too small, for instance , then Step 4 is likely to end up with a very small interval . Since approximating on small intervals will not be consistent, it can lead to the failure of size control under . In practice, one may select by applying the Algorithm 1 on , where the multipliers are i.i.d. standard Gaussian random variables that are independent of . Since and , the transformed data can mimic without any structural assumption. Simulation result for Algorithm 1 is presented in Section A.5 in the Appendix.

4.4 Backward detection approach for change points estimation

As shown in aforementioned forward searching solutions, the drawbacks of BS include cancellation of signals and requirement of change point estimators. Instead of repeatedly splitting intervals after each detection of change point, we can reversely merge consecutive segments in a backward detection way [47, Section 3.2.2]. Then, our test can work as a stopping rule.

Precisely, denote the initial partition of data segments as and the corresponding data blocks as , where . For each pair of consecutive blocks , we can compute a Dissimilarity Index based on using truncated data sequence, i.e.

| (4.4) |

Since each component of is the standardized Hodges-Lehmann type estimator of location shift in each dimension, large indicates strong dissimilarity between and . Therefore, we can pick the pair of data blocks with the smallest and perform our bootstrapped test to decide whether to merge them. If the test fails to reject the null hypothesis of no change point, we merge the two blocks into one. Otherwise, we move on to test the next pair of data blocks with the second smallest . The process will continue until no blocks can be merged. The Backward Detection (BD) algorithm is summarized in Algorithm 2.

Compared to forward detection, BD is able to detect short sequence. Hence, the Backward Detection algorithm will be more powerful compared to the direct extension or the block testing at the beginning of this section. There is no signal cancellation issue for BD. Besides, it can identify change points without introducing new estimators or statistics. However, there is a risk of Type I error inflation since BD recursively performs testing procedure. Let , where is the largest integer not exceeding . Then small can cause over rejection, while large may affect estimation accuracy and bring signal cancellation issue back. We should tune the initial partition size carefully. To the best of our knowledge, there is no theoretical result on the consistency of backward detection in change point estimation. For testing purpose, we can take as discussed in Section 4.2. Empirical performance are investigated in simulation and real data application.

5 Simulation study

In this section, we first report simulation results of our method in size approximation and power performance under single change point model. Independent random vectors are generated according to the location-shift model (1.1). Comparison with other methods follows. In the end, we evaluate the global test of direct extension and the Backward Detection of estimation for multiple change points.

5.1 Simulation setup

We generate i.i.d. from the following distributions.

-

1.

Multivariate Gaussian distribution: .

-

2.

Multivariate elliptical -distribution with degree of freedom (): with the probability density function [46, Chapter 1]

The covariance matrix of is . In our simulation, we use .

-

3.

Contaminated Gaussian distribution (i.e., Gaussian mixture model): with the probability density function

The covariance matrix of is . We set and .

-

4.

Scale transformation of Cauchy distribution: , where and are i.i.d. standard (univariate) Cauchy distribution.

For each distribution, we consider three spatial dependence structures of .

-

(I)

Independent: , where is the identity matrix.

-

(II)

Strongly dependent: , where is the matrix of all ones.

-

(III)

Moderately dependent: .

Unless explicitly indicated, bootstrap samples are drawn for each testing procedure and all results are averaged on 500 simulations. We fix the sample size and dimension for single change point scenario and focus on the performance of two kernels: the linear kernel and the sign kernel .

5.2 Size approximation

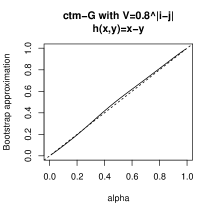

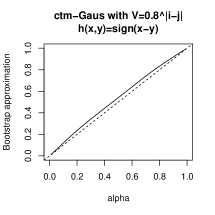

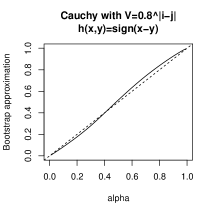

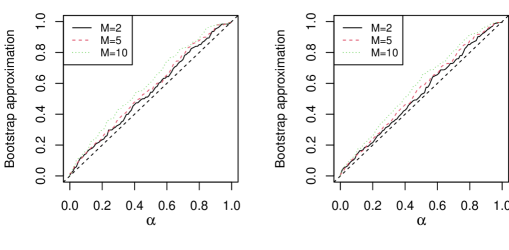

Let be the proportion of empirically rejected null hypothesis at significance level . There are several observations we can draw from Table 1, which shows the empirical uniform error-in-size, . First, the dependence structure of does not influence the errors remarkably. Second, for Gaussian, and contaminated Gaussian (ctm-G) distributions, the two kernels have very similar errors in size. For the Cauchy distribution which is only applicable for the sign kernel, error-in-size is comparable with the other three distribution settings. Therefore, we conclude that under , the sign kernel gains robustness without losing much accuracy. Three example curves are displayed additional in Figure 1 to visualize the size approximation.

| linear kernel | sign kernel | |||||||

|---|---|---|---|---|---|---|---|---|

| Gaussian | ctm-G | Gaussian | ctm-G | Cauchy | ||||

| I | 0.034 | 0.086 | 0.040 | 0.026 | 0.066 | 0.032 | 0.028 | |

| II | 0.054 | 0.020 | 0.058 | 0.064 | 0.040 | 0.050 | 0.060 | |

| III | 0.026 | 0.048 | 0.040 | 0.040 | 0.036 | 0.060 | 0.058 | |

We also compare our test using the linear kernel to the CUSUM counterpart in [61, BABS] under the same setting with the boundary removal parameter as . Table 2 displays corresponding simulation results. By comparing it to Table 1, we observe that the CUSUM approach suffers from greater size distortion as it has larger uniform errors in general. When we focus on the maximum error within the interval (that are common choices in real applications), our linear kernel based algorithm still outperforms. In addition, our test demands no more computational costs and it enjoys flexibility of no tuning parameter.

| CUSUM approach | CUSUM approach | linear kernel | |||||||

| Gaussian | ctm-G | Gaussian | ctm-G | Gaussian | ctm-G | ||||

| I | 0.072 | 0.122 | 0.096 | 0.040 | 0.036 | 0.064 | 0.012 | 0.010 | 0.020 |

| II | 0.066 | 0.044 | 0.048 | 0.026 | 0.014 | 0.024 | 0.008 | 0.014 | 0.012 |

| III | 0.074 | 0.092 | 0.066 | 0.022 | 0.038 | 0.048 | 0.020 | 0.018 | 0.012 |

5.3 Power of the bootstrap test

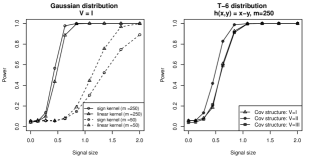

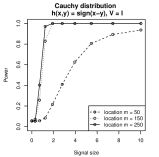

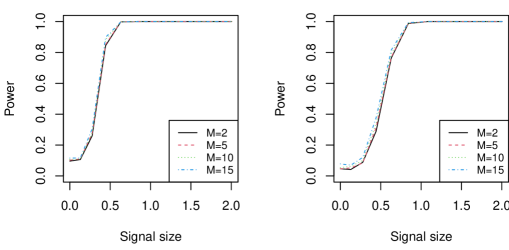

Under , the signal vector is chosen as such that . We vary the change point location . Figure 2 displays the power curves for different kernels, change point location and dependence structure . The left panel investigates kernel and location impact. Change point at center (solid curves) is easier to detect than that of at boundary (dashed curves) regardless of the choice of kernel. For standard Gaussian distribution, the linear kernel has greater power than the sign kernel when the change occurs at boundary point , but the relation reverses when . The middle panel uses linear kernel as an example to illustrate the observation that the dependence structure does not significantly influence the power, though our -type test statistic has advantage in the strong dependence case. The right panel displays the power of the sign kernel for Cauchy distributed data to highlight its robustness to location parameter and the impact from change point position . Regarding to the exact power values, see Table 11 (linear kernel) and 12 (sign kernel) in Appendix.

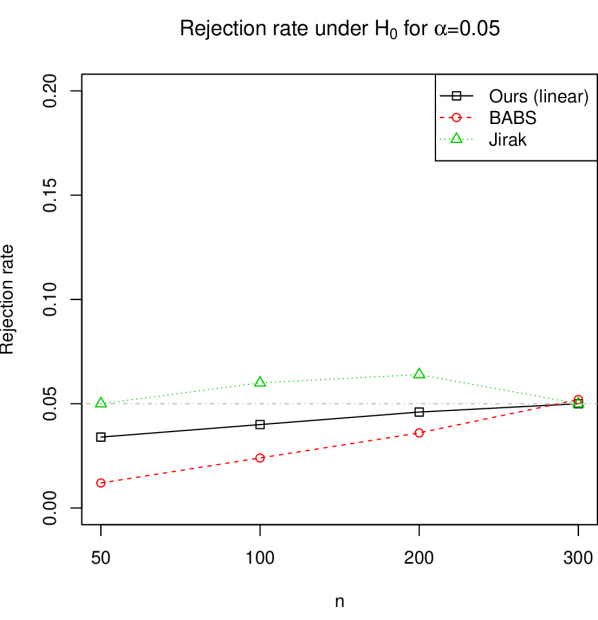

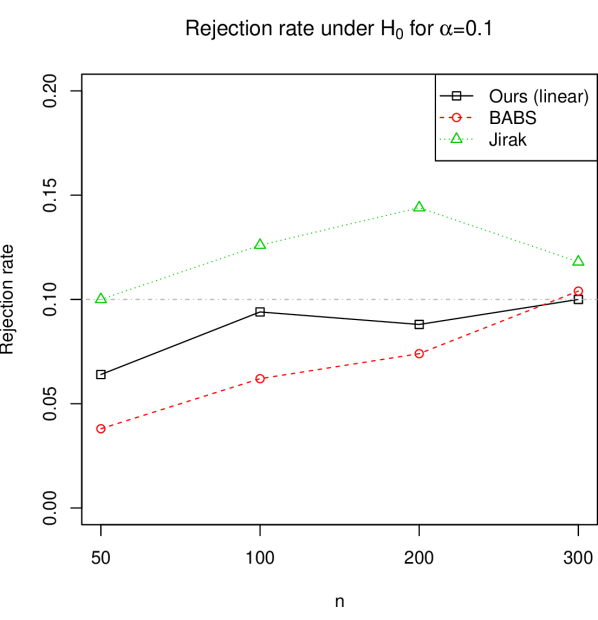

5.4 Comparison with other methods

We compare our -statistic approach to other competing algorithms in change point literature. The linear and sign kernels of our approach are used. All of the four competitors, namely [61, BABS], [38, Jirak], [20, SBS] and [57, Inspect], are based on CUSUM statistics. Among them, BABS and Jirak are -type bootstrap test for single change point using different weights on in (1.5), the latter of which needs cross-sectional variance estimation on each dimension and it is sensitive to mean shift near the center of data sequence. The last two competitors target on multiple change point estimation where SBS is thresholded -type estimator and Inspect is projection based. We adopt their single change point version function in corresponding R packages and convert them to tests using their default threshold computing functions. In our simulation, we set , and set boundary removal as 40 for BABS, Jirak and SBS.

Table 3 compares the power of different tests when the signal is growing. It is clear that SBS and Inspect are not suitable in our setting since the location shift parameter is extremely sparse. When the data generating mechanism is not standard multivariate Gaussian (i.e. not Gaussian-I in the table), these two algorithms trigger excessive false alarms when and do not return monotone powers as increase. The other two competitors BABS and Jirak behave similarly and return slightly higher powers than ours in general. Note that these two approaches need to pick boundary removal parameter, which can harm powers if it is too large to include true in the working interval. The contrasts between linear and sign kernel have been discussed in the previous part. Therefore, Table 3 indicates that our method, which enjoys tuning-free and intermediate-estimation-free properties, is competent in empirical studies.

| Gaussian-I | Gaussian-II | |||||||||||

| linear | sign | BABS | Jirak | SBS | Inspect | linear | sign | BABS | Jirak | SBS | Inspect | |

| 0 | 0.030 | 0.049 | 0.042 | 0.061 | 0.764 | 0.020 | 0.042 | 0.037 | 0.056 | 0.052 | 0.092 | 0.833 |

| 0.28 | 0.088 | 0.070 | 0.087 | 0.110 | 0.836 | 0.021 | 0.216 | 0.154 | 0.209 | 0.232 | 0.264 | 0.724 |

| 0.44 | 0.414 | 0.342 | 0.502 | 0.553 | 0.928 | 0.006 | 0.738 | 0.619 | 0.756 | 0.828 | 0.744 | 0.458 |

| 0.63 | 0.890 | 0.830 | 0.966 | 0.967 | 0.976 | 0.001 | 0.996 | 0.982 | 0.996 | 0.999 | 0.926 | 0.287 |

| 0.84 | 0.998 | 0.992 | 1 | 1 | 0.966 | 0.003 | 1 | 1 | 1 | 1 | 0.906 | 0.205 |

| 1.08 | 1 | 1 | 1 | 1 | 0.972 | 0.093 | 1 | 1 | 1 | 1 | 0.898 | 0.183 |

| 1.35 | 1 | 1 | 1 | 1 | 0.954 | 0.789 | 1 | 1 | 1 | 1 | 0.858 | 0.287 |

| 1.66 | 1 | 1 | 1 | 1 | 0.938 | 0.999 | 1 | 1 | 1 | 1 | 0.838 | 0.997 |

| 2.00 | 1 | 1 | 1 | 1 | 0.936 | 1 | 1 | 1 | 1 | 1 | 0.834 | 1 |

| ctm-Gaussian-I | -II | |||||||||||

| linear | sign | BABS | Jirak | SBS | Inspect | linear | sign | BABS | Jirak | SBS | Inspect | |

| 0 | 0.030 | 0.051 | 0.020 | 0.067 | 0.592 | 1 | 0.060 | 0.068 | 0.044 | 0.053 | 0.060 | 0.975 |

| 0.28 | 0.036 | 0.073 | 0.033 | 0.076 | 0.630 | 1 | 0.124 | 0.148 | 0.109 | 0.132 | 0.108 | 0.942 |

| 0.44 | 0.150 | 0.189 | 0.186 | 0.245 | 0.752 | 1 | 0.418 | 0.451 | 0.477 | 0.537 | 0.418 | 0.791 |

| 0.63 | 0.524 | 0.593 | 0.675 | 0.750 | 0.904 | 1 | 0.878 | 0.912 | 0.919 | 0.936 | 0.856 | 0.629 |

| 0.84 | 0.940 | 0.941 | 0.977 | 0.987 | 0.954 | 1 | 0.998 | 1 | 0.997 | 1 | 0.928 | 0.507 |

| 1.08 | 1 | 1 | 0.999 | 1 | 0.946 | 1 | 1 | 1 | 1 | 1 | 0.898 | 0.453 |

| 1.35 | 1 | 1 | 1 | 1 | 0.938 | 1 | 1 | 1 | 1 | 1 | 0.878 | 0.609 |

| 1.66 | 1 | 1 | 1 | 1 | 0.918 | 1 | 1 | 1 | 1 | 1 | 0.846 | 1 |

| 2.00 | 1 | 1 | 1 | 1 | 0.902 | 1 | 1 | 1 | 1 | 1 | 0.864 | 1 |

For fair comparison, we do not use Cauchy distribution, since all methods, except for our sign kernel method, will fail when there is no well-defined mean parameter in the heavy tailed distribution. Unreported results show that SBS and Inspect perform better when the mean change is denser. We also remark that the Double CUSUM Binary Segmentation [19, DCBS] cannot detect any change point under our setting when because the setup is an extremely sparse case, so the table does not include it.

Section A.6 in Appendix presents some further comparison for the size control of BABS, Jirak and our linear kernel approach under with fixed and boundary removal fraction while varying the sample size .

5.5 Multiple change-point detection

In the multiple change-point scenario, we first let the -th component of to have the same location shift, i.e. . Since change point estimation can be viewed as a special case of clustering, the accuracy can be measured by the adjusted Rand index (ARI) [50, 36]. We also report average ARI over all 500 runs. The bootstrap resampling is .

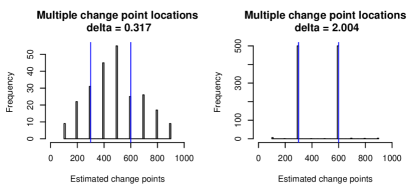

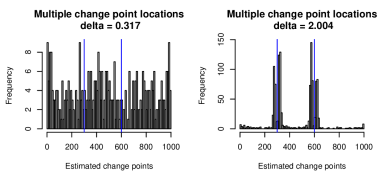

To start with, we consider the direct application of our test using Gaussian distribution and linear kernel as a representative. Let , , and the two change points . The powers are shown in Table 4. Our test works well as there is no signal cancellation.

| 0 | 0.317 | 0.733 | 1.282 | 2.004 | ||

|---|---|---|---|---|---|---|

| Spacial dependent structures | I | 0.052 | 0.278 | 1 | 1 | 1 |

| II | 0.064 | 0.510 | 1 | 1 | 1 | |

| III | 0.070 | 0.222 | 0.996 | 1 | 1 |

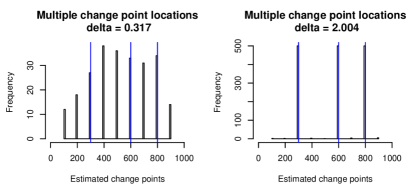

Next, we apply the Backward Detection algorithm to estimate change points. We set the initial data blocks as segments of every data points and take the Gaussian distribution with moderate dependence structure (III) for instance. The estimated change points are summarized in Table 5 (counts and ARIs) and Figure 3 (estimates). When signal is small, BD fails to reject in about half of the time (276 out of 500) and it cannot locate the shifts accurately (small ARIs). However, as signal gets larger, both the number and the locations of change points can be detected consistently (under proper setup of initial data blocks). Meanwhile, ARIs are also increasing to 1, which stands for the perfect estimation. We further add one more change where . The results in Table 5 and Figure 3 are similar to that of two change point case.

| 0 | 0.317 | 0.733 | 1.282 | 2.004 | 0 | 0.317 | 0.733 | 1.282 | 2.004 | ||

| Estimated number of change points | 0 | 497 | 276 | 0 | 0 | 0 | 494 | 270 | 0 | 0 | 0 |

| 1 | 3 | 209 | 0 | 0 | 0 | 6 | 217 | 0 | 0 | 0 | |

| 2 | 0 | 15 | 484 | 492 | 483 | 0 | 13 | 32 | 0 | 0 | |

| 3 | 0 | 0 | 16 | 7 | 17 | 0 | 0 | 455 | 474 | 483 | |

| 4 | 0 | 0 | 0 | 1 | 0 | 0 | 0 | 13 | 25 | 17 | |

| 5 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 0 | |

| Sum | 500 | 500 | 500 | 500 | 500 | 500 | 500 | 500 | 500 | 500 | |

| ARI | 0.994 | 0.195 | 0.933 | 0.998 | 0.996 | 0.988 | 0.152 | 0.920 | 0.995 | 0.997 | |

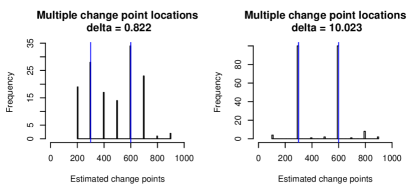

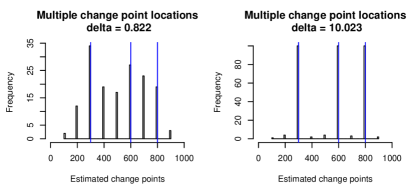

Then, we also use the sign kernel to detect location shift for Cauchy distribution with dependence structure (III). Analogously, initial data blocks are segments of every data points in sequence. The cases of 2 change points and 3 change points are implemented and the results are shown in Table 6 and Figure 4. Similar conclusion can be drawn except that stronger signal strength is required as Cauchy distribution has extremely heavy tails.

| 0 | 0.822 | 2.320 | 5.050 | 10.023 | 0 | 0.822 | 2.320 | 5.050 | 10.023 | ||

| Estimated number of change points | 0 | 465 | 44 | 0 | 0 | 0 | 460 | 36 | 0 | 0 | 0 |

| 1 | 6 | 257 | 0 | 0 | 0 | 11 | 221 | 0 | 0 | 0 | |

| 2 | 6 | 173 | 365 | 470 | 470 | 4 | 172 | 0 | 0 | 0 | |

| 3 | 6 | 9 | 18 | 12 | 10 | 3 | 50 | 401 | 470 | 477 | |

| 4 | 5 | 11 | 21 | 15 | 12 | 8 | 9 | 19 | 11 | 8 | |

| 5 | 6 | 1 | 59 | 1 | 1 | 5 | 6 | 66 | 1 | 0 | |

| 6 | 6 | 5 | 46 | 2 | 7 | 9 | 6 | 14 | 18 | 15 | |

| Sum | 500 | 500 | 500 | 500 | 500 | 500 | 500 | 500 | 500 | 500 | |

| ARI | 0.930 | 0.557 | 0.888 | 0.986 | 0.983 | 0.920 | 0.495 | 0.951 | 0.986 | 0.989 | |

Lastly, we set and repeat the experiment using linear kernel and Gaussian distribution with dependence structure (III). The results are summarized in Table 7 and Figure 5. Compared to Table 5 and Figure 4 which correspond to the same setting but , we can easily observe over rejection issue since more change points are concluded than the truth for both cases. However, when signal is large (), estimated change points still concentrate around the true ’s. In practice, a threshold can be introduced to force merging two blocks if the cardinality of their union is small.

| 0 | 0.317 | 0.733 | 1.282 | 2.004 | 0 | 0.317 | 0.733 | 1.282 | 2.004 | ||

| Estimated number of change points | 0 | 475 | 205 | 0 | 0 | 0 | 477 | 195 | 0 | 0 | 0 |

| 1 | 21 | 230 | 3 | 0 | 0 | 20 | 224 | 0 | 0 | 0 | |

| 2 | 3 | 59 | 367 | 343 | 344 | 3 | 77 | 51 | 0 | 0 | |

| 3 | 1 | 5 | 114 | 135 | 133 | 0 | 4 | 324 | 289 | 293 | |

| 4 | 0 | 1 | 16 | 22 | 23 | 0 | 0 | 111 | 167 | 172 | |

| 5 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 13 | 38 | 32 | |

| 6 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | 6 | 2 | |

| 8 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 1 | |

| Sum | 500 | 500 | 500 | 500 | 500 | 500 | 500 | 500 | 500 | 500 | |

| ARI | 0.950 | 0.186 | 0.634 | 0.785 | 0.858 | 0.954 | 0.160 | 0.582 | 0.747 | 0.834 | |

5.6 Simulation results for time series data

We shall study the empirical performance of the bootstrap test for some dependent process . In our simulation, we consider the stationary vector autoregression of order 1 (denote as VAR(1)) error process: where is a sequence of i.i.d. mean-zero random vectors in and is a coefficient matrix, where random matrix is generated with i.i.d. entries. To ensure the stationarity of process, is normalized such that .

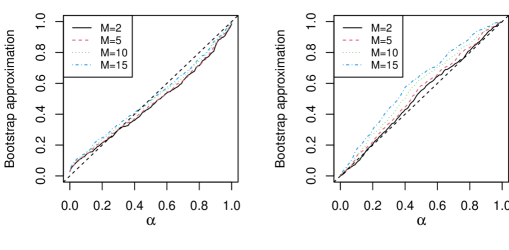

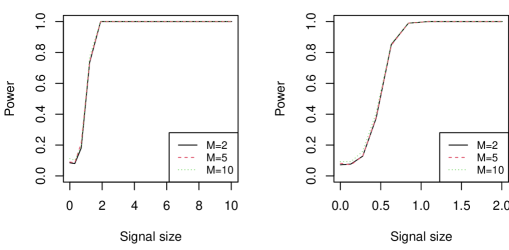

We first use the linear kernel and consider different trimming parameters . We fix and under the location-shift model of single change point. Let be the proportion of empirically rejected null hypothesis in 500 simulations. In Table 8 which provides uniform error-in-size , we can observe that larger needs to be selected if stronger dependence (i.e., the compound symmetry structure II) presents regardless of distribution families. This is the trade-off effect through . We can also find that the best error-in-sizes in each column are comparable to the corresponding values in Table 1. This indicates the effectiveness of our modified approach under temporal dependency. Figure 6 displays two examples of under and power under , where the signal vector is chosen as such that .

Next we use sign kernel and consider the trimming parameters . For illustration purpose, we only select the data-generating schemes of Cauchy distribution with Covariance I-III and ctm-Gaussian distribution with Covariance III. The other parameters remain the same as above. The uniform error-in-size for each scenario is give in Table 9. In general, works the best under each scenario. The non-linear projection by the sign kernel makes the correlation between data pairs weaker. Therefore, it makes the sign kernel more attractive in terms of its robustness against weak temporal dependency. Similarly, two examples are given in Figure 7.

| Gaussian | ctm-Gaussian | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| I | II | III | I | II | III | I | II | III | |

| M=2 | 0.058 | 0.092 | 0.030 | 0.054 | 0.082 | 0.028 | 0.038 | 0.086 | 0.054 |

| M=5 | 0.076 | 0.088 | 0.056 | 0.092 | 0.074 | 0.050 | 0.058 | 0.082 | 0.086 |

| M=10 | 0.128 | 0.064 | 0.102 | 0.134 | 0.080 | 0.080 | 0.106 | 0.084 | 0.136 |

| M=15 | 0.180 | 0.066 | 0.150 | 0.172 | 0.086 | 0.126 | 0.156 | 0.094 | 0.174 |

| Cauchy (I) | Cauchy (II) | Cauchy (III) | ctm-Gaussian (III) | |

|---|---|---|---|---|

| M=2 | 0.068 | 0.057 | 0.068 | 0.060 |

| M=5 | 0.094 | 0.062 | 0.096 | 0.088 |

| M=10 | 0.144 | 0.078 | 0.150 | 0.142 |

6 Real Data Applications

6.1 Single change point: Enron email dataset

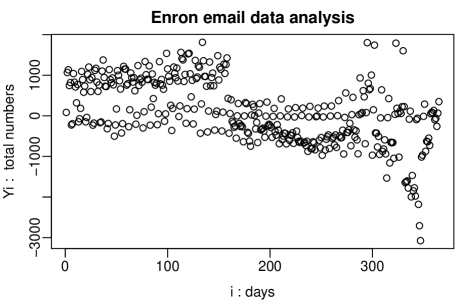

Enron Corporation used to be one of the leading American energy companies. In an accounting scandal, Enron share prices decreased from around $80 during the summer of 2000 to pennies at the end of 2001. The bankruptcy was filed on 12/02/2001 and it became the largest bankruptcy reorganization in American history at that time. The Enron email dataset that contains more than 500,000 messages from about 150 users (mostly senior management) was publicly available during the investigation by the Federal Energy Regulatory Commission in 2002 111 The raw data is organized in folders (http://www.cs.cmu.edu/~enron/) and its tabular format version is available at https://data.world/brianray/enron-email-dataset. The timeline of major events can be found at http://www.agsm.edu.au/bobm/teaching/BE/Enron/timeline.html. .

We study the collection of messages sent in 2000-2001. To test for the existence of an abrupt changes in email discussions, our analysis is based on the number of emails sent from each user. In order to exclude the yearly trend and temporal dependence, we apply our method to which is the difference of emails sent from user on the -th day for the two years. The leap day (02/29/2000) and the users who were inactive during 2000 or 2001 are removed such that the final data matrix is of dimension and . We set bootstrap repetition number . For the linear kernel, our test statistic has the value and the 95% quantile of bootstrapped statistic is 117.17. For the sign kernel, our test statistic has the value and the 95% quantile of bootstrapped statistic is 1.44. Both tests reject the null hypothesis of no abrupt change. As an illustration of the test results, the aggregated trend of in Figure 8 indicates the presence of extensive email communication from the second half of 2000 to the first half of 2001. Our test confirms that there was abnormal email activity in these two years.

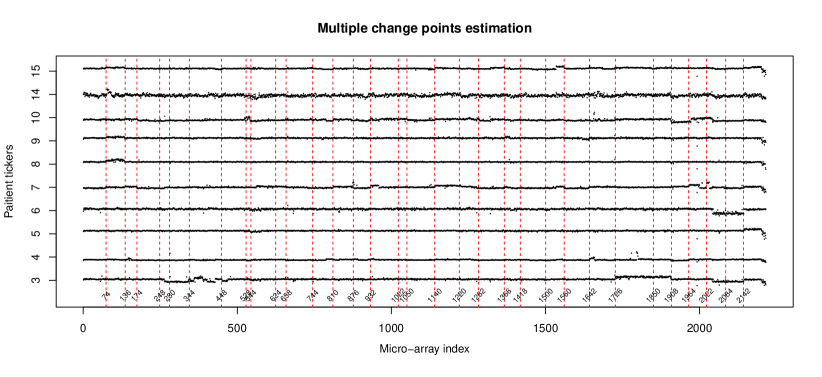

6.2 Multiple change point: Micro-array dataset

The array comparative genomic hybridization data, ACGH [37, R package ecp], consists of patients with bladder tumor. We consider to detect change points among their DNA copy number profiles each of which contains log-intensity-ratio fluorescent measurements. We apply the BD algorithm using linear kernel and set bootstrap repeats , significance level and initial data block size . The measurements for the first 10 individuals are shown in Figure 9. Our BD algorithm finds 32 change points that marked in red vertical dashed lines. This number is in a reasonable level as indicated in [57] where the authors only reported 30 most significant ones while their default Inspect algorithm found 254 change points. The ARI between ours and the bootstrap-assisted binary segmentation [61, BABS] which identifies 27 change points is 0.779. As shown in Table 10, the two methods have overlapped detection that are close loci numbers such as .

| BABS | 73, 185, 263, 342, 428, 521, 581, 657, 741, 801, 871, 960, 1051, 1141, 1216, 1276, 1367, 1427, 1503, 1563, 1664, 1724, 1836, 1905, 1965, 2044, 2143. |

| BD | 74, 136, 174, 248, 280, 344, 448, 528, 544, 624, 658, 744, 810, 876, 932, 1022, 1050, 1140, 1220, 1282, 1366, 1418, 1500, 1560, 1642, 1726, 1850, 1908, 1964, 2022, 2084, 2142. |

Appendix A Proofs and additional numeric results

A.1 Proof of main results

Throughout the whole proofs, we assume , and otherwise the rates will automatically hold. The and are large constants that may vary part by part.

Proof of Theorem 3.1.

Suppose is true. Without loss of generality, we may assume .

Step 1. Gaussian approximation to .

Denote . Since the kernel is anti-symmetric, we have . Thus and

By Jensen’s inequality, we have for , and . Then it follows

In addition, note that By Proposition 2.1 in [17] (applied to the max-hyperrectangles), we have

where and . Let . By the Gaussian comparison inequality (cf. Lemma C.5 in [14]), we have

Since , it follows from the Cauchy-Schwarz inequality that

Then by triangle inequality, we have

| (A.1) |

Applying Corollary 5.6 in [15] with , we have

| (A.2) |

Then for any and , we have

where step follows from Markov’s inequality, step from the Gaussian approximation error bound (A.1) for the linear part, step from Nazarov’s inequality (cf. Lemma A.1 in [17]), and step from the maximal inequality (A.2) for the degenerate term. Likewise, we can deduce the reverse inequality

Choosing , we get .

Proof of Theorem 3.2.

This proof is similar to the proof of Theorem 3.1 so that only the key steps are given below. Without loss of generality, we may assume .

Step 1. Gaussian approximation to . Let , then . So the correlation matrix of is the same as the correlation matrix of . By (A1), . By Jensen’s inequality, under (A2), we have for , whereas under (A3’), we have . Therefore,

where . By [18, Corollary 2.1], the Conditions (M) and (E.2) are satisfied so that

| (A.4) |

where and . Let . We still have

Hence, by triangle inequality, , where .

Note that, by choosing , the following approximation still holds

Step 2. Bootstrap approximation to . Recall . By [18, Lemma 2.1],

where

by Lemma A.1. Without loss of generality, we assume . Then, with probability greater than , . If , then

so that and therefore (3.4) holds. If , then observing that the function for any on , we have

Taking and plugging in , we still have (3.4) holds with probability greater than . ∎

Proof of Theorem 3.3.

Denote and . Define

Note that, . It follows that

| Type II error | |||

Let . Now denote

We will quantify , and to conclude that the Type II error is bounded when satisfies (3.6).

(1) Quantify . Without loss of generality, we may assume . Recall (2.3) where . Denote in similar way. By shift-invariant assumption and the two-sample projection in Section 2,

| (A.5) | |||||

By Lemma A.5, with probability smaller than ,

Similarly, with probability smaller than . By Lemma A.6,

From Markov inequality, .

Similarly, with probability smaller than .

Therefore,

with probability no smaller than .

(2) Bound . Recall , where is defined in (A.3). By the Bonferroni inequality, , where . By the Cauchy-Schwarz inequality, for each ,

which implies

By Condition [A2] and [B2], for any and . From Lemma A.2, it shows that with probability grater than ,

Therefore, . In addition, for (as ), Gaussian tail bound (Chernoff method) shows . Then, with probability greater than ,

Since and , the rate of leads to . For bounded kernel , a simpler bound of directly lead to without assuming .

(3) Bound . Note that has the same distribution as . By the approximation in Theorem 3.1 Step1, we have holds for with probability grater than . Since by [54, Lemma 2.2.2] and . Choosing for large enough , we have . Hence, . Let . Then with probability grater than ,

Combining Step (1)-(3), when ,

with probability no smaller than . That is, the Type II error is less than , where we set . As , the conclusion of Theorem 3.3 immediately follows for some large enough .

∎

Proof of Lemma 4.1.

Let

where

Similar to the proof of Theorem 3.3, we shall quantify , and to conclude that the Type II error is bounded when satisfies (4.3).

(1) Quantify .

Applying the results in Step (1) to , we have each of the following inequalities satisfied with probability greater than :

Combining all pairs of for , it follows

with probability greater than .

(2) Bound . Under , , where is defined the same as in (A.3). To control the magnitude of , note that

So we can modify Lemma A.2 from the following two cases. For the case of where are in different segments, , based on modified Lemma A.2 we have

For the case of where are in the same segments, and

Take . Then, adding all and together,

holds with probability greater than . Therefore, , where and

(3) Bound . Since does not depend on , it obeys the same bound

with probability grater than for .

Combining Step (1)-(3), when

the Type II error will be smaller than for . Substitute by , we reach the conclusion of theorem. ∎

A.2 Proof of lemmas in theorems

Lemma A.1 (Bounding under .).

Proof of Lemma A.1.

Note and let . Then

Note that, the summation in can split into two parts

In Steps 1 and 2 below, we will deal with and respectively, where . Then conclusion will be made in Step 3.

Step 1: Term . Define to be . To symmetrize , let , where

and is a permutation of . Then,

is a -statistics of order 3 and . Let

Apply Lemma E.1 in [13] to for and ,

| (A.6) |

where

and for . By Cauchy-Schwarz and Condition (A2),

So . From (i) [54, Lemma 2.2.2], (ii) the fact of and (iii) Condition (A3), we obtain

By [16, Lemma 8],

Therefore, (A.6) leads to

Recall and . Choose

for some large enough . Then,

Step 2: Term . Let be defined as . Denote . By Lemma E.1 in [13],

where

and for . Similarly,

So . In addition,

Then by [16, Lemma 8], we have . Similar to Step 1, taking for some large enough , we end up with

i.e. .

Step 3: Approximating to . By Cauchy-Schwarz inequality and Condition (A2),

Notice that

where

Combine Step 1 and 2 and take for some large enough, we have

∎

Lemma A.2 (Bounding under .).

Proof of Lemma A.2.

Note that and the summation breaks down to

Apply [13, Lemma E.1] to , calculation (similar to Lemma A.1 Step 2) shows

Take . It follows that

So for some large enough . Therefore, the diagonal part obeys the same bound such that the first term has a tail bound

Next, apply the two-sample tail bound Lemma A.4 to the middle term. Thus,

holds for , where . At last, apply [13, Lemma E.1] to for the third term, we have

Since and , it suffices to take such that

Then, the third term has a tail bound

Since there exists a large enough constant such that

we conclude . ∎

A.3 Lemma for tail probability of the maximum of two-sample -statistics

Let and be two random samples taking values in a measurable space . Suppose are independent with . Let be a measurable function and

be the two-sample -statistics. WLOG, we may first assume . Consider a permutation on and the sum of first pairs

The symmetry leads to , i.e.

This representation reduce the bounds on to those of , where . Define

By similar argument of Lemma E.1 in [13], we have the following result.

Lemma A.3 (Sub-exponential inequality for the maxima of centered two-sample -statistics).

Let and be two independent sets of iid random vectors from and , respectively. Suppose and for and all . Let , then for any and , there exists a constant such that

| (A.7) |

holds for all .

By Lemma A.3, we can have the following result.

Lemma A.4 (Tail bound of the maxima of two-sample -statistics in second order).

Let and be two independent sets of iid random vectors from and , respectively. Let , and be a constant s.t. . Suppose and for all and . Denote , where . Then,

| (A.8) |

holds for .

Proof of Lemma A.4.

Without loss of generality, we may assume . Let , and define , , and for accordingly. Apply Lemma A.3 to and follow the fact , we have

Note that and . By Lemma 2.2.2 in [54],

Since , by Lemma 8 in [16] and Jensen inequality,

Therefore,

Recall and .

(i) If , then take such that

(ii) If , then take such that

Observing . Hence,

∎

A.4 Lemma for two-sample Hoeffding decomposition

Lemma A.5 (Tail bound of the maxima of the first order projection).

Let be i.i.d. random vectors from and is independently draw from . Suppose , and for all and . Let be a constant s.t. . Define the projection . Then,

Therefore when ,

Proof of Lemma A.5.

Lemma A.6 (Maximal inequality for canonical two-sample -statistics).

Let and be two independent sets of iid random vectors from and , respectively. Let , and . Suppose and for all and . We have

Proof of Lemma A.6.

The structure of this proof is similar to the one-sample version in [13, Thm 5.1]. By constructing randomization from iid Rademacher random variables (i.e. for all and , ), [23, Thm 3.5.3] shows

Fix an . Let be a -by- matrix with zero diagonal blocks, where if and . Apply Hanson-Wright inequality [52, Thm 1] conditioning on and ,

where and . Denote and . Let

such that

Apply the tail bound of standard Gaussian random variables for , and note that , we have

Similarly,

By Jensen’s inequality and the fact , we have

| (A.9) |

Our last task is to bound . Consider Hoeffding decomposition of ,

where and for are two random vectors independent from , and all from the measurable space of and , respectively. Then,

| (A.10) |

Note that, conditioning on , Hoeffding inequality shows for

Denote . Following arguments in beginning and the symmetrization inequality [54, Lemma 2.3.1], we have

| (A.11) | |||

| (A.12) | |||

| (A.13) |

The last step of (A.11) comes from [13, Equation (58)]. The (A.12) follows the same procedure. And the first step of (A.13) is dealt the same way as (A.4) with

Since and , we know and . Besides, we have . Plug (A.11)-(A.13) in (A.10) and the solution of quadratic inequality for gives

Therefore, the square-root of is less than the square-root of each term on RHS. Plug the result in A.4. A simplified result is obtained in the statement of Lemma A.6. ∎

A.5 Additional simulation and tables

| Gaussian | ctm-Gaussian | ||||||||

| I | II | III | I | II | III | I | II | III | |

| 0 | 0.042 | 0.050 | 0.032 | 0.058 | 0.060 | 0.040 | 0.052 | 0.050 | 0.048 |

| 0.28 | 0.100 | 0.178 | 0.082 | 0.082 | 0.134 | 0.072 | 0.066 | 0.102 | 0.070 |

| 0.44 | 0.436 | 0.628 | 0.390 | 0.186 | 0.420 | 0.212 | 0.154 | 0.356 | 0.200 |

| 0.63 | 0.886 | 0.970 | 0.896 | 0.610 | 0.828 | 0.590 | 0.554 | 0.810 | 0.578 |

| 0.84 | 0.996 | 1 | 0.996 | 0.926 | 0.988 | 0.912 | 0.918 | 0.990 | 0.910 |

| 0 | 0.030 | 0.042 | 0.066 | 0.038 | 0.060 | 0.026 | 0.030 | 0.072 | 0.060 |

| 0.28 | 0.088 | 0.216 | 0.108 | 0.068 | 0.124 | 0.036 | 0.036 | 0.156 | 0.082 |

| 0.44 | 0.414 | 0.738 | 0.384 | 0.222 | 0.418 | 0.178 | 0.150 | 0.440 | 0.200 |

| 0.63 | 0.890 | 0.996 | 0.908 | 0.594 | 0.878 | 0.634 | 0.524 | 0.846 | 0.570 |

| 0.84 | 0.998 | 1 | 0.998 | 0.930 | 0.998 | 0.960 | 0.940 | 0.996 | 0.940 |

| 0 | 0.054 | 0.060 | 0.050 | 0.064 | 0.058 | 0.060 | 0.054 | 0.054 | 0.064 |

| 0.63 | 0.082 | 0.210 | 0.086 | 0.078 | 0.126 | 0.082 | 0.058 | 0.118 | 0.086 |

| 0.84 | 0.190 | 0.472 | 0.224 | 0.144 | 0.278 | 0.120 | 0.116 | 0.240 | 0.120 |

| 1.08 | 0.446 | 0.768 | 0.446 | 0.268 | 0.492 | 0.252 | 0.208 | 0.470 | 0.230 |

| 1.35 | 0.756 | 0.966 | 0.770 | 0.486 | 0.762 | 0.516 | 0.444 | 0.760 | 0.462 |

| 2.00 | 0.998 | 1.000 | 0.998 | 0.954 | 0.996 | 0.960 | 0.962 | 0.994 | 0.956 |

| Gaussian | ctm-Gaussian | Cauchy | |||||||||||

| I | II | III | I | II | III | I | II | III | I | II | III | ||

| 0 | 0.056 | 0.043 | 0.048 | 0.066 | 0.062 | 0.066 | 0.067 | 0.032 | 0.055 | 0 | 0.054 | 0.062 | 0.039 |

| 0.28 | 0.136 | 0.289 | 0.147 | 0.110 | 0.229 | 0.099 | 0.105 | 0.204 | 0.083 | 0.71 | 0.403 | 0.651 | 0.432 |

| 0.44 | 0.566 | 0.870 | 0.624 | 0.452 | 0.738 | 0.479 | 0.364 | 0.674 | 0.397 | 1.23 | 0.971 | 1 | 0.981 |

| 0.63 | 0.977 | 1 | 0.971 | 0.915 | 0.996 | 0.913 | 0.854 | 0.980 | 0.872 | 1.91 | 1 | 1 | 1 |

| 0.84 | 1 | 1 | 1 | 0.998 | 1 | 1 | 0.988 | 1 | 0.998 | 2.79 | 1 | 1 | 1 |

| 0 | 0.049 | 0.037 | 0.047 | 0.039 | 0.068 | 0.056 | 0.051 | 0.049 | 0.055 | 0 | 0.055 | 0.035 | 0.065 |

| 0.28 | 0.070 | 0.154 | 0.068 | 0.058 | 0.148 | 0.078 | 0.073 | 0.104 | 0.083 | 0.71 | 0.257 | 0.386 | 0.280 |

| 0.44 | 0.342 | 0.619 | 0.342 | 0.218 | 0.451 | 0.230 | 0.189 | 0.427 | 0.240 | 1.23 | 0.829 | 0.969 | 0.876 |

| 0.63 | 0.830 | 0.982 | 0.848 | 0.663 | 0.912 | 0.706 | 0.593 | 0.872 | 0.628 | 1.91 | 1 | 1 | 1 |

| 0.84 | 0.992 | 1 | 0.996 | 0.975 | 1 | 0.973 | 0.941 | 0.994 | 0.945 | 2.79 | 1 | 1 | 1 |

| 0 | 0.042 | 0.046 | 0.065 | 0.053 | 0.046 | 0.046 | 0.050 | 0.048 | 0.050 | 0 | 0.057 | 0.059 | 0.080 |

| 0.63 | 0.078 | 0.139 | 0.082 | 0.063 | 0.107 | 0.078 | 0.060 | 0.110 | 0.075 | 1.91 | 0.216 | 0.394 | 0.243 |

| 0.84 | 0.147 | 0.309 | 0.155 | 0.097 | 0.231 | 0.132 | 0.104 | 0.218 | 0.110 | 2.79 | 0.410 | 0.680 | 0.433 |

| 1.08 | 0.305 | 0.580 | 0.336 | 0.214 | 0.458 | 0.248 | 0.183 | 0.423 | 0.222 | 3.95 | 0.627 | 0.873 | 0.647 |

| 1.35 | 0.523 | 0.796 | 0.588 | 0.405 | 0.706 | 0.439 | 0.367 | 0.660 | 0.351 | 5.47 | 0.806 | 0.931 | 0.806 |

| 2.00 | 0.891 | 0.992 | 0.931 | 0.794 | 0.964 | 0.834 | 0.815 | 0.950 | 0.828 | 10.02 | 0.937 | 0.980 | 0.933 |

In this section, we test the performance of the WBS-type procedure (Algorithm 1). Let and data be i.i.d. Gaussian distributed with covariance structure III. The two change points are and only the -th component of the -th change point has signal . The powers along for each are shown in the rows of Table 13. We find that when , the power is close to the nominal levels, respectively. Besides, the power grows as increases.

| Power | |||||

|---|---|---|---|---|---|

| 0 | 0.317 | 0.733 | 1.282 | 2.004 | |

| 0.012 | 0.046 | 0.806 | 0.900 | 0.908 | |

| 0.032 | 0.100 | 0.818 | 0.898 | 0.926 | |

| 0.088 | 0.198 | 0.882 | 0.926 | 0.938 | |

A.6 Additional comparisons with BABS and Jirak

We further compare the size control of [61, BABS], [38, Jirak] and our linear kernel approach under . As suggested, we fix and vary from 50 to 300. The bootstrap repeat is , are i.i.d. Gaussian with dependence structure III, and each simulation repeats 500 times. The boundary removal parameters in BABS and Jirak are both .

From Figure 10(a), we can find that all three methods have a decreasing trend when grows, but our -statistic approach has the lowest uniform error-in-size under each choice of . This confirms that our -statistic test performs better than the others for small . From Figure 10(b) where empirical rejection rates at are provided, we may observe that the difference among three methods diminishes for . However, our approach is closer to the corresponding nominal significance level except for . Therefore, the simulation indicates that the no-boundary-removal property in our proposed test is beneficial to size control under small sample size.

[Acknowledgments] Research partially supported by NSF DMS-1404891, NSF CAREER Award DMS-1752614, and University of Illinois at Urbana-Champaign (UIUC) Research Board Awards (RB17092, RB18099). This work is completed in part with the high-performance computing resource provided by the Illinois Campus Cluster Program at UIUC. The authors are grateful to the editor, associate editor, and referee for their insightful comments.

References

- [1] {barticle}[author] \bauthor\bsnmAdamczak, \bfnmRadosław\binitsR. (\byear2008). \btitleA tail inequality for suprema of unbounded empirical processes with applications to Markov chains. \bjournalElectronic Journal of Probability \bvolume13 \bpages1000-1034. \endbibitem

- [2] {barticle}[author] \bauthor\bsnmArlot, \bfnmSylvain\binitsS., \bauthor\bsnmCelisse, \bfnmAlain\binitsA. and \bauthor\bsnmHarchaoui, \bfnmZaid\binitsZ. (\byear2019). \btitleA kernel multiple change-point algorithm via model selection. \bjournalJournal of Machine Learning Research \bvolume20 \bpages1–56. \endbibitem

- [3] {barticle}[author] \bauthor\bsnmAston, \bfnmJohn AD\binitsJ. A. and \bauthor\bsnmKirch, \bfnmClaudia\binitsC. (\byear2012). \btitleDetecting and estimating changes in dependent functional data. \bjournalJournal of Multivariate Analysis \bvolume109 \bpages204–220. \endbibitem

- [4] {barticle}[author] \bauthor\bsnmAston, \bfnmJohn AD\binitsJ. A., \bauthor\bsnmKirch, \bfnmClaudia\binitsC. \betalet al. (\byear2012). \btitleEvaluating stationarity via change-point alternatives with applications to fMRI data. \bjournalThe Annals of Applied Statistics \bvolume6 \bpages1906–1948. \endbibitem

- [5] {barticle}[author] \bauthor\bsnmAston, \bfnmJohn AD\binitsJ. A., \bauthor\bsnmKirch, \bfnmClaudia\binitsC. \betalet al. (\byear2018). \btitleHigh dimensional efficiency with applications to change point tests. \bjournalElectronic Journal of Statistics \bvolume12 \bpages1901–1947. \endbibitem

- [6] {barticle}[author] \bauthor\bsnmAue, \bfnmAlexander\binitsA., \bauthor\bsnmGabrys, \bfnmRobertas\binitsR., \bauthor\bsnmHorváth, \bfnmLajos\binitsL. and \bauthor\bsnmKokoszka, \bfnmPiotr\binitsP. (\byear2009). \btitleEstimation of a change-point in the mean function of functional data. \bjournalJournal of Multivariate Analysis \bvolume100 \bpages2254–2269. \endbibitem

- [7] {barticle}[author] \bauthor\bsnmAue, \bfnmAlexander\binitsA., \bauthor\bsnmHörmann, \bfnmSiegfried\binitsS., \bauthor\bsnmHorváth, \bfnmLajos\binitsL., \bauthor\bsnmReimherr, \bfnmMatthew\binitsM. \betalet al. (\byear2009). \btitleBreak detection in the covariance structure of multivariate time series models. \bjournalThe Annals of Statistics \bvolume37 \bpages4046–4087. \endbibitem

- [8] {barticle}[author] \bauthor\bsnmBai, \bfnmJushan\binitsJ. (\byear2010). \btitleCommon breaks in means and variances for panel data. \bjournalJournal of Econometrics \bvolume157 \bpages78–92. \endbibitem

- [9] {barticle}[author] \bauthor\bsnmBarigozzi, \bfnmMatteo\binitsM., \bauthor\bsnmCho, \bfnmHaeran\binitsH. and \bauthor\bsnmFryzlewicz, \bfnmPiotr\binitsP. (\byear2018). \btitleSimultaneous multiple change-point and factor analysis for high-dimensional time series. \bjournalJournal of Econometrics \bvolume206 \bpages187-225. \endbibitem

- [10] {barticle}[author] \bauthor\bsnmBhattacharjee, \bfnmMonika\binitsM., \bauthor\bsnmBanerjee, \bfnmMoulinath\binitsM. and \bauthor\bsnmMichailidis, \bfnmGeorge\binitsG. (\byear2019). \btitleChange Point Estimation in Panel Data with Temporal and Cross-sectional Dependence. \bjournalarXiv preprint arXiv:1904.11101. \endbibitem

- [11] {barticle}[author] \bauthor\bsnmBrault, \bfnmVincent\binitsV., \bauthor\bsnmOuadah, \bfnmSarah\binitsS., \bauthor\bsnmSansonnet, \bfnmLaure\binitsL. and \bauthor\bsnmLévy-Leduc, \bfnmCéline\binitsC. (\byear2018). \btitleNonparametric multiple change-point estimation for analyzing large Hi-C data matrices. \bjournalJournal of Multivariate Analysis \bvolume165 \bpages143–165. \endbibitem

- [12] {barticle}[author] \bauthor\bsnmChen, \bfnmLikai\binitsL., \bauthor\bsnmWang, \bfnmWeining\binitsW. and \bauthor\bsnmWu, \bfnmWeibiao\binitsW. (\byear2019). \btitleInference of Break-Points in High-Dimensional Time Series. \bjournalAvailable at SSRN 3378221. \endbibitem

- [13] {barticle}[author] \bauthor\bsnmChen, \bfnmXiaohui\binitsX. (\byear2018). \btitleGaussian and bootstrap approximations for high-dimensional U-statistics and their applications. \bjournalThe Annals of Statistics \bvolume46 \bpages642–678. \endbibitem

- [14] {barticle}[author] \bauthor\bsnmChen, \bfnmXiaohui\binitsX. and \bauthor\bsnmKato, \bfnmKengo\binitsK. (\byear2019). \btitleRandomized incomplete -statistics in high dimensions. \bjournalThe Annals of Statistics \bvolume47 \bpages3127-3156. \endbibitem

- [15] {barticle}[author] \bauthor\bsnmChen, \bfnmXiaohui\binitsX. and \bauthor\bsnmKato, \bfnmKengo\binitsK. (\byear2020). \btitleJackknife multiplier bootstrap: finite sample approximations to the -process supremum with applications. \bjournalProbability Theory and Related Fields \bvolume176 \bpages1097-1163. \endbibitem

- [16] {barticle}[author] \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmChetverikov, \bfnmDenis\binitsD. and \bauthor\bsnmKato, \bfnmKengo\binitsK. (\byear2015). \btitleComparison and anti-concentration bounds for maxima of Gaussian random vectors. \bjournalProbab. Theory Related Fields \bvolume162 \bpages47-70. \endbibitem

- [17] {barticle}[author] \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmChetverikov, \bfnmDenis\binitsD. and \bauthor\bsnmKato, \bfnmKengo\binitsK. (\byear2017). \btitleCentral limit theorems and bootstrap in high dimensions. \bjournalAnnals of Probability \bvolume45 \bpages2309-2352. \endbibitem

- [18] {barticle}[author] \bauthor\bsnmChernozhukov, \bfnmVictor\binitsV., \bauthor\bsnmChetverikov, \bfnmDenis\binitsD. and \bauthor\bsnmKoike, \bfnmYuta\binitsY. (\byear2020). \btitleNearly optimal central limit theorem and bootstrap approximations in high dimensions. \bjournalarXiv:2012.09513. \endbibitem

- [19] {barticle}[author] \bauthor\bsnmCho, \bfnmHaeran\binitsH. (\byear2016). \btitleChange-point detection in panel data via double CUSUM statistic. \bjournalElectronic Journal of Statistics \bvolume10 \bpages2000-2038. \endbibitem

- [20] {barticle}[author] \bauthor\bsnmCho, \bfnmHaeran\binitsH. and \bauthor\bsnmFryzlewicz, \bfnmPiotr\binitsP. (\byear2015). \btitleMultiple-change-point detection for high dimensional time series via sparsified binary segmentation. \bjournalJournal of the Royal Statistical Society: Series B \bvolume77 \bpages475-507. \endbibitem

- [21] {bbook}[author] \bauthor\bsnmCsörgő, \bfnmM.\binitsM. and \bauthor\bsnmHorváth, \bfnmL\binitsL. (\byear1997). \btitleLimit Theorems in Change-Point Analysis. \bpublisherNew York: Wiley. \endbibitem