Bivariate change point detection:

joint detection of changes in expectation and variance

Abstract

A method for change point detection is proposed. We consider a univariate sequence of independent random variables with piecewise constant expectation and variance, apart from which the distribution may vary periodically. We aim to detect change points in both expectation and variance.

For that, we propose a statistical test for the null hypothesis of no change points and an algorithm for change point detection. Both are based on a bivariate moving sum approach that jointly evaluates the mean and the empirical variance. The joint consideration helps improve inference as compared to separate univariate approaches. We infer on the strength and the type of changes with confidence. Nonparametric methodology supports the analysis of diverse data. Additionally, a multi-scale approach addresses complex patterns in change points and effects. We demonstrate the performance through theoretical results and simulation studies. A companion R-package jcp (available on CRAN) is discussed.

Keywords: bivariate, change point detection, jcp, moving sum, multi-scale

1 Introduction

The paper contributes to the field of change point detection which provides methods for the detection of structural breaks – change points – in stochastic sequences. Change point detection finds application in many areas of research, e.g., oceanographic sciences (Killick et al., , 2010), neuroimaging (Aston and Kirch, , 2012), telecommunication (Zhang et al., , 2009), DNA sequencing (Braun et al., , 2000), econometrics (Zeileis et al., , 2010), to name a few. Change point problems are studied extensively, thus, many aspects of statistical methodology are addressed, e.g., hypothesis testing, change point estimation, model complexity, computational feasibility, data structures, practical performance, etc., see for example the textbooks Basseville and Nikiforov, (1993); Csörgő and Horváth, (1997); Brodsky and Darkhovsky, (1993); Chen and Gupta, (2000); Brodsky, (2017) or the review articles Aue and Horváth, (2013); Jandhyala et al., (2013).

We study independent univariate random variables (RVs) that have piecewise constant expectation () and variance (). The goal is to detect changes in both and . Apart from constant first and second moments within each section, the distribution is allowed to vary periodically, allowing for variability in higher moments. This periodicity can improve the mimicking of real data as compared to i.i.d. RVs, the latter of which are contained as a special case. We provide a nonparametric method for the detection of change points which may occur on multiple time scales. There is vast literature on all aspects mentioned. Regarding independence, we mention Csörgő and Horváth, (1988); Gombay and Horváth, (2002); Horváth and Hušková, (2005) (-statistics), Horváth and Shao, (2007); Holmes et al., (2013) (empirical processes), and Siegmund, (1988); Frick et al., (2014); Fang et al., (2020) (likelihood ratios), the last two tackling multiple change points. For the detection of changes in we mention the nonparametric methods of Wolfe and Schechtman, (1984); Horváth et al., (2008); Jarušková, (2010); or Dehling et al., (2013), and in particular regarding change points on multiple time scales we refer to Spokoiny, (2009); Fryzlewicz, (2014); Matteson and James, (2014). For the detection of changes in we mention the articles of Hsu, (1977); Inclán and Tiao, (1994); Chen and Gupta, (1997); Whitcher et al., (2000); Killick et al., (2013); Korkas and Fryzlewicz, (2017) and a paper for changes in scale by Gerstenberger et al., (2020). Combining both, changes in and , we refer to Pein et al., (2017) who aim at detecting changes in by allowing to change simultaneously. Vice versa, Gao et al., (2019) or Dette et al., (2015) study changes in allowing to vary smoothly. Further, we note that Górecki et al., (2018) and Messer et al., (2014) aim at detecting changes in (first moment) while a certain degree of heteroscedasticity, i.e., variability in the second moment, is allowed. In this work, the latter is extended in the sense that we detect changes in both and , while we also allow for variability in higher moments.

We propose a bivariate method to jointly quantify change in and . For that we consider two moving sum processes (MOSUM): data are pointwise restricted to adjacent windows from which first the means and second the empirical variances are compared. The first statistic is sensitive to changes in and the second to changes in . See Figure 1 for an example of the two univariate processes (B,C) and their joint consideration (D), details are explained later. Regarding univariate MOSUM we mention Steinebach and Eastwood, (1995); Antoch and Hušková, (1999); Hušková and Slabý, (2001) and Eichinger and Kirch, (2018). Importantly, the bivariate approach presented here helps overcome flawed inference as compared to separate univariate approaches. Also, it enables a straightforward interpretation of the types of changes (, or both), as well as their strengths (effect sizes), while also controlling the error (confidence) of such statements. Methodologically, we construct first a test for the null hypothesis of an absence of change points. Second, we propose an algorithm for change point detection which is run if the null hypothesis is rejected.

We mention three benefits: first, the proposed theory is highly nonparametric which enables wide-ranging applicability. Strong performance is shown under different distributional assumptions, including normal-, exponential- or gamma-distributed data. Second, multi-scale aspects are captured, meaning that the occurrence of fast as well as slow change points with different strengths of effects are tackled. Third, the method is ready to use. Theory is proven with all unknown quantities replaced by appropriate estimators. A companion R-package jcp (joint change point detection, Messer, (2020)) is provided whose graphical output facilitates interpretation.

The paper is organized as follows: in Section 2 we present basic concepts. In Section 3 we introduce the model, and in Section 4 we define the MOSUM statistics. We construct the test in Section 5 and discuss change point detection in Section 6. In Section 7 we give additional theory. In Section 8 practical aspects are considered: methodology is extended, the R-package jcp is discussed, simulation studies are performed, and a real data example is shown. Proofs and auxiliary results are given in the Appendix.

2 The idea of testing and change point detection

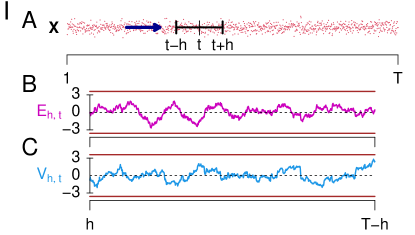

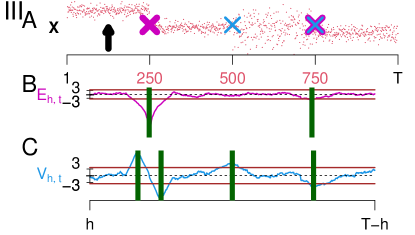

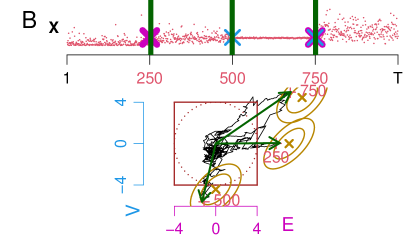

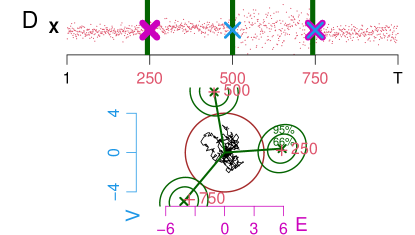

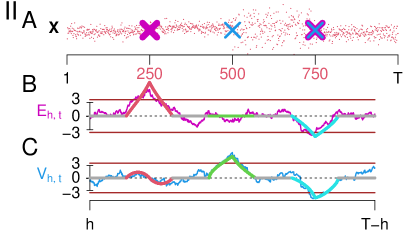

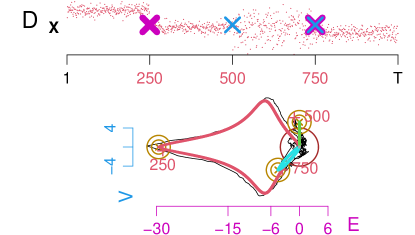

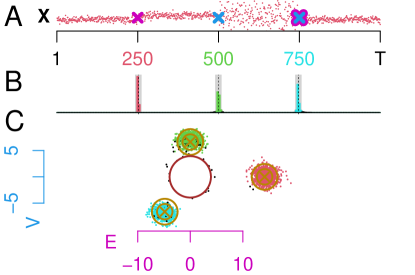

We show how MOSUM processes are used for testing and change point detection. Particularly, we motivate the bivariate aspect. For that, consider the three processes in Figure 1, differentiated in panels I, II, and III.

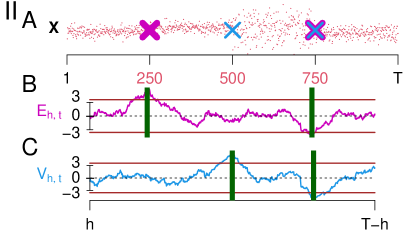

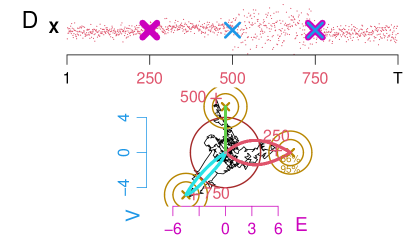

We consider independent RVs that are piecewise distributed, see red points in segments A and top D (coinciding). In panel I, there are no change points, . In panels II and III there are three change points . In both II and III the types of changes coincide: a change in at (purple cross), an increase in at (blue cross), and a decrease in both and at (purple and blue cross). II and III only differ at : there is a small increase in in II and a prominent decrease in in III.

MOSUM processes are shown in segments B, C, and D. Two adjacent windows of size (see panel IA) are shifted through time and statistics are evaluated locally from the RVs in the windows. The first statistics (B, magenta) is Student’s unpooled -statistic, i.e., Welch’s statistic, which compares the empirical means, see (5). It is sensitive to changes in . The second statistic (C, blue) similarly compares the emprical variances and is thus sensitive to changes in . In segment D we see a bivariate process (black) given by the joint statistic , where denotes transposing. If the windows do not overlap a change point, then the two estimates from the left and right window typically resemble each other, resulting in a statistic close to zero. A strong deviation from zero indicates a change. We see brown rejection boundaries (B, C horizontal lines at , D circle with radius . The boundaries coincide between the panels but appear different due to the scaling of axes). The idea is that the processes entirely lie within the boundaries with a predefined probability of , here , in case null hypothesis holds true, see panel I and Section 5 for details. If the boundaries are crossed at some point (II and III in B,C and D), the null hypothesis is rejected. After rejection, the set is estimated (green bars) via successive estimation: find the largest deviation form zero, take the argument as a change point estimate, delete the process in the -neighborhood of the estimate and repeat until the remaining process lies within the boundaries (also see Figure 4). In Figure 1 panel II inference is reasonable as in B the two changes in , in segment C the two changes in , and in D all three change points were detected. In III expectation change detection succeeds in B, but unfortunately variance inference in segment C fails as two changes in are falsely estimated. This is caused by the prominent change in . For an intuition, recall that the empirical variance is the mean squared deviation from the mean. Thus, when changes, this impacts the mean and thus the variance. This problem also appears in panel II, but it is practically negligible as the change in is small. Vice versa, changes in practically do not impact expectation change detection, intuitively, because the mean is the first moment and not affected if only the second moment changes. Statements about robustness are subject of Section 7. One way to tackle false -inference is to incorporate information about : if the empirical variances are centered correctly then -estimation will not systematically react falsely to changes in . In the context of stochastic point processes this was studied in Albert et al., (2017). A second way of treating this problem is presented in this paper: the joint observation of both processes. In panel IIID the bivariate MOSUM overcomes the problem and successfully detected three change points.

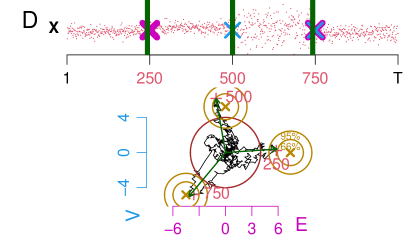

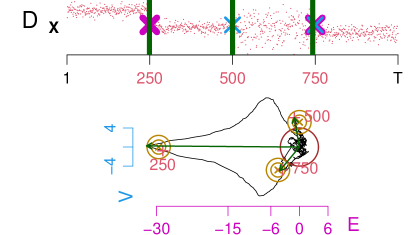

The golden dartboards in segment D show the asymptotic distribution of at a true change point . This distribution is bivariate normal, the golden cross marks the expectation and the circles the - and -contour lines, see Proposition 6.2. When the sliding windows run into , then starts an excursion approaching the center of the dartboard. The red crosses () mark i.e., they can be considered a realization from a dartboard. When the sliding windows trespass , the process returns to zero fluctuation. Glimpse at Figure 5 for the systematics of the excursions. The type and the strength of the change affect the systematic aspect of the excursion: if there is a change only in , the process tends to leave the circle in horizontal direction, to the right if there is an increase in and to the left in case of a decrease. Indeed, at time the dartboard is shifted only along the abscissa. In panel II it is found at the right side as there is an increase in , and in III it is shifted left due to the decrease in . Further, in panel III it lies far out as the change in is strong. If there is a change only in , the process systematically moves along the ordinate, upwards in case of an increase and downwards in case of decrease. At the dartboard is shifted only along the ordinate. In case of a change in both and , the process leaves the circle in both horizontal and vertical direction. Indeed, at the dartboard lies south-west due to the decline in both and . Vice versa, the location of a dartboard facilitates change point interpretation, see Section 6.

3 The Model

Auxiliary processes

Consider a single probability space throughout.

Definition 3.1.

A sequence of independent RVs of is called an auxiliary process, if there exists a such that for all it holds that for all , and also that

| and | (1) |

The distribution varies with period while the first two moments are constant. This includes i.i.d. sequences. Higher moments may vary periodically. Thus, for we abbreviate the -th moment and centered moment via and . We set averaged moments within a period

| and | (2) |

For , (1) implies constants , , and . Further set and the average

| and also set | (3) |

Note that implies and thus . Further note . It is as is not linear in . Call the averages , , , , and in (1), (2) and (3) the population parameters.

Condition (1) is sufficient for moment estimators to appropriately estimate all population parameters – the periodicity is averaged out over large samples.

For let denote the -variate normal distribution with expectation and covariance matrix .

For the mean and the empirical variance we jointly obtain as

| (4) |

while denotes convergence in distribution, see Proposition 6.2. is regular as .

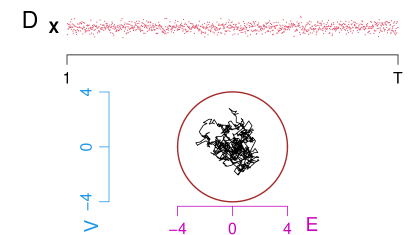

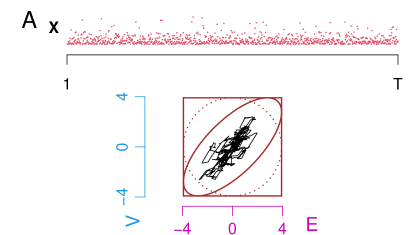

We give an example: let be a mix of uniform RVs with density for and . Then and , and has positive skewness as . Further, let have density , i.e., results from by mirroring at . Thus, also and , but skewness switches the sign. Consider independent copies of and . Set even. Repeatedly let copies of follow of . This is an auxiliary process with period , see Figure 2 .

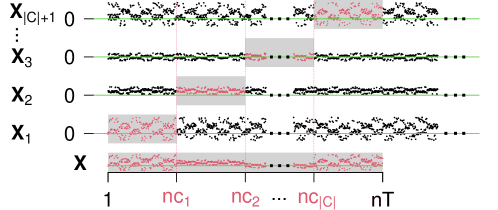

The Model

A piecewise combination of auxiliary processes constitutes a process with change points: we fix and consider a subset of cardinality with ordered elements . Call the -th change point and the set of change points. Given , we consider independent auxiliary processes , with and population parameters indexed by , e.g., and , for . We assume , for , i.e., at any either the expectation or the variance (or both) change, while other parameters may change too. For asymptotics we let and depend on a factor , i.e., we switch to and . For we define a compound process

i.e., after we enter with . Given , the set of such processes constitutes the model. For asymptotics we let and treat , as well as all population parameters including the periods, as fixed, i.e., not depending on , but unknown. By increasing , the time we remain in each increases linearly, constituting a triangular setup. We call the real time scenario, see Figure 2.

For we want to test . In case of rejection we aim at estimating . If we omit indices , , etc.

4 The moving sum processes

For we study moving sum processes in which we locally evaluate the RVs restricted to a left window and an adjacent right window . A comparison of means is sensitive to changes in the expectation and a comparison of empirical variances is sensitive to changes in the variance.

Definition of and via local parameter estimators

Let be a window size independent of , while denotes the floor function, and let . For set

| (5) |

We define the estimators in (5). The subscripts and indicate local evaluation, while and are the indices associated with the windows. We strengthen the dependence on , and , which is inherited to the estimators below, but omitted for simplicity. For and we define estimators for the moments in (2) and (3) via

| (6) |

and further , and .

We study statistics in function space. For an interval let and denote the spaces of -valued càdlàg-functions on equipped with Skorokhod topology or the supremum norm . Convergence w.r.t. implies convergence regarding . Analogously, for consider . For the estimators in (6) and thus and constitute processes in . Omitting the superscript abbreviates , e.g., . See Figure 1 for (B, magenta) and (C, blue) evaluated from (A, red). If then the estimators are functionally strongly consistent for their population parameters:

Lemma 4.1.

Let with . For it holds in as almost surely that and , for .

Consequently, and as almost surely (a.s.).

The joint process

We consider the joint process via in , see Figure 1D. Weak convergence to a bivariate Gaussian process is shown under , see Proposition 4.2 below. From this the test is constructed in Section 5. Further, convergences are extended to in Propositions 6.2 and 7.1, supporting change point detection in Section 6.

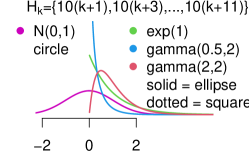

In the remainder of this section let . In general, the components of are correlated as both rely on X: in Figure 3A primarily varies along the diagonal . Symmetry of the RVs (see (3)) is necessary and sufficient for the components to be asymptotically independent. Vice versa, skewness results in correlated components. We abusively speak about symmetry and skewness, meaning the average to be or .

Skewness is captured in the correlation matrix

| (7) |

is regular as . The eigenvalue decomposition (7) yields and . Unit diagonals of imply that the columns of span the diagonals and in . Symmetry means , with identity . For an example of a skewed distribution consider with shape and rate , see also Figure 3A. We obtain , and , and depending only on .

Proposition 4.2.

Let with . In it holds as that .

The bivariate limit process is given via

| (8) |

while denotes a planar Brownian motion. The double windows are preserved. is a continuous -dependent bivariate Gaussian process that is isotropic. It is for all .

5 The statistical test

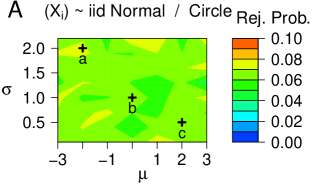

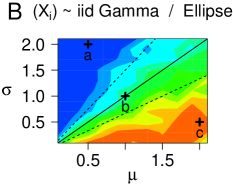

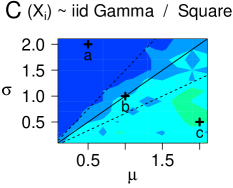

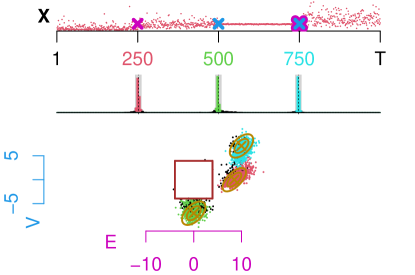

We test . A large deviation of from zero speaks against . We apply Proposition 4.2 to derive a rejection boundary from in simulations. Symmetry implies asymptotic isotropy of and we set the boundary as a circle, see Figure 1. Generally, for possibly skewed RVs, primarily varies along or , resulting in a rejection ellipse or square, see Figure 3.

Derivation of the test

Let . For let denote the Euclidean and the Mahalanobis distance. Noting , Proposition 4.2 and continuous mapping imply convergence of the maximum, as

| (9) |

We use as a test statistic. We reject iff exceeds the -quantile of the limit distribution in (9), given . To the best of our knowledge there is no closed formula available. We choose as a quantile of the approximated distribution derived in Monte Carlo simulations.

In a similar setup Jarušková and Piterbarg, (2011) derived tail approximations for functionals of Brownian bridges to adjust . Here, constitutes a -process, which should allow to derive tail bounds as well, see Albin, (1990); Lindgren, (1980); Adler, (1990); Talagrand, (2014). We mention high accuracy of simulations.

Equivalently, instead of comparing the maximum to , we can judge the entire process w.r.t. a rejection area . For that, define an ellipse , see Figure 3A. is rejected iff enters at any time, while the superscript indicates the complement in . In case of symmetry , equals a circle with radius , i.e., thus , see Figure 1. For the skewed case, derives from by squeezing, .

Treatment of the unknown correlation

depends on unknown . We propose three ways to cope with in practice. First, the symmetry assumption yields . Second, we consistently estimate locally by

| (10) |

recall (6). We define by replacing with in (7), and consider the statistic

| (11) |

Convergence of as in (9) holds true because in it is a.s., see Lemma (4.1). In terms of , the rejection ellipse is time dependent. Under estimation is consistent and the asymptotic -level is kept. Third, we propose a conservative approach to avoid estimation. Define a square , while denotes the maximum norm. has center zero and edge length equal to the diameter of . Because has unit diagonals, any is trapped in , see Figure 3A. Thus, with the asymptotic probability to falsely reject is less than . The test statistic is

| (12) |

This approach is optimal in the sense that touches each edge of exactly once, thus can not be shrunk. The tests are summarized as follows, see also Table 1.

Theorem 5.1.

Let , and for let be the -quantile of the limit in (9). Assume . Then it holds . Further, it holds first given , second , and third .

| test statistic | asymp. level | rejection area w.r.t. | assumption |

|---|---|---|---|

| (9) | symmetry | ||

| (11) | , time dependent | / | |

| (12) | / |

Note that Proposition 6.2 below yields asymptotic power one. Further, the bivariate approach avoids double testing unlike the two univariate approaches from Section 2: Set . With the univariate approaches we obtain the boundaries , by simulation of the quantile of the temporal maximum of a single component of , see Figure 1B and C. With the bivariate procedure we get (radius in D). This slight increase is the price for avoiding -error accumulation.

6 Change point detection

After rejection of we detect change points via successive estimation, see Figure 4. Proposition 6.2 below states asymptotic normality of at , see dartboards in Figures 1 and 3. This facilitates inference about the effects, i.e., the strength and the type of the change, and enables interpretation in practice.

Algorithm 6.1.

Set as either , or as used in the test. Set and . While for any , update and as follows: among all for which , choose the candidate that maximizes the Euclidean distance of , add to and delete its -neighborhood from .

Note that for any choice of , either , or , it is always the Euclidean distance that inference is based on, see interpretation below. For single see similar procedures in Antoch and Hušková, (1999) and Eichinger and Kirch, (2018).

Asymptotic normality of

Proposition 6.2.

Near the process derives from and . W.l.o.g. let . Set

| (13) |

and call the asymptotic expectation of . Further, replaces the true scaling of with the local estimators. Lemma 4.1 implies a.s. componentwise as . The asymptotic correlation matrix is

| (14) |

Note the analogy of and its estimator in (10). In Figures 1 and 3 the distribution of is approximated by for the three change points. The golden dartboards describe the - and -contour lines with center . A stronger increases the squeezing of the dartboards in Figure 3B. Symmetry implies circles in Figure 1. The size of a dartboard is unique up to squeezing as has unit diagonals: implies that for any -contour ellipse is trapped optimally in a square with edge lengths , while denotes the -quantile of the -distribution with two degrees of freedom.

Change point interpretation

To interpret effects we decompose , with , and the angle between and the abscissa. Then is a signal to noise ratio that captures the effects: the Euclidean distance measures the strength of the change, and the angle the type of the change, with change only in expectation , and change only in variance . Generally, a dartboard is shifted towards , see Figure 1 or 3. A dartboard lies far off of zero if either or is large. This implies asymptotic power one, also note extensions to local changes where the parameters imply , see e.g., Antoch and Hušková, (1999). Further note that the location does not depend on the symmetry of which is captured in . Thus, in Algorithm 6.1 it is always the Euclidean distance that is judged by, regardless of .

In practice, for an estimate interpretation is based on , see green arrows in Figure 4. We assign the - and -contour lines of with as in (10), see green dartboards in Figure 4D. This strengthens confidence in interpretation: it is plausible that the smallest estimate refers to a change only in (right dartboard close to abscissa) and that the middle one indicates a change only in (upper dartboard close to ordinate). A single parameter change at the largest estimate, however, is rather implausible (dartboard bottom left).

7 The joint process in case of change points

Let with (symmetry). Proposition 7.1 below yields approximately, with non-random describing excursions from zero in the -neighborhood of any . is a Gaussian process with .

Figure 5 extends Figure 1II and III: fluctuates close to (red, green or light blue). The sensitivity of to the effects is explicated in : is sensitive to changes in and robust against higher order changes, and reacts to changes in but not to higher order changes. This supports Algorithm 6.1. Also, reveals the error caused by a change in , see IIIC (red). In IIID (red) the bivariate approach overcomes the error: for any excursion, is maximal at . We consider but note direct generalization to any with .

Proposition 7.1.

Let with and be a window size such that , and let . In it holds as

| (15) |

is a bivariate continuous -dependent process with for all , and for it equals from (8). We give in (18), and and in (19). The result extends Proposition 4.2. The marginal at is Proposition 6.2. We first extend Lemma 4.1.

Lemma 7.2.

Let with and a window size such that . For it holds in as almost surely , and .

See (16) and (17) for the limits. They are non-random functions in , in depending on parameters of both and . The tilde marks dependence on . For set as a placeholder for the limits, and and as the associated parameters. E.g., choose with and , see Figure 6.

If a window does not lap , then the RVs refer to a single and equals ,

| (16) |

e.g., in Figure 6, also see Lemma 4.1. If a window laps , then depends on both and , see left window in Figure 6. Set for

| (17) | ||||

and define for by replacing in (17) all subscripts with and with . We comment on the left window . A proportion of RVs belongs to and to . Then is a linear interpolation between and . The higher orders are further affected by via the error with . E.g., in we find deriving from as relies on all RVs in irrespective of . All errors vanish iff .

We now define the centering from and via

| (18) |

see and in (5). For we discuss and w.r.t. the type of change. For , see Figure 5B. Message 1: constant expectation implies (green). This is because implies see (17), regardless of higher moments. Thus, is robust against higher order changes. Message 2: a change in expectation causes to deviate from zero (red or light blue). Thus, is sensitive to expectation changes. linearly interpolates and , thus has a hat shape peaking at and is additionally scaled by .

For see Figure 5C. Complexity rises as a change in expectation affects higher moments. Message 1: constant expectation results in behaving analogously to : first, constant variance implies , as for and we find , see (17). Second, a change in variance causes a deviation from zero (green): if , then linearly interpolates and , thus has a hat shape that is scaled with . Thus, given constant expectation, is sensitive to changes in variance and robust against higher order changes. Regarding note a linear trajectory along the ordinate, see Figure 5D (green). Message 2: a change in expectation falsely results in a systematic deviation of from zero even if the variance is constant (red). Thus, is also sensitive to changes in expectation.

replaces the limits with the estimators. It is a.s. componentwise as , see Lemma 7.2. is (13). replaces the limits with the true scaling of the numerators of yielding asymptotic unit variance. captures inconsistent parameter estimation. Outside and at both windows in their entirety refer to a single , stating consistency . In Figure 5IIID (red) is close to but slightly shifted, as we had to distort with . Note that considers while does not: if then as . If then , note the absence of the error in contrast to in (17).

8 Practical Performance

In Subsection 8.1 we extend methodology to multiple windows. This improves the detection of change points on multiple time scales and with different effects. In Subsection 8.2 we discuss the companion R-package jcp. In Subsection 8.3 we provide simulation studies for . We find the asymptotic significance level of the test to be kept in many scenarios. In Subsection 8.4 we discuss simulations for . We confirm reliable detection accuracy and adequate interpretation. To conclude, we present a real data example in Subsection 8.5.

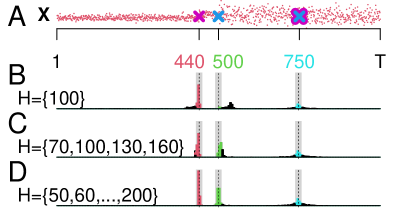

8.1 Extension to multiple windows

For let be a set of increasingly ordered windows , yielding multiple processes . Smaller are sensitive to rapid changes, as they do no overlap adjacent change points and thus ensure an unbiased excursion of which supports precise detection. Larger improve detection of small effects, as at a a dartboard is shifted outwards with order , see Proposition 6.2.

We extend the test: for , let denote the product space with distance metrizing the product topology. Poposition 4.2 extends to

Corollary 8.1.

Under continuous mapping yields convergence of the global maximum

| (20) |

for , which extends (9). We use as a test statistic and reject iff it exceeds the -quantile of the limit distribution. The latter is approximated in simulations. We treat analogously to the case of single , see Table 1: first, symmetry assumption yields , and thus . Second, consistent estimation depends on and now also on , see (10), yielding . Third, using avoids estimation and is conservative. For the process perspective choose such that any enters only with probability , if . Let be the circle with center zero and radius . For the three cases we obtain first , second with depending on and , and third with being the square with center zero and edge length . We extend Theorem 5.1.

Theorem 8.2.

Let , and for let be the -quantile of the limit in (20). Assume . Then it holds . Further, it holds first given , second , and third .

If is rejected we aim at estimating . We use a bottom-up approach similar to Messer et al., (2014). First detect candidates for each . Then merge the candidates into a final set favoring smaller over larger windows.

Algorithm 8.3.

Set as either , or as used in the test. For each obtain using Algorithm 6.1 w.r.t. . Set . For increasing update as follows: add any to that satisfies .

A candidate from the -th step is dismissed if a previously accepted estimate falls into the candidates -neighborhood. See Figure 7 with and yielding three estimates . Note that , i.e., no single estimates all three change points, as small lack power to detect the small effect at , while larger are not sensitive to the close proximity of and .

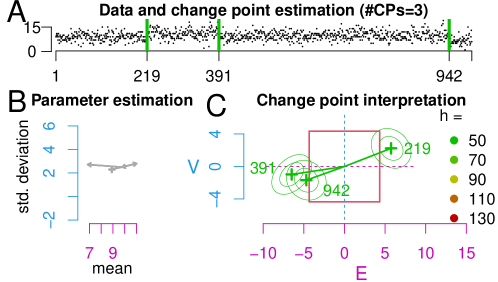

8.2 The jcp-package

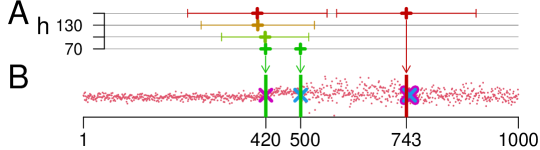

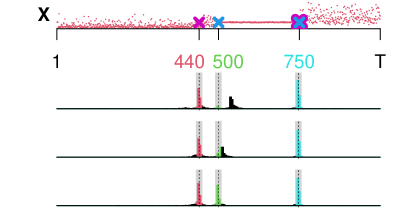

The method is made available in the R-package jcp (joint change point detection) on CRAN. The package also contains a summary and a plotting routine. For the example of Figure 7 it generates Figure 8.

Panel A shows . is rejected. The bars mark . Panel B shows the means () and standard deviations () calculated from all in the estimated sections: we start at ’’ (first section) and follow the arrows, i.e., point right (increase at ), then upwards (increase in at ), and then south-east (decrease in both and at ). The length of an arrow marks the effect size. Panel C facilitates interpretation, recall Section 6: the symmetry assumption yields . The are omitted for overview. The are color-coded (legend). The effect at is strong as it is detected by the smallest (light green), also the dartboard lies far off. The dartboard touches the abscissa suggesting a change only in . The effect at is less strong. However, it was still that registered the change point. The dartboard lies close to the ordinate suggesting a change only in . The largest (dark red) was necessary to detect . The effect is the smallest among all (compare short arrow in B). The dartboard is positioned diagonally suggesting changes in both parameters.

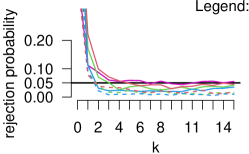

8.3 Significance level and window choice

Significance level

We constructed an asymptotic test, where asymptotically keeps the -level, while reduces it, see Table 1 above. We fixed , linked it to via , and let . In practice however, we set . Thus, for a suitable approximation of (resp. ), we need the smallest window to be sufficiently large. Here we evaluate the rejection probability under for in simulations. It turns out that typically keeps .

In the following let . Processes with and (here i.i.d. RVs) are simulated. The relative frequency of rejections ( simulations) approximates the rejection probability.

Figure 9 shows as a function of the window set , differentiating four distributions: (magenta), (green), (blue) and (red) with shape and rate . For we use , else (solid lines) or (dotted lines). We choose for , i.e., and all windows increase by when rises one unit. We see that tends to the true when increasing , if or . Also, is reduced for . Overall, the approximation is adequate for of about to . Note that is overestimated for small (): intuitively, consider RVs, such that and is heavy-tailed (especially for small), while its limit is . Larger may also help decrease susceptibility to outliers.

Figure 10 shows the dependence of on and . Again we see that is kept for . We fix and consider with (A), and with (B) or (C), mentioning and . The legend in A shows the color-coding of : green indicates , red an increase and blue a decrease.

For we choose and ( combinations) and find for most combinations (entirely green). For we use ( combinations). In B, varies with and . For (diagonal line, , ), it is , which is decreased for , and increased for , but with throughout. The figure suggests to be constant for fixed and varying , i.e., along the lines (dotted lines, upper , lower ), for which we mention rescaling in as well as the scaling property . Note that in B due to the estimator increases variability. The pattern in C is similar to B as the same distributions are considered, but overall it is more blue with throughout, aligning with the conservative nature of .

Window choice

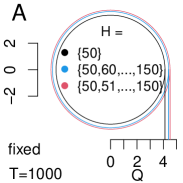

We comment on the choice of . For that we evaluate the dependence of on , recall (20). The radii in Figure 11 show simulations of (also denoted , simulations).

Figure 11A shows three window sets for fix: first yields (black), second () gives (blue) and third () yields (red). We mention monotonicity: implies which follows from global maximization over all , see (20). But we also observe a flattening in the increase, i.e., (black to blue) is larger than (blue to red) although there are much more added when going from blue to red. The reason is that in , over all the rely on a single Brownian motion such that for with equality if . Thus, if is a fine grid then additional have minor impact on the global maximum. Figure 11B shows four choices of for fixed . yields (black), results in (blue - same setup as in A), yields (red) and results in (magenta). Again, we mention monotonicity: implies . This is because in (20) the are evaluated for i.e., for larger the maxima are taken over longer intervals.

For the choice of we now argue that first, the richer the better a scenario of unknown change points and effects is exploited: for we find an preferably large but with free from other change points, resulting in an unbiased excursion of , see Propositions 6.2 and 7.1. The order of the excursion is , while the competitor is bounded (for fixed and ) by the quantile associated with all possible windows. Second, the smallest window should be chosen large enough, e.g., , for the -level of the test to be approximately kept.

8.4 Performance evaluation

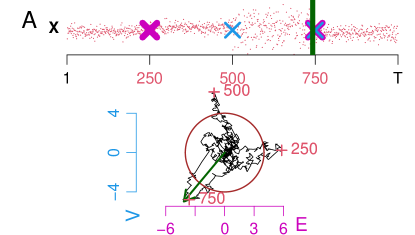

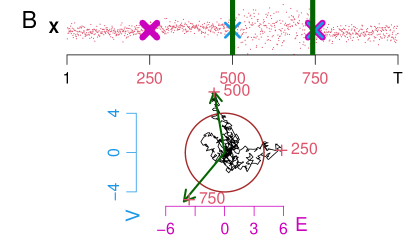

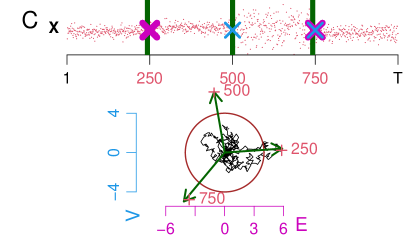

For we evaluate the detection performance in simulations. We show precise estimation of the number and location of , and appropriate interpretation of effects. First, we consider well-disposed setups using a single , see Figure 12. Then we reduce effects and show improvement for multiple , see Figure 13. Finally, we consider more complex processes, see Table 2. We set , describing ’correct’ estimates of at distance , for default, and or . We perform simulations with and throughout.

In Figure 12 and 13 we differentiate with (left) and with (right). We consider piecewise i.i.d. RVs. It is with a change only in at (magenta cross), a change only in at (blue cross), and change in both at (magenta and blue cross), see in A. simulations yield change points. The -neighborhood of any is accentuated by a gray box. are color-coded according to ( red, green, light blue, incorrect black).

| left | 3019 | 998 (1000, 988) | 948 (998, 864) | 946 (989, 852) |

|---|---|---|---|---|

| right | 2993 | 926 (989, 817) | 815 (911, 720) | 962 (996, 913) |

In Figure 12 we set , , for it is and , and for it is and . B shows : three narrow histograms around the true support precise estimation (frequencies reported in table), e.g., left . Of thousand it is for , i.e., estimates yield the red, the green, the light blue histogram. It is (black, low number hardly visible). Panel C shows for all , e.g., left red points. The distribute closely to the asymptotic distribution of for (golden dartboards). Thus, interpretation of effects based on is plausible: e.g., a typical red point indicates a change only in . We see black points: those close to the brown rejection boundary represent real false positives resulting from chance. In contrast, those in the area of the dartboards refer to true but are classified incorrect due to (tails of the histograms in B).

| left B | 2040 | 778 (903, 662) | 71 (160, 43) | 270 (398, 191) |

|---|---|---|---|---|

| left C | 2648 | 953 (999, 631) | 677 (894,353) | 375 (538, 254) |

| left D | 2735 | 1000 (1000, 984) | 872 (924, 779) | 394 (583, 271) |

| right B | 2773 | 786 (874, 697) | 97 (123, 77) | 969 (998, 928) |

| right C | 2786 | 795 (927, 684) | 367 (728, 138) | 980 (999, 938) |

| right D | 2775 | 861 (959, 745) | 676 (740, 607) | 985 (999, 928) |

Before, we showed strong performance under a well-disposed setup for a single . We now show improvement for richer . We choose closer distances of the first two change points , see Figure 13, and also reduce effects for to and . For parameters are as before. We consider three sets (B), (C) and (D). Richer almost always improve the performance: first, increases. Second, the increase. Third, B,C and D show improvement in location precision as the lie closer to the true . The small capture the rapid and , and the larger improve detection of the small effect at .

We further support the quality of the performance now considering five change points and different distributional assumptions, including processes with higher varying moments, see Table 2. We use and set with , , i.e., changes in , , , and . We consider with , with , as well as for the periodic processes as in Section 3 (mix of uniforms) with . Indeed, the estimates lie close to the true , and the often approach .

| 4963 | 957 (996, 853) | 845 (919, 705) | 698 (883, 531) | 854 (974, 687) | 943 (994, 841) | |

| 4598 | 970 (999, 854) | 853 (917, 710) | 662 (879, 513) | 811 (935, 687) | 476 (584, 381) | |

| 4908 | 989 (1000, 916) | 844 (906, 706) | 707 (893, 536) | 869 (953, 713) | 987 (1000, 956) | |

| 4953 | 979 (1000, 920) | 840 (922, 702) | 682 (879, 509) | 867 (977, 711) | 973 (999, 899) | |

| 4958 | 981 (1000, 899) | 863 (931, 731) | 701 (884, 551) | 856 (975, 691) | 973 (998, 890) | |

| 4944 | 988 (1000, 904) | 856 (928, 744) | 686 (884, 561) | 872 (973, 755) | 971 (1000, 905) |

There are other prominent methods available on CRAN, e.g., mosum (Meier et al., , 2019), wbs (Baranowski and Fryzlewicz, , 2019), changepoint (Killick et al., , 2016), stepR (Pein et al., , 2020), cumSeg (Muggeo, , 2020) or FDRSeg (Li and Sieling, , 2017). But none of them captures all aspects covered by jcp, i.e., changes in both and , multiple time scales, and nonparametric methodology allowing piecewise different distributions, e.g., mosum essentially uses to address with a single .

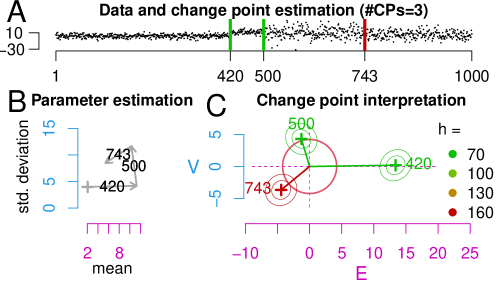

8.5 Data example

We analyze the frequency of the nucleobase uracil in the genome of the severe acute respiratory syndrome coronavirus 2 isolate Wuhan-Hu-1 (SARS-CoV-2), Wu et al., (2020, GenBank: MN908947.3). The genome contains a sequence of bases, which we decompose into subsequent sections of length , in each of which we compute the frequency of uracil, see Figure 14A.

We set , and . was rejected. Three change points were detected . Figure 14C indicates a decrease in at and , and an increase in and also slightly in at . The periodicity captured in the model (see Figure 2) helps mimic the data as compared to i.i.d. sequences (see e.g. Figure 1). None of the four segments shows serial correlation. Other decomposition lengths (e.g., or ) yield analogous results.

9 Discussion

We proposed a method for change point detection in univariate sequences. Data are modeled as independent RVs with piecewise constant and , apart from which the distribution is allowed to vary periodically. In order to jointly detect changes in and , we developed a bivariate MOSUM approach: a comparison of means in adjacent windows is sensitive to changes in , and a comparison of empirical variances addresses . Methodologically, first an asymptotic test was constructed to test the null hypothesis that no change occurred, . Second, an algorithm for change point detection was presented that can be run if is rejected.

The method is grounded on the asymptotic behavior of the MOSUM. Under it was shown to approach a zero mean Gaussian process from which the rejection boundary of the test was derived in simulations. Under the alternative it asymptotically describes a Gaussian process that systematically deviates from zero locally around a change point. The quantification of this deviation supported the sensitivity of the MOSUM process to change points. The first component was shown to be sensitive to changes in and robust against higher order changes. The second component was shown to be sensitive to changes in , but unfortunately it also reacts to changes in . Therefore, it is the joint consideration of both components that supports adequate estimation. Inference on the strength of a change (effect size) as well as its type (, , or both) is enabled with confidence.

The bivariate MOSUM was classified according to the presence or absence of symmetry (more precisely the averaged third centered moment) of the underlying distributions. Symmetry, on the one hand, was shown to result in independent asymptotic components and is thus related to Euklid’s notion of distance: under , symmetry results first in the isotropy of the MOSUM process and thus in a rejection area given by a circle. Second, in case of change points, we found the marginals at the change points to be asymptotically uncorrelated, depicted by round contour lines. On the other hand, a lack of symmetry of the underlying distribution was shown to result in correlated components of the MOSUM process, and is therefore related to Mahalanobis’ distance: first, under the MOSUM has a preferred direction of variability along the main diagonals in , which results in an elliptic rejection boundary. Second, the marginals at the change points have correlated components, resulting in elliptic contour lines. We presented three ways to treat the unknown correlation in applications: first, symmetry assumption results in vanishing correlation. Second, correlation can be estimated consistently. Third, a conservative approach that avoids to address correlation was proposed.

The method was further extended to improve the detection of change points on different scales. For that, multiple bivariate MOSUM processes were applied simultaneously. Indeed, various simulation studies revealed strong performance under different distributional assumptions, including piecewise i.i.d. sequences and processes with varying higher moments. Generally, weak distributional assumptions allow for a wide range of applications. The method is implemented in the R package jcp, which performs the test and the algorithm, summarizes the results and provides a graphical output to facilitate interpretation.

Acknowledgements

The author is very grateful for valuable comments by Götz Kersting, Brooks Ferebee, Ralph Neininger and Anja Nowak, and for helpful suggestions of three anonymous referees.

References

- Adler, (1990) Adler, R. J. (1990). An introduction to continuity, extrema, and related topics for general gaussian processes. Lecture Notes-Monograph Series, 12:i–155.

- Albert et al., (2017) Albert, S., Messer, M., Schiemann, J., Roeper, J., and Schneider, G. (2017). Multi-scale detection of variance changes in renewal processes in the presence of rate change points. J. Time Ser. Anal, 38(6):1028–1052.

- Albin, (1990) Albin, J. M. P. (1990). On extremal theory for stationary processes. Ann. Probab., 18(1):92–128.

- Antoch and Hušková, (1999) Antoch, J. and Hušková, M. (1999). Estimators of changes. In Asymptotics, nonparametrics, and time series, volume 158 of Statist. Textbooks Monogr., pages 533–577. Dekker, New York.

- Aston and Kirch, (2012) Aston, J. A. D. and Kirch, C. (2012). Evaluating stationarity via change-point alternatives with applications to fmri data. Ann. Appl. Stat., 6(4):1906–1948.

- Aue and Horváth, (2013) Aue, A. and Horváth, L. (2013). Structural breaks in time series. J. Time Ser. Anal, 34(1):1–16.

- Baranowski and Fryzlewicz, (2019) Baranowski, R. and Fryzlewicz, P. (2019). wbs: Wild Binary Segmentation for Multiple Change-Point Detection. R package version 1.4.

- Basseville and Nikiforov, (1993) Basseville, M. and Nikiforov, I. (1993). Detection of Abrupt Changes: Theory and Application. Prentice Hall Information and System Sciences Series. Prentice Hall Inc., Englewood Cliffs, NJ.

- Braun et al., (2000) Braun, J. V., Braun, R. K., and Muller, H. G. (2000). Multiple changepoint fitting via quasilikelihood, with application to dna sequence segmentation. Biometrika, 87(2):301–314.

- Brodsky, (2017) Brodsky, B. (2017). Change-point analysis in nonstationary stochastic models. CRC Press, Boca Raton, FL.

- Brodsky and Darkhovsky, (1993) Brodsky, B. E. and Darkhovsky, B. S. (1993). Nonparametric methods in change-point problems, volume 243 of Mathematics and its Applications. Kluwer Academic Publishers, Dordrecht.

- Chen and Gupta, (1997) Chen, J. and Gupta, A. K. (1997). Testing and locating variance changepoints with application to stock prices. J. Amer. Statist. Assoc., 92(438):739–747.

- Chen and Gupta, (2000) Chen, J. and Gupta, A. K. (2000). Parametric statistical change point analysis. Birkhäuser Boston, Inc., Boston, MA.

- Csörgő and Horváth, (1988) Csörgő, M. and Horváth, L. (1988). Invariance principles for changepoint problems. J. Multivariate Anal., 27(1):151–168.

- Csörgő and Horváth, (1997) Csörgő, M. and Horváth, L. (1997). Limit theorems in change-point analysis. Wiley Series in Probability and Statistics. John Wiley & Sons, Ltd., Chichester. With a foreword by David Kendall.

- Dehling et al., (2013) Dehling, H., Rooch, A., and Taqqu, M. S. (2013). Non-parametric change-point tests for long-range dependent data. Scand. J. Stat., 40(1):153–173.

- Dette et al., (2015) Dette, H., Wu, W., and Zhou, Z. (2015). Change point analysis of second order characteristics in non-stationary time series. arXiv:1503.08610.

- Eichinger and Kirch, (2018) Eichinger, B. and Kirch, C. (2018). A mosum procedure for the estimation of multiple random change points. Bernoulli, 24(1):526–564.

- Fang et al., (2020) Fang, X., Li, J., and Siegmund, D. (2020). Segmentation and estimation of change-point models: false positive control and confidence regions. Ann. Statist., 48(3):1615–1647.

- Frick et al., (2014) Frick, K., Munk, A., and Sieling, H. (2014). Multiscale change point inference. J. R. Stat. Soc. Ser. B Stat. Methodol., 76(3):495–580.

- Fryzlewicz, (2014) Fryzlewicz, P. (2014). Wild binary segmentation for multiple change-point detection. Ann. Statist., 42(6):2243 – 2281.

- Gao et al., (2019) Gao, Z., Shang, Z., Du, P., and Robertson, J. L. (2019). Variance change point detection under a smoothly-changing mean trend with application to liver procurement. J. Amer. Statist. Assoc., 114(526):773–781.

- Gerstenberger et al., (2020) Gerstenberger, C., Vogel, D., and Wendler, M. (2020). Tests for scale changes based on pairwise differences. J. Amer. Statist. Assoc., 115(531):1336–1348.

- Gombay and Horváth, (2002) Gombay, E. and Horváth, L. (2002). Rates of convergence for -statistic processes and their bootstrapped versions. J. Statist. Plann. Inference, 102(2):247–272.

- Górecki et al., (2018) Górecki, T., Horváth, L., and Kokoszka, P. (2018). Change point detection in heteroscedastic time series. Econom. Stat., 7:63–88.

- Holmes et al., (2013) Holmes, M., Kojadinovic, I., and Quessy, J.-F. (2013). Nonparametric tests for change-point detection à la Gombay and Horváth. J. Multivariate Anal., 115:16–32.

- Horváth et al., (2008) Horváth, L., Horváth, Z., and Hušková, M. (2008). Ratio tests for change point detection, volume Volume 1 of Collections, pages 293–304. Institute of Mathematical Statistics, Beachwood, Ohio, USA.

- Horváth and Hušková, (2005) Horváth, L. and Hušková, M. (2005). Testing for changes using permutations of U-statistics. J. Statist. Plann. Inference, 128(2):351–371.

- Horváth and Shao, (2007) Horváth, L. and Shao, Q.-M. (2007). Limit theorems for permutations of empirical processes with applications to change point analysis. Stochastic Process. Appl., 117(12):1870–1888.

- Hsu, (1977) Hsu, D. A. (1977). Tests for variance shift at an unknown time point. J. Roy. Statist. Soc. Ser. C, 26(3):279–284.

- Hušková and Slabý, (2001) Hušková, M. and Slabý, A. (2001). Permutation tests for multiple changes. Kybernetika (Prague), 37(5):605–622.

- Inclán and Tiao, (1994) Inclán, C. and Tiao, G. C. (1994). Use of cumulative sums of squares for retrospective detection of changes of variance. J. Amer. Statist. Assoc., 89(427):913–923.

- Jandhyala et al., (2013) Jandhyala, V., Fotopoulos, S., MacNeill, I., and Liu, P. (2013). Inference for single and multiple change-points in time series. J. Time Ser. Anal, 34(4):423–446.

- Jarušková, (2010) Jarušková, D. (2010). Asymptotic behaviour of a test statistic for detection of change in mean of vectors. J. Statist. Plann. Inference, 140(3):616–625.

- Jarušková and Piterbarg, (2011) Jarušková, D. and Piterbarg, V. I. (2011). Log-likelihood ratio test for detecting transient change. Statist. Probab. Lett., 81(5):552–559.

- Killick et al., (2010) Killick, R., Eckley, I. A., Ewans, K., and Jonathan, P. (2010). Detection of changes in variance of oceanographic time-series using changepoint analysis. Ocean Engineering, 37(13):1120 – 1126.

- Killick et al., (2013) Killick, R., Eckley, I. A., and Jonathan, P. (2013). A wavelet-based approach for detecting changes in second order structure within nonstationary time series. Electron. J. Statist., 7(none):1167 – 1183.

- Killick et al., (2016) Killick, R., Haynes, K., and Eckley, I. A. (2016). changepoint: An R package for changepoint analysis. R package version 2.2.2.

- Korkas and Fryzlewicz, (2017) Korkas, K. K. and Fryzlewicz, P. (2017). Multiple change-point detection for non-stationary time series using wild binary segmentation. Statist. Sinica, 27(1):287–311.

- Kuelbs, (1973) Kuelbs, J. (1973). The invariance principle for Banach space valued random variables. J. Multivariate Anal., 3:161–172.

- Li and Sieling, (2017) Li, H. and Sieling, H. (2017). FDRSeg: FDR-Control in Multiscale Change-Point Segmentation. R package version 1.0-3.

- Lindgren, (1980) Lindgren, G. (1980). Point processes of exits by bivariate Gaussian processes and extremal theory for the -process and its concomitants. J. Multivariate Anal., 10(2):181–206.

- Matteson and James, (2014) Matteson, D. S. and James, N. A. (2014). A nonparametric approach for multiple change point analysis of multivariate data. J. Amer. Statist. Assoc., 109(505):334–345.

- Meier et al., (2019) Meier, A., Cho, H., and Kirch, C. (2019). mosum: Moving Sum Based Procedures for Changes in the Mean. R package version 1.2.3.

- Messer, (2020) Messer, M. (2020). jcp: Joint Change Point Detection. R package version 1.1.

- Messer et al., (2014) Messer, M., Kirchner, M., Schiemann, J., Roeper, J., Neininger, R., and Schneider, G. (2014). A multiple filter test for the detection of rate changes in renewal processes with varying variance. Ann. Appl. Stat., 8(4):2027–2067.

- Muggeo, (2020) Muggeo, V. M. (2020). cumSeg: Change Point Detection in Genomic Sequences. R package version 1.3.

- Pein et al., (2020) Pein, F., Hotz, T., Sieling, H., and Aspelmeier, T. (2020). stepR: Multiscale change-point inference. R package version 2.1-1.

- Pein et al., (2017) Pein, F., Sieling, H., and Munk, A. (2017). Heterogeneous change point inference. J. R. Stat. Soc. Ser. B Stat. Methodol., 79(4):1207–1227.

- Siegmund, (1988) Siegmund, D. (1988). Confidence sets in change-point problems. Internat. Statist. Rev., 56(1):31–48.

- Spokoiny, (2009) Spokoiny, V. (2009). Multiscale local change point detection with applications to value-at-risk. Ann. Statist., 37(3):1405–1436.

- Steinebach and Eastwood, (1995) Steinebach, J. and Eastwood, V. R. (1995). On extreme value asymptotics for increments of renewal processes. J. Statist. Plann. Inference, 45:301–12.

- Talagrand, (2014) Talagrand, M. (2014). Upper and lower bounds for stochastic processes, volume 60. Springer, Heidelberg. Modern methods and classical problems.

- Whitcher et al., (2000) Whitcher, B., Guttorp, P., and Percival, D. B. (2000). Multiscale detection and location of multiple variance changes in the presence of long memory. J. Stat. Comput. Simul., 68(1):65–87.

- Wolfe and Schechtman, (1984) Wolfe, D. A. and Schechtman, E. (1984). Nonparametric statistical procedures for the changepoint problem. J. Statist. Plann. Inference, 9(3):389–396.

- Wu et al., (2020) Wu, F., Zhao, S., Yu, B., Chen, Y., Wang, W., Song, Z., Hu, Y., Tao, Z., Tian, J., Pei, Y., Yuan, M., Zhang, Y., Dai, F., Liu, Y., Wang, Q., Zheng, J., Xu, L., Holmes, E., and Zhang, Y. (2020). A new coronavirus associated with human respiratory disease in china. Nature, 579(7798).

- Zeileis et al., (2010) Zeileis, A., Shah, A., and Patnaik, I. (2010). Testing, monitoring, and dating structural changes in exchange rate regimes. Comput. Statist. Data Anal., 54(6):1696–1706.

- Zhang et al., (2009) Zhang, H., Dantu, R., and Cangussu, J. W. (2009). Change point detection based on call detail records. In 2009 IEEE International Conference on Intelligence and Security Informatics, pages 55–60.

Contact information

Michael Messer

Vienna University of Technology,

Institute of Statistics and Mathematical Methods in Economics,

Wiedner Hauptstraße 8-10/105, 1040 Vienna, Austria

tel.: +43 -1 -58801 -10588, email.: michael.messer@tuwien.ac.at

Appendix

We give here all proofs and additional auxiliary results.

ad Section 4

First we state a functional strong law of large numbers (SLLN) for the auxiliary processes, see Definition 3.1.

Lemma 9.1.

For an auxiliary process of period and moments it is for in a.s. as

| (21) |

Proof: The consecutive blocks of length constitute an i.i.d. sequence. Define the mean . Then, for a.s.

| (22) |

The SLLN applied to shows the first summand to tend to . The second summand is the remainder of the last block and vanishes as the moment assumptions imply a.s. as . From (22) we obtain by discretizing time. ∎

Proof of Lemma 4.1: We aim to apply Lemma 9.1, for which we express the centered population parameters from (2) through the non-centered moments as

| (23) |

and analogously and . Note that constant implies . This is favorable, as Lemma 9.1 only states estimation of , but not of if is not constant. Analogously, the average

from (3) behaves well as constant yields . If was not constant,

would fail in estimating .

We consider . Note that from (6) can be expressed through as

,

and .

A comparison with (23) reveals that it suffices

to have

a.s. in , which we obtain by Lemma 9.1 as for

In order to prepare the proof of Proposition 4.2, we state a bivariate functional central limit theorem (CLT) for the first and second moment of an auxiliary process.

Lemma 9.2.

Let be an auxiliary process with population parameters , , and . Rescale variables as and and let be as in (7). Then it holds in as

| (24) |

while constitutes a planar Brownian motion.

Proof: The blocks are i.i.d. Set and . Then is an i.i.d. sequence with components having zero mean and unit variance. Regarding (24) we rewrite

| (25) |

using .

The second summand vanishes as in probability as . We treat the second component of (24) analogously. As , the result follows from a functional CLT w.r.t. , see Kuelbs, (1973) working on general Banach space valued RVs.

∎

Proof of Proposition 4.2: We define a continuous map from to , for both components via

| (26) |

Applying on (24) yields in as

The centering and canceled. In the second component replace with yielding

| (27) |

Regarding the replacement we note that for

while the second summand vanishes uniformly over a.s. as , as first Lemma 4.1 states a.s., and second square-root scaling in yields weak convergence to a Gaussian process limit. Finally, Lemma 4.1 also implies that and in (27) can be replaced by and . ∎

ad Section 5

ad Section 6

Proof of Proposition 6.2:

We write

with

| (28) |

We need to show as , as a.s. by components, see Lemma 4.1. Set and . As

using the Lindeberg-Feller CLT in each component while periodicity of the RVs implies the Lindeberg condition. Cramér-Wold device yields joint convergence. Set

Then, the continuous mapping theorem yields as

and further

since , while denotes the diagonal matrix of the latter display. ∎

ad Section 7

Proof of Lemma 7.2: W.l.o.g. let . Lemma 4.1 implies pointwise a.s. convergence to the population parameter if . Else, a proportion of RVs belongs to , and to .

Regarding we obtain a.s. as

| (29) | ||||

Uniform convergence follows from Lemma 9.1. Analogously, for and it remains to consider . We replace in (29) and discuss the left subinterval . For we find a.s. as

For that, decompose . The first summand yields , the second vanishes, and the third summand yields . Use here a.s. For it remains to comment on . We find a.s. as

For this we decompose

using and a.s. The fourth summand vanishes. ∎

Proof of Proposition 7.1:

relies on independent and . Let . has population parameters , and . We standardize and .

The functional CLT from Lemma 9.2 states that for it holds in as

| (30) |

while is a planar Brownian motion. It is as . The independence of and inherits to and . It also implies joint convergence (30) over and . We replace and with and , see (16) and (17), yielding in as

| (31) |

To switch to the moving sum perspective, we define a continuous map For that we write an element from the domain of as , with associated with the -th component of the first process , and with the -th component of the second process , for . Define componentwise for identical via

We apply on (31). Continuous mapping preserves convergence. The first () and the fourth () summand in refer to a single for which we obtain as in Proposition 4.2. We need to discuss . We focus on the case that lies in the right window , and consider the first component . Application of on the left hand side of (31) yields

| (32) | ||||

For the right hand side of (31) we obtain

| (33) |

which has zero expectation. Replacing and with a single Brownian motion yields continuity. We replace the scaling: first, multiplication of (32) with the first entry of preserves the limit as a.s. Second, multiplication of both (32) and (33) with the first entry of scales (33) to unit variance. Set the latter as the first component of . In total, the first component of (15) holds true. Analogously, derive the second component. It is . ∎